Assurant: The Silent Operating System Behind Your Devices and Home

I. Introduction & Episode Roadmap

Picture the worst fifteen seconds of your week. Your phone slips out of your hand in a parking lot, hits the pavement face-down, and the screen blooms into a spiderweb of cracks. You walk into a T-Mobile store the next morning expecting a fight. Instead, a rep taps a few fields, and by tomorrow a replacement device is in your hand, your data restored, your old handset boxed up for return. You thank T-Mobile. You never learn the name of the company that actually underwrote the risk, ran the claim, inspected the broken device, wiped its memory, and decided whether to repair or refurbish it.

That company is Assurant. It trades on the New York Stock Exchange under the ticker AIZ, carries a market value north of $12 billion, and is one of the most quietly consequential financial institutions in American consumer life. It sits behind the phone in your pocket, the extended warranty on your washing machine, the service contract on your car, and — in a stranger and more controversial way — the hazard insurance that gets slapped onto a house when a homeowner lets their own policy lapse. Assurant is a business you interact with constantly and almost never see, because its entire strategy is to be invisible. Its customers are not really you; its customers are the brands you already trust.

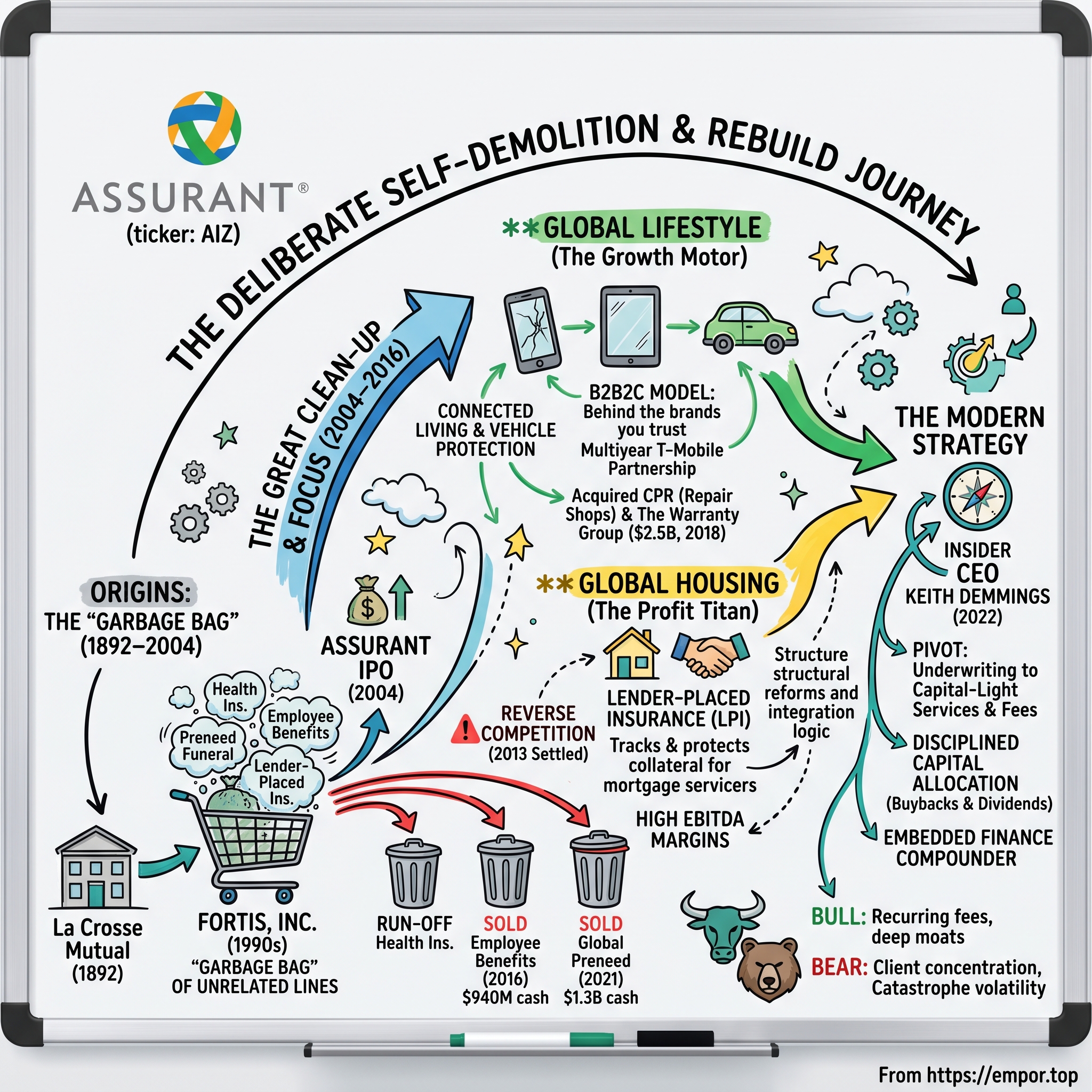

This is a story about deliberate self-demolition. The Assurant of 2026 is a focused, capital-light, tech-and-services machine. But it was born as the opposite: a sprawling, capital-heavy grab-bag of specialty insurance lines that a European conglomerate quite literally wanted off its books. The arc of the last two decades is the story of management systematically dismantling the company it inherited — running off individual health insurance, selling employee benefits, selling funeral insurance — to rebuild around two engines that most people have never heard described together.

The first engine is Global Lifestyle, the high-volume growth motor. In 2025 it generated roughly $9.58 billion in net earned premiums, fees and other income, protecting connected devices and vehicles across the globe.1 The second is Global Housing, smaller on the top line at roughly $2.77 billion but startlingly profitable, throwing off $858.7 million of adjusted EBITDA in 2025 — a margin profile that dwarfs the far larger Lifestyle segment.1 One engine grows; the other prints cash. Understanding how those two very different economic animals live inside the same corporate skin is the whole game.

Over the next several sections we will trace how a Wisconsin mutual aid society founded in 1892 became a Belgian-Dutch conglomerate's American afterthought, then a public company, then a focused compounder. We will benchmark its largest and most transformative acquisition. We will dissect the mechanics of "reverse competition," a phrase most investors have never heard but that once cost Assurant hundreds of millions of dollars. And we will stress-test the bull case from the perspective of a skeptic who thinks the market is right to value this company like an insurer rather than a tech platform. The goal throughout is not to cheerlead. It is to figure out what Assurant actually is, where its moat is real and where it is rhetoric, and what would have to break for the story to fall apart.

Let's start where the story starts: not in Silicon Valley or on Wall Street, but on the frozen banks of the Mississippi River in the 1890s.

II. The Origins: From Wisconsin Mutual to the Fortis "Garbage Bag" (1892–2004)

La Crosse, Wisconsin, in 1892 was a lumber-and-brewing town where a workplace injury could destroy a family. There was no workers' compensation, no disability system, no safety net beyond church and kin. Into that gap stepped the La Crosse Mutual Aid Association, a small outfit selling disability policies to Midwestern laborers — a promise that if a millworker lost a hand or a railwayman broke his back, some money would keep arriving. It was insurance in its most elemental and moral form: pooling risk among people who could not individually absorb catastrophe. That founding DNA — protecting ordinary people against the small disasters of daily life — is worth holding onto, because in a strange way it is the same business Assurant runs today, just applied to phones and dishwashers instead of severed limbs.

The company that grew out of that association eventually became Time Insurance Company, a respectable Wisconsin health and disability underwriter. For most of the twentieth century it was a domestic story. The plot twist came from Europe. In 1978, the Dutch insurer NV AMEV acquired Time Insurance as its beachhead into the enormous American market — a foreign carrier planting a flag in the U.S. specialty insurance business. Cross-border insurance expansion was fashionable, and the American middle market looked like fertile ground.

Then came the merger that gave the whole enterprise its eventual character. In 1990, NV AMEV combined with Belgian counterparts to form Fortis, the Belgian-Dutch financial powerhouse that would spend the next two decades assembling one of Europe's largest banking-and-insurance conglomerates. The American operations were consolidated under Fortis, Inc., and here is where the story turns instructive. Fortis was a European bancassurance giant. Its American arm became a catch-all — an uncoordinated portfolio into which nearly every specialty line got tossed. Under one roof sat individual health insurance, long-term care, pre-funded funeral plans, group dental and vision, employee benefits, and lender-placed mortgage insurance. Inside Fortis, insiders reportedly referred to the American unit with a nickname that captured its lack of strategic logic: the "garbage bag." It was not an insult about quality so much as about coherence. These were businesses with almost nothing in common — different customers, different regulators, different risk durations, different capital demands — bolted together because they happened to be American and happened to be for sale at some point.

That incoherence mattered enormously, because a conglomerate of unrelated insurance lines is very hard to value and very hard to run. Individual health underwriting is a brutal, cyclical business where a bad year can swallow years of profit. Pre-funded funeral insurance — money paid today against a death benefit decades away — is a long-duration asset-liability puzzle that ties up capital for a generation. Lender-placed insurance is a high-margin, politically sensitive niche. Managing all of them from one balance sheet meant the good businesses subsidized the volatile ones and no single strategy could be told to investors.

By the early 2000s, Fortis had made its decision. The parent wanted to refocus its capital on core European banking and insurance, and the American garbage bag was going to be cut loose. The mechanism was an initial public offering. On February 5, 2004, the unit was rebranded Assurant, Inc., redomesticated as a Delaware corporation, and floated on the NYSE. Fortis sold roughly 65% of the company at $22 per share, raising about $1.76 billion in what was one of the year's largest and most complex financial-services IPOs.5 Complex is the operative word: underwriters had to price a company that was really six companies, each with its own risk profile, wrapped in the uncertainty of a parent that clearly wanted out.

Assurant walked onto the public stage as a paradox — a company with deep century-old roots and a genuinely confused identity. It had scale, licenses in all fifty states, and real underwriting expertise. It also had no clear reason to exist as a single entity. The next twelve years would be spent answering the question the IPO had left open: if you strip away everything that doesn't fit, what is this company actually good at?

III. The Spin-Off and the Great Clean-Up (2004–2016)

Freedom from Fortis did not solve Assurant's core problem; it exposed it. As a newly public company, Assurant now had to justify itself quarter by quarter to investors who could see, with uncomfortable clarity, that its earnings lurched around in ways that had nothing to do with management skill. The culprit was the very diversification that had once seemed like a virtue. When individual health insurance turned, it turned hard — pricing cycles in small-group and individual medical underwriting are savage, and a subscale player is a passenger on that rollercoaster, not the driver.

The event that structurally broke the old model arrived in 2010: the Affordable Care Act. For a large integrated health insurer, the ACA was a challenge to be managed. For a small, independent individual-health underwriter like Assurant Health, it was closer to an extinction event. The law's guaranteed-issue rules, minimum loss ratios, and exchange-based distribution rewrote the economics of the exact niche Assurant occupied, stripping away the underwriting levers that had made the business viable and replacing them with a competitive dynamic that favored scale players Assurant could never match. The writing was on the wall, and it took a new kind of CEO to read it and act.

That CEO was Alan Colberg, who took the top job in 2015 after years inside the company and immediately made simplification the organizing principle of his tenure. Colberg's insight was less about any single business than about the portfolio itself: Assurant would never be re-rated by the market as long as it was a bundle of unrelated bets, some of them capital-hungry and cyclical. The path to a higher-quality company — and a higher-quality stock — ran through subtraction. The strategy was to run off or sell the non-core, capital-heavy divisions, absorb the short-term restructuring pain, and free up billions of dollars of statutory capital that could be redeployed into businesses that actually earned high returns.

The divestiture campaign unfolded methodically. First came the exit from commercial health insurance in 2015 and 2016 — a clean amputation of the most volatile limb, taken with restructuring charges that hurt in the near term but eliminated a source of earnings chaos that had haunted the company since the IPO. Then, in March 2016, Assurant sold its employee benefits business — group dental, vision, and life — to Sun Life Financial for roughly $940 million in cash.7 That was a good business, but it was not Assurant's business; it competed against far larger benefits carriers with no obvious edge. Selling it to an owner who could scale it was the rational move, and the cash was worth more inside Assurant's transformation than the slow-grinding earnings were.

The capstone came in 2021, after Colberg had reshaped nearly the whole portfolio. Assurant agreed to sell Global Preneed — its pre-funded funeral insurance division — to CUNA Mutual Group for approximately $1.3 billion, with the deal closing that August.6 Preneed was the ultimate legacy line: long-duration liabilities, decades of asset-liability matching, capital locked up against death benefits that might not be paid for thirty years. Exiting it completed Assurant's escape from the world of long-tail, spread-based insurance and confirmed the new identity.

Where did all that freed-up capital go? Into two deeply embedded, high-returning niches that would become the company's entire future: Connected Living, the mobile-device protection engine, and Specialty Property, home to lender-placed and renters insurance. The genius — and the risk — of this pivot was concentration. Assurant deliberately traded a diversified grab-bag for a focused pair of bets, wagering that being essential in two workflows beat being mediocre in six. Whether that wager paid off depends entirely on how good those two businesses actually are. So let's open them up, starting with the one that touches the most people.

IV. The Connected Lifestyle Engine: Mobile Device and Trade-In Economics

For most of the mobile era, phone insurance was a joke — a $5 add-on hustled at the register on a cheap flip phone that cost less to replace than to insure. Then the economics of the device in your pocket changed completely. The moment a smartphone became a $1,000-plus pocket computer holding your photos, your banking, your identity, and your entire digital life, "phone insurance" stopped being a fringe upsell and became something closer to a necessity. Losing a $1,200 device you paid for over 24 monthly installments is a real financial event, and suddenly a whole category of sophisticated consumer protection had a reason to exist. Assurant had spent years quietly building exactly the machinery to serve it.

Here is the crucial structural insight, and it is the key to understanding the entire company: the mobile carrier owns the customer, but the carrier does not want to own the risk or the operations. T-Mobile, Spectrum, Comcast — these companies are brilliant at acquiring and billing subscribers. They have no desire whatsoever to hold underwriting reserves, build reverse-logistics warehouses, staff claims centers, or run device-repair supply chains. Those are grubby, capital-and-labor-intensive functions that would drag down a telecom's returns. So they outsource the entire apparatus to Assurant, which embeds its systems — its APIs, its claims logic, its customer service — directly inside the carrier's own storefront and app. This is the B2B2C model in its purest form: business-to-business-to-consumer. Assurant sells to the carrier; the carrier sells to you; and to you, it all just looks like your carrier taking care of you.

Nowhere is this more visible than in the T-Mobile relationship, a partnership stretching back well over a decade and repeatedly renewed. In September 2022, Assurant announced a multiyear extension of the arrangement, cementing its role as the engine behind T-Mobile's flagship protection, trade-in, and repair program.8 When a T-Mobile customer signs up for device protection, files a claim, trades in an old handset, or gets a screen repaired, Assurant is the invisible operator processing the transaction. The lock-in is structural and it compounds at the point of sale: when you upgrade your phone in a T-Mobile store, the same integrated flow that sells you the new device also inspects your trade-in, grades its condition, and re-attaches your protection plan — all in one seamless motion that would be enormously disruptive to rip out and replace.

But the deepest misunderstanding about this business is thinking of it as insurance at all. Assurant is, in operational reality, a supply-chain and reverse-logistics company wearing an insurance license. When your phone breaks and you get a replacement, someone has to receive your damaged device, diagnose it, wipe its data to protect your privacy, repair or refurbish it, and re-market it into the secondary market where used smartphones fetch real money. Assurant runs state-of-the-art facilities doing exactly this at industrial scale, processing millions of used devices a year. The refurbished-device resale is not a byproduct; it is a genuine profit center that offsets claim costs. Every broken phone that can be economically repaired and resold instead of replaced with a brand-new unit is money saved.

That logic is precisely why Assurant went out and bought a chain of repair shops. In October 2019 it acquired CPR — Cell Phone Repair — one of the largest global franchisors of device-repair storefronts, with more than 700 locations at the time.[^9] The strategic point was cost. If a cracked screen can be fixed at a local CPR counter for a modest component-and-labor cost, that is dramatically cheaper than shipping the customer a replacement device and eating the full handset value. Owning the physical repair footprint let Assurant substitute cheap local repairs for expensive full replacements, directly compressing the loss cost inside every protection plan. By 2022, T-Mobile's in-person repair program was being routed through Assurant's network of nearly 500 CPR-branded locations.8

What does all this tell an investor? That Connected Living's economics are less about clever underwriting and more about operational scale — the ability to process, repair, and re-market devices at a unit cost sub-scale competitors cannot touch. That is a real advantage, but it is also a low-drama, grinding one: margins here are thinner than in Housing, and growth depends on device values staying high, upgrade cycles staying active, and the handful of giant carrier relationships staying intact. It is a volume business with a scale moat and a concentration problem. And in 2018, Assurant made a $2.5 billion bet to widen that moat into an entirely new vertical.

V. The Transforming Deal: Benchmarking the $2.5 Billion Warranty Group Acquisition (2018)

By 2017, Assurant had a problem that most companies would envy: it had freed up piles of capital by shedding its legacy lines, and it needed to redeploy that capital into something that fit the new identity. The device business was growing but concentrated. What Assurant lacked was a second leg of embedded, fee-based protection with long-duration, predictable cash flows — something to counterbalance the choppiness of the mobile cycle. The answer was sitting inside a private-equity portfolio.

On October 18, 2017, Assurant announced it would acquire The Warranty Group from TPG Capital for an enterprise value of roughly $2.5 billion, with the deal closing on May 31, 2018.23 The Warranty Group was a global specialist in vehicle service contracts and extended warranties, distributing through auto dealerships and the finance-and-insurance ("F&I") desks where car buyers sign paperwork. With annualized revenue north of $2 billion at the time of closing, it instantly made Assurant a premier global player in vehicle protection.2

The deal structure is worth slowing down on, because it reveals how Assurant thought about the risk. The transaction was financed with roughly $1.5 billion in cash — a figure that already accounted for retiring about $596 million of The Warranty Group's existing debt — plus roughly 10.4 million Assurant shares worth about $993 million.3 Critically, TPG did not simply cash out and walk away. The private-equity seller retained a stake of roughly 23% in the combined public company, worth about $1.5 billion at the time.3 That is an unusual and telling structure. A seller who keeps a quarter of the combined entity is signaling confidence in the integration — and is also, conveniently for Assurant, sharing in the downside if the deal disappointed. It softened the cash outlay and aligned the seller with a smooth handoff.

Strategically, the rationale was twofold. First, vehicle protection. Auto service contracts are a genuinely attractive category: they are sold at the point of financing, they run for multiple years, and they generate predictable fee income that does not swing with quarterly phone-upgrade patterns. Overnight, Assurant became a scaled provider protecting a large and growing base of vehicles worldwide. Second, geography. The Warranty Group brought established operational networks across Europe, Latin America, and Asia-Pacific — infrastructure that would have taken Assurant years and enormous expense to build organically.

Now the skeptic's question: did Assurant overpay? The multiple was a premium to some sector comps, and $2.5 billion is a large check for a company Assurant's size. Management's defense rested on synergies — a target of roughly $60 million in annual pre-tax operating synergies by the end of 2019, achieved by consolidating overlapping global operations.2 Synergy promises are cheap to make and easy to miss, so the honest way to judge the deal is by what it produced rather than what was pledged. On that score, the integration looks defensible: the acquisition folded in exactly the stable, long-duration, multi-year fee income Assurant wanted, and the vehicle-protection franchise it created — today protecting more than 40 million vehicles — has become a genuine counterweight to the shorter mobile cycle. The upfront capital intensity was real, and a critic can fairly argue Assurant paid full price. But the strategic logic — buying predictable cash flow to stabilize a concentrated, cyclical growth engine — was sound, and the business has delivered the diversification it promised. Vehicle protection now sits alongside Connected Living inside Global Lifestyle, and together they explain how that segment grew to $9.58 billion in earned premiums and fees by 2025.1

That is the growth engine. But growth is not where Assurant makes its most spectacular margins. For that, we have to leave the world of phones and cars and walk into the strangest, most profitable, and most legally fraught corner of the entire company.

VI. The Profit Titan: Global Housing and Lender-Placed Insurance (LPI) Economics

Imagine you own a home with a mortgage, and — through hardship, forgetfulness, or a lapsed payment — your homeowners insurance quietly expires. You may not even notice. But your mortgage servicer notices, because the house is the collateral behind a loan the servicer is responsible for, and an uninsured house that burns down is a catastrophic loss to the lender. So the servicer does something you did not ask for and cannot refuse: it buys an insurance policy on your home to protect the collateral, and it bills you for it. This is lender-placed insurance, sometimes called "force-placed" insurance, and it is the profit titan hiding inside Assurant.

The mechanics reveal why the business is so extraordinary. The homeowner does not choose the insurer, does not shop the price, and often does not want the policy at all. The buyer who matters is the mortgage servicer, and the servicer's priority is not cheapness but reliability — flawless tracking, instant placement, and airtight compliance across millions of loans. This is where Assurant's real moat lives. Its proprietary tracking software integrates directly into the core loan-servicing platforms that the big servicers run, monitoring millions of mortgages in real time and automatically flagging the moment a borrower's voluntary coverage lapses. The instant a policy expires, the system can place coverage. That integration — sitting inside the servicer's own operational plumbing — is not a product a competitor can dislodge with a lower quote. Ripping out Assurant's tracking engine and threading in a rival's would mean re-plumbing a mission-critical, regulator-scrutinized workflow across an entire loan book. Servicers simply do not do that lightly.

The financial result is a margin profile that looks almost unfair next to the rest of the company. In 2025, Global Housing produced $858.7 million of adjusted EBITDA on just $2.77 billion of net earned premiums and fees.1 Put those two numbers side by side and the story jumps out: Housing earned nearly as much bottom-line profit as the far larger Lifestyle segment, on less than a third of the revenue. Housing's 2025 EBITDA actually grew 28% year over year, helped by a lighter catastrophe load.1 This is the cash-printing heart of Assurant — the engine whose profits fund the dividends and buybacks. And its profitability is precisely why it has attracted the intense scrutiny of regulators.

The "reverse competition" reckoning

Here is the controversy that once threatened the whole franchise. In a normal insurance market, carriers compete for your business by offering you a lower price. In lender-placed insurance, the person paying the premium — the homeowner — has no say, so the carriers competed instead for the servicer's business. And the way they competed was perverse: rather than lowering prices for the captive consumer, insurers paid the servicers rich commissions and other considerations to win their books. This is "reverse competition" — competition that pushes prices up for the end consumer instead of down, because the party choosing the product is not the party paying for it. The homeowner, force-placed at often expensive rates, footed a bill inflated by kickbacks flowing to the very servicer that placed the coverage.

The reckoning came in 2013. The New York Department of Financial Services, under the Cuomo administration, led a landmark investigation into the practice. On March 21, 2013, Assurant's insurance subsidiaries reached a settlement with the NYDFS: a $14 million penalty, restitution for harmed homeowners force-placed after January 1, 2008, and — most consequentially — a set of structural reforms including prohibitions on paying commissions to mortgage servicers for force-placed business and bans on placing coverage on properties serviced by affiliated banks.4 New York was the largest force-placed insurer's lead domino; the reforms rippled nationwide, and government-sponsored enterprises later barred servicer commissions on the loans they backed. On top of the regulatory action came class-action litigation that cost Assurant substantial sums over the following years.

Here is the counterintuitive part, and it is central to the investment case. The commission bans should, in theory, have gutted the business — remove the kickbacks and the whole model collapses, right? It did not. The business remained enormously profitable, and the reason is the moat described above: the durable advantage was never the commissions. It was the integration, the tracking systems, and the switching costs. Take away the ability to bribe servicers, and Assurant still wins because it is embedded in the servicer's operations and does the job reliably at scale. The proof shows up in renewals. In the first quarter of 2026, Assurant completed two long-term renewals with large lender-placed partners representing over 5 million loans combined — hard evidence that even in a post-commission world, the switching costs are real and clients stay.9

The volatility wildcard

There is a catch, and it is the reason the market treats Housing warily: catastrophe. A book of homeowners-type risk concentrated in places with hurricanes, wildfires, and freeze events means a single bad season can shred the loss ratio. Assurant manages this with a large, multi-layered catastrophe reinsurance program that caps its net exposure — for 2026, management set its catastrophe assumption at roughly $185 million and budgeted around $180 million of reinsurance premium to protect the balance sheet.9 Reinsurance turns an unbounded tail risk into a manageable, budgeted cost, but it is a cost, and in a heavy year the retained losses still bite. That tension — spectacular margins in calm years, exposure to the sky in violent ones — is the defining feature of the profit titan, and it is why the person steering the whole company matters so much.

VII. The Underwriting to B2B2C Pivot: Keith Demmings and Modern Strategy

In 1997, a young Canadian named Keith Demmings took a job as a sales intern at Assurant's operation in Toronto. It is the kind of entry-level role thousands of people pass through and forget. Demmings did not pass through. He rose to run the Canadian business by 2005, took over the fast-growing Global Lifestyle segment in 2016, and in January 2022 became chief executive officer of the entire company — a quarter-century climb from intern to CEO, entirely inside one organization.8 There is an argument for and against this kind of ultimate-insider ascension. The case for: nobody understands the plumbing of Assurant's device and warranty businesses better than the person who built much of it. The case against: insiders rarely torch the strategy they inherited, so investors should not expect radical reinvention from a Demmings CEO — they should expect intensification.

That is exactly what they got. Demmings inherited Colberg's transformed portfolio and doubled down on its central bet: keep pushing from traditional, capital-heavy underwriting risk toward capital-light, high-margin service fees. The philosophical shift is subtle but important. An old-line insurer makes money by holding risk and being right about it. A B2B2C service platform makes money by running the workflow — the claims, the logistics, the tracking, the repairs — and collecting fees, while offloading as much pure insurance risk as it prudently can. The more Assurant looks like the latter, the more its earnings should be stable, recurring, and worthy of a higher valuation multiple. That is the thesis Demmings is executing, and it is fair to ask whether the market believes it (we will return to that skepticism shortly).

On capital allocation, the record is the best available window into whether management's discipline is real or rhetorical. Assurant has behaved like a company that means what it says about shareholder returns. In 2025 it returned $468 million to shareholders — $300 million of share repurchases retiring 1.4 million shares, and $168 million in dividends — and in November 2025 it raised its dividend by 10%, marking the twenty-first consecutive year of dividend increases since the 2004 IPO.1 Twenty-one straight years of dividend hikes is not a slogan; it is a two-decade behavioral track record spanning a financial crisis, a pandemic, and multiple catastrophe years. The buybacks matter too: consistently retiring shares shrinks the count and lifts per-share metrics, and it signals management's belief that the cash-generative Housing engine can be trusted to keep funding returns.

The incentive design reinforces the story. Assurant structures its CEO's long-term equity heavily toward performance — the bulk in performance share units rather than time-vesting stock — and ties those units to metrics that align management with genuine compounding: multi-year adjusted EBITDA growth (measured excluding catastrophes, so managers are judged on the business they control rather than the weather) and relative total shareholder return against peers. Excluding catastrophes from the growth metric is a sensible and honest design choice; it would be perverse to reward or punish executives for hurricane frequency. But it also quietly concedes the point a bear would press: catastrophe is a real, recurring feature of the earnings, and defining it away for compensation purposes does not define it away for shareholders.

How credible is Demmings when he sets targets? The live evidence comes from the earnings calls, and the tone there is measured rather than triumphant. On the Q1 2026 call, management framed the year around Global Lifestyle "leading the growth," guiding that segment to roughly 10% growth, while noting Connected Living EBITDA rose 18% on expansion with existing clients.9 When catastrophes ran heavy, management guided full-year EBITDA and EPS to grow only "low single digits" excluding cats — a candid, unglamorous number rather than a stretch promise.9 That willingness to guide down when the facts warrant, and to separate the controllable business from the weather, is the kind of behavior that builds credibility over time. It is not flashy. For a company whose entire identity is being the invisible operator, unflashy competence is arguably the point. The harder question is whether that competence adds up to a durable moat — and that requires putting Assurant on the war-game table.

VIII. The Competitive Moat: Hamilton Helmer's 7 Powers & Porter's 5 Forces Analysis

Strip away the narrative and ask the cold question a strategist asks: what actually stops a competitor from taking Assurant's business? The answer differs sharply between the two engines, and running the company through two classic frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — exposes both where the moat is genuinely deep and where it is shallower than management's confidence implies.

Hamilton Helmer's 7 Powers

Switching costs are the primary power, and they are real. Once T-Mobile has woven Assurant's claims and logistics into its retail and billing flow, or once a mortgage servicer has embedded Assurant's tracking software into its loan-servicing core, replacement is not a procurement decision — it is a high-risk operational surgery. The 5-million-loan renewals of early 2026 and the repeatedly extended T-Mobile relationship are the observable proof that clients, once integrated, tend to stay.98 This is the strongest and most defensible element of the entire thesis.

Scale economies are real but partial. In Connected Living, Assurant's reverse-logistics infrastructure, automated device diagnostics, and global re-marketing channels let it process and refurbish devices at a unit cost a small entrant could not match. That is a genuine cost moat. But it is a moat shared with an equally scaled rival, which limits its pricing power — a scale advantage you hold jointly with your one large competitor is a barrier to new entrants, not a source of premium margins against the incumbent you already face.

Cornered resource shows up as exclusive, multi-year distribution. Being the embedded protection provider for major wireless brands is a form of cornered access to the point of sale. But it is a contracted resource, not an owned one — the carrier can, in principle, let the contract lapse or split the book. That contingency is the hinge of the entire bear case.

The other powers — network economies, counter-positioning, branded differentiation, and process power — are largely absent or weak. Assurant has no consumer brand power precisely because its strategy is to be invisible; consumers bond with T-Mobile, not with the underwriter behind the counter. That invisibility is a feature for winning B2B contracts and a vulnerability for capturing consumer loyalty.

Porter's Five Forces

Bargaining power of buyers is the sharpest asymmetry in the whole business. In Lifestyle, the buyers are colossal — a T-Mobile can squeeze margins at renewal, demand better economics, or dangle its book in front of a competitor. Buyer power there is very high, and it is the single biggest structural weakness. In Housing's lender-placed line, the picture inverts entirely: the individual homeowner has zero bargaining power because they do not choose the insurer, and the servicer who does choose is locked in by integration. Same company, opposite ends of the buyer-power spectrum — which is exactly why the two segments carry such different margins.

Threat of new entrants is extremely low in both engines. To compete in either lender-placed or carrier-device protection, a would-be entrant needs statutory insurance licenses across all fifty states, deep capital reserves, complex multi-state compliance machinery, and — hardest of all — years of software integration into partners who have no incentive to take the risk of switching. That thicket of requirements is why these are consolidated, not fragmented, markets.

Competitive rivalry is oligopolistic, which cuts both ways. In mobile protection, the market is effectively a duopoly between Assurant and Asurion — a privately held giant that is every bit as capable and, being private, unbothered by quarterly optics. A duopoly means rational pricing most of the time, but it also means a single lost mega-account is a body blow with nowhere to hide. In lender-placed insurance, the field has historically been a tight oligopoly shared with players such as QBE and State National (now part of Markel). Consolidated markets are comfortable until they are not; the discipline holds right up until a rival decides to buy share on price or a giant client decides to run a competitive process.

The war-game conclusion is nuanced. Assurant's moat is deep where it is built on integration and switching costs, and thin where it depends on the goodwill of a few enormous buyers. That is not a contradiction the company can resolve with better execution — it is the permanent shape of a B2B2C business that sits between powerful partners and captive consumers. Which brings us to the part of the story where we stop admiring the moat and start attacking it.

IX. Investor Stress Test, Risk Radar, and Bull vs. Bear Case

Every good business story eventually has to face its own prosecution. Assurant's is not a fragile company — twenty-one years of dividend growth and a genuinely embedded position in two industries attest to that — but a serious investor's job is to find the fault lines, not admire the façade. Here is where a skeptical long-short investor or activist would press.

The risk radar

Client concentration is the first and loudest alarm. A substantial share of Global Lifestyle's economics runs through a small number of enormous carrier relationships, with T-Mobile the most important single node. If that relationship were renegotiated on materially worse terms, or if the book were split with Asurion, the damage to the core growth engine would be severe and immediate. Notably, on the Q1 2026 call, no analyst pressed management directly on T-Mobile concentration — which tells you the risk is well understood and priced, not that it is absent.9 Concentration is not a hidden risk here; it is a known, standing one.

Catastrophe and climate exposure is the second. Global Housing's spectacular margins come attached to a tail: hurricanes on the Gulf and Florida coasts, wildfires in California, and freeze events can inflate loss ratios and drive up the cost of the reinsurance that caps the damage. As the frequency and severity of severe weather trend upward, so does the structural cost of protecting the collateral book. Reinsurance transfers the peak risk but not the rising baseline expense, and a genuinely bad year can compress the very earnings that fund the capital-return story.

Upgrade cycles and consumer behavior are the quiet third. Assurant's device economics assume phones keep breaking, keep being expensive, and keep being upgraded. If hardware innovation stalls and consumers hold devices for four or five years instead of two, trade-in and upgrade volumes fall, and the high-margin fee-for-service logistics revenue softens with them. This is a slow risk, not a cliff — but it runs directly against the grain of a maturing smartphone market.

The skeptic's core challenge

Here is the sharpest version of the bear thesis, and it is worth stating plainly: the market values Assurant like a legacy insurer — a low-teens price-to-earnings multiple — rather than like the high-moat tech-services platform management describes. Why the discount? Because the market is not fully convinced. It sees the catastrophe volatility in Housing and the customer concentration in Lifestyle, and it concludes that these earnings are lumpier and less certain than a true asset-light software business. The uncomfortable implication: if a catastrophe-heavy year hollows out Housing's profits, the buyback-and-dividend engine that props up the equity story stutters. A skeptic would argue the valuation is not a mistake to be corrected but a rational discount for real, structural risk. The burden of proof sits on management to show, through a full cycle, that the business is more resilient than the multiple implies.

Bull versus bear

The bull case is that Assurant is a genuine embedded-finance compounder whose partners bear the cost of customer acquisition, freeing it from the marketing spend that grinds down consumer-facing insurers. The cash-rich Housing engine funds relentless buybacks; the Lifestyle engine rides the secular rise in device values and the migration of the auto fleet toward complex, electronics-laden vehicles — including electric vehicles — that command higher-priced, higher-content service contracts. On this view, invisibility is the whole advantage: no acquisition costs, deep switching costs, recurring fees, and a two-decade record of disciplined capital return.

The bear case is that the stock is already priced fairly for exactly what it is. The business carries a high-beta dependence on a handful of carrier renewals; lose a marquee account to Asurion and growth stalls. Reopen the regulatory book on lender-placed pricing and reverse competition, and Housing's margins face fresh scrutiny. Add a severe catastrophe year, and the earnings that justify the capital return evaporate on cue. Nothing here is broken — but nothing here is cheap for the risk, either.

The most intellectually honest read is that both cases are partly right, and the tension between them is the investment. That resolves into a short, concrete watch-list — and a set of durable lessons the whole saga teaches.

X. Playbook, Durable Business Lessons, & Epilogue

Step back from the quarter-to-quarter and the Assurant story resolves into a few durable lessons that travel well beyond this one company.

Lesson one: the "garbage bag" to "focused compounder" playbook. Assurant's central act of value creation was subtraction. By running off individual health insurance, selling employee benefits to Sun Life, and offloading Global Preneed to CUNA Mutual, it converted a capital-heavy, cyclical grab-bag into a focused pair of high-moat franchises — and in doing so freed billions in statutory capital and structurally lifted its return on equity.76 The lesson for any conglomerate trading at a discount is uncomfortable but clear: the fastest path to a re-rating is often the courage to sell good businesses that don't fit, not to buy more.

Lesson two: the power of embedded distribution. Assurant's deepest edge is that it never has to find a customer. It sells at the precise moment a consumer buys a phone, finances a car, or originates a mortgage, riding inside a partner's transaction. That eliminates direct-to-consumer marketing cost and builds recurring revenue that is sticky because it is wired into someone else's workflow. Embedded finance is fashionable language in 2026, but Assurant has been quietly living it for two decades.

Lesson three: the danger of the servicer-payer split. The most profitable corner of the company — lender-placed insurance — is also its most perpetually vulnerable, precisely because the party choosing the product is not the party paying for it. That split is a money machine and a regulatory magnet at the same time. The 2013 New York settlement is the permanent reminder that business models built on a captive payer must treat transparency and compliance not as costs but as the price of durability. The margins survive only as long as the practices can withstand daylight.

If you track only a few things about Assurant from here, track these. First, Global Lifestyle organic growth and device-subscriber trends — the health of the growth engine, and the early-warning system for any softening in carrier relationships or upgrade cycles. Second, Global Housing adjusted EBITDA and its catastrophe load — the true measure of whether the profit titan is compounding or merely surviving the weather in a given year. Third, capital returned per share through buybacks and dividends — the proof, quarter after quarter, that the cash actually reaches shareholders rather than getting absorbed by losses or overpriced acquisitions. Those three tell you almost everything about whether the thesis is intact.

The epilogue belongs to the intern. Keith Demmings walked into a Toronto sales office in 1997 selling protection products, and in 2026 he runs a company worth more than $12 billion that quietly underwrites, tracks, repairs, and refurbishes the physical infrastructure of modern life — the phone in your hand, the car in your driveway, the roof over your head when your own policy lapses. Assurant's genius, and its curse, is that almost no one knows it is there. It is the silent operating system running behind the brands you actually trust. Whether that invisibility remains a fortress or becomes a ceiling — whether a company no consumer roots for can keep compounding when its giant partners hold the leverage — is the question the next decade will answer. For now, the machine keeps running, one broken screen and one lapsed policy at a time.

References

-

Assurant Reports Strong Fourth Quarter and Full Year 2025 Financial Results — Business Wire, 2026-02-10 ↩↩↩↩↩↩

-

Assurant Closes Acquisition of The Warranty Group — Business Wire, 2018-05-31 ↩↩↩

-

Assurant to Acquire The Warranty Group for $2.5B, With Eye on Quicker Global Growth — Carrier Management, 2017-10-18 ↩↩↩

-

Cuomo Administration Settles with Country's Largest Force-Placed Insurer — New York Department of Financial Services, 2013-03-21 ↩

-

Assurant, Inc. Form 10-K (FY2004) — U.S. Securities and Exchange Commission ↩

-

Assurant to Sell Global Preneed to CUNA Mutual Group for $1.3 Billion — Assurant, 2021-03-01 ↩↩

-

Assurant Completes $940 Million Sale of Employee Benefits Business to Sun Life — Assurant Form 8-K, U.S. Securities and Exchange Commission, 2016-03-01 ↩↩

-

Assurant Extends Longstanding T-Mobile Partnership with New Multiyear Agreement — Business Wire, 2022-09-26 ↩↩↩↩

-

Assurant (AIZ) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-05-06 ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube