Akamai Technologies: The Edge of Survival, Security, and the AI Frontier

I. Introduction & Episode Roadmap

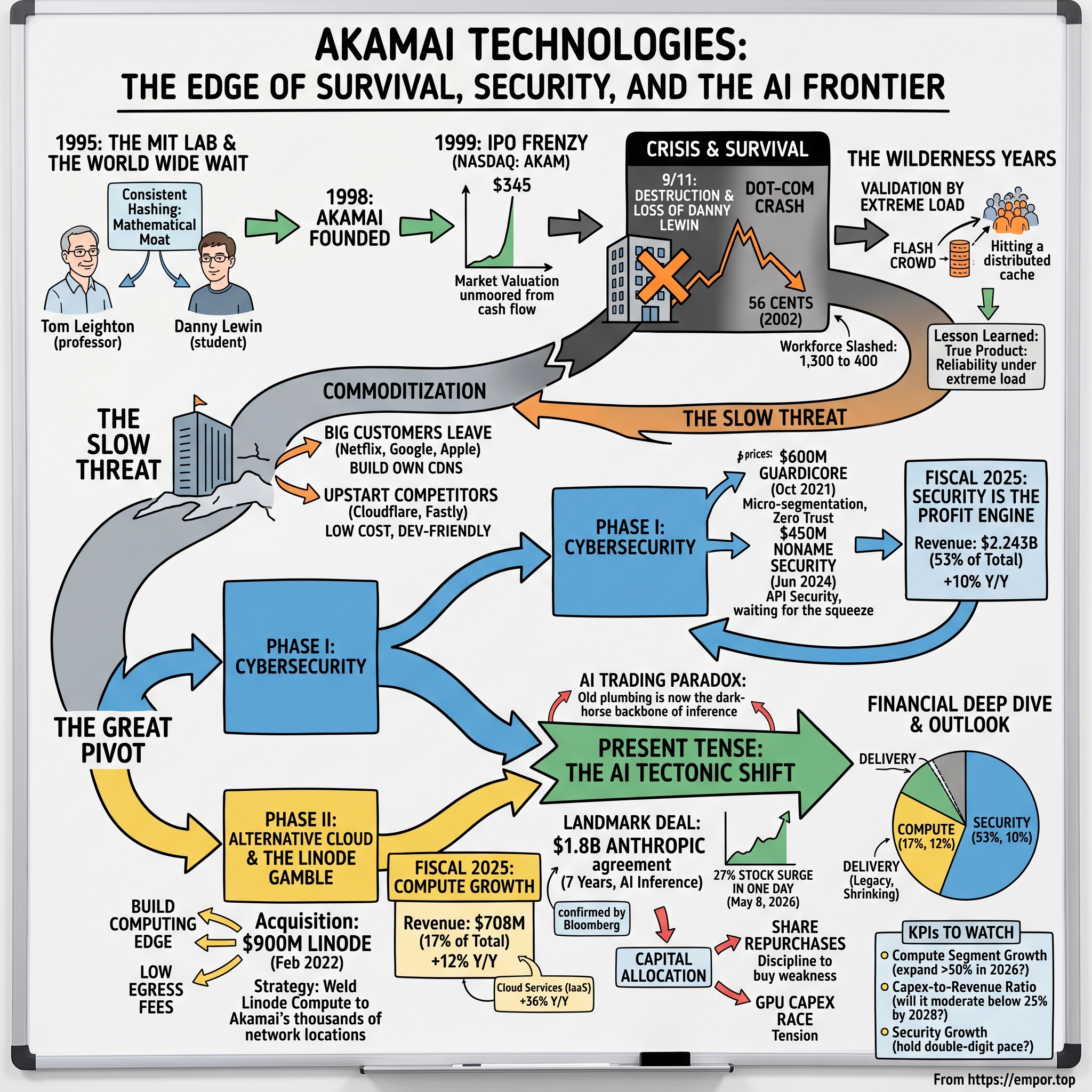

On the morning of May 8, 2026, traders who had spent two decades treating Akamai Technologies as a slow-motion melting ice cube watched something they had not seen since the Bush administration. The stock ripped 27% higher in a single session — its largest one-day move in more than twenty-two years.1 For a company that most of Wall Street had filed under "legacy internet plumbing, in managed decline," it was the equivalent of a retiree suddenly qualifying for the Olympics.

The catalyst was a sentence buried in a first-quarter earnings release: a leading United States frontier model provider had committed roughly $1.8 billion over seven years to run its artificial-intelligence workloads on Akamai's cloud.2 Bloomberg quickly identified the customer as Anthropic, the maker of Claude, and the number instantly recontextualized the entire company.1 Here was a firm born in a 1990s MIT lab, one whose stock had once crashed from a split-adjusted peak of roughly $345 all the way to fifty-six cents, being cast as a dark-horse backbone of the AI inference era.

That is the paradox at the heart of this story. Akamai practically invented the content delivery network — the invisible layer of caches that makes the web feel fast — and then spent fifteen years watching that very business get commoditized into a utility. Cloudflare and Fastly emerged as cheaper, developer-friendly upstarts. Netflix, Google, and Apple built their own delivery networks and walked away as customers. By any reasonable script, Akamai should have become another tech relic, a Yahoo or a RealNetworks, coasting on maintenance revenue until an acquirer put it out of its misery.

Instead, management did something rarer than surviving disruption: it cannibalized itself on purpose. It turned the world's largest edge network into a global security sensor, then bolted on a low-cost alternative cloud, and is now betting billions of dollars of borrowed capital that the geography of AI inference will favor exactly the kind of sprawling, close-to-the-user infrastructure it spent twenty-five years building.

Whether that bet is visionary or a capital-intensive trap is the question this episode exists to interrogate. So here is the roadmap. We begin in an MIT laboratory where a mathematician and his graduate student answered Tim Berners-Lee's warning about the "World Wide Wait." We pass through the darkest day imaginable — the murder of co-founder Danny Lewin aboard the first plane to strike the World Trade Center — and the near-death experience of the dot-com bust. We trace the Great Pivot in two phases: security, built through the Guardicore and Noname Security acquisitions, and compute, anchored by the $900 million purchase of Linode. Then we reach the present tense: the mechanics of the Anthropic deal, a $3 billion convertible bond issue, and a capital-expenditure race that will either mint a new growth company or drown an old one in depreciation. We will run the bull case and the bear case against each other, and end with the handful of numbers that will tell you, over the next three years, which story is true.

Let us start where all of it started — with a problem nobody had yet learned to name.

II. The MIT Lab & The World Wide Wait: Founding Context

Picture the Laboratory for Computer Science at MIT in 1995. The web is four years old as a public phenomenon and already groaning under its own popularity. A page that took two seconds to load on a quiet morning could take thirty in the afternoon crush, as thousands of requests funneled back to a single overwhelmed origin server on the far side of the country. Tim Berners-Lee, the physicist who had invented the World Wide Web and now worked down the hall at MIT, saw the bottleneck with unusual clarity. He warned colleagues that without a fundamental fix, the "World Wide Web" would degrade into the "World Wide Wait," and he issued a challenge: solve the delivery problem before congestion strangled the medium in its cradle.

The person who took the challenge most seriously was not a networking engineer at all. Tom Leighton was a professor of applied mathematics, a specialist in parallel algorithms and the mathematics of distributed systems — the sort of academic who saw the internet not as cables and routers but as a giant graph waiting to be optimized. Down the corridor from Berners-Lee, Leighton became fascinated by a question with an elegant framing: if you cannot make the single central server bigger, can you make the whole network smarter?

The conventional instinct in the mid-1990s was brute force — buy a more powerful server, add more bandwidth at the origin, and hope demand did not outrun the budget. Leighton's instinct was the opposite. Rather than one enormous server, he imagined thousands of ordinary machines scattered across the internet, each holding copies of popular content close to the users requesting it. When someone in Denver asked for a file, they would be served from a nearby cache in Denver rather than a distant data center in Boston. It was less like building a bigger warehouse and more like opening a corner store on every block.

The trouble with that vision was mathematical. If you spread content across a constantly changing fleet of servers — machines crash, get added, get removed every minute — how do you keep track of which server holds what, without reshuffling the entire index each time the fleet changes? Solve it clumsily and the system spends all its energy re-cataloging itself. This is where Leighton's most gifted student entered the story.

Daniel "Danny" Lewin was not a typical graduate student. Born in the United States and raised largely in Jerusalem, he had served as an officer in the Israel Defense Forces' elite Sayeret Matkal unit before arriving at MIT, and he carried that intensity into everything — a mix of physical fearlessness and relentless drive that colleagues never forgot.5 Working with Leighton, Lewin helped crack the indexing problem with an algorithm called consistent hashing.

Here is consistent hashing in plain terms. Imagine arranging every server and every piece of content around the rim of a clock face, each assigned a position by a mathematical hash. To find where a file lives, you start at the file's position and walk clockwise to the next server. The beauty is what happens when a server dies or a new one joins: only the small slice of content adjacent to that one server needs to move. The other 99% of the map is untouched. A system that would otherwise convulse every time a machine changed instead absorbs churn gracefully. This was the mathematical moat — a way to scale a distributed cache to internet size without the coordination collapsing under its own weight.

Theory became a company the way many MIT projects do: through a contest. In 1998, Leighton and Lewin's plan won recognition in MIT's celebrated $50K Entrepreneurship Competition, the validation that convinced them the algorithms were a business, not just a paper. Later that year they incorporated Akamai Technologies in Delaware. The name is a Hawaiian word meaning intelligent, clever, or cool — a fittingly playful label for a very serious piece of mathematics.

Then came the frenzy. Akamai listed on NASDAQ under the ticker AKAM, debuting on October 29, 1999 at an IPO price of $26. The market, in the full delirium of the dot-com bubble, did not so much price the stock as detonate it — shares opened around $110 and vaulted higher from there, and by the close of that fourth quarter the stock had traded as high as roughly $345.6 A company with negligible revenue was briefly worth tens of billions of dollars. It was, in retrospect, an almost perfect artifact of its moment: real technology, genuine brilliance, and a valuation completely unmoored from anything a cash flow could justify. That gap between the mathematics and the market capitalization was about to close in the most violent way imaginable.

III. 9/11, The Dot-Com Crash, and the Battle for Survival

The morning of September 11, 2001 began, for Danny Lewin, like a routine business trip. He boarded American Airlines Flight 11 out of Boston, bound for Los Angeles. He was thirty-one years old, Akamai's chief technology officer, and by most accounts the beating heart of the company's engineering culture.

What happened aboard that aircraft has been pieced together from the 9/11 Commission's investigation. Lewin was seated close to several of the hijackers. As a former Sayeret Matkal officer trained in close-quarters counterterrorism, he appears to have grasped what was unfolding faster than anyone and attempted to intervene against the men seizing the plane. He was stabbed and killed during the takeover — very likely the first person murdered in the attacks of that day, before Flight 11 struck the North Tower of the World Trade Center.5 The company's co-founder, its technical visionary, and one of the more extraordinary personalities in American technology died in the opening minutes of the worst terrorist attack in the nation's history.

It is difficult to overstate the compounding cruelty of the timing. Akamai was already reeling. The dot-com bubble had burst eighteen months earlier, and Akamai's customer base — cash-incinerating internet startups — was evaporating in real time. The stock that had touched roughly $345 collapsed toward a rock-bottom fifty-six cents in 2002. Revenue that depended on companies buying traffic delivery cratered as those companies went bankrupt. The workforce was slashed from around 1,300 employees to roughly 400. And now the person who might have rallied that shrunken team through the wreckage was gone.

The people left holding the company were George Conrades, the veteran executive who had come in as CEO, and Tom Leighton, who stepped back from any illusion of retirement and settled in as chief scientist and the keeper of the founding technical vision. Their approach in these years was not glamorous. It was survival accounting: hoard cash, cut relentlessly, and prove — over and over, event by event — that the network actually worked when it mattered most.

And here the story turns, quietly, on a point that would define the next two decades. Akamai's network did not just survive the crisis; it was validated by it. When 9/11 sent the entire country to news websites simultaneously, most media sites buckled under a traffic spike they had never designed for. Akamai's distributed caches absorbed the surge, keeping information flowing precisely when centralized infrastructure failed. The same pattern repeated with software downloads, live sports streaming, and enterprise media over the following years. Every time the internet faced a "flash crowd," Akamai's corner-store-on-every-block architecture proved its worth.

That is the strategically important takeaway from the wilderness years: Akamai learned that its true product was not cheap bandwidth but reliability under extreme load — a reputation for never going down when everyone showed up at once. Banks, governments, and broadcasters would pay a premium for that assurance. It was the seed of a moat built on trust and mission-critical dependency rather than raw price.

But a moat built on reliability is not the same as a moat built on uniqueness. As the 2000s wore on, the painful truth emerged that delivering bytes quickly, however heroically, was becoming something anyone with data centers and capital could do. The company had survived the crash. It now faced a slower, more insidious threat: commoditization. To beat that, Akamai would have to become something other than a content delivery network — and the raw material for its reinvention was hiding in plain sight, inside the very traffic it was already carrying.

IV. The Great Pivot Phase I: The Shift from Content to Cybersecurity

By the late 2000s, the CDN business had a structural problem that no amount of engineering excellence could fix. Bandwidth was turning into a utility, priced like electricity and trending toward zero. Worse, Akamai's biggest customers were becoming its competitors. Netflix, whose streaming traffic once made it a marquee Akamai client, built its own Open Connect delivery network and walked. Google and Apple did the same. Why rent the corner store when you generate enough volume to own the whole supply chain?

Meanwhile a new generation of attackers arrived from below. Cloudflare, founded in 2009, offered a freemium model and a developer-friendly, programmable edge that made Akamai's enterprise sales motion look ponderous and expensive. Fastly courted engineers with real-time configurability. Both undercut Akamai on price and out-marketed it on developer love. The delivery business was being squeezed from the top by hyperscalers insourcing and from the bottom by cloud-native upstarts. Managed decline beckoned.

The insight that saved the company came from reframing what Akamai actually was. Running the world's largest edge network meant sitting astride an enormous fraction of global internet traffic. And a network that can see traffic can inspect it; a network that can inspect it can filter it. If you can cache a web page, you can also stand in front of that page and block the malicious requests trying to knock it offline or break into it. The same distributed footprint that delivered content could deliver defense.

Akamai had dabbled here for years — Kona Site Defender and its web application firewall (WAF) products let customers absorb distributed denial-of-service attacks by soaking up the flood across Akamai's global capacity, and its scale made it a natural DDoS shock absorber. But dabbling was not a strategy. Turning security into the company's center of gravity required buying capabilities Akamai did not have, and doing it with discipline. That is where the acquisition story gets interesting, because it doubles as a test of management's capital-allocation judgment.

The first landmark move came in 2021, when Akamai acquired the Israeli micro-segmentation pioneer Guardicore for roughly $600 million in cash, completing the deal that October.7 Micro-segmentation is worth explaining in plain terms, because it is the crown jewel of the modern portfolio. Traditional network security is a castle wall: hard on the outside, soft in the middle. Once an attacker breaches the perimeter, they can move freely from server to server inside — the way ransomware spreads across a hospital in hours. Micro-segmentation puts a locked door between every pair of rooms inside the castle, so a breach in one workload cannot leap to the next. It is the practical machinery of "zero trust," the security philosophy that assumes the attacker is already inside.

At the price paid, Guardicore was generating only an estimated $30–$35 million of annual recurring revenue, which implies a heady mid-to-high-teens multiple of forward revenue. Taken in isolation that looks aggressive. But 2021 was the peak of the cybersecurity bubble, when public comparables like CrowdStrike and SentinelOne traded at thirty to fifty times revenue, so Akamai was arguably buying a scarce asset at a relative discount. The proof, though, is in what the asset became. By fiscal 2025, the combined Guardicore Segmentation and API Security line grew 43% year over year to $293 million.3 A business bought for its promise had, four years later, more than validated the price — a genuinely successful integration, and evidence that Akamai's enterprise sales force could scale a bolt-on acquisition faster than the founders could have alone.

The second move revealed a different management muscle: patience. In June 2024, Akamai acquired Noname Security — a leader in API security, the discipline of protecting the application programming interfaces that modern software uses to talk to itself — for roughly $450 million.8 The instructive detail is the price relative to history. Noname had been valued at about $1.0 billion in a December 2021 private funding round. Akamai bought it for well under half that, a discount of more than fifty percent, by waiting for the venture-capital funding squeeze to break the seller's leverage. Where the Guardicore deal showed a willingness to pay up for scarcity at a market top, the Noname deal showed the discipline to buy the same category near a market bottom. Two acquisitions, two very different environments, one consistent instinct about where the value was.

The cumulative result reordered the company. By the end of fiscal 2025, Security contributed $2.243 billion of revenue, roughly 53% of the total, growing about 10% year over year and dwarfing the legacy delivery business.3 The segment that barely existed as a category fifteen years earlier had become the profit engine. For investors, the meaning is straightforward: Akamai is now, first and foremost, a cybersecurity company with a CDN attached, not the other way around — and the market's stubborn refusal to price it that way is the central tension of the bull case we will reach later.

Security answered the question of how Akamai would make money. It did not answer the question of where the next wave of computing would happen. For that, management placed a second, structurally different bet — one that traded software-like margins for the heavier economics of iron and electricity.

V. The Great Pivot Phase II: Alternative Cloud & The Linode Gamble

There was an architectural hole in Akamai's story, and management knew it. Cloudflare and Fastly had spent years building serverless runtimes — Workers, Compute@Edge — that let developers run small snippets of code directly on the edge. That was clever, but it was lightweight by design. What large enterprise customers increasingly wanted was heavier: full-scale, developer-friendly Infrastructure-as-a-Service, the ability to spin up real virtual servers and databases — but without paying the premium the "Big Three" hyperscalers charged. Akamai had a magnificent edge network and no proper cloud to run on it.

Rather than build one from scratch — a multi-year slog against AWS, Azure, and Google Cloud's enormous head start — Akamai bought one. In February 2022 it agreed to acquire Linode for approximately $900 million.9 Linode was a beloved, almost cult-favorite alternative cloud provider, founded in 2003, known for straightforward pricing and a developer base that valued simplicity over the dizzying menu of hyperscaler services. It generated roughly $100 million of annual revenue, which put the headline multiple at about nine times trailing revenue. Factoring in an estimated $120 million net present value of cash tax savings from structuring the deal as an asset purchase, the effective net price fell to around $780 million, or closer to eight times revenue — a reasonable figure against a peer like DigitalOcean, which traded richer at the time.

The strategy was to weld Linode's compute engine to Akamai's edge. Linode brought the machinery for spinning up virtual servers; Akamai brought thousands of network locations sitting inside local internet service providers around the world. Marketed as the Akamai Connected Cloud, the pitch centered on one of the most quietly resented features of hyperscaler pricing: egress fees. When you store data with a big cloud provider, moving that data out — to your users, to another vendor, to your own premises — triggers per-gigabyte charges that can dominate a bill and quietly lock customers in. It is the roach-motel economics of the cloud: data checks in, but it costs a fortune to check out. Akamai positioned Connected Cloud as the low-egress alternative, bundling compute, security, and delivery on a single network and pitching itself as the neutral, cheaper option for companies wary of hyperscaler lock-in.

The economics, however, come with a catch that investors must hold in view. In fiscal 2025 the Compute segment generated $708 million, up about 12% year over year, with the newer Cloud Infrastructure Services (the true Linode-descended IaaS business) growing far faster — on the order of 36% to reach roughly $314 million.3 Healthy growth. But running physical servers is fundamentally a lower-margin business than selling security software. Cloud compute carries gross margins in the rough neighborhood of 50–55%, against the 75–80% economics of high-end cybersecurity. As compute grows into the mix, it structurally dilutes the company's blended profitability. Consolidated GAAP gross margin settled around 60% in 2025, down from the loftier levels of the pure-CDN era.

That trade-off frames the honest question hanging over Phase II: is Akamai buying its way into a large, strategically vital, but permanently capital-hungry business — or is it building the distribution layer that will let it monetize the single biggest computing shift in a generation at margins that improve with scale? For three years, that was a debate about a modest, steadily growing compute line. Then, in the spring of 2026, one customer turned the debate into an emergency.

VI. The AI Tectonic Shift: The $1.8B Anthropic Deal & The GPU Capex Explosion

To understand why a $1.8 billion contract could move a mature stock 27% in a day, you have to understand a distinction that the AI boom has made suddenly enormous: the difference between training a model and serving it.

Training a frontier model like Claude is the part everyone photographs — tens of thousands of GPUs packed into a handful of gargantuan data centers, humming for months to grind through the mathematics of learning. It is centralized by nature; the chips need to talk to each other at blistering speed, so they sit together. Inference — actually answering a user's question once the model is trained — is a different animal. It happens billions of times a day, and it is exquisitely sensitive to latency. When a user in Jakarta or São Paulo types a prompt, every hundred milliseconds of round-trip delay to a distant mega-cluster degrades the experience. Inference wants to be close to the user.

Close to the user is precisely, almost eerily, what Akamai has spent a quarter-century building. Its network of thousands of edge locations, wedged inside local ISPs across more than 130 countries, was designed to put content one short hop from the person requesting it. Repurpose those locations to hold GPUs, and you have a natural home for latency-sensitive inference that also sidesteps the hyperscaler egress tax on moving all that data around. That is the strategic logic behind the deal Akamai disclosed on May 7, 2026, alongside its first-quarter results: a seven-year committed-capacity agreement, later confirmed to be with Anthropic, worth roughly $1.8 billion for AI inference on Akamai Connected Cloud.21

The demand context matters, and it cuts both ways. Anthropic was not choosing Akamai out of loyalty; it was buying compute from everyone in sight. Chief executive Dario Amodei described roughly 80-fold growth in the company's annualized run-rate over a span of months and said the firm was securing capacity "as quickly as possible," having struck parallel deals with other suppliers.10 So the bull reads this as validation that frontier labs cannot rely on hyperscalers alone and need independent edge capacity. The bear reads the same fact as a warning: a customer buying from everyone is a customer with no particular attachment to you, and demand assembled in a panic can be unwound just as quickly.

Then came the money question. Filling edge locations with GPUs is brutally capital-intensive, and Akamai did not pretend otherwise. Management guided 2026 capital expenditure to a startling 40–42% of revenue — implying something like $800–$825 million of spending in a single year — against a historical CDN baseline closer to 10–15% and an early-compute baseline around 25–26%.[^10] For a company whose identity for a decade rested on generating dependable free cash flow, this was a philosophical rupture as much as a financial one.

To fund it without gutting the balance sheet, Akamai reached for a classic piece of financial engineering. In May 2026 it issued $3.0 billion of 0% convertible senior notes, split between tranches maturing in 2030 and 2032, upsized from an initially smaller deal amid strong demand.4 Zero-coupon convertibles are an elegant instrument for exactly this situation: Akamai pays no cash interest, and the bonds only convert into stock if the share price climbs well above conversion prices set around $190–$201 — a substantial premium to where the stock traded when the notes were priced.4 In effect, the company borrowed $3 billion for free in cash terms, betting it can invest the proceeds at a return far above zero.

But "free" money still creates two hazards, and management moved to blunt both. The first is dilution — if the stock soars past the conversion price, bondholders become shareholders and existing owners get diluted. To offset this, Akamai layered on convertible-note hedges and cash-settled warrants, a structure designed to push the effective dilution threshold higher. The second is optics: issuing $3 billion of debt while simultaneously spending on GPUs could look like a company losing its financial discipline. So Akamai carved out roughly $350 million of the proceeds to repurchase its own shares alongside the offering — a signal to skeptical investors that the balance sheet was being managed, not merely levered up.

The tension came to a head on the May 7 earnings call, where analysts pressed management on whether this was "good capex" — capacity locked in by a signed contract with a knowable return — or speculative GPU hoarding of the kind that has burned capital-intensive businesses before.[^10] Management's defense rested on the word committed: the Anthropic capacity is contracted, not built on spec, so the GPUs have a customer before they are switched on. The candor, to management's credit, extended to the pain. Executives acknowledged that near-term GAAP operating margins and free cash flow would be heavily compressed by the depreciation and build-out costs, that the Anthropic revenue would only begin ramping in the fourth quarter of 2026 — contributing a modest $20–$25 million in that first quarter — and that the real top-line payoff would not arrive until 2027.21

For an investor, that framing is the whole ballgame. If the capex is genuinely underwritten by contracted, multi-year demand at a healthy return on invested capital, Akamai is pre-funding a growth business at zero cash interest cost — a coup. If demand softens, or if serving AI inference proves to be a low-margin, chip-cycle treadmill, the company will have swapped dependable free cash flow for a mountain of depreciating silicon and $3 billion of debt. The next section puts hard numbers around both possibilities.

VII. Financial Deep Dive: Segment Economics, Comps, and Capital Allocation

Strip away the narrative and Akamai in fiscal 2025 was a $4.208 billion revenue business growing about 5% a year — a number that, on its own, explains the market's "legacy" verdict.3 But the consolidated figure hides three companies moving in three different directions, and the whole investment case lives in the divergence.

The first company is Security, at $2.243 billion and roughly 53% of revenue, growing around 10%.3 This is the cash cow and the value engine — high gross margins, high switching costs, and the kind of low churn you get when a bank has wired your web application firewall and your micro-segmentation into the guts of its infrastructure. The second is Delivery and other legacy cloud applications, at roughly $1.257 billion and about 30% of revenue, and shrinking.3 This is the original CDN business in structural decline, commoditized and under permanent pricing pressure; in the fourth quarter alone delivery revenue fell about 2% year over year.3 It is the anchor dragging on consolidated growth and blended margin. The third is Compute, at $708 million and roughly 17% of revenue, growing about 12% overall but far faster in its core IaaS layer — and now carrying the enormous optionality of the Anthropic deployment, which management expects to expand the segment by well over 50% in 2026.32

Put those three together and you see why the stock is so hard to price. Security and Compute already represent over 70% of revenue, yet the market applies a multiple closer to that of the declining 30% than the growing 70%. The peer comparison sharpens the point. Cloudflare, at roughly $2.17 billion of revenue, was growing around 30% with GAAP gross margins near 74.5% and commanded a premium growth multiple to match.[^13] Fastly, far smaller at roughly $624 million, grew around 15% with gross margins near 57.1% and reached its first year of non-GAAP profitability.[^13] Akamai is nearly twice Cloudflare's size and many times Fastly's, throws off far more cash than either, and yet trades at a fraction of Cloudflare's valuation multiple. The bull says that is a mispricing waiting to correct; the bear says slower growth and lower margins earn a lower multiple, and the market is simply right.

Which brings us to capital allocation — the arena where management's character shows most clearly. Akamai has for years been an aggressive buyer of its own stock, and the recent pace tells a story. In 2024 it repurchased 5.6 million shares for roughly $557 million, at an average price around $99.14. Through 2025 it repurchased about 10.0 million shares for roughly $800 million, at an average price around $79.77.11 Read those two lines together and note the discipline: the company bought more shares for more money at a lower average price as the stock fell. That is buying weakness rather than chasing strength — the correct direction, and a mark in management's favor.

But there is an obvious and uncomfortable conflict. How can a company sustain an $800 million-a-year buyback while simultaneously committing $800 million-plus a year to GPU infrastructure? The honest answer is that it cannot do both from free cash flow alone — which is precisely what the $3 billion convertible was for. The zero-coupon debt lets Akamai push the capital-intensive build-out onto the balance sheet while preserving operating cash for buybacks. It is internally coherent. It is also a bet: it works cleanly only if the AI investments earn their contracted returns and the stock recovers enough to make the whole structure look shrewd in hindsight rather than reckless. An activist would fairly ask whether shrinking the share count with borrowed money, in the same breath as levering up for an unproven business, is disciplined capital allocation or financial sleight of hand. The answer will not be known until the Anthropic capacity is fully utilized — or isn't.

Those are the numbers. Underneath them sits a set of structural advantages — and vulnerabilities — that determine whether the whole edifice holds. It is worth stepping back from the quarterly figures to ask what, if anything, actually protects this business.

VIII. Playbook: Durable Business & Investing Lessons

Every great business story eventually resolves into a question of durability: not "did it win?" but "can it keep winning, and why?" Akamai offers an unusually rich case study, because its moat is real in some places and rhetorical in others, and telling the two apart is the entire discipline of analyzing it.

The most tangible advantage is switching cost. Consider what it actually takes for a global bank, a government agency, or a media conglomerate to remove Akamai. Its web application firewall inspects the customer's live traffic; its Guardicore micro-segmentation is threaded through the customer's internal routing, defining which workload is allowed to talk to which. Ripping that out is not a procurement decision — it is open-heart surgery on a system that cannot go down. The operational friction, the risk of a botched migration, the recertification with regulators: all of it makes the incumbent enormously sticky once embedded. This is a genuine power, and it is why the Security segment churns so little.

The second advantage is subtler and, in the language of strategy, closer to a cornered resource. Over twenty-five years, Akamai negotiated physical co-location agreements to place its servers directly inside thousands of local ISP facilities across more than 130 countries. Competitors that lean on public peering exchanges connect to the internet's highways; Akamai has, in many places, parked inside the last-mile driveways where users actually live. That physical density is expensive and slow to replicate — you cannot conjure twenty-five years of relationship-building and rack space overnight — and it is the literal ground on which the AI inference thesis stands. If edge inference matters, this footprint is the asset. The honest caveat is that its value depends entirely on whether latency-sensitive edge compute becomes a large market; a cornered resource nobody needs is just an expensive habit.

The third lesson is strategic rather than structural, and it is the one other management teams should study: Akamai chose to cannibalize its own core business before competitors finished the job. Most incumbents cling to a declining cash cow until it is too late, defending yesterday's economics into irrelevance — the fate of the Yahoos and BlackBerrys of the world. Akamai instead read the terminal decline of CDN early and deliberately redirected the cash flows from that dying business into Security and Compute. Whether the destination proves right is still unsettled, but the willingness to fund your own disruption is rare, and it is why the company is still a protagonist rather than a footnote.

The fourth is a smaller, tactical lesson in build-versus-buy: rather than spend years and hundreds of millions building a developer cloud from zero against entrenched hyperscalers, Akamai bought Linode's product and community outright and scaled it through an enterprise sales machine the founders never had. Acquiring distribution-ready technology and pouring your existing customer relationships through it is a repeatable playbook — the same logic that turned Guardicore from a $30-odd-million startup into a $293 million product line.

The unifying thread is that Akamai's durable advantages are concentrated in Security and in the physical edge, not in the commodity delivery business that made its name. That is why the bull and bear cases both hinge on the same uncertainty: not whether the moat exists, but whether it is deep enough, and in the right place, to justify betting the balance sheet on AI. Time to war-game it.

IX. The Investor Spine: Bull vs. Bear Case and the Skeptic's Stress Test

Let us stage the argument as a debate between two sophisticated investors who have read the same filings and reached opposite conclusions.

The bull's case — why Akamai wins from here. The bull starts with the Anthropic deal not as a windfall but as proof of concept. A frontier AI lab, with its pick of suppliers, signed a seven-year commitment to run inference on Akamai's edge. That is a customer voting with $1.8 billion that hyperscalers alone cannot serve latency-sensitive, planet-scale inference, and that Akamai is the rare independent player with the physical footprint to do it.2 If edge inference becomes a meaningful slice of AI compute, Akamai owns distribution that took twenty-five years to assemble and cannot be cloned. Layer on the underappreciated-moat argument: Security and Compute are already more than 70% of revenue, growing at healthy rates, yet the stock carries a depressed, CDN-like multiple far below cybersecurity and cloud peers.[^13] The bull sees a re-rating waiting to happen the moment the market stops mistaking a security-and-compute company for a dying CDN. Finally, alignment: Tom Leighton, still running the company he co-founded in 1998, draws a nominal $1 base salary and remains Akamai's largest individual shareholder, with his personal fortune tied overwhelmingly to the stock rather than to cash compensation.12 A founder-CEO with hundreds of millions of dollars of skin in the game, who has personally survived every cycle since the dot-com crash, is precisely the person you want steering a bet-the-balance-sheet pivot.

In the language of Hamilton Helmer's 7 Powers, the bull is claiming three: switching costs in security, a cornered resource in the ISP-embedded edge, and counter-positioning against hyperscalers whose egress-fee business model makes it painful for them to match Akamai's low-egress pitch without cannibalizing their own margins. Run Porter's five forces and the same story appears: high switching costs weaken buyer power in security, the physical edge raises barriers to entry, and Akamai's neutrality is a defense against the threat of hyperscaler substitution.

The bear's case — what breaks the thesis. The bear does not dispute the history; the bear disputes the future's economics. Start with the capex treadmill. Serving AI inference means owning GPUs, and GPUs are depreciating assets on a relentless upgrade cycle dictated by NVIDIA, not by Akamai. Every two years a faster chip arrives, and yesterday's cluster is worth a fraction of its cost. A business model that requires perpetually re-buying the hardware just to stay competitive is one where free cash flow can be permanently consumed by the next generation of silicon — the opposite of the capital-light, cash-gushing profile that made Akamai investable in the first place. The bear notes that management guided capex to an eye-watering 40–42% of revenue for 2026, and asks the uncomfortable question: what if that never comes back down?[^10]

Next, the convertible overhang. Three billion dollars of debt, even at a zero coupon, is still $3 billion that must eventually be refinanced or converted. The hedges soften the dilution math but do not erase the leverage. If the stock languishes below the conversion prices, the notes stay debt, and a company that spent a generation as a fortress balance sheet finds itself managing a genuine liability into maturity.4 And underneath it all, the CDN drag never stops: a declining, low-margin delivery business that keeps pulling down consolidated growth and blended gross margin quarter after quarter, so that even successful security and compute growth shows up as merely mid-single-digit total revenue growth.3

The skeptic's stress test. Now push past the ordinary bear to the genuinely adversarial scenario, because it is the one that should keep an Akamai owner up at night. The entire AI thesis rests on a single large customer buying committed capacity during a demand frenzy. What happens if that frenzy cools — if AI model demand plateaus, or if Anthropic, having assembled compute from every supplier in a scramble, later rationalizes down to the cheapest? Worse, what if Anthropic or its peers move to custom silicon or build their own inference edge, the way Netflix once built its own CDN and walked away from Akamai a decade ago? That precedent is not hypothetical; it is Akamai's own history. In that scenario, Akamai is left holding massively underutilized, rapidly depreciating GPU clusters, $3 billion of debt raised to buy them, and compressed margins with no contracted demand to absorb the fixed cost. The very concentration that makes the deal exciting is what makes it fragile.

An activist stress test would add a governance and capital-allocation challenge on top: is it coherent to run an $800 million buyback funded partly by cash while simultaneously issuing $3 billion of debt for an unproven, capital-hungry business? Is the board underwriting the AI capex with the same rigor it would demand of an acquisition, or is it chasing a narrative that finally made the stock move after years of stagnation? These are fair questions, and management's answer — that the capacity is contracted and the returns are underwritten — is a claim to be verified over the coming years, not a fact already in evidence.

The honest synthesis is that both cases are live. Akamai is neither the obvious re-rating the bulls describe nor the obvious value trap the bears fear. It is a genuine bet, and like all genuine bets, it will be settled by a small number of observable outcomes.

X. Epilogue & KPIs to Watch

Step back and the shape of the thing is clear. Akamai is attempting one of the harder corporate metamorphoses in modern technology: from caching web pages in 1999 to defending the internet's traffic in the 2010s to hosting the computation behind artificial intelligence in the late 2020s. It is doing so by taking a twenty-five-year-old physical network built for one purpose and wagering that it is the right shape for an entirely different one. That is either an act of strategic foresight — using an old asset to win a new war — or an expensive rationalization for stepping onto a capital treadmill that never stops. The evidence to date supports neither triumph nor disaster; it supports watchfulness.

Rather than a verdict, the honest close is a short list of what to actually watch — the handful of numbers that will, over the next three years, reveal which story is true. Three stand out above the noise.

The first is Compute segment growth, and specifically whether it expands by more than 50% in 2026 as management has guided.2 This is the direct, quarter-by-quarter readout on the Anthropic ramp. If compute accelerates on schedule from the fourth quarter of 2026 into 2027, the AI thesis is converting from press release to revenue. If it stalls or slips, the whole capex justification wobbles.

The second is the capex-to-revenue ratio, and whether the 40–42% spike of 2026 moderates back toward historical norms — below roughly 25% by 2028 — or proves to be permanent.[^10] This is the single cleanest test of the bull-versus-bear divide. A temporary build-out that normalizes means Akamai front-loaded the investment for a durable revenue stream. A ratio that stays elevated means the GPU treadmill is real and free cash flow is structurally impaired. Watch this number more closely than any other.

The third is Security growth, and whether the segment — Guardicore, API security, and the web application firewall together — holds a consistent double-digit pace above 10%.3 This is the ballast. The entire compute gamble is being financed, directly and indirectly, by the cash the security business throws off. As long as that engine keeps humming, Akamai has the resources and the patience to see the AI bet through. If security growth falters, the company loses the financial cushion that makes the whole high-wire act survivable.

Danny Lewin's consistent hashing solved a problem of scale by refusing to build a bigger central server and instead distributing the work to the edges of the network. A quarter-century later, his co-founder is making the same wager against the same instinct — that the future of computing belongs not to the giant centralized cluster but to the intelligence pushed out to where the users are. Whether the AI era proves that thesis right, as the early internet did, is the question every Akamai investor is now, knowingly or not, holding a position on.

References

-

Akamai Lands $1.8 Billion Anthropic Deal As CDN Becomes AI Cloud — Forbes, 2026-05-08 ↩↩↩↩

-

Akamai Announces Landmark Cloud Infrastructure Agreement with Anthropic — Akamai Newsroom, 2026-05 ↩↩↩↩↩↩

-

Akamai Reports Fourth Quarter 2025 and Full-Year 2025 Financial Results — GlobeNewswire, 2026-02-19 ↩↩↩↩↩↩↩↩↩↩

-

Akamai Technologies Inc. Form 8-K, Convertible Senior Notes Offering — SEC EDGAR, 2026-05 ↩↩↩

-

How Danny Lewin's Legacy Lives on at Akamai and the Tech World — Bloomberg, 2021-09-10 ↩↩

-

Akamai Technologies Inc. Form 10-K405 for Fiscal Year 1999 — SEC EDGAR, 2000 ↩

-

Akamai Completes Acquisition of Guardicore to Extend Zero Trust Security Portfolio — Akamai Newsroom, 2021-10 ↩

-

Akamai Completes Acquisition of Noname Security for $450 Million — Akamai Newsroom, 2024-06 ↩

-

Akamai to Acquire Linode for $900 Million to Create the World's Most Distributed Cloud Platform — Akamai Newsroom, 2022-02 ↩

-

Akamai stock surges on $1.8B Anthropic cloud deal as CDN company pivots to AI infrastructure — The Next Web, 2026-05 ↩

-

Akamai Reports Third Quarter 2025 Financial Results — Akamai Newsroom, 2025-11 ↩

-

Akamai Technologies Inc. 2026 Proxy Statement — Akamai Investor Relations, 2026 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube