ACEN Corporation: The Great Energy Pivot

I. Introduction & The "Renewable Tiger"

Picture a fluorescent-lit boardroom on the 34th floor of the Tower One building in Makati, the financial heart of Manila, sometime in late 2020. The Philippines is in the middle of one of the world's longest COVID lockdowns. Outside the windows, the city is unnaturally quiet. Jeepneys are parked. Construction cranes are still. And inside, a small group of executives from a company called AC Energy is staring at a slide deck that proposes something almost heretical for a Philippine utility.

The slide says, in essence: shut down the coal plants. All of them. By 2030.

For a country that gets nearly 60% of its electricity from coal, for a holding company whose parent has spent more than a decade carefully assembling a portfolio of thermal generation assets, this is not a marketing pivot. It is a controlled demolition of the existing business model. And the man at the head of the table, a former McKinsey partner named Eric Francia, is not asking whether to do it. He is asking how fast.

Less than five years later, the answer was visible in the numbers. The company, by then renamed ACEN Corporation, had grown its renewable energy capacity from a few hundred megawatts to roughly 4.8 gigawatts of attributable capacity across the Philippines, Vietnam, Indonesia, India, Australia, and the United States. Its market capitalization had brushed against the equivalent of $10 billion at peak. It had become, in many quarters, the de facto reference name for "Southeast Asian renewables platform."

And it had done something no other listed power company in the world had done at the time. It had used a structured finance instrument called the Energy Transition Mechanism to retire a coal plant, the SLTEC plant in Batangas, roughly 15 years ahead of schedule, while still earning a return on the asset. In the very dry, very technical world of project finance, that maneuver was the equivalent of inventing a new chord.

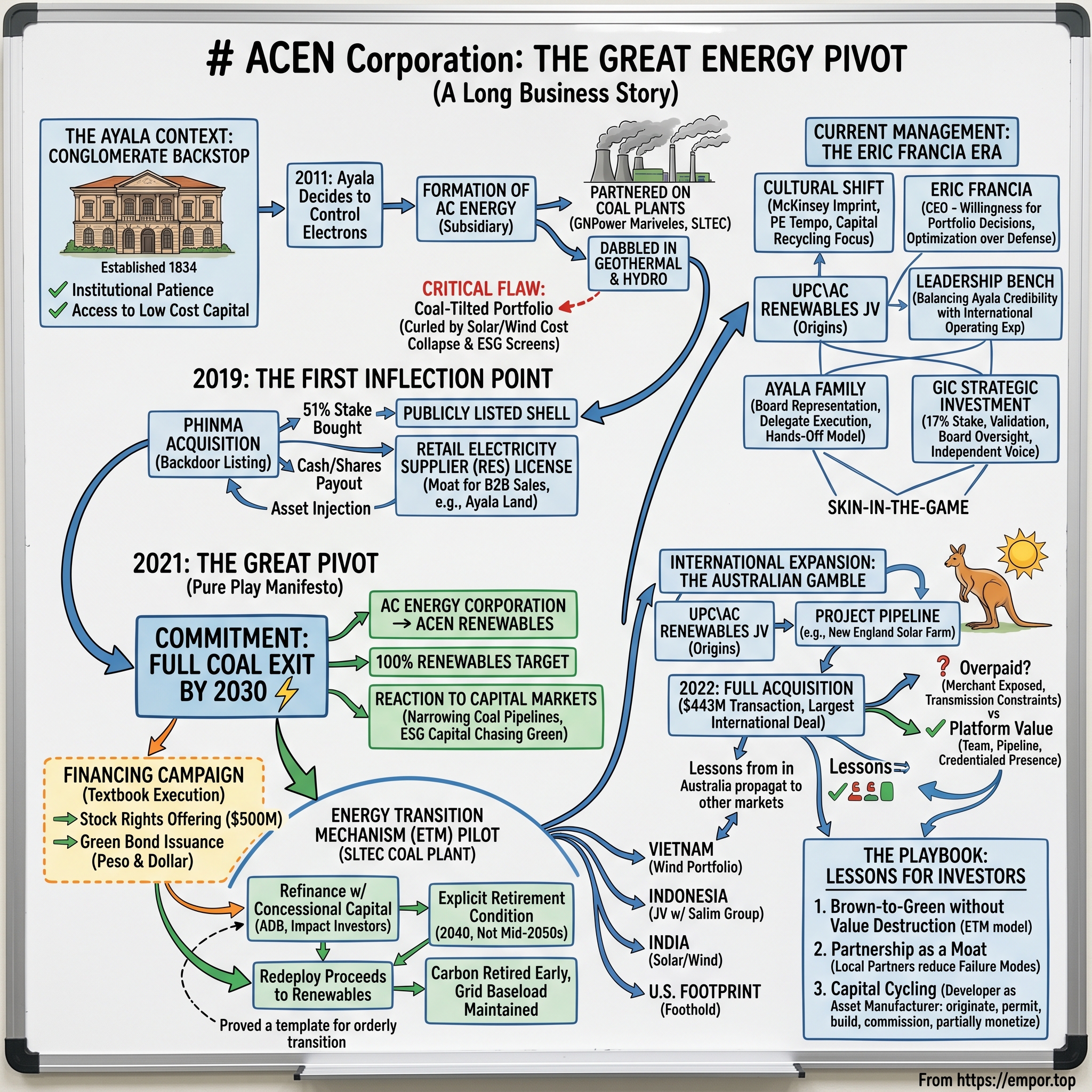

The roadmap of this story is the story of a pivot. It begins with the Ayala family, the oldest commercial dynasty in the Philippines, deciding in 2011 that they needed to control their own electrons. It runs through a reverse merger that quietly delivered a stock listing, a brand-defining 2021 strategic reset, an Australian acquisition that stress-tested everything, and a sovereign wealth fund partnership with Singapore's GIC that signaled global validation. It is a story about cost of capital as a competitive weapon. It is a story about replacing a generalist conglomerate sensibility with a private-equity tempo. And it is a story still very much in motion as the company tries to grow from roughly 5 gigawatts today to a stated ambition of 20 gigawatts by 2030.

The hook, the one that makes this a business school case rather than a press release, is this: ACEN is not a renewables pure play that raised money on a green narrative. It is the inverse. It is the cleaning-up of an old, brown-energy business by a 191-year-old conglomerate that decided the math no longer worked, and then turned that act of housekeeping into a regional growth platform. That is a much harder, much more interesting transformation, and it is the one global incumbents from European utilities to American oil majors have been attempting, with mixed results, for years.

ACEN's bet is that brown-to-green, done right, is not a sacrifice trade. It is the trade.

II. The Ayala Context: The Conglomerate Backstop

To understand ACEN, one has to first understand the house that built it, and the house is old. Casa Ayala, founded in 1834 as Casa Roxas by Antonio de Ayala and Domingo Roxas, predates the photograph, the telephone, and the modern corporation as a legal form. Its first business was distilling alcohol in colonial Manila. Over the next century and a half it would, in turn, become a real estate developer that effectively built the Makati central business district from cow pasture, a banking franchise through Bank of the Philippine Islands (BPI), one of the country's largest telecoms through Globe, a water utility through Manila Water, a healthcare network, and a string of other enterprises stitched together under the public holding company Ayala Corporation.

The Ayala identity is not loud. It is not a swashbuckling family office that buys distressed assets at the bottom of cycles and flips them. It is, instead, a profoundly Philippine institution that has institutionalized patience: long-duration assets, intergenerational stewardship, professional management trained in the Western mold, and a near-religious focus on what Filipinos call "license to operate," meaning the social and political legitimacy required to do business in a developing country with deep distrust of oligarchs.

That cultural backdrop matters because it explains why Ayala approached power the way it did, and why it eventually had to change.

In 2011, the holding company made a decision that, in retrospect, was less about energy and more about supply chain control. Ayala Land was building cities. BPI was financing them. Globe was wiring them. Manila Water was hydrating them. And every one of those businesses was getting strangled, slowly, by an unreliable and expensive power grid. The Philippines, an archipelago of more than 7,000 islands, has structurally high electricity prices, often the highest in Southeast Asia, because of geography, fuel imports, and a fragmented generation mix. If Ayala was going to power its own real estate empire reliably, it needed a seat at the generation table.

So Ayala spun up AC Energy Holdings, a wholly owned subsidiary, to build that seat. The early playbook, however, was very much a product of its time. The early 2010s were the high-water mark of Asian coal financing. Multilateral banks still funded thermal plants. Long-term, dollar-denominated power purchase agreements with state offtakers made coal look like the safest bet on the planet. And so AC Energy did what almost every other regional player did. It bought into coal. It partnered with Indonesian developers on the GNPower Mariveles plant. It took stakes in the South Luzon Thermal Energy Corporation (SLTEC), a coal-fired station in Batangas. It dabbled in geothermal and small hydro on the side. By 2015, on paper, it was a balanced thermal-and-renewables portfolio. In practice, it was a coal-tilted utility wearing a green ribbon.

This is the original sin worth lingering on, because it shapes everything that follows. ACEN's coal exposure was not the result of negligence or bad faith. It was the result of doing exactly what professional, sober capital allocators were supposed to do in 2011 through 2015. The technology was proven. The contracts were bankable. The IRRs were defensible. The thesis simply curdled when the cost of solar and wind collapsed by roughly 80% over the following decade, when European banks pulled out of fossil financing, and when the global investor base for power assets bifurcated into "ESG-acceptable" and "stranded."

This is what Ayala had to unlearn. And it is also the conglomerate's quiet superpower. Because Ayala is not a single-business operator with quarterly earnings PTSD, it could absorb the cost of a strategic U-turn. It could underwrite the brand transition. It could backstop the balance sheet during a multi-year capital raise. It could send its own treasury and BPI relationships into the green bond market and price paper at levels a standalone Philippine power IPP could not dream of.

In renewables, where there is no fuel cost and the entire economic engine runs on the spread between project IRR and the cost of debt, having a triple-A-adjacent conglomerate as your majority shareholder is not just nice to have. It is the product. That insight, more than any single asset, is what made what came next possible.

III. The First Inflection Point: The 2019 Phinma Acquisition

By 2018, AC Energy had a problem that successful private subsidiaries always eventually face. It had grown faster than its parent's balance sheet wanted to keep funding, and it had ambitions, particularly outside the Philippines, that needed a public currency. Acquiring assets across Vietnam, Indonesia, and Australia in a sustained way meant being able to issue listed equity and tap public debt markets in your own name. It meant having a stock ticker.

There were two ways to get one. The slow way was a traditional IPO, which in the Philippine market often meant 18 to 24 months of regulatory choreography and a valuation set by a window that might or might not be open. The fast way was a backdoor listing, the elegantly Filipino term for a reverse merger.

In late 2018 and through 2019, AC Energy executed the fast way. The vehicle was Phinma Energy Corporation, a small-to-mid-cap listed power company controlled by the Phinma group, one of the country's older industrial families. The transaction was a multi-step affair: AC Energy acquired roughly a 51% controlling stake in the listed shell, paid out cash and shares to existing holders, and then, over the following months, injected its own operating assets into the public entity. The entity was renamed AC Energy Philippines, then later, AC Energy Corporation, and ultimately, ACEN.

The headline price for that initial controlling stake was roughly $70 million, a number that, viewed in isolation, looks like a steal. To benchmark properly, one has to look across the Strait at Thailand, where regional comparables like B.Grimm Power and Gulf Energy Development were trading at EV/EBITDA multiples of 15 to 20 times and market caps in the multi-billion dollar range. AC Energy paid a fraction of those valuations to gain access to a fully licensed, publicly listed, retail-electricity-supply-licensed Philippine power vehicle. The asset was not pristine, the underlying operating performance was uneven, and the company carried legacy thermal exposure of its own. But the strategic optionality of holding a public listing in a market with high barriers to entry was worth far more than the sticker.

The genuinely underappreciated piece of the Phinma transaction was not the generation assets. It was the Retail Electricity Supplier (RES) license. In the Philippines, the retail competition market allows large commercial and industrial users, those drawing more than a certain monthly threshold, to bypass distribution utilities and contract directly with licensed retailers for their electricity supply. The license is finite. The big malls, the BPO call centers, the data centers, the manufacturing plants, the hotels, all of these contestable customers are effectively a B2B sales market. Whoever controls the contracts controls the electrons.

For Ayala, this was a near-perfect strategic fit. Ayala Land alone owns and operates dozens of malls, office towers, and master-planned communities. BPO operators inside those buildings are some of the largest contestable customers in the country. By owning a RES license through ACEN, Ayala gained the ability to be both the landlord and the power supplier, an internal vertical integration that would have been competitively difficult to assemble from scratch.

The Phinma deal was therefore best understood as a license acquisition with assets attached, not the other way around. It was the moment AC Energy stopped being a private holding subsidiary and became a publicly addressable platform. And it set up the larger strategic question that the next two years would force into the open: now that the company had the listing and the license, what kind of company did it want to be?

IV. The Great Pivot: 2021 & The "Pure Play" Manifesto

By the end of 2020, the global capital markets had answered the question for them. Coal-financing pipelines from Korean development banks, Japanese megabanks, and the World Bank had been narrowing for years. In 2020 and into 2021, they slammed shut. European insurers refused to underwrite new coal projects. The largest pension funds in the Netherlands and the Nordics began divestment screens. Even in Asia, where coal had been the backbone of post-2000 industrialization, the cost of capital for thermal generation began to widen against renewables in a way that was no longer ignorable.

Inside ACEN, this trend was not theoretical. It showed up directly in the offer letters from banks. A new wind farm could attract syndicated debt at one set of terms; a thermal asset acquisition would be quoted, if at all, at a meaningful spread. The same balance sheet metrics produced two completely different outcomes depending on color.

The decision in 2021 to commit to a full coal exit by 2030 was therefore not, despite the press release language, primarily an act of corporate altruism. It was an act of capital structure. It was the recognition that for ACEN to fund the gigawatt-scale ambitions it was lining up across the region, it needed access to the deepest and cheapest pool of capital available, and that pool was now defined by climate policy. The company rebranded from AC Energy Corporation to ACEN, formally launched the "ACEN Renewables" identity, and committed publicly to transitioning to 100% renewables by the end of the decade.

What followed was a financing campaign that, in retrospect, looks textbook. ACEN executed a stock rights offering in mid-2021 that raised approximately PHP 25 billion (roughly $500 million at the time), priced at a level that signaled real institutional appetite. It tapped the green bond market repeatedly, issuing peso-denominated and dollar-denominated paper that paid spreads more typical of investment-grade corporates than of Philippine power developers. And it set the table for what would become, two years later, the GIC strategic investment.

The most intellectually interesting part of this pivot, the part that turned heads inside global development finance circles, was the Energy Transition Mechanism, or ETM. The challenge with retiring a coal plant early in an emerging market is not technical. It is contractual and financial. Coal plants are typically financed against long-dated power purchase agreements that run 20 to 25 years. The lender expects to be paid out of those cash flows. The host government expects baseload electricity until replacement capacity is ready. Simply walking away from the asset is a default. Selling it to another operator just transfers the emissions to a new owner without removing them from the system.

The ETM, piloted by ACEN in partnership with the Asian Development Bank and structured around the SLTEC coal plant in Batangas, was a workaround. In simplified terms, the structure used a special-purpose vehicle to refinance the plant with concessional, lower-cost capital from development finance institutions and impact investors. That capital was provided on the explicit condition that the plant would be retired by a specific date, in this case 2040 instead of the original useful life that would have stretched into the mid-2050s, with the proceeds redeployed into renewables. ACEN, as the operator, agreed to the early retirement schedule. Lenders got their money back, plus a return calibrated to the lower risk profile of a defined wind-down. The grid kept its baseload through the transition window. And the carbon got retired ahead of schedule.

It was the first time, anywhere in the world, that a commercial finance mechanism had been used to deliberately accelerate the retirement of a working coal plant. To investors, this was important not because of the SLTEC asset itself, which was modest, but because it proved a template. If the ETM model could be replicated, the entire Asian thermal fleet, hundreds of plants and hundreds of gigawatts, became potentially addressable as orderly transition projects rather than stranded assets. ACEN had effectively prototyped a financial product that the rest of the region's transition would need.

The pivot, in other words, was not just a renewable buildout. It was a re-rating of what kind of business ACEN was. From "Philippine power IPP with growth ambitions" to "the company that figured out how to monetize the coal transition." That repositioning is what justified the multiple expansion that followed and what set up the foreign expansion to come.

V. International Expansion: The Australian Gamble

If the Philippines was where ACEN proved it could rewire the legacy business, Australia was where it was supposed to prove it could compete on the open ocean of global renewables.

The Australian power market is, by global standards, a small-population market with an oversized strategic complexity. It is one of the most fully unbundled and merchant-exposed electricity systems in the world. Generators bid into a five-minute spot market on the National Electricity Market (NEM), and the marginal price can swing from negative to several thousand dollars per megawatt-hour within hours. Wind and solar have penetrated heavily; rooftop solar adoption is among the highest on earth; coal retirements are scheduled in waves; and the policy environment shifts with each federal election. For an operator, it is the closest thing to a wind tunnel test for renewables capability.

ACEN's entry vehicle was UPC\AC Renewables Australia, a joint venture established several years earlier with UPC Renewables, a developer with a long track record of greenfield project origination across Asia-Pacific. The joint venture had been steadily building a project pipeline anchored by the New England Solar Farm in northern New South Wales, a project that, when completed, would be one of the largest unsubsidized solar facilities in Australia.

In late 2022, ACEN moved to consolidate. It announced the acquisition of the remaining stake in the joint venture, taking full ownership of the Australian platform for a purchase consideration that ultimately worked out to approximately $443 million when settlement and project-level payments were combined. It was, by far, the largest single international transaction in ACEN's history.

Whether ACEN overpaid is the kind of question on which reasonable people disagree, and the answer depends almost entirely on what one believes about Australian merchant power prices over the next decade. New England Solar, the centerpiece of the deal, was partially commissioned but not yet contracted with stable long-term offtake at the time of acquisition. The project sits in the New England Renewable Energy Zone, a part of the grid that has experienced significant transmission constraints, the polite industry term for congestion that can curtail output and depress realized prices. On a discounted-cash-flow basis using bullish merchant assumptions, the price looks reasonable. On a more conservative basis that assumes ongoing transmission bottlenecks and aggressive solar build-out continuing to suppress middle-of-the-day prices, it looks rich.

But to evaluate the Australian play purely on the New England Solar Farm is to miss the point. What ACEN was buying was a development platform, a team, a pipeline, and a credentialed presence in a sophisticated power market. The pipeline included future solar, wind, and battery storage projects across multiple Australian states. The team had origination, permitting, and grid-connection expertise that takes a decade to build organically. And the credibility of operating in Australia, of clearing its grid-connection process, of dealing with its regulators, became a calling card when ACEN went to lenders in any other market.

The Australia bridge, as it began to be called internally, was the laboratory. Lessons from there propagated. The company's playbook in Vietnam, where it built one of the largest wind portfolios in the country in partnership with local developers ahead of the country's renewable energy policy shifts, drew on Australian project management discipline. Its entry into Indonesia, in joint venture with the Salim group's Indika Energy and through the Salim-linked Salim Group's family-office capital, used a similar developer-plus-operator structure. Its Indian platform, originally built around solar and wind assets in partnership with the UPC India team and others, leaned on Australian-derived processes for grid connection studies and battery integration. Even the Vietnamese hydro and wind portfolio, with its own challenges around payment certainty from the state utility EVN, benefited from financial structuring honed in the more mature Australian environment.

The U.S. footprint, smaller and more recent, came through the same UPC platform, with Texas-based solar and battery development assets that gave ACEN a foothold in the world's largest renewables market without committing the kind of capital that a true U.S. push would require.

The strategic logic across all of these geographies was consistent. ACEN was not buying finished, contracted plants at terminal cap rates. It was buying or partnering into the early-stage development funnel, taking development risk in exchange for the much higher returns that come from carrying a project from greenfield through commissioning. The risk, of course, was that development assets in emerging markets are exactly where things go wrong. Permits get delayed. Currencies devalue. Grid codes change. Local partners disagree. The discipline of the Australian operation was meant to be the antibody.

Whether that antibody is strong enough to manage a portfolio spread across seven countries is, even now in 2026, the open question. The company's reported attributable capacity has continued to climb, but project-level returns in the international segment have not yet matched the more sheltered, PPA-backed economics of the Philippine portfolio. The Australia bridge is built. The traffic on it is still being measured.

VI. Current Management: The Eric Francia Era

Walk into ACEN's Makati offices and the cultural cues are deliberately not those of a traditional Filipino utility. There is no commemorative wall of family photos. The senior team is a mix of Filipino veterans of the Ayala system and external hires from international consulting, banking, and renewable energy backgrounds. The internal vocabulary is heavy on terms like "capital recycling," "platform value," and "pipeline conversion." The pace, by all accounts of those who have moved between the two worlds, is closer to a private equity portfolio company than to a regulated utility.

That cultural setting did not happen by accident. It was, in large part, the imprint of one person: Eric Francia, the company's President and CEO.

Francia is not a power industry lifer. He spent the formative years of his career at McKinsey & Company, where he rose to partner, doing the kind of strategy and capital allocation work that consultancies are hired for in Southeast Asia, sitting alongside conglomerate boards and helping them think through portfolio reshaping, capital structure, and growth strategy. He moved from McKinsey into the Ayala system in the early 2010s, eventually taking over leadership of AC Energy and shepherding it through the Phinma transaction, the rebrand, and the strategic reset.

Francia's signature, as far as one can identify it from the outside, is a willingness to make portfolio decisions that produce visible short-term ugliness in service of long-term repositioning. The decision to commit to coal divestment by 2030 fits that pattern. So does the willingness to write down or exit assets that did not fit the renewable strategy, even when they were producing cash. So does the bet on Australia at a price that triggered analyst handwringing. The McKinsey-trained instinct to optimize across the portfolio, rather than defend each asset, runs through every public communication the company has issued in the last five years.

Around Francia, the leadership bench has been deliberately constructed to balance Ayala-system institutional credibility with renewable-energy operating experience. The CFO function has cycled through capital-markets-fluent operators who brought relationships into both the local debt market and the regional ESG-focused investor base. Country heads in Australia, Vietnam, India, and Indonesia have been hired with backgrounds in those specific markets rather than rotated in from the Philippine office. The development team, the people who actually spend their lives walking land sites, negotiating with grid operators, and shepherding permits, has been built up to a scale that, on a per-MW basis, looks more like a developer than an asset operator.

Sitting above all of that is the Ayala family, represented on the board through Fernando Zobel de Ayala and Jaime Augusto Zobel de Ayala, the brothers who lead the parent holding company. The Zobels, by long-standing Ayala tradition, do not micromanage operating companies. They set portfolio strategy at the holding-company level and delegate execution. The hands-off model has been part of Ayala's longevity, and it is what made it possible for Francia to push through a strategy that, in a more interventionist conglomerate, would have died at the parent's audit committee.

Skin-in-the-game analysis for ACEN runs through this dual structure. The Ayala family, through Ayala Corporation, holds a controlling economic interest in ACEN that is large enough to make strategic outcomes existentially important to the holding company's NAV. That single relationship aligns more incentive than any individual stock-option scheme could. Management itself participates in equity-linked compensation, and senior leaders have, over the past several years, been visibly accumulating personal stakes through company plans, though not at the kind of founder-CEO levels one might see at, say, a U.S. tech company.

The third leg of the governance stool was added in 2023, when Singapore's sovereign wealth fund, GIC, completed a strategic investment that gave it approximately 17% of ACEN, becoming a significant minority shareholder alongside the Ayala parent. GIC's involvement did several things at once. It validated, externally, the strategic thesis at a time when global ESG capital was becoming more discriminating. It brought a sovereign-grade balance sheet partner who could co-invest in large projects. It added board-level oversight from one of the most respected institutional investors in the world, with a long-duration mandate matched to renewables economics. And, perhaps most importantly for governance, it provided a counterweight on the board to the controlling shareholder, the kind of independent institutional voice that minority public investors often value disproportionately.

The picture that emerges is of a company that has, in less than a decade, professionalized its management depth from "competent conglomerate division" to "institutional infrastructure platform." The next chapter of execution, the one investors are watching closely now, will test whether that professionalization can hold under the scale of the projects in the pipeline.

VII. Segment Data & "Hidden" Businesses

Most public commentary on ACEN focuses on installed capacity, which makes sense because gigawatts are the unit that conditions the renewables conversation. But viewed from the inside, the company is not really one business. It is at least three, and the differences between them matter.

The first is the Philippine generation portfolio. This is the cash engine. It consists of solar plants, wind farms, hydro facilities, and the residual thermal interests that are being run down through the ETM mechanism. The defining feature of the Philippine generation business is that most of its revenue is locked in under long-term Power Purchase Agreements with creditworthy offtakers, including distribution utilities like Meralco and contracts with affiliated and contestable buyers. Those PPAs produce predictable, dollar-equivalent cash flows that can be levered against project finance debt. Margins are stable. Returns on equity, at the project level, sit in the high teens. This segment, by itself, would constitute a respectable mid-cap regional utility.

The second is the international development platform. Australia, Vietnam, Indonesia, India, the United States, all sit here. The economics could not be more different. International revenue is a mix of contracted offtake, partial merchant exposure, and, in the most aggressive markets like Australia, almost fully merchant pricing on uncontracted volumes. EBITDA margins swing with spot power prices. Project IRRs are higher on paper but carry materially more variance. And the growth rate of capacity, on a percentage basis, is much faster than in the home market. This is the segment that drives the gigawatt headlines, and it is the segment that determines whether ACEN will hit its 2030 ambitions.

The third, and the one that gets the least airtime, is the retail electricity supply business. This is the offspring of the Phinma RES license and a deliberate build-out of commercial customer relationships. ACEN's retail arm contracts directly with large commercial and industrial users, typically buying power from a mix of its own generation, third-party generation, and the wholesale electricity spot market, then selling it to those customers under bilateral supply agreements. The economics of retail supply are not those of a generator. They are those of a trader and a logistics business, with margins on the spread between sourcing and selling, and value-added services like green-energy attestations becoming increasingly important to corporate buyers chasing their own scope-2 emissions targets.

The retail segment is, in some ways, the most strategically interesting because it is where ACEN can earn returns that are decoupled from generation capex. As more multinationals operating in the Philippines commit to 100% renewable sourcing, ACEN's ability to bundle generation, retail supply, and renewable energy certificates into a single contract becomes a moat. Not many competitors in the local market can offer that integrated package end to end.

Layered across all three segments is the increasingly important business of battery energy storage. ACEN has been moving aggressively into utility-scale BESS, particularly in Australia and the Philippines, with deployments designed to capture the price arbitrage between low-priced midday solar generation and the evening peak when residential demand spikes. In a world where solar capacity is expanding faster than the grid's ability to absorb midday output, batteries are increasingly the difference between a project that earns its target IRR and one that gets its earnings curtailed away. ACEN's storage push is, in essence, a hedge on its own solar fleet, with optionality on becoming a pure trading-and-storage business in markets where merchant economics make sense.

Putting it together, the operating segmentation that matters most is not country-by-country. It is more like:

- A predictable, contracted Philippine cash machine that funds dividends and strategic flexibility.

- A high-growth, higher-variance international platform that is meant to compound capacity and optionality.

- A capital-light retail and trading business that monetizes commercial relationships and the regulatory framework of the home market.

- A growing storage layer that sits across all three.

Investors who model ACEN as a single utility, applying one cap rate or one EV/EBITDA multiple, almost certainly miss the variance. The company is closer to a portfolio of three businesses with different risk profiles, different return characteristics, and different time horizons.

VIII. The Strategy Analysis: 7 Powers & 5 Forces

To pressure-test the long-term thesis, it is useful to run ACEN through two of the most cited frameworks in strategy: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. The exercise is not academic. It surfaces where the durable advantages actually live and where the company is more exposed than the marketing suggests.

Start with the Cornered Resource. In Helmer's framework, this is preferential access to a scarce input that competitors cannot replicate. ACEN's cornered resource is twofold. The first is its captive offtake base inside the Ayala ecosystem, the malls, towers, and BPO buildings owned and managed by Ayala Land and serviced under retail electricity contracts. No competing generator can simply buy its way into that customer base. The second, more subtle, is its pipeline of permitted, grid-connected sites across the region, which represent thousands of cumulative hours of permitting work that competitors would have to redo from scratch. In renewables, the project is not the panel. It is the permitted, grid-connected piece of land.

Counter-Positioning is the next, and arguably the most important. ACEN's position as a renewable-pure-play operator gives it access to a cost of capital that legacy regional utilities cannot match without restructuring their own balance sheets. Companies still carrying meaningful coal exposure, including some of the largest local incumbents, find themselves quoted wider spreads on debt and excluded from the pool of ESG-mandated equity capital. Even when they want to compete for the same renewable projects, their weighted average cost of capital is structurally higher. Counter-positioning works because the incumbent literally cannot do what the challenger can do without destroying parts of its existing business. That is the situation ACEN's pure-play stance creates.

Scale Economies show up in development infrastructure rather than in unit cost of generation. Solar panels and wind turbines are commoditized; nobody gets a fundamentally cheaper module than anybody else. But the scale of a regional development team, a regional procurement function, a regional financing capability, and a regional grid-engineering practice spread across 5+ markets does produce real economies in the cost of getting projects from concept to commissioning. ACEN's ability to amortize a sophisticated head office across a multi-country portfolio is a form of scale economy that smaller, single-country developers cannot match.

Brand power, Network Economies, Switching Costs, and Process Power are weaker in this business. Power is fungible. End customers do not care about the brand of the electrons. There are no meaningful network effects in generation. Switching is regulated and contractual rather than psychological. Process power, the kind that takes years to copy and is hidden inside operating routines, is plausible at the development level but not yet proven at scale.

Net of the Helmer analysis, ACEN's most durable advantages are Counter-Positioning and the Cornered Resource of its captive ecosystem and permitted pipeline. The other powers are nice to have but not where the moat lives.

Run the same company through Porter. Bargaining power of buyers in Southeast Asian power markets is structurally low. The region is short of electricity, demand growth is among the highest in the world, and offtakers, whether utilities or industrial customers, generally need more capacity than they can find. That is a tailwind ACEN did not engineer but benefits from.

Bargaining power of suppliers, principally module and turbine manufacturers, has become more nuanced. The Chinese solar module industry is in deep oversupply, which depresses panel prices and benefits developers. Wind turbine OEMs have had a rougher cycle, with several major Western suppliers struggling with quality and warranty issues. Storage suppliers, dominated by Chinese battery manufacturers, are in fierce price competition. On balance, suppliers have less power than they did three years ago, which is good for project IRRs.

Threat of new entrants is high in raw renewable development. Anyone with capital can buy panels and lease land. The barrier to a credible, scaled, regional renewables platform, however, is not capital. It is the combination of permitting expertise, grid connection rights, regulatory relationships, and balance sheet that ACEN has accumulated. New entrants can do small projects. They cannot easily replicate a 5-gigawatt regional platform.

Threat of substitutes, in electricity, is essentially zero. Customers cannot substitute electricity with anything else for most use cases. The question is which generator supplies it, not whether the demand exists.

Industry rivalry is the most pointed of the five forces. ACEN competes regionally with names like Aboitiz Power and Meralco PowerGen at home, with B.Grimm Power and Gulf Energy Development in Thailand, with EDP Renewables and Iberdrola in international development markets, and increasingly with global infrastructure funds like Brookfield, BlackRock, and Macquarie that have built out renewable platforms with deeper pockets. Rivalry has intensified meaningfully over the past three years as global capital has chased renewable assets, compressing returns on auctioned projects. ACEN's response, focusing on early-stage development where competition is thinner and returns are higher, is the right one, but it does mean the company is taking on more development risk than a pure asset acquirer.

Putting both frameworks together, ACEN's edge is a real edge, but it is not a moat in the Buffett sense of "wide and growing." It is a configurational advantage, a particular combination of cost of capital, captive offtake, permitting depth, and management quality that, if maintained, allows the company to compound. If any of those legs erode, the structural advantage compresses with it.

IX. The Playbook: Lessons for Investors

ACEN's transformation contains a playbook that will be studied long after the immediate stock chart is forgotten, because what the company has done is something many global incumbents are still trying to figure out. Three lessons stand out.

The first is the brown-to-green transition without value destruction. The conventional wisdom around legacy energy assets is that they are stranded, that the only path is to write them down and start over. ACEN's experience with the ETM and SLTEC suggests a more nuanced reality. With the right structure, brown assets can be transitioned, monetized, and recycled into green capital in ways that preserve, and even create, shareholder value. The trick is being early enough, structurally creative enough, and financially flexible enough to attract concessional capital. Not every operator can do this, but those that can will find that the transition itself is a profit center, not a cost.

The second lesson is partnership as a moat. ACEN almost never enters a new market alone. In Vietnam, it partnered with local developers familiar with the country's regulatory whiplash. In Indonesia, it worked with Salim-affiliated capital that opened doors closed to outsiders. In Australia, it built on UPC's existing platform rather than parachuting in cold. The pattern is consistent: use local partners to compress the learning curve, share the execution risk, and accelerate time to operation. The downside of the model is that partnerships add governance complexity and limit upside capture; the upside is that they reduce the most expensive failure modes in cross-border infrastructure investment, which are the ones that come from not knowing what you do not know.

The third lesson, perhaps the most important for any investor trying to understand renewables economics, is capital cycling. The right way to think about a renewable energy developer is not as a buy-and-hold operator. It is as an asset manufacturer. The developer originates a project, takes it through permitting, builds it, commissions it, demonstrates operating performance, and then frequently sells a partial stake to a financial investor like a pension fund or infrastructure fund at a much higher multiple than the developer's blended cost of capital. The recycled proceeds fund the next project. Done well, this creates a capital-light compounding machine where the developer's equity is constantly being redeployed into the highest-return parts of the lifecycle. ACEN has begun to articulate and practice this model explicitly, with selective partial monetizations of operating assets across its portfolio.

For investors, the implication is that traditional utility metrics, particularly steady-state EBITDA and dividend yield, do not capture the full economic engine of a developer-operator like ACEN. The right metric set is closer to one used for asset managers: cost of incremental capital, capacity additions, IRR on new commitments, and the multiple at which developed capacity can be partially monetized. None of those numbers show up on the income statement in clean form, which is why this kind of company is harder to value and, periodically, mispriced in either direction.

Watching the playbook execute over the next three to five years will be the most important thing for long-term holders. It is a playbook with real strategic logic, but it is unforgiving of execution slips, particularly in the international segment.

X. Conclusion & Bull/Bear Case

Step back from the project lists and the financing structures and ask the question that matters: what is the actual investable thesis on ACEN, and where could it go right or wrong?

The bull case is straightforward and powerful. Asia needs power. The region accounts for the majority of incremental global electricity demand for the foreseeable future. Renewable economics, having already crossed below thermal on a levelized cost basis, will continue to improve as battery storage scales. A regional platform with a low cost of capital, deep development capability, captive offtake, and a credible international footprint is a compounding machine. ACEN's stated ambition of 20 GW by 2030, on top of its current installed and contracted base of around 5 GW, is enormous but not absurd. If executed, it produces a business several times larger than today, with the kind of scale that fundamentally changes the company's bargaining position with suppliers, lenders, and offtakers. The "NextEra Energy of Asia" comparison gets thrown around, and while the U.S. utility model does not transplant cleanly, the directional logic is real. NextEra became the most valuable utility in the world by being the largest renewables developer; ACEN's regional position has at least the right ingredients to attempt a regional version of the same arc.

The bear case is equally serious. The first concern is execution risk in the international segment. Building 15 GW of additional capacity across multiple countries in less than five years requires a sustained operational excellence that is rare in any industry, let alone in cross-border infrastructure. Permitting delays, grid connection bottlenecks, supplier issues, and currency volatility are all live risks. The Australian platform, in particular, is exposed to merchant power price compression, transmission congestion, and the political volatility of Australian climate policy.

The second concern is the balance sheet. Building gigawatts requires capital. Even with green bond access and strategic investors like GIC, the absolute scale of the financing required to hit 20 GW by 2030 is substantial. Rising global rates, while moderating from peaks, raise the bar for project economics and increase the sensitivity of returns to execution. A debt-funded growth plan that runs into operational delays can compound problems quickly.

The third concern is industry rivalry. The very same investor capital that powered ACEN's rise has flooded the regional renewables space, compressing project returns at auction. Competitors with deeper pockets, including global infrastructure funds, can outbid ACEN on individual projects. The company's response, focusing on development risk rather than acquisition, is strategically correct but operationally harder.

The fourth concern is the parent-company structure. Holding-company-controlled subsidiaries, especially those funded in part by related-party transactions and ecosystem offtake, carry minority shareholder risks that can show up in subtle ways: pricing of intracompany contracts, allocation of strategic opportunities across Ayala entities, and timing of capital actions. GIC's presence on the board is a meaningful counterweight, but the structural issue does not go away.

The myth-versus-reality fact-check that often gets lost in the renewables conversation is worth a beat. The myth is that ACEN's cost of capital advantage comes from being green. The reality is more nuanced: it comes from being a Philippine conglomerate-backed pure play green company, where the conglomerate backstop and the pure-play branding compound on each other. Strip away either leg, and the advantage compresses. The myth is that international expansion is the growth story. The reality is that international expansion is the growth volatility, and the Philippine business is the cash engine that funds it. The myth is that ACEN is a utility. The reality is closer to a renewables developer with a utility attached.

The KPIs to track, the small set that actually matters, are these. First, attributable installed capacity, broken down between the Philippines and international, and the rate of net additions year over year. Second, weighted average cost of capital on new project debt, particularly in international markets, because that is the lever on which the entire economics of the model turn. Third, capital recycling cadence, meaning the volume and pricing of partial asset monetizations to financial investors, because that is the proof point on whether the developer-operator model is actually generating capital efficiency or merely accumulating gross capacity.

Finally, a brief overlay on the second-layer items. Credit ratings on ACEN's local issuance have been a focus area for fixed-income analysts as the company has scaled debt issuance, with rating agencies generally maintaining investment-grade ratings on the back of Ayala parent support and the contracted PPA portfolio. Regulatory and climate context in the Philippines is broadly supportive, with the country's renewable portfolio standards and contestable market reforms continuing to favor renewable developers, though spot market volatility and grid reliability issues remain real operational risks. The 17% GIC stake represents one of the most visible ownership signals in the regional ESG space, and its persistence, or any directional change, will be a meaningful sentiment indicator. Auditor and accounting changes have been routine to date, with no public going-concern flags, and the more interesting accounting judgments live in the project-level cost capitalization and impairment testing of merchant-exposed international assets. Diworsification risk is modest because the geographic expansion has remained inside the company's core competency of renewables, but the expansion across so many jurisdictions in a short period is its own form of operational complexity that warrants ongoing scrutiny.

The final reflection is the one ACEN's story keeps returning to. The energy transition, in most of the world, has been framed as a generational rebuild that requires entirely new companies to lead. ACEN's trajectory suggests a different model is possible: a legacy industrial group with the patience, the balance sheet, and the institutional credibility to execute the pivot from inside, using the conglomerate backstop as a catapult rather than as a constraint. Whether that model holds up under the operational stress of the next five years will determine whether ACEN becomes a genuinely durable regional infrastructure platform or a cautionary tale about renewable ambition outrunning execution capacity. The answer matters not just for ACEN's shareholders but for every legacy industrial company in the world that is staring at the same pivot and wondering whether it can be done at all.

The bet, and it is a bet, is that the answer is yes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube