Zaggle Prepaid Ocean Services: The Master of the SaaS-Plus-Fintech Flywheel

I. Introduction & Episode Roadmap

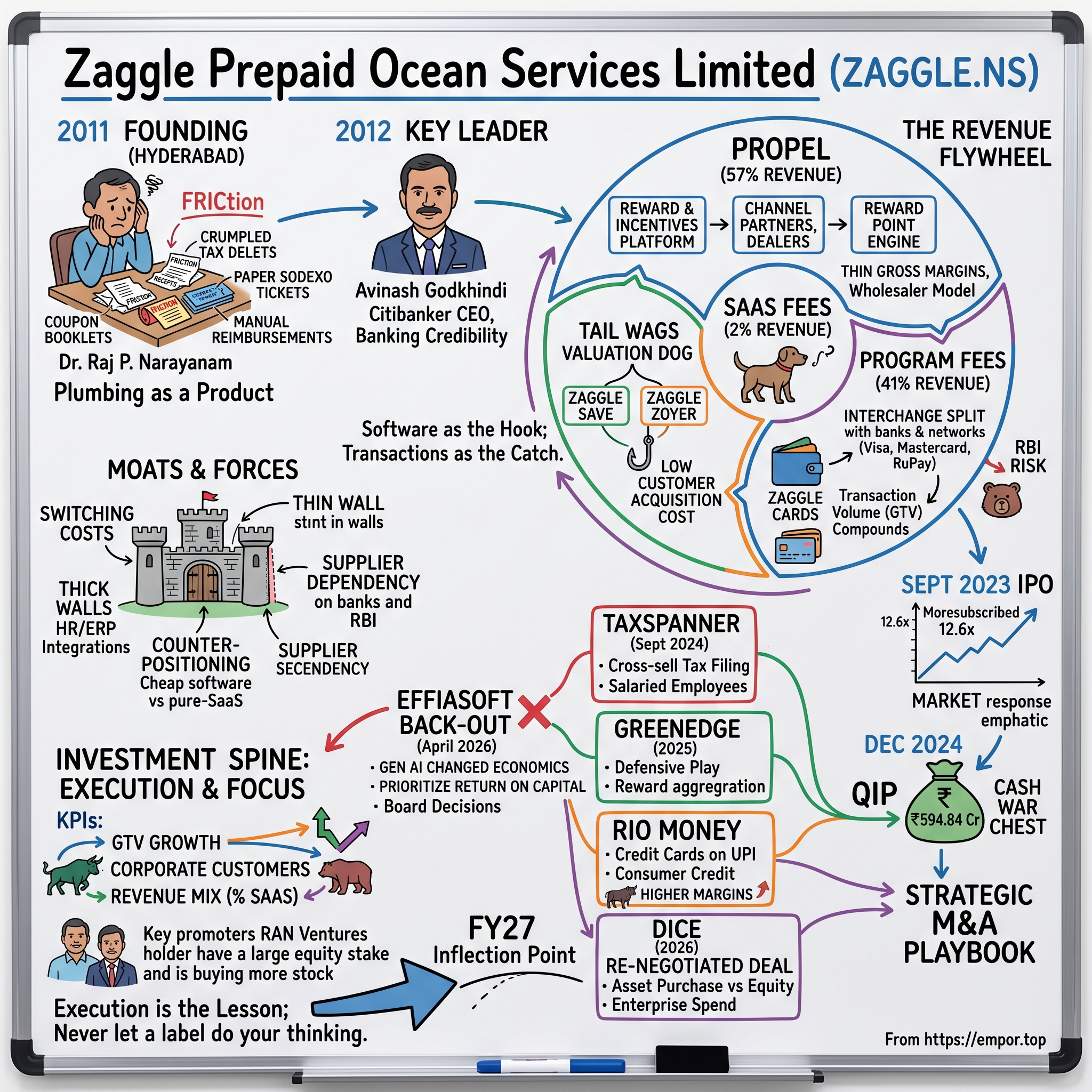

Picture the finance department of a mid-sized Indian company somewhere around 2015. An employee returns from a client trip in Mumbai with a fistful of crumpled taxi receipts, a hotel bill, and a restaurant tab. She staples them to a paper form, drops it in a tray, and waits three weeks for a reimbursement that arrives with an arithmetic error. Multiply that scene across a thousand employees, add the annual chaos of Diwali gifting — cardboard boxes of dry fruit, envelopes of Sodexo meal coupons, spreadsheets tracking who got what — and you have a perfect portrait of the friction that Indian corporate spending used to run on. It was slow, it was manual, and almost nobody thought of it as a market.

That friction is the raw material out of which Zaggle Prepaid Ocean Services Limited built a business. Listed on the National Stock Exchange of India as ZAGGLE.NS, this Hyderabad-headquartered company reported consolidated revenue of ₹19,076 million — roughly ₹1,908 crore, or north of $220 million — for the fiscal year ended March 31, 2026, a 46.3% jump over the prior year, with profit after tax rising 51.8% to about ₹1,388 million.1 Those are numbers that would make most global fintechs envious, and they were produced by a company most Western investors have never heard of.

Here is the puzzle that makes Zaggle worth an episode. It is marketed to public-market investors as a SaaS company — software as a service, the category that commands the richest valuation multiples in technology. Yet software subscription fees account for only about 2% of its revenue.2 The other 98% comes from things that look nothing like a recurring software licence: a share of the interchange banks earn every time an employee swipes a Zaggle-branded card, and the bulk monetization of reward points and gift vouchers flowing through its rewards platform. Zaggle, in other words, gives the software away close to cost and gets paid on the transactions the software unlocks.

The thesis we will test across this episode is whether that structure — call it the SaaS-plus-Fintech flywheel — is a genuine, durable engine or a clever piece of narrative framing that happens to be working while the Indian corporate-payments market grows quickly. The bull sees a low-cost Trojan Horse: cheap software wedges into a company's payroll and ERP systems, employees get cards, and transaction revenue compounds for years. The bear sees a transaction processor wearing a software costume, whose margins depend on interchange economics that the Reserve Bank of India can rewrite at any time.

We will trace the arc from the company's founding in 2011, through its September 2023 IPO and a cash-raising 2024 QIP, into a rapid-fire acquisition spree and a first push into consumer credit cards on India's UPI rails. Along the way we will keep asking the two questions that matter to a long-term investor: why does this company win from here, and what could break the case? Let us start where every good origin story does — with a founder and a problem nobody else wanted.

II. Genesis of Zaggle: Hyderabad, Dr. Raj P. Narayanam, and Early Card Experiments

Hyderabad in 2011 was not yet the fintech city it would become. It was better known for pharmaceuticals and IT services outsourcing than for financial innovation. It was here, on June 2, 2011, that Dr. Raj P. Narayanam incorporated the company that would become Zaggle.[^3] Narayanam's background was not that of a typical payments entrepreneur; his instinct was to look at the unglamorous plumbing of how companies moved money to and on behalf of their employees, and to see a mess worth cleaning up.

The mess was real. Corporate India in that era managed employee perks and spending through a patchwork of instruments that had barely changed in decades. Tax-free meal allowances came as paper Sodexo coupons — physical booklets an employee tore out and handed to a restaurant. Fuel and travel reimbursements ran on receipts and cash. Corporate gifting during festivals was a logistics headache. Each of these flows was governed by its own tax rule, its own vendor, and its own reconciliation nightmare. Narayanam's founding vision was deceptively simple: put these fragmented allowances onto software and cards, and let the plumbing become a product.

A vision needs an operator, and in 2012 Zaggle found one. Avinash Ramesh Godkhindi, a former Citibanker with deep institutional banking experience, joined as Managing Director and Chief Executive Officer.[^3] The pairing mattered more than it might appear. Building the kind of product Narayanam imagined meant integrating with conservative Indian commercial banks — institutions that move at the speed of compliance committees and are constitutionally allergic to risk. Godkhindi's years inside a global bank gave Zaggle the vocabulary and the credibility to negotiate the technical and regulatory arrangements that a founder-engineer alone would have struggled to close. In a business where the real barrier is not writing software but persuading a bank to co-brand a card on its licence, having a career banker in the CEO chair was less a nice-to-have than a precondition.

The years from 2011 to 2018 were an exercise in navigating regulation as much as building product. The Reserve Bank of India governs Prepaid Payment Instruments — the umbrella category that includes wallets and prepaid cards — through master directions that dictate what such instruments can and cannot do, from KYC requirements to how customer balances must be held.3 Zaggle had to design its products inside those lines, and the lines kept moving. Early iterations evolved from simple single-merchant gift vouchers toward multi-wallet co-branded prepaid cards — a single physical card that could hold segregated pools of money for meals, fuel, and travel, each carved out to respect the tax treatment attached to it. That segregation was the clever bit: it turned a compliance headache into a feature a CFO could love.

Underneath it all sat a decision that would define Zaggle's economics for the next decade: it would not become a bank. Instead it partnered with RBL Bank as an early issuing bank, letting the bank hold the regulated licence and the customer float while Zaggle supplied the software, the corporate relationships, and the user experience. This was the birth of the asset-light model — Zaggle riding on someone else's balance sheet and someone else's licence. It kept capital requirements low and let the company scale without becoming a regulated deposit-taker. It also planted the dependency that critics would circle years later: a company whose entire product sits on top of partner banks' licences is only ever as free as those banks and their regulator allow it to be. With the plumbing laid and the first cards in wallets, the question became how Zaggle actually made money — and the answer is stranger than the SaaS label suggests.

III. The SaaS-plus-Fintech Illusion: Decoding the Three Revenue Engines

Every investor who buys Zaggle should be made to do one exercise: open the segment note and find the SaaS. It is there — but you have to squint. For all the "SaaS-led fintech" branding, recurring software subscription revenue is roughly 2% of the top line.2 The other 98% is transactional. Understanding where that money actually comes from is the single most important act of diligence on this company, because it determines what kind of business you are really buying and what multiple it deserves.

Zaggle's revenue runs on three engines, and the biggest one is the least intuitive.

Propel: the reward-point engine (~57% of revenue). Propel is Zaggle's rewards and incentives platform — a configurable, gamified system corporations use to run channel-partner incentives, dealer rewards, and employee recognition programs. In FY26 the Propel platform's standalone revenue crossed ₹10,000 million for the first time, reaching about ₹10,555 million and contributing roughly 57% of standalone revenue.2 But here is the mechanic that trips people up: Zaggle does not earn this as a software licence. When a company wants to reward a thousand dealers with points redeemable for gift vouchers, it buys those points and vouchers through Zaggle, and Zaggle earns its margin on the bulk sourcing and monetization of that reward inventory. Think of it less like Salesforce charging a seat fee and more like a wholesaler who buys gift cards in bulk at a discount and distributes them at a spread. The revenue is large, but it is transactional and its gross margin is thin relative to true software.

Program fees: the interchange engine (~41% of revenue). This is the piece that looks most like classic fintech. Every time an employee swipes a Zaggle co-branded card — issued through partners such as RBL Bank, IndusInd Bank, ICICI Bank, and Yes Bank, running on Visa, Mastercard, or RuPay rails — a small interchange fee is generated, and Zaggle captures a share of it along with network incentives. Program-fee revenue grew to about ₹7,523 million in FY26 from ₹5,456 million the year before.2 The beauty of this engine is that it scales with Gross Transaction Value: the more money flows across the cards, the more Zaggle earns, with almost no incremental cost per swipe. The vulnerability is that interchange is set by networks and constrained by regulators — Zaggle is a price-taker, not a price-maker, on the very fee that drives 41% of its business.

SaaS and platform fees: the actual software (~2% of revenue). These are the recurring subscription fees for products like Zaggle Save, the employee-benefits and expense-management workhorse, and Zaggle Zoyer, an accounts-payable automation and invoice-to-pay tool. Platform, SaaS, and service fees together reached only about ₹479 million in FY26.2 This is the tail that wags the valuation dog: it is the smallest engine, but it is the one that justifies the "SaaS" premium the market has at times been willing to pay.

So why structure a business this way on purpose? Because of what the tiny SaaS engine does for the two big ones. By pricing Save and Zoyer at close to cost, Zaggle keeps its customer acquisition cost extraordinarily low and gets its software embedded inside a corporation's HR, accounting, and ERP systems — SAP, Oracle, Tally. Once it is in there, and once thousands of employees are carrying Zaggle cards, the transaction volume that feeds Propel and program fees follows almost automatically. The software is the hook; the transactions are the catch. It is a genuinely elegant design — provided the interchange and reward economics that fund it stay intact. That is the pivot on which the entire investment case turns, and it is exactly where a skeptic should push hardest. Having built this engine organically, Zaggle's next move was to pour fuel on it from the public markets.

IV. Capital Inflections: The 2023 IPO and the 2024 QIP Cash War Chest

By 2023, Zaggle had a working flywheel and a growth rate to show for it, and it did what growing Indian companies with a story to tell increasingly do: it went public. The IPO opened for bidding from September 14 to 18, 2023, at a price band of ₹156–164 per share, with the issue priced at the top end.4 The roughly ₹563 crore offering was a mix of fresh capital and an offer for sale, and the market response was emphatic — the book was oversubscribed about 12.6 times by the final day, with the qualified institutional buyer portion covered nearly 17 times.4 The shares listed on the NSE and BSE on September 22, 2023.4

Enthusiastic subscription numbers, though, are not the same as settled conviction. Beneath the demand sat real skepticism about the business model — the very questions this episode is built around. How dependent was Zaggle on a handful of banking partners? What happened to its economics if interchange rules changed? Was this really a software company, or a payments company enjoying a software multiple? The IPO did not answer those questions; it simply gave Zaggle the currency to keep growing while the market made up its mind.

If the IPO was the debut, the December 2024 Qualified Institutions Placement was the statement of ambition. With the stock having climbed well above its issue price, Zaggle raised ₹594.84 crore — roughly $70 million — by issuing about 1.13 crore new shares to institutions at ₹523.20 apiece, a modest discount to the floor price.5 The buyers were a credible institutional roster; Bank of India's ELSS tax-saver fund took the largest slice, with participation from Societe Generale and ICICI Prudential's technology fund among others.5 Raising equity at a share price more than three times the IPO price was, in the cold arithmetic of dilution, an efficient way to fund growth — the company sold relatively few shares for a large sum.

What that QIP really signaled was a change in identity. Up to that point, Zaggle had been a largely organic operator: win a corporate customer, deploy the software, earn on the transactions, repeat. The war chest changed the game. Management now had the cash to become an inorganic compounder — to buy capabilities, software assets, and customer books rather than build them all in-house. The balance sheet was deliberately shifting from asset-light toward investment-heavy. That is a consequential choice, because acquisition-led growth is where a lot of promising companies quietly destroy value: they overpay, they mis-integrate, they buy revenue that turns out to be rented. The interesting test of Zaggle's management, then, was not whether it could raise money — the market clearly wanted to give it some — but what it did with the money next.

V. The Strategic M&A Playbook: Compounding Through Inorganic Bets

Armed with its QIP proceeds, Zaggle went shopping. Between late 2024 and mid-2026 it executed a string of acquisitions, each aimed at a specific hole in the flywheel. Read individually they look opportunistic; read together they trace a fairly coherent thesis — deepen the moat around the corporate customer, then use that captive base to sell higher-margin products. Whether the thesis survives contact with integration reality is the open question, and it is worth walking through the deals to judge.

TaxSpanner (September 2024). The first move was into the employee's own tax life. Zaggle acquired a 98.32% controlling stake in Span Across IT Solutions — better known by its consumer brand TaxSpanner — for about ₹32 crore, buying the shares at ₹300.80 each.6 TaxSpanner is a legacy consumer tax-filing and advisory engine, a small business in its own right (its FY24 turnover was only around ₹4.7 crore).6 The strategic logic was cross-sell: bundle automated tax e-filing into Zaggle Save, so that the same salaried employee who uses a Zaggle card for tax-free meal and fuel allowances can also file their return through the platform. It tightens the loop between the corporation, the employee, and Zaggle — and it deepens the switching cost for the employer, since more of the employee's financial life now runs through one system.

Greenedge Enterprises (2025). Zaggle moved from a majority position to full ownership of Greenedge, a step aimed at bolstering the travel, lifestyle, and loyalty capabilities inside the Propel platform. The rationale here was defensive: Propel competes against entrenched reward aggregators, and owning more of the redemption and loyalty stack helps protect margins on the reward inventory that drives the majority of Zaggle's revenue. This is the least flashy of the deals and, appropriately, the outline treats it as a smaller bolt-on than the others.

Rio Money / Rivpe Technology (2026). This is the bet with the most optionality and the most risk. Zaggle acquired Rivpe Technology Private Limited — the fintech startup known as Rio.Money, founded only in July 2023 — for ₹22 crore in an all-cash deal for 100% of the equity, and it earmarked a substantially larger capital infusion, on the order of ₹100 crore-plus, to build the business out.7 Rebranded as Zagg.money, the acquisition is Zaggle's entry into "credit cards on UPI," a distinctly Indian product that lets consumers link a credit line to the ubiquitous Unified Payments Interface and pay by QR code. The strategy is to cross-sell consumer credit to the millions of salaried employees Zaggle already reaches through its corporate relationships. The prize is real — consumer credit carries far richer margins than corporate interchange — but so is the danger. Consumer lending is a different sport, with different regulation, different risk management, and a well-earned reputation for burning cash before it earns any. This is the part of the story where a prudent investor watches the cash flow statement, not the press release.

Dice Enterprises (2026). The most recent move was a return to Zaggle's home turf of enterprise spend management. Notably, the deal was restructured on the way to closing: Zaggle originally contemplated buying the Pune-based startup outright for around ₹123 crore, but the Board, on May 8, 2026, approved a modified structure — an asset purchase of Dice's software, databases, intellectual property, contracts, and domain names for roughly ₹67.9 crore plus taxes.8 The strategic aim was to capture larger mid-market and enterprise B2B accounts by absorbing Dice's spend-management engine and customer contracts. The restructuring itself is the tell worth noting: cutting the price nearly in half and shifting from an equity purchase to an asset purchase suggests a management team willing to renegotiate hard rather than honor a headline number for appearances. Which sets up the most revealing capital-allocation episode of the lot — the deal Zaggle chose not to do.

VI. Capital Discipline: The EffiaSoft Walk-Away and Board-level Decisions

In March 2025, Zaggle announced plans to acquire a 51% controlling stake in EffiaSoft Private Limited, an enterprise-software business, part of the same acquisitive push that produced the TaxSpanner deal.6 For a year it sat on the roadmap as a done-deal-in-waiting. Then, on April 3, 2026, the Board pulled the plug and walked away.

The stated reason is one of the more genuinely modern pieces of corporate reasoning in this whole story: generative AI. Management's explanation was that the rapid emergence of generative-AI coding and development tools had upended the economics of building enterprise software — collapsing the cost and timeline of writing the very kind of product EffiaSoft represented. On the company's own account, AI automation had cut internal product-development time from more than 75 days to under 30.9 If you can now build a capability in a month that used to take a legacy vendor years to accumulate, paying a full acquisition premium for that vendor's aging codebase starts to look like buying a horse in the early days of the automobile. Rather than overpay for legacy software, Zaggle redirected its capital toward the Dice asset purchase, where it was buying customer contracts and IP at a renegotiated price.

For an investor trying to assess management credibility, the EffiaSoft back-out is a more useful data point than any earnings beat. Announced acquisitions develop a gravity of their own; walking away invites the awkward question of why you announced it in the first place, and it can read as indecision. But pushing forward with a deal purely to avoid that embarrassment — spending real cash to protect a press release — is exactly the kind of value destruction that acquisitive companies are prone to. Zaggle chose the harder, more defensible path. It is a single episode and should not be over-read, but it is consistent with the Dice renegotiation: a management team that appears willing to change its mind when the facts change, and to prioritize return on capital over the optics of consistency. The more skeptical framing is that a company doing this many deals this quickly will inevitably start some it should abandon — and that the real test is not the walk-away but whether the deals it does complete get digested. Which brings us to the question of what actually protects this business once the deal-making stops.

VII. Moats, Powers, and Forces: Switching Costs and Counter-Positioning

Strip away the acquisition headlines and one question decides whether Zaggle is a compounding machine or a fast-growing commodity: what stops a customer, a bank, or a competitor from walking away? To answer it, put the business through two classic lenses — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and be honest about where the walls are thick and where they are thin.

Start with switching costs, the power Zaggle can most credibly claim. Once Zaggle Save or Zaggle Zoyer is wired into an enterprise's HR, accounting, and ERP workflows, and once physical and digital co-branded cards are in the hands of thousands of employees, ripping it out is a genuine operational ordeal. It is not just a software migration; it is re-issuing cards, re-training finance teams, re-mapping approval workflows, and disrupting the tax-free allowances employees actually rely on in their monthly pay. The TaxSpanner and Greenedge acquisitions were, in part, an attempt to raise these switching costs further by making more of the employee's and employer's financial life dependent on the platform. This is Zaggle's strongest and most defensible moat, and it is real — though it is worth remembering that switching costs deter defection more than they command higher prices, and Zaggle's pricing power on its software is deliberately near zero.

Then there is counter-positioning, the most intellectually interesting power in the story. A pure-SaaS expense-management competitor has to charge meaningful subscription fees to survive — that is its whole business model. A legacy voucher player like Pluxee (the former Sodexo benefits business) has the corporate relationships but lacks a modern, automated spend-management stack. Zaggle sits in the gap: it can price software at close to cost precisely because it does not need software margins — it recoups superior economics on interchange and reward redemption. A SaaS incumbent cannot easily copy this without cannibalizing its own subscription revenue, which is the essence of counter-positioning. The caveat is that this only holds as long as the transaction economics stay rich enough to subsidize the software; if interchange compresses, the counter-position collapses.

Scale economies are a more modest claim. As Zaggle's Gross Transaction Value grows, it can in principle negotiate better interchange splits with banks and deeper merchant discounts on the Propel network. But Zaggle is not the scale player in Indian payments — the banks and networks are — so this power is partial at best.

Running Porter's Five Forces sharpens the same picture from the outside in. The threat of new entrants is low-to-medium: writing expense software is easy, but securing RBI-compliant co-branding arrangements and deep bank integrations is slow and hard, which is the real barrier. The bargaining power of suppliers is high and is the central structural weakness — Zaggle depends on partner banks (RBL, Yes Bank, IndusInd, ICICI) and networks (Visa, Mastercard, RuPay) for the licences and rails its entire model rides on, and those suppliers capture the regulated economics. Competitive rivalry is intense, with well-funded SaaS players and entrenched global incumbents all circling the same CFOs. The honest synthesis: Zaggle has one strong power (switching costs), one clever one (counter-positioning), and a supplier-dependency that no amount of clever positioning fully neutralizes. That dependency is not a footnote — it is the next section.

VIII. Regulatory Tightropes & Banking Partner Co-branding Mechanics

Here is a sentence that should focus any Zaggle investor's mind: the company does not hold a banking licence, and it never has. Everything it does with cards and balances, it does on top of someone else's regulated permission. Zaggle is, in the language of the industry, a co-branding and marketing distributor — it designs the product, wins the corporate customer, and runs the software, while a partner bank holds the licence, issues the instrument, and keeps customer balances in bank-controlled escrows.3 This is the source of both its capital-light elegance and its structural fragility.

The fragility used to have a name: RBL Bank. In its earlier years Zaggle leaned heavily on a single issuing-bank relationship, which meant a single point of failure — if that bank changed terms, hit a regulatory snag, or simply decided the arrangement no longer suited it, Zaggle's business would have been in serious trouble. Much of the company's maturation has been an exercise in diversifying that dependency: onboarding Yes Bank, IndusInd Bank, and ICICI Bank as additional partners, and locking in longer-term arrangements with the global card networks. Spreading the risk across multiple banks and networks does not eliminate the dependency — Zaggle still earns nothing without a licensed partner in the loop — but it converts a single point of failure into a portfolio, which is a meaningful improvement in resilience even if it is not a moat.

Looming over all of it is the Reserve Bank of India, which regulates this space with a reputation for acting decisively and without much warning. The RBI's master directions on Prepaid Payment Instruments already dictate the shape of Zaggle's products.3 The genuine tail risks are specific and worth naming plainly: a tightening of KYC requirements that raises the cost of onboarding users; a cap on interchange fees, which would hit the 41% of revenue that comes from program fees directly and immediately; or restrictions on loading credit lines onto prepaid instruments, which would strike at the newer Zagg.money ambitions. India has seen the RBI move against fintech businesses abruptly before, and a company whose margins live and die on interchange and PPI rules is permanently exposed to a rule change it cannot control or predict. This is not a reason to dismiss the business, but it is the single risk that most deserves a permanent line in any Zaggle investment memo. And it is precisely in this regulated, relationship-heavy arena that Zaggle's competitors are trying to take the same ground.

IX. The Competitive Arena: Competing with Pluxee (Sodexo) and VC-Backed Disruptors

Zaggle is not competing in an empty field. It is fighting on two fronts at once — against a slow, entrenched giant on one side and a swarm of hungry, well-funded startups on the other — and the way it positions between them tells you a lot about how it wins deals.

The giant is Pluxee, the employee-benefits and rewards business formerly known as Sodexo Benefits and Rewards Services. For decades, Sodexo's meal coupons were so ubiquitous in Indian offices that the brand became a generic term for a tax-free food allowance. Pluxee owns the incumbent corporate relationships and the mind-share that comes from being the default for a generation. But its heritage is in vouchers and benefits, not in integrated spend management. Zaggle's competitive answer is bundling: instead of selling a rewards product and asking the CFO to manage yet another vendor, it offers rewards and expense management and card issuance and tax filing as one financial system. For a finance chief tired of stitching together fragmented suppliers, the single-platform pitch is genuinely attractive — consolidation of vendors is a language every CFO speaks.

The challengers come from the venture-funded fintech world. Happay, now part of Razorpay, competes head-on in enterprise travel-and-expense management. A cluster of others — EnKash, Volopay, Karbon Card — chase startups and SMEs with slick corporate-card products and aggressive pricing. These players are fast, design-forward, and unencumbered by legacy systems. What they mostly lack, relative to Zaggle, is the combination of a public listing, a track record of regulatory compliance, and a multi-bank network built over more than a decade. When the buyer is a conservative enterprise rather than a startup, those attributes matter: a large company entrusting its employee payments and tax-free allowances to a vendor wants to know that vendor will still exist, and still be compliant, in five years. A listed company with audited results and diversified bank relationships is an easier internal sell than an unlisted startup burning venture money.

That is the real battleground — not features, but CFO mindshare and institutional trust. Zaggle's edge here is credible but not unassailable: the startups are improving their compliance credentials and raising capital, and Razorpay-backed Happay has deep pockets and a large existing merchant footprint to cross-sell into. The competitive question for the next few years is whether Zaggle's integrated, listed, multi-bank positioning is a durable advantage or a temporary lead that better-funded rivals eventually erode. Judging that requires looking hard at who actually owns and runs the company, and whether their incentives are pointed at the long game.

X. The Investment Spine: Valuation, Management Credibility, and Ongoing KPIs

Behind every capital-allocation decision in this story sits a specific set of incentives, and Zaggle's are unusually well-aligned in one respect and worth scrutinizing in another. The promoter group — led by founder Raj P. Narayanam and CEO Avinash Godkhindi, acting through vehicles including RAN Ventures Private Limited — held roughly 44% of the company through 2026, a stake the group was actively increasing through open-market purchases rather than trimming.10 Narayanam's holding sat around a third of the company, with Godkhindi holding a mid-single-digit percentage, and executive remuneration kept deliberately modest.10 When founders are buying more stock in the open market and keeping their salaries low, the message to outside shareholders is that they expect to make their money the same way you do — through the equity, over time. That is the kind of alignment a long-term investor wants to see, and it is a genuine positive.

Alignment, though, is not the same as performance, and performance is where the record has to speak. The growth trajectory has been steep and consistent. Revenue climbed from ₹7,756 million in FY24, to ₹13,038 million in FY25, to ₹19,076 million in FY26 — three straight years of growth in the 40-plus-percent range.1 Profit after tax followed the same arc, from ₹440 million to ₹879 million to ₹1,388 million.1 Adjusted EBITDA in FY26 rose about 51% to roughly ₹191.6 crore, with the company guiding to consolidated growth of about 40% for FY27 and a longer-term aspiration, stated repeatedly on earnings calls, of reaching $1 billion in revenue with 14–15% adjusted EBITDA margins over the next five to seven years.19 The consistency of that guidance across quarters is itself a credibility signal — management has been telling the same story about the same targets rather than moving the goalposts each call.

But numbers this good in a business this dependent on transaction economics demand interrogation rather than applause. Note that on the day the strong Q4 FY26 results landed, the stock actually fell sharply — around 19% — as the market weighed the results against valuation and the quality-of-revenue questions we have been circling.1 That reaction is a useful reminder that the market is not naively paying a SaaS multiple for this business; part of the investor base is already pricing in the transaction-processor reality.

For an investor who wants to track this company without drowning in disclosure, three KPIs carry most of the signal. First, Gross Transaction Value growth — the total spend flowing across Zaggle's cards and platform, because it is the fuel for both program fees and Propel. Second, corporate customer count and active employee-user base, which measures whether the distribution engine is still winning and retaining accounts. Third, and most important for the valuation debate, the revenue mix — specifically whether higher-margin platform/SaaS fees can grow from that 2% sliver into meaningful double digits, or whether transaction-linked revenue remains overwhelmingly dominant. That third metric is, in a single number, the referendum on whether Zaggle is becoming more of a software business or staying a payments business dressed as one. Which is exactly the fault line along which the bull and bear cases divide.

XI. Risk Radar, Bull vs. Bear Case, and Activist Stress Test

Lay the two cases side by side and Zaggle becomes a genuinely balanced debate rather than an obvious call in either direction.

The bull case rests on distribution and optionality. Zaggle has built an enviable channel into corporate India — thousands of company relationships and, through them, access to millions of salaried employees — at a low customer-acquisition cost, thanks to the near-free software wedge. On top of that distribution, the flywheel throws off operating leverage: as transaction volume grows across a largely fixed technology base, adjusted EBITDA margins should expand, which is precisely what management's 14–15% margin aspiration encodes. And then there is the optionality — Zagg.money's consumer credit-on-UPI push into a far higher-margin product, and cross-border expansion through a UAE entity and GIFT City incorporation that could extend the SaaS-plus-fintech model beyond India.9 If even one of those options pays off, the current business is being valued without credit for a large potential upside.

The bear case is the mirror image of each of those strengths. The regulatory risk is not hypothetical: a single RBI decision on interchange caps, PPI credit-loading, or co-branding fee shares could compress the economics that fund the entire model, and Zaggle has no vote in that decision. The valuation risk is what we might call SaaS-premium deflation — if the market fully internalizes that this is a business earning transaction-linked margins with only a 2% software core, the multiple could re-rate down toward payment-processor peers, and the Q4 FY26 share-price drop suggests that repricing may already be underway. And the integration risk is the natural cost of the acquisition spree: TaxSpanner, Greenedge, Rio Money, and Dice all have to be absorbed at once, and rapid-fire dealmaking is a classic route to indigestion, distraction, and write-downs.

Now run the activist stress test — imagine a skeptical long/short investor building the short thesis. They would lead with the gap between marketing and mechanics: a company presented with SaaS framing that derives 98% of revenue from transactions, inviting the charge that the valuation rests on a category error. They would press on the concentration risk in partner banks — a supplier dependency that management can mitigate but not remove. And they would zero in on Zagg.money as the swing factor: consumer lending is cash-hungry and risk-laden, and a corporate-payments company teaching itself to underwrite consumer credit is exactly the kind of adjacency that looks like optionality on the way in and looks like a cash drain on the way out. Management has said it expects positive operating cash flow around FY27 even while funding this build-out, a claim the market will hold it to.9

Filtered through Helmer and Porter, the verdict is nuanced. Zaggle has real switching costs and a clever counter-position, wrapped around a supplier dependency and a regulatory exposure it cannot control, in an intensely competitive market. That is not a fortress, but it is a defensible, fast-growing franchise with genuine embedded optionality — which is a more honest place to end than either the bull's or the bear's caricature. What separates the two outcomes, in the end, is execution and capital discipline, and that is where the founders' playbook comes back into focus.

XII. Playbook Lessons & Epilogue

Zaggle's story leaves two lessons on the table — one for operators, one for investors — and they are really the same insight viewed from opposite sides of the ledger.

For founders, the lesson is about where value actually lives. Zaggle's insight was that you do not have to win the hard, expensive fight of selling premium software to cost-conscious enterprises if you can instead give the software away and monetize the transactions it unlocks. Subsidizing a product to capture a strategic channel — and then earning on the flow that runs through that channel — is a powerful and under-appreciated growth tactic. It only works where the subsidized product creates a durable hook and the backend flow carries real economics, but where those conditions hold, as they did in Indian corporate spending, it can build a fast-growing business out of a market nobody thought to name.

For investors, the lesson is the exact inverse: never let a category label do your thinking for you. A "SaaS-led fintech" can be a wonderful business and still be badly mispriced if you assume you are buying recurring software margins when you are actually buying transaction-linked ones. The entire Zaggle debate — bull versus bear, the valuation question, the RBI risk, the Zagg.money bet — reduces to whether you have correctly understood which of those two things you own. Do the segment-note exercise, find the 2%, and price the other 98% for what it is.

As Zaggle moves into FY27, it stands at a real inflection point. It is simultaneously trying to digest the Dice assets, prove out the consumer-credit thesis at Zagg.money, expand internationally through GIFT City and the UAE, and grow its core corporate franchise at roughly 40% — all while defending its interchange economics against a regulator that has shown it will act. The company has earned some benefit of the doubt through consistent growth, aligned founder ownership, and a couple of encouraging capital-discipline decisions in the EffiaSoft walk-away and the Dice renegotiation. But the case is unproven where it matters most: whether that low-margin, transaction-heavy engine can be steered toward the higher-margin software and credit mix management aspires to, and whether the acquisition spree compounds value or quietly erodes it. The next several years of GTV, revenue mix, and cash flow will settle which story this turns out to be — and those, not the SaaS label, are the numbers to watch.

References

-

Zaggle Prepaid FY26 Revenue Soars 46% to INR 1,908 Cr; Profit Jumps 52% — Whalesbook Corporate News, 2026-05 ↩↩↩↩↩

-

Zaggle Q4: Profit Jumps 30% To ₹40.6 Cr, Revenue Up 50% YoY — Inc42, 2026-05-13 ↩↩↩↩↩

-

Master Directions on Prepaid Payment Instruments (PPIs) — Reserve Bank of India ↩↩↩

-

Zaggle Prepaid Ocean Services IPO Closed: Oversubscribed 12.57x On Day 3 — Goodreturns, 2023-09-18 ↩↩↩

-

Zaggle Raises ₹594.8 Crore via Qualified Institutional Placement at ₹523.20 Per Share — Angel One, 2024-12-24 ↩↩

-

Board of Zaggle approves acquisition of majority stake in Span Across — Business Standard, 2024-09-26 ↩↩↩

-

Zaggle acquires fintech startup Rio.Money for Rs 22 Cr — Entrackr, 2026-03 ↩

-

Board of Zaggle approves modification in agreement for acquisition of Dice Enterprises — Business Standard, 2026-05-08 ↩

-

Inside Zaggle's Push Towards An Agentic AI-Powered $1 Bn Enterprise Platform — Inc42, 2026 ↩↩↩↩

-

RAN Ventures acquires 30,000 Zaggle Prepaid shares, raising promoter group stake to 44.41% — Dealroom.co, 2026-02 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube