Yatharth Hospital & Trauma Care Services: Building North India's Healthcare Fortress

I. Introduction & Episode Roadmap

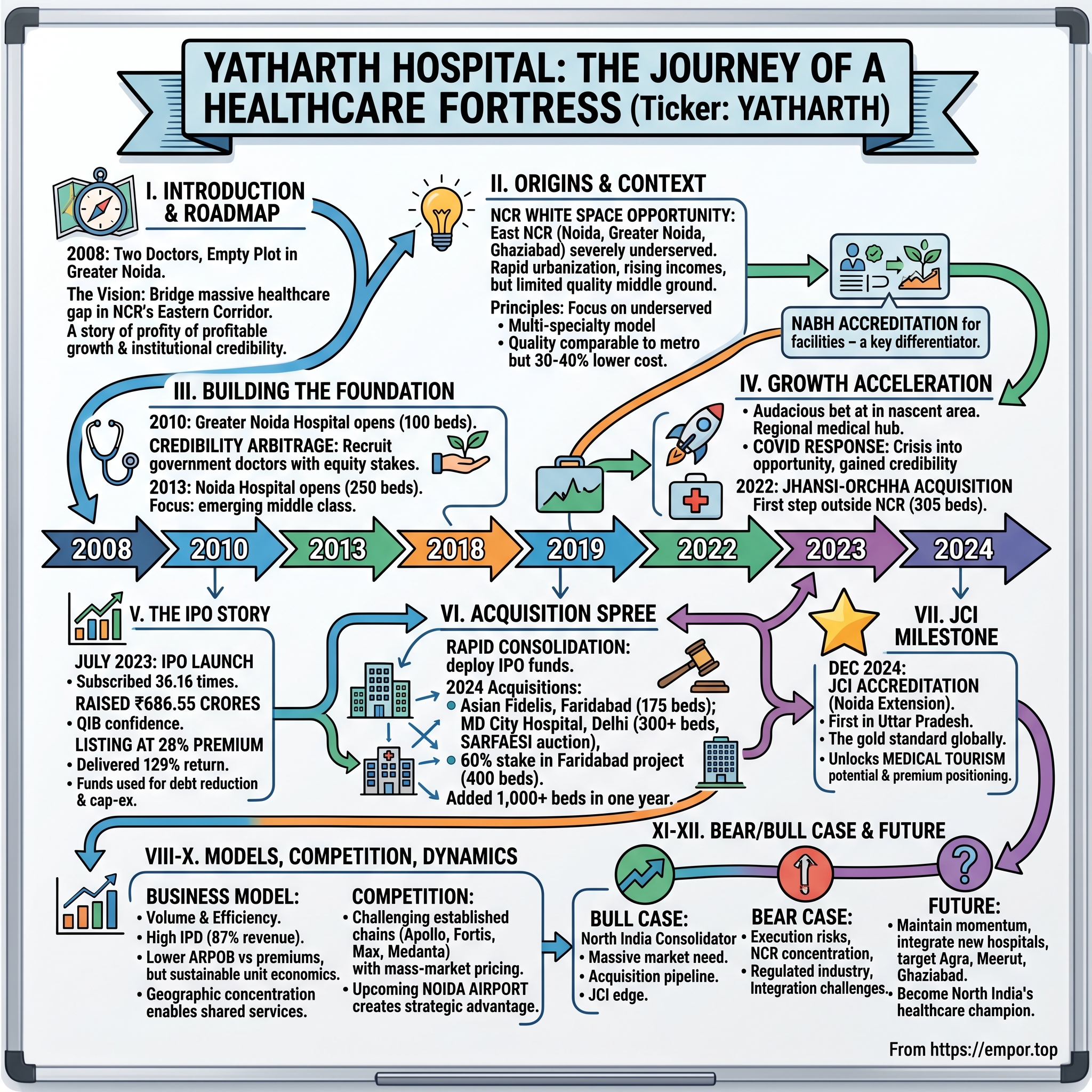

Picture this: It's 2008, and two doctors stand in an empty plot in Greater Noida, surveying what would become their first hospital. The global financial crisis is unfolding, credit markets are frozen, and launching a capital-intensive healthcare venture seems almost foolhardy. Yet Dr. Ajay Kumar Tyagi and Dr. Kapil Kumar see something others don't—a massive healthcare gap in one of India's fastest-growing regions, where millions of middle-class families drive hours to Delhi for quality medical care.

Fast forward sixteen years. That empty plot has transformed into North India's emerging healthcare powerhouse—Yatharth Hospital & Trauma Care Services, operating seven hospitals with over 2,300 beds across three states. The company that started with borrowed capital and a 250-bed facility now commands a market capitalization exceeding ₹4,000 crores, having delivered a stunning 129% return to IPO investors within months of listing.

The central question driving today's analysis: How did two doctors build a hospital empire that went from zero to IPO in just 15 years, while established players with decades of experience struggled to expand beyond metro cities?

This is a story about more than just healthcare—it's about understanding emerging market dynamics, mastering the art of strategic acquisitions, and building institutional credibility in a trust-deficit industry. We'll explore how Yatharth cracked the code of profitable growth in Tier 2 and 3 cities, why their acquisition spree in 2024 represents a calculated bet on consolidation, and what their recent Joint Commission International (JCI) accreditation means for India's medical tourism ambitions.

What you'll discover today: the playbook for building a healthcare business in emerging markets, the economics of hospital operations that most investors miss, and why the next decade might belong to regional healthcare champions rather than national chains. Let's begin where all great business stories start—with the problem that needed solving.

II. Origins & Healthcare Context in India

The year 2008 marked a peculiar moment in Indian healthcare. Apollo Hospitals, the country's largest private chain, was celebrating its 25th anniversary. Fortis was aggressively expanding through acquisitions. Max Healthcare was focusing on the premium segment. Yet in the National Capital Region—home to over 20 million people—quality healthcare remained concentrated in South Delhi's expensive corridors and Gurgaon's corporate hospitals.

Enter Dr. Ajay Kumar Tyagi, an orthopedic surgeon who had spent years watching patients from Noida, Greater Noida, and western Uttar Pradesh undertake exhausting journeys to Delhi for treatments that should have been available locally. Partnering with Dr. Kapil Kumar, they identified what venture capitalists would later call a "white space opportunity"—the NCR's eastern corridor, where rapid urbanization had outpaced healthcare infrastructure by at least a decade.

The Indian healthcare landscape they entered was a study in contradictions. Government hospitals, handling 80% of inpatient load, were overwhelmed and under-resourced. Private hospitals, catering to just 20% of patients, captured 70% of healthcare spending. The urban-rural divide was stark: cities with 30% of the population had 70% of hospital beds. Most telling was the trust deficit—patients viewed private hospitals as either unaffordable five-stars or questionable nursing homes, with little quality middle ground. Delhi NCR's healthcare dynamics presented a unique opportunity. The region's population was growing at 4% annually, household incomes were rising 8-10% yearly, and health insurance penetration was accelerating. Yet eastern NCR—Noida, Greater Noida, Ghaziabad—remained severely underserved. Patients routinely traveled 30-50 kilometers to Delhi's established hospitals, often arriving too late for critical interventions.

Dr. Tyagi brought credentials from LLRM Medical College and a diploma in orthopedics from King George Medical College, Lucknow, while Dr. Kapil Kumar held degrees from SN Medical College, Agra University, and a master's in orthopedic surgery from Lucknow University. But credentials alone wouldn't suffice—they needed a differentiated model.

Their vision crystallized around three principles: First, focus on underserved geographies where competition was minimal but demand was surging. Second, build multi-specialty hospitals rather than single-specialty clinics to capture the full patient journey. Third, maintain quality standards comparable to metro hospitals while keeping costs 30-40% lower through operational efficiency.

The business model choice—multi-specialty versus single-specialty—proved crucial. While chains like Narayana Hrudayalaya succeeded with cardiac focus and Centre for Sight dominated ophthalmology, the founders believed NCR's emerging markets needed comprehensive care. A patient arriving with chest pain might need cardiac intervention, but could also require diabetology, nephrology, or critical care—services that single-specialty centers couldn't provide.

Why NCR specifically? The math was compelling. The region's per capita healthcare spending was growing at 15% annually. Private healthcare penetration was below 15% compared to 25% in South India. Most critically, the supply-demand gap was widening—NCR needed an additional 20,000 beds by 2015, but only 5,000 were being added. For two doctors with limited capital but deep operational knowledge, this represented a once-in-a-generation opportunity to build something transformative.

III. The First Decade: Building the Foundation (2008–2018)

The global financial meltdown of 2008 created an unlikely opening. As international hospital chains paused expansion and domestic players conserved capital, land prices in Greater Noida corrected 40%. Construction costs dropped as contractors scrambled for projects. The founders, operating on bootstrap mode with personal savings and small loans from friends, seized the moment.

Yatharth Hospitals commenced its operations in 2008, but the real breakthrough came in 2010 with the establishment of their first full-scale hospital in Greater Noida. Starting with just 100 operational beds in a 250-bed facility, they faced the classic chicken-and-egg problem of new hospitals—doctors wouldn't join without patients, and patients wouldn't come without renowned doctors.

The solution came through what they called "credibility arbitrage." Instead of competing for star doctors from Apollo or Fortis, they recruited talented specialists from government medical colleges who wanted private practice opportunities. They offered these doctors not just consultancy fees but equity participation—turning potential employees into invested partners. By 2012, they had 50 consultants across 15 specialties, many holding senior positions at government institutions.

The 2013 launch of their second hospital in Noida marked a strategic evolution. This 250-bed facility targeted a different segment—the emerging middle class that found government hospitals inadequate but Apollo-Fortis unaffordable. Located strategically near the Noida-Greater Noida expressway, it captured patients from western Uttar Pradesh districts like Bulandshahr, Aligarh, and Agra.

Building medical credibility required more than infrastructure. The founders instituted weekly clinical audits, mortality reviews, and outcome tracking—practices uncommon in Tier 2 hospitals then. They invested heavily in equipment, acquiring MRI and CT scan machines when competitors relied on outsourcing. Most importantly, they pursued NABH (National Accreditation Board for Hospitals) accreditation for all facilities—a costly, time-consuming process that many regional players avoided. All of Yatharth's hospitals achieved NABH accreditation—a remarkable feat considering many established chains had only partially accredited facilities. The process meant documenting over 600 parameters, implementing clinical protocols, and creating quality control systems that most Tier 2 hospitals considered unnecessary overhead.

By 2018, the expansion of their Greater Noida hospital to 400 beds represented more than physical growth. They had developed what insiders called the "Yatharth way"—a unique operating philosophy combining government hospital affordability with private sector efficiency. Nurses were cross-trained across departments to handle surge capacity. Doctors received equity stakes tied to patient outcomes, not just volumes. Administrative staff rotated through clinical areas to understand patient journeys.

The financial struggles during this period were acute. Banks remained skeptical of lending to unknown healthcare brands. Equipment suppliers demanded upfront payments. Insurance companies delayed empanelments. Yet the founders persisted, often deferring their own compensation to fund operations. By 2018, they had achieved what seemed impossible a decade earlier—three profitable hospitals with combined revenues exceeding ₹200 crores, setting the stage for aggressive expansion.

IV. The Growth Acceleration: Third Hospital & Geographic Expansion (2019–2022)

The opening of Yatharth's third hospital in Noida Extension in 2019 marked a pivotal strategic shift. This wasn't just another facility—at 450 beds, it was designed as a regional medical hub, one of the largest hospitals in the area. The location choice was prescient: Noida Extension, despite being dismissed by competitors as too nascent, was experiencing explosive residential growth with over 100,000 new apartments under construction.

The facility incorporated lessons from their first decade. Instead of gradually adding specialties, they launched with 15 departments operational from day one. The emergency department alone had 30 beds—larger than entire hospitals in the vicinity. They invested ₹50 crores in medical equipment, including advanced imaging systems that most Tier 2 hospitals outsourced. The bet was audacious: build infrastructure for tomorrow's demand, not today's.

COVID-19 arrived just as this facility was gaining traction. While the pandemic devastated elective procedures industrywide, Yatharth's crisis response became a masterclass in operational agility. Within weeks, they converted 60% of beds to COVID care, established separate entry/exit protocols, and created India's first drive-through testing facility outside a metro city. When oxygen shortages hit Delhi, their pre-installed liquid oxygen plants—considered excessive just months earlier—saved hundreds of lives.

The pandemic paradoxically accelerated their growth. As government hospitals overflowed and premium chains charged astronomical rates for COVID care, Yatharth occupied the middle ground—quality care at regulated prices. They treated over 15,000 COVID patients, earning credibility that years of marketing couldn't have achieved. Insurance companies, witnessing their clinical outcomes and cost management, fast-tracked empanelments.

The 2022 acquisition of the Jhansi-Orchha hospital marked their first geographic diversification outside NCR. This 305-bed multi-specialty facility, one of the largest in the Jhansi-Orchha-Gwalior region, came with an established patient base but outdated operations. The turnaround strategy was surgical: retain the medical staff while overhauling everything else—from IT systems to clinical protocols to cafeteria menus.

Technology investments during this period went beyond equipment. They implemented hospital information systems (HIS) enabling real-time bed availability tracking, automated inventory management reducing wastage by 30%, and telemedicine capabilities connecting rural patients to specialists. The focus on Centers of Excellence—cardiac sciences, neuro sciences, renal sciences—meant concentrated investments in specific departments rather than spreading resources thin.

By 2022's end, Yatharth operated four hospitals with 1,400+ beds, employed over 400 doctors, and generated revenues approaching ₹500 crores. The company that had struggled for bank loans just five years earlier was now preparing for something unprecedented—taking a Tier 2-focused hospital chain public.

V. The IPO Story: Going Public in 2023

The boardroom at Yatharth's Noida headquarters buzzed with tension in early 2023. Investment bankers from ICICI Securities, IIFL Securities, and Ambit laid out the IPO roadmap. The market timing seemed challenging—interest rates were rising, startup IPOs had underperformed, and healthcare stocks traded at modest valuations. Yet the founders saw opportunity where others saw obstacles.

The pre-IPO preparation was meticulous. Yatharth raised ₹120 crores via pre-IPO placement from institutional investors, providing validation and balance sheet strength. Financial reporting was upgraded to quarterly reviews. Clinical outcome data was digitized and audited. Every related-party transaction was unwound or disclosed transparently. The IPO opened on July 26, 2023, and closed on July 28, 2023, with a price band set at ₹300 per share (upper band). The issue size totaled ₹686.55 crores, comprising a fresh issue of ₹490 crores and an offer for sale (OFS) of ₹196.55 crores.

What happened next stunned even the optimistic bankers. The IPO was subscribed 36.16 times overall by close. The granular data revealed institutional confidence: retail investors subscribed 8.34 times, QIBs (Qualified Institutional Buyers) subscribed 85.10 times, and NIIs (Non-Institutional Investors) subscribed 37.22 times. The QIB oversubscription—among the highest for healthcare IPOs that year—signaled that sophisticated investors saw something special in Yatharth's model.

The company raised ₹205.97 crores from anchor investors a day before the IPO opened, with marquee names participating at the upper price band. The anchor allocation provided crucial price discovery and momentum heading into the public offering.

Post-listing performance exceeded all expectations. Shares listed on BSE and NSE on August 7, 2023, opening at ₹384—a 28% premium to the issue price. Within months, the stock zoomed to ₹684.40, delivering a staggering 129% return to IPO investors. For context, the broader healthcare index gained just 15% during the same period.

The use of IPO proceeds reflected strategic priorities. Debt reduction took precedence—₹250 crores allocated to repay high-cost borrowings, immediately improving interest coverage ratios. Another ₹150 crores funded capital expenditure for upgrading existing facilities, particularly ICU expansions and diagnostic equipment. The remaining proceeds strengthened working capital, crucial for the acquisition spree that would follow.

What made this IPO remarkable wasn't just the numbers but the validation it represented. A company focused on Tier 2 cities, with no presence in metros, had commanded valuations comparable to established chains. The market was betting not on Yatharth's present but its future—a future where healthcare consolidation would create regional champions.

VI. The Acquisition Spree: Rapid Consolidation (2024)

January 2024 found Yatharth's management team in an unusual setting—a bankruptcy court auction room in Delhi. They weren't there as troubled debtors but as aggressive bidders, ready to deploy their IPO war chest. The strategy had shifted dramatically from organic growth to inorganic expansion, recognizing that distressed healthcare assets offered once-in-a-decade opportunities. The February 2024 acquisition of Asian Fidelis Hospital in Faridabad marked the beginning. Yatharth acquired the Faridabad-based facility for ₹116 crore, gaining a 175-bed hospital with plans to expand capacity to 200-220 beds post acquisition. Built just three years earlier, the facility came with modern infrastructure and existing accreditations—critical for immediate operationalization.

The acquisition playbook was becoming clear. Target hospitals with: solid infrastructure but poor management, existing NABH accreditations to avoid lengthy approval processes, strategic locations complementing existing facilities, and distressed sellers willing to accept reasonable valuations. Integration would focus on standardizing clinical protocols, upgrading IT systems, and cross-selling specialties from other Yatharth hospitals. October 2024 brought the most dramatic acquisition yet. Yatharth emerged as the successful bidder for MD City Hospital in Model Town, Delhi, acquiring the 300+ bed facility for approximately ₹160 crores through a SARFAESI (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act) auction. This wasn't just any acquisition—it marked Yatharth's entry into Delhi proper, the most competitive healthcare market in North India.

The SARFAESI auction process revealed Yatharth's newfound financial muscle and operational confidence. Competing against established chains, they bid aggressively, understanding that Delhi presence was worth premium pricing. The facility, though requiring operational turnaround, offered immediate access to Delhi's affluent patient base and insurance networks. November 2024 saw the most ambitious move yet—acquiring a 60% stake in a 400-bed hospital project in Faridabad for ₹91.20 crores (enterprise value of ₹152 crores). Unlike previous acquisitions of operational facilities, this was a bet on the future—a hospital under construction, expected to be operational by fiscal 2025. The company planned an additional ₹100 crore investment for medical equipment, including oncology suites and robotic surgery capabilities.

The acquisition spree's strategic logic was becoming clear. Within a single year, Yatharth had added over 1,000 beds to its network, entered Delhi proper, and become the dominant player in Faridabad. The total investment exceeded ₹500 crores, but the market rewarded the aggression—the stock price touched ₹684.40, delivering 84% returns year-to-date.

Financial engineering supported this expansion. The company maintained a net-cash position despite aggressive acquisitions, using a combination of internal accruals, strategic debt, and the upcoming QIP proceeds. Integration happened rapidly—standardized IT systems within 30 days, clinical protocol alignment within 60 days, and full operational integration within a quarter.

The vision articulated by Yatharth Tyagi, now whole-time director, was audacious: double bed capacity to 3,000 within three years. What seemed impossible for a Tier 2-focused chain just years ago was becoming reality through disciplined execution and strategic capital deployment.

VII. The JCI Milestone: First in Uttar Pradesh (2024)

The conference room at Yatharth's Greater Noida West facility hummed with nervous energy on a December morning in 2024. Five international surveyors from Joint Commission International had just completed their final assessment rounds. After five grueling days evaluating 282 standards and 1,192 measurable elements, they were ready to deliver their verdict. On December 23, 2024, Yatharth Hospital, Noida Extension, achieved a historic milestone by becoming the first hospital in Uttar Pradesh to earn the prestigious Joint Commission International (JCI) accreditation. The announcement sent ripples through India's healthcare industry—a Tier 2-focused hospital had achieved what many metro giants hadn't.

JCI accreditation represents healthcare's gold standard globally. Only 45-55 hospitals across India held this distinction, most being flagship facilities of national chains in major metros. The rigorous evaluation process examined everything from patient identification protocols to medication management, infection control to leadership governance. Every process, every protocol, every outcome metric faced scrutiny against international benchmarks.

The JCI accreditation represented a year-long process of preparation and continuous improvement at Yatharth Hospital. Infrastructure upgrades alone exceeded ₹50 crores—new air handling units for operation theaters, advanced sterilization equipment, computerized physician order entry systems. But the real transformation was cultural. Nurses learned to question doctors' orders if patient safety protocols weren't followed. Housekeeping staff understood their role in infection prevention. Even parking attendants received training on emergency response.

The five-day audit itself became organizational folklore. Surveyors traced patient journeys from admission to discharge, interviewed staff across all shifts, reviewed thousands of medical records. They tested emergency response times, evaluated medication storage temperatures, assessed hand hygiene compliance. One surveyor spent hours in the ICU, observing nurse-to-patient ratios and communication protocols during shift changes.

What JCI meant for business was transformational. International patients, particularly from Africa and Middle East, preferred JCI-accredited facilities. Insurance companies offered preferential rates. Corporate clients included JCI accreditation as selection criteria. Most importantly, it enabled premium pricing—patients willingly paid 15-20% more for internationally certified care.

Yatharth Tyagi captured the significance: "Achieving JCI accreditation is a proud milestone for Yatharth Hospital and a testament to our unwavering commitment to delivering world-class healthcare in Uttar Pradesh. This prestigious recognition is not only a reflection of the hard work and dedication of our entire team but also an assurance to our patients that they are receiving care that meets the highest international standards. We are committed to continuously raising the bar in healthcare quality, safety, and patient-centered care, and this accreditation strengthens our resolve to set new benchmarks for medical excellence in the region."

The preparation journey revealed organizational maturity. Quality indicators were digitized and monitored real-time. Clinical pathways standardized treatment protocols while allowing physician discretion. Adverse events triggered root cause analyses, not blame games. The hospital that started as a local provider had evolved into an institution matching global standards.

For Uttar Pradesh, India's most populous state with 240 million residents, having its first JCI-accredited hospital was symbolic. It challenged the narrative that world-class healthcare required Delhi or Mumbai addresses. It proved that excellence could emerge from unexpected geographies, given the right vision and execution.

VIII. Business Model & Unit Economics Deep Dive

The analyst presentation slides at Yatharth's investor meet tell a story that challenges conventional healthcare wisdom. While Apollo and Fortis chase premium segments with ARPOB (Average Revenue Per Occupied Bed) exceeding ₹50,000, Yatharth thrives at ₹30,652—proving that volume and efficiency can trump pricing power. The revenue mix tells the strategic story. IPD (In-Patient Department) contributes 87% of total revenue, significantly higher than industry average where OPD (Out-Patient Department) typically contributes 30%. This isn't accidental—it's deliberate focus on high-acuity cases requiring hospitalization, driving better unit economics despite lower prices.

ARPOB for 9MFY25 stood at ₹30,652, up 8% year-on-year, with management guiding for 10% annual growth targeting ₹35,000+ for new hospitals. The variation across facilities reveals operational maturity—Noida Extension commands ₹38,806 while Jhansi-Orchha manages just ₹13,038, highlighting the improvement potential as newer facilities mature.

Occupancy improved to 61% in 9MFY25 from 54% in FY24, with mature facilities like Noida achieving 83% while newer ones like Jhansi-Orchha improved dramatically from 27% to 47%. This occupancy leverage is crucial—fixed costs get absorbed across more patients, driving margin expansion without price increases.

Average length of stay at 4.30 days for 9MFY25 exceeds industry norms, suggesting complex case mix but also operational improvement opportunities. Longer stays increase costs but also indicate tertiary care capabilities that command premium reimbursements.

Geographic concentration shapes economics profoundly. Four of five operational hospitals cluster in NCR, enabling shared services—centralized labs, common procurement, rotating specialist pools. A single blood bank serves three facilities. One CEO manages multiple hospitals. This density drives 200-300 basis points of margin advantage versus dispersed networks.

The payer mix reveals both strength and vulnerability. Government schemes (CGHS, ECHS, Ayushman Bharat) contribute 37% of revenues—providing volume stability but creating receivable challenges with 120+ day payment cycles. Insurance and TPA payments account for 35%, while cash patients contribute 28%. The strategic shift toward insurance and cash segments drives ARPOB improvement without volume sacrifice.

Doctor engagement models differentiate Yatharth fundamentally. Unlike competitors paying 60-70% revenue shares to star doctors, Yatharth employs a mixed model—core specialists on salary plus incentives (30-35% of department revenues), visiting consultants on case basis (40-45%), and resident doctors on fixed compensation. This structure maintains quality while preserving margins.

Technology investments, though less visible than building acquisitions, drive operational efficiency. Electronic medical records reduce errors and improve billing capture. Automated pharmacy systems minimize inventory holding. Digital imaging enables remote consultations. These systems, standardized across facilities, cost ₹15-20 crores annually but generate 5-7% productivity improvements.

EBITDA margins stabilized around 25% for 9MFY25, with management expecting 26-27% once new hospitals achieve breakeven. This consistency despite rapid expansion demonstrates operational discipline—many chains see 500+ basis points margin compression during growth phases.

What makes Yatharth's model defensible isn't just current metrics but the trajectory. Each new facility starts with 15-20% EBITDA losses, achieves breakeven within 18-24 months, and reaches mature margins within 3-4 years. This predictable maturation curve, proven across multiple launches, provides confidence in future returns from current investments.

IX. Playbook: Lessons in Healthcare Entrepreneurship

The conference room at IIM Ahmedabad's healthcare management program buzzed with anticipation. Yatharth Tyagi, now whole-time director, had agreed to share the company's playbook—the strategic framework that transformed two doctors' vision into North India's fastest-growing hospital chain.

"Everyone asks about our secret sauce," Tyagi began, his presentation titled 'Building in Bharat: The Tier 2/3 Arbitrage.' "The truth is simpler and harder than any formula—we went where others wouldn't, served whom others ignored, and built what markets actually needed rather than what looked prestigious."

The arbitrage opportunity in Tier 2/3 cities remains massive even today. Land costs are 60-70% lower than metros. Construction runs 30-40% cheaper. Doctor salaries are 40-50% lower, yet quality remains comparable—many specialists prefer hometown practice over metro rat races. Most critically, competition is minimal—while South Delhi has one bed per 200 people, cities like Moradabad have one per 2,000.

But arbitrage alone doesn't build sustainable businesses. The consolidation thesis recognizes healthcare's fragmentation problem. India has 70,000+ hospitals, but 90% have fewer than 100 beds. These subscale operations lack bargaining power with suppliers, can't afford modern equipment, struggle with specialist recruitment. Consolidation creates value through procurement synergies (15-20% cost reduction), shared services (billing, labs, laundry), and network effects (patient referrals, doctor rotations).

Managing stakeholder complexity represents healthcare's unique challenge. Doctors demand autonomy yet need protocols. Nurses want respect and career growth. Patients expect hotel-like amenities with ICU-level attention. Regulators require compliance without providing clarity. Insurance companies negotiate rates while delaying payments. Each stakeholder group requires different engagement strategies, communication styles, and incentive structures.

The quality versus affordability tension defines every decision. Yatharth's solution: tiered service delivery. Critical care maintains zero compromise—same equipment, protocols, and outcomes as premium hospitals. But non-clinical services differentiate—shared rooms versus private, basic meals versus gourmet, essential diagnostics versus comprehensive panels. This enables 40-50% lower pricing while maintaining clinical excellence.

Accreditations emerged as trust accelerators. In healthcare, brand building typically requires generations. NABH accreditation shortcuts this by providing third-party validation. JCI accreditation enables premium positioning. The investment—₹2-3 crores per hospital—returns through higher occupancy (10-15% improvement), better rates (5-10% premium), and faster insurance empanelment.

Capital intensity and working capital management separate successful healthcare ventures from failures. Hospitals require ₹1-1.5 crores per bed in initial investment. Breakeven takes 2-3 years. Working capital needs are massive—inventory (medicines, consumables), receivables (insurance claims), and cash reserves (doctor payments, utilities). Yatharth's solution: staged capacity addition (opening 50% beds initially), aggressive receivable management (dedicated teams for government claims), and vendor financing arrangements.

The buy versus build decision framework evolved through experience. Build when: land is available below ₹50 lakhs per acre, the location lacks quality competition, population exceeds 500,000 in 10-kilometer radius, and time permits 3-4 year gestation. Buy when: distressed assets offer 40%+ discounts, existing infrastructure needs only cosmetic upgrades, licenses and accreditations transfer, and immediate market entry is critical.

Technology adoption strategies reflect pragmatism over glamour. While competitors tout AI and robotics, Yatharth focused on basics—EMR systems that actually work, inventory management that prevents stockouts, billing systems that capture all charges. The principle: implement technology that pays back within 18 months through either cost savings or revenue enhancement.

Cultural elements proved decisive. Unlike corporate chains importing western management styles, Yatharth maintained Indian ethos—doctors addressed with respect, family involvement in patient care encouraged, vegetarian food options prioritized, prayer rooms maintained. This cultural alignment improved both patient satisfaction and employee retention.

Risk management frameworks encompassed clinical, financial, and regulatory dimensions. Clinical risks managed through protocols, audits, and insurance. Financial risks mitigated through diversified payer mix and conservative leverage. Regulatory risks addressed through proactive compliance and government relations. The principle: accept risks you understand, hedge those you don't, avoid those you can't manage.

The lesson that resonated most: success in healthcare requires patient capital and patient temperament. Quick returns don't exist. Brand building takes years. Operational excellence emerges through repetition. But for those willing to commit—to serve underserved markets, to build systematically, to prioritize purpose alongside profit—the opportunity remains immense.

X. Competition & Market Dynamics

The battle lines in North India's healthcare market resemble a complex chess game where Yatharth plays the ambitious challenger against entrenched champions. Yatharth's Noida Extension and Greater Noida hospitals rank as the 8th and 10th largest private hospitals in Delhi NCR by bed count—impressive for a 16-year-old company competing against chains with 40+ year histories.

Apollo Hospitals, the 800-pound gorilla with 10,000+ beds nationally, operates its flagship Indraprastha Apollo Hospital in Delhi with 700+ beds. Their strategy focuses on medical tourism, quaternary care, and premium pricing. Yet Apollo's expansion into Tier 2 cities has been cautious—their ARPOB of ₹55,000+ doesn't translate to markets where household incomes average ₹30,000 monthly.

Fortis Healthcare, with 4,500+ beds across 27 hospitals, maintains strong NCR presence through Fortis Escorts and Fortis Memorial Research Institute. Post-2018's corporate governance crisis and ownership changes, Fortis shifted from aggressive expansion to consolidation and margin improvement. Their focus on metros leaves Tier 2 markets relatively uncontested.

Max Healthcare emerged from near-bankruptcy in 2020 to become India's most profitable hospital chain by margins. Operating 3,500+ beds primarily in Delhi NCR, Max pursues a "deep not wide" strategy—extracting maximum value from existing facilities through service mix optimization. Their ₹65,000+ ARPOB targets a different segment entirely from Yatharth's mass market.

Medanta, founded by cardiac surgeon Dr. Naresh Trehan, operates a 1,600-bed flagship in Gurugram plus smaller facilities. Their strategy mirrors Yatharth's more closely—expansion into Tier 2 cities like Lucknow and Patna, focus on clinical excellence over hospitality, and competitive pricing. The rivalry intensifies as both chase similar markets with comparable positioning.

Regional players present different challenges. In Uttar Pradesh, chains like Apollomedics (Lucknow), Yashoda (Ghaziabad), and Sharda Hospital (Greater Noida) compete locally but lack scale for network effects. In Haryana, Asian Hospital and Park Group focus on specific cities. These players know local markets intimately but struggle with capital access for expansion. The medical tourism opportunity represents a game-changer. India's medical value travel market, estimated at $8-10 billion in 2024, is projected to grow at 13-17% CAGR reaching $14-27 billion by 2030. For context, this equals the entire domestic healthcare market of many countries. Yatharth's JCI accreditation positions it to capture disproportionate share—international patients typically contribute 2-3x higher ARPOB than domestic patients.

Government initiatives reshape competitive dynamics. Ayushman Bharat, covering 500 million Indians with ₹5 lakh annual health coverage, drives volumes but pressures pricing. The upcoming National Health Authority's standardized treatment packages will commoditize basic procedures but advantage scale players. Proposed insurance reforms mandating minimum network hospitals benefit chains over standalones.

Technology disruption looms but hasn't arrived. Telemedicine platforms like Practo and 1mg capture OPD consultations but can't replace hospital admissions. AI diagnostics improve accuracy but require radiologist validation. Robot-assisted surgeries enhance outcomes but cost ₹3-5 crores per system. Yatharth's pragmatic approach—adopting proven technologies while avoiding bleeding-edge experiments—seems prudent.

The competitive landscape reveals strategic divergence. National chains pursue premium positioning in metros. Regional players dominate specific geographies. Specialty chains focus on single departments. Yatharth occupies a unique position—regional scale with multi-specialty offerings at mass-market pricing. This "wide moat" strategy proves harder to replicate than premium positioning or ultra-specialization.

Upcoming Noida International Airport, operational by 2025, creates a competitive advantage. Located 40 kilometers from Yatharth's Greater Noida facility, it will handle 12 million passengers annually initially, scaling to 70 million. Direct international connectivity enhances medical tourism potential while improving catchment for domestic patients. Competitors lack similar proximity to upcoming infrastructure.

Market dynamics increasingly favor consolidators. Standalone hospitals struggle with insurance empanelment, equipment financing, and specialist recruitment. Regulatory compliance costs escalate annually. Digital health records mandates require IT investments. These pressures create acquisition opportunities for well-capitalized chains—explaining Yatharth's aggressive expansion.

XI. Bear vs. Bull Case Analysis

The investment committee room at a Mumbai-based mutual fund crackles with debate. The healthcare analyst presents Yatharth as the next multi-bagger. The risk manager counters with a litany of concerns. Both make compelling cases—the truth, as always, lies somewhere between.

The Bull Case: North India's Healthcare Consolidator

The addressable market opportunity staggers even optimists. North India, with 600+ million population, has just 2.5 hospital beds per 1,000 people versus WHO's recommended 5 beds. The region needs 1.5 million additional beds by 2030—creating a ₹3 trillion investment opportunity. Even capturing 0.5% market share implies 7,500 beds, triple Yatharth's current capacity.

The acquisition pipeline provides immediate growth visibility. Management has identified 15+ potential targets in Delhi NCR alone, with combined capacity exceeding 3,000 beds. Distressed asset availability remains high—COVID's financial impact lingers, with many hospitals seeking exits. Yatharth's proven integration capabilities and access to capital position it as consolidator of choice.

JCI accreditation unlocks the medical tourism opportunity exponentially. Countries like Bangladesh, Afghanistan, and African nations contribute 500,000+ patients annually to India, spending $3,000-5,000 per visit. Even 1,000 international patients annually at Yatharth would add ₹30-50 crores in high-margin revenue. The certification also enables partnerships with global insurance companies and foreign governments.

Improving unit economics demonstrate operational leverage. ARPOB growing at 10% annually while costs increase 5-6% drives margin expansion. Occupancy improvements from 61% to 70% add 200+ basis points to EBITDA margins. New hospitals achieving breakeven faster—18 months versus industry's 36 months—validates the model.

Strategic location advantages compound over time. The upcoming Noida International Airport, Jewar-Tappal Road expansion, and Delhi-Mumbai Industrial Corridor pass through Yatharth's catchment areas. These infrastructure projects will improve accessibility and expand addressable markets by 30-40%.

Management quality and execution track record inspire confidence. Successfully integrating four acquisitions within a year while maintaining operational metrics demonstrates exceptional capability. The combination of founder-doctors' clinical credibility with second-generation professional management creates ideal leadership structure.

The Bear Case: Execution Risks in a Regulated Industry

Geographic concentration in NCR creates vulnerability. Four of seven hospitals cluster within 50 kilometers, exposing Yatharth to regional economic slowdowns, competitive intensity, or regulatory changes. A new super-specialty hospital by Apollo or Medanta in Noida could significantly impact occupancy and pricing.

Integration challenges multiply with scale. Managing seven hospitals with different cultures, systems, and processes strains management bandwidth. Each acquisition brings legacy issues—employee resistance, patient attrition, vendor contracts. The MD City Hospital acquisition, through SARFAESI auction, likely involves legal complexities and operational challenges.

Capital intensity limits return on equity potential. Healthcare requires continuous reinvestment—equipment upgrades, infrastructure maintenance, technology updates. Even mature hospitals need 15-20% of revenues as maintenance capex. Growth capex for new facilities and acquisitions could perpetually dilute returns.

Regulatory and compliance risks escalate with size. Healthcare faces stringent regulations—clinical establishment acts, biomedical waste rules, drug pricing controls. Any adverse event triggering regulatory scrutiny could damage reputation irreparably. The 2023 income tax searches and past associations with organ transplant investigations, though cleared, highlight vulnerability.

Competition from established players intensifies. As Tier 2 markets mature, national chains will inevitably enter. Apollo's recent announcements about 1,000-bed additions, Max's expansion beyond Delhi, and new players like Aster DM Healthcare entering North India signal increasing competition.

Dependence on government schemes and insurance creates payment risks. With 37% revenue from government programs notorious for 120+ day payment cycles, working capital remains stressed. Insurance companies increasingly demand discounts and reject claims, pressuring both margins and cash flows.

Quality at scale remains unproven. Maintaining clinical standards across multiple locations with rapid expansion challenges even experienced operators. One major clinical incident could trigger regulatory action, insurance delistings, and reputation damage that takes years to recover.

Technology disruption poses medium-term threats. While hospital admissions won't disappear, technology could disintermediate parts of the value chain. Home healthcare, diagnostic chains, and specialized clinics could cherry-pick profitable procedures, leaving hospitals with complex, lower-margin cases.

The Balanced View

The truth incorporates both perspectives. Yatharth operates in an industry with massive tailwinds but execution complexity. The company has demonstrated exceptional growth and operational capabilities but faces scaling challenges. The valuation at 35x P/E prices in perfect execution, leaving little room for disappointment.

For investors, the decision depends on time horizon and risk tolerance. Those believing in India's healthcare opportunity and Yatharth's execution capabilities might find current valuations reasonable for a 5-7 year holding period. Conservative investors might await correction or evidence of successful integration before committing capital.

The key monitorables: occupancy trends at new facilities, ARPOB progression, integration success metrics, competitive developments, and regulatory changes. Any deviation from management guidance on 30% revenue growth or 25% EBITDA margins would signal reassessment need.

XII. Epilogue & Looking Forward

The December sky over Noida glowed with promise as Yatharth's board announced the successful completion of their ₹625 crore Qualified Institutional Placement (QIP). Priced at ₹595 per share, the offering was oversubscribed with marquee institutions including Kotak Mutual Fund, SBI Life Insurance, Citigroup, and Societe Generale participating. The capital raise, coming just 16 months after the IPO, signaled institutional confidence in the expansion strategy.

The QIP proceeds earmarked for specific purposes reveal strategic priorities. Debt reduction takes precedence—maintaining financial flexibility for future acquisitions. Funding for Model Town (Delhi) and Faridabad hospitals ensures smooth operationalization. Medical equipment purchases for new facilities avoid operational delays. The disciplined capital allocation reflects management's understanding that in healthcare, timing determines success.

The next phase promises unprecedented transformation. Integration of seven hospitals into a cohesive network, operationalization of 700+ beds in Q1 FY26, achieving 65%+ occupancy across facilities by FY27, and maintaining 30% revenue growth while preserving margins—each milestone builds toward the vision of becoming North India's dominant healthcare provider.

Healthcare trends reshaping the industry favor prepared players. Preventive care and wellness segments, growing at 25% annually, offer higher margins than traditional treatment. Home healthcare, projected to reach ₹50,000 crores by 2027, enables extending services beyond hospital walls. Digital health integration—teleconsultations, remote monitoring, AI diagnostics—reduces costs while improving outcomes. Yatharth's investments in these areas, though nascent, position it for next-generation healthcare delivery.

The strategic roadmap appears clear. Geographic expansion continues with potential acquisitions in Agra (already announced at ₹260 crores for 150-bed Shantived Hospital), Meerut, and Ghaziabad. Service line extensions into high-margin specialties like organ transplants, robotic surgery, and IVF treatments drive ARPOB improvement. Medical tourism initiatives leveraging JCI accreditation target 5% revenue contribution by FY27.

Operational excellence initiatives promise margin expansion despite scale. Centralized procurement leveraging 2,300+ bed bargaining power, shared services for diagnostics and pathology across locations, and standardized clinical protocols reducing variability and improving outcomes—each initiative contributes 50-100 basis points to EBITDA margins.

What Yatharth's story reveals transcends one company's journey. It demonstrates how focused execution in fragmented industries creates extraordinary value. How serving underserved markets generates both profit and purpose. How operational discipline matters more than financial engineering. How building healthcare infrastructure in emerging markets represents not just business opportunity but social impact at scale.

The lessons for entrepreneurs are profound. Start where others won't go—geographic or segment arbitrage creates initial advantage. Build capabilities systematically—clinical excellence before brand building, operational efficiency before aggressive expansion. Maintain financial discipline—avoid leverage that constrains flexibility, time capital raises for maximum optionality. Think in decades—healthcare businesses compound over time, patience gets rewarded.

For investors, Yatharth represents a lens into India's healthcare transformation. The sector will add $200 billion in value over the next decade. Winners will combine scale with efficiency, quality with affordability, growth with profitability. Whether Yatharth becomes the defining success story remains uncertain, but its playbook—proven across multiple cycles—offers a template others will surely follow.

The story that began with two doctors in an empty Noida plot has evolved into something larger—a testament to entrepreneurial vision, operational excellence, and the profound opportunity in building essential infrastructure for emerging markets. As India's healthcare sector stands at an inflection point, companies like Yatharth aren't just participants but architects of transformation.

The next chapters remain unwritten, but the trajectory seems clear. More acquisitions, deeper specialization, broader geographic reach, and eventually, perhaps, emergence as North India's healthcare champion. For those watching this space, Yatharth offers not just investment opportunity but insight into how great businesses get built—one patient, one hospital, one milestone at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube