ACI Worldwide: The Invisible Giant Powering Global Payments

I. Introduction & Episode Roadmap

Somewhere right now, a person is tapping their phone to pay for coffee. A treasurer at a Fortune 500 company is wiring $40 million across borders. A grandmother is paying her electric bill online. A fraudster in Eastern Europe is attempting to use a stolen credit card at a British retailer. And every single one of these transactions, in one way or another, is flowing through software built by a company most people have never heard of, headquartered in a place most people would never guess: Omaha, Nebraska.

ACI Worldwide processes over 90 billion transactions per year. Its software touches $14 trillion in payments and securities daily. It serves all ten of the world's largest financial institutions by asset value, and six of the top ten global merchants. Nearly half of all electronic transactions on the planet run through ACI's flagship product. And yet, if you stopped a hundred people on the street and asked them what ACI Worldwide does, you would get a hundred blank stares.

This is the story of how a tiny software shop founded in 1975 by a handful of programmers in Nebraska built the invisible plumbing of global payments. It is a story about timing mega-trends before they become obvious, about the extraordinary power of switching costs, and about what happens when your product is so deeply embedded in the world's financial infrastructure that replacing it would be, for many institutions, unthinkable.

The thesis is simple: ACI Worldwide is one of the most strategically important companies in financial technology, and almost nobody outside the payments industry knows it exists. Over the next several sections, we will trace ACI's journey from its humble origins automating bank transactions on fault-tolerant computers, through its transformation into the backbone of real-time payments in over 40 countries, to its current reinvention as a cloud-native platform provider in an era when fintech disruptors threaten to unbundle everything. Along the way, we will examine the strategic decisions that built durable competitive moats, the acquisitions that reshaped the company's trajectory, and the fundamental question that defines ACI's future: can a 50-year-old payments infrastructure company not only survive the fintech revolution but lead it?

The answer, as it turns out, is far more interesting than the question suggests.

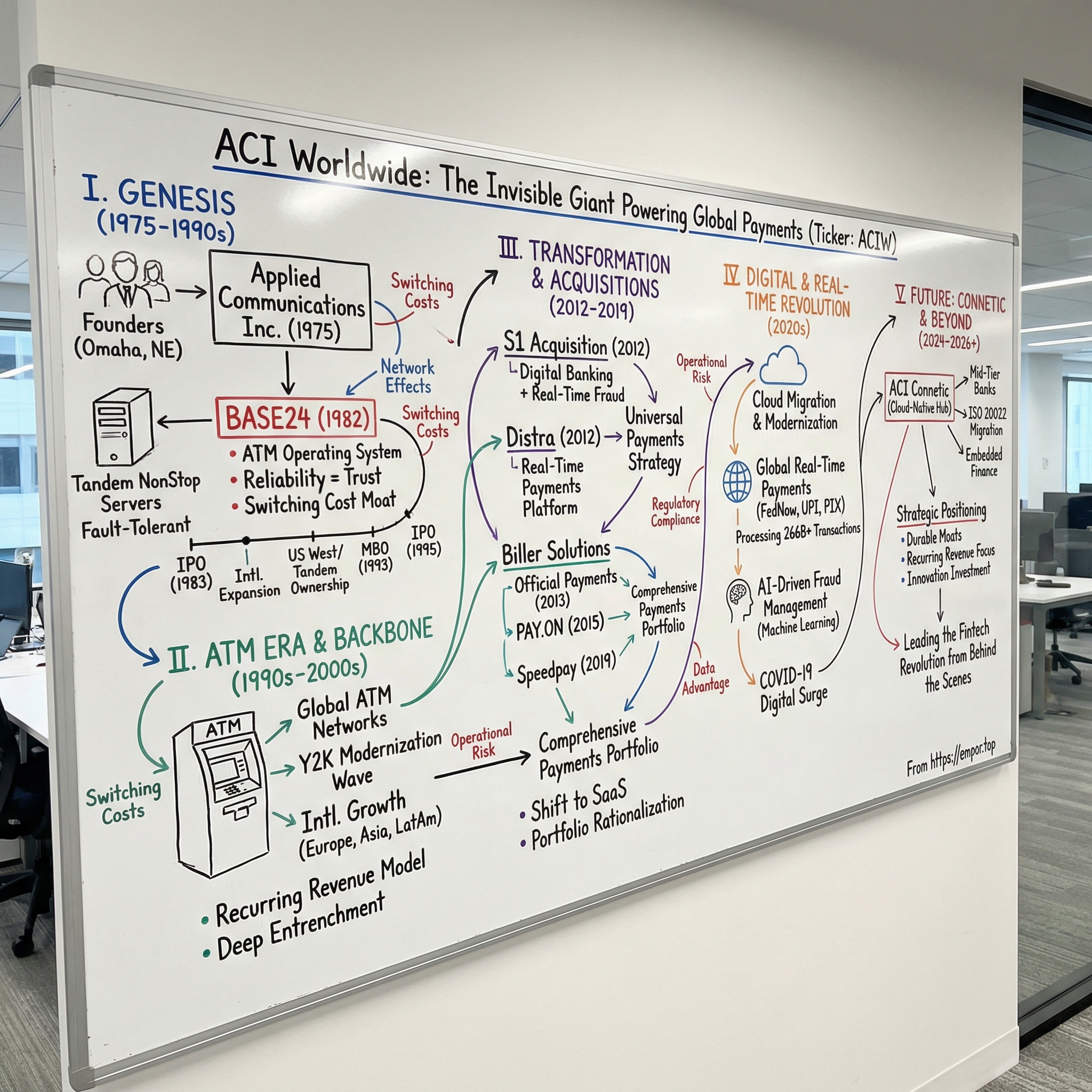

II. The Genesis: Applied Communications and the Dawn of Electronic Payments (1975–1990s)

On September 1, 1975, three men in Omaha, Nebraska incorporated a company called Applied Communications Inc. James Cody, a computer programmer, along with co-founders Dave Willadsen and Dennis Gates, had spotted something that most of the technology world had not yet noticed. Tandem Computers had just introduced the NonStop line of fault-tolerant servers, machines designed to run continuously without ever going down. The founders' insight was deceptively simple: banks needed systems that never failed. If you could write software for these indestructible machines that automated the messy, error-prone process of electronic funds transfer, you could build something very valuable.

To understand why this mattered, you have to understand what banking looked like in the mid-1970s. The ATM was still a novelty. Most bank transactions were processed in batches overnight. Reconciliation was largely manual. Fraud detection consisted of a clerk noticing something odd. The idea that a consumer could insert a plastic card into a machine on a street corner and receive cash from their account in real time was revolutionary, and it required software that absolutely could not crash.

Applied Communications built that software. Working on Tandem's NonStop platform, they developed systems to handle ATM networks, electronic funds transfer, and the emerging world of card-based transactions. The work was deeply technical, unglamorous, and utterly essential. By the early 1980s, the company had established itself as a specialist in the narrow but critical niche of payment switching software, the layer of technology that sits between a card reader and a bank's core systems and makes the transaction actually happen.

In 1982, the company launched the product that would define its next four decades: BASE24. The name was coined by a salesman and stood for "Baseline Software for 24-hour-per-day system operations." BASE24 was designed to be the operating system for ATM networks, a single software platform that could handle card authorization, routing, and settlement around the clock. It was reliable, it was fast, and it scaled. Banks adopted it because the alternative was building their own transaction switching systems from scratch, a project that would consume years of development time and carry enormous operational risk.

What made BASE24 remarkable was not any single technological breakthrough but rather the compound effect of reliability over time. Every hour that BASE24 ran without failing was another data point that convinced the next bank to adopt it. Every new customer added to the network of institutions that had validated the technology. Payment processing is an industry where the cost of failure is measured not in lost productivity but in frozen bank accounts, stranded consumers, and regulatory investigations. In that environment, a proven track record is worth more than any feature set.

The company grew rapidly through the 1980s. In 1983, Applied Communications went public for the first time. By 1987, it had earned the President's "E" Award for export excellence, a signal of how aggressively the company was expanding internationally. By 1989, ACI was operating in 29 countries, with international sales exceeding 50 percent of revenue. The workforce had expanded more than sixfold between 1982 and 1989.

But ACI's corporate journey through this period was anything but straightforward. In 1986, US West acquired Applied Communications. The telco giant saw value in the payments software business but proved to be an awkward corporate parent. Five years later, in 1991, Tandem Computers purchased the company from US West for slightly less than $60 million, essentially rescuing a key software partner. As a Tandem official said at the time: "We didn't see Applied Communications flourishing under US West ownership, so we decided to acquire them to protect our joint customer base."

Then, in 1993, came the move that would set the stage for ACI's modern era. Tandem sold Applied Communications to a management-led group for $80 million, reorganizing the company as Transaction Systems Architects, Inc. under the leadership of William E. Fisher. The management buyout liberated the company from corporate ownership and gave its leaders the freedom to chart their own course. The company marketed its products under the "ACI Worldwide" brand and, in January 1995, returned to the public markets with an IPO of 2.75 million shares at $15 per share on NASDAQ.

By this point, BASE24 had become something close to an industry standard. The product processed card authorization for major banks on every continent. Its installed base created a self-reinforcing cycle: the more banks that used BASE24, the more proven it became, the more new banks adopted it, and the harder it became for anyone to displace. This was not a network effect in the Facebook sense, but it was something equally powerful: an ecosystem effect, where the sheer weight of adoption and institutional validation created a gravitational pull that competitors could not overcome.

The strategic lesson from ACI's first two decades is worth pausing on. The founders did not set out to build a monopoly. They set out to solve a specific technical problem, reliable software for banks, on a specific hardware platform. But the nature of payment processing created dynamics that rewarded incumbency in ways that few other software markets do. When the cost of switching is measured not in dollars but in operational risk to a nation's payment infrastructure, customers do not switch. They stay. And they stay for decades.

III. The ATM Era: Building the Backbone (1990s–Early 2000s)

By the mid-1990s, the ATM had gone from novelty to necessity. There were over 100,000 ATMs in the United States alone, and the number was climbing rapidly worldwide. Behind nearly half of them, in some form, sat ACI's BASE24 software. The company had become the invisible backbone of a daily ritual that billions of people took entirely for granted: walking up to a machine, inserting a card, and receiving cash.

The Y2K scare of the late 1990s proved to be an unexpected windfall. Banks, terrified that their legacy systems would collapse when the calendar rolled over to January 1, 2000, embarked on massive modernization programs. ACI, as a trusted infrastructure provider, was perfectly positioned to capture this spending wave. Banks that might have deferred system upgrades for years were suddenly racing to replace aging transaction processing software, and ACI had the proven, Y2K-compliant product to sell them. The Y2K scare taught the payments industry an uncomfortable lesson about the fragility of its infrastructure, and the companies that had already invested in modern, reliable systems reaped the rewards.

International expansion accelerated through this period. ACI pushed aggressively into Europe, Asia-Pacific, and Latin America, establishing local offices, building partnerships with regional banks, and adapting its products to the regulatory and technical requirements of each market. The payments landscape varied enormously by geography. European banks operated under different clearing and settlement systems than their American counterparts. Asian markets were leapfrogging directly from cash to electronic payments. Latin American banks faced unique challenges around currency volatility and regulatory complexity. ACI's ability to serve all of these markets with a single core platform, adapted to local requirements, was a significant competitive advantage.

The business model that emerged during this era was beautifully sticky. ACI sold software licenses to banks, but the real value was in the ongoing relationship. Once a bank implemented BASE24, it paid annual maintenance fees for software updates and support. Transaction processing fees generated recurring revenue that grew with the bank's transaction volume. And the switching costs were enormous: a bank that wanted to replace BASE24 would face an implementation timeline of 18 to 36 months, massive operational risk during the transition, and the need to retrain staff on entirely new systems. In an industry where the consequences of a failed payment system are severe, the rational decision was almost always to stay with the incumbent.

Competition did emerge during this period. Fiserv, FIS, and Jack Henry & Associates all built significant positions in bank technology. But the competitive dynamics were more about market segmentation than head-to-head warfare. Fiserv became dominant in serving smaller community banks. FIS focused on large-bank core processing. Jack Henry carved out a niche with small and mid-sized institutions. ACI occupied a different layer of the stack entirely, the payment switching and transaction processing layer that sat on top of core banking systems. This meant ACI often coexisted alongside its nominal competitors rather than displacing them.

The Nebraska headquarters, which might seem like a disadvantage for a global technology company, was actually a strategic asset. Omaha offered a dramatically lower cost structure than Silicon Valley or New York. The city's deep bench of financial services talent, anchored by companies like Mutual of Omaha and First Data, provided a steady pipeline of engineers and product managers who understood payments at a fundamental level. And the Midwestern culture, understated, methodical, focused on reliability rather than flash, aligned perfectly with the values that bank CIOs prized when selecting infrastructure vendors.

By the early 2000s, ACI had established a position that would prove remarkably durable. It was not the largest financial technology company, nor the most glamorous. But it had something more valuable: deep entrenchment in the most critical layer of global payment infrastructure. The question was whether that position could survive the tectonic shifts that were about to reshape the payments industry.

IV. The S1 Acquisition: Betting on Digital Payments (2012)

For a decade after its 1995 IPO, ACI grew steadily but faced an existential strategic question. BASE24 was a proven cash cow, but the payments world was changing rapidly. The internet was transforming how consumers interacted with their banks. Online banking, bill pay, and e-commerce were creating entirely new payment flows that traditional ATM switching software was not designed to handle. ACI needed to evolve from a transaction processing company into a broader payments infrastructure platform, or risk becoming a relic of the ATM era.

The answer came in February 2012, when ACI completed its acquisition of S1 Corporation for approximately $515 to $540 million in a combination of cash and stock. This was the largest deal in ACI's history at the time, and it represented a fundamental bet on the future of digital payments.

S1 Corporation brought ACI a portfolio of capabilities that extended far beyond ATM switching. S1 had built significant products in digital banking, online and mobile banking platforms, card management systems, and, critically, real-time fraud detection. The acquisition gave ACI a presence in the digital banking layer, the systems that consumers actually interacted with when they logged into their bank's website or mobile app. It also brought advanced fraud management capabilities that could analyze transactions in real time and flag suspicious activity before a fraudulent payment was completed.

Why did this matter? Because the internet era had fundamentally changed the fraud landscape. In the ATM world, fraud required physical access: a stolen card, a cloned magnetic stripe, a shoulder-surfer watching a PIN entry. In the digital world, fraud could happen from anywhere on the planet, at any time, at massive scale. Banks needed fraud detection systems that could analyze thousands of transactions per second, apply machine learning models to identify suspicious patterns, and make approve-or-decline decisions in milliseconds. S1's fraud capabilities gave ACI a foothold in this critical and rapidly growing market.

The integration was not without challenges. Combining two large software companies with overlapping products, different engineering cultures, and thousands of bank customers requires painstaking work. Customer migrations had to be managed carefully to avoid disrupting live payment systems. Product lines had to be rationalized, with some legacy systems sunset and others consolidated. And the cultural merger, bringing together ACI's infrastructure engineering DNA with S1's digital banking orientation, took years to fully resolve.

But the strategic logic was sound. The S1 acquisition transformed ACI from a company that primarily processed card transactions into a company that could offer banks a much broader suite of payment capabilities: card switching, fraud detection, digital banking, and bill payment. This expansion of scope was essential for ACI's land-and-expand strategy: once a bank was running ACI software for one function, the company could cross-sell additional modules, increasing revenue per customer and deepening the switching costs that were already formidable.

The same year, ACI made another acquisition that would prove prescient. The company acquired Distra Pty Ltd, an Australian company, for $49.8 million. Distra brought a real-time Universal Payments Platform that would become the foundation for ACI's next-generation architecture. At a time when the phrase "real-time payments" was barely in the lexicon of most American bankers, ACI was quietly assembling the technology it would need to lead the real-time revolution.

Looking back, the 2012 acquisitions mark the moment when ACI began its transformation from a legacy transaction processor into a modern payments platform company. The timing was not accidental. Phil Heasley, who had become CEO in 2005, had spent decades in the payments industry, including 13 years at Citicorp and a stint as chairman of Visa USA. He understood, from his vantage point inside the largest payment networks in the world, that the future belonged to companies that could process any payment type, across any channel, in real time. The S1 and Distra acquisitions were the first major moves in a multi-year strategy to build exactly that capability.

The challenge, as always with transformational acquisitions, was execution. ACI had just roughly doubled its revenue base and dramatically expanded its product portfolio. The question was whether the company could integrate these assets, rationalize the product lines, and emerge as a coherent platform provider, all while keeping mission-critical payment systems running for thousands of banks around the world.

V. The Transformation Years (2005–2013)

Phil Heasley arrived as CEO of Transaction Systems Architects (the corporate parent of ACI Worldwide) in 2005, and his biography read like a roadmap of the payments industry itself. A 45-year veteran of financial services, Heasley had spent 13 years at Citicorp, including three years running Diners Club. He had served as chairman and CEO of First USA Bank, the credit card subsidiary of Bank One. He had chaired the board of Visa USA from 1996 to 2003 and sat on the board of Visa International. He had even served on the National Infrastructure Advisory Council. If anyone understood the strategic trajectory of global payments, it was Heasley.

What Heasley found when he arrived was a company with extraordinary technology and market position but a business model that needed fundamental restructuring. ACI was still heavily dependent on perpetual software licenses, the traditional model where banks paid a large upfront fee and then annual maintenance charges. This model generated lumpy, unpredictable revenue and left ACI vulnerable to the budget cycles of its bank customers. When banks froze IT spending, as they did during the financial crisis, ACI's revenue suffered.

The financial crisis of 2008 hit ACI hard, as it hit the entire bank technology ecosystem. Banks slashed discretionary spending. New system implementations were delayed or cancelled. ACI's stock fell sharply, and activist investors began circling, questioning whether the company's management was maximizing shareholder value.

Heasley's response was a multi-year transformation that would prove to be one of the most important strategic pivots in ACI's history. He began shifting the company from perpetual licenses to a recurring revenue model built on SaaS subscriptions and transaction processing fees. This transition was painful in the short term: perpetual licenses generated large upfront revenue, while SaaS subscriptions produced smaller amounts spread over longer periods. Wall Street, with its obsession with quarterly results, punished ACI for the transition. But Heasley understood that recurring revenue was more predictable, more valuable over time, and better aligned with how banks actually wanted to consume technology.

Simultaneously, Heasley drove cost restructuring and portfolio rationalization. ACI had accumulated a sprawling product portfolio over decades, and some products were overlapping, redundant, or nearing end of life. Heasley's team systematically evaluated each product line, investing in the platforms with the highest strategic potential and sunsetting those that were draining resources.

In 2007, the company took a symbolic step that reflected its evolving identity: Transaction Systems Architects formally changed its corporate name to ACI Worldwide, Inc., the brand name under which it had been marketing products since 1993. The new name signaled that ACI was no longer just a provider of transaction processing architectures. It was a worldwide payments platform company.

The transformation years also saw ACI begin to build what would become its real-time payments capability. In 2011, ACI signed early deals to support the UK's Faster Payments system, one of the world's first real-time payment networks. This was years before most American bankers had even heard the term "real-time payments." ACI was betting that the global payments industry would eventually move from batch processing, where transactions were settled overnight, to instant settlement, where money moved in seconds, 24 hours a day, 365 days a year. It was a bet that would take a decade to fully pay off, but when it did, the returns would be transformational.

By 2013, the combination of the S1 acquisition, organic product development, and the Faster Payments wins had positioned ACI at the intersection of several converging trends: the digitization of banking, the shift to real-time payments, and the escalating arms race in fraud detection. Revenue had grown from $313 million in 2005 to $865 million in 2013. The company was no longer just an ATM switching vendor. It was becoming the plumbing of global electronic payments.

But the transformation was far from complete. The next phase would require even bigger bets, and the competitive landscape was about to get much more crowded.

VI. The Real-Time Payments Platform and Fraud Management Pivot (2011–2016)

To understand why real-time payments matter, consider what happens when you wire money to someone at a different bank today. In many countries, you initiate the transfer during business hours, and the money arrives sometime later, perhaps the next day, perhaps several days later. The payment passes through a series of intermediary systems, each operating on its own schedule, each adding delay and cost. The receiving bank does not credit the funds until it has verified the transfer through a batch settlement process that typically runs overnight.

Now imagine the alternative: you send money and it arrives in the recipient's account in seconds. Not minutes. Not hours. Seconds. Available immediately to spend. Twenty-four hours a day, seven days a week, including holidays. That is real-time payments, and over the past 15 years, it has gone from a theoretical concept to a global movement that is fundamentally reshaping how money moves.

The United Kingdom led the way with its Faster Payments Service, launched in 2008. India followed with UPI, which now processes over 10 billion transactions per month. Brazil launched PIX, which exploded to hundreds of millions of users within its first year. Singapore, Australia, Malaysia, Thailand, and dozens of other countries built their own real-time payment networks. And in the United States, the Federal Reserve launched FedNow in 2023, finally bringing real-time payments to the world's largest economy.

ACI positioned itself at the center of this revolution. Building on the Distra acquisition and its own internal development, ACI created what it called the Universal Payments platform, a real-time payments infrastructure that could support any payment type, across any channel, in any currency. The platform was designed from the ground up for the demands of instant settlement: event-driven architecture that could process transactions in milliseconds, extreme reliability requirements of 99.999 percent uptime, and the flexibility to support the unique technical specifications of dozens of different national real-time payment schemes.

The early wins were critical. ACI's work with UK Faster Payments, which ultimately saw ACI processing roughly half of all UK Faster Payments transactions, validated the platform's capabilities and created a powerful reference customer for other markets. Singapore, Thailand, and Malaysia followed. By the mid-2010s, ACI was supporting real-time payment networks across multiple continents, building a portfolio of implementations that no competitor could match.

In 2014, ACI made another acquisition that deepened its position in the emerging fraud management arms race. The company acquired Retail Decisions, known as ReD, for $205 million. ReD was a SaaS-based e-commerce fraud detection platform serving over 1,500 retailers, issuers, acquirers, and processors globally. The acquisition was driven by a simple insight: real-time payments create real-time fraud. When money moves in seconds, fraudsters have seconds to exploit vulnerabilities before anyone can intervene. Banks and merchants needed fraud detection systems that could keep pace with the speed of payment, analyzing transactions and making approve-or-decline decisions in the same milliseconds that the payment itself took to process.

This fusion of real-time payments and real-time fraud detection would become one of ACI's most powerful strategic positions. The company was building both the rails on which money moved and the security systems that protected those rails. For a bank deploying a real-time payment system, the ability to get both capabilities from a single vendor, deeply integrated and proven at scale, was enormously attractive.

The competitive moat deepened during this period in ways that were not immediately visible from the outside. Each new real-time payment implementation added to ACI's institutional knowledge. The engineers who built the UK system brought that experience to the Singapore implementation, and the Singapore team brought their learnings to Malaysia. Over time, ACI accumulated a body of expertise in real-time payment deployment that was extraordinarily difficult for competitors to replicate. This was not intellectual property in the patent sense. It was process power, the accumulated knowledge of thousands of deployments, distilled into implementation methodologies, testing frameworks, and operational playbooks that no startup could reproduce overnight.

For investors watching during these years, the key question was whether ACI's real-time payments bet would pay off at scale. The technology was proven, the early wins were encouraging, but real-time payments adoption in the largest markets, particularly the United States, was still years away. ACI was investing heavily in a future that had not yet arrived. Whether that future would come fast enough to justify the investment remained an open question.

VII. The Bill Pay Wars & Strategic Acquisitions (2013–2019)

While ACI was building its real-time payments platform, the company was simultaneously expanding into a market that might seem mundane but was strategically vital: bill payment. Every month, hundreds of millions of Americans pay their utility bills, mortgage payments, insurance premiums, tax obligations, and DMV fees. The infrastructure that processes these payments is enormous, unglamorous, and surprisingly profitable.

In 2013, ACI acquired Official Payments Holdings for approximately $140 to $150 million. Official Payments was a specialist in electronic bill payment technology, serving over 3,000 customers and providing access to more than 100 million end users. The company processed approximately 20 million payments per year, representing over $9 billion in payment volume. The acquisition gave ACI a foothold in government and utility payments, a market characterized by stable, recurring transaction volumes and relatively low competitive intensity.

Two years later, in 2015, ACI made another strategic acquisition: PAY.ON AG, a European payment gateway provider, for approximately 180 million euros. PAY.ON operated a white-label hosted payment gateway that connected merchants to over 300 domestic and international acquirers and alternative payment methods. The acquisition gave ACI a European merchant acquiring footprint that complemented its traditional strength in bank-side infrastructure.

The logic behind these acquisitions was to build what ACI called a three-sided platform connecting banks, merchants, and billers. Traditional payment processors tended to focus on one side of this triangle: bank processing, merchant acquiring, or bill payment. ACI was attempting to build a platform that spanned all three, creating cross-selling opportunities and network effects that a single-sided competitor could not match.

But the crown jewel of ACI's bill payment strategy came in 2019, when the company acquired Speedpay from Western Union for $750 million in an all-cash deal. This was ACI's largest acquisition ever, and it was a bold statement of strategic intent. Speedpay was a comprehensive electronic bill presentment and payment platform that had generated over $350 million in revenue and $90 million in adjusted EBITDA in 2018. The platform served customers across consumer finance, insurance, healthcare, higher education, utilities, government, and mortgage, and it processed hundreds of millions of bill pay transactions annually.

The Speedpay acquisition transformed ACI's bill payment business from a nice-to-have into a strategic pillar. The platform's breadth of coverage across industries meant that ACI was now processing payments in virtually every corner of the economy where consumers interact with billers. And the business model was attractive: transaction fees generated predictable recurring revenue, customer relationships were long-term, and the switching costs were significant because billers had integrated Speedpay into their customer-facing payment portals, their back-office reconciliation systems, and their compliance workflows.

The competitive landscape in bill payment was intense. PayPal, Amazon Pay, and Apple Pay were all expanding into utility and government payments. Fiserv had its own bill payment capabilities through its CheckFree acquisition. But ACI's advantage was different from what the consumer-facing players offered. ACI provided the back-end infrastructure, the regulatory compliance, security, and bank-grade reliability that billers required. A utility company processing millions of monthly payments needed a platform that could handle peak loads without failure, that met PCI compliance requirements, and that integrated with dozens of different payment methods. This was enterprise infrastructure, not consumer experience, and it was the kind of work that ACI had been doing for decades.

By 2019, with Speedpay integrated and the bill payment platform scaling, ACI had assembled a comprehensive payments portfolio that few competitors could match. The company could process card transactions through BASE24, detect fraud through its machine learning platform, settle real-time payments across multiple national networks, and handle bill payments for thousands of billers. Revenue had reached $1.26 billion, and the company was processing over 40 billion transactions annually.

The question was whether this portfolio could withstand the next wave of disruption, one that was already crashing onto the shores of the payments industry.

VIII. The Digital Transformation Era: Modernization at Scale (2016–2020)

By 2016, the payments industry was in the midst of a tectonic shift that threatened to redraw the competitive landscape entirely. A new generation of fintech companies, Stripe, Square, Adyen, and dozens of others, were building payment platforms from scratch, using cloud-native architectures, developer-friendly APIs, and modern user experiences that made traditional payment infrastructure look like something from a different century. For decades, bank CIOs had chosen vendors based on reliability, compliance, and institutional trust. Now, a new generation of buyers was choosing based on speed of integration, developer documentation, and the ability to spin up payment capabilities in days rather than months.

ACI's response was what it called the "Universal Payments" strategy: any payment type, any channel, any currency. The vision was ambitious. Rather than operating separate product lines for card switching, fraud detection, real-time payments, and bill payment, ACI would consolidate everything into a unified platform that could handle the full spectrum of payment flows through a single architecture.

The execution required sunsetting over 40 legacy products and consolidating them into three core platforms. This was a wrenching process for a company that had accumulated technology through decades of organic development and acquisitions. Legacy products had loyal customer bases, dedicated engineering teams, and revenue streams that could not be turned off overnight. The consolidation required careful migration planning, customer communication, and the willingness to accept short-term revenue disruption for long-term strategic clarity.

Cloud migration added another layer of complexity. ACI's traditional customers ran its software on-premises, in their own data centers, managed by their own IT teams. The shift to SaaS meant moving these customers to cloud-hosted environments where ACI operated the software on their behalf. For banks, this was not a trivial decision. Payment processing systems are among the most regulated and security-sensitive applications in any bank's technology stack. Moving them to the cloud required extensive security assessments, regulatory approvals, and risk management reviews.

Then COVID-19 hit, and everything accelerated. The pandemic drove a massive surge in digital payments as consumers shifted from cash and in-person transactions to contactless payments and e-commerce. Banks that had been cautiously evaluating digital payment capabilities suddenly needed them urgently. The companies that had already invested in modern payment infrastructure, including ACI, found themselves in enormous demand.

ACI's 2020 revenue reached $1.29 billion, buoyed by the digital payments surge. The company was now processing over 40 billion transactions annually across its various platforms. But the pandemic also exposed a vulnerability that had been building for years: customer concentration risk. ACI's largest customers, the world's biggest banks, represented a significant portion of total revenue. Any loss of a major customer, or any delay in a major implementation, could have an outsized impact on the company's financial results.

The fintech threat was real but nuanced. Stripe and Adyen were not competing with ACI for the same customers. They were competing for a different layer of the payments stack: the merchant-facing experience, the developer tools, the ease of integration. ACI operated at the infrastructure layer, the payment switches, real-time rails, and fraud engines that sat beneath the merchant-facing experience. In many cases, fintech payment platforms actually relied on infrastructure like ACI's to process their transactions. But the risk was that over time, as fintech platforms grew more capable, they might vertically integrate into the infrastructure layer, displacing traditional vendors like ACI.

The strategic response required ACI to become more like a fintech without losing the reliability, compliance, and institutional trust that had made it the vendor of choice for the world's largest banks. It was a delicate balance, and one that would define the company's trajectory for years to come.

IX. The Biller Platform & Speedpay Evolution (2019–2026)

By 2020, Speedpay had become ACI's crown jewel in the biller direct payments market. The platform processed over 521 million bill pay transactions annually, serving more than 4,000 customers across virtually every sector of the economy that sends bills to consumers. When a homeowner paid their mortgage online, when a driver renewed their car registration at their state's DMV website, when a patient settled a hospital bill through a payment portal, there was a significant chance that ACI's Speedpay was processing that transaction behind the scenes.

The competitive dynamics in biller payments were different from those in bank infrastructure. In the bank world, ACI competed against other enterprise software vendors on the basis of reliability, scale, and compliance. In the biller world, ACI faced a different set of challengers: consumer payment platforms like PayPal, Apple Pay, and Amazon Pay, which were trying to become the default payment method for every type of bill. These platforms offered convenience to consumers but lacked the specialized back-end infrastructure that billers required.

ACI's advantage in the biller market came down to three things. First, regulatory compliance: utility companies, government agencies, and healthcare providers operated in heavily regulated environments where payment processing had to meet specific legal and security requirements. ACI had decades of experience navigating these requirements. Second, scale and reliability: a large utility company might process millions of payments per month, with sharp peaks around due dates. The platform had to handle these peaks without failure, because a payment system outage at a utility company is not just an inconvenience; it is a customer service crisis and a regulatory problem. Third, integration depth: Speedpay was not a standalone payment page. It was deeply integrated into billers' customer-facing portals, back-office reconciliation systems, and financial reporting workflows. Ripping it out and replacing it with an alternative would require rebuilding those integrations from scratch.

The network effects in the biller market, while not as dramatic as those in consumer social networks, were real. Every new biller that joined the Speedpay platform expanded the range of bills that consumers could pay through ACI-powered portals. Every additional consumer who registered a payment method on a Speedpay-powered site increased the platform's value to billers. Over time, this flywheel effect created a growing base of payment relationships that made the platform increasingly difficult to displace.

The revenue model evolved during this period from pure transaction fees to a hybrid of transaction fees and platform subscriptions. This shift reflected ACI's broader strategic transition toward recurring revenue. By bundling transaction processing with platform capabilities like analytics, customer communication tools, and multi-channel payment support, ACI could charge subscription fees that were more predictable than purely volume-based pricing.

By 2025, ACI's recurring revenue had reached $1.21 billion, representing approximately 69 percent of total revenue. Within that, SaaS and platform-as-a-service fees accounted for $1.01 billion, up 12 percent from $898 million the prior year. The bill payment platform, with its steady transaction volumes and deep customer relationships, was a major contributor to this recurring revenue base.

X. The Real-Time Revolution Goes Global (2019–2025)

In July 2023, the Federal Reserve launched FedNow, the United States' first real-time payment system. It was a watershed moment for the American payments industry, and for ACI, it represented the arrival of a future the company had been building toward for over a decade.

But the US was actually late to the party. By the time FedNow launched, real-time payment systems were already operating in over 70 countries. India's UPI was processing roughly 10 billion transactions per month, making it the largest real-time payment system in the world by volume. Brazil's PIX had been adopted by hundreds of millions of users within its first two years. The UK's Faster Payments system, where ACI had some of its earliest real-time payment wins, had been operating for 15 years. The global movement toward instant settlement was not a trend; it was a transformation.

ACI had positioned itself at the center of this transformation. The company supported 18 real-time domestic payment schemes across more than 17 countries, and powered 25 domestic and pan-regional real-time schemes across six continents. It supported 10 central payment infrastructures. By ACI's own calculations, its real-time payment platforms covered approximately one-third of the countries offering real-time payment services, reaching roughly 1.8 billion people.

The competitive landscape was shifting as these systems matured. In the early days of real-time payments, the key challenge was simply building the infrastructure: designing the message formats, establishing the clearing and settlement rules, building the software that could process transactions in milliseconds. ACI's deep experience with these implementations gave it a significant first-mover advantage. But as real-time payment systems matured and became operational, the competitive focus shifted from infrastructure build-out to value-added services: fraud detection, data analytics, cross-border interoperability, and compliance reporting.

This shift played directly to ACI's strengths. The company's fraud management platform, which had grown through the ReD acquisition and continued internal investment, now incorporated machine learning models that analyzed transactions using over 10,000 signals and 8,000 AI features. The platform could identify suspicious patterns, score transaction risk, and make approve-or-decline decisions in the same milliseconds that the real-time payment itself took to process. ACI's patented Incremental Learning technology automatically refreshed machine learning models based on data drift, performance degradation, or scheduled intervals, ensuring that fraud models stayed current as attack patterns evolved.

The fraud arms race became a major competitive differentiator. Real-time payments created real-time fraud risk: when money settles in seconds, there is no window to review a flagged transaction before the funds are irreversibly transferred. This made fraud detection not just important but existential for real-time payment systems. Banks needed fraud models that could keep pace with the speed of settlement, and they needed those models to be accurate enough to minimize false positives that would block legitimate transactions. Every false positive was a frustrated customer, and in a competitive banking environment, frustrated customers switched banks.

ACI published an annual report, "Prime Time for Real-Time," in partnership with the Centre for Economics and Business Research, that tracked global real-time payment adoption. The 2023 edition documented 266.2 billion real-time payment transactions globally, up 42.2 percent year over year. ACI's role as both a participant in the real-time payments ecosystem and a thought leader in documenting its growth reinforced the company's position as the go-to infrastructure provider for banks and central banks deploying these systems.

For investors, the key question was the total addressable market. Real-time payments were still in early stages of adoption in many of the world's largest economies. The United States, despite FedNow's launch, was years away from ubiquitous real-time payment adoption. Continental Europe was still working through its SEPA Instant rollout. Africa and large parts of Southeast Asia were just beginning to deploy real-time infrastructure. If ACI could maintain its share of the global real-time payments market as these regions scaled, the revenue growth runway extended for decades.

XI. The Private Equity Question That Wasn't

In January 2023, Bloomberg reported that ACI Worldwide was weighing a potential sale, working with financial advisers as it fielded takeover interest from private equity firms. Motive Partners, a fintech-focused PE firm, was reportedly in advanced talks to acquire the company. The deal made strategic sense on paper: ACI's mission-critical infrastructure, recurring revenue streams, and long customer relationships were exactly the kind of assets that private equity firms valued in payments companies. Other PE-backed payments plays, such as the buyouts of Worldpay, First Data, and Nets, had generated strong returns by investing in platform modernization and then driving revenue growth through cross-selling and geographic expansion.

But the deal never materialized. By mid-2023, talks had reportedly slowed due to banking industry upheaval, including the regional banking crisis triggered by the failures of Silicon Valley Bank and Signature Bank, and difficult conditions in the leveraged financing markets. ACI Worldwide remains a publicly traded company on NASDAQ as of early 2026, trading under the ticker ACIW.

The episode was revealing nonetheless. The PE interest validated ACI's strategic positioning: these were sophisticated financial buyers who saw long-term value in ACI's assets, competitive moats, and growth runway. The fact that the deal did not close was a function of market timing, not strategic logic. And ACI's subsequent performance suggested that remaining public was not necessarily a disadvantage.

In June 2023, Thomas W. Warsop III was appointed as permanent President and CEO. Warsop, who had served as non-executive Board Chairman and been named interim CEO in November 2022 following the departure of Odilon Almeida, brought a different leadership style. Where his predecessor had been a globetrotting payments executive recruited from Western Union, Warsop was a Board insider who understood ACI's technology, customers, and competitive dynamics from years of oversight.

Under Warsop, ACI accelerated its product development and returned to double-digit revenue growth. The company's revenue grew 10 percent in 2024 to $1.59 billion, and another 10 percent in 2025 to $1.76 billion, marking the first back-to-back years of double-digit growth in the company's modern history. Operating cash flow in 2025 reached $323 million, and the company returned $203 million to shareholders through share repurchases, retiring 4.2 million shares.

The company's 2026 guidance called for revenue of $1.88 to $1.91 billion and adjusted EBITDA of $530 to $550 million, with plans to allocate up to 60 percent of operating cash flow to share repurchases. These were numbers that told a clear story: ACI was not just surviving in the age of fintech disruption; it was thriving.

The strategic lesson is worth noting. In an era when many payments companies went private to escape quarterly earnings pressure and invest for the long term, ACI found a way to make the same investments while remaining accountable to public shareholders. Whether this approach was superior to the PE alternative is a question that only time can answer. But ACI's recent performance suggests that patient capital is not exclusively a private-market phenomenon.

XII. The Business Model Deep Dive

ACI's business model, when examined closely, reveals why the company has proven so durable in an industry marked by relentless disruption. Three revenue streams compose the business: software licensing, which is declining as a share of total revenue; transaction processing fees, which are stable and growing with volume; and SaaS subscriptions, which are growing the fastest and now dominate the revenue mix.

The economics of payment processing scale beautifully. The infrastructure required to process one million transactions and the infrastructure required to process one billion transactions are not fundamentally different in cost. Once the platform is built, tested, and deployed, the marginal cost of processing an additional transaction approaches zero. This means that as transaction volumes grow, margins expand. It is one of the most attractive economic characteristics in enterprise software, and it explains why payments infrastructure companies command premium valuations.

But the real engine of ACI's business model is switching costs. An 18-to-36-month implementation timeline is just the beginning. A bank that deploys ACI's payment processing software must integrate it with core banking systems, card networks, clearing houses, and dozens of other internal and external systems. Staff must be trained on the new platform. Regulatory approvals must be obtained. Testing and validation procedures must be completed. Once all of this work is done, the bank has made an investment of tens of millions of dollars and thousands of person-hours. The prospect of doing it again with a different vendor is, for most institutions, unthinkable.

The result is customer lifetimes that are extraordinary by any software industry standard. Banks stay with ACI for 15 to 25 years or more. This is not because they are locked in by contracts; it is because the operational risk of switching is too great and the cost of reimplementation is too high. The switching costs are not merely financial; they are existential. A failed payment system migration could freeze millions of transactions, strand consumers without access to their money, and trigger regulatory investigations. No bank CIO wants to be the person who approved that risk.

ACI's land-and-expand playbook leverages these dynamics. A bank that initially deploys ACI for ATM switching is a natural candidate for real-time payments processing, fraud detection, and bill payment capabilities. Each additional module deepens the integration, increases the switching costs, and generates incremental recurring revenue. ACI's revenue per customer grows over time, not because ACI raises prices, but because customers expand their use of the platform.

The pricing power that comes with mission-critical infrastructure is significant but not unlimited. Large banks have negotiating leverage, and they use it. But even the largest banks face the same switching cost calculus: the cost of changing payment infrastructure vendors is so high, and the risk so significant, that price negotiations tend to happen within a range rather than as genuine competitive bidding processes. Smaller banks have less negotiating power, which is why ACI's expansion into the mid-tier financial institution market, currently being driven by the new Connetic platform, represents a significant growth opportunity.

ACI reinvests 12 to 15 percent of revenue in research and development annually, a level of R&D intensity that reflects both the complexity of the payments technology stack and the pace of innovation required to stay ahead of competitors. Geographic diversification adds another dimension to the business model, with approximately half of revenue coming from international markets. This diversification provides a natural hedge against economic cycles in any single market, though it introduces complexity in managing currency exposure and navigating regulatory environments across 94 countries.

XIII. Competitive Landscape & Strategic Positioning

The payments technology landscape can be divided into three distinct competitive arenas, and ACI occupies a unique position across all of them.

In the first arena, enterprise bank infrastructure, the dominant players are the "Big Three" of American bank technology: Fiserv, FIS, and Jack Henry. But ACI does not compete directly with these companies for core banking contracts. Fiserv, which serves 42 percent of US banks and 31 percent of credit unions, provides core processing, account management, and a broad suite of banking applications. FIS is dominant among the largest banks, serving 78 institutions with over $10 billion in assets. Jack Henry focuses on community banks and credit unions. ACI operates at a different layer of the stack: the payment switching, fraud detection, and real-time settlement infrastructure that sits on top of or alongside core banking systems. In many implementations, ACI coexists with Fiserv, FIS, or Jack Henry rather than replacing them.

In the second arena, real-time payments infrastructure, ACI has relatively few direct competitors with comparable global reach. Most real-time payment implementations have been done by a small number of vendors, and ACI's track record of 25 domestic and pan-regional schemes across six continents gives it a reference portfolio that new entrants cannot match. Temenos and Finastra compete in adjacent markets but are primarily core banking vendors rather than real-time payments specialists. The Clearing House's RTP network and the Fed's FedNow are platforms, not vendors; ACI provides the software that enables banks to connect to these platforms.

In the third arena, merchant and biller payments, ACI faces a more fragmented competitive landscape. Stripe and Adyen are formidable competitors in merchant acquiring, though they tend to focus on different customer segments: Stripe on developers and digital-native businesses, Adyen on enterprise retailers. ACI's Speedpay platform competes with Fiserv's bill payment capabilities and with consumer payment platforms like PayPal and Apple Pay. The differentiation comes down to infrastructure depth versus consumer experience: ACI wins when the buyer values regulatory compliance, reliability, and integration with back-office systems; fintech challengers win when the buyer prioritizes developer experience and speed of deployment.

Where ACI is most vulnerable is in greenfield markets where buyers have no legacy infrastructure to integrate with and can choose a cloud-native solution from scratch. A new digital bank launching in Southeast Asia can adopt a modern payment platform in weeks, without the need for ACI's decades of institutional knowledge about integrating with legacy core banking systems. This is the counter-positioning threat that Hamilton Helmer describes: new entrants can offer a fundamentally different value proposition that incumbents cannot match without cannibalizing their existing business.

ACI's response to this threat is its newest product, ACI Connetic, launched in 2025 and representing the company's bet on the next generation of payment infrastructure. But before we get there, it is worth examining the structural dynamics of the payments industry through a more systematic lens.

XIV. Porter's Five Forces Analysis

The structural attractiveness of the payments infrastructure industry can be understood through the lens of Michael Porter's five competitive forces.

The threat of new entrants is low. Building a payment processing platform that meets the reliability, security, and compliance requirements of the world's largest banks requires massive capital investment, years of development, and a track record that can only be built one implementation at a time. Regulatory certifications and bank security audits alone can take three to five years. New entrants face a chicken-and-egg problem: banks will not deploy unproven payment infrastructure, and infrastructure cannot be proven without bank deployments. The capital requirements are formidable, the regulatory barriers are high, and the reference customer requirements create a moat that money alone cannot overcome.

Supplier power is low to medium. ACI's primary inputs are cloud infrastructure, provided by AWS and Azure, and specialized engineering talent. Cloud infrastructure is increasingly commoditized, with multiple providers competing on price and capability. However, ACI's 2025 decision to build Connetic on Microsoft Azure does create some platform dependency. On the talent side, payments engineers with deep domain expertise are in high demand and short supply, which gives individual contributors some negotiating leverage. But ACI's Omaha headquarters provides a cost advantage in talent acquisition, and the company's mission-critical customer base is an attractive draw for engineers who want to work on systems that matter.

Buyer power is medium to high at the top of the market and lower in the middle. The world's largest banks have significant negotiating leverage because they represent large revenue concentrations and have the resources to credibly evaluate alternatives. However, the switching costs that are so central to ACI's competitive position limit the practical exercise of buyer power. A bank may negotiate hard on pricing, but it is unlikely to walk away from an ACI implementation once it is in place. Tier two and three banks have less negotiating strength, which is one reason why ACI's expansion into the mid-tier market through Connetic is strategically important.

The threat of substitutes is medium. Fintech companies can unbundle specific payment functions and offer them as standalone services. A bank that uses ACI for card switching might use a fintech solution for mobile payments or a different vendor for cross-border transfers. The most extreme substitute threat comes from the largest banks building payment infrastructure in-house, but this is rare because the cost and complexity of maintaining a proprietary payment platform are enormous. Blockchain and cryptocurrency alternatives remain emerging and unproven at the scale of traditional payment systems.

Competitive rivalry is high. Fiserv and FIS are well-capitalized, deeply entrenched, and constantly innovating. The payments industry requires continuous investment in new capabilities, platform modernization, and regulatory compliance. Price pressure is real in mature markets where banks are sophisticated buyers with access to detailed competitive benchmarks. Innovation is not optional: the company that stops investing falls behind within a few years.

The overall assessment is a structurally attractive industry with durable moats, but one that demands continuous investment to maintain competitive position. Payments infrastructure is not a business where a company can coast on its installed base; the pace of change in payment types, regulatory requirements, and fraud threats ensures that even the most entrenched incumbent must keep running to stay in place.

XV. Hamilton's Seven Powers Analysis

Hamilton Helmer's Seven Powers framework provides a complementary lens for understanding ACI's competitive position, one that focuses on the sources of durable advantage rather than the intensity of competitive forces.

Scale economies are strong. The fixed costs of building, maintaining, and operating payment processing infrastructure are enormous, but they are amortized across trillions of dollars in transaction volume. Once ACI has built a real-time payments platform, the cost of processing an additional transaction is negligible. This means that per-transaction margins expand as volumes grow, creating a structural advantage over smaller competitors who must spread similar fixed costs across fewer transactions. The 10 percent revenue growth ACI achieved in both 2024 and 2025, while maintaining or expanding margins, demonstrated this dynamic in practice.

Network effects are moderate. ACI's biller and merchant networks exhibit two-sided dynamics: more billers on the Speedpay platform make it more valuable to consumers, and more consumers using the platform make it more attractive to billers. Bank-to-bank real-time payment rails similarly strengthen as adoption grows. But ACI's network effects are not as powerful as those of pure network businesses like Visa or Mastercard, where the network itself is the product. ACI's value is in the infrastructure that connects to these networks, not in the network connections themselves.

Counter-positioning is weak. ACI does not have a business model innovation that incumbents cannot copy without damaging their own businesses. In fact, ACI faces counter-positioning risk from cloud-native fintechs that can offer modern, API-first payment platforms without the legacy technology and migration complexity that ACI carries. These new entrants can serve greenfield customers who have no legacy systems to integrate with, at price points and deployment speeds that ACI struggles to match with its traditional approach.

Switching costs are very strong. This is ACI's primary moat. The 18-to-36-month implementation cycles, the operational risk of payment system failure, the regulatory re-approval requirements, and the employee training and process redesign that accompany any migration create a barrier to exit that keeps customers on ACI's platform for decades. When the cost of failure is catastrophic, the rational decision is to stay with the incumbent. This single power explains more about ACI's durability than any other factor.

Branding is moderate. ACI has a strong reputation among bank CIOs and payment executives: the "nobody gets fired for choosing ACI" dynamic that IBM long enjoyed in enterprise computing. But ACI is not consumer-facing, which limits the premium it can charge for brand recognition. The brand matters in competitive evaluations, where ACI's track record of reliability and global scale provides reassurance to risk-averse bank buyers, but it does not create the kind of consumer loyalty premium that powers consumer-facing brands.

Cornered resource is weak. ACI does not possess unique patents, exclusive data, or irreplaceable talent that competitors cannot access. Its technology is proprietary but not uniquely patented in ways that prevent competitors from building similar capabilities. Its engineering talent is specialized but exists in a labor market where payments expertise can be hired by anyone willing to pay. Its geographic presence, while extensive, is replicable by a well-capitalized competitor.

Process power is moderate to strong. This may be ACI's most underappreciated advantage. Decades of payment processing expertise have been distilled into implementation methodologies, testing frameworks, incident response procedures, and operational playbooks that represent genuine institutional knowledge. When ACI deploys a real-time payment system in a new country, it brings the accumulated learnings of dozens of previous deployments. This knowledge is embedded in processes, documentation, and organizational culture in ways that are difficult for competitors to observe, let alone replicate. It is the kind of advantage that only reveals itself over time, as competitors discover that building the technology is the easy part and deploying it reliably at scale is the hard part.

The synthesis is clear: switching costs and scale economies are ACI's primary powers, reinforced by moderate process power and network effects. The vulnerability comes from counter-positioning by cloud-native fintechs in greenfield markets where ACI's switching cost moat does not yet exist. The strategic imperative for ACI is to extend its moat into these new markets before competitors can establish themselves, which is precisely the objective of the Connetic platform.

XVI. The Modern Era: AI, ISO 20022, and ACI Connetic (2024–2026)

The ISO 20022 migration is, without exaggeration, the biggest infrastructure upgrade in banking history. ISO 20022 is a global standard for financial messaging, a common language that allows payment systems around the world to communicate with each other using rich, structured data rather than the compressed, cryptic formats that have been the norm for decades. SWIFT required all financial institutions to receive and process ISO 20022 messages by November 2022, with full adoption for cross-border payments targeted for late 2025. Fedwire, the Federal Reserve's high-value payment system, launched its ISO 20022 migration in 2025. European systems like TARGET2 and SEPA have undergone their own transitions.

For banks, migrating to ISO 20022 is an enormous undertaking. Every system that touches a payment message, from front-end applications to back-office reconciliation engines, must be updated to handle the new format. Legacy systems that have been running for decades must be either replaced or wrapped in translation layers that convert between old and new formats. The compliance deadlines are fixed, the technical complexity is significant, and the risk of getting it wrong includes the inability to process payments through major clearing systems.

ACI positioned itself as an enabler of this migration, offering an insulation and translation layer approach that allows banks to adopt ISO 20022 without ripping out and replacing their existing infrastructure. Rather than requiring a wholesale system replacement, ACI's approach lets banks maintain their current payment processing systems while adding a translation layer that converts messages between legacy formats and ISO 20022. The company estimated implementation timelines of 9 to 12 months for basic send-and-receive capabilities, far shorter than a full system replacement.

But the most significant product development in ACI's recent history is the launch of ACI Connetic in 2025. Connetic is a cloud-native payments hub built on Microsoft Azure that unifies account-to-account payments, card payments, and AI-driven fraud prevention on a single platform. It represents ACI's answer to the cloud-native fintech threat, a ground-up rebuild of the company's payment processing capabilities using modern architecture rather than an incremental upgrade of legacy systems.

The timing of Connetic's launch was strategic. By 2025, a critical mass of banks had accepted that cloud-based payment processing was not just viable but necessary. The security, compliance, and reliability concerns that had held back cloud adoption in payments were being addressed by cloud providers and regulators alike. ACI's decision to build Connetic on Azure reflected both a technology choice and a go-to-market partnership with Microsoft, whose presence in enterprise financial services provided a channel into bank IT departments.

The first UK deployment of Connetic was announced in February 2026, unifying SWIFT, CHAPS, and Faster Payments on a single cloud-native platform. This was a significant milestone: a major market where ACI already had deep relationships was validating the next-generation platform for production use. The company reported that approximately two-thirds of its 2026 pipeline opportunities were targeting the mid-tier financial institution market, a segment that ACI had historically underserved.

This mid-tier expansion was strategically important for two reasons. First, mid-tier banks were more likely to adopt cloud-native platforms because they lacked the IT resources to manage on-premises infrastructure. Second, the mid-tier market represented a large pool of potential customers that ACI had not previously been able to serve cost-effectively. Connetic's cloud-native architecture reduced the implementation cost and timeline, making ACI's enterprise-grade payment capabilities accessible to banks that could not have afforded a traditional ACI deployment.

ACI's fraud management capabilities continued to evolve with artificial intelligence. The company's machine learning models now utilized over 10,000 signals, 8,000 AI features, and 500 behavior attributes to detect and prevent fraud. The ACI Model Generator allowed business users to build and deploy machine learning models without deep technical expertise. And the company's Incremental Learning technology, which automatically refreshed models based on changing fraud patterns, addressed one of the most persistent challenges in fraud detection: keeping models current as attackers evolve their tactics.

In November 2025, ACI acquired Payment Components, a European fintech specializing in AI-powered financial messaging and Open Banking solutions, to augment the Connetic platform. The acquisition signaled ACI's intent to integrate Open Banking capabilities, which allow third-party applications to access bank account data and initiate payments through standardized APIs, into its core infrastructure offering.

The embedded finance threat, where banking-as-a-service platforms like Unit and Treasury Prime enable non-financial companies to offer banking products, represents a longer-term competitive challenge. If major technology companies or retailers embed payment capabilities directly into their platforms, bypassing traditional bank infrastructure entirely, ACI's bank-centric model could be disrupted. For now, however, embedded finance platforms still rely on underlying banking infrastructure, and ACI's payment processing capabilities are part of the infrastructure that these platforms need to function.

XVII. Bull vs. Bear Case

The investment case for ACI Worldwide, as the company enters its sixth decade, rests on a fundamental question: is ACI's entrenched position in global payment infrastructure a source of durable advantage or a legacy position that will slowly erode as the industry modernizes?

The bull case begins with mission-critical infrastructure and extraordinary customer longevity. Banks that have been running ACI's payment processing software for 15 to 25 years are not going to switch because a startup offers a better API. The operational risk of migrating payment infrastructure is simply too great, and the cost of implementation is too high. This is not vendor lock-in through contractual terms; it is lock-in through the physics of payment processing, where the consequences of a failed migration are measured in billions of frozen transactions and regulatory penalties.

The real-time payments opportunity extends the growth runway for decades. As of early 2026, real-time payment systems were still in early stages of adoption in many of the world's largest economies. The United States was just beginning to scale FedNow. Continental Europe was working through SEPA Instant adoption. Africa and large parts of Asia were deploying real-time infrastructure for the first time. If ACI maintains its current share of this market, the revenue growth from real-time payments alone could sustain double-digit growth for years.

The fraud management opportunity is equally compelling. Real-time payments create real-time fraud risk, and the sophistication of fraud attacks is increasing at a pace that only AI-driven detection can match. ACI's data advantage, the ability to see fraud patterns across ecosystems in 94 countries, provides the training data needed to build machine learning models that are more accurate than anything a single bank could build on its own. As fraud becomes more sophisticated, banks will increasingly need enterprise-grade AI fraud platforms, and ACI's head start in this market is significant.

The recurring revenue trajectory supports premium valuation. With $1.21 billion in recurring revenue in 2025, representing 69 percent of total revenue and growing at 11 percent annually, ACI's revenue base is increasingly predictable and durable. The SaaS and PaaS component, at $1.01 billion, represents the fastest-growing segment. If ACI can push recurring revenue above 80 percent of total revenue over the next few years, the company's valuation could rerate significantly.

The bear case centers on growth rate and competitive dynamics. ACI's revenue growth over the past decade has been in the low to mid-single digits for most years, only recently accelerating to double digits. Whether this acceleration is sustainable or represents a temporary catch-up from post-pandemic tailwinds remains to be seen. The payments industry is mature in many of ACI's core markets, and organic growth rates may revert to historical levels once the current modernization cycle plays out.

Cloud-native competitors pose a genuine threat in greenfield markets. A new digital bank launching today has no reason to choose a legacy payment processing platform when it can deploy a modern, API-first solution in days. ACI's Connetic platform is designed to address this threat, but it is early in its adoption cycle and has yet to prove itself at scale. If Connetic fails to gain traction in the mid-tier market, ACI could find itself trapped in a declining base of large-bank customers while cloud-native competitors capture the growth segment.

Technology debt from decades of acquisitions is a persistent concern. ACI has absorbed numerous companies over its history, each bringing its own technology stack, customer base, and engineering culture. The consolidation of 40-plus legacy products into three core platforms was a major undertaking, and residual complexity from historical acquisitions continues to consume engineering resources that could otherwise be invested in new capabilities.

Margin pressure from cloud infrastructure costs is another consideration. As ACI migrates more customers to cloud-hosted environments, it takes on the cost of cloud infrastructure that was previously borne by customers running on-premises. While the SaaS model generates more predictable revenue, the gross margin profile of cloud-hosted software can be lower than on-premises licensing, particularly at early scale.

The most important KPIs to track ACI's ongoing performance are: recurring revenue as a percentage of total revenue, which measures the durability and predictability of the revenue base (target north of 70 percent and heading toward 80 percent); and real-time payment transaction volume growth, which measures ACI's positioning in the highest-growth segment of the payments industry. These two metrics together capture both the quality of ACI's revenue and the trajectory of its most strategically important business line. An investor watching these two numbers will have a clear signal of whether ACI's thesis is playing out.

XVIII. Strategic Lessons & Playbook

ACI's half-century of history offers a masterclass in building durable infrastructure businesses, with lessons that extend far beyond the payments industry.

The first lesson is about timing mega-trends before they become obvious. ACI began investing in real-time payment capabilities in 2011 and 2012, years before most American banks had heard the term "real-time payments." The acquisitions of Distra and S1 Corporation, the early work with UK Faster Payments, and the development of the Universal Payments platform were all bets placed on a future that had not yet arrived. When that future finally materialized with FedNow in 2023, ACI was not scrambling to build capability; it was already the market leader with a decade of production deployments behind it. The lesson is that in infrastructure markets, the returns on early investment compound over time, because each implementation builds institutional knowledge and reference customers that late entrants cannot replicate.

The second lesson is about the power of boring, mission-critical infrastructure. Payment processing will never generate the excitement of a consumer app launch or a self-driving car demonstration. But payments will always be necessary, and the institutions that process them will always need reliable, secure, compliant software to do so. The durability of ACI's business comes precisely from this necessity: payments are not a discretionary activity, and payment infrastructure is not a discretionary purchase. In a world where technology trends come and go with dizzying speed, there is something deeply reassuring about a business built on the certainty that people will always need to move money.

The third lesson is about switching costs as the ultimate moat. ACI's customer relationships last for decades not because of superior marketing or brand loyalty but because the cost of switching is simply too high. When the alternative to staying with your current vendor is an 18-to-36-month migration project with material risk of operational failure, the rational decision is to stay. This is a moat that does not erode over time; it deepens, because every year that a bank runs ACI's software is another year of integration, customization, and institutional knowledge that makes switching more expensive.

The fourth lesson is about strategic M&A as a tool for entering new categories. ACI's acquisitions of S1, ReD, PAY.ON, Official Payments, and Speedpay each opened new markets that organic growth alone could not have reached. The key to successful M&A in infrastructure markets is recognizing that you are not buying revenue; you are buying capability, customer relationships, and market position. Each of ACI's major acquisitions brought technology or market access that would have taken years to build organically.

The fifth lesson is about the SaaS transition challenge. Moving from perpetual licenses to recurring revenue is one of the most difficult transformations an enterprise software company can undertake. ACI navigated this transition over the course of a decade, accepting short-term revenue compression in exchange for a more predictable, higher-quality revenue base. By 2025, with recurring revenue at 69 percent of total, the transition was largely complete, but the journey required patience, strategic conviction, and the willingness to endure years of underperformance in reported metrics.

The final lesson is about geographic diversification as risk management. ACI's roughly 50/50 split between domestic and international revenue provides a natural hedge against economic cycles, regulatory changes, and competitive dynamics in any single market. When US banking consolidation slowed growth in one market, emerging market expansion provided offsetting momentum. This diversification does not come free: managing operations across 94 countries introduces currency risk, regulatory complexity, and cultural challenges. But the portfolio effect is real, and it has allowed ACI to navigate economic cycles that would have been far more damaging to a geographically concentrated competitor.

XIX. Epilogue: What's Next for the Invisible Giant

In October 2025, ACI Worldwide celebrated its 50th anniversary. Half a century of building the invisible infrastructure that moves the world's money. From three programmers in Omaha writing software for fault-tolerant computers to a global platform processing over 90 billion transactions per year. From the early days of the ATM to the real-time payments revolution. From perpetual software licenses to cloud-native SaaS. The arc of ACI's history is a story about quiet, persistent, unglamorous innovation in the systems that everyone depends on and almost nobody sees.

The invisible infrastructure thesis, the idea that some of the most strategically valuable companies in the world are ones that consumers never interact with directly, is not new. But ACI is perhaps its purest expression in the payments industry. When a consumer taps their phone to pay for coffee, they see the Apple Pay logo, or their bank's app, or the merchant's point-of-sale terminal. They do not see the transaction switching software that routed the payment, the fraud detection engine that scored it in milliseconds, or the real-time settlement system that moved the money from one account to another. But all of those invisible layers exist, and ACI built many of them.