AECOM: Building the World's Infrastructure Giant

I. Introduction & Episode Roadmap

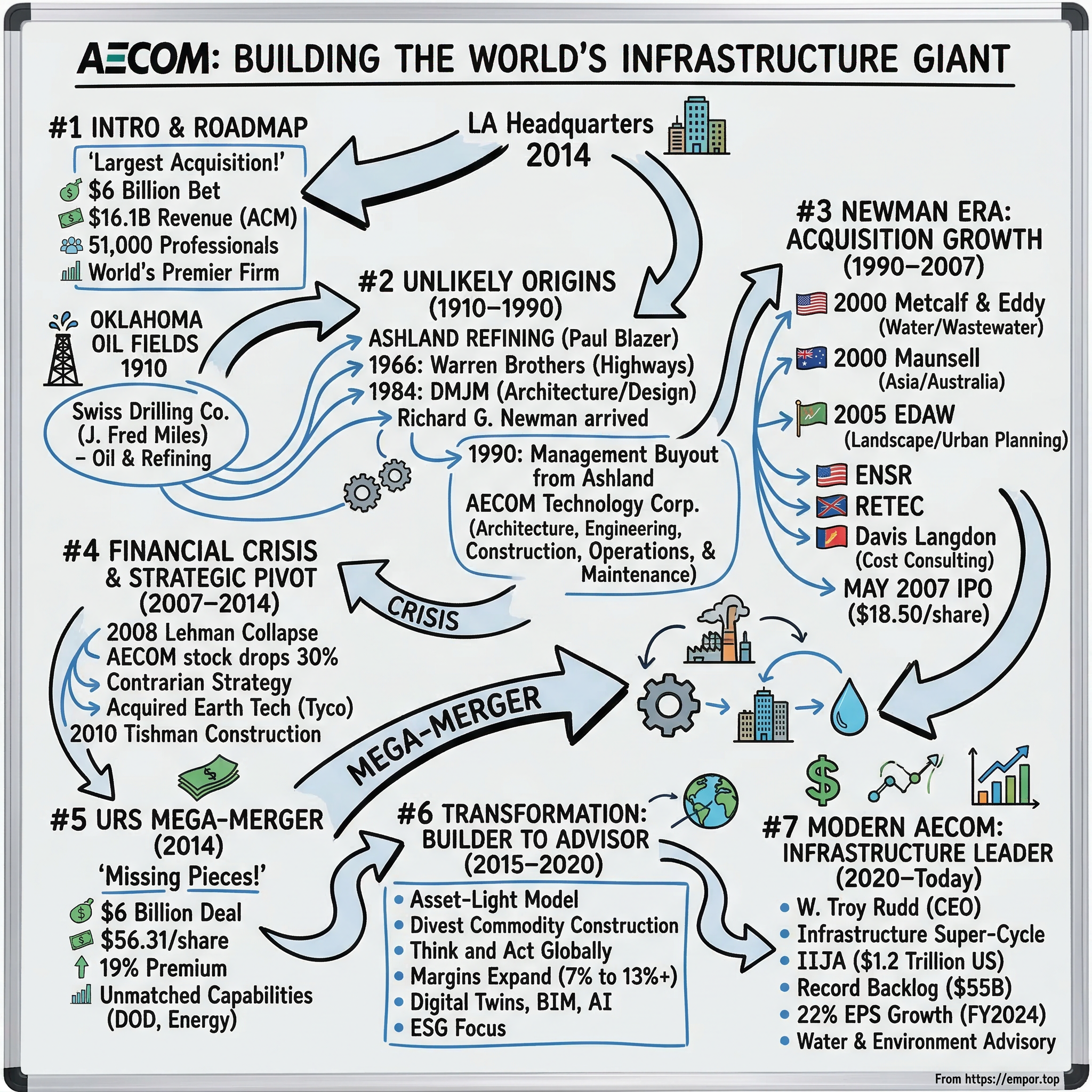

Picture this: It's 2014, and Michael Burke is standing in AECOM's Los Angeles headquarters, staring at a wall of architectural drawings. The Burj Khalifa. The Second Avenue Subway. The London Olympics. Each project represents not just concrete and steel, but a piece of the modern world's infrastructure DNA. In a few hours, he'll announce the largest acquisition in the company's history—a $6 billion bet that will transform AECOM from a major player into the undisputed infrastructure giant. But to understand how a company born from an oil refiner's castoff division became the architect of the world's skylines, we need to go back to an unlikely beginning in the Oklahoma oil fields.

AECOM today stands as a $16.1 billion revenue colossus, employing approximately 51,000 professionals across 150 countries. Ranked #291 on the Fortune 500, it's the world's premier infrastructure consulting firm—a title earned not through organic growth alone, but through one of the most aggressive acquisition strategies in corporate history. The company has designed everything from NASA facilities to Olympic venues, from water treatment plants serving millions to transportation networks connecting continents.

Yet here's the paradox: AECOM is simultaneously everywhere and invisible. Its fingerprints are on virtually every major infrastructure project of the past three decades, but most people have never heard of it. It's a company that builds without building, designs without owning, and operates at the intersection of public need and private enterprise. How did a 1990 management buyout from Ashland Oil transform into the world's #1 ranked infrastructure design firm? How did they execute over 50 acquisitions while maintaining operational excellence? And what does their story tell us about the future of global infrastructure?

This is a tale of three transformations: first, from oil to infrastructure; second, from regional player to global powerhouse; and third, from asset-heavy builder to asset-light advisor. It's about timing markets perfectly while others panicked, about seeing opportunity in complexity, and about the audacious belief that one company could master every aspect of the built environment. Along the way, we'll meet the visionaries who saw infrastructure not as concrete and steel, but as the circulatory system of civilization itself.

II. The Unlikely Origins: From Oil to Infrastructure (1910–1990)

The story begins not in a boardroom but in the red dirt of Oklahoma, 1910. J. Fred Miles wasn't thinking about infrastructure when he founded Swiss Drilling Company—he was chasing black gold. By the time he established Swiss Oil Company in Lexington, Kentucky, the vision was simple: find oil, refine it, sell it. But companies, like rivers, rarely flow in straight lines. When Paul Blazer took the helm of what became Ashland Refining Company in 1924, he inherited not just refineries but a culture of opportunistic expansion that would, decades later, give birth to AECOM.

Blazer was a chemical engineer by training but a empire-builder by temperament. Under his leadership, Ashland grew from a regional refiner into a diversified industrial conglomerate. The pivotal moment came in 1966—long after Blazer's era—when Ashland acquired Warren Brothers Company, a highway construction firm with a century-old pedigree. The logic was beautifully circular: Ashland's refineries produced asphalt as a byproduct; Warren Brothers laid that asphalt on America's expanding highway system. It was vertical integration at its most elegant, turning waste into profit, byproduct into business line.

But the real DNA of future AECOM came through a 1984 acquisition that seemed, at the time, almost random. Daniel, Mann, Johnson & Mendenhall (DMJM) was a Los Angeles architectural firm with a fascinating backstory. Founded in 1946 by four partners who'd met working on military projects during World War II, DMJM had evolved from designing air bases to creating the infrastructure of post-war America. They'd worked on everything from aerospace facilities to urban planning projects, developing a reputation for tackling complex, multi-disciplinary challenges that scared off traditional firms.

With DMJM came Richard G. Newman, a man whose vision would prove transformative. Newman wasn't your typical infrastructure executive—he thought like a software entrepreneur trapped in a hard-asset industry. When he arrived at Ashland Technology Corporation (as the infrastructure division was known) in 1987 as CEO, he inherited a hodgepodge of engineering firms, construction companies, and technical services providers. Revenue was respectable but growth was sluggish. The business was profitable but unloved by Ashland's board, which increasingly saw oil refining and chemicals as the future.

Newman saw opportunity where others saw orphaned assets. Throughout 1989, he orchestrated one of the more unusual transactions in corporate history: proposing that employees buy back the division from Ashland. The negotiations were delicate—Ashland wanted out but didn't want to give away value; Newman needed to convince both sellers and buyers that this collection of engineering firms could stand alone. The financing was complex, involving employee stock ownership plans, management equity, and creative debt structures that would make a private equity firm blush.

The name itself—AECOM—was Newman's invention, an acronym that captured the full scope of ambition: Architecture, Engineering, Construction, Operations, and Maintenance. It was deliberately broad, almost hubristically so. While competitors focused on niches, Newman was declaring his intention to own the entire infrastructure value chain. When the deal closed in 1990, AECOM Technology Corporation was born with approximately 3,300 employees and a handful of offices. Nobody could have predicted that this management buyout from an oil company would become the foundation for the world's largest infrastructure firm.

III. The Newman Era: Building Through Acquisition (1990–2007)

Richard Newman's first day as CEO of the newly independent AECOM Technology Corporation began with a paradox. He had just led one of the more audacious employee buyouts in corporate history, yet the company's bank account was essentially empty after the transaction costs. The five entities that merged to form AECOM—with predecessor firms dating back more than 120 years—brought impressive credentials but limited synergies. Newman's solution would define AECOM's DNA for the next three decades: grow through strategic acquisition, but make each deal about capability, not just capacity.

The 1990s were a masterclass in disciplined expansion. While dot-com millionaires were being minted in Silicon Valley, Newman was quietly assembling an infrastructure empire through unglamorous but essential acquisitions. Each target was selected with surgical precision—not for revenue alone, but for the specific expertise it brought to AECOM's growing portfolio. The company became known in M&A circles for its unusual due diligence process: instead of just examining financials, AECOM teams would spend weeks understanding a target's project methodology, client relationships, and technical capabilities.

The year 2000 marked a watershed with the acquisition of Metcalf & Eddy, a firm whose history read like an encyclopedia of American water infrastructure. Founded in 1907, Metcalf & Eddy had literally written the book on wastewater treatment—their technical manuals were standard texts in engineering schools. The acquisition brought not just revenue but institutional knowledge that couldn't be replicated. Newman understood something his competitors missed: in infrastructure, reputation and expertise compound over decades. You couldn't just hire smart engineers and compete; you needed the accumulated wisdom of thousands of projects.

By 2004, AECOM was ready for international expansion, acquiring UMA Engineering Ltd. in Canada. The move seemed modest—UMA was a mid-sized firm focused on transportation and municipal infrastructure. But Newman saw Canada as a proving ground for AECOM's global ambitions. The integration went flawlessly, validating the company's ability to absorb firms across borders while maintaining operational excellence.

Then came the acquisition spree that transformed AECOM from a solid regional player into a global force. In rapid succession, the company acquired Maunsell (bringing Asian and Australian expertise), EDAW (landscape architecture and planning), Economic Research Associates (economic consulting), ENSR (environmental services), The RETEC Group (environmental remediation), Ellerbe Becket (sports facilities and healthcare), and Davis Langdon (cost consulting). Each acquisition was a chess move, filling gaps in either geographic coverage or technical capability.

The Maunsell acquisition deserves special attention. Founded in 1955 by Guy Maunsell, the firm had pioneered innovative engineering solutions across Asia-Pacific, including the iconic Tsing Ma Bridge in Hong Kong. When AECOM acquired Maunsell in 2000, it wasn't just buying projects and people—it was buying decades of relationships with Asian governments and understanding of how to operate in emerging markets. Newman would later call it "the acquisition that made us truly global."

EDAW, acquired in 2005, brought something different: design sensibility. Known for landscape architecture and urban planning, EDAW had worked on projects ranging from the 1996 Atlanta Olympics to Disneyland Paris. The cultural integration was challenging—EDAW's designers initially clashed with AECOM's engineers, each group viewing the other with suspicion. But Newman personally intervened, hosting integration sessions where he emphasized that future infrastructure projects would require both technical excellence and design innovation.

The IPO in May 2007 was Newman's crowning achievement. AECOM went public on the NYSE at $18.50 per share, raising $468.3 million and valuing the company at over $2 billion. The timing seemed perfect—infrastructure spending was booming globally, and AECOM was positioned as the pure-play infrastructure investment. The roadshow had been a triumph, with Newman personally charming institutional investors with his vision of infrastructure as "the business that makes all other businesses possible."

But even as champagne flowed at the NYSE that May morning, storm clouds were gathering. The subprime mortgage crisis was beginning to metastasize into something larger. Within months, the financial world would be in freefall. The question wasn't whether AECOM could continue its growth trajectory, but whether it could survive what was coming.

IV. The Financial Crisis & Strategic Pivot (2007–2014)

Michael S. Burke was in London when Lehman Brothers collapsed on September 15, 2008. As AECOM's CFO, he'd been meeting with investors, trying to explain why an infrastructure company was actually countercyclical to financial markets. The theory was elegant: governments respond to recessions with infrastructure spending. The reality was messier. By the time Burke's plane landed back in Los Angeles, AECOM's stock had dropped 30%. Credit markets were frozen. Competitors were laying off thousands. And somehow, in this chaos, Burke and Newman saw the opportunity of a lifetime.

The Earth Tech acquisition in July 2008 was either brilliantly contrarian or monumentally reckless. Tyco International, desperate for cash, was selling its environmental and infrastructure division for $510 million—a fraction of what it might have commanded a year earlier. Earth Tech brought 7,500 employees and deep expertise in water and environmental services. But the real prize was its government relationships, particularly with federal agencies that would soon be deploying stimulus spending. While other firms were retrenching, AECOM was doubling down, using its relatively strong balance sheet to acquire assets at distressed prices.

The integration of Earth Tech became a template for crisis-era acquisitions. Instead of the usual post-merger layoffs, AECOM retained nearly all Earth Tech employees, betting that stimulus spending would create more work than existing staff could handle. Burke, who was increasingly taking operational control as Newman prepared for retirement, instituted weekly cash flow meetings and daily project reviews. The message was clear: preserve capabilities, manage cash religiously, and position for the rebound.

By 2010, Burke's contrarian strategy was paying dividends. The American Recovery and Reinvestment Act had unleashed $105 billion in infrastructure spending. China's massive stimulus program was creating opportunities across Asia. And AECOM, having maintained its capabilities while competitors downsized, was perfectly positioned to capture this work. The July 2010 acquisition of Tishman Construction for $245 million was the exclamation point—AECOM was not just surviving the crisis but using it to transform its business model.

Tishman wasn't just any construction company. Founded in 1898, it had built New York landmarks from Madison Square Garden to the World Trade Center. The firm brought something AECOM desperately wanted: construction management expertise for complex, high-profile projects. This wasn't about owning bulldozers and cranes; it was about managing the intricate dance of subcontractors, suppliers, and stakeholders that modern mega-projects required.

Burke officially became CEO in 2014, inheriting a company that had grown to over 45,000 employees. His style was different from Newman's—less visionary, more operational. Where Newman would paint broad strategic pictures, Burke would dive into project-level details. Employees joked that Burke knew the status of every major project in the company's portfolio, and they weren't entirely wrong. His background as CFO had given him an unusual appreciation for the economics of individual projects, and he used this knowledge to drive margin improvement across the business.

The 2014 acquisition of Hunt Construction Group continued the strategic pivot toward construction services. Hunt brought expertise in sports facilities, having built venues for multiple professional teams. But more importantly, it validated Burke's thesis that AECOM could be both designer and builder without conflicts of interest. The traditional industry model—where designers and constructors were strictly separated—was breaking down. Clients increasingly wanted integrated delivery, where one firm could handle everything from concept to completion.

Throughout this period, AECOM was also quietly building capabilities that would prove crucial for its next phase. The company invested heavily in Building Information Modeling (BIM) technology, making it one of the first major firms to fully digitize its design process. It established a global center of excellence for project management in Delhi, leveraging India's technical talent to support projects worldwide. And perhaps most presciently, it began developing expertise in climate resilience and adaptation, anticipating that extreme weather would drive a new wave of infrastructure investment.

By early 2014, AECOM had emerged from the financial crisis not just intact but transformed. Revenue had grown from $5 billion to over $8 billion. The company had successfully integrated multiple major acquisitions while maintaining operational excellence. But Burke wasn't satisfied. In his office, he kept a chart showing the global infrastructure market—worth over $4 trillion annually. AECOM's share was less than 0.2%. The opportunity was massive, but capturing it would require a bold move. That move would come in the form of the largest acquisition in company history.

V. The URS Mega-Merger: Doubling Down (2014)

The phone call came on a Sunday evening in June 2014. Martin Koffel, CEO of URS Corporation, had finally agreed to serious merger discussions. Michael Burke had been courting URS for two years, seeing in it the missing pieces of AECOM's global puzzle. URS brought oil and gas expertise just as the shale revolution was transforming America's energy landscape. It had deep federal government relationships, particularly with the Department of Defense and Department of Energy. Most tantalizingly, it would make AECOM indisputably the world's largest infrastructure firm. The only question was price.

The negotiation that followed was a masterclass in strategic M&A. URS, founded in 1951 and incorporated in 1957, had its oldest predecessor firm dating back to 1904. It was a proud company with 50,000 employees and its own acquisition history—including Washington Group International and EG&G Technical Services. But URS had struggled since the financial crisis, with margins lagging peers and growth stalling. Activist investors were circling. Koffel knew he needed a deal, but he wasn't going to give the company away.

Burke's opening offer in early July was $53 per share. Koffel countered at $62. For three intense days, teams of bankers and lawyers shuttled between conference rooms in San Francisco and Los Angeles. The breakthrough came when Burke proposed a creative structure: $56.31 per share, representing a 19% premium over URS's 30-day average, paid in a combination of cash and stock. The stock component would let URS shareholders participate in the upside of the combined company. The total enterprise value, including URS's debt, would approach $6 billion—by far the largest deal in the infrastructure sector's history.

The announcement on July 13, 2014, sent shockwaves through the industry. Competitors scrambled to understand the implications. Clients worried about conflicts of interest. Employees on both sides wondered about layoffs. Burke went on an exhausting roadshow, explaining the strategic rationale to anyone who would listen. His message was consistent: this wasn't about cost-cutting but capability-building. The combined company would have the scale to compete for the world's largest projects, the expertise to handle any technical challenge, and the geographic reach to serve clients globally.

The integration planning was unprecedented in its scope and detail. Burke established 47 separate integration teams, each focused on a specific function or geography. The teams were co-led by AECOM and URS executives, forcing collaboration from day one. The target was $250 million in annual cost synergies, but Burke privately believed the revenue synergies would be even larger. URS's federal government relationships could open doors for AECOM's commercial expertise. AECOM's international presence could globalize URS's specialized capabilities.

The cultural challenges were real. URS employees, particularly in the oil and gas division, viewed themselves as energy specialists being absorbed by an infrastructure generalist. AECOM employees worried about URS's lower margins dragging down the combined company's performance. The first town hall after the October 17, 2014, closing was tense. Burke stood before 500 employees in URS's San Francisco headquarters and made a bold promise: "In five years, you'll look back on this merger as the moment AECOM became unstoppable."

The early months were rocky. Several high-profile URS executives departed. Some clients, particularly in the federal space, expressed concerns about the combined company's size and potential conflicts. The stock price, which had risen on the merger announcement, began to drift lower as integration costs mounted. Analysts questioned whether AECOM had overpaid, whether the cultures could truly mesh, whether the synergies were achievable.

But Burke and his team pressed forward with methodical execution. They retained URS's best technical experts by creating centers of excellence where they could lead global practices. They invested in systems integration, spending $100 million to create a unified project management platform. Most importantly, they began winning work that neither company could have won alone—massive, complex projects that required both AECOM's design excellence and URS's execution capabilities.

The transformation wasn't just operational but strategic. The combined company had unmatched capabilities across the entire infrastructure value chain. It could design a liquefied natural gas facility, manage its construction, and provide operations support once completed. It could plan a city's transportation network, engineer its implementation, and maintain it for decades. The breadth was staggering: 95,000+ employees in 150 countries, working on everything from NASA facilities to nuclear cleanup, from Olympic venues to offshore oil platforms.

By late 2015, the merger was beginning to deliver results. Revenue synergies were exceeding expectations as the combined company won several billion-dollar programs. Cost synergies were on track, achieved through office consolidations and administrative efficiencies rather than mass layoffs. The stock price had recovered and was reaching new highs. But Burke knew that size alone wouldn't guarantee success. The infrastructure industry was changing, driven by digitalization, sustainability concerns, and new delivery models. AECOM needed to transform again, this time from builder to advisor, from asset-heavy to asset-light. The mega-merger with URS had created the platform. Now it was time to optimize it.

VI. The Transformation Strategy: From Builder to Advisor (2015–2020)

The rebranding ceremony in October 2015 was deliberately understated. No fanfare, no celebrity speakers—just Michael Burke standing in front of a simple backdrop announcing that AECOM Technology Corporation would now be simply "AECOM." The name change symbolized something deeper: a company shedding its conglomerate past to become a focused professional services powerhouse. Behind the scenes, Burke had been orchestrating one of the most dramatic strategic pivots in the infrastructure sector.

The thesis was counterintuitive. While competitors were racing to own more hard assets—equipment, real estate, construction yards—Burke was systematically divesting them. The 2017 acquisition of Shimmick Construction seemed to contradict this strategy, but it was actually the exception that proved the rule. Shimmick brought specialized expertise in complex water infrastructure, the kind of high-margin, technically demanding work that fit Burke's vision. Everything else that smacked of commoditized construction was on the chopping block.

The divestiture program was surgical in its precision. AECOM sold its claim construction business, its energy construction unit, and various real estate holdings. Each sale was small enough to avoid headlines but meaningful enough to improve margins. The cumulative impact was transformative: asset intensity dropped by 40%, return on invested capital doubled, and free cash flow generation improved dramatically. Wall Street initially misunderstood, viewing the divestitures as retreat. Burke saw them as liberation from capital-intensive, low-margin businesses that obscured AECOM's true value.

"Think and Act Globally" became the internal mantra, but it meant something specific. AECOM would no longer chase every project in every geography. Instead, it would focus on complex, high-value challenges where its integrated expertise provided genuine differentiation. A water treatment plant in Cincinnati might share technical DNA with one in Singapore. A transportation hub in London could inform designs in Los Angeles. The company built a knowledge management system that could capture lessons from 10,000 simultaneous projects and apply them globally.

The digital transformation was perhaps the most underappreciated aspect of this period. While headlines focused on divestitures and reorganizations, AECOM was quietly building one of the industry's most sophisticated digital capabilities. The company hired data scientists from Silicon Valley, creating predictive models for project risk and resource allocation. It pioneered the use of digital twins—virtual replicas of physical infrastructure that could simulate performance under different scenarios. By 2019, every major AECOM project had a digital component, whether drone surveying, 3D modeling, or artificial intelligence-assisted design optimization.

The margin improvement was dramatic. Adjusted EBITDA margins expanded from 7% in 2015 to over 13% by 2019. But this wasn't achieved through cost-cutting alone. AECOM was fundamentally changing its business mix, emphasizing design and program management over construction, consulting over contracting, advisory over assembly. The company's win rate on major pursuits improved as clients recognized the value of integrated expertise. Average project size increased as AECOM positioned itself for mega-programs rather than scattered small contracts.

Cultural transformation proved the hardest challenge. Engineers who had spent careers managing construction sites were being asked to become client advisors. Project managers accustomed to controlling physical assets were now orchestrating networks of partners and subcontractors. Burke instituted mandatory "client centricity" training for all senior staff, bringing in consultants from McKinsey to teach relationship management and value selling. The old AECOM had won work through technical excellence; the new AECOM would win through strategic partnership.

The environmental, social, and governance (ESG) transformation was more than window dressing. AECOM had always worked on environmental projects, but now sustainability became central to its identity. The company committed to net-zero emissions by 2030, not just for its own operations but across its entire value chain. It developed proprietary tools for calculating the carbon footprint of infrastructure projects and designing lower-impact alternatives. When the Business Roundtable redefined corporate purpose in 2019, AECOM was already there, having embedded stakeholder value into its strategy years earlier.

By early 2020, the transformation was largely complete. AECOM had evolved from a sprawling conglomerate to a focused professional services firm. Revenue might have been flat, but margins had expanded dramatically. The stock price had nearly doubled from its 2015 lows. Burke's vision of an asset-light, high-margin, digitally enabled infrastructure advisor was becoming reality. Then, in March 2020, the world shut down. COVID-19 would test every aspect of the transformation, but it would also validate Burke's strategic choices in ways nobody could have anticipated.

VII. Modern AECOM: The Infrastructure Leader (2020–Today)

W. Troy Rudd had been CEO for exactly six months when the full magnitude of COVID-19 became clear. Replacing Michael Burke in October 2019, Rudd inherited a transformed but untested organization. By March 2020, he faced an existential challenge: how do you manage 47,000 employees across 150 countries when nobody can travel, meet, or even access job sites? His response would define modern AECOM and position it for its most successful period ever.

The immediate transition to remote work was surprisingly smooth. Years of digital investment paid off as design teams seamlessly shifted to virtual collaboration. Project managers who had resisted video conferencing suddenly became Zoom experts. Client meetings that once required cross-country flights happened from home offices. But Rudd saw beyond crisis management to strategic opportunity. While competitors furloughed staff and froze hiring, AECOM accelerated its transformation, betting that post-pandemic infrastructure investment would be massive. The bet paid off spectacularly. Full year revenue increased 12% to $16.1 billion in fiscal 2024, with adjusted EBITDA and adjusted EPS increased 14% and 22%, respectively for the full year. But these numbers only tell part of the story. The real transformation was in AECOM's positioning for the infrastructure super-cycle that everyone could see coming but few were prepared to capture.

The Infrastructure Investment and Jobs Act (IIJA), signed in November 2021, allocated $1.2 trillion for American infrastructure over five years. AECOM wasn't just a beneficiary—it had helped shape the legislation through technical advisory work with government agencies. The company's experts had literally written sections of guidance documents that would govern how the money would be spent. When state and local governments needed help accessing and deploying IIJA funds, AECOM was already at the table. The numbers tell an extraordinary story. Design book-to-burn in the fourth quarter was 1.2x, including 1.2x in both the Americas and International segments, while design backlog increased by 5% and total backlog increased 3% to a new record. The Company's pipeline of opportunities increased by 10% and achieved a new high, driven by robust funding across all of its largest markets. More remarkably, the Company's design win rate of 50% remains at an all-time high and was even higher on larger pursuits. Gained market share as the number one ranked Water design firm by Engineering News-Record, now holding the number one position as top design firm in all key markets — including water, transportation, environment, and facilities. The rankings weren't just accolades—they represented billions in potential project wins. When governments and corporations needed expertise for their most complex challenges, AECOM was inevitably at the table.

The creation of the Water and Environment Advisory business in 2024 exemplified Rudd's strategic vision. This wasn't just another service line but an entirely new business model. Technology optimization is a major growth catalyst, with AECOM last month announcing a new "business line" offering data analytics and advanced digital tools for water asset management, environmental permitting and PFAS pollution remediation. The unit would operate at the intersection of traditional engineering and management consulting, commanding premium margins by helping clients navigate the complexity of multi-decade, multi-billion-dollar programs.

Lara Poloni, AECOM's president, became the face of this transformation. A civil engineer who had risen through the ranks over two decades, Poloni understood both the technical and commercial dimensions of infrastructure. She pioneered AECOM's "Think and Act Globally" philosophy in practice, creating centers of excellence that could deploy specialized expertise anywhere in the world within days. When a water crisis emerged in one geography, lessons learned from similar challenges elsewhere could be applied immediately.

The financial performance validated every strategic choice. For the full year, adjusted EBTDA and adjusted EPS increased 14% and 22%, respectively. "We have compounded earnings per share by 21% annually since fiscal 2020, including 22% growth in fiscal 2024," said Gaurav Kapoor, AECOM's chief financial and operations officer. These weren't just good numbers—they were exceptional for a traditionally cyclical, capital-intensive industry.

But perhaps the most remarkable achievement was the balance sheet transformation. AECOM had returned approximately $560 million to shareholders through repurchases and dividends in fiscal 2024 alone. Since initiating its repurchase program in September 2020, the company had bought back more than $2.2 billion of stock—approximately one-third of the Company's market capitalization at the time it began repurchases. This wasn't financial engineering but confidence in the business model's cash generation capabilities.

The pandemic had accelerated trends that AECOM had been positioning for years: the digitalization of infrastructure, the urgency of climate adaptation, the need for integrated delivery models. While competitors scrambled to adapt, AECOM was already there. The company's investments in Building Information Modeling, digital twins, and artificial intelligence-assisted design weren't pandemic responses but strategic choices made years earlier that suddenly became essential.

Looking forward, AECOM's positioning seems almost prescient. The global infrastructure gap—estimated at $15 trillion through 2040—represents not a challenge but an opportunity. Climate change will require trillions in adaptation spending. The energy transition will demand new transmission networks, renewable generation facilities, and grid modernization. Urban growth in emerging markets will necessitate water systems, transportation networks, and sustainable buildings. Every major trend points toward more demand for AECOM's expertise.

The Company expects to maintain an approximately 24% tax rate for the next several years. With Design backlog increased by 5% and total backlog increased 3% to a new record. Design book-to-burn in the fourth quarter was 1.2x, including 1.2x in both the Americas and International segments. The Company's pipeline of opportunities increased by 10% and achieved a new high, driven by robust funding across all of its largest markets. The visibility into future growth has never been clearer.

VIII. Playbook: The AECOM Method

The conference room on the 47th floor of AECOM's Dallas headquarters has witnessed dozens of acquisition negotiations. The walls are lined with tombstones—not of failures, but commemorative plaques from successful deals. Each represents not just a transaction but a piece of AECOM's DNA, absorbed and integrated into what has become the industry's most successful serial acquisition machine. The playbook that emerged from these experiences reads like a masterclass in corporate development, but its lessons extend far beyond M&A.

The Art of Serial Acquisition

AECOM's acquisition strategy defies conventional wisdom. While most companies struggle to integrate one major acquisition every few years, AECOM has successfully absorbed over 50 companies since 1990. The secret isn't in the deal-making—though AECOM has become exceptionally skilled at valuation and negotiation—but in the integration philosophy.

Every acquisition follows what internally is called the "Heritage Preservation Model." Instead of imposing AECOM's culture and erasing the acquired company's identity, the integration team identifies what made the target successful and preserves it. When AECOM acquired Maunsell, they didn't just keep the Asia-Pacific relationships; they elevated Maunsell's leaders to run AECOM's entire Asian operations. When Davis Langdon joined, their cost consulting methodology became the global standard. This approach turns potential cultural conflicts into competitive advantages.

The integration timeline is methodical: Day 1 focuses on employee retention and client communication. Week 1 establishes unified project management systems. Month 1 completes financial integration. Quarter 1 achieves operational synergies. Year 1 realizes revenue synergies. But the real magic happens in Year 2 and beyond, when the acquired company's expertise begins cross-pollinating with AECOM's existing capabilities, creating solutions neither company could have developed alone.

Leveraging Predecessor Heritage

AECOM doesn't have a founding myth—it has dozens of them. The company traces its lineage through firms dating back to 1904, each with its own legacy of innovation and excellence. This isn't corporate genealogy for its own sake; it's a strategic asset that opens doors and wins projects.

When competing for a water infrastructure project in Boston, AECOM can invoke Metcalf & Eddy's century of local expertise. When pursuing transportation work in Asia, Maunsell's heritage resonates. When bidding on iconic buildings, Ellerbe Becket's portfolio—including the Fiserv Forum and multiple Olympic venues—provides instant credibility. Competitors might have similar technical capabilities, but they can't replicate this accumulated trust.

The company maintains what it calls "technical genealogy"—detailed records of which predecessor firms worked on major infrastructure assets. When the Golden Gate Bridge needs rehabilitation, AECOM can demonstrate that its corporate ancestors helped build it. When Singapore plans a new metro line, AECOM can point to Maunsell's role in the original system. This isn't nostalgia; it's proof of capability spanning generations.

Government Contracting Excellence

AECOM's relationship with government isn't transactional—it's symbiotic. The company doesn't just bid on government contracts; it helps shape the programs that generate them. AECOM experts sit on advisory committees, contribute to policy papers, and provide technical expertise that informs legislation. When the Infrastructure Investment and Jobs Act was being drafted, AECOM's input helped define fundable project categories.

The company maintains a sophisticated government relations apparatus that goes beyond traditional lobbying. AECOM's Government Relations University trains project managers in the intricacies of federal acquisition regulations, state procurement processes, and local government dynamics. Every major office has specialists who understand not just the technical requirements but the political context of government work.

The approach to government contracting emphasizes long-term relationships over individual wins. AECOM will often accept lower-margin initial contracts to establish presence, knowing that incumbent advantages and relationship depth drive higher-margin follow-on work. The company's federal IDIQ (Indefinite Delivery/Indefinite Quantity) contracts provide a portfolio of potential projects worth billions, offering revenue visibility that pure commercial firms lack.

Global Scale with Local Execution

AECOM's operational philosophy sounds paradoxical: be everywhere but feel local. The company achieves this through a hub-and-spoke model that combines global centers of excellence with deep local presence. A transportation project in Denver might be led by local engineers who understand Colorado's specific requirements, supported by bridge specialists from San Francisco, seismic experts from Tokyo, and traffic modelers from London.

The company's Global Excellence Networks (GENs) connect specialists across geographies and time zones. The Water GEN includes 3,000 professionals who share knowledge, collaborate on proposals, and deploy rapidly to emerging opportunities. When Chennai faced a water crisis, AECOM assembled a team drawing on drought expertise from California, desalination experience from the Middle East, and water recycling knowledge from Singapore—all coordinated through the GEN structure.

This model provides competitive advantages beyond technical capability. AECOM can pursue projects that would overwhelm local firms while maintaining the community relationships and cultural understanding that global competitors often lack. It's not unusual for AECOM to have former city engineers, state transportation officials, and federal agency leaders on staff—people who understand not just how infrastructure works, but how decisions get made.

Margin Expansion Through Portfolio Optimization

The transformation from builder to advisor wasn't just strategic repositioning—it was margin arbitrage on a massive scale. Construction carries margins of 2-5%; design services achieve 10-15%; program management commands 15-20%; strategic advisory can exceed 25%. By systematically shifting its portfolio toward higher-margin services, AECOM has nearly doubled its profitability without doubling revenue.

The portfolio optimization follows clear principles. First, divest commodity services where differentiation is impossible. Second, retain specialized construction only where it enhances design credibility. Third, invest in advisory capabilities that leverage existing technical expertise. Fourth, develop recurring revenue streams through long-term program management contracts. Fifth, create intellectual property that can be licensed or productized.

The margin expansion strategy extends to project selection. AECOM has become increasingly selective, pursuing fewer but larger, more complex projects where its integrated capabilities provide clear differentiation. The company's "Win What Matters" initiative focuses business development on opportunities that not only generate revenue but enhance reputation, develop capabilities, and create follow-on opportunities.

The Asset-Light Revolution

AECOM's shift to an asset-light model represents one of the most successful business model transformations in industrial history. The company systematically eliminated capital-intensive operations while retaining high-value services. This wasn't just selling equipment and real estate—it was fundamentally reimagining how infrastructure services are delivered.

The transformation required rethinking every aspect of operations. Instead of owning construction equipment, AECOM manages equipment providers. Instead of maintaining fabrication facilities, it coordinates manufacturing networks. Instead of employing thousands of craft workers, it oversees specialized subcontractors. The company became an orchestrator rather than an operator, a brain rather than brawn.

The financial impact has been dramatic. Return on invested capital has more than doubled. Free cash flow conversion has improved from 60% to over 100% of net income. The balance sheet has strengthened, with net leverage dropping below 1x. Most importantly, the business has become more resilient—less sensitive to economic cycles, less dependent on capital markets, more adaptable to changing conditions.

Capital Allocation Discipline

AECOM's capital allocation framework prioritizes returns over growth, quality over quantity, sustainability over quick wins. The hierarchy is clear: first, invest in organic growth through hiring, training, and technology; second, return capital to shareholders through buybacks and dividends; third, pursue acquisitions only when they're strategically compelling and financially attractive.

The buyback program has been particularly successful. By repurchasing shares when the stock was undervalued, AECOM has created significant value for remaining shareholders. The company times buybacks countercyclically, accelerating purchases during market weaknesses and moderating during strength. This isn't market timing—it's disciplined capital allocation based on intrinsic value calculations.

Dividend policy balances growth and income investor needs. The company has committed to double-digit annual dividend increases, funded by growing free cash flow rather than stretching the balance sheet. This sustainable approach has attracted a different investor base—long-term holders who appreciate predictable capital returns alongside business growth.

The integration of ESG considerations into capital allocation has become a differentiator. AECOM won't pursue projects that conflict with its sustainability commitments, even if they're financially attractive. This principled approach has actually enhanced returns by positioning the company for the global energy transition and avoiding stranded assets in declining industries.

IX. Analysis & Investment Case

The investment case for AECOM requires understanding not just what the company is today, but what it's becoming. This isn't a traditional infrastructure company anymore—it's a professional services firm that happens to focus on infrastructure. The distinction matters because it fundamentally changes the valuation framework, competitive dynamics, and growth potential.

Competitive Positioning: The Moat Widens

AECOM's competitive position against peers like Jacobs, Fluor, WSP, and Stantec has strengthened dramatically over the past five years. While competitors remain formidable in specific niches, none match AECOM's combination of scale, scope, and strategic positioning. Jacobs has exited government services to focus on commercial markets—precisely as AECOM doubles down on public sector relationships. Fluor remains construction-heavy while AECOM pivots to design and advisory. WSP and Stantec have grown through acquisition but lack AECOM's global reach and technical depth.

The competitive moat isn't just about size—it's about capabilities that take decades to build. AECOM's security clearances for sensitive government work can't be quickly replicated. Its relationships with infrastructure agencies span generations of personnel. Its technical expertise in complex domains like nuclear remediation, military base design, and mega-project management requires experienced professionals who are increasingly scarce.

Network effects have become increasingly important. As AECOM wins more large programs, it gains experience that makes it more likely to win the next one. As it works with more government agencies, it understands procurement processes that befuddle competitors. As it completes more complex projects, it builds the resume that risk-averse clients require. These advantages compound over time, making it increasingly difficult for competitors to catch up.

Record Margins: Sustainable or Peak?

The adjusted EBITDA margin was 16.7% in the fourth quarter and 16.0% for the full year, reflecting an increase of 140 basis points and 100 basis points, respectively. These aren't just record margins for AECOM—they're approaching best-in-class for the entire infrastructure sector. The question investors must answer: Is this sustainable or cyclical?

The bull case for margin sustainability rests on structural changes rather than cyclical factors. The shift to higher-value services is permanent—AECOM isn't going back to low-margin construction. The operational improvements from digital transformation are cumulative—AI-assisted design and project management will only get better. The pricing power from market leadership is growing—as one of the few firms capable of handling mega-projects, AECOM can be selective.

The bear case warns that margins have benefited from extraordinary factors that won't repeat. Government stimulus spending has created a seller's market that will normalize. Competition will eventually respond to AECOM's premium pricing. Labor costs will rise as the war for talent intensifies. Technology investments will require continued spending that could pressure margins.

The reality likely lies between these extremes. AECOM's 17% long-term margin target seems achievable given the business mix shift and operational improvements. But expecting margins to expand indefinitely ignores competitive dynamics and market cycles. A normalized 16-17% EBITDA margin would still represent best-in-class performance and support attractive returns.

Infrastructure Tailwinds: How Long, How Strong?

The infrastructure spending boom isn't a cycle—it's a secular shift driven by multiple converging factors. The $1.2 trillion Infrastructure Investment and Jobs Act is just the beginning. Climate change will require trillions in adaptation spending—seawalls, flood defenses, drought-resistant water systems. The energy transition demands new transmission networks, renewable generation, and grid modernization. Urbanization in emerging markets necessitates entirely new infrastructure systems.

AECOM is positioned to benefit regardless of which infrastructure themes dominate. If climate adaptation accelerates, the company's water and environmental expertise becomes critical. If transportation modernization takes priority, AECOM's position as the #1 transportation designer captures value. If energy transition dominates, the company's power and industrial capabilities are essential. This isn't a bet on one trend but a portfolio positioned for multiple scenarios.

The duration of infrastructure spending is often underestimated. The IIJA funds projects through 2026, but the planning, design, and construction timeline extends well beyond. Major infrastructure projects take 10-20 years from conception to completion. AECOM's role in early-stage planning and design provides visibility into projects that won't generate construction revenue for years. This long-cycle dynamic provides more stability than markets often recognize.

The Backlog Story: Visibility or Illusion?

Our record backlog and pipeline, including a 1.2x book-to-burn in the design business in the fourth quarter, gives us confidence in delivering on our 2025 guidance. A backlog approaching $55 billion sounds impressive, but backlog quality matters more than quantity. Not all backlog converts to revenue at the same rate, and government contracts can be modified, delayed, or canceled.

AECOM's backlog quality has improved significantly. The shift toward design and program management means backlog converts to revenue more predictably than construction backlog. Multi-year program management contracts provide recurring revenue that's almost subscription-like. Framework agreements with government agencies create option value—the right but not obligation to perform work as needs arise.

The geographic and sector diversification of backlog reduces concentration risk. No single project represents more than 2% of backlog. Government and commercial work is balanced. Developed and emerging market exposure is mixed. This diversification means that project delays or cancellations have limited impact on overall performance.

Key Risks: What Could Go Wrong?

Government spending dependency remains AECOM's primary risk. Despite diversification efforts, over 50% of revenue derives from government and quasi-government entities. A significant reduction in infrastructure spending, whether from fiscal constraints, political changes, or economic recession, would impact AECOM disproportionately. The company's operating leverage means revenue declines flow through to earnings at a multiple.

Execution risk on mega-projects can't be ignored. While AECOM has exited construction, it still manages complex programs where problems can cascade. A major project failure could damage reputation, trigger liability claims, and make clients hesitant to award future work. The company's professional liability insurance provides some protection, but reputational damage can persist.

Competition is intensifying as the infrastructure market attracts new entrants. Technology companies are entering infrastructure services through smart city initiatives. Management consultancies are building infrastructure practices. Private equity is rolling up regional engineering firms. While AECOM's scale and expertise provide protection, pricing pressure and talent competition are real threats.

Bull Case: The Infrastructure Super-Cycle

The bull case for AECOM rests on three pillars: secular growth, margin expansion, and capital allocation. The infrastructure super-cycle isn't just about government stimulus—it's about replacing century-old systems, adapting to climate change, and building for demographic shifts. AECOM's unique position to capture this spending creates a multi-decade growth runway.

Margin expansion has room to run. The shift to advisory services is still early—less than 20% of revenue comes from these highest-margin activities. Digital transformation is accelerating—AI and automation will drive productivity gains. Pricing power is increasing—as one of few firms capable of handling complexity, AECOM can command premiums.

Capital allocation will drive shareholder returns even if operations merely meet expectations. With $700+ million in annual free cash flow and a $1 billion buyback authorization, AECOM can retire 10% of shares annually at current prices. Combined with dividend growth and modest organic expansion, this creates a path to 15-20% annual returns without heroic assumptions.

Bear Case: Cyclical Reversion

The bear case sees AECOM as a cyclical company at peak earnings. Infrastructure spending is elevated by historical standards and will normalize. Government deficits will constrain future spending. Interest rates will make infrastructure projects less economical. The current boom is pulling forward demand that will create a future air pocket.

Margin expansion has gone too far, too fast. AECOM's margins have doubled from historical levels—reversion to the mean would crush earnings. Competition will respond to premium pricing. Talent costs will escalate as employees demand their share of profits. Technology investments will disappoint as infrastructure remains stubbornly physical.

Valuation already reflects perfection. At current multiples, AECOM is priced like a high-quality industrial, not a cyclical construction services firm. Any disappointment in growth, margins, or capital allocation will trigger multiple compression. The stock's outperformance has created unrealistic expectations that the company can't meet.

The Verdict: Quality at a Reasonable Price

AECOM represents a rare combination: a high-quality business in a structurally growing market trading at a reasonable valuation. This isn't a hyper-growth technology stock or a deep-value cigar butt—it's a competitively advantaged business generating predictable cash flows with multiple levers for value creation.

The transformation from construction conglomerate to professional services firm is real and sustainable. The infrastructure spending backdrop provides tailwinds, but AECOM would prosper even in a normal environment given its competitive position. Management has demonstrated operational excellence and capital allocation discipline. The risks are real but manageable and well-understood by a leadership team that has navigated multiple cycles.

X. Epilogue & Reflections

Standing in AECOM's Dallas headquarters, you can see the Dallas North Tollway stretching toward the horizon—a piece of infrastructure that predecessor firm HNTB helped design decades ago. It's a fitting metaphor for AECOM itself: built on foundations laid by others, constantly expanding, connecting previously isolated areas, and enabling economic activity that wouldn't exist without it. The view from the top floor isn't just of a city; it's of a company that has helped build the modern world.

The transformation from conglomerate castoff to industry leader reads like a business school case study, but it's more than that. It's a story about seeing value where others saw remnants, about building through patience rather than financial engineering, about the power of compound advantages in an industry that rewards experience. When Richard Newman led that employee buyout in 1990, he wasn't just creating a company—he was preserving and combining a century of infrastructure expertise that might otherwise have been scattered to the winds.

Lessons in Timing

AECOM's history is a masterclass in contrarian timing. The company was born during a recession, went public just before a financial crisis, made its largest acquisition while competitors were retrenching, and transformed its business model when everyone else was chasing revenue growth. This wasn't luck—it was discipline combined with a long-term perspective that looked beyond quarterly earnings to decade-long trends.

The lesson extends beyond corporate strategy to investment philosophy. The best opportunities often come when sentiment is worst. AECOM's stock traded below $20 in March 2020; it's now above $100. The company bought back shares aggressively when everyone was hoarding cash. It invested in capabilities when others were cutting costs. This countercyclical courage, backed by operational excellence, created extraordinary value.

The Power of Strategic Pivots

Most companies tinker at the margins; AECOM transformed its entire business model—twice. The first pivot from regional engineering firm to global infrastructure conglomerate through serial acquisition. The second from asset-heavy builder to asset-light advisor through portfolio optimization. Each transformation required not just strategic vision but operational execution and cultural change.

The pivots worked because they were grounded in capability rather than financial engineering. AECOM didn't just divest construction assets; it retained and enhanced the technical expertise that made those assets valuable. It didn't just acquire companies; it preserved and integrated their unique capabilities. This focus on building and preserving competitive advantages, rather than just reshuffling assets, created lasting value.

Building Through Cycles

Infrastructure is inherently cyclical, but AECOM has managed to grow through every cycle since 1990. The secret isn't avoiding cycles—it's being positioned to benefit from them. During downturns, AECOM acquires capabilities at attractive prices. During upturns, it invests in organic growth and returns capital to shareholders. This through-cycle mentality requires financial discipline, operational flexibility, and most importantly, patience.

The company's resilience comes from diversification across geographies, sectors, and services. When commercial construction collapsed in 2008, government stimulus spending accelerated. When developed markets slowed, emerging markets grew. When construction margins compressed, design margins expanded. This portfolio approach doesn't eliminate volatility, but it dampens it enough to enable long-term planning and investment.

What AECOM Tells Us About American Infrastructure

AECOM's evolution mirrors the changing nature of American infrastructure itself. The era of simply building more highways and bridges has given way to complex challenges: making existing infrastructure resilient to climate change, integrating digital technology into physical systems, balancing economic development with environmental protection. AECOM's transformation from builder to advisor reflects infrastructure's transformation from hardware to software, from construction to optimization.

The company's success also highlights the unique American approach to infrastructure: a complex dance between public needs and private capabilities. Unlike countries with state-owned engineering firms or purely private infrastructure developers, America relies on companies like AECOM that exist at the intersection, translating public policy into physical reality while maintaining private sector efficiency and innovation.

The Human Element

Behind every acquisition, every project, every strategic pivot are people making decisions under uncertainty. Richard Newman betting his career on a management buyout. Michael Burke choosing to acquire rather than retrench during the financial crisis. Troy Rudd investing in advisory capabilities while others chase construction volume. These weren't inevitable decisions—they were choices made by individuals who saw opportunity where others saw risk.

The 51,000 employees of AECOM aren't just workers—they're inheritors and stewards of engineering traditions stretching back over a century. When a young engineer in Singapore designs a water treatment plant, she's building on knowledge accumulated by Metcalf & Eddy in Boston a century ago. When a project manager in London coordinates a transportation program, he's applying lessons learned by Maunsell in Hong Kong decades earlier. This accumulated wisdom, passed down and enhanced through generations, is AECOM's true competitive advantage.

Future Opportunities: The Next Transformation

AECOM's future opportunities read like science fiction becoming reality. Digital twins that create virtual replicas of physical infrastructure, enabling predictive maintenance and optimization. Artificial intelligence that can design infrastructure solutions faster and better than human engineers. Climate adaptation projects that will dwarf anything built before—sea walls protecting entire coastlines, water systems serving mega-cities, transportation networks resilient to extreme weather.

The company is already positioning for these opportunities. Its investment in digital capabilities isn't just about efficiency—it's about reimagining what infrastructure services can be. Its focus on sustainability isn't just about ESG scores—it's about being essential to the energy transition. Its expansion into advisory services isn't just about margins—it's about influencing how trillions in infrastructure spending gets deployed.

The Deeper Questions

AECOM's story raises profound questions about the nature of corporate success. Is it better to be excellent at one thing or competent at everything? AECOM chose breadth and made it work through integration and scale. Should companies own assets or orchestrate them? AECOM proved that asset-light can work even in asset-heavy industries. Can serial acquisition create lasting value? AECOM shows it can, with the right integration philosophy and operational discipline.

The company also embodies tensions that define modern capitalism. It profits from government spending while enabling public services. It promotes sustainability while working on carbon-intensive projects. It celebrates local expertise while operating globally. These aren't contradictions to be resolved but tensions to be managed, and AECOM's success comes partly from navigating them skillfully.

The Ultimate Lesson

If there's one lesson from AECOM's journey, it's that transformation is possible but not easy. It requires vision to see what others miss, courage to act when others hesitate, discipline to execute when others give up, and patience to build when others demand immediate results. AECOM didn't become the world's infrastructure leader overnight—it took 34 years of acquisitions, integrations, pivots, and innovations.

For investors, AECOM offers a compelling opportunity: a high-quality business with competitive advantages, structural growth tailwinds, improving margins, and shareholder-friendly capital allocation. But more than that, it offers participation in the fundamental task of building and maintaining civilization's infrastructure. Every bridge, tunnel, water system, and power grid that AECOM designs or manages becomes part of the physical foundation on which society operates.

As we face challenges from climate change to urbanization to aging infrastructure, companies like AECOM become not just good investments but essential institutions. They possess the expertise, scale, and relationships necessary to translate policy into projects, plans into reality, ideas into infrastructure. In a world that increasingly recognizes infrastructure as destiny, AECOM has positioned itself as indispensable.

The view from AECOM's headquarters encompasses more than Dallas—it captures a company that has evolved from an orphaned division of an oil refiner into the architect of the modern world. The transformation isn't complete; in many ways, it's just beginning. As infrastructure becomes increasingly complex, digital, and critical to addressing global challenges, AECOM's combination of technical expertise, global scale, and strategic positioning becomes more valuable. The company that helped build the last century's infrastructure is well-positioned to design the next century's.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube