Alamos Gold: The Masterclass in Low-Cost Consolidation

I. Introduction: The Mid-Tier Unicorn

Picture the gold mining industry as a casino where the house almost always wins—except the house isn't the customer, it's geology, and the players are CEOs convinced their next acquisition will be the one that finally pays off. For two decades, the script has been remarkably consistent: gold price rises, mid-tier producers issue equity, buy something at a peak multiple, watch synergies evaporate, and quietly impair the goodwill three years later. The Gold Miners ETF (GDX) has been a graveyard of these stories. Between 2015 and 2025, the GDX traded essentially sideways while the underlying gold price more than doubled—an extraordinary indictment of the industry's capital discipline.[^1]

And then there's Alamos Gold.

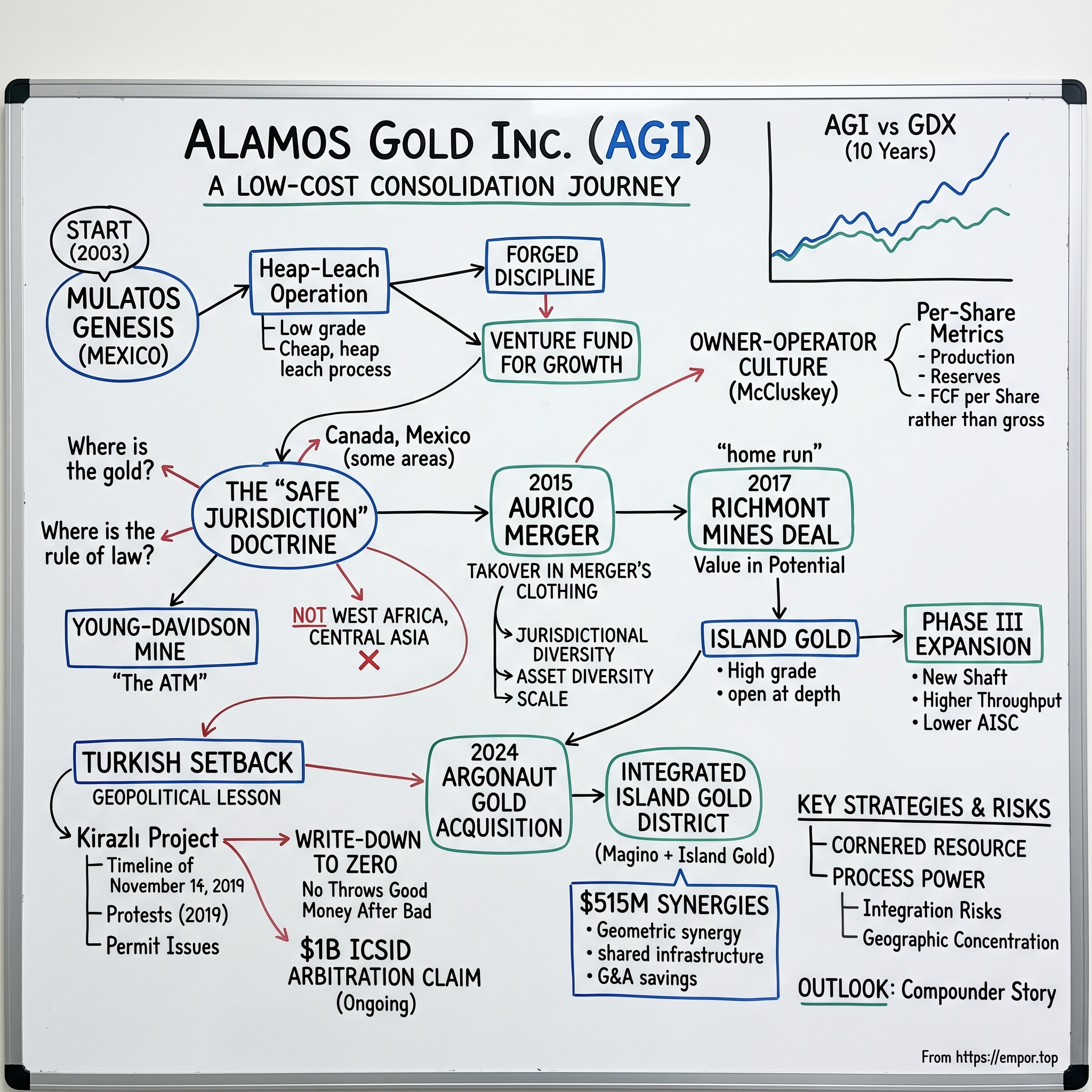

A single chart tells the story. Stack the AGI share price against the GDX over the last ten years and the divergence is almost embarrassing for the rest of the sector. While the average gold miner gave investors a ride to nowhere, shareholders of this Toronto-headquartered mid-tier compounded capital at a rate that wouldn't look out of place in a software portfolio. The company crossed a $10 billion market capitalization in 2025 on the back of disciplined production growth, expanding margins, and an All-In Sustaining Cost (AISC) profile that put it inside the lowest quartile of senior global producers.1

So what's the hook? How did a company that started in 2003 with a single open-pit heap-leach operation in the dusty hills of Sonora, Mexico end up with one of the best long-duration track records in gold mining?

The thesis we'll defend across this episode is that Alamos Gold is not really a mining company. It's a capital allocation machine with a very specific arbitrage at its core—what the team internally calls "safe jurisdiction" investing. Every major decision the company has made—the Mexico exit decisions, the Canadian doubling-down, the Turkey walk-away, the Argonaut acquisition—maps onto a single, almost obsessive question: where can we deploy a dollar of capital, in a jurisdiction with predictable rule of law, and earn an after-tax return that compounds for decades? Most mining CEOs ask "where is the gold?" The Alamos answer has been "where is the gold and the rule of law and the workforce and the power grid?"

It's not glamorous. It is, however, what has separated Alamos from peers who chased grade in Burkina Faso, Mali, Eritrea, and the Democratic Republic of the Congo—peers who are now writing down billions of dollars in expropriated or stranded assets.

Our roadmap looks like this. We'll begin with founder and CEO John McCluskey's 2003 bet on the Mulatos heap-leach project—a piece of ground that several majors had walked away from. We'll trace the 2015 AuRico merger that transformed a single-asset producer into a North American mid-tier and brought the Young-Davidson mine into the portfolio. We'll spend serious time on the 2017 Richmont Mines deal, which delivered Island Gold—arguably the best high-grade underground asset acquired in Canadian mining history at the price paid. We'll dissect the Turkey debacle around the Kirazlı Altın Madeni Projesi and the $1 billion ICSID arbitration that followed.[^3] And we'll examine the 2024 Argonaut Gold acquisition that bolted the Magino mine literally next door to Island Gold, creating what management now calls the "Integrated Island Gold District."

By the end, you'll understand why some institutional investors are convinced that AGI is the cleanest free-cash-flow story in mid-tier gold mining—and why the bear case isn't really about gold prices at all, but about whether the team can pull off one more integration without missing a step.

Let's begin where every Acquired story begins—at the founding, when nobody was paying attention.

II. Founding & The Mulatos Genesis

To understand why Alamos exists at all, you have to step back into the early 2000s gold market, which is to say, you have to step into a graveyard. Gold had spent the late 1990s in a brutal multi-year decline, bottoming around $250 an ounce in 1999, a price at which a substantial portion of global mine production was uneconomic. Bre-X had detonated investor trust in 1997 with one of the largest mining frauds in history. Senior producers were hedging their future production, which is to say, mortgaging the gold in the ground at distressed prices because their balance sheets were broken. The phrase "value investor in gold equities" was practically an oxymoron.

This is the moment John McCluskey, then a relatively unknown mining entrepreneur, decided to bet his career on a heap-leach project in Sonora, Mexico that the majors had quietly shelved.[^4] The deposit was called Mulatos. It sat in the Sierra Madre Occidental, accessible only by a rough mountain road, with grades so low—around one gram per tonne—that no underground mining method could touch it. The previous operators had concluded that even at the higher 1990s gold prices, the economics didn't pencil. McCluskey's view was the opposite: with the right heap-leach process at scale, with the right contractor model, and with a tight focus on cost per ounce rather than ounces per year, Mulatos would print cash. He just needed gold to cooperate.

Heap leaching deserves a brief explanation, because it's central to the Alamos origin story. Imagine taking ore so low-grade that it would be a waste rock pile at a higher-grade mine. You crush it, stack it on an impermeable plastic liner the size of several football fields, drip a dilute cyanide solution over the top, and collect the gold-bearing liquid at the bottom. There's no underground tunneling, no expensive mill, no flotation circuit. The capital intensity is a fraction of a conventional gold operation. The trade-off is that recovery rates are lower—you might get only 60-75% of the contained gold instead of 90%+ in a conventional mill—but if your ore is cheap enough and your operating cost is low enough, the math works.

The Mulatos Mine—Mina de Mulatos to its Mexican workforce—poured its first gold in 2005, almost exactly when the gold bull market began to take hold. Within a few years, all-in cash costs were running in the bottom quartile of the industry. The asset became, in McCluskey's later phrasing, the venture fund for everything that followed. Cash flow from Mulatos funded exploration, paid down debt, and—critically—was retained on the balance sheet rather than distributed as a special dividend during the 2010-2011 gold peak.

That last point is non-obvious and worth dwelling on. In 2011, when gold crossed $1,900 an ounce, the rational thing to do as a single-asset producer would have been to celebrate, raise equity at the top, and acquire something. The mid-tier herd did exactly that—and the asset base they bought at 2011 prices became the goodwill impairments of 2013-2015. Alamos didn't. McCluskey and his team sat on the cash. They watched a generation of competitors lever up at the peak and then face their reckonings.

The "old history" tie-in to today's company is this: every cost-discipline reflex you see at modern Alamos was forged at Mulatos. The relentless focus on AISC. The skepticism of grand growth-for-growth's-sake projects. The willingness to walk away from deals that don't pencil. None of this is corporate folklore. It's the muscle memory of a team that learned to operate a real mine when gold was structurally cheap.

And by 2014, with Mulatos maturing and the broader gold price collapsing back toward $1,100 an ounce, McCluskey began looking for the next chess move. The juniors and mid-tiers were once again broken. It was time to be a buyer.

III. The 2015 Inflection: The AuRico Merger

If you want to understand the rhythm of how this industry works, walk through any mid-tier producer's investor deck from early 2011. Production growth charts curving up and to the right. Exploration upside in eight countries. A "transformative" acquisition just closed. Now flip to that same producer's deck in 2014. The growth chart has flattened. The eight countries have become four. The "transformative" acquisition is referenced once, briefly, with an asterisk pointing to an impairment note. This isn't anomalous. It is the industry.

By late 2014, AuRico Gold was sitting in roughly that condition. It had a sprawling portfolio assembled during the boom, an underground mine in northern Ontario called Young-Davidson that was scaling up production, and a balance sheet that had seen better days. The market had stopped giving the company credit for any of its development assets. Its share price was a fraction of its 2011 peak. To shareholders, the company looked stuck.

On April 13, 2015, Alamos and AuRico announced what was described as a "merger of equals."[^5] The structure was elegant: each company's shareholders would end up owning approximately half of a combined entity, the AuRico royalty business would be spun out into a separate vehicle called AuRico Metals, and the new Alamos would emerge as a roughly $1.5 billion mid-tier with diversified production across Mexico and Canada.

Strip away the press-release language and what was actually happening was a takeover dressed in a merger's clothing. McCluskey would lead the combined company. The strategy, the culture, and the capital allocation discipline would be Alamos's. AuRico shareholders were essentially trading exposure to a struggling sub-scale operator for ownership in a more rationally-capitalized vehicle with a CEO who had spent a decade proving he could run mines for cash. AuRico shareholders ended up with the better long-term outcome despite holding what the market initially saw as the "cheaper" paper.

The strategic logic of the deal had three layers. First, jurisdictional diversification: Alamos was a single-country, single-asset Mexico story before AuRico. After, it had a meaningful Canadian footprint. Second, asset diversification: Mulatos was a heap-leach open pit; Young-Davidson was an underground mine using a sub-level cave method, fundamentally a different operating discipline. Third, scale: combined production crossed the threshold where institutional investors—pension funds, sovereign wealth funds, generalist asset managers—could write meaningful tickets.

But the prize, the asset that justified the whole transaction in retrospect, was Young-Davidson. Located in Matachewan, Ontario, on the site of a historical gold camp dating to the early 20th century, Young-Davidson was a long-life underground asset that had only just begun ramping toward its full production rate when the deal closed. The mine had decades of reserves. Its labor and power costs were Canadian-dollar denominated against a U.S.-dollar revenue line, which during the 2015-2020 period when the Canadian dollar weakened against the USD provided a substantial natural margin boost.

Within five years, Young-Davidson was generating mid-hundreds of millions of dollars in annual mine-site free cash flow, comfortably more than the entire purchase price implied by the AuRico share exchange.1 It became, in the team's own internal phrasing, "the ATM" of the portfolio—the asset that paid for everything else, including the next deal.

Did Alamos overpay in 2015? Reasonable analysts at the time said yes—they pointed to the price-per-reserve-ounce metric and grumbled that AuRico's portfolio had hidden liabilities. Reasonable analysts in 2025 looking back at the same deal say the opposite—they note that gold was at multi-year lows when the deal closed, that the team timed the cycle almost perfectly, and that Young-Davidson alone has more than justified the consideration paid. Both groups are looking at the same facts. The difference is time horizon.

The lesson Alamos drew from the deal was that the best M&A in mining happens when the rest of the industry is being marched to the woodshed. That conviction would set up the next deal—and the one that, by most accountings, became one of the greatest mining acquisitions of the modern era.

IV. The "Home Run" Deal: Richmont & Island Gold

Imagine the scene on the morning of September 11, 2017. Gold has been grinding higher through 2016 and into 2017 but is nowhere near the highs of 2011. The gold mining sector is in the early stages of a recovery, but most CEOs are still nursing balance sheets from the previous cycle's mistakes. M&A activity is muted. Then a press release crosses the wires: Alamos Gold has agreed to acquire Richmont Mines in an all-stock deal valued at approximately $770 million.2

The market's first reaction was not enthusiasm. Richmont, a Montreal-based junior with a single producing asset, had traded at high valuation multiples on a price-per-ounce basis for several quarters, supported by improving operational results. Acquiring it required Alamos to pay what looked like a full price during what looked like an early-cycle recovery. Sell-side analysts immediately started writing notes asking whether McCluskey had abandoned his vaunted discipline.

The asset at the center of the deal was Island Gold, an underground mine located near Dubreuilville in Ontario, north of Sault Ste. Marie. At the time of acquisition, Island Gold was producing modestly—a few thousand ounces per quarter, with reserves of around 1 million ounces at industry-respectable grades. To most observers, Richmont was being valued at a premium because of operational momentum, not because of any spectacular geological revelation.

Here's the part the market missed.

Island Gold sits in a steeply-dipping high-grade gold vein system that, based on early drill data, appeared to extend significantly down-plunge into rock that had not yet been adequately tested. Mining geologists call this "open at depth"—a phrase that hides one of the most consequential ambiguities in mining valuation. An asset that is "open at depth" might continue at grade for another 500 meters, or it might pinch out 100 meters below the deepest drill hole. Markets, on average, assign these uncertain extensions a fraction of the value they assign to drilled-out reserves. What Alamos believed, based on technical work that had been quietly accumulating, was that the down-plunge extension at Island Gold was not a maybe—it was a very high-probability yes.

History has vindicated that view emphatically. In the years following the acquisition, exploration drilling at Island Gold transformed the resource base. The mineral reserve grew from roughly 1 million ounces at the time of the deal to multiples of that figure, and the average reserve grade ticked higher as deeper drilling intersected progressively richer veins.[^7] The asset is now arguably the highest-grade, lowest-cost underground gold mine in Canada and one of the most economic ounces in the global development pipeline.

The company also committed to a major capital investment to extend the mine's life: the Phase III expansion, which involves sinking a new shaft to access the deeper, higher-grade ore at greater throughput than the existing decline-and-truck haulage system can support.[^7] Phase III is, in effect, the moment Alamos converts a great mine into a tier-one asset. When the shaft commissioning was completed and the ramp-up began, throughput rose materially, all-in sustaining costs dropped to among the lowest in the industry, and Island Gold's annual gold production stepped up to a level that put it in the top decile of Canadian underground mines.

The benchmarking exercise here is fun. Use the standard mining valuation metric of price per acquired reserve ounce—the way analysts compare deals across the industry. At the announced price, Alamos paid in the range of a few hundred dollars per ounce of Richmont's then-existing reserves. After Phase III commissioning and a multi-year drilling program, the implied price per ounce of total resource ended up being a tiny fraction of that initial number. Put differently, Richmont turned out to be one of the cheapest ounces ever bought in Canadian mining—and the market, in the days after the deal was announced, thought it was expensive.

What does this say about strategy? Three things. First, that the best M&A in mining isn't about buying ounces—it's about buying optionality. Reserves are a snapshot. Resource potential, particularly in proven mineralized systems, is a future. Second, that geological conviction is a real edge. The Alamos technical team had spent careful time on the Island Gold data before bidding. Third, that "the market thinks you overpaid" is sometimes the best confirmation that you didn't. If a deal looks obviously cheap to consensus, the seller wouldn't have sold.

And looming at the edge of this story, though nobody knew it yet, was a tiny piece of ground roughly two kilometers west of the Island Gold portal owned by a different company entirely—a piece of ground called Magino. We'll come back to that shortly. First, though, the story turns to the people who made all this possible.

V. Management Spotlight: The Owner-Operator Culture

If you spend any time in the mining industry, you start to notice a particular type of CEO. They tend to be from one of the major firms—Barrick, Newmont, AngloGold—where they spent thirty years climbing the operations ladder. They take the top job at a mid-tier, draw a multi-million-dollar salary, get a generous restricted-share grant tied to relative total shareholder return over three years, and then start thinking about what their next deal will look like in next year's annual report. Their personal shareholding in the company they run is rarely more than a year or two of salary. They are, in the language of academic finance, agents. They are not owners.

John McCluskey is not that.

McCluskey co-founded Alamos in 2003, took it public during the early years of the gold bull market, and has held the CEO seat for the entirety of the company's existence.3 His personal shareholding in Alamos, while precise figures fluctuate quarter-to-quarter, has consistently represented a meaningful multiple of his annual compensation—a level of skin-in-the-game that puts him in a different category from his peer-group CEOs at larger producers. When he sells a share, the market notices. When he buys, it notices more.

What's interesting is the way that ownership orientation shows up in the operating decisions. It's not that owner-CEOs are uniformly smarter than agent-CEOs. It's that they ask different questions. An owner-CEO asks "is this asset going to generate cash for fifteen years?" An agent-CEO asks "will this asset improve my quarterly production guidance?" In a long-cycle, capital-intensive business like mining, those two questions produce dramatically different decisions.

The compensation philosophy at Alamos reinforces this. The board's executive compensation framework, disclosed in successive management information circulars, has explicitly weighted per-share metrics—production per share, reserves per share, free cash flow per share—rather than gross production volume.1 This sounds like a footnote until you realize what it does to behavior. A CEO incentivized on gross production tonnage will favor large, dilutive acquisitions that grow the top line while shrinking what each existing shareholder owns. A CEO incentivized on per-share metrics will only do deals that are accretive to the existing owner. The compensation design alone explains a substantial portion of the divergence between Alamos and its peer group over the last decade.

The team around McCluskey has been remarkably stable. The CFO, the COO, the head of corporate development, the head of exploration—the seats have rotated less than at most peers, and the senior bench has been built largely through internal promotion. This is unusual in mining, where executive musical chairs across companies is the default. Long tenure has a few effects: institutional knowledge of the asset base is dense, cultural transmission across deals is high, and the team's mental model of "what we do and what we don't do" is shared without much active reinforcement.

The defining operational philosophy that came out of the McCluskey years is the "safe jurisdictions only" doctrine. Alamos does not operate in West Africa, despite the high grades available there. It does not operate in Central Asia. It does not operate in countries with histories of resource nationalism. The team has been explicit, in public conference calls and investor presentations, that they will not bid on assets in jurisdictions where the rule of law cannot be relied upon for a multi-decade project life.1

This costs them deals. There are higher-grade ounces sitting in the Sahel that they could acquire at a fraction of the per-ounce price of Island Gold. They have repeatedly declined. The doctrine is observable in their counterfactual decisions—what they didn't buy—as much as in what they did.

We'll see in the next section that even the safe-jurisdiction doctrine has its blind spots. Turkey, for the better part of a decade, looked safe. Then, suddenly, it didn't. The Alamos response to that surprise tells you almost everything you need to know about the company's risk culture.

VI. The Turkish Setback & Geopolitical Lessons

In the mining industry, there's a saying: the ore body doesn't care where the border is. You can find world-class deposits in countries that treat foreign capital as a partner and in countries that treat foreign capital as a piggy bank to be smashed when convenient. The challenge for management teams is not finding the ore; it is correctly forecasting which kind of country you are dealing with—and that forecast horizon, for a mine, is measured in decades.

For roughly a decade beginning in the early 2010s, Türkiye looked like a reasonable jurisdiction. It had a developing mining code, a track record of permitting foreign-owned projects, and—critically for Alamos—a known mineralized district near the Aegean coast called Çanakkale that hosted the Kirazlı Altın Madeni Projesi, the Kirazlı Gold Mine Project. Through a series of transactions in earlier years, Alamos had assembled a Turkish portfolio comprising Kirazlı and two adjacent development projects, Ağı Dağı and Çamyurt, with a combined resource base capable of supporting decades of production.[^3] The expected capital investment in Turkey was material. Permits, environmental approvals, and detailed engineering work had all progressed.

Then the wheels came off.

In the summer of 2019, a series of protests erupted in Çanakkale focused on Kirazlı's planned use of cyanide for gold processing and on the clearance of trees on the project footprint. Some of the imagery that circulated globally—aerial photographs of cleared forest land—was politically explosive. The Turkish government, which had been signaling continued support for the project, abruptly went silent on permit renewals. The operating license that allowed Alamos to continue site activities was not renewed when it expired. The company effectively could not proceed.

For two years, Alamos worked through diplomatic and commercial channels to restart the project. They engaged Turkish counsel. They communicated with senior government officials. They preserved the technical work. They also, critically, did something most companies in their position would not have done: they stopped pouring capital into the ground. The team made a decision to write down the carrying value of the Turkish assets and to fully accept that the project might be permanently stranded.

In 2021, after exhausting diplomatic avenues, Alamos filed a notice of dispute under the bilateral investment treaty between Canada and Türkiye, escalating the matter into formal investor-state arbitration at the International Centre for Settlement of Investment Disputes (ICSID). The claim was sized at over $1 billion in damages.4 Arbitration proceedings of this kind take years to resolve and are confidential in their substantive deliberations, but the public filings make clear that Alamos is arguing for the full investment-protection treaty remedy: compensation for the value of an investment effectively expropriated by state inaction.

The Turkish setback would have been an existential event for many mid-tier miners. A billion-dollar-plus development project effectively zeroed; years of management bandwidth diverted to a dispute; a public-relations narrative that could easily have spiraled into broader investor skepticism about the company's judgment. None of that happened at Alamos. Why?

Three reasons stand out. First, balance sheet strength. Alamos had managed its leverage conservatively through the cycle, and the company entered the Turkish crisis with net cash on the balance sheet rather than net debt. The impairment, while painful, did not threaten solvency or covenants. Second, asset diversification. Mulatos, Young-Davidson, and Island Gold continued producing through the Turkish crisis at attractive margins, and operating cash flow funded continued investment in Canada. Third—and this is more cultural than financial—the team's willingness to write a project down to zero rather than throw additional capital at a deteriorating situation. There is a phenomenon in capital allocation known as "throwing good money after bad," in which a sunk-cost-anchored team continues funding a failing project in the hope of recovering the original investment. The Alamos team simply did not do this.

The lesson Alamos drew from Türkiye was not "jurisdictions are unpredictable, therefore everything is risky." It was the more nuanced version: even in jurisdictions that appear safe at acquisition, you must structure the capital deployment to assume tail risks can materialize. A project should not be allowed to swallow more capital than the consolidated free cash flow can absorb without distress. This discipline became visible in subsequent capital allocation decisions, including, ironically, the very next big acquisition.

If you are looking for the philosophical hinge between the old Alamos and the new Alamos, the Türkiye experience is it. The doctrine that emerged—that even within "safe" countries, asset concentration risk must be managed deliberately—is the discipline that shaped the next decade of moves. And the next move, the Argonaut deal, was less a new direction than a doubling-down on the safest jurisdiction Alamos already knew.

VII. Hidden Business: The "Magino" Synergy & District Scale

For years, the most maddening fact in the Alamos corporate development team's life was the geographical accident of Magino. If you fly over Dubreuilville, Ontario at low altitude, you can see two separate mining complexes, each with its own surface infrastructure, its own access roads, its own mill or processing facility, its own headframe or portal. One is Island Gold. The other, sitting almost directly adjacent on a separately-staked land package, was Magino—owned not by Alamos, but by Argonaut Gold, a struggling mid-tier with operations in Mexico, Nevada, and Ontario.

Magino was, on paper, a viable operation. It was a large-tonnage, lower-grade open-pit and underground project with reserves measured in millions of ounces. Argonaut had spent years and a substantial amount of capital developing it, and the first gold pour occurred in mid-2023.[^10] But by late 2023, Argonaut was in trouble. The Magino capital build had run over budget. The company carried significant net debt. Its Mexican assets were generating less cash than expected. The market had stopped giving the company the benefit of the doubt, and the share price had collapsed.

This is the moment Alamos made its move. On March 27, 2024, the company announced an agreement to acquire Argonaut Gold in a transaction with an implied equity value of approximately $325 million, with Argonaut's Mexican and U.S. assets to be spun out into a separate vehicle (later named Florida Canyon Gold) and the Magino asset to be retained by Alamos.[^11] The pure-play Alamos consideration for Magino, after the spin, was the lowest implied price-per-ounce on a major Canadian asset acquisition in recent memory.

The market reaction was immediate and ambiguous. Argonaut's existing shareholders did the math on the spin structure and the implied Magino value and concluded that the deal undervalued their asset. Alamos shareholders looked at the Magino capital structure—particularly the residual debt being assumed—and asked whether the company was taking on integration complexity at exactly the moment it needed to be focused on Phase III commissioning at Island Gold.

Here's why the deal made sense, and why it was probably going to make sense regardless of what the headline price implied.

Magino's mill is approximately 10,000 tonnes per day of installed capacity. Island Gold's existing operations rely on a smaller mill running ore trucked from underground. When the Phase III expansion is fully ramped, Island Gold throughput will increase, and the existing mill will be a constraint. The synergy is geometric: stop running two mills in close proximity, route all ore to the larger and more modern Magino mill, and immediately reduce per-tonne processing costs while extending the operating life of the consolidated complex.

There's more. Both operations were paying for their own surface infrastructure—their own roads, their own power tie-ins, their own administrative complexes, their own warehousing, their own tailings management. By consolidating, the duplicated G&A and infrastructure can be eliminated. The labor force can be deployed more efficiently across the combined district rather than competing for the same skilled underground miners in a tight Ontario labor market.

Management has publicly quantified the expected synergies in the range of $515 million in net present value terms over the project life, encompassing operating, capital, and tax efficiencies from the combination.[^11] In an industry where claimed synergies routinely fail to materialize, the Magino-Island Gold case is unusual in one critical respect: the synergy is not based on combining management teams or systems, where most synergy programs disappoint. It is based on combining two pieces of physical infrastructure that sit in line-of-sight of each other. That kind of synergy actually shows up in the financial statements.

The strategic frame that management has wrapped around the combination is the "Integrated Island Gold District." The pitch is that what was formerly a single mine, even a great one, is now a multi-decade mining camp with the throughput, infrastructure, and exploration footprint to remain a tier-one producing asset for the better part of half a century. By global standards, very few gold districts can claim that combination of life, grade, cost profile, and jurisdictional safety.

There is, however, an integration risk that cannot be hand-waved away. Magino's mill needs to perform at design specifications on Island Gold's ore characteristics, which differ from Magino's open-pit feed. The transition from two operations to one requires reconfiguring underground haulage, tailings handling, and ore-blending strategies. The capital plan for the integration is multi-year. And the underlying assumption—that Phase III at Island Gold ramps according to schedule—remains a forward-looking projection rather than a realized outcome.

If the integration succeeds, what Alamos will have built is something that genuinely changes the company's profile within the global gold mining industry. It moves the company from "great mid-tier with good assets" to "owner of a top-decile global gold mine by cost profile." That is the prize. That is the trade. And as the next section explores, it is also the source of substantial framework-level competitive advantages that are not visible in any quarterly earnings report.

VIII. Playbook: Business & Investing Lessons

Now we get to the part of the episode where we put the company through the analytical frameworks—and where the picture sharpens from "this team has had a good run" into "here is the structural reason their run was likely, and likely to continue."

Start with Hamilton Helmer's 7 Powers framework, which organizes durable competitive advantage into seven categories. Two of them apply to Alamos with unusual force.

The first is Cornered Resource. A cornered resource exists when a firm has preferential access to something of value that competitors cannot replicate at any price. The classic example is a mineral deposit—you cannot manufacture a new Island Gold by spending more money on exploration in southern Ontario. The down-plunge extension at Island Gold is, in this sense, a literal cornered resource. There are not many high-grade, vein-hosted gold systems of that size and continuity remaining undeveloped in safe jurisdictions globally. The geology is what it is, the title is what it is, and as long as Alamos owns the property, no competitor can replicate it. After the Magino consolidation, the cornered-resource argument extends to district scale: the only way to be in this specific piece of ground at this specific cost profile is to own these specific titles.

The second is Process Power. Process power exists when a firm has internal operating practices that competitors cannot easily replicate. In Alamos's case, the relevant process is North American underground gold mining at scale, with low all-in sustaining costs, in a tight labor environment. The team has now spent over a decade refining its underground mining practices at Young-Davidson and Island Gold. The institutional knowledge—how to develop a long-hole stope safely and economically in this rock type, how to manage water and ventilation at depth, how to integrate exploration drilling into production planning—is not something a competitor can hire away in a single year.

Other Helmer powers apply less directly. There is no meaningful Network Economy in gold production—the marginal ounce sells into a globally fungible commodity market. Scale Economies exist but matter less for AGI than for the supermajors. Branding is irrelevant; gold buyers do not care about provenance to any economically meaningful degree. Counter-Positioning is mostly absent. Switching Costs are essentially nil for buyers of gold.

So the durable competitive advantage at Alamos reduces to two specific powers: ownership of specific high-quality ore bodies in specific jurisdictions, and the operating culture and capabilities to extract those ore bodies at industry-leading costs. Both are real. Both compound over time.

Now switch to Porter's Five Forces, which examines the competitive intensity of the industry. The gold producer industry has unusual dynamics. Buyer power is low to nil—gold trades in a deep, liquid market where individual producers are price-takers. Supplier power, by contrast, is meaningful and rising. The most relevant supplier in the underground mining business is skilled labor. Ontario's underground mining workforce is finite, aging, and increasingly competed-for by every operator and every infrastructure project. Wage inflation in this segment has run materially above general inflation for several years. Power and reagent costs—diesel, cyanide, electricity, steel for ground support—are commodities whose prices fluctuate with broader cycles. Threat of new entrants is moderated by the long timelines and high capital intensity of bringing a new mine into production; a deposit found today might pour first gold in eight to twelve years if everything goes well. Rivalry among existing competitors is fierce in M&A but largely irrelevant in product markets because the product itself is commoditized.

The most interesting Porter category for gold producers is Threat of Substitutes. For a generation, the implicit substitute for monetary gold was government bonds—until government bonds started trading at negative real yields. Now the more contested substitute is Bitcoin. The "digital gold" narrative has unquestionably siphoned some marginal flow from the traditional gold investment universe into cryptocurrencies. Whether that is structural or cyclical is one of the great open questions in macro investing. For Alamos and its peers, the implication is that the long-run gold price path is somewhat more uncertain than it was twenty years ago, even setting aside ordinary cyclical variation. Producers respond to this either by reducing operating leverage (Alamos's approach—lower costs, lower debt) or by maximizing operating leverage and hoping for a high-price denouement (a number of higher-cost peers).

Beyond the frameworks, the most important playbook lesson from the Alamos story is what we might call the Anti-Dilution Playbook. Most mining companies grow by issuing shares. Production rises, but so does the denominator. The investor's per-share ounces, per-share reserves, and per-share free cash flow grow much more slowly than the company's reported gross numbers. Alamos's share count has grown over the past decade, but at a rate that, when divided into the growth in production and reserves, has produced meaningful expansion in per-share metrics. The Argonaut deal is illustrative: at the announced price, the share issuance to Argonaut shareholders was modest relative to the resource brought in, and the per-share reserve and production growth was positive.[^11]

This is the discipline that, more than anything else, has separated AGI from the GDX index. The math of compounding per-share value through accretive, well-timed acquisitions over a 20-year horizon, in an industry of value-destroying acquisitions, produces the kind of outperformance we noted in the introduction. There is no secret. There is just relentless application of the discipline.

IX. Analysis & Bear vs. Bull Case

Every great investment thesis has a credible bear case alongside it, and you should be suspicious of any equity story whose bears can be dismissed in a sentence. Alamos has real bears, and their arguments deserve to be taken seriously.

The bear case begins with geographic concentration. After Magino, a very large share of Alamos's production, reserves, and forward free cash flow is concentrated in a single Canadian district. Young-Davidson is a separate operation in northern Ontario, but the center of gravity of the company is now Dubreuilville. Concentration creates exposures: any single permit issue, any single labor disruption, any single technical problem at the Island Gold-Magino complex can affect a meaningful fraction of consolidated production. The mitigation is that Ontario is a stable, well-understood mining jurisdiction with a long history of accommodating long-life operations. But the concentration is real.

The second bear-case pillar is integration execution. The Magino synergies are credible, but they are also forward-looking. The Phase III ramp at Island Gold is forward-looking. Bringing two physical operations into one consolidated complex requires reconfiguring underground haulage, surface infrastructure, water and tailings management, and labor allocation across what used to be two separate teams. In an industry where integrations routinely take longer and cost more than projected, the bear-case scenario is that the synergies materialize slowly and the period between deal closing and synergy realization sees compressed margins.

The third bear-case pillar is the Türkiye recovery. The $1 billion ICSID claim is a real asset on the balance sheet in the sense that it could deliver a material cash recovery—but the timeline is years, the outcome is uncertain, and even a favorable arbitration award must be enforced. In a scenario where Türkiye remains effectively a zero, the historical impairments are baked in but the upside option from arbitration disappears.

The fourth pillar is gold price exposure. Alamos's all-in sustaining cost structure positions it well in any plausible gold price environment, but the company is not immune to gold price risk. A sustained period of materially lower gold prices would compress margins industry-wide and would compress AGI's margins too, albeit from a higher starting point than most peers.

The bull case is the inverse of each of those pillars, plus a strategic option that the bear case does not weigh.

On geography, the bull view is that concentration in the best district you own is exactly what disciplined capital allocation is supposed to produce. The alternative—diversifying into less-attractive jurisdictions to reduce concentration—is precisely the value-destroying playbook that has crippled peers. Concentration in a top-tier asset in a stable jurisdiction is a feature, not a bug.

On integration, the bull view is that the synergies are based on physical infrastructure consolidation rather than corporate integration—a far easier kind of synergy to actually capture. Throughput improvements from sending all ore to a single larger mill, and unit cost reductions from eliminating duplicated surface infrastructure, are tangible engineering outcomes rather than spreadsheet exercises.

On Türkiye, the bull view notes that ICSID arbitration outcomes in cases of treaty-grade investor protection violations have historically been substantial, and that even a partial recovery would represent a material non-operating cash inflow against an already-impaired carrying value. The downside is bounded; the upside is real.

On gold prices, the bull view is structural: the post-2020 global macro environment, with elevated sovereign debt levels, persistent fiscal deficits in major developed economies, and central bank diversification toward gold reserves, has supported a higher gold price floor than prior decades. Alamos's cost structure means that even at modestly lower gold prices than today's, the company would continue generating substantial free cash flow.

And the strategic option that the bear case omits: Alamos as an acquisition target. The supermajors—Barrick Gold (now part of a different corporate combination), Newmont, Agnico Eagle—have growth challenges of their own. Newer ounces in stable jurisdictions are scarce. An ESG-acceptable, North-American, mid-tier producer with a cornered-resource asset like Island Gold is a logical target for a major looking to refresh its production base without the geopolitical risk of African or Central Asian acquisitions. We are not arguing that an acquisition is imminent. We are noting that the strategic optionality is non-zero and asymmetric: a takeout would deliver value to existing shareholders, while no takeout simply leaves the standalone thesis intact.

A word on myth vs reality. The consensus narrative around Alamos is "well-run mid-tier with good Canadian assets." The reality is more interesting: it is a North American gold consolidation vehicle whose cumulative capital allocation track record, on a per-share basis, has more in common with selective compounders than with typical mining peers. The "good mid-tier" framing systematically understates what the team has actually built. Conversely, the narrative occasionally attached to AGI by its biggest fans—that the team is uniformly brilliant and the next ten years will mirror the last—understates the integration risk and the gold-price beta the equity continues to carry.

For long-term fundamental investors, the two or three KPIs that matter most for tracking ongoing performance are straightforward. First, All-In Sustaining Cost (AISC) per ounce—the most important single metric in gold mining, capturing not just direct cash costs but sustaining capital and stay-in-business spending. Sustained downward trajectory in AISC, particularly through the Magino-Island Gold integration period, would be the strongest single signal that the strategic thesis is intact. Second, Reserve Replacement Ratio—the rate at which new reserves are added through exploration relative to mined depletion. Mining companies that consistently replace more than 100% of mined reserves are growing per-share value over time; those that don't are liquidating themselves slowly. Third, in this specific period, integration milestones at the Island Gold District: Phase III shaft commissioning, Magino mill throughput at full design rates, and synergy capture against management's $500 million-plus NPV target. These are not numbers an investor calculates from scratch; they are numbers a careful reader can extract from quarterly disclosures.

That's the analytical picture. Now to close the loop with the human one.

X. Epilogue

There's a certain kind of corporate story that doesn't lend itself to dramatic narrative. There was no founding garage. There was no almost-bankruptcy. There was no late-night decision to bet the company on a single product launch. The Alamos Gold story, instead, is the story of a CEO and a team who showed up to work for two decades, did the unglamorous things competently, declined the deals that didn't pencil, and compounded patient capital across cycles in an industry not famous for either patience or capital discipline.

John McCluskey was thirty-something when he started the company in 2003. He is, in 2026, still the CEO. He has watched gold trade from $300 to $2,500 and back to $1,000 and up to $3,000. He has seen peers acquired and disappear, seen entire mid-tier sub-sectors get reorganized through bankruptcy, seen the rise and fall of various "growth at any cost" doctrines and the executives who championed them.

The Alamos story is, more than anything else, an argument that in an industry of compounding capital destruction, the simple act of not destroying capital—year after year, deal after deal—produces, over a long enough horizon, an extraordinary divergence from the average.

Twenty years in, the question is whether the next decade looks like a continuation of the same patterns or like something different. The shape of the assets has changed: from a single Mexican heap-leach pad to a portfolio anchored on the highest-grade underground mine in Canada, with a consolidated district adjacent to it. The scale has changed: a single-asset junior is now a $10-billion-plus mid-tier with institutional ownership and global research coverage. The team has changed less than the assets have, which is, in management succession terms, the most important fact of all.

What hasn't changed is the operating doctrine. Safe jurisdictions. Low cost. Per-share accretion. Disciplined M&A timed to industry distress rather than industry euphoria. As long as those four principles continue to guide capital allocation, the patterns of the past twenty years are more likely than not to extend into the next several.

From a single mine in the Sonoran hills to the integrated production complex in northern Ontario, the journey describes a particular shape of leadership: patient, opportunistic when others are forced sellers, willing to walk away when geopolitics turns hostile, focused on the per-share number that ordinary mining executives rarely seem to remember exists. That shape of leadership is rare. It is, in the gold industry of the early 21st century, possibly unique. And it is the underlying reason a generation of patient shareholders found themselves, twenty years on, holding one of the more interesting compounders in a sector that has produced very few.

The next chapter of the Alamos story is unfolding now—at the Magino mill, in the deepening shaft at Island Gold, in the slow grind of arbitration in Washington, in the choices the team makes about what to acquire next and what to walk past. The framework for evaluating those choices, however, is already in place. Watch the AISC. Watch the reserve replacement. Watch the per-share metrics. Watch what they don't buy. The numbers and the absences will tell the story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube