Agilent Technologies: From HP's Instruments Division to Life Sciences Leader

I. Introduction & Episode Setup

Picture this: November 18, 1999. The NASDAQ is touching record highs, the dot-com boom is in full swing, and in Silicon Valley, a company born from the oldest startup in the region is about to make history. Agilent Technologies debuts on the New York Stock Exchange at $30 per share, immediately soaring to $42.44—making it the largest initial public offering in Silicon Valley history at that time, raising $2.1 billion. The company, spun out from Hewlett-Packard with 35,000 employees and operations in 40 countries, represents something profound: the original DNA of HP, the test and measurement business that Bill Hewlett and Dave Packard started in that famous Palo Alto garage.

Fast forward to today, and Agilent is a $6.51 billion revenue company with 18,000 employees globally—but here's the twist that makes this story fascinating: it's no longer primarily in the test and measurement business at all. The company that once made oscilloscopes and signal analyzers now derives the majority of its revenue from life sciences, diagnostics, and laboratory services. Its instruments analyze everything from cancer biopsies to environmental contaminants, from pharmaceutical compounds to food safety.

The big question we're exploring: How did HP's test and measurement division—the very foundation of Silicon Valley's hardware legacy—transform itself into a life sciences powerhouse? And what can this metamorphosis teach us about corporate evolution, strategic focus, and the art of the spin-off?

This is a story of three major transformations: first, the 1999 separation from HP that created Agilent; second, the painful but necessary restructuring through the dot-com crash that forced the company to find its true north star; and third, the 2014 split that created Keysight Technologies and left Agilent as a pure-play life sciences company. It's a masterclass in portfolio management, strategic pivots, and the courage to abandon your origins in pursuit of a better future.

II. The HP Legacy: Origins & DNA (1939-1999)

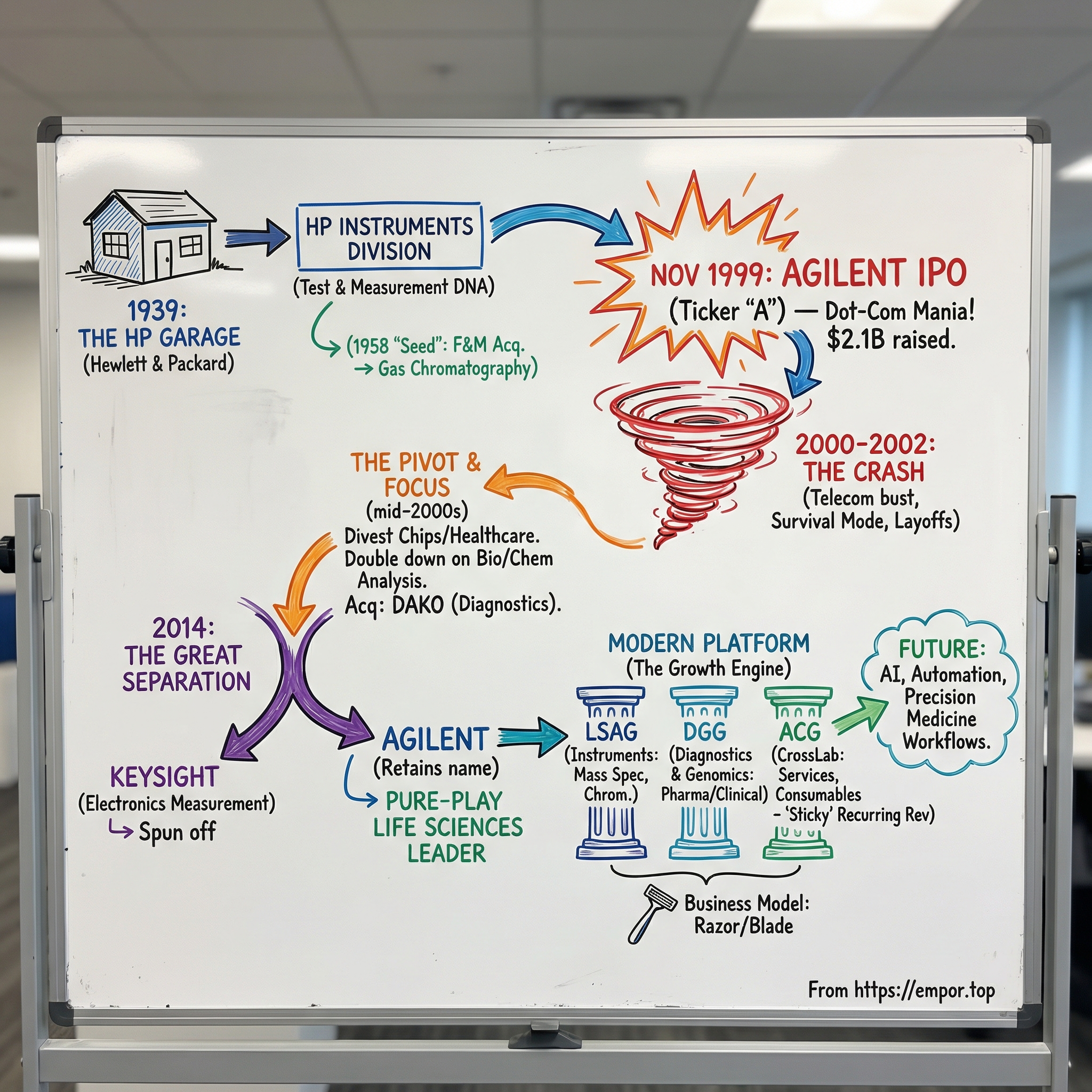

The story begins not in 1999, but in 1938, in a garage at 367 Addison Avenue in Palo Alto—the birthplace of Silicon Valley itself. Bill Hewlett and Dave Packard, fresh Stanford electrical engineering graduates mentored by Professor Frederick Terman, pooled $538 in working capital to start their company. Their first product? The HP 200A, an audio oscillator that generated test tones with unprecedented stability and at a fraction of competitors' prices. The killer app came quickly: Walt Disney Studios bought eight units of the improved 200B model for $71.50 each to test the revolutionary Fantasound stereo system for "Fantasia." The garage startup was officially in business.

What made HP different from the beginning was its approach to measurement and precision. While other companies built instruments, HP built better instruments—more accurate, more reliable, more innovative. This obsession with measurement excellence became the company's calling card. By the 1950s, HP had expanded beyond oscillators into voltmeters, signal generators, and wave analyzers. The company went public in 1957, and by the 1960s, it was the undisputed leader in electronic test and measurement equipment.

A pivotal moment came in 1965 when HP acquired F&M Scientific Corporation for $25 million—a move that would plant the seeds for Agilent's future transformation. F&M brought gas chromatography technology, instruments that could separate and analyze chemical compounds with extraordinary precision. At the time, it seemed like a natural extension of HP's measurement capabilities. Little did anyone know this would become the cornerstone of a life sciences empire decades later.

The medical products division was actually HP's second-oldest business line, established through acquisitions in the late 1950s. HP saw healthcare as another frontier for precision measurement—after all, what is an EKG machine but an oscilloscope for the human heart? By the 1970s, HP was making patient monitors, defibrillators, and ultrasound equipment alongside its traditional test gear.

But perhaps more important than any product was the cultural DNA that HP embedded in its operations: "The HP Way." This wasn't just corporate speak—it was a genuine management philosophy that emphasized respect for individuals, contribution to communities, and uncompromising integrity. HP pioneered concepts like profit-sharing (introduced in 1957), flexible working hours, and the radical idea that companies should avoid layoffs during downturns. When the 1970 recession hit, HP chose a 10% pay cut and every-other-Friday furlough for all employees rather than layoffs—a decision that became Silicon Valley legend.

By the 1990s, however, HP faced a classic innovator's dilemma. The company had grown to over $31 billion in revenue, but its test and measurement division—the original business—was becoming increasingly marginalized. The real growth and excitement were in computers and printers, where HP competed with IBM, Compaq, and Dell. The instruments business, while profitable and technologically advanced, generated only about 19% of total revenue and was seen as a drag on HP's valuation multiples.

CEO Lew Platt, who took over from John Young in 1992, faced mounting pressure. Wall Street analysts complained that HP was too diversified, that the slow-growth instruments business was obscuring the value of the computing and imaging divisions. Smaller, more focused competitors like Tektronix and National Instruments were eating into HP's market share by being more agile and responsive to customer needs. The instruments division needed massive R&D investment to stay competitive, but that money was increasingly being diverted to the computer wars.

Internal tensions were rising too. The instruments division engineers—many of whom saw themselves as keepers of the true HP flame—felt neglected and undervalued. They watched resources flow to the computer division while their budgets stayed flat. Customer relationships that had been cultivated over decades were straining as HP's attention wandered. Something had to give.

The decision to split wasn't made lightly. This wasn't just divesting a business unit—it was cleaving HP's soul in half. The test and measurement business wasn't just where HP started; it embodied the company's core values of precision, innovation, and engineering excellence. But by early 1999, the logic had become inescapable. The instruments business needed freedom to chart its own course, and HP needed to focus on the computing battle ahead. The stage was set for one of the most significant corporate divorces in Silicon Valley history.

III. The Great Spin-Off: Creating Agilent (1999-2000)

March 2, 1999, started like any other day at HP's Palo Alto headquarters, but by noon, shockwaves were reverberating through Silicon Valley. Lew Platt stood before assembled media and announced what many considered unthinkable: Hewlett-Packard would split itself in two. The test and measurement business—Bill and Dave's original baby—would become an independent company. HP would retain the computing and imaging businesses. "This is not about good businesses and bad businesses," Platt insisted. "This is about focus."

The announcement triggered months of intense preparation. Investment bankers from Goldman Sachs and Morgan Stanley descended on HP's offices, carving up six decades of shared infrastructure, patents, and people. Who would get which buildings? How would they divide the 83,000 employees? What about the thousands of shared patents? Every decision carried weight—this wasn't just a financial transaction but a cultural mitosis.

The naming process alone revealed the complexity of the split. HP would keep its name—the computing business had more consumer recognition. But what to call the instruments company? Teams of consultants generated hundreds of possibilities. They needed something that conveyed precision and innovation while avoiding the 1990s tech-naming clichés. On July 28, 1999, they unveiled "Agilent Technologies"—a portmanteau of "agile" and the tech-friendly suffix "-ent." The name was meant to signal nimbleness and forward momentum, qualities the instruments division had arguably lost under HP's massive corporate umbrella.

Ned Barnholt was tapped to lead the new company—a choice that spoke volumes about Agilent's intended direction. Barnholt wasn't from the instruments division; he'd spent most of his HP career in computers and components. But he understood something crucial: Agilent couldn't simply be "HP's instruments division with a new name." It needed a new identity, new strategy, and new ambitions. In his first all-hands meeting, Barnholt declared, "We're not leaving HP. We're launching Agilent."

The IPO machinery kicked into high gear by fall 1999. This was peak dot-com mania—the NASDAQ had risen 80% in the past year, and anything tech-related was gold. But Agilent's roadshow faced unique challenges. How do you sell Wall Street on a company making oscilloscopes and spectrum analyzers when everyone wanted the next Amazon or Yahoo? The pitch became about transformation potential: yes, Agilent made traditional instruments, but it also had semiconductor test equipment for the booming chip industry, fiber-optic components for the telecommunications revolution, and life sciences instruments for the genomics age.

November 18, 1999: IPO day. The scene at the New York Stock Exchange was electric. Agilent priced 65 million shares at $30, the high end of the expected range. HP retained 85% ownership initially—this would be distributed to HP shareholders later—but the public offering alone raised $2.1 billion, valuing the company at roughly $20 billion. When trading opened, the stock immediately jumped to $42.44, a 41% first-day pop. Floor traders who'd been skeptical about "another boring instruments company" were stunned by the demand.

But the real independence day came June 2, 2000, when HP distributed its remaining Agilent shares to HP stockholders—a tax-free spin-off that gave HP shareholders one Agilent share for every two HP shares owned. This wasn't just financial engineering; it was the final cut of the umbilical cord. Agilent employees who'd shown up to work that morning at what had been HP facilities now worked for a fully independent company. The HP logos came down, replaced by Agilent's distinctive blue and orange wave. Even the business cards had to be reprinted.

The initial portfolio was ambitious—perhaps too ambitious. Agilent comprised four major segments: Test and Measurement (the traditional instruments), Semiconductor Products (chips and components), Healthcare Solutions (medical devices and supplies), and Chemical Analysis (the descendants of that 1965 F&M Scientific acquisition). Combined revenue was about $8.3 billion, with 43,000 employees across 40 countries. The company inherited 26 manufacturing sites, 10,000 patents, and customer relationships dating back decades.

Yet beneath the IPO euphoria, warning signs were already visible. The company's largest segment, Communications Test, was heavily dependent on telecommunications equipment makers who were spending like drunken sailors on infrastructure for the internet boom. The semiconductor test business was riding the PC wave. Both markets were priced for perfection, with any slowdown potentially devastating. Meanwhile, the life sciences and chemical analysis businesses—while showing promise—were subscale compared to focused competitors like Waters Corporation and PerkinElmer.

Barnholt's strategy initially focused on leveraging Agilent's broad portfolio—selling "solutions" that combined instruments from different divisions. A pharmaceutical company, for instance, might buy chemical analysis instruments, semiconductor chips for medical devices, and test equipment for quality control. The synergy story sounded compelling in PowerPoint presentations. Reality would prove far messier, as the company was about to discover when the music stopped on the dot-com party.

IV. The Dot-Com Crash & Survival Mode (2000-2005)

The NASDAQ peaked at 5,048 on March 10, 2000—just three months before Agilent's full independence. By October, it had lost 40% of its value. For a company whose largest customers were telecommunications equipment manufacturers and semiconductor companies, the timing couldn't have been worse. Agilent was like a surfer who'd just stood up on their board when the wave suddenly disappeared.

The numbers were brutal. In fiscal 2001, Agilent recorded $500 million in canceled orders from semiconductor and communications customers—companies that had been spending millions on test equipment simply stopped buying overnight. Nortel Networks, Lucent Technologies, and Cisco Systems—Agilent's largest customers—were themselves imploding. The communications test division, which had generated 40% of revenue, saw orders drop 80% in some quarters. The semiconductor test business wasn't far behind.

But the real surprise came from an unexpected quarter: healthcare. The medical products division, which generated 60% of revenue, also began struggling. Hospitals, facing their own financial pressures and Y2K hangover, delayed equipment purchases. What was supposed to be Agilent's stable, defensive business became another source of pain. The company that had just celebrated independence was now fighting for survival.

Ned Barnholt faced an agonizing decision. The HP Way explicitly discouraged layoffs—it was part of Agilent's inherited DNA. But the math was undeniable. The company had expanded to 48,000 employees by May 2001, betting on continued growth. Revenue was collapsing. Something had to give. In a series of painful announcements between 2001 and 2003, Agilent cut 18,500 positions—nearly 40% of its workforce. Manufacturing sites were shuttered. Entire product lines were discontinued. The HP Way, it seemed, couldn't survive the new economy's volatility.

The crisis forced a strategic reckoning. Barnholt and his team realized Agilent was trying to be too many things to too many customers. The broad portfolio that had seemed like an advantage during the IPO now looked like a liability. The company needed focus, which meant making hard choices about what to keep and what to shed.

The first major divestiture came in 2001: the healthcare products business, sold to Philips Medical Systems for $1.7 billion. This was the division HP had built through acquisitions in the 1950s and 60s—patient monitors, ultrasound systems, defibrillators. The decision was controversial internally; many saw healthcare as a growth market. But Barnholt recognized that Agilent lacked the scale to compete with GE, Siemens, and Philips in medical devices. Better to take the cash and redeploy it elsewhere.

The semiconductor business was next. By 2005, this division had recovered somewhat from the crash, making it an attractive asset. KKR and Silver Lake, private equity firms with a nose for opportunity, offered $2.66 billion for the semiconductor unit. The deal closed in December 2005, creating a new company called Avago Technologies. (In a twist of Silicon Valley fate, Avago would later acquire Broadcom for $37 billion and take its name, becoming one of the world's largest chip companies—but that's another story.)

That same year, Agilent sold its 47% stake in Lumileds, a light-emitting diode joint venture, to Philips for $1 billion. The company was systematically shedding anything that wasn't core to its emerging vision. But what exactly was that vision? Even Barnholt seemed uncertain, describing Agilent's future as centered on its "test-and-measurement business at its historic core."

Yet something interesting was happening in the divisions Agilent kept. The chemical analysis business—those gas chromatographs and mass spectrometers descended from the 1965 F&M acquisition—was thriving. Pharmaceutical companies were spending heavily on drug discovery and quality control. Environmental regulations were driving demand for contamination testing. Food safety scares were creating new markets for analytical instruments. While Agilent's traditional electronics test business struggled with cyclical markets, the life sciences and chemical analysis divisions showed steady, secular growth.

Bill Sullivan, who ran the life sciences business, became an internal evangelist for a radical pivot. Why compete in the commoditizing electronics test market when Agilent could dominate in life sciences? The company had unique assets: world-class analytical instruments, deep customer relationships with pharmaceutical companies, and expertise in both hardware and software. Sullivan argued that Agilent could build something unprecedented—a technology platform company for the life sciences revolution.

By 2005, Agilent had survived the worst. Revenue had stabilized around $5 billion, less than at independence but far more focused. The company had $2 billion in cash from divestitures. The question now wasn't survival but direction. The electronics heritage still dominated—test and measurement remained the largest division—but the growth was clearly in life sciences. Barnholt, exhausted from navigating the crisis, announced his retirement. His successor would need to make the ultimate choice: embrace the electronic instruments legacy or chase the life sciences future. As it turned out, the answer would be both—until it couldn't be.

V. The Life Sciences Pivot: Finding the New North Star (2005-2014)

When Bill Sullivan took over as CEO in March 2005, he didn't immediately announce a dramatic shift to life sciences. That would have been too jarring for a company still finding its footing. Instead, he spoke of "leveraging measurement science across multiple markets." But those who watched closely could see where things were heading. Sullivan's first major acquisition wasn't in electronics—it was Stratagene, a molecular biology tools company, purchased for $270 million in 2007.

The Stratagene deal was revealing in multiple ways. First, it showed Agilent was serious about building capabilities beyond analytical instruments. Stratagene made reagents, enzymes, and other "consumables" that scientists used daily. This opened up the razor-and-blade business model—sell the instrument once, sell consumables forever. Second, it signaled a move upstream in the research workflow. Agilent wasn't content to just analyze samples; it wanted to help prepare them too.

But the real transformation accelerated under Sullivan's successor, Mike McMullen, who became CEO in March 2010. McMullen was a chemical engineer by training who'd run the chemical analysis business—he viscerally understood the life sciences opportunity. In his first town hall, he laid out a simple but profound observation: "The 20th century was the century of physics. The 21st century will be the century of biology. We need to position Agilent at the intersection of biology and technology."

The acquisition pace quickened. Halo Genomics brought next-generation sequencing technology. Velocity11 added laboratory automation. Each deal was relatively small—$50 million here, $100 million there—but collectively they were transforming Agilent's capabilities. The company was building what McMullen called an "analytical platform"—not just instruments but complete workflows for life sciences research. The game-changer came in 2012 with the Dako acquisition. At $2.2 billion in cash, it was the largest acquisition in Agilent's history. Dako was a Danish maker of cancer-diagnostics tools, providing antibodies, reagents, scientific instruments and software primarily to customers in pathology laboratories, and collaborating with major pharmaceutical companies to develop companion diagnostics. The deal wasn't just about size—it was about strategic intent. Dako gave Agilent instant credibility in clinical diagnostics, a market with vastly different dynamics than research instruments.

The Dako acquisition was transformative in ways beyond the obvious. With 2010 annual revenue of approximately $340 million and more than 1,000 employees, primarily in Denmark and Carpinteria, California, Dako brought deep expertise in immunohistochemistry—the staining techniques pathologists use to identify cancer cells. But more importantly, it brought relationships with hospital pathology labs and understanding of the clinical workflow. This wasn't selling to PhD researchers anymore; it was selling to MDs making life-or-death diagnoses.

The internal transformation was equally dramatic. McMullen reorganized the company around end markets rather than technologies. Instead of a "mass spectrometry division" selling to everyone, Agilent created focused teams for pharmaceuticals, diagnostics, food safety, and environmental testing. Each team combined instruments, consumables, software, and services into complete solutions. A pharmaceutical customer didn't just buy a liquid chromatograph; they bought a validated workflow for drug quality control.

By early 2013, the strategic direction was becoming clear, but McMullen knew half-measures wouldn't work. The electronic measurement business—still generating about 45% of revenue—was increasingly a distraction. It needed different R&D investments, different sales channels, different everything. On September 19, 2013, Agilent announced what many saw coming: it would split again, separating the electronic measurement business into a new company while keeping life sciences and diagnostics.

The announcement was met with relief rather than surprise. Unlike the traumatic 1999 HP split, this felt natural, even inevitable. The electronic measurement business was still profitable and technologically advanced, but it was fighting in mature markets against focused competitors. Meanwhile, the life sciences opportunity was exploding—genomic sequencing costs were plummeting, personalized medicine was becoming reality, and regulatory requirements were driving demand for analytical testing.

McMullen framed it perfectly: "Both businesses are leaders in attractive markets, but they serve different customers, need different innovation strategies, and require different operating models. Separating them allows each to optimize for their specific opportunities." What he didn't say but everyone understood: Agilent had chosen its side. The company that began as an electronics test company was betting its future on biology.

VI. The Keysight Spin-Off: Completing the Transformation (2014)

Ron Nersesian remembers the exact moment he knew the split was real. It was February 2014, and he'd just been named CEO of what would become Keysight Technologies. Walking through Agilent's Santa Rosa facility—soon to be Keysight's headquarters—he saw engineers removing Agilent logos from oscilloscopes that hadn't even shipped yet. "That's when it hit me," he later recalled. "We weren't just dividing assets. We were creating two entirely different destinies."

The mechanics of the split were remarkably smooth compared to the HP separation 15 years earlier. Agilent had learned from that experience—and from watching other companies botch their spin-offs. The project team, code-named "Project Gear," had 18 months to untangle four decades of shared infrastructure. Every patent had to be assigned, every customer contract reviewed, every employee given a new home. But unlike 1999, there was no existential angst about identity. Everyone knew which side they belonged on.

The naming process for the electronic measurement company was deliberately forward-looking. "Keysight" combined "key" (as in crucial) with "insight"—positioning the company as essential for customers gaining visibility into their electronic designs. The logo, a bold red triangle, pointed upward and forward. Everything about the branding said: we're not nostalgic for the past; we're building the future.

October 14, 2014, marked another strategic move: Agilent exited the nuclear magnetic resonance (NMR) business, selling it to Bruker Corporation. NMR was prestigious—it was used by Nobel Prize winners to determine molecular structures—but it was also capital-intensive and subscale. The message was clear: Agilent would rather be number one or two in its chosen markets than spread itself thin trying to compete everywhere.

November 1, 2014: separation day. Keysight Technologies began trading on the NYSE under the ticker "KEYS." The market's reaction was telling—both stocks rose. Agilent jumped 3.4% while Keysight gained 6.2%. Combined, the two companies were worth about $2 billion more than Agilent alone had been worth before the announcement. The conglomerate discount had been real, and investors were rewarding focus.

The financial engineering was elegant. Agilent shareholders received one share of Keysight for every two shares of Agilent owned—a tax-free distribution that let investors decide whether to hold both companies or pick sides. Keysight took with it about $1.8 billion in revenue and 9,500 employees. Agilent kept $4.0 billion in revenue and 12,500 employees. The debt was split proportionally, and each company had adequate cash to fund operations.

But the real genius was in how cleanly the businesses separated. Unlike many spin-offs where companies remain entangled through transition service agreements and shared facilities, Agilent and Keysight achieved near-complete independence from day one. They had different customers (electronics designers vs. life scientists), different sales channels (direct vs. through distributors), and different innovation cycles (Moore's Law vs. biological discovery).

For Agilent, the split was liberating. The company could now speak purely to life sciences customers without confusing them with talk of 5G testing or semiconductor yields. Marketing became simpler—instead of explaining why an oscilloscope company also made DNA sequencers, Agilent could position itself as "your partner in life sciences discovery." The sales force could specialize, the R&D budget could focus, and acquisitions could be evaluated through a single strategic lens.

The transformation numbers told the story. In fiscal 2014, Agilent's last year before the split, life sciences and diagnostics represented about 55% of revenue. By fiscal 2015, as a pure-play life sciences company, that was 100%. The company's price-to-earnings multiple expanded from about 16x to 20x within a year—investors were paying a premium for focus and growth potential over diversification.

McMullen's post-split strategy was aggressive. With the distraction of managing two different businesses gone, he accelerated the acquisition pace. Every deal now had to answer one question: does this strengthen our life sciences platform? The discipline was refreshing after years of trying to balance competing priorities. Agilent was no longer trying to be all things to all customers—it was trying to be the essential technology partner for life sciences and diagnostics. The final transformation from HP's test and measurement division was complete.

VII. Modern Era: Building the Life Sciences Platform (2015-Present)

The acquisition announcement came on a sleepy August morning in 2015, but for Mike McMullen, it represented the culmination of a two-year courtship. Agilent acquired Seahorse Bioscience for $235 million in cash, bringing in technology that allowed researchers to measure cellular metabolism in real-time. Seahorse's FY15 revenue was estimated to be $49 million, making it a relatively small but strategically vital acquisition. The technology filled a crucial gap—while Agilent's mass spectrometers could tell you what molecules were present in a cell, Seahorse's instruments could show you how cells were actually using energy in real-time, critical for drug discovery and disease research. The pace accelerated with larger deals. In 2019, Agilent announced the acquisition of BioTek Instruments for $1.165 billion, with anticipated tax benefits bringing the net price to approximately $1.05 billion. BioTek, generating $162 million in revenue in 2018 with nearly 500 employees, brought critical cell imaging systems and microplate readers that complemented Agilent's existing cell analysis portfolio. The deal pushed Agilent's cell analysis business to over $250 million in annual revenues, positioning the company strongly in the immuno-oncology and immunotherapy markets. Each acquisition was a building block. In 2016, Agilent acquired UK-based Cobalt Light Systems for £40 million in cash. Cobalt developed and manufactured Raman spectroscopy instruments, with proprietary technology that could identify chemicals through opaque barriers—critical for pharmaceutical quality control and airport security. Cobalt's customers included more than 20 of the largest 25 global pharmaceutical companies, and more than 75 airports across Europe and Asia-Pacific.

The strategy wasn't just about buying companies—it was about building an integrated platform. McMullen reorganized the company around three business segments: Life Sciences and Applied Markets (the analytical instruments), Diagnostics and Genomics (the clinical business), and Agilent CrossLab (services and consumables). Each segment was further focused on six key markets: food safety, environmental and forensics, diagnostics with a cancer focus, chemicals and advanced materials, pharmaceuticals, and academic research.

The CrossLab division deserves special attention as it represents Agilent's evolution from hardware vendor to solution provider. CrossLab doesn't just service instruments—it manages entire laboratory workflows, providing everything from sample preparation to data analysis. In 2021, Agilent partnered with ABB Robotics to develop automated laboratory solutions, recognizing that the future of life sciences isn't just better instruments but fully integrated, automated workflows. The leadership transition in May 2024 marked another evolution. Padraig McDonnell became president and CEO in May 2024, succeeding Mike McMullen who had led the company through its life sciences transformation. McDonnell, 52, had served as president of the Agilent CrossLab Group (ACG) since May 2020 and in his most recent role, McDonnell drove exceptional growth in Agilent's Services business, with significant improvements in profitability and customer satisfaction. His appointment signaled continuity—he'd been with HP/Agilent since 1998—but also change, as he brought deep expertise in the services and consumables business that now drives recurring revenue.

VIII. Business Model & Competitive Dynamics

Understanding Agilent's business model requires appreciating a fundamental shift that occurred over the past decade: the company transformed from selling boxes to selling outcomes. Yes, they still manufacture world-class chromatographs and mass spectrometers, but increasingly, customers aren't just buying instruments—they're buying complete analytical workflows, ongoing service relationships, and most importantly, confidence in their results.

The razor-and-blade model is central to this strategy. A pharmaceutical company might spend $500,000 on a liquid chromatograph-mass spectrometer system, but over its 10-year lifetime, they'll spend multiples of that on columns, solvents, standards, maintenance, and software upgrades. The instrument sale is just the beginning of the relationship. This recurring revenue stream—now approaching 40% of total revenue—provides stability that pure equipment sales never could.

Take the CrossLab division as the exemplar of this evolution. CrossLab doesn't manufacture instruments; it provides everything else a laboratory needs to function. Enterprise software that manages instrument utilization across an entire organization. Asset management services that ensure compliance with FDA regulations. Method development and validation services. Even something as mundane as laboratory supplies—but delivered with predictive analytics that ensure a lab never runs out of critical consumables. One pharmaceutical executive described it perfectly: "Agilent used to be our vendor. Now they're our laboratory operations partner."

The technology platforms themselves span an impressive range. In chromatography, Agilent offers everything from simple gas chromatographs for routine quality control to ultra-high-performance liquid chromatography systems capable of separating complex biological molecules. Their mass spectrometry portfolio includes triple quadrupole systems for targeted analysis, time-of-flight instruments for discovery work, and the flagship 6500 series Q-TOF systems that combine the best of both worlds. In spectroscopy, beyond the Cobalt-derived Raman systems, they offer atomic absorption, inductively coupled plasma, and microwave plasma instruments. Each platform represents decades of refinement and thousands of patents.

The competitive landscape is both concentrated and fragmented. At the top, four companies dominate: Thermo Fisher Scientific ($40+ billion revenue), Danaher ($30+ billion), Waters Corporation ($3 billion), and Agilent. Thermo Fisher is the colossus, offering everything from basic lab equipment to complex bioprocessing systems. Danaher, through its life sciences platform including Beckman Coulter and Pall, focuses on bioprocessing and diagnostics. Waters, like Agilent, specializes in analytical instruments but with a narrower focus on chromatography and mass spectrometry.

But the real competition often comes from unexpected quarters. In genomics, Illumina dominates sequencing while Agilent provides sample preparation and target enrichment. In cell analysis, companies like Becton Dickinson and Bio-Rad compete fiercely. In diagnostics, Roche and Abbott are giants that dwarf Agilent's presence. The strategy isn't to compete everywhere but to pick battles where Agilent's analytical expertise provides genuine differentiation.

Geographic exposure tells another story. The United States generates about 35% of revenue—stable but mature. Europe contributes 25%, with particular strength in pharmaceutical and environmental markets. But the real growth engine—and risk—is China, representing nearly 20% of revenue. China's investment in life sciences research, environmental monitoring, and food safety has been massive. When the Chinese government announces a food safety initiative or environmental crackdown, Agilent's order book swells. But this also creates vulnerability to trade tensions and economic cycles. The PFAS (per- and polyfluoroalkyl substances) testing opportunity exemplifies Agilent's ability to capitalize on regulatory tailwinds. Many PFAS compounds do not breakdown in the environment and there is evidence that PFAS exposure can lead to adverse human health. Increasingly, many regulatory agencies like EPA are recommending PFAS testing in water. Agilent has developed a portfolio of PFAS standards that are based on EPA guidelines, such as EPA 537.1, EPA 533, and EPA 8327 methods. Management has noted that PFAS testing solutions are contributing 75 basis points to revenue growth—significant for a company of Agilent's size. The company offers complete workflows including sample preparation, standards, instruments, and software, positioning itself as the single-source solution for laboratories scrambling to meet new regulations.

The partnership with ABB Robotics, announced in 2021, represents another dimension of the business model evolution. Laboratory automation isn't just about replacing human workers—it's about enabling experiments that weren't previously possible. A fully automated lab can run 24/7, generating data at scales that transform how drug discovery and development work. Agilent doesn't just sell the robots; they integrate them into complete laboratory workflows, another recurring revenue stream through service and software.

IX. Financial Analysis & Performance

The numbers tell a story of transformation and resilience. Fiscal year 2024 revenue of $6.51 billion represents modest growth, but the composition of that revenue has fundamentally changed from a decade ago. The shift from capital equipment to consumables and services has created a more predictable, higher-margin business model that commands premium valuations.

Q4 2024 provides a snapshot of current dynamics: $1.70 billion in revenue, up just 0.8% year-over-year, but with GAAP earnings per share of $1.22 and non-GAAP EPS of $1.46. The modest top-line growth masks significant margin expansion—the company has systematically improved operational efficiency while investing in higher-margin businesses. Operating margins have expanded from the mid-teens a decade ago to consistently above 20% on a non-GAAP basis.

Segment performance reveals the strategic priorities. Life Sciences and Applied Markets, the largest segment at roughly 55% of revenue, showed resilience despite pharmaceutical customer cautiousness. The Diagnostics and Genomics segment, about 25% of revenue, faced headwinds from declining COVID-related testing but is recovering as routine procedures normalize. CrossLab, at 20% of revenue, continues its steady march upward, with services and consumables providing that crucial recurring revenue stream.

The China story deserves special attention. After several quarters of weakness driven by anti-corruption campaigns and economic uncertainty, green shoots are emerging. Management reported a 50% win rate on recent stimulus tenders, translating to $35 million in expected Q1 2025 revenue. But this also highlights the feast-or-famine nature of the Chinese market—when the government opens the spending taps, orders flood in; when it tightens, they dry up just as quickly.

Geographic revenue mix shows both diversification and concentration risks. The Americas at 35% and Europe at 25% provide stable, mature market exposure. Asia-Pacific excluding China at 20% offers growth potential, particularly in markets like India and Southeast Asia investing heavily in laboratory infrastructure. But China's 20% creates vulnerability—not just to economic cycles but to geopolitical tensions that could disrupt access to this critical market.

The balance sheet remains fortress-like, with over $2 billion in cash and modest debt levels. This financial flexibility enables continued acquisitions without diluting shareholders or taking on excessive leverage. Return on invested capital consistently exceeds 15%, demonstrating efficient capital deployment even with an active acquisition strategy.

Capital allocation follows a balanced approach. The company spends about 6-7% of revenue on R&D, essential for maintaining technological leadership. Capital expenditures run 3-4% of revenue, sufficient for capacity expansion without the massive factory investments required in semiconductors or other capital-intensive industries. The dividend yields about 1%, with consistent increases demonstrating confidence in cash flow generation. Share buybacks opportunistically return excess cash, though acquisitions take priority when strategic targets emerge.

Free cash flow generation is particularly impressive, consistently exceeding $1 billion annually. The conversion from earnings to cash is high because the business model doesn't require massive working capital or capital expenditure investments. A new instrument sale might require some inventory investment, but the ongoing consumables and services revenue drops straight to cash flow.

Yet challenges are evident in certain metrics. Organic growth has been sluggish, often in the low single digits excluding acquisitions. This reflects both market maturity and customer budget pressures. Academic and government markets, traditionally 15-20% of revenue, have been particularly weak, down 7% recently due to NIH budget uncertainty and general fiscal constraints. The pharmaceutical industry, while still investing in R&D, has become more selective about capital equipment purchases, extending replacement cycles and demanding greater value justification.

The financial profile ultimately reflects a company in transition—no longer the high-growth story of the early 2000s, but not the stagnant industrial conglomerate either. It's a steady compounding machine, generating predictable cash flows, making strategic acquisitions, and gradually shifting toward higher-value, stickier revenue streams. For investors, it's less about explosive growth and more about consistent execution and capital allocation in an essential but overlooked corner of the economy.

X. Playbook: Key Business Lessons

The Agilent story offers a masterclass in corporate evolution, with lessons that extend far beyond the life sciences industry. The journey from HP's test and measurement division to today's life sciences platform company required decisions that seemed counterintuitive at the time but proved prescient in hindsight.

The Art of the Spin-Off: Knowing When to Divide

The 1999 HP split and 2014 Keysight separation weren't just financial engineering—they were recognition that different businesses require different strategies, cultures, and capital allocation priorities. HP's instruments division was being starved of resources as the company chased the computing wars. As an independent Agilent, it could invest appropriately in its markets. Similarly, by 2014, the electronic measurement and life sciences businesses had diverged so significantly that keeping them together was destroying value for both.

The key insight: conglomerate discounts are real, but they're not just about valuation multiples. They're about strategic focus, talent allocation, and the ability to make bold moves without worrying about other divisions. Post-Keysight spin, Agilent could speak purely to life sciences customers without confusing its message. Investment decisions became clearer. Acquisition targets were evaluated through a single strategic lens. Sometimes, 1+1 really does equal 3—when you divide them.

Portfolio Management: The Courage to Walk Away

Selling the healthcare division to Philips in 2001 for $1.7 billion seemed like retreat. Medical devices were a growth market; why exit? Because Agilent recognized it lacked the scale to compete with GE, Siemens, and Philips. Better to take the cash and redeploy it where they could win. The semiconductor division sale to KKR/Silver Lake in 2005 followed similar logic. That business became Avago, then Broadcom—massively successful, but in ways Agilent could never have achieved while managing disparate businesses.

The discipline to exit good businesses that aren't great fits is rare in corporate America. CEOs fall in love with growth stories, boards hesitate to shrink revenue, and employees resist change. But Agilent's willingness to prune enabled it to flourish in its chosen markets. The lesson: in portfolio management, what you don't do is as important as what you do.

From Products to Platforms: The Ecosystem Play

The transformation from selling instruments to providing complete analytical workflows represents a fundamental business model shift. In the old model, Agilent sold a mass spectrometer and hoped the customer bought another in 7-10 years. In the new model, that same customer buys consumables monthly, service contracts annually, and software upgrades continuously. The instrument sale is just the beginning of a long-term relationship.

This required changing everything—sales compensation, R&D priorities, even how they measure success. Instrument reliability, once the holy grail, became table stakes. Now success meant share of wallet, customer workflow integration, and lifetime value. The CrossLab division epitomizes this shift, providing not just service but complete laboratory management. They're not selling products; they're selling outcomes.

Building Moats in B2B Markets

Consumer companies build moats through brands. Enterprise software companies through network effects. But how does a B2B analytical instruments company build competitive advantages? Agilent's approach is instructive: technical excellence as the foundation, but regulatory compliance as the moat. When a pharmaceutical company validates an Agilent method with the FDA, switching vendors requires re-validation—expensive, time-consuming, and risky. When a environmental lab invests in training technicians on Agilent instruments, switching means retraining.

The company has also built switching costs through ecosystem integration. Agilent's software doesn't just run instruments; it manages entire laboratory workflows. Data from different instruments integrates seamlessly. Service technicians understand the complete system, not just individual boxes. Customers aren't just buying instruments; they're buying into an ecosystem that becomes harder to leave the deeper they integrate.

Managing Cyclicality: The Recurring Revenue Hedge

Capital equipment markets are inherently cyclical. When budgets tighten, customers delay purchases, extend replacement cycles, and make do with existing equipment. Agilent's shift toward consumables and services provides a hedge—even if customers don't buy new instruments, they still need columns, standards, and maintenance. This recurring revenue now approaches 40% of total revenue, providing stability through cycles.

But the real insight is that different customer segments have different cycles. Pharmaceutical companies might pull back when facing patent cliffs, but environmental testing surges with new regulations. Academic research suffers during government budget crises, but food safety testing remains steady. Geographic diversification adds another layer—when China slows, India might accelerate. The portfolio approach to end markets smooths the inherent volatility.

The Power of Patient Capital

Unlike software companies that can scale rapidly with minimal capital, life sciences requires patient investment. Developing a new mass spectrometer takes years and millions in R&D. Building customer relationships in regulated industries takes decades. Market positions are won slowly and defended tenaciously. Agilent's willingness to invest consistently through cycles, to make acquisitions that might not pay off for years, and to build capabilities methodically rather than chase quick wins has created durable competitive advantages.

This patience extends to acquisitions. The Dako deal in 2012 didn't immediately transform Agilent into a diagnostics powerhouse, but it provided the foundation for building that business. Smaller deals like Seahorse and Cobalt might seem insignificant individually, but collectively they've created new platforms. The discipline to make many small bets rather than betting the company on transformative deals has reduced risk while steadily expanding capabilities.

XI. Bear vs. Bull Case

The Bear Case: Structural Headwinds and Cyclical Pressures

The pessimistic view starts with end-market exposure. Pharmaceutical companies, Agilent's largest customer segment, face their own pressures—patent cliffs, pricing pushback, and the shift toward biologics that require different analytical tools. The golden age of blockbuster drugs is over; the industry is becoming more specialized, which could mean fewer but more complex instruments rather than volume growth.

China dependency looms large. At 20% of revenue, China isn't just another market—it's essential for growth. But US-China tensions aren't abating. Technology restrictions could limit Agilent's ability to sell advanced instruments. Local competition is emerging, with companies like Shimadzu and domestic Chinese players offering "good enough" solutions at lower prices. The feast-or-famine nature of Chinese government spending adds volatility that makes planning difficult.

Competition from larger players presents another challenge. Thermo Fisher, with 6x Agilent's revenue, has scale advantages in R&D, distribution, and customer relationships. Danaher's business system—their vaunted continuous improvement culture—drives operational excellence Agilent struggles to match. These competitors can bundle products, offer enterprise-wide deals, and invest more aggressively in emerging technologies.

Academic and government weakness isn't just cyclical—it might be structural. Academia/government weakness (down 7% due to NIH budget uncertainty) reflects broader funding pressures unlikely to reverse soon. Universities face enrollment challenges, government research budgets are constrained, and the shift toward applied rather than basic research reduces demand for high-end analytical instruments.

The capital equipment cycle is extending. Instruments that once needed replacement every 5-7 years now last 10-15 years thanks to improved reliability and modular upgrades. While good for customers, this extends replacement cycles and reduces revenue opportunities. The secondary market for used instruments is growing, with companies refurbishing and reselling equipment that once would have been scrapped.

Technology disruption presents a longer-term threat. What if AI-driven analysis reduces the need for physical testing? What if point-of-care diagnostics eliminates centralized laboratory testing? What if synthetic biology creates new analytical challenges that current instruments can't address? Agilent must constantly invest to stay relevant, but picking the right technologies to pursue is increasingly difficult.

The Bull Case: Secular Growth and Strategic Positioning

The optimistic view starts with secular tailwinds in life sciences. Global healthcare spending continues growing faster than GDP. Personalized medicine requires more, not less, analytical testing. Cell and gene therapies need sophisticated quality control. The microbiome, proteomics, metabolomics—entire fields of biology are opening up that require analytical tools. Agilent is selling picks and shovels to the life sciences gold rush.

Regulatory requirements keep expanding, creating mandated demand. PFAS testing is just beginning—thousands of compounds need monitoring across water, soil, and food supplies. Food safety regulations are globalizing, with developing countries adopting first-world standards. Environmental monitoring is becoming non-negotiable as climate concerns intensify. Each new regulation creates instrument sales, but more importantly, ongoing consumables and service revenue.

The recurring revenue transformation is still early. At 40% of revenue, consumables and services have room to grow—best-in-class life sciences tools companies achieve 60-70%. Each instrument installation creates an annuity stream. The CrossLab division's enterprise software creates switching costs. As laboratories increasingly outsource non-core activities, Agilent's service offerings become more valuable.

Market leadership in key segments provides pricing power. In certain applications—like comprehensive two-dimensional gas chromatography or specific mass spectrometry configurations—Agilent has dominant share. Customers specify Agilent methods in their protocols. Regulatory filings reference Agilent instruments. This installed base creates a defensive moat and offensive launching pad for new products.

Geographic expansion opportunities remain significant. India, Southeast Asia, Latin America, and Africa are building laboratory infrastructure. As these markets develop, they'll need analytical capabilities for food safety, environmental monitoring, and pharmaceutical quality control. Agilent's global presence and reputation position it well to capture this growth.

The innovation pipeline suggests continued differentiation. Investments in automation, artificial intelligence integration, and cloud connectivity are creating next-generation laboratory platforms. The partnership with ABB Robotics could revolutionize laboratory workflows. Digital twin technology could enable remote operation and predictive maintenance. These aren't just incremental improvements but potential step-changes in how laboratories operate.

Management's track record inspires confidence. The successful navigation of multiple transformations—from HP spin-off through dot-com crash to life sciences pivot—demonstrates strategic agility. The Keysight separation was executed flawlessly. Recent acquisitions have been integrated successfully. Capital allocation has been disciplined. This isn't a management team likely to make bet-the-company mistakes.

Valuation remains reasonable despite quality. Trading at roughly 20x forward earnings, Agilent is valued at a discount to peers like Thermo Fisher (24x) and Danaher (26x) despite similar growth profiles and returns on capital. As the business model continues shifting toward recurring revenue and margins expand, multiple expansion seems likely.

XII. Epilogue: The Path Forward

December 17, 2024, marked another inflection point. At the company's Investor Day, new CEO Padraig McDonnell unveiled what he called "Agilent 2.0"—not a revolution but an evolution of the strategy McMullen had pursued. The focus: accelerating the shift to recurring revenue, expanding in high-growth end markets like cell and gene therapy, and leveraging artificial intelligence to transform both internal operations and customer solutions.

The AI opportunity is particularly intriguing. Agilent isn't trying to become an AI company, but rather embed intelligence throughout its ecosystem. Imagine mass spectrometers that self-optimize based on sample characteristics. Software that predicts instrument maintenance needs before failures occur. Laboratory information systems that automatically flag anomalous results and suggest root causes. This isn't science fiction—pilot programs are already running with select customers.

The precision medicine revolution presents another growth vector. As treatments become more targeted, the need for sophisticated diagnostics and companion diagnostics grows. Agilent's pathology business, built on the Dako foundation, is well-positioned for this shift. The company's genomics capabilities, while subscale compared to Illumina, provide essential tools for target enrichment and sample preparation.

Sustainability initiatives, often dismissed as corporate virtue signaling, represent real business opportunities. Pharmaceutical companies need to reduce solvent usage—Agilent's developing "green" chromatography methods. Laboratories want to reduce energy consumption—Agilent's instruments are becoming more efficient. The circular economy demands better recycling—Agilent's analytical tools enable materials identification and separation.

Yet the biggest lesson from Agilent's journey might be about corporate patience and strategic courage. In an era of activist investors and quarterly earnings obsession, Agilent methodically transformed itself over two decades. It walked away from good businesses to focus on better ones. It invested through downturns. It made dozens of small acquisitions rather than one transformative deal. It chose strategic clarity over revenue maximization.

The transformation from HP's test and measurement division to today's life sciences leader wasn't inevitable—it required difficult decisions at every turn. The company that once made oscilloscopes for NASA now makes instruments that analyze cancer biopsies. The engineers who designed equipment for the Apollo program have been succeeded by scientists developing tools for personalized medicine. It's a profound evolution that required abandoning the very identity that created the company.

For other conglomerates considering splits, Agilent offers both inspiration and caution. Separation can unlock value, but only with clear strategic rationale. Focus beats diversification, but only if you pick the right focus. Portfolio pruning enables growth, but requires courage to walk away from revenue. The path from separation to success is long and winding—Agilent took 25 years to complete its transformation.

Looking ahead, Agilent faces a familiar challenge: how to maintain growth while defending market position. The company is no longer the scrappy spin-off fighting for relevance but an established player with markets to defend. New competitors emerge constantly—some from unexpected directions like consumer genomics companies moving upstream or software companies offering virtual testing. Maintaining innovation while improving operations, pursuing growth while defending margins, expanding globally while focusing strategically—these tensions never resolve, only evolve.

The ultimate judgment on Agilent's transformation won't come for years. Will the life sciences bet pay off as healthcare spending continues growing? Can the company maintain its innovation edge as Chinese competitors emerge? Will recurring revenue truly provide stability through the next downturn? These questions remain open, their answers to be written by the next generation of Agilent leaders.

But one thing seems certain: the company that emerges from the next decade will look as different from today's Agilent as today's company looks from the HP spin-off of 1999. The willingness to evolve, to abandon successful strategies for better ones, to transform rather than merely adapt—this might be Agilent's most valuable asset. In a world where the only constant is change, the ability to reinvent yourself isn't just an advantage—it's essential for survival.

The story that began in a Palo Alto garage in 1938 continues, each chapter building on the last while moving in directions the founders could never have imagined. Bill Hewlett and Dave Packard built instruments to measure electronic signals. Their successors build tools to decode the mysteries of life itself. It's a transformation that captures something essential about American business: the ability to honor your heritage while refusing to be constrained by it, to respect your past while inventing your future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube