Arch Capital Group Ltd.: The Underwriting Machine

I. Introduction & Episode Roadmap

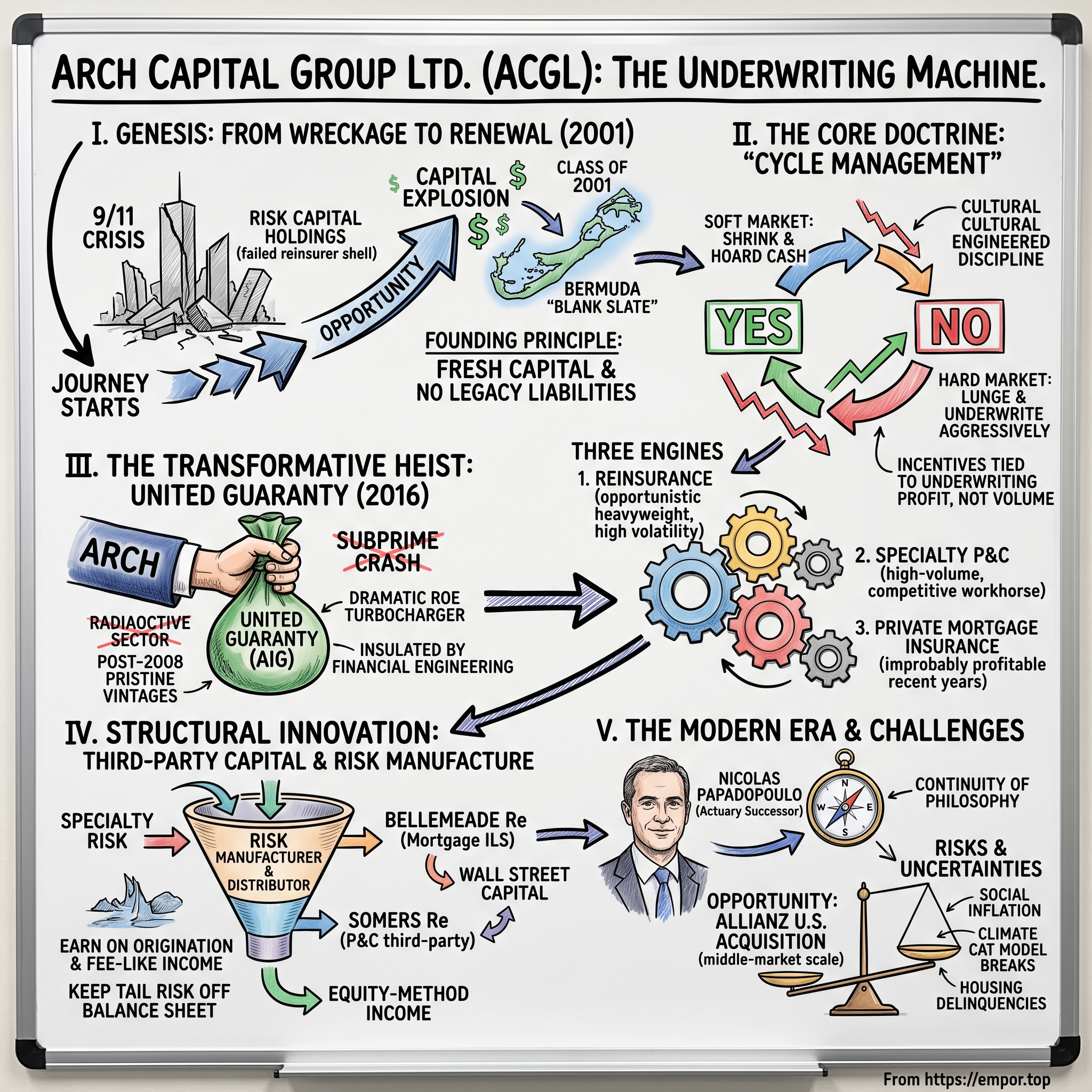

Start with a number that sounds like a typo. Since it began underwriting in late 2001, Arch Capital Group has grown its book value per share — the single figure its own management treats as the scoreboard of the entire enterprise — at a compound annual rate in excess of 15 percent, a pace it has now sustained for the better part of twenty-five years.20 In the insurance industry, where the average company is lucky to earn its cost of capital across a full cycle, that is not a good result. It is an aberration. Compounding at 15 percent for a quarter-century turns one dollar into roughly thirty. In the most recent stretch the pace has been faster still: book value per share rose 22.6 percent in 2025 alone.17

Here is the part that makes it strange. The company that produced this record was, in the year 2000, essentially a corpse. It was the stripped-down shell of a failed reinsurer called Risk Capital Holdings, a business that had tried and given up. There was no famous founder, no proprietary technology, no consumer brand. There was a Bermuda mailing address, a securities listing, and a small amount of leftover capital. What Arch had — the only thing it had — was the option to start over with a blank sheet of paper at exactly the moment the insurance world was thrown into its deepest crisis in a generation.

That crisis was September 11, 2001. And out of the smoke came a peculiar opportunity that a small group of insurance veterans understood better than almost anyone: when catastrophe destroys enough of the industry's capital, the survivors and the newcomers can charge whatever they want. Arch raised three-quarters of a billion dollars, hired an underwriting dream team, and pointed it at the richest pricing environment in decades. That is the origin story. The harder question — the one this episode is really about — is how a company keeps compounding for twenty-five years after the crisis that birthed it has faded, when its industry is a brutal, cyclical commodity business that periodically incinerates the naive.

The answer Arch would give you has three parts, and they map to three engines. The first is Specialty Property & Casualty Insurance — the workhorse, high-volume, competitive, and lower-margin. The second is Reinsurance — the opportunistic heavyweight that scales up violently when catastrophe pricing spikes and shrinks when it doesn't. The third, and the one that turned Arch from a good insurer into a great compounder, is Private Mortgage Insurance — a business so improbably profitable in recent years that it has, at times, thrown off as much underwriting profit as the reinsurance arm on roughly one-seventh the premium. Binding all three together is a single doctrine that Arch repeats like a catechism: cycle management. The willingness, culturally engineered and financially incentivized, to shrink a business and hoard cash when the price of risk is too low, and to lunge when it is high.

