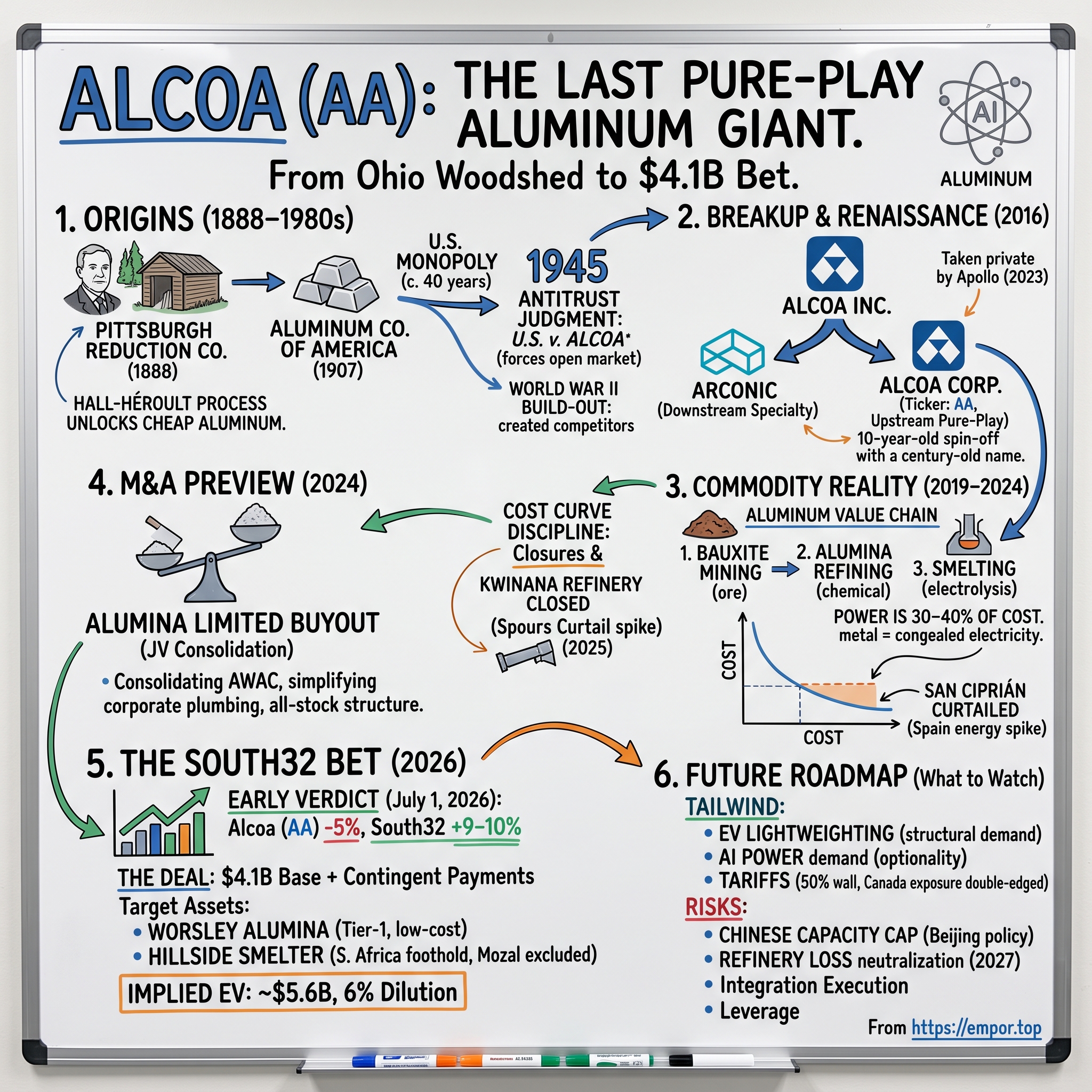

Alcoa: The Last Pure-Play Aluminum Giant Bets Big

I. Introduction & Episode Roadmap

On the morning of July 1, 2026, aluminum traders in Sydney watched two stocks move in opposite directions with unusual conviction. Shares of South32, the Australian miner spun out of BHP a decade earlier, jumped roughly 9–10% in early trading. Shares of Alcoa, the American company that had effectively invented the modern aluminum industry, fell about 5%.23 The two moves told a single story: Alcoa had agreed to buy South32's entire bauxite-alumina-aluminum chain, and the market's first instinct was that the seller had gotten the better end of the trade.

The headline number was $4.1 billion — a base price of roughly $3.1 billion in cash plus about 17 million newly issued Alcoa shares worth around $1.0 billion.3 But layer in up to $750 million of contingent payments tied to future metal prices, plus assumed liabilities and site-remediation obligations, and the implied enterprise value climbed toward $5.6 billion.12 For a company with a market capitalization that spends most of its life bouncing between $6 billion and $12 billion depending on where the London Metal Exchange price sits on any given Tuesday, this was not a bolt-on. It was the largest acquisition in Alcoa's life as a stand-alone upstream producer — its second multi-billion-dollar consolidation move in three years.

Here is the tension worth sitting with for the next two hours. Alcoa is 137 years old. It was, for the first half of the twentieth century, so completely synonymous with aluminum that a federal court had to legally pry the market open because one company controlled essentially all of it. Then it spent the back half of its life diversifying into a sprawling industrial conglomerate, got itself broken in two in 2016, and emerged as a "pure play" — a company that does one thing, makes one metal, and lives or dies by a commodity price it cannot control. For most of the last decade, its entire investment thesis has been discipline: closing high-cost smelters, curtailing money-losing refineries, and refusing to chase growth for its own sake. Management has built real credibility on that story.

And now it is growing again — through acquisition, with borrowed money and diluted shares, into a business with no pricing power. So which is it? Is the South32 deal the logical capstone of a decade of cost-curve discipline — buying tier-one assets that lower Alcoa's position on the global cost curve? Or is it the moment a management team, flush with the cash flow of a cyclical peak, quietly reverts to the empire-building instincts that got the old Alcoa broken up in the first place?

Before we walk the arc, it's worth puncturing the central myth, because it distorts how many investors approach the stock. The myth is that Alcoa is aluminum — a blue-chip industrial titan, a proxy for American manufacturing might, a company with the pricing power and market position its brand implies. The reality is almost the opposite: today's Alcoa is a roughly ten-year-old, mid-sized, price-taking commodity producer with no pricing power, a portfolio it is constantly pruning, and earnings that can swing from a large loss to a large profit in the space of two years without management changing a single strategy. The famous name is a century-old inheritance, not a description of the modern business. Getting that gap right — between the brand's aura and the business's actual economics — is the first and most important act of analysis on this company.

To answer the discipline-versus-empire question, this article walks the full arc: the origin story of how one company became aluminum; the 2016 breakup that actually created the company trading today; the brutal, unforgiving economics of a commodity business where power is 30–40% of your cost; the operating discipline of the Oplinger era; the 2024 Alumina Limited buyout that was the dress rehearsal for this; the South32 bet itself; the competitive landscape and where Alcoa really sits on the cost curve; and finally the bull and bear cases, the KPIs that matter, and the lessons. Let's start at the beginning — with a chemistry experiment in an Ohio woodshed.

II. Origins: How One Company Became "Aluminum" (1888–1980s)

In 1886, in a woodshed behind his family home in Oberlin, Ohio, a 22-year-old chemistry graduate named Charles Martin Hall passed an electric current through a bath of molten cryolite in which he had dissolved aluminum oxide, and watched small buttons of pure aluminum settle at the bottom of his crucible.14 It sounds unremarkable now. It was, at the time, close to alchemy. Aluminum is the most abundant metal in the earth's crust, but it never occurs in pure form — it clings to oxygen with a ferocity that had made it, for most of the nineteenth century, more precious than gold. Napoleon III reputedly reserved aluminum cutlery for his most honored guests and made everyone else use silver. Hall's electrolytic process — discovered, in one of history's great coincidences, almost simultaneously by Paul Héroult in France, which is why metallurgists call it the Hall-Héroult process — was the key that unlocked cheap aluminum.14

Two years later, in 1888, Hall and a group of Pittsburgh investors founded the Pittsburgh Reduction Company to commercialize it.15 The economics were seductive and they remain, in their essential shape, the economics of the business today: turn cheap electricity and processed ore into a light, corrosion-resistant, infinitely recyclable metal. In 1907 the company renamed itself the Aluminum Company of America; the contraction "Alcoa" followed a few years later and eventually became the legal name.15 For roughly the next forty years, Alcoa didn't compete in the American aluminum market. It was the American aluminum market.

That near-total control ended not through competition but through the courts. In a landmark 1945 decision — United States v. Aluminum Co. of America — Judge Learned Hand ruled that Alcoa had illegally monopolized the domestic aluminum market, a ruling that reshaped American antitrust doctrine and forced the industry open to rivals like Reynolds and Kaiser.16 It is a piece of trivia that turns out to matter enormously for the modern thesis: this is a business whose competitive structure has always been shaped as much by government action — antitrust, tariffs, capacity caps — as by any operating decision a manager ever made. Keep that in your pocket; we'll return to it.

There's a second reason to linger on that antitrust chapter, beyond the legal precedent. World War II had turned aluminum into a strategic material — you cannot build an air force without it — and the wartime buildout of smelting capacity, much of it financed by the U.S. government, is what created the post-war competitors that finally ended Alcoa's monopoly. The lesson embedded there is one that recurs across the whole story: aluminum has always sat at the intersection of industrial policy and national security, which is precisely why governments keep intervening in it. A metal that goes into fighter jets, power grids, and food packaging is never going to be left purely to the market.

Through the Cold War decades, Alcoa did what almost every great American industrial did in that era: it diversified. It moved downstream and sideways into packaging (the aluminum can — Alcoa was central to the mid-century revolution that replaced steel cans and glass bottles with light, cheap, recyclable aluminum), building products, aerospace components, and forged aluminum wheels for trucks. By the 2000s the company that the public still thought of as "the aluminum company" had quietly become something else — a diversified manufacturer whose profits leaned heavily on fabricated and engineered products rather than the raw metal. The brand said commodity; the P&L increasingly said specialty manufacturing. It was, in the language of a later era of activist investors, a company whose parts were probably worth more than its whole.

That gap between identity and reality is the setup for everything that follows. Because a company that is really two businesses — a cyclical commodity producer bolted to a higher-margin engineered-products maker — is a company that eventually attracts a very specific question from investors and bankers: why are these two things inside the same building? That question got its answer in 2016.

III. The 2016 Break: Becoming a Pure-Play Producer

By the middle of the 2010s, Klaus Kleinfeld — the German-born former Siemens chief who had run Alcoa since 2008 — was presiding over a company caught in a strategic contradiction. Aluminum prices were weak. The upstream smelting business was capital-hungry and cyclical. Meanwhile the downstream engineered-products division, selling into aerospace and automotive, was growing, higher-margin, and valued by investors on completely different multiples. Holding both together meant the market applied a mediocre blended valuation to the whole and rewarded neither. The conglomerate discount had come for aluminum.

The solution was surgery. On November 1, 2016, Alcoa Inc. split itself into two independent, publicly traded companies.9 The value-add, downstream manufacturing business kept the corporate lineage and took a new name: Arconic. The upstream business — bauxite mining, alumina refining, aluminum smelting, and casting — was spun off into a newly created entity that took the old, storied name: Alcoa Corporation. Shareholders received one share of the new Alcoa for every three shares they held, in a distribution structured to be tax-free.9

Pause on the irony, because it's delicious. The company that got to keep the famous name was the commodity smelting business — the oldest, most capital-intensive, most cyclical part of the enterprise. The glamorous, higher-margin manufacturing arm had to invent a name nobody had ever heard. It was a signal about where management thought the identity truly lived, even as the financial logic pointed the other way.

Here is the operationally important fact for anyone analyzing "Alcoa" today: the company trading under the ticker AA is not the 137-year-old original. It is the roughly ten-year-old spin-off. Its financial history, its balance sheet, its management incentives, and its entire strategic self-conception date from November 2016. When you pull up a long-run chart, you are looking at a decade-old commodity producer wearing a century-old name.

The intellectual case for the split was the standard "pure-play" argument, and it's worth stating fairly because it is the mirror image of the question hanging over the South32 deal. The theory holds that focused companies get valued more accurately and managed more sharply than sprawling conglomerates: specialist investors can own exactly the exposure they want, management stops cross-subsidizing weak divisions with strong ones, and each business gets a capital-allocation discipline suited to its own economics. A cyclical commodity smelter and a growth-oriented aerospace-parts maker have almost nothing in common as investments; forcing shareholders to own them as a bundle served neither. Splitting them was, in that framing, an act of clarity.

Did the separation logic actually pay off? The cleanest test is what happened to the other half. Arconic, the downstream business, went on to be taken private by the private-equity firm Apollo Global Management in 2023 — the classic end state for a mature manufacturing asset that public markets had stopped loving. The split, in other words, ultimately let each half find its natural owner: the commodity producer stayed public and cyclical, the specialty manufacturer went private. Here is the irony worth flagging for later, though: a company created in 2016 on the premise that focus and simplicity create value has spent the years since 2024 growing larger and more complex through acquisition. That is not necessarily a contradiction — you can be a focused pure-play and still get bigger within your lane — but it is a tension a careful investor should keep in view. For the pure-play Alcoa that remained, the separation set up the only game it would play from then on — and it is a genuinely hard one. To understand why the last decade of Alcoa's story is dominated by closures rather than growth, you have to understand the economics of the business it was left holding.

IV. The Economics of Aluminum: Why This Is a Hard Business

Imagine you run a business with three brutal characteristics at once. First, your main product is a globally traded commodity whose price is set on an exchange in London, and you have no ability to charge a penny more than that price — a customer choosing between your aluminum ingot and a Russian or Chinese one is choosing on price and logistics, full stop. Second, your single largest variable cost is electricity, which can run 30–40% of the cash cost of producing a tonne of metal, and you consume it in staggering quantities — an aluminum smelter is essentially a machine for converting electric power into metal. Third, your assets cost billions and take years to build, and once a smelter's molten "pots" are running you cannot easily switch them off without enormous cost and damage. You are a price-taker with a huge fixed cost base and an enormous, inflexible power bill. Welcome to aluminum.

Let's walk the value chain, because each step has different economics. It starts with bauxite, a reddish ore mined from the ground, largely in tropical regions like Western Australia, Guinea, and Brazil. Bauxite gets refined into alumina (aluminum oxide, a white powder) in large chemical refineries using the Bayer process — dissolving the ore in hot caustic soda, then precipitating out purified alumina — an energy- and heat-intensive step, and the one where Alcoa has historically been most exposed to swings in both energy prices and caustic soda costs. It typically takes roughly four to five tonnes of bauxite to make two tonnes of alumina, and two tonnes of alumina to make one tonne of aluminum, so the whole chain is a funnel: enormous volumes of rock at the top, a comparatively thin stream of finished metal at the bottom. Alumina is then fed into smelters, where the Hall-Héroult process — the same electrochemistry from that Ohio woodshed — passes a massive electric current through cells (the "pots") to strip the oxygen away and produce molten aluminum, which is finally cast into ingots, slabs, and billets. Roughly speaking: bauxite is a mining business, alumina is a chemical-refining business, and smelting is an electricity-arbitrage business. Alcoa spans all three, which is both a source of integration advantage and a reason its earnings can be whipsawed at multiple points in the chain at once.

The electricity point deserves dwelling on, because it is the single fact that explains most of the industry's geography and strategy. A modern aluminum smelter running at full tilt draws power on the scale of a small city — which is why smelters are almost never built near their customers and almost always built next to cheap, abundant power: hydroelectric dams in Canada, Norway, and Brazil; historically cheap coal or gas elsewhere. The metal, in a real sense, is just a way of storing and shipping electricity in solid form. Aluminum is sometimes called "congealed electricity," and that is not a metaphor — it is the business model. It also explains why a smelter is so painful to switch off: the molten cryolite bath inside each pot must be kept hot and liquid, and if you let a pot "freeze," restarting it can mean rebuilding it. That inflexibility is why the decision to curtail a smelter is such a high-stakes, semi-permanent act — and why the managers who are willing to make it are so valuable.

Because Alcoa is a price-taker, the only two levers that truly matter are where its cost sits on the global cost curve and how much metal it can produce. There is no brand premium, no pricing power, no switching cost locking in a customer. This is where it's worth applying the frameworks investors reach for — Michael Porter's Five Forces and Hamilton Helmer's 7 Powers — honestly rather than flatteringly. Bargaining power of buyers? High; they can buy identical metal anywhere. Threat of substitutes and rivalry? Intense and global. Supplier power? Real, especially for power and, increasingly, for tier-one bauxite. Of Helmer's seven durable power types — scale economies, network effects, counter-positioning, switching costs, branding, cornered resources, and process power — most simply don't apply to a commodity producer. The one that does is cornered resource: owning genuinely advantaged, low-cost, long-life assets — a tier-one bauxite deposit, a legacy hydroelectric power contract signed decades ago at a price no one could get today. That is the closest thing to a moat this industry offers, and it is exactly the logic that will drive the South32 deal.

It's worth being concrete about what "no pricing power" actually feels like on the ground, because investors coming from software or consumer businesses often underestimate how total it is. When Alcoa sells a tonne of aluminum, the base price is whatever the LME three-month contract says it is at that moment — a number set by traders in London reacting to Chinese production data, global inventory levels, and macro sentiment, none of which Alcoa influences. The only slivers of price Alcoa can add are regional premiums (the extra buyers pay for physical metal delivered to, say, the U.S. Midwest rather than an LME warehouse) and product premiums (a bit more for a value-added billet versus a raw ingot). Those premiums matter at the margin — and tariffs feed directly into them — but they are toppings, not the meal. The meal is the LME price, and it belongs to the market. A company in this position cannot decide to earn more; it can only decide to cost less. That is the entire strategic universe.

There is one structural feature working in Alcoa's favor, and it is, fittingly, a government-imposed one. China produces well over half the world's aluminum, but Beijing has for years enforced an effective capacity ceiling of roughly 45 million tonnes on its domestic smelting industry — part of a broader push under 双碳 dual-carbon goals to curb energy-intensive, high-emission industries.12 Because aluminum smelting is so power-hungry and China's grid is still heavily coal-fired, capping smelting capacity is also climate policy. For non-Chinese producers, that cap functions as a supply governor on the world's dominant player — a structural tailwind that, again, no Alcoa manager created or controls.

So the honest takeaway is this: aluminum is a cost-curve business, not a differentiated one. You do not win by being loved; you win by being cheap, by owning great rocks and cheap power, and by having the discipline to shut down the parts of your portfolio that are neither. Which means the entire fundamental story reduces to two questions — what does Alcoa own, and how well does it manage the cost curve? Let's open the business up.

V. Inside the Business: Two Segments, One Balance Sheet

Alcoa reports through two segments, and the way their revenue splits tells you something subtle about the company's shape. In fiscal 2025, total revenue was $12.8 billion, up about 8% year over year.4 The Aluminum segment generated roughly $8.4 billion of third-party sales and the Alumina segment about $3.7 billion.4 But that third-party split undersells how alumina-heavy the company really is, because a large share of Alcoa's alumina never leaves the building — it's produced by the refining segment and consumed internally by its own smelters. Alcoa is, in truth, one of the world's largest bauxite and alumina producers that also happens to smelt; the metal you see in the revenue line rests on an upstream base of ore and refined powder that the company mostly feeds to itself.

The backbone of that upstream position is a joint venture with a wonderfully bureaucratic name: AWAC — Alcoa World Alumina and Chemicals. For decades, AWAC's bauxite mines and alumina refineries were owned 60% by Alcoa and 40% by a separately listed Australian company called Alumina Limited, whose entire reason for existing was to hold that 40% stake. It was an arrangement that leaked value: minority partners in a joint venture take their share of the cash flow and complicate every decision. So in 2024, in what would turn out to be a preview of everything that followed, Alcoa bought Alumina Limited outright in an all-stock deal, completing the acquisition on August 1, 2024 and taking full ownership of its own upstream engine.6 The deal was valued in the low-single-digit billions, and it was CEO Bill Oplinger's first major capital call.

Study the logic of the Alumina Limited buyout, because it is the Rosetta Stone for the South32 deal. Alcoa didn't buy an unfamiliar business in an unfamiliar geography. It bought out a minority partner in a joint venture it already operated and understood intimately. The risk was almost entirely financial (did we pay the right price?) rather than operational (can we run this?). It also simplified the corporate plumbing: no more sharing AWAC's cash flows and decisions with an outside shareholder, no more of the friction that comes from a joint venture where partners can disagree about when to curtail, when to invest, and how much to distribute. Management's pitch — that consolidating known JV stakes is the lowest-risk form of M&A a commodity producer can do — is a genuinely defensible one, and it's the template they would reach for again. The all-stock structure also mattered: rather than draining cash or loading up on debt at the bottom of a cycle, Alcoa paid Alumina Limited's shareholders in its own paper, effectively inviting them to stay along for the ride. Whether that was the right template to scale up dramatically two years later, with a cash-heavy check at what looked like a cyclical top, is exactly the question the market started asking in mid-2026.

Now for the number that should be tattooed on the forehead of anyone tempted to extrapolate: net income was $1,157 million in 2025, versus just $60 million in 2024, versus a loss of roughly $651 million in 2023.4 Same assets. Same management. Same strategy. The swing from a $651 million loss to a $1.16 billion profit in 24 months is not a story about execution; it is a story about the LME aluminum price and the alumina price moving in Alcoa's favor. On a per-share basis, 2025 delivered $4.42 of net income and about $3.77 on an adjusted basis, against a paltry $0.26 in 2024.4 Return on equity of roughly 16% in 2025 looks like a fine business — until you remember it followed a year of near-breakeven and a year of outright loss.

There's a subtler point buried in that earnings volatility that's easy to miss. Because Alcoa is integrated across bauxite, alumina, and aluminum, its earnings don't just swing with one price — they swing with the relationship between prices at each stage. When alumina prices spike (as they did in periods of the recent cycle, partly on supply disruptions), Alcoa's refining segment feasts, but its own smelters have to pay more for the alumina they consume, muddying the picture. Integration is a hedge in some conditions and a double-exposure in others. This is why reading Alcoa off a single LME chart is a trap: the company sits at several points on the chain at once, and the spreads between those points move independently. It is genuinely harder to model than a pure smelter or a pure miner would be.

The analytical conclusion is unavoidable and it colors the entire rest of this story: 2025 was a cyclical peak, not a baseline. Any assessment of the South32 acquisition — the leverage it adds, the returns it promises — has to be stress-tested against the possibility that the cash flows financing it evaporate when the cycle turns. Management knows this better than anyone, which is why the credibility they've built matters so much. And that credibility was built in the down-cycle, closing things.

VI. Discipline in the Down-Cycle: Curtailments, Closures, and Credibility (2019–2024)

The most important thing to understand about Alcoa's management culture cannot be found in a growth chart. It's found in the list of things they've turned off. In a price-taker business, the highest-value skill is not building — it's the willingness to shut down an asset that is losing money, absorb the write-offs and the union grief, and take the metal off the market. It is unglamorous, it is politically painful, and it is the entire ballgame.

Through the late 2010s, Alcoa built a track record of doing exactly that. It curtailed capacity at high-cost smelters — Wenatchee in Washington State, several Spanish operations — when power economics made them uneconomic. Each closure followed the same cold logic: if a smelter's all-in cost sits above where the LME price is likely to trade through the cycle, keeping it running is just a slow way of setting cash on fire. The discipline was in the saying no — resisting the temptation, common in commodity firms, to keep every plant open for the sake of volume, jobs, and political goodwill.

The San Ciprián complex in Spain became the clearest test of nerve. Facing punishing European energy prices — the same energy crisis that hammered European industry broadly after natural gas prices spiked — Alcoa held the line, keeping capacity curtailed from late 2023 until the power economics could justify a restart rather than reflexively firing the smelter back up to please politicians and unions. This is harder than it sounds. A curtailed smelter in a small town is a political grenade: hundreds of jobs, a local economy built around the plant, national governments that view domestic aluminum as strategic infrastructure and lean hard on the company to keep it running. The temptation to restart prematurely — to trade shareholder cash for political goodwill — is constant. The restart, when it eventually came, was framed as conditional and economics-driven, structured with government and energy-supply support rather than offered as a favor. That's the behavior investors reward: a management team treating each plant as a financial decision rather than a birthright, and negotiating from the position that it will not run a loss-making asset simply because closing it is unpopular.

But the sharpest illustration — and the one that best tests whether the "we act on the cost curve" story is real — is Kwinana. The Kwinana alumina refinery in Western Australia had become a persistent money-loser; the company curtailed it in 2024 after flagging a pretax loss on the order of $130 million tied to the facility.8 The human cost was real and Alcoa did not hide it: a workforce that had numbered around 800 was cut in stages, first to a few hundred and eventually to a skeleton crew, as the curtailment hardened into a permanent closure decision announced in 2025.7 There was no pretense that the refinery might come back. Management called it: the asset was uncompetitive, it was gone, and the restructuring charges were taken.

This is the evidentiary foundation for the entire Alcoa investment narrative. When management says "we allocate capital on the cost curve," the Kwinana and San Ciprián decisions are Exhibit A that they mean it — that they will take the pain of closure rather than subsidize a losing asset. It's a genuinely credible record, and it should earn management the benefit of the doubt.

But credibility earned by closing things does not automatically transfer to buying things — they are almost opposite skills. A team that has spent a decade proving it can subtract has, by definition, not proven it can add. Which is exactly the lens to bring to the person who now has to do both: the CEO who built his reputation as the discipline guy is the same CEO now writing the biggest check in company history.

VII. Current Management: The Oplinger Era

William "Bill" Oplinger is not a charismatic outsider brought in to shake things up. He is the opposite — a finance-trained lifer who has been inside Alcoa's numbers for the entire life of the pure-play company and longer. He was there at the 2016 spin-off as the new company's Chief Financial Officer, the person who built the balance sheet the standalone Alcoa was launched with. He became Chief Operating Officer in 2023, and then, in September 2023, he stepped up to Chief Executive Officer.5 The path — CFO to COO to CEO — matters. This is a leader who understands the company as a spreadsheet first and an operation second, which is both his great strength and the thing a skeptic should watch most closely.

That financial DNA shows up in how Oplinger talks. On Alcoa's earnings calls his register is unfailingly operational and numeric — production records, cost per tonne, net-debt targets — rather than visionary. On the Q1 2026 call in April, with the world economy rattled by a Middle East conflict that was inflating freight and diesel costs, his framing was characteristically flat and controlled: "Execution matters, and we are delivering," and, pointedly, "the conflict has not changed our capital allocation framework."5 That is the voice of a man who wants investors to see him as a steady hand on the cost curve, not a dreamer.

Alongside him sits CFO Molly Beerman, whose role has become central precisely because the South32 deal is fundamentally a financing and balance-sheet problem. On the same Q1 call, Beerman laid out a capital-allocation hierarchy that is worth quoting because it is the yardstick against which the South32 deal should be measured: fund operational sustainability first, then drive net debt down into a target range of roughly $1.0–1.5 billion, and only then evaluate returns to shareholders.5 It is a conservative, deleveraging-first framework — which makes the decision to take on a multi-billion-dollar acquisition, weeks later, a genuine tension worth interrogating rather than waving away.

What about alignment — does management eat its own cooking? Oplinger's total compensation runs in the mid-teens of millions of dollars, of which roughly 90% is variable, tied to bonus and equity rather than salary, which is the right structure for a cyclical business. But his personal ownership stake is modest — on the order of a fraction of a percent of the shares outstanding — so the alignment is real but not the kind of founder-level, life-savings-on-the-line ownership that changes behavior in a crisis. He is a well-paid, well-incentivized professional manager, not an owner-operator. This distinction matters more than usual for the South32 question, because empire-building is precisely the failure mode that professional managers — as opposed to owners — are structurally prone to: a larger company generally justifies a larger pay package, and there is a well-documented tendency across corporate history for CEOs to grow the enterprise beyond the point of shareholder value. That is not an accusation against Oplinger; it is the base rate a skeptical investor should have in mind when a professionally managed, mid-pack producer makes its biggest-ever acquisition at a cyclical high. The incentive to build is always there; the discipline record is the counterweight, and the two are now in direct tension.

The most useful thing on the Q1 2026 call, for judging credibility, was how management handled a genuine sore spot: the refineries. Beerman was blunt that Alcoa was "continuing to have significant losses at the refinery," and that in 2026 "the smelter will not generate enough cash flow to cover the refinery's free cash flow losses" — with the company targeting neutralization of those losses only by 2027.5 Notice what that is: a specific, testable, and somewhat unflattering forecast, with a date attached. That is the behavior of a management team that explains its misses concretely rather than waving at macro conditions — and concrete, falsifiable guidance is exactly what you want to see before extending trust to a team about to make its biggest bet. Speaking of which.

VIII. The South32 Deal: Consolidation or Overreach?

For years, aluminum bankers had a favorite parlor game: which of South32's aluminum assets would eventually end up inside Alcoa? The two companies' portfolios fit together like puzzle pieces, and both had partial stakes in the same Brazilian operations. Even JPMorgan, reacting to the news, noted dryly that "this deal has been hypothesized before."13 So when it finally came on June 30, 2026, the surprise was not the logic — it was the price, the structure, and the timing at what looked like a cyclical top.

Start with what Alcoa is actually buying. The centerpiece is an 86% interest in Worsley Alumina, one of the world's largest and most cost-competitive alumina refineries, in Western Australia. Then comes the Hillside aluminum smelter in South Africa — a large, modern smelter that hands Alcoa an entirely new geographic foothold on a continent where it had no smelting presence. Add a 33% stake in the MRN bauxite mine and additional stakes in Brazilian operations where Alcoa was already a partner.12 Critically, the deal excludes South32's troubled Mozal smelter in Mozambique — a facility dogged by power-supply and political risk. Alcoa, in other words, cherry-picked the assets it wanted and left the problem child behind, which is itself a small tell about who was negotiating from strength on asset selection even if not on headline price.

Why does Worsley matter so much? Because it is exactly the kind of cornered resource the frameworks in Section IV identified as the only durable edge in this business. Worsley is a large, long-life, integrated bauxite-mining and alumina-refining operation that sits low on the global cost curve — the opposite of a Kwinana. If Alcoa spent the last decade proving it would close the assets at the top of the cost curve, buying Worsley is the same strategy from the other direction: acquire assets at the bottom of the curve and blend down your average cost. On paper, that is the most coherent thing a disciplined cost-curve operator could possibly do. Hillside, meanwhile, is one of the largest aluminum smelters in the Southern Hemisphere and hands Alcoa a foothold on a continent where it had none — attractive if you believe in African power and metal, riskier if you worry about grid reliability and political stability. The exclusion of Mozal tells you management was thinking hard about exactly those risks.

Now the money, because the structure is where the debate lives. The base consideration was $4.1 billion: roughly $3.1 billion in cash plus about 17.0 million newly issued Alcoa shares worth around $1.0 billion — which equates to roughly 6% dilution of Alcoa's share count.3 On top of the base sits up to $750 million in contingent consideration, payable over four annual periods depending on where alumina and aluminum prices land.3 Fold in assumed net debt and site-remediation and closure liabilities — which some accounts put north of a billion dollars — and the total implied enterprise value stretches toward $5.6 billion.12 Against that, Alcoa pointed to roughly $900 million in net-present-value cost savings it expects to capture.2 The deal is expected to close in the second half of 2027, subject to regulatory approvals across multiple jurisdictions.2

That long runway to close — well over a year — is itself double-edged. It gives Alcoa time to arrange financing and gives regulators in Australia, South Africa, and Brazil time to scrutinize the deal, but it also means Alcoa is committing to a cyclical asset base at 2026 prices while assuming the risk of what alumina and aluminum do between now and late 2027. The contingent structure hedges part of that — if prices fall, Alcoa keeps the $750 million — but the bulk of the price is fixed. A buyer signing a large, mostly-fixed check into a fifteen-month close window is making an implicit bet that the cycle does not roll over hard in the interim.

Read the two sides of that structure carefully, because it's a well-designed piece of financial engineering and a real risk simultaneously. The contingent payments are clever: Alcoa only pays the extra $750 million if metal prices are high, meaning the deal partly self-finances out of the very upside that would make it affordable — a built-in hedge against overpaying at the top of the cycle. But the cash-heavy base and the 6% dilution are the flip side: Alcoa is spending real balance-sheet capacity and issuing equity at a moment when its own management had, weeks earlier, been preaching deleveraging toward a $1.0–1.5 billion net-debt target.5 Analysts flagged the dilution and leverage overhang immediately, and JPMorgan's Bill Peterson kept a Neutral rating with a $70 target, calling the assets "strategically attractive" while withholding judgment on the price.13

The market's verdict on day one was the most striking data point of all. Alcoa fell about 5%; South32 rose roughly 9–10% in Sydney and announced it would return around $500 million to its own shareholders via a special dividend.23 When the seller's stock rallies double digits and the buyer's falls, the market is delivering an early, blunt message: it thinks South32 monetized these assets near the top and handed Alcoa the integration risk and the cyclical timing risk. South32's new CEO, Matt Daley, reinforced that read by framing the sale as a strategic sharpening — a pivot toward base metals with, as one analyst put it, "a war chest for acquisition."2 One side was celebrating a clean exit; the other was explaining a bold bet. That asymmetry is the single most important thing a skeptical investor should sit with. The bull case is that the market is myopic and these tier-one assets will look cheap across a full cycle; the bear case is that the market read it exactly right. We'll adjudicate that. But first, the tailwinds Alcoa is betting on.

IX. Tailwinds: Tariffs, AI Power Demand, and the EV Aluminum Story

There is a reason Alcoa felt confident enough to write the biggest check in its history, and it's not just the cyclically fat 2025 cash flows. Management sees three demand-side stories converging — and the honest analyst's job is to size each one as real optionality rather than swallow it as gospel.

Start with tariffs, the most double-edged of the three. In February 2025 the U.S. government raised Section 232 tariffs on imported aluminum to 25%, and then in June 2025 doubled them again to 50%.1011 On its face, this is a gift to a domestic American producer: a 50% wall against foreign metal should lift the U.S. Midwest premium — the extra amount buyers pay for physically delivered domestic metal — and fatten margins on every tonne Alcoa sells into the United States. But here's the catch that makes tariffs a genuine two-edged sword for Alcoa specifically: a large share of Alcoa's own smelting capacity sits in Canada, drawn there decades ago by cheap, clean hydroelectric power. Metal that crosses from a Canadian Alcoa smelter into the U.S. market can itself get caught in the tariff machinery. And on the Q1 2026 call, management quantified the near-term hit rather than spinning it, guiding to roughly $35 million of incremental tariff cost in the second quarter alone.5 A policy that helps Alcoa the U.S. seller can simultaneously tax Alcoa the Canadian producer. It is not a clean win.

The second story is the flashiest: artificial intelligence. The data centers being built to train and run large AI models are voracious consumers of electricity — and increasingly, of the low-carbon power that Alcoa's legacy hydro-linked sites can supply.12 This has created a genuinely interesting piece of optionality: some of Alcoa's older or idled industrial sites sit on top of exactly the thing AI infrastructure is desperate for — large, permitted, grid-connected power access. The optionality is real: an idled smelter site with a legacy power contract can be worth more as a data-center power asset than as a metal plant. But discipline requires sizing this correctly. It is optionality on non-core assets, not a new business line. Alcoa is a metals company that happens to own some valuable power real estate, not an energy company. Treating a handful of potential site monetizations as a re-rating catalyst would be exactly the kind of narrative inflation this analysis is meant to resist.

The third story is the most durable and the least hyped: lightweighting. As the world electrifies its vehicle fleet, automakers reach for aluminum to offset the dead weight of heavy battery packs — every kilogram of aluminum that replaces steel extends an EV's range, and range is the currency of the entire EV value proposition. An electric vehicle typically contains substantially more aluminum than a comparable internal-combustion car, in the battery enclosure, the body structure, and the wheels. Multiply that content increase across a global fleet transitioning over a decade or more, and you get a slow, grinding, structural lift to aluminum demand that does not depend on any single year's economy. This is real, grounded in physics rather than sentiment, and it's the tailwind most likely to still be intact a decade from now. It is also, notably, the one Alcoa talks about least — perhaps because it is the least dramatic, or perhaps because as an upstream producer of raw metal, Alcoa captures it only indirectly through overall demand rather than through selling specialized auto parts (that was Arconic's game). The point stands: the demand side of the aluminum story is genuinely improving, on more than one axis.

But here's the counterweight that keeps all three stories honest, and it's the one the LME keeps whispering: near-term price forecasts for aluminum have actually been softening even as these demand narratives swell. Demand tailwinds and price weakness can coexist, because supply — especially the slow, grinding return of curtailed capacity when prices rise — pushes back. A company whose earnings swing from a $651 million loss to a $1.16 billion profit on price alone cannot afford to confuse a good structural story with a guaranteed high price. Which brings us to where Alcoa actually sits against everyone else trying to make the same bet.

X. Competitive Landscape: Where Alcoa Sits on the Global Cost Curve

Picture the global aluminum industry as a single, giant staircase — the cost curve — with every smelter in the world placed on a step according to how cheaply it can produce a tonne of metal. The cheapest producers stand at the bottom, comfortable and profitable even when prices are low. The most expensive teeter at the top, profitable only at the cycle's peak and the first to drown when it turns. The LME price is a waterline that rises and falls across those steps. Every strategic move in this industry — every closure, every acquisition — is ultimately an attempt to move down a step or two. So where does Alcoa stand, and against whom?

At the top of the industry by sheer size sit the Chinese giants. 中国宏桥 China Hongqiao is the single largest aluminum producer on earth, with something like 12–14% of global output, and the state-controlled 中国铝业 Chalco (Aluminum Corporation of China) commands roughly 10–12%. Together with the rest of China's smelters, they dominate world production — which is precisely why Beijing's 45-million-tonne capacity cap functions as such a load-bearing pillar of the non-Chinese thesis. Strip that cap away — imagine China deciding to add another ten million tonnes of capacity — and the global cost curve floods with cheap metal, prices sink, and every Western producer's strategy is instantly underwater. The single biggest exogenous risk to the entire Alcoa thesis is therefore not anything Alcoa does; it is a policy decision made in Beijing. That is worth sitting with: the most important variable in a Pittsburgh-headquartered company's future is Chinese industrial policy.

Outside China, the majors are Rio Tinto (around 10%, and blessed with some of the best hydro-powered Canadian smelters in the world), Russia's Rusal (roughly 6–7%, but carrying sanctions and geopolitical baggage that makes its metal hard to place in Western markets), and then Alcoa itself at roughly 4–5%. Behind them come Norsk Hydro, Emirates Global Aluminium, and Century Aluminum. Alcoa, in other words, is a respected, tier-one operator but a mid-pack player by scale — bigger than most, dwarfed by the Chinese leaders. Note the strategic contrast with Rio Tinto, its closest Western peer in quality: Rio is a diversified mining giant for whom aluminum is one business among iron ore, copper, and more, so a bad aluminum year is cushioned by other commodities. Alcoa has no such cushion. It is the pure-play, which is exactly what makes it attractive to an investor who wants clean aluminum exposure and exactly what makes it dangerous when the cycle turns. Purity cuts both ways.

So run the war-game honestly. Where does Alcoa genuinely win? On assets. Its edge — its cornered resource — is a portfolio of high-quality bauxite and alumina positions and a set of legacy hydroelectric power contracts that competitors simply cannot replicate at today's prices. Cheap, clean, contracted power is the single most valuable thing you can own in this business, and Alcoa has a lot of it. The South32 deal is, at its core, an attempt to deepen exactly this advantage: Worsley is a bottom-of-the-cost-curve refinery, and Hillside is a large, efficient smelter. If the deal works, it nudges Alcoa's blended position down the staircase.

And where does Alcoa not win? On everything the frameworks in Section IV already flagged: it has no pricing power, no brand premium, no switching costs, and no scale advantage over the Chinese leaders. It also still carries a tail of legacy high-cost assets — the very Kwinanas and San Cipriáns whose closures define its discipline story. The competitive reality is stark and worth stating plainly: Alcoa cannot out-price, out-brand, or out-scale its way to superior returns. Its only durable lever is being a lower-cost producer of a commodity than the marginal tonne. Everything — the closures, the Alumina Limited buyout, the South32 bet — is in service of that one lever. Which sets up the real question every investor has to answer for themselves.

XI. Bull vs. Bear: The Investment Case

Let's put the two cases in the ring and let them fight, because on Alcoa the bull and bear are unusually well-matched — they're often looking at the same facts and reaching opposite conclusions.

The bull case runs like this. Alcoa is the last major pure-play Western bet on aluminum — a metal facing genuine structural demand growth (EV lightweighting, electrification, AI-driven power buildout) against a genuinely supply-constrained backdrop (China's capacity cap, sanctioned Russian metal, Western tariffs walling out imports). Management has spent a decade proving it will act on the cost curve with real discipline — Kwinana and San Ciprián are the receipts. The Alumina Limited buyout showed it can consolidate known stakes accretively. And now South32 upgrades the asset base with Worsley and Hillside, deepening precisely the cornered-resource advantage that is the only moat this industry offers, with a cleverly structured contingent payment that self-finances out of the upside. Buy tier-one assets from a motivated seller, integrate them, ride a supply-constrained commodity through a demand supercycle. That's the bull.

The bear case looks at the identical facts and sees a leveraged, cyclical price-taker doing the most dangerous thing a cyclical price-taker can do: making its largest-ever acquisition, with cash and dilutive equity, at what looks like a cyclical peak — funded by earnings that swung from a $651 million loss to a $1.16 billion profit in two years on price alone.4 The 6% dilution and the assumed debt push leverage up just weeks after management preached deleveraging toward a $1.0–1.5 billion net-debt target.5 The refineries are still losing money with neutralization not promised until 2027.5 The tariff "tailwind" is double-edged given Canadian exposure. And the deal requires flawless integration across Australia, South Africa, and Brazil — three jurisdictions, multiple regulators, and years of execution risk into a 2027 close. The market's day-one verdict — buyer down 5%, seller up double digits — is the bear case rendered in ticks.23

Now the frameworks, applied as a tiebreaker rather than decoration. Through Porter's Five Forces, aluminum is a structurally unattractive industry: buyer power is high (undifferentiated product), rivalry is intense and global, substitute and supplier pressures are real, and the threat of new entry is capped mainly by the enormous capital and power requirements rather than by anything the incumbents control. When every force points against you, industry-average returns are poor, and the only way to earn above-average returns is to hold a genuinely differentiated cost position — not a differentiated product, which doesn't exist here, but a differentiated place on the cost curve. Through Helmer's 7 Powers, Alcoa's only credible power is a cornered resource — advantaged rocks and cheap contracted power — and the entire strategic question is whether the South32 deal strengthens that cornered-resource position enough to justify the leverage and dilution, or merely enlarges a structurally low-return business. Bigger is not the same as better in a price-taker industry; scale without cost advantage just means more exposure to the same LME waterline. The most charitable and the most damning readings of the deal both accept this framework — they simply disagree about whether Worsley and Hillside are cheap enough, and low enough on the curve, to clear the bar. That is an empirical question that only years of realized cost data will answer.

Which surfaces the activist-style stress test that hangs over the whole thing. As of mid-2026 there was no confirmed activist campaign at Alcoa. But it's worth war-gaming what a skeptical activist would attack if one showed up, because that is the cleanest way to pressure-test the bull case. The obvious lines of assault: the timing and price of the South32 deal (buying cyclical assets at a high with dilutive equity); the leverage taken on just after management preached deleveraging; the persistent, still-unfixed refinery losses; the modest insider ownership relative to the size of the bet being made; and the broader charge that a pure-play created to be simple is drifting back toward the complexity that got the old Alcoa dismantled. Against all of that, management's defense is its record — Kwinana, San Ciprián, the accretive Alumina Limited buyout, the contingent-payment structure that hedges the cyclical timing, and the genuine quality of the Worsley and Hillside assets. The question the skeptic would ultimately put to Oplinger is the through-line of this entire article: is this discipline — the same cost-curve logic that closed Kwinana, now applied to acquiring better assets — or is it empire-building, a finance-trained CEO deploying peak-cycle cash flow to grow the balance sheet just as the company that used to do exactly that got itself broken up in 2016? The honest answer is that we do not yet know, and anyone claiming certainty in either direction is selling something. What we can do is specify exactly which numbers will tell us.

XII. KPIs and Risk Radar

If you are going to track Alcoa over the next several years — and especially through the pendency and integration of the South32 deal — resist the temptation to drown in the dozens of metrics the company reports. Three things matter more than all the rest combined.

First, realized prices versus the LME (and the alumina index), and Alcoa's cost position against them. This is the master variable. Because Alcoa is a price-taker, the single most important thing to watch is the spread between what Alcoa actually realizes per tonne — LME price plus regional premiums, net of tariffs and freight — and what it costs Alcoa to produce that tonne. A widening spread means the cost-curve strategy is working; a compressing one means the cycle is turning against it regardless of how good the operating story sounds. Everything else is downstream of this.

Second, the net-debt and free-cash-flow trajectory through the 2027 close. Management set its own scoreboard here: a net-debt target range of roughly $1.0–1.5 billion, deleveraging-first, returns-to-shareholders-later.5 The South32 deal directly stresses that commitment. Watching whether net debt actually behaves through the acquisition — or blows through the stated range and stays there — is the cleanest available test of whether "discipline" survived contact with the biggest deal in company history. This is the KPI where management's words and actions can be directly checked against each other.

Third, and more specifically, the refinery-loss-neutralization timeline. Beerman put a date on it — 2027.5 Either the refineries stop bleeding cash by then or they don't, and that binary is a concrete, near-term credibility test that requires no faith in commodity forecasts to evaluate.

On the risk radar, focus only on mechanisms that actually bite this business. Price cyclicality is the existential one — already covered, and the reason peak-cycle acquisitions are dangerous. Regional energy-cost inflation strikes directly at the 30–40% of cash cost that is power, and can turn a competitive smelter into a Kwinana. Trade and tariff policy shifts cut both ways given the Canadian smelting footprint. Integration execution across three continents is the specific, elevated risk the South32 deal introduces. Leverage amplifies every one of the above if the cycle turns before the deal is digested. And Western Australian permitting and environmental risk — around bauxite mining approvals near sensitive water catchments — is a genuine, asset-specific overhang on the very refining base the company is doubling down on. Notice what's not on this list: no AI-disruption risk to the core metal, no data-privacy exposure of consequence. This is an industrial business, and its risks are industrial. The lessons, then, are industrial too.

XIII. Playbook: Business & Investing Lessons

Strip away the 137-year history and the multi-continent asset map, and Alcoa distills into a handful of transferable lessons about how value is actually created — and destroyed — in a true commodity business.

Capital allocation is the whole game. In a differentiated business, management can create value through product, brand, or pricing. In a price-taker business, none of those levers exist, so capital allocation is not a lever — it is the lever. When to build, when to close, when to buy, when to return cash: get those four decisions right across a cycle and you win; get them wrong and no amount of operational excellence saves you. Alcoa's entire investment case, bull and bear, reduces to a judgment about the quality of a single management team's capital-allocation decisions. That is a useful mental model for evaluating any commodity producer.

Consolidating known stakes is lower-risk M&A than diversification. The Alumina Limited buyout worked as a template precisely because it removed a minority partner from a business Alcoa already ran — financial risk, not operational risk. The South32 deal is the more ambitious cousin of that logic: still adjacent, still within the same value chain, but now spanning new geographies and requiring genuine integration. The lesson isn't that adjacency is safe — it's that the degree of adjacency is exactly what an investor should be measuring, because it maps directly onto execution risk. The further a deal drifts from "buy out a partner in something we already do," the more it starts to look like the diversification that gets conglomerates broken up.

Government-imposed structure can matter more than operating skill. This is the throughline from Judge Learned Hand's 1945 antitrust ruling to Beijing's capacity cap to Washington's Section 232 tariffs. Alcoa's competitive environment has been shaped, again and again, by policy decisions no manager controlled. For investors, the lesson is to spend real time on the regulatory and geopolitical structure of an industry — the capacity caps, the tariffs, the trade rules — because in commodities that structure often determines returns more than any individual company's cleverness.

Credibility is built in the specifics. The reason Alcoa's management earned the benefit of the doubt is not that they promised discipline — everyone promises discipline. It's that they closed Kwinana, took the charges, cut the workforce, and put testable dates on their refinery-loss forecasts. Specific, falsifiable, occasionally unflattering guidance is the currency of management credibility, and it's what lets an investor extend trust into an uncertain bet like South32. Vague optimism should be discounted; concrete, checkable commitments should be weighted. That distinction is worth more than any single quarter's numbers.

XIV. Epilogue & What to Watch

So we arrive back where we began, on that July 2026 morning with two stocks moving in opposite directions, and the question still open. A company that invented the aluminum industry, got broken up for being too diversified, spent a decade proving it could shrink itself into a disciplined pure-play, and has now, at a cyclical high, made the largest acquisition of its post-spin-off life. Is it the capstone of the discipline story or the first crack in it?

There is one more thing to watch that sits underneath all the operational metrics: the consistency of management's own story across time. The most reliable tell in corporate analysis is not what a management team says in any single quarter but whether its language holds together across quarters — whether the deleveraging framework Beerman articulated in April survives contact with the acquisition announced in June, whether the "we act on the cost curve" narrative that justified closing Kwinana is deployed with equal honesty to justify buying Worsley, and whether misses continue to be explained with specific dates rather than vague macro hand-waving. If the narrative stays coherent and the promised numbers arrive on schedule, the discipline reading strengthens. If the story starts shifting — if net-debt targets quietly move, if refinery-loss dates slip without explanation, if the language turns promotional — that is the empire-building reading announcing itself. Watch the words as closely as the numbers.

The honest answer is that the next several years will settle it, and they will settle it on specifics rather than narrative. Watch the 2027 close: whether the South32 deal clears its multi-jurisdiction regulatory gauntlet on schedule, and whether the assumed liabilities and integration costs come in near the numbers management sketched. Watch the next two or three earnings calls for the refinery-loss neutralization that Beerman promised by 2027 — a clean, binary credibility test. Watch the net-debt trajectory against management's own $1.0–1.5 billion target, because that number is where the words "capital allocation discipline" either hold or dissolve.5 And watch, always, the spread between Alcoa's realized price and its cost per tonne, because that is the tide beneath everything else.

The deepest question this story poses is not really about aluminum at all. It's about whether a management skill honed entirely on subtraction — closing plants, cutting workforces, saying no — can translate into the very different discipline of addition done well. A decade of cost-curve credibility is now being wagered on a single, large, cross-continental acquisition. If it works, Alcoa emerges as a structurally lower-cost producer positioned for a supply-constrained decade. If it doesn't, it becomes a cautionary tale about a cyclical company that mistook a peak for a plateau. The market cast an early, skeptical vote. The company will spend the next several years arguing the other side — not in press releases, but in the only language a commodity business ultimately speaks: cost, cash, and where it sits on the curve when the tide goes out.

References

-

Alcoa Bets on Aluminum Boom With $5.6 Billion South32 Deal — Bloomberg, 2026-06-30 ↩↩↩

-

Australia's South32 sells aluminum assets to Alcoa for $5.6bn — Nikkei Asia, 2026-07-01 ↩↩↩↩↩↩↩↩↩

-

Alcoa stock falls 5% on $4.1 billion South32 acquisition — Investing.com, 2026-07-01 ↩↩↩↩↩↩

-

Alcoa Corporation Reports Fourth Quarter and Full Year 2025 Results — Alcoa Newsroom, 2026-01-17 ↩↩↩↩↩

-

Alcoa (AA) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-04-16 ↩↩↩↩↩↩↩↩↩↩↩

-

Alcoa Completes Acquisition of Alumina Limited — Alcoa Newsroom, 2024-08-01 ↩

-

Alcoa Announces Closure of Kwinana Refinery, Also Updates Third Quarter 2025 Outlook — Alcoa Newsroom, 2025 ↩

-

Alcoa announces curtailment of Kwinana Alumina Refinery in Western Australia — Alcoa Newsroom, 2024 ↩

-

Arconic Inc. — Form 8-K, spin-off completion exhibit (SEC EDGAR), 2016 ↩↩

-

Section 232 Tariffs on Steel and Aluminum — Congressional Research Service via Congress.gov ↩

-

United States modifies steel, aluminum, and copper Section 232 tariffs — White & Case, 2025 ↩

-

AI data centers have massive demand for aluminum. It's crushing the US aluminum industry — Yahoo Finance, 2025 ↩↩

-

JPMorgan reiterates Alcoa stock rating on South32 acquisition — Investing.com, 2026-07-01 ↩↩

-

Production of Aluminum: The Hall-Héroult Process — National Historic Chemical Landmark, American Chemical Society ↩↩

-

United States v. Aluminum Co. of America, 148 F.2d 416 (2d Cir. 1945) — Justia ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube