ACM Research: The Clean Room Insurgent

I. Introduction: The "Picks and Shovels" of the Chip War

Walk through the airlock of any leading-edge semiconductor fabrication plant—Samsung's Pyeongtaek campus, TSMC's Fab 18 in Tainan, or SMIC's South Site in Shanghai—and the first thing that hits you is the silence. The bunny-suited engineers move with the choreography of monks. The ceiling pumps down filtered air thirty thousand times cleaner than a hospital operating room. Robotic FOUPs glide past on overhead conveyors carrying twenty-five wafers worth, by the time they reach the end of the line, more than the GDP of a small Pacific island.

In that cathedral of precision, the most important machines are not the ones the financial press obsesses over. EUV lithography from ASML gets the magazine covers. Nvidia gets the trillion-dollar headlines. But ask any process integration engineer what kills yield faster than anything else, and the answer is always the same—particles. A single speck of dust two hundred times smaller than the diameter of a human hair, settling on a wafer at the wrong moment, can render a chip worth thousands of dollars into landfill. Wafers get cleaned more than two hundred times during their journey from bare silicon to packaged product. Cleaning is, in a very real sense, the toothbrush of the semiconductor world.

For four decades that toothbrush market belonged to three companies—Lam Research and DNS Screen of Japan, with Tokyo Electron and SEMES rounding out the field. They split the global wafer-cleaning equipment market like an old aristocracy, with quiet pricing discipline, decades-deep customer relationships, and installed bases at every major fab from Hsinchu to Hillsboro. It looked like one of those markets where nothing ever changes.

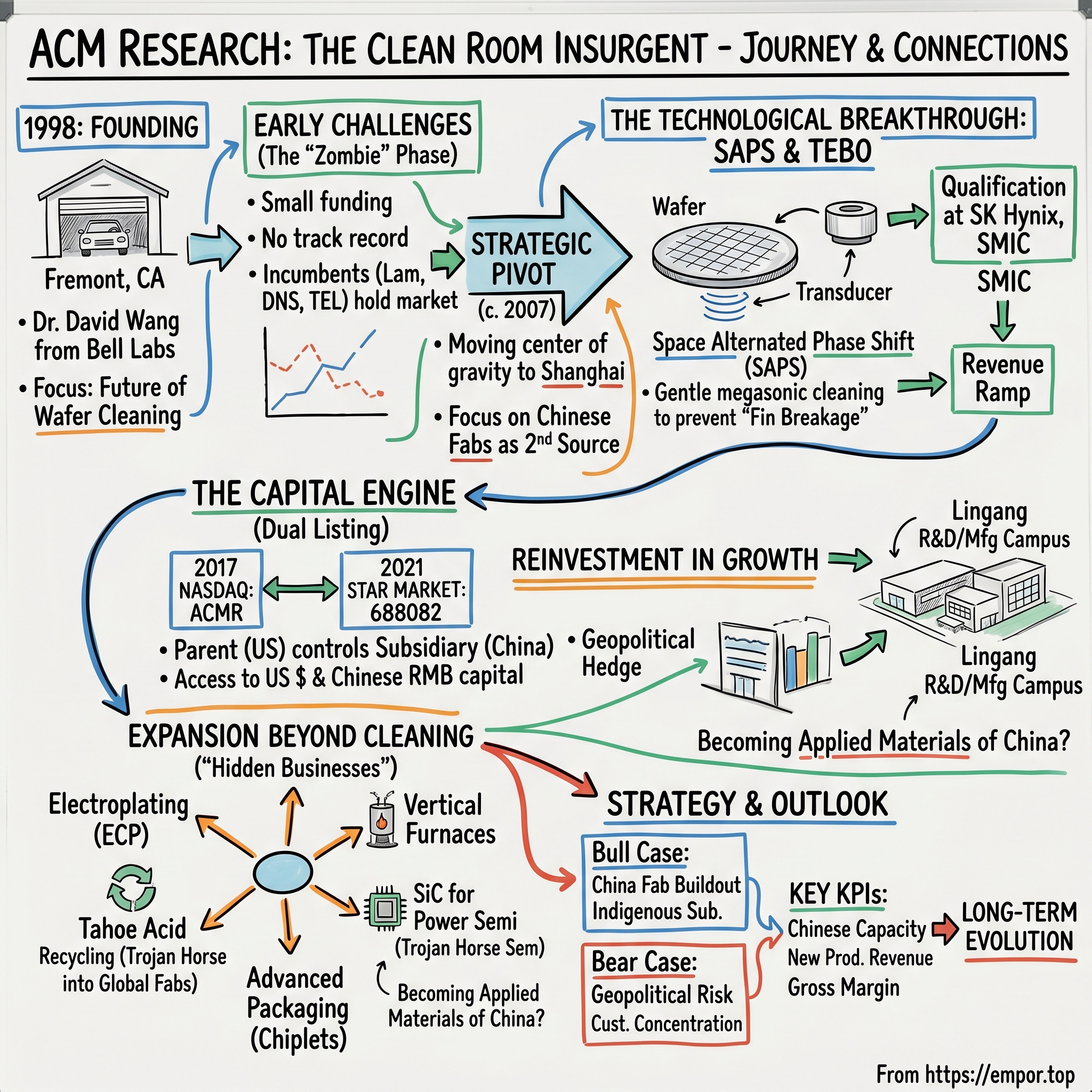

And then a small company born in a Fremont, California garage in 1998—a company that spent its first ten years as what its own founder later called a "zombie"—broke in. It did so not by being cheaper, not by being a copycat, but by inventing a fundamentally new way to clean a wafer. Then it did something even stranger. It moved its center of gravity to Shanghai, listed on two stock exchanges across the Pacific from each other, and turned itself into something the semiconductor industry had not seen before—a Silicon-Valley-incorporated, Shanghai-anchored, dual-listed national champion of mainland China's chip independence drive.

This is the story of ACM Research, ticker ACMR on NASDAQ, ticker 688082 on the Shanghai STAR Market. It is the story of how Dr. David Wang and a handful of engineers used a single technological insight—how to clean a chip without breaking the increasingly fragile structures on it—to insurgent their way into one of the most concentrated and unforgiving markets on earth. It is also the story of capital arbitrage, of a holding-company structure that turned the geopolitical squeeze into a feature rather than a bug, and of a quiet expansion into electroplating, furnace tools, and acid recycling that has analysts wondering whether ACMR is on its way to becoming the Applied Materials of China.

The roadmap for the next two hours: we will start in a garage, take a long detour through the physics of megasonic cavitation and a piece of wizardry called SAPS, follow the money through a 2017 NASDAQ IPO and a 2021 STAR market listing that effectively created a parallel currency for the Chinese subsidiary, profile the Bell Labs–trained founder who still runs the show, then unpack the "hidden businesses"—plating, furnaces, advanced packaging, sulfuric acid recycling—that may matter more than the cleaning core. We will close with a 7 Powers and Porter's Five Forces stress test, the bull and bear case, and the small handful of KPIs that actually matter for tracking this company.

It is, in many ways, the most underappreciated business story in the global chip war. So let us begin where every good Silicon Valley story begins—in a garage.

II. The Founding & The "Silicon Valley" DNA

In the spring of 1998 a soft-spoken physicist named Hui (David) Wang walked out of Bell Labs' Murray Hill campus in New Jersey for the last time, drove west, and rented a small commercial space in Fremont, California, just off Interstate 880. He was forty-something, married, with two children, and had spent the previous decade and a half doing some of the deepest work in semiconductor process physics anywhere on the planet. Bell Labs was already past its absolute peak, but the people who came out of it carried something rare—a willingness to look at the messiness of an industrial process and ask, from first principles, whether the conventional wisdom actually held up.

Wang's wager was that wafer cleaning, of all things, was about to break. Not the existing cleaning methods—those were fine for the chips of the late 1990s. But he could see, in the technology roadmaps the industry consortium SEMATECH was publishing, that line widths were collapsing. The chips of the next decade were going to have transistor structures so small and so fragile that the standard megasonic cleaning techniques—essentially blasting the wafer with high-frequency sound waves that created tiny imploding bubbles to scrub off particles—were going to start damaging the very structures they were meant to clean. There was, he believed, a chance for a small company to invent the cleaning tool of the post-planar era.

So he founded ACM, Inc.—the initials standing for "Advanced Cleaning Microelectronics," though the company would later quietly retire the expansion in favor of the brand. The early team was tiny. Funding came in dribs and drabs from Asian-American angel investors, some of whom Wang knew from the Chinese-engineer network around Stanford and Berkeley, and from a handful of Asian semiconductor families. There was no Sequoia round. There was no breathless Forbes profile. ACM in its first incarnation looked like dozens of other semicap startups dotted across Silicon Valley—a few engineers, a wet bench they had cobbled together in the back, customers who would not return their phone calls.

For the better part of a decade, ACM tried to sell into the only customers that would talk to a Fremont startup—small US fabs, a few research lines, a couple of integrated device manufacturers willing to humor a science experiment. It did not work. The incumbents—Lam Research's Steag wet division, DNS, TEL—had something ACM did not, which was a thirty-year track record of running on a fab floor at three in the morning without a single yield excursion. In the cleaning business, customers do not buy the better mousetrap. They buy the mousetrap that has already proven, on someone else's wafers, that it will not eat their Tuesday production run. ACM had no such track record. So the calls did not get returned.

By the mid-2000s the company was, in the founder's later words, a "zombie"—technically alive, with payroll being met month by month from small consulting contracts and the patience of long-suffering investors, but going nowhere. The R&D was beautiful. The commercial traction was nonexistent. Several of Wang's peers in the Silicon Valley semicap diaspora privately wrote ACM off.

The pivot, when it came, was driven less by inspiration than by demographics. Around 2007 it was becoming obvious to anyone watching capital flows in the semiconductor industry that the next generation of leading-edge fabs was not going to be built in Phoenix or Albany. They were going to be built in Wuxi, in Shanghai, in Beijing, in Hsinchu, in Hwaseong. The center of gravity of new fab capacity was migrating decisively across the Pacific. And the new Chinese fabs, in particular, faced a structural problem—they could not get the same level of attention from the Western tool vendors that the old Western fabs enjoyed. The big incumbents would sell them last-generation equipment and put their best engineers on Intel's and TSMC's accounts.

For a tiny outfit like ACM, that was the opening. The Chinese fabs, especially the ones being stood up under government-supported industrial policy, were desperate for credible alternative suppliers. Not as cost savers—as second sources. As insurance. They were willing to do the painful, multi-quarter qualification work to bring a new vendor onto a tool slot, because they could not afford to be wholly dependent on a tool vendor whose home government might one day decide to restrict exports.

So Wang made the bet that defined the rest of the company's life. He moved manufacturing and the bulk of his engineering team to a small leased facility in the Pudong district of Shanghai, set up a Chinese operating subsidiary called ACM Shanghai, and started camping out in the conference rooms of SMIC and YMTC. The American parent stayed put as a holding company, with corporate, IP, and a small US sales-and-engineering function. The center of gravity moved east. And it was in those Shanghai meeting rooms, talking to process integration engineers who actually had a problem to solve, that the technical breakthrough finally came.

III. The SAPS Breakthrough: Solving the "Megasonic" Problem

To understand why a wafer-cleaning insight became the ignition point for an entire company, you have to spend a moment with the physics of cavitation. Picture a silicon wafer, three hundred millimeters across, sitting in a shallow bath of ultra-pure water with a trace of ammonia and a dash of hydrogen peroxide. Above the bath, a transducer plate vibrates at roughly one megahertz, sending pressure waves down into the liquid. Those waves create microscopic bubbles in the water. The bubbles grow, oscillate, and then, at certain points in the wave cycle, collapse violently inward. That implosion releases a tiny shockwave—on the scale of a transistor, an explosion. Those explosions are what physically dislodge nanometer-scale particles from the wafer surface. This is megasonic cleaning, and from the early 1990s through the mid-2000s it was the gold standard for cleaning the more delicate post-litho and post-etch surfaces.

The problem, as transistor geometries shrank below 45 nanometers and structures became three-dimensional with the move toward FinFET, was that those microscopic shockwaves did not know the difference between a stray particle and a fin. The same energy that knocked off a contaminating speck could break off the upper portion of a delicate fin, ruining the device. Yield engineers across the industry watched their precious advanced-node wafers go from clean and intact to clean and bald—the particles gone, but with the structures torn off too. By 2008 the megasonic cleaning method was, for the most demanding applications, effectively dying as a viable approach. The big incumbents knew it. So did everyone else.

Wang and a small team of his engineers in Shanghai and Fremont, hunched over wafer benches and high-speed video footage of cavitation events, asked a different question. What if the issue was not megasonic cleaning itself, but the way the energy was delivered? Conventional megasonic systems energized the entire wafer surface uniformly. The cavitation events were random in space, unpredictable in intensity, and concentrated where they should not be. The team's insight was that if you could move the source of acoustic energy across the wafer in a controlled spatial pattern—if you could phase-shift the waves so that the high-energy zones were always sweeping rather than dwelling—you could distribute the cleaning energy in a way that scrubbed off particles without ever delivering enough sustained intensity to break a fin.

They called the technology Space Alternated Phase Shift, or SAPS. In practical terms, the system used a transducer that physically moved across the wafer in a precisely choreographed pattern, with the phase of the acoustic wave shifted in a way that smoothed out the energy distribution and eliminated the hot spots where structures were most likely to be damaged. The internal demonstrations on test wafers were arresting. With conventional megasonic, fin breakage rates were unacceptable for FinFET-class processes. With SAPS, the fins remained standing, and the particles came off.

But internal demonstrations are not industrial qualification. To turn a clever lab idea into a tool that a billion-dollar fab will trust on its production line takes years of grueling work. Every single failure mode has to be characterized. Every defect has to be traced back to a root cause. The tool has to run, twenty-four hours a day, for thousands of wafers, without producing the kind of yield excursion that gets a process engineer fired. The first customers, the engineers will tell you, were SK Hynix in Korea and SMIC in Shanghai, and the qualification cycles took the better part of three years each. Wang himself spent weeks at a time in customer labs, sleeping in business hotels in Icheon and Pudong, watching the data come in.

What is striking, looking back from 2026, is how perfectly ACM's pivot timed the inflection. In 2010 the global semiconductor industry was in the early throes of the FinFET transition. Foundry leaders Intel, Samsung, and TSMC were ramping their 22- and 14-nanometer nodes. Memory makers were squeezing toward 1xnm DRAM. Every one of those transitions amplified the need for a cleaning method that did not damage delicate three-dimensional structures. ACM had the right tool at exactly the right moment.

By the early 2010s SAPS-equipped wet cleaning tools were running production wafers at SK Hynix. By the middle of the decade SMIC and YMTC were standardizing on ACM cleaning equipment for swathes of their advanced-node lines. The company followed up with a second wave of innovation it called TEBO—Timely Energized Bubble Oscillation—which extended the same gentle-cleaning logic to even more delicate 3D NAND and FinFET structures. Where SAPS handled the relatively flat post-litho cleaning, TEBO handled the deep, high-aspect-ratio structures where any vigorous bubble action was lethal.

The qualification wins changed the company's center of gravity. Suddenly there was a real revenue ramp. The Shanghai facility started running two shifts. The Fremont team turned its attention from desperate sales calls to roadmap planning. The financial inflection was sharp—revenue went from a rounding error in the early 2010s to roughly forty million dollars by 2016, with gross margins that rivaled Lam Research and Tokyo Electron. The investor base started to take notice. And someone, somewhere in Sand Hill Road, finally typed "ACM Research" into a model.

The company that had been a zombie for ten years was, suddenly, an industrial toolmaker with a real product, real customers, and a real growth story. The next question was how to fund the next decade.

IV. The Capital Engine: The 2017 IPO and the STAR Market Pivot

By late 2017 ACM was, on paper, ready to go public. Revenue was ramping fast. Gross margin was healthy. The customer concentration was uncomfortable—a couple of Korean and Chinese fabs accounted for the lion's share of sales—but the qualification list was lengthening, and the SAPS and TEBO platforms were starting to win slots in process flows that would lock the company in for ten years or more once production ramped. So in November 2017 ACM Research listed on the NASDAQ at a modest valuation, raising about ten million dollars in net proceeds, with the ticker ACMR. By the standards of Silicon Valley IPOs it was tiny—a small-cap with light coverage and a confusing dual-geography story that most American buyside analysts initially could not be bothered to spend an afternoon understanding.

For the first eighteen months as a public company ACMR traded as if its NASDAQ listing was a curiosity. The float was thin. Two or three small-cap funds did the work, and the stock traded mostly on the strength of customer wins. But beneath the surface a much more interesting question was being worked on inside the founder's head and on the desks of the company's bankers in Shanghai. The growth, the talent, the manufacturing, the customer base—all of it was sitting inside the Chinese subsidiary, ACM Shanghai. The American parent was an ownership structure with a NASDAQ listing. Was there a way to unlock the value of the Chinese operating company without having to liquidate the parent or unwind the structure?

The answer, when it came, was a piece of capital-markets engineering as elegant as anything in the playbooks of the great holding-company architects. In 2019 the Chinese government opened the Shanghai Stock Exchange's Science and Technology Innovation Board—the STAR Market—as a NASDAQ analog for domestic technology companies. The new board allowed loss-making and dual-class structures, simplified the listing process, and—critically—was designed to channel domestic Chinese capital into national-priority technology sectors. Semiconductor equipment was at the very top of the priority list.

ACM saw the opportunity and moved. In late 2021 ACM Shanghai listed on the STAR Market under the ticker 688082, while remaining a majority-owned subsidiary of the US parent ACMR. The Chinese listing raised the equivalent of roughly six hundred million US dollars in fresh capital at valuation multiples that the same business never could have commanded in dollar terms in New York. Domestic Chinese investors—mutual funds, retail, state-linked vehicles—were hungry for any pure-play exposure to indigenous semiconductor equipment, and they paid up handsomely for it.

The ACMR American parent retained the controlling stake in ACM Shanghai. The STAR-listed shares represented the public float of the subsidiary. The structure was, in financial terms, a parent-and-subsidiary listing of the kind that Asian conglomerates have used for decades but that almost no US-domiciled company had executed in this particular way. In one stroke ACMR had acquired access to two pools of capital—dollar-denominated US institutional money for the parent, and renminbi-denominated Chinese domestic money for the subsidiary—each priced at the multiples its respective home market was willing to pay. It was the cleanest arbitrage of two capital regimes any small-cap semicap company had ever pulled off.

The deployment of the proceeds was equally striking. Where many newly cashed-up semicap companies have, over the years, splurged on legacy IP acquisitions—paying ten times the normal price for some moribund competitor's patent portfolio, or buying a tired Japanese tool company for vanity—ACM did the opposite. The bulk of the STAR capital was poured into a brand-new R&D and manufacturing campus in Lingang, the special economic zone south of Shanghai's Pudong airport. The Lingang facility, when fully built out, would more than triple the company's manufacturing footprint and house the engineering teams for the new product categories the company was opening up—electroplating, vertical and horizontal furnaces, sulfuric-acid recycling tools, advanced packaging wet equipment.

The R&D-to-revenue ratio in the years since the STAR listing tells the strategic story. Where Lam Research and Applied Materials run R&D at roughly twelve to fifteen percent of sales—the natural number for a mature, scale-driven leader—ACMR has been running its R&D intensity in the high teens to low twenties as a percentage of its US-consolidated revenue, depending on the year and the timing of customer-funded development. In dollar terms it is a fraction of what Lam spends. As a share of revenue, it is closer to what a company in growth-stage hyper-investment mode looks like. The signal is unambiguous—management is plowing the windfall back into the next product, not stripping it for dividends.

The benchmarking against industry peers also reveals where ACMR has been disciplined and where it is taking risk. The company has not made a major acquisition. It has not bought legacy patent estates at a markup. It has not, so far, done a deal that cost more than a single quarter's revenue. The growth has been overwhelmingly organic, funded by the dual-listing capital pile, and aimed at extending the cleaning-tool franchise into adjacent wet and thermal processes where the same customer relationships and the same engineering DNA can be levered. That organic discipline is rare in semicap, where the temptation to buy growth via a tuck-in acquisition is always strong.

The cost, of course, is structural complexity. The dual listing creates a parent-subsidiary value gap that has caused recurring confusion in the US market about how to value ACMR. At various points in 2023 and 2024 the implied valuation of ACMR's stake in ACM Shanghai—based on the STAR market price—was actually higher than the entire market capitalization of the US parent, meaning the American market was effectively assigning negative value to the rest of the consolidated business. That kind of holding-company discount is a classic sign of a market that does not know how to price a complex structure. It also creates a permanent strategic question—if the discount persists, does the parent ever consider a more aggressive structural simplification? That tension is one of the live questions for the next chapter of the story.

V. Current Management: The David Wang Era

Walk into the conference room of ACM's Lingang headquarters and the first thing that strikes you is what is not on the walls. There are no founder portraits, no inspirational mission statements rendered in glass and aluminum, no rows of awards. The single decorative element, in most photos, is a long whiteboard covered in dense engineering diagrams. The man who built the company likes it that way. Dr. Hui (David) Wang—Founder, Chairman, and Chief Executive Officer of ACM Research and Chairman of ACM Shanghai—has the unmistakable affect of a process physicist, not a Silicon Valley showman. He talks slowly, in long technical sentences, and his investor calls are punctuated by the kind of long pauses that suggest he is genuinely thinking about the question rather than reaching for a pre-cooked answer.

Wang's biography reads like a perfectly engineered Bell Labs résumé. Born in mainland China, educated through the Chinese university system in the late 1970s and early 1980s, he came to the United States for graduate work and ultimately landed at Bell Labs Murray Hill, then still one of the great industrial research institutions in the world. At Bell Labs he worked on the physics of semiconductor processing, particularly the chemistry and acoustics of wet cleaning. He had patents to his name before he ever started a company. The transition from research scientist to entrepreneur was not, in his own telling, a romantic narrative arc—it was a calculation that the existing tool vendors were not going to solve the problem he could see coming, and that someone smaller and faster would have to.

Twenty-eight years on, Wang remains the largest single individual shareholder of ACMR—the most recent proxy disclosures put his beneficial ownership in the mid-single-digit percent range of the common stock, with concentrated voting control through Class B shares that carry roughly twenty votes per share to Class A's one. The dual-class structure is not unusual in technology companies, but the specific calibration here gives Wang and a handful of co-founders effective long-term governance control even as the public float has grown. The strategic message is clear—the company does not intend to be flipped to a strategic acquirer or steered by short-term activist pressure. The patient, organic, multi-decade build is the explicit plan.

What makes the management story unusual is the layered incentive structure created by the parent-subsidiary listing. At the US parent level Wang and the other senior executives hold equity that responds to the ACMR share price on NASDAQ. But the operating leadership of the Chinese subsidiary—and that is the bulk of the engineering and manufacturing team—holds equity-like instruments tied to ACM Shanghai's STAR listing. In practice that means the people actually building furnace tools and acid recyclers in Lingang see their compensation move with the Chinese capital market's enthusiasm for indigenous semiconductor equipment, which has been more generous and more stable than the US small-cap market's view of the consolidated entity. It is a carefully designed arrangement. It aligns the local engineering team with the local growth opportunity, and it makes ACM Shanghai a magnet for talent in a Chinese semiconductor labor market where the very best process engineers are being aggressively recruited by every domestic fab and tool company.

Wang's leadership style, by all accounts of those who have worked with him, is engineering-first. He spends an unusual share of his time in the lab and on the customer floor. He is famous for asking process integration engineers at customer fabs to walk him through, in detail, the failure modes of competing tools—not to sell them on his own, but because he genuinely wants to understand the physics. The senior team around him is a mixture of long-tenured Silicon Valley veterans, many of whom came with him from the early days, and Chinese engineering leaders who have been promoted up through the Shanghai operations. The cultural blend—Silicon Valley engineering rigor on top, mainland Chinese manufacturing speed and customer intimacy on the ground—is, in Wang's own description, the company's distinguishing operating advantage.

There are tensions in the structure, of course. The most obvious is governance. ACMR is a Delaware-incorporated, NASDAQ-listed company that consolidates a Shanghai-listed Chinese operating subsidiary. The Chinese subsidiary is subject to Chinese regulatory oversight, including national security review of certain technologies. The American parent is subject to US securities law, US export control law, and the disclosure regime of the SEC. The board of directors at the parent level includes both US-domiciled independents and directors familiar with the Chinese capital market. The audit firm is one of the global Big Four. The combination has, so far, satisfied both regulatory regimes, but the surface area for potential conflict is large and gets larger every year as US-China technology tensions escalate.

The succession question is also live. Wang is in his sixties. The senior team includes capable lieutenants, particularly in the Shanghai operations, but there has been no formal public discussion of a long-term succession plan. For a company whose strategy and culture are so closely identified with the founder, that is a non-trivial overhang for long-term holders to think about.

And yet, for all the complexity, the top-of-house alignment is unusually clean. The founder is also the CEO, the largest individual shareholder, and the lead architect of the technology. He has been in the chair for twenty-eight years. He has skin in both stock prices, the parent and the subsidiary. He has resisted the tempting acquisition path, plowed capital into R&D and capacity, and bet the company's next decade on a half-dozen new product lines. Whatever else one says about ACMR, this is not a company being run for the next quarterly earnings call.

VI. "Hidden" Businesses: Beyond the Cleaning Tank

Most investors who follow ACMR think of it as a cleaning company. The story they tell each other—and the story analysts tell in their initiation reports—is "SAPS, TEBO, FinFET, China." That story is roughly seventy percent right. Cleaning tools, broadly defined, still account for the majority of revenue. But the most interesting question for the next five years is what is happening in the other thirty percent, where a half-dozen new product lines are being incubated under the same roof. Each of them targets a multi-billion-dollar global tool segment currently dominated by an American or Japanese incumbent. Each of them is in a different stage of customer qualification. And each of them gives ACMR a new vector of growth that does not depend on yet another generation of FinFET cleaning.

The first hidden business is electroplating—what the industry calls ECP. To clean a wafer is to scrub off contamination after a process step. To plate a wafer is to deposit metal—copper, in particular—into the trenches and vias that form the interconnect layers of a chip. The ECP step is fundamental to building the seventeen or so metal layers that wire up a modern logic chip, and the global market for the equipment that does it has been overwhelmingly dominated by Lam Research, with Tokyo Electron a distant second. ACM's bet is that the same wet-process engineering capability that produced SAPS can be levered into ECP, because at a deep level both are wet chemistry on a wafer with extreme precision requirements. The early evidence is encouraging. The company has been winning slots in mainland Chinese fabs for ECP tools targeting both copper interconnect and advanced packaging applications, with the advanced packaging variant—Wafer Level Packaging ECP—seeing particularly strong traction. The growth rate of the segment, off a small base, has been running well above the rate for the cleaning core. If ACMR can keep that ramp going for a few more years, ECP could be a meaningful contributor to revenue and a structural diversification away from the cleaning concentration.

The second hidden business is furnaces. In semiconductor manufacturing, a furnace is a vertical or horizontal heated tube into which batches of wafers are loaded for thermal process steps—oxidation, diffusion, anneal, low-pressure CVD. The furnace business has been one of the quietly profitable corners of the global semicap industry for decades, with Tokyo Electron's TELindy furnace franchise and Hitachi-Kokusai's Kokusai division (now part of Applied Materials) splitting most of the global market. Furnace tools are not glamorous. They are not nodes-defining. But they are essential, they are sticky, and they generate excellent gross margins. ACM has been incubating its own vertical furnace and atomic layer deposition platforms, with initial customer evaluations underway and first shipments to Chinese customers in the past two years. Strategically it is a direct shot at TEL's bread and butter, with the same customer-base advantage—Chinese fabs need credible alternative suppliers for everything, and a furnace tool from a vendor they already trust on cleaning is an easier sell than a furnace tool from a brand they have never bought from.

The third hidden business, and arguably the most strategically interesting, is what the company calls Tahoe. The Tahoe platform is a sulfuric-acid-based cleaning tool that incorporates a patented onboard recycling system. Sulfuric acid is the workhorse chemical of semiconductor cleaning. The conventional sulfuric peroxide mix used in industry consumes prodigious quantities of the chemical and generates correspondingly massive volumes of contaminated waste. Fab operators have been under increasing pressure—from environmental regulators, from corporate ESG commitments, from the simple cost arithmetic of disposing of acid waste—to reduce sulfuric acid consumption. ACM's Tahoe platform reduces sulfuric acid usage by something on the order of eighty to ninety percent compared with traditional single-wafer or batch sulfuric tools, by recycling the acid in a closed loop on the tool itself. That is a step-change improvement in operating cost and environmental footprint. More importantly for ACMR, it is a Trojan horse into Tier-1 global fabs—the Samsungs and Intels and TSMCs of the world—that have so far been beyond the reach of the company's traditional product line. A non-Chinese fab that wants to dramatically reduce its acid consumption and waste volume has, at the moment, very few alternatives to Tahoe. The win opens a door.

The fourth hidden business, related to but distinct from advanced packaging ECP, is the broader advanced packaging wet equipment opportunity. As Moore's Law has slowed at the transistor level, the leading edge of the industry has moved to "more than Moore" architectures—chiplet designs, 2.5D and 3D integration, hybrid bonding, through-silicon vias. Each of these techniques requires new wet processes for cleaning, plating, and surface preparation, often on bonded wafer pairs or reconstituted carrier wafers. The advanced packaging tool market is growing rapidly and is much less consolidated than the front-end wet cleaning market. ACM has been building product specifically for advanced packaging applications—wet etch, wet clean, copper plating, photoresist strip—and has been winning customer evaluations at OSATs and at the packaging arms of integrated device manufacturers. If chiplet-based design becomes the dominant paradigm for high-performance computing, as most industry observers now expect, the advanced packaging tool market will be one of the structural growth engines of the next decade, and ACMR is one of a small number of companies positioning to capture it.

The fifth hidden business is the company's expanding presence in the emerging silicon-carbide and compound-semiconductor processing market. As power electronics for electric vehicles, charging infrastructure, and industrial drives migrate from silicon to silicon carbide and gallium nitride, the wet processing requirements of the new substrates have created opportunities for new tool platforms. ACM has begun shipping cleaning tools optimized for SiC wafer processing into the rapidly expanding Chinese power-semi ecosystem. It is a small business today but a meaningful option on the next wave of semiconductor capital spending.

Taken together, the hidden businesses represent something like a second ACM forming inside the first. The cleaning core continues to provide the cash flow, the customer relationships, and the manufacturing scale. The new businesses—ECP, furnaces, Tahoe, advanced packaging, SiC—each ride on top of those assets and extend the company's reachable served market by multiples of the cleaning core alone. The pattern is the classic Applied Materials playbook of forty years ago—use a strong franchise in one wet or dry process step to bootstrap into adjacent steps, until the company is selling thirty different tool families to the same customers. Whether ACM can pull off the same multi-segment expansion at a much larger scale than it has yet demonstrated is one of the critical open questions for the next five years.

VII. The Playbook: Business and Investing Lessons

Look across the Acquired catalog of company stories and one of the patterns that recurs is the question of what made an underdog actually win. It is rarely a single thing. It is usually a combination of an honest assessment of where the incumbents are weak, a willingness to redefine the competitive terrain rather than fight on the incumbent's ground, and a piece of structural luck that turns into a moat. ACM is, in some ways, a pristine specimen of the underdog playbook executed correctly.

The first piece of the playbook is what Hamilton Helmer, in his Seven Powers framework, would call counter-positioning. The big incumbents—Lam Research, Tokyo Electron, DNS Screen—had massive installed bases of conventional megasonic cleaning tools. Those installed bases were generating service revenue and customer lock-in for decades to come. To switch their own architectures to something like SAPS would have meant cannibalizing their own franchise, writing down their installed-base support business, and signaling to customers that the conventional tools were obsolete. None of them moved. ACM, with no installed base to defend, had every reason to push the new architecture as aggressively as possible. The asymmetry was the wedge.

The second piece is the second-source strategy. The instinct of a small competitor in a concentrated market is often to try to be cheaper. That almost never works in capital equipment, where the customer is buying decades of operating reliability rather than a single transaction. ACM took the opposite approach—it positioned itself not as the cheap alternative but as the credible second source. For a Chinese fab in 2015 worried about its dependence on US and Japanese tool vendors, the question was not "is ACM cheaper than Lam?" The question was "if a future US export control rule restricts my access to Lam's tools, do I have a qualified alternative on my line?" In that framing, ACM was selling insurance, not equipment, and insurance carries a different price point and a different urgency than equipment.

The third piece is geopolitical hedging at the corporate structure level. The Delaware-incorporated, NASDAQ-listed parent owns the Chinese operating subsidiary, which itself is independently listed in Shanghai. When the United States imposed escalating chip export controls on China starting in 2018 and accelerating under the Biden administration's October 2022 controls and the subsequent updates, the question for every American-headquartered semicap company was how to navigate the new restrictions. ACM's structure gave it more degrees of freedom than most. The Chinese subsidiary, with its own listed stock, its own Chinese supply chain, and its own deeply embedded position in the Chinese fab base, looks to Beijing like a domestic champion. The American parent, with its US listing and US-domiciled IP holdings, looks to Washington like a US company. That dual identity is not a permanent solution to the geopolitical squeeze, but it has bought the company room to operate in a regulatory environment where many peers have found themselves stuck on one side or the other.

The fourth piece is what could be called reverse globalization. The conventional model of US semiconductor companies in the 1990s and 2000s was to design in California and outsource manufacturing or assembly to Asia. ACM did something different. The headquarters and the legal entity stayed in California, but the operating heart—engineering, manufacturing, customer support, the lion's share of revenue—rooted itself in China to capture the fastest-growing fab buildout in industry history. It was not outsourcing. It was rooting. The distinction matters because rooting creates a level of customer intimacy and supply-chain integration that pure outsourcing never could.

The fifth piece, perhaps the most underappreciated, is patience. ACM was a zombie for ten years. The first five years of trying to sell into the US fab market produced essentially nothing. The pivot to China took another three years to translate into real revenue. The first SAPS qualification at SK Hynix took the better part of a decade from invention to volume. None of this was fast. None of it was the kind of story that fits comfortably into a venture capital fund's seven-year horizon. The company survived because the founder and a small group of patient capital providers were willing to wait. In capital equipment more than almost any other industry, time is the moat.

Pulling these threads together yields a few lessons that travel beyond this particular case. In a concentrated industrial market with high switching costs, do not try to be cheaper—try to be differently better, in a way the incumbents cannot follow without cannibalizing themselves. Use corporate structure as a strategic tool, particularly when geopolitical risk is bifurcating customer markets. Be willing to lose money for a decade if the long-term position is worth it. And when capital becomes available—as it did for ACM in the STAR listing—reinvest aggressively in product breadth rather than buying growth through acquisitions priced for a different cycle.

It is the kind of playbook that is easier to read about than to execute. But the structure of the next chapter for ACMR—and for any investor watching it—turns on whether the same playbook can be repeated in the new product categories the company is opening up. The same questions of timing, customer qualification, incumbent response, and capital deployment apply to ECP, to furnaces, and to Tahoe as applied a decade ago to SAPS.

VIII. Strategy Framework: 7 Powers and Porter's Five Forces

The question for any investor in a capital equipment company is whether the position the company occupies is structurally durable. Cyclical revenue can come and go. Margin compression and expansion are part of the business. What matters over a multi-decade horizon is whether the moat is real and whether it widens or narrows over time. Hamilton Helmer's Seven Powers framework and Michael Porter's Five Forces are the right lenses for thinking through that question, and ACMR fits cleanly into both.

Start with counter-positioning, which is the cleanest of the seven powers in the ACMR story. The incumbent wet-cleaning vendors built their franchises around conventional megasonic and single-wafer cleaning architectures. Their tens of thousands of installed tools generate billions in service revenue and lock customers into a particular workflow. For Lam Research or Tokyo Electron to adopt a SAPS-equivalent architecture would mean obsoleting that installed base. They cannot. So the new architecture has had open field to grow into the new node transitions. That structural inability of the incumbents to follow is exactly what counter-positioning means in Helmer's framework.

The second power at work is switching costs. Once a wet cleaning tool is qualified into a particular process flow at a particular fab—for a particular layer at a particular node—the cost of swapping it out for a competitor's tool is enormous. Re-qualification can take six to twelve months. It risks yield excursions. It pulls process integration engineers away from new-node ramps. So once ACM tools are in, they tend to stay in for the life of the node, which in the case of mature nodes can be ten to fifteen years. Every win compounds into a very long-tail revenue stream.

The third power is process power, in Helmer's terminology. ACM has accumulated, over twenty-five years, a depth of know-how in wet chemistry, megasonic cavitation, bubble dynamics, acid recycling, and copper plating chemistry that is genuinely difficult to replicate. New entrants face not just patent moats—although the company has built a substantial patent estate around SAPS, TEBO, and Tahoe—but also tacit knowledge moats that exist only inside the heads of a few hundred process engineers in Fremont and Lingang.

The fourth power, scale economies, is more limited in the cleaning equipment business than in, say, lithography. The capital-equipment industry as a whole is a large-scale cottage industry, with most tool families produced at low single-digit-thousand units per year globally. But within the niches ACM occupies, scale matters at the customer-relationship level—the company that is qualified at twenty fabs has a much easier time getting qualified at the twenty-first than a company qualified at zero. ACMR is now well past the threshold where scale economics work in its favor.

The remaining three powers—network economies, branding, and cornered resource—are weaker for ACMR. There is no network effect in cleaning tools. The brand premium, if any, is modest. The cornered resource is partial—the company has access to a particular pool of Chinese semiconductor engineering talent through its Shanghai operations that competitors find hard to replicate, but that is a regional advantage rather than a global one.

Turning to Porter's Five Forces, the picture is also generally favorable. Buyer power is, on the surface, high—there are only a few dozen meaningful customers in the global wafer fab industry, and the largest among them—TSMC, Samsung, Intel, Hynix, Micron, SMIC, YMTC—have enormous purchasing leverage. But within the cleaning niche, those buyers' need for a credible second or third source means the negotiating dynamic is more balanced than headline market concentration would suggest. ACMR is not in the position of a commodity supplier being squeezed on price; it is closer to the position of a strategic alternative whose presence keeps the dominant vendor honest.

Supplier power is moderate and is, frankly, one of the structural risks in the business. Wet cleaning tools require specialized components—high-purity chemical-handling valves and pumps, megasonic transducers, robot end-effectors, contamination-controlled enclosures—many of which are sourced from a small number of US, European, and Japanese specialty suppliers. Export controls or supply disruptions on any of these inputs could constrain ACMR's ability to ship. The company has been visibly working to localize its supply chain, particularly within China, but the localization is incomplete and is one of the genuine vulnerabilities investors have to track.

Competitive rivalry within the immediate niche is intense at the technology level but limited at the headline market-share level. Lam Research, Tokyo Electron, and DNS Screen are formidable competitors with deep customer relationships and large installed bases. But the tacit truce that often characterizes mature semicap niches—each player has its own customer strongholds and process specialties—has held more or less. ACM has carved out its strongholds in mainland Chinese fabs, in certain Korean memory operations, and in particular advanced-node cleaning steps where its architecture has a structural advantage.

The threat of new entrants is low. The combination of multi-year qualification cycles, deep know-how requirements, large capital intensity for R&D and demonstration tools, and a customer base that is reluctant to take risks on new vendors creates a barrier to entry that is among the highest in any industrial market. The two most plausible sources of new competitive pressure are other Chinese domestic semiconductor equipment companies—Naura, AMEC, SMEE—pushing into adjacent wet process areas, and a possible reorganization or restructuring of the existing global incumbents that produces a more aggressive pricing posture. Neither has materialized in a way that has shifted the structural dynamics, but both are worth tracking.

The threat of substitutes is moderate. Dry cleaning processes—plasma cleaning, supercritical CO2 cleaning—have been advancing for decades and at the margin have substituted for wet cleaning in certain applications. The trend has not been existential, and wet cleaning continues to be the dominant approach for the great majority of cleaning steps, but the pace at which the substitution accelerates is one of the longer-term forces shaping the wet cleaning market.

Synthesizing across both frameworks, ACMR sits in a structurally attractive position with multiple powers operating in its favor and most of the five forces favorable. The moat is genuine. The risks are real but manageable. The most acute risk is not competitive—it is geopolitical, and that is the subject of the next section.

IX. The Bull and Bear Case

Every long-form deep-dive on a complex company eventually arrives at the same exercise—line up the strongest version of the optimistic case, line up the strongest version of the pessimistic case, and let the listener decide which set of probabilities looks more compelling. For ACMR the bull and bear case hinge on the same handful of variables, just weighted differently.

The bull case starts with the addressable market. China is in the middle of the largest sustained semiconductor fab buildout in history. The country has, depending on the count, somewhere between fifty and seventy fabs at various stages of construction or planning, ranging from mature-node power and analog facilities to advanced-node logic and memory. Each of those fabs requires hundreds of millions of dollars of wet processing equipment alone. Indigenous substitution—the policy and commercial preference for Chinese-made equipment in Chinese fabs—has been escalating, partly in response to US export controls and partly as an industrial policy objective in its own right. ACMR is the dominant indigenous wet equipment supplier and one of only a few companies positioned to capture meaningful share across cleaning, plating, furnace, and packaging tools. If the Chinese fab buildout continues at anything like its current pace, ACMR's served addressable market will multiply over the next decade.

The bull case continues with the hidden businesses. ECP, furnaces, Tahoe, advanced packaging, and SiC processing each represent extension opportunities into market segments many times larger than the current revenue base. If even half of those new businesses scale into meaningful contributors, the company's revenue mix and growth profile shift fundamentally. Margin profile also stands to improve as the new product categories mature, because the gross margin headwind from product introductions in the first few years tends to reverse as volumes ramp and cost engineering kicks in.

The bull case also points to capital structure. ACMR's consolidated balance sheet carries a substantial cash position—the result of the STAR listing proceeds, retained operating cash flow, and a relatively conservative capital allocation posture. The company's enterprise value, particularly when the holding-company discount is at its widest, can look surprisingly modest relative to the cash on the balance sheet and the value of the listed Chinese subsidiary stake. The hidden balance-sheet asset is one of the recurring elements of the bull case.

The bear case is fundamentally about the geopolitical squeeze. ACMR is structurally exposed to the worst-case scenarios of US-China technology decoupling. The October 2022 US export controls, the various entity list expansions, the ongoing tightening of which equipment can be exported to which Chinese fabs—all of it creates compliance overhead and, in extreme scenarios, could materially impair the company's ability to operate. ACMR has not been added to any major US restriction list, and its products do not generally fall into the categories most directly targeted by current export controls. But the surface area of risk is large. A sudden change in US policy that restricts ACM's ability to ship US-origin components to Chinese customers, or that restricts the parent's relationship with the Chinese subsidiary, would be highly disruptive. The bear case takes the view that the political risk is non-trivial and largely outside management's control.

The bear case also raises customer concentration. A meaningful portion of ACMR's revenue comes from a relatively small number of large mainland Chinese customers. Some of those customers are themselves on US restriction lists, which complicates the operating relationship even when the tool sales themselves are not directly restricted. Any disruption at one or two key Chinese customers—whether from sanctions, financial distress, or strategic reorientation—would have an outsized impact on revenue.

The bear case also questions the new business momentum. ECP, furnace, and Tahoe revenues are still relatively small compared with the cleaning core. The bear view is that incumbent vendors—Lam, TEL, AMAT—are not standing still and have the resources to push back hard if any of the new businesses start to take meaningful share. The bull case's vision of ACMR scaling into a multi-segment Applied-Materials-of-China requires execution at a level the company has not yet demonstrated at the scale required.

The bear case finally points to the dual-listing structural risk. The complexity of the parent-subsidiary listing creates ongoing valuation friction, and any structural change—an attempted privatization of one or the other entity, a forced delisting from a US exchange under PCAOB or HFCAA pressure, a Chinese regulatory action affecting the subsidiary—would create binary risk for the equity. The structure that has been such an asset could become a liability under specific stress scenarios.

A holistic view weighing these forces points to a few KPIs that genuinely matter for tracking the company. The first is mainland Chinese fab capacity additions—particularly mature-node and 28-nanometer-class capacity—because that is the single best leading indicator of ACMR's served market over the next two to three years. The second is the revenue contribution from new product categories, particularly ECP and furnace, as a share of total revenue—because that is the cleanest measure of whether the multi-segment expansion thesis is playing out. The third is gross margin—because in capital equipment, sustained gross margin in the high forties or low fifties is the marker of a structurally advantaged player rather than a commodity supplier, and watching the trajectory tells you whether the company is winning on price or on technology.

Beyond those, a handful of secondary indicators are worth watching as overlay diligence. The company's audit firm and any changes to its disclosure regime under the PCAOB inspection regime that has progressed in fits and starts since 2022. Any insider transactions or 13F changes by sophisticated holders—particularly those concentrated holders who entered the name during the post-STAR-listing dislocation. Any movement on the Lingang campus buildout, which is the physical proxy for the company's growth ambition. And, of course, every twist of the US export control regime as it affects semiconductor equipment shipments to mainland China.

The "myth versus reality" exercise here is also worth doing briefly. The consensus market narrative on ACMR is sometimes that it is essentially a Chinese company with a NASDAQ wrapper, and therefore should trade at the discount applied to other US-listed Chinese companies. The reality is more nuanced—the parent is a Delaware-incorporated, US-headquartered company with a substantial portion of its R&D and IP in the United States, and the operating subsidiary is genuinely Chinese, but the relationship is a real one and the consolidated entity has, so far, maintained the disclosure and audit standards of a US-listed company. Whether the market eventually closes the holding-company discount, or whether structural change is required to close it, is one of the live questions that any investor in the equity has to form a view on.

The other piece of consensus mythology is that ACMR's competitive advantage is its low-cost Chinese manufacturing. The reality is that the competitive advantage is the technology and the customer intimacy at Chinese fabs. Manufacturing cost matters but it is not the moat. Investors who think of ACMR as a low-cost producer are pattern-matching to a different industry. The right comparison is Applied Materials in the mid-1980s or Lam Research in the late 1990s—a focused, technology-driven, customer-obsessed semicap company in the early years of a long compounding ramp, just with the specific tailwind of being the indigenous champion of the world's largest fab buildout.

The story is, of course, still being written. The chip war continues to evolve. The Chinese fab buildout continues to accelerate. The hidden businesses continue to either prove themselves out or fall short. Twenty-eight years after a Bell Labs physicist rented a small commercial space in Fremont, the company he built is not yet finished becoming whatever it is going to be. For long-term observers and patient capital, that ongoing evolution is precisely what makes it worth watching.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube