Winsol Engineers Ltd.: Powering the Green Tsunami

I. Introduction & Episode Roadmap

Picture the Kutch desert at dawn. The salt flats stretch to a flat horizon, and against the pale sky a row of wind turbines turns with the slow, deliberate patience of something enormous. Each of those machines is a marvel of German and Chinese and Indian engineering — a 300-ton nacelle perched atop an 80-meter tower, blades longer than a Boeing's wingspan carving arcs through the Gujarat wind. This is the image the world has of the energy transition: clean, high-tech, almost serene.

But zoom in on the base of that turbine, and the romance evaporates. There is a crater filled with reinforced concrete, poured to withstand the aerodynamic shear of a blade catching a gust. There is a rough access road that had to be cut across farmland so a 250-foot blade on a specialized trailer could reach the site without decapitating a power line. There is a substation humming a few kilometers away, and miles of extra-high-voltage cable trenched under dry soil, and a small army of people who spent months negotiating with farmers over crop compensation and right-of-way. None of it is glamorous. All of it is essential. Without it, that beautiful turbine is a very expensive metal sculpture.

The industry has a bloodless name for all of this unglamorous essential work: Balance of Plant, or BoP — everything at a power plant that isn't the turbine or the solar panel itself. It is the plumbing and the wiring and the concrete and the paperwork of the green revolution. And it is a genuine bottleneck. India can manufacture or import all the turbines and panels it wants, but if it cannot anchor them, wire them, and connect them to the grid fast enough, the gigawatts stay on paper.

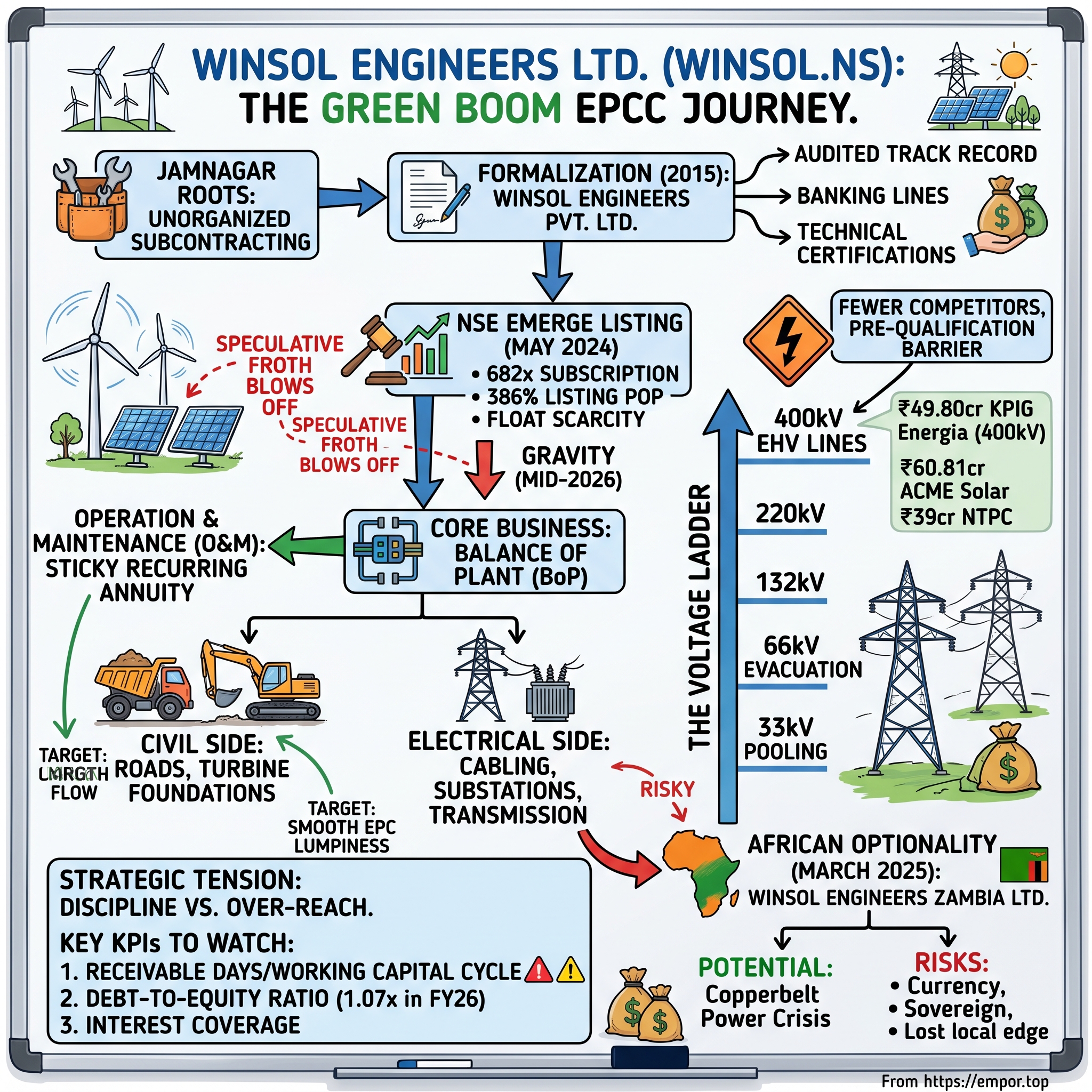

Enter our protagonist: Winsol Engineers Ltd. (WINSOL.NS), a micro-cap engineering, procurement, construction, and commissioning — EPCC — contractor out of Jamnagar, Gujarat. Winsol is not a household name. It does not make turbines. It does not own power plants. It does the digging, the pouring, the cabling, and the substation-building for green energy giants — Suzlon, Adani Green, CleanMax, Envision Energy, and a growing roster of independent power producers.1 It is, in the truest sense, a picks-and-shovels business in a gold rush.

For two years Winsol has also been a small drama in India's capital markets. In May 2024 it went public on the NSE Emerge SME platform, seeking a modest ₹23.36 crore. The offer was subscribed 682 times over, and the stock listed at ₹365 against a ₹75 issue price — a 386% opening premium — before the speculative froth blew off and the shares drifted down to around ₹119 by mid-2026, valuing the whole company at roughly ₹137 crore.[^2][^3]9 That arc — euphoria to gravity — is itself a lesson in what SME listings do to fundamentals.

Here is where we're going. First, what BoP actually is and how money is made in it. Then the Pindariya family's three-decade climb from Jamnagar sub-contracting to a listed company. The anatomy of that May 2024 listing mania and its hangover. A war-game against the sector's giant, KP Energy. A financial stress test — rising debt, the working-capital trap, and the leap from 66kV substations to 400kV transmission. And finally, the African wildcard: a small subsidiary in Lusaka, Zambia, that is either real optionality or a classic small-cap distraction. Let's start where the value chain starts.

II. What is "Balance of Plant" (BoP) & Why Does it Control the Green Grid?

To understand why a company like Winsol exists, you have to understand who doesn't want to do its job. Consider Adani Green or CleanMax, developers who own renewable plants and sell the electricity. Their expertise is capital — raising billions, winning power-purchase auctions, managing a portfolio of assets that throw off decades of cash. Now consider Suzlon or Envision, the OEMs who design and build the turbines themselves. Their expertise is machinery — aerodynamics, gearboxes, blade metallurgy. Neither of these players wants to spend its scarce management attention arguing with a farmer in interior Gujarat about whether a transmission tower can cross his groundnut field.

That gap — between the people with the capital and the people with the machines — is where the BoP contractor lives. Winsol is the boots-on-the-ground execution partner who does everything the developers and OEMs would rather outsource. And "everything" is a genuinely wide brief.

The civil side is brute-force engineering. A wind turbine foundation is not a slab; it is a precisely engineered mass of concrete and rebar, designed to transfer the twisting, oscillating load of a spinning rotor into bedrock without cracking over a 25-year life. Get the mix or the curing wrong and you don't find out for years — and then you find out catastrophically. Around that foundation come the access roads, graded and reinforced to carry trailers hauling blades the length of a football field across terrain that was, until recently, scrubland or farm.

The electrical side is where the real technical differentiation lives, and it's worth slowing down on because it's the heart of Winsol's growth story. Power comes off a wind or solar array at a relatively modest voltage. Inside the plant, "pooling" cables — typically around 33kV — gather the output and funnel it to a substation. That substation is the plant's beating heart: transformers that step the voltage up, and switchgear (increasingly gas-insulated for compactness and reliability) that controls and protects the flow. From there, extra-high-voltage transmission lines carry the power out to the grid. And here is the ladder that matters for Winsol's economics: those evacuation lines run at 66kV, then 132kV, then 220kV, and — at the top of the ladder — 400kV. Each rung up is exponentially harder. Higher voltage means bigger clearances, more sophisticated protection, tighter tolerances, and far fewer contractors qualified to touch it. A 400kV line is a different animal from a 66kV line the way a commercial airliner is a different animal from a Cessna.

Here's a useful analogy for why the voltage ladder matters so much. Think of electricity moving through a wire like water moving through a pipe. Push the same amount of power through at low voltage and you need enormous current — a fat pipe, heavy losses, heat bleeding away as waste along every kilometer. Raise the voltage and you can push the same power through with far less current, which means thinner conductors and dramatically lower losses over long distances. That's why every power system on Earth steps voltage up to travel and down to be used. But high voltage is unforgiving. At 400kV, electricity will happily jump through open air to find ground; the engineering is a constant negotiation with a force that wants to escape. Clearances get bigger, insulation gets more exotic, protection systems get faster, and the consequences of an error escalate from "expensive" to "lethal." Which is exactly why the list of contractors who can credibly do it is short — and why climbing that ladder is the most important strategic question in Winsol's business.

The third piece has no engineering at all, and it's the one that kills projects: Right of Way (RoW). A transmission line has to physically cross land that other people own — farms, village commons, the odd municipal boundary. Each crossing requires permissions, crop compensation, and the patience to sit with local landowners and administrators until they say yes. In India, RoW is the single most common reason renewable projects slip their deadlines. A contractor who is genuinely good at the human, bureaucratic, feet-in-the-mud work of clearing RoW has something a spreadsheet can't easily replicate.

It's worth dwelling on RoW, because outsiders consistently underestimate it and insiders never do. A transmission line is a linear asset — it must cross every parcel between the plant and the grid, and a single holdout in the middle can stall the entire route. You cannot go around a farmer the way you can route software around a bug. The negotiation is intensely local: what the standing crop is worth, whether a tower footing takes land out of cultivation permanently, whether the village panchayat is amenable, whether a neighboring landowner will now demand the same terms. It is slow, relational work conducted in the local language by people who will still be in that district next year. Multinational engineering firms are structurally bad at it. A Jamnagar contractor whose founder has spent thirty years in those districts is structurally good at it. That asymmetry — not concrete, not cable — is the most defensible thing about a company like Winsol.

Now, the economics. Winsol's revenue splits into two very different businesses. The EPCC core drives well over 90% of the top line: lump-sum turnkey projects where the contractor bids a fixed price to design and build the whole balance of plant.9 This is high-volume, capital- and working-capital-intensive work, fought over in competitive tenders. Win the bid and you eat cost overruns; lose it and you starve. The margins are decent but the model is hungry for cash.

Consider how a single EPCC project actually breathes, because the rhythm explains almost everything about the financial statements later. It begins with a tender, where the contractor must first pre-qualify — demonstrating past projects of comparable size and voltage, technical certifications, and enough balance-sheet strength that the client believes you can finish what you start. Pre-qualification is a gate, and it's a gate that gets narrower as voltage rises. Clear it, and you bid a fixed price against rivals doing the same. Win, and you post a bank guarantee — a promise from your bank, backed by your credit lines, that the client can call if you fail. Then you mobilize: crews, equipment, and, critically, procurement. You buy the steel, the conductor, the transformers, the switchgear — often the majority of the contract value — and you buy it now, months before you'll be paid for it. You build. You hit milestones, and against each milestone you raise an invoice. Then you wait: thirty days, sixty, ninety, sometimes far longer, while a very large client's accounts department processes a very small vendor's bill. Finally, at handover, a retention amount — a slice of the contract held back as a warranty against defects — stays with the client for a year or more before it comes home.

Read that sequence again and you can see the trap already forming. Cash goes out at the beginning and comes back at the end, and the gap in between has to be funded by somebody. That somebody is the contractor. This is the structural, unavoidable physics of the EPCC business model, and it is why a fast-growing contractor can be simultaneously profitable and starved of cash. Growth isn't free here; it is pre-paid.

The second business is smaller but strategically far more interesting: Operation & Maintenance (O&M), which contributes on the order of 10% of revenue. Once a plant is built, someone has to keep it running — 24/7 monitoring, SCADA management, preventative electrical maintenance, substation upkeep. Unlike EPC, O&M is not a one-shot bid; it's a recurring, sticky, high-margin annuity. The June 2026 CleanMax contract is a small but telling example — roughly ₹3.60 crore to operate and maintain a solar plant at Kalavad, including deploying security personnel, running for the life of the agreement rather than the length of a build.6 Every substation Winsol constructs is a potential O&M annuity in waiting. If there is a strategic jewel buried in this business, it is the slow accumulation of that recurring maintenance book — the thing that could one day smooth out the lumpy, cash-hungry EPC cycle. Whether Winsol actually converts its build pipeline into a durable O&M portfolio, rather than handing that annuity to someone else, is one of the real questions we'll keep returning to.

Why does O&M matter so disproportionately for so little revenue? Because the two businesses have opposite financial personalities. EPC is a series of one-time transactions: you win a bid, build the thing, get paid once (eventually), and then you have to go win the next bid all over again, from zero, against the same hungry competitors. It is a treadmill. O&M is the opposite — a multi-year contract that renews, that requires little working capital, that the customer is loath to switch because the incumbent already knows every quirk of the plant, and that throws off predictable cash rather than consuming it. In valuation terms, a rupee of recurring O&M profit is worth far more than a rupee of one-shot EPC profit, because it is stickier, less capital-hungry, and more visible. Companies that build things and then walk away are perpetually re-earning their revenue; companies that build things and then keep the maintenance contract are compounding. The strategic prize for Winsol is not the next big EPC order — those will come as long as the macro holds. The prize is quietly converting a decade of substation builds into a maintenance book large enough to change the character of the whole company. Right now, at roughly a tenth of revenue, that book is a promising seed, not a tree.

That's the machine. Now let's meet the family that built it.

III. Jamnagar Roots: The Promoter Journey and Hyper-Localization

If you want to understand Winsol, you first have to understand Jamnagar. This is not a sleepy provincial town. It sits in the industrial heartland of Gujarat, in the shadow of the largest oil-refining complex on Earth — Reliance's Jamnagar refinery — surrounded by a dense ecosystem of brass casting, shipbreaking, and metal fabrication. It is a place where heavy industry is in the water, where a generation of tradesmen and small contractors grew up around pipes, steel, transformers, and the practical problem of moving big things and connecting them to power. It is exactly the kind of soil from which a company like Winsol grows.

The founder is Ramesh Jivabhai Pindariya, Winsol's Chairman and Managing Director. His is not a business-school story. Ramesh spent more than three decades as an on-the-ground contractor, and the knowledge he accumulated is the kind you cannot download: which patch of Gujarat soil will fight a foundation, how the state grid utility GETCO actually processes an interconnection, which village will hold up a right-of-way and how to bring it around. That tacit, hyper-local knowledge — geology, grid bureaucracy, and land administration braided together — is the real founding asset of the company. Everything Winsol sells is, at bottom, a monetization of Ramesh Pindariya's decades of showing up on site.

There's an important point buried in that biography about what kind of asset this is. Most of the moats investors admire are legible: a patent, a brand, a network. Ramesh Pindariya's asset is the opposite — it is almost entirely illegible, existing as relationships and pattern-recognition in the heads of a small group of people who have worked the same districts for thirty years. That illegibility is a double-edged thing. On one hand it is genuinely hard to copy; a well-funded competitor from Mumbai cannot simply buy three decades of standing in Jamnagar's villages and grid offices. On the other hand, it doesn't scale and it doesn't transfer. It is the kind of advantage that works brilliantly inside a hundred-kilometer radius and evaporates the moment you cross a state line — a constraint that becomes very relevant later when we get to Rajasthan-scale ambitions and a subsidiary in Zambia.

The formalization came in 2015, when the family incorporated Winsol Engineers Private Limited and began the deliberate transition from unorganized sub-contracting toward formal corporate bidding.10 This is a more consequential move than it sounds. In the unorganized world, you are a sub-sub-contractor, taking scraps of work off larger players, invisible on paper, unable to bid directly for the big tenders because you lack the balance sheet and the compliance history to pre-qualify. Incorporating was the first step on a decade-long climb toward being able to sit across the table from a Suzlon or an Adani as a named counterparty.

Think about what that climb actually required, because it's the least told and most impressive part of the Winsol story. To go from unorganized sub-contractor to prime EPCC vendor, a firm has to build three things it doesn't start with. It needs an audited track record — a paper history of completed projects that a procurement department can verify, which means years of doing work under your own name before anyone will trust you with the big jobs. It needs banking relationships deep enough to issue bank guarantees, because without guarantees you cannot even enter a serious tender; the bank effectively becomes your co-signer on every promise. And it needs technical certifications and qualified engineers on the payroll, the credentials that let you touch higher-voltage assets at all. Each of these takes years, and each is a chicken-and-egg problem: you need the track record to get the work, and the work to get the track record. The decade between 2015 and the listing was, in essence, Winsol grinding through that bootstrap — building the paper history and the banking lines that would eventually let it bid for a 400kV line rather than sub-contract on someone else's.

The Pindariyas run this as a family enterprise, and they own it like one. After the IPO, the promoter group — Ramesh, along with Amri, Kishor, Kashmira, and Kashish Pindariya — retained 73.73% of the equity, and none of it is pledged.910 The treasury is managed by the CFO, Kishor Jivabhai Pindariya, Ramesh's brother. There is genuine skin in the game here; a family that has bet three-quarters of its net worth on the company, unencumbered by pledge loans, is aligned with outside shareholders in the most literal way.

But the same fact that reads as alignment reads, from a governance seat, as concentration. This is a family-dominated board in an SME environment, where the checks that constrain a large-cap — independent directors with real standing, seasoned audit oversight, institutional shareholders who can vote — are thin. High promoter ownership can align interests; it can also mean related-party dynamics and board decisions that never meet serious independent challenge. The honest read is that the transition to a public company is forcing a degree of professionalization that a private family firm would never have adopted on its own — the discipline of quarterly disclosure, the addition of independent directors, the scrutiny of a listed audit trail.11 Whether that professionalization is substantive or cosmetic is exactly the kind of thing a careful investor watches over several years, not one AGM. For now, the story is a family firm learning, in public and in real time, how to behave like a corporation. And the moment it was forced to grow up fastest was the day it listed.

IV. The May 2024 SME Frenzy: Anatomy of a 682x Oversubscription

To appreciate what happened to Winsol's stock, you have to remember what the NSE Emerge platform had become by 2024. India's SME exchanges — designed as a modest on-ramp for small companies to raise capital — had turned into something closer to a casino. Retail liquidity was sloshing through the system in unprecedented volumes, and small IPOs were being bid to absurd multiples on the strength of little more than a compelling one-line story and the near-certainty of a listing-day pop. Grey-market premiums were the real prospectus. In that environment, a profitable little green-energy contractor with a good narrative was catnip.

It's worth understanding why the SME platform produces this behavior, because the mechanics are not an accident. SME IPOs are small by design, which means the free float — the number of shares actually available to trade after promoters keep their stake — is tiny. Winsol's promoters retained nearly three-quarters of the company, leaving roughly a quarter in public hands, and a quarter of a small company is a very small pool of stock. Meanwhile, lot sizes on SME issues are large, which was meant to keep unsophisticated retail investors out but in practice simply concentrated the bidding among people willing to write big cheques for a lottery ticket. Layer on the grey market — an informal, unregulated market where IPO shares trade before listing, generating a "GMP" that functions as a self-fulfilling prophecy about the listing pop — and you have a machine that reliably converts a modest fundraise into a speculative frenzy. Tiny float plus enormous demand plus a widely advertised expected pop equals a listing price that has essentially nothing to do with discounted cash flows.

Winsol came to market with a deliberately small fresh issue — 3,115,200 shares at a price band of ₹71 to ₹75, raising just ₹23.36 crore.2 For a company doing real revenue, that is a tiny raise; the scarcity was almost engineered. And the market responded to scarcity the way markets always do.

The subscription numbers, when the book closed on May 9, 2024, were staggering. The retail portion was subscribed 780 times. The non-institutional (HNI/NII) segment went to 1,087 times. Even the institutional tranche, ordinarily the sober end of the room, was bid 207 times. The whole issue was covered 682.14 times over, meaning the demand book ran to well over ₹11,000 crore chasing an issue worth ₹23 crore.[^2] Read that ratio again. Investors collectively offered to hand this company roughly five hundred times the money it was actually asking for.

The listing, on May 14, 2024, was the inevitable release valve. The stock opened at ₹365 — a 386.67% premium to the ₹75 issue price — and promptly hit its upper circuit.[^3] Anyone who received an allotment and sold at the open made nearly 5x their money in a matter of days. It was a spectacular payday for the lucky few who got shares in a 682x-subscribed lottery, and a textbook illustration of how SME scarcity plus retail mania manufactures a price with no relationship to underlying value.

Pause on what this meant for the company itself, as opposed to the traders. Winsol got exactly ₹23.36 crore — the amount it asked for. It did not get ₹11,000 crore; that money was never on offer to the business, only to the auction. In fact, the company arguably left value on the table: had it known demand was that deep, it could have raised multiples more at a far higher price and funded years of working capital without touching the debt markets. Instead, the entire surplus between the ₹75 issue price and the ₹365 opening print — an enormous transfer — went to whoever got an allotment and sold. The company was the one entity in this drama that captured almost none of the frenzy it created. That is worth remembering the next time you read about a blockbuster listing: the pop is not the company's money.

Then gravity did its work. There is no polite way to say it: a stock cannot open at nearly 5x its issue price on speculative flow and stay there once the flippers have flipped and the story has to be carried by earnings. By mid-2026 the shares had rationalized to around ₹119, a market cap near ₹137 crore, trading at roughly 9.5x trailing earnings.9 Notice what happened underneath: over those same two years, the company's actual profits grew — and yet the stock fell by two-thirds from its listing high. The earnings caught up while the price came down to meet them. That is the whole SME cycle in miniature, and it is the cruelest lesson a first-time IPO investor learns: buying a great macro story at 40x hype and watching it de-rate to 10x reality can lose you money even as the business does everything right. The froth was never Winsol's fault, and it was never Winsol's benefit either — it was the market's. What matters now is whether the business underneath is worth the ₹137 crore the market currently assigns it. To judge that, you need a yardstick.

V. Competitive Benchmarking: Winsol vs. KP Energy (KPEL)

Winsol does not operate in a vacuum, and the most instructive way to size it up is to stand it next to the giant of its own backyard. Gujarat's wind-BoP world has one dominant listed player, and it is KP Energy (KPEL), part of the sprawling KP Group. Putting the two side by side is like putting a nimble specialist trawler next to a factory ship — they fish the same waters, but they are not the same kind of vessel at all.

Start with sheer scale, because it's jarring. In FY26, KP Energy posted consolidated revenue of about ₹1,497 crore with net profit north of ₹181 crore and EBITDA of roughly ₹328 crore.5 Winsol, the same year, did ₹136.57 crore of revenue and ₹14.39 crore of profit.1 KP Energy is, in round numbers, more than ten times Winsol's size. Any narrative that positions Winsol as a peer of KP Energy is simply wrong; Winsol is a fraction of one segment of what KP Energy does.

The more important difference is in the business model, not the size. KP Energy behaves as an end-to-end master developer. It buys land, develops wind infrastructure, acts as an independent power producer owning generating assets, and sits on a multi-gigawatt order pipeline. That means KP Energy carries a heavy, asset-owning balance sheet — capital-intensive, but also capturing the full value stack from land to electrons. Winsol, by contrast, runs a deliberately lighter, purely service-oriented EPCC model. It owns almost no generating assets. It mobilizes, builds, hands over, and — increasingly — maintains. It is a sub-EPC partner, not a master developer.

This distinction has a consequence that flatters Winsol, and it's only fair to note it. Owning assets means deploying enormous capital, and enormous capital deployed at ordinary returns produces ordinary returns on capital. Winsol's asset-light service model, by contrast, generates a return on equity around 25% and a return on capital employed near 24.5% — genuinely strong numbers that reflect a business turning modest capital quickly rather than parking huge capital slowly.9 The trade-off is ceiling versus efficiency: KP Energy captures the whole value stack and can grow into a multi-thousand-crore enterprise, while Winsol captures one thin slice but earns a high return on the little capital that slice requires. Neither model is superior in the abstract. They're different bets on where the durable profit in renewables actually sits.

Nor is KP Energy the only competitor that matters — and the more dangerous rivals may be the ones that don't show up in a stock screener. Winsol is squeezed from two directions. From above, national infrastructure heavyweights like L&T and KEC International can descend into any state and out-procure, out-finance, and out-pre-qualify a Jamnagar micro-cap on the largest projects. From below sits a long tail of unlisted, fragmented local civil contractors with almost no overhead, willing to bid a 33kV cabling job at margins that would starve a listed company with compliance costs and a public audit. Winsol occupies the middle: too small to fight the nationals for mega-projects, too formal to win a race to the bottom against the informal sector. Middles can be profitable places — but only if you're climbing out of them, which is precisely what the voltage-ladder strategy is for.

So how does a company one-tenth the size actually win work in a market with a giant in it? The honest answer is that Winsol wins where the giants would rather not bother. Its edge is being a localized, fast-mobilizing sub-contractor for OEMs and developers who need reliable execution in the Jamnagar-Kutch corridor without personally wrangling local landowners, GETCO paperwork, and the daily grind of a construction site. When Suzlon or Envision needs a substation and evacuation line built in interior Gujarat, they don't want to relocate a project team to babysit it — they want a trusted local who already knows the soil, the officials, and the farmers. That is a real, if modest, franchise.

But we should be skeptical of how durable that franchise is, because Winsol's own numbers hint at its limits. Management frames the company as having a "cost position advantage" from low overheads. Yet its operating margins — in the roughly 18–19% EBITDA range — are broadly comparable to peers rather than conspicuously fatter.15 If Winsol truly had a structural cost edge, you'd expect it to show up as superior margins or as market-share gains against those peers. Instead, the margins look ordinary and the customers are enormous. That tells you something important: Winsol is a competent, well-located execution shop, not a company with obvious pricing power over the likes of Adani Green and Suzlon. Its advantage is relationship and location, which is genuine but modest — the kind of edge that wins the next contract, not the kind that lets you dictate terms. And the thinness of that edge is exactly why the financials deserve a hard look.

VI. Financial Analysis: Growth, Leverage, and the Working Capital Trap

On the surface, Winsol's income statement is the kind of chart that makes a growth investor lean forward. Trace the top line across four years and it climbs like a staircase. In FY23 the company did ₹65.39 crore of revenue and ₹5.17 crore of net profit. In FY24, the IPO year, revenue reached ₹75.16 crore and profit ₹8.68 crore, with EBITDA margins expanding toward 17%. FY25 was the breakout: revenue jumped to ₹111.42 crore and profit to ₹11.79 crore. And FY26, the latest audited year, delivered ₹136.57 crore of revenue and ₹14.39 crore of profit — roughly 22.5% top-line growth and 22% profit growth.19 A three-year revenue CAGR near 28% and a profit CAGR above 40%, on a business with a 25% return on equity, is a legitimately strong operating record.9 The company is not a story stock pretending to grow; it is actually growing, and profitably.

But here is where a seasoned investor stops admiring the growth and starts interrogating how it was funded — because for an EPCC contractor, the income statement is the seductive half of the truth, and the balance sheet is the sobering half.

The number that should stop you is leverage. Winsol's debt-to-equity ratio jumped from roughly 0.34 in FY25 to about 1.07 in FY26 — total borrowings of around ₹68 crore against a net worth near ₹64 crore.9 In a single year the company went from lightly levered to carrying more debt than equity. Why? Not because it was in trouble, but because of the structural curse of the EPCC model: working capital. To bid for and execute larger, higher-voltage projects, Winsol has to fund the gap between spending and getting paid. It buys the steel, the transformers, the switchgear, and pours the concrete now; it posts bank guarantees to even qualify for the tender; it carries months of trade receivables while a client processes payment. The money goes out long before it comes back. Scaling up a contracting business, paradoxically, consumes cash rather than generating it — the faster you grow, the more working capital you have to fund, and the more you borrow to fund it.

The June 2026 KPIG Energia contract is the perfect illustration of this dynamic and of where Winsol is headed. It's a ₹49.80 crore order for the supply and erection of a 400kV EHV transmission line in Gujarat — the largest and most technically demanding class of project Winsol has taken on, dwarfing its typical ticket size.3 Landmark orders like this, along with the ₹60.81 crore ACME Solar contract and a ₹39 crore order from NTPC, are exactly the kind of wins that management touts in its disclosures.78 But every one of them also enlarges the working-capital hole that has to be pre-funded before the first rupee of payment arrives. Growth and cash strain are, for this business, two faces of the same coin.

There's a subtler point worth making about why leverage jumped so violently in one year, because "the company took on debt" undersells it. Winsol raised ₹23.36 crore at IPO and, in the two years since, has grown revenue from ₹75 crore to ₹137 crore. Roughly speaking, an EPCC contractor needs working capital scaling with revenue — so adding ₹60 crore of revenue demands a substantial permanent increase in the capital tied up in receivables, inventory, and retention money. The IPO proceeds covered part of that. The rest had to come from banks. In other words, the leverage spike isn't evidence of distress or of a failed business; it's the arithmetic consequence of growing 80% in two years on a capital base that a ₹23 crore raise could not possibly fund. The company essentially outgrew its IPO. That's a better problem than the alternative, but it is still a problem, because it means the growth rate is now hostage to the willingness of Winsol's bankers to keep extending credit and guarantee lines.

And this is where the asymmetry from earlier bites hardest. A company with pricing power responds to a working-capital squeeze by tightening payment terms with its customers. Winsol cannot do that. Its customers are Adani Green and Suzlon and NTPC — counterparties who set terms rather than accept them. So the only levers Winsol actually controls are bidding discipline (walk away from projects with punishing terms) and collection intensity (chase the money hard). Both are real, but both are far weaker than the lever it doesn't have.

This is why the single most important thing to watch at Winsol is not revenue — it's the cash conversion cycle. If receivables from clients like Suzlon or Adani Green stretch out, or if a state discom sits on a payment, the working-capital model can freeze. And when it freezes, the company loses the very thing that lets it bid for the next project: available cash and unused bank-guarantee capacity. For an EPC contractor, a receivables crunch isn't just a margin problem; it's an existential brake on growth. Free cash flow to the firm can stay negative for years even as accounting profit rises, precisely because that profit is being reinvested into an ever-growing pile of receivables and inventory.

Which brings us to a genuinely debatable capital-allocation decision. In May 2026, the board proposed a final dividend of ₹1 per share — an 8% payout ratio, modest but symbolically real, and the company's first dividend after paying nothing in prior years.19 On its face, a maiden dividend signals confidence and shareholder-friendliness. But a skeptic is entitled to ask the obvious question: why send cash out the door as dividends in the very year your debt-to-equity tripled to fund working capital? A rupee paid to shareholders is a rupee not available to fund the next receivables cycle, or a rupee that has to be borrowed back at interest. The dividend is best read as a signaling device — a young public company demonstrating that it can pay, planting a flag with SME retail investors — rather than as an act of capital abundance. Reasonable people can disagree on whether that signal is worth the cash. What isn't debatable is that a company funding growth with debt while distributing cash deserves to have that tension named out loud. And it's precisely that appetite for growth-at-the-edge-of-capacity that makes the next move — an overseas subsidiary — worth scrutinizing.

VII. The African Optionality: Winsol Engineers Zambia Limited

In March 2025, a curious line item appeared in Winsol's disclosures. On March 24, 2025, the company incorporated a foreign subsidiary in Lusaka, Zambia — Winsol Engineers Zambia Limited — to engage in electric power generation, transmission, and distribution.4 For a company with a market capitalization around ₹150 crore whose entire operating history is in coastal Gujarat, planting a flag in southern Africa is, at minimum, an eyebrow-raising move.

The strategic logic, in fairness, is not absurd. Zambia and its neighbors across the Southern African Copperbelt are in the grip of an acute, chronic power crisis. Copper mining — the economic engine of the region — is enormously electricity-hungry, and the grid cannot keep up; Zambia in particular has leaned heavily on hydropower that drought has repeatedly crippled. That combination is driving a wave of public and private investment into renewable generation, mini-grids, and transmission infrastructure. Tariffs can be attractive, and there is a genuine scarcity of localized EPCC engineers who know how to build and commission a substation on the ground. In theory, everything Winsol has learned in Gujarat — how to pour a foundation, wire a substation, energize a line, and keep it running — is portable to a market that desperately needs exactly those skills and has far less domestic competition.

So the case for Zambia is real optionality: a low-cost call option on a large, underserved market, bought for a minor cash outlay while it's still cheap. As of 2026 this is exactly what it is — highly speculative, financially immaterial, a toe in the water rather than a plunge. The specific financial terms, contribution, and any order pipeline for the Zambian entity have not been disclosed in detail, which is itself informative: a subsidiary material enough to move the needle would have to be quantified. Its absence from the numbers is the clearest evidence of how early this is.

But run the skeptic's checklist and the flags multiply. Cross-border contracting introduces risks Winsol has never managed: currency exposure, where a Zambian kwacha contract earns revenue in a currency that can devalue sharply against the rupee costs of imported equipment. Sovereign and counterparty risk, where the paying entity may be a state utility with its own fiscal stress — and if Winsol finds Indian discoms slow to pay, it should think hard about the collection dynamics in a market where it has no relationships, no local standing, and no realistic legal recourse. And most acutely: recall that Winsol's entire competitive advantage, as we established, is a cornered resource that is cornered to Gujarat. Local geology, GETCO's standards, three decades of relationships with district officials and farmers — none of it exists in Lusaka. In Zambia, Winsol is not the trusted local contractor with an unfair edge. It is a foreign entrant with no edge at all, competing on the one dimension where it is weakest: raw scale and capital.

But the case against deserves equal airtime, and it's the classic small-cap trap. Winsol is a sub-₹150-crore contractor that is already stretching its balance sheet to fund domestic growth, moving up the voltage ladder into 400kV work it hasn't done at scale before, and learning to be a public company all at once. Against that backdrop, sending management attention and capital to a distant, unfamiliar market thousands of kilometers away — different legal system, different currency risk, different counterparties, different everything — is the kind of "diworsification" that has quietly wrecked many an ambitious small company. The domestic Indian opportunity is enormous and right on Winsol's doorstep; every hour spent on Lusaka is an hour not spent executing the KPIG line in Gujarat. The honest verdict is that Zambia is neither the growth engine bulls might spin it into nor yet a proven mistake — it is an unvalidated experiment whose main risk is not the cash at stake but the executive bandwidth it could quietly consume. It belongs in the "watch, don't underwrite" column. And whether it becomes optionality or distraction depends entirely on the structural forces shaping Winsol's core business — which is where a framework helps.

VIII. Porter's Five Forces & Hamilton Helmer's Seven Powers Analysis

Strip away the growth narrative and the macro tailwind, and ask the coldest question an investor can ask: does Winsol have any durable competitive advantage — a moat — or is it simply a competent operator riding a wave that anyone could ride? Two frameworks help discipline the answer. Let's run Hamilton Helmer's Seven Powers first, because it's ruthless about distinguishing a real edge from a nice story.

Scale Economies — Weak. Winsol has none of the procurement muscle of an L&T or a KEC International, national infrastructure players who buy steel and cable by the trainload. What it has instead is a localized density advantage in the Jamnagar-Kutch corridor: enough repeat work in one geography to keep crews, equipment, and relationships busy and mobilized. That's a real efficiency, but it's regional and modest, not a structural cost moat.

Network Effects — None. Connecting a power plant to the grid is a linear, transactional job. No customer benefits because another customer used Winsol. There is no flywheel here.

Counter-Positioning — Not applicable in the classic sense, but its inverse is Winsol's defining vulnerability: Counter-Power is extremely poor. Winsol's customers are multi-billion-dollar conglomerates — Suzlon, Adani, Envision. When your buyer is a hundred times your size, you have essentially no leverage. If a client stretches your payment by ninety days, your only recourse is to wait, because the relationship matters far more to you than to them. This asymmetry is the single most important structural fact about the business, and it shows up directly in the working-capital risk we've already traced.

Switching Costs — Low to moderate. A developer can hire a different contractor for the next project, and often does. But there is a mild relationship-based barrier: a contractor with a track record of completing high-voltage substations on time with a clean safety record accumulates regulatory trust that a new entrant lacks. It's a soft moat — a preference, not a lock-in.

Brand — None that commands a price. Tender decisions are made on bid price, execution capability, and balance-sheet strength to pre-qualify. Nobody pays a premium for the Winsol name.

Cornered Resource — Moderate, and this is the most interesting one. Winsol's genuinely scarce asset is the tacit, hyper-local capability we met in Jamnagar: the right-of-way clearing know-how and the deep familiarity with GETCO grid-interconnection standards in Gujarat. That bundle of relationships and local knowledge is hard for an outsider to replicate quickly, and it's the closest thing Winsol has to a defensible edge. But note its boundary — it is cornered to Gujarat. Carry Winsol to Rajasthan or Zambia and the cornered resource largely evaporates.

Process Power — Weak. EPCC engineering is fairly standardized; there is no proprietary process that competitors can't learn.

Now Porter's Five Forces, which mostly confirms the picture from the industry side. Bargaining power of buyers is extreme — client concentration is high and giant buyers dictate price and payment terms. Bargaining power of suppliers is moderate — steel, copper, and transformer prices swing, and on a fixed-price contract those swings come straight out of Winsol's margin. Threat of new entrants is bifurcated, and this is the crux of the bull case: anyone with a crew and a truck can bid a 33kV civil-cabling job, so the low-voltage end is a commodity bloodbath — but constructing a 400kV substation requires technical certifications and balance-sheet pre-qualifications that most local contractors simply cannot meet. Threat of substitutes is essentially nil — all renewable power must eventually flow through physical transmission infrastructure; there is no software that replaces a copper line. And competitive rivalry is intense, with bidding wars on public tenders capable of compressing margins across the sector.

Put it together and the strategic truth is clear-eyed: Winsol's only credible path to a durable edge is to climb the voltage ladder faster than its competitors can follow, using its Gujarat cornered resource as the launchpad. At the bottom of the ladder it is a price-taker in a crowded field. Near the top — at 220kV and 400kV — the field thins dramatically and pre-qualification itself becomes the moat. The KPIG order is not just a big contract; it's a test of whether Winsol can convert local trust into technical altitude before it gets commoditized from below. That's the whole game, and it's a game with real ways to lose.

IX. Risks Radar & Skeptical Investor Stress Test

Let's now do what a short-seller or an activist would do: assume the bull case is wrong and hunt for what breaks it. Winsol has three risks that genuinely matter, and they compound one another.

Risk one is client concentration, and specifically the Suzlon dependency. Historically, a large slice of Winsol's revenue has come from a handful of big OEMs and developers. Concentration cuts both ways — it means efficient, repeatable relationships, but it also means that the financial health of a couple of customers effectively is Winsol's financial health. Suzlon is the cautionary name here. Anyone who watched Indian renewables in the 2010s remembers Suzlon's near-death debt spiral, the years of restructuring, the diluted shareholders. Suzlon has recovered, but the episode is a permanent reminder that Winsol's biggest customers are not risk-free counterparties. If a key client hit distress and stopped paying, Winsol's balance sheet — already carrying more debt than equity, already stretched by receivables — would be impaired almost overnight. A small contractor cannot out-wait a large distressed customer.

Risk two is the leverage-and-cash-flow gap, which is really the working-capital trap wearing a different hat. We've established that debt-to-equity tripled to roughly 1.07 in a single year to fund growth. The metrics a skeptic watches from here are the interest-coverage ratio — can operating profit comfortably service the growing interest bill? — and free cash flow to the firm, which for a fast-growing EPC contractor is frequently negative because every rupee of profit and then some is swallowed by working capital. The danger scenario is mechanical: rising rates or a tightening of bank-guarantee lines raises the cost and shrinks the availability of the very financing that makes bidding possible, and the growth engine stalls not for lack of orders but for lack of funding capacity.

Risk three is commodity inflation, the quiet killer of fixed-price contractors. Winsol bids lump-sum turnkey projects — it commits to a price today for work delivered over many months. If global copper, steel, or aluminum prices spike between the bid and the build, there is often no pass-through; the difference simply eats the margin. A single inflationary shock across a book of open fixed-price contracts can turn a good year into a mediocre one.

There are two further exposures worth naming briefly, because they're material even if they're not headline risks. The first is key-person concentration. Winsol's cornered resource — the local knowledge, the relationships, the standing in Gujarat's districts and grid offices — lives substantially in Ramesh Pindariya and a small circle around him. That is not a risk you can hedge or insure. Succession at a founder-led contractor whose primary asset is the founder's three decades of relationships is a genuine, if unquantifiable, overhang, and it is the kind of thing that only becomes visible when it's already a problem. The second is project-level accounting judgment. EPCC firms recognize revenue on percentage-of-completion — booking revenue as a project progresses, based on management's estimate of costs incurred versus total costs expected. That method is standard and legitimate, but it is inherently an estimate, and it gives management meaningful discretion over the timing of reported profit. It also produces "unbilled revenue": profit recognized on the income statement for work done but not yet invoiced. For any percentage-of-completion contractor, the relationship between reported profit, unbilled revenue, and cash actually collected is where the truth lives — and it deserves scrutiny not because anything is amiss at Winsol, but because it is precisely where things go wrong at contractors generally.

Now overlay these on how management communicates, because that gap is itself analytically useful. In its regulatory disclosures and order-win announcements, management leans hard on the growth story — the expanding pipeline, the landmark KPIG and ACME and NTPC wins, the march up the voltage ladder.378 That's the natural instinct of a young public company, and the wins are real. But the questions a skeptical analyst presses on — receivable days, unbilled revenue, the actual timing of cash collection from state discoms and large private clients — are precisely the ones where disclosures tend to be thinner and management commentary more optimistic than specific. This isn't an accusation of bad faith; it's the normal tension between a management team that wants to sell the runway and an investor who needs to see the cash. The tell to watch over the next several years is whether Winsol's communication matures — whether it starts volunteering hard working-capital metrics and collection timelines with the same enthusiasm it announces orders. Consistent, specific disclosure on the uncomfortable numbers is one of the surest signals that an SME is genuinely institutionalizing. Vague, growth-only messaging when the balance sheet is levering up is a yellow flag. With the risks framed, we can finally weigh the two sides of the case honestly.

X. The Balanced Investment Story: Bull vs. Bear Case

Every real investment thesis is a fight between two coherent stories. Here are Winsol's, argued at full strength.

The bull case starts with a tailwind so large it's almost unfair. India has committed to installing 500 GW of non-fossil generating capacity by 2030, an infrastructure build-out of staggering scale.12 Every gigawatt of that target needs foundations, substations, cabling, and evacuation lines — which is to say, every gigawatt needs balance-of-plant contractors. Demand for Winsol's core service is, for the foreseeable future, effectively unlimited; the constraint is execution capacity, not order availability. On top of that structural tailwind sits the value-chain migration story: Winsol is visibly climbing from basic 66kV substation work toward high-value 220kV and 400kV EHV transmission, where competitors are fewer, pre-qualification is a barrier, and pricing is better. If it can establish itself at the top of the voltage ladder, it graduates from commodity contractor to specialist. And beneath both sits the slow-compounding O&M accumulator — every substation built is a potential recurring maintenance annuity, and as that sticky, high-margin book grows, it should gradually stabilize the lumpy, cash-hungry EPC revenue underneath it. A cheap stock at under 10x earnings, growing revenue at ~28% with a 25% ROE, riding a decade-long macro wave, moving up the complexity curve — that's the bull case, and it's a serious one.

The bear case doesn't dispute the tailwind; it disputes whether Winsol captures the value. Start with the working-capital trap, which we've now seen from every angle: high growth here produces negative free cash flow, and a business that must borrow to grow is fragile to exactly the wrong things — a rate spike, a tightened credit line, a client that pays late. Add the loss-of-pricing-power problem: the buyers are consolidating and gigantic, and consolidated giant buyers squeeze sub-EPC margins as a matter of routine. Winsol has no counter-power, so in any margin negotiation it is the one that blinks. And finally, execution risk, which for a contractor is binary and brutal. A single major delay on a critical transmission project — a right-of-way dispute that drags through village land litigation, a foundation that has to be redone — can trigger liquidated-damages penalties that erase a full year's profit. The bigger and higher-voltage the projects get, the larger these single-project bets become, and the more a stumble hurts. In the bear story, Winsol is a fragile, low-power intermediary between commodity inputs and monopsonistic buyers, one receivables crunch or one botched 400kV line away from a very bad year.

An activist or skeptical long/short investor, handed this company, would press on a specific set of pressure points, and it's worth naming them because they sharpen the bear case beyond generic worry. They would challenge the capital allocation: paying a maiden dividend in the same year leverage tripled invites the question of whether the board is managing for signaling or for the business. They would probe governance: a family-dominated board owning 73.73% in an SME environment, where independent oversight is thin and related-party dynamics are hard for outsiders to see. They would demand better disclosure on receivables aging, unbilled revenue, and collection timelines — the numbers most diagnostic of an EPC contractor's health and, not coincidentally, the ones companies are slowest to volunteer. They would flag the Zambian subsidiary as potential diworsification, a scarce-attention drain from a management team that has plenty to prove at home. And they would want to see the interest coverage trajectory before applauding any of the growth, because growth funded by debt is only value-creating if the returns clear the cost of the borrowing. None of these is necessarily damning. All of them are legitimate, and a management team that engages them directly rather than deflecting would itself be sending a bullish signal about its own maturity.

Which story wins? The frameworks tell us the answer isn't fixed — it depends on execution, and that's why you don't need to guess. You can watch. Three KPIs cut through everything else and tell you, quarter by quarter, which case is playing out. First, the order-book-to-bill ratio — the size of the confirmed pipeline relative to current revenue — which tells you whether the top-line runway is intact. Second, and most important, the working-capital cycle, and specifically receivable days, with particular attention to receivables aging past 180 days; this is the single number that most directly reveals whether the growth is real cash or accounting mirage. Third, the debt-to-equity ratio, watching whether leverage stabilizes back below 1.0x as the IPO-era growth funding gets deployed and starts converting to cash, or whether it keeps climbing. Track those three, and you don't have to pick the bull or the bear in advance — the company will tell you which it is. That, ultimately, is the lesson Winsol teaches.

XI. Playbook: Business & Investing Lessons

Every good business story leaves behind a few durable lessons. Winsol offers three.

Lesson one: sell the picks and shovels during a gold rush. The renewable build-out is one of the largest capital-deployment events in history, and there are many ways to play it. You can manufacture turbines and shoulder brutal technology and warranty risk. You can develop and own power plants and shoulder enormous capital and regulatory risk. Or you can be the contractor who digs the holes and lays the cables — participating in the identical macro trend with a far lighter, more capital-nimble footprint and none of the asset-ownership exposure. Winsol chose the picks-and-shovels lane deliberately. It's a lower-ceiling strategy than being KP Energy, but it's also a lower-risk one, and in a gold rush the tool-seller sometimes sleeps better than the miner.

Lesson two: SME markets are double-edged swords. The NSE Emerge listing gave the Pindariya family liquidity, a currency for future growth, and a public profile they could never have bought. But the same platform's structural quirks — tiny floats, retail mania, 682x subscriptions — manufactured a listing price so divorced from fundamentals that long-term shareholders endured a multi-year, two-thirds de-rating even as the underlying business grew handsomely. The lesson for investors is to separate the company from the listing event. A great business can be a terrible stock if you buy it at a manic price, and the SME casino specializes in manic prices.

Lesson three: growth without cash flow is a mirage. This is the deepest lesson, and it's specific to contracting and project businesses. Revenue is vanity, profit is sanity, but for an EPCC firm, cash is reality. It is entirely possible for such a company to report rising revenue and rising accounting profit for years while generating negative free cash flow the entire time, because the "profit" is continuously reinvested into a swelling pile of receivables and work-in-progress. An investor who values an EPC contractor on a P/E multiple alone, without ever opening the cash-flow statement and studying the working-capital trend, is valuing a mirage. The number that matters most is the one that's hardest to fake: cash actually collected.

There is a fourth lesson, quieter than the others but worth stating: know the difference between an advantage that scales and one that doesn't. Winsol's edge is real, but it is a local edge — the illegible, relationship-bound cornered resource of Gujarat. Businesses fail in two opposite ways with such advantages. Some never leverage them, staying so hyper-local that they never grow. Others over-extrapolate them, assuming that what worked in one district will work in a new state or a new country, and marching confidently into markets where the very source of their edge doesn't exist. The art is knowing which of your advantages travel and which stay home — and Winsol's dual ambitions, up the voltage ladder at home and across an ocean to Zambia, are a live test of exactly that judgment. Climbing to 400kV in Gujarat leverages the local edge; landing in Lusaka abandons it. Same management, same year, two very different bets on the transferability of what makes the company special.

Those lessons — the wisdom of the picks-and-shovels lane, the treachery of the SME listing cycle, the primacy of cash over profit, and the discipline of knowing which advantages travel — are the through-lines of Winsol's short public life so far. They also frame the only question that matters from here.

XII. Epilogue

Step back, and Winsol resolves into something archetypal: a family-led, hyper-local Indian contracting firm attempting the hardest transition in business — to scale up and institutionalize at the same time. It rides a genuine, multi-decade macro tailwind. It has a real, if narrow, cornered resource in its Gujarat roots. It is run by a family with three-quarters of its net worth on the line and none of it pledged. And it is, simultaneously, structurally low-power against giant buyers, chronically hungry for working capital, and newly levered in service of ambitions — 400kV transmission, a Zambian subsidiary — that outstrip anything it has yet proven it can execute at scale.

The tension in the story is not really bull versus bear. It's discipline versus over-reach. The same appetite that drives Winsol up the voltage ladder and toward Lusaka is the appetite that could, mishandled, pull it into the oldest trap in contracting: over-expansion funded by debt, chasing revenue that never converts to cash. The green tsunami is real, and it will lift a great many boats. Whether Winsol is a boat that rises with it or one that takes on water in the swell depends on things no macro tailwind can supply — collection discipline, bid discipline, and the maturity to say no to the wrong project and the wrong geography.

So what to watch, in the end, is temperament as much as numbers. Will Winsol move into 400kV projects and international markets with the receivables under control and the leverage stabilizing — or will it fall for the classic EPC seduction of growth at any cash cost? The order wins will keep coming; the macro guarantees that. The real story, the one that will define whether this micro-cap becomes a durable compounder or a cautionary tale, is being written quietly, quarter by quarter, in the working-capital line of a balance sheet almost nobody reads. That's where to keep your eyes.

References

-

Winsol FY26 net profit rises 22% to ₹1,439.39 lakh — ScanX, 2026 ↩↩↩↩↩

-

Winsol Engineers IPO Date, Price, GMP, Review, Details — Chittorgarh, 2024 ↩

-

Winsol Engineers wins ₹49.8 crore order for 400 kV EHV project in Gujarat — ScanX, 2026-06 ↩↩

-

Winsol Engineers Incorporates Foreign Subsidiary in Lusaka, Zambia — MarketScreener, 2025-03-24 ↩

-

K.P. Energy Reports Record-Breaking Q4 FY26 Performance With ₹1,505 Crore Annual Revenue — SolarQuarter, 2026-05-08 ↩↩

-

Winsol Engineers secures ₹3.59 crore solar O&M order — ScanX, 2026-06 ↩

-

Winsol Engineers secures Rs 60.81 crore order from ACME Solar Holdings — Business Upturn, 2026 ↩↩

-

Winsol Engineers Share Price Rises 4% After Securing ₹39 Crore Order from NTPC — Angel One, 2026 ↩↩

-

Winsol Engineers Ltd — Financial snapshot and shareholding, Screener.in ↩↩↩↩↩↩↩↩↩

-

Winsol Engineers Limited — Board Meeting Outcome and promoter details, NSE Archives, 2024-06-03 ↩↩

-

Winsol Engineers Limited — AGM Outcome, NSE Archives, 2025-09-26 ↩

-

India's Renewable Energy Target: 500 GW by 2030 — Ministry of New and Renewable Energy (MNRE) ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube