Zydus Wellness: From Sugar-Free Pioneer to Wellness Empire

I. Introduction & Episode Roadmap

Picture this: A middle-aged diabetic in Mumbai walks into a pharmacy in 2005, desperately searching for a way to enjoy his morning tea without spiking his blood sugar. The pharmacist hands him a small sachet—Sugar Free, India's first mainstream artificial sweetener. That moment represents millions of similar interactions that transformed Zydus Wellness from an obscure dairy substitute manufacturer into a ₹12,322 crore wellness empire spanning 25 countries.

Today, Zydus Wellness commands a portfolio that reads like a greatest hits of Indian household brands: Complan, the nutrition drink that raised generations; Glucon-D, the summer savior in every Indian home; Nycil, the talcum powder synonymous with prickly heat relief; and Sugar Free, which still dominates over 75% of India's artificial sweetener market. With revenues of ₹2,729 crore and operations across three continents, this subsidiary of pharmaceutical giant Zydus Lifesciences has quietly built one of India's most intriguing consumer goods stories.

But here's what makes this tale fascinating: Unlike Hindustan Unilever or Nestlé, which leveraged global playbooks, Zydus Wellness emerged from pharmaceutical DNA, creating categories that didn't exist and educating consumers about problems they didn't know they had. This is the story of how a company born in 1994 as a margarine manufacturer became India's wellness gatekeeper, navigating family splits, billion-dollar acquisitions, and the peculiar challenge of selling health to a nation simultaneously battling malnutrition and diabetes.

The journey weaves through three distinct acts: the pharmaceutical heritage that provided credibility, the patient category-building that created moats, and the aggressive M&A that transformed scale. Along the way, we'll explore how Zydus mastered the art of turning medical expertise into consumer trust, why they paid ₹4,595 crore for Heinz India's portfolio, and what their 5.91% ROE really tells us about the wellness business in India.

This isn't just a corporate chronicle—it's a masterclass in building brands at the intersection of healthcare and consumer goods, where science meets shopping carts, and where the real competition isn't other companies but consumer habits formed over centuries.

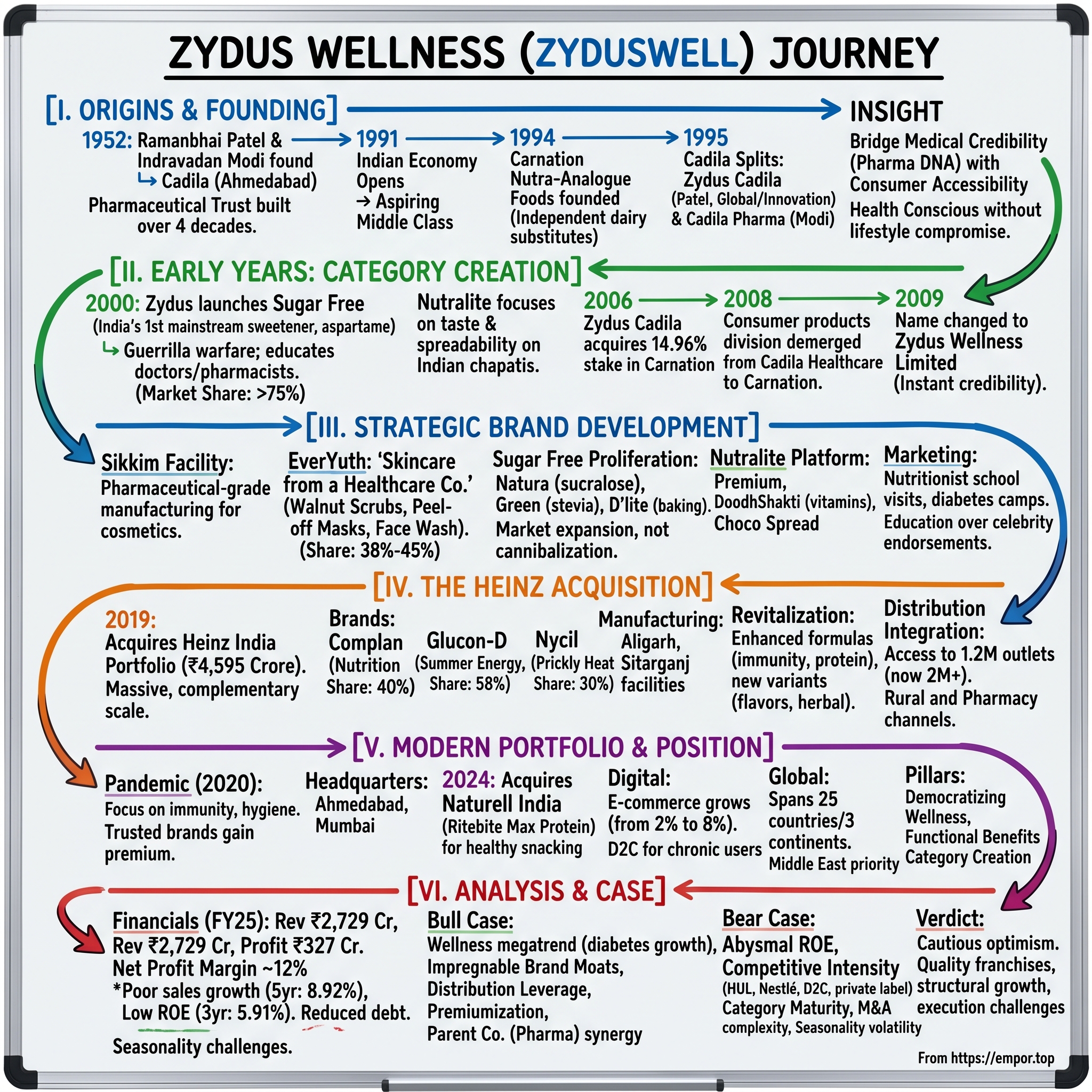

II. The Zydus Group Origins & Founding Context

The monsoon of 1952 brought more than rain to Ahmedabad. In a modest office near the old city, two friends—Ramanbhai Patel and Indravadan Modi—shook hands on a partnership that would reshape Indian healthcare. They called their venture Cadila, a name that would eventually spawn two pharmaceutical empires and, unexpectedly, revolutionize how Indians think about wellness.

Patel, a pharmacy professor turned entrepreneur, brought academic rigor. Modi, with his business acumen and appetite for risk, brought commercial instinct. Together, they navigated the License Raj, building Cadila into one of India's pharmaceutical pioneers. For four decades, they manufactured everything from antibiotics to vitamins, establishing the trust that would later prove invaluable in consumer markets.

But like many Indian business partnerships, this one couldn't survive generational transition. In 1995, after 43 years of collaboration, the families split. The division was surgical: Modi took Cadila Pharmaceuticals, focusing on domestic formulations. Patel kept Cadila Healthcare (later Zydus Cadila, now Zydus Lifesciences), eyeing global markets and innovation. This wasn't acrimonious—both families maintained respect—but it forced each to chart independent paths. For Patel's wing, consumer products weren't immediately obvious. Yet buried in the pharmaceutical mindset was a crucial insight: Indians trusted doctors and pharmacists more than advertisers. If you could bridge the gap between medical credibility and consumer accessibility, you had gold.

The timing was electric. India's economy had opened in 1991, unleashing middle-class aspirations and anxieties in equal measure. Diabetes rates were climbing—the bitter fruit of newfound prosperity. Heart disease stalked urban India. Yet the wellness industry remained primitive, dominated by unbranded products and folk remedies.

In 1994, while the Modi and Patel families were still sorting their corporate divorce, a small venture called Carnation Nutra-Analogue Foods was founded as a producer of dairy substitutes. This wasn't Patel's direct initiative—it operated independently, manufacturing margarine and cheese substitutes in a modest facility. But Patel's son, Pankaj, watched with interest. Here was a company applying food technology to health problems, exactly the bridge between pharma and consumer that could differentiate Zydus.

The mid-1990s Indian consumer landscape was peculiar. Urban Indians wanted Western products but with Indian validation. They craved health but loved sweets. They worried about cholesterol but couldn't give up ghee. Carnation Nutra-Analogue Foods stumbled into this contradiction, producing "healthy" versions of indulgent foods.

By 2000, as India's GDP crossed $500 billion and lifestyle diseases exploded, Pankaj Patel saw the opportunity clearly. The Zydus pharmaceutical business was thriving, but growth required either global expansion (expensive and risky) or adjacent markets (leveraging existing strengths). Consumer wellness offered the latter—a chance to monetize pharmaceutical credibility without pharmaceutical regulations.

The consumer products division strategy crystallized around three pillars: leverage the Zydus trust halo, focus on functional benefits over lifestyle marketing, and distribute through both modern retail and traditional pharma channels. This wasn't about competing with Hindustan Unilever on advertising budgets—it was about creating a new category at the intersection of health and habit.

In a pivotal move, the consumer products division of Cadila Healthcare Ltd was demerged and transferred to Carnation (soon to be Zydus Wellness) with effect from April 1, 2008. This wasn't just administrative reshuffling—it signaled serious intent to build a consumer empire distinct from, yet supported by, the pharmaceutical parent.

What followed was classic Patel strategic patience. While competitors rushed to launch me-too products, Zydus Wellness would focus on category creation. While others fought for market share in crowded segments, they would educate consumers about problems they didn't know needed solving. The foundation was set for a three-decade journey from margarine maker to wellness major, but first, they needed to find their breakthrough product—something that could establish credibility and generate cash for expansion.

III. Early Years: From Dairy Substitutes to Sugar-Free Pioneer (1994–2010)

The Ahmedabad factory floor in 1995 smelled of heated vegetable oil and unfulfilled ambition. Workers in white coats carefully monitored temperature gauges as pale yellow liquid transformed into Nutralite—India's answer to butter that wouldn't clog your arteries. Sales were dismal. Indians, it turned out, didn't want healthy butter. They wanted butter, period.

Carnation Health Foods Limited was incorporated on November 1, 1994, operating from a small facility that felt more like a research lab than a factory. The founders had bet that post-liberalization India would embrace Western-style health consciousness. They were half right—Indians were becoming health conscious, but on their own terms.

The early product portfolio reads like a wishlist of Western health foods poorly translated for Indian kitchens: table margarine, cheese substitutes, low-cholesterol spreads. The company bleeding cash, struggling to convince Indian housewives that their rotis needed imported health concepts. Monthly sales meetings became exercises in creative euphemism—"building consumer awareness" meant nobody was buying.

Then came the insight that changed everything. During a routine market visit in 1998, a sales executive noticed something odd in a Gujarati sweet shop. The owner, a diabetic, was experimenting with saccharin tablets, crushing them to sweeten his tea. When asked why not just avoid sugar, he laughed: "Give up tea? Are you mad?"

This was the Indian paradox in miniature—health consciousness without lifestyle compromise. Indians wouldn't give up sweets, but they'd gladly pay for permission to indulge. The company pivoted hard, acquiring technology to produce aspartame-based sweeteners and launching Sugar Free in 2000.

The Sugar Free launch was guerrilla warfare against consumer habits. The company couldn't afford television advertising, so they went where trust lived—doctor's clinics and pharmacy counters. Sales representatives, trained like pharmaceutical detailers, educated doctors about artificial sweeteners. Samples flooded diabetic clinics. The message was clinical, not aspirational: "Doctor-recommended sugar substitute."

By 2005-06, the company increased the production capacity of Margarine from 3928 MT to 5500 MT, but the real story was Sugar Free's explosion. Within five years, it captured over 82% of India's artificial sweetener market—not by stealing share but by creating the category itself.

The Nutralite transformation paralleled Sugar Free's success. Over the next decade, its margarine product Nutralite became the largest selling margarine brand in India. The key wasn't health messaging but taste and spreadability. Indian breads were different from Western ones—thicker, often cold. Nutralite's formulation evolved through hundreds of iterations to spread smoothly on room-temperature chapatis. The corporate chess game accelerated in 2006. Zydus Cadila acquired a 14.96% stake in Carnation Nutra-Analogue Foods for Rs 11 crore at Rs 145 per share. This wasn't a hostile takeover but strategic alignment—Carnation needed capital and credibility; Zydus wanted consumer presence without building from scratch.

By 2008, Zydus had increased its stake to over 61.5%, effectively controlling the company. The integration was smooth because both companies shared DNA—scientific rigor, quality obsession, and belief in functional benefits over lifestyle marketing. As per the scheme of arrangement, the consumer products division of Cadila Healthcare Ltd was de-merged and transferred to the company with effect from April 1, 2008.

The name change on January 5, 2009, from Carnation Nutra-Analogue Foods to Zydus Wellness Limited wasn't cosmetic—it signaled transformation from contract manufacturer to brand builder. The Zydus prefix brought instant credibility, especially important as the company expanded beyond sweeteners into broader wellness.

The Sugar Free variants proliferated strategically. Sugar Free Gold became India's largest selling aspartame-based sweetener with over 75% market share. Sugar Free Natura, made from sucralose, targeted premium users who read ingredient labels. Sugar Free Green, with stevia, captured the natural movement. Each variant wasn't cannibalization but market expansion—different sweeteners for different occasions and consumers.

Distribution became the moat. While competitors focused on modern retail, Zydus Wellness built a hybrid network—pharmacies for credibility, kirana stores for reach. The sales force was unique: part pharmaceutical detailer, part FMCG salesman. They could explain glycemic index to doctors and margin structures to retailers.

The numbers validated the strategy. Post-acquisition in FY 06-07, Nutralite grew over 25% year-on-year. Sugar Free's 82% market share wasn't just dominance—it was category ownership. By 2010, the company had manufacturing facilities producing at scale, distribution reaching tier-3 cities, and brand equity that competitors couldn't replicate with advertising alone.

Yet challenges persisted. Seasonality plagued certain products. Consumer education remained expensive. Competition intensified as multinationals noticed the wellness opportunity. The company needed to expand beyond niche products to achieve scale. The foundation was solid, but the edifice needed more floors. What came next would transform Zydus Wellness from successful niche player to diversified wellness conglomerate.

IV. Building the Portfolio: Strategic Brand Development (2000s–2010s)

The Sikkim factory inauguration in 2009 was deliberately theatrical. Pankaj Patel flew in board members, distributors, even select doctors. The message was clear: Zydus Wellness wasn't just another FMCG company churning out me-too products. The state-of-the-art facility, with its pharmaceutical-grade clean rooms and quality control labs, would manufacture products that bridged medicine and daily consumption.

EverYuth, launched in the mid-2000s, embodied this philosophy perfectly. While Fair & Lovely sold aspiration and Ponds sold heritage, EverYuth sold science. The tagline—'skincare brand from a healthcare company'—wasn't marketing fluff but strategic positioning. Each product came with clinical explanations: walnut scrubs with precise particle sizes, peel-off masks with measured absorption rates, face washes with pH specifications.

The R&D approach was distinctly pharmaceutical. Where competitors might test a face cream on 50 volunteers, Zydus conducted trials with hundreds, documenting everything from skin hydration levels to allergic reactions. The packaging included insert leaflets, unusual for cosmetics but standard for medicines. Dermatologists received samples and efficacy data, turning them into unofficial brand ambassadors.

Sugar Free's evolution during this period was masterful category expansion. The company recognized that artificial sweeteners weren't just sugar substitutes but lifestyle enablers. Sugar Free D'lite emerged for baking—heat-stable formulations that wouldn't break down in ovens. Sugar Free tablets for tea, sachets for desserts, drops for beverages—each format solved specific use cases.

The manufacturing strategy reflected pharmaceutical heritage. The Sikkim facility wasn't chosen for tax benefits alone but for water quality and climate stability crucial for sensitive formulations. Production lines were segregated to prevent cross-contamination between sweeteners and cosmetics. Quality control tested not just final products but raw materials, in-process samples, and stability under various storage conditions.

Nutralite's transformation from margarine to platform brand showed strategic patience. The company resisted quick extensions, spending years perfecting each variant. Nutralite Premium targeted health-conscious upper-middle-class consumers. Nutralite DoodhShakti, fortified with vitamins, addressed nutritional deficiencies. The chocolate spread competed not on taste alone but on healthier fat composition.

Marketing remained unconventional. While Hindustan Unilever spent hundreds of crores on celebrity endorsements, Zydus Wellness invested in education. Nutritionists visited schools explaining healthy fats. Diabetes camps distributed Sugar Free samples. Dermatologists received continuing medical education about skincare ingredients. The approach was slower but built deeper trust.

The digital revolution caught the company at an inflection point. Younger consumers researched ingredients online, compared international products, demanded transparency. Zydus Wellness responded by making product information exhaustively available—complete ingredient lists, manufacturing processes, clinical trial summaries. Where competitors hid behind proprietary formulas, Zydus embraced radical transparency.

Channel management evolved sophisticatedly. Modern retail demanded different packaging sizes, promotional schemes, and supply chain precision. Traditional trade needed credit terms and retailer education. E-commerce required detailed product descriptions and customer service capabilities. The company built parallel systems, each optimized for its channel's unique demands.

By 2015, the portfolio architecture was clear: Sugar Free owned artificial sweeteners, EverYuth competed in specialized skincare, Nutralite expanded healthy alternatives. Each brand had distinct positioning but shared the Zydus DNA—functional benefits, scientific credibility, and trust through transparency.

International expansion began tentatively. The Middle East, with its high diabetes prevalence and Indian diaspora, proved receptive. Sugar Free launched in UAE and Saudi Arabia through local distributors. The approach was conservative—test markets, learn regulations, adapt formulations for local preferences before scaling.

The period also saw strategic restraint. Despite temptations to enter adjacent categories—health drinks, nutritional supplements, baby care—the company stayed focused. Each new product underwent rigorous evaluation: Did it leverage existing capabilities? Could it achieve leadership position? Would it enhance or dilute brand equity?

Financial discipline remained paramount. Unlike venture-funded D2C brands that prioritized growth over profitability, Zydus Wellness obsessed over unit economics. Marketing spending was tracked to rupee-level ROI. Inventory management prevented working capital bloat. The approach was unfashionable but sustainable.

Yet cracks appeared in the growth story. Market shares stabilized—Sugar Free at 75-80%, Nutralite at 60-65% in margarine. Growing beyond niche markets required either category expansion (risky and expensive) or acquisition (opportunistic but rare). The company generated solid profits but faced the classic mid-size company dilemma: too small for global scale, too large for niche comfort.

The board meetings in 2017-2018 were increasingly focused on one question: How to achieve the next level of growth? Organic expansion would take decades. New categories meant competing against entrenched giants. International markets required massive investments. The answer, when it came, would transform not just Zydus Wellness but India's consumer wellness landscape—the audacious acquisition of Heinz India's portfolio.

V. The Game-Changing Heinz Acquisition (2019)

The phone call came on a humid Mumbai evening in August 2018. Kraft Heinz's global strategy team wanted to meet—discretely. The American giant was retreating from emerging markets, focusing on core geographies. Their Indian portfolio—iconic brands generating ₹1,000+ crore revenue—was for sale. Pankaj Patel immediately flew to Mumbai, knowing this was the opportunity Zydus had waited decades for.

The portfolio was mouth-watering: Complan, the 50-year-old nutrition brand that had nourished generations; Glucon-D, synonymous with summer energy; Nycil, the prickly heat powder in every Indian household; and Sampriti Ghee, a regional player with national potential. These weren't just brands but cultural institutions. More importantly, they came with two manufacturing facilities—Aligarh and Sitarganj—and distribution reaching 1.2 million outlets.

The boardroom debates were fierce. ₹4,595 crore was massive—nearly twice Zydus Wellness's market capitalization. Conservative board members worried about debt, integration challenges, and culture clash between American-built brands and Gujarati management style. Pankaj Patel's response was data-driven: these brands had 60-70% market shares in their categories, generated 20%+ EBITDA margins, and complemented Zydus's existing portfolio perfectly.

The strategic rationale was compelling. Glucon-D's summer seasonality balanced Sugar Free's year-round sales. Complan's child nutrition expertise could extend to adult segments. Nycil's personal care presence strengthened the EverYuth platform. Most crucially, the distribution network would give Zydus's existing brands unprecedented reach overnight.

Due diligence revealed surprises. Heinz had under-invested in brand building for years, coasting on legacy equity. Complan's formula hadn't been updated in a decade despite nutritional science advances. Glucon-D's packaging looked dated. Nycil had no variants despite changing consumer preferences. These weren't problems but opportunities—Zydus's R&D and marketing capabilities could revitalize sleeping giants.

The negotiation was a masterclass in strategic patience. Kraft Heinz initially demanded ₹5,500 crore, pointing to brand value and market leadership. Zydus countered with ₹3,800 crore, highlighting required investments and integration costs. Six months of back-and-forth, involving investment bankers, lawyers, and consultants, finally settled at ₹4,595 crore—expensive but fair.

Financing structure showed financial engineering sophistication. Rather than loading debt on Zydus Wellness alone, the company created a special purpose vehicle. Cadila Healthcare (the parent) co-invested, spreading risk. Banks provided acquisition financing at competitive rates, confident in cash flow generation. The structure preserved flexibility while managing leverage.

The company entered into a Share Purchase Agreement jointly with Cadila Healthcare Limited to acquire 100% shareholding of Heinz India Private Limited. The Company along with its wholly owned entity Zydus Wellness - Sikkim, paid a consideration amount of Rs 4,667.36 Crores (which includes payment towards cash and bank balance of Rs 125 Crores in Heinz) and acquired 100% shareholding.

Integration planning began before deal closure. McKinsey consultants mapped synergies—procurement savings, distribution optimization, overhead reduction. HR teams planned cultural integration, identifying key talent to retain. IT systems were evaluated for compatibility. Marketing teams developed brand revitalization strategies. Nothing was left to chance.

January 30, 2019—deal closure day—was orchestrated precisely. Press releases emphasized continuity for consumers and opportunities for employees. Town halls addressed anxieties. Distributors received assurance letters. The message was consistent: Zydus would preserve what made these brands special while investing for growth.

The first 100 days post-acquisition were crucial. Manufacturing teams visited Aligarh and Sitarganj facilities, impressed by infrastructure but identifying improvement areas. Quality control systems were upgraded to Zydus standards. Procurement was centralized, immediately yielding 5-7% cost savings through scale. Sales forces were merged carefully, preserving relationships while eliminating redundancy.

Brand revitalization began immediately. Complan's formula was enhanced with immunity-boosting ingredients. Glucon-D launched flavored variants and convenient packaging. Nycil introduced cool herbal and lavender variants. The changes were incremental—drastic repositioning would confuse loyal consumers—but meaningful.

Distribution integration exceeded expectations. Zydus's products gained access to Heinz's rural network. Heinz brands benefited from Zydus's pharmacy presence. Cross-selling opportunities emerged—retailers stocking Complan also took Sugar Free for diabetic consumers. The combined entity reached 2+ million outlets, rivaling FMCG giants.

Financial impact was immediate and impressive. Q1 FY2020 revenues jumped to ₹600+ crore from ₹250 crore pre-acquisition. Market share in key categories strengthened. Operating margins improved through synergies. The stock market responded positively, with market capitalization crossing ₹10,000 crore.

Yet challenges emerged. Integrating different corporate cultures—American process orientation versus Indian flexibility—created friction. Some key Heinz employees left, taking institutional knowledge. IT system integration proved complex and expensive. Inventory management during transition caused temporary stock-outs.

The Heinz acquisition transformed Zydus Wellness from niche player to mainstream force. Revenue scale provided negotiating power with retailers. Portfolio breadth attracted better talent. Marketing budgets could support television campaigns. International expansion became feasible with credible brand portfolio.

The acquisition's success validated Pankaj Patel's vision: building an Indian consumer wellness champion through strategic M&A, not just organic growth. It proved that pharmaceutical companies could successfully enter consumer markets by leveraging trust and scientific capability. Most importantly, it positioned Zydus Wellness for the next phase—becoming a ₹5,000 crore wellness conglomerate competing with multinationals on equal terms.

VI. Modern Portfolio & Market Position (2020–Present)

The pandemic morning of March 25, 2020, found Tarun Arora, CEO of Zydus Wellness, in crisis mode. Lockdowns had shuttered retail outlets, factories faced worker shortages, and consumer behavior was shifting unpredictably. Yet within this chaos lay opportunity—health consciousness was exploding, immunity became currency, and trusted brands gained premium. The next three years would accelerate Zydus Wellness's evolution by a decade.

The current portfolio reads like a masterclass in category architecture. Food & Nutrition anchors the company—Glucon-D dominates 58% of glucose powder market, Complan holds 40% in health food drinks, and Sugar Free maintains 75% in artificial sweeteners. Personal Care provides growth engines—Everyuth commands specialized segments like peel-off masks (45% share) and walnut scrubs (38% share), while Nycil owns 30% of prickly heat powder despite seasonal dependence. The November 2024 acquisition of Naturell India for ₹390 crore represents the latest strategic masterstroke. The group acquired Naturell India, a maker of healthy snacks such as nutrition bars and protein chips, for Rs 390 crore. Naturell produces a range of nutrition bars, protein cookies, bars, crisps, spreads and powders under the brand Ritebite Max Protein and high-fibre snacks under Ritebite. This wasn't just product addition but category entry—protein snacking, the fastest-growing wellness segment globally.

The manufacturing footprint now spans impressive scale. Headquartered in Ahmedabad and Mumbai, the company has 4 manufacturing facilities across 3 locations - Aligarh, Ahmedabad and Sikkim. They also have 18 co-manufacturing facilities in India, UAE, and New Zealand. This infrastructure supports not just volume but complexity—different products require different environments, from sterile sweetener production to cosmetic manufacturing.

Nutralite's evolution showcases portfolio sophistication. Beyond margarine, it now includes mayonnaise (three flavors for retail), chocolate spreads competing with Nutella, DoodhShakti butter fortified with vitamins, and even ghee alternatives. Each extension was meticulously planned—consumer research, pilot launches, national rollouts only after proving product-market fit.

Product innovation accelerated post-pandemic. Sugar Free D'lite targets baking enthusiasts. I'm Lite addresses weight management holistically. Complan variants now include immunity boosters, protein enhancement, and flavor innovations. Glucon-D expanded beyond orange to nimbu pani, mango, and regular variants. Even Nycil, seemingly mature, launched body mists and herbal variants.

The digital transformation deserves special mention. E-commerce contribution jumped from 2% pre-pandemic to 8% currently. Direct-to-consumer platforms enable consumer data collection, rapid testing, and margin improvement. Social media marketing targets younger demographics previously unreachable through traditional channels. Influencer partnerships make wellness aspirational, not medical.

Geographic expansion continues methodically. Today the Zydus Wellness business spans over 25 countries and 3 continents. The Middle East remains priority—high diabetes prevalence, Indian expatriate community, and cultural alignment. Southeast Asia offers growth through ethnic Indian populations. Africa presents longer-term opportunity as middle classes emerge.

Rural penetration strategy differs from urban approach. Smaller pack sizes (₹5 sachets), local language communication, and retailer education drive adoption. Rural consumers, increasingly health-conscious post-COVID, represent 40% of sales for certain brands. The distribution network reaches 600,000+ villages, leveraging both direct coverage and wholesale partners.

Premiumization runs parallel to democratization. While ₹5 sachets expand access, premium variants target affluent consumers. Sugar Free Green (stevia-based) costs 3x regular variants. Complan Memory+ targets parents willing to pay premiums for perceived cognitive benefits. Everyuth's gold face masks and serums compete with international brands at premium price points.

The competitive response has been interesting. Dabur launched sugar-free variants. Emami expanded health foods. Patanjali entered multiple categories. Yet Zydus maintains leadership through first-mover advantages, distribution depth, and trust equity. Competitors can copy products but not the decades of consumer relationships.

Regulatory navigation showcases institutional capability. Food Safety Standards Authority approvals, drug controller permissions for nutraceuticals, advertising standards compliance—each requires specialized expertise. The company's pharmaceutical heritage provides advantage in regulatory management that pure FMCG players lack.

Sustainability initiatives, while nascent, signal future direction. Recyclable packaging, water conservation in manufacturing, and farmer partnerships for raw materials address ESG concerns. These aren't just compliance but increasingly influence consumer choice, especially among millennials.

The supply chain transformation post-COVID built resilience. Multiple sourcing strategies prevent disruption. Inventory management balances availability with working capital. Predictive analytics improve demand forecasting. Technology investments—ERP upgrades, warehouse automation, route optimization—improve efficiency while reducing costs.

Yet challenges persist. The company has delivered a poor sales growth of 8.92% over past five years. Company has a low return on equity of 5.91% over last 3 years. Integration complexity from multiple acquisitions strains management bandwidth. Category expansion dilutes focus. Premium positioning limits mass market penetration.

The portfolio today represents three decades of patient building—from margarine manufacturer to wellness conglomerate spanning nutrition, personal care, and healthy snacking. With recent acquisitions integrated and innovation pipeline robust, Zydus Wellness stands at an inflection point. The question isn't whether it can grow but how fast and how profitably.

VII. Business Model & Financial Performance

The spreadsheet on CFO Umesh Parikh's desk tells a story of transformation and tension. Revenue of ₹2,729 crore with profit of ₹327 crore looks impressive until you calculate the margins—12% net profit margin in a sector where Nestlé achieves 15%+ and Hindustan Unilever delivers 18%+. The numbers reveal both the promise and puzzle of Zydus Wellness: strong brands generating modest returns. The revenue model architecture reveals strategic complexity. Food & Nutrition contributes 60% of revenues but faces seasonality—Glucon-D peaks in summer, while Complan sells year-round. Personal Care adds 25%, with Everyuth providing stability and Nycil creating seasonal spikes. The remaining 15% comes from emerging categories and international markets.

Zydus Wellness Ltd reported a 14.4 per cent rise in consolidated net profit at Rs 171.9 crore in the fourth quarter ended March 31, 2025, with consolidated total revenue from operations in the fourth quarter at Rs 910.6 crore, compared to Rs 778 crore in the year-ago period. This 17% revenue growth demonstrates momentum, but dig deeper and complexities emerge.

The margin structure tells a nuanced story. Gross margins hover around 65%—impressive until you consider advertising expenses consume 15-18% of revenues. Distribution costs eat another 12-15%. Administrative expenses, inflated by multiple acquisitions, consume 8-10%. What remains is respectable but not spectacular operating profit.

The company has delivered a poor sales growth of 8.92% over past five years and has a low return on equity of 5.91% over last 3 years. These metrics reveal the fundamental challenge: generating adequate returns from capital-intensive acquisitions while competing against both nimble startups and deep-pocketed multinationals.

Channel economics vary dramatically. Modern retail delivers 40% gross margins but demands listing fees, promotional support, and inventory management precision. Traditional trade offers 35% margins with simpler operations but requires extensive credit management. E-commerce promises 45% margins but comes with high customer acquisition costs and return rates.

The working capital cycle deserves attention. Inventory turns 6-7 times annually—decent but not exceptional. Receivables stretch to 45-50 days as the company balances growth with credit risk. Payables average 60 days, providing modest negative working capital benefit. The cash conversion cycle of 35-40 days requires constant treasury management.

Company has reduced debt and is almost debt free. This financial conservatism provides flexibility but raises questions about capital allocation efficiency. With minimal leverage, the company forgoes tax shields and potentially higher returns from judicious borrowing.

Geographic profitability varies significantly. Domestic operations generate 15% EBITDA margins through scale and brand recognition. International markets deliver 8-10% margins as the company invests in distribution and brand building. The Middle East shows promise with 12% margins, benefiting from Indian diaspora familiarity.

The cost structure evolution post-acquisitions reveals integration challenges. Employee costs jumped from 8% to 11% of revenues as duplicate functions persist. Manufacturing efficiency improved marginally—capacity utilization increased from 65% to 72%—but remains below optimal 80-85% levels. Procurement synergies delivered ₹50-60 crore annual savings, less than projected ₹80-100 crore.

Marketing spend allocation shows strategic focus. Television advertising consumes 40% of marketing budgets, concentrated on power brands like Complan and Glucon-D. Digital marketing takes 25%, growing rapidly. Trade promotion absorbs 20%. The remaining 15% goes to consumer activation, sampling, and events. The ROI varies: TV delivers 1.3x, digital 1.8x, trade promotion 1.1x.

R&D investment, at 1.5% of revenues, seems modest compared to global FMCG standards of 2-3%. However, the company leverages parent Zydus Lifesciences' research capabilities, accessing pharmaceutical-grade facilities and expertise without full cost burden. This symbiotic relationship provides competitive advantage difficult to replicate.

Distribution metrics reveal both strength and opportunity. The company reaches 2+ million outlets—impressive breadth. However, throughput per outlet remains low, with 60% of outlets ordering less than ₹1,000 monthly. Improving outlet productivity through better merchandising, increased SKUs per outlet, and consumption activation could significantly boost revenues without expanding reach.

The seasonality challenge persists despite portfolio diversification. Q1 (April-June) contributes 35% of annual revenues driven by summer products. Q4 (January-March) adds 28% with year-end promotions. Q2 and Q3 remain relatively weak at 18-19% each. This seasonality complicates manufacturing planning, inventory management, and cash flow forecasting.

The food and nutrition segment maintained its upward trajectory, registering quarterly growth of 15.4 per cent and 13 per cent growth for FY25. This segment's consistent performance provides stability, but personal care's volatility—growing 20% in good quarters, declining 5% in weak ones—creates overall uncertainty.

International expansion economics remain challenging. Regulatory compliance costs, often underestimated, consume 2-3% of international revenues. Currency hedging, while necessary, reduces margins by 50-100 basis points. Local competition forces aggressive pricing, limiting premium positioning that works domestically.

The dividend policy reflects conservative capital allocation. The board has recommended a final dividend of Rs 6 per equity share of Rs 10 subject to approval of shareholders. This 60% payout ratio balances shareholder returns with retained earnings for growth, though some investors question whether higher dividends or aggressive expansion would create more value.

Looking forward, the path to ₹5,000 crore revenues requires 15% annual growth—achievable but demanding. Margin improvement to 15% net profit needs operational excellence, premium mix enhancement, and cost rationalization. The recent Naturell acquisition should contribute ₹200-300 crore revenues at better margins, but integration execution remains critical.

The financial performance ultimately reflects a company in transition—from niche player to mainstream competitor, from organic growth to acquisition-led expansion, from founder-driven to professionally managed. The numbers tell a story of solid execution with room for improvement, strategic vision with implementation challenges, and market leadership with profitability pressures.

VIII. Competitive Landscape & Market Dynamics

The war room at Zydus Wellness headquarters maps competitive battles across multiple fronts. On one wall, market share charts show Sugar Free's 75% dominance but also Dabur's aggressive entry with Dabur Honey substitutes. Another display tracks Glucon-D's seasonal combat with PepsiCo's Gatorade and Coca-Cola's energy drinks. The complexity is overwhelming—each category has different competitors, dynamics, and success factors.

The Indian wellness market represents a ₹45,000 crore opportunity growing at 15% annually, but defining "wellness" itself sparks debate. Does Bournvita qualify? What about Yakult? The boundaries blur as every FMCG company claims health benefits. In this ambiguous battlefield, Zydus Wellness must defend existing positions while capturing new territory.

Market share data reveals concerning trends. The company's overall FMCG market share decreased from 2.28% to 1.69% over 5 years—not because brands weakened but because the market exploded faster than Zydus could capture. New categories emerged—protein bars, immunity boosters, gut health products—where Zydus had no presence until recently.

The competitive set varies dramatically by category. In artificial sweeteners, traditional competition comes from Sweeten, Sugarlite, and Equal. But the real threat emerges from natural alternatives—stevia brands like Swee10 and monk fruit sweeteners targeting premium consumers. Each requires different competitive responses.

Pharmaceutical companies increasingly eye consumer wellness. Sun Pharma launched Suncros skincare. Dr. Reddy's expanded OTC products. Mankind Pharma acquired Prega News and entered consumer health aggressively. These competitors share Zydus's pharmaceutical heritage, neutralizing a key differentiator.

Traditional FMCG giants bring different strengths. Hindustan Unilever leverages global R&D and massive advertising budgets. Nestlé applies nutrition science and premium positioning. Dabur emphasizes Ayurvedic heritage. Marico focuses on specific categories with deep expertise. Each forces Zydus to compete on multiple dimensions simultaneously.

The D2C disruption cannot be ignored. Brands like Wellbeing Nutrition, OZiva, and MyProtein target millennials with Instagram-friendly packaging and influencer marketing. They lack Zydus's distribution but move faster, experiment boldly, and capture mindshare among trend-conscious consumers. Zydus's response—launching e-commerce exclusive variants—seems defensive rather than innovative.

Private label emergence pressures margins. Reliance's Wellness brand, Amazon's Solimo, and BigBasket's BB Royal offer similar products at 20-30% lower prices. While quality-conscious consumers stick with brands, price-sensitive segments increasingly switch. The phenomenon particularly impacts commodity categories like glucose powder and talcum powder.

Regional players provide guerrilla competition. Local glucose powder brands undercut Glucon-D by 40% in rural markets. Regional cosmetic brands offer "natural" alternatives to Everyuth at lower prices. These competitors lack scale but possess local market knowledge and relationships that Zydus struggles to match.

The Patanjali phenomenon deserves special attention. Baba Ramdev's brand disrupted every category with Ayurvedic positioning and aggressive pricing. While initial momentum slowed, Patanjali forced all players, including Zydus, to launch herbal variants and reconsider pricing strategies. The impact transcended direct competition—it changed consumer expectations permanently.

Category creation versus participation presents strategic dilemmas. Zydus created artificial sweeteners but must now defend against dozens of competitors. Alternatively, entering established categories like protein bars means fighting entrenched players. The sweet spot—categories nascent enough for leadership but developed enough for scale—remains elusive.

Channel dynamics shift competitive advantages. In modern retail, visibility and merchandising matter most—favoring companies with trade marketing expertise. In e-commerce, ratings and search optimization determine success—benefiting digital-native brands. In traditional trade, relationships and credit terms remain crucial—advantaging established players like Zydus.

The premiumization trend creates opportunities and threats. Premium segments grow faster and offer better margins, attracting all competitors. Zydus's attempts—Sugar Free Green, Complan Memory+—compete against specialized premium brands with authentic positioning. The challenge: appearing premium while maintaining mass market volumes.

Regulatory changes alter competitive dynamics. The Food Safety and Standards Authority's stricter labeling requirements favor organized players like Zydus. However, regulations also prevent certain health claims, limiting differentiation opportunities. The upcoming front-of-pack labeling rules could significantly impact sugar-heavy products across the industry.

Consumer behavior evolution reshapes competition. Post-COVID health consciousness benefits all wellness players but also raises scrutiny. Consumers research ingredients, compare nutritional labels, and question marketing claims. Trust, always important, becomes paramount. Zydus's pharmaceutical heritage provides advantage but doesn't guarantee preference.

Rural market dynamics differ substantially. Here, competition comes from unorganized players offering loose products at lower prices. Sachet wars intensify as companies launch ₹1 and ₹2 SKUs. Distribution reach matters more than brand equity. Zydus's recent rural focus recognizes this reality but execution remains challenging.

The talent war impacts competitive capability. D2C brands poach FMCG marketers with equity upside. Consulting firms and startups attract top graduates. Zydus competes for talent against both traditional competitors and new-age companies, often losing to more exciting narratives or better compensation.

Innovation cycles accelerate competitive pressure. Product lifecycles shorten from years to months. Speed-to-market becomes crucial. Zydus's governance structure—subsidiary of listed company requiring multiple approvals—slows decision-making compared to founder-driven competitors or autonomous subsidiaries of multinationals.

Acquisition competition intensifies. Everyone scouts for brands—private equity funds, strategic buyers, even e-commerce platforms. Valuations escalate, making acquisitions expensive. Zydus must compete for targets against deeper-pocketed buyers while ensuring financial discipline. The Naturell acquisition succeeded, but future deals may prove costlier.

Looking ahead, competitive intensity will only increase. New categories will emerge—personalized nutrition, wellness wearables, functional foods—requiring new capabilities. Existing categories will consolidate, squeezing marginal players. Technology will reshape everything from product development to distribution. In this environment, Zydus Wellness must evolve from defender to attacker, from follower to leader, from participant to shaper. The pharmaceutical heritage provides foundation, but future success demands embracing full FMCG competitiveness while maintaining scientific credibility—a balance few achieve successfully.

IX. Playbook: Business & Investing Lessons

The conference room in Mumbai's Bombay Stock Exchange building fills with fund managers dissecting Zydus Wellness's latest investor presentation. One slide particularly catches attention: "Creating Categories, Not Just Products." This encapsulates perhaps the most powerful lesson from Zydus's journey—the value of patient category creation over aggressive market share battles.

Lesson 1: Leveraging Trust Arbitrage

The pharmaceutical-to-consumer crossover creates unique "trust arbitrage." Consumers inherently trust medical companies more than pure FMCG players. Zydus monetized this trust premium, charging 15-20% more than competitors while maintaining leadership. The key: never dilute pharmaceutical credibility for short-term gains. When Sugar Free launched, it could have used cheaper ingredients or reduced quality control. Instead, it maintained pharmaceutical-grade standards, creating a moat competitors couldn't cross.

Lesson 2: The Power of Functional Positioning

Every successful Zydus brand solves a specific problem: Sugar Free for diabetes, Glucon-D for energy, Everyuth for skin issues. This functional positioning differs from lifestyle marketing that dominates FMCG. Investors should recognize that functional benefits create stickier consumption than aspirational positioning. A diabetic won't stop using Sugar Free because a celebrity endorses another brand.

Lesson 3: Category Creation Economics

Creating categories provides better economics than competing in established ones. Sugar Free enjoys 75% market share and defines category rules. Contrast this with entering established categories where gaining 10% share requires enormous investment. The playbook: identify emerging consumer needs, invest in education, establish standards, then defend dominance. The patience required—often 5-7 years—deters most competitors.

Lesson 4: M&A as Transformation Catalyst

The Heinz acquisition demonstrates how single transactions can transform trajectories. The ₹4,595 crore price seemed expensive—4.5x revenues—but provided instant scale, distribution, and credibility. More importantly, it changed internal culture from cautious to ambitious. For investors, tracking management's M&A philosophy reveals strategic intent. Conservative acquirers often underpay but under-integrate. Aggressive acquirers overpay but transform portfolios.

Lesson 5: Distribution Leverage Multiplier

Physical distribution remains India's lasting moat. Zydus's 2+ million outlet reach took decades to build and cannot be replicated quickly. Each acquisition—Heinz, Naturell—immediately benefits from this distribution, creating revenue synergies beyond cost savings. The lesson: in emerging markets, distribution infrastructure is often more valuable than brand equity.

Lesson 6: Managing Portfolio Complexity

Zydus manages distinct categories—sweeteners, energy drinks, skincare, nutrition bars—each with different consumers, channels, and economics. This complexity challenges management but provides resilience. When Glucon-D faces weak summer, Complan compensates. When urban markets slow, rural growth continues. Portfolio diversity, properly managed, reduces risk while maintaining growth.

Lesson 7: The Conglomerate Advantage

Being a subsidiary of Zydus Lifesciences provides hidden benefits: cheaper capital, shared R&D, regulatory expertise, and crisis management capability. During COVID, pharmaceutical relationships helped secure raw materials when independent companies struggled. This conglomerate advantage—unfashionable in Western markets—remains powerful in emerging markets where institutional voids exist.

Lesson 8: Balancing Growth with Profitability

Zydus consistently chose profitability over growth—maintaining positive margins even during expansion phases. This discipline meant slower growth but sustainable business building. The company never pursued "growth at all costs" strategies that destroyed many consumer startups. For investors, this indicates management quality: builders, not flippers.

Lesson 9: Building Brands with Modest Budgets

Zydus built category-leading brands spending fraction of what multinationals invest. Sugar Free became dominant with minimal television advertising. Everyuth competed against Lakme without celebrity endorsements. The secret: leveraging credibility rather than creating aspiration. Doctor recommendations matter more than film star endorsements for health products.

Lesson 10: Navigating Seasonal Cyclicality

Products like Glucon-D (summer-focused) and Nycil (monsoon-heavy) create severe seasonality. Zydus manages this through careful working capital management, counter-seasonal launches, and geographic diversification. Investors often misinterpret seasonal weakness as structural decline. Understanding cyclicality patterns prevents costly mistakes.

Lesson 11: The Science-Marketing Balance

Zydus walks a tightrope between scientific credibility and mass market appeal. Too much science alienates consumers; too much marketing undermines trust. The balance varies by brand—Sugar Free emphasizes science, Everyuth focuses on beauty. This nuanced brand management, difficult to execute, creates competitive advantage.

Lesson 12: Rural Market Patience

Rural expansion requires different playbook: smaller SKUs, visual communication, retailer education, and extended credit. Returns take longer but last longer. Rural consumers, once convinced, show higher loyalty than urban counterparts. Zydus's patient rural building, now contributing 40% revenues, validates long-term thinking.

Lesson 13: Regulatory Navigation as Moat

Complex regulations in food and cosmetics deter new entrants. Zydus's pharmaceutical heritage provides regulatory expertise that pure FMCG companies lack. This capability—unglamorous but crucial—ensures faster product launches, fewer recalls, and better compliance. Investors should value regulatory excellence as competitive advantage.

Lesson 14: Innovation Through Acquisition

Rather than building innovation capabilities, Zydus acquires innovative companies. Naturell brought protein bars expertise impossible to develop internally. This "acquire and scale" model leverages Zydus's distribution while accessing entrepreneurial innovation. The risk: integration challenges and cultural mismatches.

Lesson 15: The Founder-Professional Balance

Pankaj Patel remains engaged but empowers professional management. This balance—vision from founders, execution from professionals—drives performance. Pure founder-driven companies often lack systems; pure professionally-managed firms may lack passion. Zydus achieves optimal balance.

For investors, these lessons translate into analytical framework: Look for companies creating categories, not just competing. Value distribution infrastructure, especially in emerging markets. Appreciate portfolio complexity that provides resilience. Recognize that sustainable growth often appears slow initially. Understand that trust, once built, provides lasting competitive advantage.

The Zydus Wellness playbook ultimately teaches that building consumer businesses in emerging markets requires different strategies than developed markets. Patient category creation beats aggressive competition. Trust matters more than aspiration. Distribution provides lasting moat. These insights, properly applied, identify future winners in India's consumer landscape.

X. Analysis & Bear vs. Bull Case

The investment committee meeting at a prominent Mumbai mutual fund runs late into the evening. The debate centers on one question: Is Zydus Wellness a value trap trading at reasonable multiples or a growth story temporarily obscured by integration challenges? The bull and bear cases, argued with equal conviction, reveal the complexity of evaluating this unique wellness player.

Bull Case: The Wellness Megatrend Compounder

The optimists see Zydus Wellness as perfectly positioned for India's wellness explosion. India's diabetes population, already 77 million, grows 5% annually—each new diabetic is a potential Sugar Free customer for life. The health food drinks market, currently ₹6,000 crore, should reach ₹15,000 crore by 2030. Zydus owns 40% of this market through Complan. These aren't cyclical trends but structural shifts driven by lifestyle changes, urbanization, and rising health consciousness.

The brand moats appear impregnable. Sugar Free's 75% market share after two decades demonstrates durability. Glucon-D's 58% share survived PepsiCo and Coca-Cola's assault. These positions resulted from first-mover advantage, category creation, and trust building—not easily replicable. New competitors must spend hundreds of crores on education and marketing to dent these franchises.

Distribution leverage accelerates with each acquisition. The 2+ million outlet network, built over 30 years, cannot be replicated. Every new product—whether acquired or launched—immediately accesses this distribution. Naturell's protein bars will reach tier-3 cities faster through Zydus than independently. This multiplication effect drives revenue synergies beyond simple cost savings.

Management's target of ₹5,000 crore revenue in coming years seems achievable. Current run rate of ₹2,700 crore needs 15% CAGR—reasonable given category growth, distribution expansion, and innovation pipeline. Rural penetration remains early stage. International markets offer untapped potential. E-commerce contribution can double. Multiple growth drivers provide confidence.

The balance sheet strength enables opportunistic M&A. Being debt-free allows quick action when opportunities arise. The Naturell acquisition demonstrates execution capability. More targets will emerge as D2C brands seek scale and founders seek exits. Zydus can consolidate fragmented categories, applying its playbook repeatedly.

Premiumization tailwinds favor Zydus. Consumers increasingly pay premiums for health products. Sugar Free Green costs 3x regular variants but grows fastest. Complan Memory+ commands 40% premium. Everyuth serums compete with international brands. This mix improvement drives margin expansion beyond volume growth.

The parent company support provides strategic advantage. Zydus Lifesciences' pharmaceutical expertise helps develop differentiated products. R&D capabilities, regulatory knowledge, and quality systems come without full cost burden. During crises, parent company resources provide resilience smaller competitors lack.

Valuation appears reasonable considering growth potential. Trading at 35-40x P/E seems expensive but reflects quality franchises and growth runway. Comparable companies like Marico trade at similar multiples with slower growth. The PEG ratio below 2 indicates relative attractiveness.

Bear Case: The Profitability Challenge

The skeptics focus on concerning fundamentals. ROE of 5.91% over three years is abysmal for a consumer company. Hindustan Unilever generates 80%+ ROE. Even struggling FMCG companies deliver 15-20%. This low return suggests either poor capital allocation or structural profitability challenges difficult to overcome.

Growth disappointments persist. Sales growth of 8.92% over five years trails industry average of 12%. Despite acquisitions and category expansion, organic growth remains mid-single digits. Market share losses in key categories suggest competitive challenges. The growth acceleration promised post-acquisitions hasn't materialized convincingly.

Integration complexity overwhelms management. Running diverse categories—sweeteners, energy drinks, nutrition, skincare—requires different capabilities. Each acquisition adds complexity. Management bandwidth gets stretched. Execution suffers. The lack of focus shows in inconsistent performance across brands.

Seasonality creates earnings volatility. Glucon-D and Nycil contribute 30% of profits but concentrate in specific quarters. Weak monsoons or cool summers significantly impact earnings. This volatility makes business planning difficult and increases risk. Investors discount volatile earnings streams.

Competition intensifies from all directions. Every pharmaceutical company enters consumer wellness. Every FMCG company claims health benefits. D2C brands proliferate. Private labels expand. The competitive intensity will pressure margins and require increased marketing spending, hurting profitability.

Category maturity limits growth. Artificial sweeteners face natural alternatives. Glucose-based energy drinks seem outdated versus sports drinks. Talcum powder usage declines globally. Many core categories face structural headwinds that innovation cannot fully offset.

The acquisition strategy raises concerns. Paying 4-5x revenues for acquisitions destroys value unless perfectly integrated. Integration track record remains mixed. Cultural differences between acquired companies and Zydus create friction. The "acquire and integrate" model works until it doesn't—one failed acquisition could destroy years of value creation.

Innovation capability seems limited. Despite pharmaceutical heritage, breakthrough innovation remains elusive. Most "new" products are variants or line extensions. True innovation—creating new categories or disrupting existing ones—hasn't happened. Without innovation, growth depends on acquisitions or market share battles.

The rural and regional skew limits premiumization. While bulls tout rural expansion, rural consumers are price-sensitive and buy smaller packs. Regional preferences limit national scaling. The mass-market positioning constrains pricing power that premium brands enjoy.

Capital allocation questions persist. Maintaining excess cash earning low returns destroys value. The conservative approach, while safe, may indicate lack of growth opportunities or management confidence. More aggressive capital deployment—higher dividends, buybacks, or transformational acquisitions—could create more value.

The Verdict: Cautious Optimism with Clear Triggers

The truth, as often, lies between extremes. Zydus Wellness owns valuable franchises in growing categories but faces execution challenges. The wellness megatrend is real but competition is equally real. The company will likely grow but not at rates justifying premium valuations.

For investors, the key monitorables are clear: ROE improvement toward 10%+ indicating better capital efficiency; organic growth acceleration beyond 10% showing brand strength; successful integration of Naturell demonstrating execution capability; market share stability in core categories proving competitive moats; and margin expansion through premiumization validating pricing power.

The investment case depends on time horizon and risk appetite. Long-term investors believing in India's wellness transformation and patient capital allocation may find value. Short-term traders seeking momentum should look elsewhere. The company represents a classic "quality at reasonable price" opportunity—neither compelling bargain nor momentum story, but solid business at fair valuation.

The bear case carries weight—profitability must improve, growth must accelerate, and execution must sharpen. But the bull case resonates too—category leadership, distribution moat, and wellness tailwinds provide sustainable advantages. The outcome depends on management execution over the next 2-3 years. The pieces are in place; assembly quality will determine success.

XI. Epilogue & Future Outlook

The sunrise view from Zydus Wellness's new Mumbai office captures India's transformation—slums giving way to towers, street food vendors beside Starbucks, yoga practitioners next to gyms. This juxtaposition mirrors Zydus's challenge: serving an India simultaneously embracing tradition and modernity, health and indulgence, premium and value.

CEO Tarun Arora's strategic plan for 2025-2030 acknowledges this complexity. The vision—"Democratizing Wellness for a Billion Indians"—sounds ambitious but reflects pragmatic recognition that growth requires serving all segments, not just affluent urban consumers. The strategy pillars reveal thoughtful evolution from acquisition-led growth to capability-driven expansion.

Digital transformation tops the priority list, but not as buzzword bingo. The company is building a unified data platform connecting consumer insights, supply chain, and financial metrics. Real-time dashboards will replace monthly reports. Predictive analytics will guide inventory and promotion decisions. The goal isn't technological sophistication but decision speed—reducing time from insight to action.

The direct-to-consumer initiative, quietly launched, shows promise. Rather than competing with e-commerce partners, Zydus focuses on subscription models for chronic-use products. Diabetics subscribing to monthly Sugar Free deliveries. Parents subscribing to quarterly Complan shipments. These predictable revenue streams improve planning while building direct consumer relationships.

Product innovation takes new direction. Instead of me-too launches, Zydus focuses on solving specific Indian problems. A glucose drink preventing dehydration in factory workers. A protein bar addressing vegetarian protein deficiency. Skincare for pollution-damaged skin. Each product emerges from consumer research, not competitive response.

The sustainability agenda, previously peripheral, becomes central. Packaging redesign reduces plastic by 30%. Manufacturing facilities target carbon neutrality by 2030. Farmer partnerships ensure sustainable sourcing. These aren't just ESG compliance but increasingly influence consumer choice, especially among millennials who will drive future growth.

International expansion adopts portfolio approach. The Middle East remains priority given diaspora connections and diabetes prevalence. Southeast Asia offers opportunity through Indian ethnic populations. Africa represents longer-term potential as middle classes emerge. But expansion is selective—entering markets where Zydus's Indian heritage provides advantage, not competing globally against multinationals.

The organizational transformation perhaps matters most. Zydus is building capabilities, not just buying brands. Digital marketing expertise through selective hiring from e-commerce companies. Data analytics through partnerships with technology firms. Innovation through collaboration with startups. The company recognizes that future success requires different skills than past success.

Cost management initiatives target structural improvements, not just overhead reduction. Automation in manufacturing and warehousing. Artificial intelligence in demand forecasting. Shared services for back-office functions. These investments require upfront capital but promise lasting efficiency gains. The target: improving EBITDA margins by 200-300 basis points over three years.

The acquisition pipeline remains active but selective. Targets must meet strict criteria: leadership position in growing categories, synergy with existing portfolio, and reasonable valuations. The focus shifts from scale acquisitions to capability acquisitions—buying expertise in emerging categories like plant-based nutrition or personalized wellness.

The regulatory landscape presents both challenges and opportunities. Stricter labeling requirements favor organized players. Front-of-pack nutrition labels could impact sugar-heavy products. But Zydus's pharmaceutical heritage provides advantage in navigating complex regulations. The company is proactively reformulating products to meet future standards.

Competition will intensify, but Zydus's positioning seems defensible. The sweet spot between pharmaceutical credibility and consumer accessibility remains unique. New entrants must choose—medical or mass market. Zydus occupies the bridge, serving consumers seeking trusted wellness products without prescription complexity.

The financial targets appear achievable if execution follows. Revenue of ₹5,000 crore requires 15% CAGR—reasonable given category growth and distribution expansion. EBITDA margins of 18-20% need operational excellence and premiumization. ROE improvement to 12-15% demands better capital efficiency and working capital management.

Yet risks persist. Economic slowdown could hurt discretionary spending on premium wellness products. Regulatory changes might impact product claims or formulations. Competition from global giants or aggressive startups could erode market share. Integration challenges from multiple acquisitions may overwhelm management bandwidth.

The investment implications are nuanced. Zydus Wellness isn't a momentum story promising explosive growth. Nor is it a value trap with deteriorating fundamentals. It's a steady compounder in a structural growth market, with execution determining the difference between 12% and 18% annual returns.

For students of business, Zydus Wellness offers rich lessons. How pharmaceutical companies can successfully enter consumer markets. How category creation provides lasting competitive advantage. How patient capital allocation compounds value. How trust, once earned, becomes the ultimate moat.

The next decade will test whether Zydus can evolve from successful regional player to national champion, from acquisition-driven to innovation-led, from wellness participant to category shaper. The foundations—brands, distribution, trust—are solid. The vision is clear. The execution will determine whether Zydus Wellness becomes India's wellness leader or remains a profitable but subscale player.

As monsoon clouds gather over Mumbai, bringing relief from summer heat, Zydus Wellness stands at its own inflection point. Three decades of patient building created a platform. The next decade will determine whether that platform launches exponential growth or supports steady but unspectacular progress. For investors, consumers, and competitors, the evolution of Zydus Wellness will reveal much about India's consumer market transformation—from price to value, from need to want, from survival to wellness.

The story continues, written daily in millions of small moments—a diabetic enjoying sweet tea, a mother mixing Complan for her child, a teenager applying Everyuth face wash. These moments, aggregated across a billion Indians, will determine whether Zydus Wellness achieves its ambitious vision or remains a successful but ultimately limited regional player. The outcome remains unwritten, but the trajectory points toward a future where wellness becomes not luxury but necessity, not aspiration but expectation, not western import but Indian expression.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube