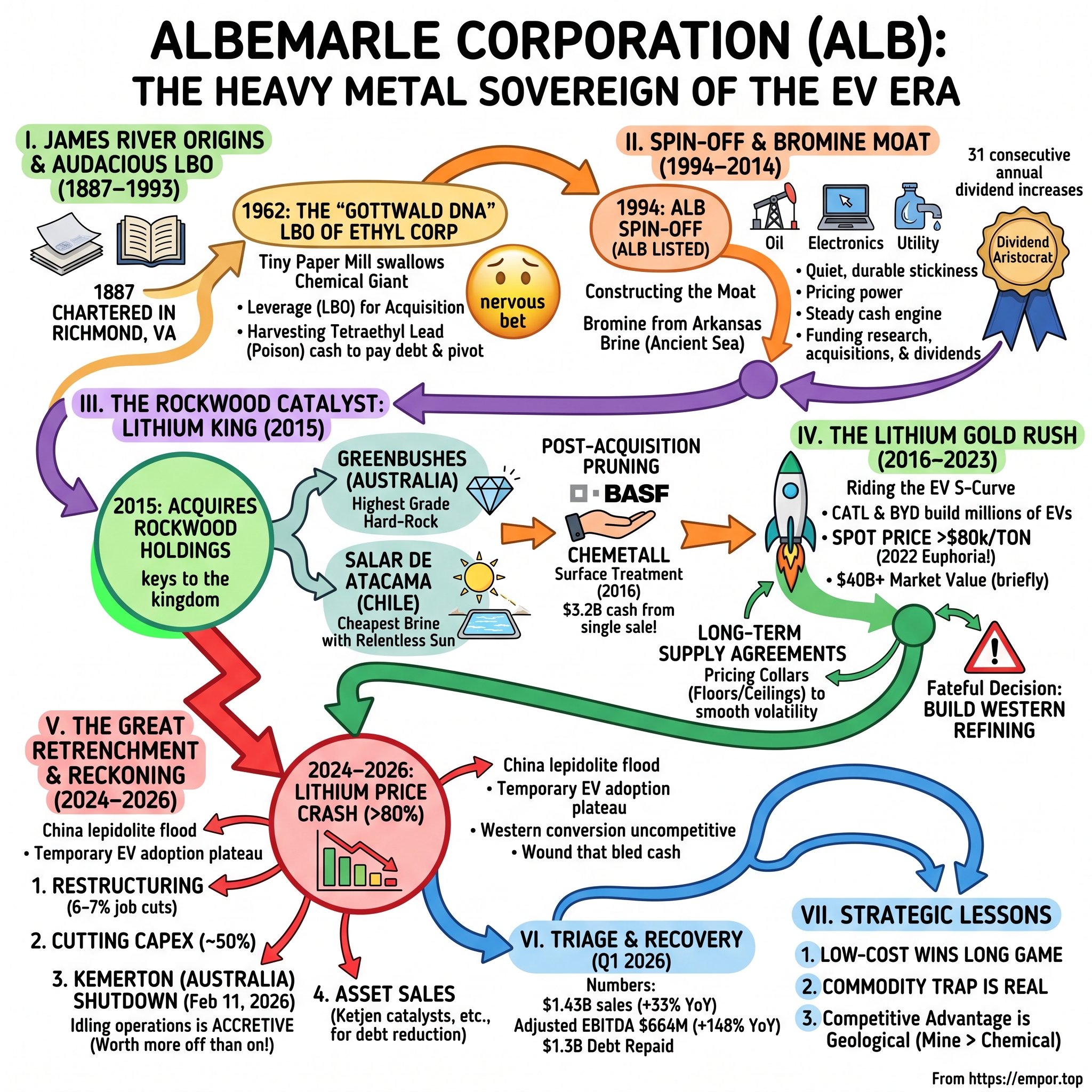

Albemarle Corporation: The Heavy Metal Sovereign of the EV Era

I. Introduction & Episode Roadmap

Picture a strip of dusty red earth in the Atacama Desert of northern Chile, the driest non-polar place on the planet, where it has not rained meaningfully in recorded human memory. Beneath that crust sits a brine so rich in dissolved lithium that when you pump it into evaporation ponds the size of small cities and let the relentless sun do the work, what remains is one of the cheapest sources of the metal that powers the modern world. Now travel eleven thousand kilometers to the other side of the Pacific, to the town of Greenbushes in Western Australia, where a hard-rock mine has been dug and blasted continuously for more than a century — first for tin, then tantalum, and now for spodumene ore graded so high it has no rival on Earth. A single American company, headquartered not in a mining town but in a glass office tower in Charlotte, North Carolina, controls a commanding share of both. That company is Albemarle.

Here is the puzzle this story exists to unravel. How did a business that began in 1887 as a paper mill on the banks of the James River in Richmond, Virginia — a maker of blotting paper and book stock — end up as the physical backbone of the global electric-vehicle revolution, the single most important Western supplier of the element that stores the energy of the twenty-first century?1

And then the harder, more uncomfortable question. If Albemarle sits on the two finest lithium deposits in the world, at the very bottom of the global cost curve, how did the same company manage to reach a market value north of $40 billion during the manic lithium boom of 2022 and 2023, only to spend the following three years in a grinding, humiliating retreat — cutting thousands of jobs, deferring billions in projects, and on February 11, 2026, pulling the plug entirely on its flagship Western processing plant in Kemerton, Western Australia?23

This is a story about the difference between owning a resource and running a business. It is possible to sit atop the best rocks on the planet and still destroy capital, if you make the wrong bets on where and how to turn those rocks into product. Albemarle is the case study.

Over the next several hours we will trace five threads. The first is what we will call the "Gottwald DNA" — the leverage-heavy, audacious buyout instinct planted in 1962 when a tiny paper company swallowed a chemical giant many times its size. The second is the Rockwood catalyst, the 2015 acquisition that handed Albemarle the keys to Greenbushes and the Salar de Atacama almost as a byproduct of buying something else entirely. The third is the China trap: the brutal economic lesson that mining lithium can be gloriously profitable while processing it in high-cost Western jurisdictions can be a capital-destruction machine. The fourth is the great retrenchment of 2024 through 2026, the cost-cutting and asset sales and the Kemerton shutdown. And the fifth, running underneath all of it, is a question every commodity investor eventually confronts: when the cycle turns, who survives — and at what price to the shareholders who rode it up?

Let us begin where it began, on a slow-moving river in Virginia.

II. The James River Origins & The Audacious LBO (1887–1993)

The Albemarle Paper Manufacturing Company was chartered in Richmond, Virginia, in 1887, and for the better part of seventy years it was exactly what it sounded like: a regional maker of paper products — blotting paper, cover stock, the unglamorous cellulose of an industrial economy.1 It was profitable enough, stable enough, and utterly unremarkable. Nothing about a Reconstruction-era paper mill on the James River suggested it would one day set the price of a strategic mineral in Santiago and Perth. The company that Albemarle would become was not born from paper. It was born from a single act of financial nerve.

The man who supplied the nerve was Floyd Gottwald, and to understand Albemarle's corporate personality — its comfort with debt, its willingness to bet the entire enterprise on a portfolio pivot — you have to understand what he did in 1962. That year, Albemarle Paper Manufacturing, a company with roughly $50 million in sales, acquired the Ethyl Corporation, a chemical business several times its size, for about $200 million.4 Ethyl was not some struggling target. It was the joint creation of General Motors and Standard Oil of New Jersey, the company that had commercialized tetraethyl lead — the anti-knock compound that made leaded gasoline possible and, for decades, poured a fortune into its owners' laps.

Think about the audacity. This was a leveraged buyout before the term "leveraged buyout" was part of the American business vocabulary, before the KKRs and the barbarians and the 1980s junk-bond boom. A minnow borrowed heavily to swallow a whale, and it worked for one reason: Ethyl's tetraethyl lead franchise threw off cash like a broken fire hydrant, and Gottwald used that torrent to pay down the acquisition debt at speed. The tiny paper company took the giant's name, kept its own leadership, and quietly began transforming itself from a cellulose manufacturer into a specialty chemicals house.

It is worth pausing on the human dimension here, because the Gottwalds were not private-equity financiers parachuting in for a quick flip. They were a Richmond family who ran Ethyl as an operating business for decades, and Floyd Gottwald's sons — Bruce and Floyd Jr. — carried the enterprise forward through the leaded-gasoline wind-down and into the specialty-chemicals era. This was a controlled, patient, multi-generational stewardship of a cyclical cash engine, not a raid. That distinction matters for understanding Albemarle's character: the leverage was audacious, but the operating mindset behind it was conservative and long-horizoned. The family bet big, but they bet on assets they intended to hold and manage for a generation, and they used debt as a tool of acquisition, not as an end in itself. That combination — bold at the moment of purchase, disciplined in the years of ownership — is the pattern to keep in mind when we reach the Rockwood deal half a century later.

The lesson planted in that transaction would echo for sixty years. Gottwald had demonstrated that you could use aggressive but calculated leverage to acquire assets far larger than yourself, provided the target generated enough cash to service the debt — and that you should not sentimentalize your legacy business. Paper was the company's history; Gottwald walked away from it. That willingness to abandon a declining core would matter enormously, because the crown jewel he had bought was itself living on borrowed time. Tetraethyl lead was a neurotoxin. As the scientific and regulatory consensus hardened through the 1970s and 1980s, leaded gasoline was legislated out of existence across the developed world, and Ethyl's golden goose was slated for slaughter.

Here is where the DNA proved itself. A company built on a single doomed molecule managed the decline not by denial but by redeployment. Ethyl used the cash from the dying lead franchise — exactly as Gottwald had used it to pay down the paper-company debt — to build out bromine chemistry, agricultural products, and other specialty lines that would outlive the poison that funded them. Managing highly cyclical, structurally declining cash flows and rotating the proceeds into the next thing became the house style.

For long-term investors, the takeaway from the pre-history is not nostalgia. It is a behavioral fingerprint. This is a company culturally comfortable with three things that would define its entire modern arc: heavy leverage deployed with conviction, brutal portfolio surgery when an end-market breaks, and the discipline of harvesting a cash cow to fund the future. By the early 1990s, the leaded-gasoline chapter was closing, and Ethyl's specialty chemicals had grown into a real business tangled up inside a corporate structure that no longer made sense. The obvious next move was to set it free.

III. The Spin-off & Constructing the Bromine Moat (1994–2014)

In 1994, Ethyl Corporation spun off its specialty chemicals operations into a separate, publicly traded company, and the new entity reached back into the family history for its name. It became Albemarle Corporation, listed on the New York Stock Exchange under the ticker ALB.1 The paper company's name had traveled a long, strange road — from blotting paper to leaded gasoline to, now, an independent specialty chemicals concern with one genuinely exceptional asset at its heart: bromine.

Bromine is not a household word, and that anonymity is precisely the point. It is a dense, reddish-brown element extracted from ancient underground brines, and Albemarle draws it from one of the richest sources on the continent — the Smackover Formation in Magnolia, Arkansas, a geological layer of concentrated, mineral-laden brine left behind by a sea that dried up in the Jurassic.5 The company pumps this brine, strips out the bromine, and reinjects what remains. The applications are deeply unglamorous and deeply essential: flame retardants that keep electronics and furniture from igniting, completion fluids used in oil and gas drilling, and specialty compounds for pharmaceuticals and semiconductor manufacturing.

What makes bromine such a beautiful business is the shape of its economics. This is a domestic oligopoly, dominated by a small handful of producers who control access to the best brine. New entrants cannot simply will a Smackover Formation into existence; the resource is geologically fixed and the permitting is onerous. Customers who have engineered a specific brominated flame retardant into a product face real cost and re-qualification pain if they try to switch suppliers, which creates the kind of quiet, durable stickiness that shows up as pricing power. And crucially, once the wells and plants are built, the segment demands relatively little fresh capital to keep the cash flowing. It grows slowly, but it grows reliably, and it converts a high share of its earnings into free cash.

In the language of moats, bromine gave Albemarle two of them at once: a resource that competitors cannot replicate, and switching costs baked into customer supply chains. It is worth being precise about what this moat is and is not. It does not deliver explosive growth — bromine demand tracks the broad industrial economy, not a technology S-curve. What it delivers is consistency, and for two decades that consistency did something invaluable. It made Albemarle a cash machine.

There is a useful analogy for understanding why a business this obscure is so valuable. Bromine is to Albemarle what a municipal water utility is to a diversified holding company: unexciting, un-sexy, entirely dependent on a physical resource in the ground, and almost impossible to dislodge. Nobody writes magazine covers about flame-retardant chemistry. But the customer who has spent years engineering a specific brominated compound into a circuit board or a piece of upholstery, and has certified that product for safety, cannot casually swap suppliers without re-testing and re-certifying — a process that costs money and time and risk. The result is that Albemarle's bromine customers tend to stay, and to accept price increases that roughly track inflation and input costs, year after year. During this two-decade stretch, the company also expanded internationally, adding bromine production from the Dead Sea region and building a global specialties footprint, but the economic logic never changed: control a scarce brine, serve customers who cannot easily leave, and harvest the cash.

The other business Albemarle carried through these years, and one that would matter to the 2026 restructuring, was refining catalysts — the specialized chemistries that oil refineries use to crack heavy crude into gasoline and diesel. This catalysts arm, later branded Ketjen, was a competent, cyclical, capital-intensive business tied to the fortunes of the global refining industry. Hold that thread; it becomes a divestiture candidate when the lithium crisis forces Albemarle to raise cash. For now, the point is simply that Albemarle entered the 2010s as a three-legged specialty-chemicals company — bromine, catalysts, and a modest lithium operation inherited from earlier acquisitions — with bromine as the profit anchor.

That cash cushion is the unsung hero of everything that follows. The steady, high-margin bromine profits funded research, funded acquisitions, and — most visibly to shareholders — funded an unbroken and steadily rising dividend. Albemarle would build, over these years, a record of consecutive annual dividend increases long enough to earn it the coveted status of a Dividend Aristocrat, a distinction reserved for S&P 500 companies that raise their payout every single year for at least a quarter century.6 The bromine engine was what made that promise credible.

But a reliable cash cow presents its owner with a permanent temptation and a permanent question: what do you do with all that money? A management team can return it, or it can hunt for the next big thing. By the early 2010s, Albemarle's leadership was looking hard at a market that was beginning to stir — a light, silvery metal that, for the moment, was mostly used in ceramics, greases, and mood-stabilizing pharmaceuticals, but that a handful of forward-looking chemists and automakers believed was about to become the most important industrial input on the planet. To seize it, Albemarle would have to make the biggest bet in its history. And it would get there almost by accident.

IV. The Rockwood Catalyst: Becoming the Lithium King (2015)

In July 2014, Albemarle stunned Wall Street by agreeing to acquire Rockwood Holdings for approximately $6.2 billion in cash and stock, a deal that closed in January 2015.[^7] To the analysts covering the stock, the logic was not obvious, and the reaction was skeptical bordering on hostile. Here was a conservative, cash-generative specialty chemicals company — a Dividend Aristocrat in the making — proposing to take on a mountain of debt to buy a business loaded with two things the market considered dangerous: high-beta lithium exposure and a sprawling surface-treatment operation. The transaction carried a bid premium of roughly 12% and pushed Albemarle's leverage to something in the neighborhood of three-and-a-half times net debt to EBITDA, a level that made bondholders and dividend investors distinctly nervous.[^7]

The surface skepticism missed what was buried inside Rockwood. Because tucked into that $6.2 billion price were two of the most extraordinary mineral assets on the face of the Earth — assets whose full value almost nobody, including arguably Albemarle's own board, could yet appreciate. The first was a 49% stake in the Greenbushes mine in Western Australia, held through the Talison Lithium joint venture — the highest-grade hard-rock spodumene deposit in the world, a resource of a quality that quite literally cannot be replicated because deposits like it are geological accidents that occur perhaps once on a continent. The second was a commanding position in the brine concessions of the Salar de Atacama in Chile, the desert flats whose lithium-rich brine can be concentrated by nothing more expensive than sunshine.

To appreciate why Greenbushes is such an anomaly, it helps to understand what "grade" means in hard-rock mining. Spodumene is the mineral that contains lithium in hard rock, and its value hinges on how much lithium oxide is packed into each tonne of ore you dig, blast, and haul. A higher grade means you move less rock, use less energy, and generate less waste to produce the same amount of lithium — every step of the process is cheaper. Greenbushes runs at grades that competitors simply cannot match, which is why its cash cost per tonne of concentrate sits at the very floor of the global cost curve. You cannot engineer your way to a deposit like this; you can only be lucky enough to own it. Rockwood owned a 49% slice of it through the Talison Lithium joint venture, and that slice came along in the deal.

The Atacama position was the mirror image on the brine side. Whereas hard rock requires you to dig and crush, brine lithium is dissolved in underground water; at the Salar de Atacama you pump it into vast ponds and let the desert sun evaporate the water over roughly a year until the lithium concentrates enough to process. The energy input is mostly free sunlight. Rockwood's Chilean concessions gave Albemarle access to the richest, cheapest such brine on Earth. So the deal handed Albemarle the best hard rock and the best brine simultaneously — a combination no other company on the planet could claim.

Whether Albemarle bought Rockwood for the lithium or bought it and then discovered what it truly held is a question the company's public statements answer more confidently in hindsight than the contemporaneous record supports. What is not in dispute is what management did next, and this is where the story turns from a merely large acquisition into a genuine masterclass in capital allocation.

Rockwood came with a business Albemarle did not want: Chemetall, a large and respected maker of surface-treatment chemicals — the coatings and processes that prepare metal surfaces for painting and protect them from corrosion. It was a fine business. It was simply not the business Albemarle now realized it was in. So in 2016, Albemarle sold Chemetall to the German chemical giant BASF for $3.2 billion in cash.7 Read that number against the Rockwood purchase price and the elegance becomes clear: by divesting a single non-core division, Albemarle recovered more than half of what it had paid for the entire company. BASF paid a rich multiple — reported at north of fifteen times the business's trailing EBITDA — because Chemetall was exactly the kind of stable, global specialty franchise a strategic buyer covets.7

Now do the arithmetic that made careers on Albemarle's corporate development team. Purchase price of roughly $6.2 billion, less $3.2 billion recovered from Chemetall, and Albemarle was left holding the crown jewels — a controlling interest in the world's best brine and a large stake in the world's best hard rock — for a net cost of under $3 billion. This is the deeper lesson the Rockwood episode teaches, and it is one sophisticated acquirers understand and amateurs miss: the greatness of a deal is often made not at signing but in the pruning afterward. The art was not in paying $6.2 billion. It was in knowing which $3.2 billion to sell, to whom, and when.

There is a subtlety worth flagging for the skeptic, however, because the "masterclass" framing can be told too cleanly. The Chemetall sale looks like genius partly because of when it happened — 2016, before the lithium boom had fully arrived, when Albemarle needed to de-lever and the lithium optionality was still cheap in the market's eyes. It is fair to ask whether management fully grasped what it was sitting on at the time or whether it simply needed cash and sold the most obviously saleable division at a good price, with the lithium windfall arriving as a fortunate consequence rather than a fully premeditated plan. The record supports a blend: the strategic intent to become a lithium company was real, but the sheer magnitude of the resource's value was clarified by events, not foreseen in full. Either way, the outcome was the same, and it is the outcome that made the next seven years possible.

Albemarle had, almost casually, positioned itself at the bottom of the global lithium cost curve just as the largest demand event in the metal's history was about to arrive. What no one could have scripted was how violently — in both directions — the market was about to reward and then punish that position.

V. The Lithium Gold Rush: Riding the EV S-Curve (2016–2023)

For most of industrial history, lithium was a sleepy backwater — a specialty chemical with a slow-growing customer list. Then the automobile decided to run on it. As Chinese battery champions like 宁德时代 CATL scaled to become the largest cell manufacturer on the planet, and as vertically integrated pioneers like 比亚迪 BYD proved that electric vehicles could be built at mass-market prices and sold by the millions, the demand curve for lithium bent from a gentle slope into a near-vertical wall. Every gigafactory that broke ground, every automaker that pledged an all-electric future, translated directly into contracted demand for lithium carbonate and hydroxide. Albemarle, sitting on the cheapest supply in the world, was suddenly the belle of the ball.

The price action told the story with brutal clarity. Lithium carbonate, which had traded in a comfortable range around $10,000 per metric ton for years, began to climb, then to sprint, then to levitate. By late 2022, at the euphoric peak, benchmark prices had blown past $80,000 per ton — an eightfold move that turned Albemarle's low-cost tonnes into some of the most profitable industrial output anywhere in the economy. Cash generation exploded. The stock, which had spent years in the low hundreds, rocketed to an all-time high above $330 in November 2022, and the company briefly commanded a market capitalization north of $40 billion.2 For a moment, a former Virginia paper mill was one of the most valuable materials companies in the world.

Underneath the headline lithium price sat an architecture of joint ventures that is essential to understanding how Albemarle actually makes money — and how exposed it is. It does not simply own mines outright; it shares the best ones. Greenbushes is operated through Talison Lithium, in which Albemarle holds 49% and the balance is controlled by a partnership between 天齐锂业 Tianqi Lithium and Australia's IGO Limited. Greenbushes sits at the absolute floor of the global hard-rock cost curve, meaning it produces spodumene more cheaply than essentially any competitor, which is exactly why every party at the table guards its stake jealously. Separately, Albemarle developed the Wodgina mine through the MARBL joint venture, a 50/50 partnership with the Australian miner Mineral Resources Limited, known as MinRes.

These joint-venture structures are a double-edged sword, and the boom obscured the sharper edge. On one hand, they gave Albemarle access to world-class resources it could never have developed alone and spread the enormous capital cost of building mines across deep-pocketed partners. On the other, they mean Albemarle does not fully control its own crown jewels. Decisions at Greenbushes require consensus with partners who are themselves lithium producers with their own agendas — 天齐锂业 Tianqi Lithium is a Chinese company whose strategic interests do not always align with a Western supplier's. And the relationship with MinRes at Wodgina proved contentious over the years, with the partners repeatedly renegotiating the terms and structure of their arrangement. For an investor, the lesson is that Albemarle's headline resource position is genuinely elite but partially shared, which dilutes both the economics and the control. You own the best rocks, but you own them alongside people who would happily own more of them.

The other feature of the boom worth understanding is how Albemarle actually sold its lithium, because it was not simply dumping tonnes onto the spot market at whatever the day's frenzied price happened to be. Increasingly, the company signed long-term supply agreements with battery makers and automakers that embedded pricing collars — negotiated floors and ceilings that constrained how far the contract price could move regardless of where the spot benchmark went. During the mania, this looked like leaving money on the table: with spot lithium above $80,000 a ton, a contract ceiling meant Albemarle captured less than the peak. Management defended the collars as a deliberate trade of upside for stability, arguing that predictable pricing served both the company and its customers better than the casino of the spot market. Whether that was wisdom or timidity was impossible to judge at the top of the cycle. It would only become clear on the way down.

Owning cheap rock and cheap brine, however, was not the whole ambition. Automakers and Western governments wanted battery-grade lithium hydroxide refined in jurisdictions they trusted, not routed exclusively through Chinese conversion plants — and refining, in theory, captured a fat margin on top of mining. So Albemarle made the fateful decision to build that refining capacity in the West. It committed billions to construct the Kemerton lithium hydroxide plant in Western Australia, designed as a multi-train conversion complex, and drew up plans for a $1.3 billion "mega-flex" processing facility in South Carolina alongside a new technology park near its Charlotte headquarters.

The strategic reasoning was not stupid. Western governments were, and are, genuinely anxious about depending on China for the refined lithium that goes into everything from cars to grid batteries to defense systems, and they were dangling subsidies and sourcing mandates to build a non-Chinese supply chain. If any Western company was positioned to capture that premium, it was Albemarle, sitting on Australian rock and Chilean brine. The bet was that geopolitics would pay Albemarle to refine at home. The flaw was in the size and timing of the wager, not its underlying premise.

This was the pivotal strategic error, though it did not look like one at the time. The decision rested on an assumption — implicit, and rarely stress-tested in the boardroom during the boom — that lithium prices would stay elevated indefinitely, and that Western refining costs, however high, would be comfortably covered by permanently rich margins. Management pushed capital expenditure aggressively higher, waving away the warning signs already flashing in Western Australia: acute labor shortages, ballooning construction costs, and the specific, grinding difficulty of commissioning complex chemical plants far from the deep pool of experienced process engineers concentrated in China. On the way up, hubris and momentum are indistinguishable. The market was minting money, the stock was at record highs, and questioning whether the good times would last was not a way to get promoted.

The good times did not last. And when they broke, they broke the entire logic of the Western refining bet in one merciless move.

VI. The Great Lithium Crash & The February 2026 Reckoning (2024–2026)

Commodity cycles do not end with a whimper; they end with a stampede for the exits. By 2024, the lithium market that had minted fortunes was in free fall. Two forces collided. On the supply side, Chinese producers unleashed a flood of lithium extracted from lepidolite — a lower-grade, higher-cost ore that becomes economic to process only when prices are high, and that comes roaring back offline and online with the cycle. On the demand side, Western EV adoption, which everyone had modeled as a smooth exponential, hit a temporary plateau as subsidies shifted, interest rates bit, and consumers balked at price and charging anxiety. The result was a price collapse of more than 80% from the peak, dragging the benchmark down toward the $10 to $12 per kilogram range — a level at which the entire premise of high-cost Western conversion simply stopped making sense.8

Here the chickens of the refining strategy came home in a flock. Refining spodumene into battery-grade hydroxide in Western Australia or South Carolina was structurally more expensive than doing it in China's mature, integrated, subsidized conversion hubs. Kemerton, the flagship of the Western processing dream, had already been a case study in execution pain — plagued by delays, severe labor inflation, and operating costs that ran well above the original budget. When lithium was at $80,000 a ton, an over-budget refinery was an annoyance. At $10,000 a ton, it was a wound that bled cash every single day it ran.

Albemarle's management, to its credit, did not deny the arithmetic — though it took two and a half years of escalating retreat to fully accept it. The first major concession came in the autumn of 2024. Effective November 1, 2024, the company announced a restructuring that cut roughly 6 to 7% of its global workforce — on the order of 500 roles — with the axe falling hardest on non-manufacturing functions, where headcount was reduced by about 15%.9 Management targeted annual run-rate cost savings of $300 million to $400 million and slashed planned capital expenditure, guiding 2025 capex down roughly 50% versus 2024.9 At Kemerton itself, the company idled Train 2 and abandoned the expansion plans for Trains 3 and 4. The message was clear: growth was over; survival was the job now.

Then came the reckoning that gives this section its name. On February 11, 2026, after another year of grinding price pressure, Albemarle announced it would idle Train 1 — the last operating train at Kemerton — and place the entire plant into care and maintenance, effective immediately.3 The Western refining dream, the multibillion-dollar bet on capturing conversion margin outside China, was over. "Idling operations at Kemerton was a difficult decision," CEO Kent Masters said in the announcement, and then he said the sentence that indicts the entire strategy: "Unfortunately, recent lithium price improvements alone are not enough to offset the challenges facing Western hard-rock lithium conversion operations."3 Read carefully, that is management conceding that the problem was not merely a cyclical low price — it was that Western conversion was structurally uncompetitive, even after prices had begun to recover. The company said the idling would actually be accretive to adjusted EBITDA starting in the second quarter of 2026, with no hit to 2026 volumes, because Albemarle could meet customer hydroxide demand more cheaply through other channels.3 In plain terms: the refinery was worth more switched off than running.

Alongside the shutdown came a broader campaign of balance-sheet triage. Having already deferred the $1.3 billion South Carolina mega-flex plant and the Charlotte technology park, and having driven $450 million of run-rate cost and productivity improvements into the business by the end of 2025 while cutting capital expenditure by roughly 65% year over year, management turned to selling assets outright.10 In late 2025, Albemarle agreed to sell a controlling stake in its Ketjen refining-catalyst business to affiliates of KPS Capital Partners, retaining roughly 49% while KPS took operational control; combined with the sale of its 50% interest in the Eurecat joint venture to Axens, Albemarle expected total pre-tax proceeds of approximately $660 million, earmarked for debt reduction.11 Both catalyst transactions closed by early March 2026.11

The proof that the medicine was working — and a reminder of how violently this business swings — arrived with the first-quarter 2026 results. As lithium prices bounced off the bottom, Albemarle reported net sales of $1.43 billion, up 33% year over year, and adjusted EBITDA of $664 million, up 148%, with net income attributable to shareholders leaping to $319 million from just $41 million a year earlier.12 The Energy Storage segment alone generated $551 million of adjusted EBITDA, up nearly 200%.12 The company had used its divestiture proceeds and cash generation to repay $1.3 billion of debt in the quarter, cutting its net-debt-to-EBITDA leverage ratio to roughly one times and its weighted-average interest rate to about 3.1%.1213 Idling Kemerton's Train 1 cost about $25 million in the quarter — the price of keeping the option to restart, without the bleeding of running.13

But the numbers are only half the story, and for an independent investor the more revealing material is in the transcripts. Across the Q4 2025 and Q1 2026 earnings calls, Wall Street's analysts turned the Q&A into an interrogation. The essential question was as blunt as it was fair: why did you spend billions building Kemerton only to mothball it, and what does that say about your judgment on capital allocation going forward? Masters and CFO Neal Sheorey did not have a satisfying answer to the counterfactual — you cannot un-spend billions — so they pivoted the narrative hard, from the hyper-growth language of the boom to an almost monastic emphasis on capital discipline, financial flexibility, and protecting the balance sheet.1013 Sheorey leaned on the numbers he could defend: 2025 EBITDA-to-operating-cash conversion of 117%, leverage down to one times, debt slashed.1013 It was a credible recovery story told by the same people who had authored the mistake — which is exactly the tension a careful investor should sit with rather than resolve too quickly. The retreat was well executed. That does not make the advance forgivable.

It is worth pausing to fact-check two pieces of consensus narrative that tend to circulate about this episode, because both are half-wrong. The first myth is that Albemarle "gambled and lost" — that the Kemerton write-down proves the whole lithium strategy was a mistake. The reality is narrower and more interesting: the mining strategy was vindicated even as the refining strategy failed. Albemarle's mines never stopped being among the cheapest in the world; it was only the downstream conversion bet, layered on top of the mines, that destroyed capital. Conflating the two obscures the actual lesson. The second myth, popular during the boom, was the reverse — that Albemarle was a secular growth stock riding an unstoppable EV megatrend, essentially decoupled from commodity cyclicality by its long-term contracts and its cost position. The 80%-plus price collapse and the earnings whipsaw that followed demolished that story. Albemarle is, was, and will remain a cyclical commodity producer whose fortunes are dominated by the lithium price. Its cost position determines whether it survives the troughs; it does not exempt it from having them.

That reframing bears directly on how to judge management. The fairest read of Kent Masters and Neal Sheorey is that they were excellent at the response and questionable at the setup. The capital expenditure that built Kemerton and greenlit the South Carolina complex was authorized in the boom years on assumptions that a more skeptical board might have stress-tested harder — and management's own words in February 2026, conceding that Western conversion is structurally uncompetitive "even after" price recovery, imply the problem was foreseeable, not merely bad luck. Against that, the execution of the retreat has been genuinely disciplined: the guidance on cost savings was set and then delivered, the leverage targets were hit, the asset sales were completed on schedule, and the narrative across the 2024, 2025, and early-2026 calls has been consistent rather than lurching. Management has not tried to blame the weather; it has named the structural problem and acted on it. For an investor weighing credibility, that is the balance to strike: this is a team that made an expensive strategic error and then managed the consequences about as well as could be asked. The open question is whether the same team's judgment on the next big allocation decision — a Greenbushes expansion, an Atacama renegotiation, a DLE build-out — has been chastened into wisdom or merely into caution.

With the strategic wreckage cleared and the balance sheet stabilized, the question becomes what Albemarle actually is underneath the cycle — and for that we have to open the hood and look at the segments and the rocks.

VII. Segment-Level Data & Unit Economics

Strip away the drama of the cycle and Albemarle is, at its core, a tale of two businesses with opposite temperaments — one a volatile prizefighter, the other a patient accountant — and understanding the difference between them is the whole game.

The prizefighter is Energy Storage, the lithium segment. At the peak of the boom it drove roughly three-quarters of Albemarle's revenue and more than four-fifths of its EBITDA, and it remains the primary engine of the company's enterprise value.12 But its earnings breathe with the lithium price in a way that can be dizzying. At $12 per kilogram, the segment's margins compress severely; a year later, with prices recovering, that same segment can post a near-tripling of EBITDA, as the first quarter of 2026 demonstrated when Energy Storage delivered $551 million of adjusted EBITDA on $891 million of sales.12 This is operating leverage in its rawest form. Because a large share of Albemarle's mining costs are fixed, every dollar of price increase above cash cost falls almost straight to the bottom line — which is wonderful on the way up and terrifying on the way down.

The accountant is Specialties, built on the bromine franchise described earlier. It does not sprint; it compounds. Through the worst of the lithium winter, bromine kept generating steady EBITDA at margins in the neighborhood of 30%, providing exactly the cash cushion that let Albemarle service its debt and defend its dividend while the lithium business gasped.6 In a cyclical commodity company, a stable segment is not boring — it is the thing that keeps you solvent long enough to see the next upturn.

To understand why Albemarle can survive a price crash that kills weaker producers, you have to understand the cost curve — a concept worth explaining plainly. Imagine lining up every lithium producer in the world from cheapest to most expensive and plotting their cost to produce a tonne. When the price falls, it falls from the right — the high-cost producers lose money first and shut down. Whoever sits farthest to the left survives the longest. Albemarle owns two of the leftmost positions on the entire chart.

At the Salar de Atacama in Chile, the brine is so concentrated and the extraction so cheap — powered largely by solar evaporation — that cash costs can run below $4,000 per tonne of lithium carbonate equivalent, economics essentially no hard-rock miner can touch.[^15] There is, however, a crucial asterisk: the Atacama concessions are governed by an agreement with Corfo, the Chilean state development agency, that imposes a steeply progressive royalty — a sliding scale that can climb toward 40% of the lithium price at high price levels.[^15] The government, in effect, is a silent partner that takes a bigger slice precisely when the business is most profitable. The rock cost is unmatched; the political rent is real.

At Greenbushes in Western Australia, the story is grade. The spodumene there is the highest-grade in the world, which means cash costs per tonne of concentrate run at the very bottom of the hard-rock curve — a resource quality no amount of competitor capital spending can conjure into existence, because you cannot buy geology.[^7] Between Atacama's brine and Greenbushes' rock, Albemarle holds two natural monopolies of cost.

Which brings us back to Kemerton, the conversion plant, and its unit economics — the numbers that explain the February 2026 shutdown better than any press release. Refining raw spodumene into battery-grade hydroxide at Kemerton simply cost more than doing the same work at a modern Chinese converter, and no operational tweak could close a gap that was structural — a function of labor markets, engineering depth, integration, and scale that favored China's conversion hubs.3 The cash costs at Kemerton were high enough that running the plant actively eroded consolidated EBITDA at prevailing prices. That is the entire, unsentimental logic of care and maintenance: when a facility loses money on every tonne it makes, the value-maximizing move is to stop making tonnes.

There is one more asset worth a brief mention, sized to its speculative weight. Back in Arkansas, in the same Smackover brines that feed the bromine business, Albemarle has been piloting Direct Lithium Extraction — DLE — a technology that chemically strips lithium from brine without the sprawling evaporation ponds of Chile. The appeal is easy to state: conventional brine evaporation takes a year or more and works only in a handful of desert basins, while DLE promises to pull lithium from lower-grade brines quickly and in far less space, which would open up sources that were previously uneconomic. It is genuinely early-stage and highly speculative — no one has yet proven DLE at massive commercial scale at competitive cost — and nothing in Albemarle's current numbers depends on it. But it carries an interesting quality: because the Arkansas project could piggyback on existing pipeline and processing infrastructure already built over decades for bromine, it functions as a low-capital call option on domestic U.S. lithium supply, exactly the kind of IRA-compliant tonnage Western automakers say they want. It is optionality, not a plan. Investors should size it accordingly — a lottery ticket the company already owns, not a pillar of the thesis, and one whose value is almost entirely a bet on a technology that has not yet been de-risked.

The through-line across all these unit economics is a single, slightly counterintuitive truth about Albemarle. The company's competitive advantage lives almost entirely at the mine, and almost not at all in the chemistry downstream of it. For a business that markets itself as a specialty-chemicals company, that is a striking admission — its edge is geological, not chemical. The 2024–2026 crisis was, in essence, the market forcibly teaching Albemarle where its moat actually was: not in the refineries it built, but in the deposits it owns. Every dollar of value the company defended through the downturn traced back to Atacama's brine and Greenbushes' rock. That clarity, however painful to acquire, is the foundation on which the recovery — if there is one — will be built.

Numbers and rocks, though, do not allocate capital. People do — and the people running Albemarle through its worst downturn in a decade deserve their own scrutiny.

VIII. Current Management & The Dividend Aristocrat Tension

Kent Masters did not build Albemarle's lithium empire; he inherited it, along with the bill. He became chairman and CEO in 2020, but his history with the crown jewels runs deeper than that: Masters had served on the board of Rockwood Holdings before Albemarle acquired it, which means the man now running the company had a front-row seat to the very transaction that defined its destiny.[^16] A veteran industrial executive with a reputation for a clinical, understated, distinctly non-promotional operating style, Masters is temperamentally the opposite of a boom-time hype man — which is either a liability or an asset depending on which half of the cycle you catch him in. On the way up, his measured demeanor looked like a lack of ambition. On the way down, it looks like exactly the steady hand you want holding the tiller.

Beside him sits Neal Sheorey, the executive vice president and chief financial officer, whose job since taking the role has been arguably the hardest in the company: managing a balance sheet through the most brutal lithium down-cycle in years, deciding which assets to sell, how much debt to retire, and how to keep the company's investment-grade credibility intact while EBITDA whipsawed by hundreds of millions of dollars from quarter to quarter. The debt reduction, the divestitures, the leverage cut to roughly one times — these are Sheorey's fingerprints, and they represent the concrete, defensible half of a management story whose other half is an unforced strategic error.1213

On the question of alignment, the disclosures offer some reassurance. Masters directly held 87,519 shares of Albemarle as of mid-2026, a stake worth well over $10 million at prevailing prices — and even after some minor tax-related sales in early 2026, his holdings remained comfortably above the company's own executive stock-ownership guidelines.14 Skin in the game is not a strategy, and insider ownership has never stopped a capable executive from making a poor capital-allocation call. But it does mean the people who decided to keep, sell, and idle assets were doing so with a meaningful share of their own net worth riding on the outcome — which is worth more than a proxy-statement platitude, even if it is not worth everything.

The sharpest live tension in the current management story is the dividend. Albemarle is a proud Dividend Aristocrat, having raised its payout for 31 consecutive years — a streak that stretches back through the entire modern history of the company and that management treats as close to sacred.6 Maintaining it costs roughly $190 million a year.6 And here two coherent, opposing arguments collide, and the investor has to hold both in mind at once.

The skeptic's case is uncomfortable and legitimate. Is it responsible to pay out $190 million a year to shareholders while simultaneously laying off thousands of workers, idling your flagship refinery, deferring growth projects, and absorbing large write-downs on assets you overbuilt? From that angle, the unbroken dividend streak looks less like financial strength and more like a vanity project — an expensive totem defended to protect a reputation and placate yield-focused holders, even as cash that could shore up the industrial base walks out the door. An activist investor would put exactly this question on the table.

The defender's case is more about market access than yield. For a capital-intensive commodity producer that must periodically return to the debt markets to refinance, the blue-chip credibility conferred by Aristocrat status is not cosmetic — it helps anchor a stable institutional shareholder base of the Vanguards and BlackRocks of the world and signals a discipline that lowers the cost of capital over time. Cutting the dividend to save $190 million could, on this view, cost far more than $190 million in lost confidence and higher borrowing costs when the company can least afford them. Which case is right depends entirely on how deep and how long the trough runs — and that, in turn, depends on forces larger than any management team, which is where the competitive and macro analysis has to take over.

IX. Strategic Competitive Framework: 7 Powers & Porter's 5 Forces

Great businesses are not defined by good years; they are defined by what protects them in bad ones. To judge whether Albemarle is a genuinely advantaged enterprise or merely a leveraged bet on a commodity price, it helps to run it through two disciplined frameworks and see what survives the interrogation.

Start with Hamilton Helmer's 7 Powers, and specifically the one Power that matters most here: Cornered Resource. This is the ownership of a coveted asset on terms that competitors cannot match, and it is the beating heart of Albemarle's entire investment case. The Salar de Atacama brine and the 49% of Greenbushes are, quite literally, irreplaceable. A rival with unlimited capital cannot build a second Atacama or a second Greenbushes, because these are geological singularities — the product of specific ancient conditions that occurred where they occurred and nowhere else. This is what separates Albemarle from a merely large lithium producer: its cost advantage is not the result of superior operations that a competitor could copy, but of superior rocks that no one can copy. When the price crashes and the high-cost producers switch off, the owner of the cornered resource is still printing cash. That is the one Power in this story that is unambiguously real and unambiguously durable.

The second Power, Scale Economies, is more qualified. Albemarle's global scale lets it sign long-term, direct supply agreements with major automakers — Tesla, Ford, BMW and others — and, importantly, to negotiate pricing collars into those contracts: floors and ceilings that dampen the company's exposure to the wildest swings of the spot market. A price floor meant Albemarle bled less than the spot benchmark implied during the 2024–2026 crash; a ceiling meant it captured less than the spot peak in 2022. This is a real advantage in a volatile commodity — smoothing is worth money — but it is a shared one, since Albemarle's closest peer, SQM, can play the same game. Scale here buys resilience, not monopoly.

The third Power, Switching Costs, lives almost entirely in the bromine business rather than lithium, and it was covered earlier: the deep chemical integration of a brominated compound into a customer's product creates re-qualification friction that locks in demand. It is a genuine moat, but it protects the steady segment, not the growth engine. Lithium, by contrast, is a fungible commodity — a battery cell does not care whose atacama the lithium came from — so switching costs there are minimal. It is worth being honest that Albemarle's dominant segment enjoys the least customer lock-in; its defense is cost, not stickiness.

Now Porter's Five Forces, which reframes the same reality from the industry's angle. Rivalry is high: the tier-one lithium world is a handful of heavyweights — SQM, 天齐锂业 Tianqi Lithium, 赣锋锂业 Ganfeng Lithium, and Arcadium Lithium — plus a fringe of higher-cost Chinese lepidolite producers who swing in and out with the price and act as the market's shock absorbers and its ceiling. Buyer power is moderate-to-high: automakers are enormous, sophisticated, and cost-obsessed, and they push hard on price — but their own constraints cut the other way. Their ESG commitments, their need for gigantic and utterly reliable volumes, and above all the IRA's requirement for minerals sourced outside "foreign entities of concern" narrow the field of acceptable suppliers to a short list on which Albemarle and SQM feature prominently. The threat of substitutes is low-to-moderate: sodium-ion chemistry is emerging as a credible option for stationary grid storage where weight does not matter, and it bears watching, but for the energy density that an electric vehicle's range demands, lithium remains irreplaceable for the foreseeable future. There is no material threat of forward or backward integration displacing Albemarle's core resource position.

Put the two frameworks together and a clear picture emerges. Albemarle's moat is narrow but deep: it is fundamentally a cost moat rooted in a cornered resource, reinforced modestly by scale-driven contract structures, and buttressed by a genuinely sticky but non-lithium bromine franchise. It is not a business with pricing power over its main product — no one has pricing power over a global commodity — and its fortunes will always rise and fall with the lithium cycle. What the moat guarantees is not immunity from the cycle but survival through it, and the ability to be among the last producers standing when weaker hands fold. Whether that survival translates into attractive returns depends on where the cycle goes from here — which is the argument the bulls and bears are having right now.

X. The Bull vs. Bear Case Stress Test

Every commodity story eventually reduces to a single disagreement about the future price of the commodity, dressed up in the language of strategy. Albemarle is no exception, and the honest way to frame it is as a genuine debate with real evidence on both sides, not a foregone conclusion.

Before the bull and bear square off, both must reckon with the risk radar. The most material structural risk is Chilean resource nationalism. Chile has moved decisively to assert state control over its lithium — SQM was compelled into a joint venture with the state-owned copper giant Codelco, driven by the looming 2030 expiration of its Atacama concession.15 Albemarle's own Corfo agreement runs considerably longer, to 2043, which buys it years of breathing room its rival did not have.[^15] But "later" is not "never." When Albemarle's contract eventually comes up for renegotiation, the counterparty will be a Chilean state that has already demonstrated exactly how it intends to divide the spoils — and a forced 50/50 with Codelco, or a heavier royalty, would permanently compress the margins of the single best asset in the portfolio. That is a slow-moving but material threat to the core of the thesis.

The second overhang is geopolitical supply-chain fracturing, and it cuts in a way that is not entirely in Albemarle's favor. The IRA's foreign-entity-of-concern rules should let Albemarle's non-Chinese tonnes command a premium in the Western market — an American-and-Australian supply chain selling into IRA-compliant demand at prices above the Chinese-influenced global benchmark. The company's Western strategy is implicitly a bet that this premium materializes. But if it fails to show up in the size and durability management hopes — if the global market stays integrated enough that Western molecules trade close to the global price — then Albemarle's higher-cost Western assets are structurally disadvantaged with no premium to compensate them. The Kemerton shutdown is, in part, an admission that the premium has not yet arrived at a scale that justifies Western conversion.

The bear case flows naturally from those risks. In the bear's world, lithium prices stay pinned near $10 per kilogram more or less permanently, because every time prices twitch upward the vast, elastic reservoir of Chinese lepidolite supply comes back online and caps the recovery. Kemerton's care-and-maintenance costs — that $25 million-a-quarter drag — grind on with no restart in sight. And the Chilean government, watching Codelco's template, moves to renegotiate or partially reclaim the Atacama concession early, taking a scalpel to the equity value embedded in Albemarle's best asset. In this scenario the company survives — the cornered resource guarantees that — but survival at $10 lithium is not a return; it is a long, flat purgatory for shareholders who bought the dream at $300.

The bull case is a mirror image built on the logic of the cost curve. In the bull's world, the very shutdowns of 2026 — Kemerton and the high-cost Chinese lepidolite producers going dark — mark the definitive structural bottom, because a commodity cannot trade below the cash cost of the marginal supply for long without that supply disappearing and rebalancing the market. As global EV demand re-accelerates and stationary grid storage adds a second, enormous demand vector — with credible forecasts pointing to something like 15% to 40% annual demand growth in various segments — a supply deficit emerges by around 2028, and lithium recovers to a healthy, sustainable $20 to $25 per kilogram. In that world Albemarle's ultra-low-cost Atacama and Greenbushes tonnes print cash at rates the market has forgotten is possible, while the bromine cash cow keeps the dividend streak alive through the wait. The Q1 2026 EBITDA surge is the bull's exhibit A: proof of how violently the earnings lever swings the moment prices lift off the floor.12

An activist or skeptical long/short investor would press on several specific pressure points that the bull case tends to gloss over. The first is the joint-venture complexity: Albemarle's most valuable assets are shared, its Wodgina relationship has a history of renegotiation, and a determined critic would argue the company should either buy out or exit partial positions rather than remain a minority voice in its own crown jewels. The second is disclosure — commodity producers with pricing collars and JV accounting can be genuinely hard to model, and an activist might demand cleaner segment reporting on realized pricing versus spot. The third is the dividend-versus-buyback question: paying $190 million a year to sustain an Aristocrat streak while the stock trades well below its boom-era highs invites the argument that the capital would be better deployed retiring debt or repurchasing deeply discounted shares. And the fourth is governance and accountability: the same board and management that authorized the Kemerton capital are the ones now praised for cleaning it up, and a hard-nosed investor would want to see explicit acknowledgment of the allocation error reflected in how future capital decisions are governed, not just in the cost-cutting response. None of these are fatal, but they are the questions a friendly narrative skips and a rigorous one does not.

Both cases are internally coherent, which is precisely why this is a real debate and not a solved problem. The deciding variable is exogenous — the future lithium price — and no framework can predict it with confidence. What an investor can do is stop guessing the price and instead watch the handful of measurable signals that will reveal, in real time, which world is unfolding. There are three that matter above all others.

The first is the net-debt-to-EBITDA leverage ratio. Management has steered it down toward one times as of Q1 2026, and the target is to hold it comfortably below roughly 2.5x through the cycle.1213 Leverage is the mechanism through which a commodity downturn actually kills a producer; watching this number is watching the company's oxygen supply. The second is the spread between realized and spot lithium pricing — the degree to which Albemarle's contractual collars let it capture more than the spot benchmark on the way down (and, as the trade-off, less on the way up). This number reveals how much the company's contracting strategy is actually shielding it, as opposed to how much management merely claims it is. The third is the spodumene cash cost per tonne at Greenbushes, the single cleanest proxy for whether the cornered resource remains at the absolute bottom of the global cost curve. If that cost creeps up and the gap to competitors narrows, the entire "last one standing" thesis erodes at its foundation. Track those three, and the noise of any single quarter's headline resolves into signal.

XI. Outro & Business Lessons

The arc from a Richmond blotting-paper mill to the idled trains of Kemerton is not a straight line of triumph, and it should not be told as one. It is a story of a company that got the single most important decision of its modern life exactly right — and one of the most expensive decisions exactly wrong — and the two are worth holding side by side, because together they teach more than either would alone.

The first lesson is the Rockwood lesson, and it is about the underappreciated art of the un-acquisition. Buying Rockwood for $6.2 billion was bold; the genius was in selling Chemetall to BASF for $3.2 billion and thereby acquiring the two best lithium resources on Earth for a net cost under $3 billion. Great M&A is frequently made not at the signing table but in the disciplined pruning afterward — in knowing which parts of what you bought you never actually wanted, and having the nerve to sell them at a premium into a strategic buyer's hunger. The value was created by subtraction.

The second lesson is the commodity trap, and it is a lesson in humility. Even a sophisticated, century-old operator with the best rocks in the world proved susceptible to peak-of-cycle hubris. Building high-cost refining capacity in Western nations during the manic phase — on the unexamined assumption that $80,000 lithium was a new normal rather than a spike — was a textbook capital-destruction event, and no quality of resource ownership rescued it. The billions committed to Kemerton and the deferred South Carolina complex are a permanent reminder that owning a cheap resource does not license you to build expensive things around it. The discipline that governs the mine must also govern the refinery.

The third lesson is the one that may yet redeem the story: low-cost wins the long game. When a commodity market crashes, the questions of narrative and ambition fall away, and only one thing determines who survives — position on the cost curve. Albemarle's ownership of the Salar de Atacama and Greenbushes means that when the weaker producers switch off, as they did in 2026, Albemarle is still standing, still generating cash from its best assets, still able to fund a dividend that has now risen for three decades without interruption. Whether that survival ultimately rewards shareholders who bought near the top depends on a lithium price no one controls and no one can honestly forecast. But survival itself — the right to be there when the cycle turns — is not nothing. In commodities, it is very nearly everything. The heavy-metal sovereign has been humbled. Whether it has been dethroned is a question only the next cycle will answer.

References

-

Albemarle Corporation — Company Overview and History, SEC EDGAR CIK 0000915913 ↩↩↩

-

Albemarle Corporation — Company Profile and Historical Stock Data ↩↩

-

Albemarle Announces Plans to Idle its Kemerton Lithium Hydroxide Processing Plant — Albemarle Corporation, 2026-02-11 ↩↩↩↩↩

-

Albemarle Corporation — Bromine Specialties and Magnolia, Arkansas Operations ↩

-

Albemarle Corporation (ALB): Resilience and Recovery in the Post-Lithium Winter Era — FinancialContent, 2025-12-29 ↩↩↩↩

-

BASF to Acquire Chemetall Surface Treatment Business — BASF Press Release, 2016-06-17 ↩↩

-

Albemarle to idle lithium hydroxide plant in Western Australia — MINING.COM, 2026-02-11 ↩

-

Charlotte-based Albemarle to lay off 7 percent of workforce after losing $1 billion: CEO — QC News, 2024 ↩↩

-

Earnings call transcript: Albemarle Q4 2025 sees mixed results, stock drops — Investing.com, 2026-02-12 ↩↩↩

-

Albemarle Announces Sale of a Controlling Stake in Ketjen to KPS Capital Partners — PR Newswire, 2025 ↩↩

-

Albemarle Q1 2026 slides: lithium recovery drives 148% EBITDA surge — Investing.com, 2026-05-07 ↩↩↩↩↩↩↩↩

-

Earnings call transcript: Albemarle's Q1 2026 earnings soar past expectations — Investing.com, 2026-05-07 ↩↩↩↩↩↩

-

Albemarle Corporation — SEC Filings and Insider Ownership, SEC EDGAR CIK 0000915913 ↩

-

Albemarle to raise $660 million in catalyst sales — MINING.COM, 2026 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube