Achieve Life Sciences: The Cold War Cure for a $20B Addiction

I. Introduction & The "Natural" Contender

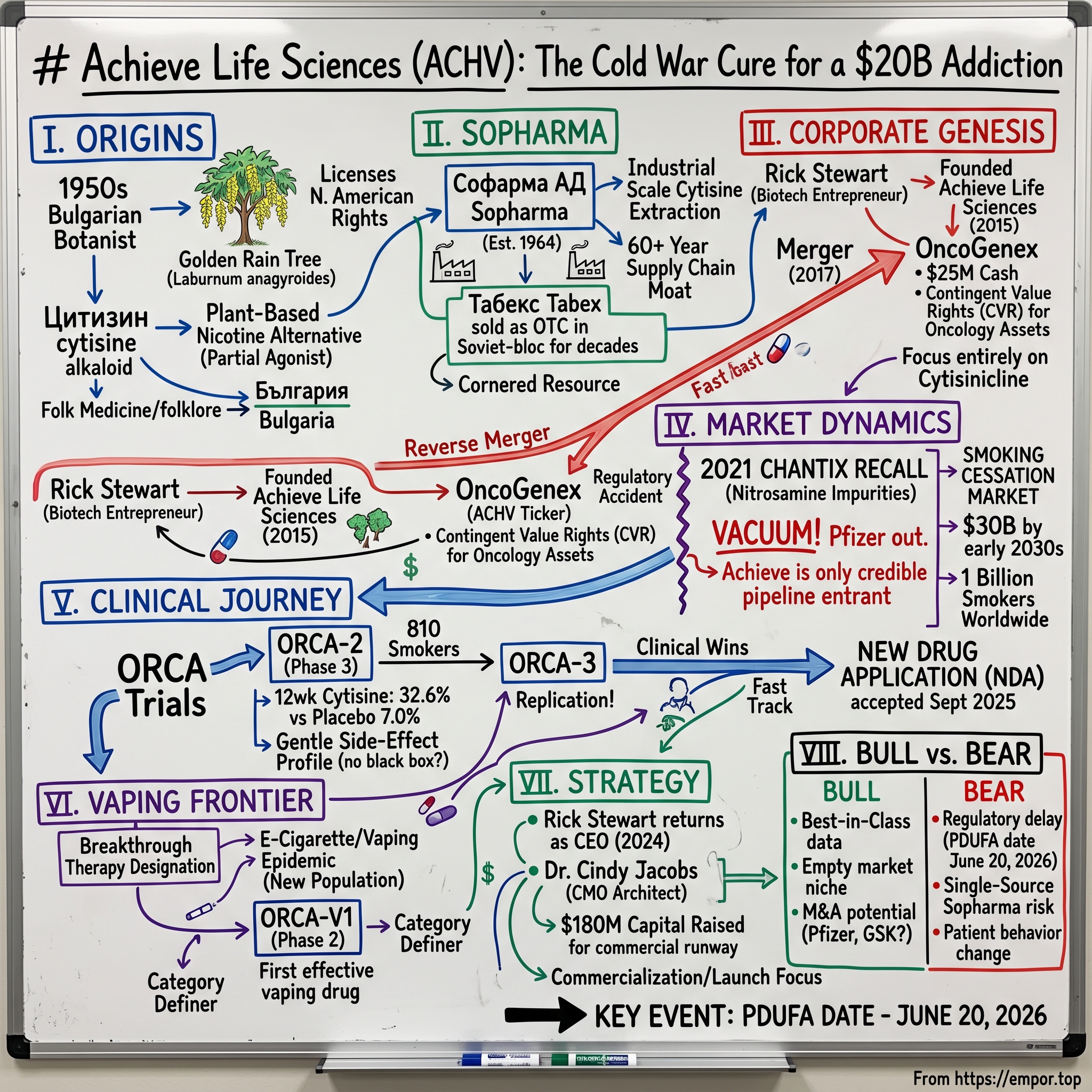

Picture a Bulgarian botanist in the late 1950s, walking through a garden in Sofia under a pale, post-Stalin sun. He pauses beneath a Laburnum anagyroides — the "golden rain tree" — its drooping yellow blossoms ripening into seed pods that look almost edible, almost ornamental. They are, in fact, neither. Those seeds contain Цитизин cytisine, an alkaloid so structurally close to nicotine that the human brain mistakes one for the other. Local farmers had known for generations that horses grazing too close to laburnum hedges grew listless and stopped eating; Soviet-bloc pharmacologists, working behind the Iron Curtain with fewer dollars but no shortage of patience, took that folklore and built a drug on top of it. While Western pharmaceutical giants would spend the next half-century chasing synthetic smoking-cessation molecules, the Bulgarians had already cornered the plant.

That is the strange, almost mythic ancestry behind Achieve Life Sciences, a NASDAQ-listed micro-cap based in Vancouver, Washington that today sits on the cusp of an FDA decision that could redefine the smoking-cessation market for the first time in twenty years.1 The drug at the center of the story is cytisinicline — the modernized, pharmaceutical-grade descendant of the very same molecule those Bulgarian chemists isolated during the Cold War. And the timing could hardly be more dramatic. The global smoking-cessation pharmacotherapy market is on a path toward roughly $30 billion by the early 2030s, with smoking-cessation aids more broadly already topping $20 billion when nicotine replacement and digital tools are included.2 One billion people still smoke worldwide. Tens of millions more have migrated to e-cigarettes, creating an entirely new patient population that did not exist when the last cessation drugs were approved. And the dominant prescription incumbent — Pfizer's Chantix (varenicline), once a billion-dollar franchise — vanished from American pharmacy shelves in 2021 after being recalled for carcinogenic nitrosamine impurities.[^3]

Into that vacuum walks a plant-based molecule with a sixty-year safety record in Eastern Europe, a single-source Bulgarian manufacturer with no equal at industrial scale, and a tiny American biotech that has bet everything on getting it across the FDA finish line. The Prescription Drug User Fee Act (PDUFA) goal date on cytisinicline's New Drug Application is June 20, 2026 — less than a month from the day this article is being written.[^4]

This is the story of how a Bulgarian "folk remedy" became the most asymmetric bet in late-stage biotech. It is a story about cornered resources and regulatory accidents, about a reverse merger that gave a tiny molecule a NASDAQ ticker, and about a founder-CEO who walked back into the corner office at exactly the moment his company needed a closer. From the laburnum hedges of България Bulgaria to a possible commercial launch in Indianapolis pharmacies — this is Achieve Life Sciences.

II. The Cold War Origins: The Golden Rain Tree & Sopharma

Long before there was an FDA application, before there was a NASDAQ ticker, before Achieve Life Sciences even existed as an idea, there was Софарма АД Sopharma — and there was a problem that the entire Eastern Bloc was suddenly motivated to solve. In the years after World War II, smoking rates across the Soviet sphere climbed to among the highest in the world. Tobacco was cheap. It was state-subsidized. And it was, increasingly, killing people. By the early 1960s, Bulgaria's communist health authorities began searching their domestic pharmacopoeia for something — anything — that could help workers quit. They did not have the luxury of Western R&D budgets. They had what grew in their own forests and gardens.

What grew, in abundance, was Laburnum anagyroides, the golden rain tree. Its seeds had been used in folk medicine across the Balkans for centuries, and they had also been studied for their pharmacological effects in the early twentieth century, when researchers noticed that cytisine bound to the same nicotinic acetylcholine receptors that nicotine itself targeted in the human brain. The analogy is almost too tidy: nicotine is the master key that opens the brain's reward locks; cytisine is a slightly worn-down version of that same key. It fits the lock, turns it just enough to dampen withdrawal, but never quite enough to deliver the full dopamine rush that keeps smokers smoking. In modern pharmacology, this is called a "partial agonist." In Soviet-era plain language, it was a way to let workers ease off the cigarette without going cold turkey.

Sopharma, then Bulgaria's flagship state pharmaceutical conglomerate, commercialized cytisine in tablet form under the brand name Табекс Tabex in 1964.[^5] For decades, Tabex was sold across the Warsaw Pact countries as a low-cost over-the-counter smoking-cessation aid. Generations of Eastern Europeans took it. The drug accumulated an extraordinary real-world safety record — not because anyone was running rigorous Western-style trials in Cold War Sofia, but simply because so many millions of people took it, for so many years, with so few reports of serious harm. When Western researchers finally turned their attention to cytisine in the 2000s, what they found was striking: in a head-to-head trial published in the New England Journal of Medicine in 2014, cytisine outperformed nicotine replacement therapy at a fraction of the cost.3 A follow-up NEJM study in 2021 compared cytisine directly with varenicline — Pfizer's Chantix — and found it non-inferior, with a notably gentler side-effect profile.4

Here is the part that matters for investors. Sopharma did not just develop cytisine; it became, over time, the only company in the world that knows how to extract and purify it at industrial scale. The supply chain is unglamorous and almost agricultural: Bulgarian foragers and contracted growers harvest laburnum seed pods, which are then processed through Sopharma's facilities using a proprietary extraction method refined over six decades.[^8] No Indian generics manufacturer figured this out. No Chinese API supplier matched it. The molecule is not patentable in the traditional sense — it is, after all, a plant alkaloid known since the nineteenth century — but the manufacturing process and the scale economics were quietly compounding behind the Iron Curtain while the rest of the pharmaceutical world ignored them.

That is what Hamilton Helmer would call a Cornered Resource. And it is the deepest moat in this entire story — not a patent, not a brand, but a single Balkan factory that has spent sixty years learning how to turn yellow flowers into white pills. Everything Achieve Life Sciences built afterward sits on top of that foundation, and any analysis of the company has to start with the uncomfortable fact that the company does not own its own supply chain. It rents it, exclusively for North America, from a Bulgarian partner with whom it shares destiny.

III. Corporate Genesis: Rick Stewart's Bet & The OncoGenex Shell

If Sopharma is the agricultural backbone of this story, Rick Stewart is its commercial brain. A serial biotech entrepreneur with the particular kind of Pacific Northwest pragmatism that the Vancouver–Seattle biotech corridor produces in abundance, Stewart had spent decades shepherding small-molecule programs through the FDA gauntlet before he ever heard the word "cytisinicline." His prior company, Corus Pharma, had been acquired by Gilead in 2006; his next venture, Calistoga Pharmaceuticals, was acquired by Gilead again in 2011. By the early 2010s, he was, in industry parlance, "between vehicles" — looking for the next asset to build a company around.

What Stewart noticed, and what most of his Big Pharma counterparts did not, was that Eastern Europe had been quietly running a multi-decade naturalistic experiment on cytisine. The data was there. The safety profile was there. The mechanism was elegant. What was missing was the regulatory infrastructure to bring it into North American medicine — randomized controlled trials run to FDA standards, a US-compliant manufacturing partnership, and a corporate structure that could raise capital on Western public markets. Stewart founded Achieve Life Sciences in 2015 with exactly that gap in mind. The plan was simple in the way the best biotech plans always are: license the North American rights to cytisinicline from Sopharma, run the clinical trials the Bulgarians had never needed to run, and unlock a market that had been hiding in plain sight.

But a private biotech, no matter how clever its thesis, cannot run Phase 3 trials on a credit card. Achieve needed access to the public markets — and in early 2017, it found a door. OncoGenex Pharmaceuticals, a Vancouver, BC-based oncology company, had just watched its lead asset, custirsen, fail in pivotal prostate cancer trials. OncoGenex had a NASDAQ listing, roughly $25 million in cash, and a board of directors looking for any path that did not involve a slow liquidation. On January 5, 2017, the two companies announced an all-stock merger that gave Achieve shareholders approximately 75% of the combined entity and OncoGenex shareholders 25%.[^9] The transaction closed in August 2017, and the combined company took the Achieve name and the ACHV ticker symbol.5

This is a transaction worth dwelling on, because reverse mergers of this kind are how a meaningful share of small-cap biotech actually reaches the public markets. The conventional path — a traditional IPO — typically costs a sponsor 7% in underwriting fees, plus another 10–15% IPO discount that bankers price in to ensure a clean first-day pop. In practical terms, that means a company raising $50 million on the public market often walks away with closer to $40 million in usable cash, with the difference accruing to Wall Street and aftermarket buyers. A reverse merger into a "clean shell" — that is, into a public company whose only remaining asset is its NASDAQ listing and a clean balance sheet — bypasses those frictions. Achieve, in effect, paid for its NASDAQ listing in stock rather than in fees, and inherited OncoGenex's residual cash to fund early clinical work.

The challenge with reverse mergers is what to do with the inherited assets. OncoGenex came with two failed oncology programs that nobody wanted — but that, in the unlikely event of an out-licensing deal or a partnership, might be worth something to someone someday. The elegant solution, and the one Achieve adopted, was a Contingent Value Right, or CVR, granted to legacy OncoGenex shareholders. If the oncology assets generated any future value, that value flowed to the pre-merger holders. Achieve, meanwhile, focused 100% of its forward energy on the Bulgarian molecule. It was a clean-slate strategy executed through a deal structure that gave both sides what they wanted: the OncoGenex holders kept the optionality on their dying assets, and Achieve got a public listing with no legacy distractions.

What Stewart bought, in retrospect, was the most expensive thing in biotech — time and access to capital — at the cheapest possible price. The thesis he had been carrying around for years now had a vehicle. All it needed was a catalyst.

IV. Inflection Point 1: The Chantix Vacuum

For most of the 2010s, that catalyst seemed unlikely to arrive. Pfizer's Chantix — generic name varenicline — was the dominant prescription smoking-cessation drug in the United States, generating peak revenues that climbed past $1 billion globally before the patent cliff began to bite. Varenicline worked. It was approved by the FDA in 2006. It had its problems — Pfizer spent years fighting black-box warning labels about neuropsychiatric side effects, including reports of vivid dreams, depression, and in rare cases, suicidality — but it was the standard of care. Any new entrant had to demonstrate superiority not just over placebo, but over a well-entrenched and well-studied prescription competitor. That is an expensive proposition for a micro-cap biotech.

Then, in the summer of 2021, the most unlikely catalyst in modern pharma materialized: a manufacturing contaminant. Pfizer disclosed that certain lots of Chantix contained elevated levels of N-nitroso-varenicline, a member of the nitrosamine family of impurities that the FDA had been tracking with increasing alarm since the 2018 valsartan recalls. Nitrosamines are probable human carcinogens. The acceptable daily intake threshold the FDA had begun applying to them was so stringent — measured in nanograms — that even trace contamination was enough to trigger a recall. On September 16, 2021, Pfizer announced a voluntary nationwide recall of all lots of Chantix.[^11] Within months, the drug was effectively unavailable in the United States.

If you have ever wondered what a "regulatory accident" looks like for a competitor in the same therapeutic class, this was it. Overnight, the largest prescription smoking-cessation product in America simply ceased to exist on pharmacy shelves. Insurers had to redirect prescriptions. Quitline counselors had to retrain. Patients on multi-month tapering protocols were left with no clear path forward. And the market that Pfizer had spent fifteen years building was suddenly an open lane. Pfizer eventually returned a reformulated varenicline to the market under generic licensing arrangements, but the brand equity, the prescriber loyalty, and the marketing infrastructure had all been dismantled. The category — once a textbook example of a moated incumbent — became contestable for the first time since the early 2000s.

For Achieve, this was the corporate equivalent of finding a vacant penthouse in a rent-controlled building. The strategic conversation inside the company shifted almost overnight. Cytisinicline had been positioned, up to that point, as a potential "me-too" — a plant-based alternative to varenicline that might appeal to patients seeking a more natural option. After September 2021, the positioning could be more ambitious: best-in-class. With Chantix gone and no other novel prescription smoking-cessation drug in late-stage development at any major pharma company, cytisinicline was suddenly the only credible new entrant in the pipeline. Investors who had previously viewed Achieve as a niche specialty-pharma story began modeling it as a potential category leader.

The lesson here, for any investor trying to understand small-cap biotech, is that timing is often as important as data. Achieve had been running its first Phase 3 trial — ORCA-2 — at exactly the moment Chantix imploded. The trial's design assumed Chantix would still be the comparator and the competitor. The trial's readout, when it arrived, would land in a market with no competitor at all. Few founders ever get a tailwind that strong, and even fewer have the courage to lean into it without overplaying their hand. Stewart and his team did neither. They kept their heads down and finished the trial.

V. The Clinical Journey: The ORCA Trials

The clinical program that brought cytisinicline to the brink of FDA approval is called ORCA — Ongoing Research of Cytisinicline for Addiction. It is one of those biotech acronyms that does double duty as a branding device, evoking something powerful, deliberate, and slightly predatory. The program itself was deliberately designed to do something the Bulgarians had never bothered to do: prove cytisinicline's efficacy and safety to Western regulatory standards, with the kind of statistical rigor and trial design that the FDA's Division of Anesthesiology, Addiction Medicine and Pain Medicine demands.

ORCA-2, the first of the pivotal trials, enrolled 810 adult smokers across the United States and randomized them into three arms: cytisinicline for six weeks, cytisinicline for twelve weeks, and placebo, each combined with behavioral support. The primary endpoint was biochemically verified continuous smoking abstinence during the last four weeks of treatment. The results, published in JAMA Internal Medicine on July 11, 2023, were the kind of clean win that small-cap biotech rarely delivers: 32.6% abstinence in the twelve-week cytisinicline arm versus 7.0% in the placebo arm, with the six-week arm also significantly outperforming placebo.6 Safety was the story underneath the story. The most commonly reported adverse events were mild — insomnia, abnormal dreams, nausea — and the rates were notably lower than the historical comparator data for varenicline. There were no significant signals on neuropsychiatric endpoints, the exact area that had haunted Chantix for fifteen years.

ORCA-3, the confirmatory Phase 3 trial that completed enrollment in 2023, repeated the design with 792 patients and reported topline data consistent with ORCA-2 — replication being the single most important word in any FDA submission. By the end of 2023, Achieve had two large, well-controlled, positive Phase 3 trials in its pocket, with consistent efficacy and safety profiles across both. The company filed its New Drug Application with the FDA in mid-2025, and on September 15, 2025, the agency formally accepted the NDA for review, setting the PDUFA action date for June 20, 2026.[^4]

Here is where the cytisinicline story takes a turn that most clinicians find more interesting than the headline efficacy numbers. The ORCA program tested a six-week treatment course, not the twelve-week course that varenicline requires. That distinction sounds bureaucratic, but it is profoundly important in the real world. Patients on smoking-cessation drugs notoriously fail to complete twelve-week courses. They feel better, they feel "cured," they stop refilling. A six-week protocol turns adherence from a marathon into a sprint. It also cuts the cost of therapy roughly in half, an important consideration in a market where most prescriptions are reimbursed by Medicaid, Medicare, and commercial plans that scrutinize per-quit cost-effectiveness. If cytisinicline launches with a label allowing a six-week course of treatment, it will have an adherence advantage and a pharmacoeconomic argument that no incumbent can easily counter.

The second clinical pillar of the ORCA program is ORCA-V1, the first major Phase 2 trial of any prescription drug specifically designed for e-cigarette cessation. Results published in 2024 showed cytisinicline significantly outperforming placebo in helping adult vapers quit nicotine entirely.7 This is, as the company likes to point out, an entirely new patient population — one that did not meaningfully exist when varenicline or nicotine replacement therapy was approved. The FDA granted cytisinicline Breakthrough Therapy Designation for vaping cessation, a formal regulatory signal that the agency considers this an unmet medical need worth fast-tracking. We will come back to that in Section VII, because the vaping opportunity is, in many ways, the more interesting half of the entire investment case.

What ties all of this together is that Achieve, against the long odds typical of late-stage biotech, has not yet stumbled. Two Phase 3 trials read out positive. The NDA was filed. The PDUFA date is set. From a clinical-execution standpoint, this is a company that has done the work.

VI. Management & Capital Deployment

Every biotech story is also, ultimately, a story about the people who run it — and in Achieve's case, that story is unusual because the founder did something that biotech founders rarely do. He walked away, and then he came back.

Rick Stewart founded Achieve in 2015 and served as its CEO through the OncoGenex merger and the early years of clinical development. In 2020, he transitioned to executive chairman and handed day-to-day operations to a series of operating CEOs, the most prominent of whom was John Bencich, who led the company through the ORCA-2 readout and the early stages of NDA preparation. Then, in August 2024 — with the FDA filing imminent and a commercial launch on the horizon — Stewart resumed the CEO role.[^14] The official framing was that the company was entering a new phase: commercialization, business development, and possible M&A. The unofficial framing, audible in conversations with analysts who cover the stock, was that the founder wanted to be at the wheel for the most consequential year in the company's history.

Standing beside Stewart through all of this has been Dr. Cindy Jacobs, Achieve's President and Chief Medical Officer, and arguably the single most important non-founder figure in the company. Jacobs is a clinical trial veteran with decades of experience navigating the FDA's regulatory machinery. She is the architect of the ORCA program — the person who chose the endpoints, designed the comparators, negotiated the special protocol assessments, and ultimately built the data package that the FDA is now reviewing. In a small biotech, the CMO is often more important than the CEO, because the CMO controls the asset that defines the entire enterprise. Jacobs is also a holdover from the OncoGenex era; she joined that company in 2003 and made the transition through the merger, providing a continuity of clinical leadership that few small-caps can claim.

The compensation structure at Achieve tells a more nuanced story than the headline numbers suggest. According to the most recent proxy statement, direct insider beneficial ownership across the executive team and board was modest — a single-digit percentage of shares outstanding, with the largest individual blocks held by Stewart and Jacobs.8 That kind of low insider ownership is sometimes a red flag in investor circles, particularly for those who like to see a founder with skin in the game measured in tens of millions of dollars. But the proxy also reveals that a substantial portion of executive compensation is tied to Performance-based Stock Units (PSUs) that vest on specific clinical and regulatory milestones — including, most importantly, the FDA approval decision tied to the June 20, 2026 PDUFA date. In other words, the team is not paid by base salary alone. They are paid by hitting a date that is now less than a month away.

Now to the capital. A company with no product revenue and a Phase 3 clinical program needs cash, and Achieve has spent the last several years staging a careful series of equity raises designed to extend its runway across each major catalyst. The pivotal transaction was a $124.2 million underwritten public offering completed on February 29, 2024 — the largest single financing in the company's history, and one that the team subsequently expanded through follow-on issuances to bring the total 2024 capital raised to roughly $180 million in headline terms.9 At the time of the offering, Achieve was trading at a market capitalization measured in the low hundreds of millions of dollars. Raising $124 million at that scale is, in plain terms, dilutive — but it is also the kind of dilution that small-cap biotechs are forced to accept if they want to walk into a PDUFA date with enough runway to also fund a commercial launch.

The benchmarking question is whether Achieve overpaid for that capital. Comparable late-stage Phase 3 biotechs in 2023 and 2024 were raising capital at gross-to-net spreads of 6–7% to underwriters, with discounts to the prior close ranging from 10% in hot deals to 25% in cold ones. Achieve's February 2024 raise was priced inside the median of that range, and the deal cleared without the kind of aftermarket selling pressure that signals a forced offering. The fact that the company has, by mid-2026, more than a year of operating runway in front of it, with the FDA decision on the immediate horizon, is the practical proof that the capital strategy worked. The team raised when it could, not when it had to — and that is the difference between biotech survival and biotech ruin.

VII. The Hidden Business: The Vaping Frontier

If the smoking-cessation market were the entire story of Achieve Life Sciences, the company would still be interesting — a tiny biotech challenging a wounded incumbent in a multi-billion-dollar therapeutic category. But the smoking market is, in some ways, the wrong story to focus on. Smoking rates in the United States have been declining for forty years. Globally, the trend is more nuanced, but in the developed markets that anchor pharmaceutical pricing, traditional cigarette use is in structural retreat. Meanwhile, a different nicotine market is exploding: electronic cigarettes, vapes, pods, and the entire ecosystem of nicotine-delivery devices that emerged after the 2007 launch of the first commercial e-cigarettes.

The vape market did something to American public health that nobody quite predicted. It created a new addiction, in a new population, with no approved cessation treatment whatsoever. By the early 2020s, the CDC was reporting that more than 2 million American teenagers were regular e-cigarette users — a generation that, in many cases, had never smoked a traditional cigarette but had become physiologically dependent on nicotine through pod-based delivery systems with concentrations several times higher than a typical cigarette. The "vaping epidemic," as the surgeon general's office began calling it, was a regulatory and clinical emergency, and the FDA's existing toolkit was inadequate. Nicotine replacement therapy had not been studied in the vaping population. Neither had varenicline. There was no on-label drug for vaping cessation.

This is where Achieve made the strategic move that, in hindsight, may matter more than anything else in its corporate history. Rather than treat vaping as a side indication, the team designed the ORCA-V1 trial as a serious Phase 2 program in its own right. The trial enrolled adult e-cigarette users who wanted to quit nicotine entirely, randomized them to cytisinicline or placebo, and measured biochemically verified abstinence from all nicotine products. The results, published in the American Journal of Medicine, demonstrated a clinically and statistically significant benefit — the first prescription drug ever to do so in a vaping-cessation trial.7

The regulatory response was not subtle. The FDA granted cytisinicline Breakthrough Therapy Designation for the treatment of nicotine dependence in adult e-cigarette users — a designation that fast-tracks development, increases FDA engagement throughout the process, and signals to the broader market that the agency considers this an unmet medical need worth prioritizing.1 In practical terms, Breakthrough Therapy Designation is the regulatory equivalent of a green light at every intersection. It does not guarantee approval, but it dramatically shortens the path.

The economic implications of a second indication are easy to underestimate. Smoking cessation has a defined addressable population that, in the United States, has been declining for decades. Vaping cessation has a defined addressable population that has been growing for fifteen years and now includes a meaningful share of Americans under thirty. That demographic shift matters not just for unit volume but for payer dynamics: younger patients tend to have longer life expectancies, which makes cessation therapy more cost-effective from a health economics standpoint, which in turn makes commercial insurers more willing to cover it without aggressive utilization management. A drug approved for both smoking and vaping cessation could plausibly capture multiple distinct revenue streams from the same regulatory and manufacturing footprint.

The second-order implication is even more interesting. If cytisinicline becomes the first approved drug for vaping cessation, it will, by definition, define the standard of care in that indication. Future competitors will be benchmarked against it. Future trials will use it as the comparator. The brand will become the category, and a category with no incumbent is the rarest thing in pharmaceutical commerce. Whether Achieve commercializes that opportunity on its own or licenses it to a larger partner with established primary-care infrastructure remains an open question. But the option value of having Breakthrough Therapy Designation in a virgin indication is, in any reasonable framework, significant.

VIII. Playbook: Power, Position, and the Five Forces

Step back from the clinical and regulatory narrative for a moment and ask the question that Hamilton Helmer would ask in his 7 Powers framework: what, exactly, allows Achieve Life Sciences to earn persistent differential returns relative to its competitors? The answer, when you work through it carefully, is more interesting than the typical biotech bull case.

The first and most durable power is the Cornered Resource. Sopharma's industrial-scale cytisine extraction capability is not replicable on any reasonable timeline. The Bulgarian company has a sixty-year head start on supply chain optimization, regulatory inspections in multiple jurisdictions, and the kind of accumulated process knowledge that does not exist in patents or filings but only in the muscle memory of the people who run the plant. Achieve's exclusive North American commercialization rights to cytisinicline create what is, in effect, a manufacturing monopoly for the duration of that agreement. A would-be generic competitor cannot simply file an ANDA on a plant alkaloid; it would have to build the entire supply chain from scratch, against a producer that has been refining its yields since the year Lyndon Johnson took office. The Sopharma agreement is, structurally, what makes Achieve more than just another biotech with a Phase 3 win.

The second power is Counter-Positioning. This is the framework Helmer uses to describe a competitive stance that is structurally difficult for the incumbent to copy. In Achieve's case, the counter-positioning is the "natural, plant-based" identity of cytisinicline relative to the synthetic Chantix franchise — and, more importantly, the cleaner side-effect profile that flows from cytisinicline's gentler receptor-binding kinetics. Pfizer cannot simply reformulate Chantix to be plant-based. Reformulating to remove the nitrosamine impurity required years of work and ultimately a reentry to the market under generic licensing rather than a relaunch of the original brand. Counter-positioning of this kind is rarely about marketing; it is about a product's underlying chemistry being something the incumbent cannot match without abandoning its own franchise.

The third power, which matters less but is worth naming, is Switching Costs. For patients, the switching cost from Chantix to cytisinicline is essentially zero — both are orally administered prescription tablets. For prescribers, however, the cognitive switching cost is meaningful. Primary care physicians have been writing varenicline prescriptions for nearly two decades. Their habits, their counseling scripts, their EHR templates, and their understanding of the side-effect profile are all calibrated around the incumbent. A new drug needs not just a positive label but a sales infrastructure capable of changing prescriber behavior — and that is precisely the operational challenge that Achieve will face if and when cytisinicline reaches the market in late 2026.

Turning to Michael Porter's classic Five Forces analysis, the picture is more mixed. Threat of new entrants is moderate; the cornered resource at the upstream end creates real barriers, but a well-capitalized generics player could, given enough time, build an alternative cytisine supply chain. Threat of substitutes is substantial; behavioral therapy, nicotine replacement therapy, and even "cold turkey" quitting all compete with prescription cessation drugs, and the long-term policy trend toward harm reduction (heated tobacco products, lower-nicotine cigarettes) creates additional substitution pressure. Bargaining power of buyers — meaning insurers and PBMs — is high, as it is in any small-molecule prescription category, and Achieve will need to demonstrate compelling pharmacoeconomics to secure formulary placement.

The most distinctive Porter force in this case is Bargaining Power of Suppliers, and it concentrates almost entirely in one place: Sopharma. The Bulgarian company is, by design, the source of the molecule, the manufacturer of the active pharmaceutical ingredient, and the contractual partner without whom Achieve has no business. Any disruption to Sopharma — political, regulatory, operational — flows through directly to Achieve's commercial future. The relationship has been remarkably stable over the past decade, but it remains the single largest structural risk in the entire investment case, and any sophisticated investor needs to think hard about it before underwriting the equity. We will return to this risk in the bear case.

IX. Myth vs. Reality, Bull vs. Bear

Around any late-stage biotech with a binary catalyst, a familiar set of narratives accumulates — some of them grounded in the data, some of them inherited from analogous stories in other corners of the industry. Before walking through the bull and bear cases, it is worth fact-checking three of the most common consensus narratives that float around Achieve.

Myth: "Cytisinicline is just generic Tabex with a new label." Reality: cytisinicline is the same active molecule as Tabex, but the FDA does not approve molecules — it approves products, with specific manufacturing standards, specific labels, specific dosing regimens, and specific clinical data packages. Tabex was never run through a Western Phase 3 program, never manufactured to FDA cGMP standards, and never approved as a prescription drug in the United States. Importing Bulgarian tablets is not a substitute for an approved US label. The regulatory moat is real.

Myth: "Smoking is a dying market — who cares?" Reality: smoking cessation is a growing market, even as smoking rates decline, because the patient cohort still numbers in the tens of millions and the demand for effective interventions is durable. Add the vaping opportunity, and the combined addressable population is meaningfully larger than the underlying smoker base alone.2

Myth: "If this drug were really that good, Pfizer or GSK would have bought it years ago." Reality: large pharma rarely acquires single-asset clinical-stage biotechs ahead of a PDUFA date — the risk-adjusted price is too high before approval and too high after. The window for a strategic transaction, if there is one, sits in the months immediately following approval, not before.

The Bull Case rests on three pillars. First, the regulatory math: cytisinicline has positive Phase 3 data, an accepted NDA, and an active PDUFA date, in a category where the leading incumbent was forced off the market four years ago and has yet to fully recover its franchise. Second, the addressable market: even a conservative penetration assumption on combined smoking and vaping cessation produces a revenue opportunity that supports a valuation meaningfully above the current market capitalization. Third, the strategic optionality: a Big Pharma partner facing the long-tail revenue loss of expiring respiratory or cardiovascular franchises could plausibly view cytisinicline as a tuck-in acquisition that complements an existing primary care field force. Pfizer itself is the most discussed acquirer in the rumor cycle, for obvious structural reasons. GSK, with its long history in smoking cessation through Zyban and Nicorette, is another candidate. Neither has telegraphed any intent. Both have the strategic logic.

The Bear Case rests on different pillars. First, regulatory risk: even with positive Phase 3 data, the FDA can delay, require additional information, or impose label restrictions that change the commercial calculus. The PDUFA date is a goal date, not a guarantee. Second, supply chain concentration: the single-source Sopharma dependency is the most uncomfortable feature of the entire business model, and a serious adverse event at the Bulgarian facility — geopolitical, regulatory, or operational — could disrupt commercial supply at exactly the moment the company would be ramping a launch. Third, the behavior change problem: even an effective drug cannot make a patient quit smoking if the patient is not motivated to quit. Cessation drugs work in patients who want to quit and need help; they do not work in patients who have no intention of quitting. The addressable market is, in practice, smaller than the headline population of smokers and vapers.

Competitive benchmarking sharpens both cases. Chantix at its peak generated more than $1 billion in annual global revenue and made it to the top of the smoking-cessation category for nearly a decade. Zyban (bupropion), the previous incumbent in the late 1990s and early 2000s, peaked at several hundred million dollars before being supplanted. If cytisinicline captures even a fraction of the historical Chantix franchise, the implied valuation for a single-asset commercial-stage biotech in the current market environment looks substantial relative to where the stock trades today. Equally, if the drug stalls — through regulatory delay, payer pushback, or weak prescriber adoption — the equity could compress sharply, as the company has no diversified revenue base to fall back on.

The three KPIs that, in my view, will matter most to any long-term investor in Achieve over the next twenty-four months are: (1) the PDUFA outcome and the specific contents of the approved label, particularly with respect to treatment duration and the vaping indication; (2) the gross-to-net pricing trajectory and formulary coverage achieved in the first four quarters post-launch, which together will define the early commercial slope; and (3) the operational reliability of the Sopharma supply relationship, including any disclosures about inventory positioning, dual sourcing, or contract extensions. These are the variables that, more than any others, will determine whether the cytisinicline story compounds into a category franchise or sputters into a niche specialty product.

X. Epilogue: From Folk Remedy to Modern Medicine

Imagine, if you can, the strangeness of the journey this molecule has taken. A plant alkaloid first isolated in nineteenth-century European pharmacology, rediscovered by Soviet-bloc chemists who needed something cheap and domestic to help their workers quit smoking, commercialized in a single Bulgarian factory under a brand sold across the Warsaw Pact, ignored by Western pharmaceutical giants for half a century, finally noticed by a Pacific Northwest biotech entrepreneur who saw what the incumbents missed, packaged through a reverse merger with a failed oncology shell, advanced through two pivotal trials at exactly the moment the dominant prescription competitor imploded, expanded into an entirely new indication for an addiction that did not exist when the drug was discovered — and now sitting, in late May 2026, less than a month from an FDA decision that could redefine the smoking-cessation market.

There is a useful way to think about companies like this, borrowed from the venture capital framework of "non-consensus and right." The bullish case for Achieve is not the consensus case. The consensus on smoking-cessation drugs has been negative for two decades — a slow-growth, side-effect-laden corner of primary care that nobody at the major pharmaceutical companies wanted to staff with their best people. The case for cytisinicline requires believing that the market has been mispriced because the incumbent imploded and the patient population has changed, and that a plant-based mechanism with a sixty-year safety record can do what synthetic chemistry could not. That is, almost by definition, a contrarian thesis. Whether it is also a correct one will be answered, in part, by an FDA letter dated June 20, 2026.

What is undeniable is that Achieve Life Sciences sits at the intersection of three of the most interesting structural forces in modern pharmaceuticals: the rediscovery of natural-product drug discovery, the regulatory empowerment of breakthrough designations, and the strategic vacuum created when an incumbent franchise collapses. Each of those forces, taken alone, would make for an interesting case study. Stacked together, they form the kind of asymmetric setup that defines this category of small-cap biotech investing.

The Bulgarian foragers harvesting laburnum pods this spring almost certainly do not know that the molecule inside those pods will, in the coming weeks, be the subject of an FDA decision that could reshape an American therapeutic category. The chemists in Sofia who modernized Tabex's extraction process across decades of communist and post-communist Bulgaria probably do not realize that their accumulated process knowledge is the most valuable cornered resource in a NASDAQ-listed company half a world away. And the patients who, if cytisinicline is approved, will eventually pick up a prescription at a CVS in Cleveland or a Walgreens in Phoenix will almost certainly never know that the active ingredient in their tablet was first identified in a Soviet-era pharmacopoeia. That is, in some sense, exactly the point. Good drugs do not need their patients to know their origin stories. The origin story is for the investors.

And the investors, right now, are watching a clock count down to June 20.

References

-

Smoking Cessation Market Size and Share — Fortune Business Insights ↩↩

-

Comparing Cytisine and Varenicline for Smoking Cessation — New England Journal of Medicine, 2021-07-15 ↩

-

Comparing Cytisine and Varenicline — New England Journal of Medicine, 2021-07-15 ↩

-

Phase 3 ORCA-2 Results — JAMA Internal Medicine, 2023-07-11 ↩

-

Cytisinicline for Vaping Cessation (ORCA-V1) — American Journal of Medicine, 2024 ↩↩

-

Achieve Life Sciences Announces $124.2 Million Financing — GlobeNewswire, 2024-02-29 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube