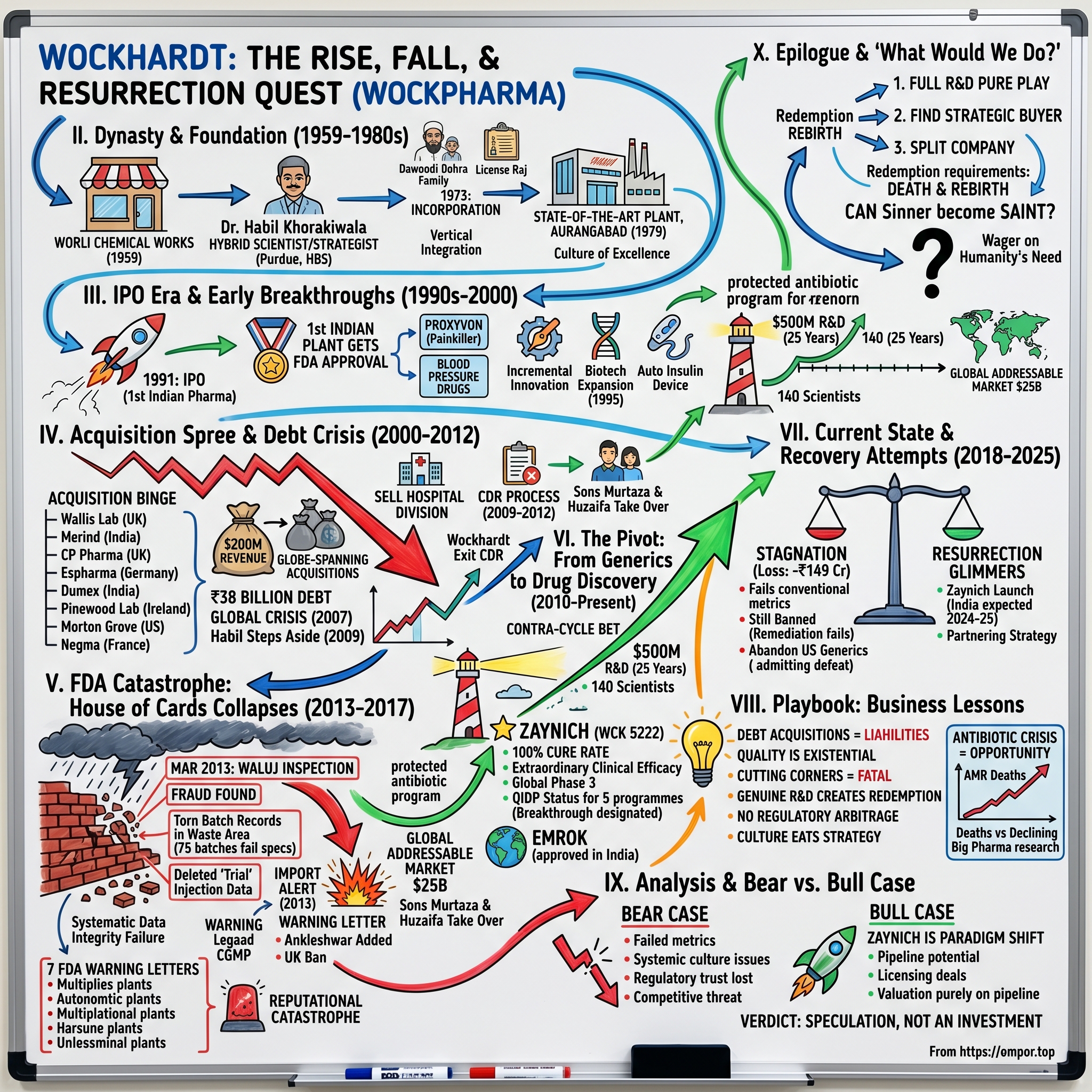

Wockhardt: The Rise, Fall, and Resurrection Quest of India's Antibiotic Pioneer

I. Introduction & Episode Roadmap

Picture this: A pharmaceutical company sitting on what could be the most valuable antibiotic pipeline in the world, with a market cap of ₹24,645 crores, yet bleeding money with losses of ₹149 crores. A company that holds the potential cure for humanity's next superbug crisis, but can't sell its products in America because the FDA has blacklisted seven of its plants. This is Wockhardt in 2025—simultaneously India's greatest pharmaceutical cautionary tale and its most audacious redemption story.

The central tension of Wockhardt's saga reads like a Shakespearean tragedy with a potential third act resurrection. How did a company that pioneered Indian pharma's global ambitions—the first to get FDA approval for an Indian plant, the acquirer of facilities across three continents—become the poster child for everything wrong with emerging market quality standards? And more intriguingly, how did that same company, while banned from the world's largest pharmaceutical market, quietly build what might be the world's most important antibiotic research program?

This is a story about family business dynamics playing out on a global stage. About how debt-fueled international expansion can transform vision into nightmare. About the hubris of thinking you can outsmart the world's toughest regulators. But it's also about scientific redemption—how a company can pivot from being a copycat generic manufacturer to potentially saving humanity from the antibiotic apocalypse.

What makes Wockhardt fascinating isn't just its spectacular fall—it's the economics of its chosen path to redemption. While the world's big pharma abandoned antibiotic research (you cure the patient in 10 days, versus lifetime treatment for chronic diseases), Wockhardt doubled down. They've increased their antibiotic patent filings by 315% while global filings dropped 60%. They're betting the company on drugs that governments don't want to use until absolutely necessary—the opposite of a blockbuster business model.

Today, Wockhardt operates as a global pharmaceutical and biotechnology organization, manufacturing finished dosage formulations, injectables, and biopharmaceuticals. But those corporate descriptors hide a far more dramatic reality: This is a company fighting for its life while simultaneously trying to save ours.

II. The Khorakiwala Dynasty & Foundation (1959-1980s)

The Wockhardt story begins not in a laboratory or boardroom, but in the bustling commercial district of 1950s Bombay, where Fakhruddin T. Khorakiwala saw opportunity in a small chemical works. In 1959, he acquired Worli Chemical Works—a modest operation that would become the foundation stone of an empire. But the real architect of Wockhardt's destiny was his son, Dr. Habil Khorakiwala, born in 1942 into a Dawoodi Bohra family known for their entrepreneurial spirit and tight-knit community bonds.

Habil wasn't content with the traditional trading businesses that many Bohra families pursued. He had grander ambitions, shaped by an education that spanned continents. After completing his Bachelor's degree in Pharmacy in India, he headed to Purdue University for a Master's in Pharmaceutical Science—a rarity for Indians in that era. Later, he would add Harvard Business School's Advanced Management Program to his credentials, becoming a unique hybrid of scientist and strategist. (In 2010, Purdue would honor him as the first non-American in 125 years to receive an honorary doctorate—though by then, his empire would be teetering on the edge.)

The transformation from Worli Chemical Works to Wockhardt began in earnest when Habil returned from America with ideas that seemed almost heretical in License Raj India. In 1973, he incorporated Wockhardt Private Limited, choosing a name that cleverly combined "Worli," "Chemical," and "Khorakiwala"—branding that suggested both continuity and ambition. This wasn't going to be another trading company or basic chemical manufacturer. Habil envisioned a pharmaceutical company that could compete globally, starting with domestic formulations.

The License Raj—India's byzantine system of permits and quotas—meant that every business decision required navigation through government bureaucracy. Where others saw obstacles, Habil saw competitive moats. If you could master the system, you had protection from competition. He became expert at working the corridors of power in Delhi, securing licenses for products that others hadn't thought viable.

But Habil's masterstroke came with a decision that his advisors thought was madness: building a state-of-the-art manufacturing facility in Aurangabad. In the 1970s, Aurangabad was a backwater—poor infrastructure, limited skilled labor, far from both suppliers and markets. Conventional wisdom said pharmaceutical plants belonged near Mumbai or Delhi. Habil saw differently. Land was cheap, the Maharashtra government was offering incentives to develop backward regions, and being away from competitors meant he could build a unique culture. The Aurangabad facility, built in 1979, would become both the crown jewel and the Achilles' heel of Wockhardt's empire. It set up a pharmaceutical formulation manufacturing plant at Aurangabad, Maharashtra, India in what was then considered a risky bet on an underdeveloped region. But Habil understood something fundamental about pharmaceutical manufacturing: if you could build a culture of excellence in isolation, away from the bad habits of established industrial centers, you could leapfrog the competition.

By the early 1980s, Wockhardt was no longer just Habil's project—it was becoming a family dynasty. The Khorakiwala name carried weight in Bohra business circles, and Habil was grooming the next generation. The company culture reflected Bohra values: tight loyalty, conservative financial management (ironically, given what would come later), and a preference for keeping control within the family. This would prove both a strength—enabling quick decision-making—and eventually a weakness when external oversight was desperately needed.

The 1980s saw Wockhardt methodically building capabilities. While other Indian pharma companies were content being traders or basic manufacturers, Habil was investing in R&D, even if modest by global standards. He understood that the License Raj wouldn't last forever, and when India opened up, only companies with real manufacturing and development capabilities would survive. The company floated Wockhardt Synchem Pvt. Ltd. (WSPL) to manufacture bulk drugs at Ankleshwar, Gujarat, creating vertical integration that would give them control over their supply chain—a prescient move that would pay dividends in the liberalized economy to come.

III. The IPO Era & Early Breakthroughs (1990s-2000)

When India's economy cracked open in 1991, most businesses were caught flat-footed. Not Wockhardt. Habil Khorakiwala had been preparing for this moment for a decade. As the License Raj crumbled and global competition loomed, Wockhardt made a bold move that would define its trajectory: becoming the first pharmaceutical company to tap India's newly liberalized capital markets with an IPO.

The initial public offering wasn't just about raising money—it was a statement of intent. Wockhardt was declaring itself ready to compete not just in India, but globally. And they backed up that ambition with a historic achievement: becoming the first Indian pharmaceutical company to receive FDA approval for a manufacturing facility. This wasn't just a regulatory milestone; it was a psychological breakthrough for Indian pharma. If Wockhardt could meet FDA standards, it proved Indian companies could compete in regulated markets.

Wockhardt gained market share with its painkiller Proxyvon (opioid tramadol + paracetamol) and blood pressure drugs during this period. Proxyvon became a phenomenon—a combination painkiller that cleverly mixed tramadol with paracetamol, creating a product that was effective enough to build loyalty but not so potent as to attract regulatory scrutiny. It was classic Habil thinking: find the sweet spot between innovation and practicality.

The Proxyvon success revealed Wockhardt's emerging playbook: identify therapeutic gaps in the Indian market, develop combinations or formulations that addressed local needs, then use the cash flow to fund international ambitions. They weren't trying to discover new molecules—that was too expensive and risky. Instead, they were becoming masters of what's known as "incremental innovation"—taking existing drugs and making them better, cheaper, or more convenient.

In 1995, it expanded into biotechnology, and subsequently started producing intravenous fluids. This wasn't following fashion—biotech was barely understood in India then. But Habil saw that biologics would eventually dominate high-value therapeutics. Starting with simple products like vaccines (they launched BIOVAC-B, a recombinant hepatitis B vaccine), Wockhardt was building capabilities that would take decades to mature.

The company also pioneered drug delivery innovation in India, launching the country's first automatic insulin delivery device. These weren't blockbuster products, but they demonstrated something important to regulators and partners: Wockhardt wasn't just a copycat generic company. They could innovate, even if incrementally.

By the late 1990s, Wockhardt had built significant domestic market share and was generating substantial cash flow. The company philosophy during this period could be summed up as "dominate locally, aspire globally." They were among the top players in several therapeutic categories in India, giving them the financial cushion to think bigger.

The international strategy began modestly. Rather than immediately targeting the US market like some competitors, Wockhardt focused on less regulated but still profitable markets—Russia, Southeast Asia, Africa. These markets wanted quality medicines at affordable prices but didn't have the stringent regulatory requirements of the FDA or European authorities. It was a smart intermediate step, allowing Wockhardt to learn international business without betting the company.

Wockhardt Ltd. was incorporated on 8 July 1999, restructuring the company for its global ambitions. The new millennium was approaching, and Habil Khorakiwala had positioned Wockhardt perfectly: strong domestic business, growing international presence, FDA-approved facilities, and access to capital markets. What could go wrong?

The answer, as we'll see, was everything—when ambition outran capability, when debt replaced discipline, and when the culture that enabled rapid growth proved incompatible with the meticulous requirements of global pharmaceutical manufacturing. But in 2000, standing at the threshold of global expansion, Wockhardt looked unstoppable.

IV. The Acquisition Spree & Debt Crisis (2000-2012)

If you want to understand how a company can go from hero to zero in pharmaceutical circles, study Wockhardt's acquisition binge of the 2000s. It reads like a cautionary MBA case study: a company with roughly $200 million in revenues deciding it could swallow companies across three continents, funded almost entirely by debt.

The buying spree started innocuously enough. Wockhardt's acquisitions include Wallis Laboratory, UK (1998); Merind, India (1998); CP Pharmaceuticals, UK (2003); Espharma GmbH, Germany (2004); Dumex, India (2006); Pinewood Laboratory Ireland (2006); Morton Grove Pharmaceuticals, US (2007); and Negma, France (2007). Each acquisition had its own logic. Wallis gave them UK market access. CP Pharmaceuticals brought hospital injectables expertise. Morton Grove provided a US platform. Negma offered European registrations.

Habil Khorakiwala's strategy seemed brilliant on PowerPoint slides: acquire distressed or undervalued assets in developed markets, inject Indian cost efficiency, and leverage Wockhardt's emerging market relationships. He called it "acquiring technological competencies"—buying not just facilities but knowledge, registrations, and customer relationships that would take decades to build organically.

The crown jewel was Morton Grove Pharmaceuticals, acquired in 2007 for $33 million. Based in Illinois, Morton Grove specialized in liquid formulations—syrups, suspensions, solutions—products that seemed pedestrian but had stable demand and decent margins. More importantly, it had FDA-approved facilities and established relationships with US pharmacy chains. For Wockhardt, it was their beachhead in the world's largest pharmaceutical market.

But timing, as they say, is everything. The 2007 acquisitions closed just as the global financial crisis erupted. Credit markets froze. The rupee plummeted. Suddenly, dollar-denominated debt taken to fund acquisitions became crushingly expensive to service. Wockhardt's debt following the acquisitions was close to Rs 38 billion, and Habil Khorakiwala quit as managing director.

The debt number—₹38 billion—doesn't capture the full disaster. This was roughly double Wockhardt's annual revenues. Interest payments were consuming nearly all operating cash flow. The acquired companies, rather than generating synergies, were bleeding money as Wockhardt discovered that running facilities in UK, France, and Ireland was vastly more complex than managing plants in Aurangabad.

The first emergency measure came in 2009: selling the hospital division. Wockhardt had built a chain of super-specialty hospitals—another of Habil's diversification dreams. These were sold to Fortis for ₹909 crores, providing temporary relief but also removing a stable, cash-generating business. It was like selling furniture to pay the mortgage—necessary but ultimately self-defeating.

Corporate Debt Restructuring (CDR) became Wockhardt's new reality. The CDR mechanism, created by Indian banks to help overleveraged companies, essentially meant convincing lenders to accept delayed payments and restructured terms rather than forcing bankruptcy. For Wockhardt, it meant years of negotiations, asset sales, and operating under the watchful eye of bankers who now effectively controlled the company.

The human drama played out in parallel with the financial crisis. The board of directors, on 31 March 2009 approved the appointments of Habil Khorakiwala's sons Murtaza Khorakiwala and Huzaifa Khorakiwala as managing director and executive director respectively. Habil, the visionary who built the company, stepped aside (officially, at least) while his sons took operational control. It was a generational transition under the worst possible circumstances—like taking the wheel of a car that's already skidding off the road. The CDR process, which began in 2009, wasn't concluded until 2012. By 2012, Wockhardt was ready to announce that it had completed the restructuring exercise and would be exiting the CDR cell by the year end, but the celebration was premature. The restructuring involved concessional interest rate of 10%; of which 8% was payable on a monthly basis and rest 2% was converted into preference share capital, substantially reducing the immediate cash burden.

During this period, Wockhardt's operations continued, but it was like running a marathon with weights strapped to your legs. Every decision was scrutinized by lenders. Capital expenditure was frozen. R&D budgets were slashed (except, interestingly, for the antibiotic program—more on that later). Key talent left for competitors. The company that had once dreamed of challenging Big Pharma was now struggling to keep the lights on.

The international facilities that were supposed to be Wockhardt's pathway to global dominance became albatrosses. European operations were hemorrhaging money. The cultural integration that consultants had promised never materialized. French workers at Negma didn't suddenly embrace Indian cost-cutting measures. Irish regulators at Pinewood didn't become more flexible because the owner was from Mumbai. Morton Grove in America continued operating, but without investment, it was a wasting asset.

What's remarkable, looking back, is that Wockhardt survived at all. Wockhardt's share price increased from Rs 391.4 in Feb, 2012 to Rs 1685 in Jan 2013, registering a growth of 331%! Markets were betting on recovery. The CDR had bought time. The Khorakiwala family had managed to retain control. But the worst was yet to come—because while Wockhardt was restructuring its finances, the FDA was preparing to restructure their entire understanding of quality control.

V. The FDA Catastrophe: A House of Cards Collapses (2013-2017)

If you want to understand how quickly a pharmaceutical company can go from recovery to catastrophe, study what happened to Wockhardt in 2013. Just months after exiting CDR and with its stock price soaring, FDA investigators walked into the Waluj facility for what should have been a routine inspection. What they found would become one of the most shocking quality scandals in pharmaceutical history. The March 2013 inspection at Waluj facility revealed significant CGMP violations and documented that firm withheld truthful information, delayed and limited inspection. But the true horror emerged in what the investigators discovered in a waste area: FDA investigators found unofficial batch records for approximately 75 batches torn in half in waste area, with data indicating batches failed specifications while official records stated they met specifications, with up to 14% of vials having defects including black particles, fibers, glass particles.

Think about that for a moment. This wasn't one rogue employee doctoring a single batch. This was systematic fraud involving dozens of batches, with quality control personnel actively destroying evidence of failures. The torn records in the trash weren't just paper—they were the smoking gun of a culture that had completely lost its way.

The deletion of "trial" injection data from HPLC hard drives as part of internal audit following the FDA inspection showed this wasn't accidental—it was deliberate cover-up. When investigators started asking questions, quality-assurance personnel tried to hide records of batch failures, started to destroy test samples. During the inspection, an employee tried to dispose of unlabeled vials in a drainage sink when inspectors approached with questions.

The FDA's response was swift and brutal. Wockhardt Waluj was placed on Import Alert on May 22, 2013, followed by a Warning Letter dated July 18, 2013. The language in these documents is extraordinary for a regulatory agency—they essentially accused Wockhardt of criminal behavior. "Because you directed FDA investigators away from the requested documents... you limited our ability to conduct a meaningful inspection," the FDA wrote, barely containing their fury.

But Waluj was just the beginning. FDA added Wockhardt's bulk manufacturing plant in Ankleshwar to import alert list, joining plants in Waluj and Chikalthana that were banned in 2013. The Chikalthana facility was testing "trial samples" of drugs, then linking results from those to official samples that had not met requirements—a different method of fraud, but fraud nonetheless.

The financial impact was immediate and devastating. U.S. import ban could cost $100 million in lost sales, UK followed suit with ban and recalled 16 Wockhardt drugs from market. But the numbers don't capture the reputational catastrophe. Wockhardt had become the poster child for everything wrong with emerging market pharmaceutical manufacturing.

By 2017, Wockhardt had amassed a record seven FDA warning letters for plants on three continents. The FDA's frustration was palpable in their communications: "These repeated failures at multiple sites demonstrate your company's inadequate oversight and control over the manufacture of drugs," they wrote. In multiple meetings, Wockhardt officials "have repeatedly discussed and promised corporate-wide corrective actions," yet when inspectors returned, they found the same violations.

The cultural clash between Indian manufacturing practices and FDA standards was at the heart of the problem. In India's domestic market, quality standards existed but enforcement was lax. The jugaad mentality—finding workarounds and shortcuts—that served entrepreneurs well in navigating bureaucracy was poison in a regulated environment where every deviation could kill patients.

What made Wockhardt's violations particularly shocking was their brazenness. This wasn't subtle manipulation of borderline results—this was outright fabrication. The company that had once proudly claimed to be the first Indian firm with FDA approval had become the first with seven warning letters. The very facilities that were supposed to showcase Indian pharma's global competitiveness had become symbols of its failures.

VI. The Pivot: From Generics to Drug Discovery (2010-Present)

While Wockhardt's manufacturing facilities were imploding under FDA scrutiny, something remarkable was happening in a different corner of the company. Even as revenues collapsed and trust evaporated, Habil Khorakiwala made a decision that seemed either visionary or delusional: he protected the antibiotic research program from budget cuts. Wockhardt's Drug Discovery team has 140 scientists working on antibiotic research for the last 20 years. This wasn't a recent pivot—even during the acquisition spree, even during the CDR crisis, Habil had maintained this team. Wockhardt has spent $500 mn in research and development in the last 25 years. Half a billion dollars, while the company was drowning in debt and regulatory violations.

The antibiotic crisis provided the opportunity. From 1983 to 1992 there were 30 antibiotics launched in regulated countries, but from 2008 to 2016, only 7 drugs approved. Big Pharma had essentially abandoned antibiotic research. The economics were terrible: you cure a patient in 10 days versus treating chronic conditions for life. Governments and health systems wanted new antibiotics held in reserve for emergencies, meaning even successful drugs wouldn't generate blockbuster revenues.

But Wockhardt saw what others didn't: this market failure created a massive unmet need. Antimicrobial resistance was killing 700,000 people annually and projected to reach 10 million by 2050. Someone had to develop new antibiotics, and whoever succeeded would have pricing power and government support that normal drugs never receive.

The crown jewel of their program is WCK 5222 (Zaynich): Contains Zidebactam, a new drug developed by Wockhardt, combination of Zidebactam and Cefepime. This isn't just another me-too antibiotic. Zidebactam is a first-in-class β-lactam enhancer with a potent inhibition of penicillin binding protein (PBP) 2 of all the clinically relevant Gram-negative organisms including Pseudomonas aeruginosa, Acinetobacter baumannii and Enterobacterales. It is also a potent inhibitor of Ambler class A and C β-lactamases including Klebsiella pneumoniae carbapenemases. By virtue of its universal stability to serine or metallo β-lactamases, zidebactam synergizes with PBP 3-binding cefepime and overcomes nearly all the known enzymatic and non-enzymatic resistance mechanisms in Gram-negative pathogens.

The clinical results have been extraordinary. Clinical trials demonstrated a remarkable 100% cure rate among 30 critically ill patients with life-threatening drug-resistant infections, has also been found to be safe even after prolonged use for 70 days in critical patients. In the broader Indian study, Zaynich® demonstrated over 97% clinical efficacy in a pivotal study targeting carbapenem-resistant Gram-negative pathogens. Conducted across 15 leading tertiary hospitals in India, the study included patients with severe infections such as bloodstream infections (BSI), hospital-acquired bacterial pneumonia (HABP), and complicated urinary tract infections (cUTI). Overall clinical efficacy: 98% across indications, with 100% success in treating BSI, HABP, and cIAI (complicated intra-abdominal infections).

US FDA granted fast track clinical trial and approval process (QIDP status)—essentially acknowledging that this drug addresses a critical public health need. Zaynich has been granted a susceptibility breakpoint of 64 mg per litre for around 10 gram negative pathogens showing high resistance rates by the American Clinical and Laboratory Standards Institute—compared to 4-8 mg/litre for recent antibiotics, meaning it's effective at much higher concentrations than existing drugs.

Total addressable market estimated at $25 billion globally, expects no competition for at least 15 years as there's no similar drug in development pipelines globally. This isn't hyperbole—antibiotic development is so difficult and unprofitable that Wockhardt genuinely might have the field to itself.

WCK 771 & WCK 2349 represent another achievement: First two NCEs from Wockhardt's antibiotic discovery program approved in India in 2019 as first ever India discovered novel antibiotics, introduced under brand name EMROK. While these don't have the global potential of Zaynich, they prove Wockhardt can take molecules from discovery through approval.

The numbers tell the story of Wockhardt's contrarian bet: Over last 10 years global patents filed for antibacterial declined by 60%, whereas patents filed by Wockhardt increased by 315%. They're essentially betting the company on a therapeutic area everyone else has abandoned.

Only company where USFDA has given QIDP Status for 5 Anti-bacterial discovery programmes. Think about that—a company banned from selling in America has more FDA-designated breakthrough antibiotics than most Big Pharma companies combined.

The economics of antibiotic development versus chronic disease drugs remains challenging. "We have decided to market ZAYNICH in India and emerging markets and licence it for the US, Europe, and developed countries to one of the global pharmaceutical companies," explained Dr Khorakiwala. This licensing strategy acknowledges reality: Wockhardt doesn't have the credibility or infrastructure to market in developed markets themselves, but they can capture value through partnerships.

What makes this pivot remarkable isn't just the science—it's the timing. While Wockhardt was being pilloried for quality failures in generic manufacturing, they were quietly building world-class capabilities in the hardest area of drug development. It's like a student expelled for cheating who goes on to win a Nobel Prize. The contradiction is almost too perfect to believe, yet the data is undeniable.

VII. Current State & Recovery Attempts (2018-2025)

Today's Wockhardt is a company frozen between death and resurrection. The numbers tell a story of stagnation: Market Cap ₹24,645 Cr, Revenue ₹3,011 Cr, Profit: -₹149 Cr. Poor sales growth of 1.15% over past five years, low return on equity of -6.95% over last 3 years. By any conventional metric, this is a failing company. The remediation efforts at banned facilities have been ongoing for over a decade with little to show. As of 2024, multiple Wockhardt facilities remain under FDA import alerts. The factories are still banned, but in July, Wockhardt announced that it would no longer make generics for the U.S. market—essentially admitting defeat in the world's largest pharmaceutical market.

Yet there have been glimmers of hope. COVID-19 contract: Signed with UK Government to fill-finish Oxford–AstraZeneca vaccine at Wrexham facility, extended until August 2022. This wasn't a huge business, but it showed that at least one developed market government still trusted Wockhardt with critical manufacturing.

The real hope lies in Zaynich. India launch strategy for Zaynich: DCGI asked for trial on 60 patients resistant to Meropenem, trial expected to complete in 6-8 months, launch likely by end of 2024-25. The global Phase 3 study for WCK 5222 involves 70 centres worldwide in 11 countries including US, Europe, India, China and Latin America, with recruitment of around 415 patients (of 535 total) already done.

The challenge of rebuilding trust with regulators remains monumental. Seven warning letters across multiple continents suggest systemic cultural issues that go beyond individual plant problems. The FDA's frustration is palpable: "These repeated failures at multiple sites demonstrate your company's inadequate oversight and control over the manufacture of drugs."

The financial metrics reflect this regulatory purgatory. The share of the firm's US business in total sales dropped to 22 per cent in FY16 from previous highs of over 40%. Without access to the US market, Wockhardt is essentially a domestic Indian player with some emerging market presence—a far cry from the global ambitions that drove the acquisition spree.

Management has tried various strategies. They've hired consultants, implemented remediation programs, and promised comprehensive overhauls. But the fundamental problem persists: how do you change a culture that saw quality violations as acceptable shortcuts? How do you convince regulators who've been lied to repeatedly that this time is different?

The company's strategy now seems to be a bifurcation: abandon the generic dreams that led to disaster, focus on the antibiotic research that could provide redemption. It's a high-risk pivot—betting everything on drugs that might never generate blockbuster revenues even if successful.

The irony is striking: Wockhardt might save more lives with its antibiotics than it ever could have with generics, but the financial rewards may never match the ambitions that nearly destroyed the company. It's a morality tale where doing good might not mean doing well, at least not in the way markets typically measure success.

VIII. Playbook: Business & Investing Lessons

The Wockhardt saga offers a masterclass in how ambitious companies from emerging markets can spectacularly self-destruct—and potentially resurrect themselves. Each mistake and each pivot contains lessons worth billions in avoided losses.

The Perils of Debt-Fueled International Expansion

Wockhardt's acquisition spree teaches us that buying your way to global relevance is like trying to buy friends—expensive and usually unsuccessful. The company spent roughly $2 billion acquiring facilities across three continents, funded almost entirely by debt. The math never worked: you're buying high-cost operations in developed markets, funding them with emerging market revenues, and hoping somehow to create synergies that overcome both the debt service and the operational complexity.

The real lesson isn't "don't acquire"—it's that acquisitions without operational excellence are just expensive liabilities. Wockhardt bought facilities but couldn't integrate cultures. They acquired registrations but couldn't maintain standards. They purchased market access but destroyed it through quality failures.

Quality Systems as Existential Risk in Pharma

In pharma, quality isn't a department—it's the entire business. Wockhardt's violations weren't minor paperwork issues. They were fundamental failures of integrity: torn batch records in trash, deleted test data, lying to inspectors. Once you've been caught destroying evidence, no amount of remediation can quickly restore trust.

The deeper lesson is about organizational culture. The jugaad mentality—finding creative workarounds—that helps navigate Indian bureaucracy becomes criminal when applied to FDA regulations. What's celebrated as entrepreneurial flexibility in one context becomes fraud in another.

The False Economy of Cutting Corners in Regulated Industries

Wockhardt saved perhaps millions by manipulating test results and hiding failures. They've now lost billions in market value and revenues. The asymmetry is stark: every shortcut in a regulated industry carries potentially company-ending downside risk.

This extends beyond compliance to investment. Wockhardt underinvested in quality systems while overspending on acquisitions. They prioritized growth over governance. In regulated industries, this sequencing is always fatal—you must build the foundation before the edifice.

Family Business Succession Challenges in Crisis

The transition from Habil to his sons Murtaza and Huzaifa during the CDR crisis illustrates a universal challenge: how do you hand over leadership when the ship is sinking? The sons inherited not just a company but its accumulated sins. They had to manage crisis while establishing credibility, reform culture while maintaining operations.

The lesson for family businesses: succession planning must include scenario planning for crisis. The next generation needs to be prepared not just for growth but for disaster recovery. And sometimes, as Wockhardt shows, the founder's vision can become a liability that the next generation must overcome.

The Strategic Value of Genuine R&D in Emerging Markets

While Wockhardt was destroying value in manufacturing, it was creating potential value in R&D. The antibiotic program, maintained through financial crisis and regulatory disaster, might ultimately save the company. This teaches us that genuine innovation—not just copying or incremental improvement—can provide redemption even for the most troubled companies.

The broader lesson for emerging market companies: you can't cost-cut your way to global relevance. At some point, you must create something the world needs that nobody else can provide. For Wockhardt, that's antibiotics everyone else abandoned.

Regulatory Arbitrage and Its Limits

Wockhardt initially thrived by arbitraging between Indian costs and global prices. They could make drugs cheaper in India and sell them at developed market prices. But regulatory arbitrage—trying to apply emerging market quality standards while selling to developed markets—doesn't work. The FDA doesn't grade on a curve.

This applies beyond pharma. Any business model based on regulatory arbitrage eventually faces a reckoning. Standards converge upward, not downward. Companies must plan for the highest global standard, not the local minimum.

Why Antibiotics Are a Terrible Business (But Critical for Humanity)

Wockhardt's antibiotic focus illustrates a profound market failure. These drugs save lives but destroy economics: you cure patients quickly (destroying recurring revenue), governments want them held in reserve (limiting volume), and resistance eventually develops (ensuring obsolescence). No rational profit-maximizing company should develop antibiotics.

Yet Wockhardt is betting everything on them. This teaches us about the potential for contrarian value creation. Sometimes the worst businesses economically can become the most valuable strategically—if you can survive long enough for the world to recognize their importance and adjust compensation accordingly.

The Importance of Corporate Culture in Highly Regulated Industries

Culture eats strategy for breakfast, but in regulated industries, culture can eat your entire company for lunch. Wockhardt's culture of shortcuts and workarounds, probably adaptive in domestic markets, proved catastrophic under FDA scrutiny. You can't have different cultures for different markets—eventually, the lowest standard contaminates everything.

The lesson extends beyond compliance to innovation. The same culture that led to quality failures has, paradoxically, enabled antibiotic breakthroughs. This suggests cultures aren't simply good or bad—they must align with strategic objectives. Wockhardt needed a culture of meticulous process for generics but creative risk-taking for drug discovery. Managing this duality might have been impossible.

IX. Analysis & Bear vs. Bull Case

Bear Case: The Skeptic's View

The bear case for Wockhardt writes itself in red ink and warning letters. Low interest coverage ratio, return on equity of -6.95% over last 3 years—these aren't metrics of a struggling company, they're vital signs of a corporate coma. The company hasn't generated meaningful returns for shareholders in over a decade.

Seven FDA warning letters suggest systemic cultural issues that may be unfixable. This isn't one bad apple or one problematic plant—it's a pattern across continents and decades. The fact that violations persist despite repeated promises of reform suggests either incompetence or unwillingness to change. Neither is investable.

The antibiotic market economics remain challenging despite Wockhardt's scientific success. Even if Zaynich succeeds clinically, it faces the fundamental problem of all antibiotics: governments want them available but unused, like nuclear weapons for bacteria. The $25 billion addressable market sounds impressive until you realize it's spread across decades and geographies, with most sales coming only when resistance makes current drugs obsolete.

Competition from Chinese and other Indian pharma companies continues to intensify. While Wockhardt was dealing with regulatory issues, competitors like Sun Pharma, Dr. Reddy's, and Cipla have built global businesses with better reputations. In the commodity generic business, trust is everything—and Wockhardt has none.

The trust deficit with global regulators may be permanent. Once you've been caught destroying evidence and lying to investigators, every future interaction carries that baggage. FDA inspectors will forever approach Wockhardt facilities with heightened scrutiny. This creates a permanent cost disadvantage—more documentation, more oversight, more time.

Management's track record suggests persistent governance issues. The same leadership that oversaw the quality disasters remains in place. The board that approved debt-funded acquisitions still governs. Without fundamental leadership change, why expect different outcomes?

Bull Case: The Believer's Thesis

The bull case rests on one extraordinary fact: CLSI granted WCK 5222 susceptibility breakpoint of 64 mg/litre vs 4-8 mg/litre for recent antibiotics. This technical detail hides a profound reality—Wockhardt has created an antibiotic that works where everything else fails.

100% success rate in 30 compassionate use patients, safe even after 70 days use in critical patients—these aren't incremental improvements, they're paradigm shifts. Every one of those patients would likely be dead without Zaynich. As antimicrobial resistance accelerates, the value of such drugs approaches infinity for those who need them.

Only company where USFDA has given QIDP Status for 5 Anti-bacterial discovery programmes. Think about the irony—the FDA that banned Wockhardt's manufacturing has simultaneously designated five of their discoveries as breakthrough therapies. This suggests the quality issues were about culture and process in manufacturing, not scientific capability.

Market position remains strong in certain segments: Among top 3 Indian generic companies in UK, No. 1 Methycobalamin brand in India. Despite everything, Wockhardt still has valuable commercial assets and market positions. These provide cash flow to fund the antibiotic development.

The potential for massive value creation if even one antibiotic succeeds globally is enormous. Antibiotic developers that succeed can command premium pricing and government support. Gilead's experience with remdesivir during COVID shows how quickly a drug addressing urgent public health needs can generate billions in revenue.

The licensing strategy for Zaynich de-risks commercialization. By partnering with global pharma companies for developed markets, Wockhardt can capture value without rebuilding its damaged commercial infrastructure. A successful licensing deal could bring upfront payments, milestones, and royalties without the execution risk.

Valuation reflects none of the pipeline potential. At ₹24,645 Cr market cap, the market is essentially valuing Wockhardt as a failed generic company. Any success with the antibiotic pipeline represents pure upside not reflected in current pricing.

The Verdict: A Speculation, Not an Investment

Wockhardt isn't an investment—it's a bet on whether scientific brilliance can overcome operational incompetence. It's a wager that humanity's need for new antibiotics will eventually override the market's memory of quality failures.

For fundamental investors, the bear case dominates. The company fails every traditional metric of quality, growth, and governance. The regulatory overhang may never fully clear. Management hasn't demonstrated the capability to run a global pharmaceutical company responsibly.

But for those willing to speculate on asymmetric outcomes, Wockhardt offers a fascinating proposition. If Zaynich succeeds and reaches even a fraction of its potential market, the equity could multibag from current levels. If the company can license its pipeline successfully, it could transform from a manufacturing company with a trust deficit to a research company with breakthrough drugs.

The critical question isn't whether Wockhardt's drugs work—the science seems solid. It's whether the company can exist long enough for the drugs to matter, and whether management can capture value even if the drugs succeed. History suggests skepticism, but the pipeline argues for possibility.

X. Epilogue & "What Would We Do?"

The Fundamental Question: Can You Change a Company's DNA?

Standing at the crossroads of Wockhardt's potential futures, we face a question that transcends this single company: Can corporate DNA—the deep cultural coding that determines how an organization responds to challenges—truly change? Or are some companies forever prisoners of their foundational sins?

Wockhardt's DNA was written in the 1970s Aurangabad facility, where Habil Khorakiwala built a culture of ambitious improvisation. That same DNA that enabled rapid growth also contained the code for its destruction. The jugaad gene that helped navigate License Raj became malignant under FDA scrutiny.

If we were running Wockhardt, the first decision would be whether transformation is even possible. Not all companies can be saved, and sometimes the greatest value creation comes from accepting reality rather than fighting it.

Strategic Options: Double Down on R&D

The boldest path would be to fully embrace what Wockhardt accidentally became good at: antibiotic discovery. Shut down or sell all generic manufacturing. Take the FDA bans as liberation from a business where trust matters more than capability. Become a pure-play antibiotic research company.

This would mean restructuring the entire company around the 140 scientists who've been developing antibiotics. Move headquarters to wherever the science is best—maybe Cambridge or San Francisco. Rebrand completely. Make the regulatory disasters ancient history by becoming a different company entirely.

The economics could work through aggressive partnering. License everything early and often. Take upfront payments over long-term value capture. Better to own 20% of something successful than 100% of continued failure.

Find a Strategic Buyer

The pragmatic path would be acknowledging that Wockhardt's assets are worth more to others than to Wockhardt itself. The antibiotic pipeline would be incredibly valuable to a Big Pharma company with the commercial infrastructure and regulatory credibility to maximize its potential.

A company like Pfizer, Merck, or GSK could pay multiples of Wockhardt's current market cap just for the pipeline. They have the relationships with governments, the experience with antibiotic commercialization, and critically, the trust with regulators that Wockhardt will never rebuild.

The Indian operations and brands could be sold separately to domestic players. The UK facilities might interest European generics companies. Break the company into pieces that make sense to different buyers rather than trying to hold together an incoherent whole.

Split the Company

The middle path would be formal separation of the research and manufacturing businesses. Create Wockhardt Discovery (or better, a completely new name) as a separately listed entity holding all antibiotic research assets. Leave the generic business and its regulatory baggage in the legacy entity.

This would allow markets to value the pipeline appropriately without the overhang of manufacturing issues. It would also enable different governance structures, compensation models, and cultures for fundamentally different businesses.

The research company could attract different investors—those interested in biotech-like returns rather than generic pharmaceutical margins. The manufacturing company could focus on remediation and domestic markets where the FDA issues matter less.

The Role of Emerging Market Pharma in Global Health

Wockhardt's story forces us to confront uncomfortable truths about global pharmaceutical supply chains. We depend on emerging market manufacturers for affordable medicines, yet we're shocked when they don't meet developed market standards. We want Indian and Chinese companies to supply cheap generics but also maintain Swiss quality standards.

The real lesson might be that the current model is unsustainable. Either standards must converge globally (raising costs), or we must accept tiered quality systems (raising risks). Wockhardt tried to straddle both worlds and failed spectacularly.

Going forward, emerging market pharma companies face a choice: be excellent at low-cost manufacturing for local markets, or invest to meet global standards consistently. The middle ground—where you mostly meet standards but occasionally destroy evidence of failures—isn't viable.

Lessons for Other Indian Companies Going Global

Every Indian company with global ambitions should study Wockhardt's warning letters. They're not just about pharmaceutical manufacturing—they're about what happens when emerging market business practices meet developed market regulatory expectations.

The first lesson: compliance isn't optional or negotiable. You can't charm FDA investigators like you might Indian bureaucrats. You can't fix problems with relationships when everything is documented.

Second: debt-funded international expansion is almost always a mistake. Acquisitions require not just capital but operational excellence to integrate. If you can't run facilities better than their previous owners, you're just buying expensive problems.

Third: culture must evolve before strategy. You can't have emerging market culture and developed market ambitions. The transformation must be complete and genuine, not cosmetic.

The Societal Importance of Antibiotic Development

Whatever happens to Wockhardt as a company, its antibiotic program represents something larger: the critical importance of incentivizing development of drugs we hope never to use. The market has failed to provide adequate returns for antibiotic development, leading most rational actors to abandon the field.

Wockhardt's quixotic pursuit of new antibiotics, maintained through financial crisis and regulatory disaster, demonstrates that sometimes irrational behavior serves social good. But depending on irrational actors isn't a sustainable model for addressing existential threats.

Governments and health systems need to restructure incentives for antibiotic development. Whether through advanced purchase commitments, patent buyouts, or subscription models, we must make antibiotic development economically rational. Otherwise, we're depending on companies like Wockhardt—damaged, desperate, and possibly delusional—to save us from the next superbug.

Final Thoughts on Redemption Arcs in Business

Wockhardt poses a fundamental question about redemption in business: Can a company that has betrayed trust ever truly recover? The romantic in us wants to believe in second chances, in phoenix-like rises from ashes. The realist knows that trust, once broken, leaves permanent scars.

Perhaps the answer is that redemption requires death and rebirth rather than simple recovery. Wockhardt the generic manufacturer who lied to the FDA can never be trusted again. But Wockhardt the antibiotic developer who might save humanity? That's a different story worth considering.

The ultimate irony would be if Wockhardt, banned from selling common generics, ends up developing the drug that prevents the antibiotic apocalypse. It would be a redemption arc worthy of mythology—the sinner becoming the saint, the villain becoming the hero.

But even if that happens, it won't erase the lessons of Wockhardt's fall. Quality matters. Culture matters. Trust, once broken, may never fully return. These aren't just business lessons but moral ones. In the end, Wockhardt's story is about the price of shortcuts in a world that demands excellence—and the possibility, however slim, of redemption through genuine innovation.

The choice for investors isn't just about financial returns but about what kind of stories we want to fund. Do we believe in redemption? Do we value antibiotic development despite its poor economics? Do we bet on science overcoming scandal?

These aren't questions with clear answers. They're the kinds of ambiguities that make markets—and make Wockhardt either an uninvestable disaster or the opportunity of a decade. Time, and superbugs, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube