Accenture plc: The Architecture of Total Enterprise Reinvention

I. Introduction & Episode Roadmap

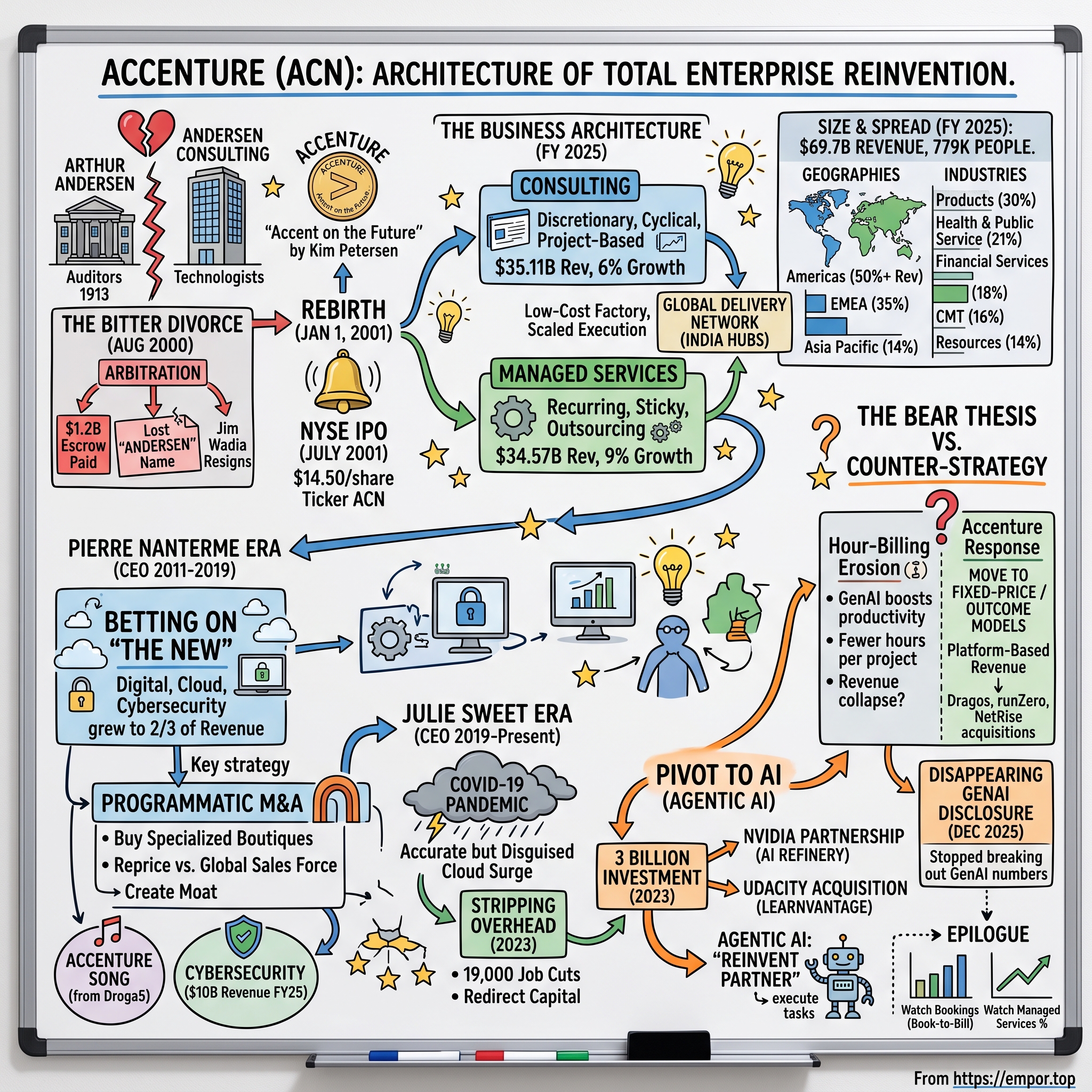

In August 2000, a small panel of arbitrators at the International Chamber of Commerce in Paris quietly ended a corporate marriage that had been curdling for a decade. The two households under one roof — the auditors of Arthur Andersen and the technologists of Andersen Consulting — had spent years fighting over money, clients, and identity. When the ruling came down, the consultants got exactly what they had demanded: freedom. But freedom came with a bill. They were ordered to walk away from roughly $1.2 billion held in escrow, and, more painfully, to surrender the one asset every professional-services firm guards most jealously — its name. The "Andersen" brand, built over eighty-seven years of audits, stayed with the auditors.1

Arthur Andersen's chief executive, Jim Wadia, had staked his job on extracting billions more from the consultants as the price of their exit. When the award came in at a fraction of that, he resigned within hours.[^2] It looked, at the time, like the auditors had won the war and the consultants had merely won a divorce. History would render the opposite verdict. On January 1, 2001, the newly untethered consulting firm rebranded itself Accenture — a coinage from a Norway-based employee, Kim Petersen, meaning "accent on the future." Barely a year later, the sibling they had fled, Arthur Andersen, was indicted for shredding documents in the Enron scandal and effectively ceased to exist.2 The firm that lost the name and paid the exit fee had, it turned out, purchased the most valuable thing on offer: distance from a catastrophe it did not yet know was coming.

That escape is where Accenture's public life begins. In July 2001 the firm converted from a partner-owned cooperative into a corporation and listed on the New York Stock Exchange under the ticker ACN at $14.50 a share.3 A quarter-century later it is one of the largest employers of white-collar labor on earth — roughly 779,000 people at the close of fiscal 2025, and nearly 799,000 by the spring of 2026 — generating $69.7 billion in annual revenue.456

Here is the paradox that makes Accenture worth a long, careful look. On paper it is the most human of businesses: it sells hours of expertise, and its cost of goods is overwhelmingly payroll. Yet it behaves like a compounding, capital-light machine. In fiscal 2025 it converted its earnings into $10.9 billion of free cash flow, ran an adjusted operating margin of 15.6%, earned a return on equity near 25%, and handed $8.3 billion back to shareholders — all while quietly buying 23 companies.4 It is a services firm that has learned to compound like a product firm.

And yet, as this story is written in mid-2026, the market has turned sharply skeptical. Accenture's shares, which changed hands above $300 in 2024, trade near $137 — the company's market value has roughly halved in under a year. The bear thesis is elegant and frightening: if generative AI makes software engineers dramatically more productive, a firm that bills by the human hour may be selling a commodity that is about to get much cheaper. This is the tension the episode will sit inside.

The roadmap: first, The Great Separation — the Andersen roots, the arbitration, and the rebirth. Then The Business Architecture — why Accenture's two engines, Consulting and Managed Services, behave so differently. The Pivot Playbook — how Pierre Nanterme bet billions on "The New." The Julie Sweet Era — COVID, the 2023 restructuring, and the pivot to agentic AI. The Strategic Engine — Porter, Helmer, and the arithmetic of programmatic M&A. The Financial Deep-Dive. And finally The Skeptic's Stress Test — the disappearing GenAI disclosures and the billable-hour trap. Let's start where the modern company was born: in a courtroom, over a name.

II. The Great Separation: From Arthur Andersen to the Rebirth as Accenture

To understand why the divorce was so bitter, you have to understand how good the marriage once was. Arthur Andersen & Co., founded in Chicago in 1913, spent decades as the conscience of American accounting — the firm whose signature on an audit meant the numbers could be trusted. Its post-war leader, Leonard Spacek, was a crusader for accounting integrity. He was also, almost by accident, the father of the business that would eventually eclipse the audit practice.

In 1954, General Electric's Appliance Park in Louisville, Kentucky, installed a UNIVAC I — the first electronic computer sold to a private American company — and used it to run payroll. Arthur Andersen was the firm that helped GE figure out how to make the machine actually do the work. That engagement, installing and programming the first commercial business computer, seeded what became Andersen's systems-consulting practice: the people who did not just check the books but built the machines that kept them. For thirty years the consultants were a curiosity attached to a prestigious audit firm. Then the curiosity grew up.

By the 1980s the systems-integration business was growing faster, and earning more per partner, than the audit and tax work that had made the Andersen name. In 1989 the firm formally split its two halves into separate units — Arthur Andersen for audit and tax, Andersen Consulting for technology — under a Swiss umbrella entity, Andersen Worldwide. On paper it was a tidy organizational chart. In practice it wired a slow-burning grievance into the partnership. The agreement required whichever unit was more profitable to transfer up to 15% of its profits to the other. In every year that mattered, that meant the consultants subsidizing the auditors — the fast horse hitched to the slow one, forced to share its winnings.

Resentment metastasized when Arthur Andersen, watching its consulting siblings pull ahead, began building its own competing systems-consulting practice under the audit umbrella. Now the consultants were subsidizing a division that was turning around to compete against them for the same clients. This was, in the consultants' view, a violation not of the contract's letter but of its entire spirit. In 1997 Andersen Consulting invoked the nuclear option and filed for binding arbitration before the International Chamber of Commerce, seeking a clean, permanent separation.

The three-year proceeding was less a trial than a slow-motion demolition of a partnership. When the final award landed in the summer of 2000, the arbitrator granted the consultants their independence and freed them from all future profit-sharing. But he rejected the consultants' claim that the auditors had so thoroughly breached the deal that the consultants owed nothing. Instead Andersen Consulting had to forfeit roughly $1.2 billion in payments held in escrow, and — the knife twist — give up the "Andersen" name entirely by the end of 2000.1 Jim Wadia, who had promised his partners a multi-billion-dollar windfall, resigned the same day the number came in far below his floor.[^2]

The consultants had eight months to find a new identity. The winning entry in an internal naming exercise came from Kim Petersen, an employee in the Oslo office: Accenture, a compression of "accent on the future." It was mocked in some quarters as corporate nonsense. It would prove to be one of the most valuable rebrands in business history — because of what happened next.

Arthur Andersen, keeping the coveted name, walked straight into the Enron scandal. As Enron collapsed in late 2001, its auditor's role — and the shredding of Enron-related documents — turned the once-gold-standard brand into a synonym for fraud. In March 2002 the U.S. Department of Justice indicted Arthur Andersen for obstruction of justice; by that summer the firm surrendered its licenses and dissolved, taking tens of thousands of jobs with it.2 The conviction was later overturned by the Supreme Court, but a professional-services brand runs on trust, and trust, once gone, does not return on appeal. The firm that had "won" the name was destroyed by it inside of two years.

Accenture, meanwhile, had spent 2001 doing something no partnership had ever needed to do: turning itself into a public company. Converting from a partner-owned cooperative to a corporation meant an initial public offering, and on July 19, 2001, Accenture listed on the NYSE at $14.50 a share, raising roughly $1.7 billion.3 The mechanics mattered less than the incentive rewiring underneath them. As a partnership, each partner cared about their own local profit pool this year. As a public corporation with equity, the partners' wealth was now tied to the long-run value of the whole enterprise — and, critically, the firm suddenly had a liquid currency, its own stock, with which to fund acquisitions anywhere on earth. The corporate structure that looked like a governance formality was in fact the launchpad for everything Accenture would become. What it did with that launchpad — how it turned a consulting brand into a two-engine industrial machine — is the next chapter.

III. The Engine of Modern Scale: Consulting vs. Managed Services

Walk into a large enterprise that Accenture serves and you will actually encounter two very different companies wearing the same badge. One arrives in the boardroom with slides and a plan: reinvent your supply chain, migrate to the cloud, redesign how your finance department works. The other never really leaves — it sits inside the client's operations, running the systems, patching the software, staffing the service desk, closing the books. Accenture calls the first Consulting and the second Managed Services, and understanding why the second one is the more interesting business is the key to the whole company.

In fiscal 2025 the two were almost exactly the same size. Consulting generated $35.11 billion, up 6% for the year; Managed Services generated $34.57 billion, up 9%.4 That near-symmetry is deliberate, and it is the source of Accenture's resilience. Consulting is discretionary, project-based, and cyclical — it is the first line item a nervous CFO freezes when the economy wobbles, because a transformation program can always wait another quarter. Managed Services is the opposite: multi-year outsourcing contracts under which Accenture takes over a function — IT infrastructure, security operations, finance and accounting, procurement, HR — and runs it for a fee. That revenue is recurring, sticky, and defended by something powerful: the sheer operational risk of ripping out the firm that runs your billing backbone.

Think of it this way. Consulting is the architect who designs the renovation and then leaves. Managed Services is the building-operations company that runs the heating, plumbing, and elevators for the next decade — and that a tenant almost never fires, because the switching cost is a building that stops working. When corporate spending is booming, Consulting sprints ahead. When it freezes, Managed Services keeps the revenue base from cratering. The two engines are counter-cyclical by design, which is why Accenture's revenue line has been so much smoother than that of pure strategy consultancies.

But the truly consequential strategic decision of Accenture's modern era was not the split between these two engines — it was the machine it built to power both of them, cheaply, at global scale. In the early 2000s, a new kind of competitor was rising out of India: the pure-play IT services firms — Tata Consultancy Services, Infosys, Wipro, and Cognizant — that had cracked labor arbitrage. They could staff enormous software and maintenance projects with skilled engineers in Bangalore and Hyderabad at a fraction of Western wages, and they were coming for exactly the large-scale IT work that had been Accenture's bread and butter.

Accenture's response was not to fight labor arbitrage but to buy it. Rather than defend its high-cost Western delivery model, it built its own vast offshore machine — the Global Delivery Network — with its single largest concentration of people in India, widely reported in the hundreds of thousands, alongside major hubs in the Philippines and elsewhere. (Accenture does not disclose a precise India headcount in its filings, so the frequently cited "300,000-plus" figure should be read as a well-sourced press estimate rather than an audited number.) The result was a hybrid no competitor could easily copy: premium, C-suite, relationship-driven consulting at the front end, wired directly into a low-cost, industrial-scale delivery factory at the back.

That combination is the moat. Pure strategy firms like McKinsey and BCG owned the boardroom but could not, and largely still cannot, execute a multi-year, ten-thousand-person systems overhaul — they don't have the delivery factory. The Indian pure-plays owned the delivery factory but struggled to win the C-suite relationship and the highest-margin strategic mandate. Accenture parked itself in the middle, able to sell the vision and build it, which let it capture the largest and most complex reinvention programs — the ones that require both a plan and an army. On its most recent earnings call, management noted that 195 of its top 200 clients had been clients for more than a decade, a statistic that only makes sense if you are embedded deeply enough to be irreplaceable.17

It is worth pausing on why Managed Services, specifically, is what generates terminal value rather than merely revenue. A consulting project is a sale that must be re-won every time; the moment it ends, Accenture is back to zero with that client and must persuade a budget committee all over again. A managed-services contract inverts that dynamic. Because Accenture is now operating something the client depends on daily, the default is renewal, and the burden of proof shifts to any rival who wants to displace it — a rival who would have to demonstrate not just that it is cheaper but that it can take over a live, mission-critical system without breaking it. In discounted-cash-flow terms, consulting revenue is a series of one-year options, while managed-services revenue behaves more like a bond with a long maturity and an embedded rollover. That is why analysts who value Accenture look past the near-even revenue split and weight the recurring engine more heavily: it is the part of the business that justifies a durable, above-market valuation, because it is the part that does not have to be re-sold each year. Management has also begun blurring the line between the two engines in a way worth noting — on recent calls it described clients increasingly asking for consulting and AI expertise to be embedded inside managed-services deals, so that the sticky, recurring contract now carries higher-value, higher-margin work along with it.5

For investors, the takeaway is precise: Accenture's durability does not come from being the smartest strategy shop or the cheapest coder. It comes from being the only firm that credibly offers both at once, and from a Managed Services base that turns one-time projects into decade-long annuities. The question that will haunt the back half of this story is whether artificial intelligence, by collapsing the cost of that back-end delivery factory, erodes the very moat that made Accenture great. But before the AI reckoning, there was an earlier pivot — the one that first proved Accenture could reinvent itself faster than its own clients. That is Pierre Nanterme's story.

IV. Pierre Nanterme's Great Pivot: Buying "the New"

Pierre Nanterme was, in every way, an Accenture lifer. A Frenchman who had spent his entire career inside the firm, he became chief executive on January 1, 2011, and added the chairman's title two years later. He was elegant, precise, and — as it turned out — willing to bet the company's future on a diagnosis most of his partners did not yet want to hear: that the business which had made Accenture rich was slowly going obsolete.

Around 2013, Nanterme looked at the core franchise — installing and integrating the big enterprise systems, the ERP and packaged-software work — and saw a mature, commoditizing business. The growth, he argued, was migrating to what he branded simply "The New": digital, cloud, and cybersecurity. At the time, "The New" was less than a fifth of Accenture's revenue. Nanterme set out to make it the majority of the company, and he largely succeeded — by the end of his tenure it had grown to roughly two-thirds of revenue, a transformation of a firm the size of a small country in under a decade.7

The genuinely novel part was not the destination but the method. Rather than try to build cloud, digital, and security capabilities organically — slow, uncertain, and culturally alien to a firm that hired generalists — Nanterme institutionalized acquisition itself as a repeatable industrial process. This is what analysts came to call programmatic M&A, and it is worth slowing down on, because it is arguably Accenture's single most distinctive competitive weapon.

Here is the logic. Accenture targets small, specialized boutiques — a Salesforce implementation shop, an elite AWS partner, a niche cybersecurity firm, a creative agency — typically doing tens of millions of dollars in revenue. Because these firms are small and privately held, they sell at modest valuations. But the moment they are absorbed, they are plugged into Accenture's distribution network — a client base that includes more than three-quarters of the Fortune Global 500 and 95 of the Fortune Global 100.18 A boutique that could sell its expertise to a handful of clients can suddenly cross-sell it to hundreds. The capability that was worth a small multiple as a standalone becomes worth vastly more inside the distribution machine. It is arbitrage — buying a capability cheaply and instantly repricing it against a global sales force. Bloomberg, dissecting the model in 2024, described a firm treating acquisitions less like bets and more like a supply chain.20

A worked example makes the arithmetic concrete. Suppose Accenture buys a fifty-person Salesforce-implementation boutique doing $30 million of revenue at, say, two times sales — a $60 million check. On its own, that boutique's ceiling is set by how many clients its partners can personally chase. Dropped inside Accenture, the same fifty specialists become the seed of a global Salesforce practice: their expertise is now offered to a client roster measured in the thousands, staffed up with offshore delivery talent, and bundled into larger reinvention programs that no boutique could ever have won a seat at. The capability that was worth two times sales as a standalone throws off a multiple of that once it is repriced against Accenture's distribution — and, crucially, the acquired partners are retained with equity and a bigger sandbox to play in, which addresses the perennial services-M&A risk that the talent simply walks out the door. Run that play a few dozen times a year, every year, and you have manufactured a growth engine that is extraordinarily hard for a rival to replicate, because the value does not live in any single deal; it lives in the distribution network that reprices all of them.

The proof points are vivid. The most audacious was in marketing. Through dozens of programmatic acquisitions of creative and digital agencies — anchored by the 2019 purchase of David Droga's celebrated New York agency Droga5 — Accenture assembled a business it eventually rebranded Accenture Song.8 The pitch was heretical to Madison Avenue: combine the creative firepower of a traditional ad agency with the back-end data, e-commerce, and technology integration that the old holding companies — WPP, Omnicom, Publicis — could not match. Song grew into one of the largest digital-experience businesses in the world, rivaling the scale of the very holding companies it was undercutting, and forcing the ad industry to reckon with a technology consultancy as a genuine creative competitor.19

The same playbook ran in security. In 2020, Accenture bought Symantec's Cyber Security Services business — including its managed security operations and global network of security operations centers — from Broadcom, instantly scaling itself into a first-tier defender of corporate and critical infrastructure.9 It was one bolt-on in a decade-long campaign that, on management's own telling, grew Accenture's cybersecurity revenue from roughly $700 million in fiscal 2016 to $10 billion in fiscal 2025 — a 35% compound growth rate, four times the pace of the company overall.5

What the programmatic machine reveals about Accenture is a temperament as much as a strategy: a willingness to treat reinvention as an operating discipline rather than a crisis response. Most firms acquire in panicked bursts at the top of a hype cycle and overpay. Accenture built a permanent, always-on pipeline that buys small, buys cheap, and buys constantly — 23 companies in fiscal 2025 alone. The skeptic's caution is warranted, though: programmatic M&A is only value-creating if the acquired capabilities genuinely reprice against the distribution base and don't quietly decay into a graveyard of orphaned brands and integration debt. That risk becomes sharper as the deals get larger and more product-like, a shift we will see clearly in the AI era. And the AI era is where the current chief executive, Julie Sweet, inherited both the machine Nanterme built and the biggest test it has ever faced.

V. The Julie Sweet Era: Total Enterprise Reinvention & The AI Shift

Pierre Nanterme's story ended in tragedy. In January 2019, gravely ill, he stepped down; weeks later he died in Paris at fifty-nine.7 The succession, however, was seamless — a mark of how deep Accenture's bench ran. The firm turned to Julie Sweet, and in doing so chose someone whose background was, on its face, unusual for a technology-services chief: she was a lawyer.

Sweet had spent more than two decades as a corporate attorney, rising to partner at the elite law firm Cravath, Swaine & Moore before joining Accenture as general counsel in 2010. In 2015 she was handed the firm's single most important operating job — chief executive of Accenture North America — and in September 2019 she became global CEO, later adding the chairman's role in 2021. She was the first woman to lead the firm. Her defining trait, by all accounts, is relentless operational discipline paired with a lawyer's instinct for framing: she talks about Accenture not as a consultancy but as its clients' "reinvention partner of choice," a phrase engineered to make transformation sound perpetual rather than episodic — and, not incidentally, to make Accenture indispensable at every turn of the technology wheel.

Her tenure opened with a gift disguised as a catastrophe. When COVID-19 shut the physical world in 2020, it forced every large enterprise to confront how analog its operations still were, and it turned cloud migration from a multi-year aspiration into an emergency. Accenture, positioned as the general contractor for corporate cloud moves, rode an enormous booking wave; the stock climbed to record highs as the pandemic accelerated exactly the digital work Nanterme had spent a decade building toward. It was a vivid demonstration of the firm's core thesis: every disruption that terrifies clients sends them, checkbook open, to the people who can rewire them.

Then the wave broke. As cloud-migration urgency normalized through 2022 and higher interest rates chilled corporate spending, Accenture did something that looked, to outsiders, like distress. In March 2023 it announced it would cut 19,000 jobs — about 2.5% of its workforce — over eighteen months, taking roughly $1.5 billion in charges, split between about $1.2 billion of severance and $300 million of office-space consolidation.10 For a firm whose entire mythology was hiring, headcount cuts read as a warning.

The detail that reframes the move is where the cuts fell: more than half were in non-billable corporate and support functions rather than client-facing delivery. This was not a firm shrinking because clients had vanished; it was a firm stripping out overhead to redirect capital toward the next wave. Management was, in effect, harvesting administrative fat to fund a technology bet it could already see coming. Whether that was prescient discipline or a convenient story to dress up a demand slowdown is a fair question — but the capital did visibly flow toward one destination.

That destination was AI. In mid-2023 Accenture committed $3 billion over three years to its Data & AI practice and pledged to double its AI workforce to 80,000 practitioners through hiring, training, and acquisition.11 Then, in October 2024, it deepened the bet with a headline partnership: a formal alliance with NVIDIA to build what Accenture called the AI Refinery on NVIDIA's full AI stack, with the newly formed Accenture NVIDIA Business Group and an initial commitment to train 30,000 professionals.12

The strategic target here was agentic AI, and it is worth translating the jargon. Early generative AI was a very capable intern that could write, summarize, and answer questions when prompted. Agentic AI is the promotion of that intern into an autonomous employee — a system that can take a goal, break it into steps, and actually execute a multi-step task across a company's software: not "draft this email" but "process this insurance claim end to end." Accenture's pitch is that turning a corporation into one that runs on AI, rather than merely uses AI, is a wholesale re-plumbing job — precisely the kind of complex, enterprise-wide reinvention it is built to sell.

There is a subtler point buried in the AI Refinery concept that explains why Accenture is so eager to own the plumbing. Enterprises adopting AI quickly discover that the model is the easy part; the hard part is the data underneath it — most large companies' data is fragmented, inconsistent, and locked in incompatible systems, and an AI agent is only as good as the data it can reach. Sweet has repeatedly told analysts that at least one in every two advanced-AI projects leads directly to a data project, because clients cannot deploy the agent until they have cleaned and unified the plumbing first.5 That is a deeply Accenture-favorable dynamic: the flashy AI use case becomes the wedge that sells a large, unglamorous, multi-year data-and-cloud modernization program — exactly the work the firm has always done best. Whether AI ultimately shrinks or grows Accenture's business may hinge on this single question of sequencing: does the AI wave trigger enough new integration work to more than replace the human hours it automates? Management's entire thesis is that it does.

The pivot also required retraining hundreds of thousands of its own people, which produced one of the more telling small acquisitions of the era. In March 2024 Accenture launched LearnVantage, a $1 billion, three-year investment in enterprise upskilling, and simultaneously agreed to acquire Udacity, the online-education pioneer that had been a $1 billion Silicon Valley unicorn before its consumer business faded.1314 Accenture did not disclose the price; press coverage framed it as a distressed shadow of Udacity's former valuation, a once-hot edtech name bought for its curriculum and platform rather than its brand.15 The logic was pure Accenture: acquire a capability cheaply, then reprice it against the distribution base — in this case, the base being both its clients' workforces and its own.

By the middle of fiscal 2026, Sweet was pushing the strategy into two new frontiers that reveal how she is trying to widen the moat rather than just defend it. The first is a deliberate move down-market. On the Q3 fiscal 2026 call she announced Accenture Edge, a new business aimed squarely at the mid-market — companies with roughly $300 million to $3 billion of revenue — which she framed as a $240 billion addressable market that Accenture had historically ignored because its high-touch, large-enterprise coverage model was too expensive to point at smaller clients.5 The bet is that AI-packaged, repeatable solutions can serve mid-market firms profitably without the bespoke army, and that doing so structurally offsets the softness in discretionary spending among large enterprises. The second frontier is a turn toward owning software-like platforms outright: the same quarter, Accenture announced it would acquire a majority stake in Dragos, a leading operational-technology cybersecurity platform, plus the security firms runZero and NetRise, stitching them into a single platform sold on a recurring, non-headcount basis.5 Both moves point the same direction — away from selling hours and toward selling products and outcomes.

The through-line of Sweet's tenure, then, is continuity of method under wildly discontinuous conditions. The same programmatic machine, the same "reinvention partner" positioning, the same harvest-overhead-to-fund-the-next-wave discipline — applied first to cloud, now to AI. The open question, which the market is currently answering in the negative, is whether AI is just another wave that sends clients to Accenture's door, or the first wave that lets clients — and cheap AI agents — bypass the door entirely. Before we adjudicate that, it helps to see exactly where Accenture's revenue comes from, because the shape of the business determines how exposed it really is.

VI. Sizing the Segments: Geographic and Industry Materiality

Numbers can obscure as easily as they reveal, so it helps to picture Accenture's $69.7 billion of fiscal 2025 revenue not as a single pool but as a portfolio deliberately spread across geographies and industries to smooth out any single shock. The spread is the strategy.

Geographically, the firm runs on three engines of very different sizes. The Americas — reorganized in fiscal 2025 to fold Latin America in alongside North America — is the largest and most profitable region, at roughly $35.1 billion, or just over half of revenue, and it grew 9% in local currency.4 This is the high-margin core, powered by the United States, where corporate technology budgets are deepest and the appetite for reinvention is highest. EMEA — Europe, the Middle East, and Africa — contributed about $24.6 billion, roughly 35% of the total, growing a more measured 6% in local currency, shaped by cautious European IT budgets and an increasingly strict web of data-sovereignty regulation.4 Asia Pacific was the smallest at about $10 billion, some 14% of revenue, growing 4% in local currency — the slow-growing but strategically important long game on the region's demographic and industrial expansion.4

That geographic spread is not academic. On the Q3 fiscal 2026 call, management disclosed that the flare-up of conflict in the Middle East had knocked roughly $100 million off quarterly revenue versus plan and hit sales in the region by around $400 million, with knock-on hesitation in discretionary spending rippling into Europe.5 A firm this global is always absorbing a geopolitical shock somewhere; the point of the portfolio is that no single one is fatal.

The industry breakdown tells an even more revealing story about resilience. Accenture organizes clients into five industry groups. The largest is Products — retail, consumer goods, manufacturing, life sciences, travel — at roughly $21.2 billion, about 30% of revenue, the engine of supply-chain, e-commerce, and digital-manufacturing work.4 Next is Health & Public Service at about $14.8 billion, or 21%.4 This is the counter-cyclical ballast of the entire company: government, defense, and healthcare contracts, including the large Accenture Federal Services business, tend to be long-dated and recession-resistant, because governments do not freeze mission-critical IT when markets wobble. Financial Services — banking, capital markets, insurance — contributed about $12.8 billion (18%), driven by the grinding, expensive work of modernizing core banking systems.4 Communications, Media & Technology added roughly $11.5 billion (16%), the most cyclical of the groups and the one hit hardest during the 2023–2024 technology-budget freeze, now recovering on AI infrastructure and network automation.4 And Resources — energy, utilities, chemicals — rounded out the portfolio at about $9.5 billion (14%), increasingly tied to the energy transition and grid modernization.4

The federal business deserves a footnote of caution, because ballast can become an anchor. Through fiscal 2026, Accenture's U.S. federal unit swung from strength to headwind: management repeatedly flagged that the federal business was subtracting about a percentage point from company growth, and guided that it expected to "anniversary" that drag and return to growth only in the fourth quarter.5 The very contracts that make Health & Public Service counter-cyclical also make it hostage to shifts in government spending priorities — a reminder that "defensive" and "immune" are not the same word.

The analytical conclusion an investor should draw from all of this is that Accenture is engineered as a diversification machine. No geography exceeds half the business, no single industry group exceeds a third, and the mix is balanced so that when discretionary Consulting freezes in one vertical, recurring Managed Services and public-sector backlog cushion the fall. That structural smoothness is a genuine, underappreciated asset — it is why Accenture's results are boring in the good sense. But diversification protects against idiosyncratic shocks, not against a systemic one that hits the entire model at once. To judge whether AI is that systemic threat, we need to weigh Accenture's durable sources of advantage against the forces arrayed against it. That is the work of the strategic blueprint.

VII. The Strategic Blueprint: Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question every long-term investor must: what, precisely, stops a competitor from taking Accenture's business? Two frameworks help war-game the answer — Hamilton Helmer's 7 Powers, which catalogs the sources of durable advantage, and Michael Porter's Five Forces, which maps the pressures bearing down on an industry. Run Accenture through both and a nuanced picture emerges: real moats, but ones that AI is actively testing.

Start with Helmer. The first and most obvious power is scale economies. With roughly 780,000 people and $70 billion of revenue, Accenture spreads its fixed costs — proprietary software and platforms, recruiting and training infrastructure, brand, and the global delivery network itself — across a base no rival can match. It is arguably the only firm on earth that can put hundreds of specialized engineers on a single client's problem, in multiple countries, within days. Scale here is not vanity; it is what lets Accenture bid credibly on the largest reinvention programs while absorbing the cost of a permanent M&A pipeline and a billion-dollar retraining budget.

The second, and for terminal value the most important, is switching costs, concentrated in Managed Services. Once Accenture runs a global enterprise's cloud architecture, its security operations, or its finance-and-accounting backbone, the client is not choosing to renew so much as declining to detonate. Ripping out the firm that operates your core systems means execution risk, transition cost, and the possibility that something mission-critical breaks. This is why 195 of the top 200 clients have stayed for a decade or more — not affection, but the gravitational pull of embedded operations.5

Third is cornered resources, held with medium strength through Accenture's ecosystem partnerships. It is the premier implementation partner for essentially every major enterprise-software platform — SAP, Salesforce, Oracle, Microsoft, AWS, Workday, ServiceNow, and now NVIDIA — and increasingly for the frontier AI labs. On its Q3 fiscal 2026 call management said it expected to more than double bookings from a roster of emerging AI and data partners that reads like a who's-who of the field: Anthropic, Databricks, Google's Gemini, Mistral AI, NVIDIA, OpenAI, Palantir, and Snowflake.5 These platforms need scaled hands to implement them; Accenture needs their technology to sell. It is mutual dependence, though "cornered" overstates it — the platforms cultivate many partners.

The fourth power is brand, or authority. In corporate technology, the buyer's dominant emotion is fear of blame, and "nobody ever got fired for hiring Accenture" is a real, monetizable asset — a trust certification that lowers the client's perceived risk and supports premium billing. Note what is absent from the list: Accenture has essentially no network economies and no process power that a determined rival couldn't replicate over time. Its moat is scale, stickiness, partnerships, and trust — powerful, but none of them a patent.

Now run Porter's Five Forces. Threat of new entrants is low: replicating a global delivery network and two decades of C-suite trust requires capital and time that no startup possesses. Bargaining power of buyers is moderate: large enterprises absolutely squeeze on price, especially in downturns, but the switching costs on their live systems cap how far they can walk. Bargaining power of suppliers is moderate, and here the "supplier" is human talent — wage inflation for elite AI engineers can compress margins, though the offshore footprint and LearnVantage retraining give Accenture levers to manage labor cost dynamically. Competitive rivalry is high, and it comes from three directions at once: the Indian pure-plays (TCS, Infosys, Cognizant) attacking from the low-cost end, McKinsey and BCG defending the strategic high ground, and Capgemini and the Big Four consulting arms (Deloitte, PwC, EY, KPMG) crowding the middle. Accenture wins, when it wins, by occupying a position none of them fully hold — strategy plus scaled execution.

Which leaves the force that has repriced the stock: the threat of substitutes, historically the weakest force and now the loudest. AI-assisted coding tools and, increasingly, autonomous agents threaten to substitute for exactly the entry-level, high-volume software engineering and maintenance hours that fill Accenture's delivery centers. This is the crack in the fortress. The bull reading is that AI is a complement, not a substitute — that it makes enterprise technology more complex and sends more work to Accenture. The bear reading is that it is a genuine substitute for the labor Accenture resells. Both cannot be fully right, and the honest analytical answer today is that the evidence is still forming. What the frameworks establish is that Accenture's advantages are real and durable against every threat except the one the market is most worried about. Whether management is allocating capital wisely in the face of that threat — and whether it has earned the benefit of the doubt — is the next test.

VIII. Management Credibility & The Capital Allocation Machine

Credibility, for a management team, is not built in a single quarter; it is accumulated or squandered over years of setting targets and either hitting them or explaining why not. On that scorecard, Accenture's leadership has, for a long time, been about as disciplined as large-cap management gets — which makes the current moment, when the market has stopped believing the story, all the more interesting to interrogate.

Start with how they get paid, because compensation reveals what a board actually rewards. Julie Sweet's total pay for fiscal 2025 came to $29.64 million, a 19.1% increase over the prior year.21 The structure matters more than the headline: only $1.55 million was fixed base salary; the overwhelming majority — roughly $22.9 million in stock awards plus a $4.5 million performance bonus — was tied to performance metrics and long-term equity that only pays off if the share price and operating results deliver over multiple years.21 That is textbook alignment on paper. But two tensions deserve a skeptic's eye. First, a 19% raise into a year when the stock would go on to halve is exactly the kind of pay-for-performance disconnect an activist would circle. Second, the raise assumes the performance scorecard "exceeds" rating reflects genuine outperformance rather than a compensation committee grading on a friendly curve — a critique that applies to most of corporate America but is worth naming here.

Now the machine itself, which is genuinely impressive. Accenture is asset-light by nature — it needs little physical capital, so a large share of profit falls through to cash. In fiscal 2025 it generated $10.9 billion of free cash flow, up sharply from $8.6 billion the year before, on capital expenditure of barely $600 million against $70 billion of revenue.4 Converting essentially all of net income into cash, year after year, is the quiet superpower of a services model done well: there is no factory to feed, no inventory to finance.

What management does with that cash is where the discipline shows. Of the roughly $10.9 billion of free cash flow in fiscal 2025, about $8.3 billion — more than three-quarters — went straight back to shareholders: roughly $4.6 billion in buybacks and $3.7 billion in dividends, the latter a double-digit increase over the prior year.4 The remainder funded the programmatic M&A pipeline — the 23 acquisitions that feed the next wave of capabilities.6 This is a deliberate, repeatable capital-allocation formula: convert profit to cash, return the majority, reinvest the rest in cheap bolt-ons, and let buybacks steadily shrink the share count. It is the behavior of a company that thinks it is a compounder, and for two decades the results validated the self-image.

A second-layer diligence point supports the cash-quality story. A recurring worry with any consulting firm is that reported profit is flattered by aggressive revenue recognition on long, fixed-price contracts — booking revenue on work not yet collected. The cleanest tell against that is the gap between earnings and cash, and Accenture's is reassuringly small: it converts roughly all of net income into free cash flow, and its days-services-outstanding — the average lag between doing the work and collecting the cash — has held in the high-forties, around 48 days in the third quarter of fiscal 2026, without the creeping deterioration that would signal a firm stuffing the channel or financing shaky clients.5 For a business that recognizes a growing share of revenue on fixed-price and outcome-based terms, where judgment about percentage-of-completion genuinely matters, that discipline is not a footnote — it is the evidence that the accounting is conservative and the cash is real. It is one of the reasons the firm has never faced a serious restatement or auditor concern, a non-trivial fact for a company that was, quite literally, born from an accounting scandal.

The guidance track record reinforces the point. Accenture has historically guided conservatively and then delivered, quarter after quarter — the kind of under-promise-and-outperform cadence that earns a premium multiple. But watch how the story has evolved through fiscal 2026, because it reveals both the discipline and the strain. Across the year, management repeatedly narrowed its full-year local-currency revenue growth guidance, landing by the third quarter at a sober 3% to 4%.5 That is not the language of a firm sprinting; it is the language of a firm managing expectations downward in real time and being candid about it. At the same time, it raised its shareholder-return commitment to "at least $9.5 billion" and reaffirmed free cash flow guidance of $10.8 billion to $11.5 billion.5 The tell is the combination: slowing top-line growth, but rising cash returns — a mature company leaning harder on the buyback to support per-share results as organic growth cools.

There is one more capital-allocation signal worth flagging for the diligence file. On the Q3 fiscal 2026 call, management disclosed that its acquisition spend for the year would jump to roughly $9 billion — nearly double the prior plan — driven by a large move into operational-technology cybersecurity, and that it would tap the long-term debt market to fund the elevated M&A and "optimize its capital structure."5 For a firm that has historically run with net cash, taking on debt to accelerate acquisitions is a meaningful shift in posture. It can be read two ways: as opportunistic capital deployment into high-growth, product-like assets at a moment of cheap software valuations, or as a company reaching for inorganic growth precisely because organic growth is getting harder to find. Which reading is correct depends entirely on whether those acquisitions perform — and that uncertainty sits at the heart of the bear case. But the sharpest test of management credibility right now is not M&A. It is a disclosure decision, and it is a genuine mystery.

IX. The Activist Stress Test & The GenAI Disclosure Mystery

Every so often a company does something with its disclosures that makes a skeptical investor sit up straight. Accenture did exactly that with its most-watched new metric, and the timing is the kind of thing short-sellers build slide decks around.

Rewind to the sequence. When generative AI erupted into corporate consciousness, Accenture did what it does best — it monetized the anxiety fast, and it told everyone. In fiscal 2024 it reported $3.0 billion in new GenAI bookings and about $900 million in GenAI revenue. In fiscal 2025 those figures leapt: GenAI bookings nearly doubled to $5.9 billion, and GenAI revenue roughly tripled to $2.7 billion.422 For two years, that soaring line was Exhibit A in the bull case — hard proof that Accenture was not a victim of AI but a prime beneficiary, selling the picks and shovels of the gold rush.

Then, having trained investors to watch that number, management announced it would stop reporting it. On the Q1 fiscal 2026 earnings call in December 2025, Accenture said that quarter would be the last in which it separately broke out AI bookings and revenue. It recast the category as "advanced AI" — folding together generative, agentic, and physical AI — and explained that the technology had become so pervasive across every offering, from cloud to ERP to Song to Managed Services, that carving it out as a distinct line had become artificial and even misleading.16

Now, the management defense is not unreasonable. There is a genuine phenomenon in technology where a hot new category stops being a category and simply becomes the way everything is done — nobody breaks out "internet revenue" or "mobile revenue" anymore, because the distinction dissolved. If AI is genuinely woven into every engagement, a standalone number really can mislead more than it informs. Management's framing — that this is a sign of maturity, not weakness — has real intellectual merit.

But an independent analyst is paid to notice pattern and timing, and both invite suspicion. A company discloses a metric enthusiastically while it is compounding at triple digits, then retires it — voluntarily, right as the base gets large enough that the growth rate must inevitably decelerate and as the first flush of corporate AI enthusiasm cools. The convenient interpretation is that Accenture is choosing to stop showing the world a number that was about to get less flattering. Is the discontinuation a signal of technological maturity, or a calculated move to obscure a decelerating GenAI bookings curve before it becomes a stick to beat the stock with? The honest answer is that outsiders cannot fully know — which is precisely the problem. Removing a disclosure removes the ability to falsify the bull case, and that asymmetry always deserves scrutiny.

This feeds directly into the structural bear thesis, which is more dangerous than any single quarter's optics: the hour-billing erosion threat. The argument runs like this. Generative AI can plausibly raise the productivity of a software engineer or an administrative worker by 30% to 50%. Accenture's business was historically built on billing clients for human hours. If a project that once took a hundred engineers now takes sixty, and the client is paying by the hour, then Accenture's revenue on that project could fall by nearly half even as it does the "same" work better. AI, in this reading, is structurally deflationary for a labor reseller — it makes the product cheaper to produce and, worse, cheaper for the client to demand.

Management's counter-strategy is to change how it charges. The push, which Sweet and CFO Angie Park emphasized repeatedly through fiscal 2026, is to move contracts away from "time and materials" — billing by the hour — toward fixed-price, outcome-based, and what they call "non-FTE" commercial models, where Accenture is paid for a result or for running a platform rather than for headcount. On the Q3 fiscal 2026 call, management noted that fixed-price work was already above 60% of the business and rising.5 Under these models, when AI makes delivery cheaper, Accenture keeps the productivity gain as margin rather than handing it all to the client through a lower hour count. The move into product-like assets — the operational-technology cybersecurity platform built from the Dragos, runZero, and NetRise acquisitions, with software-style recurring revenue growing at nearly 50% — is the same idea expressed through M&A: buy revenue that isn't priced by the hour at all.5

The bull rebuttal, which management pressed hard on the Q3 fiscal 2026 call, is that AI does not just automate old work — it creates entirely new work that only a firm like Accenture can do. Sweet offered a telling analogy: just as the rush to the cloud a decade ago left companies stunned by their runaway cloud bills and gave rise to a whole "FinOps" discipline of cost optimization, the rush to AI is now producing runaway spending on the computational "tokens" that large language models consume — and Accenture has built a practice, and its own internal platform, to help clients optimize which models they use for which problems and stop burning money.5 It is a small example of a large claim: that every efficiency AI creates also creates a new layer of complexity to manage, and that the manager of that complexity is, once again, the general contractor. The skeptic will note that this is precisely the kind of story a labor reseller would tell to reassure a nervous market, and that a token-optimization practice is a rounding error against a $70 billion revenue base. Both observations can be true at once, which is why the debate refuses to resolve.

The activist's question, then, is not whether the counter-strategy is sound — it is coherent — but whether it is happening fast enough. Can Accenture convert its pricing model and its revenue mix to capture AI's upside before AI erodes the billable-hour base underneath it? That is a race, and the market's collapsed valuation is a bet that Accenture is losing it, or at least that the outcome is too uncertain to pay up for. This is the single most important debate about the company, and it flows straight into the bull and bear cases.

X. Risk Radar & Bull vs. Bear Case

Before adjudicating the two cases, it is worth naming the material risks cleanly, because the bull and bear arguments are ultimately disagreements about which of these risks dominate.

The first and most consequential is AI labor substitution. If enterprises deploy in-house or off-the-shelf AI coding and operations agents at scale, the demand for the large offshore software-maintenance and application-management teams that anchor Managed Services could face structural — not cyclical — decline. This is the risk that has repriced the stock, and it is genuinely hard to size, because it depends on how good the agents get and how quickly enterprises trust them with production systems. The second is corporate capex sensitivity: a high-rate, uncertain macro environment freezes discretionary Consulting first, as the fiscal 2026 Middle East and federal drags demonstrated in miniature.5 The third is wage and talent inflation: the war for elite AI practitioners is expensive, and if billing rates cannot keep pace with what those people cost, margins compress. Layered under all three is execution risk — pivoting a 780,000-person organization's commercial model and skill base while keeping the machine running.

Now the bull case — the reinvention compounder. Its central claim is historical and, so far, empirically strong: every major computing wave — mainframe to client-server to internet to cloud, and now to AI — has made enterprise technology more complex, not less, and each successive layer has enlarged the market for the firm that integrates it. Enterprises do not, and largely cannot, build their own capability to fine-tune models, wire data pipelines, secure sovereign clouds, and orchestrate fleets of autonomous agents across legacy systems. They will remain structurally dependent on a general contractor, and Accenture is the general contractor with the deepest bench, the widest partnerships, and the stickiest installed base. The programmatic M&A machine keeps rolling up cheap capabilities and repricing them against global distribution. In this telling, AI is the biggest tailwind in the firm's history, and the current share price is the market mistaking an accelerating complexity engine for a dying labor arbitrageur.

The bear case — the billable-hour trap — accepts none of the comfort of history. Its claim is that this wave is categorically different because, for the first time, the technology does not merely add a layer of complexity to be integrated — it directly automates the human labor Accenture resells. The thousands of entry-level programmers in the delivery centers are not a moat in this world; they are a stranded cost. Clients, armed with their own AI productivity, capture the gains through relentless pricing pressure, while Accenture bears the expense of a billion-dollar retraining program and a rising executive pay bill. The disappearing GenAI disclosure, the debt-funded pivot into product acquisitions, the guidance narrowed to low-single-digit growth — the bear reads all of it as a firm quietly conceding that its organic engine is stalling and papering over the gap with buybacks and M&A.

It is worth grounding the debate in relative terms, because Accenture is not being repriced in isolation — the entire IT-services complex has been caught in the same downdraft, as investors reassess whether the labor-arbitrage model that powered two decades of growth survives contact with automation. The Indian pure-plays that once threatened Accenture from below now face the sharper version of the same question, since a larger share of their revenue sits in exactly the commoditized application-maintenance work that AI agents target first. Accenture's relative defense is that its revenue is skewed toward higher-value strategy-plus-execution mandates and toward the sticky Managed Services base, rather than pure staff augmentation — so if AI is a rising tide of deflation, Accenture should, in theory, drown last. But "drowns last" is a thin bull case, and the market's refusal to grant Accenture a meaningful valuation premium over its cheaper rivals suggests investors are not yet convinced that being the best-positioned firm in a threatened industry is the same as being safe. The strategic firms at the top — McKinsey, BCG, Bain — are privately held and so escape the daily verdict of the tape, but they face their own version of the reckoning, since AI erodes the leverage model of junior analysts on which their economics also depend. In short, there is no obvious hiding place in the services industry, and Accenture's scale is as likely to make it the consolidator of that disruption as its victim.

Weighing the two through the frameworks already laid out: the bull case rests on switching costs, scale, and the historical complexity-begets-integration pattern, all of which are real and none of which have visibly broken. The bear case rests on the substitutes force, which was historically Accenture's weakest and is now, for the first time, genuinely threatening the labor content of the model. The decisive evidence — is AI a complement or a substitute for Accenture's hours? — is still being written quarter by quarter, and management has just made that evidence harder to see. A neutral reading is that Accenture's competitive position remains formidable against every rival except the technology itself, and that the honest uncertainty about the substitution question is exactly why the stock now trades at a fraction of its former multiple. The market is not calling Accenture a bad business; it is pricing in a genuine, unresolved existential question about the labor-based model.

For an investor trying to cut through all of it, the noise reduces to a small number of things worth watching — the metrics that will resolve the debate before the narrative does.

XI. Epilogue & Outro

Twenty-five years ago, a consulting firm walked out of an arbitration having lost its name and $1.2 billion, and it turned out to have won its life — because the brand it surrendered was carrying a death sentence its holders could not yet see. That is the first and most durable lesson of Accenture: in professional services, independence and reputation are not soft assets. They are the whole business. The escape from Arthur Andersen was not luck; it was the payoff of a firm that valued its own future enough to pay to control it.

The second lesson is programmatic M&A as a core competency rather than a series of bets. Accenture did not out-invent its rivals; it out-bought them, treating acquisition as a disciplined, repeatable supply chain that feeds cheap capabilities into an unmatched distribution machine. It is one of the few genuinely replicable-in-theory, unreplicated-in-practice strategies in large-cap corporate life, and it is worth studying precisely because it looks boring and is anything but.

The third lesson is the power, and now the peril, of bridging strategy and execution. For two decades, owning both the C-suite relationship and the offshore delivery factory was an unassailable middle position — too executional for McKinsey, too strategic for the pure-plays. Artificial intelligence is the first force that threatens the execution half of that bridge directly, by attacking the value of the human hours the delivery factory sells. Accenture's entire response — outcome-based pricing, product-like acquisitions, a billion dollars of retraining, a pivot toward agentic AI as a thing to sell rather than merely fear — is a wager that it can move up the value chain faster than AI erodes the bottom of it.

Which brings the story to the metrics that actually matter from here. Set aside the noise and watch, first, the book-to-bill ratio and the trajectory of new bookings — because bookings are the leading indicator of whether clients are still routing their reinvention budgets through Accenture or starting to keep the work in-house; a book-to-bill durably below 1.0 would be the first hard sign the bear is right. Second, watch the mix shift toward Managed Services and non-FTE, outcome-based revenue — the share of the business that is not priced by the human hour is the single cleanest gauge of whether the pricing-model pivot is outrunning the substitution threat. Those two, more than any headline revenue number, will tell an investor which of the two futures is arriving. A reader keeping score need only track them over time; they will speak louder than any quarter's management framing.

Julie Sweet has said, in one form or another, on nearly every call, that Accenture intends to be the leader in the widespread adoption of AI. The question the next few years will answer is whether a 780,000-person organization built to sell human expertise can steer through the biggest computing transition since the internet without cannibalizing the very thing it sells. Accenture has reinvented itself before — out of a courtroom, out of a name, out of a maturing systems business, out of a pandemic. Whether it can reinvent itself out of the productivity of its own core product is the defining test of its second quarter-century, and it is being graded in real time.

References

-

Andersen Consulting Wins Independence in Arbitration Ruling — The New York Times, 2000-08-08 ↩↩

-

Deputy Attorney General Thompson news conference on Arthur Andersen indictment — U.S. Department of Justice, 2002-03-14 ↩↩

-

Accenture Ltd Form 10-12B / IPO Registration Statement — SEC EDGAR, 2001-04-19 ↩↩

-

Accenture Reports Fourth-Quarter and Full-Year Fiscal 2025 Results (Form 8-K Exhibit 99) — SEC EDGAR, 2025-09-25 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Accenture Reports Third-Quarter Fiscal 2026 Results (Form 8-K Exhibit 99) — SEC EDGAR, 2026-06-18 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Accenture plc Form 10-K for the Fiscal Year Ended August 31, 2025 — Accenture, 2025-10-23 ↩↩

-

Accenture Announces Passing of Former Chairman and CEO Pierre Nanterme — Accenture Newsroom, 2019-01-31 ↩↩

-

Accenture Interactive Completes Acquisition of Creative Agency Droga5 — Accenture Newsroom, 2019-05-01 ↩

-

Accenture Completes Acquisition of Broadcom's Symantec Cyber Security Services Business — Accenture Newsroom, 2020-04-30 ↩

-

Accenture to cut 19,000 jobs as macro uncertainty weighs — Reuters, 2023-03-23 ↩

-

Accenture to Invest $3 Billion in AI to Accelerate Clients' Reinvention — Accenture Newsroom, 2023-06-13 ↩

-

Accenture and NVIDIA Lead Enterprises into Era of AI — Accenture Newsroom, 2024-10-02 ↩

-

Accenture Launches Accenture LearnVantage — Accenture Newsroom, 2024-03-05 ↩

-

Accenture to Acquire Edtech Leader Udacity to Accelerate Capabilities of Accenture LearnVantage — Accenture Newsroom, 2024-03-05 ↩

-

Accenture to acquire Udacity to build a learning platform focused on AI — TechCrunch, 2024-03-05 ↩

-

Accenture says 'advanced AI' so pervasive it won't break it out anymore — Constellation Research, 2025-12-18 ↩

-

Accenture Q3 FY26 Earnings Conference Call — Accenture Investor Relations, 2026-06-18 ↩

-

How Accenture Song and David Droga are disrupting Madison Avenue — Financial Times, 2023-09-18 ↩

-

Accenture's Programmatic M&A Model Explained — Bloomberg, 2024-11-12 ↩

-

Accenture plc 2025 Proxy Statement (Form DEF 14A) — SEC EDGAR ↩↩

-

Accenture plc Q4 FY2025 Earnings Conference Call Transcript — Seeking Alpha, 2025-09-25 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube