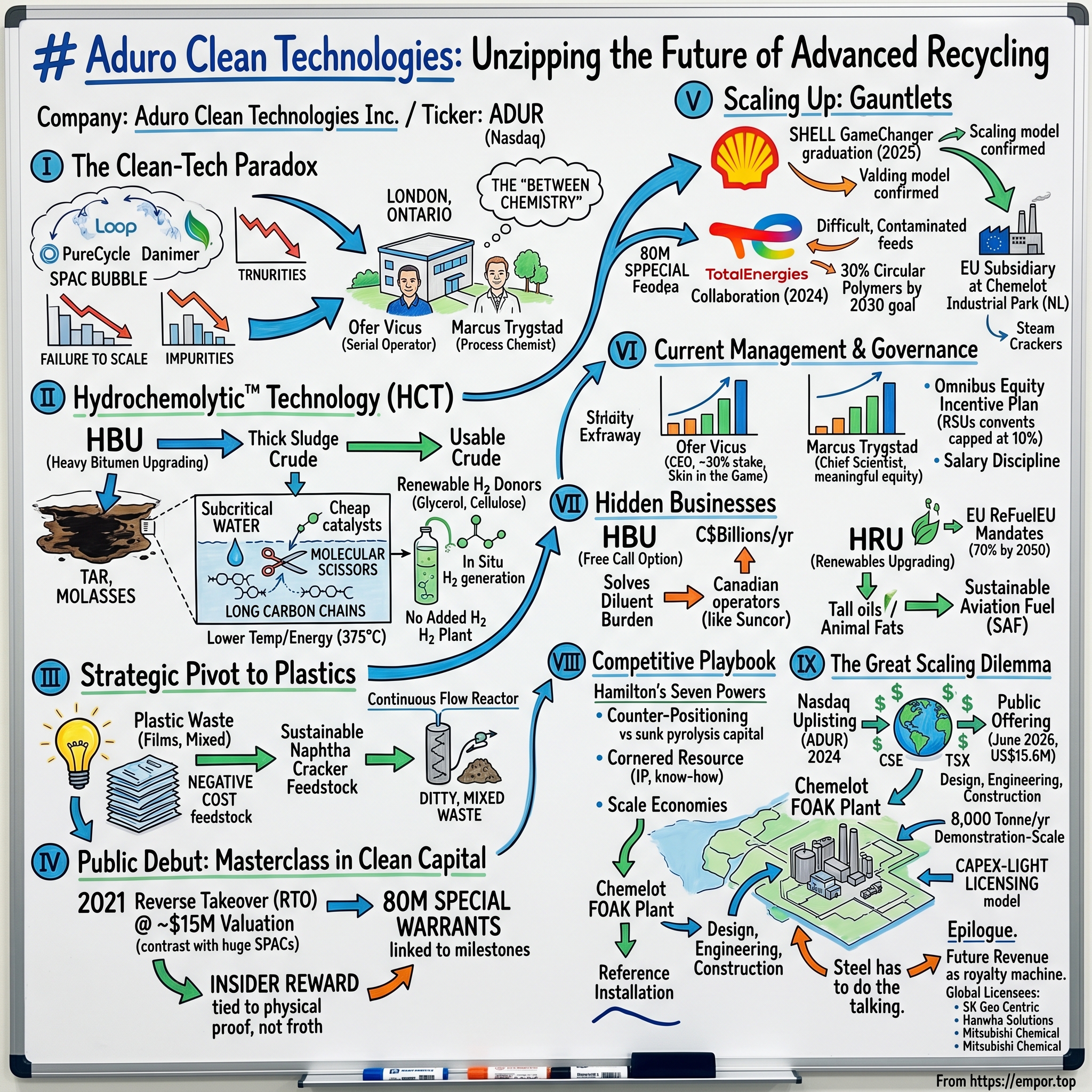

Aduro Clean Technologies: Unzipping the Future of Advanced Recycling

I. The Clean-Tech Paradox

Picture a graveyard of press releases. Between 2020 and 2022, the chemical recycling industry produced some of the most confident slide decks in the history of clean technology. Reactors that would devour the world's plastic waste. Factories that would turn yesterday's shampoo bottles into tomorrow's virgin-grade polymer. Billions of dollars of venture and SPAC capital chased the dream, and for a while the market believed every word. Then the reactors got built, the impurities showed up, the yields disappointed, and the share prices fell ninety, ninety-five, ninety-eight percent. Chemical recycling, it turned out, was easy to pitch and brutally hard to scale.

And yet, in a low-slung research building in London, Ontario — closer to Detroit than to Toronto — a tiny company was quietly running experiments that pointed in a different direction. Its core idea was almost heretical to an industry that had spent a century treating heat as the universal solvent of hydrocarbon chemistry. The heretics at Aduro Clean Technologies believed that the right tool for breaking down a stubborn carbon chain was not fire. It was water.

This is the story of how two men — Ofer Vicus, a serial operator, and Marcus Trygstad, a process chemist with more than three decades of refinery and analytical chemistry behind him — built what they called "the between chemistry": a way to sit subcritical water in between the brute-force worlds of high-temperature pyrolysis and high-pressure hydrogen addition, and use it to gently unzip the longest molecules humanity makes. It is also the story of a capital-markets decision that, in hindsight, may have been even more important than the chemistry. While their flashier peers were raising hundreds of millions through blank-check mergers at billion-dollar valuations, Aduro went public through a tiny Canadian reverse takeover at roughly a fifteen-million-dollar valuation, with two-thirds of management's shares handcuffed to operational milestones.

Over the next three and a half hours, we will trace Aduro's improbable arc: from a heavy-bitumen upgrader chasing the Alberta oil sands, to a NASDAQ-listed advanced recycling platform under the ticker ADUR. We will walk through the 2021 reverse takeover, the gauntlets run with Shell and TotalEnergies SE, the European foothold at the Chemelot industrial park in the Netherlands, and the capex-light licensing model that management hopes will turn Aduro into something like the ARM Holdings of chemical recycling — a company that designs the core and collects the royalty, rather than pouring concrete and operating plants itself.

A warning before we begin: Aduro is a pre-commercial company. As of its mid-2026 reporting it generated only token pilot revenue against meaningful cash burn.12 Almost everything that matters about this business lies in the future, which is precisely why understanding the founders' chemistry, their incentives, and their capital discipline matters more than any current income statement. Let us start where every good origin story starts: with a hard problem nobody could crack.

II. The "Between Chemistry" and the Founding Context

The hard problem, in the beginning, was not plastic at all. It was the thickest, ugliest, most valuable sludge in North America: Albertan heavy bitumen.

To understand what drew Ofer Vicus and Marcus Trygstad together around 2008 — and led them to incorporate Aduro Energy in late 2011 — you have to understand what bitumen does to chemists. Conventional crude oil flows. Bitumen, the tar-like hydrocarbon that saturates Alberta's oil sands, barely moves at room temperature; it has the consistency of cold molasses or roofing tar. The molecules are enormous, tangled, and contaminated with sulfur, nitrogen, and heavy metals. For decades the industry had exactly two tools to make this material usable, and both were sledgehammers.

The first sledgehammer is heat. In thermal cracking — the family of processes that includes pyrolysis and coking — you simply cook the hydrocarbon at temperatures north of 500°C until the long molecules shatter into shorter ones. It works, but it is indiscriminate. Cooking that hot produces large quantities of coke and char (think of the burnt crust at the bottom of a forgotten pan) and a chaotic soup of unstable molecules that have to be cleaned up downstream. The second sledgehammer is hydrogen. In hydroprocessing, you inject molecular hydrogen gas under extreme pressure to "cap" the broken carbon chains and stabilize them. The chemistry is cleaner, but the hydrogen is brutally expensive, energy-intensive to produce, and itself a major source of carbon emissions. Either way, upgrading bitumen has always been a multi-billion-dollar, capital-crushing endeavor reserved for giants.

Trygstad's career had been spent in and around exactly these processes — the analytical and process chemistry of petroleum, the slow art of figuring out what a molecule is actually doing inside a reactor. His core insight, the one the whole company would eventually be built on, was deceptively simple and physically profound: water, when you push it toward its critical point, stops behaving like ordinary water and becomes a chemically aggressive, almost solvent-like medium.

Here is the layman's version. We think of water as inert — the thing you dissolve other things in. But raise water to high temperature and pressure, below the extreme threshold where it turns fully "supercritical," and its personality changes. Its hydrogen-bonding network loosens. It becomes more willing to react, to donate and accept atoms, to participate in chemistry rather than just host it. In this subcritical state — at moderate temperatures under 375°C rather than the 500°C-plus of pyrolysis — water paired with cheap, simple metal catalysts can act less like a hammer and more like a pair of molecular scissors. It finds the weak points in a long carbon chain and snips them, cleanly.

That is the "between chemistry": operating in the temperature and pressure window between gentle and brutal, where water does the work that fire and hydrogen used to do. Aduro branded the platform Hydrochemolytic™ Technology, or HCT. The name is a mouthful, but it encodes the trick — "hydro" for water, "chemolytic" for chemical splitting.

There was still one elegant problem to solve. When you snip a long hydrocarbon, you create reactive fragments — molecular loose ends — that desperately want to recombine into tar and coke unless something stabilizes them. The conventional answer is to flood the reaction with that expensive molecular hydrogen. Aduro's answer was its quietest stroke of genius: instead of piping in costly $H_2$, HCT uses cheap, renewable hydrogen donors — molecules that carry hydrogen and willingly hand it over inside the reactor. Glycerol, the low-value waste byproduct of biodiesel production, is one. Cellulose from agricultural waste is another. The reaction generates hydrogen in situ, exactly where and when it is needed, capping the broken chains cleanly without the company ever having to buy a hydrogen plant.

Step back and appreciate the architecture of the idea. Lower temperature than pyrolysis means less energy and less char. No added hydrogen means no enormous capital and carbon burden. Cheap waste-derived donors mean the stabilizing chemistry is nearly free. On a whiteboard in 2011, it was beautiful. The problem, as the founders were about to discover, was that beautiful chemistry and a fundable business are two very different things — and the bitumen market was about to teach them that lesson the expensive way.

III. The Strategic Pivot to Plastics

For roughly seven years, from incorporation in 2011 toward the end of the decade, Aduro ran headlong into what we might call the bitumen wall.

The wall was not technical. The chemistry kept working in the lab. The wall was financial and structural. Building a bitumen upgrader in Western Canada is not a startup activity; it is a sovereign-scale infrastructure project, the domain of integrated giants like 선코어 Suncor Energy and Canadian Natural Resources (CNRL), companies that measure capital budgets in the billions and timelines in decades. For a lab-stage company with a clever catalyst and a thin balance sheet, the path from a benchtop autoclave to a commercial oil-sands installation was effectively un-fundable. You cannot ask a venture investor to write a check that only pays off after you have built a refinery unit alongside one of the most conservative industries on earth. Aduro was starved of the very thing it needed: a market that could absorb its technology in bite-sized, capital-light pieces.

Then came the reframing — the kind of lateral leap that, in retrospect, looks obvious and, in the moment, looks like a betrayal of everything you have been building. The founders looked again at the molecules in waste plastic. Polyethylene, polypropylene, polystyrene: the workhorses of single-use packaging. And they realized that the long hydrocarbon chains in these polymers are, chemically speaking, cousins of the heavy fractions in bitumen. Same essential problem — carbon chains too long and too stable to be useful — just arriving from a different direction. If subcritical water and a hydrogen donor could unzip bitumen, there was no fundamental reason they could not unzip a polyethylene bag.

The implications were enormous. Plastic waste is not a multi-billion-dollar refinery project. It is a distributed, regulation-driven, almost embarrassingly abundant feedstock that municipalities and waste handlers are often willing to pay you to take away. The economics flip: instead of competing against Suncor's balance sheet, Aduro could ride a global circular-economy mandate, with feedstock that frequently carried a negative cost. The same chemistry, pointed at a market that actually wanted a small, modular, licensable solution.

So the company pivoted its center of gravity from Hydrochemolytic Bitumen Upgrading — the original HBU vision — toward Hydrochemolytic Plastic Upcycling, internally the plastics application of the platform. Critically, the founders did not throw the bitumen work away; they shelved it as optionality, a point we will return to. But the spotlight, the scarce R&D dollars, and the corporate identity all swung toward plastics.

That pivot created a deep engineering challenge that would consume the next several years. Lab chemistry happens in batch — you load a small sealed autoclave, run the reaction, open it up, and see what you got. A real recycling business happens in continuous flow — waste goes in one end, product comes out the other, around the clock, reliably, with messy real-world feedstock that is never pure. Bridging that gap is where most clean-tech dreams quietly die. It is one thing to unzip a clean, lab-grade polymer pellet; it is another to feed your reactor a slurry of contaminated, mixed municipal plastics — the films, the colors, the food residue, the labels — and still get a stable, high-yield product out the other side.

Aduro's answer was its continuous reactor program, developed through successive pilot units. The goal was to prove that HCT could ingest genuinely dirty, mixed waste plastic and produce a high-quality, stable paraffinic oil — the kind of intermediate that a petrochemical plant could actually use. Proving continuous operation on contaminated feedstock was the hinge on which the entire investment case would turn, because it is exactly the step where the celebrated competitors would later stumble. But before Aduro could fund that proof, it had to do something its peers were doing in spectacularly more expensive ways: go public.

IV. The Public Debut: A Masterclass in Clean Capital Deployment

In the spring of 2021, the clean-tech capital markets were a casino at peak euphoria, and Aduro walked in and quietly bought the cheapest chip on the table.

On April 28, 2021, Aduro Energy completed a reverse takeover into a tiny listed shell, Dimension Five Technologies Inc. (CSE: DFT), pursuant to a securities exchange agreement originally struck in October 2020.67 The mechanics were classic small-cap Canadian plumbing: the shell acquired all of Aduro's shares and convertible notes, the company did a 3-for-1 share consolidation, renamed itself Aduro Clean Technologies, and resumed trading on the Canadian Securities Exchange under the ticker ACT on April 29, 2021.67 The implied valuation was modest — on the order of fifteen million dollars. Not fifteen billion. Fifteen million.

To appreciate how radical that restraint was, you have to remember what the neighbors were doing. This was the absolute zenith of the clean-tech SPAC bubble. PureCycle Technologies, which proposed to purify waste polypropylene with a solvent-based process, came public via blank-check merger at a valuation north of a billion dollars. Loop Industries, a depolymerization play, had at its peak commanded a market capitalization well above half a billion. Danimer Scientific, a bioplastics maker, briefly carried a multi-billion-dollar valuation. The pattern was identical across the cohort: enormous capital raised on the strength of a pitch, before a single commercial-scale plant had been proven.

And then physics arrived. PureCycle wrestled with mechanical scaling and feedstock-impurity problems at its flagship Ironton, Ohio facility, missing milestone after milestone. Loop Industries absorbed delays and a withering short-seller report that questioned its core yields. Danimer's volumes and economics disappointed. By 2022 and 2023 the entire clean-tech SPAC wave had collapsed into one of the more complete episodes of value destruction in recent market history — companies that had raised hundreds of millions trading for pennies on the dollar of their former glory.

Here is why Aduro's path was structurally brilliant rather than merely lucky. First, by going public cheaply, Aduro raised modest amounts and preserved its cash and, crucially, its ownership structure — it did not light hundreds of millions on fire trying to scale before the science was ready. Second, and this is the part worth dwelling on, the deal was built around roughly 80 million special warrants alongside the base shares.7 These were not ordinary securities. They converted into common shares only upon the achievement of defined development milestones in the Aduro business — meaning a large share of the equity that founders and insiders stood to receive was locked behind actually building and validating the technology.7

Think about the incentive that creates. In the SPAC model, the reward came at the moment of the deal — insiders were enriched the day the merger closed, before the hard engineering was even attempted. In Aduro's model, the reward came at the moment of proof — insiders were enriched only as continuous-flow reactors got built and third-party validation arrived. The structure aligned management's personal wealth with the physical reality of the technology rather than with the froth of a valuation. It is the difference between paying a contractor when they show you the blueprint and paying them when you can stand inside the finished house.

For a long-term fundamental investor, this is the single most important cultural fact about Aduro's early life. The company chose, at the height of a bubble, to be valued like a science project rather than a story stock — and in doing so it inoculated its capital structure against the dilution and disillusionment that vaporized its peers. That discipline is what bought it the time and credibility to walk into the offices of the world's largest energy companies and ask them to put HCT through their own wringers.

V. Scaling Up: The Shell and TotalEnergies Gauntlets

There is a particular kind of validation that money cannot buy and a press release cannot fake: the moment a hundred-billion-dollar energy company assigns its own scientists to try to break your technology, and they fail to.

Aduro got the first of these in late 2022, when Shell selected the company for its GameChanger program — a highly selective accelerator through which the energy major identifies early-stage technologies with the potential to decarbonize and advance, and then subjects them to its own technical scrutiny and non-dilutive support.4 For a company Aduro's size, being chosen was itself a signal; but the GameChanger program is not a grant you cash and forget. It is a multi-year process in which Shell's chemists vet your claims, probe your data, and stress-test your engineering assumptions stage by stage.

The payoff came on December 16, 2025, when Aduro announced it had successfully graduated from the program.3 The substance behind the headline is what matters. Under the collaboration — run within Shell's chemical decarbonization innovation call — Aduro applied HCT to produce sustainable naphtha cracker feedstock from waste polyethylene and polypropylene, processed both separately and as a mixed stream.3 Naphtha is the lifeblood intermediate of the petrochemical industry: it is what "steam crackers," the enormous furnaces at the heart of every chemical complex, break down to make the building blocks of new plastic. If your recycled output can be fed straight into a cracker, you are not making a degraded, downcycled material — you are making a drop-in substitute for fossil naphtha. That is the holy grail of circularity.

Just as important, Shell's involvement provided external validation of Aduro's process-design model, giving third-party confidence in the engineering scale-up pathway — from continuous-flow reactor, to a Next Generation Process pilot plant, to a future demonstration plant targeted at roughly 8,000 tonnes per year of input capacity.3 In plain terms: an oil major's engineers looked at Aduro's math for how this scales and said the math holds. For a sector littered with companies whose lab results never survived contact with industrial scale, that endorsement is the difference between a curiosity and an investable platform.

If Shell was the technical audit, TotalEnergies was the torture test. In July 2024, after positive preliminary evaluations, Aduro entered a new, formal R&D collaboration phase with TotalEnergies SE.5 The focus was deliberately nasty: not clean, sorted plastic, but the most contaminated, "difficult-to-recycle" material — waste streams with high concentrations of polyolefins blended with polyurethane, metals, and other challenging contaminants.5 These are precisely the feedstocks that destroy conventional pyrolysis reactors, fouling catalysts and choking equipment with char. The collaboration's goal was to establish process parameters for managing these variable, hard-to-recycle feedstocks, optimize the process design, and lay the groundwork for a commercial process — with TotalEnergies providing both financial and in-kind support, including access to its technical resources.5 The strategic prize for Total is concrete: the company has committed to producing 30% circular polymers by 2030, and it needs technologies that can handle the ugly two-thirds of the waste stream that pristine processes reject.5

The choice of where to scale all this was its own strategic statement. Rather than building in Canada, Aduro planted its European flag at the Chemelot industrial park in Sittard-Geleen, in the southern Netherlands — announcing in May 2024 that it would establish a European subsidiary there.9 Chemelot is not a generic business park; it is one of Europe's largest integrated petrochemical clusters, home to steam-cracking capacity, shared utilities, and the Brightlands open-innovation campus, where Aduro had been active since 2021.9 Embedding inside that ecosystem put Aduro's reactors within arm's reach of the exact customers — the crackers — that would consume its output, inside the regulatory bloc that most aggressively mandates circular content. It was the geographic equivalent of opening your store inside your biggest customer's lobby. And it set the stage for the most consequential siting decision the company would make, which we will come to. First, though, we should meet the people steering all this — and examine just how much of their own net worth rides on it.

VI. Current Management and Governance: Skin in the Game

Acquired listeners know the pattern: the best founder-led companies are the ones where the people making the decisions would personally feel a catastrophe in their own bank accounts. By that test, Aduro is about as aligned as a public company gets.

Start with the chief executive. Ofer Vicus, co-founder and CEO, holds an enormous personal stake in the company he started — a holding reported in the range of roughly 29% to 31% of the common shares depending on the filing and the moment, worth, on any given day, the overwhelming majority of his net worth.1011 This is not a hired-gun CEO with a sliver of options and a golden parachute. This is a man whose financial life is the company. He also exercises voting influence beyond his direct holdings through a voting trust arrangement covering additional shares, which has the effect of stabilizing long-term governance and insulating the company from the short-term pressures that can derail a pre-revenue science platform.11 Whether you view concentrated founder control as a feature or a risk depends on your temperament, but there is no ambiguity about alignment: Vicus does not get rich unless the technology gets commercialized.

Beside him is Marcus Trygstad, co-founder and principal scientist — the chemist whose subcritical-water insight is the intellectual bedrock of the entire platform. Trygstad holds a meaningful equity position of his own, supplemented by a substantial pool of stock options.1011 The structure of those options is the tell: by sitting much of his compensation in equity-linked instruments whose value only materializes if the share price appreciates, Aduro ties its chief scientist's payoff directly to scientific milestones translating into commercial value. The man who controls the catalyst recipes has every reason to keep making them better.

The incentive architecture around the broader team reflects the same philosophy of restraint. Equity grants flow through the company's 2022 Omnibus Equity Incentive Plan, under which options and RSUs are capped at 10% of outstanding shares — a meaningful guardrail against the silent dilution that erodes so many early-stage shareholders.10 Cash compensation, meanwhile, has been kept conspicuously lean for a company that now trades on a major U.S. exchange. Vicus's base salary climbed only as the company hit hard milestones — rising from a token six-figure level in the early days to a still-modest figure as Aduro reached its NASDAQ listing — a trajectory that ties even the cash side of pay to demonstrable corporate progress rather than to titles.13 In an industry where pre-revenue executives have routinely paid themselves like Fortune 500 chieftains, Aduro's salary discipline is a quiet but real signal of where the founders think the money should go: into reactors, not paychecks.

Rounding out the execution layer are two figures whose roles map neatly onto the company's two current obsessions — finance and Europe. CFO Mena Beshay has shepherded the capital-markets evolution, including the uplisting to the NASDAQ Capital Market under ADUR and, in May 2026, the company's additional listing on the Toronto Stock Exchange — the financial groundwork that connects a once-obscure CSE micro-cap to global institutional liquidity.14 And chief revenue officer Eric Appelman, who joined in September 2023, has driven the European commercial push — the offtake conversations and partnership scaffolding that a licensing business will ultimately live or die by.15 In early 2026 the company further reinforced that European bench, appointing a senior operations manager dedicated to the continental scale-up.16

A team this aligned and this disciplined is exactly what you want in a company whose value is almost entirely optionality. And optionality, it turns out, is the literal structure of Aduro's business — because beneath the plastics story sit two other businesses the market barely prices at all.

VII. The "Hidden" Businesses: HBU and HRU

Here is a fact that frustrates analysts and intrigues long-term investors in equal measure: Aduro reports as a single operating segment, with only minimal pilot-stage revenue, because by the accounting definition it does just one thing.12 But that single chemistry platform points at three radically different markets, and the financial statements give you no help in valuing two of them. They are, for now, invisible — call them the hidden businesses.

The first hidden business is the one the company was born to do: Hydrochemolytic Bitumen Upgrading, HBU — the original application, shelved but never abandoned. To understand the prize, you need one piece of pipeline trivia. Alberta's heavy bitumen is too thick to flow through a pipeline on its own. To move it, producers must blend it with roughly 30% diluent — typically condensate, a light, expensive hydrocarbon that does nothing but reduce viscosity so the goo will travel. The producers buy the diluent, ship it hundreds of kilometers to the oil sands, mix it in, pay to transport the diluted blend, and then often pay to separate it out again at the other end. It is one of the great hidden taxes of the Canadian energy patch.

HBU's pitch is to reduce bitumen's viscosity chemically, on-site, without the diluent — using the same gentle subcritical-water chemistry to partially upgrade the crude so it flows on its own. The aggregate value at stake is staggering: eliminating or reducing the diluent burden could, in principle, save Canadian operators like Suncor or Imperial Oil on the order of billions of Canadian dollars a year in combined diluent purchases and transport costs. For Aduro, this is a dormant, multi-billion-dollar licensing option sitting on the shelf — one it is not actively funding today, but one whose value would be enormous if plastics proves the platform and a major ever decides to pick up the phone. It is the kind of asset a fundamental investor should treat as a free call option: probably worth nothing for years, potentially transformative if it ever rings.

The second hidden business may have a faster fuse. Hydrochemolytic Renewables Upgrading, HRU, points the same chemistry at low-value bio-feedstocks — bio-oils, tall oils (a byproduct of paper pulping), and animal fats — and upgrades them into Sustainable Aviation Fuel and renewable diesel. SAF is one of the most policy-driven markets on earth right now, and the policy is unusually hard and unusually European. Under the EU's ReFuelEU Aviation regulation, fuel suppliers at EU airports must blend a rising share of SAF into conventional jet fuel — starting at 2% in 2025, climbing to 6% by 2030, and reaching 70% by 2050.17 That is not a voluntary target or a corporate aspiration; it is a legally binding demand floor that grows every year, with no near-term way for the industry to meet it at the volumes required.

When you legislate demand faster than supply can grow, you create exactly the pricing environment in which a flexible, feedstock-agnostic upgrading technology can command premium licensing terms. HRU is, in effect, the platform's growth-stage adjacency — riding a regulatory tailwind that is already law rather than hoping for one to materialize. Notice the through-line across all three businesses: plastics, bitumen, renewables. In every case, Aduro takes a low-value, messy, long-chain hydrocarbon nobody else wants to handle gently, and uses water chemistry to turn it into something valuable. One platform, three markets, two of them effectively free on today's balance sheet. The question for the competitive analyst is whether anyone can copy it — and that is where the moats come in.

VIII. The Competitive Playbook: Porter's Five Forces and Hamilton's Seven Powers

Let us war-game this business the way an Acquired episode should — coldly, through two frameworks, asking not "is the technology cool" but "is the position defensible."

Start with Michael Porter. On the bargaining power of suppliers, Aduro sits in an almost enviable spot: its feedstock is waste plastic, and the economics of waste run backwards from a normal supply chain. Municipalities and waste handlers frequently pay operators to take material off their hands through tipping fees, which means the input can carry a negative cost. Suppliers of garbage have essentially no pricing power over a company that solves their disposal problem. That is about as favorable as the supply side of an industry ever gets.

On the threat of substitutes, the picture is more contested, and honesty requires acknowledging it. The incumbent substitute is conventional pyrolysis — the high-heat approach that the bulk of today's "advanced recycling" capacity uses. Pyrolysis is real, it is deployed, and it is the default. But it carries the very weaknesses Aduro was designed to avoid: it tends to produce high volumes of toxic char, and a lower-quality pyrolysis oil that needs intensive downstream hydrotreatment before a cracker will accept it, especially when the input is contaminated. So substitutes exist, but they are arguably inferior on exactly the dimensions — contamination tolerance and product quality — that the regulatory endgame rewards. Rate this a medium threat, not a low one; pyrolysis has incumbency and installed capital on its side.

On the bargaining power of buyers, the customers are some of the most powerful companies in the world — Dow, Shell, BASF, the global petrochemical majors who would be Aduro's offtakers and licensees. In a vacuum, that concentration would be terrifying for a small supplier. But buyer power here is checked by the same regulatory machine driving the SAF market: EU and global circular-content mandates are forcing these giants to source recycled feedstock whether they like it or not. When your customer is legally required to buy what you make, the negotiating table tilts back toward the middle. We will not belabor the remaining two forces — rivalry is intense across a crowded recycling landscape, and barriers to entry are high given the capital and validation required — but the supplier and buyer dynamics are the ones that genuinely shape Aduro's economics.

Now the more interesting lens: Hamilton Helmer's Seven Powers, which asks not whether a position is good today but whether it is durable.

The primary power, and the most elegant, is counter-positioning. The incumbents in advanced recycling have collectively committed enormous capital — hundreds of millions of dollars — to pyrolysis reactors and the thermal-cracking infrastructure around them. That sunk investment is a cage. A pyrolysis operator cannot simply bolt on a subcritical-water process; the two approaches are fundamentally different in equipment, conditions, and chemistry. To adopt Aduro's model, an incumbent would have to decommission and write off the very assets it just built and financed — a move that punishes the executives who championed pyrolysis and torches shareholder capital. So the incumbents are structurally disincentivized from copying Aduro even if HCT proves superior. That is counter-positioning in its textbook form: the leaders cannot follow without harming their existing business.

The second power is a cornered resource in the form of intellectual property. Aduro holds a portfolio of global patents over the Hydrochemolytic platform, and the deepest moat is harder to file than to patent: Trygstad's accumulated know-how about which catalyst combinations, in which subcritical-water conditions, actually deliver clean, high-yield results. Recipes like that are notoriously difficult to reverse-engineer from the outside. The patents are the visible fence; the tacit chemistry is the part competitors cannot see.

The third power is prospective rather than proven: scale economies flowing from the capex-light licensing model. If Aduro designs and licenses the catalytic reactor cores rather than building and operating plants itself, then each incremental deployment carries little marginal cost to Aduro while adding a high-margin royalty stream. In theory, margins expand as the install base grows — the ARM Holdings dynamic. The honest caveat: this power does not exist yet. It is an architecture, not an achievement, and it depends entirely on the company reaching commercial scale. Which brings us to the final act, and the great open question of the whole story.

IX. The Great Scaling Dilemma: NASDAQ Uplisting and the Path Forward

Every clean-tech story eventually arrives at the same cliff edge, the place where the SPAC darlings fell: the leap from a validated pilot to a first commercial-scale plant. Aduro is now standing at that edge, and it has spent the last eighteen months methodically assembling a rope.

The first piece was access to capital. In November 2024, Aduro uplisted to the NASDAQ Capital Market under the ticker ADUR, graduating from the obscurity of the Canadian Securities Exchange to the deepest pool of institutional capital in the world.1019 For a company whose entire strategy depends on funding a capital project, an exchange listing that global institutions can actually own is not cosmetic — it is the gateway. The company reinforced that footing in May 2026 by adding a Toronto Stock Exchange listing, broadening its investor base on both sides of the border.14

The second piece was the money itself. In June 2026, Aduro executed an underwritten public offering, closing on June 11 with the issuance of 1,028,645 common shares at US$15.20 (C$21.20) each, for gross proceeds of roughly US$15.6 million, with Canaccord Genuity acting as sole bookrunning manager.12 The pricing announcement the prior day had paired the public offering with a concurrent private placement of up to US$7.17 million, and the company subsequently filed an amended LIFE offering document as the financing wrapped up.118 The use of proceeds was stated plainly and tellingly: the net proceeds are earmarked for the design, engineering, and construction of a First-of-a-Kind demonstration-scale industrial plant, alongside ongoing R&D and general corporate purposes.2

That FOAK plant is the whole ballgame, and in January 2026 Aduro answered the question of where it would rise: the Chemelot industrial park, the same Dutch petrochemical cluster where the company had been incubating since 2021.8 The siting decision followed a structured campaign that narrowed multiple candidates to four finalists before landing on Chemelot for its utilities, its proximity to regional steam-cracking capacity, its feedstock access, and its alignment with European circular-economy regulation.8 Recall the demonstration plant's target scale from the Shell graduation — on the order of 8,000 tonnes per year of input — and you can see the shape of the bet: not a giant commercial mega-plant, but a credible, industrial-scale proof that the continuous process holds at size.3

And here is the strategic heart of it, the thing that separates Aduro's endgame from the waste-management roll-ups it is often lumped with. Aduro does not want to be a recycler. It does not want to own hundreds of plants, manage thousands of tons of garbage logistics, or carry the capital and operating burden of a heavy industrial footprint. The FOAK plant is a means, not an end — a reference installation that proves the technology so the company can sell the technology. The intended business model endpoint is capex-light licensing: engineer the core catalytic reactor cores, license HCT to others, and collect high-margin royalties from petrochemical companies and waste giants around the world. The aspirational customer list spans the globe's circular-economy ambitions — from South Korea's SK지오센트릭 SK Geo Centric and 한화솔루션 Hanwha Solutions to Japan's 三菱ケミカル Mitsubishi Chemical — players who would rather license a proven core than invent their own.

The dilemma in the section's title is real, and a fundamental investor should sit with it. To prove a capex-light model, Aduro must first spend capital — the FOAK plant is, unavoidably, a heavy expenditure undertaken to escape heavy expenditure forever after. Execution risk lives entirely in this one building: the same first-of-a-kind step where PureCycle and others discovered that continuous operation on real-world feedstock is far harder than the pilot suggested. If the Chemelot plant runs as the pilots and the oil-major validations imply it should, Aduro converts a decade of chemistry into a royalty machine. If it stumbles, it joins the graveyard of press releases we opened with. There is very little middle ground.

X. Epilogue and Playbook Lessons

What should a long-term investor actually carry away from Aduro's story so far?

The first lesson is about capital discipline in clean-tech, and it is the cleanest natural experiment the sector has offered. Two cohorts of recycling companies went public at roughly the same moment. One cohort raised hundreds of millions at billion-dollar valuations through SPACs, paid insiders at the deal rather than at the proof, and was largely destroyed when physics caught up with the slide decks. The other cohort — in this telling, a cohort of one — went public through a tiny reverse takeover at a fraction of the valuation, locked two-thirds of management's shares behind operational milestones, and preserved the capital structure that would let it survive long enough to be validated by Shell and TotalEnergies. The lesson is not that RTOs beat SPACs as a matter of mechanics; it is that aligning insider reward with physical proof rather than with the moment of financing is the single best predictor of who survives a hype cycle.

The second lesson is the engineering one, and it is almost philosophical: water versus fire. The entire incumbent industry reached for the hammer — extreme heat, or expensive hydrogen under extreme pressure — to break down hydrocarbons. Aduro reached for the scissors: subcritical water and cheap catalysts operating in the gentle space between the brutal options, with renewable hydrogen donors generating stabilizing hydrogen in place. If that approach scales, it will be a reminder that in mature industries the biggest breakthroughs often come not from more force, but from a more elegant mechanism that the incumbents are structurally unable to adopt.

Which leaves the one thing every Aduro investor must watch, the handful of KPIs that will tell the story before any income statement does. Above all, track the FOAK demonstration plant at Chemelot — its construction progress against budget and timeline, and once running, its sustained uptime and yield on genuinely contaminated, mixed feedstock. That single metric is the hinge on which counter-positioning, the licensing model, and the entire valuation turn. Secondarily, watch the conversion of the Shell and TotalEnergies relationships and the broader pipeline into signed, royalty-bearing licensing or offtake agreements — the moment validation becomes revenue. Everything else, including the dormant HBU and HRU optionality, is a call option that only pays off if those two things go right first.

The FOAK plant in Chemelot will be the ultimate validation. If the scaling works — if dirty plastic goes in one end and cracker-ready feedstock comes out the other, continuously, at industrial scale — then Aduro's quiet, water-based heresy could become the standard chemical operating system for the circular economy. If it does not, it will be a cautionary footnote about how even the most disciplined capital structure and the most elegant chemistry must, in the end, answer to the reactor. The chemistry has done its talking. Now the steel has to.

References

-

Aduro Clean Technologies Announces Pricing of US$15.64 Million Underwritten Public Offering and Concurrent Private Placement of up to US$7.17 Million — GlobeNewswire, 2026-06-10 ↩↩

-

Aduro Clean Technologies Announces Closing $15.54 Million Underwritten Public Offering — GlobeNewswire, 2026-06-11 ↩↩

-

Aduro Clean Technologies Graduates from Shell GameChanger Program — GlobeNewswire, 2025-12-16 ↩↩↩↩

-

Aduro Selected for Shell GameChanger Program — GlobeNewswire, 2022-11-03 ↩

-

Aduro Clean Technologies Enters New Phase of Collaboration with TotalEnergies — GlobeNewswire, 2024-07-30 ↩↩↩↩

-

Aduro Clean Technologies Inc. closes transaction with Aduro Energy and fundamental change under Policies of CSE — Gowling WLG, 2021 ↩↩

-

Dimension Five Technologies Inc. Announces Execution of Definitive Agreement for Acquisition of Aduro Energy Inc. — Aduro Clean Technologies, 2020 ↩↩↩↩

-

Aduro Clean Technologies Selects Chemelot Industrial Park for First-of-a-Kind Industrial Plant — Nasdaq, 2026-01-29 ↩↩

-

Aduro Clean Technologies to Establish European Subsidiary at Chemelot — Aduro Clean Technologies, 2024-05-15 ↩↩

-

Aduro Clean Technologies Inc. Form 6-K (FY2026 financial statements) — SEC, 2026 ↩↩

-

Form 6-K: Strategic Corporate and Executive Updates — SEC, 2024-03-12 ↩

-

Aduro Clean Technologies to Commence Trading on the Toronto Stock Exchange — GlobeNewswire, 2026-05-26 ↩↩

-

Aduro Clean Technologies Welcomes Eric Appelman as Chief Revenue Officer — GlobeNewswire, 2023-09-12 ↩

-

Aduro Clean Technologies Appoints Senior Operations Manager for European Scale-up — Aduro Clean Technologies, 2026-02-18 ↩

-

Sustainable Aviation Fuels — EASA (European Union Aviation Safety Agency), 2026 ↩

-

Aduro Clean Technologies Announces Filing of Amended and Restated LIFE Offering Document Following Closing of Public Offering — GlobeNewswire, 2026-06-15 ↩

-

Aduro Clean Technologies Investor Relations Homepage — Aduro Clean Technologies, 2026-06-16 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube