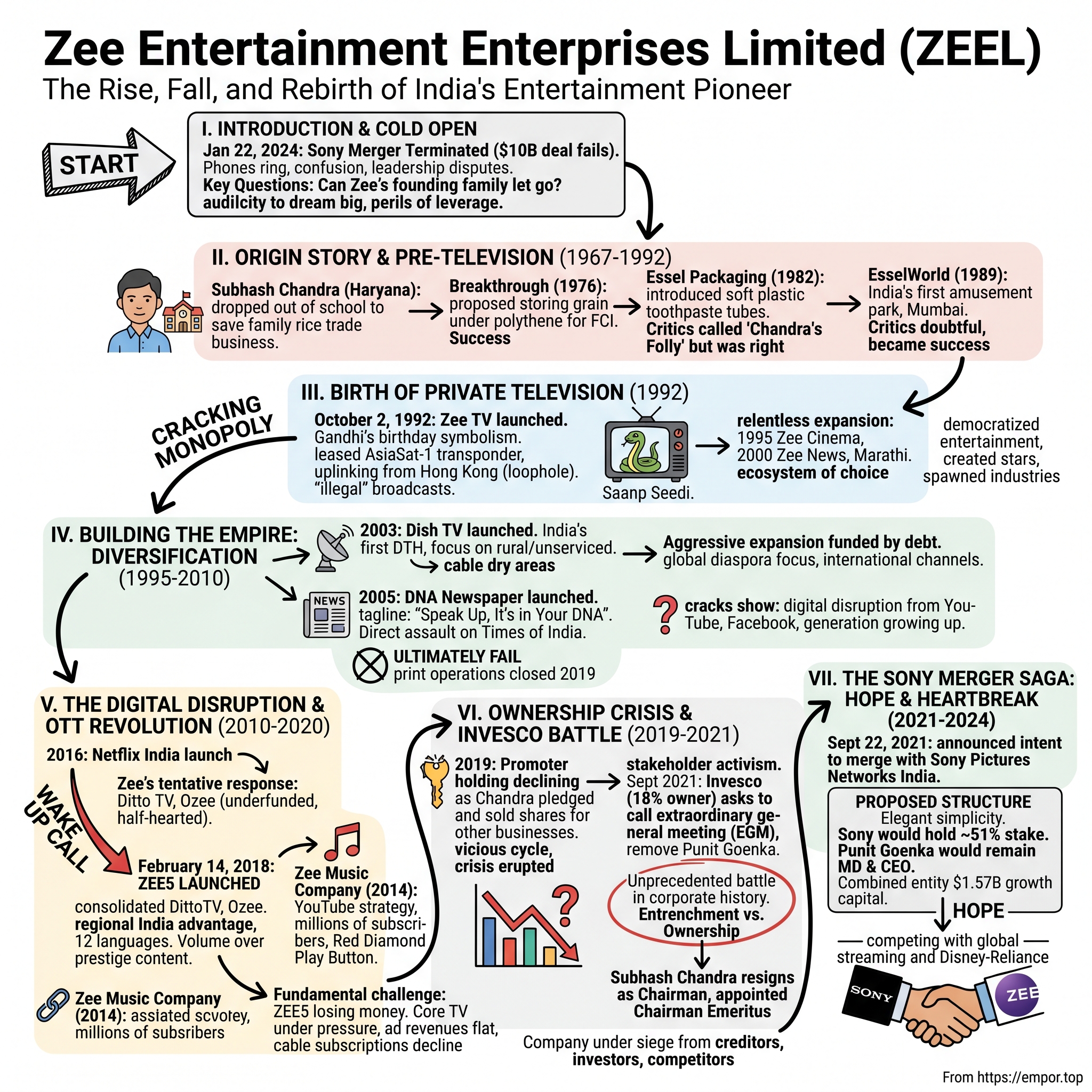

Zee Entertainment Enterprises Limited (ZEEL): The Rise, Fall, and Rebirth of India's Entertainment Pioneer

I. Introduction & Cold Open

Picture this: January 22, 2024, Mumbai's Ballard Estate. Inside the gleaming towers that house Zee Entertainment's headquarters, phones are ringing off the hook. After 26 months of negotiations, regulatory approvals, and billions in anticipated synergies, Sony has just pulled the plug on what would have been India's largest media merger—a $10 billion behemoth that would have reshaped the subcontinent's entertainment landscape. The termination letter cites "unmet conditions," but everyone knows the real story runs deeper: regulatory investigations, leadership disputes, and a fundamental question about whether Zee's founding family could truly let go.

This moment encapsulates the extraordinary arc of Zee Entertainment Enterprises Limited—a company that quite literally invented private television in India, reached 1.3 billion viewers across 174 countries, employed millions, and yet found itself on the brink of losing its independence after its founder's empire crumbled under debt. How did Subhash Chandra, a school dropout from rural Haryana who started trading rice, build India's first private broadcasting empire? How did he challenge the government monopoly, survive the satellite wars, navigate the digital disruption, and then nearly lose it all?

The Zee story isn't just about television or streaming or content. It's about the audacity to dream big in a controlled economy, the perils of leverage in pursuit of empire, and the brutal reality that in media, content may be king, but distribution and capital determine who sits on the throne. It's about a company that created an entire industry—private broadcasting in India—yet today trades at a market cap of just ₹11,214 crore, down from peaks that once made it one of India's most valuable media properties. This isn't just corporate drama—it's a window into how India's media landscape evolved, how regulatory capture gave way to market forces, and how a company that once seemed invincible now fights for relevance in a world dominated by global streaming giants and consolidated competitors. The company's market cap stands at ₹11,214 crore (down 16.5% year-over-year), while it remains almost debt-free—a remarkable turnaround from the debt crisis that nearly destroyed it.

What makes Zee's story particularly compelling for investors and students of business alike is how it mirrors India's own economic journey: from socialist controls to liberalization, from scarcity to abundance, from local to global ambitions, and now, in the digital age, from linear broadcasting to on-demand streaming. Every major inflection point in India's economic history finds reflection in Zee's corporate narrative.

As we unpack this saga, we'll explore not just what happened, but why it matters—the strategic decisions that built an empire, the leverage that nearly destroyed it, and the lessons for anyone building or investing in media businesses in emerging markets. Because ultimately, the Zee story asks a fundamental question that every media company faces today: In an age where content is abundant but attention is scarce, where does value truly lie?

II. The Subhash Chandra Origin Story & Pre-Television Days

The year was 1967 in Adampur, a dusty village in Haryana's Hisar district. Seventeen-year-old Subhash Chandra sat in his family's modest home, watching his father struggle with mounting debts from their rice trading business. The family had been traders for generations—Agarwal Banias who understood commerce in their bones—but bad harvests and poor decisions had brought them to the brink. That day, Subhash made a choice that would define his life: he dropped out of school to save the family business.

Born on November 30, 1950, Subhash wasn't supposed to become a media mogul. His destiny seemed predetermined: join the family firm Messrs Ramgopal Indraprasad, founded by his grandfather Jagannath Goenka in 1926, trade commodities, marry within the community, and pass the business to the next generation. But Subhash had something his predecessors lacked—an almost pathological appetite for risk and an ability to see opportunities where others saw only tradition. When 23-year-old Subhash took control of Messrs Ramgopal Indraprasad in 1973, the company was essentially a commodity trading house with debts of ₹3.5 lakh—a crushing sum for a small-town trading family. But Subhash had grown up watching his grandfather negotiate with traders, had learned to read market signals in the way grain prices moved with monsoons, and most importantly, had developed an instinct for spotting inefficiencies in India's controlled economy.

His first major breakthrough came in 1976 during India's bumper harvest. The Food Corporation of India (FCI) faced a crisis: 14 million tonnes of food grains with inadequate storage infrastructure. While established players wrung their hands, Subhash saw opportunity. He proposed storing grains in the open under polythene sheets—a solution so simple it seemed absurd. But it worked. The contract transformed his fortunes, and suddenly the rice trader from Haryana had capital to deploy.

This was vintage Subhash Chandra: seeing solutions where others saw problems, taking risks that seemed irrational, and having the audacity to pitch directly to power. By 1981, he'd secured an INR 16 crore deal exporting rice to the USSR under Indo-Soviet bilateral trade agreements. The Russian government renewed his contracts for 5 successive years and he exported rice, soya beans and other grains worth more than 5 billion rupees.

But commodities trading, even at this scale, wasn't enough for Subhash. He renamed the family firm Essel Group in 1976 and began his transformation from trader to industrialist. His vision fixed on something seemingly mundane: toothpaste tubes. In 1982, while India still used aluminum tubes, Subhash bought the technology of manufacturing soft plastic tubes from Germany and established Essel Packaging to produce soft plastic tubes for toothpaste and pharma industries. Industry veterans called him foolish—India wasn't ready for such innovation, they said.

They were spectacularly wrong. Essel Propack would eventually become the world's largest manufacturer of laminated tubes, a business so successful that Blackstone would acquire it in 2019 for over $450 million. But in 1982, this was just the beginning. According to a 2014 estimate, Essel Group's net worth by 1982 was over ₹100 crore—from near bankruptcy to nine figures in less than a decade.

The packaging success gave Subhash something more valuable than money: credibility with international partners and the confidence to dream bigger. In 1989, he opened EsselWorld, India's first amusement park, in Mumbai's Gorai area. Critics called it Chandra's Folly—who would travel to the outskirts of Mumbai for entertainment? But Subhash understood something fundamental about India's emerging middle class: they craved experiences, not just products. EsselWorld became a Mumbai institution, packed with families every weekend, generating steady cash flows that would fund his next, most audacious venture.

By 1991, as India stood on the brink of economic liberalization, Subhash Chandra had built a diversified conglomerate spanning packaging, entertainment, and trade. He had proven he could spot trends, execute complex projects, and most importantly, navigate India's bureaucratic maze. But his biggest insight was yet to come: India's 800 million people had only one television channel, and that monopoly was about to crack. The rice trader from Haryana was about to revolutionize how India consumed entertainment.

III. The Birth of Private Television in India (1992)

The meeting that would change Indian television forever almost didn't happen. It was 1991, and Subhash Chandra sat in the Hong Kong office of Li Ka-shing, Asia's richest man, pitching an idea so audacious that Li's team hadn't even bothered preparing properly for the presentation. Chandra wanted to lease a transponder on Li's AsiaSat-1 satellite to beam television signals into India. "There was no money in India," Li dismissed, demanding $5 million a year as lease for the transponder, more than four times the figure given by his own team for the business plan

But Chandra had done his homework. He pulled out a map of India, pointed to the 800 million people with only Doordarshan's monotonous programming, and made a bet that would define his life: "Give me the transponder. If I can't pay, I'll give you my company." Li Ka-shing, who'd built his fortune on calculated risks, recognized a kindred spirit. The deal was struck.

On October 2, 1992—Gandhi's birthday, deliberately chosen for its symbolism—Zee TV burst onto Indian screens. The launch wasn't just technical; it was theatrical. While Doordarshan offered educational programming and news bulletins read by stoic newsreaders, Zee TV opened with "Saanp Seedi," a game show hosted by the irrepressible Mohan Kapoor, followed by Hindi film music and entertainment that spoke to India's heart, not its head.

The government's reaction was swift and furious. Information & Broadcasting Ministry officials summoned Chandra, threatening to shut down his "illegal" broadcasts. India had no legal framework for private broadcasting—the Prasar Bharati Act gave Doordarshan monopoly over terrestrial signals, but said nothing about satellite. Chandra had found the loophole: he was uplinking from Hong Kong, technically making Zee a foreign channel beaming into India. "I'm not breaking any law," he told the bureaucrats. "Show me the law I'm breaking. "The technical challenges were daunting. The channel initially broadcast three hours a day, with its output consisting mainly of old Hindi movies and reruns of Doordarshan serials. The channel's initial manager was a Doordarshan news reporter who was on leave from his employer. Cable operators, accustomed to Doordarshan's terrestrial signals, didn't know how to handle satellite feeds. Chandra's team traveled village to village, installing dish antennas, training operators, sometimes literally climbing poles to splice cables.

Within less than a month after its launch, Zee TV was being criticized for its programming lineup; a cynic reviewed the network giving "A for effort" and "Z(ee) for quality", while others called it an "upbeat clone of Doordarshan." But Chandra understood that content quality could improve; what mattered was establishing distribution before competitors arrived.

And competitors were coming. Rupert Murdoch's STAR TV had launched a year earlier with English programming, but hadn't cracked the Hindi market. CNN and BBC were beaming into five-star hotels. The real threat was that STAR would pivot to Hindi content—which they eventually did with STAR Plus. Chandra needed to move fast. By April 1995, Chandra made his next strategic move: launching Zee Cinema, the premium movie channel and first channel of its sort in the country. This wasn't just another channel—it was a direct assault on the economics of Indian entertainment. Bollywood films were the crown jewels of Indian culture, and whoever controlled their television rights controlled viewer loyalty. Until 1999, programming was done by Star TV, but Zee was building its library, signing exclusive deals with production houses, creating must-watch Friday night premieres.

The expansion was relentless. By 2000, Zee had launched Zee News (converting from the failed El TV experiment), Zee Marathi for regional audiences, and Alpha channels in various languages. Each launch followed the same playbook: identify an underserved audience, create locally relevant content, establish distribution before competitors arrived, then improve quality once market position was secured.

But the real genius wasn't just in launching channels—it was in creating an ecosystem. Zee wasn't competing with Doordarshan; it was replacing it. Where Doordarshan offered one-size-fits-all programming, Zee offered choice. Where Doordarshan preached, Zee entertained. Where Doordarshan was the government speaking to citizens, Zee was India speaking to itself.

The numbers told the story. By 1999, Zee TV commanded over 40% of the cable and satellite viewership in India. The company that critics had dismissed as "Z for quality" was now setting advertising rates, dictating content trends, and most importantly, forcing Doordarshan to transform itself or become irrelevant.

The competitive landscape was evolving rapidly. STAR Plus, after years of English programming that appealed only to urban elites, finally understood Chandra's insight and pivoted to Hindi with shows like "Kyunki Saas Bhi Kabhi Bahu Thi." Sony Entertainment Television entered in 1995. Regional players emerged. The market Chandra had created single-handedly was now attracting global giants with deep pockets.

But Chandra had something they didn't: first-mover advantage in a market where relationships mattered more than capital. Every cable operator from Kashmir to Kanyakumari knew Zee. Every advertiser targeting middle India needed Zee. Every Bollywood producer looking to monetize library content called Zee first. The company wasn't just operating in the market—it had helped create the market's very structure.

The impact went beyond business metrics. Zee TV fundamentally altered India's cultural landscape. It democratized entertainment, bringing the same content to villages that cities enjoyed. It created stars—actors, hosts, singers—who weren't from film families or theater backgrounds. It spawned entire industries: event management, advertising agencies, content production houses. Conservative estimates suggest the private broadcasting industry Zee pioneered created employment for over 5 million people directly and indirectly.

Yet this success contained seeds of future challenges. The ease of launching channels meant barriers to entry were low. The reliance on Bollywood content made Zee vulnerable to content cost inflation. Most critically, the regulatory vacuum that had allowed Zee to flourish wouldn't last forever. The government, having lost its monopoly, would inevitably seek to reassert control through licensing, content regulations, and ownership restrictions.

As the 1990s drew to a close, Subhash Chandra stood at a crossroads. He had built India's first private television empire, proven that Indian content could compete with global players, and created a template that others would follow for decades. But the boy from Haryana who'd saved his family from bankruptcy wasn't satisfied with just television. He wanted to build something bigger—a media conglomerate that would rival the global giants. That ambition would drive Zee's next phase of explosive growth, and ultimately, nearly destroy everything he'd built.

IV. Building the Empire: Expansion & Diversification (1995–2010)

The millennium approached with Y2K fears gripping the world, but Subhash Chandra was focused on a different kind of system upgrade. In a boardroom overlooking Mumbai's Worli seafront, he laid out his vision to senior executives: Zee would no longer be just a broadcaster. It would become India's first vertically integrated media conglomerate, controlling everything from content creation to the last-mile delivery into homes.

"Content is king," he told his team, "but distribution is God."

This philosophy drove Zee's most audacious expansion yet. While competitors fought over content rights and advertising revenues, Chandra was quietly building the pipes through which all content would flow. In 1994, he had already established Siti Networks (then Siti Cable), which would eventually become India's largest Multi-System Operator (MSO), reaching 13.5 million households across 580 cities. But cable was just the beginning. On October 2, 2003—exactly eleven years after Zee TV's launch—Dish TV went live as India's first Direct-to-Home (DTH) service. DishTV was launched by the Zee Group on 2 October 2003, marking another industry-defining moment. The strategy was brilliantly counterintuitive: The company decided not to compete against entrenched cable operators in metros and urban areas, and instead focused on providing services to rural areas and regions not serviced by cable television.

Jawahar Goel, who led the launch, later recalled: "We hardly had four transponders and could offer only 48 channels, compared to analog cable that was giving... And, Star refused to give its channels. So, we decided to go slow and concentrate in cable-dry and cable-frustrated markets, rather than cable-rich markets and build the market step by step."

This wasn't just about technology—it was about control. Cable operators had become powerful intermediaries, often deciding which channels viewers could access, manipulating signals during cricket matches to force subscribers to upgrade packages, and providing inconsistent service quality. DTH eliminated the middleman. Viewers got direct access to satellite signals, consistent quality, and transparent pricing. Dish TV acquired 350,000 subscribers within 2 years of the launch.

The corporate transformation came in January 2007 when Zee Telefilms officially became Zee Entertainment Enterprises Limited—a signal to markets that this was no longer just a content company but a comprehensive entertainment conglomerate. The rebranding coincided with aggressive regional expansion. Zee Marathi dominated Maharashtra. Zee Bangla captured Bengal. Zee Telugu fought for Andhra Pradesh. Each regional channel wasn't just translated content but locally produced programming that understood cultural nuances—the difference between Mumbai's cosmopolitan Marathi and Pune's traditional dialect, between Kolkata's intellectual Bengali and rural Bengal's folk traditions. The most audacious diversification came in 2005 with the launch of DNA (Daily News and Analysis), an English-language broadsheet newspaper. DNA was first launched as a broadsheet newspaper out of Mumbai, Maharashtra, India on 30 July 2005 through a 50:50 joint venture between the Zee Media Corporation and the Dainik Bhaskar group under the company name Diligent Media Corporation Ltd. The venture aimed directly at the Times of India's dominance, with aggressive pricing and talent poaching. The newspaper had first launched its outdoor advertising campaign through billboards and placards in Mumbai during early 2005, with the tagline, "Speak Up, It's in Your DNA"

But DNA represented more than just another business venture—it was Chandra's attempt to influence public discourse beyond entertainment. Print media carried prestige that television, despite its reach, couldn't match. Policy makers read newspapers, not TV guides. Unfortunately, DNA struggled from the start, By 2012, Zee had taken over the rest of the ownership of DNA from the Bhaskar group, and the venture would ultimately fail, closing its print operations in 2019 after years of losses.

The international expansion during this period was more successful. Zee channels reached the global diaspora—from Jackson Heights in New York to Southall in London, from Dubai to Durban. The content strategy was sophisticated: not just exporting Indian shows, but creating locally relevant programming for NRIs navigating dual identities. Zee UK wasn't just about Bollywood; it covered British-Asian politics, second-generation identity crises, fusion cuisine shows that mixed tandoori with Sunday roast. The acquisition strategy accelerated with In 2017, the company acquired the majority stake of the Reliance Broadcast Network. Reliance Capital, part of Anil Ambani-led Reliance Group, has announced the sale of its radio and television broadcasting businesses under Reliance Broadcast Network to the Zee group for Rs 1,900 crore (US$ 276.7 million). This wasn't just about adding channels—Big Magic is a comedy channel catering to Hindi Speaking Markets while Big Ganga is a Bhojpuri entertainment channel, catering to audience in Bihar, Jharkhand and Purvanchal. The deal gave Zee entry into critical markets it had struggled to penetrate organically.

But by 2010, cracks were showing in Chandra's empire-building strategy. The aggressive expansion had been funded by debt—lots of it. Essel Group had interests in everything from infrastructure to education, from packaging to real estate. Each venture made sense individually, but collectively they stretched management bandwidth and financial resources. The global financial crisis of 2008 had tightened credit markets. Competition in every segment was intensifying.

More fundamentally, the media landscape was shifting beneath Zee's feet. YouTube launched in India in 2007. Facebook was gaining millions of users monthly. A generation was growing up that didn't schedule their lives around television programming—they expected content on demand, on their phones, for free. The distribution infrastructure Chandra had painstakingly built—cable networks, DTH satellites—suddenly seemed less like competitive advantages and more like legacy burdens.

The numbers reflected this transition. While Zee remained profitable, growth was slowing. Advertising revenues, the lifeblood of broadcast television, were increasingly flowing to digital platforms. Younger viewers were cutting cable subscriptions entirely. Regional competitors who focused on single markets were often more agile and locally relevant than Zee's pan-Indian approach.

As the decade ended, Subhash Chandra faced a stark reality: the empire he'd built on controlling distribution in a scarcity economy was struggling to adapt to an abundance economy where content was infinite and attention was scarce. The next decade would test whether Zee could transform from a traditional broadcaster to a digital entertainment company—and whether the Chandra family could maintain control as debts mounted and investors grew restless.

V. The Digital Disruption & OTT Revolution (2010–2020)

Reed Hastings stood on a Mumbai stage in January 2016, announcing Netflix's India launch with characteristic Silicon Valley confidence. "We want to be in every country in the world," he declared. In the audience, Zee executives watched nervously. They had seen this movie before—global tech giants entering India with unlimited capital and ambitions to "disrupt" traditional businesses. But this time was different. This wasn't about better technology or deeper pockets. It was about a fundamental reimagining of how entertainment was consumed.

Zee's response to the digital threat had been tentative, almost reluctant. While Netflix had been streaming since 2007 and Amazon Prime Video was preparing its India entry, Zee was still treating digital as an afterthought—a place to dump television content after broadcast. The company had launched various digital initiatives over the years—Ditto TV in 2012, Ozee in 2016—but these were half-hearted efforts, underfunded and undermargeted, as if hoping the digital revolution would somehow pass India by. The wake-up call finally came on February 14, 2018, when Zee launched ZEE5. Beginning from February 14, 2018, ZEE5 will be the one-stop digital destination for ZEE Entertainment, a global Media and Entertainment powerhouse. It was launched in India on 14 February 2018 with content in 12 languages. This wasn't another half-measure—Zee had finally committed serious resources, consolidating its failed DittoTV and Ozee platforms into a unified offering.

The timing was both late and desperate. Netflix had 5 million Indian subscribers. Amazon Prime Video, bundled with Prime shopping memberships, was growing explosively. Disney's Hotstar dominated cricket streaming. Zee was entering a knife fight with a butter knife, years after the battle had begun.

But ZEE5 had one advantage its global competitors couldn't match: understanding of regional India. Viewers can watch content across genres in any of 12 languages - English, Hindi, Bengali, Malayalam, Tamil, Telugu, Kannada, Marathi, Oriya, Bhojpuri, Gujarati and Punjabi. In a first for any OTT platform in India, and driven by the changing profile of the Indian digital consumer, viewers can also choose their preferred display language from among 11 languages While Netflix focused on urban English speakers and Amazon chased Hindi heartland, ZEE5 went hyperlocal—Bengali content for Kolkata, Bhojpuri for Bihar, Marathi for Maharashtra.

The content strategy was deliberately different. Where Netflix invested in prestige productions like "Sacred Games" with massive budgets, ZEE5 created volume—dozens of originals across languages, betting that quantity and variety would trump individual quality. With 20 Originals by the end of April 2018, ZEE5 ORIGINALS, a holistic mix of web-series and short films, strives to create an immersive experience for audiences with its potent content offerings across 6 languages - Hindi, Marathi, Tamil, Telugu, Malayalam and Bengali... Every month, the OTT platform will further strengthen its pipeline of offerings with one new web series in each of the aforementioned languages and one new short film. The music business provided an unexpected digital bright spot. Zee Music Company established in 2014, became one of India's top music labels. Zee Music Company has announced its own milestone: 30 million subscribers for its flagship YouTube channel, which mixes film and non-film music. The YouTube strategy was brilliant in its simplicity: while competitors fought over streaming rights, Zee uploaded music videos for free, monetizing through advertising. Zee Music Company, one of India's top music labels, has crossed a historic milestone—surpassing 100 million subscribers on YouTube. This achievement further cements its status as a major force in both the Indian and global music scenes. To mark this momentous occasion, YouTube presented Zee Music Company with the prestigious Red Diamond Play Button, an honor reserved for only the most followed creators worldwide. With this, Zee Music becomes just the second music label globally to receive this coveted award.

But these successes couldn't mask the fundamental challenge: ZEE5 was losing money—lots of it. The platform required massive content investments, technology infrastructure, and marketing spend. Unlike Netflix or Amazon, which could subsidize losses with other businesses, Zee's core television business was itself under pressure. Advertising revenues were flat. Cable subscriptions were declining. The company that had disrupted Doordarshan's monopoly was now being disrupted itself. The innovation attempts continued with mixed results. In 2018, Zee launched Zee Theatre, which offers a collection of recorded theatre plays also called teleplay- produced in India and internationally. Zee Theatre was officially launched on 21 September 2018 on Tata Sky (now Tata Play). The idea was noble—bringing Indian theater to television audiences—but theater on TV was a niche within a niche, hardly the mass-market solution Zee needed.

Meanwhile, the ownership structure was changing dramatically. The 2008 financial crisis had hurt Essel Group's non-media businesses. Infrastructure projects were bleeding money. The education ventures had failed. Real estate investments had turned sour. Chandra had borrowed heavily against his Zee shares, and as share prices fell, lenders demanded more collateral. By 2019, the situation was critical.

The numbers told a story of slow-motion crisis. Promoter holding, which had been over 40% in 2010, was steadily declining as Chandra pledged and sold shares. Competition was eroding market share in every segment. Digital investments were draining cash without generating proportional returns. The company that had once moved fast and broken things was now moving slowly and breaking itself.

As the decade ended in 2020, Zee faced an existential question: Could a company built for the broadcast era survive the streaming revolution? The COVID-19 pandemic, which accelerated digital adoption globally, would provide an unexpected answer—but not the one anyone expected. The next chapter would see the founding family lose control, global giants circle like vultures, and a merger saga that would captivate India's business community for years.

VI. The Ownership Crisis & Invesco Battle (2019–2021)

The call came at 3 AM. Punit Goenka, Subhash Chandra's son and Zee's CEO, was informed that Yes Bank had invoked pledged shares worth thousands of crores. It was February 2019, and the empire his father had built over four decades was collapsing in real-time. Television channels across India were already running breaking news tickers: "Zee promoters in talks to sell stake," "Subhash Chandra's debt crisis deepens."

The roots of the crisis went back years. Chandra had used his Zee shareholding as collateral to fund everything from infrastructure projects to real estate ventures. As these businesses struggled, he'd borrowed more, pledging more shares. It was a vicious cycle that worked only as long as Zee's share price kept rising. But with increased competition and slowing growth, the stock had stagnated. When lenders got nervous after the IL&FS crisis roiled Indian markets in 2018, they began calling in loans. The numbers were staggering. In February 2019, media reported that Essel Group was in talks to sell their shares from the Zee Entertainment Enterprises to save them from debt. Overall, the MF industry had debt exposure of Rs 5,000-6,000 crore to Essel Group firms. The total debt across the group was estimated at Rs 17,000 crore. Subhash Chandra's net worth, once estimated at over $4 billion, had evaporated. The Zee promoters (part of Essel Group) recently sold 11 per cent of their stake at Rs 4,224 crore to financial investor Invesco Oppenheimer, in a bid to repay their Rs11,000 crore debt.

On January 25, 2019, a crisis erupted that would change everything. Reports emerged linking Essel Group entities to suspicious post-demonetization deposits. Zee's share price crashed 26% in a single day. Mutual funds that had lent against Zee shares faced massive losses. The entire financial system's exposure to Essel Group was suddenly in question.

Subhash Chandra's response was extraordinary—and counterproductive. He wrote an open letter apologizing to lenders, admitting to "wrong decisions" including the Videocon D2H acquisition and infrastructure investments. Instead of calming markets, the letter created panic. Here was one of India's most successful entrepreneurs essentially admitting defeat. The next phase of the crisis came through stakeholder activism. On 11 September 2021, Invesco asked Zee management to call shareholders an "extraordinary general meeting" (EGM) to consider its demands. One of the main demands was the removal of Punit Goenka, son of the Zee Network founder. Invesco Fund, which owns 18 per cent of Zee Entertainment Enterprises, has reiterated its demand to oust Punit Goenka, current CEO and MD, from the board and induct its six nominees on Zee board.

This was unprecedented in Indian corporate history—a foreign institutional investor directly challenging a founding family's control. Invesco's argument was simple: the Goenkas owned less than 4% of Zee but controlled its board and management. This wasn't ownership; it was entrenchment. The Zee board rejected Invesco's demand, calling it "invalid and illegal."

What followed was a complex legal battle across multiple forums—the National Company Law Tribunal, Bombay High Court, and eventually the Supreme Court. In a setback to the Subhash Chandra family, the Bombay High Court on Tuesday allowed an appeal filed by Invesco Developing Markets Fund, a shareholder of Zee, against a single judge order of October last year that had stayed a shareholders' meeting to remove Zee's Chief Executive Officer and Managing Director, and family scion, Punit Goenka.

Meanwhile, Punit Goenka was fighting for survival. In August 2020, Subhash Chandra resigned as Chairman and was appointed Chairman Emeritus, effectively passing control to his son. But with promoter holding at just 3.99% by October 2021, the family's grip on the company was tenuous. They needed a white knight—someone who would preserve their management control while providing the capital and credibility to fend off Invesco.

The irony was stark: the company that had disrupted India's media landscape by challenging government monopoly was now itself facing disruption from activist investors. The promoters who had once pledged shares to build an empire were now reduced to minority shareholders fighting to retain relevance in their own company.

As 2021 ended, Zee was a company under siege—from creditors, investors, competitors, and its own history of aggressive expansion funded by debt. The solution, when it came, would be as dramatic as the crisis itself: a merger with Sony that promised salvation but would ultimately become another chapter in Zee's saga of near-misses and what-ifs.

VII. The Sony Merger Saga: Hope & Heartbreak (2021–2024)

The leak came on a Tuesday evening in September 2021. Financial journalists' phones lit up with tips: "Sony in talks to buy Zee." Within hours, both companies confirmed what would have been India's largest media merger—a $10 billion combination that would create an entertainment giant capable of competing with global streaming platforms and the looming Disney-Reliance combine.

On September 22, 2021, the company announced its intent to merge with Sony Pictures Networks India. Sony Pictures will hold a majority stake in the proposed merged entity, which will be headed by Zee's Punit Goenka. The timing was no coincidence. Just eleven days earlier, Invesco had demanded Punit Goenka's removal. The Sony deal was both shield and sword—protection from hostile investors and a path to remain relevant in a consolidating industry.

The proposed structure was elegant in its simplicity. Sony will hold a stake close to 51% in the company, with Zee controlling the remaining stake. Sony would invest $1.57 billion in growth capital. Punit Goenka would remain MD & CEO of the merged entity—a crucial condition for the Zee promoters. The combined entity would have 75 TV channels, two streaming platforms (ZEE5 and SonyLIV), and a film studio, creating India's largest entertainment company by revenue.

For Sony, the logic was compelling. They had strong urban, English-speaking audiences but struggled in regional markets where Zee dominated. The merger would give them instant scale and local expertise. For Zee, it meant survival—access to capital, global content, and most importantly, protection from Invesco's activism.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube