Adient plc: The $17 Billion Automotive Seating Giant That Almost Collapsed

I. Introduction and Episode Roadmap

Think about the seat you sat in the last time you were in a car. Not the dashboard, not the steering wheel, not the infotainment screen—the seat. The foam cradling your lower back. The mechanism that lets you recline with a satisfying click. The headrest positioned at exactly the right height. The trim cover stitched with invisible precision.

You probably never gave it a second thought. And that is precisely the point.

There is roughly a one-in-three chance that seat was made by a company called Adient. Not designed by the automaker whose badge adorns the hood. Not assembled by the dealer who sold the car. Made by Adient—a company most car buyers have never heard of, yet one that touches more human bodies, for more hours per day, than almost any other manufacturer on Earth.

Adient is the world's largest automotive seating supplier. Its products end up in tens of millions of vehicles every year, rolling off assembly lines from Detroit to Shanghai to Stuttgart to São Paulo. The company operates more than two hundred manufacturing and assembly plants across twenty-nine countries, employing north of sixty-five thousand people. In fiscal year 2024, it reported consolidated revenue of nearly fifteen billion dollars. By every industrial metric, this is a colossal enterprise—a company whose manufacturing footprint rivals that of the automakers it serves.

And yet, just six years before these numbers, Adient was staring into the abyss. Its stock had cratered ninety-two percent from its all-time high. It had piled up more than three billion dollars in cumulative losses over two fiscal years. Its founding CEO had been shown the door. The grand plan to build a gleaming headquarters in downtown Detroit—purchased from Mexican billionaire Carlos Slim, no less—had been abandoned at an eleven-million-dollar loss.

Analysts openly questioned whether the company could survive.

How did the world's number-one seat maker go from spin-off darling to near-bankruptcy in just three years? And more remarkably, how did it claw its way back from the edge?

This is a story about the hidden economics of automotive suppliers—an industry where razor-thin margins, enormous capital requirements, and the crushing bargaining power of a handful of giant automakers create a business environment that can break even the largest players. It is a story about the mechanics of corporate spin-offs, and what happens when a parent company loads its offspring with debt on the way out the door.

It is also a story about leadership failure, operational collapse, and the kind of turnaround that requires a CEO willing to act as—in the words of one business journalist—a "field surgeon," cutting away damaged tissue to save the patient.

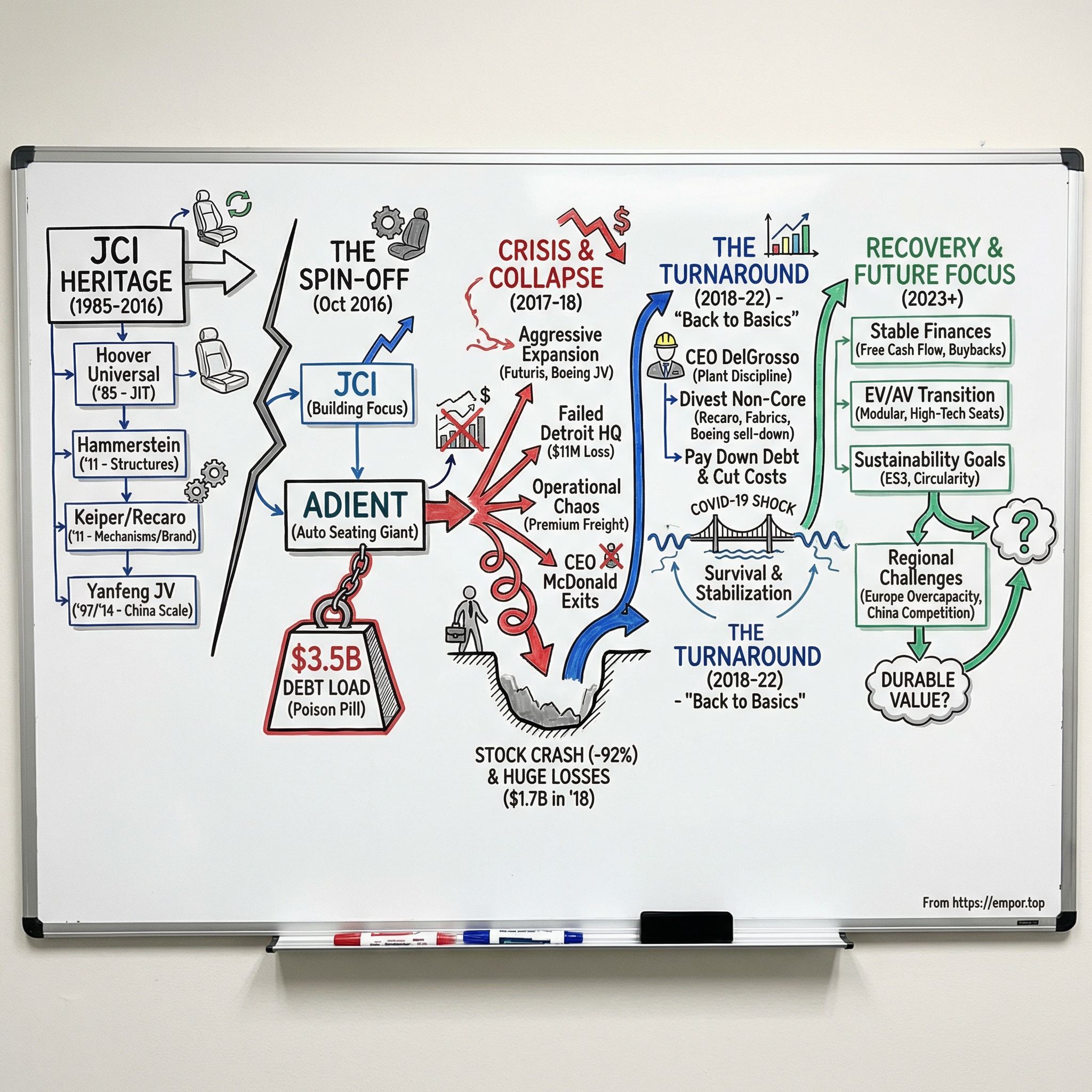

Adient officially began independent operations on October 31, 2016, following its separation from Johnson Controls International. It was born as the biggest player in its industry, with $16.6 billion in revenue and operations spanning the globe. But it was also born with what can only be described as a poison pill: $3.5 billion in debt, roughly twice its annual earnings, strapped to its balance sheet before it even opened its doors.

The themes here—spin-off dynamics, supplier economics, corporate turnarounds, and the question of whether great market position can overcome terrible capital structure—are the kinds of questions that define careers and fortunes.

To understand how Adient arrived at its moment of crisis, and how it survived, we need to go back to the beginning. Not to 2016, when the company was born. But to 1985, when the empire that would become Adient was first assembled, one acquisition at a time.

II. The Johnson Controls Heritage: Building an Empire (1985-2016)

In the spring of 1985, two CEOs sat down to negotiate what would become one of the most consequential acquisitions in automotive supplier history. Fred Brengel of Johnson Controls and John Daly of Hoover Universal shook hands on a deal worth $219 million in cash plus 6.3 million shares of common stock. On May 12, 1985, Hoover Universal officially became a wholly-owned subsidiary of Johnson Controls.

Why did a building controls company want to make car seats? The answer lay in Hoover Universal's unique capabilities. Hoover was not just stamping out seat frames—it was at the leading edge of a transformation in how automotive parts were delivered. While most suppliers shipped components in bulk and let them pile up in warehouses, Hoover had pioneered what the industry called just-in-time delivery: manufacturing exactly the right parts, in exactly the right sequence, and delivering them to the assembly line precisely when the automaker needed them. Think of it as the Amazon Prime of auto parts, decades before Jeff Bezos started selling books. In an industry obsessed with eliminating waste and inventory costs, this was a genuine competitive weapon.

That same year, Johnson Controls also acquired Ferro Manufacturing, establishing a powerful dual foundation. But the Hoover deal was the masterstroke—it gave JCI both the production capability and the delivery methodology that would become the bedrock of the world's largest seating operation.

What followed over the next quarter century was a masterclass in acquisition-driven empire building. Johnson Controls systematically assembled the world's largest seating business through a series of deals that reads like a strategic chess game. Each acquisition filled a specific gap in capability or geography, and each made the combined business harder to compete against.

The acquisitions accelerated in the 2010s. In February 2011, JCI completed the acquisition of the C. Rob. Hammerstein Group for approximately $521 million, adding deep expertise in seating metal structures and components—the skeletal framework that gives a car seat its strength and crash-worthiness. Think of Hammerstein as the bones of the operation. Without strong, precisely engineered metal frames, nothing else in a car seat works.

Just months later, in June 2011, JCI closed on German seating specialist Keiper and its premium subsidiary RECARO Automotive Seating, adding 4,750 employees across thirteen locations in seven countries. If Hammerstein was the bones, Keiper was the joints—the precision mechanisms that allow seats to tilt, slide, and recline. These are intricate metal assemblies of gears, springs, and locking devices that most passengers never see but use every single time they get in a car.

Together, these acquisitions gave Johnson Controls something no competitor could match: the ability to offer automakers a truly complete product range of metal components and mechanisms across every vehicle segment, from $15,000 economy cars to $150,000 performance machines. With RECARO—the brand that car enthusiasts associate with racing-inspired bucket seats—JCI even had a direct line to the consumer psyche, a rarity in the anonymous world of automotive supply.

But perhaps the most consequential move came not through acquisition but through partnership in the world's fastest-growing automotive market. In December 1997, Johnson Controls and Shanghai Automotive Industry Corporation's Yanfeng subsidiary formed a joint venture with a total investment of $53 million. Yanfeng Johnson Controls designed, developed, and manufactured complete seats for Chinese OEMs, including Shanghai GM and Shanghai Volkswagen. Then, in May 2014, the two partners dramatically expanded their collaboration, forming Yanfeng Automotive Interiors—a global joint venture with Yanfeng holding seventy percent and JCI holding thirty percent. When it launched in July 2015, YFAI was instantly the world's largest automotive interiors company, with revenues of approximately $8.5 billion and more than ninety manufacturing and engineering centers worldwide. This was not just a business deal—it was a bet on China's automotive future that would shape the destiny of the seating business for decades.

By the mid-2010s, Johnson Controls' automotive seating division was a behemoth generating more than sixteen billion dollars in annual revenue. But JCI itself had evolved into something else entirely—a sprawling conglomerate spanning automotive parts, building efficiency systems, HVAC controls, and batteries. And in January 2016, JCI made the decision that would change everything: it entered into a definitive merger agreement with Tyco International, the fire protection and security giant.

The combined entity would focus exclusively on building technology and efficiency—a business carrying higher margins and steadier demand than the cyclical, cutthroat world of automotive supply. Automotive seating no longer fit the vision. But the way JCI chose to exit the seating business would matter far more than the decision to exit itself.

Here is where the story takes a darker turn. Over the preceding years, Johnson Controls had intentionally allocated capital away from the automotive unit. Not accidentally, not through neglect—deliberately. As company filings later acknowledged, JCI's "strategic objectives" meant the company "intentionally allocated capital away from the automotive business over the past few years." These choices "naturally limited the automotive business unit's ability to make strategic investments."

Read that carefully. The parent company was simultaneously starving its child of investment and preparing to extract maximum financial value from it on the way out. The automotive business was strong in market position but increasingly hollowed out. It was like a landlord who stops maintaining a building while planning to sell it—the structure still stands, but the foundation is weakening.

What happened next would haunt Adient for years.

III. The Spin-Off: Born Loaded with Debt (2016)

The name they chose was Adient, derived from the Latin word meaning "approaching"—from the stem adiens, combining ad (to) and ire (go). Company marketers described it as "a positive, powerful name that underscores their unique point of differentiation—their ability to bring the right pieces together the right way at precisely the right time." It was the kind of upbeat corporate branding that reads very differently in hindsight.

The mechanics of the separation were straightforward enough. Johnson Controls completed its merger with Tyco on September 2, 2016, with Tyco changing its name to Johnson Controls International. Then, on October 31, 2016—Halloween, as it turned out—JCI distributed one Adient share for every ten Johnson Controls shares held by existing shareholders. Adient began trading on the New York Stock Exchange under the ticker ADNT, opening at $45.45 per share.

On paper, the debut was impressive. Adient was instantly the world's largest global automotive seating supplier, with $16.6 billion in revenue and approximately 75,000 employees operating across thirty-three countries. It held leading market positions in North America, Europe, and China simultaneously—a trifecta that no competitor could match. Wall Street, which generally loves spin-offs for the clarity of focus they create, greeted the new company with enthusiasm.

But buried deep in the regulatory filings was a detail that should have set off alarm bells. In connection with the spin-off, Adient obtained $3.5 billion in debt financing. Of that amount, approximately $500 million stayed with Adient for working capital and operating purposes. The other three billion dollars—eighty-six cents of every borrowed dollar—was distributed directly to Johnson Controls as a pre-separation dividend.

Let that sink in for a moment. JCI had effectively forced its newborn offspring to borrow three billion dollars and hand the cash back to its parent, keeping the debt. It is the corporate equivalent of a parent co-signing a mortgage on their child's first apartment, then taking the down payment for themselves and leaving the kid with the full monthly payments.

The average interest rate on this debt was 3.4 percent, translating to roughly $125 million in annual interest expense—money that could never be invested in new manufacturing technology, program development, or talent retention. To understand how punishing that number is, consider the math: $125 million in annual interest on a business running at five-to-six percent operating margins means a huge share of operating profit goes straight to bondholders before a single dollar reaches shareholders. In an industry where operating margins typically run in the mid-single digits, that interest burden was the equivalent of tying a concrete block to a swimmer's ankle and pushing them into the deep end.

Adient itself acknowledged the danger in remarkably candid language for a regulatory filing. The company reported at launch that its "significant leverage" put it "at a competitive disadvantage" relative to less-indebted peers. This was not boilerplate legal hedging—it was a genuine warning that the people inside the company understood exactly what they were dealing with. The debt load was roughly twice the company's annual earnings before interest and taxes. For comparison, well-run automotive suppliers typically carry leverage ratios closer to one-to-one.

R. Bruce McDonald was tapped to lead the new company as its first chairman and chief executive officer. McDonald was a quintessential Johnson Controls lifer—he had served as executive vice president and vice chairman from 2014 to 2016, and before that as vice chairman and chief financial officer from 2005 to 2014. He was a finance-oriented leader, comfortable with spreadsheets and capital allocation strategies but not an operations specialist—a distinction that would prove critical in the years ahead when the company's factories, not its balance sheet models, needed the most attention.

McDonald came out swinging with a signature move that captured the optimism of the moment. Adient would spend $100 million to renovate the historic Marquette Building in downtown Detroit—a stately structure adjacent to the Cobo Center convention hall—and relocate roughly five hundred employees there, including about one hundred new positions. The building had been purchased for $16.9 million from Mexican billionaire Carlos Slim, who had acquired it for just $5.8 million in 2014. Adient also paid approximately $19 million for a nearby parking deck and surface lot. It was intended as a bold statement: the world's largest seating company was planting its flag in the heart of the American auto industry.

What the optimists missed—or chose to ignore—was the fundamental fragility at the core of the enterprise. Adient's business plan assumed everything would go right: margins would hold, programs would launch smoothly, the global auto market would remain robust, and the company would invest enough in operations to stay competitive, all while servicing that mountain of debt. In the automotive supply business, where raw material prices fluctuate, customer disruptions cascade, and a single botched program launch can erase a quarter's profits, assuming everything goes right is the most dangerous assumption of all.

There is a well-known pattern in spin-off investing: parent companies sometimes use the separation as an opportunity to clean house, shedding debt, underperforming assets, or unfavorable contracts onto the new entity. Sophisticated spin-off investors screen for this aggressively. In Adient's case, the warning signs were in the filings—but the allure of owning the world's largest seating company, with $16.6 billion in revenue and operations on every continent, was intoxicating enough to drown out the alarms.

The first cracks would appear sooner than anyone expected.

IV. Rapid Expansion and Warning Signs (2017-2018)

For roughly twelve months, the optimists appeared vindicated. Adient's fiscal year 2017—its first full year as an independent company—delivered $16.2 billion in revenue and $877 million in net income. Profitable. Cash-generative. On track. The stock climbed steadily from its opening price of $45, reaching an all-time high of $84.06 on October 24, 2017—a near-doubling in barely a year. Bruce McDonald's compensation package for that year hit $24.3 million, making him metro Detroit's highest-paid public company CEO. The king of car seats was sitting pretty.

Rather than using this window of strength to pay down debt and fortify the core business, McDonald pursued an aggressive growth strategy that pushed Adient well beyond its wheelhouse. In September 2017, Adient acquired Futuris, an Oak Park, Michigan-based automotive seat manufacturer owned by private equity firm Clearlake Capital. The deal added fifteen manufacturing facilities across Asia and North America and was expected to contribute $500 million in additional annual revenue. For a company already straining under $3.5 billion in debt, taking on more operational complexity was a bold bet.

Then came the headline-grabbing deal that raised eyebrows across the industry. In January 2018, Adient and Boeing announced the formation of Adient Aerospace, a joint venture to design and manufacture airliner seats. Adient held 50.01 percent, Boeing 49.99 percent. The airline seat market was valued at $4.5 billion in 2017, with forecasts projecting $6 billion by 2026. Headquarters were established in Kaiserslautern, Germany, near Frankfurt, with customer service operations in Seattle. The venture planned to start with lie-flat business class seating for widebody aircraft.

On its surface, the logic was appealing—leverage seat-making expertise into an adjacent market with potentially richer margins. But the automotive seating business and the aviation seating business are vastly different animals. Aviation seats must pass extraordinarily rigorous Federal Aviation Administration certification processes. Customer relationships operate on entirely different timescales and negotiation dynamics. The competitive landscape is dominated by established players like Collins Aerospace and Safran. For a company that was already struggling to execute on its existing programs, opening a second front was the kind of strategic gamble that only works when everything else is going well.

Everything else was not going well.

Behind the confident earnings calls, Adient's Seat Structures and Mechanisms division—SS&M—was hemorrhaging money. Product launches were being mismanaged. The company struggled to obtain certain metal specifications reliably. Steel prices were climbing. Customers were defecting from the SS&M business. In the second quarter of fiscal 2018, SS&M recorded a $279 million non-cash goodwill impairment charge—a stark accounting admission that the division was worth far, far less than what had been paid for it. An impairment charge is essentially the company admitting to its shareholders: "Remember when we said this asset was worth this much? It is not. We overpaid, and now we are writing down the difference."

The Detroit headquarters dream collapsed next. In June 2018, Adient quietly informed Mayor Mike Duggan that it was scrapping the renovation plan entirely—the $100 million project, the five hundred employees, the one hundred new jobs, all of it. The company subsequently sold the Marquette Building and surrounding properties at an eleven-million-dollar loss. Detlef Juerss, Adient's VP of engineering and CTO, later offered a blunt postmortem: "Detroit was not the right timing." In business speak, that translates to: we should never have done this.

When the fiscal 2018 results arrived, the numbers were devastating. Adient reported a net loss of $1.7 billion—roughly $32 million dollars hemorrhaged every single week—on revenue of $17.4 billion. Revenue was actually at an all-time high, which made the loss even more alarming. This was not a company suffering from lack of demand. It was a company that had revenue coming in the front door and burning it in the back. The fourth quarter alone produced a $1.36 billion loss, driven by $809 million in restructuring and impairment charges. The cash dividend was suspended. The stock was in freefall.

Crain's Detroit Business would later summarize the situation with devastating precision: a company "heavily damaged by mismanaged launches, a botched attempt to move its headquarters to downtown Detroit that resulted in an $11 million loss before renovations were ever completed, and an aggressive growth strategy gone awry."

Think about the timeline. In October 2017, the stock hit $84. McDonald was the highest-paid CEO in metro Detroit. Adient was acquiring companies, launching joint ventures with Boeing, buying historic buildings from billionaires. Twelve months later, the company reported a $1.7 billion loss, abandoned its headquarters, and the CEO was gone. The speed of the collapse is the most striking feature—this was not a slow decline but a sudden, violent unraveling of a business that had been running too fast on too little foundation.

The board had seen enough. The question was no longer how to grow Adient—it was whether Adient could survive.

V. Crisis Point: The Near-Collapse (2018-2020)

The Downward Spiral

Bruce McDonald stepped down as chairman and CEO on June 11, 2018. The announcement was dressed up as a retirement, but there was nothing voluntary about it. He remained as an adviser through September 30, collecting his $1.5 million salary and $250,000 in relocation expenses. His 2017 equity award of approximately $17 million was forfeited—a costly price for departure, though a small number relative to the billions in shareholder value that had evaporated.

The board's interim choice was almost poetically appropriate: Frederick "Fritz" Henderson, an Adient board member who happened to be the former CEO of General Motors. Henderson had been installed as GM's chief executive in 2009, replacing Rick Wagoner during the government-sponsored bankruptcy that nearly destroyed the American auto industry. He knew what corporate crisis looked like from the inside. He had navigated the most dramatic near-death experience in American industrial history. Henderson served as Adient's interim CEO for roughly three months, stabilizing the ship while the board hunted for a permanent leader.

That leader arrived on October 1, 2018. Doug DelGrosso, fifty-six years old, became Adient's president and CEO. His resume read like a blueprint for exactly this moment. DelGrosso came from Chassix, a Southfield, Michigan-based automotive supplier that had filed for Chapter 11 bankruptcy in March 2015 with $556.7 million in total debt and just $34.3 million in assets. The company had missed bond payments and was on life support. Under bankruptcy protection, Chassix reorganized and emerged in July 2015. DelGrosso then rebuilt it—expanding into Europe with a $50 million investment and acquiring Benteler International's automotive casting business for approximately $30 million.

Before Chassix, DelGrosso had spent twenty-three years at Lear Corporation, rising all the way to chief operating officer before departing in 2007. He had also served as president and CEO of Henniges Automotive and held executive roles at ZF TRW. This was a man who had spent his entire career in the trenches of automotive supply, who understood the economics of stamped metal and injection-molded foam at a cellular level, and—crucially—who had already demonstrated the ability to rescue a company from bankruptcy. The question was whether he could do it again, at a company fifty times the size of Chassix.

DelGrosso's diagnosis was swift and damning. He believed Adient had been "distracted by costly ideas not core to its business" and was "too centrally focused and bloated with centralized upper management." His internal mantra became "Back to Basics"—a phrase that sounds generic until you understand what it meant in practice. It meant ripping out layers of corporate overhead. It meant killing the Boeing airline seating venture by slashing Adient's stake from 50.01 percent to 19.9 percent within his first year. It meant decentralizing decision-making to regional leaders who actually understood the factories they oversaw. And it meant confronting, with brutal honesty, the operational failures that had nearly destroyed the company.

The restructuring was enormous in scope. Approximately thirteen thousand employee positions were targeted for elimination—a staggering number even by the standards of Detroit's frequently restructured automotive industry. To put it in context, that was roughly one out of every six employees at the company.

Premium freight costs—the expensive expedited shipments required when a factory falls behind schedule and has to air-freight parts to avoid shutting down a customer's assembly line—were attacked systematically. For those unfamiliar with the term, "premium freight" is the automotive supplier's equivalent of paying for same-day delivery because you forgot to place the order on time. It is ruinously expensive, and it is often the first symptom of deeper operational dysfunction. Under McDonald, premium freight costs had ballooned as mismanaged launches cascaded into delivery failures. Under DelGrosso, they became a key metric to drive down.

Underperforming plants were identified for closure or consolidation. Regional leadership was empowered to make decisions locally rather than waiting for direction from a bloated central office—a critical change for a company where factories in Germany, China, and Mexico each face utterly different operational challenges.

On the factory floor, the improvements were tangible and immediate. At the Warren Bridgewater plant in suburban Detroit, customer disruptions—situations where Adient failed to deliver parts on time, potentially shutting down an automaker's assembly line at a cost of millions per day—had been running at more than ten per month during the first quarter of fiscal 2019. By the fourth quarter, that number was below one. That single data point captures the transformation DelGrosso was driving: from chaos to competence, one plant at a time. Not through brilliant strategy, but through blocking and tackling—the basics of manufacturing discipline that Adient had somehow lost in its rush to expand.

The fiscal 2019 results showed the surgery was working, even if the patient was far from healed. The net loss narrowed dramatically from the $1.7 billion of the prior year to $491 million. Revenue slipped five percent to $16.5 billion. The fourth-quarter loss was reduced to just $4 million—compared to $1.36 billion a year earlier. The trajectory was unmistakable.

But the personal cost was searing. On November 14, 2019, DelGrosso stood before his employees at a company-wide town hall at Adient's Plymouth Township headquarters and delivered devastating news. The five-week United Auto Workers strike against General Motors—Adient's single largest customer—had severely impacted the Americas region. Roughly 1,300 non-plant salaried employees would not work and would not be paid during the weeks of Thanksgiving and New Year's. DelGrosso was characteristically direct: "We've been pretty upfront about what needs to be done," he said, and thanked the employees "for taking the burden on." Imagine hearing that a week before Thanksgiving—that your holiday paycheck is gone, not because of anything you did, but because your company's biggest customer is in a labor dispute with its own workers. This is the cascading fragility of automotive supply chains made personal.

COVID-19 and the Brink

DelGrosso's target was ambitious but clear: reach cash-flow breakeven by fiscal 2020. The restructuring was on track. Losses were shrinking. The balance sheet, while still dangerously overleveraged, was stabilizing.

Then the pandemic arrived.

In March 2020, the global automotive industry experienced the most severe demand shock since the Great Depression. Assembly plants shut down worldwide. Consumer traffic at dealerships evaporated. Supply chains, already strained, seized up entirely. For a company carrying $3.3 billion in debt, operating on mid-single-digit margins, and in the middle of a restructuring that required continuous cash flow to execute, COVID-19 was an existential threat.

Adient's stock told the story with terrifying efficiency. From the all-time high of $84.06 set on October 24, 2017, shares plunged to an all-time low of $6.53 on March 18, 2020. A decline of approximately ninety-two percent in twenty-nine months. The company that had been spun off as the world's largest automotive seating supplier—generating $17.4 billion in revenue with operations on every continent—briefly had a market capitalization of less than $600 million. At that price, the market was essentially saying Adient's debt was worth more than the entire business. The equity was almost worthless.

Revenue for fiscal 2020 collapsed to $12.67 billion, a twenty-three percent decline from the prior year. Operating margins had contracted to roughly five percent, while competitors Lear and Magna operated above eleven percent. The company had now accumulated more than three billion dollars in cumulative losses since the spin-off.

Interest expense was consuming an ever-growing share of diminished earnings—creating a vicious cycle that every overleveraged company dreads. Here is how it works: as profitability falls, the fixed interest payments consume a larger percentage of what remains. That leaves fewer dollars for the operational investments needed to restore profitability. Which means profitability continues to fall. Which means the interest payments consume even more. It is a doom loop, and escaping it requires either generating more cash, selling assets to pay down debt, or both—preferably before lenders lose confidence and call in their loans.

This was the moment of maximum danger—the point where the line between survival and bankruptcy becomes razor-thin. The company carried approximately $3.3 billion in debt against an enterprise that the market valued at less than $600 million. When the market says your debt is worth more than you are, creditors get nervous. Suppliers start demanding upfront payment. Customers begin wondering whether you will still be around to honor warranty claims. The psychological dynamics of near-bankruptcy can become self-reinforcing.

DelGrosso, who had navigated Chassix through Chapter 11, understood this calculus with excruciating clarity. He had seen what happens inside a bankruptcy proceeding—the destruction of supplier relationships, the loss of customer confidence, the years of stigma. He was determined to avoid it.

The company secured emergency liquidity, drawing on credit facilities and managing working capital with surgical precision. Capital expenditures were slashed to maintenance levels. Every dollar was tracked. Every expenditure was questioned. Hiring was frozen. Travel was eliminated. The goal was brutally simple: do not run out of cash.

They did not run out of cash. But the margin by which they avoided it was far narrower than most people outside the company realized.

VI. The Turnaround: Portfolio Simplification and Restructuring (2020-2022)

The playbook DelGrosso executed over the next two years was brutally simple in concept and extraordinarily difficult in practice: sell everything that was not core automotive seating, use the proceeds to pay down debt, fix the operations that remained, and ride the eventual recovery in global auto production. There was no magic here. No pivoting to software, no exciting new growth narratives. Just relentless focus on doing one thing—making car seats—as well as possible.

The divestitures came in rapid succession. Effective January 1, 2020, Adient sold its RECARO Automotive Seating business—the premium performance brand acquired through the 2011 Keiper deal—to Raven Acquisitions LLC. RECARO had approximately 425 employees across three locations and generated roughly $150 million in annual revenue. It was a respected brand with genuine consumer recognition, a rarity in automotive supply. But it was a niche business, and DelGrosso had no patience for niches. Every management hour spent on RECARO was an hour not spent fixing the core.

On January 31, 2020, Adient entered into an agreement with Yanfeng to fundamentally restructure their tangled web of joint ventures. The deal, amended in June and closed on August 21, received $309 million in cash for Adient's thirty percent stake in Yanfeng Global Automotive Interior Systems, the massive YFAI interiors venture that had once been the world's largest. An additional $20 million came from selling certain mechanisms business patents, with $60 million more due on a deferred basis—roughly $379 million in total plus IP proceeds. The interiors business was gone. The seating joint venture, Yanfeng Adient Seating, was extended to December 2038, preserving Adient's crucial position in the Chinese market.

In March 2020—with the world shutting down around them—Adient announced the sale of its automotive fabrics manufacturing business to Sage Automotive Interiors, a subsidiary of Japan's Asahi Kasei, for $175 million. The deal encompassed eleven facilities globally, mostly in Europe, and approximately 1,300 employees. It closed on September 30, 2020.

In October 2019, DelGrosso had already reduced Adient's ownership in the Boeing airline seating joint venture from 50.01 percent to 19.9 percent, effectively deconsolidating it from Adient's financial statements. The airline seat dream was over before it had really begun.

Step back and consider what DelGrosso had done. In roughly two years, he sold the interiors joint venture stake, the RECARO brand, the fabrics business, and the meaningful Boeing stake. Each divestiture followed the same logic: remove complexity, generate cash, narrow focus.

By the time the portfolio simplification was complete, Adient was a fundamentally different company. The business that had tried to be everything—automotive interiors, airline seats, premium performance brands, fabric manufacturing—was now focused with almost monastic discipline on one thing: making automotive seats and their core components. Frames, foam, mechanisms, trim covers, and complete assemblies. Nothing else.

There is a temptation to view this as a retreat—the company shrinking because it could not handle its ambitions. But that misses the strategic logic. Every one of those divested businesses consumed management attention, capital, and operational complexity that the core business desperately needed. RECARO was a wonderful brand, but managing a four-hundred-person niche performance seat business was a distraction when two hundred factories needed operational discipline. The Boeing venture was intellectually exciting, but it was a startup inside a company that could not yet run its own existing operations profitably.

DelGrosso understood something that many corporate leaders miss: in a crisis, the hardest thing is not deciding what to do. It is deciding what to stop doing. And then actually stopping it.

In 2021, the China strategy underwent its most dramatic transformation. Adient sold its 49.99 percent stake in Yanfeng Adient Seating to Yanfeng for approximately $1.5 billion in cash—roughly $1.4 billion after tax. In exchange, Adient acquired direct ownership of certain Chinese operations, including YFAS's fifty percent interest in CQYFAS and one hundred percent of YFAS-Langfang. The move gave Adient its own operational footprint in China rather than relying entirely on joint venture structures. The company retained a 50/50 Keiper joint venture with Yanfeng for seat mechanisms and maintained an estimated forty to forty-five percent share of the Chinese passenger seating market—a commanding position.

Simultaneously, the company attacked its cost structure in Europe. The EMEA region was plagued by overcapacity—too many plants chasing too few vehicles as European auto production declined and Chinese imports intensified. Plant closures and workforce reductions proceeded methodically, trading short-term restructuring costs for long-term margin improvement.

On November 8, 2023, Adient announced that Doug DelGrosso would retire as president and CEO effective December 31—on his own terms, a rarity for turnaround CEOs who typically exit either in triumph or disgrace. Over five years, he had taken a company hemorrhaging $32 million per week and transformed it into one generating meaningful free cash flow. His reflection was characteristically understated: "Restoring the importance of operational excellence and execution in the business, and culturally getting back to those roots and acknowledging the importance of that as an automotive supplier."

His successor was Jerome Dorlack, an internal promotion that signaled continuity over disruption. Dorlack had joined Adient in 2018 as vice president and chief purchasing officer, risen to VP of the Americas region from 2019 to 2022, and then served as executive vice president and CFO from 2022 to 2023. Before Adient, he had held senior leadership roles at Aptiv (formerly Delphi), including president of electrical distribution systems and president of South America operations, and spent seventeen years at ZF/TRW Automotive in engineering, commercial, quality, and purchasing roles. He held an undergraduate degree and MBA from the University of Toledo. Mark Oswald, previously VP of treasury and investor relations, stepped into the CFO role.

The foundation had been built. The debris had been cleared. The five-year saga from spin-off crisis to stabilization was, for all practical purposes, complete. Now came the harder and, in some ways, more interesting question: could Adient build something durable and valuable on top of that foundation? To answer that, it helps to understand exactly how the automotive seating business creates—and captures—value.

VII. The Modern Business Model: How Adient Actually Works

To truly understand Adient's competitive position—and its structural challenges—requires understanding how the automotive seating business works in practice. It is far more complex and far less glamorous than most people realize.

A modern automotive seat is not a single product. It is a system composed of dozens of components working in concert. At the base sits a metal frame—typically stamped steel or, increasingly, lightweight materials—that provides structural integrity and crash protection. Layered onto that frame is polyurethane foam, carefully formulated and poured into molds shaped to specific ergonomic profiles. Think of it like a mattress custom-designed for a specific car model. A reclining mechanism—a precision-machined metal assembly of gears, springs, and levers—allows the seatback to tilt. A track mechanism lets the entire seat slide forward and back. Head restraints, armrests, lumbar supports, and trim covers complete the assembly. A premium front seat today might contain heating and cooling elements, massage motors, position memory electronics, and side-airbag deployment systems. All told, a complete front seat assembly can contain more than a hundred individual parts.

Adient operates across this entire value chain. Its solutions include complete seating systems—delivered fully assembled, ready to bolt into a vehicle—as well as individual components that OEMs integrate into their own designs. Some customers buy everything; others cherry-pick. This flexibility is a competitive advantage, allowing Adient to serve a wide range of customer needs, but it also means the company must maintain capabilities across a remarkably broad technical spectrum.

The just-in-time delivery model is absolutely central to understanding the economics. Automobile assembly plants operate on tightly choreographed sequences—think of a ballet performed by robots and humans together, where each vehicle moving down the line needs its specific seat configuration delivered at exactly the right moment. A red leather interior for the luxury sedan, followed by a cloth seat for the base model, followed by a heated package for the cold-weather option. A delay of even a few hours can shut down an entire assembly line, and automakers calculate that downtime in millions of dollars per day.

This constraint means Adient's manufacturing plants must be located near the assembly plants they serve—typically within a few hours' drive. You cannot ship a complete seat assembly from China to a GM plant in Michigan and maintain just-in-time delivery. This geographic proximity requirement creates an enormously expensive but practically irreplaceable manufacturing footprint. With more than two hundred plants across twenty-nine countries, Adient has spent decades and billions of dollars building this web of localized production. For any potential new entrant, replicating it would require a decade and a fortune.

The customer relationship model is equally distinctive. Winning a new seating program is not like winning a purchase order—it is more like winning a multi-year government contract. The process begins years before the first vehicle rolls off the line, with design concepts, engineering proposals, prototyping, and extensive validation testing. Once a supplier wins a program, it is generally locked in for the life of that vehicle platform—typically five to seven years—with pricing agreed upfront and annual cost-reduction targets of two to three percent baked into the contract. These cost-downs mean that Adient must continuously improve its manufacturing efficiency just to maintain the same margin on existing business. Standing still means going backward.

Innovation remains critical to winning future programs. Adient's Vision Seat concept, debuted at the 2017 North American International Auto Show, represented a ground-up rethinking of seat design. Rather than starting from traditional construction assumptions, the engineering team studied how human bodies actually move and distribute weight while sitting—drawing on the science of human anthropometry—and created a seat with interdependent sub-components producing a thinner, lighter profile with greater comfort. More recently, in August 2025, Adient unveiled the ModuGo Seat, a modular design inspired by building blocks. Built on a recyclable platform, the ModuGo enabled a thirty-six percent improvement in assembly efficiency, a thirty-four percent reduction in total processes, and output increases from fifty seats per hour to seventy-eight with the same workforce. For an industry where manufacturing efficiency directly determines profitability, these gains are not incremental—they are transformational.

The fundamental challenge, however, is the margin structure—and it is worth dwelling on this because it is the single most important fact about the automotive supply business.

Automotive seating suppliers typically operate on mid-single-digit operating margins—dramatically lower than most industries of comparable complexity and capital intensity. To put that in perspective: a software company like Microsoft might operate at forty percent margins. A consumer staple like Procter & Gamble might run at twenty percent. A well-run retailer might achieve ten percent. Adient operates at five to six percent. That means for every dollar of revenue, roughly ninety-four to ninety-five cents goes to materials, labor, factory overhead, depreciation, and selling costs. The company keeps a nickel.

Why so thin? Because the customer—the automaker—holds the power. When you have a handful of buyers who collectively determine ninety-plus percent of your revenue, and those buyers can credibly threaten to switch to your three or four major competitors for the next program, you do not have pricing power. You have pricing pressure. Annual cost-down requirements of two to three percent mean you must become meaningfully more efficient every single year just to maintain the same margin on the same contract.

This margin reality means that even small execution errors—a botched program launch, a spike in raw material costs, a customer disruption—can swing a profitable quarter to a loss. There is almost no cushion. When things go wrong, as they did spectacularly in 2018, the losses can compound with breathtaking speed because there is no fat to absorb the impact.

For investors, this margin structure is not a bug to be fixed—it is a feature of the industry's architecture, baked into the power dynamics between OEMs and suppliers. The question is whether operational excellence and scale can push that margin even modestly higher over time—from five percent to seven or eight percent, say—or whether competitive and customer pressures will forever cap returns at these levels.

VIII. The EV Transition and Strategic Positioning

The electric vehicle revolution has created a paradox for automotive seating suppliers: enormous long-term opportunity wrapped in painful near-term disruption. The global automotive industry has experienced significant uncertainty as consumer adoption of EVs proved slower and more uneven than the euphoric projections of 2021-2022 suggested. Weakening demand, shifting government subsidies, and automakers repeatedly pushing back their electrification timelines have created a choppy operating environment.

But for seating specifically, the EV transition carries a subtler—and more bullish—subtext that is easy to miss. Electric vehicles tend to feature higher seating content per vehicle than their internal combustion counterparts. This is partly because many EV platforms target the premium segment, where seat sophistication is a selling point. But it is also because EV architecture—a flat battery floor, no transmission tunnel, different packaging constraints—opens up fundamentally new possibilities for interior design.

Consider what happens when you remove the engine from the front of a car and the driveshaft running through the middle. Suddenly, the interior becomes a different space entirely. Seats can be positioned differently. The flat floor allows for more creative configurations.

And when autonomous driving eventually arrives—whether in five years or fifty—the seat transforms from a driving instrument into something fundamentally different: a living space, a workspace, a place to sleep. Picture a morning commute where you step into your autonomous vehicle, press a button, and your seat swivels to face the rear, converting the cabin into a mobile office. Or imagine a long-haul trip where all four seats recline flat and the family sleeps as the car drives itself through the night.

These configurations—swiveling, reclining, rotating, reconfiguring—require dramatically more complex seating systems than today's fixed-forward designs. More mechanisms. More electronics. More engineering. And crucially, more value per vehicle for the supplier who can deliver them.

Adient has positioned itself deliberately for this future. The company developed interiors concepts for autonomous driving featuring seats that can rotate to face rear passengers—turning a car into a mobile meeting room or living room.

As alternative usage models evolve—car sharing, urban mobility, ride-hailing fleets—the implications for seating are counterintuitive. You might think fewer cars means less demand for seats. But shared vehicles experience far more wear and need more durable, cleanable, and reconfigurable seating. Ride-hailing vehicles may need to accommodate passengers of vastly different sizes and preferences within a single day. Adient sees the potential for greater seating content and complexity per vehicle, not less.

The company won a position in General Motors' future EV car programs—a significant validation of both its technology and its competitiveness in the emerging segment. The Pure Essential Seat, designed specifically for EV platforms, exemplifies the approach: it uses just two primary eco-friendly material types—green steel and recyclable polyester—to promote product circularity while being especially lightweight, responding to EV manufacturers' acute need for mass reduction to preserve battery range. The ProX IsoDynamic Seat, developed jointly with Toyota and Multimatic, won first place in the 2023 Altair Enlighten Award in the module lightweighting category for its innovative back frame design.

On sustainability more broadly, Adient has established measurable targets validated by the Science Based Targets initiative. The company reported a thirty-eight percent reduction in global scope 1 and scope 2 greenhouse gas emissions compared to 2019, targeting a seventy-five percent reduction by 2030. Roughly thirty percent of global electricity consumption comes from renewable sources, with a goal of one hundred percent renewable electricity at manufacturing sites by 2035. Through its ES3 framework—Evolution of Seating Systems Sustainability—the company is working with suppliers to reduce scope 3 value chain emissions by thirty-five percent by 2030, embedding design for disassembly and material recyclability from the earliest development stages.

These sustainability investments are not merely corporate positioning. European automakers in particular increasingly mandate that suppliers meet specific environmental standards as a condition of doing business. For a company deriving substantial revenue from European OEMs, these are competitive necessities, not optional extras.

The near-term challenge remains the pace and unpredictability of the transition itself. Production scheduling has become less predictable as automakers repeatedly adjust their EV launch timelines—some pushing programs forward, others delaying by years or canceling entirely. For a seating supplier that commits engineering resources and manufacturing capacity three to five years before vehicles reach production, this uncertainty creates real financial risk. Tooling investments made for a vehicle program that gets delayed or canceled may never generate the returns they were designed to deliver.

But Adient possesses one significant advantage over pure-play EV component suppliers: platform agnosticism. A seat designed for an EV platform can be adapted for an internal combustion vehicle, and vice versa. The underlying engineering—foam, frames, mechanisms—is fundamentally the same regardless of what powers the drivetrain. This means Adient does not need to bet on the exact pace of EV adoption. Whether the industry electrifies in five years or twenty-five, people will still need seats. The question is whether Adient can capture the higher value per vehicle that more sophisticated EV and autonomous configurations promise.

IX. Regional Dynamics and Competitive Landscape

Adient's global business operates across three distinct theaters, each with its own competitive dynamics, growth trajectory, and risk profile. Understanding the regional picture is essential to understanding the investment case.

In the Americas, Adient benefits from deep, longstanding relationships with the Detroit Three—General Motors, Ford, and Stellantis—as well as with transplant manufacturers like Toyota, Honda, and Hyundai assembling vehicles in North America. The region's shift toward trucks and SUVs—vehicles that tend to feature more elaborate seating with heating, cooling, power adjustment, and premium materials—has been generally positive for revenue per unit.

But the Americas also carry particular vulnerability to labor actions, as the 2019 GM strike demonstrated with devastating clarity. Customer concentration risk is acute here: when your largest customer shuts down production for five weeks, the financial impact cascades immediately through your entire regional operation. Adient cannot simply redirect those seats to another buyer. They were designed for a specific vehicle, in a specific plant, on a specific schedule. When that schedule stops, everything stops.

Europe, the Middle East, and Africa represent Adient's most troubled region—and its most significant strategic concern.

EMEA faces a toxic combination of structural headwinds. Production volumes have been declining as European consumers hold onto cars longer and urbanization reduces per-capita vehicle ownership. The factories that once served higher volumes now operate with excess capacity, spreading fixed costs over fewer units and crushing margins.

To make matters worse, Chinese automotive imports are intensifying competition in a market already oversupplied. Chinese automakers like BYD and MG are gaining meaningful market share in Europe, and they often bring their own supply chain relationships with them, bypassing established Western suppliers.

The financial implications are stark. In company filings, the difference between EMEA's estimated fair value and its accounting carrying value was less than ten percent—a yellow flag in accounting terms that signals a heightened risk of impairment. If European production volumes continue to decline or Chinese competition intensifies further, Adient may be forced to write down the value of its European assets, taking a significant non-cash charge against earnings. In April 2024, the company announced further job cuts in Europe and began transferring roles to lower-cost countries, with restructuring costs surging to $125 million in a single quarter.

China presents yet another dynamic. Adient commands an estimated forty to forty-five percent of the Chinese passenger seating market—a dominant position built over decades through the Yanfeng partnership. The company continues to operate through joint ventures in China, and the dividends flowing from these ventures are an important component of overall free cash flow. But the competitive landscape is shifting. The rise of domestic Chinese automakers—BYD, NIO, Li Auto, XPeng, and others—and their preference for local suppliers creates a long-term risk of share erosion. The automotive supply market in China is intensely competitive, and Adient itself acknowledges in its filings that market participants will "act aggressively to increase or maintain their market share."

Adient's ability to leverage leadership across all three regions—using scale advantages in one geography to support competitiveness in others, particularly in emerging markets like Southeast Asia—remains a genuine advantage. But regional weakness in any one market propagates through the entire system, affecting global purchasing leverage and fixed-cost absorption.

The competitive landscape features several formidable rivals. Lear Corporation reports approximately $23.5 billion in total revenue, with operating margins consistently above eleven percent—roughly double Adient's. Lear has distinguished itself through vertically integrated operations and intelligent seating systems incorporating thermal comfort and wellness monitoring. FORVIA, the entity formed from the merger of Faurecia and Hella, brings approximately twenty-seven billion euros in total revenue and strong R&D in lightweight structures and sustainable materials. Toyota Boshoku leverages its intimate relationship with Toyota Motor Corporation. Magna International operates seating as one segment of a broadly diversified supplier business.

What distinguishes Adient is primarily scale and geographic breadth. No other seating supplier operates in as many markets with as large a manufacturing footprint. This scale advantage translates into purchasing leverage with raw material suppliers—when you buy steel and foam chemicals by the millions of tons, you negotiate from a position of strength. It also means research and development costs can be spread across more units of production, and operational best practices developed in one region can be transferred to others.

But scale in automotive supply is a double-edged sword. More factories mean more fixed costs to cover. More countries mean more regulatory complexity. More employees mean more labor relationships to manage. Whether Adient's massive scale generates sufficient returns to justify the complexity and capital it requires is the central strategic question—and one the market, with its discounted valuation, has not yet answered in the affirmative.

X. Financial Recovery and Current State

The financial trajectory from crisis to recovery tells one of the more remarkable turnaround stories in recent automotive history—not because it involved daring strategic pivots or revolutionary innovation, but because it was achieved through the relentless, unglamorous blocking and tackling of operational improvement and balance sheet repair.

For fiscal year 2024, ending September 30, Adient generated $277 million of free cash flow—real cash, after all capital expenditures, that the company could deploy as it chose. It returned $275 million to shareholders through share repurchases, buying back its own stock at what management clearly believed were depressed valuations. The company also paid down approximately $130 million in debt. Revenue was $14.69 billion, with adjusted EBITDA of approximately $881 million and a cash balance of $945 million.

Fiscal 2025 demonstrated stability in a challenging environment. Revenue came in at $14.54 billion, essentially flat year-over-year despite unfavorable volume trends across multiple regions. Adjusted EBITDA held steady at $881 million—evidence that the operational improvements were durable, not just one-time gains. Free cash flow was $204 million. The company returned $125 million through repurchases, representing approximately seven percent of shares outstanding at the start of the year. Since the board authorized a $600 million repurchase program in November 2022, Adient had bought back more than 18.4 million shares.

The balance sheet tells the most dramatic part of the story. Gross debt stood at approximately $2.4 billion as of September 30, 2025, with net debt—after subtracting cash holdings—at about $1.4 billion. Net leverage had fallen to 1.7 times adjusted EBITDA, comfortably within management's target range of 1.5 to 2.0 times. Compare that to the $3.5 billion in gross debt at spin-off, loaded onto a business whose earnings were collapsing, and the magnitude of the deleveraging becomes clear. The company's probability of financial distress was estimated at less than three percent—a dramatic change from the existential uncertainty of 2020.

The first quarter of fiscal 2026, ending December 31, 2025, showed encouraging momentum. Revenue was $3.64 billion, up 4.3 percent year-over-year. Adjusted EBITDA reached $207 million. Management raised full-year revenue guidance to $14.6 billion and maintained EBITDA guidance of $880 million, noting that tariff costs under current policies were expected to be "largely mitigated" through commercial and operational actions.

The stock, trading in the mid-twenties range in early 2026, reflects a market that acknowledges the turnaround but still prices in significant risk. A market capitalization of roughly $2 billion against nearly $15 billion in revenue and $881 million in EBITDA translates to less than four times EV/EBITDA—a valuation that remains at a meaningful discount to both historical multiples and peer averages. In February 2026, Deutsche Bank upgraded the stock from Hold to Buy, while UBS maintained a Buy rating, both citing valuation and free cash flow potential.

The dividend, suspended since fiscal 2018, has not been reinstated. Management has prioritized debt reduction and share repurchases—a decision that reflects both ongoing balance sheet prudence and an implied belief that the stock is undervalued. When a company's management chooses buybacks over dividends, they are making an implicit statement: they believe the shares are worth more than the market price. Whether that conviction is justified depends on Adient's ability to sustain and improve its earnings power—a question that brings us to the structural forces shaping the company's competitive position.

XI. Strategic Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding Adient's competitive position requires examining the structural forces that shape the automotive seating industry—forces that constrain even the best-managed companies and explain why this business is so challenging despite its enormous scale. Applying both Porter's Five Forces and Helmer's Seven Powers frameworks reveals a nuanced picture.

Threat of New Entrants: Low. This is one of the few structural factors firmly in Adient's favor. Building a global seating manufacturing footprint requires billions of dollars in capital investment, decades of customer relationship development, and the ability to pass rigorous OEM homologation and qualification processes that take years.

The just-in-time delivery requirement alone creates a towering barrier: any serious competitor needs manufacturing facilities near every major automotive production cluster worldwide. You cannot build that overnight. This is why the same handful of players—Adient, Lear, FORVIA, Magna, Toyota Boshoku—have dominated the global seating market for decades. New entrants appear only at the regional level or in niche segments, never at global scale.

Supplier Bargaining Power: Moderate. The raw materials Adient purchases—steel, foam chemicals, leather, textiles—are relatively commoditized and available from multiple sources. The company's enormous purchasing volume provides leverage.

However, specialized components, particularly seat mechanisms and embedded electronics, involve more concentrated supplier bases. The COVID pandemic exposed the fragility of these supply chains when shortages of specific materials cascaded through the entire automotive industry, shutting down assembly lines worldwide.

Buyer Bargaining Power: High. This is where the structural challenge is most acute—and it is the single most important force shaping the economics of every automotive seating supplier.

A small number of global automakers control the vast majority of vehicle production, and they use that concentration to extract aggressive pricing. Contracts are awarded through competitive bidding with multiple negotiation rounds. Annual cost-reduction targets of two to three percent are standard and non-negotiable. OEMs can credibly threaten to backward-integrate or shift volume to competitors for the next program.

This creates persistent, relentless pricing pressure that no amount of operational excellence can fully escape. It is the defining structural headwind of the industry.

Threat of Substitutes: Nil. Every vehicle needs seats. No technology exists to replace them. This provides a floor of demand stability that most industries would envy—but it also means there is no way to create scarcity or premium pricing for the core product.

Competitive Rivalry: Intense. Lear, FORVIA, Magna, and Toyota Boshoku all operate at global scale with deep engineering capabilities. Price-based competition in commoditized segments—standard cloth seats for economy vehicles, for example—leaves almost no margin. Differentiation through technology is possible at the premium end but is typically short-lived, as competitors replicate advances within a product cycle or two.

Through Hamilton Helmer's strategic framework, Adient's competitive moat rests primarily on two pillars. Scale economies are its strongest advantage: the global footprint spreads fixed costs across enormous production volume, R&D investments are amortized across millions of units, and purchasing leverage provides real cost advantages versus smaller competitors. Process power is its secondary moat: Adient employs a common product development process globally through ten core development centers using a globally consistent approach. The manufacturing excellence and JIT delivery capabilities refined over decades are genuinely difficult for competitors to replicate quickly—a factory culture of zero-disruption delivery discipline cannot be purchased; it must be built over years.

The other Helmer powers are limited. Network effects are minimal in business-to-business supply. Counter-positioning is weak because incumbents can replicate innovations. Switching costs exist mid-program but reset with each new vehicle platform award. Branding matters in the B2B context but carries minimal consumer visibility. And cornered resources are essentially absent—no unique intellectual property or talent pool that Adient exclusively controls.

The overall structural assessment is sobering but essential for any investor to internalize. Adient operates in an industry where even the market leader faces persistent pressure from powerful buyers, intense competition, and cyclical demand volatility. Scale and process excellence provide meaningful but not unassailable advantages.

Here is a useful analogy. Think of the automotive supply chain as a river system. The OEMs—Toyota, GM, Volkswagen, Hyundai—sit at the mouth of the river, controlling the flow and capturing the richest fishing grounds. Tier 1 suppliers like Adient sit upstream, essential to the ecosystem but subject to whatever flow the downstream players allow. Being the biggest boat on the river helps—you can navigate better, carry more, and weather storms more effectively. But you cannot control the current. That current is set by the automakers, and it flows in one direction: toward lower prices for suppliers.

This is an industry where structural headwinds can cap returns regardless of management quality. Understanding this context is essential for evaluating both the bull case and the bear case.

XII. Bull versus Bear Case

The bull case for Adient centers on the magnitude of the transformation already achieved and the runway that remains. This company went from losing $1.7 billion in a single year to generating nearly $300 million in free cash flow. That is not theoretical—it is demonstrated across multiple years of financial statements.

The deleveraging from $3.5 billion to $2.4 billion in gross debt has created financial flexibility that simply did not exist during the crisis years. Management is now actively returning capital to shareholders through buybacks—something that would have been unthinkable in 2019, when employees were being furloughed over the holidays and analysts were questioning the company's survival.

The EV transition, despite near-term noise, represents a structural tailwind for seating content per vehicle. Electric and eventually autonomous vehicles require more sophisticated, higher-value seats—swiveling mechanisms, lie-flat configurations, integrated electronics for comfort and wellness monitoring. As the market leader across all three major regions, Adient is positioned to capture outsized share of this growing content opportunity.

Valuation provides an additional lens. An enterprise value of roughly $3.4 billion against $881 million in EBITDA represents less than four times EV/EBITDA—a multiple implying deep skepticism about future earnings power. If operational improvements continue to close even a portion of the margin gap with competitors like Lear, the potential for multiple re-rating is meaningful. Management's choice to prioritize buybacks at these depressed levels sends a clear signal about their view of intrinsic value.

The bear case is equally serious—and it is rooted in structural industry dynamics that no management team, however talented, can fully overcome.

Automotive suppliers are inherently low-margin, cyclical businesses operating at the mercy of production volumes they do not control and pricing they cannot set. Weakening consumer demand has resulted in lower automotive production volumes across key markets, and there is no guarantee this is temporary rather than secular. The rise of remote work, ride-sharing, and urbanization may permanently reduce per-capita vehicle ownership in developed markets.

EMEA impairment risk is quantifiable and real. The fair value of the European reporting unit sits within ten percent of its carrying value—an accounting yellow flag that means further deterioration could trigger a significant writedown. European auto production continues to face headwinds from regulatory uncertainty, the slow EV transition, and intensifying Chinese competition. This is not a hypothetical risk—it is flagged in the company's own filings.

Chinese competition presents a longer-term challenge. As domestic Chinese automakers grow—BYD, NIO, Li Auto, XPeng—they are increasingly building relationships with local suppliers who can deliver at lower cost. Adient's dominant forty to forty-five percent market share in China was built during an era of foreign automaker dominance. The question is whether that share can hold as the market shifts toward domestic brands with domestic supply chain preferences.

Capital intensity constrains free cash flow conversion even in good years. Maintaining two hundred plants across twenty-nine countries requires continuous investment in equipment, tooling, and facility maintenance. And the suspended dividend—still not reinstated after nearly eight years—is a persistent reminder that the balance sheet, while improved, still demands priority attention over shareholder returns.

Myth versus reality. The consensus narrative holds that the Adient turnaround is "complete." The reality is more nuanced. Operationally, enormous progress has been made—undeniably. Financially, the balance sheet is dramatically healthier. But the margin gap versus competitors like Lear—which operates at roughly double Adient's margins—has not been closed.

This gap may reflect structural disadvantages in product mix, customer concentration, or geographic exposure rather than simply fixable operational issues. Lear has invested heavily in "intelligent seating" with electronic comfort systems, while Adient has focused more on the mechanical and structural side. The mix matters: higher-tech content commands higher margins.

Investors should ask the critical question: is the margin gap closeable, or is it permanent?

For investors tracking Adient's ongoing performance, two KPIs matter above all else.

First, adjusted EBITDA margin. This is the single most important indicator of whether operational improvements are translating into genuine earnings power. Adient currently operates at roughly six percent EBITDA margin. Lear operates above eleven percent. The question of whether Adient can close that gap—even partially—is the question of whether this is a turnaround that is still unfolding or one that has already delivered its full value. Every basis point of margin improvement on a $14.5 billion revenue base translates to roughly $14.5 million of additional EBITDA. The math is powerful if the trajectory is in the right direction.

Second, free cash flow generation. Free cash flow is the ultimate output of any industrial business—the cash remaining after all operating costs, capital expenditures, and working capital changes have been paid. It is the money available for debt reduction, share buybacks, dividends, or reinvestment. Adient generated $277 million in fiscal 2024 and $204 million in fiscal 2025. Whether that level can be sustained and grown in a cyclically challenged environment determines the company's ability to continue deleveraging while returning capital to shareholders.

These two numbers, tracked quarter by quarter, tell the essential story: is Adient gradually becoming a better business, or is it treading water in a structurally difficult industry? Everything else is commentary.

XIII. Lessons for Founders and Investors

Adient's journey from spin-off to near-bankruptcy to recovery offers lessons that extend well beyond the automotive industry—lessons about capital structure, value chain economics, and the art of corporate survival. These are the kinds of lessons that apply whether you are investing in auto parts or analyzing any company in a competitive, capital-intensive industry.

The Spin-Off Trap. The conventional wisdom holds that spin-offs create value by providing management focus, strategic clarity, and investor transparency. Academic research broadly supports this—spin-offs have historically outperformed the market over the following two to three years. But the mechanism of the spin-off matters enormously.

When Johnson Controls loaded Adient with $3.5 billion in debt and extracted $3 billion in cash before completing the separation, it created a company structurally designed to enrich its parent at the offspring's expense. This is not unique to Adient—it is a pattern that recurs across corporate separations. Investors who buy spin-offs based on the thesis that "pure-play focus creates value" must examine the balance sheet first. Market leadership means nothing if the debt load is designed to fail.

Capital Structure is Destiny. Even with the world's largest market position, the best customer relationships, and seventy-five thousand employees, Adient could not overcome its debt burden when operational execution faltered. The $125 million in annual interest expense consumed resources that should have gone toward fixing troubled plants and investing in new programs.

This is a universal lesson. In any industry with mid-single-digit margins, the distance between manageable leverage and fatal leverage can be measured in fractions. A debt load that looks comfortable when business is strong becomes crushing when volumes dip even modestly. The automotive industry's cyclicality means that downturns are not a possibility—they are a certainty. Capital structure must be built to survive the trough, not just the peak.

Value Chain Positioning. Adient is a case study in understanding where power lies in an industrial value chain. The automotive supply chain is defined by enormous power asymmetries—OEMs at the top dictating terms, suppliers competing ferociously for the right to serve them. Suppliers face high costs to serve multiple OEMs with customized products—specific tooling, dedicated engineering, proximity manufacturing. OEMs face relatively low costs to switch between competing suppliers for the next program. This asymmetry permanently constrains supplier economics and is the root cause of the thin margins that define the industry.

For investors evaluating any business, the lesson is clear: before analyzing management quality or growth prospects, understand who holds power in the value chain. If your customers can easily replace you, your margin ceiling is set by competition, not by your own capabilities.

The Turnaround Playbook. DelGrosso's approach offers enduring insights for anyone managing a troubled business. His method was defined by focus, portfolio simplification, and operational discipline—not by visionary strategy or breakthrough innovation.

He killed the Boeing venture. He sold RECARO. He divested the fabrics business. He directed every resource toward making the core automotive seating operation work. He decentralized authority to regional leaders who knew their factories. He was brutally honest with employees about the sacrifices required.

The work was unglamorous and took five years. But this is what real turnarounds look like: not dramatic pivots or flashy strategies, but incremental operational improvement compounding patiently over time. The compound effect of hundreds of small improvements—fewer customer disruptions, lower premium freight costs, better launch management, tighter cost controls—eventually adds up to a fundamentally different business.

Patient Capital Wins. An investor who bought at the March 2020 low and held through the recovery captured extraordinary returns. But recognizing that opportunity required conviction in the face of overwhelming pessimism—a company with three billion in cumulative losses, a stock at $6.53, and a global pandemic shutting down every factory on Earth.

The direction of the turnaround was visible to anyone who studied the operational metrics carefully—the shrinking losses, the declining customer disruptions, the portfolio divestitures. The timing, however, was not. Patient capital requires both the analytical conviction to see through the crisis and the emotional temperament to hold while the market prices in catastrophe.

Industry Structure Matters. Perhaps most importantly, Adient demonstrates that some businesses are structurally challenging regardless of management quality. The seating industry's economics—high buyer power, intense competition, thin margins, massive capital requirements—create a ceiling on returns that even exceptional operators struggle to exceed.

This does not mean such businesses are uninvestable. It means they must be analyzed through a different lens. You are not buying growth potential or expanding competitive moats—you are buying operational execution and cyclical positioning. The entry price matters enormously because the upside is inherently capped by industry structure. DelGrosso and Dorlack have executed admirably. Whether execution alone can generate consistently superior returns in this structural environment remains the open question.

Crisis Management Without Bankruptcy. Finally, Adient offers a masterclass in navigating near-bankruptcy without actually filing. The costs of avoiding formal restructuring proceedings were enormous—furloughs, plant closures, thirteen thousand eliminated positions, and years of financial austerity.

But the costs of filing would have been worse. In automotive supply, bankruptcy destroys the single most important intangible asset: customer trust. OEMs need to know their seating supplier will be there for the five-to-seven-year life of a vehicle program—honoring warranties, managing recalls, delivering just-in-time through every business cycle. A bankruptcy filing shatters that confidence and makes winning new business exponentially harder.

DelGrosso, having taken Chassix through Chapter 11, understood this calculus better than perhaps anyone in the industry. He chose the harder path—survival through operational repair rather than legal reset—and it worked. The scars remain. But the company is alive, functioning, and generating cash.

XIV. What Is Next for Adient

Adient enters 2026 as a fundamentally different company than the one that staggered out of the Johnson Controls separation a decade ago. The company reported consolidated revenue of $14.7 billion for fiscal 2024 and guided to approximately $14.4 billion for fiscal 2025. The operational turnaround is real, the balance sheet is meaningfully healthier, and management has demonstrated discipline in capital allocation.