This is a company that has literally acquired crown jewels from distressed sellers at the bottom of their cycles — buying AIG's private mortgage-insurance business, United Guaranty, for $3.4 billion in 2016 when the sector was still radioactive from the subprime crash,4 and absorbing Allianz's U.S. middle-market book in 2024.7 It has pioneered financial structures — the Bellemeade Re mortgage insurance-linked notes — that let it sell its scariest tail risk directly to capital-market investors.12 And in October 2024 it handed the keys to a new chief executive, an actuary who has been there since almost the first day, in a succession designed to change absolutely nothing about the philosophy.9

So the roadmap. We begin in the wreckage of 2001 and the Bermuda "blank slate" that made Arch possible. We dissect the cycle-management doctrine and the uncomfortable, un-copyable discipline it demands. We tell the story of the United Guaranty heist and ask whether Arch was brave or lucky. We take apart the three engines and the startling asymmetry of their margins. We explain how Arch sells its risk to Wall Street through Bellemeade Re. We examine the modern succession and the Allianz bet. And then we put the whole thing on the rack — the bull case, the bear case, and the specific things that could break it — because a business historian's job is not to applaud a compounding streak but to ask, coldly, whether it can continue. As management itself conceded on the most recent earnings calls, the market has turned soft, competition is intensifying, and Arch is now writing less in the places that made it rich.2021 That tension is the whole show. Let's start at the beginning, in the fall of 2001.

II. The Genesis: The Class of 2001 & Bermuda's Blank Slate

Picture the insurance industry in the last week of September 2001. The Twin Towers had fallen two weeks earlier, and beyond the human catastrophe, the financial one was still being tallied. The attacks would become the largest insured man-made loss in history to that point — a bill split across property insurers, life insurers, aviation carriers, workers'-compensation writers, and, above all, reinsurers, the companies that insure the insurers. In a single morning, the industry's carefully modeled assumptions about how much correlated loss could strike at once were exposed as fantasy. Capital that had taken years to accumulate evaporated in hours.

When capital vanishes in insurance, something mechanical happens: price explodes. Insurers set premiums against the capital they hold to pay claims, so when a cataclysm destroys capital, the remaining capacity becomes scarce and precious. Rates that had been grinding lower through a long, sleepy "soft market" in the late 1990s suddenly rocketed upward. Terrorism cover, which had been quietly bundled into commercial policies for free, was abruptly carved out and repriced. Reinsurance rates leapt. This was the beginning of one of the hardest markets — insurance jargon for the most seller-favorable pricing environment — in living memory. And into a hard market, the most valuable thing you can bring is fresh, unencumbered capital.

Money knew where to go. It went to Bermuda. The self-governing British island in the North Atlantic had, over the preceding two decades, built itself into the natural habitat for opportunistic insurance capital. Its appeal was a specific and unglamorous cluster of features: a regulator that could authorize a new carrier in weeks rather than years, a legal system rooted in English common law, tax neutrality that meant underwriting profits were not skimmed before they could compound, and a location within a short flight of New York and a manageable one of London. When the industry needed new capacity fast in late 2001, Bermuda was the only place that could stand up new balance sheets at the speed the moment demanded. The wave of carriers that formed there in the months after 9/11 earned a permanent nickname: the Class of 2001. Roughly ten new insurers raised on the order of $8.9 billion of fresh equity to fill the capacity gap.2 The names — Arch, Allied World, AXIS Capital, Endurance, Montpelier Re — would define Bermuda's reinsurance market for the next two decades.

Arch's particular path to that starting line was cleverer than a from-scratch launch. Rather than build a company from zero, a group of insurance financiers recognized that they could pour new capital into an existing, publicly listed but essentially dormant shell — Risk Capital Holdings — and thereby skip the plumbing of a fresh listing. The architects were Robert Clements, a revered insurance-industry dealmaker who had helped midwife earlier Bermuda start-ups, and Peter Appel, who took the operating reins as president and chief executive. In November 2001 they closed an equity raise of roughly $763 million, anchored by two of the most respected private-equity names in financial services, Warburg Pincus and Hellman & Friedman.122 The capital was earmarked to build two underwriting platforms at once — a specialty insurance operation and a reinsurance operation — and to do so with a balance sheet carrying no history.

That last point was the entire strategic thesis, and it deserves a beat. Arch's established competitors were not just older; they were haunted. Decades of underwriting meant decades of accumulated liabilities — asbestos and environmental claims from policies written in the 1970s and 1980s, workers'-compensation tails, mispriced casualty business whose losses would keep bleeding for years. A legacy insurer entering the 2002 hard market was, in effect, driving into a gold rush while towing a trailer full of old debts. Arch had no trailer. Every dollar of premium it wrote was priced at the new, punishingly attractive post-9/11 rates, and every dollar of loss it would pay lay in the future, under its own control. It was a pure-play bet on the best pricing in a generation, unencumbered by the sins of the past.

Capital and a clean slate are necessary but not sufficient; you need people who can price risk. Arch assembled a remarkable bench. To run the primary insurance business, it recruited Constantine "Dinos" Iordanou — universally known as Dinos — a Cyprus-born, NYU-trained aerospace engineer who had backed into insurance at AIG in the 1970s, done a stint at Berkshire Hathaway's commercial-casualty operation, and then run Zurich's North American business.3 Iordanou was the operational general: blunt, numbers-driven, a builder of underwriting cultures. He would succeed Appel as chief executive in 2003 and run Arch for the next decade and a half, the defining leadership figure of its rise.3 His engineering background was not incidental to his management style — he approached an insurance company the way an engineer approaches a system, obsessed with how the incentives, the capital, and the underwriting talent fit together as a mechanism rather than a collection of parts. The people who worked for him describe a leader who wanted underwriters to think like owners of their own book, accountable for its profitability rather than its size, and who was willing to lose an account, a quarter, or a year of growth to make the point stick. That temperament — impatient with vanity metrics, comfortable with saying no — was arguably the single most important thing Arch built in its first decade, more valuable than any particular line of business, because it was the thing that could not be bought. When Iordanou eventually stepped back and Grandisson, and later Papadopoulo, took over, the continuity of that temperament was the whole ballgame. To build the reinsurance book, Arch brought in the veteran reinsurance underwriter Paul Ingrey in October 2001.1 And among the younger talent laying the actuarial and analytical foundations was Marc Grandisson, a French-Canadian actuary who would spend the next seventeen years climbing toward the top job himself.

It is worth pausing on why the private-equity structure mattered, because it shaped Arch's temperament. Warburg Pincus and Hellman & Friedman were not passive check-writers looking for a quick flip; they were sophisticated financial investors who understood that the value in a start-up insurer is created by not deploying capital foolishly in the early innings. A public company under quarterly pressure to show premium growth might have written aggressively from day one to justify its existence. Arch, backed by patient institutional capital and led by people who had seen the cycle turn, had the luxury and the temperament to wait for the right risks. That patience — the ability to sit on capital without apologizing for it — became a permanent feature of the culture, and it is visible two decades later in a management team that would rather hand billions back to shareholders than write business at inadequate rates.22

What this founding cast shared was a worldview. They had all watched the industry's cycles chew up companies that confused growth with success. They built Arch, from day one, as a machine designed to do the opposite — to expand only when the math worked and to retreat, without apology, when it didn't. That discipline sounds obvious. It is, in practice, one of the hardest things in corporate life to execute, and it is where the real story of Arch begins.

III. The Underwriting Doctrine: "Cycle Management" & The Power of "No"

To understand why cycle management is difficult, you have to first accept an unflattering truth about insurance: at its core, it is a commodity. A dollar of coverage from Arch pays claims exactly like a dollar of coverage from a competitor. There is no brand loyalty in a reinsurance treaty, no switching cost that locks a cedent in forever, no proprietary molecule. And commodities priced by many competitors are prone to a specific, recurring pathology — the underwriting cycle.

The cycle works like a slow, destructive tide. When the industry is flush with capital and losses have been mild for a few years, insurers grow restless. Capital sitting idle earns nothing, and the temptation to deploy it — to write more business — becomes overwhelming. So carriers compete for market share the only way a commodity seller can: by cutting price. Rates drift down. Terms loosen. Underwriters, paid and promoted on how much premium they bring in, keep writing because the alternative is watching a rival take the account. This is the "soft market," and it feels wonderful right up until the losses arrive — because the business written at those thin rates was never priced to survive a bad year. When the bad year comes, the industry discovers it has been underpricing risk for a half-decade. Capital gets destroyed, capacity retreats, and prices snap violently upward into a new hard market. Then the whole thing begins again.

Most insurers are passengers on this tide. They grow in soft markets because everyone else is growing and Wall Street rewards the premium line, and then they take their beating when the cycle turns. Arch's founding proposition was that a company could instead be a navigator — deliberately shrinking into soft markets and expanding into hard ones. On the surface this is just "buy low, sell high" applied to risk. In practice it requires an organization to do something that runs against every human and institutional instinct it has.

Consider what cycle management actually demands of an underwriter. In a soft year, Arch's leadership may effectively tell a talented professional: your job this year is to write substantially less business than last year, walk away from accounts you have serviced for a decade, and watch competitors underprice you and take them. At most companies, that instruction is career poison. The underwriter's compensation, status, and internal power are tied to the size of the book. Tell your best people to shrink and they will either quietly ignore you or leave for a rival that lets them grow. This is why cycle management, though endlessly praised in insurance conference rooms, is so rarely executed: the strategy is not intellectually hard, it is culturally hard. It requires rewiring the incentives of the entire organization.

That rewiring is the actual moat, and it is worth being precise about the mechanism because it is the closest thing Arch has to an un-copyable advantage. Arch pays its underwriters for underwriting profit, net of the cost of the capital they consume — not for premium volume. Management has stated the principle repeatedly and plainly. On the fourth-quarter 2025 call, the doctrine was recited almost as scripture: leverage a diversified platform to stay flexible, use data and analytics to sharpen risk selection, and, critically, "rewarding our underwriters for profitability, not volume, and incentivizing our executives to grow book value per share above all else."20 When a person's bonus shrinks if they write bad business, telling them to walk away from bad business stops being a fight. That is what turns a slogan into a repeatable process — what the strategist Hamilton Helmer would call Process Power, an advantage embedded so deeply in how an organization operates that a rival cannot copy it without rebuilding its own culture and compensation from the studs.

There is a second Helmer power at work, subtler and more perishable: a Cornered Resource in the form of the concentrated cluster of actuarial and underwriting talent Arch assembled and retained through its long expansion. Pricing specialty risk well is not a commodity skill; it is judgment built over cycles, and Arch has kept an unusual amount of that judgment in-house for two decades. The flexibility this enables is central. Arch does not run its three engines as sealed silos competing for capital; it runs them as one portfolio, moving capacity toward wherever the risk-adjusted return is highest. When reinsurance pricing is spectacular, capital floods to reinsurance. When primary specialty lines harden, it flows there. The 2025 and early-2026 earnings calls are a live demonstration: with property-catastrophe reinsurance rates falling 10 to 20 percent at the January renewals, Arch's reinsurance team was deliberately writing less cat and hunting for casualty and specialty opportunities elsewhere, while its finance chief noted that the historically dominant reinsurance engine was, for the first time in years, no longer clearly the most attractive of the three.2021

This is the right place to fact-check the consensus narrative that surrounds Arch, because even admirers tend to overstate it. A number that circulates widely — and that appeared in the very brief that framed this story — is that Arch has grown book value per share at "roughly 20 percent" annually since inception. That is not what the company's own records show. Management's stated figure is a compound annual growth rate in excess of 15 percent since 2001, a number it repeats on its calls and in its annual reports.20 The distinction is not pedantry. Fifteen percent for a quarter-century is already an elite, top-of-peer-group result; inflating it to twenty percent conflates the recent, cycle-flattered stretch — book value grew 22.6 percent in 2025 and management has enjoyed a run of hard markets and benign catastrophes — with the durable, through-the-cycle rate.17 The reality is arguably more impressive than the myth, because 15-percent-plus compounding across multiple soft markets and the 2008 financial crisis reflects genuine discipline, not a lucky window. An investor who anchors on twenty percent is quietly assuming the good years are the normal years. They are not, and Arch's own management is careful never to claim they are.

Does the discipline actually show up in results, or is it just a good story management tells? The most honest test is behavior in soft markets, when the temptation to chase premium is strongest. Arch's own current conduct is the evidence: in the softening market of 2025–2026, the company chose to shrink property-catastrophe writings and return capital to shareholders rather than defend its top line, buying back $1.9 billion of stock in 2025 and another $783 million in the first quarter of 2026.1719 On the Q1 2026 call, chief executive Nicolas Papadopoulo framed it exactly as the doctrine would predict — the willingness "to dynamically add to areas where returns are attractive while declining those risks that no longer provide an adequate margin of safety."21 Whether that discipline holds through an entire soft cycle is the open question every long-term investor in Arch is really underwriting. But the behavior on display is at least consistent with the claim, which is more than most of the industry can say. And the clearest proof that the discipline pays came not from saying no, but from a single audacious yes — the deal that remade the company.

IV. The Transformative Heist: The United Guaranty Acquisition

In 2016, if you had proposed to a room of property-casualty insurance executives that they buy a large U.S. private mortgage insurer, you would have been met with something between a wince and a laugh. Mortgage insurance was the sector that had detonated. Private mortgage insurers — the companies that guarantee lenders against loss when a borrower with a small down payment defaults — had been at the epicenter of the 2008 subprime collapse. Several went insolvent or into runoff. The product looked like the definition of un-investable: a business whose entire fortune was chained to the direction of the U.S. housing market, capable of years of fat profits followed by a single apocalyptic wipeout. Traditional carriers wanted nothing to do with it.

Which is precisely why the opportunity existed. The largest private mortgage insurer in the country, United Guaranty Corporation, was owned by American International Group — AIG, the insurance colossus that the U.S. government had bailed out in 2008 and that spent the following years dismantling itself to repay the debt and, later, to satisfy activist investors. By 2015 and 2016, the activist Carl Icahn was publicly agitating for AIG to break itself apart and streamline, and AIG's chief executive, Peter Hancock, was under pressure to simplify a sprawling empire. United Guaranty, profitable but non-core and capital-hungry, was exactly the kind of asset a shrinking AIG would sell. It put UGC on the block.

Arch stepped up. On August 15, 2016, it agreed to acquire United Guaranty in a deal valued at roughly $3.4 billion.4 The structure was telling: about $2.2 billion in cash, plus roughly $1.2 billion in newly issued preferred and convertible preferred stock — a mix that let Arch fund the purchase without straining its balance sheet or diluting common holders more than modestly.5 To manage the risk of UGC's older policies, AIG agreed to retain a 50 percent quota share on business written in 2014 through 2016, effectively keeping half of the most recently underwritten legacy exposure on AIG's own books.5 The transaction closed at the end of 2016, and it instantly made Arch the largest private mortgage insurer in the world, adding a book with more than $180 billion of primary insurance in force.46

The skeptics had a clear thesis: Arch was buying into the most dangerous tail risk in insurance — the U.S. housing market — at what looked like a cyclical peak, seven years into a housing recovery. Were they simply catching a falling knife on a delay? The bear case was not stupid. It was just, as it turned out, looking at the wrong book.

Here is the insight Arch priced correctly and the market didn't. A mortgage insurer's risk is not a single blob; it is a stack of vintages, and the vintages could not have been more different. United Guaranty's genuinely toxic exposure — the loans underwritten in the reckless years before 2008 — had, by 2016, largely run off, been paid down, or been reinsured away. What remained and what UGC was still writing was post-2009 business, and post-2009 U.S. mortgage underwriting was arguably the most conservative in the nation's history. In the wake of the crisis, regulators and the government-sponsored enterprises had forced documentation, down-payment, and credit standards to levels that made the mid-2000s look like a fever dream. Arch was not buying the 2006 housing market. It was buying a portfolio of pristine, tightly underwritten, high-credit-quality mortgages that happened to sit inside a sector everyone else still associated with 2008. It paid a modest premium for what was, functionally, a cash machine wearing a leper's coat.

It is worth sitting with the "did they overpay?" question honestly, because with hindsight it is tempting to call the deal an obvious steal, and it was not obvious at the time. Arch paid roughly $3.4 billion for a business whose future depended on a variable — U.S. home prices — that no underwriter could control and that had, within living memory, fallen off a cliff. A disciplined skeptic in 2016 would have argued that Arch was violating its own creed by taking on precisely the kind of concentrated, macro-driven tail risk it had spent fifteen years avoiding, and paying a full price to do it near a housing peak. The structure of the deal is what answers the charge: the mix of cash and preferred and convertible securities limited the immediate strain and the common-share dilution, AIG's retained quota share on the most recent legacy vintages kept half of the freshest tail off Arch's books, and — critically — Arch had already built the Bellemeade Re machinery that would let it sell the catastrophic layer to outside investors.512 Arch was not betting the company on housing. It was buying a high-return cash stream and had a pre-existing tool to cap the downside. That is the difference between a value trap and a value buy: not the discount, but the plan for the risk.

The payoff came fast, and it reframed the entire company. Rising U.S. home prices meant that even when a borrower defaulted, the accumulated equity in the home often covered the loss, so realized claims stayed extraordinarily low. Default rates fell. Prior reserves set aside for losses that never materialized were released back into earnings. Within a few years the mortgage segment was generating profit at a scale that dwarfed the price Arch had paid, and it became a permanent, high-margin capital engine humming underneath the more volatile insurance and reinsurance operations. The United Guaranty deal is the hinge of the whole Arch story: the moment a disciplined but conventional Bermuda underwriter acquired the asset that would let it compound at a rate very few financial companies ever achieve. To see why, you have to look at the almost comic asymmetry of the three engines' economics — which is where we go next.

V. Segment Deep Dive: The Financial Disproportion

There is a single statistic that captures why Arch is unusual, and it comes from the mortgage business. In the insurance world, performance is measured by the combined ratio — the sum of claims and expenses divided by premiums earned. A combined ratio of 100 percent means you broke even on underwriting before investment income; 95 percent is very good; the low 90s across a cycle marks a genuinely excellent property-casualty franchise. In 2024, Arch's mortgage segment posted a combined ratio of 12.6 percent.16

Read that again. It means that for every dollar of premium the mortgage business earned, it paid out fewer than thirteen cents in claims and expenses combined. The other eighty-seven cents was underwriting profit. There is essentially no other line in mainstream insurance that does this. The figure is not sustainable at that exact level — it was flattered by benign losses and by the release of reserves that had been set conservatively in prior years — and indeed it drifted up to 14.6 percent in 2025 as those tailwinds normalized.18 But even a "normalized" mortgage combined ratio in the teens or twenties is a staggering economic engine. To make the point concrete: in full-year 2024 the mortgage segment produced $1,094 million of underwriting income on just $1,112 million of net premiums written — very nearly a dollar of profit for every dollar of premium.16

Now set that beside the other two engines, using the audited 2024 figures. The Specialty P&C Insurance segment — the largest by premium — wrote $6,874 million in net premiums and generated $345 million of underwriting income at a combined ratio of 94.8 percent.16 This is the high-volume, lower-margin workhorse. It competes in crowded markets, carries genuine primary-claims exposure, and is exposed to the slow poison of "social inflation" — the tendency of jury awards and legal settlements to rise faster than general inflation, inflating casualty losses years after a policy is written. A combined ratio in the mid-90s here is a solid, professional result. It is not a miracle.

The Reinsurance segment is the volatile heavyweight. In 2024 it wrote $7,746 million of net premiums and threw off $1,222 million of underwriting income at an 83.2 percent combined ratio.16 Reinsurance is where Arch takes on property-catastrophe risk, specialty treaties, and marine and aviation exposure — business that can produce spectacular margins in years without a mega-catastrophe and brutal losses in years with one. This is the engine that scales most dramatically with the cycle. When catastrophe rates spiked in 2023 and 2024 after years of costly hurricanes and wildfires, Arch poured capital into reinsurance, and the segment delivered a record $1,558 million of underwriting income in 2025 on a combined ratio of 80.8 percent — its best since 2016.1718 Then, true to the doctrine, as 2026 renewals softened by double digits, Arch began pulling back.20

Line the three up and the disproportion is the whole point. The mortgage engine, with roughly one-seventh the premium of reinsurance, has in recent years generated a comparable slug of underwriting profit — around a billion dollars a year, four years running.17 It is the highest-return, lowest-volatility, most capital-efficient of the three, and it was bought, not built, from a distressed seller. This is why the United Guaranty deal was transformative rather than merely additive: it did not just add a segment, it added the segment with the best economics in the whole company.

There is a fourth contributor that the three-segment framing can obscure, and it has quietly grown into a serious earner: the investment portfolio. Every insurer holds a pool of premiums and reserves before it pays claims, and it invests that pool for its own account. Arch's investable assets crossed $47 billion by the end of 2025, and the portfolio generated $434 million of net investment income in the fourth quarter alone, with additional income flowing in from equity-method affiliates.1718 For years, when interest rates were pinned near zero, this engine was an afterthought — a bond portfolio grinding out low-single-digit yields. The return of higher interest rates changed that arithmetic completely: a large, short-duration, high-quality fixed-income portfolio reinvesting at meaningfully higher yields throws off a materially larger and more predictable stream of income than it did a decade ago, and that income drops almost straight to book value. Management has been deliberate about keeping the portfolio conservative — short duration, high credit quality, limited exposure to the private-credit assets that have lured many peers reaching for yield — which means the investment engine is built to be a steady tailwind rather than a source of surprise losses.21 It is a reminder that Arch's compounding is not one trick but the sum of several: disciplined underwriting across three segments, plus an investment book that has gone from bit player to genuine contributor.

The deeper strategic function of that mortgage profit is what management and analysts sometimes describe as a synthetic float engine. Traditional insurance "float" is the pool of premium an insurer holds before it pays claims, which it invests for its own account — the mechanism Warren Buffett made famous. Arch's mortgage segment does something adjacent: it generates such reliable, high-margin cash that it functions as a permanent internal capital cushion. That cushion matters because of when it is available. It lets Arch lean aggressively into hard reinsurance and specialty markets — writing more risk exactly when pricing is richest — without having to run to the public markets to raise dilutive equity at the worst possible moment. The company funds its own opportunism. On the recent calls, with all three engines generating cash and few attractive places to deploy it, that surplus was flowing straight back to shareholders through buybacks rather than being stockpiled.21 But an investor should hold one caution firmly in mind: the mortgage engine's serenity is a function of a strong housing market and rising home prices. Its combined ratio has been low because borrowers rarely default and, when they do, home equity absorbs the loss. That is a benign-environment result, not a law of nature — which is exactly why Arch went to such lengths to offload the segment's worst-case risk, the subject of the next section.

VI. Structural Innovation: Third-Party Capital & Bellemeade Re

The mortgage segment poses an obvious, uncomfortable question that Arch's own risk managers surely asked themselves the day the United Guaranty deal closed: what happens to the whole company if the U.S. housing market crashes? The segment that generates a billion dollars a year in a good environment is, by its nature, the segment most exposed to a catastrophic one. A severe recession with soaring unemployment and falling home prices — the 2008 scenario — could turn that cash machine into a claims machine, and because mortgage credit risk is highly correlated (defaults cluster in downturns), the losses would arrive all at once. Concentration risk of this kind is precisely what can turn a great business into a solvency event.

Arch's answer was one of the more elegant pieces of financial engineering in modern insurance, and it is worth explaining carefully because it is central to how the mortgage engine earns its outsized returns. The vehicle is called Bellemeade Re, and the instruments it issues are mortgage insurance-linked notes.12 The mechanics, stripped of jargon, work like this. Arch takes a large pool of the mortgage risk it has insured and sets up a special-purpose reinsurance company. That company sells bonds — the insurance-linked notes — to global capital-market investors: pension funds, hedge funds, specialist credit investors. The cash those investors pay in is held in trust as collateral. In normal times, the investors earn an attractive yield. But if mortgage defaults in the covered pool spike beyond a defined threshold, the trust's collateral is used to pay Arch's claims, and the investors lose principal. In effect, Arch has sold the peak, catastrophic layer of its mortgage risk directly to Wall Street. Since the program's launch around 2015, it has grown into one of the largest of its kind, with more than twenty transactions and roughly $9 to $10 billion of notes issued protecting hundreds of billions of dollars of insured mortgages.1213

The genius of the structure is that it solves two problems at once — one about survival, one about returns. The survival problem is obvious: by ceding the tail to third parties, Arch caps the damage a housing crash can inflict on its own balance sheet. The returns problem is subtler and involves a regulatory mechanism worth understanding. Private mortgage insurers in the U.S. operate under a capital regime called PMIERs — the Private Mortgage Insurer Eligibility Requirements — which dictates how much capital an insurer must hold against its risk in force to remain an approved counterparty of the government-sponsored enterprises. Capital held is capital that cannot be deployed elsewhere or returned to shareholders, and it is the denominator in return on equity. When Arch cedes risk to Bellemeade Re, it reduces the risk it retains, and therefore reduces its required PMIERs capital.12 Less trapped capital against the same stream of profit means a dramatically higher return on the equity actually at risk. This is the hidden turbocharger under the mortgage segment's headline combined ratio: the reported profitability is high, and the capital efficiency behind it is higher still. The newest deals have grown sophisticated enough to tie their credit protection directly to the PMIERs capital calculation.13

Arch has applied the same philosophy — using other people's capital to write more business while shielding its own balance sheet — on the property-casualty side, though with a more complicated history. The relevant vehicle here traces back to Watford Re, a Bermuda "total-return" reinsurer Arch helped establish in 2014, in which third-party investors supplied capital that Arch's underwriters put to work, earning Arch management and underwriting fees while the outside investors bore much of the risk. (A note on the record, since the vehicle is easy to garble: in 2021 Arch, alongside Warburg Pincus and Kelso, took Watford Holdings private and rebranded it as Somers Re — it was not, as is sometimes reported, renamed "Vignette Re," an entity that does not exist.14) Somers appears in Arch's results today as an operating affiliate that contributes equity-method income; on the fourth-quarter 2025 call, management noted a "very good quarter at Somers Re."20 The strategic logic is the same across both the mortgage and P&C structures: Arch increasingly earns money not only by bearing risk on its own balance sheet, but by originating and managing risk on behalf of outside capital, collecting fees, and keeping the tail off its own books.

There is a broader pattern here that is easy to miss if you think of Arch only as a company that bears risk. Increasingly, Arch is also a company that manufactures and distributes risk — originating exposures with its underwriting expertise and then parceling out the pieces to whoever is best suited to hold them, whether that is Arch's own balance sheet, a Bellemeade Re note buyer, or a Somers Re third-party investor. This is a meaningfully different and more capital-efficient business model than the traditional buy-and-hold insurer, and it earns Arch a stream of fee-like income and ceding economics on top of pure underwriting profit. It also aligns neatly with the cycle-management doctrine: when Arch's own return thresholds say a risk is not worth holding, it can sometimes still be worth originating and passing on. The limitation is that this model only works as long as outside capital wants the risk on terms that leave Arch a margin — and that appetite, as management noted repeatedly on recent calls, is itself deeply cyclical.21

The honest analytical caveat is that risk transfer is not risk elimination. Bellemeade Re protects against defaults beyond a threshold, but Arch retains the first layer of mortgage losses — the losses that arrive first in any downturn. And third-party capital is fair-weather capital: it is abundant and cheap when results are good and can retreat quickly when they sour, exactly when Arch would most want it. Still, the structures are real, they are large, and they materially change the risk profile of the company's most concentrated exposure. Having built these machines, the question for the modern era became who would run them — and whether a new generation could keep the discipline intact while pushing into riskier new terrain.

VII. The Modern Era: The Succession & The Allianz Bet

Marc Grandisson's tenure as chief executive, which began in March 2018, was a study in what happens when a disciplined machine meets a favorable cycle. Over roughly the next six and a half years, Arch rode a hardening property-catastrophe market, integrated and harvested the United Guaranty acquisition, and compounded book value at a pace that put it near the top of the entire financial sector. The scoreboard, as later tallied in a press release announcing Grandisson's appointment to another company's board, was a total shareholder return of 298 percent over his tenure — about 23.2 percent annualized — against 144 percent for the S&P insurance index over the same span.11 For a business as commoditized as insurance, roughly doubling the sector's return over more than half a decade is the kind of outperformance that gets a chief executive remembered.

So the succession announced on October 14, 2024, mattered. Grandisson retired from the company, and the board handed the top job to Nicolas Papadopoulo.9 (It is worth correcting a common misreading here: Grandisson did not slide into an executive-chairman perch to keep his hand on the wheel — he left.9) A retirement of a chief executive who has just delivered sector-crushing returns is always a moment of risk for shareholders, because so much of a great insurer's edge lives in its culture and its people rather than its assets. The reassuring signal, in Arch's case, was that the successor was not an outsider brought in to shake things up but the ultimate insider brought in to change nothing.

Consider Papadopoulo's résumé, because it is almost a caricature of what Arch values. He is a French-trained actuary of the highest pedigree — a graduate of the École Polytechnique, France's most elite engineering school, and of ENSAE, its premier statistics and economics institute — and, before entering the industry, he served as an insurance examiner with the French Ministry of Finance.910 He joined Arch's Bermuda reinsurance operation in December 2001, at the very founding, and spent the next two decades running first the reinsurance group and then the worldwide insurance group before becoming president and chief underwriting officer.10 In other words, the company promoted a career actuary who had personally helped build both of its major underwriting platforms and who embodies, in his very training, the data-driven, cycle-managed, return-on-equity discipline that is the firm's entire identity. This is succession engineered explicitly for continuity — the opposite of a strategic pivot. The bet the board made is that Arch's edge is a system, not a single leader, and that handing the system to one of its architects preserves it. Whether that is right is unprovable in advance; the early evidence, in the form of Papadopoulo's Q4 2025 and Q1 2026 calls, is a management team reciting the identical doctrine of profitability-over-volume and cycle discipline, almost word for word, that Grandisson used.2021

The clearest test of the new era's judgment is the acquisition that closed just before the handover. On April 5, 2024, Arch's North American insurance arm agreed to buy Allianz's U.S. MidCorp and Entertainment insurance businesses — the middle-market commercial and specialty-entertainment books written through Allianz's Fireman's Fund operation — for $450 million in cash.7 The deal closed on August 1, 2024, moving roughly 500 employees and a book that had generated about $1.7 billion of gross written premium in 2023 into Arch.78 The headline price undersells the scale of the commitment: because Arch was assuming an in-force book of complex commercial risk along with its associated legacy loss reserves, it estimated it would need to back the business with roughly $1.4 billion of its own capital.7 The purchase price was a down payment; the real cost was the balance sheet Arch had to put behind it.

The first full quarters under the new leadership offered a useful window into how the era would actually be run, and the tone was strikingly unemotional. In the first quarter of 2026, Arch earned $2.50 per share of after-tax operating income and a 15.4 percent operating return on average common equity — a strong result, but one delivered into a visibly softening market, with reinsurance rates falling and competition intensifying across property lines.1921 Rather than reaching for growth to mask the softening, management leaned the other way: it repurchased $783 million of stock in the quarter, disclosed that the board had increased the share-repurchase authorization by $3 billion, and reiterated that its first priority is to deploy capital into the business only when returns clear its threshold, and to return the rest.21 Papadopoulo's framing on that call could have been lifted verbatim from a Grandisson or Iordanou script: Arch's "25-year record of strong returns and compounding book value at double-digit rates is a direct result of hard work and discipline. That is Arch. That is our DNA." Whether such continuity is reassuring or complacent is a fair debate, but there is no ambiguity about the intent — this is a management team that has defined its job as protecting a system rather than reinventing one.

The strategic rationale is a genuine departure worth scrutinizing. For most of its life, Arch has been a specialty underwriter — a picker of niche, hard-to-price risks — rather than a broad middle-market commercial insurer competing for the workaday coverage needs of mid-sized American companies. The Allianz deal pushes it decisively into that larger, more mainstream arena, with the logic that Arch can cross-sell its specialty products to a new base of corporate customers and build a scaled middle-market franchise that is less violently cyclical than catastrophe reinsurance. But middle-market commercial insurance is exactly the terrain where social inflation does its damage, and Arch was voluntarily assuming a large book of prior-year reserves covering accident years stretching back to 2016 — reserves set by a different company under different assumptions. If those old reserves prove inadequate in an era of nuclear jury verdicts and rising medical costs, Arch will have bought someone else's underwriting mistakes and will pay for them through future reserve strengthening. The bull reading is that Arch's superior claims-management and analytics will wring high-margin profit out of a book a bloated European insurer under-managed. The bear reading is that it bought a legacy problem. On the Q1 2026 call, management offered a revealing tell about how it is treating the acquisition: it had already identified program business inside the Allianz book that did not meet Arch's return thresholds and was deliberately non-renewing it, a move it said would reduce net premium by roughly $250 million across 2026 — and it framed the astonishingly fast 18-month systems migration of the acquired business, aided by artificial intelligence, as a strategic milestone.21 That is cycle-management discipline applied to an acquisition: keep the profitable business, shed the rest, integrate fast. Whether it produces the low-90s combined ratio management hopes the book can eventually run at is a story that will unfold over years, not quarters.20

VIII. The Investment Spine: "Why Win" vs. "Why Not"

Put Arch under the kind of scrutiny a skeptical long-short investor or an activist would bring, and the debate organizes itself into a clean confrontation between a durable-moat bull case and a set of genuine, non-trivial risks. The point of the exercise is not to declare a winner but to identify the specific evidence that would move the argument in either direction.

The bull case rests on three load-bearing pillars, each of which has real evidence behind it. The first is the cycle-management moat already dissected — the compensation-engineered, culturally embedded discipline of writing for profit rather than volume, which shows up as combined ratios that beat the industry through the cycle and, more tellingly, as the willingness to shrink and return capital in a soft market rather than chase premium.1721 The second is the mortgage cash cow, structurally insulated by Bellemeade Re, generating a billion dollars a year of the highest-quality underwriting profit in the company at a capital efficiency few can match.1218 The third is dynamic reinsurance scale — the ability, funded by internal cash, to deploy billions into hardening catastrophe markets at the top of the cycle and pull back at the bottom, which is exactly what the 2023–2026 sequence demonstrated in real time.1820

Run this through Hamilton Helmer's framework and the powers are identifiable but not all equally durable. Process Power (the cycle-management culture) is the strongest and hardest to copy. The Cornered Resource of accumulated underwriting talent is real but perishable — people retire, and the succession from Grandisson to Papadopoulo is, in part, a wager that the institution outlasts the individuals. What Arch conspicuously lacks are the powers that protect consumer franchises: there is no network effect, no meaningful switching cost binding a cedent to Arch, no brand that lets it charge more for identical coverage. Its advantage is entirely on the cost-of-risk and discipline side of the ledger, not the demand side.

Porter's five forces sharpen the same picture. Barriers to entry in reinsurance are genuinely high — you need a strong balance sheet, agency ratings that take years to earn, specialized actuarial talent, and deep broker relationships — which is why the Class of 2001 required a catastrophe and three-quarters of a billion dollars to break in. But rivalry among established players is ferocious and, crucially, price-based during soft phases, because the product is a commodity and capital is mobile. That is the force pressing on Arch right now. And there is a newer entrant to the rivalry: third-party and "alternative" capital — the pension and hedge-fund money that flows into catastrophe risk through insurance-linked securities and reinsurance sidecars. On the recent calls, management repeatedly cited exactly this dynamic as the driver of softening property-catastrophe and casualty pricing, noting that the strong industry results of recent years had "attracted significant new capacity from traditional markets and third-party capital."21 Alternative capital lowers the barriers that used to protect underwriters like Arch, and its persistence is the single biggest structural question hanging over the reinsurance engine.

The bear case, then, is not a caricature; it is three concrete ways the machine could grind. The first is Allianz integration and reserve risk: Arch has taken on a large book of legacy middle-market reserves in the teeth of social inflation, and if those reserves prove light, the write-downs would land directly on book value — the very metric the whole company is optimized around.7 The second is a fundamental break in catastrophe modeling. Arch's reinsurance engine assumes it can price the frequency and severity of natural catastrophes; if climate change is shifting the behavior of "secondary perils" — wildfires, severe convective storms, inland flooding — faster than the models can recalibrate, the segment could face successive years of losses that were supposed to be improbable. Management's own commentary betrays the tension: it now speaks of monitoring roughly fifty separate catastrophe zones individually and pulling back where returns have deteriorated, which is prudent, but it is prudence operating on models that a skeptic would argue are chronically behind the physics.21 The third is the housing downturn that the entire Bellemeade edifice is built to survive but not to profit through. Bellemeade Re absorbs the peak, but Arch retains the first-loss layer, and a genuine housing credit crisis — high rates, high unemployment, falling prices — would compress the mortgage segment's underwriting income toward zero even in the scenario where the structure works as designed. The billion-dollar engine is a fair-weather engine.

A modern risk radar has to include technology, and here the picture is genuinely two-sided. On the threat axis, artificial intelligence could commoditize parts of the insurance value chain — automating underwriting for simple, high-volume lines and empowering distribution platforms that disintermediate carriers. Management's response, offered when the stock swooned on AI fears, was that specialty insurance is complex enough that models will take time to replicate seasoned underwriters, and that Arch is more likely a net beneficiary of AI-driven efficiency than a victim of it.20 That is a self-interested answer, but not an unreasonable one — the messy, judgment-heavy risks Arch specializes in are precisely the ones hardest to automate, and Arch put the claim to a concrete test by using AI to compress the systems migration of the acquired Allianz book into eighteen months.21 On the opportunity axis, AI also creates risk to underwrite: cyber insurance is a fast-growing Arch line, and management has openly flagged that AI accelerates both the scale and speed of cyberattacks, raising the systemic, correlated tail risk in that book — a risk it says it is approaching cautiously.21 The honest read is that AI is neither the existential threat the market briefly feared nor the pure tailwind management prefers to emphasize; it is a genuine, unresolved variable that cuts in several directions at once.

There is also an activist-style stress test worth voicing, if only to dismiss part of it fairly. A critic could attack the portfolio complexity — three quite different businesses under one Bermuda holding company — as a conglomerate discount waiting to happen, and could question a capital-allocation record that includes a $1.9 billion special dividend in December 2024 followed by heavy buybacks, as evidence of a company with more capital than ideas.16 The steel-manned rebuttal is that the diversification is the point — the three engines are deliberately uncorrelated so capital can rotate to the best risk-adjusted return, which is the opposite of undisciplined diworsification — and that returning capital when underwriting opportunities are scarce is textbook discipline, not desperation. On the calls, analysts pushed management directly on why it didn't return even more, and the finance chief's answer — that the capital "is in our pockets, it's not burning anything," and that returns would follow opportunity rather than a target — reads as candid rather than evasive.20 Governance sits on the right side of the ledger too: executives are incentivized on multi-year book-value-per-share growth and return on equity rather than premium volume, with high stock-ownership requirements and prohibitions on hedging or pledging that force management's wealth to ride the same risks as common shareholders.20 The credible version of the bear case, in the end, is not that Arch is badly run. It is that Arch is superbly run in a business whose fundamental economics — commodity pricing, mobile capital, and tail risks that resist modeling — put a ceiling on how long any discipline can hold out against a rising tide of competition. That is the honest tension, and no framework resolves it in advance.

IX. Playbook: Key Lessons for Founders & Investors

Strip the Arch story down to its transferable principles and three lessons stand out, each of which generalizes well beyond insurance.

The first is the bravery to say no to revenue. In any cyclical, commodity-like business — and there are many, from memory chips to shipping to oil services — the deepest competitive advantage is not a clever product but the institutional willingness to shrink when pricing is bad and to hoard the capacity for when it is good. This is hard precisely because it is unnatural: growth is celebrated, retreat is punished, and the pressure to keep the machine running at full volume is relentless. Arch's achievement was to make the retreat structural — to pay its people for profit rather than volume so that saying no stopped being an act of individual courage and became the default behavior of the system. The lesson is that discipline you have to summon will fail under pressure; discipline you have engineered into incentives survives it.

The second lesson is non-consensus M&A structured to mitigate risk. The United Guaranty acquisition worked not merely because Arch bought a distressed, out-of-favor asset cheaply — plenty of value investors do that and get killed by the reason it was cheap. It worked because Arch understood the asset better than the market (the toxic vintages had run off; the remaining book was pristine) and because it wrapped the residual risk in modern hedging machinery like Bellemeade Re that let it keep the profit while shedding the tail. The transferable insight is that buying what others fear is only half the trade; the other half is having a specific, structural mechanism to neutralize the risk that made the asset cheap in the first place.

The third lesson is to align incentives with value, not scale. It is astonishing how many businesses — and not just insurers — reward their leaders for the size of the enterprise: revenue, assets under management, headcount, market share. Size is easy to grow and almost always available for purchase, which is exactly why it is a corrupting target. Arch tied executive compensation to multi-year growth in book value per share and return on capital, which are far harder to fake and far more aligned with what a long-term owner actually cares about.20 The result is a management team that treats the balance sheet as a scarce resource to be allocated rather than a war chest to be spent, and that will return capital to shareholders rather than deploy it badly. For any investor evaluating a management team, the compensation structure is not a footnote; it is a prediction of behavior.

None of these lessons is a formula for guaranteed success — the same discipline that protects Arch in a soft market also caps its growth, and the same conservatism that avoids blowups also forgoes the occasional home run. But together they describe a coherent, repeatable philosophy for compounding capital in a hostile, cyclical industry, which is rarer and more valuable than any single brilliant decision.

X. Epilogue & KPIs to Watch

For all the moving parts in Arch's three engines, an investor trying to track whether the twenty-five-year machine is still working can watch a very small number of things and safely ignore the rest.

The first and most important is growth in book value per share. Arch's management has said, in as many words, that this is the metric it manages the company to and rewards its executives on, and it is the cleanest single measure of value creation for a business whose product is turning underwriting profit and investment income into compounding equity.20 The relevant question is not any single year — 2025's 22.6 percent was flattered by a benign catastrophe year and strong markets — but whether Arch can sustain double-digit compounding across a full three-to-five-year cycle, including the soft years it is now entering.17 A durable slide below double digits, sustained across a cycle rather than a single hard-loss year, would be the first hard evidence that competition has finally caught the machine.

The second is the property-casualty combined ratio, measured against peers. The absolute number matters less than the spread: Arch's entire claim to a moat is that it underwrites more profitably than the industry through every phase of the cycle. In normal years, an investor should look for a P&C combined ratio comfortably under the mid-90s, and in catastrophe-heavy years, for Arch to lose less than the industry — outperforming the pack by a wide margin when everyone is bleeding. If that relative outperformance narrows during the current soft market, it would suggest the cycle-management discipline is eroding under competitive pressure, exactly the risk the bear case identifies.1821

The third, narrower gauge is the health of the mortgage engine — specifically the delinquency rate on the U.S. mortgage-insurance book and the cushion of excess capital above the PMIERs requirement. Because this segment is both the highest-return and the most macro-sensitive of the three, its delinquency trend is the earliest warning system for the one scenario that could genuinely dent the company: a housing downturn. Management now reports the figure each quarter; it sat around 2.06 percent in the first quarter of 2026, consistent with a still-healthy housing market.21 A sustained climb in that number, paired with softening home prices, is the signal that the fair-weather engine is heading into weather.

Arch enters its second quarter-century in a genuinely interesting position: at the top of its game, with record profits and a management team reciting an unchanged philosophy, but staring into a softening market where its greatest strengths — discipline, patience, the willingness to write less — will be tested in the least glamorous way possible. The company was born from a catastrophe that let it charge high prices, and it made its fortune by understanding cycles better than its competitors. The next several years, as pricing falls and capital floods in, will reveal whether the underwriting machine is truly a system that compounds through any weather, or whether it, too, has a cycle. For a business built entirely on the discipline of saying no, the hardest test is not the hard market. It is the soft one now arriving — and, unusually for this industry, it is a test Arch has spent twenty-five years preparing to pass.

References

-

The 9/11 Attacks & Bermuda's Class Of '01 — Bernews, 2011-10 ↩

-

Arch Capital Group Ltd. to Acquire United Guaranty Corporation — Arch Capital / Business Wire, 2016-08-15 ↩↩↩

-

AIG Reaches Agreement to Sell United Guaranty Corporation to Arch Capital for US$3.4 Billion — Canadian Underwriter, 2016-08-17 ↩↩↩

-

Arch Capital Completes United Guaranty Acquisition — Insurance Journal, 2017-01-04 ↩

-

Arch Insurance North America to Acquire Allianz's US MidCorp and Entertainment Insurance Businesses — Arch Capital, 2024-04-05 ↩↩↩↩↩

-

Arch Insurance North America Acquires Allianz's US MidCorp and Entertainment Insurance Businesses — Arch Capital, 2024-08-01 ↩

-

Arch Capital Group Ltd. Announces Leadership Transition — Arch Capital, 2024-10-14 ↩↩↩↩

-

Papadopoulo to Succeed Grandisson as Arch CEO — Reinsurance News, 2024-10-15 ↩↩

-

Howard Hughes Holdings Appoints Former Arch Capital CEO Marc Grandisson to Company's Board of Directors — Howard Hughes Holdings / GlobeNewswire, 2026-04-20 ↩

-

Insurance-Linked Notes (Bellemeade Re) — Arch Mortgage ↩↩↩↩↩↩

-

Arch secures $199.3m Bellemeade Re 2025-1 mortgage ILS issuance — Artemis, 2025 ↩↩

-

Arch Relaunches Watford Re as Somers Re — Arch Capital, 2021-11-04 ↩

-

Arch Capital Group Ltd. Reports Fourth Quarter and Full Year 2024 Results (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2025-02-10 ↩

-

Arch Capital Group Ltd. Q4/FY2024 Financial Supplement (Form 8-K, Exhibit 99.2) — SEC EDGAR, 2025-02-10 ↩↩↩↩↩

-

Arch Capital Group Ltd. Reports Fourth Quarter and Full Year 2025 Results (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2026-02-09 ↩↩↩↩↩↩↩↩

-

Arch Capital Group Ltd. Q4/FY2025 Financial Supplement (Form 8-K, Exhibit 99.2) — SEC EDGAR, 2026-02-09 ↩↩↩↩↩↩

-

Arch Capital Group Ltd. Reports First Quarter 2026 Results (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2026-04-28 ↩↩

-

Arch Capital Group Q4 2025 Earnings Call Transcript — Seeking Alpha, 2026-02-10 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Arch Capital Group Q1 2026 Earnings Call Transcript — Seeking Alpha, 2026-04-29 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube