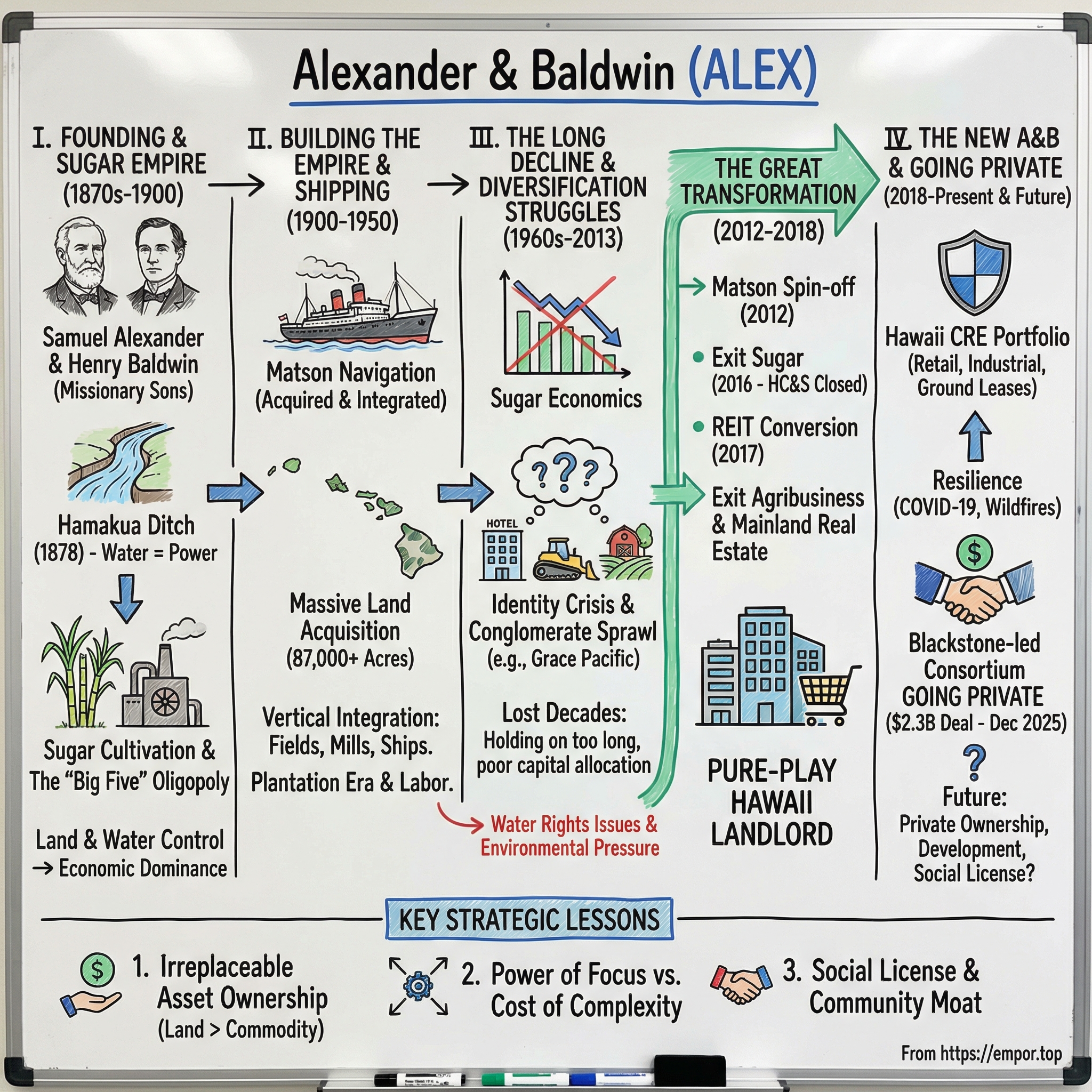

Alexander & Baldwin: From Sugar Barons to Hawaii's Landlord

I. Introduction & Episode Roadmap

Somewhere in the middle of the Pacific Ocean, roughly 2,400 miles from the nearest continent, sits a chain of volcanic islands that Americans visit for honeymoons, surf trips, and overpriced poke bowls. What most visitors do not realize is that a 155-year-old company they have never heard of owns a staggering amount of the ground beneath their feet. Alexander & Baldwin, trading under the ticker ALEX on the New York Stock Exchange, controls approximately 87,000 acres across the Hawaiian islands, making it one of the state's three largest private landowners. That is roughly equivalent to the land area of Detroit.

Here is the question that makes this story irresistible: How did two sons of Protestant missionaries, born in grass-hut Hawaii in the 1830s and 1840s, build a sugar empire so dominant that it helped overthrow a queen, reshape a kingdom, and ultimately survive every single one of its peers across a century and a half of economic upheaval? And why, after 146 consecutive years of growing sugarcane, did their company voluntarily kill the very business that made it powerful?

The answer is a masterclass in corporate adaptation, strategic pivots, and the brutal arithmetic of knowing when to harvest a dying business and plant the seeds of a new one. Alexander & Baldwin's story spans the age of clipper ships, two world wars, the rise and fall of an entire agricultural commodity, and a transformation so complete that the company founded to grow sugar now grows shopping centers, warehouses, and industrial parks. Along the way, it outlasted every one of Hawaii's infamous "Big Five" companies, the oligopoly that once controlled virtually the entire Hawaiian economy.

This is also Hawaii's story. Colonization, exploitation, transformation, and the unresolved tension between those who own the land and those who call it home. The themes that run through A&B's history, adaptation versus attachment, legacy versus reinvention, strategic focus versus conglomerate sprawl, are universal business lessons wrapped in one of the most geographically isolated economies on earth.

We will trace the arc from missionaries to monopoly, through the long and painful death of sugar, into the identity crisis of the 2000s, and finally to the decisive transformation that turned A&B into a pure-play Hawaii landlord. And we will end with the most recent chapter: a consortium led by Blackstone arriving in December 2025 to take the whole thing private for $2.3 billion, closing a public-market journey that began over a century ago.

A note on context: Alexander & Baldwin is not a household name. It does not appear on CNBC tickers or in Barron's roundtable discussions. With a market capitalization that barely cracked $1.5 billion before the going-private announcement, it was too small for most institutional portfolios and too obscure for most retail investors. But its story illuminates principles about asset ownership, strategic transformation, and the relationship between land, power, and identity that are universal in their application and fascinating in their specifics. This is a story about what happens when a company's most valuable asset turns out to be something it has owned all along but never properly valued.

II. Founding Context: Missionaries, Sugar & Empire (1870s-1900)

Picture Lahaina, Maui, in the 1840s. It is the capital of the Hawaiian Kingdom, a whaling port teeming with sailors, missionaries, and native Hawaiians navigating the collision between two worlds. In this unlikely setting, two boys are growing up in missionary households that will shape the future of an entire state.

Samuel Thomas Alexander, born in 1836, was the son of Reverend William Patterson Alexander and Mary McKinney Alexander, who had sailed from the American mainland to Hawaii in 1832 under the auspices of the American Board of Commissioners for Foreign Missions. Henry Perrine Baldwin, born in 1842, was the son of Dr. Dwight Baldwin and Charlotte Fowler Baldwin, who had arrived the year before as medical missionaries.

The two families lived in close proximity in Lahaina. Samuel and Henry grew up together, learned the Hawaiian language, and developed a friendship that would become one of the most consequential business partnerships in Pacific history. They were, in a sense, the first generation of American-born Hawaiians, neither fully Western nor fully Hawaiian, navigating between two cultures with the adaptability that would characterize their business careers.

The missionary families occupied a peculiar position in Hawaiian society. They came to save souls but quickly recognized that the islands offered something else entirely: extraordinary agricultural potential. Hawaii's volcanic soil, abundant rainfall, and tropical climate made it ideal for sugarcane, and global demand for sugar was exploding.

By the mid-nineteenth century, the sons and grandsons of missionaries were transitioning from saving Hawaiians to employing them, trading spiritual authority for economic power. It was a pivot that later generations would view with deep ambivalence, but at the time, it seemed a natural extension of the civilizing mission that had brought their parents to the islands.

In 1870, Alexander and Baldwin purchased 561 acres of land on Maui, between the towns of Pa'ia and Makawao, and began cultivating sugarcane under the name Samuel T. Alexander & Co. They were not the first sugar planters in Hawaii, but they would become among the most important, thanks to an engineering marvel that changed the economics of Maui agriculture forever.

Central Maui's plains were fertile but dry. The rain fell in the windward forests on the slopes of Haleakala, miles from where it was needed. Samuel Alexander conceived an audacious solution: a 17-mile irrigation aqueduct, the Hamakua Ditch, that would divert water from the rain-soaked eastern slopes across ravines, through lava rock, and into the arid central valley. His brother, Professor William D. Alexander, conducted the preliminary survey in 1873 and 1874, measuring the route with rods and twenty-foot chains because laser transits did not exist.

Alexander arranged financing from fellow planters, created the Hamakua Ditch Company, and negotiated a two-year construction lease from King David Kalakaua beginning September 30, 1876. What followed was an extraordinary feat of manual labor. Workers blasted tunnels through volcanic rock with pickaxes, working by candlelight and carbide lanterns. The system combined open channels, tunnels, and iron pipes.

The construction nearly killed Henry Baldwin, though not in the way anyone expected. In March 1876, just before work began, Baldwin's right arm was crushed between sugar mill cane rollers. The arm had to be amputated below the elbow. He was 33 years old.

A lesser man might have retreated. Baldwin did the opposite. At the treacherous Maliko Gulch, the deepest and most dangerous point on the route, workers refused to descend the steep walls. Baldwin, clutching a rope with his legs and his one remaining arm, scaled down the cliff face first, shaming the crew into following. The image of a one-armed man dangling over a Hawaiian gorge to build an irrigation ditch became part of A&B's founding mythology, and it was not mythology. It actually happened.

The Hamakua Ditch was completed in September 1878, within the two-year deadline, at a cost of $80,000. It could deliver 60 million gallons of water per day to the central Maui plains.

The impact was immediate and transformative. Overnight, thousands of previously unusable acres became some of the most productive sugar land in the Pacific. What had been dry scrubland became lush cane fields stretching across the valley. By 1908, the system had been incorporated into the larger East Maui Irrigation Company network, eventually spanning 74 miles of ditches, tunnels, pipes, flumes, and reservoirs with 388 stream intakes across 33,000 acres. It was one of the largest private water systems in the United States.

This was Alexander & Baldwin's founding innovation, and it established the template for everything that followed: control the critical resource, and you control the economy. Water was power, and A&B had it.

As the sugar industry matured, five companies emerged to dominate Hawaii's economy with a grip that would last nearly a century. Known as the Big Five, they were C. Brewer & Co., founded in 1826; Theo H. Davies & Co., founded in 1845; H. Hackfeld & Co., founded in 1849 and later renamed American Factors, or Amfac, after anti-German sentiment during World War I forced a rebrand; Castle & Cooke, founded in 1851; and Alexander & Baldwin, the youngest, founded in 1870.

Together, these five firms acted as agents for 36 of Hawaii's 38 sugar plantations and controlled an estimated 90 percent of the sugar business. Through interlocking directorates, intermarriage among founding families, and vertical integration, their influence extended to wholesale and retail commerce, banking, shipping, telecommunications, media, and even law enforcement. Ninety percent of retail stock in the islands passed through their warehouses. It was not just an oligopoly. It was a parallel government.

The Big Five's power was so comprehensive that it helped topple a monarchy. On January 17, 1893, a group of American sugar planters under Sanford Ballard Dole, himself born in Honolulu to missionary parents, overthrew Queen Lili'uokalani and established a provisional government. The Committee of Safety that orchestrated the coup was composed primarily of haole professionals, missionary descendants, and sugar planters, supported by U.S. Marines from the USS Boston stationed in Honolulu Harbor.

Five years later, despite fierce opposition, including a petition signed by 21,269 Native Hawaiians, the United States annexed Hawaii through a Joint Resolution of Congress on July 7, 1898, bypassing the two-thirds Senate vote required for a treaty. The primary driver was sugar: annexation meant Hawaiian sugar could enter the U.S. mainland duty-free. The political machinations of the sugar planters had reshaped the sovereignty of an entire nation to optimize their trade economics. It remains one of the most consequential examples of corporate influence over foreign policy in American history.

The men who built A&B were not passive beneficiaries of this power structure. They were architects of it. And the system they helped create, missionary sons converting spiritual authority into economic control, converting land and water into sugar and wealth, would define Hawaii's political economy for the next six decades. The wealth was real. The consequences were lasting. And the moral complexity of that legacy would haunt A&B well into the twenty-first century.

III. Building the Empire: Shipping, Land & The Matson Connection (1900-1950)

By the turn of the twentieth century, Alexander & Baldwin had established itself as the youngest but arguably most ambitious of the Big Five. Sugar was the engine, but the founders understood something that many commodity producers never grasp: controlling the supply chain matters as much as controlling the crop.

The problem was shipping. Hawaii sits in the middle of the Pacific Ocean, and every pound of sugar produced on the islands had to travel roughly 2,400 miles to reach its primary market on the U.S. mainland. Whoever controlled the ships controlled the margins. Captain William Matson had founded Matson Navigation Company in 1882, sailing his three-masted schooner Emma Claudina into Hilo Bay carrying merchandise and plantation stores, returning with cargoes of sugar. By the early 1900s, Matson's shipping line had become critical infrastructure for the Hawaiian economy, not just for sugar but for virtually every consumer good that reached the islands.

Think about the strategic geometry. Hawaii imports roughly 85 to 90 percent of its food and consumer products. Every gallon of milk, every car, every roll of toilet paper arrives by ship. Controlling the dominant shipping line between the mainland and Hawaii was not merely a vertical integration play for A&B's sugar. It was a toll booth on the entire Hawaiian economy. Matson grew from a single schooner into a fleet of steamships and eventually container vessels, pioneering innovations in Pacific shipping including the introduction of containerized cargo that dramatically reduced freight costs and handling time.

A&B recognized the strategic value early. In 1908, the company invested $200,000 to acquire a minority interest in Matson, beginning a financial relationship that would last over a century. This was vertical integration in its purest form: own the fields, own the mills, own the ships. Over the following decades, A&B steadily increased its stake. In 1964, A&B bought out the interests held by three fellow Big Five competitors, American Factors, C. Brewer, and Castle & Cooke, consolidating its position. By 1969, A&B had purchased all remaining outstanding shares, making Matson a wholly owned subsidiary. The sugar planter now controlled the dominant shipping line between Hawaii and the mainland, a position of extraordinary strategic leverage. Matson was not just carrying A&B's sugar; it was carrying Hawaii's lifeblood.

Simultaneously, A&B was accumulating land at a pace that only makes sense in the context of Hawaii's unique geography and political economy. The islands have a fixed supply of land, roughly 4.1 million acres total, and much of it is mountainous, volcanic, or otherwise undevelopable. Every acre acquired was an acre that could never be replicated.

Through plantation operations, strategic purchases, and the peculiarities of Hawaii's land tenure system, which traces back to the Great Mahele of 1848 when King Kamehameha III redistributed land ownership, A&B amassed holdings that eventually exceeded 87,000 acres, primarily on Maui and Kauai. Much of this land was held for sugar cultivation, but its long-term value would prove to be something else entirely.

The Great Mahele deserves a moment of explanation because it is the origin of modern land ownership in Hawaii and, by extension, the foundation of A&B's wealth. Prior to 1848, all land in Hawaii was held communally under the authority of the king. The Mahele divided land among the king, the chiefs, and the government, and a subsequent act in 1850 allowed commoners to claim small plots called kuleana.

But the process was confusing, poorly communicated, and conducted in a legal framework alien to Hawaiian culture. The concept of private land ownership had no equivalent in traditional Hawaiian society, where land was not "owned" but "used" under a system of reciprocal obligations between chiefs and commoners. Many Native Hawaiians never filed claims, either because they did not understand the process or because the concept itself was foreign to their worldview.

Foreign landowners, including missionary families, understood the Western legal system and moved aggressively to acquire title. Within a generation, the majority of Hawaii's arable land had passed into the hands of a small number of non-Hawaiian owners. The land that A&B would accumulate over the following century was, in many cases, acquired at prices and under conditions that reflected this fundamental imbalance. This history remains deeply contested in Hawaii and underpins the ongoing sovereignty movement and land claims disputes that continue to affect companies like A&B.

Hawaii's annexation in 1898 had removed tariff barriers, supercharging the sugar industry. The territorial period that followed, lasting from 1900 to 1959, was the golden age of Big Five dominance. The plantation owners used their power to maintain Hawaii's territorial status, which limited democratic self-governance and allowed the oligarchy to operate with minimal interference from Washington.

The plantation economy created a unique social structure: a small elite of haole, or white, managers and owners presiding over a diverse labor force recruited from Japan, China, the Philippines, Portugal, and Korea. The planters deliberately recruited from multiple countries, reasoning that ethnic diversity among workers would prevent unified labor organizing. Workers who spoke different languages and came from different cultures were less likely to unite against management. This multicultural labor force, working side by side in the cane fields, would eventually transform Hawaii into the most ethnically diverse state in America, an unintended consequence of the planters' search for cheap, divided labor.

Plantation life was a world unto itself. Each plantation operated as a self-contained community with company housing, a company store, a company school, and a company hospital. Workers were paid in scrip redeemable only at the company store, a system that kept them economically dependent on the plantation.

Housing was segregated by ethnicity, with Japanese, Filipino, Chinese, and Portuguese workers living in separate camps, another divide-and-conquer strategy. The plantation manager, invariably haole, functioned as a feudal lord, with authority over virtually every aspect of workers' lives. Workers could be evicted from company housing for insubordination. Their children attended company schools. Their medical care came from company doctors. It was paternalistic, exploitative, and, for the Big Five, enormously profitable. The system bore more resemblance to a feudal estate than to a modern corporation.

World War II changed everything. The attack on Pearl Harbor on December 7, 1941, transformed Hawaii from a sleepy plantation territory into the command center of the Pacific war. Martial law was declared and did not fully end until October 1944. Military spending flooded the islands, new industries emerged, and the political dynamics shifted irrevocably.

The war demonstrated that Hawaii's non-white population was not merely a labor pool but a community of citizens capable of extraordinary courage and sacrifice. Returning veterans of Japanese descent, many of whom had served with extraordinary distinction in the 442nd Regimental Combat Team, the most decorated unit of its size in U.S. military history, entered politics and challenged the Big Five's grip on power. These veterans had fought and bled for their country while their families were suspected of disloyalty back home. They were not going to return to the plantation hierarchy.

The rise of labor unions, particularly the International Longshoremen's and Warehousemen's Union, further eroded plantation owners' control. The ILWU organized across ethnic lines, something the Big Five had spent decades trying to prevent, and the 1946 sugar strike, in which 26,000 workers walked off the job for 79 days, signaled that the paternalistic plantation system was cracking. The strike was not just about wages. It was about dignity, equality, and the end of a feudal order.

When Hawaii finally achieved statehood on August 21, 1959, after a referendum in which 93 percent of voters supported it, the political landscape shifted decisively. The Big Five had actually resisted statehood for years, recognizing that full democratic governance would dilute their power. They were right. Democratic politicians, many of them veterans of Japanese ancestry led by figures like Daniel Inouye and Spark Matsunaga, dismantled the plantation oligarchy's political machinery. But the Big Five still held the land, the shipping lines, and the capital. A&B, with its Matson subsidiary providing essential ocean transportation and its vast Maui and Kauai holdings generating sugar revenues, entered the post-statehood era as one of Hawaii's most formidable economic forces.

The peak of this era, roughly the 1950s through the mid-1960s, represents A&B at maximum horizontal and vertical integration: growing the cane, milling the sugar, shipping it to market, and controlling the land beneath it all. It was a beautiful closed loop. It was also completely dependent on a single commodity whose economics were about to collapse.

IV. The Long Decline: Sugar's Slow Death (1960s-1990s)

The first cracks in the sugar economy did not arrive with a dramatic crash. They arrived slowly, almost imperceptibly, like termites in a wooden house. You could ignore the damage for years, even decades, before the structure became unsound.

The forces were structural and relentless. Labor costs in Hawaii were among the highest in the sugar world, driven by unionization, the cost of living on an isolated island chain, and the post-statehood political empowerment of plantation workers who were no longer willing to accept subsistence wages.

Meanwhile, sugar producers in Brazil, Thailand, India, Australia, and the Caribbean could operate at a fraction of Hawaii's cost. A plantation worker in Brazil earned a fraction of what a unionized HC&S employee earned on Maui. Brazilian land was cheaper, more abundant, and closer to major markets. The end of preferential U.S. tariff treatment, which had been the original economic justification for annexation, removed the last artificial advantage that Hawaiian sugar held over global competitors. By the 1970s, the math was simple and brutal: it cost more to grow sugar in Hawaii than the sugar was worth on the open market. The commodity that had built fortunes, toppled monarchies, and reshaped the demographics of an entire archipelago was now a money-losing operation sustained by inertia and sentiment.

A&B faced the classic strategic dilemma that confronts every company dependent on a declining core business. When do you diversify? When do you defend? And how do you know the difference between a temporary downturn and a permanent decline? The answers, in retrospect, seem obvious. In real time, they were agonizing.

The company's first significant pivot came not through diversification but through divestiture. In a paradox that illustrates the complexity of A&B's strategic evolution, 1969 was the year A&B completed its acquisition of all remaining Matson shares, making the shipping line a wholly owned subsidiary at the very moment when the logic of that integration was beginning to unravel.

The logic of owning both a sugar company and a shipping line was powerful when sugar dominated Hawaii's economy, but as sugar declined, the two businesses increasingly pulled in different directions. Matson was a thriving, growing transportation company with potential far beyond hauling sugar. A&B's sugar operations were a drag on capital and management attention.

Through the 1970s and 1980s, A&B made tentative moves toward real estate development and tourism-adjacent businesses, leveraging its enormous land holdings on Maui and Kauai. Hawaii's tourism industry was booming, driven by jet travel, the romanticization of the islands in popular culture, and Japan's economic miracle, which produced a wave of Japanese tourists and investors. The strategic logic of converting plantation land into resort and residential developments was obvious.

But these early diversification efforts were logical yet half-hearted, constrained by the institutional culture of a sugar company and a board still populated by descendants of the founding families. There was an emotional attachment to sugar that transcended financial logic. The cane fields were not just a business. They were an identity, a connection to the founders, a way of life for thousands of families across the islands. Shutting down a plantation meant not just closing a business but erasing a community.

The environmental and social pressures mounted in parallel. A&B's East Maui Irrigation system, the descendant of the original Hamakua Ditch, diverted millions of gallons of water daily from over 100 streams across 33,000 acres of public land. At peak operation, the system captured around 134 million gallons per day in winter and 268 million gallons per day in summer through 388 stream intakes.

This massive diversion devastated native stream ecosystems and harmed Native Hawaiian families who relied on kalo, or taro, farming and traditional gathering practices. Between the 1880s and 1980s, taro farming in the affected area declined from several hundred acres to just 20 acres. Streams that had flowed for millennia went dry. Native fish and shrimp populations collapsed. The water that built A&B's sugar empire came at a cost that was measured in the destruction of indigenous agriculture and ecosystems.

Failed diversification attempts peppered this era. Coffee, macadamia nuts, and other tropical agriculture were explored and found wanting. None could match sugar's scale, and A&B lacked expertise in these crops. The company was trapped in a familiar pattern: too attached to the old business to commit fully to the new, too aware of the old business's decline to ignore the problem entirely.

The water rights issue deserves deeper examination because it became a defining legal and moral challenge that persisted for decades. In 2001, the Hawaii Supreme Court established that the public trust doctrine applies to water resources, opening the door for legal challenges to A&B's century-old stream diversions. In 2018, after a 17-year legal battle, the state Commission on Water Resource Management ordered full restoration of flows to 10 streams for taro growing and limited or eliminated diversions on another 7 streams to restore habitats. In 2021, a Hawaii judge ordered A&B to limit its East Maui diversions to no more than 25 million gallons per day, a small fraction of the historical take that had once exceeded 200 million gallons daily. And in 2022, in the case of Carmichael v. BLNR and Alexander & Baldwin, the Hawaii Supreme Court found that the state had violated water leasing law by allowing A&B to divert water from state land for years without environmental review. The water saga was not just a legal headache. It was a moral reckoning. The same ditch that Henry Baldwin had risked his life to build had, over a century, drained the lifeblood from Native Hawaiian agricultural communities. The irrigation system that created A&B's wealth had destroyed someone else's livelihood. Understanding this tension is essential to understanding why A&B's transformation was not just a financial exercise but a social one.

Plantations closed one by one through the 1980s and 1990s, each closure eliminating hundreds of jobs and erasing communities that had existed for generations. The closures were not limited to A&B. Across Hawaii, the sugar industry was collapsing. Oahu's last plantation closed. Kauai's operations wound down. The Big Island's mills went silent. C. Brewer closed its last plantation. Even Amfac, which had been acquired by JMB Realty for $920 million in 1988, could not escape the gravitational pull of sugar's economics: its Hawaiian operations eventually filed for bankruptcy in 2002. By the early 2000s, only one sugar plantation remained in all of Hawaii: A&B's Hawaiian Commercial & Sugar Company, or HC&S, on the central Maui plains that the Hamakua Ditch had irrigated since 1878.

The fact that A&B held on the longest is both admirable and damning. Admirable because the company bore the social costs of being Maui's largest private employer long after the economics justified closure. Damning because every year of subsidized sugar operations was a year of capital that could have been deployed into higher-returning real estate investments. The opportunity cost, while impossible to calculate precisely, was enormous. If A&B had exited sugar in 2000 and redeployed that capital into Hawaii commercial real estate at the bottom of a cycle, the returns would have been transformative.

The final chapter played out with the slow inevitability of a Greek tragedy. On January 6, 2016, A&B announced that HC&S would close, citing roughly $30 million in agribusiness operating losses in 2015 with forecasts of continued significant losses. Six hundred and seventy-five employees would be laid off in phases from March through December. In December 2016, the Pu'unene Mill processed its final harvest, ending over 145 years of continuous sugar cultivation on those Maui lands. The last cane field was burned, the last mill run completed, and the sugar era in Hawaii was officially over.

The closure rippled through Maui's economy and psyche. For generations, the rhythm of plantation life had defined central Maui: the burning of cane fields before harvest, which would send columns of ash drifting across the island; the sweet, heavy smell of the mill processing raw cane into sugar; the whistle that marked the beginning and end of each shift. These sensory markers of a way of life vanished overnight. Some workers found positions in A&B's growing real estate operations. Others retrained. Many left Maui entirely. The transition was managed with more care than most plantation closures, including severance packages and job placement assistance, but it was still the end of an era.

It had taken A&B decades to make a decision that, in purely financial terms, should have been made years or even decades earlier. The cost of that delay, measured in accumulated operating losses, management distraction, and foregone investment in higher-return opportunities, was enormous. But the human cost of the decision itself was real too: lost jobs, lost communities, lost identity. Business strategy textbooks rarely account for the weight of 145 years of history pressing down on a boardroom table.

V. The Lost Decades: Identity Crisis & Poor Capital Allocation (2000-2013)

By the turn of the millennium, Alexander & Baldwin was a company that no longer knew what it was. The sugar business was hemorrhaging money. The real estate holdings were vast but underutilized. The Matson shipping subsidiary was valuable but strategically unrelated to everything else. And a series of acquisitions and diversification attempts had created a conglomerate so unfocused that Wall Street could not figure out how to value it.

This is the period that institutional investors sometimes call the "stranded conglomerate discount." Think of it as a department store analogy: imagine a retailer that simultaneously sold luxury watches, discount groceries, and auto parts. Each department might be individually profitable, but no customer would shop there and no investor would know how to value it.

A&B owned genuinely valuable assets: tens of thousands of acres of irreplaceable Hawaiian land, a dominant shipping position, and a portfolio of commercial properties. But the market could not see the value because it was buried inside a corporate structure that made no strategic sense. The company was simultaneously a money-losing sugar producer, a shipping company, an asphalt paver, a real estate developer, and a landlord. No analyst could model it. No investor could understand it. And no multiple could properly capture the sum of the parts.

The stock price reflected this confusion. Through much of the 2000s and early 2010s, A&B traded at a persistent discount to any reasonable sum-of-the-parts valuation. The Matson shipping business alone, as an independent entity, might have been worth more than A&B's entire market capitalization. The land, carried on the balance sheet at historical cost from decades or even a century ago, was vastly understated relative to its market value.

But investors could not unlock these values because they were trapped inside a conglomerate that showed no signs of simplifying. The irony was painful: A&B owned some of the most valuable real estate in the Pacific, but its stock traded as though the company were a struggling agricultural business with some real estate on the side.

The financial crisis of 2008 and 2009 hit Hawaii particularly hard. The state's economy, heavily dependent on tourism and real estate, contracted sharply. Hotel occupancy plummeted. Property values declined. Construction projects stalled. A&B's already-struggling sugar operations faced even worse economics, and its real estate development pipeline slowed to a crawl. The crisis exposed the fragility of a business model that depended on so many different operations performing simultaneously in an economy with a narrow economic base.

Meanwhile, the Kukui'ula development on Kauai illustrated both the ambition and the risk of A&B's real estate strategy during this period. In 2002, A&B had partnered with Arizona-based DMB Development to create a 1,000-acre master-planned resort residential community on Kauai's south shore near Poipu. The project featured a golf course, a $100 million private club and spa, and a retail center, with over 280 lots eventually sold and 125 homes completed. Kukui'ula was a trophy asset, but it was also a capital-intensive, long-cycle development project that tied up resources and management attention for nearly two decades before A&B and DMB eventually sold it to Brue Baukol Capital Partners in November 2021 for $183.5 million, retaining only the retail center.

In June 2013, A&B made what appeared to be a bold diversification move: it acquired Grace Pacific Corporation, Hawaii's preeminent infrastructure company specializing in aggregate, hot mix asphalt, and road construction, for approximately $277 million, roughly $235 million in stock and cash plus $42 million in assumed net debt. Grace Pacific had been founded in Hawaii in 1931 and was a well-known local brand. The acquisition thesis was reasonable on its face: Hawaii's infrastructure needs were growing, construction spending was recovering, and Grace Pacific would provide diversified cash flows alongside A&B's real estate operations. But the deal would ultimately prove to be a case study in the perils of acquisition-driven diversification. A&B paid a premium price for a business in a cyclical industry it did not deeply understand, and the timing was imperfect. The road paving business has fundamentally different economics from real estate: it is project-based, labor-intensive, and subject to government budget cycles. A&B was adding complexity to a company that already had too much of it.

The leadership question loomed large during this period. A&B's board composition reflected the tension between family legacy and professional management that plagues many multi-generational companies. The founding families' influence, while diminished from the days when missionary descendants personally ran the operations, still shaped corporate culture and strategic decision-making. There was an institutional reluctance to make the radical moves that the situation demanded. Analysts and investors who met with management during this period describe a company that was aware of the problem but seemingly paralyzed by its own history.

Christopher J. Benjamin represented the new guard. He had joined A&B in 2001 as Director of Corporate Development and Planning, risen to CFO from 2004 to 2011, and then became President and COO. Benjamin was an insider who understood the company's assets intimately but was not burdened by the emotional attachment to sugar that constrained earlier leadership. He brought a capital allocator's mindset to a company that desperately needed one. His background in corporate development meant he thought in terms of returns on capital, asset optimization, and portfolio rationalization rather than crop yields and plantation traditions.

The strategic reviews of this period produced a simple but uncomfortable conclusion: A&B was worth more in pieces than it was whole, and the market was right to apply a conglomerate discount. The question was whether management had the courage to act on that conclusion, to systematically dismantle a 140-year-old corporate structure and rebuild it around a single strategic thesis. What was A&B, really? The answer, buried under layers of history, sentiment, and organizational inertia, was staring everyone in the face: it was a landowner. Everything else was a distraction.

VI. The Great Transformation: Going All-In on Hawaii Real Estate (2012-2018)

The transformation of Alexander & Baldwin from a diversified conglomerate into a focused commercial real estate company was not a single decision. It was a series of increasingly bold moves executed over roughly six years, each one removing a layer of complexity and bringing the company closer to its essential identity as Hawaii's landlord. If the lost decades were about indecision, the transformation years were about ruthless clarity.

The first and arguably most important move came on June 29, 2012, when A&B and Matson formally separated in a tax-free spin-off. Shareholders received one share of each company for every share they previously held. Matson, now trading independently under the ticker MATX, became a focused ocean shipping and logistics company, the leading carrier to Hawaii and Guam. A&B retained its real estate, agricultural, and other operations.

The separation ended a 104-year financial relationship that had begun with a $200,000 investment in 1908. It was the corporate equivalent of cutting an umbilical cord, and both companies thrived as a result. Matson, freed from the conglomerate structure, could pursue its own growth strategy and has since grown its market capitalization to several times what it was as a subsidiary. A&B, freed from the distraction of a shipping subsidiary, could focus on the question of what to do with its land. The spin-off was a textbook example of how corporate simplification unlocks value: the sum of the parts, trading independently, was immediately worth more than the whole.

Christopher Benjamin was promoted to CEO effective January 1, 2016, inheriting a mandate that was now clear even if it remained painful: transform A&B into a pure-play Hawaii commercial real estate company. The timing was deliberate. The HC&S sugar closure, announced just days later on January 6, was the first major act of Benjamin's tenure. After 146 years, A&B was out of the sugar business. It was an emotional moment for the company, for Maui, and for Hawaii. But it was the necessary predicate for everything that followed.

With sugar behind it, A&B began a methodical portfolio rationalization that was remarkable for its speed and decisiveness. Consider what the company accomplished in roughly six years: it spun off a century-old shipping subsidiary, shut down a 146-year-old sugar operation, sold its entire mainland real estate portfolio, converted its corporate structure to a REIT, and exited agribusiness. Each of these moves individually would be considered a major corporate event. Together, they constitute one of the most complete corporate transformations in American business history.

The mainland real estate sales were perhaps the most telling strategic decision. A&B had accumulated a portfolio of commercial properties across the western United States, in states like California, Texas, and Colorado. These were perfectly fine assets generating reasonable returns. But Benjamin and his team recognized something that many diversified real estate companies fail to grasp: being a good landlord in a competitive market is not the same as being a great landlord in a monopolistic one. A&B had no competitive advantage owning commercial real estate in markets where it was one of thousands of landlords. In Hawaii, it was one of a handful, operating in a supply-constrained market where its 150-year history, local relationships, and institutional knowledge provided genuine moats. The mainland portfolio generated approximately $600 million in proceeds, which were reinvested in Hawaii assets, effectively concentrating A&B's capital in the market where its returns on investment would be highest.

In July 2017, A&B's board approved the company's conversion from a C-Corporation to a Real Estate Investment Trust. For non-financial readers, a REIT is a corporate structure that allows a company to avoid paying corporate income tax in exchange for distributing at least 90 percent of its taxable income to shareholders as dividends. This is why REITs typically offer higher dividend yields than other stocks: they are essentially required to pass through their profits. For A&B, the REIT conversion formalized its identity as a real estate company, attracted a new class of income-oriented investors, and aligned management's incentives with the new strategic focus. It was also an irreversible commitment: once you convert to a REIT, going back to a C-Corp is complex and tax-disadvantageous, meaning the conversion was a one-way door that locked in the transformation.

The year 2018 was the transformative crescendo. In rapid succession, A&B executed several major transactions that completed the metamorphosis. The company exited agribusiness entirely. In December 2018, A&B sold 41,000 acres of former HC&S sugar fields to Mahi Pono LLC, a joint venture between Pomona Farming of California and Canada's Public Sector Pension Investment Board, for $262 million. The sale ensured that the land would remain in agricultural use, a condition that was both a contractual requirement and a political necessity given community sensitivity about the disposition of former plantation land, while freeing A&B from the operational burden and financial losses of farming.

The strategic clarity was now unmistakable: "We are Hawaii's premier commercial real estate company." No more sugar. No more mainland properties. No more diversified confusion. A&B would own, operate, and develop commercial real estate in Hawaii, period.

Management's bet rested on a simple thesis: Hawaii's land scarcity, combined with regulatory barriers to new development, demographic tailwinds, and the islands' unique economic position, would give A&B pricing power that mainland landlords could only dream of.

Consider the math. The state has roughly 4.1 million acres of total land, much of it mountainous, volcanic, or protected by conservation designations. Only a fraction is zoned for commercial use. The entitlement process for new development takes years, sometimes decades, of environmental reviews, community hearings, and regulatory approvals. Cultural and political barriers make it extremely difficult for mainland REITs to enter the market. A&B, with its 150-year presence, local relationships, and deep understanding of Hawaii's regulatory landscape, was uniquely positioned to capitalize on these constraints. If you own a grocery-anchored shopping center in a market where no one can build a competing center, your pricing power approaches that of a monopolist. That was the bet.

The transformation also required A&B to navigate the shift from sugar fields to development projects, a process that involved complex entitlement battles, environmental reviews, and community relations. Converting agricultural land to commercial use in Hawaii is not a matter of simply rezoning a parcel the way it might be on the mainland.

In Hawaii, the process involves negotiating with Native Hawaiian cultural practitioners who may have ancestral connections to the land, environmental groups concerned about endangered species and watershed protection, community organizations representing local residents, and multiple layers of state and county government with overlapping jurisdictions. Archaeological surveys are required. Water availability must be demonstrated. Traffic impact studies must be completed. The process can take five to ten years from initial application to first building permit. A&B's institutional knowledge of this process, accumulated over decades, was itself a competitive advantage that no new entrant could easily replicate.

The human dimension of this transformation should not be understated. Benjamin and his team had to convince employees, board members, and community stakeholders that abandoning 146 years of agricultural identity was not a betrayal but an evolution. They had to persuade investors that a small-cap Hawaii REIT deserved a premium valuation.

And they had to execute flawlessly, because the margin for error in a market as small and interconnected as Hawaii is essentially zero. Everyone knows everyone. Reputations are long. A botched development project or a community relations failure would follow A&B for decades. The company could not simply move to a different market if things went wrong. This was it. Hawaii was the only game, and there were no do-overs.

VII. The New Alexander & Baldwin: Hawaii's Landlord (2018-Present)

The company that emerged from the transformation bore little resemblance to the sugar conglomerate of even a decade earlier. By 2024, A&B's commercial real estate portfolio consisted of approximately 4.0 million square feet of leasable commercial space: 21 retail centers, predominantly grocery-anchored; 14 industrial assets; 4 office properties; and 146 acres of ground lease assets. The company remained one of Hawaii's largest private landowners, with approximately 87,000 acres across the state, concentrated on Maui at roughly 65,000 acres and Kauai at over 21,000 acres, though much of this acreage was conservation or agricultural land rather than developable commercial property.

The portfolio composition reflected a deliberate strategic choice. A&B's retail centers were not high-end malls dependent on tourist foot traffic. They were neighborhood shopping centers anchored by grocery stores, pharmacies, and essential services, the kind of tenants that prove resilient in economic downturns because people still need to eat and fill prescriptions regardless of whether tourists are visiting. A&B became the largest owner of grocery-anchored shopping centers in Hawaii, a niche position that combined defensive characteristics with the scarcity value of Hawaiian real estate.

The industrial portfolio deserves particular attention because it represents the fastest-growing segment of A&B's business. Hawaii's industrial real estate market is extraordinarily tight, with vacancy rates consistently among the lowest in the nation. The islands need warehouse and distribution space to serve a population that imports nearly everything it consumes, but there is very little developable land zoned for industrial use. A&B's industrial properties, including the Komohana Industrial Park and Maui Business Park developments, serve this undersupplied market. As e-commerce penetration increases in Hawaii, the need for local last-mile distribution facilities grows, creating a structural tailwind for industrial landlords.

Ground leases represent another distinctive feature of A&B's portfolio. In a ground lease structure, A&B retains ownership of the land and leases it to a tenant who constructs and owns the building. When the lease expires, typically after 55 to 65 years, the improvements revert to the landowner. This structure generates steady income with minimal capital investment from A&B and creates an asset that appreciates over time as the lease term diminishes and the land value increases. It is, in essence, a way to monetize land without selling it, preserving optionality while generating income. A&B holds 146 acres of ground lease assets, a meaningful component of its portfolio.

The COVID-19 pandemic in 2020 served as the first real stress test for the new A&B. Hawaii's tourism industry collapsed virtually overnight, with visitor arrivals dropping by more than 70 percent. Governor David Ige imposed a mandatory 14-day quarantine on all arriving travelers, effectively shutting down the state's largest industry. Hotels emptied. Restaurants closed. Airlines slashed service.

For a company that had historically been associated with tourism-dependent Hawaii, this should have been devastating. Instead, A&B demonstrated the wisdom of its strategic repositioning. Only about 7 percent of A&B's retail portfolio was tied to resort or tourism-dependent locations. The rest served local communities with essential goods and services. The company deferred rent in 199 cases valued at $5.9 million and modified 107 leases, but it earned a modest profit of $5.2 million in 2020, a year when many REITs posted significant losses. Land sales at Maui Business Park actually maintained strong momentum throughout the pandemic.

It was a quiet vindication of the transformation thesis: essential retail in a supply-constrained market holds up even when the broader economy does not. A tourist-dependent landlord in Waikiki would have been devastated. A grocery-anchored landlord in Kahului was fine. The difference was entirely a function of strategic positioning.

The Maui wildfires of August 2023 presented a different kind of test, one that struck at the very heart of A&B's historical identity. On August 8, wind-driven fires fueled by hurricane-force winds and invasive grasses devastated the historic town of Lahaina, destroying more than 2,200 structures, killing 102 people, and causing an estimated $5.5 billion in damage. It was the deadliest wildfire in the United States in over a century.

The Baldwin Home Museum, built in 1835 and originally the residence of founder Dwight Baldwin, was burned to ashes, a poignant symbol of the destruction. The very house where Henry Baldwin had grown up, the starting point of the A&B story, was gone. A&B's direct property exposure was limited since none of its commercial centers were in the Lahaina burn zone, but the fires created broader challenges including rising insurance premiums across Hawaii and disruptions to the Maui economy that affected tourism-dependent businesses across the island.

A controversial dimension of the wildfire aftermath involved water. The day after the fires started, A&B and the Board of Land and Natural Resources filed a petition in the Hawaii Supreme Court arguing there was insufficient permitted water to battle the wildfires in Upcountry Maui, asking to overturn a June 2023 court decision that had limited A&B's stream diversions. Water rights advocates criticized the move sharply, arguing that A&B was exploiting a tragedy to relitigate long-standing water diversion disputes. The episode illustrated the enduring tension between A&B's economic interests and its social license to operate in Hawaii.

Benjamin completed his tenure as CEO on June 30, 2023, having accomplished the strategic transformation that defined his leadership. Lance K. Parker, born and raised in Hawaii, succeeded him as President and CEO effective July 1, 2023. Parker had joined A&B in 2004, worked his way through acquisition and development roles, and was named COO in 2021 and President in early 2023. His mandate was execution and optimization, taking the streamlined platform Benjamin had built and maximizing its value through disciplined operations, strategic acquisitions, and development of the existing land bank.

Under Parker's leadership, A&B delivered solid operational results. Full-year 2024 figures showed net income of $60.5 million. Funds from operations, the metric that real estate investors use instead of earnings per share because it adds back depreciation to reflect the fact that well-maintained real estate does not actually lose value the way a factory or a machine does, reached approximately $1.37 per diluted share. Leased occupancy stood at 94.6 percent. Same-store net operating income, which measures the performance of properties the company has owned for at least a year and is the single most important metric for evaluating a landlord's organic growth, grew 2.4 percent, or 2.9 percent excluding collections of prior-year reserves.

Comparable leasing spreads, which measure the difference between new lease rates and expiring lease rates on the same space, were a healthy 11.7 percent blended, with retail at 13.5 percent and industrial at 7.4 percent. In plain language, when a tenant's lease expired and they signed a new one, A&B was charging roughly 12 percent more for the same space. That is a direct measure of pricing power, and it reflects the supply-demand imbalance in Hawaii's commercial real estate market. These are not spectacular growth-company numbers, but they reflect the steady, defensive characteristics of a well-positioned landlord in a supply-constrained market.

Through the first three quarters of 2025, performance accelerated. Same-store NOI growth reached 4.2 percent in the first quarter and the company raised its full-year FFO guidance to $1.36 to $1.41 per diluted share, with same-store NOI growth guidance of 3.4 to 3.8 percent. Leasing spreads remained in double digits. The company also completed the sale of Grace Pacific in late 2023 for $57.5 million, roughly $220 million less than it had paid a decade earlier, a painful but necessary write-off that eliminated A&B's last non-real-estate operating business.

Then came the biggest development since the sugar closure.

On December 8, 2025, A&B announced a definitive merger agreement in which a joint venture formed by MW Group, Blackstone Real Estate, and DivcoWest would acquire all outstanding shares for $21.20 per share in an all-cash transaction, a 40 percent premium to the prior closing price, with an enterprise value of approximately $2.3 billion including debt. The deal is expected to close in the first quarter of 2026, with a special shareholder meeting to approve the merger scheduled for March 9, 2026.

The acquirers announced plans to retain A&B's name, brand, and Honolulu headquarters and to invest over $100 million to improve existing properties.

The going-private transaction represented a validation of the transformation strategy: the streamlined, pure-play Hawaii landlord that Benjamin and Parker had built was now attractive enough to command a significant premium from sophisticated institutional buyers. It also raised a question that long-term shareholders had been asking for years: had the public market ever truly appreciated the irreplaceable nature of A&B's Hawaiian land bank? The 40 percent premium suggested the answer was no.

VIII. Strategic Inflection Points Deep Dive

The decade from roughly 2012 to 2022 was the period that determined whether Alexander & Baldwin would survive as a relevant company or fade into irrelevance like most of its Big Five peers. This was A&B's existential decade, the window in which the company either transformed or died. Every major decision during this window involved trade-offs that looked very different in prospect than they do in retrospect.

The timing question is the one that business school case studies will debate for years. Should A&B have exited sugar in 1990, when the decline was already well advanced? In 2000, when operating losses were clearly structural? Was 2016, after 146 years, absurdly late?

The answer depends on how you weigh financial logic against social obligation and institutional identity. From a pure capital allocation standpoint, every year that A&B continued to operate HC&S after approximately 2000 was a year of value destruction. The $30 million in annual agribusiness losses reported in 2015 was not an anomaly. It was the culmination of decades of deteriorating economics. Cumulatively, the cost of holding on to sugar too long likely ran into the hundreds of millions of dollars in operating losses and foregone investment returns. If that capital had instead been deployed into Hawaii commercial real estate acquisitions during the 2008-2012 downturn, the returns would have been extraordinary.

But the counter-argument has merit too. HC&S employed hundreds of families on Maui. The plantation was not just a business but a community anchor. Closing it required A&B to navigate labor negotiations, community opposition, environmental remediation, and the political fallout of eliminating one of Maui's largest employers. The company that closed HC&S too abruptly would have faced a backlash that could have jeopardized its ability to develop the very land it was freeing up. Social license matters, especially in Hawaii, where community relationships are the currency of the realm.

The capital allocation lessons from this period are stark. The Grace Pacific acquisition in 2013 for $277 million stands as the clearest example of misguided capital allocation. It was sold in November 2023 for just $57.5 million, representing a destruction of roughly $220 million in shareholder value over a decade.

The thesis, that A&B should diversify into Hawaii infrastructure, was logical in theory but flawed in execution. Paving roads and producing asphalt are fundamentally different businesses from owning and managing commercial real estate. They require different skills, different capital structures, and different management attention. A&B was a landowner that briefly confused itself with a construction company. The market punished it accordingly. The Grace Pacific saga is a cautionary tale about the dangers of "adjacency" thinking in corporate strategy: just because two businesses operate in the same geography does not mean they belong in the same corporation.

The land bank insight is what makes A&B's story different from a generic conglomerate turnaround. Most companies in decline are sitting on depreciating assets: aging factories, obsolete technology, declining brand equity. A&B was sitting on appreciating ones. The 87,000 acres of Hawaiian land that had been used to grow sugar were, in many cases, worth far more as potential development sites, solar farms, industrial parks, and commercial properties than they ever were as cane fields.

The asymmetry was profound: the sugar business was destroying value, but the underlying asset was gaining value. The trick was recognizing this, killing the sugar business, and repositioning the land. It sounds simple. It took decades. And it required the intellectual honesty to admit that the thing the company had done for 146 years was no longer the best use of the thing the company owned.

What made the transformation possible was a confluence of factors that rarely align in corporate life. External pressure from investors who could see the hidden value forced management to confront the conglomerate discount. Leadership change brought in executives like Benjamin who were willing to act on the analysis rather than defer to tradition. A clear strategic vision, pure-play Hawaii commercial real estate, provided a north star that every subsequent decision could be measured against.

And, critically, there was a willingness to kill sacred cows: sugar, mainland properties, Grace Pacific, the conglomerate structure itself. Each divestiture faced internal resistance. Each required management to tell employees, community members, and longtime partners that a piece of A&B's identity was being sold or shut down. The emotional toll of this process should not be underestimated. But the alternative, continuing as a confused conglomerate trading at a persistent discount, was worse.

The counter-narrative is worth exploring. Did A&B leave money on the table by not developing its land bank more aggressively? Some observers argue that A&B has been too conservative, holding tens of thousands of acres in agricultural or conservation use when portions of that land could have been entitled and developed for commercial or residential purposes. The counter-counter-argument is that aggressive development in Hawaii carries enormous political and regulatory risk, and that A&B's patient approach has preserved relationships and optionality that a more aggressive developer would have destroyed. Under private ownership, with Blackstone's capital and longer time horizon, A&B may be able to pursue development opportunities that would have been difficult to justify to public market investors focused on quarterly returns.

The comparison to A&B's Big Five peers illustrates just how rare this kind of successful transformation is. C. Brewer, the oldest of the Big Five, voted to liquidate in 2001 and formally dissolved in 2006, a 175-year-old company simply ceasing to exist. Amfac, once the largest of the Big Five by revenue, was acquired by JMB Realty in 1988 for $920 million, filed Chapter 11 bankruptcy in 2002, and emerged as Kaanapali Land, a tiny OTC-traded shell owning about 5,000 acres on Maui, a shadow of its former self. Theo H. Davies was sold to Hong Kong's Jardine Matheson in 1973 and gradually dismembered over the following decades, its various divisions sold off piecemeal until little remained.

Castle & Cooke survived but in a very different form. Taken private by billionaire David Murdock, the company still controls large portions of Central Oahu. But its most famous transaction was the sale of nearly all of the island of Lanai to Oracle CEO Larry Ellison for approximately $500 million in 2012. That sale was emblematic of the Big Five's trajectory: once, these companies controlled entire islands; now, they were selling them to tech billionaires.

Of the original five companies that once controlled virtually the entire Hawaiian economy, only Alexander & Baldwin remained a publicly traded, Hawaii-focused operating company through 2025. The others dissolved, went bankrupt, were absorbed by foreign conglomerates, or retreated into private obscurity. A&B's survival is not merely satisfactory. It is extraordinary, and it is attributable to a single strategic insight that the others either missed or acted on too late: the sugar was worthless, but the land beneath it was priceless.

IX. The Playbook: Business & Strategic Lessons

Alexander & Baldwin's 155-year journey distills into a handful of strategic principles that apply far beyond Hawaii and far beyond real estate.

The most fundamental lesson is about long-term asset ownership. A&B accumulated land over generations not through any single brilliant acquisition but through patient, continuous aggregation. The founders acquired land to grow sugar. Their successors held it because it was producing. Their successors' successors held it because they could not imagine doing anything else.

And eventually, that land, which had been valued as agricultural commodity input, revealed itself to be something far more valuable: irreplaceable real estate in a supply-constrained market. The same phenomenon has played out with other long-duration landowners: the Church of England, the Crown Estate, Grosvenor Estates in London, and university endowments that have held urban land for centuries. The lesson is that owning hard assets in finite-supply environments creates optionality that compounds over very long time horizons, often in ways that the original acquirers never anticipated. The founders of A&B thought they were buying farmland. They were actually buying a perpetual option on Hawaiian development.

The second lesson concerns strategic focus and the cost of complexity. For decades, A&B operated as a conglomerate, diversified across sugar, shipping, paving, construction materials, mainland real estate, and agricultural experiments. The market applied a persistent discount to this structure because investors could not understand what they owned and could not value the individual pieces.

When A&B finally simplified to a single business, pure-play Hawaii commercial real estate, the market rewarded it with a clarity premium. The Blackstone-led going-private deal at a 40 percent premium to the prior stock price suggests that even after the simplification, the market may not have fully valued the underlying assets. The lesson is one that conglomerates chronically underestimate: the cost of complexity is not just operational. It is perceptual. If investors cannot understand you, they cannot value you, and if they cannot value you, you will trade at a discount to your intrinsic worth.

The commoditization trap is perhaps the most painful lesson in A&B's history. Sugar is the ultimate commodity: undifferentiated, globally traded, subject to tariff regimes and government subsidies, and producible at lower cost in dozens of other geographies. A&B had no pricing power in sugar, no differentiation, no moat. A pound of Hawaiian sugar is chemically identical to a pound of Brazilian sugar, and the Brazilian sugar cost less to produce and less to ship.

The only thing that made Hawaiian sugar competitive was preferential tariff treatment, and when that eroded, the business died. The contrast with A&B's current real estate business is instructive: commercial property in Hawaii offers significant pricing power because the supply is fixed, barriers to entry are extreme, and location is non-substitutable. No one can build a competing island. The lesson is that businesses built on commodity production without structural advantages will eventually be competed away, while businesses built on scarce, irreplaceable assets can sustain superior returns indefinitely.

The role of community relations as a competitive moat deserves particular attention. Operating in Hawaii requires what practitioners call social license, the tacit permission of the community, regulators, and cultural stakeholders to conduct business. A&B's 150-year presence, its deep relationships with community leaders, its institutional knowledge of Hawaiian land use law and entitlement processes, and its demonstrated willingness (however belated) to address community concerns about water rights and land use create barriers to entry that no mainland REIT can easily replicate.

The flip side of this moat is the obligation that comes with it: affordable housing pressure, Native Hawaiian land claims, water rights disputes, and the expectation that a company as embedded in Hawaii's history as A&B will contribute to the community's well-being, not just extract value from it. This is a moat that requires constant maintenance. Neglect the community relationship, and the social license evaporates, taking the development pipeline with it.

There is a myth versus reality dimension worth addressing here. The consensus narrative about A&B is that it was a sleepy, poorly managed conglomerate that finally woke up under activist pressure. The reality is more nuanced. A&B's management was not unaware of the strategic challenges. Internal discussions about exiting sugar, simplifying the portfolio, and focusing on real estate had been ongoing for years before the transformation actually occurred. What changed was not awareness but willingness, the willingness to bear the social and emotional costs of dismantling a 150-year-old institution. That willingness required the right combination of leadership, external pressure, and market conditions. It was not simply a matter of better management replacing worse management. It was a matter of the internal consensus finally catching up with the external reality.

The final lesson is about the courage to transform. A&B survived because, eventually, it was willing to kill its own history. It shut down sugar. It sold the shipping line. It dumped the construction company. It exited the mainland. It REIT-converted. Each of these decisions required overcoming institutional inertia, emotional attachment, and the very real human costs of eliminating businesses that employed people and defined communities. The companies that failed, C. Brewer, Amfac, Theo Davies, either could not make these decisions or made them too late. Legacy is powerful. It is also, when it prevents adaptation, lethal.

X. Porter's Five Forces & Hamilton's Seven Powers Analysis

Understanding A&B's competitive position requires examining the structural forces that shape its industry and the specific powers that protect its profitability. The frameworks of Michael Porter and Hamilton Helmer provide complementary lenses: Porter tells us about the industry structure, while Helmer tells us about the specific company advantages.

Starting with competitive rivalry: the commercial real estate market in Hawaii is characterized by remarkably low rivalry among landlords. Only a handful of major institutional owners operate at scale: Kamehameha Schools, one of the largest private landowners in Hawaii and a charitable trust established by Princess Bernice Pauahi Bishop; the Queen Emma Land Company; Castle & Cooke; and the State of Hawaii itself. This is not like the mainland, where thousands of REITs and private landlords compete aggressively for tenants and acquisitions. In Hawaii, the landlord community is small enough that the major players know each other, rarely compete head-to-head on the same deals, and operate in what amounts to a series of local oligopolies. Each island functions as a separate sub-market, and within each island, specific locations have only one or two institutional landlords. A&B's 11.7 percent blended leasing spreads in 2024 reflect this favorable dynamic: landlords in low-rivalry markets can push rents higher at lease renewal without losing tenants because there is simply nowhere else for those tenants to go.

The threat of new entrants is perhaps the single most favorable force in A&B's competitive environment. Hawaii's land supply is geologically fixed. You cannot manufacture more islands. The entitlement and permitting process for new commercial development takes years, sometimes decades, of environmental impact studies, community hearings, cultural assessments, and regulatory approvals. State and county regulations are among the most restrictive in the nation. And the cultural and political barriers for outsiders are substantial: mainland REITs have historically struggled to navigate Hawaii's unique regulatory and social landscape. When a mainland real estate company enters Hawaii, it faces a learning curve that involves not just different regulations but an entirely different set of stakeholder relationships: Native Hawaiian organizations, community advisory boards, environmental groups, and political entities that do not exist in the same form on the mainland. A local company with 150 years of relationships and institutional knowledge has an almost insurmountable advantage in the permitting process.

The threat of substitutes varies by property type. For essential retail, grocery-anchored shopping centers and service-oriented strip malls, substitution risk is low. This is a critical point that many mainland-focused analysts miss. People cannot buy groceries online in Hawaii the way they can on the mainland because shipping costs and delivery logistics make e-commerce fulfillment dramatically more expensive. Amazon Prime two-day delivery, which has decimated mainland retail, works differently in Hawaii: shipping a package across 2,400 miles of ocean adds significant cost and time. This insulates Hawaii's brick-and-mortar retail in a way that has no parallel on the mainland. Industrial and warehouse space faces minimal substitution risk and actually benefits from e-commerce growth, because online retailers need local fulfillment centers to serve the Hawaiian market. Office space carries higher substitution risk due to remote work trends, though A&B's relatively small office exposure, just 4 properties out of 39, limits this concern.

Supplier bargaining power is low. A&B owns the land, the primary input to its business. Construction labor and materials are commoditized, and while costs can be volatile, particularly in Hawaii where most materials must be imported by sea, they affect all developers equally and are ultimately passed through to tenants or capitalized into asset values.

Buyer bargaining power, meaning tenant power, is moderate but constrained by geography. Commercial tenants in Hawaii have some alternatives, but location-dependent businesses like grocery stores, pharmacies, and service providers have limited ability to relocate without losing their customer base. A Safeway that anchors a shopping center in Kihei, Maui, cannot move two miles down the road because there is no two-miles-down-the-road available. Long-term lease structures, typically five to ten years with annual escalators, reduce tenant leverage once a lease is signed. A&B's 94.6 percent leased occupancy rate indicates that the supply-demand balance favors the landlord.

Turning to Hamilton Helmer's Seven Powers framework, the analysis reveals one overwhelmingly dominant power and several supporting ones.

Cornered Resource is A&B's primary power, and it is overwhelmingly dominant. The company's 87,000 acres of Hawaiian land were accumulated over 155 years and literally cannot be replicated. There is no conceivable scenario in which a competitor could assemble a comparable land position in Hawaii. A new entrant would need to buy land from existing owners, none of whom are eager sellers, at current market prices rather than the historical costs at which A&B acquired its holdings decades or centuries ago.

The land was acquired at historical costs that bear no relationship to current market values, meaning A&B's cost basis is a fraction of replacement cost. This is the purest form of cornered resource: a finite, irreplaceable asset that was accumulated under historical conditions that no longer exist. In Hamilton Helmer's framework, cornered resources are the most durable of the seven powers because they cannot be replicated through competitive effort.

Switching Costs provide a meaningful secondary power. Commercial tenants who have built customer bases at specific locations, invested in tenant improvements, and established community presence face significant costs if they relocate. Ground leases, which A&B utilizes on 146 acres, create particularly strong lock-in because the tenant's improvements revert to the landowner at lease expiration.

Process Power provides a tertiary advantage. A&B's institutional knowledge of Hawaii's development and entitlement process, its relationships with regulators and community organizations, and its understanding of the cultural dimensions of Hawaiian land use represent accumulated know-how that competitors cannot easily replicate. This is not a dominant power, but it reduces execution risk on development projects and creates a meaningful advantage in the permitting timeline.

Scale Economies are moderate. Property management and corporate overhead benefit from scale, but real estate is inherently a local business, and A&B's 4 million square feet of commercial space is modest by mainland standards.

Network Effects are minimal. Tenants generally do not benefit from being in the same landlord's portfolio, though some retail clustering effects exist when complementary businesses colocate in the same shopping center.

Brand power is limited to regional recognition. Counter-Positioning is not applicable, as A&B follows a standard real estate operating playbook.

The dominant conclusion from both frameworks is that A&B's competitive position derives almost entirely from the irreplaceability of its land and the structural barriers to entry in the Hawaiian real estate market. This is a business where the asset itself is the moat. As long as Hawaii's geography does not change, and barring catastrophic climate events, these advantages are permanent.

XI. Bull vs. Bear Case & Investment Outlook

The Blackstone-led going-private transaction at $21.20 per share, representing a 40 percent premium and approximately $2.3 billion in enterprise value, effectively settled the near-term investment debate. But the strategic bull and bear cases remain relevant for understanding the long-term value proposition of Hawaii commercial real estate and A&B's position within it.

The bull case rests on structural scarcity. Hawaii's developable land supply is permanently constrained by geography, regulation, and cultural considerations. The state's population, while growing slowly, generates steady demand for essential retail and industrial space. Tourism recovery from the pandemic, despite setbacks from the Maui wildfires, continues to drive economic activity. The industrial and logistics segment benefits from a structural shift: as e-commerce penetration increases in Hawaii, the need for local warehouse and distribution space grows because the economics of shipping individual packages across 2,400 miles of ocean favor local fulfillment over direct-to-consumer shipping from the mainland.

The renewable energy opportunity is particularly interesting. A&B's former sugar lands on Maui and Kauai represent thousands of acres of flat, sun-exposed acreage with existing road access and utility connections, ideal for solar farms and battery storage facilities. A&B already has renewable energy roots: it operates hydroelectric plants on Kauai dating back over a century, a 6-megawatt solar farm at Port Allen, and a 28-megawatt solar farm with 100 megawatt-hour battery storage on Kauai that was, at its opening, the largest facility of its type in the world. Hawaii has among the highest electricity costs in the nation, creating strong demand for renewable generation. Leasing former agricultural land for solar installations converts non-revenue-generating acreage into long-term, inflation-protected income streams with minimal capital investment from A&B.

The bull case also argues that A&B has long traded at a discount to the intrinsic value of its land bank. The 87,000 acres are carried on the balance sheet at historical cost, which bears no relationship to current market values. This is a common issue in real estate companies: accounting rules require assets to be carried at cost less depreciation, but well-located real estate does not actually depreciate. It appreciates. The gap between book value and market value can be enormous, particularly for land that was acquired decades or a century ago.

The Blackstone consortium presumably saw this gap and priced their bid accordingly, though the 40 percent premium suggests they believe significant additional value remains to be captured through private ownership, where long-term development decisions do not need to satisfy quarterly earnings expectations.

Climate migration represents a speculative but plausible tailwind. As mainland coastal cities face increasing risks from extreme heat, hurricanes, and flooding, Hawaii's temperate climate and mid-Pacific location could attract remote workers and retirees seeking a more stable environment. Hawaii's strategic military importance as the headquarters of U.S. Indo-Pacific Command provides another layer of economic support. The growing geopolitical focus on the Indo-Pacific region, driven by the U.S.-China strategic competition, has increased military investment in Hawaii and is unlikely to diminish regardless of which party controls Washington.

The bear case is equally substantive and deserves equal weight. Hawaii's economy remains disproportionately dependent on tourism, which accounts for roughly a quarter of the state's GDP. This concentration makes the islands acutely vulnerable to external shocks. COVID demonstrated this with devastating clarity: when flights stopped, the economy collapsed overnight. A severe recession, a new pandemic, or a major geopolitical event that disrupted Pacific travel could repeat this pattern.