AirJoule Technologies: The Molecular Sponge and the Holy Grail of Clean Tech

I. Introduction: The Thermodynamic Paradox

Picture a server hall in the Arizona desert in the dead heat of August. Inside, tens of thousands of graphics processors are training a large language model, and every one of them is throwing off heat like a tiny furnace. To keep them from cooking themselves, the operators are spraying water—millions of gallons a year—into evaporative cooling towers, watching it hiss into vapor under a sky that hasn't seen rain in months. A few miles away, the same desert air, the air everyone assumes is bone dry, is quietly carrying more water than the entire Colorado River. It's just floating there, invisible, as humidity.

Now imagine a machine that sits next to that data center, breathes in that "dry" desert air, uses the waste heat pouring off those very servers, and exhales pure distilled water—enough to refill the cooling towers it's standing next to. No new river. No new aquifer. Just the air and the heat that were already there.

That machine is the entire bet behind AirJoule Technologies Corporation, which trades on the NASDAQ under the ticker AIRJ.1 And the thesis of this episode is deceptively simple: what if you could attack the global water crisis and the global cooling-energy crisis with the same box—a box whose secret ingredient is a crystalline powder so porous that a single gram of it, unfolded, would carpet a soccer field?

Here's what makes AirJoule a genuinely fascinating Acquired-style story rather than just another clean-tech science-fair project. The technology is real and it's grounded in a Nobel-adjacent breakthrough in material science. But the company—the corporate architecture wrapped around that technology—is arguably the more interesting invention. As of mid-2026, AirJoule is, for all practical purposes, pre-revenue. Its first commercial sale was a single roughly $100,000 unit. And yet it carries a market capitalization that has hovered around $350 million.7 8 How does a company with essentially no sales sustain a third of a billion dollars of equity value?

The answer is the architecture. Rather than raise hundreds of millions of dollars to build its own factories—the exact trap that has killed a graveyard of clean-tech startups—AirJoule's management built a web of 50/50 joint ventures with some of the largest industrial companies on Earth: power-and-grid giant GE Vernova, HVAC titan Carrier Global, and the Chinese battery king 宁德时代 Contemporary Amperex Technology Co., Limited (宁德时代 CATL).[^5] [^6] It outsourced its hardest chemistry problem to BASF, the largest chemical company in the world.10 In effect, AirJoule decided it would own the patents and the recipe, and rent everyone else's factories.

It's an asset-light strategy applied to one of the most asset-heavy problems imaginable—moving water and air around the planet. From a small-town workshop in Ronan, Montana, to the boardrooms of Boston and the manufacturing corridors of China, the question this whole story turns on is the one every frontier hardware company eventually faces: can you scale a genuine physical breakthrough globally without burning through billions of dollars and dying in the gap between a working prototype and a profitable product line?

Let's start where every good origin myth starts—not in Silicon Valley, but in a town of fewer than two thousand people in western Montana.

II. The Genesis: Matt Jore and the Montana Roots

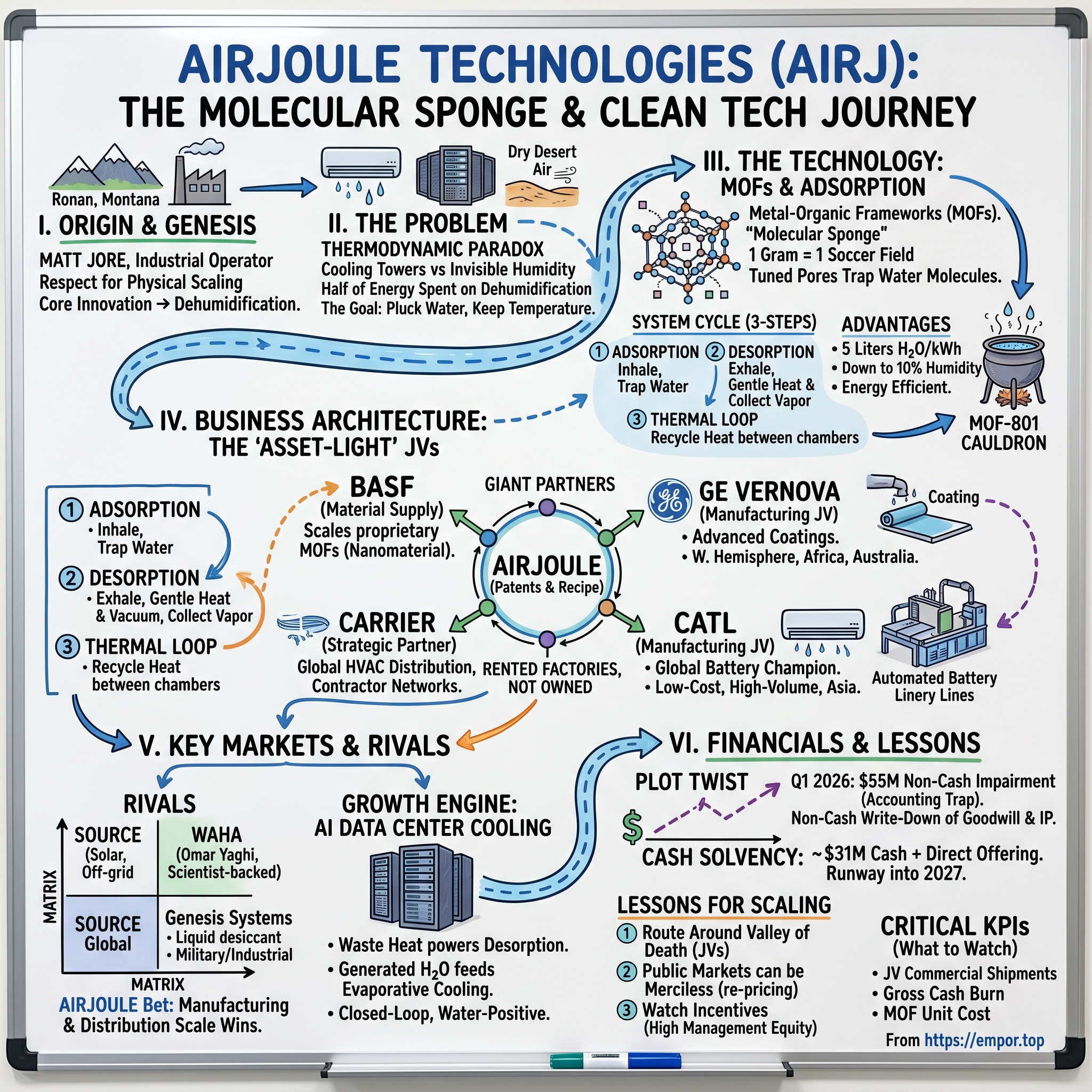

Ronan, Montana sits in the Mission Valley, hemmed in by snow-capped peaks, the kind of place where the nearest stoplight feels like a metropolis. It is not where you expect to find the headquarters of a company chasing the holy grail of clean tech. But to understand why AirJoule exists, you have to understand that its founder, Matt Jore, is not a man who solves problems with a whiteboard and a venture round. He solves them on a factory floor.

Jore is the kind of founder Acquired loves precisely because he doesn't fit the template. He is not an academic chemist, not an MIT spinout, not a thirty-year-old in a hoodie. He is a seasoned industrial operator who learned manufacturing the hard way—by building physical things and selling them by the truckload. In the 1990s, Jore founded Jore Corporation, a maker of power-tool accessories: the drill bits, driver bits, and quick-change chucks that end up in big-box hardware stores and contractors' toolboxes. He grew it into a real business, took it public, and scaled it to over $50 million in revenue.

That detail matters more than it might seem, and it's worth dwelling on. The single most common way clean-tech companies die is not that the science fails—it's that the manufacturing fails. A brilliant lab demonstration meets the brutal reality of yield rates, tolerances, supply chains, and unit costs, and the whole thing collapses. Jore had already lived inside that reality for a decade before he ever thought about humidity. He knew, in his bones, the difference between a thing that works once on a bench and a thing that can be stamped out a million times a year at a price a customer will pay. That instinct—respect for the savagery of scaling physical goods—is the genetic code of everything AirJoule later became.

In the early 2010s, Jore turned his attention to a problem that, on the surface, sounds almost mundane: pulling water out of the air. He formed a company called Core Innovation, the direct predecessor to what became Montana Technologies. His obsession was dehumidification—and here's where you need a little thermodynamics, told the way you'd tell it at a dinner party.

Think about your home air conditioner on a muggy summer day. It doesn't just cool the air; a huge fraction of its work goes into wringing the moisture out. The way it does this is crude and ancient. It takes warm, humid air and chills it down past the "dew point"—the temperature at which water vapor is forced to condense, the same way droplets form on a cold glass of iced tea. To squeeze water out, the machine has to overcool the entire air stream, water and air molecules alike, just to get the water to give up. Roughly half the energy your air conditioner burns on a humid day is spent on this single, wasteful task. And it does it using vapor-compression—a century-old process that depends on chemical refrigerants, many of which are potent greenhouse gases when they leak.

Jore's insight was a question that sounds almost childishly simple: what if you didn't have to cool the air down at all? What if you could reach into the air stream and pluck the water molecules out directly, leaving the air's temperature more or less alone? If you could do that, you'd skip the most energy-intensive step in the whole process. Back-of-the-envelope, you might save on the order of 75% of the energy spent on dehumidification.

The problem, of course, is that "plucking water molecules out of the air" is not a thing you can do with ordinary materials. You need something with an almost supernatural appetite for water—a material that acts like a microscopic sponge with an internal surface area beyond anything in nature. Jore needed a miracle material. And as it happened, chemists had spent the previous two decades inventing exactly that.

To understand AirJoule's technology, we have to go inside the molecular sponge.

III. The Science of the "Molecular Sponge": MOFs and the BASF Alliance

Here is one of the strangest facts in modern chemistry. Take a single gram of a material called a Metal-Organic Framework—a pinch of crystalline powder you could balance on your fingertip—and unfold all of its internal surface area. Lay it out flat. It would cover an area comparable to a soccer field. One gram. That is not a typo, and it is the single most important fact in this entire episode.

Let's build up what a Metal-Organic Framework, or MOF, actually is, because everything downstream depends on it. Imagine a microscopic scaffolding, like the steel skeleton of a skyscraper before the walls go on. At the joints, you place metal ions—the connector hubs. Between the hubs, you string organic molecules called ligands, which act like the steel beams. What you end up with is a crystal that is mostly empty space—a rigid, repeating cage riddled with billions of tiny, uniform pores. Because almost the entire structure is "wall" with nothing in between, the internal surface area is staggering. And here's the magic: chemists can tune those pores—their size, their shape, their chemical personality—so that they grab onto one specific kind of molecule and ignore everything else. You can build a MOF that is, essentially, a molecular trap designed for water.

The field has a godfather, and his name matters for our competition section later: Omar Yaghi, the chemist who pioneered MOFs and reticular chemistry, and who has spent his career demonstrating that you can harvest drinking water from desert air with the right framework. AirJoule's entire value proposition rests on the commercial application of that science.

So how does AirJoule's box actually work? The company calls its process a dual-chamber, vacuum-assisted pressure-swing system, which sounds intimidating but breaks down into a simple, beautiful cycle of breathing in and breathing out.

Step one, adsorption—the inhale. Ambient air, however dry, is pulled through a "contactor," a heat-exchanger surface coated with BASF-formulated MOF crystals.10 As the air passes over, the MOF pores selectively trap water molecules and hold onto them. Note the word adsorption—the water clings to the surface of the material, like dew on a spiderweb, rather than being absorbed into it like a paper towel soaking up a spill. The air comes out drier; the MOF gets loaded with water.

Step two, desorption—the exhale. Once a chamber's MOF is saturated, the company seals it off and does something clever: it draws a vacuum and applies gentle, low-grade heat. Lowering the pressure and adding a little warmth persuades the trapped water to let go of the framework and evaporate off as pure water vapor. Because the water came out of the air as vapor and is released as vapor, it's distilled—essentially clean, free of the contaminants in the original air. Condense that vapor and you have pure liquid water.

Step three, the thermal loop—the trick that makes it efficient. Here's the elegant part. AirJoule runs two chambers in tandem. While one chamber is inhaling—adsorbing water and releasing a little heat in the process—the other is exhaling, desorbing water, a process that needs heat. The system shuttles that heat back and forth between the two chambers so that the warmth from one half of the cycle does useful work in the other. It recycles its own energy instead of throwing it away. That internal heat recovery is the difference between a science experiment and an efficient product.

Now, the payoff, told in plain numbers. Traditional atmospheric water generators—the existing class of machines that pull drinking water from air—rely on those same power-hungry refrigeration coils we met earlier. They chill air to the dew point, which means they sip a lot of electricity and, critically, they basically stop working in dry climates because dry air has no dew point worth reaching. A typical refrigeration-based generator produces on the order of 3 liters of water per kilowatt-hour and struggles badly below moderate humidity. AirJoule's system, by contrast, has been designed to produce up to roughly 5 liters of pure water per kilowatt-hour and to keep working efficiently down to around 10% relative humidity—the kind of bone-dry desert air where conventional machines simply quit.1 In other words, it is meaningfully more energy-efficient and it works in exactly the water-stressed places that need it most. That combination—efficiency plus dry-climate capability—is the technical heart of the bull case.

But there's a catch that has sunk more than one clean-tech dream, and it's where Jore made his shrewdest early move. MOFs are wonderful in a lab. Manufacturing them at industrial scale—tons of consistent, high-quality crystalline powder—is a serious chemical-engineering challenge in its own right. Plenty of companies have died trying to scale their own exotic material synthesis, discovering too late that being a great inventor and being a great chemical manufacturer are completely different businesses.

Jore refused to walk into that trap. Instead of building chemical plants, AirJoule's predecessor signed a global supply agreement with BASF, the largest chemical company in the world, to manufacture the proprietary adsorbents—including the water-loving framework known as MOF-801—at industrial scale.10 Think about what this does to the balance sheet and the risk profile. The single hardest, most capital-intensive piece of the puzzle—reliably producing tons of a finicky nanomaterial—gets handed to a partner who has been running world-scale chemical production for over a century. AirJoule keeps the recipe and the system design; BASF owns the cauldron. It is the first instance of the pattern that defines this whole company: identify your deadliest scaling risk, and rent the solution from a giant who has already mastered it.

That instinct—don't build what a titan can build better—would soon be applied not just to chemistry, but to the company's entire path into the public markets.

IV. The Capital Pivot: The 2024 de-SPAC & The Capital Deployment Benchmark

By 2023, the SPAC boom that had defined the pandemic-era markets was well into its hangover. The special-purpose acquisition company—the "blank check" shell that raises money first and finds a company to merge with later—had gone from Wall Street's favorite toy to one of its dirtiest words. Hundreds of de-SPACs had cratered, taking retail investors down with them. Into that frosty environment, in March 2024, Montana Technologies chose to go public by merging with a SPAC called Power & Digital Infrastructure Acquisition II Corp., which traded under the ticker XPDB.5

The deal valued the combined company at an implied pro forma enterprise value of roughly $500 million, and the merged entity began trading—eventually under the AirJoule name and the AIRJ ticker.5 On paper, that's a half-billion-dollar valuation for a company generating zero revenue. To understand whether that was madness or shrewd positioning, you need to meet the man who engineered it.

Enter Pat Eilers. If Matt Jore is the factory-floor operator, Pat Eilers is the capital architect—and he has one of the more unusual résumés in clean tech. Before finance, Eilers played professional football in the NFL. He later became a long-time private-equity investor and founded Transition Equity Partners, a firm focused on the energy transition, and he served as CEO of the XPDB SPAC itself.5 What's notable is what he did after the merger closed. Most SPAC sponsors do the deal, collect their promote, and disappear. Eilers did the opposite: he stayed, taking the role of Executive Chairman to actively manage the capital structure of the company he'd just brought public.3 That decision—sponsor becomes steward—tells you he viewed AirJoule as a long-term project, not a transaction to flip.

Now to the question every sophisticated investor asks about a pre-revenue de-SPAC: did they overpay? The honest answer is "it depends entirely on what you think you're buying," and the comps are genuinely instructive.

At the time of the merger, the established, cash-flowing giants of the relevant industries traded at robust multiples. The big HVAC names—Carrier, Trane, Johnson Controls—were valued at roughly 18 times EBITDA. The water-technology leaders—Xylem, Watts Water, Energy Recovery—commanded even higher multiples, in the neighborhood of 23 times EBITDA. These are mature businesses with real earnings, and the market was paying up for them.

Against that backdrop, you could construct a story in which Montana Technologies' $500 million valuation looked almost cheap—a "discount" to where the cash-flowing incumbents traded. But that framing contains a sleight of hand worth naming out loud. Those incumbents trade at a multiple of actual earnings. Montana Technologies had no earnings. It had no revenue. It had intellectual property, a pile of patents, a chemistry partnership, and a pair of nascent joint ventures. So the $500 million wasn't a multiple of anything; it was a price on a promise. The deal also carried an additional earnout—on the order of $200 million in extra value—that would only vest if the company hit future performance milestones, a structure that at least tied some of the upside to actually delivering.5

Here's the reality check, and it's the lesson that echoes through the rest of this story. Public markets are merciless to pre-revenue de-SPACs. Once the lockups loosen and reality sets in, the same investors who cheered the "discount to comps" framing start asking where the revenue is. By mid-2026, AirJoule's market capitalization had compressed to around $350 million.7 8 That re-pricing isn't a scandal; it's the market doing exactly what it does—charging an early premium for "frontier tech" and then slowly extracting that premium back as it waits for the technology to prove it can actually sell. The investors who bought at the $10 de-SPAC level effectively paid up front for optionality on a breakthrough, and the market has been re-grading that optionality in real time.

The merger came with one more piece that reveals the strategy: the financing. Rather than rely on public investors alone, Eilers and Jore assembled a roughly $50 million PIPE—a Private Investment in Public Equity, where chosen investors commit capital alongside the deal. And the investors they chose were not random hedge funds; they were strategic partners with reasons to want AirJoule to succeed. Carrier Global put in $10 million. The energy-focused Rice Investment Group put in $10 million. GE Vernova participated as well.5 When your customers and manufacturing partners are also writing checks into your balance sheet, you've done something subtle and powerful: you've aligned the people who could make the company with the people who own the company.

Those strategic checks were the financial expression of a deeper structural bet—the joint ventures themselves. And that bet is where AirJoule's corporate design becomes a genuine masterclass.

V. The "Asset-Light" JV Masterclass: GE Vernova & CATL

There's a phrase that haunts every clean-tech investor, and it's worth saying slowly: the Valley of Death. It describes the gap between a technology that works and a business that scales—and it has a brutally consistent script. A startup invents something genuinely impressive. It raises $100 million on the strength of that invention. It spends nearly all of it building a single, gleaming factory. Then a manufacturing line stalls, a supplier slips, a yield problem emerges—and because the company poured every dollar into that one facility, a delay that a giant would shrug off becomes existential. The cash runs out before the factory runs right. The company dies not from bad science but from the sheer capital intensity of turning atoms into products at scale.

AirJoule's founders looked at that graveyard and made a decision that defines the company: we will not build the factory. Instead, they would leverage the existing, multi-billion-dollar manufacturing footprints of global conglomerates who already know how to make complex hardware in volume. This is the asset-light joint-venture model, and AirJoule executed it not once but three times.

The GE Vernova JV. In March 2024, AirJoule's predecessor and GE Vernova—the power, grid, and energy spin-out of General Electric—announced a 50/50 joint venture, organized as AirJoule LLC, to manufacture and commercialize atmospheric water harvesting and dehumidification systems.[^5] 6 The geographic mandate covered the Americas, Africa, and Australia. Look at what each side brought to the table, because it's a near-perfect complementarity. GE Vernova contributed world-class advanced coating capabilities—the precise, repeatable application of materials onto surfaces is exactly the kind of industrial process needed to turn raw MOF powder into functional, coated contactor surfaces—plus deep research infrastructure. AirJoule contributed the MOF know-how and the vacuum-swing patent suite. One partner had the molecules; the other had the machine shop and the labs to make them at scale. Neither could move as fast alone.

The CATL JV. If the GE Vernova partnership secured the Western industrial base, the second joint venture went after something even more strategically valuable: low-cost, high-volume Asian manufacturing. AirJoule partnered with 宁德时代 Contemporary Amperex Technology Co., Limited (宁德时代 CATL), the Chinese company that is the undisputed global champion of lithium-ion battery manufacturing, through a 50/50 venture associated with an entity called CAMT Climate Solutions Ltd. Why does CATL matter so much? Because making batteries at CATL's scale is one of the supreme achievements of modern manufacturing—it demands ferociously automated production lines, relentless cost reduction, and a global supply chain that can source materials by the megaton. That is exactly the skill set you'd want if your goal were to drive down the unit cost of a MOF-coated water-harvesting machine and crank out volume for the Asian market. A company headquartered in Ronan, Montana could not build that capability in a decade. Through the JV, it effectively rented it.

This is the moment to appreciate the audacity of the design. AirJoule, a company you could fit in a couple of office suites, had arranged to have its products built by the people who build the West's power grids and by the people who build the world's batteries. It split the planet into manufacturing territories and handed each one to a titan.

The Carrier commercialization agreement. The third leg is slightly different in structure but no less important. Carrier Global—one of the largest HVAC companies in the world, the heating-and-cooling business that traces back to the inventor of modern air conditioning—signed a strategic partnership giving it rights to integrate AirJoule's core technology directly into commercial and residential HVAC products in the Americas for a specified window.[^6] This isn't a manufacturing JV; it's a distribution and integration channel. And it may be the most valuable relationship of all, because Carrier doesn't just make air conditioners—it has a global sales force, contractor networks, and brand relationships that took a century to build. If AirJoule's "cores" become a standard component inside Carrier's product line, AirJoule gets handed a distribution channel it could never replicate.

So step back and look at what's been assembled: BASF makes the material, GE Vernova and CATL make the machines across complementary halves of the globe, and Carrier sells them into the HVAC market. AirJoule sits at the center holding the patents, collecting its share of the economics, and—crucially—keeping its own capital expenditure remarkably light. It's an elegant piece of corporate engineering. The open question, which we'll return to, is whether sitting at the center of other people's factories gives you enough control over your own destiny. For now, though, the structure is undeniably clever. Let's look at what business it actually adds up to.

VI. Deep Dive: The Core Business, Economics, & The Battle with Rivals

To understand the market AirJoule is walking into, you have to understand that atmospheric water generation has historically been a graveyard of good intentions. The idea—pull clean drinking water out of thin air—is so intuitively appealing that it has attracted decades of entrepreneurs and a fair amount of hype. But the industry has remained fragmented, niche, and low-margin for one stubborn reason: physics. Conventional machines burn too much electricity per liter, and they fail in exactly the arid places where water is scarcest. The result is a scattered field of small players serving narrow niches, none of which has cracked true mass-market scale. That's the backdrop against which AirJoule's efficiency claims either matter enormously or don't matter at all.

So who is AirJoule actually fighting? Let's war-game the competitive map, because each rival illuminates a different edge—and a different threat.

SOURCE Global, formerly Zero Mass Water, is the best-funded name in the space and the one most investors have heard of. SOURCE makes solar-powered "hydropanels" that generate drinking water entirely off-grid, using sunlight to drive the process. It's a genuinely elegant solution for remote communities, disaster zones, and homes with no reliable water infrastructure—no electricity grid required. But its model is the mirror image of AirJoule's strengths. Hydropanels are capital-intensive per liter, produce a relatively limited amount of water per square foot of panel, and are aimed squarely at residential and community drinking water. SOURCE is solving a different problem—off-grid resilience—rather than high-throughput, grid-connected efficiency. The two could even be complementary more than competitive.

Genesis Systems builds a product called the WaterCube, using liquid desiccant technology—a different chemical approach to grabbing moisture, where a water-loving liquid does the absorbing instead of a solid framework. Genesis targets the heavy end of the market: military deployments, disaster relief, and industrial-scale operations. It's a serious player in those domains. But it lacks the integrated consumer and HVAC channels that AirJoule has lined up through Carrier, which means it competes on raw water production rather than on embedding itself into the world's cooling infrastructure.

Water Harvesting Inc., or WAHA, is the one to watch most closely, and the reason is a name we met earlier: Omar Yaghi, the godfather of MOFs himself, is behind it. WAHA is building modular MOF-based water harvesters—which means it is attacking AirJoule's exact technological turf with the credibility of the person who arguably invented the underlying field. On pure science, WAHA may be AirJoule's most dangerous direct threat. But—and this is the crux of the entire AirJoule thesis—WAHA does not have GE Vernova's coating lines, CATL's manufacturing scale, BASF's material supply, or Carrier's distribution. AirJoule's bet is precisely that in hardware, the winner is rarely the purest science; it's the company that can manufacture and distribute at scale. WAHA has the better pedigree on paper; AirJoule has the better industrial machine around it. Which of those wins is one of the genuinely open questions in this story.

Now to AirJoule's own economics, and here we have to be honest about where the company actually is. It is in the pre-revenue-to-early-commercialization phase—the most fragile and most consequential stage of any hardware company's life. The starting gun fired in the fourth quarter of 2025, when AirJoule recorded its first physical sale: a roughly $0.1 million transaction for an A250 system delivered to Arizona State University.3 One hundred thousand dollars. For a company valued in the hundreds of millions, that number is almost comically small—and that's the point. It is not meant to be revenue; it is meant to be proof. The first real customer, the first system in the field, the first validation that the box does what the lab said it would.

The more important question is what the eventual economic engine looks like, and management's intended model is telling. AirJoule does not primarily want to be in the low-margin business of bolting together complete systems—that's commodity assembly work, and it's exactly the kind of capital-and-labor-heavy activity it handed to its JV partners. Instead, the high-margin prize is selling the "AirJoule Cores"—the desiccant-coated heat exchangers that are the beating heart of every unit—to Carrier and other licensees, and collecting royalty and component revenue on top.3 Think of the razor-and-blades logic, but inverted: AirJoule wants to be the proprietary blade inside everyone else's razor. If Carrier builds the cores into millions of HVAC units, AirJoule earns a high-margin clip on each one without ever touching a final assembly line. That's the dream. The gap between a single $100,000 university sale and a stream of high-margin core royalties is the entire investment journey, and crossing it is anything but guaranteed.

There's one more market—barely on most investors' radar, and potentially the biggest of all—where AirJoule's particular physics turns into an unfair advantage. To see it, we have to follow the heat.

VII. The "Hidden" Growth Engine: The Data Center AI Cooling Pivot

Return to that Arizona server hall from the opening, because this is where the story stops being about drinking water and starts being about the defining infrastructure boom of the decade. The artificial-intelligence build-out is, at its physical core, a heat problem. High-performance AI servers packed with accelerators run blisteringly hot, and the hotter the chips, the harder they are to keep alive. The dominant way hyperscalers manage that heat is evaporative cooling—essentially, evaporating water to carry heat away—and it is thirsty work. Data centers consume billions of gallons of water a year, and increasingly they're doing it in precisely the wrong places: water-stressed states like Arizona, Texas, and Oregon, where every gallon a data center evaporates is a gallon a community doesn't drink. The public backlash has been growing, and it's becoming a genuine constraint on where these facilities can be built.

This is why the data-center angle is not a speculative novelty bolted onto the AirJoule story—it may be the single most important value driver in the entire investment case. Here's the mechanism, and it's almost too neat.

AirJoule's process, recall, needs two things to run efficiently: air to harvest water from, and low-grade heat to drive the desorption step—the exhale that releases captured water as vapor. Now ask yourself: what does a data center produce in enormous, continuous, otherwise-useless quantities? Low-grade waste heat, pouring off the servers, normally just dumped into the environment. AirJoule's system can sit directly adjacent to the cooling infrastructure and use that waste heat as its energy source. The heat that the data center desperately wants to get rid of becomes the fuel that powers the water-harvesting cycle. It's a genuine arbitrage—two facilities' problems canceling each other out.

And then comes the closing of the loop, which is the part that makes hyperscaler executives lean forward. The pure distilled water that AirJoule generates from the intake air can be fed directly back into the data center's evaporative cooling system. The facility stops drawing down the local aquifer and starts recycling moisture out of the very air around it. In the ideal case, you get a self-sustaining, closed-loop, water-positive data center—a facility that no longer competes with farmers and towns for water, because it makes its own.

Sit with the strategic elegance of that for a moment. AirJoule's technology potentially solves the two hardest operational constraints facing the AI build-out simultaneously: it reduces the energy penalty of cooling, and it slashes—or eliminates—the water draw that is increasingly blocking permits and inflaming communities. A hyperscaler choosing where to put its next multi-billion-dollar campus cares enormously about both. If AirJoule can credibly deliver water-positive cooling, it isn't selling a clean-tech curiosity; it's selling itself into the capital-expenditure flood of the most aggressive infrastructure spending cycle in modern technology.

Now, the necessary dose of realism: as of mid-2026, this is an early-stage pilot opportunity, not booked revenue. The data-center vision is exactly that—a vision, with pilots to prove and economics to validate at scale. The gap between "the physics works beautifully on a slide" and "hyperscalers have written nine-figure orders" is vast, and it's littered with the bones of companies whose elegant loops never quite closed in the real world. But of all the things that could make AirJoule a far larger company than its current pre-revenue reality, this is the one with both the biggest market and the tightest fit to the technology's genuine strengths. It's the call option embedded in the stock.

Which makes the events of early 2026 all the more jarring—because just as the commercial story was supposed to be accelerating, AirJoule's own financial statements delivered a shock.

VIII. The 2026 Plot Twist: The $55M Accounting Impairment

In May 2026, AirJoule filed its quarterly report for the first quarter, and the headline number landed like a thunderclap: a net loss of $49.8 million for a single quarter.4 For a company with cash in the low tens of millions and revenue measured in the hundreds of thousands, a near-$50 million loss is the kind of figure that makes a casual reader assume the wheels have come off. The stock-watching crowd recoiled. But as with so much in accounting, the headline and the reality were two very different things—and untangling them is one of the most instructive moments in this entire story.

The culprit behind the loss was a $55 million non-cash impairment charge flowing through AirJoule's equity-method investment in its AirJoule JV.4 To understand what that means, you have to understand a peculiar and somewhat cruel feature of de-SPAC accounting—a trap that has snared many a newly public company.

Here's the mechanism, explained without the jargon. When the JV was formed and the company went public, accountants assigned values to the intangible assets created in the process—chiefly, the in-process research and development (the value ascribed to the technology still being commercialized) and goodwill (the premium paid above the identifiable net assets). Those carrying values were anchored, in part, to the company's public-market valuation at the time—roughly the $10-per-share world of the de-SPAC. Accounting rules, specifically the standard governing goodwill and intangibles (ASC 350), require companies to periodically test whether those carrying values still hold up. And critically, a sustained decline in your public stock price below where you started is a textbook trigger for an interim impairment test.

AirJoule's stock had done exactly that—drifted well below its $10 de-SPAC entry price and stayed there. That sustained decline forced the test. And the test concluded what the falling stock price implied: the carrying value of the JV's intangible assets exceeded their current fair value under prevailing public-market pricing. The result was a write-down at the JV level on the order of a $110.3 million reduction in in-process R&D and a $76.1 million reduction in goodwill, of which AirJoule absorbed its 50% share—flowing through as that roughly $55 million charge.4

So how should a thoughtful investor read this? This is a genuinely useful lesson in separating noise from signal, and there are two honest interpretations.

The bear's reading is pointed and not unreasonable. Writing down in-process R&D is the accounting system effectively confessing that the technology was valued too richly at the time of the deal. In plain terms, the market is saying: this technology is worth less today than you told us it was worth when you took it public. For a company whose entire valuation rests on the promise of its intellectual property, an impairment of that exact IP is not a comfortable thing to wave away. It is evidence, however formulaic, that the original de-SPAC valuation contained more hope than the public market is now willing to pay for.

The bull's—and management's—reading is equally legitimate and centers on one word: non-cash. CFO Sze-Yin Pang and CEO Matt Jore moved quickly to frame the charge as a purely accounting-driven adjustment, mechanically triggered by the stock price rather than by any deterioration in the technology, the partnerships, or the commercial roadmap.4 No cash left the building. No customer canceled. No JV dissolved. The write-down is, in this view, an artifact of the rule that ties intangible values to market capitalization—a rule that can make a falling stock price cause an accounting loss, which can in turn pressure the stock price further, in a slightly circular dance that has nothing to do with whether the machines work.

And on the metric that actually determines survival—cash—the picture was far steadier than the loss headline suggested. AirJoule held roughly $31.1 million in cash at the parent level, a position it bolstered with a $15 million direct equity offering in mid-2026.4 Against a 2026 cash-burn framework guided to roughly $25 million, that combination implied an operational runway extending well into 2027.4 In other words, the company that just reported a $49.8 million loss had plenty of actual money to keep operating—because the loss never touched the bank account. This is the difference between accounting solvency and cash solvency, and for a pre-revenue hardware company, cash is the only one that decides whether you live to see the next milestone.

The impairment episode is, in miniature, the whole AirJoule investment debate: a company whose reported financials can swing wildly on market sentiment, sitting on real technology and real partnerships, with just enough cash to keep proving—or disproving—itself. To weigh that debate properly, it helps to put it through a couple of rigorous strategic frameworks.

IX. The Strategic Toolkit: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the storytelling and the strategic question is simple: does AirJoule have a moat, or just a head start? A head start gets competed away; a moat compounds. Two frameworks help us pressure-test the answer—Hamilton Helmer's 7 Powers, which asks what durable advantages a business holds, and Michael Porter's 5 Forces, which asks how attractive the surrounding industry actually is. Run honestly, they paint a picture of a company with real potential power that is mostly still latent—promised by the structure but not yet proven by results.

Hamilton's 7 Powers Applied to AirJoule

Cornered Resource — currently AirJoule's strongest claim. A cornered resource is preferential access to something valuable that others can't easily get. AirJoule arguably has a stack of them: the exclusive supply relationship with BASF for scaling specialized MOFs, the proprietary vacuum-swing patent suite, and the sorbent-coating intellectual property contributed through the GE Vernova partnership.[^5] 10 Together these form a genuine chemical-and-materials barrier—a rival can't simply order MOF-801 and coating expertise off a shelf. This is the most defensible thing the company owns today.

Process Power — real but modest. Process power comes from doing something complex that competitors struggle to replicate even when they know what you're doing. AirJoule has spent over a decade mastering the finicky mechanical engineering of vacuum-assisted pressure-swing adsorption cycles—the heat shuttling, the timing, the integration. That's hard-won and not trivially copied. But process power grows with operational repetition, and AirJoule simply hasn't manufactured at volume yet, so this remains medium-strength at best.

Scale Economies — purely potential. Here's where the JV structure could eventually pay off enormously. By piggybacking on CATL's battery-line manufacturing model and GE Vernova's industrial footprint, AirJoule could one day enjoy scale economics far beyond what its own size would allow.[^5] But "could" is doing heavy lifting. You don't have scale economies until you have scale. Today this is a blueprint, not a moat.

Switching Costs — high, but in the future tense. If Carrier integrates AirJoule Cores directly into the physical architecture of its global HVAC product lines, ripping them out later would require a multi-year, multi-million-dollar engineering redesign.[^6] That's a powerful lock-in—once you're designed into a product platform, you're extraordinarily sticky. The catch, again, is tense: this switching cost exists only once the integration actually happens at scale.

Counter-Positioning — structurally strong. This is the subtle one. AirJoule sells refrigerant-free, low-energy dehumidification, which directly undercuts the core business model of traditional compressor-based HVAC players. Incumbents whose entire economics rest on vapor-compression face a painful dilemma: embracing AirJoule's approach cannibalizes their existing product lines and supply chains. That reluctance to self-disrupt is exactly the gap a counter-positioned challenger exploits.

Network Effects — none. Water machines don't get more valuable to each user as more users join. Honest answer: zero.

Brand — none. AirJoule has no consumer brand power; nobody pays a premium because it says AirJoule on the box. Zero.

The verdict from the 7 Powers lens: AirJoule's moats are real in kind but mostly unrealized in degree. The cornered resource is here now; the switching costs and scale economies are promissory notes that only pay out if commercialization succeeds.

Porter's 5 Forces Analysis

Threat of New Entrants — high. Clean tech is crowded with well-funded startups racing to commercialize alternative desiccants and water-harvesting systems. The space is hot, capital is available, and there's no shortage of teams chasing the same prize.

Bargaining Power of Suppliers — very high, and this is a genuine vulnerability. AirJoule's reliance on BASF for specialized MOF production is both its masterstroke and its Achilles' heel.10 Outsourcing the chemistry removed enormous risk and capital—but it also means a single supplier sits astride the company's most critical input. Any disruption, pricing pressure, or strategic shift at BASF would hit AirJoule's gross margins directly. Concentration risk cuts both ways.

Bargaining Power of Buyers — high. The customers are sophisticated and powerful: HVAC OEMs and hyperscale data-center operators who already run trusted, proven cooling solutions. They will demand rigorous, validated efficiency metrics and reliability data before betting their products or facilities on an unproven newcomer. They hold the leverage.

Threat of Substitutes — high. Traditional condensation cooling is entrenched and works. Liquid-desiccant systems are a live alternative. And in the data-center niche specifically, plume-water recovery approaches (such as those pursued by Infinite Cooling) attack the same water-reuse problem from a different angle. AirJoule is not the only path to the goal.

Competitive Rivalry — moderate. The clean-tech water and dehumidification sector is young and fragmented, with players mostly focused on basic survival and initial commercial validation rather than head-to-head price wars. Rivalry will intensify as the market matures, but for now it's a land-grab, not a bloodbath.

Put the two frameworks together and you get a coherent investor's-eye summary: AirJoule operates in an industry that is not structurally easy—powerful suppliers, demanding buyers, real substitutes—but it has assembled a set of latent powers, anchored by its cornered chemical resource and its potential switching costs, that could harden into a durable moat if, and only if, the commercial machine actually turns over. The whole thesis lives in that conditional.

So what does a disciplined investor actually do with all of this? Let's distill the playbook.

X. Playbook: Key Lessons for Clean-Tech Scaling & Management Profile

Step back from the details and AirJoule offers a set of transferable lessons about how to build—and how to read—a frontier hardware company in the 2020s. Three stand out.

Lesson one: the asset-light blueprint. The defining strategic choice of this company was the decision not to build. Don't pour your scarce capital into a factory you'll struggle to fill. Instead, own the intellectual property, secure your hardest input from a world-class supplier (BASF), and license the manufacturing to giants who have already mastered it at scale (GE Vernova, CATL), while plugging into an incumbent's distribution (Carrier).[^5] [^6] 10 It's a genuinely modern answer to the clean-tech Valley of Death—route around capital intensity by renting everyone else's hard assets. The trade-off, never to be forgotten, is control: when titans build and sell your product, your destiny is partly in their hands, and a partner's shifting priorities can matter as much as your own execution.

Lesson two: de-SPAC valuations are mirages, and accounting will eventually say so. The $55 million impairment is a cautionary tale written in the language of GAAP.4 When you go public pre-revenue at a valuation built on promise, and the public market subsequently re-prices your equity downward, the accounting rules don't politely ignore it—they force you to write down the very intellectual and physical assets your story is built on, regardless of whether your operational progress is real. A long-term investor learns to read through these non-cash charges to the underlying cash and milestones, while never dismissing what the write-down implies about how richly the original deal was priced.

Lesson three: follow the incentives. In a pre-revenue company where everything hinges on management delivering a distant payoff, the alignment of leadership's personal wealth with shareholders is not a footnote—it's central. And here the picture is encouraging. CEO Matt Jore holds an 11.32% direct stake in the company, worth roughly $37.58 million, and his compensation of about $2.13 million is 81.3% equity-weighted, dominated by restricted stock units and options rather than cash.3 Tellingly, he converted all of his Class B common stock into Class A shares—collapsing a dual-class structure that would have given him outsized voting control, and signaling a long-term commitment to a single, clean share class alongside ordinary shareholders.3 Executive Chairman Pat Eilers holds over 1.87 million shares directly, plus millions more through trusts, and his roughly $5.69 million in annual compensation is almost entirely equity-driven, with about $5.24 million coming as stock awards.3 Both men, in other words, get rich only if the common stock does—which is exactly the alignment you want when you're betting on a multi-year commercialization journey.

The myth versus the reality. It's worth ending on a clear-eyed separation of the two stories you can tell about AirJoule. The myth—the one that animated the de-SPAC—is of a company that has already cracked the holy grail, ringed by the world's industrial titans, sitting on the inevitable future of water and cooling. The reality in mid-2026 is more sober: a genuinely promising and scientifically grounded technology, an elegantly engineered but still-unproven corporate structure, a first commercial sale of $100,000, an accounting impairment that bruised the optics, and just enough cash to keep proving itself for another year or so.3 4 7 Neither story is dishonest; the gap between them is precisely the investment. The technology's strengths—real efficiency, real dry-climate capability, a real fit with the AI cooling problem—are matched by real risks: supplier concentration in BASF, dependence on partners' factories, demanding buyers, and the eternal hardware question of whether the lab numbers survive contact with the field.

The KPIs that actually matter. If you're tracking this company as a long-term investor, ignore the quarterly noise and the accounting swings, and watch three things.

First, JV commercial shipments—the number of AirJoule Cores actually delivered to Carrier and to early data-center pilot sites through 2026 and 2027. This is the single cleanest signal that the asset-light model is converting from blueprint into revenue. Units in the field are truth; everything else is narrative.

Second, gross cash burn—whether the company holds its combined burn within the roughly $25 million annualized framework management has guided to.4 For a pre-revenue company, runway is life, and the rate at which cash leaves the building determines how many more shots on goal it gets before it must raise again, dilute, or fold.

Third, MOF unit cost—the pace at which BASF can drive down the cost of synthesized MOF-801. Because the material is the heart of every unit and BASF is the sole supplier, the trajectory of that cost will quietly govern the eventual gross margins of the entire product line.10 Cheaper MOFs mean fatter margins and a wider competitive moat; stalled costs mean the whole high-margin-core thesis comes under pressure.

Shipments, burn, and material cost. Watch those three numbers over the next several years, and you'll know whether the molecular sponge from a small town in Montana is becoming a real business—or remaining, as so many clean-tech dreams have, a beautiful idea waiting for a world that never quite arrives.

References

-

AirJoule Technologies Investor Relations — Official Portal ↩↩

-

AirJoule Technologies SEC Edgar Filings Index — CIK 0001925345 ↩

-

Form 10-K Annual Report (FY2025) — AirJoule Technologies Corporation, 2026-03-31 ↩↩↩↩↩↩↩

-

Form 10-Q Quarterly Report (Q1 2026) — AirJoule Technologies Corporation, 2026-05-15 ↩↩↩↩↩↩↩↩↩

-

Form S-4/A Business Combination Prospectus — Power & Digital Infrastructure Acquisition II Corp, 2024-02-12 ↩↩↩↩↩

-

GE Vernova & Montana Technologies Form Clean Energy JV — Reuters, 2024-03-14 ↩

-

AirJoule Technologies Corporation (AIRJ) Market Summary — Bloomberg ↩↩↩

-

AirJoule Technologies Corporation (AIRJ) Profile & Metrics — Simply Wall St ↩↩

-

AirJoule Technologies Analysis and SEC Filing Breakdowns — Seeking Alpha ↩

-

Strategic MOF Material Global Supply Agreement — BASF & Montana Technologies, 2024-01-22 ↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube