Archer Daniels Midland: The Soybean King's Empire

I. Introduction & Episode Roadmap

Picture this: It's 1972, and a cargo ship loaded with American soybeans docks at a Soviet port. The Cold War is at its peak, yet here's an American agricultural executive shaking hands with Communist Party officials. That executive is Dwayne Andreas, and his company, Archer Daniels Midland, has just orchestrated one of the most audacious deals in commodity trading history—selling millions of tons of grain to the Soviet Union during a global food crisis. This moment encapsulates everything ADM would become: politically connected, globally ambitious, and utterly essential to feeding the world.

Today, ADM is a $85.53 billion revenue colossus that processes the corn in your soda, the soybeans in your burger, and the wheat in your bread. From its headquarters in Chicago (though spiritually still rooted in Decatur, Illinois), the company operates over 270 plants and 420 crop procurement facilities across six continents. It's the kind of company that most Americans have never heard of, yet touches their lives three times a day at every meal.

But how did a Minneapolis linseed crusher founded in 1902 transform into what Fortune magazine once called "the supermarket to the world"? The answer involves political kingmaking, technological revolution, corporate scandal that inspired a Hollywood movie, and the fundamental transformation of how humanity feeds itself.

This is a story of three distinct eras: the consolidation play that built an agricultural processing empire (1902-1970), the Andreas dynasty that weaponized political influence to reshape global food systems (1970-1997), and the modern struggle to reinvent commodity trading for a world demanding sustainability and transparency (1997-present). Along the way, we'll encounter FBI raids, price-fixing conspiracies, and the complex moral calculus of feeding 8 billion people while navigating capitalism's darker impulses.

The ADM story poses fundamental questions: Can a company be both essential infrastructure for civilization and a monument to corporate excess? What happens when the line between public good and private profit becomes so blurred that even the participants can't see it? And perhaps most importantly—in an age of climate change and resource scarcity, what role should these agricultural giants play in humanity's future?

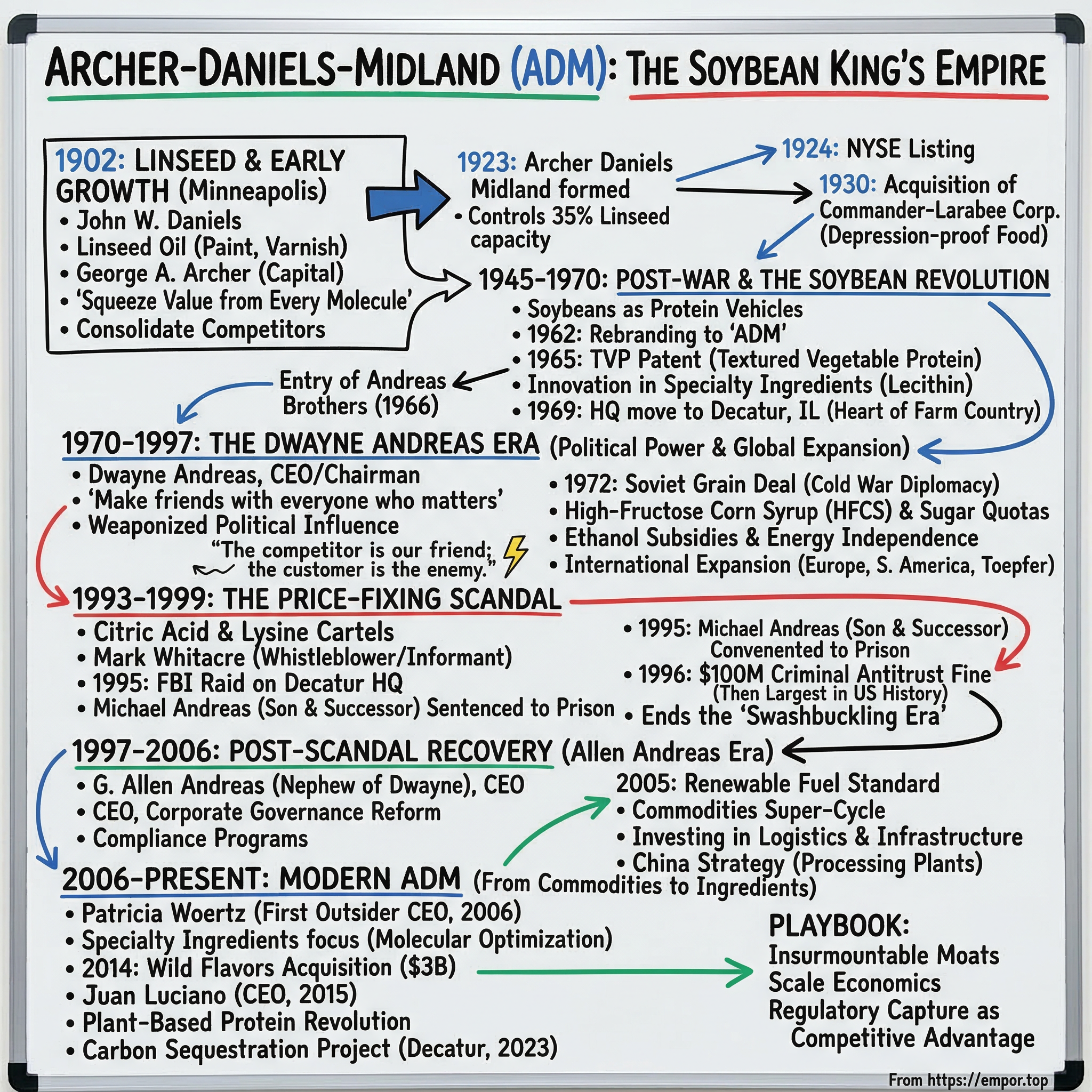

II. The Minneapolis Origins: Linseed to Empire (1902-1945)

The American Midwest in 1902 was experiencing its own version of a gold rush—except instead of precious metals, entrepreneurs were chasing the oils hidden inside humble seeds. John W. Daniels, a former traveling salesman who'd spent years learning the grain trade, saw opportunity where others saw agricultural waste. Linseed oil, pressed from flax seeds, was becoming industrial gold—essential for paints, varnishes, and the booming construction industry of a rapidly urbanizing America.

Daniels started his crushing operation in Minneapolis with a simple premise: buy flax from farmers, extract the oil, sell both the oil and the protein-rich meal left behind as animal feed. Nothing was wasted. It was a philosophy that would define ADM for the next century—squeeze value from every molecule of agricultural output.

When George A. Archer joined the operation in 1903, he brought something Daniels lacked: serious capital and financial sophistication. Archer had made his fortune in oilseed trading and understood that the real money wasn't just in processing, but in controlling the entire supply chain. Together, they incorporated as Archer-Daniels Linseed Company in 1905, setting up a partnership structure that would endure: operational expertise married to financial engineering.

The company's early growth strategy was brutally simple—buy out competitors during downturns when prices were cheap. The agricultural commodities business has always been cyclical, with boom years followed by devastating busts. While other processors went bankrupt during bad harvests or price collapses, Archer-Daniels had the capital to survive and acquire. By 1923, this roll-up strategy reached its crescendo with the acquisition of Midland Linseed Products Company. The combined entity, now christened Archer Daniels Midland Company, controlled 35% of America's linseed crushing capacity with assets exceeding $11 million—massive for that era. The listing on the New York Stock Exchange on Christmas Eve 1924—December 24, 1924—represented more than financial legitimacy. It was ADM joining the ranks of America's industrial elite, transforming from a regional processor into a company with national ambitions. The timing was perfect: America's agricultural abundance was becoming its competitive advantage in global markets.

But it was the acquisition of Commander-Larabee Corp. in 1930 that revealed ADM's true strategic genius. While the country descended into the Great Depression, ADM gained the ability to produce 32,000 barrels of flour daily. This wasn't just vertical integration—it was a bet that even in economic catastrophe, people still needed to eat. The company's focus on essential foodstuffs rather than discretionary products would prove prescient.

The 1927 establishment of ADM's grain division marked another crucial pivot. Rather than just processing what farmers brought them, ADM began actively trading and storing grain. They built massive silos along rail lines, creating a physical network that would later become their moat. By controlling storage and transportation bottlenecks, ADM could smooth out the violent price swings that destroyed smaller competitors.

World War II transformed ADM from a successful regional player into a critical component of the American war machine. The company's facilities ran 24/7 producing oils for military applications—everything from protective coatings for equipment to ingredients for K-rations. Government contracts provided guaranteed demand and profits, allowing ADM to modernize its facilities with taxpayer support. It was the beginning of a beautiful friendship between ADM and Washington that would define the company's next half-century.

By 1945, ADM had established the playbook it would follow for decades: consolidate fragmented markets, build scale advantages, maintain close government relationships, and focus relentlessly on turning agricultural commodities into higher-value products. The linseed crushers had become an agricultural-industrial complex, perfectly positioned for the post-war boom about to transform American agriculture.

III. Post-War Expansion & The Soybean Revolution (1945-1970)

The year 1952 marked a psychological turning point for ADM. With 5,000 employees and operations spanning the globe, manufacturing over 700 products, the company had achieved something remarkable: it had become too big to see. Unlike the consumer brands filling American supermarkets, ADM operated in the shadows of the food system, its products hidden inside other companies' products. This invisibility would become its greatest strategic asset.

The real revolution began with a humble bean that most Americans couldn't even pronounce correctly. Soybeans had been cultivated in Asia for millennia, but in post-war America, they were about to become the most important crop nobody talked about. ADM recognized what others missed: soybeans were protein-delivery vehicles that could transform American agriculture from a carbohydrate business into a protein business.

The 1962 rebranding to "ADM" wasn't mere corporate vanity. Those three letters would become synonymous with agricultural innovation, starting with the company's 1965 patent for textured vegetable protein (TVP). This wasn't just a new product—it was alchemy. ADM had figured out how to turn soy flour into something that looked, felt, and tasted remarkably like meat. By 1966, the Decatur East Plant was churning out this miracle ingredient that would quietly revolutionize processed foods.

The technology behind TVP revealed ADM's approach to innovation: take abundant, cheap agricultural inputs and transform them through industrial processes into specialized, high-margin ingredients. It was a philosophy that turned the company into an R&D powerhouse, employing more food scientists than many universities. The entry of the Andreas brothers in 1966 marked the beginning of ADM's transformation from a competent regional processor into a global powerhouse. Dwayne Andreas and his brother Lowell Andreas became minority shareholders in ADM after Shreve "Bud" Archer, Jr. offered to sell them 100,000 shares at about half its book value, for a total of $3.3 million. The company was struggling—ADM had decreases in net income for four years in a row, from $4.421 million in 1962 to $2.765 million in 1965. The Andreas brothers saw opportunity where others saw decline.

The 1969 headquarters relocation from Minneapolis to Decatur, Illinois was more than geographic repositioning. Decatur sat in the heart of corn and soybean country, surrounded by the raw materials that would fuel ADM's growth. The move signaled a strategic shift: ADM would no longer be content processing whatever farmers brought them. They would shape American agriculture itself.

By this point, ADM was already considered one of the world's largest agribusiness companies, with a labor force of more than 24,000 employees. The company had quietly built an empire while America obsessed over space races and social revolutions. ADM's revolution was happening in farm fields and processing plants, transforming how the world would eat.

The soybean revolution wasn't just about production—it was about creating demand for products nobody knew they needed. TVP could extend ground beef in school lunches, making budgets stretch further. Soy protein isolates could improve the texture of processed foods. Lecithin became an essential emulsifier in everything from chocolate to cosmetics. ADM wasn't just processing soybeans; they were creating an entire ecosystem of soy-based ingredients that would become invisible yet indispensable to modern food production.

IV. The Dwayne Andreas Era: Political Power & Global Expansion (1970-1997)

Dwayne Andreas was named CEO of ADM in 1970, and two years later was elected chairman of the company's board. What followed was perhaps the most audacious expansion of corporate political influence in American history. Andreas didn't just run a company—he architected a system where ADM's interests became indistinguishable from national agricultural policy.

The Andreas doctrine was elegantly simple: make friends with everyone who matters, regardless of party. Andreas was one of the most prominent political campaign donors in the United States, having contributed millions of dollars to Democratic and Republican candidates alike. While not well known to the public, Andreas commanded much respect among Washington politicians for his largesse. This wasn't corruption in the traditional sense—it was something more sophisticated. Andreas had discovered that in the agricultural-industrial complex, the line between public policy and private profit had already been erased.

Consider the breathtaking scope of his relationships: President Harry S. Truman sent Mr. Andreas to Argentina to cut a deal with President Juan Perón and his wife, Eva "Evita" Perón. Mr. Andreas took Cuba's Fidel Castro to dinner in New York, rode on Air Force One with President Bill Clinton to Nixon's funeral, sold Dole a condominium in Florida and helped broker a meeting between Gorbachev and President Ronald Reagan. When O'Neill was introduced to Gorbachev in Moscow, Gorbachev reportedly told him, "I hear you know my friend Dwayne Andreas".

This wasn't mere socializing. Every relationship served ADM's strategic interests. The Soviet grain deals of the 1970s, which Andreas helped orchestrate, turned ADM into a critical player in Cold War diplomacy. The company could feed America's enemies when it served U.S. foreign policy—and make massive profits doing so. The real genius of Andreas's strategy became clear with the twin innovations that would define modern American food: high-fructose corn syrup and ethanol. In the mid-1970s, ADM had begun developing a method originally from Japan for making a concentrated liquid sweetener out of corn. The timing was perfect—or rather, Andreas made it perfect. In the mid-1970s, ADM had begun tinkering with a method developed in Japan for making a concentrated liquid sweetener out of corn — high-fructose corn syrup — that might appeal to the booming soft-drink industry.

But there was a problem: HFCS couldn't compete with sugar on price. So Andreas orchestrated one of the most audacious market manipulations in corporate history. In 1978, as oil prices soared in response to a Middle East crisis, Dwayne Andreas approached President Carter with a plan for energy independence: jumpstart ethanol production with a tax break. Meanwhile, he lobbied for sugar import quotas that would artificially inflate domestic sugar prices. The 1981 sugar quotas changed everything overnight—suddenly HFCS was cheaper than sugar, and Andreas had created a captive market worth billions.

In 1977, the average American consumed 9.6 pounds of high fructose corn syrup per year. By 1990 they were consuming almost 50 pounds per year. This wasn't just market share capture—it was dietary transformation on a civilizational scale. ADM had literally changed what Americans ate, how food tasted, and arguably, the shape of American bodies themselves.

The ethanol story followed a similar playbook. Turn corn into fuel, get the government to mandate its use, collect subsidies for production. It was corporate welfare perfected, with ADM collecting what critics estimated to be billions in direct and indirect government support while maintaining the fiction of free-market capitalism.

The international expansion during this period was equally strategic. Under his leadership, Archer Daniels Midland acquired many smaller agricultural companies and expanded into international markets, eventually becoming one of the world's largest agricultural processing companies. Under his leadership, ADM grew from 40 processing plants and about 3,000 employees in the Midwest to 274 processing plants with 23,000 workers around the world. Its soybean exports shot up from $1.5 billion to $7 billion.

The 1974 expansion into Europe and South America with soybean plants in Holland and Brazil wasn't just geographic diversification—it was about controlling global agricultural flows. The 1982 acquisition of a portion of Toepfer International, Germany's largest grain trader, gave ADM unprecedented insight into global commodity movements. They could see supply and demand shifts before competitors, positioning themselves to profit from every market dislocation.

But perhaps the most revealing aspect of the Andreas era was the corporate culture it created. In a tape played at the trial, ADM's President said that a single phrase inspired the company: "Our competitors are our friends. Our customers are the enemy." This wasn't a slip of the tongue—it was corporate philosophy. In ADM's worldview, competition was something to be managed through cartels and price-fixing, not market forces.

The sheer audacity of Andreas's influence-peddling defied belief. When critics accused ADM of corporate welfare, Andreas didn't deny it—he celebrated it. He famously said "There isn't one grain of anything in the world that is sold in a free market. Not one! The only place you see a free market is in the speeches of politicians." It was breathtakingly cynical and absolutely accurate.

By the mid-1990s, ADM had become something unprecedented in American business: a company whose political influence was so vast that it had essentially privatized agricultural policy. The federal government's farm programs, trade policies, and even foreign relations often seemed designed primarily to benefit ADM's bottom line. It was a masterpiece of regulatory capture, executed with such skill that most Americans never even knew it was happening.

V. The Price-Fixing Scandal: FBI Raids & The Informant (1993-1999)

The morning of June 27, 1995, started like any other at ADM's Decatur headquarters. Then the FBI arrived. Not just a few agents making inquiries—dozens of them, armed with search warrants, boxes for evidence, and the kind of grim determination that meant someone was going to prison. The raid was the culmination of one of the most bizarre corporate espionage cases in American history, featuring a whistleblower who was simultaneously stealing millions from the company he was helping to investigate.

At the center of it all was Mark Whitacre, a rising star at ADM who had been secretly recording his colleagues for three years. Whitacre would later become the highest-ranking corporate whistleblower in FBI history, though his motivations remained murky even after everything came to light. Was he a hero exposing corporate corruption, a delusional fantasist, or simply another corporate criminal who got caught and tried to trade his way out? The answer was somehow all three.

The scheme itself was elegantly simple in its criminality. ADM and its competitors would meet—sometimes in hotel rooms, sometimes at trade conferences—and agree on prices for lysine, an amino acid used in animal feed, and citric acid, used in soft drinks and detergents. They divided up market share like mob bosses carving up territory. The executives even had a motto for their cartel: "The competitor is our friend; the customer is our enemy."

What made the conspiracy particularly brazen was how open they were about it. In recordings made by Whitacre, executives can be heard laughing about price-fixing, comparing themselves to the mafia, and expressing zero concern about getting caught. One executive joked that they should be meeting in a phone booth with trench coats and sunglasses. They thought they were untouchable.

Andreas remained CEO until 1997, the year that Archer Daniels pleaded guilty to price-fixing and paid $100 million in fines. This scandal also sent his only son, Michael Andreas to prison. Michael was the anointed successor as Andreas started to devolve his power. It was his son who hatched the plan to create global cartels in citric acid and lysine.

The involvement of Michael Andreas, Dwayne's son and heir apparent, transformed the scandal from corporate crime to Greek tragedy. Michael had been groomed since childhood to take over ADM. He had his father's intelligence and ambition but apparently also inherited a belief that rules simply didn't apply to the Andreas family. The price-fixing scheme was partially his attempt to prove he could deliver profits just like his father—except his father's methods, while ethically questionable, were generally legal.

In 1999, Michael Andreas, and two colleagues were sentenced to prison terms ranging from 24 to 36 months. The sight of Michael Andreas in handcuffs was shocking not just because of who he was, but because it suggested that even ADM wasn't above the law—a proposition that had seemed dubious given the company's political connections.

The $100 million fine ADM paid in 1996 was the largest criminal antitrust fine in U.S. history at the time, though for a company with ADM's revenues, it was essentially a rounding error. More damaging was the reputational hit and the scrutiny it brought to ADM's entire business model. Suddenly, journalists and regulators were asking uncomfortable questions about everything from ethanol subsidies to campaign contributions.

The scandal also exposed the weakness of ADM's corporate governance. The board was stacked with Andreas allies and family members, creating what critics called a "culture of entitlement" where executives believed they were beyond accountability. Some shareholders said the board was too cozy with management to prevent the price-fixing scandal that erupted when FBI agents raided ADM's Decatur headquarters.

Mark Whitacre's story added another layer of absurdity to an already surreal scandal. While working as an FBI informant, he was embezzling millions from ADM, money he claimed was owed to him as bonuses. When this came to light, it destroyed his credibility as a witness and complicated the prosecution's case. Whitacre eventually served more time in prison than the executives he exposed—eight and a half years for embezzlement versus the two to three years the price-fixers received.

The 2009 film "The Informant!" starring Matt Damon captured the dark comedy of the situation but perhaps understated just how damaging the scandal was to ADM's carefully cultivated image. For decades, the company had portrayed itself as feeding the world, a noble enterprise essential to human survival. The price-fixing scandal revealed something uglier: a company so obsessed with profits that it would conspire to overcharge the very farmers it claimed to serve.

Dwayne Andreas's response to the scandal was revealing. Andreas remained CEO until 1997, the year that Archer Daniels pleaded guilty to price-fixing and paid $100 million in fines... Andreas stepped down as chairman in 1999 and was succeeded by his nephew, G. Allen Andreas. He maintained he knew nothing about the price-fixing, a claim that stretched credulity given his famous attention to detail and the involvement of his own son. But whether through genuine ignorance or plausible deniability, Andreas avoided prosecution.

The scandal's aftermath fundamentally changed how antitrust law was enforced in America. The FBI's use of extensive wiretapping and video surveillance in the ADM case became a template for future investigations. The large fines and actual prison sentences for executives sent a message that white-collar crime would be taken seriously—at least sometimes.

For ADM, the scandal marked the end of an era. The swashbuckling, anything-goes culture of the Andreas years was no longer tenable in an age of increased scrutiny and activist shareholders. The company would have to find a new way forward, one that at least maintained the appearance of ethical business practices. The question was whether ADM could survive without the political manipulation and market-rigging that had fueled its growth for so long.

VI. Post-Scandal Recovery & The Allen Andreas Era (1997-2006)

When G. Allen Andreas took over as CEO in 1997, he inherited a company in crisis. ADM's stock price had plummeted, its reputation was in tatters, and federal investigators were still prowling through corporate documents. The nephew of Dwayne Andreas faced an impossible task: maintain ADM's profitability while dismantling the very systems that had made those profits possible.

Allen Andreas was everything his uncle wasn't—quiet, analytical, and allergic to publicity. Where Dwayne had ruled through force of personality and political connections, Allen governed through spreadsheets and strategic planning. His first priority was corporate governance reform. The board was restructured to include more independent directors, though critics noted that true independence was relative when dealing with a company as politically connected as ADM.

The new compliance programs ADM implemented were extensive and expensive. Every international meeting required documentation. Price discussions with competitors became forbidden territory. Employees underwent hours of antitrust training. It was corporate rehabilitation theater, necessary to convince regulators and investors that ADM had changed. Whether the culture had truly shifted was another question entirely.

Fortunately for Allen Andreas, external forces were aligning in ADM's favor. The early 2000s saw the beginning of what economists would later call the commodities super-cycle. China's explosive economic growth was creating unprecedented demand for soybeans and other agricultural products. Global population growth and rising meat consumption in developing countries meant more demand for animal feed. ADM didn't need to fix prices when legitimate demand was driving them skyward anyway.

The ethanol boom provided another lifeline. The Renewable Fuel Standard, passed in 2005, mandated that billions of gallons of renewable fuel be blended into America's gasoline supply. It was exactly the kind of government intervention that Dwayne Andreas had spent decades cultivating, except now it was even more lucrative. Ethanol production capacity exploded, and ADM was perfectly positioned to capture the profits.

But Allen Andreas understood something his uncle perhaps hadn't: the world was changing, and ADM needed to change with it. The company began investing heavily in logistics and infrastructure, building port facilities, railcar fleets, and river barges. This wasn't as sexy as political influence-peddling, but it created real competitive advantages that couldn't be legislated away.

The company also began a quiet shift from pure commodity processing toward higher-value ingredients. While ADM would always be in the business of crushing soybeans and milling corn, the real margins were in specialized products—proteins for sports drinks, fibers for health foods, enzymes for industrial applications. It was a strategy that required actual innovation rather than political manipulation.

The China strategy during this period deserves special attention. While American politicians debated farm bills, ADM was building processing plants in China, establishing joint ventures with local companies, and creating supply chains that would fundamentally reshape global agriculture. By 2006, China had become ADM's fastest-growing market, a position that would have seemed impossible just a decade earlier.

Allen Andreas also had to navigate the continuing legal fallout from the price-fixing scandal. In addition ADM's 2005 annual report revealed that earlier that year the company settled a class-action antitrust suit for a payment of $400 million. These settlements were expensive, but they allowed ADM to close the book on the scandal and move forward.

The post-scandal era also saw ADM become more sophisticated in its political activities. Rather than the crude influence-buying of the Dwayne Andreas era, the company focused on shaping policy through trade associations, think tanks, and academic research. It was a subtler approach, though no less effective. ADM remained one of Washington's biggest corporate players, just with better lawyers and more careful documentation.

By 2006, when Allen Andreas stepped down, ADM had largely recovered from the price-fixing scandal. Revenues were growing, the stock price had recovered, and the company had avoided any new major scandals. It was a competent, professional performance that lacked the drama of his uncle's tenure but provided the stability ADM needed.

The Allen Andreas era proved that ADM could survive without the swashbuckling corruption of its past, though whether it could thrive was still an open question. The company remained dependent on government subsidies, trade policies, and agricultural programs that favored large processors. The fundamental business model—turning government-subsidized crops into products that often required government mandates to sell—hadn't changed. Only the tactics had become more sophisticated.

VII. Modern ADM: From Commodities to Ingredients (2006-Present)

Patricia Woertz's appointment as CEO in 2006 was revolutionary for ADM—not just because she was the first woman to lead the company, but because she was the first outsider. A former Chevron executive, Woertz brought an oil industry perspective to agricultural processing, seeing commodities not as food but as molecules to be optimized. Her arrival signaled ADM's ambition to transform from an old-economy processor into a modern industrial biotechnology company.

Woertz immediately grasped that ADM's future lay not in bulk commodities but in specialty ingredients. The strategy was simple but profound: instead of selling corn syrup by the tanker, sell specific molecular components by the gram. Instead of generic soy protein, develop targeted nutritional solutions for specific health conditions. The margins on these specialty products could be ten times higher than traditional commodity processing.

The 2014 acquisition of Wild Flavors for $3 billion represented the boldest move in this transformation. Wild Flavors didn't crush soybeans or mill corn—it created natural flavors, colors, and ingredients for food companies desperate to clean up their labels. Suddenly, ADM could offer customers not just raw ingredients but complete sensory solutions. It was a business Dwayne Andreas would barely recognize. When Juan Luciano took over as CEO in January 2015, becoming the ninth chief executive in ADM's 112-year history, he brought yet another outsider perspective—this time from Dow Chemical. He was named president in February 2014, and in January 2015 became the ninth chief executive in ADM's 112-year history. Luciano understood that ADM's transformation needed to accelerate. The commodities super-cycle was ending, China's growth was slowing, and consumers were becoming increasingly conscious about what they ate.

Under Luciano's leadership, ADM has undergone a remarkable evolution, building on more than a century of heritage to create a global nutrition business, with an industry-leading array of ingredients and solutions that are opening the door to growth opportunities in key global macro trend areas. The company restructured into three main segments: Ag Services and Oilseeds, Carbohydrate Solutions, and Nutrition—with the Nutrition segment representing the future.

The numbers tell the story of transformation. Full-Year Reported EPS of $3.65, Adjusted EPS of $4.74 in recent results show a company that remains profitable despite massive strategic shifts. But more importantly, the Nutrition division now generates margins multiple times higher than traditional commodity processing, even as it represents a smaller portion of total revenue.

The plant-based protein revolution presented both opportunity and threat. ADM had been making textured vegetable protein since 1965, but suddenly everyone from venture-backed startups to established food giants wanted sophisticated protein ingredients. ADM responded by investing hundreds of millions in new protein facilities, developing everything from pea protein isolates to fermented proteins that could replicate the texture and taste of animal products.

Sustainability, once an afterthought, became central to ADM's strategy. He has spearheaded the increased use of innovative technologies to meet customer needs, and led a strategic growth campaign that has expanded ADM's global footprint, building capabilities and adding talent and expertise that allow it to create value at every part of the global value chain. The company announced ambitious carbon reduction targets, invested in regenerative agriculture programs, and began marketing "low-carbon" versions of its commodities to sustainability-conscious customers.

The carbon sequestration project in Decatur represents this new approach. In March 2023, the Decatur City Council voted unanimously to allow ADM to expand its carbon sequestration program onto city land, with the company paying the city $450 per acre of land. The agreement enabled ADM to inject liquified carbon dioxide into "pore space" 1.25 miles under land owned by the city of Decatur. It's a project that generates both environmental benefits and potential carbon credit revenue—the kind of win-win that defines modern ADM.

But challenges remain formidable. Commodity price volatility has intensified, not diminished. The biofuel policy landscape remains uncertain as electric vehicles threaten long-term ethanol demand. Climate change is making agricultural production increasingly unpredictable. And new competitors, from tech companies to alternative protein startups, are attacking ADM's traditional markets with novel approaches.

The company's response has been to become more technology-focused. ADM now employs data scientists alongside food scientists, using artificial intelligence to optimize everything from crop yields to ingredient formulations. Digital tools track shipments in real-time, predict equipment failures before they happen, and identify new ingredient applications through computational modeling.

Yet for all the transformation, ADM remains fundamentally what it has always been: a company that profits from the inefficiencies in global food systems. Whether processing soybeans into oil and meal or developing novel proteins for plant-based burgers, the business model is consistent—take abundant agricultural inputs and transform them into higher-value outputs. The sophistication has increased dramatically, but the basic arbitrage remains.

The modern ADM operates in a world Dwayne Andreas would barely recognize—one where ESG scores matter as much as earnings, where consumers track supply chains, where carbon footprints affect purchasing decisions. Yet in another sense, nothing has changed. ADM still depends on government policies, still benefits from agricultural subsidies, still profits from its position between farmers and food companies. The methods have evolved, but the game remains the same.

VIII. Playbook: Business & Investing Lessons

The ADM story offers a masterclass in how to build and maintain a commodity processing empire, though perhaps not always for the right reasons. The lessons are both tactical and philosophical, revealing uncomfortable truths about how American capitalism actually works versus how we pretend it works.

Lesson 1: Vertical Integration in Commodities Creates Insurmountable Moats

ADM's genius wasn't in processing grain—anyone with capital could build a mill. The genius was in controlling every step from farm to fork. Own the storage, own the transportation, own the processing, own the distribution. When you control the entire supply chain, you don't compete on price; you set the price. Competitors can't enter the market because they'd need to replicate billions in infrastructure. It's the commodity equivalent of Amazon's fulfillment network—theoretically replicable, practically impossible.

Lesson 2: Political Relationships Are the Ultimate Competitive Advantage (Until They're Not)

Dwayne Andreas understood something most CEOs don't: in heavily regulated industries, political capital is more valuable than financial capital. Every dollar donated to politicians returned hundreds in subsidies, tax breaks, and favorable regulations. The ethanol mandate alone has generated tens of billions in revenue for ADM. But the price-fixing scandal showed the danger of believing you're above the law. Political protection has limits, especially when the FBI has you on tape.

Lesson 3: Scale Economics in Agricultural Processing Are Exponential

The difference between processing 1,000 bushels and 10,000 bushels isn't 10x—it's perhaps 3x in costs but 10x in revenue. This creates a winner-take-all dynamic where the biggest processors can offer better prices to farmers and still maintain higher margins than smaller competitors. ADM understood this mathematics early and pursued scale relentlessly, even when individual acquisitions seemed expensive.

Lesson 4: Commodity Cycles Are Features, Not Bugs

Most companies fear commodity price volatility. ADM learned to profit from it. When prices spike, their inventory becomes more valuable. When prices crash, they can buy cheap inputs. The key is maintaining flexible processing capabilities that can shift between products based on relative pricing. A plant that can make either ethanol or corn syrup depending on market conditions is far more valuable than one locked into a single product.

Lesson 5: Information Asymmetry Is Everything

ADM's global network didn't just move grain—it moved information. Knowing that drought hit Australian wheat fields or that China was about to increase soybean purchases provided massive trading advantages. In commodity markets, information arrives in microseconds but understanding its implications takes expertise. ADM had both the data and the knowledge to interpret it.

Lesson 6: Corporate Governance Actually Matters (Eventually)

For decades, ADM's board was a rubber stamp for Andreas family decisions. This worked until it didn't. The price-fixing scandal might have been prevented by independent directors asking uncomfortable questions. The modern ADM, with its improved governance, may be less swashbuckling but it's also less likely to see executives in handcuffs.

Lesson 7: Transformation Requires External DNA

Every major transformation at ADM came from outside leadership. Patricia Woertz brought oil industry discipline. Juan Luciano brought chemical industry innovation. Internal promotions maintain culture but external hires drive change. For investors, leadership transitions from outside the industry often signal strategic inflection points.

Lesson 8: The Power of Boring Businesses

ADM has never been sexy. It's never had the cache of tech companies or the visibility of consumer brands. This invisibility is a feature, not a bug. It allowed ADM to build dominant positions without attracting attention from regulators or competitors. The best businesses are often the ones nobody talks about at cocktail parties.

Lesson 9: Regulatory Capture Is a Sustainable Competitive Advantage

This is the uncomfortable truth of ADM's success. By shaping the very regulations that govern their industry, they created competitive advantages that no amount of innovation or efficiency could overcome. Ethanol mandates, sugar quotas, crop subsidies—these weren't market distortions ADM adapted to; they were market distortions ADM created.

Lesson 10: ESG Is the New Political Influence

Modern ADM can't buy politicians as brazenly as Dwayne Andreas did. But they can fund sustainability research, support regenerative agriculture, and position themselves as essential to fighting climate change. ESG isn't just about doing good—it's about creating the same kind of regulatory moat that political donations once provided, just with better optics.

The ADM playbook ultimately reveals an uncomfortable truth about American business: the most successful companies aren't necessarily the most innovative or efficient. They're the ones that best understand and exploit the intersection of business and government. Whether that's through campaign contributions or carbon credits, the game remains the same—privatize profits while socializing costs, all while maintaining the fiction of free-market capitalism.

IX. Analysis & Bear vs. Bull Case

The Bull Case: Essential Infrastructure for Humanity

ADM bulls start with an irrefutable fact: the world needs to eat, and ADM sits at the center of the global food system. With operations spanning six continents and touching virtually every agricultural supply chain, ADM has achieved a scale and scope that would take competitors decades and hundreds of billions to replicate.

The demographic math is compelling. Global population will reach 9.7 billion by 2050, with most growth in regions transitioning to protein-rich diets. Every additional middle-class consumer in Asia or Africa represents increased demand for the animal feed, cooking oils, and processed ingredients that form ADM's core business. The protein transition alone—as developing nations increase meat consumption—could double demand for soybean meal and other feed ingredients.

Climate change, paradoxically, strengthens ADM's position. As weather becomes more volatile and crop failures more common, ADM's global sourcing network becomes increasingly valuable. They can source Brazilian soybeans when U.S. crops fail, or pivot to Ukrainian corn when Argentine harvests disappoint. This flexibility commands premium pricing in an uncertain world.

The financial characteristics are attractive for value investors. ADM generates robust free cash flow even in down cycles—typically $2-3 billion annually. The dividend has been paid continuously since 1927, through Depression, wars, and scandals. At current valuations, the company trades at roughly 10-12x earnings, a significant discount to the broader market despite its essential nature.

The transformation story adds growth to value. The Nutrition segment, while still small, grows at double-digit rates with margins 3-4x higher than commodity processing. If ADM can successfully shift even 20% of revenue to specialty ingredients, overall margins could expand by 200-300 basis points. Plant-based proteins, precision fermentation, and personalized nutrition represent multi-billion dollar opportunities where ADM's capabilities provide real advantages.

The Bear Case: Structural Decline Masked by Cyclical Gains

Bears see ADM as a melting ice cube, generating cash today but facing inexorable decline tomorrow. The core business—turning subsidized corn into ethanol and high-fructose corn syrup—depends on government policies increasingly under attack. Electric vehicles will eventually destroy ethanol demand. Health concerns are crushing high-fructose corn syrup consumption. When these props disappear, what's left?

Commodity processing is a terrible business getting worse. Margins have compressed for decades as information asymmetries disappear and markets become more efficient. ADM's vaunted scale advantages matter less when farmers can check global prices on smartphones and sell directly to end users through digital platforms. The moat is wide but shallow and evaporating.

Climate change is an existential threat, not an opportunity. ADM's assets are concentrated in regions becoming increasingly vulnerable to extreme weather. Droughts, floods, and heat waves don't just affect individual harvests—they can destroy processing infrastructure, disrupt transportation networks, and render long-term investments worthless. The company's carbon footprint also makes it a target for increasingly aggressive climate regulation.

Competition is intensifying from unexpected directions. Tech companies are using AI and satellite imagery to provide the market intelligence that was once ADM's exclusive domain. Vertical farms and cellular agriculture threaten to bypass traditional agriculture entirely. Even in traditional markets, state-backed Chinese competitors with unlimited capital are building competing infrastructure.

The governance and regulatory risks remain substantial. ADM operates in countries where corruption is endemic and regulatory capture is being challenged. The next price-fixing scandal, environmental disaster, or food safety crisis could trigger billions in liabilities. The company's history suggests these aren't theoretical risks but inevitable realities.

Valuation and Comparative Analysis

Compared to peers, ADM trades at a modest discount. Bunge trades at similar multiples but with more emerging market exposure. Cargill remains private, denying investors comparable metrics. Louis Dreyfus, also private, reportedly generates similar margins but with a more trading-focused model.

The key valuation question isn't whether ADM is cheap—it clearly is on traditional metrics. The question is whether those metrics matter if the business model is structurally impaired. A company trading at 10x earnings is expensive if those earnings are about to disappear.

The balance sheet provides some comfort, with moderate leverage and substantial asset backing. But those assets—processing plants, storage facilities, transportation infrastructure—have value only if the underlying commodity flows continue. In a world of declining meat consumption, reduced biofuel demand, and localized food systems, these assets could become stranded.

The Verdict: A Value Trap or Opportunity?

ADM represents a fascinating investment paradox. It's simultaneously essential and endangered, dominant and disrupted, transforming and trapped by its past. The bull case rests on humanity's basic needs and ADM's irreplaceable position. The bear case sees structural decline accelerated by technological and social change.

For investors, ADM is best viewed as an option on the status quo. If global food systems continue operating roughly as they have, ADM will generate substantial cash flows for decades. If systemic change accelerates—through climate catastrophe, technological disruption, or political upheaval—ADM could face existential challenges.

The most likely scenario is somewhere between: a slow transformation where ADM gradually shifts from commodity processing to specialty ingredients, maintains relevance through strategic adaptation, but never again achieves the extraordinary returns of its politically connected past. For patient investors who believe in management's ability to navigate this transition, current valuations may offer attractive risk-reward. For those who see accelerating disruption, ADM looks like a value trap—cheap for good reason.

X. Epilogue & Reflections

Standing in Decatur, Illinois today, you can still smell the sweet, yeasty aroma of corn processing that blankets the city like morning fog. The ADM plants run 24/7, their industrial cathedral towers and pipeline mazes transforming midwest grain into the molecular building blocks of modern food. It's a smell that residents have lived with for generations—the olfactory signature of American agricultural capitalism.

What ADM tells us about American agriculture is both inspiring and troubling. On one hand, companies like ADM solved humanity's oldest problem: hunger. The efficient processing and distribution of agricultural products helped feed billions, prevented famines, and enabled the population growth that defines our modern world. The technical achievements are staggering—turning inedible soybeans into protein that sustains livestock, creating sweeteners that make processed food affordable, developing ingredients that extend shelf life and prevent waste.

Yet ADM also embodies the moral compromises of industrial agriculture. The company profited from turning food into fuel while millions remained malnourished. It corrupted political systems, fixed prices, and concentrated power in ways that would make the robber barons blush. The same efficiency that fed the world also created monocultures, depleted soils, and contributed to obesity epidemics.

The tension between feeding the world and corporate concentration remains unresolved. ADM and its peers have created a system so efficient that food has never been cheaper in human history. But that efficiency comes from scale, and scale leads to concentration, and concentration leads to power that corrupts. Can we have one without the other? Can we feed 10 billion people without corporate giants like ADM? The answer remains unclear.

Looking forward, the future of agribusiness will be shaped by three forces: technology, climate, and geopolitics. Precision agriculture, gene editing, and alternative proteins will transform what we grow and how we grow it. Climate change will reshape where food can be produced and how it moves around the world. Rising nationalism and resource competition will challenge the global trade systems that companies like ADM depend upon.

ADM's response to these challenges will determine whether it remains relevant for another century or becomes a relic of industrial age agriculture. The company's investments in sustainability, nutrition, and technology suggest an understanding that transformation is necessary. But transformation is easier to announce than achieve, especially for a company with ADM's history and complexity.

The governance and culture questions remain particularly relevant. Has ADM truly reformed from its price-fixing past, or has it simply become more sophisticated in its methods? The company's continued dependence on government subsidies and regulations suggests that while the tactics have evolved, the fundamental strategy—profiting from the intersection of business and government—remains unchanged.

Perhaps the most profound question ADM raises is about the nature of essential industries in democratic societies. Some companies become so important to basic functioning that they transcend normal business categories. They're neither fully private nor fully public, but exist in a gray zone where profit motives mix with public obligations. ADM feeds the world, but to whom is it ultimately accountable?

The final reflection must be on Dwayne Andreas's famous quote: "There isn't one grain of anything in the world that is sold in a free market. Not one!" He meant it as justification for ADM's political manipulations, but perhaps it's better understood as diagnosis. In industries essential to human survival, pure free markets may be neither possible nor desirable. The question isn't whether governments should intervene in agricultural markets, but how those interventions should be structured and who should benefit.

ADM's story continues to unfold, shaped by forces beyond any single company's control. Climate change, technological disruption, and shifting consumer preferences will create opportunities and challenges we can barely imagine. Whether ADM navigates these successfully will depend not just on strategic choices and operational excellence, but on its ability to balance private profits with public purpose.

The smell of corn processing still hangs over Decatur, a reminder that for all our technological progress, we remain dependent on the ancient alchemy of turning seeds into sustenance. ADM has industrialized that alchemy, scaled it globally, and profited enormously from it. Whether that model survives the 21st century—and whether we want it to—remains an open question. What's certain is that the story of ADM, like the story of modern agriculture itself, is far from over.

XI. Recent News

ADM reported full-year 2024 net earnings of $1.8 billion with adjusted net earnings of $2.3 billion. Full-year earnings per share came in at $3.65, with adjusted earnings per share of $4.74, both declining from the previous year. The company's trailing four-quarter average return on invested capital (ROIC) was 6.7%, with adjusted ROIC at 8.3%.

In a significant strategic move, ADM announced targeted actions to deliver $500-750 million in cost savings over the next several years, signaling management's recognition of challenging market conditions ahead. Looking ahead, ADM is managing expectations with a cautious outlook for 2025, indicating potential challenges due to market fundamentals and policy uncertainties. The company plans to focus on strategic investments and cost management to navigate the evolving market landscape.

The company continues to face legal challenges related to accounting irregularities. A federal court denied four motions to dismiss a securities lawsuit filed against Archer Daniels Midland and four of its current and former executives in connection with irregular accounting practices revealed by the company. The U.S. District Court for the District of Northern Illinois last week denied dismissal motions filed by ADM and its CEO Juan Luciano, now-former CFO Vikram Luthar, former vice chairman and CFO Ray G. Young, along with Vince Macciocchi, former president of nutrition and chief sales and marketing officer. U.S. District Judge Thomas M. Durkin said in his opinion and order handed down on March 12 that he believed there is sufficient evidence for the case to continue.

The accounting issues center on ADM's Nutrition segment, which had been positioned as a key growth driver. The shareholders alleged that ADM and its officers made "false or misleading" statements about the "performance and prospects of ADM's nutrition segment and its accounting practices." In particular, the lawsuit said ADM made "positive statements" about that segment of the business as a "future profit-driver" for the company. "Defendants also created the impression that the nutrition segment's growth would provide more diversification and earnings stability for ADM," the lawsuit said. "This was an appealing strategy because the company's results were historically tied to the highly cyclical commodities market." The shareholders allege that ADM's nutrition segment growth from 2020 to 2022 was "inaccurate and subject to improper accounting practices".

On the operational front, ADM's Board of Directors has extended and expanded its share repurchase program. The program, which originally authorized the purchase of 100 million shares between 2015-2019, was first extended to 2024 and increased to 200 million shares in 2019. Now, it has been further extended to December 31, 2029, with an additional authorization of 100 million shares, bringing the total program authorization to 300 million shares. Currently, 114,764,049 shares remain available for future repurchases.

In a positive development, ADM has been awarded the 2025 BIG Innovation Award by the Business Intelligence Group for its groundbreaking regenerative agriculture program. The program was recognized for its innovative approach to transforming global food systems through advanced technologies, partnerships, and sustainable farming practices. The award, which celebrates industry-advancing organizations, was determined by a panel of business leaders evaluating creativity, measurable results, and overall impact. ADM's program specifically focuses on reducing greenhouse gas emissions and enhancing soil health, creating tangible benefits for both farmers and the environment.

The company also experienced a product recall issue. The recall spans 33 lot numbers of feed products distributed between January 16-February 27, 2025, across six states: Illinois, Missouri, Tennessee, Iowa, Georgia, and Ohio. While no illnesses have been reported, excessive copper exposure could cause gastroenteritis symptoms including anorexia, depression, and diarrhea, while zinc deficiency may impact feed intake and growth. The issue was discovered during routine production testing. ADM has begun notifying customers and removing affected products from retail shelves. Customers are advised to stop using the recalled feed immediately and return it for a full replacement or refund.

XII. Links & References

Long-Form Articles & Books

- "The Informant" by Kurt Eichenwald (2000) - The definitive account of the ADM price-fixing scandal

- "Rats in the Grain" by James B. Lieber (2000) - Alternative perspective on the price-fixing case

- "Against the Grain" by Richard Manning (2005) - Critical examination of industrial agriculture including ADM's role

- "A Case Study in Corporate Welfare" by James Bovard, Cato Institute (1995) - Detailed analysis of ADM's subsidy dependence

Academic Papers & Case Studies

- Harvard Business School Case: "Archer Daniels Midland: Direction and Strategy"

- "The ADM Price-Fixing Conspiracy" - Antitrust case studies from various law schools

- "Political Connections and Corporate Performance" - Studies citing ADM as primary example

Documentary & Media

- "The Informant!" (2009) - Steven Soderbergh film starring Matt Damon

- "King Corn" (2007) - Documentary examining corn's dominance in American agriculture

- "Food, Inc." (2008) - Features ADM's role in industrial food production

Industry Reports & Analysis

- USDA Economic Research Service reports on agricultural processing

- Annual agribusiness reports from Rabobank and CoBank

- Commodity market analysis from CME Group

- ESG reports from Sustainalytics and MSCI covering ADM

Primary Sources

- ADM Annual Reports and 10-K filings (1970-present)

- Congressional testimony from various ADM executives

- FBI files related to the price-fixing investigation (partially declassified)

- Court documents from various ADM-related cases

Historical Context

- "Merchants of Grain" by Dan Morgan - Classic history of grain trading companies

- Federal Reserve Bank histories on agricultural finance

- Chicago Board of Trade historical archives

Regulatory & Policy

- USDA reports on ethanol and biofuel policies

- EPA documents on renewable fuel standards

- SEC filings and enforcement actions

- Department of Justice antitrust division records

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube