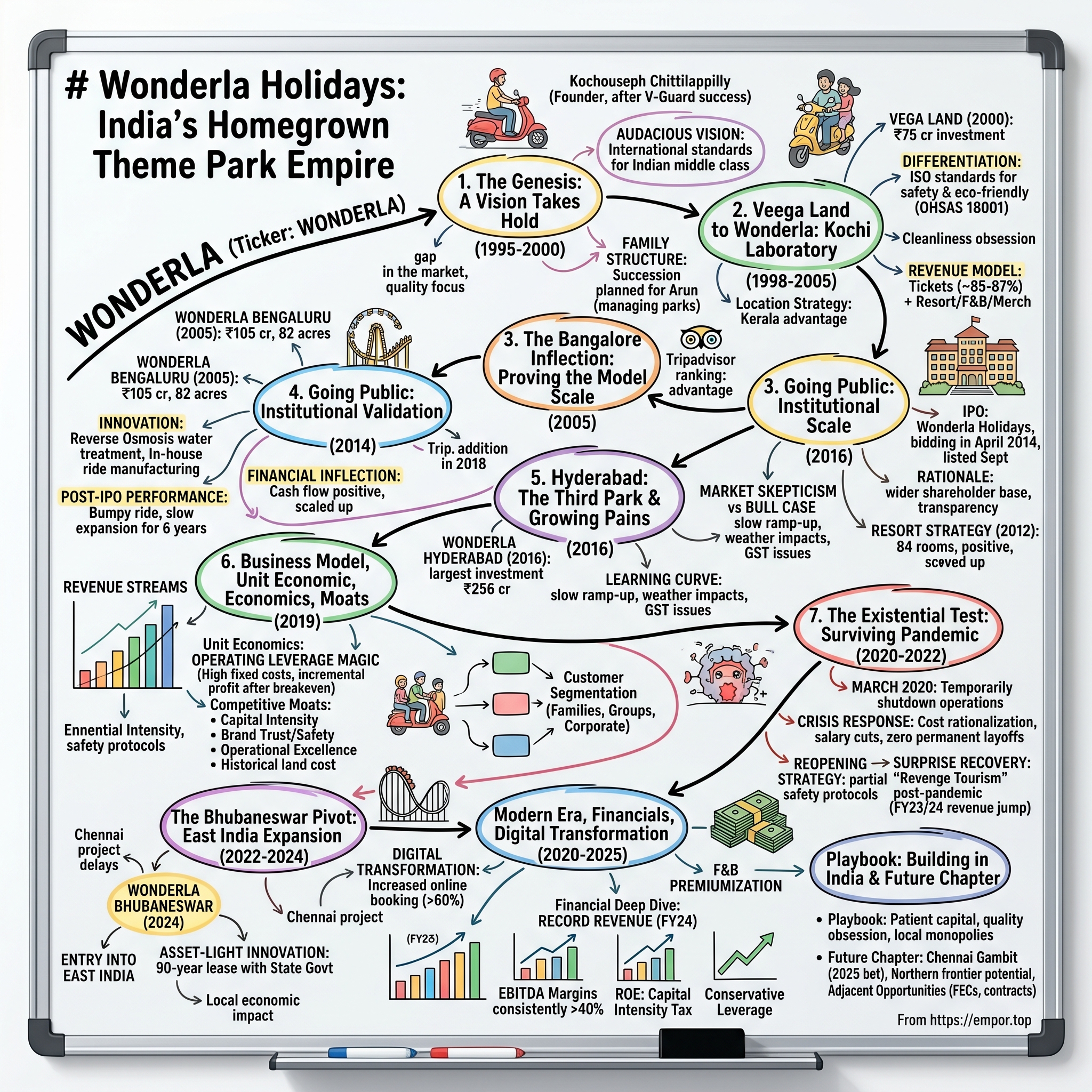

Wonderla Holidays: India's Homegrown Theme Park Empire

Picture this: Kochi, Kerala, in the late 1990s. A successful industrialist named Kochouseph Chittilappilly, having built V-Guard Industries from a ₹1 lakh borrowed capital into India's leading voltage stabilizer brand, stood at an inflection point. After decades of manufacturing electrical goods, he did something counterintuitive—he decided to get into the amusement park business. Not just any amusement park, but one that would rival international standards in a country where "theme park" meant poorly maintained rides and questionable safety protocols.

The skeptics were many. Capital-intensive businesses in India's emerging economy? Entertainment in a country where discretionary spending barely registered? A Kerala-based entrepreneur trying to compete in an industry dominated by Mumbai's Essel World? The odds seemed insurmountable.

Yet today, Wonderla operates 4 amusement parks in Kochi, Bangalore, Hyderabad and Bhubaneswar, commands a market capitalization exceeding ₹4,000 crores, and stands as the only operator at scale with pan-India ambitions in a fragmented industry of 170+ parks. This is the story of how a family business challenged Disney's playbook, survived an existential pandemic crisis, and built what might be India's only true national amusement park chain.

I. The Genesis: When an Industrialist Saw a Family on a Scooter

The year was 1995. Kochouseph Thomas Chittilappilly, born in 1950, had already established himself as the founder and CEO of V-Guard Industries—a company that had grown from a small electronics manufacturing unit started in 1977 with a capital of ₹100,000 into India's largest selling stabilizer brand.

But Kochouseph wasn't satisfied with just one successful venture. In 2000, 23 years after starting V-Guard, Wonderla was inaugurated, representing a dramatic departure from his core business. The trigger? International exposure and a keen observation of India's demographic dividend.

The gap in the market was glaring. India in the late 1990s had only a handful of amusement parks—Delhi's Appu Ghar and Mumbai's Essel World being the most prominent. But these facilities suffered from chronic underinvestment, poor maintenance, and outdated attractions. Families had few options for quality weekend entertainment. Meanwhile, Kochouseph had graduated from Christ College, Irinjalakuda and earned a master's degree in Physics from St. Thomas College, Thrissur in 1970, giving him an engineer's mindset for problem-solving.

The vision was audacious: bring international-standard amusement park experiences to India, but make them accessible to the burgeoning middle class. Not the imported Disney model with its premium pricing, but something uniquely calibrated for Indian families—clean, safe, affordable, and experiential.

The V-Guard Foundation

Understanding Wonderla requires understanding V-Guard. Kochouseph's career kickstarted in 1973 at Telics, a Thiruvananthapuram based electronics company. In 1977, he founded V-Guard Industries with 2 employees at its modest manufacturing facility in Thrissur, which grew over the years to become the largest selling stabilizer brand in India.

This wasn't just a business story—it established a playbook. Patient capital. Obsessive focus on quality. Building trust through after-sales service. Understanding Indian consumers' price sensitivity while refusing to compromise on standards. These principles, forged over two decades in electronics manufacturing, would become the DNA of Wonderla.

Kochouseph, one of the largest income tax payers since his early days, had built his businesses with a rare mix of accountability and growth appetite. This reputation for integrity would prove crucial when Wonderla needed institutional capital years later.

The Family Architecture

The Chittilappilly business empire was carefully structured for succession. Arun heads the amusement park business, Wonderla and Mithun is the incumbent Managing Director of V-Guard Industries. This wasn't accidental—it was deliberate family business planning.

Arun completed his Masters in Industrial Engineering from Swinburne University in Melbourne, Australia. After graduating, he wasn't sure if he wanted to become an entrepreneur, and was considering working for Australia's auto majors Holden or Ford for research projects. But the pull of the family business—and specifically the new amusement park venture—proved irresistible.

Arun's education at Swinburne gave him the framework for planning and engineering large spaces. He learned to see parks not just as fun places, but as intricate systems that need to be efficient, safe, and comfortable for guests. This training would prove invaluable as Wonderla scaled.

The family structure ensured alignment: Kochouseph as the patriarch and visionary, Arun as the operational driver for Wonderla, and Mithun managing the cash-generating V-Guard. No sibling rivalry, no disputes—just clear demarcation and shared values.

II. Veega Land to Wonderla: The Kochi Laboratory (1998-2005)

In 2000, Kochouseph Chittilappilly started the flagship amusement water theme park under the name Veegaland in Kochi, Kerala, investing ₹75 crore in construction and development. The name wasn't coincidental—"Veega" came from V-Guard, signaling the connection to the family's established brand.

But this wasn't a vanity project or a side hobby. From day one, the park aimed for operational excellence that would shame Indian competitors and approach international standards.

Location Strategy: The Kerala Advantage

Why Kochi? The decision revealed sophisticated thinking. Kerala in 2000 offered several advantages:

Lower land costs: Acquiring 30+ acres near a major city was prohibitively expensive in metros like Mumbai or Delhi. Kerala's land prices made the capital intensity manageable.

NRI market: Kerala's large Non-Resident Indian population provided a built-in customer base familiar with international park standards. These families, returning for holidays, had both disposable income and high expectations.

Tourism infrastructure: Kerala was already marketing itself as "God's Own Country" with growing domestic and international tourism.

Government support: State authorities were eager to support job-creating ventures in a state criticized for being entrepreneurship-unfriendly.

The location also provided a natural moat—being first-to-market in a growing region, Wonderla could establish brand dominance before competition emerged.

The Differentiation From Day One

When Veegaland opened in Kochi in 2000, it was a different landscape altogether. People weren't really used to the idea of spending on this kind of leisure. Plus, the initial investment was huge.

But Wonderla made deliberate choices that set it apart:

Cleanliness obsession: While competitors let parks deteriorate, Wonderla maintained Singapore-level standards. The entire park, including restrooms and food courts, is maintained with exceptional hygiene standards. Wonderla Bangalore earned ISO 14001 certification for its eco-friendly practices, including effective waste management and water recycling systems.

Safety protocols: Wonderla Kochi became the first park in India to get ISO 14001 certificate for eco-friendliness and OHSAS 18001 certificate for safety. This wasn't marketing fluff—it meant documented procedures, regular audits, and accountability.

Staff training: Unlike parks where ride operators were casual labor, Wonderla invested in comprehensive training programs. Employees were taught not just operational procedures but customer service principles.

Women-friendly environment: In a country where public spaces often felt unsafe for women, Wonderla emphasized security, cleanliness, and family-friendly atmosphere. This opened up a market segment competitors missed.

The Business Model Takes Shape

The early years established what would become Wonderla's enduring revenue model:

Ticket revenue dominated, accounting for 85%+ of income. But importantly, while 86% of revenues came from ticket sales, the rest were from resort, food & beverage and merchandising activities.

The economics were brutal: massive upfront capital expenditure, long payback periods, high fixed costs, but extraordinary operating leverage once breakeven was crossed. Every incremental visitor after covering fixed costs fell almost entirely to the bottom line.

The Kochi park was re-branded in 2011 to "Wonderla," dropping the V-Guard association. By then, the brand had established independent identity and national ambitions required a standalone presence.

III. The Bangalore Inflection: Proving the Model Could Scale (2005)

In 2005, with the overwhelming success of the Veegaland project, Kochouseph Chittilappilly and his son Arun launched another amusement park on a larger scale at a cost of around ₹105 crore in Bengaluru by the name Wonderla, spread over an area of 82 acres.

This wasn't just expansion—it was a bet-the-company moment. Bangalore represented a different test case entirely:

Demographics: Wonderla Bangalore, spanning over 82 acres, offers a spectacular range of entertainment with 61 rides. The city's booming IT sector created a young, affluent customer base with discretionary income and international exposure.

Competition: Unlike Kerala, Bangalore had no dominant amusement park, creating a land-grab opportunity.

Scale: At 82 acres versus Kochi's 30 acres, Bangalore represented a quantum leap in ambition and capital intensity.

The Innovation Engine

Bangalore became Wonderla's laboratory for innovation:

Water recycling technology: Wonderla is the only park in India to use Reverse Osmosis Treatment Technology for treating water in pools. The park has a fully-fledged water quality control laboratory that carries out rigorous tests on a regular basis. This wasn't just environmental virtue-signaling—in water-scarce Bangalore, it was essential for regulatory compliance and cost management.

European ride imports: Rides like Recoil, India's only reverse-looping roller coaster at Wonderla Bengaluru, show how the company took international concepts and tailored them for Indian thrill-seekers. But importing wasn't enough—Wonderla developed in-house engineering capabilities.

Manufacturing capability: The cost of in-house manufacturing is just 30% of what they'd have to pay if importing rides. And maintenance costs reduce too as they don't need to rely on others. While not self-sufficient yet, 42 out of the 160 odd rides across parks have been made in-house.

Operational excellence: Wonderla Bangalore was ranked 1st in India and 7th best in Asia by Tripadvisor for 2014, the highest for any Amusement park in India. This validation from visitors signaled that Indian operators could match international standards.

The Resort Strategy Emerges

Wonderla Holidays opened its first luxury resort in 2012—an 84-room hotel complex spread over 100,000 square feet operational since then. The resort features dedicated children's play areas and recreational and conferencing facilities, located next to Wonderla Bangalore.

This diversification made strategic sense: capture overnight visitors, tap into corporate MICE (Meetings, Incentives, Conferences, Exhibitions) revenue, and improve per-visitor economics. A family staying at the resort might spend ₹8,000-10,000 total versus ₹3,000 for just park entry—dramatically better unit economics.

The Financial Inflection

Bangalore proved the model could scale. The park achieved profitability faster than Kochi, validated the premium positioning, and generated cash flows that could fund further expansion. By 2010, Wonderla operated two successful parks and controlled the South Indian amusement park market.

But the family faced a strategic question: How to fund the next phase? V-Guard could provide only so much capital, and bank debt had limits given the capital intensity. The answer would be public markets.

IV. Going Public: The 2014 IPO & Institutional Validation

Wonderla Holidays IPO bidding started from April 21, 2014 and ended on April 23, 2014. The shares got listed on BSE, NSE on September 5, 2014. The IPO price band was set at ₹125.00 per share.

The timing was notable—after the highly successful Justdial IPO, the year passed without major IPOs due to more regulatory tightening and lower promoter enthusiasm. But the Chittilappillys were unfazed. They kept knocking at SEBI's doors, complying with whatever the newly cautious regulator asked. The result was the ₹190 crore Wonderla IPO, the first major IPO to get regulatory approval after Justdial.

The IPO Rationale

When asked why they chose the IPO route instead of private equity, Arun explained: "We could have gone the PE route any day, and obtained better valuations too. But such funds would ask for an eventual exit route, and then we'd be required to go for an IPO under pressure. So we thought it would be better to go for an IPO now itself. Public Offer has advantages, like wider shareholder base, better transparency, better visibility".

This revealed sophisticated thinking. Unlike entrepreneurs who view IPO as an exit, the Chittilappillys saw it as permanent capital—patient money aligned with long-term vision.

The IPO proceeds were ₹178 crores for setting up an amusement park in Hyderabad and the rest for general corporate purposes. The capital allocation was crystal clear.

Market Skepticism

Investors were wary:

"Theme parks don't scale": Only 3 locations in 14 years suggested limited expansion potential.

"Too capital intensive": ₹250-300 crores per park with 4-5 year payback meant returns would be mediocre.

"Disney will crush you": Once international players entered India, local operators would be obsolete.

"Discretionary spending risk": In economic downturns, amusement parks would be first casualties.

Yet the offering attracted interest. The IPO was oversubscribed 38.06 times (7.55 times in retail). Why?

The Bull Case

Income, EBITDA and Profits had grown at 21.7%, 22.1% and 26.4% CAGR respectively over 5 years. The margins were excellent with Operating Margins at 45.9% and Profit margins at 24.3% for FY13.

Compare this to V-Guard: V-Guard's IPO was in 2008, and the share performed very well, appreciating 7 times from its IPO level. Income, EBITDA and Profits had grown at 44%, 34% and 38% CAGR over 5 years. Investors were well rewarded for their shareholding. This was a great positive for the new offering from the same promoters.

V-Guard went in for its IPO in 2008 and became a 7X multibagger within six years. Whereas institutional enthusiasm had been low during V-Guard's IPO time, the reverse was expected in Wonderla's case—not only was the group now well-known in capital markets, but the market was likely to appreciate Wonderla's much better profitability and Return on Equity.

The Chittilappilly track record mattered. The company, incorporated in 2002, was one of the largest operators of amusement parks in India. Currently operating two amusement parks under the brand name 'Wonderla' at Kochi and Bangalore, it was setting up its third amusement park in Hyderabad and also operated a resort beside the Bangalore park under the brand name 'Wonderla Resort' operational since March 2012.

Post-IPO Performance: The Reality Check

Despite its might, Wonderla had a bumpy ride since going public in 2014. For 6 years, the stock price did nothing. It languished and barely returned 9% per year. It seems that investors just didn't love the amusement park business.

The reasons were multiple: slow expansion pace (just Hyderabad added in next 6 years), GST implementation hitting ticket pricing, investor preference for asset-light tech models over capital-intensive physical businesses.

But something would change dramatically—and ironically, the catalyst would be a global pandemic that shut down every amusement park on Earth.

V. Hyderabad: The Third Park & Growing Pains (2016)

A third amusement park, Wonderla Hyderabad, was commissioned in April 2016, representing Wonderla's largest investment yet. Total cost was estimated at ₹256 crore, of which ₹173 crore was funded via IPO proceeds, ₹50 crore via debt tied-up from State Bank of Travencore, and balance ₹33 crore from internal accruals. By then, ₹38 crore had already been spent, mainly towards land purchase and placing orders for new rides.

Hyderabad made strategic sense: large metro, Telugu states market, no dominant amusement park, and government support. Wonderla Hyderabad offers 28 land-based rides and 18 water-based attractions on 50 acres of land, positioned 28 kilometers from the city.

The Learning Curve

But Hyderabad proved challenging:

Slower ramp-up: Unlike Bangalore's quick profitability, Hyderabad took longer to build footfall and brand awareness. Competition from Ramoji Film City—though a different model—split the entertainment market.

Weather impact: In FY17, a service tax of 14% was imposed, the park was closed for 22 days in Q2 due to the Cauvery Water Dispute, and school exams were postponed to Q4 due to bandhs. In FY18, GST of 28% was imposed on amusement park entrance tickets. In FY19, the company reduced ticket prices to pass on the GST reduction from 28% to 18%.

Seasonality: Hyderabad's extreme summers made outdoor activities less appealing, while monsoons disrupted operations. The company had to fine-tune marketing and promotional strategies around school holidays and festivals.

The Resort Addition

A resort was launched in January 2018 adjacent to the Hyderabad park, replicating the Bangalore model. The logic remained consistent: improve per-visitor revenue, capture overnight stays, tap into corporate MICE business.

But the slow ramp-up taught valuable lessons: not every location would replicate Bangalore's success. Geography, demographics, competition, and weather all mattered. The capital intensity required disciplined site selection and patient capital—rushing expansion would destroy returns.

VI. The Business Model: How Wonderla Actually Makes Money

By 2019, Wonderla operated three parks and one resort, serving 2+ million visitors annually. Understanding the business model reveals why this works—and its inherent constraints.

Revenue Streams

Ticket sales: ~85-87% of revenue. Pricing ranged from ₹1,261 for adult regular tickets to ₹2,547 for fastrack adults, with variations for weekdays versus weekends. The pricing philosophy: affordable aspiration—high enough to maintain quality perception, low enough for middle-class affordability.

Food & Beverage: Prior to FY15, management used to lease out restaurant spaces to third party caterers on a revenue sharing basis. From FY15 onwards, they started operating restaurants themselves (took control of all restaurants from FY18). They offered deals like three meals for just ₹299, leading to significant increase in F&B revenues. Management also mandated compulsory nylon clothing for water parks "to maintain water hygiene," which increased merchandise sales where t-shirts started from ₹150.

Resort operations: Contributing ~4-5% of total revenue, but improving per-guest economics significantly.

Merchandise & photography: Lockers, branded merchandise, professional photo packages added incremental revenue.

Unit Economics: The Operating Leverage Magic

Wonderla has consistently made profits over the past decade, with operating margins consistently over 40%. The launch of the new Hyderabad park in FY17 affected profitability with increased advertising spend and employee expenses.

The magic was operating leverage. Once you covered massive fixed costs (land, rides, maintenance staff, utilities), incremental visitors had minimal variable cost. A park at 80% capacity versus 50% capacity might see profit margins double—the additional 30% capacity dropped almost entirely to the bottom line.

Capacity utilization remained the eternal challenge: weekends and holidays at 80-90% capacity, weekdays at 20-30%. School groups and corporate outings helped fill weekday gaps, but seasonality created feast-or-famine revenue patterns.

Customer Segmentation

Families: ~50% of visitors, highest per-capita spending due to F&B and merchandise purchases.

School/college groups: ~30%, lower per-capita spending but filled weekday capacity.

Corporate outings: ~20%, premium pricing for private events and team-building activities.

The Competitive Moats

What prevented competitors from replicating Wonderla?

Capital intensity: ₹250-350 crores per park created enormous entry barriers. Few entrepreneurs could access that capital, and fewer still had patience for 4-5 year payback periods.

Brand trust & safety reputation: Safety is a major concern in amusement parks, and Wonderla places it as top priority. The park adheres to rigorous international safety norms. Trained professionals routinely inspect and maintain every ride, ride operators undergo extensive safety training, and there are well-marked emergency stations, lifeguards for water rides, and staff trained in first aid throughout the park premises. Two decades of zero major accidents created enormous trust.

Operational excellence: The company has an amazing team that designed over 60 rides ourselves, on par with international standards. They even handle complex installations of foreign rides in-house after initial design consultations. This manufacturing capability dramatically reduced costs and dependence on foreign suppliers.

Land at historical costs: Wonderla owned prime land acquired years earlier at pre-boom prices. New entrants faced 5-10x higher land costs, destroying project economics.

Cleanliness culture: The "Singapore standards" obsession wasn't just marketing—it created repeat visitors and word-of-mouth growth that couldn't be bought with advertising.

VII. The Existential Test: Surviving the 2020 Pandemic

March 2020 brought an existential crisis. In view of the pandemic breakout, the company temporarily shut down operations in March. The Kochi park closed on March 11, while Bangalore Park, Resort and Hyderabad park closed between March 14-15.

Zero revenue overnight. Massive fixed costs continuing. Uncertainty about whether people would ever return to crowded public spaces. Theme parks worldwide faced bankruptcy—would Wonderla join them?

The Crisis Response

With nearly three quarters of non-operations, the company undertook massive cost rationalization—expenditure fell to ₹9.32 crore in Q2 from ₹11.90 crore in Q1. The company had around three quarters of workforce as contract labor, so they reduced that drastically. Everybody took a salary cut of more than 50 percent. Other costs like rentals were stemmed by moving the corporate office into the park premises. The idea was to survive the pandemic. Depending on operations, labor force could be ramped up quickly.

But critically, there were zero layoffs of permanent staff. This wasn't just altruism—it was the family business ethos. For the year-ended March 2021, the company made a net loss of about ₹49.9 crore, which was higher than its full year revenue of ₹44.71 crore.

The Reopening Strategy

Bangalore Park announced resumption of partial operations after closing in March due to coronavirus lockdown. Wonderla hoped to get approval soon for operations in Hyderabad, while there was still no certainty around the Kochi park. Being first to reopen became a competitive advantage.

The new operating model included: - Mandatory online booking for contact tracing - 50% capacity caps - Temperature checks at entry - Enhanced sanitization protocols - Mask mandates in common areas

Visitors confirmed: "I think that's being done very diligently—the rides, even water rides, are sanitised properly. So there's no reason to be scared".

The Surprise Recovery

Maybe Wonderla has the pandemic to thank for this change in fortunes. FY21 and FY22 were washout years with restrictions fighting the pandemic. But FY23 was different. The pandemic faded away and Wonderla's revenues rose by nearly 60% over the pre-pandemic FY20. Footfalls soared by nearly 40%. People took to leisure with a vengeance. Investors believed the pandemic was the catalyst for Indians to really enjoy life more.

The "revenge tourism" phenomenon surprised everyone. Families that had postponed celebrations, couples that missed anniversaries, children who'd spent two years in lockdown—all came flooding back. Weekends sold out. Pricing power emerged. The experience economy, far from dying, exploded.

Gross revenue for FY24 was ₹506 crores against ₹452 crores in FY23, and the company recorded highest ever Earnings Per Share at ₹27.93 in FY24.

The Strategic Insight

While asset-light digital businesses (Zomato, Swiggy, Netflix) thrived during lockdowns, physical experience businesses faced extinction. But post-pandemic, the tables turned. Physical experiences couldn't be replicated online. The scarcity of outdoor activities during lockdowns created pent-up demand that digital entertainment couldn't satisfy.

Wonderla's capital intensity—once seen as a disadvantage—became a feature, not a bug. The massive investment created barriers competitors couldn't surmount, and the brand trust built over 20 years meant families felt safe returning to Wonderla first.

VIII. The Bhubaneswar Pivot: East India Expansion (2022-2024)

In 2015, Wonderla signed MoU with the Tamil Nadu government to set up an amusement park in Chennai. The logic was obvious—Chennai was India's fourth-largest metro, had no major amusement park, and could tap into Tamil Nadu's 7 crore population.

But by 2020, something shifted. Clearance was awaited from the Town & Country Planning department for the Chennai project. Land acquisition proved challenging, costs escalated, and regulatory hurdles multiplied.

The Bhubaneswar Surprise

Wonderla Odisha began with an invitation from the government during the Odisha Tourism Investor Interaction Meet in 2019, with "in principle" approval from the State Level Window Authority for a 90-year lease. Their support was crucial, and with approval for the 90-year lease, Wonderla embarked on this journey. Challenges existed, but dedication and unwavering support from the Odisha government, notably Tourism and Industries departments, made this possible.

With an investment of approximately ₹190 crores, Wonderla Bhubaneswar showcases over 21 exhilarating dry & wet rides on 50 acres. Situated just 22.5 kilometers from Bhubaneswar, strategically positioned near NH 16 (Calcutta-Chennai), designed as a tribute to Odisha's rich cultural heritage and natural splendor.

The park opened to the public on May 24, 2024, marking Wonderla's entry into East India—and its biggest geographic gamble yet.

The Asset-Light Innovation

The property is developed on a 50-acre patch of land at an investment of ₹115 crore. The company signed an agreement with the State government for leasing land for a period of 90 years for the amusement park on an asset-light business model at Kumbharbasta village in Bhubaneswar.

This represented strategic evolution. Instead of purchasing land (major capital outlay), Wonderla negotiated a 90-year lease, dramatically reducing upfront investment. The government wanted tourism infrastructure; Wonderla wanted lower capital intensity. Both objectives aligned.

The park is committed to driving economic growth in the local community. With an estimated 450 employment opportunities, particularly in the unskilled sector, the park provides livelihood for many residents of Bhubaneswar and surrounding areas.

The Risk & Opportunity

Bhubaneswar represented a test: Could Wonderla succeed outside South Indian metros? The city had lower per capita income, less international exposure, and no amusement park culture. But it also had:

- Untapped market: Odisha's 4.5 crore population had no quality amusement park options.

- Tourism infrastructure: Bhubaneswar-Puri-Konark triangle attracted domestic tourists.

- Government support: State actively promoted tourism investments.

- East India gateway: Success here could open Kolkata, Jharkhand, and Northeast markets.

Early results looked promising. The park started commercial operations on May 24, 2024. The newest park in Bhubaneswar, launched on May 24, 2024, exceeded expectations, receiving great reception since inception.

The park with capacity of 3,500 people was constructed within 13 months with an investment of ₹190 crore over 50 acres. Since its soft launch in May, Wonderla Bhubaneswar created more than 400 employment opportunities and contributed significantly to the local economy.

IX. The Modern Era: Digital Transformation & Competitive Dynamics (2020-2025)

The pandemic accelerated digital adoption across Wonderla's operations. This quarter saw a notable rise in online bookings especially across established parks in Bangalore, Kochi, and Hyderabad compared to the same period last year. This aligns with Wonderla's focused efforts to expand its online presence each year.

Pre-pandemic, only ~20% of tickets were booked online. By 2024, this had exceeded 60%, bringing multiple advantages: demand forecasting, surge pricing capability, reduced operational overhead, customer data for targeted marketing.

Dynamic pricing experiments allowed the company to optimize revenue—charging premium prices during peak periods while offering discounts to fill weekday capacity. Annual passes and loyalty programs created recurring revenue and increased customer lifetime value.

F&B Premiumization

While discretionary spending showed caution, strategic emphasis on growing non-ticket revenue and engaging higher-value visitors supported profitability. Food evolved from basic samosas and sandwiches to gourmet burgers, international cuisines, and premium dining experiences. Average F&B spend per visitor increased 40-50% even as footfall growth moderated.

The Competition Landscape

When Monarch Capital checked Google Trends results for theme parks in India, they found Wonderla was receiving twice the interest of other big parks such as Imagicaa, EsselWorld, and Ramoji Film City.

Domestic competitors:

EsselWorld, established in 1989, was one of the first and largest amusement parks in India with more than 70 rides, a water park named Water Kingdom, a bowling alley, ice-skating rink, and Aquadrome dance floor, expanding over 64 acres. But years of underinvestment and competition from newer entertainment options eroded its dominance.

Imagicaa: Located near Mumbai, Imagicaa attempted premium positioning with significant capital investment. But high debt levels, location challenges, and execution issues led to financial struggles.

Ramoji Film City: Ramoji Film City in Hyderabad ranks sixth in 'TripAdvisor 2018 Travellers' choice awards for amusement parks and water parks', while Wonderla Amusement Park in Bengaluru secured seventh place. But Ramoji operated a different model—film tourism with some rides—rather than pure amusement park competition.

Look around and there isn't anything else that operates at Wonderla's size and scale with pan-India ambitions. Most of the 170 parks are small ones run by regional entrepreneurs. So from an investment standpoint, if you want to bet on amusement park growth, you've only got Wonderla.

International players: Disney's much-discussed India entry never materialized. Universal focused on Southeast Asia. High land costs, regulatory complexity, and uncertain returns deterred foreign investment. Wonderla won by default—being the only serious national player.

The Stock Performance

After languishing for years post-IPO, Wonderla's stock exploded post-pandemic. From the IPO price of ₹125 in 2014, the stock recorded a 52-week high of ₹947.40, representing a 7-8x return at peak. The re-rating reflected:

- Pandemic survival proving business resilience

- Post-COVID demand surge validating the experience economy thesis

- Bhubaneswar expansion signaling growth potential

- Digital transformation improving unit economics

- No viable competition emerging

Current market cap stands at ₹3,629 Crore (down 34.4% from peak in 2024), with recent revenue of ₹454 Cr.

X. Financial Deep Dive: The Numbers Behind the Magic

FY24 delivered record revenue of ₹506 crore and highest Earnings Per Share of ₹27.93. Annual footfalls of 32.52 lakhs reflected unwavering commitment to delivering unparalleled amusement experiences.

But FY25 proved challenging. For FY25, Wonderla recorded revenue of ₹458.57 crore, a 5% decline from ₹483.04 crore in FY24. Net profit for FY25 stood at ₹109.27 crore, falling sharply from ₹157.96 crore in the previous financial year.

The headwinds were multiple: Footfalls were notably affected by unprecedented heatwave, water shortages, and disruptions related to ongoing election activities, especially in key markets like Bangalore and Kochi. Additionally, there was sluggishness in discretionary spending following a surge in 'revenge tourism' post-COVID in FY 23/24.

EBITDA Margins: The Cash Generation Machine

Wonderla has consistently made profits over the past decade, with operating margins consistently over 40%. At mature parks (Bangalore, Kochi), EBITDA margins reached 45-50%. Hyderabad, still ramping up, generated 25-30% margins. Bhubaneswar, in launch phase, operated at losses initially.

The margin profile reflected operating leverage. Fixed costs (depreciation, park maintenance, base staffing) remained constant. Variable costs (incremental staff for peak periods, F&B cost of goods sold) were modest. Therefore, every rupee of incremental revenue contributed 60-70 paise to EBITDA once baseline capacity was covered.

Return on Equity: The Capital Intensity Tax

The company has a low return on equity of 12.1% over last 3 years. This ROE, while respectable, lagged asset-light businesses that could generate 25-30%+ ROE.

The reason: massive capital tied up in land, rides, and infrastructure. A ₹300 crore park generating ₹100 crore revenue and ₹40 crore EBITDA produced solid cash flows, but return on invested capital remained constrained by the denominator.

This fundamental truth limited Wonderla's valuation multiple. Investors would always discount capital-intensive businesses versus asset-light models—unless growth prospects justified re-rating.

Debt Profile: Conservative Leverage

Company is almost debt free. As of December 31, 2013, company had debt of ₹18 crore and liquid investments of ₹15 crore, making it nearly debt-free.

This conservative approach reflected family business values—avoid excessive leverage that could threaten control or survival during downturns. The pandemic vindicated this caution; highly leveraged competitors faced bankruptcy while Wonderla weathered the storm.

Recently though, expansion needs prompted capital raising. The company raised ₹540 crore through private placement, with a significant portion allocated for Chennai park development.

Cash Flow Characteristics

Each new park followed a predictable pattern: - Years 0-2: Heavy capex, no revenue, negative cash flow - Years 3-5: Operations begin, losses narrow, approaching breakeven - Years 6-20: Positive cash generation, minimal capex (only maintenance and new rides)

Bangalore, operational since 2005, had generated cumulative cash flows exceeding ₹1,000 crores—multiple times the initial investment. This long-tail economics worked, but required patient capital and nerves of steel during the gestation period.

Per-Visitor Metrics

Average spend per visitor reached ₹1,000-1,200 (including ticket, F&B, merchandise). This compared to ₹2,500+ at international parks. The gap represented both challenge (lower revenue intensity) and opportunity (pricing power as incomes rise).

Apparently, only 3% of Indian expenses go towards leisure activities. In China, it's 11%. So maybe we'll all spend a little bit more from now. If India's leisure spending even doubled to 6% of household budgets, Wonderla's addressable market would explode.

XI. The Chittilappilly Family: Values, Governance & Succession

Currently the company is run by Arun Chittilappilly as managing director, with Wonderla promoted by Kochouseph Chittilappilly and his son Arun.

Ownership Structure

Promoter holding stands at 62.26% as of June 2025, maintaining majority control. Promoter Holding is 62.3%. The family retained control post-IPO, signaling long-term commitment versus treating public offering as exit opportunity.

Promoter holding was currently at 95.48% and would decline to 70.97% post IPO. Balance pre-IPO stake was held by employees.

Governance Standards

Public listing brought discipline: quarterly earnings calls, independent directors, audit committee oversight, transparent related party transaction policies. The company operated a resort beside the Bangalore amusement park under the brand name 'Wonderla Resort' which had been operational since March 2012, with all related entities clearly disclosed.

Dividend policy maintained 20-30% payout ratio—returning cash to shareholders while retaining capital for expansion. No financial irregularities, no governance scandals, no land grab allegations. In India's corporate landscape, this clean record mattered enormously.

The Family Culture

K. Chittilappilly Foundation, a non-profit organization founded by Kochouseph, serves as the conduit for his philanthropic activities. The foundation oversees Thomas Chittilapilly Trust, running an old age home providing elderly people sustenance and medical care, and Shantimandiram, a home for destitute children providing shelter, education, and food.

In addition, Kochouseph's charitable deeds of voluntarily donating one of his kidneys at the age of 60 to a poor lorry driver caught attention of the world and set a precedent in the field of organ donation.

This wasn't wealth ostentatious display—it was rooted values from a Kerala Christian family tradition. The zero-layoffs decision during pandemic reflected this ethos. Employees weren't just labor—they were family.

Succession Planning

With two sons Mithun and Arun now active in the business, Kochouseph plays the role of grand old advisor, Chairman Emeritus. V-Guard is being managed by second son Mithun and Wonderla by elder son Arun.

The succession appeared seamless. Arun, with engineering training and hands-on experience building Bangalore and Hyderabad parks, had operational credibility. His wife Priya served as Executive Director, bringing additional leadership bandwidth.

The family's three verticals include V-Guard industries (electrical goods manufacturing that Mithun manages), V-Star apparel (mother manages), and new construction business (father launched). Arun looks after Wonderla theme parks and loves making people happy. Arun even set up the Wonderla resort, first of its kind luxury resort in India with the amusement park right in its backyard.

XII. The Playbook: What Wonderla Teaches About Building in India

Wonderla's 25-year journey offers lessons that transcend the amusement park industry:

1. Patient Capital Wins in Capital-Intensive Businesses

Resisting temptation to overexpand, the Chittilappillys opened just 4 parks in 24 years. Competitors rushed expansion, loaded debt, and collapsed. Wonderla survived by respecting capital intensity and accepting that growth would be slow but compounding.

2. Quality Obsession Creates Compounding Returns

Whether V-Guard or Wonderla or Veegaland, quality consciousness and straight forward approach in dealings with customers, suppliers, distributors, stakeholders, and after sales service all matter for success. Twenty years of zero major accidents, immaculate cleanliness, and maintained rides created word-of-mouth marketing that no advertising budget could buy.

3. Premium Positioning at Accessible Price Points

Wonderla rejected the false choice between premium quality and mass affordability. By importing European rides but manufacturing in-house, using RO water treatment but harvesting rainwater, the company delivered international standards at Indian price points. This positioning proved unassailable—premium brands couldn't match Wonderla's prices; budget operators couldn't match quality.

4. Family Business Advantages in Long-Term Games

Public company pressures would have forced faster expansion, higher debt, and shortcuts on quality. Family ownership provided patient capital, values-driven culture, and founder's mentality even after IPO. The trade-off—slower growth—proved worthwhile when competitors collapsed.

5. Local Monopolies Beat National Scale

Rather than spreading thin nationally, Wonderla dominated South India completely. Wonderla has pretty much cornered the market for fun. Each park became the unquestioned leader in its region—no viable alternative existed. These local monopolies generated pricing power and sustainable economics.

6. Capital Intensity as Moat

The business model's greatest weakness—capital intensity—became its strongest moat. ₹300-400 crore investment per park with 5-year payback deterred competitors more effectively than any patent. Scale economies in manufacturing rides, negotiating with suppliers, and training staff reinforced advantages.

7. Operational Leverage Magic

Once fixed costs were covered, incremental visitors contributed pure profit. A park operating at 70% capacity versus 50% might see profits triple—the additional 20% capacity had near-100% incremental margins. This made Wonderla extraordinarily sensitive to demand cycles but also incredibly profitable in good times.

8. The Experience Economy in Emerging Markets

Physical, shareable, memory-creating businesses thrived in India's digital age. Instagram-worthy moments, family bonding, childhood nostalgia—these couldn't be digitized. As India's middle class grew, "experiences" spending accelerated faster than goods spending.

9. Infrastructure Advantage of Moving Early

Locking in land at historical costs provided enormous advantage. While a new park currently costs around ₹500 crore to establish, rising costs make it difficult to replicate this in other locations. New entrants faced 2-3x higher land and construction costs, destroying project economics.

10. Environmental Sustainability as Competitive Advantage

Wonderla conserves natural resources and energy through minimizing consumption and wastage. Minimize process waste & promote recovery, reuse and recycling of materials. Water scarcity in Bangalore and Hyderabad made RO treatment and rainwater harvesting not just ethical but essential for regulatory compliance.

XIII. Bear vs. Bull: The Investment Debate

The Bear Case: Why Skeptics Worry

Limited scalability: Just 4 parks in 24 years suggests growth will remain glacial. At this pace, reaching 10 parks takes another 15+ years—hardly exciting for growth investors.

Geographic concentration: All parks in South/East India makes the business vulnerable to regional economic shocks, natural disasters, or competitive entry. No presence in lucrative North/West markets.

Competition from alternative entertainment: Movie theaters, gaming zones, travel, streaming—infinite options compete for leisure spending. Why assume amusement parks will gain share?

Climate risk: Water scarcity, extreme weather, and heat waves directly threaten outdoor parks. Climate change could make operations unsustainable in certain locations.

Bhubaneswar execution risk: If the East India experiment fails, it would shake confidence in geographic expansion. The Chennai project delays already raise concerns about site selection capability.

Valuation concerns: At recent multiples (30-35x P/E at peak), the stock priced in perfection. Any earnings disappointment triggers severe re-rating.

Structural ROE limitations: Capital intensity caps returns. Without 20%+ ROE, Wonderla deserves modest valuations versus asset-light businesses commanding premium multiples.

No international expansion: Being India-only limits total addressable market. Why not explore Southeast Asia, Middle East, or Africa?

Promoter selling: Promoter holding has decreased over last 3 years: -7.48%. Any significant selling could signal family's confidence wavering.

The Bull Case: Why Believers Are Optimistic

Monopoly-like economics: One company has a monopoly on this kind of fun in India. We're talking about Wonderla Holidays. Being the only scaled national player provides pricing power and market dominance.

Untapped markets: Discussions are reportedly underway for projects in Delhi, with additional parks being considered in Madhya Pradesh, Ahmedabad, Goa, and Mumbai. There have been exploratory talks about setting up a park in Ayodhya. Success in new markets could transform growth trajectory.

Pricing power emergence: As Indian incomes rise, willingness to pay for quality experiences increases. Wonderla could raise prices 7-10% annually for years while remaining affordable versus alternatives.

Resorts and MICE revenue: Chittilappilly noted a shift in visitor behaviour, with guests increasingly prioritising food options during visits. In response, Wonderla introduced new dining facilities. Doubling non-ticket revenue per visitor transforms economics without requiring more parks.

ESG credentials: Wonderla Kochi is the first park in India to get ISO 14001 certificate for eco-friendliness and OHSAS 18001 certificate for safety. Water recycling, solar power, and women-friendly employment policies attract ESG-focused institutional investors.

Recession-resistant characteristics: At ₹1,000-1,500 per person, Wonderla remains "affordable luxury"—expensive enough to feel special, cheap enough to survive downturns. The staycation trend during economic uncertainty benefits local amusement parks.

Asset-light model adoption: Wonderla is trying to convince state governments it's in their best interest to have high-quality amusement parks in their big cities. The Bhubaneswar 90-year lease model dramatically lowers capital intensity, enabling faster expansion.

Successful second-generation transition: Arun bringing professional management, digital capabilities, and aggressive growth mindset could accelerate expansion while maintaining quality.

Structural shift in leisure spending: Only 3% of Indian expenses go towards leisure activities. In China, it's 11%. As India's GDP per capita rises from $2,500 to $5,000-7,000 over the next decade, leisure spending could triple.

XIV. The Road Ahead: Wonderla's Next Chapter (2025-2030)

The Chennai Gambit

WHL is set to unveil an amusement park 45 kilometers from Chennai along Old Mahabalipuram Road. It involves investment of approximately ₹400 crore, spanning 62 acres in Illalur village, Thiruporur taluk of Chengalpet district.

Wonderla secured a six-month extension from Tamil Nadu Government for commissioning the Chennai Park. The company now has until December 2, 2025, to commence commercial operations, while retaining its previously granted 10-year Local Body Tax exemption. The original order dated June 2, 2023, stipulated 24-month construction timeline setting deadline of June 2, 2025. The successful representation means the company can complete the project by the new December 2, 2025 deadline with the full decade-long LBT exemption intact.

Chennai represents Wonderla's largest single investment and highest-stakes bet. Success validates the expansion model; failure would devastate growth narrative.

The Northern Frontier

Wonderla has set target to expand portfolio to 10 parks shortly. While a new park currently costs around ₹500 crore to establish, discussions are underway for projects in Delhi, with additional parks being considered in Madhya Pradesh, Ahmedabad, Goa, and Mumbai. There have been exploratory talks about setting up a park in Ayodhya.

North and West India remain white spaces. Delhi NCR's 3 crore population, Ahmedabad's 8 million people, Mumbai's 2 crore metro residents—all underserved by quality amusement parks. But challenges are formidable: higher land costs, more aggressive competition, different consumer preferences, extreme weather (Delhi summers/winters).

Technology Integration

Digital transformation continues: AI-powered demand forecasting, IoT sensors for predictive maintenance, AR/VR attractions, cashless payments, and personalized marketing based on visitor data. The pandemic accelerated tech adoption; the question is whether Wonderla can leverage data to improve operations and customer experience.

Mobile apps could enable queue-skipping (pay premium to reduce wait times), personalized ride recommendations, gamification (collect digital badges), and post-visit engagement (share photos, book next visit).

Content & IP: The Missing Piece?

Disney's power comes not just from rides but from beloved characters and stories. Should Wonderla create mascots, develop storylines, or license Indian IP (Chhota Bheem, mythological characters)? Or remain a pure operations business focused on quality rides?

The family has resisted this path, perhaps wisely. Creating content requires different skills; failed IP investments could destroy returns. Better to stay focused on operational excellence—the core competency that built the business.

Adjacent Opportunities

Indoor FECs: Family Entertainment Centers in malls (smaller footprint, 10,000-20,000 sq ft, lower capex) could extend the Wonderla brand into cities too expensive for full parks.

Management contracts: Operate parks for others (government, developers) without capital investment—asset-light revenue stream leveraging brand and operational expertise.

International: Southeast Asia, Middle East, or Africa could offer growth, but execution complexity, cultural differences, and regulatory challenges make this unlikely near-term.

Franchise model: License the Wonderla brand to regional operators. But quality control challenges could damage reputation—family business ethos makes this unattractive.

M&A Possibilities

Would Wonderla acquire struggling competitors like Imagicaa? The opportunity exists: distressed sellers, established infrastructure, and immediate footfall. But integration challenges, cultural fit concerns, and requirement to fix broken operations make acquisitions risky. Organic growth through greenfield parks maintains quality control.

XV. Why Wonderla Matters Beyond the Stock

Wonderla's significance transcends market capitalization and quarterly earnings:

Proof of Concept: World-Class Indian Consumer Businesses

In an economy often criticized for copycat models and foreign dependency, Wonderla demonstrated Indians could build world-class consumer brands without foreign capital, partnerships, or imported management. The company aims to bring the best of international amusement to India in a way that feels right for Indian families, taking inspiration from rides around the world but adapting them for our climate, culture, and price points.

Manufacturing to Services Evolution

India's economic transition—from agriculture to manufacturing to services—found embodiment in the Chittilappilly family journey. Kochouseph manufactured voltage stabilizers; Arun created experiences. The evolution from making products to creating memories paralleled India's GDP composition shift.

The Founder Archetype

The Chittilappilly family had been traditional agricultural family for generations with roots firmly in soil. Starting with seed capital of $1,500, V Guard industries built up a huge empire of $1.2 billion net worth four decades later. The journey from Kerala farmland to public company CEO embodied Indian entrepreneurship's potential.

Employment & Skill Development

Since soft launch in May, Wonderla Bhubaneswar created more than 400 employment opportunities and contributed significantly to the local economy. Across all operations, Wonderla employed 1,500+ direct staff and 5,000+ indirect workers, providing hospitality training, safety certification, and career development in a sector often characterized by informal employment.

Safe Public Spaces

In a country where public spaces often felt unsafe, particularly for women and children, Wonderla created islands of security. Safety is a major concern in amusement parks, and Wonderla places it as top priority with well-marked emergency stations, lifeguards for water rides, and staff trained in first aid throughout the park premises. The social value—enabling families to create memories without fear—defied easy quantification.

Benchmark for Patient Capital

For private equity firms and venture capitalists, Wonderla illustrated that capital-intensive, long-gestation businesses could generate attractive returns with patient capital and operational excellence. The lesson: not everything needed to be asset-light and digitally scalable.

XVI. Final Reflections: The Wonderla Way

On November 2, 2025, Wonderla stands at an inflection point. For FY25, revenue declined 5% to ₹458.57 crore from ₹483.04 crore in FY24, with net profit falling to ₹109.27 crore from ₹157.96 crore. The post-pandemic euphoria faded; now comes the hard work of sustained profitable growth.

The Chennai park, expected to open by December 2025, represents a ₹400 crore bet on South India's largest untapped market. Bhubaneswar, operational for just six months, must prove that the Wonderla model works beyond traditional metros. And ambitious plans for North/West India await capital allocation decisions that will define the next decade.

The bears see a capital-intensive, slow-growth business trapped in South India with limited international comparison and structural ROE challenges. The bulls see India's only scaled amusement park operator, sitting on valuable land, with pricing power, operational excellence, and decades of runway as India's middle class explodes.

Who's right? Perhaps both.

Wonderla will never be a 10x stock in 5 years. The physics of capital intensity prevent that. But as a 15-20% annual compounder over decades, with dividend yield cushioning returns, it offers something rare: boring consistency in a market obsessed with glamorous growth.

The Chittilappilly playbook—patient capital, quality obsession, family values, operational excellence, conservative leverage—worked for 25 years. It survived competitive intensity, regulatory whiplash, taxation volatility, and a global pandemic that closed every park worldwide.

If India's GDP grows 6-7% annually, per capita income doubles by 2035, and leisure spending as percentage of household budgets even partially converges to developed country levels, Wonderla's addressable market expands dramatically. The company could operate 10-12 parks generating ₹2,000+ crores revenue and ₹500+ crores EBITDA by 2035. That's a business worth ₹10,000-15,000 crores—3-4x today's market cap.

But execution risk looms large. Every new park must succeed. Quality must never slip. Safety cannot have single major incident. Competition, while currently weak, could emerge. Climate change threatens water availability. Consumer preferences could shift to virtual experiences.

The path forward requires the same discipline that built the business: site selection patience, construction quality, operational paranoia, financial conservatism, and family stewardship that thinks in decades rather than quarters.

As Arun recently noted, reflecting on the company's mission: At Wonderla, we aim to bring the best of international amusement to India in a way that feels right for Indian families. That simple philosophy—world-class quality at Indian value—captured Wonderla's enduring formula.

Twenty-five years after a Kerala industrialist decided to build an amusement park, Wonderla has created something rare in Indian business: a sustainable, profitable, trusted consumer brand with genuine competitive moats. Not sexy, not viral, not disrupting anything—just consistently delivering joy to millions of families year after year.

In a market obsessed with the next unicorn, maybe there's something wonderful about that.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube