Astera Labs: The Connectivity Superhero Powering AI Infrastructure

I. Introduction & Episode Roadmap

Picture this: It's March 20, 2024, and the Nasdaq trading floor is buzzing with an energy not seen since the pre-pandemic IPO boom. At 9:30 AM, a semiconductor company that most retail investors have never heard of begins trading. By the closing bell, Astera Labs has surged 72%, creating $4 billion in market value in a single day. The financial press scrambles to explain why a company making something as seemingly mundane as "PCIe retimers" has become Wall Street's new obsession.

Here's the thing about gold rushes—the biggest fortunes aren't usually made by the miners. They're made by the people selling picks and shovels. And in the AI infrastructure boom of 2024, Astera Labs positioned itself as the premier supplier of the most critical tool: the connectivity solutions that allow AI chips to actually talk to each other.

How did three engineers from Texas Instruments, working out of a Santa Clara garage in 2017, build what would become a $31 billion market cap company? How did they crack into a duopoly dominated by semiconductor giants Broadcom and Marvell? And perhaps most intriguingly, why did they bet their entire company on solving a problem that most people didn't even know existed?

This is the story of Astera Labs—a company that understood, years before ChatGPT captured the world's imagination, that AI's dirty secret wasn't compute power. It was connectivity. As data centers evolved from housing servers to housing what are essentially supercomputers, the bottleneck shifted from processing to communication. Every nanosecond of latency, every dropped packet, every signal degradation became a critical failure point in the AI revolution.

We'll trace their journey from that garage in 2017 through their explosive IPO, examining how they navigated the semiconductor shortage, survived their largest customer's cloud crisis, and emerged as an essential player in every major AI deployment. Along the way, we'll unpack the technical moats they've built, the strategic decisions that separated them from would-be competitors, and the massive tailwinds that could propel them through the next decade.

The story of Astera Labs isn't just about semiconductors or AI infrastructure. It's about timing markets perfectly, building technical moats in "boring" spaces, and recognizing that sometimes the most valuable companies are the ones solving problems that nobody else wants to touch. Let's dive in.

II. The Founding Story: From TI to the Garage (2017)

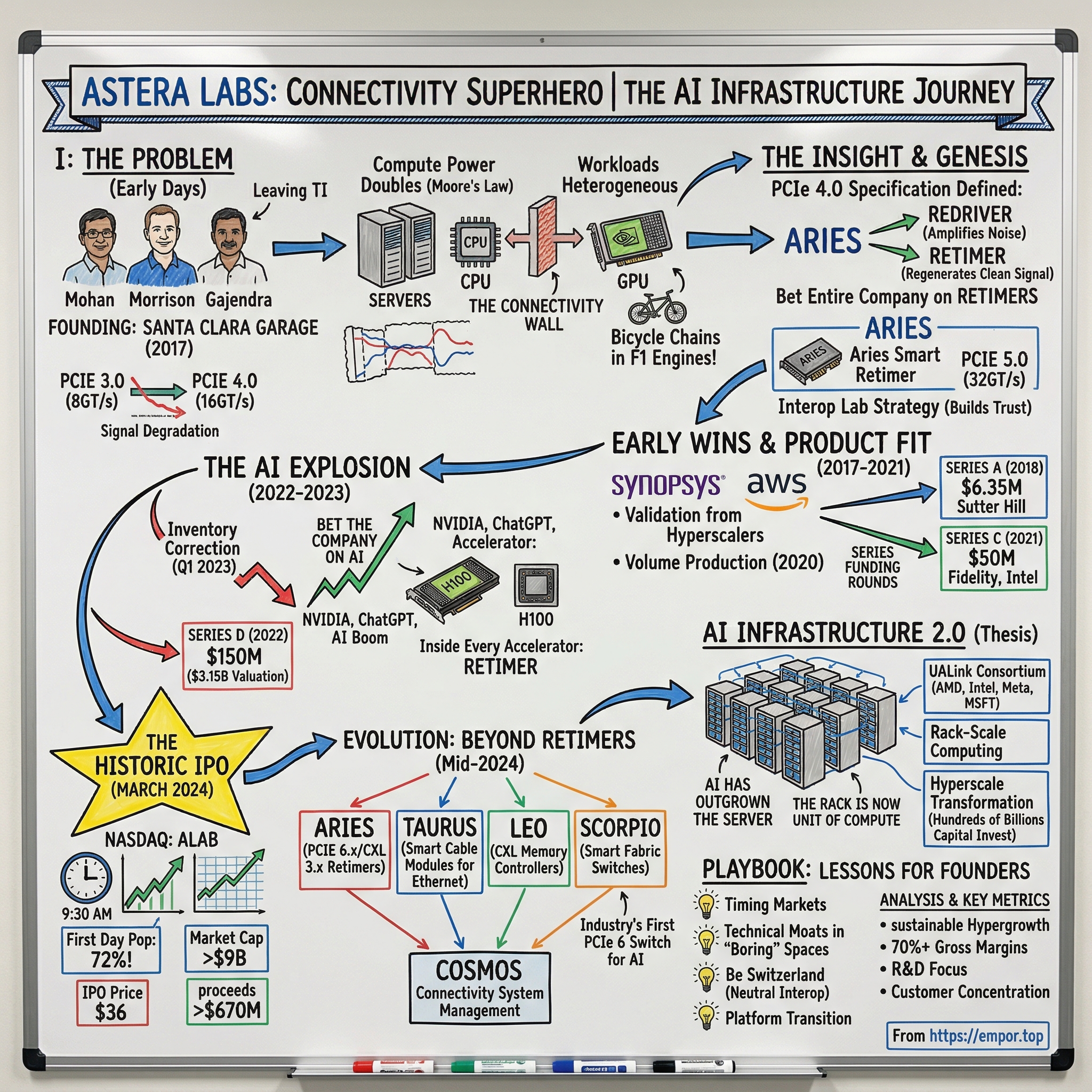

The conference room at Texas Instruments' High Speed Interface division in Santa Clara had seen better days. It was late 2016, and Jitendra Mohan, Casey Morrison, and Sanjay Gajendra found themselves in yet another meeting about incremental improvements to legacy products. These weren't just any engineers—they were the core team behind TI's most advanced connectivity solutions, products that quietly powered much of Silicon Valley's data infrastructure.

Jitendra Mohan's path to that conference room had been anything but typical. After completing his electrical engineering degree at IIT Bombay—India's MIT—he'd come to Stanford for his master's, where he discovered something crucial: the best engineers weren't always the best product managers. So he pivoted, spending years at Xilinx and Tabula learning the art of translating technical complexity into market opportunity. By the time he reached TI, he'd developed an unusual superpower: he could see around corners in the semiconductor industry.

What Mohan saw in late 2016 made him restless. The entire computing industry was about to hit a wall. Not a processing wall—Moore's Law still had some life left in it. Not a memory wall—new technologies were emerging there too. But a connectivity wall that nobody was talking about. Jitendra co-founded Astera Labs in 2017 with a vision to remove performance bottlenecks in rack-scale AI infrastructure, bringing more than two decades of engineering and general management experience, having previously worked as the General Manager for Texas Instruments' High Speed Interface Business. Sanjay Gajendra, who would become COO, had served as Product Line Manager at TI from 2014 to 2017 and brought deep product management expertise from National Semiconductor, holding a Master of Engineering in Engineering Management from University of Colorado Boulder. Casey Morrison, who would lead the product organization, had built his career helping customers solve complex challenges related to high-bandwidth, low-latency data interconnects.

The problem they saw was elegantly simple and terrifyingly complex. As compute power doubled every 18 months following Moore's Law, and as workloads became increasingly heterogeneous—mixing CPUs, GPUs, FPGAs, and custom silicon—the connections between these components were becoming the bottleneck. It was like building Formula One engines but connecting them with bicycle chains.

The timing wasn't accidental. In 2017, the PCI Special Interest Group released the PCIe 4.0 specification, doubling bandwidth from 8 GT/s to 16 GT/s per lane. But here was the kicker: for the first time, the specification formally defined two critical terms: "redriver" and "retimer." These weren't just technical jargon—they represented an acknowledgment that signal integrity had become such a problem that the industry needed standardized solutions to maintain data integrity over longer distances and higher speeds.

Most people in the industry saw this as a minor technical challenge. The TI trio saw it as the foundation of a company. The PCIe 4.0 specification took the unprecedented step of formally defining the terms "retimer," "redriver" and the superset term "repeater," marking a critical inflection point in the industry's acknowledgment that signal integrity had become a first-class problem. A retimer was defined as "a physical layer protocol-aware, software-transparent extension device that forms two separate electrical link segments," while a redriver was "a non-protocol-aware software-transparent extension device."

The insight was profound. As data rates climbed from PCIe 3.0's 8 GT/s to PCIe 4.0's 16 GT/s and beyond, redrivers began to struggle with PCIe 4.0's 16 Gbps lanes, and by PCIe 5.0 in 2019 with 32 Gbps lanes, the era of the redriver was effectively over. The world needed retimers—devices that didn't just amplify signals but completely regenerated them, resetting jitter budgets and extending reach by twice the specification.

In November 2017, the three engineers officially incorporated Astera Labs. They didn't have a product. They didn't have customers. They didn't even have an office—just a garage in Santa Clara and a conviction that the entire computing industry was about to discover it had a massive connectivity problem.

The vision was audacious in its simplicity: remove performance bottlenecks in rack-scale AI infrastructure. But in 2017, "AI infrastructure" wasn't even a category most VCs understood. The founders weren't selling to the present—they were building for a future where compute would be distributed, heterogeneous, and desperately in need of reliable connectivity.

As 2017 turned to 2018, the trio began reaching out to potential investors. The pitch was technical, dense, and required deep semiconductor knowledge to appreciate. Most VCs passed. But a few saw what the founders saw: the coming explosion in data center complexity and the critical need for signal integrity solutions. The stage was set for one of the most prescient infrastructure bets of the decade.

III. Early Days & Product Genesis: The PCIe Retimer Revolution (2017–2021)

The conference room at Sutter Hill Ventures in Palo Alto felt different in March 2018. Stefan Dyckerhoff, the managing director, had seen thousands of pitches over his career, but rarely had he encountered founders with such precise vision about an unsexy technical problem. Astera Labs secured its first funding round on March 21, 2018, raising what would initially be reported as $6.35 million in a Venture Round.

The pitch wasn't about revolutionary new architectures or breakthrough physics. It was about making existing infrastructure work at the speeds it promised. Mohan pulled up a slide showing the exponential growth in PCIe lane speeds—from 2.5 GT/s in Gen1 to the coming 32 GT/s in Gen5. "Every doubling of speed," he explained, "cuts the maximum trace length in half. At PCIe 5.0, you can barely get a signal across a motherboard without degradation."

The solution Astera Labs proposed was elegant: the Aries product line, a family of PCIe retimers that would act like signal regeneration stations, completely recovering and retransmitting data with fresh timing. Unlike redrivers that simply amplified signals (noise and all), Aries retimers would use Clock Data Recovery (CDR) to fully recover the data stream and retransmit it on a clean clock.

But building these devices required solving multiple technical challenges simultaneously. First, they needed to be protocol-aware, understanding the intricacies of PCIe handshakes, timeouts, and state machines. Second, they needed to maintain ultra-low latency—adding nanoseconds to a data path could destroy application performance. Third, and perhaps most challenging, they needed to work with every possible combination of CPUs, GPUs, and endpoints in the ecosystem. Astera Labs' breakthrough came from an unexpected quarter. Astera Labs's first major customer was actually Amazon for "typical" (non-AI) cloud workloads, not the AI infrastructure that would later define the company. This validation from one of the world's largest hyperscalers was transformative. It proved that even in standard data center deployments, the connectivity bottleneck was real and growing.

The technical approach Astera Labs took was revolutionary for its time. In 2019, they collaborated with Synopsys to achieve two industry milestones: the first large-scale design fully implemented and verified from start to finish on a third-party public cloud, and the industry's first PCIe 5.0 retimer for heterogenous compute and workload-optimized servers. This cloud-first approach to chip design wasn't just about cost savings—it was about speed and flexibility.

The interoperability testing strategy became Astera Labs' secret weapon. Rather than just designing to specifications, they built what they called the "Cloud-Scale Interop Lab," where they could test their retimers against every major CPU, GPU, and endpoint in the market. This wasn't glamorous work—it meant thousands of hours of compatibility testing, debugging edge cases, and working with competitors' products. But it built something invaluable: trust.

Astera Labs was first to market with their Aries Smart Retimer for PCIe 4.0 as well as PCIe 5.0 and securing their first design wins in 2019. Volume production started in 2020, using a TSMC process and in 2021, the company generated revenue of $34.8M. The growth trajectory was impressive for a hardware startup, but it was about to accelerate beyond anyone's wildest predictions.

By late 2021, Astera Labs had proven its technical capabilities and market fit. The September 2021 Series C funding round, raising $50M as part of an oversubscribed Series-C funding round led by Fidelity Management and Research, joined by Atreides Management and Valor Equity Partners, with continued participation from existing investors Avigdor Willenz Group, GlobalLink1 Capital, Intel Capital, Sutter Hill Ventures, and VentureTech Alliance, valued the company at $950 million.

Avigdor Willenz, the legendary semiconductor investor who had founded Annapurna Labs (sold to Amazon) and Habana Labs (sold to Intel), saw something special: "Astera Labs has done a tremendous job in developing a portfolio of multiple innovative products that address critical needs of heterogeneous computing and composable disaggregation infrastructure".

The technical moat was deepening. While competitors could theoretically build retimers, Astera Labs had accumulated years of real-world data on signal integrity challenges, interoperability quirks, and customer requirements. Every design win created a virtuous cycle—more deployment data, better products, stronger customer relationships. As 2021 turned to 2022, the company was perfectly positioned for what would become the most significant technology shift of the decade.

IV. The AI Explosion & Product Market Fit (2022–2023)

The boardroom at Astera Labs in early 2023 felt like a war room. Q1 results were in, and they were brutal. Revenue had declined quarter-over-quarter, continuing a trend from late 2022. The culprit? An inventory correction affecting the general purpose datacenter & networking markets, driven by the cloud crisis of their largest hyperscaler customer. For a company that had been on a rocket ship trajectory, this felt like hitting a brick wall.

CEO Jitendra Mohan faced a choice that would define the company's future. They could diversify, hedge their bets, try to reduce dependency on hyperscalers. Or they could double down on their conviction that AI infrastructure was about to explode. Looking at the early signals—NVIDIA's data center revenue starting to spike, OpenAI's ChatGPT capturing the world's imagination, every major tech company scrambling to build AI capabilities—Mohan chose to bet the company on AI.

The turnaround was swift and dramatic. After generating $79.9 million in 2022, plagued by the inventory correction, something extraordinary happened in the second half of 2023. Q3 and Q4 showed explosive growth as hyperscalers began their massive AI infrastructure buildout. Revenue swelled 45% in 2023 to $115.8 million, but the quarterly progression told the real story—each quarter stronger than the last, with Q4 2023 setting the stage for what would become a historic 2024.The November 17, 2022 Series D funding round proved pivotal. Astera Labs raised $150M from its Series-D funding round led by Fidelity Management & Research with a $3.15B valuation. Fidelity was joined by other existing investors, including Atreides Management, Intel Capital, and Sutter Hill Ventures. This wasn't just capital—it was validation from some of the smartest money in tech that Astera Labs was positioned for the AI boom.

The technical insight driving the company's resurgence was profound. As AI accelerator demand continues to fire, the PCIe retimer market will grow too. Indeed, inside each accelerator card is included a retimer. Every NVIDIA H100, every AMD MI300, every custom AI chip needed connectivity solutions. And as these chips got faster and more power-hungry, the signal integrity challenges multiplied exponentially.

The product-market fit crystallized around a simple reality: Astera Labs had become essential infrastructure for AI. Their retimers weren't just in servers anymore—they were in every AI training cluster, every inference pod, every high-bandwidth memory system. The company's ability to support PCIe 5.0 at scale, when competitors were still struggling with PCIe 4.0 reliability, created a moat measured in years, not quarters.

Stefan Dyckerhoff from Sutter Hill Ventures captured the moment perfectly: "Astera Labs has successfully executed on its vision to be the Cloud industry's trusted connectivity partner. I'm extremely impressed by the company's ability to assert itself as the leader in the Cloud infrastructure market that increasingly demands purpose-built connectivity solutions."

The board additions in late 2022 signaled the company's ambitions. Dr. Alexis Black Bjorlin, VP of Infrastructure at Meta, and Michael Hurlston, President and CEO of Synaptics, brought deep operational expertise in scaling semiconductor companies. These weren't advisors for a startup—they were operators who could help navigate the transition to becoming a major supplier to the world's largest tech companies.

As 2023 progressed, the transformation was complete. What had started as a challenging year with inventory corrections and customer pullbacks had become the launching pad for explosive growth. The AI infrastructure boom wasn't coming—it had arrived. And Astera Labs had positioned itself perfectly at the nexus of this transformation, ready to ride the wave that would carry them to a historic IPO.

V. The IPO: Timing the AI Infrastructure Boom (March 2024)

The Morgan Stanley trading floor at 1585 Broadway had an electric energy on the morning of March 20, 2024. Lead bankers huddled around screens showing pre-market indications while Jitendra Mohan and his team watched from Astera Labs' Santa Clara headquarters via video link. The initial price talk had been $27-30. Then it was raised to $32-34. Now, moments before trading began, they were pricing at $36—already above the raised range.

The timing was exquisite. Just days earlier, NVIDIA's GTC conference had showcased the Blackwell architecture, sending shockwaves through the industry about the scale of AI infrastructure investment ahead. Every hyperscaler was in an arms race to build out AI capacity. And hidden in every server, every accelerator, every high-speed interconnect, were Astera Labs' connectivity solutions. At 9:30 AM Eastern, the first trade crossed at $52.56 per share, up 46% from the IPO price. The floodgates opened. Within minutes, the stock touched $70 before settling into a trading range. By the closing bell, shares closed at $62.03, a gain of 72%—the kind of first-day pop not seen since the 2021 IPO boom.

The numbers were staggering. The company priced its initial public offering of 19,800,000 shares at $36.00 per share, above its raised price range of $32 to $34 apiece, giving it a valuation of about $5.5 billion. Total gross proceeds from the offering to Astera and the selling stockholders were approximately $672.2 million and $102.4 million, respectively. In a single day, Astera Labs' market capitalization had swelled to almost $9.5 billion—three times its last private valuation of $3.15 billion from November 2022.

Nick Einhorn, VP of research at Renaissance Capital, captured the market's thinking: "They're not an AI company. But they're certainly benefiting from that trend. Astera's most recent quarter of revenue growth is the most compelling argument for them."

The IPO prospectus revealed stunning growth metrics that justified the enthusiasm. Q1 2024 revenue of $65.3 million represented 29% quarter-over-quarter growth and an eye-popping 269% year-over-year increase. But buried in the financials was an even more important number: gross margins of 78%. This wasn't just a growth story—it was a growth story with software-like margins in a hardware business.

The timing couldn't have been more perfect. The day after Astera's triumph, Reddit would price its own IPO, closing up 48% on its first day. The IPO window, frozen shut for nearly two years, had blown wide open. But while Reddit rode the AI hype train with its data licensing deals, Astera Labs was the real AI infrastructure play—the company actually building the plumbing for the AI revolution.

Morgan Stanley's lead banker would later describe the Astera Labs IPO as "a watershed moment for semiconductor IPOs." The company had achieved something remarkable: going public at a significant premium to its last private round, in a market that had been skeptical of new issues, with a business model that required deep technical knowledge to understand.

The success sent ripples through Silicon Valley. Late-stage companies that had been waiting for the "right moment" suddenly saw that moment had arrived. VCs who had been sitting on portfolio companies for years longer than planned saw an exit path. And most importantly for Astera Labs, the public market validation meant access to capital to fund the next phase of growth—a phase that would require massive R&D investment to stay ahead of the connectivity curve.

VI. Product Portfolio Evolution: Beyond Retimers

The engineering lab at Astera Labs' Santa Clara headquarters in mid-2024 looked like mission control for the AI revolution. Oscilloscopes displayed eye diagrams at 64 GT/s. Thermal chambers tested components at extreme temperatures. And in the center of it all, Casey Morrison, the Chief Product Officer, stood before a whiteboard covered in architectural diagrams that would define the company's next five years.

"Retimers got us here," Morrison told his team, "but they won't get us where we're going. AI isn't just changing compute—it's changing the entire definition of what a server is."

The Aries family had been the company's cash cow, and 2024's revenue growth was largely driven by Aries PCIe Retimer products. But Morrison and his team saw what was coming: a fundamental architectural shift in data centers where the rack, not the server, would become the unit of compute. This vision drove the expansion into four distinct product families, each addressing a different connectivity challenge in AI infrastructure.

The evolution of Aries itself told the story. The company expanded its Aries portfolio with Aries 6 Retimers, marketed as the industry's lowest power PCIe 6.x/CXL 3.x Retimer solution. Through collaboration with AMD, Arm, Intel, and NVIDIA, Aries 6 underwent rigorous testing at Astera Labs' Cloud-Scale Interop Lab. The technical achievement was remarkable—supporting 64 GT/s while maintaining backward compatibility and consuming less power than previous generations.

But the real innovation came with Taurus Smart Cable Modules. As AI clusters grew from hundreds to thousands of GPUs, copper traces on PCBs couldn't handle the distances. The industry needed active cables—cables with built-in signal conditioning. Taurus modules, embedded directly into cable assemblies, enabled reliable 400G and 800G Ethernet connections across entire data center rows. By Q4 2024, Taurus Smart Cable Modules for Ethernet were coming in strongly, validating the product strategy.

The Leo CXL Memory Controllers addressed a different bottleneck entirely. AI models were becoming memory-constrained, not compute-constrained. CXL (Compute Express Link) promised to pool memory across multiple servers, but someone needed to build the controllers to make it work. Leo enabled memory pooling and sharing across heterogeneous compute resources, essentially turning a rack of servers into one giant shared-memory supercomputer. But the crown jewel of the portfolio was Scorpio Smart Fabric Switches, announced in October 2024 as the industry's first PCIe 6 switch built from the ground up for AI workloads. Scorpio represented a fundamental rethinking of what a switch should be. Traditional PCIe switches were designed for general-purpose computing—they treated all data equally. Scorpio was different. It understood AI dataflows and optimized for them.

The Scorpio portfolio featured two application-specific product lines: Scorpio P-Series for GPU-to-CPU/NIC/SSD PCIe 6 connectivity—architected for mixed traffic head-node connectivity—and Scorpio X-Series for back-end GPU clustering, delivering the highest back-end GPU-to-GPU bandwidth with platform-specific customization. This wasn't just faster switching; it was intelligent switching that understood the difference between a model checkpoint and inference data.

Brian Kelleher, Senior VP of GPU Engineering at NVIDIA, validated the approach: "AI infrastructure requires the right balance of interconnect performance, efficiency and capabilities to enable accelerated computing for AI workloads at scale. The new Scorpio fabric switch portfolio can support NVIDIA accelerated AI infrastructure deployments."

Tying it all together was COSMOS—the COnnectivity System Management and Optimization Software suite. This wasn't an afterthought but a fundamental part of the value proposition. COSMOS provided unprecedented visibility into data center operations, allowing operators to see bottlenecks in real-time, predict failures before they happened, and optimize traffic patterns dynamically.

The financial implications were staggering. Management projected that 2025 would be a breakout year with revenue from all four product families contributing meaningfully. Scorpio revenues alone were expected to account for more than 10% of total revenues in 2025, while becoming the largest product line for Astera Labs over the next several years.

The product portfolio evolution represented more than diversification—it was a bet on the future architecture of AI infrastructure. While competitors were still optimizing for yesterday's workloads, Astera Labs was building for a future where every rack would be a supercomputer, every cable would be smart, and every byte of data would be optimized for AI processing.

VII. Financial Performance & Business Model

Michael Tate, Astera Labs' CFO, stood before a packed conference room at the Levi's Stadium Club in Santa Clara during the company's first investor day as a public company in November 2024. Behind him, a slide showed a hockey stick graph that would make any growth investor salivate. "Let me walk you through what sustainable hypergrowth looks like," he began.

The numbers told a story of explosive acceleration. Full year 2024 revenue of $396 million marked a 242% year-over-year growth from 2023's $115.8 million. But the quarterly progression revealed the real momentum: Q1 2024 at $65.3 million, Q2 at $80 million, Q3 at $113 million, and Q4 closing at $137.7 million. Each quarter wasn't just growing—it was accelerating.

"The beauty of our model," Tate explained, "is that we're achieving software-like margins in a hardware business." Q4 non-GAAP gross margin was 74.1%, a number that made traditional semiconductor companies envious and software companies respectful. This wasn't achieved through pricing power alone—it was architectural.

The fabless model was central to the strategy. Astera Labs owned no fabs, no assembly lines, no test facilities. Everything was outsourced to TSMC for silicon fabrication and to established assembly and test partners. This meant zero capital expenditure on manufacturing, allowing the company to scale revenues without proportional increases in fixed costs.

But fabless alone didn't explain the margins. The real secret was the value-per-chip. A typical Astera Labs retimer might sell for $50-200, compared to a basic analog chip selling for pennies. When you're enabling a $40,000 GPU to actually function in a system, customers don't quibble over the price of the connectivity solution.

The R&D investment strategy was aggressive but calculated. The company successfully increased headcount by nearly 80% in 2024, with the majority being engineers. This wasn't growth for growth's sake—each hire was targeted at specific product lines or customer engagements. The company maintained R&D spending at roughly 40% of revenue, a level that would be unsustainable for most hardware companies but essential for staying ahead in the connectivity arms race. Customer concentration was both a strength and a risk. The largest shareholder is FMR LLC with 14% of shares. Second and third largest shareholders hold about 7.2% and 6.7%. CEO Jitendra Mohan owns 4.6% of the company, aligning his interests with shareholders. But operational concentration was more concerning—a small number of hyperscalers drove the majority of revenue. This concentration created both incredible growth when these customers were building out AI infrastructure and significant risk if any single customer pulled back.

The unit economics told a compelling story. Average selling prices (ASPs) had grown from roughly $30 per retimer in early generations to over $100 for advanced products. The Scorpio switches commanded even higher ASPs, with some configurations exceeding $1,000. When you multiply these ASPs by millions of units shipped annually, the revenue potential becomes clear.

Cash generation was robust. Q4 2024 cash flow from operations hit $39.7 million, and the company ended the year with $914 million in cash, cash equivalents, and marketable securities—a war chest for R&D and potential acquisitions. The balance sheet was pristine with no debt, giving the company maximum flexibility to invest aggressively.

Looking forward, the financial model suggested sustainable hypergrowth. Management's Q1 2025 guidance of $151-155 million implied continued sequential growth, though at a moderating pace. More importantly, the diversification across four product lines meant multiple growth drivers. Even if one product line faced headwinds, others could compensate.

The financial story of Astera Labs wasn't just about impressive numbers—it was about proving that a semiconductor company could achieve SaaS-like economics through focus, innovation, and perfect market timing. As data centers transformed into AI factories, Astera Labs had positioned itself as an essential supplier of the connectivity tissue that held it all together.

VIII. Competition & Market Dynamics

The semiconductor industry graveyard is littered with companies that tried to take on Broadcom and Marvell in connectivity. Standing in Astera Labs' boardroom in late 2024, you could see why most had failed. On the whiteboard, someone had drawn the market share pie chart: Broadcom and Marvell controlled more than 80% of datacenter connectivity revenue, commanding 65%+ gross margins that seemed unassailable.

"David versus Goliath doesn't capture it," said Sanjay Gajendra, the COO, during a strategy session. "It's more like David versus two Goliaths who also happen to be best friends."

The duopoly had existed for decades. Broadcom, with its $600 billion market cap, could outspend Astera Labs' entire annual revenue on R&D for a single product line. Marvell, though smaller at $70 billion, had deep relationships with every major OEM and hyperscaler. Both companies had vast patent portfolios, established supply chains, and the ability to bundle connectivity solutions with other products. But Astera Labs had found cracks in the armor. Connectivity is historically an extremely competitive, but sticky high margin portion of the datacenter market. Broadcom and Marvell have been able to dominate with more than 80% revenue share at >65% gross margins, but they'd grown complacent. Their products were designed for general-purpose computing, not optimized for AI workloads. Their development cycles stretched 18-24 months. And crucially, they viewed connectivity as one product line among many, not as the core strategic battleground it was becoming.

The global retimer market size is projected to grow from USD 613.6 million in 2024 to USD 1,022.2 million by 2029, growing at a CAGR of 10.7%. This might seem like a small market, but it represented just one segment of the broader connectivity opportunity. When you added in switches, cables, controllers, and emerging standards like UALink and CXL, the total addressable market expanded into the tens of billions.

Astera Labs' competitive strategy was surgical. Rather than compete across the board, they picked specific battles where they could win. First-mover advantage became their primary weapon. They were first to market with PCIe 4.0 retimers, first with PCIe 5.0, and now first with PCIe 6.0. By the time competitors caught up to one generation, Astera was already shipping the next.

The interoperability leadership created another moat. While Broadcom and Marvell tested their products primarily with their own ecosystems, Astera Labs tested with everyone—NVIDIA, AMD, Intel, every major OEM. This Switzerland approach meant that when a hyperscaler needed a connectivity solution that worked with mixed vendor environments, Astera Labs was often the only choice.

Technical differentiation went beyond speeds and feeds. Astera's products were designed specifically for AI workloads, understanding the difference between training and inference traffic patterns, optimizing for the bursty nature of gradient updates, and minimizing tail latencies that could stall entire clusters. A Broadcom switch might have higher aggregate bandwidth, but an Astera Labs Scorpio switch delivered more effective bandwidth for AI workloads.

The partnership ecosystem reinforced these advantages. When NVIDIA mentioned Astera Labs by name at product launches, it wasn't just validation—it was a signal to the entire industry. When Intel Capital invested in the Series D, it wasn't just money—it was strategic alignment. These relationships created a virtuous cycle where success bred more success.

But the risk of commoditization loomed. As the market matured, would connectivity become a commodity where price mattered more than performance? The company's answer was to keep climbing the value stack. COSMOS software, custom silicon for specific customers, and complete reference designs that reduced time-to-market—each addition made Astera Labs harder to displace.

The competitive landscape was also evolving with new entrants. Startups flush with venture capital were targeting specific niches. Chinese companies were developing alternatives for their domestic market. Even cloud providers were considering building their own connectivity silicon. The moat that seemed impregnable in 2024 would require constant innovation to maintain.

Yet as 2024 closed, Astera Labs had achieved something remarkable: they'd carved out a profitable, defensible position in one of the semiconductor industry's most competitive segments. The question wasn't whether they could compete with Broadcom and Marvell—they'd already proven that. The question was whether they could maintain their edge as the entire industry recognized that connectivity had become the critical bottleneck in AI infrastructure.

IX. The AI Infrastructure 2.0 Thesis

Standing before a packed auditorium at the Open Compute Project Summit in San Jose in October 2024, Jitendra Mohan delivered a presentation that would reshape how the industry thought about data center architecture. Behind him, a single slide displayed a provocative statement: "AI has outgrown the server. The rack is now the unit of compute."

The traditional data center, Mohan explained, was built on a fundamental assumption: servers were independent units that occasionally needed to communicate. But AI had shattered this assumption. A single large language model training run might require thousands of GPUs working in perfect synchronization, sharing gradients millions of times per second. The server boundary had become meaningless.

"We're not building data centers anymore," Mohan said. "We're building city-sized supercomputers, and the rack is just the neighborhood."

This wasn't just marketing rhetoric. The numbers backed it up. A single training run for a frontier model could cost $100 million in compute time. A few microseconds of additional latency, multiplied across billions of operations, could add millions to that cost. The old approach of treating connectivity as plumbing—important but not strategic—was over. The infrastructure transformation was being codified in new standards. The Ultra Accelerator Link (UALink) Consortium, led by Board Members from AMD, Amazon Web Services (AWS), Astera Labs, Cisco, Google, Hewlett Packard Enterprise (HPE), Intel, Meta and Microsoft, had incorporated in October 2024. The UALink 1.0 specification would enable up to 200Gbps per lane scale-up connection for up to 1024 accelerators within an AI pod.

Astera Labs wasn't just a member—they were on the board, helping define the standard that would govern AI connectivity for the next decade. This wasn't about selling products; it was about shaping the entire industry architecture. When the standard launched, Astera would be ready with silicon, while competitors would be scrambling to understand the specification.

The rack-scale computing transformation went beyond standards. Hyperscalers were embarking on a significant transformation of their data centers to support AI applications with increased capital investment—not millions or billions, but hundreds of billions of dollars. Microsoft alone was planning to spend $80 billion on data centers in fiscal 2025. Google, Amazon, Meta—each was racing to build AI infrastructure at unprecedented scale.

In this new world, connectivity became the critical bottleneck. A modern AI training cluster might have 20,000 GPUs, each capable of 2 petaflops of compute. But if those GPUs couldn't communicate efficiently, all that compute power was wasted. The difference between 99% and 99.9% network efficiency could mean millions of dollars in wasted compute time.

Astera Labs' products were perfectly positioned for this transition. Aries retimers ensured signals could travel the longer distances required in rack-scale systems. Taurus cables connected racks to each other with minimal latency. Leo controllers pooled memory across the entire cluster. And Scorpio switches intelligently routed traffic based on workload requirements.

But the real insight was deeper. AI Infrastructure 2.0 wasn't just about faster connections—it was about intelligent connections. The COSMOS software suite could identify bottlenecks in real-time, predict failures before they happened, and automatically reroute traffic to maintain performance. This wasn't just hardware; it was infrastructure intelligence.

The multi-year growth cycle ahead was staggering in its implications. If AI models continued to double in size every year, and if training those models required proportionally more infrastructure, then the connectivity market wasn't just growing—it was exploding. The TAM that looked like $1 billion in 2024 could be $10 billion by 2030.

Patrick Moorhead from Moor Insights & Strategy captured the transformation: "Hyperscalers and AI platform providers developing systems for training and inferencing workloads have traditionally used PCIe switches that were initially designed for general purpose applications. Astera Labs is focused on the industry's need for a more performant, efficient fabric solution that's purpose-built for AI."

As 2024 drew to a close, the AI Infrastructure 2.0 thesis was no longer a thesis—it was reality. Data centers were being rebuilt from the ground up for AI. And at the heart of this transformation, connecting every GPU to every other GPU, every accelerator to memory, every compute node to storage, was Astera Labs' silicon. The company hadn't just ridden the AI wave; they'd helped create it.

X. Playbook: Lessons for Founders & Investors

In a packed auditorium at Stanford's Graduate School of Business in January 2025, Jitendra Mohan stood before an audience of aspiring entrepreneurs and venture capitalists. The moderator had just asked him the question everyone wanted answered: "How do you build a multi-billion dollar company in a space everyone else thinks is boring?"

Mohan smiled. "First, you need to understand that 'boring' is often code for 'essential but difficult.' The best opportunities often hide in plain sight, dismissed because they require deep technical knowledge to appreciate."

The Astera Labs playbook offered several crucial lessons for the next generation of infrastructure entrepreneurs:

Timing Markets: Infrastructure Before Applications

"We started building for AI in 2017, before ChatGPT, before the transformer paper had even been widely adopted," Mohan explained. "The key insight is that infrastructure investments must precede application waves by 3-5 years. By the time everyone sees the opportunity, it's too late to build the foundational technology."

The pattern was consistent across technology waves. Amazon built AWS years before cloud computing went mainstream. NVIDIA invested in CUDA a decade before deep learning took off. The founders and investors who win big are those who can see around corners, who understand that today's research paper is tomorrow's trillion-dollar industry.

Building Technical Moats in "Boring" Spaces

The connectivity market seemed commoditized from the outside. But Astera Labs understood that complexity could be a moat. Every new PCIe generation doubled the technical challenges. Signal integrity at 64 GT/s wasn't just incrementally harder than 32 GT/s—it required fundamental innovations in circuit design, materials science, and manufacturing.

"Our moat wasn't a single patent or innovation," Gajendra explained in a separate session. "It was the accumulation of thousands of small insights, each insignificant alone but collectively insurmountable. Every customer deployment taught us something new. Every edge case we solved became part of our institutional knowledge."

The Power of Being Switzerland

In a world of walled gardens and proprietary ecosystems, Astera Labs chose to support everyone. They tested with NVIDIA GPUs, AMD accelerators, Intel CPUs, and every ARM variant. This wasn't just about market coverage—it was about becoming indispensable.

"When you're the only company that can guarantee interoperability across vendors, you become the default choice," Morrison noted. "Hyperscalers don't want vendor lock-in. By being neutral, we became essential."

Capital Efficiency in Fabless Models

The fabless model wasn't just about avoiding capital expenditure—it was about focus. While competitors managed fabs, dealt with yield issues, and worried about utilization, Astera Labs focused entirely on design and customer engagement.

"Every dollar we didn't spend on fabs was a dollar we could invest in R&D or customer support," CFO Michael Tate explained. "In a business where being six months late means missing the entire market window, that focus is everything."

When to Go Public: Riding Momentum

The decision to go public in March 2024 seemed risky at the time. The IPO window had been closed for two years. Many advisors suggested waiting for more certainty. But Mohan and his team understood that momentum matters more than perfection.

"We could have waited for another year of results, gotten our revenue to $500 million, reduced our customer concentration," Mohan reflected. "But we would have missed the moment when the market was desperate to invest in AI infrastructure. Sometimes the best time to go public is when it feels slightly uncomfortable."

Customer Concentration: Feature or Bug?

Most investors saw Astera Labs' customer concentration as a risk. The company saw it as validation. Having Amazon, Microsoft, and Google as your primary customers meant you'd solved the hardest problems for the most demanding users.

"The key is to use concentration as a launching pad, not a crutch," Gajendra advised. "Those early lighthouse customers validate your technology. Then you systematically expand. But you can't be afraid to start focused."

The Platform Transition

The evolution from single products to platforms was crucial. Aries retimers were a product. The Intelligent Connectivity Platform—spanning four product families and unified by COSMOS software—was a platform. The difference wasn't just semantic; it was strategic.

"Products can be replaced. Platforms become embedded in customer workflows," Morrison explained. "When your software is managing thousands of devices, generating terabytes of telemetry data, and informing billion-dollar infrastructure decisions, you've moved beyond vendor to partner."

Recruiting in Hypergrowth

Growing headcount by 80% in a year while maintaining culture and quality seemed impossible. The key was systematic onboarding and clear cultural values. Every new hire spent their first week not in technical training but in understanding the company's mission and values.

"We hired for slope, not intercept," Mohan said, borrowing a favorite Silicon Valley phrase. "We'd rather have someone who could grow with us than someone who knew everything but couldn't adapt."

The Long Game in Short-Term Markets

Public markets demanded quarterly results, but infrastructure required multi-year commitments. Astera Labs squared this circle by being transparent about their long-term strategy while delivering consistent short-term execution.

"We told investors from day one: we're building for the next decade of AI infrastructure," Tate explained. "Some quarters will be spectacular, others merely good. But the trajectory is clear."

As the Stanford session concluded, a venture capitalist in the audience asked the ultimate question: "What's the next Astera Labs? Where should we be looking?"

Mohan paused, then offered his final insight: "Look for problems that everyone agrees exist but nobody wants to solve. Look for technical challenges that require years of patient capital. Look for markets where the incumbents have stopped innovating. And most importantly, look for founders who are building for a future that doesn't quite exist yet—but inevitably will."

XI. Analysis & Investment Case

Sitting in Fidelity's Boston headquarters in early 2025, portfolio manager Sarah Chen stared at her screens showing Astera Labs' stock chart—up over 300% since IPO less than a year ago. Her team was debating whether to increase their position, already the fund's largest semiconductor holding. The investment case had evolved dramatically since their Series C investment in 2021.

Bull Case: The Infrastructure Supercycle

The bullish argument was compelling in its simplicity: AI infrastructure spending was entering a multi-year supercycle with no end in sight. Every hyperscaler had announced massive capacity expansions. Microsoft's $80 billion fiscal 2025 infrastructure budget was just the beginning. Google, Amazon, Meta, Oracle—combined, they were approaching $300 billion in annual infrastructure spending.

Within this tsunami of investment, connectivity was becoming the critical bottleneck. As one analyst noted, "You can have the world's fastest GPU, but if it can't talk to memory or other GPUs efficiently, it's just an expensive paperweight." Astera Labs was uniquely positioned to benefit from this dynamic, with all four product lines hitting stride simultaneously.

The TAM expansion was breathtaking. The retimer market alone was projected to grow from $613 million to over $1 billion by 2029. But that was just one product line. Add in switches (a $5 billion market), smart cables ($3 billion), and memory controllers ($2 billion), and the total addressable market exceeded $11 billion by 2029. Astera Labs didn't need to dominate every segment—even 10% market share would imply $1 billion in revenue.

The competitive position appeared sustainable. While Broadcom and Marvell dominated legacy connectivity, they'd been slow to optimize for AI workloads. Their general-purpose products worked but weren't optimal. By the time they fully pivoted to AI-specific solutions, Astera Labs would have years of deployment data and customer relationships.

Perhaps most compelling was the margin structure. Maintaining 70%+ gross margins while growing revenue at triple-digit rates defied conventional semiconductor economics. This wasn't commoditized silicon but essential infrastructure with high switching costs. Once deployed, Astera Labs' products became embedded in customer operations, with COSMOS providing ongoing value through optimization and monitoring.

Bear Case: The Shadows on the Horizon

But the bear case had merit too. Customer concentration remained alarming—what happened if even one hyperscaler pulled back? The macro environment was uncertain, with potential recessions, geopolitical tensions, and questions about AI ROI. Could companies really justify hundreds of billions in AI infrastructure investment if the killer applications didn't materialize?

Competition was intensifying. Broadcom had awakened to the threat and was pouring resources into AI-optimized connectivity. Marvell had acquired several smaller players to accelerate their roadmap. Even NVIDIA was expanding beyond compute into networking and connectivity. The cozy dynamic of 2024 might not last.

Technology transitions posed another risk. PCIe 7.0 specifications were already being drafted, and new standards like UALink might obsolete current products. While Astera Labs was participating in these standards bodies, there was no guarantee they'd maintain their first-mover advantage in new generations.

The valuation had become stretched by any traditional metric. Trading at over 60x forward earnings and 15x forward sales, Astera Labs was priced for perfection. Any stumble—a delayed product, a customer pushback, a competitive loss—could trigger a violent repricing.

Supply chain vulnerabilities lurked beneath the surface. TSMC manufactured most of Astera Labs' silicon. Any disruption—whether from geopolitical tensions over Taiwan, natural disasters, or capacity constraints—could cripple production. The fabless model that enabled capital efficiency also created dependence.

Valuation Framework: Finding Fair Value

Traditional semiconductor valuation metrics struggled with Astera Labs. The company traded like software (15x revenue) but manufactured hardware. It grew like a startup (200%+ annually) but generated profits like a mature company.

Chen's team developed a hybrid framework. They valued the base retimer business using traditional semiconductor multiples—roughly 5x revenue or 25x earnings. This implied a $2 billion valuation for the core business. They then added option value for emerging product lines: $3 billion for Scorpio switches, $2 billion for Taurus cables, $1 billion for Leo controllers. Finally, they assigned $2 billion in platform value for COSMOS and the integrated ecosystem.

This summed to roughly $10 billion in fair value, compared to the current $31 billion market cap. Bulls argued the market was correctly pricing in five years of growth. Bears saw a bubble waiting to burst.

Key Metrics to Watch

Several indicators would determine which narrative proved correct:

Customer diversification was critical. If Astera Labs could reduce their top three customers from 70% of revenue to below 50%, it would dramatically reduce risk. Early signs were positive, with smaller cloud providers and enterprise customers beginning to adopt their products.

Product mix would determine margins. Scorpio switches and COSMOS software commanded higher margins than retimers. If these became 50% of revenue by 2026, gross margins could expand to 80%, justifying premium valuations.

Competitive wins mattered more than aggregate growth. Each design win against Broadcom or Marvell proved Astera Labs' technical superiority. Conversely, any high-profile loss would raise questions about their moat.

R&D productivity would determine long-term success. The company needed to maintain their 12-month product development cycle while expanding into new categories. Any delays or quality issues could prove fatal in such a fast-moving market.

The Investment Decision

Chen's team ultimately decided to maintain their position but not add. The company had exceptional fundamentals and massive tailwinds, but the valuation left no room for error. They would wait for either a pullback to add or evidence that the company could sustain 50%+ growth beyond 2025.

For new investors, the calculus was different. Those believing in the AI infrastructure supercycle saw Astera Labs as essential exposure to the theme. Even at premium valuations, owning the "picks and shovels" of the AI revolution made strategic sense.

The investment case for Astera Labs ultimately came down to a simple question: Was AI infrastructure investment a temporary bubble or a fundamental platform shift comparable to the internet? If the former, Astera Labs was wildly overvalued. If the latter, it might still be early innings for one of the decade's great growth stories.

XII. Epilogue: What's Next for Astera Labs

As dawn broke over Silicon Valley on January 2, 2025, Jitendra Mohan stood in Astera Labs' new San Jose headquarters—a gleaming complex designed to house 900 employees. Through his office window, he could see construction crews already at work on the second phase. The company that had started in a garage with three engineers now employed over 500 people across six global offices.

But Mohan wasn't looking back. On his desk lay product roadmaps extending to 2030, architectural diagrams for systems that wouldn't exist for years, and strategic plans that would seem like science fiction to most. The journey from zero to $31 billion in market cap had been remarkable. The journey from here might be even more extraordinary.

The immediate future was clear. 2025 would be the year of Scorpio, with the flagship fabric products for head-node PCIe connectivity and backend AI accelerator scale-up clustering becoming the company's largest revenue driver. Early customer feedback had been exceptional. One hyperscaler's architect called Scorpio "the missing piece we didn't know we needed."

The PCIe 7.0 transition loomed on the horizon. Specifications would be finalized in 2025, with products shipping in 2026. At 128 GT/s—double PCIe 6.0's speed—the technical challenges were staggering. But Astera Labs' engineers were already deep in development, working with advanced materials and novel circuit designs that seemed impossible just years ago.

Geographic expansion offered another growth vector. While North American hyperscalers drove current revenue, Asian markets were investing aggressively in AI infrastructure. China, despite trade tensions, was building its own AI ecosystem. Japanese companies were pioneering edge AI deployments. Indian data centers were scaling rapidly. Each market needed connectivity solutions, and Astera Labs' Switzerland approach positioned them uniquely.

The M&A landscape was intriguing. With nearly $1 billion in cash and a valuable stock currency, Astera Labs could acquire complementary technologies. Optical connectivity, advanced cooling solutions, or AI acceleration IP—each could extend their platform. But Mohan was cautious: "We'll only acquire if it accelerates our roadmap by years, not quarters."

Perhaps most exciting was the vision Mohan shared with his leadership team: becoming the connectivity layer for all AI—not just in data centers but at the edge, in vehicles, in robots. Wherever AI compute happened, it would need connectivity. And increasingly, that connectivity would be intelligent, adaptive, and optimized in real-time.

"We've proven that connectivity matters," Mohan said at the company's 2025 kickoff. "Now we're going to prove that intelligent connectivity is the foundation of AI infrastructure."

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube