Allegiant Travel Company: The Leisure Platform and the Sun Country Synergy

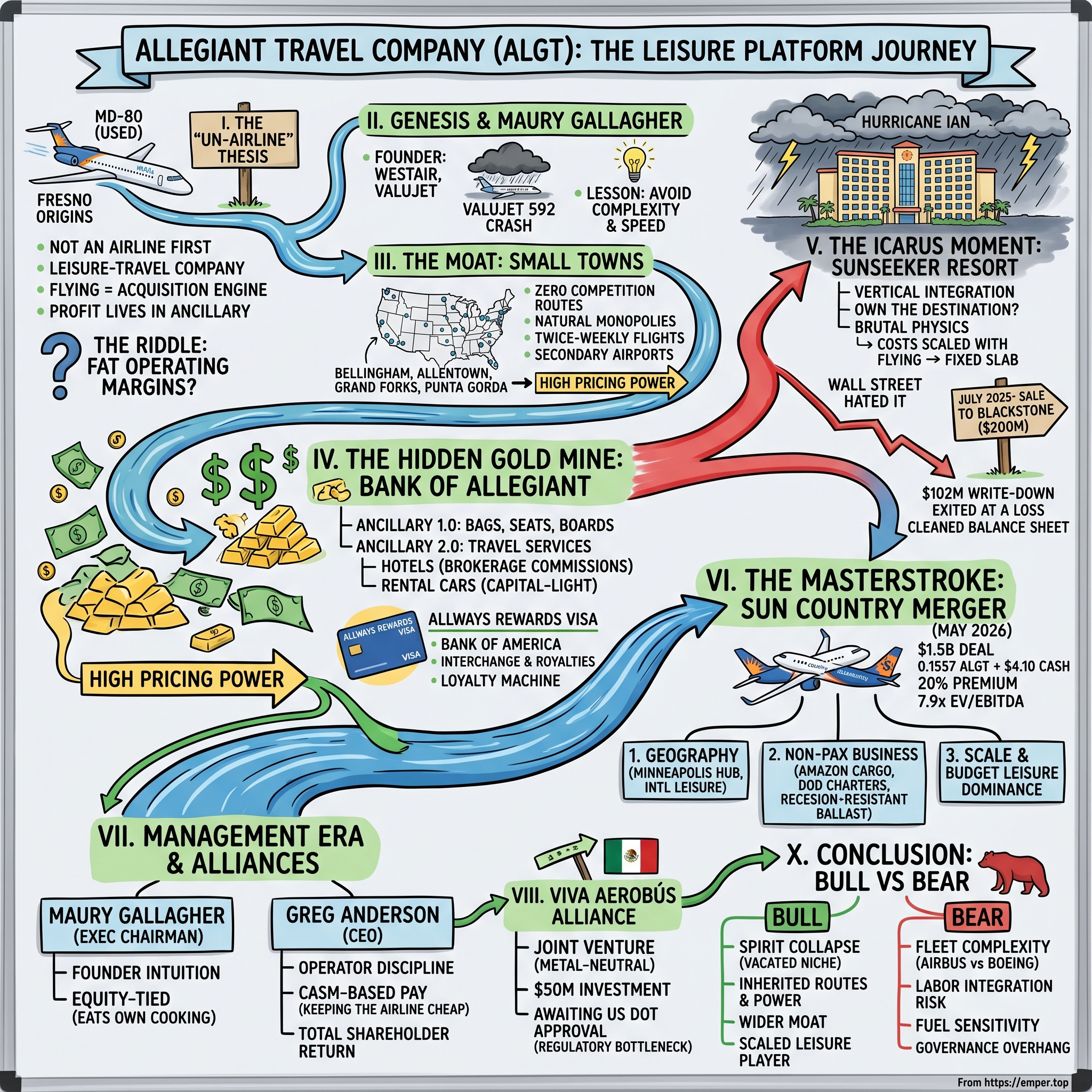

I. The "Un-Airline" Thesis

Picture a Friday afternoon in Sanford, Florida, roughly thirty miles north of the Orlando airport that everyone else flies into. There is no rental-car super-mall, no people-mover train, no four-hour line snaking through TSA. There is a single concourse, a sunburnt family of four wheeling a cooler, and a fifteen-year-old Airbus A320 that spent the morning parked on the tarmac doing absolutely nothing. By Tuesday, that same jet will be parked again. And yet, for two decades, the company that owns it produced some of the fattest operating margins in the entire global airline industry.

That is the riddle at the heart of Allegiant Travel Company. Almost everything it does looks like a mistake if you grade it on the standard airline report card. Its planes sit idle most of the week. It flies between cities you have to squint to find on a map. It buys aircraft that other carriers are trying to get rid of. It does not interline, does not codeshare in the traditional sense, does not chase the road warrior willing to pay $1,400 for a Tuesday morning trip to a sales meeting. By every textbook metric of "asset utilization," Allegiant is doing it wrong.

And that, precisely, is the point. Allegiant is not really an airline that happens to sell vacations. It is a leisure-travel company that happens to own airplanes. The flying is the customer-acquisition engine; the profit lives in the bags, the seat assignments, the hotel rooms, the rental cars, and a co-branded credit card. The founder who reverse-engineered this model, Maurice J. Gallagher Jr., did not arrive at it from a business-school whiteboard. He arrived from one of the most traumatic chapters in modern aviation history.

The hook of this story is that a man whose name was once attached to the deadliest discount-airline disaster in American memory took a tiny bankrupt carrier out of Fresno, California, and turned the conventional wisdom of the industry inside out. The reveal is that in May 2026, after twenty-five years of doing the opposite of everyone else, Allegiant finally did something orthodox. It bought a competitor.

On May 13, 2026, Allegiant closed its roughly $1.5 billion acquisition of Sun Country Airlines, the deal having been agreed in January at $18.89 per Sun Country share — a mix of 0.1557 Allegiant shares plus $4.10 in cash, a premium of about 20% over the prior close.12 In one stroke, the niche carrier that built a fortress out of small towns became something larger and stranger: a diversified leisure platform with a Minneapolis hub, eighteen-odd international leisure destinations, an Amazon cargo operation, and a fleet of Department of Defense charters.

This is the arc we will trace. From the ashes of ValuJet to the $700 million Sunseeker Resort "Icarus" moment, from the Blackstone write-down that closed the book on Gallagher's real-estate dream, to the consolidation of a budget-airline market that lost its biggest disruptor when Spirit collapsed. It is a story about counter-positioning so disciplined it looked like negligence — until you read the margins.

II. Genesis: The Gallagher Pivot

Maurice Gallagher built airlines before most people in the industry knew his name, and then he built the one that nearly buried it. In the 1980s he was a co-founder of WestAir, a California commuter carrier that fed passengers into the bigger networks of the era. He understood the economics of small markets long before "small markets" became a strategy — he understood them as a supplier, the guy flying the unglamorous spokes that the majors didn't want.

Then came ValuJet. Launched in 1993, ValuJet was the original cheap-and-cheerful disruptor: secondhand DC-9s, rock-bottom fares, an Atlanta base, and an explosive growth rate that made Wall Street swoon. Gallagher was a founder and major shareholder. For three years it was a darling. And then, on May 11, 1996, ValuJet Flight 592 crashed into the Florida Everglades minutes after takeoff, killing all 110 people aboard. The cause was improperly handled oxygen generators loaded into the cargo hold by a contractor — a maintenance and oversight failure that became a national symbol of what happens when an airline grows faster than its safety culture.

The brand did not survive the scrutiny. ValuJet was grounded, then merged into AirTran, and the ValuJet name disappeared. For Gallagher, it was a defining trauma and a defining education. The lesson he drew was not "discount flying is dangerous." The lesson was that complexity, speed, and the chase for scale-at-all-costs are what kill you — operationally and reputationally. The man who would build Allegiant came out of the Everglades with a deep, almost religious suspicion of doing what everyone else in aviation was doing.

The vehicle for his second act was almost comically humble. Allegiant Air had been founded in 1997 and flew a handful of routes out of Fresno. It was undercapitalized, overextended, and by 2000 it was in Chapter 11 bankruptcy.3 Gallagher, as a major creditor, took control of the wreckage and effectively started over. The question he asked was not "how do I build the next Southwest?" It was "what is everyone else assuming that I can afford to ignore?"

The answer he landed on was a kind of heresy. Every other airline organized itself around the high-value business traveler — frequent, schedule-sensitive, willing to pay enormous premiums for a 7 a.m. departure and a refundable ticket. To serve that traveler you needed frequency, you needed major hubs, you needed planes flying twelve and fourteen hours a day to spread their cost across as many seats as possible. The entire religion of airline finance was built on one word: utilization. Keep the metal in the air. An idle airplane is a sin.

Gallagher decided to commit the sin on purpose. His customer was not the road warrior. It was the family in Peoria, Illinois, or Grand Forks, North Dakota, who wanted to go to Las Vegas or Orlando once or twice a year and would happily fly on a Thursday and come back on a Sunday. That traveler did not care about frequency. They cared about one thing: the lowest possible nonstop fare from their hometown to somewhere fun. Nobody was serving them, because by conventional math the route couldn't support daily service.

So Allegiant didn't fly it daily. It flew it twice a week.

The genius — and this is the counter-positioning move that defines the whole company — is what that decision unlocked on the cost side. If you fly a route twice a week, you cannot justify a $40 million new Boeing that needs to be in the air twelve hours a day to earn its keep. But you can absolutely justify a twenty-year-old McDonnell Douglas MD-80 bought for a few million dollars at the bottom of a fleet-disposal cycle. When the legacy carriers dumped their MD-80s in the early 2000s, Allegiant scooped them up cheap and made them the backbone of its operation for the next decade and a half.4[^5]

A cheap airplane changes the entire equation. Ownership cost is low, so the breakeven load doesn't depend on heavy utilization. The jet can sit on the ground in Sanford on a Tuesday and the company still makes money, because it barely cost anything to own in the first place. Legacy carriers literally could not copy this — their balance sheets were stuffed with expensive new metal that screamed to be flown around the clock. Allegiant's apparent weakness, its idle fleet, was the visible shadow of its real strength: structurally low fixed costs. The retired ValuJet founder had found his moat, and it was buried in airports nobody else wanted.

III. The Moat: Small Towns and Secondary Gates

If you want to understand why Allegiant could earn airline-industry margins that bordered on the obscene, get a map of the United States and start crossing out the big cities. Cross out the hubs — Atlanta, Chicago, Dallas, Denver. Now look at what's left: Bellingham, Washington. Allentown, Pennsylvania. Bismarck, North Dakota. Appleton, Wisconsin. Belleville, Illinois. These are the dots where Allegiant built an empire, because in most of them, on most of its routes, it had no competition at all.

This is the part of the story that sounds too good to be true and mostly isn't. For the bulk of its history, the large majority of Allegiant's routes had zero direct nonstop competition. If you lived in one of these towns and wanted a nonstop flight to a Florida beach or the Vegas Strip, Allegiant was not the cheapest option — it was the only option. The alternative wasn't a rival airline; it was driving two hours to a bigger airport, parking for a week, and connecting through a hub.

To grasp why no competitor showed up, you have to think like a network planner at a major carrier. A route from a small town to a leisure destination might generate enough demand for, say, three flights a week. A legacy airline can't build a profitable operation around three weekly flights — its cost structure demands daily, high-frequency service feeding a connecting hub. So the major carriers rationally ignored these markets. They weren't being lazy; the markets genuinely couldn't support the legacy model. Allegiant's model was the only one the math allowed, which meant Allegiant got the whole market or nobody did. This is the closest thing in commercial aviation to a natural monopoly on a route.

The second layer of the fortress was the airports themselves. Allegiant gravitated to secondary fields — Sanford instead of Orlando International, Punta Gorda and St. Pete-Clearwater instead of Tampa, Mesa Gateway instead of Phoenix Sky Harbor, Bellingham instead of Seattle. These airports were desperate for traffic. They offered low gate fees, low landing charges, fast turns, and frequently cash incentives or marketing support to land a carrier that would actually bring passengers. For a primary hub, an airline is one tenant among hundreds. For Punta Gorda, Allegiant was the airport. That asymmetry of importance translated directly into pricing power on the cost side.

Run it through Porter's five forces and the picture is almost serene. The threat of new entrants into a Bellingham-to-Las Vegas route is minimal, because the market supports exactly one low-frequency leisure carrier and Allegiant already occupies the slot — a second entrant would simply split a thin market and both would lose money. The bargaining power of the small-town airport as a supplier is weak, because that airport needs Allegiant more than Allegiant needs any single field. Rivalry, on most routes, is theoretical rather than real. The one force that bites is the bargaining power of buyers, because leisure travelers are exquisitely price-sensitive and disloyal — and we'll see how Allegiant tried to staple them down with a credit card.

There is a quieter strategic elegance here that long-term investors should appreciate: a route network like this is not winner-take-all in a glamorous way, but it is durable in an unglamorous way. Allegiant wasn't defending a brand or a technology that could be leapfrogged. It was defending geography. And geography doesn't get disrupted by a better app. The risk to the moat was never a startup; it was Allegiant itself over-expanding into markets that couldn't bear two flights, or a fuel spike that broke the leisure consumer's willingness to fly at all.

But owning the only nonstop ticket out of a sunny-deprived town is just the top of the funnel. The reason Allegiant could obsess over $39 fares is that the fare was never really where it made its money. To see the actual engine, you have to follow the customer past the ticket counter and into what insiders have only half-jokingly called the Bank of Allegiant.

IV. The Hidden Gold Mine: The Bank of Allegiant

Here is a thought experiment that captures the whole business. Allegiant has, at various points, sold one-way fares so low — twenty, thirty, forty dollars — that the ticket itself barely covers the fuel and the gate fee. A rational outsider asks: how does anyone make money selling a flight for less than it costs to drive? The answer is that the flight is a loss-leader, and the profit is everything that happens around it. The base fare is bait. The catch is the ancillary.

Allegiant studied the original master of this art, Ireland's Ryanair, and imported the playbook wholesale: charge for everything that isn't the seat itself, and price the seat itself as low as the market will allow. Want to bring a carry-on bag that goes in the overhead bin? That's a fee — often more than the checked bag, deliberately, to push you toward whatever Allegiant would rather you do. Want to pick your seat in advance? Fee. Want to board early? Fee. Want a bottle of water? Fee. Print your boarding pass at the airport instead of at home? For years, fee. This is the unbundling philosophy: take the thing that used to be "a plane ticket" and atomize it into a dozen separately priced components, so the headline price screams cheap and the real average price the customer pays is meaningfully higher.

Critics called it nickel-and-diming. Allegiant called it choice, and the math vindicated the strategy. Ancillary revenue per passenger climbed into the territory where it rivaled or exceeded the average base fare itself. The psychological trick is potent: a traveler who would never book a $90 advertised fare will happily book a $49 fare and then, click by click, add $45 of bags and seats and priority boarding, walking away feeling like they got a deal. Both sides win on their own terms. That's the durable kind of pricing power — the kind the customer doesn't resent enough to abandon.

But charging for bags is Ancillary 1.0. The more interesting evolution is what we might call Ancillary 2.0 — the "travel company" vision embedded in the corporate name. Allegiant is not called Allegiant Air; it is Allegiant Travel Company, and that word "Travel" was deliberate. Because once you have a captive vacationer from Bellingham who has just bought a flight to Las Vegas, you have the most qualified lead imaginable for a hotel room on the Strip and a rental car at the airport. They are, by definition, going to Las Vegas. They need somewhere to sleep and something to drive.

So Allegiant sells them the hotel and the car, taking a healthy commission — often in the range of a fifth to a third of the booking value — while owning none of the underlying inventory. No hotel to maintain, no car fleet to depreciate, no rooms to fill in the off-season. It is a pure capital-light brokerage margin layered on top of a customer the company already paid to acquire with the flight. This is the part of the model that genuinely resembles an online travel agency more than an airline, and it carries the economics to match.

And then there is the loyalty machine, which is where the "Bank of Allegiant" nickname becomes literal. Through its Allways Rewards program and a co-branded Allways Rewards Visa issued by Bank of America, Allegiant participates in one of the most quietly lucrative arrangements in modern consumer finance.5 When a cardholder swipes that card at a grocery store, the bank earns interchange and pays the airline a royalty for every point it issues, plus a bounty for every new account opened. The airline's marginal cost to mint those points is close to zero — a point is just a promise of a future seat that often would have flown empty anyway. The result, across the industry, is a stream of high-margin, recurring, recession-resistant cash that looks far more like a payments business than a transportation business.6

But here is where the consensus narrative needs a cold splash of reality. The popular telling — that the credit card alone throws off a couple hundred million dollars a year and out-earns the entire flying operation — describes American Airlines or Delta, whose co-brand programs are gigantic. Allegiant is not there. Its co-brand revenue per passenger has historically run a small fraction of what the legacy carriers extract; industry analysis has pegged the gap at roughly a few dollars per passenger for Allegiant versus thirty-plus at the majors. In other words, the loyalty business is not yet the dominant profit engine at Allegiant — it is the underpenetrated optionality. Management talks about it precisely because there is so much room to grow it, not because it is already maxed out. For an investor, that distinction matters: the card is a call option on Allegiant's customer base, not a mature annuity. The bull case requires that option to be exercised; the bear case is that low-frequency leisure flyers simply don't generate enough card spend to ever close the gap.

That gap between the dream and the balance sheet — between what the model could be and what it currently earns — is the through-line of the next chapter, because it is exactly the kind of gap that tempted Maury Gallagher into the most expensive mistake of his career.

V. The Icarus Moment: The Sunseeker Saga

Every founder who builds something improbable eventually starts to believe he can build anything. Maury Gallagher had taken a bankrupt Fresno airline and turned it into a margin machine by relentlessly owning the customer relationship from the moment they searched for a fare. So he asked the logical next question, the one that has lured countless operators to their doom: if I already sell the flight, the hotel, and the car, why am I letting someone else own the destination? Why don't I own the beach resort, too?

The answer to that question was Sunseeker Resort Charlotte Harbor, a sprawling waterfront development in Port Charlotte, Florida. It was vertical integration taken to its logical, vertiginous extreme — an airline building its own resort so it could fly its own passengers to its own hotel and capture the entire vacation dollar end to end. On a whiteboard, it was beautiful. The Allegiant customer was already a Florida-bound leisure traveler. Why not give them somewhere Allegiant-branded to land?

In practice, it was a different business with different physics, and the physics were brutal. An airline's costs scale with flying; a resort's costs are a fixed slab of concrete you pour years before the first guest arrives, exposed to construction inflation, hurricanes, and the small matter of being completely outside the company's circle of competence. Allegiant was very good at squeezing margin out of a used A320. It had never poured a luxury hotel foundation in its life.

Then came Hurricane Ian. In September 2022, the Category 4 storm slammed directly into the Charlotte Harbor area, devastating the region and the half-built resort site. The project absorbed storm damage, supply-chain chaos, and labor shortages, and the budget detonated. Sunseeker had been pitched as a few-hundred-million-dollar project; by the time it finally opened in December 2023, Allegiant had sunk roughly $695 million into it — hundreds of millions over the original plan.7 For a company Allegiant's size, that was not a side project. It was a bet-the-margin diversion of capital and management attention away from the only thing the company had ever been world-class at.

Wall Street hated it, and hated it loudly. Analysts began applying what amounted to a "resort tax" to the stock — a discount for the distraction, the leverage, and the uncertainty of a hospitality venture grafted onto an airline. Every earnings call featured questions about Sunseeker occupancy and ramp instead of about load factors and ancillary growth. The market was effectively telling Gallagher that it had bought shares in a disciplined leisure airline and did not want to be a hotel REIT against its will. The cleanest signal of all: investors seemed to value the airline more highly when they imagined the resort gone.

To his credit, this is where the founder's ego gave way to the operator's discipline — though the new management deserves much of that credit, as we'll see. In 2025, Allegiant executed the great rationalization. On July 7, 2025, it announced that Blackstone's real-estate arm would acquire Sunseeker Resort Charlotte Harbor for $200 million.89 Read that against the roughly $695 million Allegiant had poured in, and the scale of the retreat is stark: the company booked a special charge of about $102 million writing the asset down to fair value, and the all-in economic loss on the Sunseeker adventure ran to several hundred million dollars over its life.10

It is tempting to score this as a simple failure, and financially it was a large one. But strategically the exit was the right and even the brave move, because it did something subtler than just stop the bleeding. It removed the resort tax. By handing the asset to Blackstone — a buyer that actually is a world-class operator of real estate — Allegiant let the market go back to valuing the company as what it is: a leisure airline with a capital-light ancillary engine. The proceeds went to paying down debt and cleaning up the balance sheet ahead of a far more consequential transaction. The Icarus flight ended not in a crash but in a controlled, expensive landing. And the discipline to take that landing tells you something important about who was now actually running the company.

Because by the time the Sunseeker keys changed hands, Gallagher was no longer CEO. The man who had to clean up the founder's most expensive dream was already steering toward a very different kind of bet — not building something new, but buying something proven.

VI. The Masterstroke: The Sun Country Merger

For twenty-five years, Allegiant's entire identity was built on not doing what other airlines did. It did not chase business travelers, did not fly daily, did not buy new planes, and conspicuously did not do mergers. The U.S. airline industry spent the 2000s and 2010s in a frenzy of consolidation — Delta-Northwest, United-Continental, American-US Airways, Southwest-AirTran — and Allegiant sat it all out, growing organically one small town at a time. So when Allegiant agreed to buy Sun Country, it was not just a transaction. It was a philosophical conversion. The contrarian had decided it was time to consolidate.

The deal, agreed in January 2026 and closed on May 13, 2026, valued Sun Country at roughly $1.5 billion including assumed debt. Sun Country shareholders received $18.89 per share — 0.1557 of an Allegiant share plus $4.10 in cash for each Sun Country share — a premium of about 20% over the undisturbed price.12 Allegiant remained the public parent, and crucially, the combined company would eventually fly under a single operating certificate and the Allegiant name, with Sun Country folded in over time.2

The valuation is where the discipline shows, and it is worth dwelling on because it is so out of character for an airline buyer to pay a sane price. At roughly 7.9 times EV/EBITDA, Allegiant paid a fair, modest premium for a profitable carrier. Set that against the cautionary tale that had just played out in the same industry: the JetBlue bid for Spirit, which valued Spirit at a far richer multiple in the neighborhood of 12 times before regulators blew the whole thing up and Spirit spiraled toward collapse. Allegiant watched two competitors bid each other into the stratosphere for an asset that ultimately went bankrupt, and it drew the obvious lesson — buy a good business at a reasonable price, not a troubled one at a trophy price. Management guided to roughly $140 million in annual synergies on conservative assumptions, which against a $1.5 billion price is a meaningful return on its own.1

But the synergy math is the boring part. The strategic logic is what makes this a masterstroke rather than just a deal. Sun Country brought three things Allegiant did not have, and each one patches a specific structural weakness in the old model.

First, geography that complements rather than overlaps. Sun Country's fortress is Minneapolis-St. Paul, a genuine metropolitan hub in the upper Midwest, plus a network reaching roughly eighteen international leisure destinations across Mexico, Central America, and the Caribbean. Allegiant had spent its life in domestic small-town markets; it had almost no international leisure presence and no major-metro stronghold. The two route maps barely touched, which is exactly what you want in a merger — minimal cannibalization, maximum addition. Overnight, the company gained beach destinations south of the border and a real hub in a major city.

Second, and this is the part the market underappreciated, Sun Country is not just a passenger airline. It runs what its own management has called a "three-legged stool": scheduled passenger flying, yes, but also a substantial fixed-fee charter business and a dedicated cargo operation flying Boeing 737 freighters for Amazon under a long-term contract.[^12] This is the hidden business inside the hidden business. The Amazon cargo flying and the heavy charter work — including Department of Defense and other government charter — generate revenue that has nothing to do with whether leisure consumers feel like booking a Vegas trip this quarter. Amazon pays Sun Country to fly boxes whether or not gas is $2 or $5 a gallon and whether or not there's a recession.[^13]

That decoupling is strategically enormous for a company whose original sin was extreme cyclicality. Allegiant's pure-leisure model is wonderful in good times and frightening in bad ones — when consumers stop taking discretionary vacations, there is no business traveler and no cargo contract to cushion the fall. Bolting on fixed-fee cargo and government charter gives the combined company a counter-cyclical ballast it never had. In a downturn, the Amazon planes keep flying. The combined entity is meaningfully more recession-resistant than either airline alone, and that is worth more than the $140 million synergy line will ever capture.

Third, fleet and scale in an industry where scale suddenly matters again. We'll come to the complications of the fleet — they are real and they belong in the bear case — but the headline is that Allegiant roughly tripled down on the budget-leisure niche at the precise moment that niche was being vacated by its largest occupant. To understand why the timing was a masterstroke and not just a deal, you have to understand who was making the decision, because this was not Maury Gallagher's instinct. It was his successor's.

VII. Current Management: The Gallagher and Anderson Era

There is a specific kind of corporate transition that almost never goes well: the founder who is also the largest shareholder, who built the company in his own contrarian image, tries to hand the controls to a professional manager while keeping his hands near the wheel. The graveyard of public companies is full of these awkward two-headed arrangements. Allegiant's version is unusually clean, and the reason is that the two men appear to genuinely agree on the division of labor.

Maurice Gallagher Jr. — Maury to everyone — stepped down as CEO effective September 1, 2024, moving up to Executive Chairman of the Board.11 He did not, however, step away. He remains the company's largest individual shareholder, controlling roughly 12-13% of the stock, which means his net worth rises and falls with the share price and nothing else. His cash compensation is almost beside the point — a base salary in the neighborhood of $666,000 with no annual bonus. Think about what that signals. A man who could pay himself almost anything chose to tie his entire financial outcome to the equity. He does not get richer by hitting a quarterly target; he gets richer only if the long-term value of the company compounds. For a long-term fundamental investor, that is close to the ideal owner-operator incentive structure — Gallagher eats his own cooking, and only his own cooking.

The man who took the operating controls is Gregory C. Anderson, and his profile is the deliberate opposite of the founder's. Where Gallagher is the experimenter — the man who bought used MD-80s and built a resort — Anderson is the operator. He joined Allegiant in 2010 and climbed through the finance ranks, serving as chief financial officer and steering the company through the brutal cash-management crucible of the pandemic before being named CEO.1112 This matters because the skills that built Allegiant are not the skills that will run it from here. Gallagher's era demanded a visionary willing to ignore industry orthodoxy. Anderson's era demands a disciplined integrator who can absorb Sun Country, harmonize two fleets and two labor groups, and execute synergies without breaking the cost machine. The board picked the resume that fit the next chapter.

Anderson's compensation tells the same story in reverse of Gallagher's. Where the founder is paid almost entirely through his existing equity stake, the CEO is paid through performance. A large majority of his target pay — on the order of 70% or more — is variable rather than fixed, and roughly half of his equity grants are tied to hard, measurable performance conditions rather than just time-vesting.13 The two metrics that anchor those grants are exactly the ones a thoughtful investor would choose: CASM — cost per available seat mile, the fundamental measure of how cheaply the airline can produce a seat — and total shareholder return. In plain terms, Anderson gets paid for keeping the airline cheap to run and for delivering returns to the people who own it. He does not get paid for growing the fleet for its own sake or chasing revenue at any cost.

It is hard to overstate how well this maps onto the strategic moment. The single greatest risk in the years ahead is integration — that the cost of merging two airlines erodes the very cost advantage that makes Allegiant special. By bolting Anderson's pay to CASM, the board has aligned the CEO's wallet with the one number that the merger most threatens. The professionalized consolidator is being paid, quite specifically, not to let the consolidation ruin the thing being consolidated.

That said, the two-headed structure is not risk-free, and a diligent investor should watch it. Founder-chairmen who retain large stakes and strong opinions can second-guess their successors, and the Sunseeker episode is a reminder that Gallagher's instincts can be expensive when they wander outside the core. The healthy reading is that the Sunseeker exit, executed on Anderson's watch, was the new regime asserting itself — the operator cleaning up the experimenter's overreach and redirecting capital toward a deal that actually fits. The next test of that dynamic is already unfolding south of the border.

VIII. Strategic Alliances: Viva Aerobús

Long before the Sun Country deal, Allegiant had been quietly working on a different way to grow internationally — one that required no merger and very little capital. The target was Mexico, the largest leisure market on America's doorstep, and the partner was Grupo Viva, the parent of México's brash ultra-low-cost carrier Aeroenlaces Nacionales, S.A. de C.V. — known to travelers as Viva Aerobús. The logic was almost too neat: two ULCCs with nearly identical DNA, one flying Americans to the border and the other flying Mexicans to it, each unable to economically operate the other's domestic network.

In December 2021, the two carriers announced what they billed as a first-of-its-kind commercial alliance between two ultra-low-cost carriers, and they did not do it halfway.14 The structure they proposed was a fully integrated, "metal-neutral" joint venture — the holy grail of airline partnerships. Metal-neutral is industry jargon for an arrangement in which the two airlines stop caring whose airplane (whose "metal") a passenger actually flies on, because they share the revenue and coordinate schedules and pricing as if they were one carrier. It is the difference between a loose marketing handshake and a genuine economic marriage. To make that marriage credible, Allegiant put real money on the table: a $50 million equity investment in Viva.14

The prize is large. The two carriers identified more than 250 potential new nonstop routes between the U.S. and Mexico — leisure markets connecting American small towns to Mexican beaches that neither airline could profitably serve alone but both could serve together.14 If you remember Allegiant's core insight — that it owns the only nonstop ticket out of forgotten towns — the Viva alliance is that same insight projected across an international border, with Viva supplying the Mexican half of the network at Mexican cost structures.

But a metal-neutral JV cannot simply be willed into existence, because coordinating pricing and scheduling between two competitors is, on its face, the kind of thing antitrust law exists to prevent. To do it legally, the partners need antitrust immunity from the U.S. Department of Transportation — an explicit government blessing to behave as one company on these routes. And here the story stalls. The DOT suspended the procedural schedule for the application, citing unresolved questions about whether Mexico was living up to the terms of the U.S.-Mexico air-transport agreement.15 The holdup has had little to do with Allegiant or Viva on the merits and a great deal to do with a broader diplomatic dispute between Washington and Mexico City over slots, cargo operations at Mexico City's airports, and aviation-treaty compliance. Mexican competition authorities, for their part, endorsed the tie-up; the bottleneck has been on the U.S. side.

For investors, the Viva alliance is best understood as embedded optionality rather than a current earnings driver. The $50 million stake is small relative to Allegiant's size, so the downside is contained. The upside — a metal-neutral leisure network spanning North America, with Allegiant and Viva functioning as the budget gateway to Mexico — is substantial but gated entirely behind a regulatory decision that is hostage to geopolitics. It is the kind of asset that contributes nothing to this year's numbers and could be transformational the day the DOT relents, or worth little if it never does. The diligent move is to track the regulatory docket, not the press releases.

Step back, and the Viva alliance and the Sun Country acquisition rhyme. Both extend the leisure platform into territory the core model couldn't reach alone — one by ownership, one by partnership. Both are bets that the future of budget leisure travel is consolidation and coordination, not the lone-wolf organic growth of Allegiant's first quarter-century. Which raises the question that any serious investor has to answer before owning this stock: what, exactly, are the durable sources of advantage here, and which of them survive contact with a much larger, more complex company?

IX. The Playbook: 7 Powers and Business Lessons

Strip away the airplanes and the suntans, and Allegiant is a case study in a single strategic idea executed with unusual stubbornness. It is worth running the company through Hamilton Helmer's 7 Powers framework, because doing so reveals both why Allegiant earned exceptional returns and why those returns might be harder to sustain at scale.

The foundational power, the one everything else rests on, is counter-positioning. Helmer's definition is precise: a newcomer adopts a superior business model that the incumbent cannot copy without damaging its existing business. Allegiant is almost a textbook illustration. The legacy carriers worship high aircraft utilization because their expensive fleets demand it; that worship is rational for them and impossible for them to abandon. Allegiant built a model — cheap used aircraft, low-frequency flying, idle planes midweek — that is only profitable precisely because it inverts the utilization dogma. A legacy carrier cannot copy it without writing down its fleet and blowing up its hub-and-spoke network. The incumbent's strength is the prison that keeps it from responding. That is counter-positioning in its purest form, and it is why Allegiant could earn fat margins for years without a serious imitator from the major-carrier ranks.

The second power is a cornered resource: access to spoke airports and routes that can structurally support only one carrier. This is the geographic moat from earlier — the natural monopoly on a Bellingham or a Punta Gorda route. It is "cornered" because the market itself is too small to share; whoever gets there first owns it, and Allegiant got there first across hundreds of city pairs. Unlike a patent, this resource never expires, though it can be eroded if Allegiant itself over-saturates a market or if demand grows enough to invite a second entrant.

The third power, switching costs, is the weakest of the three and the most aspirational. The Allways Rewards credit card is designed to create switching costs — to make the Bellingham vacationer just loyal enough to choose Allegiant again next year. But as we saw, the co-brand program is underpenetrated, and leisure travelers are notoriously promiscuous. The switching cost exists, but it is thin. This is the power Allegiant most needs to strengthen, and the one the bull case is implicitly betting management can deepen over time.

What about the more glamorous powers? Scale economies — the dominant power in most of the airline industry, where bigger networks spread fixed costs and feed more connections — was historically not Allegiant's game; its whole point was to avoid the scale-dependent hub model. The Sun Country deal is, in part, Allegiant finally reaching for some scale, which is a genuine strategic shift. Network economies, the flywheel where each new node makes the network more valuable to every user, barely apply to a point-to-point leisure carrier that doesn't connect passengers. And branding power is modest; nobody pays a premium to fly Allegiant. The brand stands for "cheapest nonstop from my town," which is a position, not a premium.

The platform question is the most interesting and the most contested. Allegiant's "leisure platform" thesis — flight plus hotel plus car plus card, all monetized off one acquired customer — is the closest any U.S. airline comes to genuine platform economics, where the company sits between travelers and a marketplace of travel suppliers and takes a cut without owning the inventory. If that vision matures, Allegiant is less an airline than a distribution layer for leisure travel, with airline-grade cyclicality replaced by software-grade margins on the ancillary stack. That is the bull's dream. The skeptic notes that for now, the overwhelming majority of revenue still comes from flying people, and the platform is a promising overlay rather than the main event.

The single most transferable lesson for any operator or investor is this: Allegiant won not by being better at the incumbents' game but by refusing to play it. It found the assumption everyone treated as a law of nature — keep the metal in the air — and built an entire company in the gap that assumption left open. The hardest part was not the insight. It was the discipline to keep saying no to growth, frequency, and prestige for twenty-five years. Whether that discipline survives a $1.5 billion acquisition is the question the bull and bear cases now have to fight over.

X. Conclusion: Bull versus Bear

Stand back and look at the company that closed the Sun Country deal in May 2026, and you are looking at something genuinely new — not the lone-wolf small-town carrier of the 2000s, nor the resort-builder of the early 2020s, but a consolidated leisure platform with a hub in Minneapolis, beaches in Mexico, freighters flying for Amazon, charters for the Pentagon, and an option on a North American budget monopoly waiting on a regulator's signature. The question for a long-term owner is whether this is a stronger business or merely a bigger and more complicated one. Both readings are defensible.

Start with the bear case, because it is concrete. The most immediate risk is fleet complexity. Allegiant spent years simplifying to an all-Airbus A320-family fleet, and a single fleet type is one of the great hidden cost advantages in aviation — one set of spare parts, one pilot type-rating, one maintenance program, one training pipeline. Sun Country flies Boeing 737s. The combined company now operates two incompatible fleet families, and unless management rationalizes that over time, it imports exactly the kind of operational complexity that Allegiant's whole philosophy was built to avoid.4 Layered on top is labor integration: merging two pilot groups and two sets of work rules and seniority lists is the single most reliable way to destroy value and morale in an airline merger, and the history of the industry is littered with integrations that took years and arbitration to settle. And underneath everything sits fuel — a pure-leisure passenger network is acutely sensitive to fuel prices and to the discretionary mood of the consumer, and while the Sun Country cargo and charter businesses cushion that exposure, they do not eliminate it.

There is also the governance overhang worth naming honestly: a founder-chairman with a 12-13% stake and a demonstrated willingness to chase expensive non-core dreams. Sunseeker cost shareholders the better part of half a billion dollars in economic value before it was unwound. The bear asks, reasonably, what guarantees the next big idea won't be another Sunseeker — and notes that the answer rests heavily on Anderson's discipline and the board's spine.

Now the bull case, which is equally real and arguably stronger. The dominant fact of the 2026 budget-airline landscape is absence. Spirit Airlines — for two decades the largest and most aggressive ultra-low-cost carrier in America — collapsed, its liquidation in 2026 leaving a gaping hole in the budget-leisure market.16 When the biggest, cheapest competitor in your niche disappears, the survivors inherit its routes, its customers, and its pricing power. Allegiant and the newly absorbed Sun Country are now among the very few scale players left standing in budget leisure, at exactly the moment the niche's chief disruptor exited the stage. The supply of cheap leisure seats contracted; Allegiant's relative position expanded. That is the kind of structural tailwind that does not come around often.

Run the combined entity back through Porter's framework and the picture has strengthened on the dimension that used to be Allegiant's weakness. The threat of new entrants into ultra-low-cost flying just got dramatically more daunting — the most credible recent attempt to scale that model ended in bankruptcy, which is a powerful deterrent to capital. Rivalry within the niche has thinned. The bargaining power of buyers, still the sharpest force given price-sensitive leisure travelers, is now partly offset by the counter-cyclical cargo and charter revenue that doesn't depend on those buyers' moods at all. The moat, in other words, looks wider after the deal than before it — provided the integration doesn't squander the cost advantage that is the whole point.

For investors trying to cut through all of this, the noise reduces to a small number of things that actually matter to track. The first is CASM ex-fuel — cost per available seat mile excluding fuel — because it is the single cleanest readout of whether the merger is preserving or eroding Allegiant's core cost advantage; it is, not coincidentally, the metric the board chose to anchor the CEO's pay. The second is total revenue per passenger, especially the ancillary and co-brand components, because that figure reveals whether the "leisure platform" and the Bank of Allegiant are actually deepening the monetization of each customer or merely treading water. If you want a third, watch the contribution from fixed-fee cargo and charter, because that is the proof of whether the recession-resistance thesis is real or merely a slide in an investor deck.

Is this the Southwest of the 21st century? The comparison is seductive — a disciplined, low-cost, contrarian carrier that out-executed bloated legacies for decades. But it is also incomplete, because Southwest's genius was a single fleet, a single product, and relentless operational simplicity, and Allegiant has just taken on two fleets and a far more complex revenue model in pursuit of something Southwest never attempted: not a better airline, but a leisure-travel platform that uses an airline as its front door. Whether that ambition compounds into the next great consumer-travel franchise or merely complicates a once-elegant niche machine is the open question. The flight that began in a bankrupt Fresno terminal, survived the shadow of the Everglades, and nearly singed its wings on a Florida resort is now carrying considerably more than vacationers. What it is ultimately carrying is a bet that the future of cheap leisure travel belongs to whoever owns the whole journey, and Allegiant has just spent $1.5 billion to find out.

References

-

Sun Country Airlines Holdings, Inc. — Merger Agreement Press Release (Form 425) — SEC.gov, 2026 ↩↩↩

-

Sun Country Airlines Holdings, Inc. — Merger Announcement (Form 8-K Exhibit 99.1) — SEC.gov, 2026 ↩↩↩

-

Which Milestones Have Defined Allegiant Air's History? — Simple Flying ↩

-

Allegiant Bids Farewell to MD-80s After 16 Years — Flight Global ↩↩

-

How the Airline Credit Card Financial Model Works — Cranky Flier, 2025-03-24 ↩

-

Sunseeker Sold: Blackstone Pays $200M for Resort Allegiant Spent $700M to Build — Port Charlotte Sun, 2025 ↩

-

Blackstone Real Estate to Acquire Sunseeker Resort Charlotte Harbor for $200 Million — Allegiant Newsroom, 2025-07-07 ↩

-

Blackstone Real Estate to Acquire Sunseeker Resort Charlotte Harbor for $200 Million — PRNewswire, 2025-07-07 ↩

-

Allegiant CEO Says Sunseeker Sale Expected to Close Shortly, Writes Down $102M to Fair Value — Fox4Now, 2025 ↩

-

Allegiant Announces President Greg Anderson as Next CEO — PRNewswire, 2024 ↩↩

-

Greg Anderson Promoted to CEO at Allegiant — Travel Weekly, 2024-09-01 ↩

-

Allegiant Travel Company 2025 Annual Report (Form 10-K) — SEC.gov ↩

-

Allegiant, Viva Aerobus Announce First-Of-Its-Kind Commercial Alliance Agreement — PRNewswire, 2021-12 ↩↩↩

-

DOT Suspends Review of Proposed Joint Venture Between Viva Aerobus and Allegiant Air — Simple Flying ↩

-

Spirit Airlines Bankruptcy and the ULCC Consolidation Wave — Reuters, 2026-05-20 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube