Align Technology: The Invisible $4B Empire of Digital Dentistry

I. Introduction & The Razor-and-Blade Masterclass

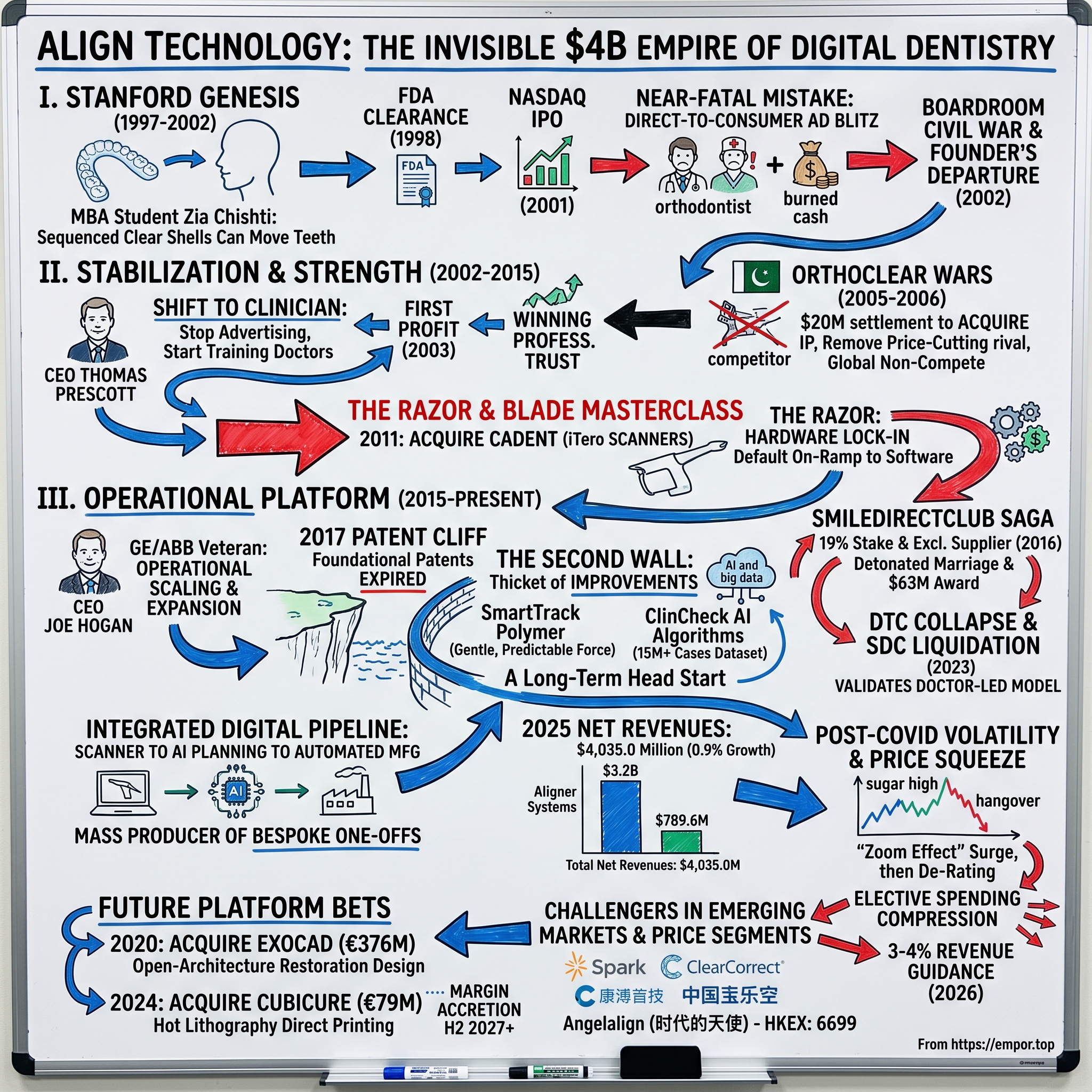

Somewhere in the world, roughly every fraction of a second, a machine in Ciudad Juárez or Cartago or Wrocław is spitting out a thin, transparent shell of medical-grade plastic that is unlike any other shell it will ever make. It has been shaped to the sub-millimeter geometry of one specific human mouth, calculated to nudge one specific set of teeth a fraction of a millimeter closer to where an algorithm has decided they should be. Then the machine makes another one — different mouth, different geometry, different nudge. It does this a million-plus times a day. There is no assembly line in the world that produces a million bespoke, single-use, individually engineered products every day. Except this one.

That is Align Technology, and it is one of the strangest manufacturing companies on the planet: a mass producer of one-offs. In fiscal 2025 it turned that oddity into total net revenues of $4,035.0 million, a record, though a record that arrived at a crawl — up just 0.9% over 2024.1 The business splits into two very different halves. The Clear Aligner segment — the Invisalign franchise — generated roughly $3.2 billion, about 80% of revenue, on a record 2.6 million cases shipped.1 The other segment, Systems and Services — the iTero intraoral scanners and the exocad design software — brought in $789.6 million.1 The market knows Align for the aligners. But the whole thing only works because of the scanners.

Here is the trick, and it is the reason this is a business story and not a plastics story. The aligners are the blades: high-volume, high-margin, consumed and replaced every two weeks by the patient, reordered case after case by the doctor. The iTero scanner is the razor: a $20,000-to-$40,000 piece of hardware that sits in the corner of the operatory and quietly determines which company's blades the doctor will buy for the next decade. When a dentist scans a patient's mouth with an iTero, the 3D model flows by default into Align's ClinCheck planning software, where an Invisalign treatment plan materializes on screen in minutes — ready to show the patient, ready to sell, ready to manufacture. A competitor's aligner doesn't live inside that workflow. It has to be smuggled in from outside it.

Consider what those two numbers do to the company's identity. The blade — the aligner — is a consumable that a patient chews through in fortnightly increments across a treatment that runs a year or more, so a single case is not one sale but a dozen reorders, each one a small margin harvest for a product whose marginal manufacturing cost is a rounding error against a $1,000-plus average selling price. The razor — the scanner — is sold at a price that looks expensive to the dentist but is trivial next to the decade of aligner volume it unlocks. That is the classic Gillette architecture, except Align has done something Gillette never could: it made the razor smart. A King Camp Gillette razor doesn't know which blades you're loading into it. An iTero scanner is, in effect, a razor that quietly refuses to load anyone else's blades — because the software that turns a scan into a treatment plan is Align's, and the default path from that plan to a finished product runs through Align's factories. The lock-in isn't contractual. It's the shape of the workday.

So the honest way to frame Align is not "the company that replaced metal braces with clear plastic." Plenty of companies now sell clear plastic. The interesting claim is that two Stanford MBAs with no dental training built an integrated digital pipeline — scanner to AI planning software to automated direct manufacturing — and used it to convert independent dental practices into captive nodes on their platform. That is the thesis this article will test. Because a thesis about switching costs and workflow lock-in is easy to assert and hard to prove, especially now, with foundational patents expired, growth flattened to low single digits, and a wall of cheaper competitors pressing in from China, Europe, and the orthodontist's own chairside. Align says its integration is a moat. The skeptic says integration is just a nicer word for a lead that erodes.

And the skeptic has fresh ammunition. The stock that traded above $700 at the pandemic's peak spent the years since being cut down to a fraction of that, a de-rating that says the market no longer prices Align as a hyper-growth compounder but as something more ambiguous — a dominant franchise whose best growth may be behind it.13 Revenue that once compounded at 20-plus percent a year now inches forward at low single digits. The whole investment question is whether that deceleration is the temporary hangover of a demand spike pulled forward by COVID, or the permanent signature of a maturing category bumping against the ceiling of what elective dental spending can bear. The story of how the company got here is the best way to judge which is right — and it starts, improbably, with a Stanford business student who kept forgetting to wear his retainer.

II. The Stanford Genesis & The Co-Founder Era (1997–2002)

The origin story is almost too neat, which is usually a warning sign, except in this case it appears to be true. In the mid-1990s, Zia Chishti was a Stanford MBA student who had finished adult orthodontic treatment and been handed the standard parting gift: a clear plastic retainer to keep his newly straightened teeth in line. Like most patients, he didn't always wear it. And he noticed something. When he skipped the retainer for a few days, his teeth drifted; when he put it back in, the retainer pushed them back. A clear plastic shell, it turned out, could move teeth, not just hold them. Which raised the obvious, faintly heretical question: if one clear shell could move a tooth a little, could a sequence of slightly different shells move a whole mouth, all the way, with no metal at all?

Orthodontists had understood the underlying mechanics for a century. What nobody had was a way to design and manufacture dozens of subtly different shells for a single patient at acceptable cost. That was a computing and manufacturing problem, not a dental one — which, conveniently, meant it could be attacked by people who were not dentists. In 1997 Chishti teamed with classmate Kelsey Wirth to found Align Technology.5 Neither had a medical background, and in the founding mythology that is treated as an asset rather than a handicap: they were unencumbered by the profession's assumption that serious tooth movement required serious hardware. Wirth, the daughter of a U.S. senator, brought the operational and fundraising drive; Chishti brought the technical obsession and the origin insight. Together they were doing what business schools in the late 1990s trained people to do — spot an analog industry ripe for digitization and attack it from outside.

The hard part was the software, and it is worth dwelling on why, because the difficulty is the whole moat's origin. Reconstructing a patient's teeth as a manipulable 3D model, then computing a physically plausible sequence of intermediate positions that walks every tooth from crooked to straight without asking any single tooth to move too far too fast — that is a genuinely gnarly geometry-and-physics problem, and in the late 1990s it was near the edge of what commodity computing could do. To crack it, the founders recruited software talent, including Brian Freyburger and Apostolos Lerios, and set them loose on what became the seed of ClinCheck. The plan married three immature technologies: 3D modeling, early stereolithography — a form of 3D printing that traces a laser across a vat of liquid resin, curing it layer by microscopic layer into a solid object, so that a digital tooth model becomes a physical mold you can vacuum-form plastic over — and the algorithmic choreography of tooth movement. Each was hard alone. Chaining them into a repeatable industrial process was the actual invention.

The regulatory door opened first. Invisalign received FDA clearance in 1998, and commercial sales began in 1999.5 Then the capital door: on January 26, 2001, Align went public on Nasdaq, raising roughly $130 million5 — a striking sum for a pre-profit company selling a product most orthodontists had never used and many actively distrusted. And that distrust is where the founders made their near-fatal mistake.

Convinced that consumer demand could steamroll professional skepticism, Align poured enormous sums — a campaign the company would later peg in the tens of millions of dollars — into direct-to-consumer television advertising, blanketing the airwaves to make "Invisalign" a household word before the profession was ready. The logic was seductive and, in a different industry, might have worked: create irresistible consumer pull, and the supply side has to follow. The campaign worked at generating the pull — in the worst possible way. Patients marched into orthodontic offices asking for Invisalign by name.

But this was the mistake that reveals how differently medicine behaves from consumer goods. The orthodontists hadn't been trained on the system, didn't trust the clinical outcomes, and deeply resented a pair of MBAs marketing over their heads to commoditize a specialty they'd spent years mastering. Some flatly refused to offer it. Others tried it, produced poor results because they didn't understand its limits, and blamed the product. A dissatisfied orthodontist is not a neutral party — he is the gatekeeper, and Align had spent its marketing budget making him an enemy. The demand the company manufactured had nowhere to land, because the only people who could deliver the treatment were the ones it had alienated. Cash burned at a rate the young company could not sustain. Margins cratered. And the internal disagreement over how to fix it curdled into a boardroom civil war that ended with co-founder Zia Chishti's departure in 2002.

The lesson buried in that failure would shape everything after: in medicine, the person who controls the sale is not the patient. It is the clinician. A brand that consumers pull for is worthless if the professional who has to deliver it is standing in the doorway with his arms crossed. Align had built consumer demand on top of professional hostility — exactly backwards. Fixing that inversion would require someone who understood that the orthodontist, not the patient, was the customer to win.

III. The Prescott Stabilization & The OrthoClear Wars (2002–2015)

Thomas Prescott arrived in March 2002 to run a company that had confused a marketing budget for a business model. He came from the enterprise-technology and medical-device world, not from dentistry, but unlike the founders he grasped the central fact instantly: in this market, the customer with the money in his pocket — the patient — does not decide what gets bought. The customer who decides is the clinician. So the entire commercial machine had to be pointed at winning the clinician, not the consumer. His diagnosis was unsentimental and immediate: stop shouting at consumers, start courting doctors. He slashed the expensive consumer advertising, redirected the money into clinician training, certification, and the accumulation of clinical-efficacy data that skeptical orthodontists would actually respect, and set about the unglamorous work of rebuilding relationships with a profession that regarded Align as an arrogant intruder.

It was a deliberate downshift from a Silicon Valley growth story to something closer to a disciplined medical-device company — slower, deferential to the profession, obsessed with whether the treatment actually worked and could be shown to work. The unsexiness was the point. Trust in medicine is rebuilt one trained doctor and one good outcome at a time, and it compounds only if you resist the temptation to shortcut it with advertising. By 2003 Align turned its first profit, and the survival question was, for the moment, answered. The more important thing Prescott had done was cultural: he had turned Align from a company that tried to go around dentists into one that went through them — the posture that every subsequent strategic move, from scanners to software, would depend on.

Then the ghost of the founding returned. In 2005 Zia Chishti resurfaced with a competitor, OrthoClear, operating largely out of Pakistan, undercutting Align on price and — Align alleged — poaching its people and its know-how. For a young company that had just clawed its way to profitability, a well-funded rival built by its own co-founder, armed with intimate knowledge of the technology, was an existential threat. Align's response was not to compete on price. It was to go to war on intellectual property, launching a multi-front patent and trade-secret assault, including at the U.S. International Trade Commission, the venue that can block infringing imports at the border.

The choice of venue told you how seriously Align took the threat. The ITC does not award damages; it does something more surgical — it can issue an exclusion order barring infringing products from entering the United States at all, enforced by customs at the border. For a rival manufacturing abroad and importing into Align's home market, an ITC exclusion order is not a fine to be absorbed but a death sentence to the business. By choosing that weapon, Align signaled it wasn't looking for a settlement check; it was looking to end OrthoClear.

The war ended almost as fast as it began, and decisively. In October 2006 the two sides settled: Align paid $20 million to acquire OrthoClear's intellectual property, OrthoClear ceased operations worldwide, and Chishti accepted a multi-year global non-compete.[^7] Read the economics of that deal and its brilliance jumps out. Align paid $20 million — a striking move for a company that believed it was in the right — but in exchange it acquired the rival's entire IP portfolio, removed a price-cutting competitor from every market on earth, and, most valuably, sidelined the one person alive who understood the technology from the inside. It bought back its own origin story and converted an existential threat into a footnote for the price of a modest acquisition. It was the moment Align's monopoly stopped being a slogan and started being a fact. But a monopoly on plastic shells is only as durable as the moat around it, and Prescott's most important move was still ahead — and it wasn't about aligners at all.

In 2011 Align agreed to acquire Cadent Holdings, a New Jersey maker of intraoral scanners, for approximately $190 million.6 To understand why this was the strategic hinge of the entire company, picture the workflow before it. A doctor who wanted to order Invisalign had to take a physical impression of the patient's teeth — pressing a tray of gooey silicone (polyvinyl siloxane, or "PVS") into the mouth, holding it while it set, then packing the mold into a box and mailing it to Align's facility in Costa Rica, where it would be scanned into a digital model days later. It was slow, messy, error-prone, and — crucially — it happened outside any software Align controlled.

Anyone who has had a traditional impression taken remembers the discomfort: a tray loaded with cold, dense putty jammed against the palate, the gag reflex, the several minutes of sitting still while it hardens. Now multiply that misery by the failure rate — a bubble, a smear, a patient who flinched, and the whole impression is useless and must be retaken — and add the days lost mailing a physical object across a continent to Costa Rica. That friction wasn't a minor inconvenience; it was a tax on every single case, paid in chair time, remakes, and turnaround.

Cadent's iTero scanner detonated that friction. A wand passed around the mouth captured a precise 3D model in minutes — no goo, no gagging, no shipping, and the operator could see on screen instantly whether the capture was complete. But the impression-taking convenience, real as it was, was the least of it, and framing iTero as merely "a nicer way to take an impression" misses the strategic masterstroke entirely. By owning the hardware that captured the digital impression, Align now owned the on-ramp to its own software. The scan flowed by default into ClinCheck; the treatment plan rendered chairside; the patient saw a simulated preview of their future smile before they'd left the chair; the case was submitted with a click. Every step that used to be an opening for friction — or for a competitor — was now a paved road running straight into Align's ecosystem.

Align had quietly converted a plastics business into a workflow business, and the distinction is everything. A product can be swapped for a cheaper equivalent the moment one appears. A workflow — the actual sequence of physical and digital steps a practice performs dozens of times a day, the muscle memory of the assistants, the interface the doctor has internalized — is embedded in how the business runs, and ripping it out imposes costs that have nothing to do with the price of the next aligner. The doctor wasn't just buying aligners anymore. The doctor was living inside Align's software all day, and every hour spent there raised the cost of ever leaving. That realization — that whoever owns the scanner owns the funnel — is the single most important strategic idea in the company's history, and the next CEO would spend a decade pressing on it with the resources of a global industrialist.

IV. The Joe Hogan Era & The 2017 Patent Cliff (2015–2020)

In June 2015 Align handed the company to a heavyweight. Joe Hogan had spent much of his career inside the GE machine, ultimately running GE Healthcare, one of the crown jewels of the Jack Welch empire and a business that sold complex medical hardware into hospitals and imaging suites worldwide. From there he became CEO of ABB, the Swiss-Swedish industrial giant, where he ran a sprawling global enterprise measured in the tens of billions. This was a man steeped in the operating disciplines Welch made famous — process rigor, global scale, relentless margin management — and utterly at home selling capital equipment through professional channels. He was not a dental-industry man, and that was precisely the point.

Consider what the board was actually hiring for. Align in 2015 was a roughly $845 million company with a dominant position in a narrow niche: adult, cash-pay, orthodontist-delivered clear aligners in wealthy markets. The prize was an order of magnitude larger — general dentists, who outnumber orthodontists many times over; teenagers, who make up the overwhelming majority of the world's orthodontic starts; and geographies where Invisalign was barely known. Turning a niche premium product into a global platform across those adjacencies is fundamentally an operations-and-scaling problem, and Hogan was, above all, an operator and scaler. His mandate was volume, geography, and category expansion. His timing, though, looked catastrophic to Wall Street, because a cliff was coming into view — one that threatened to make the whole scaling project moot.

Align's foundational patents — the ones protecting the core methods of digital treatment planning and sequential aligner manufacturing — began expiring in October 2017. Wall Street's bear case wrote itself: with the patents gone, a swarm of low-cost generic aligner makers would flood in, the technology would commoditize, and Align's enviable gross margins north of 70% would collapse toward the cost of vacuum-forming plastic. On paper, the moat was about to drain.

It didn't, and the reason is a lesson in how sophisticated companies defend a franchise long after the original patents die. A patent is a wasting asset — it grants a fixed window of exclusivity and then, on a known date, hands the invention to the world. A company that owns a category has a decade or two of warning before its core patents expire, and the sophisticated ones use that window to build a second wall of protection inside the first. Align spent the preceding decade quietly filing thousands of secondary patents around the edges of the expiring core — a technique sometimes called patent thicketing. In cynical hands a thicket is just a swarm of trivial paperwork designed to intimidate; in Align's case the improvements were substantive, and that distinction matters because substantive improvements also make the product better, not just the legal position.

Three of those improvements matter most, and each deserves translation out of marketing language. SmartTrack is a proprietary multi-layer polymer engineered to deliver gentler, more constant force than the rigid plastics that came before. The analogy is the difference between yanking a fence post and easing it back and forth: a material that applies a light, continuous pressure moves a tooth more predictably and more comfortably than one that delivers a hard initial shove and then goes slack. Predictability is the whole game in orthodontics, because a movement the software can reliably forecast is one the doctor can trust. SmartForce attachments are small, tooth-colored bumps of composite that a doctor bonds to specific teeth, giving the smooth aligner something to push against so it can execute movements — rotating a stubborn canine, extruding a tooth vertically — that a plain shell physically cannot grip well enough to perform. They are, in effect, tiny custom handles that let plastic do a metal bracket's job. And the ClinCheck algorithms sit atop a training dataset built from well over fifteen million completed cases,2 a corpus of real-world tooth-movement outcomes — what the software predicted, what actually happened, where it needed correction — that no new entrant can conjure from scratch at any price.

Here is the crux the bears of 2017 missed: a generic maker could copy the idea of a clear aligner the day the core patents lapsed. What it could not copy was the material science locked behind SmartTrack's own patents, the attachment system, or — most importantly — two decades of accumulated data on what actually works in a real human mouth. The idea was free; the execution advantage was not. The patent cliff arrived on schedule, the feared flood of gross-margin-destroying generics never materially dented the premium business, and the margins held above 70%. Whether that data-and-materials advantage is a permanent moat or merely a very long head start that competitors are slowly closing is a question the bear case will revisit with real force. But in 2017, the bears were simply wrong, and the episode bought Hogan the credibility to run the scaling playbook he'd been hired for.

While Hogan defended the flank, a stranger drama unfolded on the consumer front — and it is worth telling carefully, because it became the industry's defining morality play. In 2016 Align took a stake of roughly 19% in SmileDirectClub, the brash direct-to-consumer upstart that mailed aligners straight to customers with no dentist in the room, and agreed to manufacture SDC's aligners as its exclusive supplier.10 It looked like a clever hedge: Align would keep a foot in the DTC camp it had abandoned in 2002 while protecting its professional core. The marriage detonated. SDC accused Align of violating their non-compete by opening physical "Invisalign" retail stores that competed for the same consumers. An arbitrator agreed, and in 2019 ordered Align to shut those stores and return its SDC equity, barring it from competing until August 2020.10 Then the relationship inverted again: Align pursued SDC for breaching their supply agreement, and in May 2023 an arbitrator awarded Align $63 million, an award a California court confirmed that August.10

Notice the pattern the SDC saga exposes about Align's institutional psychology. Twice now — the 2001 advertising blitz and the 2016 SDC stake — the company had been tempted back toward the consumer, toward the seductive idea that it could sell straight to the patient and cut the friction of the professional channel. Both times it got burned, and the second time it got burned in two directions at once, first for competing too aggressively with its own partner and then by that partner's failure to honor its contracts. The tangle of rulings mattered less than the strategic verdict it forced: the doctor is not a cost to be disintermediated but the load-bearing element of the entire model. Chastened out of the DTC experiment for a second time, Align re-committed to the doctor-led approach that Prescott had rescued the company with in 2002 — and, as the next chapter shows, that decision would look less like caution and more like prophecy within a few short years, when the loudest evangelist for cutting the doctor out went bankrupt proving Align's point.

V. Post-COVID Volatility, The DTC Collapse, & Material Science M&A (2020–Present)

For a brief, delirious stretch, Align looked like it had cracked the code on demand. When COVID-19 sent the world onto video calls in 2020 and 2021, millions of people spent their days staring at their own faces in a little rectangle — and deciding they didn't love their teeth. Orthodontists later gave the phenomenon a name: the "Zoom effect." With vacations cancelled and disposable income piling up, elective dental work boomed. Align's revenue surged and its stock ripped above $700 in late 2021, a valuation that implied the pandemic's demand spike was a new permanent baseline rather than a sugar high.

It was a sugar high, and the hangover is central to understanding the company today. As 2022 arrived with inflation and rising interest rates, the arithmetic of a $3,000-to-$6,000 elective purchase turned hostile. This is the uncomfortable truth the pandemic peak obscured: straightening your teeth, for the adult cash-pay patient who drove Align's growth, is elective in the most literal sense — it is a purchase a household can simply defer for a year, or two, or three, when the mortgage payment resets and groceries cost more and the credit-card rate climbs into the twenties. Unlike a filling for an abscessed tooth, nobody's health collapses if the cosmetic case waits. So the moment discretionary budgets tightened, Align's demand curve bent with them.

Case volume growth decelerated from its pandemic sprint to a walk, and by fiscal 2025 the company that had once compounded at double digits grew total revenue by that same faint 0.9%.1 The most plausible reading is that the Zoom boom did not create durable new orthodontic demand so much as pull future demand forward — patients who might have started treatment in 2023 or 2024 did it in 2021 instead — and the bill came due as a multi-year air pocket. For investors, this is the single most important thing to internalize about the business, and it complicates the tidy platform narrative: a large slice of Align's revenue is discretionary consumer spending wearing a medical-device costume. It carries medical-device margins and a medical-device moat, but it flexes with the consumer cycle in a way a true medical necessity never would. Any thesis about Align has to hold that cyclicality alongside the moat, not in place of it.

The clearest verdict on the era, though, was delivered not by Align's income statement but by a competitor's bankruptcy. In September 2023 SmileDirectClub filed for Chapter 11,8 and in December, after failing to find a buyer or a lifeline, it shut down entirely and liquidated.9 SDC had been the poster child for the thesis that technology would disintermediate the dentist — mail-order aligners, no chair, no clinician, a fraction of the price. At its 2019 IPO it had been valued in the billions. Four years later it was worth nothing.

The post-mortem is worth doing carefully, because it validates the exact structural choice Align kept making. Pure direct-to-consumer aligners were unprofitable not by accident but by design flaw: acquiring a customer through relentless advertising cost roughly as much as, or more than, the treatment sold for. When your customer-acquisition cost rivals your selling price, every incremental customer deepens the loss, and scale becomes an accelerant of failure rather than a cure for it — the opposite of how a healthy consumer business works. Worse, stripping the dentist out doesn't merely remove clinical oversight (though it removes that too, with real safety consequences for complex cases pushed onto a mail-order product). It removes the trusted professional who closes the sale for free — the orthodontist whose recommendation a patient acts on without a marketing funnel — and who stands behind the outcome when something goes wrong. Align pays nothing to acquire the patient who walks into a certified Invisalign provider's office already sold; SDC had to buy every single customer at full retail cost of attention. Align's insistence on keeping the doctor in the loop, which had once looked like a failure of nerve against the swaggering DTC disruptors, turned out to be the only economically sustainable structure in the entire category. The medical establishment won, and Align — having flirted with the losing side twice and retreated both times — won with it.

Freed from the DTC distraction, Hogan spent the period making a very different kind of bet — not on marketing, but on materials science and software, the parts of the moat that don't erode with a macro cycle. Two acquisitions define the strategy, and it is no accident that both landed at the very start of the pandemic era, when a confident management team could go on offense while rivals hunkered down.

In April 2020 — the depths of the COVID shutdown, when elective dentistry had briefly ground to a halt — Align completed its purchase of exocad, the German maker of open-architecture CAD/CAM software that dental labs and practices use to design crowns, bridges, implants, and smile makeovers, for approximately €376 million in cash, a total consideration of about $430 million.[^8] The word that matters in that description is open-architecture. exocad's software is used across the industry, including by labs and practices that have nothing to do with Invisalign, and Align has largely kept it that way rather than walling it off — a deliberate choice to own the neutral standard rather than convert it into a captive tool. The price was rich, on the order of high-single-digit multiples of revenue, the kind of multiple you pay for a category-defining software asset rather than a commodity. What it bought was strategic reach: the de facto standard for restorative dental design, stitched into Align's orthodontic and scanning workflow, widening the platform's ambition from "straighten teeth" to "sit at the center of everything a modern practice designs digitally" — orthodontics and implants and prosthetics and cosmetics. If iTero is the on-ramp and ClinCheck is the aligner engine, exocad is the bid to own the design layer for the rest of dentistry too, so that the practice's entire digital day runs on Align rails. Whether that broader platform ambition ever throws off returns commensurate with the price paid is still unproven — restorative software is a slower, more fragmented market than aligners — but the strategic logic of surrounding the scanner with indispensable software is coherent.

The second bet is the more radical one, and it aims at the very heart of Align's cost structure — the way it physically makes the product. In January 2024 Align completed the acquisition of Cubicure, an Austrian pioneer of a 3D-printing process called Hot Lithography, for approximately €79 million.7 To see why a plastics giant would buy a small printing startup, you have to understand the strange, wasteful choreography of how an aligner is manufactured today. Align does not print the aligner. It 3D-prints a hard resin model of the patient's teeth — a solid replica of the mouth at that step of treatment — then heats a sheet of SmartTrack plastic and vacuum-forms it down over the model, trims the resulting shell off, and throws the printed model away. Every single aligner requires its own disposable mold that exists for seconds and is then discarded. Across millions of aligners a day, that is an ocean of printed plastic manufactured only to be trash.

Cubicure's Hot Lithography attacks that waste at its root. Conventional resin 3D printing struggles with thick, tough, temperature-resistant materials because they're too viscous to flow and cure cleanly; Hot Lithography heats the resin so those high-performance polymers can be printed. The prize is direct fabrication: printing the tough final polymer straight into the aligner's finished geometry — no intermediate model, no vacuum-forming, no thermoforming waste. If Align can scale it, direct fabrication would collapse a multi-step, mold-and-discard process into a single print, strip material and labor out of cost of goods, and compress turnaround time — a structural gross-margin lever rather than a one-off cost cut.

The critical word, though, is if. Management has been unusually candid that this is a long game, and the candor itself is a data point about credibility. On the Q4 2025 earnings call, CFO John Morici warned plainly that direct fabrication is margin-dilutive during its early rollout, with only a limited market release of directly printed retainers and attachments planned for 2026 and margin accretion not expected until the second half of 2027.3 That is the opposite of the hype a management team eager to prop up a decelerating stock might be tempted to sell — it would have been easy to wave Cubicure around as an imminent margin miracle. Instead they told investors it would cost money first and pay off years later. The technology is real and the strategic logic is sound; whether it scales into the gross-margin windfall the bulls imagine remains unproven, and by the company's own timeline it is a story for 2027 and beyond, not for the next few quarters. It belongs in the bull case as an option, not in the base case as a certainty.

VI. The Core Business: Industry Structure & Competitive Dynamics

Start with the counterintuitive fact that frames the whole competitive map: after almost three decades, most orthodontic patients still get metal. Traditional bracket-and-wire braces remain the dominant treatment worldwide, and clear aligners — the entire category, not just Align — are a still-underpenetrated slice of orthodontic starts. That is the bull's favorite statistic and it is genuinely important, because it means Align's biggest competitor is not another aligner company. It is inertia, tradition, and the metal bracket. Roughly 70% of orthodontic starts globally are teenagers, a cohort where braces are the entrenched default and where aligners have historically struggled on both cost and compliance — a teenager has to actually wear the things twenty-two hours a day. Crack the teen segment and the category could grow for a decade. Fail to, and aligners stay a mostly-adult, mostly-elective niche.

Within the aligner category, the structure is a consolidating oligopoly, and Align sits unambiguously at the top of it — though how far at the top is a genuinely contested question that investors should not gloss over. Align's own materials and industry trackers place its global clear-aligner share in the high-60s percent; several independent market-research firms put it considerably lower, closer to the high-40s, once low-cost DTC and Chinese domestic volume are counted in the denominator.16 The gap is not a rounding error — it reflects a real disagreement about what "the market" is. In the premium, doctor-led, comprehensive-case segment where Align competes hardest, its share is very high. In the total global unit count including cheap mild-correction cases, it is meaningfully diluted. A careful investor holds both numbers in mind: Align is the clear leader, and its leadership is being chipped at from the low end.

The challengers are worth knowing by name, because each attacks a different flank. Envista Holdings sells the Spark aligner through its Ormco division, the storied orthodontic brand, and Spark has become the most credible direct-to-orthodontist threat — targeting exactly the specialists who most value clinical control and are most willing to switch for a better material or better economics.14 Straumann Group, the Swiss dental-implant powerhouse, owns ClearCorrect and pushes it through its enormous global implant-sales channel into general dentists' offices, cross-selling aligners to practices it already visits.15 Dentsply Sirona fields SureSmile, leveraging Sirona's deep imaging-hardware footprint. And then there is 时代天使 Angelalign Technology (HKEX: 6699), the Chinese leader that already dominates its home market — industry estimates put its China share around 40% — and is now pushing aggressively into Europe, Latin America, and North America with sharp pricing and local clinician support.[^16]16 Angelalign is the one that should worry Align most over the long run, because it competes on precisely the axis — price — where Align is most exposed and least willing to follow.

The deepest strategic battle, though, is not between brands. It is between two kinds of dentist, and understanding it is the key to understanding where Align's growth must come from and why it is getting harder. Orthodontists are specialists — years of extra training, a practice built around moving teeth — who prize clinical control, handle the hard comprehensive cases, and gravitate to whatever system gives them the most command over the outcome. They are demanding, sophisticated, and exactly the customers most willing to defect to a rival like Spark if its material or economics edge ahead, because they have the expertise to judge the difference and the volume to make switching worth it. They are Align's most loyal and most contestable customers at once.

General practitioners are the volume of the future, and a fundamentally different animal. There are far more of them than orthodontists, they are increasingly equipped with intraoral scanners for restorative work anyway, and they are hungry to add lucrative cosmetic and aligner cases to a practice that otherwise runs on cleanings, fillings, and crowns. But a GP is not an orthodontic expert and does not want to become one; the GP wants the treatment to be easy — easy to visualize, easy to sell, easy to execute without fear of a case going sideways. This is precisely the psychology Align's iTero strategy is engineered around. Scan the patient during a routine visit, let the software render a simulated "after" smile on the monitor while the patient is still in the chair looking at their own teeth, quote a price, and close the case on the spot — no referral out to a specialist, no lost revenue. For the GP, iTero plus ClinCheck turns orthodontics from an intimidating specialty into a point-and-click upsell. Win the GP's scanner, and you win the GP's aligner volume for years, because the GP has neither the incentive nor the expertise to go shopping for an alternative workflow.

The catch — and it is the catch that defines Align's next decade — is that the GP and teen segments where the growth lives are also the segments most exposed to price competition and highest in selling friction, exactly where Angelalign and the cheaper challengers are strongest. Align is being pulled toward its growth by a current that also carries its most dangerous rivals. That is the funnel Prescott glimpsed in 2011, now industrialized and globalized — and it is the mechanism the next section puts under the microscope of a formal moat framework.

VII. The Playbook: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question a long-term investor has to ask: what, precisely, stops a competitor from taking Align's business, and how durable is it? Hamilton Helmer's 7 Powers framework is a useful scalpel here, because Align's moat is not one thing but a stack of overlapping advantages that reinforce each other.

Switching costs are the load-bearing wall. A practice that has spent $20,000–$40,000 on an iTero scanner, trained its assistants to use it, wired it into the daily patient flow, and mastered the ClinCheck interface has not merely bought a product — it has rebuilt its operations around a platform. Ripping that out to adopt Spark or ClearCorrect means new hardware, retraining, workflow disruption, and a period of lower productivity, all for a benefit the doctor may not perceive as worth the pain. The cost isn't the scanner's price tag; it's the operational friction of change. This is the most important and most defensible of Align's powers, and it is why the razor-and-blade design is not a metaphor but the actual strategy.

Scale economies compound it. Producing over a million unique, custom products every day demands a colossal, highly automated, vertically integrated manufacturing base — Align's plants in Juárez, Cartago, and Wrocław run at a unit cost no regional lab or startup can approach.2 Bespoke manufacturing usually means high unit cost; Align has inverted that by industrializing customization itself, and scale is what makes the inversion possible. Cornered resources form the third layer: the proprietary SmartTrack polymer, which competitors cannot simply buy, and the ClinCheck dataset of well over fifteen million completed cases, which competitors cannot buy at any price because it is the accumulated exhaust of two decades of being first.2 Brand is the fourth and subtlest — "Invisalign" has become a generic verb the way "Google" did, with patients asking for it by name, which quietly pressures clinicians to keep an Align relationship even when a rival product might serve. That consumer pull, the very thing that nearly killed the company in 2001, has matured into an asset now that the professional channel is firmly onside.

There is a fifth Helmer power worth flagging by its absence: Align has no meaningful process power or counter-positioning left to deploy against incumbents, because it is the incumbent, and the counter-positioning now runs the other way. Angelalign and the DTC-adjacent low-cost players are the ones positioned against Align's high-price model, daring it to either cut prices and cannibalize its premium franchise or hold prices and cede the value segment. That is the classic innovator's dilemma pointed at the pioneer, and it is why the moat's shape matters as much as its size.

Porter's Five Forces sharpen where the pressure actually comes from. The bargaining power of buyers is rising, and this is the underappreciated risk hiding inside a growth story: Dental Support Organizations — corporate entities rolling up thousands of formerly independent practices into centrally managed groups — are becoming huge, sophisticated buyers who negotiate bulk discounts and lean hard on Align's average selling price. On the Q4 2025 call, management highlighted that DSOs already represent about a quarter of volume and are growing double digits.3 Read that carefully: the fastest-growing part of the customer base is also the part with the most negotiating leverage. It is a growth engine and a margin threat wearing the same suit, and management presents it entirely as the former — a framing a skeptic should hold up to the light. The bargaining power of suppliers is low, which helps Align; it makes its own proprietary material and, increasingly, its own printing hardware. The threat of substitutes is moderate and mostly means metal braces, still the default for the hardest cases and the most price-sensitive families, plus the ever-present option of simply not treating at all when money is tight. Rivalry is intensifying and, crucially, concentrated at the low-to-moderate-complexity end — exactly the GP and mild-correction and teen segments Align must grow into — where Spark, ClearCorrect, SureSmile, and Angelalign compete on price against a company whose entire cost structure and brand are built around a premium.

The uncomfortable synthesis writes the investment debate for you. Align's moat is real, layered, and strongest precisely where it already dominates: premium, comprehensive, orthodontist-led cases in wealthy markets. It is thinnest exactly where its future growth has to come from: price-sensitive GPs, teenagers, DSO buying blocs, and emerging markets. A moat that is deepest around the mature core and shallowest around the growth frontier is not a contradiction — it is the normal condition of a maturing category leader — but it does mean the bull and bear cases are not really arguing about whether Align has a moat. They are arguing about whether the moat extends to the only ground that matters from here. And that runs straight into the question of whether management is allocating capital and setting expectations as if it understands the stakes.

VIII. Current Management, Incentives, & Capital Allocation Stress Test

Joe Hogan is still in the chair a decade on, alongside CFO John Morici, who has held the finance reins since 2016 — a stable, long-tenured team that has grown the company from roughly $845 million in revenue the year Hogan arrived to more than $4.0 billion today.1 Longevity cuts both ways as a signal. It means accumulated operational mastery and a narrative that has stayed consistent across dozens of earnings calls; it also means a leadership team now presiding over a maturing core it spent a decade scaling, with the harder question of what the next decade of growth looks like landing squarely on the same desks that engineered the last one.

Management credibility is best judged by behavior over time, not by any single statement, and here Align's record is genuinely mixed in an instructive way. On the positive side, the narrative has been strikingly consistent across a decade of calls — doctor-led model, iTero as the funnel, teen and international as the growth vectors, digital platform as the moat — and the team has generally guided with realism rather than bravado, most visibly in refusing to oversell Cubicure. When the patent cliff came, they had a specific, prepared answer (the secondary-patent wall) rather than a scramble. On the less flattering side, the pandemic era exposed the limits of anyone's forecasting: like most of its industry, Align read the 2020–21 surge as a step-change rather than a pull-forward, and the subsequent deceleration humbled a lot of confident language about durable double-digit growth. A fair verdict is that this is a credible, experienced team that communicates candidly about the near term but has been no better than the market at seeing cyclical turns coming — which argues for weighting its KPIs over its adjectives.

On paper, incentives are aligned the way governance textbooks prescribe. Hogan is required to hold company stock worth six times his base salary, other senior executives three times, so management's personal wealth rides on the share price rather than on hitting a one-year bonus target.11 His fiscal 2025 total compensation was about $19.2 million, and the mix is the part worth reading closely: roughly $16.6 million of it was stock awards, with only about $1.4 million in salary and $1.2 million in cash bonus.1112 Pay is overwhelmingly equity, and equity that vests on multi-year performance conditions — which is what long-term holders want to see, because it ties the CEO's outcome to theirs rather than to short-term optics. It is also worth noting that the $19.2 million figure was down nearly 30% from the prior year's $27.3 million,12 a decline that tracks the stock's own de-rating from its pandemic peak. That is the incentive structure doing its job: a flat operating year and a fallen share price showed up as a materially lighter payday in the corner office, rather than the ratchet-only compensation that erodes trust at so many mature companies.

Capital allocation is where a maturing growth company reveals what it really believes about itself, and Align's behavior tells a consistent — and quietly telling — story. The company has become a steady repurchaser of its own shares; in fiscal 2025 it bought back 2.9 million shares for $465.9 million at an average of about $162.1 Then, reporting first-quarter 2026 results, it announced yet another $200 million repurchase program and reaffirmed its full-year guidance.4 Buybacks at this cadence carry a two-sided message that management would prefer you read only one way. The bullish reading is that management views the shares as undervalued and is returning cash to owners with discipline. The skeptical reading, equally valid, is that a company buying back this much stock is telling you it cannot find enough high-return projects to reinvest in — that the reinvestment runway inside the core has narrowed to the point where handing cash back beats plowing it forward. Both can be true at once, and for a maturing franchise generating strong free cash flow that no longer needs to fund breakneck expansion, buybacks are a defensible use of capital. But an investor should hear the second message as clearly as the first: this is what capital allocation looks like at a company transitioning from growth to maturity, whatever the guidance deck calls it.

Capital expenditure, by contrast, is deliberately restrained, budgeted in a tight band as the company funds manufacturing capacity and software rather than empire-building — a discipline consistent with the operator's-DNA Hogan brought from GE and ABB. And to the credit of the M&A track record, there is no sign of "diworsification," the value-destroying habit of buying unrelated businesses to look busy. The two significant acquisitions of the era, exocad and Cubicure, were adjacent, strategic, and digestible: one deepened the software layer that surrounds the scanner, the other attacked the cost structure of the core product. Neither was a vanity purchase, and both fit the platform logic. A stress-test of the capital story, in other words, finds discipline on capex and coherence on M&A — the concern is not that management is wasting money, but that its steadiest use of cash is the one that implicitly concedes the growth deceleration it verbally resists.

Now the stress test a skeptical activist would actually run. The core concern is not fraud or governance rot — it is maturity dressed up as strategy. Case-volume growth has decelerated from historic double digits to mid-single digits, and management's own fiscal 2026 guidance calls for just 3% to 4% revenue growth.3 The bear reading is that the lucrative adult-elective market in wealthy countries is saturating, and that the two paths to reacceleration — the teen segment and emerging markets — both require lower prices and more selling friction, precisely the conditions under which margins compress. Management is guiding to a non-GAAP operating margin around 23.7% in 2026, roughly 100 basis points of improvement,34 and simultaneously guiding clear-aligner ASP to decline 1–2% on geographic and product mix.3 Those two commitments — expanding margins while prices fall — are only reconcilable through cost discipline and manufacturing efficiency, which is exactly why the Cubicure direct-fabrication bet matters so much and why its multi-year, margin-dilutive-first timeline is a live risk rather than a settled win. The activist's sharpest question writes itself: if a real price war breaks out at the low end, does the margin guidance survive contact with the enemy? Management says its cost position and mix management protect it. The honest answer is that we will find out in the KPIs.

IX. The Bull vs. Bear Case & Key KPIs to Watch

Every debate about Align eventually collapses into three numbers, and a disciplined investor can largely ignore the rest of the noise by watching them move over time — not calculating them, just tracking the direction and rate of change quarter after quarter.

The first is clear-aligner case volume, sliced by GP-versus-orthodontist adoption and by how many cases the average trained doctor actually submits per year — utilization. Volume is the purest read on real end-demand, stripped of price and mix effects, and it is the number that will tell you first whether the post-COVID air pocket is filling in or hardening into a permanent plateau. Utilization is the subtler tell: it reveals whether Align is genuinely deepening its grip on existing accounts — getting each doctor to do more cases through the platform — or merely adding logos that never ramp into real volume, a distinction that separates durable share gains from vanity distribution. The second is the iTero installed base and its associated software and subscription revenue, because the scanner fleet is the leading indicator for everything downstream: every iTero placed today is a funnel that will feed Invisalign volume for years, so the sequential growth of the fleet is a preview of aligner volume one to two years out. That iTero Lumina made up roughly 86% of full-system units in Q4 2025 shows the newest, higher-capability hardware is landing with buyers rather than gathering dust — a healthy sign for the funnel's future throughput.3

The third is clear-aligner average selling price, the single cleanest gauge of whether competitors are successfully eroding Align's pricing power. This is the canary in the competitive coal mine. Management has already guided to a 1–2% ASP decline for 2026, attributing it to geographic and product mix rather than head-to-head discounting.3 The whole bear-versus-bull argument about commoditization will show up here first: if ASP declines stay shallow and mix-explained, the moat is holding; if they accelerate and management's explanations shift from "mix" to something closer to "competitive environment," the pricing power is cracking in real time. Track those three — volume, the scanner fleet, and ASP — and you are tracking the actual business, not the narrative the company tells about it.

The bull case rests on three engines, each a real mechanism rather than a hope. Teen expansion is the biggest: if Invisalign — via products like Invisalign First and the palate expander — displaces metal brackets in the 70%-of-starts adolescent market, the category's ceiling lifts dramatically, and Align noted 936,000 teens and kids started treatment in 2025, up 7.8%.3 Direct 3D printing via Cubicure is the second: if Hot Lithography scales, it cuts a step and a mold out of every aligner, structurally lowering COGS and speeding turnaround in a way competitors can't quickly match. And the digital-workflow standard is the third: if iTero and exocad become the default operating system of the modern dental office, the switching costs deepen into something closer to true lock-in, and Align's platform becomes the ground the whole practice stands on.

The bear case attacks each engine at its weakest joint. On commoditization: with the core patents expired, the technology gap narrows every year, and a well-resourced orthodontist can increasingly buy open CAD software, print models or even aligners in-house, or source comparable shells from Angelalign or Spark for materially less — the moat holds only as long as Align's integrated convenience is worth the premium, and that premium is a choice competitors get a vote on. On the elective squeeze: prolonged consumer weakness can pin revenue growth in the low single digits indefinitely, because you cannot force a household to buy a $5,000 discretionary smile when money is tight. And on DSO power: the consolidation of practices into corporate buying blocs steadily strips Align of the pricing power it enjoyed against fragmented solo dentists, turning a high-margin franchise into a volume-discount grind.

It is worth pausing on one consensus narrative that deserves fact-checking, because both bulls and bears sometimes overstate it: the idea that Align's moat is essentially impregnable because of switching costs. Reality is more contingent. Switching costs are high for a practice that has already standardized on iTero and ClinCheck — but they are close to zero for the tens of thousands of GPs and emerging-market practices that have not yet chosen a platform, and those unclaimed practices are precisely the growth pool everyone is fighting over. A moat protects the territory already inside it; it does nothing to guarantee the new land. So the honest version of the switching-cost story is that Align has strong retention power and unproven acquisition power in the very segments that will determine the next decade. That is a materially different, and more sober, claim than "the platform is a fortress."

The risk radar, kept to what is genuinely material, has three live items beyond the demand and pricing pressures already discussed. First, China policy: volume-based procurement (VBP) programs that force down medical-device prices are a structural overhang for any premium player, and management noted it has not baked China VBP assumptions into its 2026 forecast given implementation delays3 — prudent, but it means a downside scenario sits outside the guidance rather than inside it. Second, technology diffusion: the same direct-3D-printing capability Align is buying through Cubicure will, over time, become available to competitors and even to in-house printing at large practices, so the very innovation framed as a bull-case moat-widener could, a decade out, become a commoditizing force if the underlying materials and printers democratize. Third, execution risk in the transitions themselves — teen expansion, emerging-market entry, and direct fabrication are all multi-year build-outs running simultaneously against a decelerating core, and any of them slipping turns a slow-growth story into a no-growth one.

The synthesis is not a verdict but a tension worth stating plainly. Align remains the clear leader with a genuine, multi-layered moat — switching costs, scale, proprietary materials and data, and a brand that has become a verb. But it is a leader whose defenses are strongest in the mature, premium segment it already owns and thinnest in the price-sensitive, high-growth segments it now needs, arriving just as the macro cycle turned against elective spending and low-cost rivals found their footing. The company that spent a decade proving the bears wrong about the patent cliff now faces a subtler bear thesis — not that the moat will be dramatically breached, but that growth will simply grind at low single digits while margins are defended by the quarter and the multiple stays compressed. That is a harder thesis to disprove than the patent-cliff panic was, because it doesn't require anything to break; it only requires the status quo to persist. Whether Cubicure's printers, the teen market, and international expansion rewrite that story into reacceleration, or merely soften a long maturation, is the open question the KPIs — and only the KPIs, not the narrative — will answer over the next several years.

X. Epilogue

The enduring lesson of Align Technology is one of transformation in the most literal sense — of turning a simple, mechanical, physical object, a shell of clear plastic, into the visible tip of a deep and integrated technology-and-data platform. The two Stanford students who started it understood almost nothing about orthodontics and, at first, even less about how to sell to orthodontists; they nearly destroyed the company learning that the clinician, not the consumer, holds the pen. What survived that lesson was rebuilt by operators — Prescott, who bought the scanner that became the funnel, and Hogan, who scaled the funnel into a global platform and defended it through a patent cliff the market was sure would be fatal.

The road ahead is genuinely uncertain, and the honest framing keeps the two forces in view at once. On one side, direct 3D printing and an ever-deepening dataset of completed cases could keep Align several steps ahead of everyone else, compounding the workflow lock-in until the modern dental practice is simply unimaginable without it. On the other, the slow gravity of expired patents, price-competitive challengers from China and the orthodontist's own chairside, and a maturing core in the wealthy markets that made the company rich could grind that lead down to something ordinary. The pioneer of digital dentistry built an invisible empire on the insight that whoever owns the scanner owns the mouth. The next chapter will test whether owning the mouth is still enough when everyone else has learned to make the plastic.

References

-

Align Technology Announces Fourth Quarter and Fiscal 2025 Financial Results — Align Technology / Business Wire, 2026-02-03 ↩↩↩↩↩↩

-

Align Technology, Inc. Form 10-K for fiscal year ended December 31, 2025 — U.S. Securities and Exchange Commission ↩↩↩

-

Align Technology (ALGN) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-02-04 ↩↩↩↩↩↩↩↩↩

-

Align Technology Announces First Quarter 2026 Financial Results, $200M Stock Repurchase, and Reaffirms Fiscal 2026 Guidance — Align Technology ↩↩

-

Align Technology SEC Filings Profile — CIK 0001097149, U.S. Securities and Exchange Commission ↩↩↩

-

Align Technology to Acquire Intra-Oral Scanning Leader Cadent for $190 Million — Align Technology, 2011-03-29 ↩

-

Align Technology Completes Acquisition of Cubicure, a Pioneer of Direct 3D Printing Solutions for Polymer Additive Manufacturing — Business Wire, 2024-01-03 ↩

-

SmileDirectClub files for Chapter 11 bankruptcy protection — Reuters, 2023-09-29 ↩

-

SmileDirectClub to shut down operations after bankruptcy filing — Reuters, 2023-12-09 ↩

-

Superior Court of California, County of Santa Clara, Confirms $63 Million Arbitration Award in Favor of Align Technology — Business Wire, 2023-08-23 ↩↩↩

-

Align Technology, Inc. Definitive Proxy Statement (DEF 14A), 2026-04-07 — U.S. Securities and Exchange Commission ↩↩

-

Executive pay decreases at Invisalign maker Align Technology — Medical Design & Outsourcing ↩↩

-

Align Technology (ALGN) NASDAQ Stock Quote — The Wall Street Journal ↩

-

Ormco Spark Clear Aligners Official Page — Ormco / Envista Holdings ↩

-

Straumann Group Orthodontics and ClearCorrect Platform — Straumann Group ↩

-

Clear Aligners Market Size And Share Report, 2026-2033 — Grand View Research ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube