ADT: The Story of America's Original Home Security Company

I. Introduction and Episode Roadmap

There is a blue octagon that hangs on the front of roughly six million American homes. It does not light up. It does not connect to WiFi. It does not stream video to a smartphone. And yet, for over a century, that little blue sign has been one of the most recognized symbols in American residential life, a quiet declaration that this house is protected. The company behind it, ADT, is the oldest and largest home security provider in the United States, pulling in more than five billion dollars in annual revenue and monitoring more homes than any competitor by a factor of three.

But behind the familiar yard sign lies one of the strangest corporate odysseys in American business. ADT started life in 1874 as a telegraph messenger company, decades before the telephone existed. It survived antitrust rulings, conglomerate acquisitions, a spectacular fraud scandal that put its parent company's CEO in prison, a leveraged buyout that loaded it with nine billion dollars of debt, and the emergence of a Silicon Valley insurgent whose founder was rejected on Shark Tank before selling to Amazon for over a billion dollars.

The central paradox of ADT is striking. Here is a company with brand recognition that most consumer businesses would kill for, a recurring revenue model that generates hundreds of millions in monthly cash flow, and a customer base that has been growing since the Ulysses S. Grant administration. And yet the stock trades around eight dollars a share. Private equity has owned it for nearly a decade. A billion-dollar insurance partnership fizzled. An eight-hundred-million-dollar solar acquisition was written off almost entirely. The company carries more than seven billion dollars in long-term debt.

How did a telegraph company become synonymous with home security? Why has one of the most recognized brands in America struggled to create value for shareholders? And can a hundred-and-fifty-year-old company reinvent itself in the age of Ring doorbells, Google Nest, and Amazon Alexa? The answers reveal something fundamental about the nature of brand power, the limits of financial engineering, and why the innovator's dilemma is not just a theory but a lived experience for millions of homeowners and the companies that serve them.

This is a story with heroes and villains, brilliant strategies and catastrophic miscalculations, and a central question that applies to every legacy business watching a wave of digital disruption approach: When your greatest strength, the thing that made you dominant for a century, becomes the thing that holds you back, what do you do?

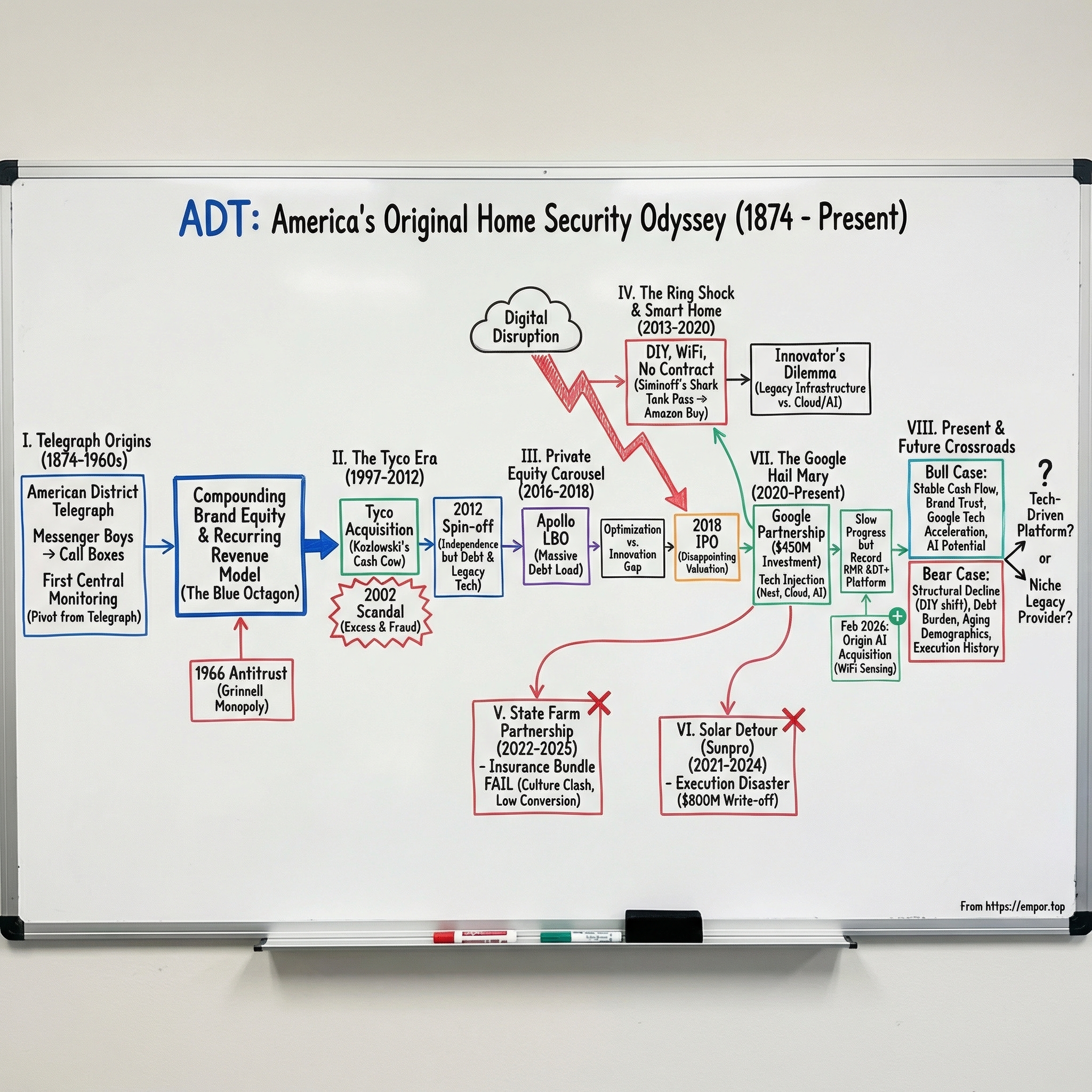

II. The Telegraph Origins: American District Telegraph (1874-1960s)

The year was 1874. Alexander Graham Bell had not yet patented the telephone. Thomas Edison was still tinkering with the telegraph. And in New York City, an inventor named Edward A. Calahan had a problem to solve. Calahan had already made his name inventing the stock ticker in 1863, the device that transmitted stock exchange prices over telegraph lines and transformed Wall Street. But his next innovation came from a more personal place. The president of Gold and Stock Telegraph Company, the firm that commercialized Calahan's stock ticker, was awoken one night by a burglar breaking into his home. The experience shook him, and Calahan saw an opportunity.

What if you could wire homes to a central station using telegraph technology, allowing residents to summon help at the push of a button? Calahan installed his first system in that executive's home and then wired fifty neighboring residences to a central monitoring station, creating the first residential security network in American history. On August 14, 1874, the American District Telegraph Company was formally incorporated in Baltimore, consolidating fifty-seven district telegraph delivery companies from cities across the eastern seaboard into a single entity.

The original business model was elegant in its simplicity. ADT installed "call boxes" on street corners and in private residences. A customer could activate the box to summon a messenger boy, who would then carry a message wherever it needed to go. Think of it as the Uber of the 1870s, except instead of a car, you got a teenager on foot. But the call boxes quickly evolved. Improved models allowed customers to send differentiated signals, one for the police, another for a doctor, a third for the fire department, a fourth for a coach. The central station could identify the type of emergency before dispatching help. This was, in essence, the first 911 system, predating the actual 911 service by nearly a century.

As the telephone rendered messenger services obsolete through the early twentieth century, ADT did something that most companies of its era failed to do: it pivoted. Rather than clinging to the telegraph, ADT leaned into what its network was really good at, connecting homes and businesses to centralized monitoring stations. By the 1890s, the company had begun transitioning to telephone-based systems and pioneered the first central station monitoring centers, enabling round-the-clock remote oversight of alarms. By the 1940s, ADT had developed the first automated burglar alarm and the first automated fire alarm system, with threats reported directly to ADT's monitoring centers.

This pivot established the template that would define the company for the next eighty years: install hardware in a building, wire it to a central station, charge a monthly fee for monitoring, and respond when something goes wrong.

The recurring revenue model that Wall Street would later obsess over was not a creation of modern financial engineering. It was baked into ADT's DNA from the beginning. And that model had a beautiful characteristic: once a system was installed, the customer was almost certain to keep paying month after month, year after year. Moving to a new home? You needed a new system installed. Renovating? The alarm company had to come back. The switching costs were physical, not just contractual. The alarm panel on your wall, the sensors on your doors and windows, the wiring behind your drywall, all of it was ADT's. Leaving ADT meant ripping out the infrastructure and starting over with someone new. For most homeowners, the monthly fee was simply easier to keep paying than the hassle of switching.

But ADT's dominance eventually attracted scrutiny. In 1953, Grinnell Corporation acquired a seventy-six percent controlling stake in ADT's stock. Grinnell also owned controlling interests in Automatic Fire Alarm Company and Holmes Electric Protective Company. Together, these affiliates controlled a staggering eighty-seven percent of the accredited central station protective service market in the United States, with ADT alone holding seventy-three percent. It was a monopoly by any definition, and the Justice Department came calling. In 1966, the Supreme Court ruled in United States v. Grinnell Corp. that Grinnell and its affiliates had achieved monopoly power through unlawful and exclusionary practices, ordering divestiture.

Three years later, the conglomerate ITT acquired Grinnell, bringing ADT along as part of the package. Then in 1976, a small company called Tyco Laboratories purchased the spun-off Grinnell fire protection division, beginning a relationship that would define ADT's next three decades.

The antitrust saga deserves a moment of reflection because it reveals something essential about ADT's market position. Even in 1966, long before the modern home security industry existed in its current form, ADT controlled nearly three-quarters of the professional monitoring market. That dominance was not built through aggressive marketing or technological superiority. It was built through sheer longevity and the compounding advantage of being first. When you have been installing alarm systems in American homes since the Grant administration, you accumulate a customer base that is extraordinarily difficult to dislodge. Each new generation of homeowners grew up seeing the ADT sign on their neighbors' lawns, creating a default preference that no amount of competitor advertising could easily overcome.

By the time ADT reached its centennial, the company had transformed from a telegraph messenger service into the dominant player in American security, with a brand built not on advertising but on a century of presence in American neighborhoods. That brand equity, accumulated over generations, would prove to be both ADT's greatest asset and, eventually, its most dangerous source of complacency. The question that would haunt ADT for the next fifty years was whether legacy market position built on analog infrastructure could survive the transition to a digital, software-defined world.

III. The Tyco Era: Roll-Up Strategy and Massive Expansion (1997-2012)

By the mid-1990s, ADT had been operating as an independent publicly traded company, growing steadily but not spectacularly in the fragmented security industry. Then Dennis Kozlowski entered the picture. Kozlowski was the CEO of Tyco International, a company he was transforming from a modest New Hampshire manufacturer into one of the largest conglomerates on earth through an aggressive acquisition strategy. Kozlowski believed in buying companies with strong cash flows, integrating them tightly, and using the combined earnings to fuel the next acquisition. ADT, with its millions of subscribers generating predictable monthly revenue, was the perfect target.

The courtship began with drama. In December 1996, Western Resources, which held a twenty-seven percent stake in ADT, launched a hostile takeover bid of approximately three and a half billion dollars, offering twenty-two dollars and fifty cents per share. ADT's management rejected it as a lowball offer and went looking for a white knight.

They found one in Kozlowski. On March 17, 1997, Tyco swooped in with a friendly bid of approximately five point six billion dollars, roughly twenty-nine dollars per share in stock, a massive premium over the hostile bid. The deal closed in July 1997, and ADT became a subsidiary of Tyco International. It was a classic white knight rescue: ADT's board traded one corporate suitor for another, preserving management continuity and gaining a parent company with deeper pockets and broader ambitions.

Under Tyco, ADT became the conglomerate's cash cow, and understanding why requires grasping what made the monitoring business so attractive. When a customer signed a three-to-five-year monitoring contract, they were essentially committing to a stream of payments that was almost impossible to cancel. Breaking a contract meant paying a hefty termination fee. And unlike most consumer subscriptions, home security monitoring was psychologically sticky in a way that a gym membership or streaming service was not. People would cancel Netflix before they would cancel the service that protected their family while they slept. The monitoring revenue was beautifully predictable. Cancellation rates were low, and the monthly fees flowed with the reliability of a utility bill.

Kozlowski understood this better than most. He used ADT's cash flow, along with revenue from Tyco's other divisions, to finance an ever-expanding empire that eventually encompassed electronics, healthcare, fire protection, and undersea fiber optic cables. The strategy was elegant in theory: acquire companies with predictable cash flows, lever them up, use the combined earnings to acquire more companies, and watch the stock price rise as the conglomerate's reported earnings grew. At its peak, Tyco was doing forty billion dollars in annual revenue and was one of the most valuable companies on the New York Stock Exchange. Wall Street analysts compared Kozlowski to Jack Welch. The comparison would prove apt, though not in the way anyone intended.

Then it all came apart. In 2002, Manhattan District Attorney Robert Morgenthau began investigating Kozlowski and Tyco CFO Mark Swartz for systematic looting of the company. The details that emerged were almost comically excessive.

Kozlowski had taken approximately two hundred and seventy million dollars from Tyco's key employee loan program and used two hundred and forty-two million of those funds for personal expenses. The spending became the stuff of corporate scandal legend: a six-thousand-dollar shower curtain, a two-million-dollar birthday party for his wife on the island of Sardinia featuring an ice sculpture of Michelangelo's David urinating Stolichnaya vodka and a two-hundred-and-fifty-thousand-dollar private Jimmy Buffett concert. There were fourteen million dollars in Monet and Renoir paintings, fifteen-thousand-dollar dog umbrella stands, and luxury properties from Nantucket to Boca Raton. The sheer excess made Kozlowski the poster child for early-2000s corporate greed, alongside Enron's Jeffrey Skilling and WorldCom's Bernie Ebbers.

The first trial ended in a mistrial after a juror was allegedly threatened. The second trial, concluding on June 17, 2005, resulted in convictions on twenty-two counts of grand larceny, securities fraud, falsifying business records, and conspiracy. The jury found Kozlowski and Swartz guilty of stealing a hundred and fifty million dollars from Tyco and making another four hundred and thirty million through stock price manipulation. Kozlowski received a sentence of up to twenty-five years.

For ADT, the scandal was simultaneously devastating and irrelevant. Devastating because the parent company's stock collapsed and the Tyco brand became toxic. Irrelevant because the blue octagon on six million American homes had nothing to do with Dennis Kozlowski's shower curtain. ADT's customers kept paying their monthly bills. The monitoring centers kept operating. The brand, built over more than a century, proved remarkably resilient to corporate malfeasance at the holding company level.

But the aftermath shaped ADT's future in important ways. In the years following the scandal, Tyco's new management concluded that the conglomerate structure was destroying value. On September 28, 2012, Tyco completed a three-way split into ADT Corporation (the North American residential and small business security operation), Tyco International (fire protection and security, later acquired by Johnson Controls for twenty billion dollars), and a flow control business that merged with Pentair. ADT was finally independent again, for the first time since the 1990s.

The spin-off was supposed to be a liberation. Free from the conglomerate, ADT could focus entirely on home security, invest in technology, and compete with the new wave of competitors that were beginning to emerge. Naren Gursahaney, the executive tapped to lead the newly independent ADT, spoke optimistically about the company's ability to accelerate innovation and pursue growth strategies that had been constrained under the Tyco umbrella.

But independence came with baggage. ADT inherited a debt-heavy balance sheet, aging technology infrastructure, and a business model built for the pre-smartphone era. The company's technology stack ran on proprietary hardware and landline connections. Its customer interaction model was built around a technician visiting your home, not an app on your phone. Its product development process moved at the pace of a manufacturing company, not a software company. Most critically, the fifteen years under Tyco had been a period of optimization, not innovation. ADT had been managed as a cash cow, milked to fund Kozlowski's empire and then cleaned up after the scandal. The investment in next-generation products and capabilities that should have occurred during the 2000s, when the smartphone was being invented and cloud computing was emerging, never happened.

The security industry was about to undergo its most disruptive decade, and ADT was entering it with one hand tied behind its back. What the company needed was a patient, well-capitalized owner willing to invest for five to ten years in technological transformation. What it got instead was private equity.

IV. The Private Equity Carousel Begins: Apollo Takes ADT Private (2016)

By 2015, the home security landscape had shifted dramatically from the world ADT had dominated for decades. Cable companies like Comcast and AT&T were bundling basic home security into their triple-play packages, offering customers monitoring for a few dollars a month as an add-on to their internet and TV subscriptions. Meanwhile, a new breed of DIY competitors was emerging. SimpliSafe, founded in 2006 by Chad and Eleanor Laurans while at Harvard Business School, had proven that consumers would enthusiastically adopt a self-installed security system with no long-term contracts. Ring, launched in 2013, was turning the humble doorbell into a connected security device. The message from the market was clear: the days of paying a technician to hardwire sensors into your walls and then locking into a three-year contract were numbered.

Enter Apollo Global Management, one of the largest and most aggressive private equity firms in the world, founded by Leon Black, Marc Rowan, and Josh Harris. Apollo had built its reputation on contrarian bets in distressed and out-of-favor assets, and ADT fit the profile perfectly: a dominant brand in a disrupted industry, trading at a valuation that reflected the market's skepticism about its future.

On February 16, 2016, Apollo announced it would acquire ADT for forty-two dollars per share in cash, a fifty-six percent premium over the prior closing price, valuing ADT's equity at approximately six point nine billion dollars. The total transaction value, including debt, approached fifteen billion. Apollo merged ADT with Protection 1, a smaller home security company it had acquired the prior year, creating the industry's undisputed giant with a combined subscriber base that dwarfed all competitors. The deal closed on May 2, 2016, and ADT went dark from public markets.

The private equity playbook for ADT was familiar. Apollo loaded the company with leverage, financing the deal with approximately one point six billion in first-lien term loans and three point one billion in second-lien financing. They consolidated operations, cut costs, rationalized the dealer network, and invested selectively in technology upgrades. The thesis was straightforward: ADT's brand was an underappreciated asset, the recurring revenue model was a cash flow machine, and with proper management, the company could modernize while maintaining its market position.

But the execution revealed the fundamental tension at the heart of every private equity turnaround of a legacy business. The debt service consumed capital that could have been invested in technology. The cost-cutting improved margins but did nothing to address the structural challenges of an installation-heavy business model in an increasingly DIY world. And the clock was ticking: Apollo needed an exit, and exits require growth stories.

That exit came faster than many expected. On January 19, 2018, less than two years after going private, ADT returned to public markets in an IPO that raised approximately one point five billion dollars. But the offering was widely characterized as disappointing. ADT priced at fourteen dollars per share, well below the initial target range of seventeen to nineteen dollars. The underwriters, led by Morgan Stanley and Goldman Sachs, cut the number of shares offered from a hundred and eleven million to a hundred and five million. Apollo retained roughly eighty-five percent ownership, maintaining control while extracting cash.

The IPO price told a story that the prospectus could not fully convey. Investors were skeptical about ADT's ability to compete in a world where a Ring doorbell camera cost two hundred dollars and came with no monthly commitment, while ADT's professional installation ran hundreds of dollars with a three-year contract at forty-five to sixty-five dollars per month. The S-1 filing was a revealing document: it showed a company generating substantial recurring revenue but spending aggressively on subscriber acquisition, carrying enormous debt, and facing competitive threats from every direction. The financial profile was that of a utility, but the competitive environment was that of a technology market in the midst of disruption. Investors could not figure out which analogy to apply, and in that uncertainty, they applied the less generous one.

The stock would never trade significantly above its IPO price. Apollo, for its part, conducted multiple secondary offerings in subsequent years, selling blocks of hundreds of millions of dollars in ADT shares and gradually reducing its stake. By mid-2025, Apollo held approximately a hundred and eighty-four million shares, continuing its slow exit. By most estimates, Apollo earned roughly a three-times return on its original equity investment, a respectable outcome for the private equity firm but one that came largely from financial engineering rather than fundamental value creation. For public shareholders who bought in at the IPO, the returns would be negative for years to come.

The Apollo chapter of ADT's story illustrates a tension that pervades private equity ownership of businesses facing secular disruption. The PE model is designed to buy, optimize, and exit within a defined timeframe, typically five to seven years. Genuine technological transformation of a legacy business takes a decade or more. These timelines are fundamentally incompatible. Apollo did not destroy ADT, but neither did it position the company to thrive in the emerging competitive landscape. It extracted returns for its fund investors, left ADT with substantial debt, and returned it to public markets still grappling with the same strategic challenges it faced when Apollo first knocked on the door.

V. The Ring Shock and Smart Home Revolution (2013-2020)

In 2013, a serial entrepreneur named Jamie Siminoff walked onto the set of Shark Tank with a product he called the Doorbot, a Wi-Fi-enabled video doorbell he had built in his garage. The pitch was simple: see and speak to whoever is at your door from your smartphone, anywhere in the world. The Sharks were unimpressed. Kevin O'Leary made a lowball offer that Siminoff declined. The other Sharks passed entirely. It was one of those Shark Tank moments that becomes famous not for the deal that was made but for the one that was missed.

Siminoff went back to his garage, rebranded the product as Ring, and attracted a group of investors that included Shaquille O'Neal and Richard Branson. The company tapped into something that ADT's leadership had failed to recognize: security was becoming democratized. For a hundred years, protecting your home required a professional assessment, professional installation, and a professional monitoring contract. Ring said you could do it yourself, for a fraction of the cost, and your smartphone would be the monitoring center.

On February 27, 2018, Amazon acquired Ring for approximately one point one billion dollars, its second-largest acquisition at the time after Whole Foods. The deal validated the DIY security model and sent a chill through every executive suite in the traditional alarm industry.

Amazon was not just buying a doorbell company. It was buying a beachhead into the American home, a distribution channel for its Alexa ecosystem, and a data source that would inform everything from package delivery to neighborhood safety apps. Consider the strategic brilliance: every Ring doorbell sold was a sensor on a front door that fed data back to Amazon's cloud. Every Ring camera was a node in a neighborhood surveillance network. Every Neighbors app notification was a touchpoint that kept customers within the Amazon ecosystem. Ring quickly became the dominant video doorbell brand, capturing an estimated forty-seven percent market share and serving as the entry point for millions of consumers into the smart home security ecosystem.

The Shark Tank irony was not lost on the industry. Kevin O'Leary had offered Siminoff a deal that valued the company at roughly seven hundred thousand dollars. Amazon paid over a billion. It was perhaps the most expensive pass in Shark Tank history, and it illustrated something important about innovation timing: sometimes the market is not ready for an idea until a massive platform company sees the distribution opportunity that a panel of individual investors cannot.

The implications for ADT were profound and worth dwelling on, because they illustrate the anatomy of disruption in a way that is almost textbook.

Ring's business model was the inverse of everything ADT had built. Where ADT charged over a thousand dollars for professional installation, Ring products could be mounted with a screwdriver in fifteen minutes. Where ADT locked customers into three-year contracts at forty-five to sixty-five dollars per month, Ring offered optional monitoring at around twenty dollars per month with no contract. Where ADT's technology was proprietary and closed, Ring integrated seamlessly with Amazon's Alexa, other smart home devices, and the Neighbors app that crowdsourced neighborhood safety information.

The asymmetry was not just in pricing. It was in the entire customer experience. Buying a Ring device meant going to Amazon.com, clicking a button, waiting two days for delivery, and spending fifteen minutes on installation. Buying an ADT system meant calling a sales number, scheduling an in-home consultation, waiting for a technician visit, enduring a multi-hour installation, and signing a thick contract. In a world where consumers expected instant gratification, ADT's process felt like buying a car when the competitor was selling a bicycle.

And Ring was not alone. Google was building its own ecosystem around Nest, which it had acquired in 2014 for three point two billion dollars, starting with smart thermostats and expanding into cameras, doorbells, and home speakers. Apple had HomeKit, its framework for smart home device integration that allowed third-party devices to be controlled through Siri and the Apple Home app. SimpliSafe continued to grow rapidly, backed by private equity and eventually acquired by GTCR in 2025, with its no-contract, self-installed systems appealing to exactly the younger demographic that ADT was struggling to attract. Even Wyze, a company that made cameras for twenty dollars, was eating into the market from the ultra-low end, proving that acceptable security hardware could be produced at price points that made ADT's equipment costs look absurd.

The traditional alarm companies were being encircled by technology giants with effectively unlimited capital and software expertise that legacy security firms could not match. But the encirclement was more subtle than a direct assault. Amazon, Google, and Apple were not trying to replace ADT. They were making ADT irrelevant by turning home security into a feature of a broader smart home ecosystem rather than a standalone service requiring a dedicated provider. When a consumer set up an Amazon Echo, a Ring doorbell, a smart lock, and a few cameras, they had a functional security system without ever thinking of themselves as buying "home security." The category was being unbundled, not disrupted in the traditional sense.

ADT's response was a series of partnerships and acquisitions that revealed both the urgency and the difficulty of its position. The company tried building its own smart home platform, acquiring smaller technology companies, and launching updated product lines. But the cultural gap between a hundred-and-forty-year-old alarm company and a Silicon Valley startup was enormous. ADT's technology stack was built on proprietary hardware and on-premise servers. Its product development cycles moved in quarters and years, not weeks and months. Its engineering talent was concentrated in hardware and monitoring operations, not software and AI. The mobile app, the primary interface between a modern security company and its customers, was widely regarded as clunky and outdated compared to Ring's intuitive design.

In August 2020, ADT struck what it hoped would be a game-changing partnership with Google. The tech giant invested four hundred and fifty million dollars for a six point six percent stake, and the two companies announced a long-term strategic alliance to integrate Google Nest hardware and AI capabilities into ADT's offerings. The deal was an implicit admission: ADT could not build the technology itself. It needed a partner who could. Whether that partnership would prove transformative or merely cosmetic would become one of the defining questions of ADT's next chapter.

VI. The State Farm Partnership: A Billion-Dollar Disappointment (2022-2025)

In September 2022, ADT announced what appeared to be a masterstroke of strategic thinking. State Farm, the largest property and casualty insurer in America, would invest one point two billion dollars for an approximately fifteen percent stake in ADT. The deal closed on October 13, 2022, with State Farm purchasing roughly a hundred and thirty-three million shares at nine dollars per share. State Farm also committed up to three hundred million dollars in additional funding for product development, technology innovation, customer growth, and marketing.

The strategic rationale was compelling on paper. Insurance companies have a powerful incentive to reduce claims, and monitored home security systems demonstrably reduce the likelihood of burglary, fire damage, and water damage. If State Farm could offer its policyholders a discount on insurance premiums in exchange for subscribing to ADT's monitoring service, both companies would win. State Farm would pay fewer claims. ADT would gain access to State Farm's enormous customer base of roughly seventy million policies. The homeowner would get cheaper insurance and a professionally monitored security system. It was the kind of vertical integration play that business school case studies are made of.

In practice, the partnership struggled from the start. The integration challenges were substantial, and they illuminate a dynamic that recurs whenever two large organizations with different DNA attempt to collaborate.

State Farm is a mutual insurance company, owned by its policyholders, with a culture built around actuarial precision and risk-averse decision-making. Its employees think in terms of loss ratios, policy retention, and regulatory compliance. Decisions move through layers of committee review. ADT was a private-equity-backed technology company trying to transform itself in real time. Its culture was shaped by quarterly earnings pressure, sales targets, and the urgency of competing against nimble startups.

The two organizations operated on different timescales, with different incentive structures, and with fundamentally different relationships to their customers. State Farm's agents are trusted advisors who manage policies across years and decades. ADT's dealers are salespeople who install a system and move on. The notion that these two organizations could seamlessly hand off customers between each other proved far too optimistic.

Privacy concerns also complicated matters. Sharing customer data between an insurance company and a security monitoring firm raised questions that neither organization had fully thought through. Would State Farm use ADT's monitoring data to adjust premiums? Would ADT share information about alarm activations with the insurer? The regulatory and reputational risks of data sharing in a post-Cambridge Analytica world made both organizations cautious, which further slowed integration.

The numbers told the story most starkly. Over roughly three years, the State Farm partnership generated only about thirty-three thousand new ADT subscribers. For context, ADT has more than six million existing customers and adds hundreds of thousands through its dealer network annually. Thirty-three thousand subscribers from a billion-dollar partnership backed by the largest insurer in America was, by any measure, a failure to launch. The insurance discount of two to fifteen percent on homeowners premiums proved insufficient to motivate mass adoption of a thirty-five to fifty dollar monthly monitoring commitment through the insurance channel.

By the third quarter of 2025, the partnership was effectively wound down. State Farm was left holding shares worth significantly less than its nine-dollar purchase price, with ADT trading around seven to eight dollars. The unrealized loss on the equity investment alone exceeded a hundred and fifty million dollars, to say nothing of the additional hundreds of millions committed to marketing and development.

The failure of the State Farm partnership contained a lesson that went beyond ADT. The concept of bundling home security with insurance was sound. Plenty of data showed that monitored homes experienced fewer burglaries and lower fire damage, translating directly into fewer insurance claims. The math should have worked. But the execution exposed a reality that strategic partnerships between large, dissimilar organizations consistently demonstrate: alignment of incentives on a PowerPoint slide does not translate into alignment of organizations, cultures, and customer journeys.

Consider the customer journey. A State Farm policyholder renewing their homeowners insurance encounters an offer for an ADT discount. The potential savings amount to perhaps a hundred dollars per year on their insurance premium. To capture that savings, they need to agree to a security system installation, schedule a technician visit, sign a multi-year monitoring contract costing five hundred to seven hundred dollars annually, and integrate new hardware into their home. The friction in that conversion path was enormous, and the incentive, a hundred-dollar insurance discount, was nowhere near large enough to motivate the behavioral change required. The insurance distribution channel, which seemed like a shortcut to millions of new subscribers, instead produced a trickle that could not justify the capital invested.

VII. The Google Hail Mary (2020-Present)

On August 3, 2020, ADT and Google announced a partnership that represented ADT's most ambitious bet on technological transformation. Google invested four hundred and fifty million dollars through a private placement, receiving newly created Class B shares representing six point six percent of ADT's outstanding equity. The Class B shares carried all the economic rights of common stock but could not vote on director elections, giving Google a financial stake without governance control. Each company committed an additional hundred and fifty million dollars, totaling three hundred million in combined funding for co-marketing, product development, technology, and employee training.

The strategic logic cut both ways, and understanding both sides of the equation is important for assessing whether the partnership can succeed.

For ADT, Google offered something it desperately needed: modern technology. Google Nest's hardware, including cameras, doorbells, speakers, and thermostats, was consumer-grade in quality and design, a massive upgrade from ADT's aging proprietary equipment. Google's cloud infrastructure offered scalable computing that could handle millions of video feeds simultaneously. Its artificial intelligence capabilities could power smart alerts, facial recognition, and the kind of predictive analytics that differentiate a modern security platform from a dumb alarm. And Google's software engineering talent represented the kind of workforce that ADT, paying alarm industry salaries in Boca Raton, Florida, could never recruit.

For Google, ADT offered distribution. Getting smart home devices installed professionally in six million homes was a distribution play that even Google's marketing budget could not easily replicate. Each ADT installation became a Google Nest installation, putting Google hardware in living rooms and on front doors across America. ADT's professional monitoring network also provided a layer of human oversight that purely automated systems could not match, a reassurance for consumers who were not quite ready to trust an algorithm with their family's safety.

Progress, however, was slow, and the reasons illuminate why technology partnerships between legacy companies and Big Tech are so difficult. On Google's side, the Nest division was one of many priorities competing for engineering resources. Google's core business is search advertising; hardware and home automation are strategically important but not existential. On ADT's side, integrating Google's technology required rearchitecting systems that had been in place for decades, retraining thousands of technicians, and managing a dealer network that was accustomed to selling proprietary equipment.

The partnership took more than three years to produce its first major consumer-facing product. In December 2023, ADT launched the ADT+ platform in select markets, built on Google Nest integration and offering enhanced video analytics and camera capabilities. In May 2024, ADT introduced the Trusted Neighbor feature, an automated system allowing homeowners to grant trusted individuals access to their security system through Google Nest devices. These were meaningful product improvements, but the pace of innovation was glacial by technology industry standards. In the time it took ADT and Google to ship one platform, Ring had released multiple generations of hardware and iterated its software dozens of times.

By mid-2025, the partnership was beginning to show results in the metrics that mattered most. ADT achieved its highest-ever recurring monthly revenue balance, reaching three hundred and sixty-three million dollars per month by the second quarter of 2025. The Google Nest integration was credited with improving customer satisfaction and reducing churn. In October 2025, ADT announced plans to integrate Google Gemini AI features for subscribers, though the rollout would be phased and carefully tested before broad deployment given the critical nature of security applications.

Then came a move that signaled ADT's growing confidence in AI-driven home security. On February 24, 2026, just days before this writing, ADT acquired Origin AI, a company specializing in WiFi-based ambient intelligence, for a hundred and seventy million dollars in cash. Origin's technology enables motion and human detection without cameras, audio, or wearables, using WiFi signals to sense movement and presence throughout a home. ADT expects to commercialize Origin-based offerings by 2027, a potentially transformative capability that could differentiate its monitoring service from pure camera-based alternatives.

The bigger question looming over the Google partnership is whether professional monitoring itself is a moat or an anchor. Google's AI capabilities are advancing rapidly. Computer vision, natural language processing, and ambient sensing are all improving at exponential rates. At some point, an AI system may be able to assess threats, dispatch emergency services, and manage home security with the same or better reliability than a human monitoring center. If that day arrives, ADT's core value proposition, the twenty-four-seven human monitoring that justifies its monthly premium, could become a cost center rather than a competitive advantage. The Google partnership could accelerate that transition, which would be simultaneously the best and worst outcome for ADT.

VIII. The Solar Detour: Sunpro Acquisition and Retreat (2021-2024)

In the annals of failed corporate diversification strategies, ADT's solar adventure deserves a prominent place. In November 2021, ADT announced the acquisition of Sunpro Solar, then ranked as the second-largest residential rooftop solar contractor in the United States, for approximately eight hundred and twenty-five million dollars, paid as a combination of a hundred and sixty million in cash and roughly seventy-eight million shares of ADT stock. The deal closed in December 2021, and the business was rebranded as ADT Solar.

The strategic vision was not unreasonable. ADT's trucks were already rolling through neighborhoods every day to install security systems. The company had a built-in sales force that interacted with homeowners regularly. Solar installation shared some operational overlap with security installation: both involved working on residential rooftops, managing complex scheduling, and selling a product with long payback periods. The Inflation Reduction Act was creating tailwinds for residential solar adoption. Why not become a one-stop shop for home services?

The answer became apparent almost immediately. Solar installation and home security monitoring are fundamentally different businesses in almost every dimension that matters. Solar is a capital-intensive, project-based business with thin margins, complex permitting requirements that vary by municipality, and intense competition from specialized installers. Home security monitoring is a recurring revenue business with relatively stable margins and predictable cash flows. The skill sets do not overlap: solar installers need electrical licensing, roof structural knowledge, and utility interconnection expertise. Security technicians need low-voltage wiring and panel programming skills. Combining them created operational complexity without generating meaningful synergies.

ADT's monitoring centers had nothing to do with solar panels. The cross-selling thesis, that security customers would enthusiastically add solar panels, proved far weaker than projected. The sales cycles were entirely different: a security system decision happens in days, while a solar installation involves weeks or months of assessment, financing, and permitting. A homeowner who trusts ADT to monitor their burglar alarm does not necessarily trust the same company to put panels on their roof.

The financial carnage was staggering and unfolded in slow motion, quarter after quarter, like watching an ice cream cone melt on a hot sidewalk.

In 2022, ADT had to restate financial results after discovering goodwill impairment charges had been understated by approximately fifty-two million dollars, along with internal controls weaknesses related to impairment calculations. This alone was a red flag that the solar acquisition had been poorly integrated from an accounting and governance perspective.

Then came the impairment waterfall. The first quarter of 2023 brought a non-cash goodwill impairment charge of a hundred and ninety-three million dollars on the solar segment. The second quarter added another roughly a hundred and sixty-five million. The third quarter piled on eighty-eight million more. By the end of 2023, total solar segment goodwill impairment charges for the year exceeded five hundred million dollars. Each quarterly earnings call brought a fresh write-down, eroding whatever credibility management had built with investors around the diversification thesis.

In November 2023, ADT announced restructuring, closing twenty-two of its thirty-eight solar branches. Then, on January 24, 2024, ADT's board approved a full exit from residential solar, shutting down all remaining branches. The cumulative impairment losses exceeded eight hundred million dollars, nearly the entire original purchase price. An acquisition that was supposed to transform ADT into a diversified home services platform instead became one of the most value-destructive deals in the recent history of the security industry.

The Sunpro disaster revealed something important about ADT's organizational capabilities. The company's challenge was not a lack of vision. The concept of bundling home services made strategic sense. The problem was execution: the ability to integrate an acquisition, manage a business outside its core competency, and allocate capital effectively. The same execution gap that slowed the Google partnership and limited the State Farm collaboration manifested as a catastrophic loss in the solar venture. For investors watching ADT, the Sunpro write-down was a data point that weighed heavily on credibility.

Notably, in October 2023, ADT also completed the sale of its commercial security, fire, and life safety business to GTCR for one point six billion dollars, using approximately one point five billion of the proceeds for debt reduction. The commercial divestiture and solar exit together represented a dramatic narrowing of ADT's focus back to its core: residential and small business security monitoring. Whether this focus would prove to be discipline or retreat remained an open question.

IX. The Fundamental Business Model Challenge

To understand ADT's predicament, you need to understand the economics of a monitored home security subscriber. Think of it like a cell phone contract from the early 2000s, before no-contract plans existed. A customer signs up, ADT sends a technician to install sensors, cameras, and a control panel. That installation costs ADT money, typically several hundred dollars when factoring in equipment, labor, and the dealer commission if the customer came through the authorized dealer channel. Then the customer pays a monthly monitoring fee, currently ranging from about twenty-five to fifty dollars depending on the service tier, locked into a thirty-six-month contract with a seventy-five percent early termination fee on the remaining balance.

ADT's revenue payback period on subscriber acquisition costs runs about two point one to two point three years. With an average customer tenure of roughly eight years and gross revenue attrition of about thirteen percent annually, the lifetime value to customer acquisition cost ratio works out to approximately three point six times. That is within the range that most subscription businesses consider healthy. ADT's total quarterly net subscriber acquisition cost spending runs approximately three hundred million dollars, a significant investment in growth that constrains free cash flow.

The dealer channel adds a layer of complexity that is worth understanding in detail, because it is both the engine of ADT's growth and one of its most persistent problems. ADT's authorized dealer network consists of independent companies that sell, install, and then transfer subscriber accounts to ADT in exchange for a multiple of the monthly recurring revenue. Think of it like a franchise model, except instead of selling hamburgers, dealers are selling monitoring contracts.

This model gives ADT enormous geographic reach without the overhead of maintaining a nationwide direct sales force. A homeowner in rural Montana and a homeowner in downtown Miami can both get an ADT system installed by a local dealer who knows the market. But the model creates quality control problems, brand consistency challenges, and misaligned incentives. Dealers are incentivized to sign up customers regardless of long-term retention probability, because they get paid upfront based on the monthly revenue of the accounts they create. ADT bears the attrition risk downstream. If a dealer signs up a customer who cancels after six months, the dealer has already been paid. ADT absorbs the loss.

This dynamic has led to persistent issues with customer complaints, installation quality, and pricing transparency. Online reviews frequently cite aggressive sales tactics by ADT-authorized dealers as a pain point, even though ADT corporate has limited control over how independent dealers conduct their business. The company has been shifting toward more direct sales through its own channels and the ADT+ platform, but the dealer network still accounts for a significant portion of new subscriber additions.

Compare this to the DIY model. A Ring alarm system costs two hundred to five hundred dollars upfront, installs in under an hour without a technician, and offers optional professional monitoring at about twenty dollars per month with no contract. SimpliSafe offers a similar proposition at roughly twenty to thirty-two dollars monthly. On a three-year total cost basis, DIY systems run forty to sixty percent cheaper than ADT's professional installation packages. The question is whether the professional installation, twenty-four-seven human monitoring, and the peace of mind of the blue octagon sign justify the premium.

For older homeowners, the answer is often yes. ADT's core demographic skews older, wealthier, and more likely to value white-glove service. These customers do not want to mount a camera on their doorframe. They do not want to troubleshoot WiFi connectivity issues with their motion sensors. They want a technician to handle everything, and they are willing to pay for it. But this demographic is, by definition, aging. Millennials and Gen Z consumers, raised on smartphones and self-service, overwhelmingly prefer the DIY approach. ADT's customer base is gradually shifting toward a demographic that is both harder to replace and more expensive to serve.

The innovator's dilemma is textbook here, almost as if Clayton Christensen wrote the theory with ADT in mind.

ADT cannot offer a bare-bones, self-installed, no-contract monitoring plan at twenty dollars per month without cannibalizing its existing base of subscribers paying fifty dollars per month with professional installation. The margin structure of the two models is fundamentally different. ADT's monitoring centers, dealer networks, and installation workforce are fixed costs that need to be amortized over the higher-priced subscription. A twenty-dollar-per-month plan could not support that infrastructure.

But failing to offer it means ceding the fastest-growing segment of the market to competitors who face no such constraint. Ring and SimpliSafe do not have legacy monitoring centers. They do not have dealer networks to protect. They do not have an existing subscriber base that would revolt at seeing new customers get the same service for half the price. They are free to price aggressively, iterate quickly, and let the market come to them. ADT is trapped by its own success.

X. Competitive Landscape and Market Dynamics

The American home security market is one of those industries that appears concentrated from one angle and wildly fragmented from another. ADT commands roughly twenty-seven percent of new system acquisitions and twenty-nine percent of alarm system households, a substantial lead over any individual competitor. But that means more than seventy percent of the market belongs to someone else. The industry is a patchwork.

Vivint, now owned by NRG Energy following a two point eight billion dollar acquisition in 2023, serves approximately two million subscribers and positions itself as the premium smart home alternative to ADT. Brinks Home Security has over a million subscribers, competing primarily in the professionally installed segment. Then there is a long tail of thousands of regional alarm companies, many of them family-owned operations that have served their local markets for decades. These small operators often have deeper community relationships and lower overhead than the national players, making them surprisingly durable competitors.

But measuring ADT's competitive position against other traditional alarm companies misses the more important dynamic. The real competition is coming from an entirely different category: technology companies that do not think of themselves as security businesses at all. Amazon's Ring has become the default entry point for home security for millions of Americans. When a homeowner installs a Ring doorbell, they are not necessarily thinking about replacing ADT. But they are satisfying much of the same need, the ability to see who is at the door, monitor their property remotely, and receive alerts, at a fraction of the cost and with zero commitment.

The unmonitored market represents both the opportunity and the challenge, and how you interpret the data reveals your fundamental view on ADT's future.

Of roughly a hundred and forty million US households, approximately thirty-seven million have professionally monitored alarm systems. Another ninety-four million have some type of security device, a camera, a video doorbell, a smart lock, but do not pay for professional monitoring.

That means roughly seventy-five percent of American homes with security devices are choosing not to pay for the kind of service that is ADT's core offering. Bulls see this as an enormous addressable market waiting to be converted. Bears see it as a revealed consumer preference: the majority of security-conscious homeowners have explicitly decided that professional monitoring is not worth the cost. The question is whether that seventy-five percent represents untapped demand that ADT can convert with better products and lower prices, or whether it represents a permanent consumer preference for self-monitoring that no amount of marketing can change.

The cable and telecom companies have proven to be less of a threat than initially feared, and the reasons why are instructive. Comcast's Xfinity Home and AT&T's Digital Life were supposed to leverage their existing billing relationships and in-home technician networks to dominate home security. They had the trucks, the customer relationships, and the billing infrastructure. On paper, adding security monitoring to a triple-play bundle seemed like a natural extension. In practice, security was never a priority for these companies. It was a feature that reduced churn in their core video and broadband businesses, not a standalone growth driver. The marketing investment, product development, and customer support required to compete seriously with ADT and the DIY players were never fully committed. Security monitoring requires a level of operational seriousness, twenty-four-seven monitoring centers, trained dispatchers, regulatory compliance, that cable companies found burdensome relative to the incremental revenue it generated. The lesson: distribution alone is not enough. You need operational commitment to a category to win in it.

The insurance bundling model, despite State Farm's disappointing results with ADT, remains a concept that the industry has not fully exploited. Standard home insurance discounts for monitored security systems range from two to fifteen percent, which translates to fifty to two hundred dollars per year for most homeowners. That is not enough to offset a five hundred to seven hundred dollar annual monitoring bill. But if insurers were to offer more aggressive discounts, perhaps twenty to thirty percent for homes with comprehensive smart monitoring including water leak sensors, smoke detectors, and video verification, the economics could shift meaningfully. Similarly, if advances in AI-powered monitoring could demonstrate clear, actuarially significant reductions in claim frequency and severity, insurers would have a financial incentive to subsidize monitoring costs directly. The concept is sound; the execution and incentive alignment have not been cracked. Whoever cracks it first could unlock a massive channel for subscriber growth.

One emerging competitive dynamic worth noting is the convergence of home security with energy management and home services. NRG Energy's acquisition of Vivint signaled a bet that consumers want a single provider for energy, security, and home automation. If that thesis proves correct, ADT's narrow focus on security monitoring, even with the Google partnership, may prove insufficient against bundled competitors. The company's ill-fated solar experiment with Sunpro was, in some ways, an attempt to position for exactly this convergence, but the execution failed before the strategic thesis could be tested.

XI. Technology Transformation: Can a 150-Year-Old Company Become a Tech Company?

ADT's technology infrastructure tells the story of a company that grew up in the analog age and has struggled to make the transition to digital. For decades, ADT's systems ran on proprietary hardware connected to on-premise servers at its monitoring centers. The control panels in customer homes communicated over landline phone connections, a technology that worked reliably but offered none of the capabilities that modern consumers expect: smartphone control, video streaming, cloud storage, remote access, intelligent alerts.

The migration to modern technology is not simply a matter of swapping out hardware. Think of it like renovating a house while still living in it: you cannot tear down the walls while the family is inside. ADT had to migrate millions of active subscribers from legacy systems to modern ones without disrupting the monitoring service that those subscribers depended on every night.

The technical challenges were layered. The communication protocols between home alarm panels and monitoring centers needed to be updated from landline to cellular and IP-based connections. The customer database, built over decades on proprietary formats, needed to be migrated to modern cloud architecture. The device ecosystem, historically based on closed, ADT-only hardware, needed to open up to support third-party devices like Google Nest products. Each layer of the stack had dependencies on the others, making the migration a years-long, multi-phase engineering effort.

ADT's mobile app, for years, was notoriously clunky compared to Ring's intuitive interface or Nest's polished design. The app is the primary touchpoint between a security company and its customers in the smartphone era, and ADT's version felt like it was designed by a hardware company rather than a software company, because it was. When a homeowner receives an alert at three in the morning, the difference between a responsive, clear app and a sluggish, confusing one is the difference between confidence and anxiety. For years, ADT delivered the latter.

The Google partnership was explicitly designed to address this gap. Google's Nest hardware provides ADT with consumer-grade devices that it could not have developed on its own. Google's cloud infrastructure offers scalable computing and storage. And Google's AI and machine learning capabilities hold the promise of solving one of the industry's most persistent and expensive problems: false alarms.

False alarms are the bane of the security industry, and understanding why reveals one of the most promising applications of AI in the home security context. By some estimates, ninety-four to ninety-eight percent of all alarm activations are false, triggered by pets, malfunctioning sensors, user error, or environmental factors like strong winds or temperature changes. This is an astonishing number. Imagine if ninety-six percent of fire truck dispatches were for non-fires. That is the reality that security monitoring companies live with every day.

Each false alarm that generates a police dispatch costs the monitoring company money in response fees and penalties. Many municipalities now charge fees for repeat false alarms, sometimes hundreds of dollars per incident. More importantly, false alarms damage the relationship between security companies and local law enforcement, which can lead to slower response times for genuine emergencies. Some police departments have deprioritized alarm calls entirely because of the false alarm epidemic. This creates a perverse outcome where the very system designed to protect people becomes less effective because it cries wolf too often.

AI-powered analysis of camera feeds, motion patterns, and environmental data could dramatically reduce false alarm rates. A system that can distinguish between a dog walking past a motion sensor and a person trying to open a window would eliminate the vast majority of false activations, saving money and transforming the value proposition of professional monitoring from reactive alarm response to intelligent threat assessment.

The Origin AI acquisition in February 2026 represents a potentially significant leap forward. Origin's WiFi-based ambient intelligence technology can detect motion and human presence without cameras or microphones, using the WiFi signals that already permeate modern homes. This addresses growing consumer privacy concerns about cameras in the home while providing a new sensing modality that complements traditional security hardware. If ADT can successfully commercialize this technology, it could offer a differentiated product that neither Ring nor SimpliSafe currently matches.

But the deeper question remains: can a company whose core competency is truck-rolling technicians and staffing monitoring centers genuinely transform into a technology-driven platform?

The history of legacy companies attempting this transition is not encouraging. Kodak had brilliant digital photography technology but could not escape its film economics. Blockbuster understood streaming but could not abandon its stores. Nokia saw the smartphone revolution coming but could not match Apple's software ecosystem. In each case, the barrier was not awareness or vision. It was the organizational muscle memory, the incentive structures, the talent profile, and the pace of decision-making that made transformation feel impossible even when the leadership understood its necessity.

ADT is not trying to become Google. It is trying to incorporate enough of Google's capabilities to remain relevant, which may be a more achievable but still formidable challenge. The question is whether "good enough" technology married to professional monitoring and a trusted brand can carve out a sustainable middle ground between the pure DIY players and the Big Tech ecosystems. If it can, ADT survives. If it cannot, the company slowly becomes a niche provider for a shrinking demographic that values human monitoring above all else.

XII. Porter's Five Forces Analysis

Understanding ADT's competitive position requires examining the structural forces shaping the home security industry.

The threat of new entrants is high and rising. The historical barriers to entry in professional security, the need for monitoring centers, regulatory licensing requirements, a trained installation workforce, and brand trust, were substantial. But the DIY revolution has lowered these barriers dramatically. A startup can now build a credible home security product using off-the-shelf cameras, cloud computing infrastructure from AWS or Google Cloud, and a mobile app developed by a small engineering team. Ring proved that a garage startup could challenge a hundred-and-forty-year incumbent. The remaining barriers, particularly the regulatory requirements for professional monitoring and the brand trust that customers place in established names, still matter but are not sufficient to keep determined entrants out.

The bargaining power of suppliers is relatively low. The hardware components in security systems, cameras, sensors, control panels, are largely commoditized. ADT can source from multiple manufacturers and has enough scale to negotiate favorable pricing. However, the Google partnership creates a dependency that cuts both ways. ADT's strategic direction is now deeply intertwined with Google's product roadmap and priorities. If Google were to deprioritize the Nest home security platform, or redirect its AI capabilities toward other applications, ADT would be left without a critical technology partner.

Buyer power is high and increasing. Before a customer signs a contract, they have enormous leverage: pricing is transparent online, competitors offer free installation promotions, and no-contract alternatives abound. A prospective customer can compare ADT, Vivint, Ring, SimpliSafe, and a dozen other options within minutes of opening a browser tab.

However, once a customer is installed and under contract, switching costs rise significantly. The equipment is often proprietary or at least not interchangeable with competitors' systems, and the thirty-six-month contract creates financial friction through early termination penalties. This bifurcation, high buyer power before signing and moderate switching costs after, defines ADT's customer acquisition challenge. The company must spend heavily to win customers in a hyper-competitive pre-sale environment, then rely on inertia and contract terms to retain them.

The threat of substitutes is the most powerful force in the industry. DIY security systems, smart home devices that provide security as a secondary feature, smartphone-based self-monitoring, neighborhood watch apps like Citizen and Neighbors, and even social media groups that share security information all serve as substitutes for professional monitoring. The substitution threat is especially acute because many of these alternatives are either free or dramatically cheaper than ADT's service. When a two-hundred-dollar Ring camera connected to a free smartphone app provides eighty percent of the functionality of a professionally monitored system, the value proposition of the remaining twenty percent becomes increasingly difficult to justify to cost-conscious consumers.

Competitive rivalry is intense and shows no signs of easing. The market is fragmented enough that no single competitor can set prices, but consolidated enough that ADT's every move is closely watched and quickly matched. When ADT launches a new product tier, Vivint responds within weeks. When Ring drops its monitoring price, SimpliSafe follows within months.

The combination of high fixed costs in monitoring infrastructure, declining differentiation in hardware, and aggressive promotional pricing creates a dynamic where profitability is under constant pressure. Brand matters, but in an industry where the product is largely invisible, functioning silently in the background until something goes wrong, brand loyalty is thinner than in consumer-facing categories. Nobody shows off their alarm system to dinner guests the way they might show off a new kitchen or sound system.

The overall structural assessment is challenging for incumbents. ADT's scale and brand provide advantages, but they are not the kind of durable competitive advantages that insulate a business from secular disruption. The forces arrayed against professional monitoring companies are not cyclical; they are structural. That does not mean ADT will disappear, but it does mean the company must work harder every year just to maintain its position.

What is particularly striking about the five forces analysis for home security is how rapidly the dynamics have shifted. Even a decade ago, the threat of new entrants was low, substitutes were limited, and buyer power was constrained by information asymmetry. The smartphone revolution and the rise of cloud computing fundamentally altered every force simultaneously, which is why the traditional alarm industry has found the disruption so disorienting. It was not one force that changed; it was all of them, at the same time.

XIII. Hamilton's Seven Powers Framework

Hamilton Helmer's Seven Powers framework provides a more granular view of ADT's strategic position by examining the specific sources of durable competitive advantage.

Scale economies are moderate, and the distinction between scale in physical services versus scale in software is critical to understanding why. ADT's six-plus million subscribers provide meaningful leverage in negotiations with hardware suppliers and operational efficiencies in monitoring center operations. Spreading the fixed costs of a monitoring center across millions of subscribers reduces the per-subscriber cost in a way that smaller competitors cannot match.

However, the industry's unit economics do not exhibit the kind of winner-take-all dynamics seen in software businesses. When Netflix adds a subscriber, the marginal cost is essentially zero: the content is already produced, the servers are already running. When ADT adds a subscriber, a technician must drive to the home, install hardware, and configure the system. Equipment must be purchased. The dealer must be paid. These are real, incremental costs that do not decline meaningfully with scale beyond a certain point.

And in the DIY segment, scale advantages tilt toward the technology platforms: Ring, backed by Amazon's cloud infrastructure and logistics, can serve millions of customers at a marginal cost that approaches software economics. The hardware is shipped by Amazon's unmatched logistics network. The software runs on AWS. The customer support is digital-first. This is a fundamentally different cost structure than ADT's, and no amount of subscriber growth on ADT's side can close the gap.

Network effects are essentially absent, and this is one of the most glaring strategic gaps in ADT's position. Your neighbor using ADT does not make your system work better. There is no shared dashboard, no community alert feature, no collaborative intelligence that improves as more homes join the network.

Compare this to Ring's Neighbors app, where each additional user in a neighborhood contributes safety information, shared video clips, and community alerts that make the app more valuable for everyone. That is a classic network effect: the product gets better as more people use it. ADT has missed the opportunity to build network effects into its offering, and at this stage, it may be too late to create them organically. The Origin AI acquisition could theoretically enable neighborhood-level ambient intelligence, but turning that theoretical possibility into a shipping product with genuine network dynamics is an enormous execution challenge.

Counter-positioning is perhaps the most damaging dynamic for ADT. In Helmer's framework, counter-positioning occurs when a newcomer adopts a business model that the incumbent cannot replicate without damaging its existing business. Ring and SimpliSafe have done exactly this. Their low-cost, no-contract, self-installed models are directly at odds with ADT's high-touch, high-cost, contract-based approach. ADT cannot match their pricing without destroying its own economics. It cannot offer self-installation without undermining its dealer network and installation workforce. It cannot eliminate contracts without losing the predictable revenue stream that supports its debt service. ADT is not counter-positioning others; it is being counter-positioned.

Switching costs are moderate but declining. ADT's equipment, contracts, and established monitoring relationships create friction that makes customers less likely to leave on any given day. But contract lengths have shortened from five years to three, and increasingly to month-to-month for new customers under competitive pressure. Equipment costs have dropped, making it cheaper to switch to a new system. And for younger customers who grew up in a world of cancel-anytime subscriptions, the idea of being locked into a security contract feels increasingly anachronistic. The switching cost advantage is real but depreciating.

Branding is ADT's strongest power. The blue octagon is one of the most recognized symbols in American residential life. In consumer surveys, ADT consistently ranks as the most recalled home security brand. This brand recognition is the product of a hundred and fifty years of presence, not just in advertising but on the front of American homes. It conveys trust, reliability, and seriousness in a category where those attributes matter deeply, particularly in moments of genuine fear or crisis. But even strong brands face erosion when they become associated with being expensive and outdated. For younger consumers, ADT's brand may carry more baggage than cachet.

Cornered resources are weak, and this is perhaps the most concerning assessment of all. A cornered resource is something a company has that competitors cannot obtain: a patent portfolio, an exclusive license, a uniquely talented team, a critical data asset. ADT does not possess proprietary technology that competitors cannot replicate or license. Its customer data, while valuable, is not unique since Ring and other DIY players also collect substantial home security data. Its monitoring centers, while expensive to build, are not defensible since third-party monitoring services are available to any competitor.

The Google partnership provides access to leading technology, but it is a partnership, not a proprietary advantage. Google could, in theory, offer similar capabilities to other security companies or build its own competing monitoring service. The Origin AI acquisition in February 2026 could change this dynamic if the WiFi-based sensing technology proves difficult to replicate, but it is too early to assess whether Origin's capabilities constitute a genuine cornered resource.

Process power is also weak. ADT's operational capability in professional installation is real, built over decades of training technicians and optimizing scheduling. But this is not the kind of process advantage that creates durable value. It is a competency that competitors can develop and that technology may eventually render less relevant as self-installation becomes the norm.

The overall seven powers assessment paints a picture of a company defending its position with brand recognition and moderate scale advantages but lacking the compounding strategic advantages needed for sustained value creation. ADT is playing defense, not building power.

The contrast with the DIY insurgents is instructive. Ring, under Amazon, benefits from network effects through the Neighbors app, counter-positioning against traditional alarm companies, the cornered resource of Amazon's distribution and data infrastructure, and the process power of a software-first development culture. SimpliSafe benefits from counter-positioning through its no-contract model and branding as the anti-ADT for cost-conscious consumers. These companies are accumulating powers. ADT is depleting them. That asymmetry is the most important strategic fact about the competitive landscape.

XIV. The Bull Case for ADT

Despite the structural challenges, a credible bull case exists, and dismissing it entirely would be intellectually lazy.

Start with the cash flow. ADT generates more than four hundred million dollars in annual free cash flow from its monitoring subscriber base. This is not speculative revenue from a product that might find a market. It is not dependent on a technological breakthrough or regulatory approval. It is money flowing in every month from more than six million homes, as reliable as a utility payment. For investors who believe in the durability of that cash flow stream, ADT's current valuation implies a deeply discounted price.

The addressable market argument is genuinely compelling. Roughly seventy-five percent of American homes with some form of security device do not pay for professional monitoring. If ADT, powered by Google Nest technology and AI capabilities, can develop a product that converts even a small fraction of those self-monitoring households into paying subscribers, the growth potential is substantial.

The math is straightforward: converting just five percent of the unmonitored installed base, roughly four to five million households, would nearly double ADT's subscriber count. The ADT+ platform and Origin AI acquisition suggest the company is building toward an offering that could appeal to a broader demographic than its traditional customer base.

The brand remains an extraordinary asset, perhaps the single most valuable thing on ADT's balance sheet. In a category defined by trust, ADT's hundred-and-fifty-year history and universal recognition create an advantage that no amount of venture capital can buy.

When homeowners search for security systems, ADT is the first name most people think of. That awareness drives organic customer acquisition that competitors must spend heavily to match. The blue octagon itself functions as a deterrent, something that cannot be said about a Ring doorbell or a SimpliSafe keypad. There is established criminology research suggesting that visible alarm signage reduces the probability of burglary attempts, and ADT's sign is the most recognized in the industry.

The Google partnership, despite its slow start, is beginning to deliver tangible results. Record-high recurring monthly revenue, improved customer satisfaction, and the pipeline of Gemini AI features suggest the technology integration is gaining momentum. If Google deepens its commitment, perhaps increasing its stake or expanding the scope of the partnership, ADT could benefit from a technology acceleration that transforms its competitive position. The Origin AI acquisition in February 2026 suggests ADT is becoming more aggressive about building a differentiated technology stack, not merely reselling Google hardware.

ADT's financial discipline has improved materially since the Sunpro debacle. The company used proceeds from the commercial business sale to pay down one point five billion in debt. In February 2025, it refinanced five hundred million in first-lien notes due 2026 with a new six-hundred-million-dollar seven-year term loan, extending its maturity profile. Additional debt paydowns of two hundred million dollars have been announced. The solar exit, while painful, demonstrated a willingness to acknowledge mistakes and refocus. The debt-to-equity ratio, while still elevated at roughly three times, is trending in the right direction. Apollo's gradual exit through secondary offerings is slowly resolving the overhang of private equity control that has weighed on the stock since the IPO.

The commercial security divestiture also strengthened the bull case in an unexpected way. By selling the commercial segment for one point six billion dollars, ADT simplified its business and eliminated a division that operated under different competitive dynamics than residential security. The commercial security market is dominated by large systems integrators and involves complex enterprise sales cycles that have little in common with the residential subscriber model. Focusing exclusively on residential and small business security allows management to concentrate resources and attention on the transformation challenge that matters most.

For older demographics, which still represent a substantial portion of homeowners with significant assets to protect, professional installation and human monitoring remain genuinely valued. Not every homeowner wants to troubleshoot their WiFi camera at two in the morning when an alarm goes off. The peace of mind that comes from knowing a trained professional is watching your home and will dispatch emergency services if needed is worth the premium for many Americans.