Windlas Biotech: From Family Pharma to CDMO Powerhouse

I. Introduction & Episode Roadmap

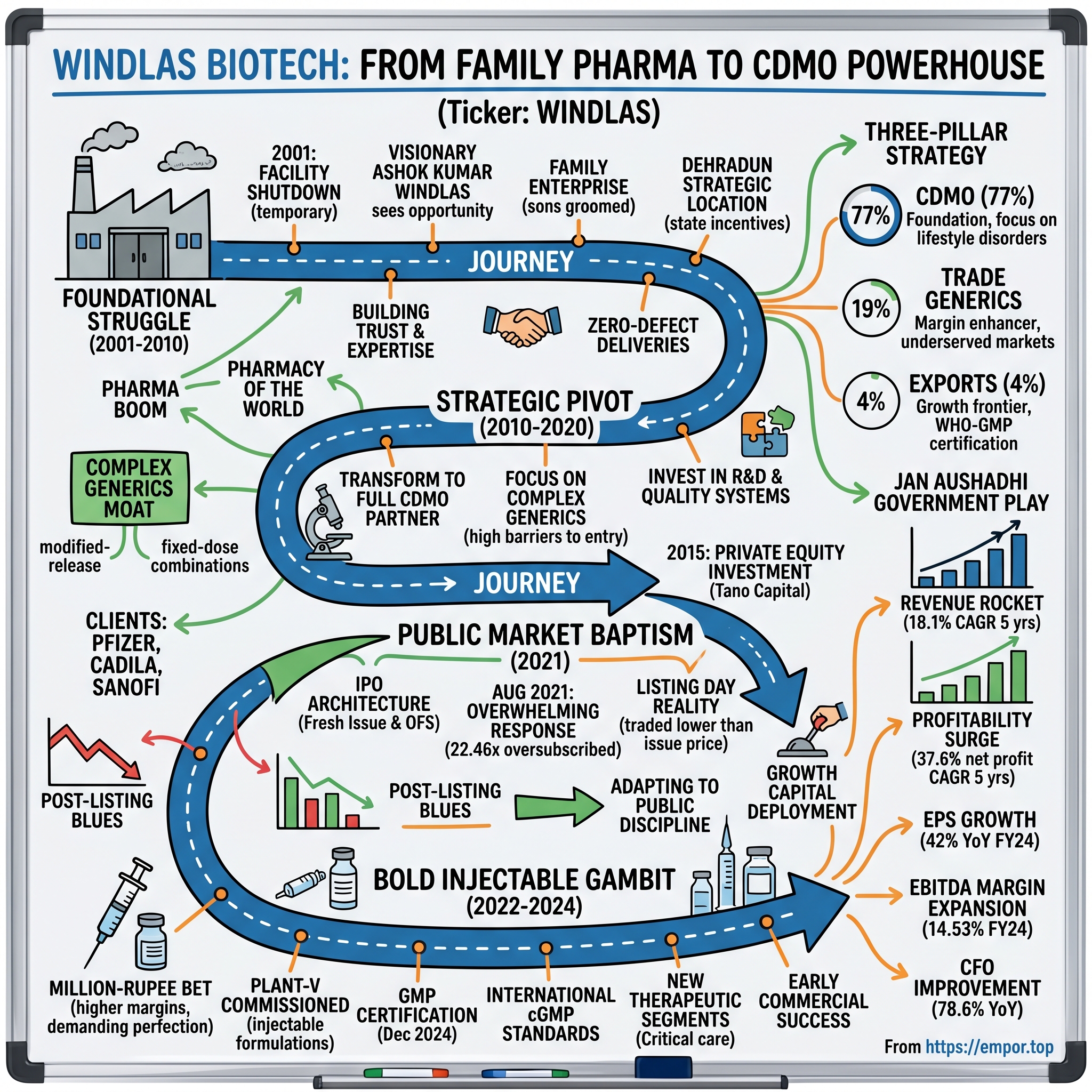

Picture the foothills of the Himalayas in Dehradun, 2001. A manufacturing facility sits temporarily shuttered—not the most auspicious beginning for what would become one of India's top five pharmaceutical CDMO companies. Windlas Biotech embarked on its journey in 2000, starting with a manufacturing facility that faced a temporary shutdown. Yet from this challenging start, Ashok Kumar Windlas saw opportunity where others might have seen obstacles.

Today, Windlas Biotech Limited is a leading pharmaceutical manufacturing and development company, committed to providing high-quality and affordable pharmaceutical and nutraceutical products across 19 countries. The company has transformed from a struggling startup into a formidable player, among the top five CDMO formulation companies in India, with a market capitalization hovering around ₹2,000 crores.

How did a family-run pharmaceutical company from the Himalayan foothills navigate the complex world of contract manufacturing, survive the brutal consolidation of India's pharma sector, and emerge as a trusted partner to over 100 pharmaceutical giants? This is the story of calculated risks, strategic pivots, and the delicate balance between family legacy and professional management—a playbook for building a pharmaceutical powerhouse in modern India.

Our journey will traverse the company's evolution through four distinct phases: the foundational struggle (2001-2010), the strategic pivot to complex generics (2010-2020), the public market baptism (2021), and the bold injectable gambit (2022-2024). Along the way, we'll decode their three-pillar business model, analyze their financial alchemy, and examine what their future might hold in India's rapidly evolving pharmaceutical landscape.

II. Origins & Founding Context (2001)

The Visionary and His Sons

It was founded in 2001, headquartered in Dehradun, Uttarakhand. But the real story begins with Ashok Kumar Windlas, a man who had spent decades as an entrepreneur before venturing into pharmaceuticals. Mr. Ashok Windlass has been a quintessential entrepreneur since last 42 years and has been responsible for the growth of Windlass family in various verticals.

The timing was both challenging and opportune. Post-liberalization India in the early 2000s was experiencing a pharmaceutical boom. The 1970 Patent Act had been the turning point, allowing Indian companies to reverse-engineer patented drugs and create affordable generics. By 2001, India was already being called the "pharmacy of the world," but the industry was also becoming increasingly competitive and consolidated.

Ashok Kumar Windlas didn't come from a pharmaceutical dynasty. He was building something from scratch, which meant every decision carried existential weight. Windlas Biotech Ltd was founded in 2001 by Mr. Ashok Kumar Windlas, and over the next 2 decades, it has grown to a revenue of INR 600 Cr with 4 plants located in Dehradun.

The Family Architecture

From the beginning, this was designed as a family enterprise with succession in mind. Ashok Kumar Windlass (70 years old) is the founder of Windlas Biotech and serves as a whole-time director. His sons, Hitesh Windlass (44 years old) and Manoj Windlass (42 years old) serve as Managing Director and Joint Managing Director, respectively. This wasn't just nepotism—both sons were groomed for their roles, understanding that they would inherit not just a company, but the responsibility of hundreds of employees and partnerships.

The family structure extended beyond just the immediate family. Hitesh's wife, Prachi Jain Windlass, is a non-executive director, creating a tight-knit governance structure that would prove both a strength and a potential concern for future investors.

Dehradun: Strategic Geography

The choice of Dehradun wasn't accidental. Located in Uttarakhand, the location offered several advantages that a bootstrapped pharmaceutical company desperately needed. The state government was offering incentives to manufacturers, land was relatively affordable, and the location provided good connectivity to North India's major markets while maintaining lower operational costs than metro cities.

But Dehradun also presented challenges. Attracting top talent to a tier-2 city wasn't easy. The pharmaceutical ecosystem—suppliers, testing labs, regulatory consultants—was thin compared to established hubs like Hyderabad or Ahmedabad. Every small victory had to be earned twice over.

The Initial Crisis and Transformation

Over the years, it has transformed into a fully integrated partner, providing an array of products and services to leading pharmaceutical companies. But this transformation didn't happen overnight. The temporary shutdown of their first facility was a baptism by fire. Rather than seeing it as a setback, Ashok Kumar Windlas used it as an opportunity to recalibrate.

The company initially positioned itself as a contract manufacturer for domestic pharmaceutical companies—essentially making tablets and syrups for brands that would sell them under their own labels. It wasn't glamorous work, but it was steady, and it allowed the company to build two critical assets: manufacturing expertise and trust.

Building in the Shadows

In those early years, Windlas Biotech was essentially invisible to consumers. They were the company behind the companies, manufacturing products that would carry other brands' names. This B2B model meant that success depended entirely on reliability, quality, and cost-effectiveness. One batch failure, one delayed delivery, could mean losing a client forever.

The company focused on solid and liquid dosage forms—tablets, capsules, and syrups—the bread and butter of pharmaceutical manufacturing. Nothing fancy, nothing complex, just consistent quality at competitive prices. By the end of the first decade, they had quietly built manufacturing capabilities that would become the foundation for everything that followed.

III. Early Years: Building The Foundation (2001–2010)

The Trust Equation

In the pharmaceutical contract manufacturing world, trust isn't just important—it's everything. When Pfizer or Cadila hands over a formulation to a third-party manufacturer, they're not just outsourcing production; they're putting their reputation in someone else's hands. A single quality issue can trigger regulatory action, destroy brand value, and end partnerships that took years to build.

Windlas understood this implicitly. In those early years, while competitors were racing to add capacity, Windlas focused obsessively on building systems. Quality control wasn't just a department—it was a religion. Every batch was tested multiple times. Documentation was meticulous. When clients visited the Dehradun facility, they found processes that matched or exceeded their own standards.

Trusted partnerships with over 100 pharmaceutical companies—this wasn't achieved through aggressive salesmanship but through a track record of zero-defect deliveries and absolute confidentiality. In an industry where formulations are closely guarded secrets, Windlas became known as a vault.

The Capacity Build-Out

By the mid-2000s, the company was ready to scale. The trust was established, the systems were in place, and demand was growing. But scaling in pharmaceuticals isn't like scaling in software—you can't just spin up new servers. Every new production line requires regulatory approval, every expansion needs to maintain the same quality standards, and every piece of equipment represents millions in capital investment.

The company methodically built out its capabilities, eventually reaching a staggering scale: With three state-of-the-art manufacturing plants in Dehradun, Uttarakhand, Windlas Biotech has an impressive installed capacity, producing 7063.83 million tablets, 54.46 million pouches, and 61.08 million liquid bottles.

These aren't just numbers—each represents a strategic decision. The tablet capacity meant they could handle large-volume orders from major pharmaceutical companies. The pouch capability opened doors to nutraceutical and OTC products. The liquid bottle capacity positioned them for pediatric formulations and syrups, higher-margin products that required specialized manufacturing capabilities.

The Client Portfolio: A Who's Who of Indian Pharma

By 2010, Windlas had quietly assembled a client roster that would make any CDMO envious. The company exports its products to leading pharmaceutical companies, including Cadila Healthcare Limited, Pfizer Limited, Emcure Pharmaceutical Ltd, Sanofi India Limited. These weren't small, experimental contracts—these were multi-year relationships with some of the biggest names in pharmaceuticals.

How did a relatively unknown company from Dehradun land such prestigious clients? The answer lay in their approach to partnership. While larger CDMOs treated clients as customers, Windlas treated them as collaborators. They didn't just manufacture to specifications; they provided input on formulation optimization, helped navigate regulatory requirements, and even assisted with packaging innovations that could reduce costs.

The Innovation Seeds

Strong focus on innovation with a diverse health portfolio spanning anti-diabetic, cardiovascular, respiratory, and gastroenterological products. Even in these early years, Windlas wasn't content being just a contract manufacturer. They were quietly building capabilities in complex formulations—products that required special knowledge and expertise to manufacture.

This focus on complexity would become their moat. While any manufacturer could make simple paracetamol tablets, creating fixed-dose combinations for diabetes management or modified-release formulations for cardiovascular conditions required deep pharmaceutical knowledge. Each successful complex product added to their reputation and created barriers for competitors.

Timeline Milestones: The Quiet Ascent

2001: Windlas Biotech inaugurated its first production plant in Dehradun. 2007: The company established its own brand and marketing division. 2009: Windlas ventured into international markets and surpassed the milestone of Rs 100 Crore in revenue by establishing Windlas Healthcare. 2014: A second manufacturing plant was set up, revenue crossed Rs 200 Crore, and the company cleared its first USFDA inspection.

Each milestone represented a strategic evolution. The 2007 decision to establish their own brand wasn't just about forward integration—it was about understanding the market from the brand owner's perspective, insights that would make them better partners to their CDMO clients. The 2009 international venture through Windlas Healthcare wasn't just about exports—it was about understanding global quality standards that would elevate their entire operation.

The Financial Discipline

Throughout this period, the company maintained remarkable financial discipline. Unlike many Indian pharmaceutical companies that leveraged heavily to fund growth, Windlas grew organically, reinvesting profits rather than taking on significant debt. This conservative approach meant slower growth, but it also meant survival during the downturns that claimed many of their peers.

IV. Strategic Pivot: CDMO & Complex Generics (2010–2020)

From Contract Manufacturer to Strategic Partner

The transformation from simple contract manufacturing to becoming a Contract Development and Manufacturing Organization (CDMO) wasn't just a rebranding exercise—it represented a fundamental shift in business model. While contract manufacturers simply execute, CDMOs collaborate from the earliest stages of drug development. They become partners in formulation, help navigate regulatory pathways, and share the technical risk of bringing new products to market.

Windlas recognized that the future belonged to companies that could offer more than just manufacturing muscle. The company has firmly established itself as a leader, offering a comprehensive range of services in the Contract Development and Manufacturing Organization (CDMO) segment. They began investing heavily in R&D capabilities, hiring formulation scientists, and building analytical laboratories that could support everything from stability studies to bioequivalence testing.

The Complex Generics Moat

The real strategic masterstroke was the focus on complex generics. These aren't your simple, single-molecule drugs—these are pharmaceutical puzzles that require sophisticated chemistry and manufacturing expertise to solve. It provides a comprehensive range of CDMO products ranging from product development, licensing, and commercial manufacturing of generic products, including complex generics for its domestic customers.

What exactly makes a generic "complex"? Fixed-dose combinations that combine multiple active ingredients in precise ratios. Modified-release formulations that control how quickly a drug is absorbed. Chewable or dispersible tablets that maintain stability despite unconventional delivery methods. Each of these requires specialized equipment, deep formulation expertise, and—critically—regulatory know-how that takes years to develop.

The complexity created a beautiful business dynamic. High barriers to entry meant less competition. Fewer manufacturers meant better pricing power. And once a client invested in validating Windlas for a complex product, switching costs became prohibitively high. It was a virtuous cycle that would drive margins and growth through the decade.

Building the Branded Portfolio

The company also developed its own branded products, distributing them through a rapidly expanding network of more than 500 wholesale partners across India. This wasn't abandoning their CDMO roots—it was complementing them. By 2015, Windlas had learned enough about what products succeeded in the market, what formulations doctors preferred, and what price points worked in different segments.

The branded products served multiple strategic purposes. They provided higher margins than contract manufacturing. They gave Windlas direct market feedback that made them better CDMO partners. And crucially, they diversified revenue streams, reducing dependence on any single client or segment.

The Private Equity Validation

2015: Windlas Biotech received a private equity investment from Tano Capital. This was more than just capital—it was validation. Tano Capital, a healthcare-focused private equity firm, had evaluated dozens of pharmaceutical companies. Their investment in Windlas signaled that professional investors saw something special in this family-run operation from Dehradun.

The private equity partnership brought more than money. It brought governance disciplines, strategic connections, and pressure to professionalize operations. For a family business, this could have been disruptive. Instead, the Windlas family embraced it, understanding that professional management and family ownership weren't mutually exclusive.

Navigating Regulatory Complexity

2014: A second manufacturing plant was set up, revenue crossed Rs 200 Crore, and the company cleared its first USFDA inspection. That USFDA inspection clearance was a watershed moment. It meant Windlas could now manufacture for the US market—not directly, but for Indian companies exporting to the US. It was a quality certification that put them in an elite group of Indian manufacturers.

But with greater capability came greater scrutiny. USFDA inspections are notoriously rigorous, and a single observation can shut down a facility. Windlas had to upgrade not just equipment but entire quality systems. Standard operating procedures that had worked for years had to be rewritten. Documentation that was good enough for Indian regulators had to meet the exacting standards of the FDA.

The Relationship Capital

By 2020, relationships with major pharmaceutical companies had deepened beyond simple client-vendor dynamics. Windlas wasn't just a manufacturer; they were a strategic partner who understood their clients' businesses almost as well as the clients themselves. When a major pharmaceutical company wanted to launch a new fixed-dose combination for diabetes, Windlas wasn't just asked to manufacture—they were consulted on formulation, involved in stability studies, and partnered on regulatory submissions.

The company exports its products to leading pharmaceutical companies, including Cadila Healthcare Limited, Pfizer Limited, Emcure Pharmaceutical Ltd, Sanofi India Limited, Intas Pharmaceutical Ltd, and Systolic Laboratories Private Ltd. Each of these relationships represented years of trust-building, consistent delivery, and shared success.

Setting the Stage for Public Markets

2016: The company achieved a turnover of Rs 300 Crore. 2017: Windlas set up its third manufacturing plant and launched its first product in the US through Windlas Healthcare. 2018: Windlas Biotech secured a $23 million investment from Zydus Cadila in Windlas Healthcare. 2019: The company executed a buyback of Zydus shares in Windlas Healthcare.

The Zydus Cadila investment and subsequent buyback was particularly telling. One of India's largest pharmaceutical companies had invested in Windlas's subsidiary, validating their capabilities. But the buyback showed that Windlas was confident enough in their trajectory to go it alone. They were ready for the next chapter: the public markets.

V. The IPO Story & Public Market Entry (2021)

The Perfect Storm

August 2021. India's stock markets were on fire. The pandemic had created a newfound respect for pharmaceutical companies. Retail participation in IPOs was at an all-time high. And quality mid-cap companies were commanding premium valuations. For Windlas Biotech, twenty years after its founding, the stars had aligned.

But the decision to go public wasn't driven by market exuberance. The company had ambitious expansion plans that required significant capital. The proceeds from the fresh issue of the IPO will be utilised for purchasing of equipment required for capacity expansion of the facility at Dehradun Plant-IV and addition of injectables dosage capability at the facility at Dehradun Plant-II.

The injectable facility wasn't just another production line—it represented Windlas's entry into a completely new and highly lucrative segment of pharmaceutical manufacturing. But building a sterile injectable facility to international standards would require serious capital, and the public markets offered the most efficient path.

The IPO Architecture

Windlas Biotech initiated its public offering with the aim of raising Rs 401.54 Crore. This offering comprises a fresh issue of Rs 165 Crore and an offer for sale of Rs 236.54 Crore. The structure was telling. The fresh issue would fund growth, while the offer for sale would provide an exit for early investors, particularly investor Tano India Private Equity Fund II will offload its entire stake of 40.1 m equity shares (22% of pre-offer paid-up equity).

The IPO opens on Aug 4, 2021, and closes on Aug 6, 2021. The IPO of is priced at ₹448-460 per equity share. The price band reflected confidence—at ₹460 per share, the company was valued at over ₹1,000 crores, a remarkable valuation for a company that had started with a shuttered facility just two decades earlier.

The Overwhelming Response

Windlas Biotech IPO oversubscribed 22.46 times on closing day. In the world of IPOs, subscription numbers tell a story. Less than 1x means trouble. 2-5x suggests healthy interest. But 22.46x? That's a vote of confidence that borders on euphoria.

The retail portion saw massive oversubscription, with small investors betting that this Dehradun-based CDMO would be the next pharmaceutical multi-bagger. Institutional investors, typically more measured, also showed strong interest, validating the company's fundamentals beyond just market sentiment.

The Listing Day Reality Check

Monday, August 16, 2021. The moment of truth. The pharmaceutical company stock made its exchange debut on Monday, August 16, 2021, around 10 per cent lower premium to Rs 419 per share on both BSE and NSE. The listing at ₹419 against the issue price of ₹460 was sobering—an immediate loss of about 9% for investors who had bid at the upper band.

But the real story unfolded as the day progressed. The stocks counter on the first day of its trading session had ended weak by over 7 per cent to Rs 406.7 per share, below the issue price of Rs 460 per share at the upper end. By the end of the first day, investors who had entered at ₹460 were sitting on losses of nearly 12%.

The Post-Listing Blues

The days following the listing were brutal. Shares of Windlas Biotech (WBL) extended their decline and were trading lower for the third straight day since listing. In the intra-day trade on Wednesday, the shares dropped 4 per cent at Rs 385.50 on the BSE, and are down 16 per cent from its issue price of Rs 460 per share.

For a company that had received such overwhelming subscription, the post-listing performance was a harsh lesson in market dynamics. The high subscription had created expectations of listing gains, attracting flippers who sold immediately when those gains didn't materialize. The selling pressure created a downward spiral that had little to do with the company's fundamentals.

Learning to Be Public

For the Windlas family, the transition from private to public company was jarring. Suddenly, every quarterly result was scrutinized. Stock price movements of a few percent triggered worried calls from investors. The business they had built methodically over two decades was now being valued every second by the market.

But they adapted. Investor calls became more polished. Financial reporting became more detailed. The company began providing guidance, something they had never needed to do as a private entity. promoters held 78% stake in Windlas Biotech including Vimla Windlass's 7.8% shareholding, ensuring that despite being public, control remained firmly with the founding family.

Capital Deployment and Validation

Despite the challenging start in public markets, the IPO had achieved its primary purpose: raising growth capital. The company immediately began deploying the proceeds toward its stated objectives. The injectable facility that had been a dream was becoming reality. Equipment was being ordered, clean rooms were being constructed, and regulatory approvals were being sought.

More importantly, the discipline required of a public company was making Windlas stronger. Quarterly reporting forced more rigorous financial planning. Investor scrutiny encouraged clearer strategic communication. The governance requirements of being listed brought in independent directors who added valuable expertise.

VI. The Injectable Gambit: New Frontiers (2022–2024)

The Billion-Rupee Bet

In the pharmaceutical world, moving from oral solids to injectables isn't just an expansion—it's a transformation. It's like a chef who's mastered Italian cuisine deciding to open a sushi restaurant. The skills are related but different. The equipment is entirely different. The regulations are more stringent. And the stakes—particularly for sterile injectables where contamination can be fatal—are exponentially higher.

In FY 2023-24, it commissioned Plant-V used in injectable formulations. This wasn't a small addition to existing capabilities. This was Windlas betting that they could master an entirely new domain of pharmaceutical manufacturing, one that promised higher margins but demanded perfection.

Breaking Ground in April 2024

Windlas Biotech Limited announced the commissioning of its state-of-the-art injectable facility for manufacturing of Small Volume Parenteral products, built to meet international cGMP standards. The Company has received manufacturing license from the Drug Controlling & Licensing Authority of Uttarakhand after joint inspection conducted by Central Drugs Standard Control Organisation and State Licensing Authority of Uttarakhand.

The facility represented everything Windlas had learned in two decades, condensed into one ambitious project. Small Volume Parenterals (SVPs) aren't just technically complex—they're unforgiving. A tablet with slightly off specifications might have reduced efficacy. An injectable with contamination could kill. There's no margin for error.

The Technical Marvel

This milestone marks company's continued foray in development and manufacturing of complex dosage forms like Ampoules, Liquid Vials and Lyophilized Vials thereby extending its product portfolio to critical care and other specialized therapeutic segments.

Each of these dosage forms represents a different technical challenge. Ampoules require precise glass-sealing technology. Liquid vials need aseptic filling capabilities. But lyophilized vials—freeze-dried injectables—are the crown jewel of complexity. The drug is dissolved, filled into vials, frozen, and then subjected to vacuum to remove water through sublimation. It's pharmaceutical manufacturing at its most sophisticated.

The facility wasn't just about manufacturing capability; it was about entering entirely new therapeutic areas. Critical care medications, emergency room drugs, specialized treatments that could only be delivered through injection—these commanded premium prices and enjoyed less competition than the crowded oral formulation market.

The Financial Mathematics

The injectables facility has the potential to generate about 100 Cr INR in revenues at peak utilization with an EBITDA margin profile of 18-20%. In a business where CDMO margins typically hover around 12-14%, the promise of 18-20% EBITDA margins was transformative. This wasn't just growth—it was margin-accretive growth, the holy grail for any manufacturing business.

But the investment was substantial. Building a sterile facility to international standards doesn't come cheap. Every surface must be cleanable. Air handling systems must maintain precise pressure differentials. Water systems must produce pharmaceutical-grade water consistently. The entire facility must be validated through extensive testing before a single commercial batch can be produced.

The Strategic Trifecta

This Injectable plant shall cater to all three of business verticals: CDMO, Trade Generics & Institutional, and Exports. This wasn't just about adding capacity—it was about creating synergies across their entire business model.

For CDMO clients, Windlas could now offer complete solutions—from oral formulations to injectables. For their trade generics business, they could enter higher-value therapeutic areas. For exports, particularly to less-regulated markets, Indian-made injectables commanded premium prices due to quality perceptions.

GMP Certification: The Final Validation

December 2024 marked a crucial milestone. Windlas Biotech Limited, one of the leading domestic pharmaceutical formulations contract development and manufacturing organization (CDMO) industry in India, is pleased to announce that it has received Good Manufacturing Practices (GMP) certification for its new injectable facility from the Food Safety & Drugs Administration Authority of Uttarakhand, following the inspection in December 2024.

GMP certification isn't just a regulatory checkbox—it's a passport to global markets. The certification states that the firm is following the Good Manufacturing Practices as per World Health Organization (WHO) TRS Guidelines. WHO-GMP compliance means the facility meets international standards, opening doors to exports and partnerships that wouldn't otherwise be possible.

The Competitive Implications

With this new GMP-certified injectable facility, all five of Windlas Biotech Manufacturing plants are complying with this standard and we are well poised to expand our product portfolio offerings in the CDMO space. Five GMP-certified plants—that's a statement. In India's CDMO industry, where many players operate with regulatory issues at one facility or another, having five clean facilities is a powerful differentiator.

The injectable capability also changed Windlas's competitive positioning. They were no longer competing just with oral formulation CDMOs. They were now in the same league as integrated pharmaceutical manufacturers, able to offer services across the entire spectrum of dosage forms.

Early Commercial Success

The facility has initiated manufacturing of commercial batches and expect to introduce several new products over the course of Financial Year 2025. The transition from validation batches to commercial production is always delicate. The first commercial batches are scrutinized intensely. Any quality issue could damage the facility's reputation before it's even established.

But Windlas navigated this transition smoothly. Years of manufacturing discipline in oral formulations translated well to injectables. The quality systems that had impressed USFDA inspectors were adapted and enhanced for sterile manufacturing. The company's reputation for reliability, built over two decades, gave clients confidence to trust them with injectable products.

VII. Business Model & Three Pillars Strategy

The Three-Legged Stool

The company's business operates in three segments: CDMO products and services, domestic trade generics and OTC markets, and exports. This three-pillar structure wasn't accidental—it was architected to balance growth, margins, and risk.

Think of it as a three-legged stool. CDMO services provide steady, predictable revenue with deep client relationships. Trade generics offer higher margins and direct market feedback. Exports represent the growth frontier with access to global markets. Remove any leg, and the stool wobbles. Together, they create stability.

CDMO: The Foundation

Windlas Biotech Ltd derives its revenue from three main business segments: 77% from CDMO services and products, 19% from the domestic trade generics segment, and 4% from exports as of FY24. With over three-quarters of revenue from CDMO, this remains the cornerstone of the business.

But this isn't the commoditized contract manufacturing of the past. Notably, Windlas focuses on complex generic products in the chronic therapeutic sectors related to lifestyle disorders. Lifestyle diseases—diabetes, hypertension, cholesterol—these are the pharmaceutical industry's gold mines. Patients need medication for life. Treatment often requires multiple drugs. And the prevalence is exploding in India's increasingly affluent, increasingly sedentary population.

The CDMO model has evolved to become deeply integrated with clients' operations. Windlas doesn't just wait for manufacturing orders. They're involved from the development phase, helping optimize formulations for manufacturability. They conduct stability studies. They assist with regulatory filings. By the time a product reaches commercial manufacturing, Windlas knows it as intimately as the brand owner.

Trade Generics: The Margin Enhancer

The trade generics business was the surprise success story. Windlas Biotech Ltd is going to comfortably overshoot the trade generics revenue target of 130 Cr INR by FY26, as the FY24 run-rate itself has reached 115 Cr INR. Trade generics segment continues to grow at 25%+ CAGR on a yearly basis.

This wasn't supposed to happen. When Windlas launched their own brands, it was meant to be a small, complementary business. But they discovered an underserved market: quality generic medicines for India's tier-2 and tier-3 cities. These markets were price-sensitive but not quality-agnostic. Doctors wanted reliable generics they could prescribe with confidence. Windlas, with their manufacturing pedigree, could provide exactly that.

The trade generics business also provided valuable margin expansion. Trade generics have 4-5% higher gross margins than formulations CDMO sales. In a business where every percentage point of margin matters, this differential was significant.

Exports: The Frontier

More than 95% of Windlas Biotech Ltd's revenues are from India, and exports comprise less than 5% of the company's current revenues. The target export market for Windlas Biotech Ltd is non-regulated and semi-regulated geographies.

At first glance, less than 5% exports might seem like a weakness. But it's actually a massive opportunity. Indian pharmaceutical companies have built global reputations in markets like Africa, Southeast Asia, and Latin America. These markets value quality Indian generics but don't require the extensive regulatory compliance of US or European markets.

For Windlas, exports represent optionality. They've built the quality systems. They have WHO-GMP certification. When they choose to accelerate exports, the infrastructure is ready. But for now, the domestic opportunity is so large that exports remain a future growth lever rather than a current priority.

Jan Aushadhi: The Government Play

One of the most interesting opportunities lies in the government's Jan Aushadhi scheme—a program to provide quality generic medicines at affordable prices through dedicated stores. For a company like Windlas, with strong generic manufacturing capabilities and cost leadership, this represents a significant opportunity.

The institutional business isn't just about volume—it's about validation. Being selected as a supplier for government programs provides credibility that helps in other segments. It's also relatively sticky business. Once approved and integrated into government supply chains, displacement is rare unless there are quality issues.

The Network Effects

What makes Windlas's three-pillar model particularly powerful are the network effects between segments. A formulation developed for a CDMO client might later be launched as a trade generic. Experience gained in trade generics provides market insights that make them a better CDMO partner. Export market learnings enhance quality systems that benefit all segments.

The company also developed its own branded products, distributing them through a rapidly expanding network of more than 500 wholesale partners across India. This distribution network, built for trade generics, becomes an asset that CDMO clients value. They know Windlas understands not just manufacturing but also distribution and market dynamics.

Capacity as Currency

In pharmaceutical manufacturing, capacity isn't just about production capability—it's currency. With three state-of-the-art manufacturing plants in Dehradun, Uttarakhand, Windlas Biotech has an impressive installed capacity, producing 7063.83 million tablets, 54.46 million pouches, and 61.08 million liquid bottles.

These numbers represent flexibility. A large order from a CDMO client? They have capacity. A surge in demand for trade generics? They can handle it. An export opportunity? They're ready. This capacity buffer means they rarely have to turn away business, and it gives them negotiating leverage with clients who need reliable supply.

VIII. Financial Performance & Growth Trajectory

The Revenue Rocket

The revenues of WINDLAS BIOTECH stood at Rs 6,444 m in FY24, which was up 23.2% compared to Rs 5,230 m reported in FY23. WINDLAS BIOTECH's revenue has grown from Rs 3,313 m in FY20 to Rs 6,444 m in FY24. Over the past 5 years, the revenue of WINDLAS BIOTECH has grown at a CAGR of 18.1%.

These aren't just numbers—they tell a story of consistent execution. An 18.1% CAGR over five years in a mature industry like pharmaceutical manufacturing is exceptional. It means Windlas was growing faster than the market, taking share from competitors, and successfully executing on their expansion strategy.

But the headline numbers don't tell the full story. The growth was quality growth—not just volume expansion but movement up the value chain. Complex generics commanded better prices than simple formulations. Trade generics earned higher margins than CDMO services. Each year's growth made the next year's growth more valuable.

The Profitability Surge

The net profit of WINDLAS BIOTECH stood at Rs 581 m in FY24, which was up 36.4% compared to Rs 426 m reported in FY23. This compares to a net profit of Rs 381 m in FY22 and a net profit of Rs 156 m in FY21. Over the past 5 years, WINDLAS BIOTECH net profit has grown at a CAGR of 37.6%.

A 37.6% profit CAGR while revenues grew at 18.1%—this is the definition of operational leverage. It means margins were expanding, efficiency was improving, and the business model was demonstrating its inherent profitability. Fixed costs were being spread across a larger revenue base. Pricing power was improving. The business was scaling beautifully.

The Cash Generation Machine

WINDLAS BIOTECH's cash flow from operating activities (CFO) during FY24 stood at Rs 1 billion, an improvement of 78.6% on a YoY basis. In manufacturing businesses, cash flow is the ultimate truth teller. You can manipulate earnings through accounting, but cash doesn't lie.

₹100 crores in operating cash flow—this is real money that can fund expansion, pay dividends, or weather downturns. The 78.6% year-over-year improvement suggests that not only is the business profitable, but it's also becoming more efficient at converting profits to cash.

EPS: The Shareholder Scorecard

In FY24, the EPS stood at Rs 27.97, a 42% YoY growth rate. For shareholders who entered at the IPO price of ₹460, this meant they were buying at about 16.5 times earnings—reasonable for a growing pharmaceutical company. For those who weathered the post-listing storm and accumulated at lower prices, the returns were even better.

The EPS growth rate of 42% significantly outpacing revenue growth of 23% tells us that the company wasn't just growing—it was growing profitably. Share buybacks hadn't inflated the EPS. This was genuine earnings growth flowing through to shareholders.

Margin Expansion: The Quality Story

EBITDA margins improved from 11% in FY20 to a high of 14.53% in FY24. In a competitive industry where pricing pressure is constant, expanding margins by 350 basis points is remarkable. It speaks to improved operational efficiency, better product mix, and growing pricing power.

The margin expansion wasn't just about cost-cutting. It was about strategic choices. The growing contribution from trade generics, with their higher margins, was pulling up overall profitability. The focus on complex generics meant better pricing. The injectable facility, once operational, promised even better margins.

Q2 FY24: The Milestone Quarter

The company crossed Rs 150 Cr revenue milestone in Q2 FY24 and hat-trick of record-breaking quarterly revenue. We delivered our best first half revenues, EBITDA and cashflow on record.

Crossing ₹150 crores in quarterly revenue was psychological as much as financial. It put Windlas in a new league, making them more attractive to large CDMO clients who need scale. It validated the investment thesis for public market investors. And internally, it proved that the aggressive growth targets weren't just aspirations—they were achievable.

The Liquidity Position

Strong liquidity Rs 213 crore. In pharmaceutical manufacturing, liquidity is like oxygen. You need working capital to buy raw materials. You need cash to fund the 60-90 day payment cycles typical in the industry. You need reserves for opportunistic capacity expansion or strategic acquisitions.

₹213 crores in liquidity meant Windlas could weather any short-term disruption. It meant they could take on large orders without working capital constraints. It meant they could invest in growth without diluting shareholders or taking on expensive debt.

Return on Equity: The Efficiency Metric

Return on Assets (ROA): The ROA of the company improved and stood at 9.5% during FY24, from 8.2% during FY23. The ROA measures how efficiently the company uses its assets to generate earnings.

An improving ROA in a capital-intensive business like pharmaceutical manufacturing is noteworthy. It means the company is getting more output from its invested capital. The new plants are ramping up efficiently. The equipment is being utilized effectively. Capital allocation is disciplined.

IX. Competition & Market Dynamics

The Fragmented Battlefield

The largest player in this industry is Akums Drugs and Pharmaceuticals Ltd, with a topline of ~3500Cr INR (10% domestic market share) in FY23. Think about that—the largest player has only 10% market share. In most industries, that would signal consolidation opportunities. In Indian pharma CDMO, it reflects the incredible diversity of the market.

The Indian domestic formulations CDMO industry is estimated to be ~35000-40000 Cr INR in size as of FY23. Including exports, the formulations CDMO industry size may be around 65000-70000 Cr INR. This is a massive market, growing at double digits, with room for multiple winners.

The Competitive Landscape

Windlas's key competitors read like a who's who of Indian CDMO: Windlas' top competitors are Akums, Jubilant Life Sciences and Unither. Each has their strengths. Akums has scale. Jubilant has international presence. But Windlas has carved out its niche through reliability, complex generics capability, and deep client relationships.

The competition isn't just about capabilities—it's about trust. In an industry where a single quality issue can trigger regulatory action and destroy years of reputation, clients value reliability over rock-bottom prices. Windlas's track record of zero significant regulatory issues becomes a powerful competitive advantage.

The Consolidation Thesis

The formulations CDMO industry is highly fragmented, with few large, organised players. The industry is expected to consolidate gradually, and the larger players will gain more market share as outsourcing companies look for larger partners to work with and regulatory requirements become more stringent.

This consolidation thesis particularly favors Windlas. They're large enough to be taken seriously by major pharmaceutical companies but small enough to be nimble. They have the quality systems to meet increasing regulatory requirements. And with their injectable capability, they can offer comprehensive solutions that smaller players cannot match.

Trade Generics: The Blue Ocean

Trade generics only 10% of total generic medicines market (~₹20,000 Cr market size in 2023). If trade generics are only 10% of a ₹20,000 crore market, that's a ₹2,000 crore opportunity with room to grow. As branded generics face pricing pressure and patients become more cost-conscious, trade generics are poised for expansion.

Windlas is well-positioned to capture this growth. Their manufacturing pedigree gives them credibility with doctors. Their focus on quality differentiates them from fly-by-night operators. And their distribution network, built over years, provides reach that new entrants would struggle to replicate.

Regulatory Moats

In pharmaceuticals, regulations aren't just compliance requirements—they're competitive moats. Every certificate, every successful inspection, every regulatory approval makes it harder for new entrants to compete. Windlas's collection of certifications—WHO-GMP, state FDA approvals, USFDA inspection clearance—represents years of investment and expertise that cannot be quickly replicated.

The regulatory landscape is only getting more stringent. Data integrity requirements are increasing. Quality standards are harmonizing globally at the highest levels. Environmental regulations are tightening. Each new requirement raises the bar for competition and favors established players with robust systems.

Differentiation Through Integration

While competitors typically excel in one area—manufacturing or development or distribution—Windlas has integrated across the value chain. They can develop formulations, manufacture at scale, and even distribute through their own network. This integration creates switching costs for clients and provides multiple touchpoints for value creation.

At Windlas Biotech, we offer a comprehensive range of contract manufacturing and research services (CRAMS), customized formulations, and end-to-end pharmaceutical solutions designed to meet the specific needs of our clients. The keyword is "comprehensive"—clients can get everything from one partner, reducing complexity and transaction costs.

X. Playbook: Business & Investing Lessons

Lesson 1: Family Business Succession Done Right

The Windlas story offers a masterclass in family business transition. Windlas Biotech Ltd. has a traditional family business structure where leadership is passed down to the next generation. Ashok Kumar Windlass (70 years old) is the founder of Windlas Biotech and serves as a whole-time director. His sons, Hitesh Windlass (44 years old) and Manoj Windlass (42 years old) serve as Managing Director and Joint Managing Director, respectively.

But this wasn't nepotism—it was planned succession. Both sons were groomed for years, understanding not just the business but the responsibility. They brought complementary skills. They respected the founder's vision while pushing for modernization. Most critically, they professionalized operations while maintaining family values.

Lesson 2: Complexity as a Moat

In commodity businesses, the only differentiation is price, and that's a race to the bottom. Windlas chose a different path. By focusing on complex generics—products requiring special know-how with high barriers to entry—they created defensible positions.

Once you can reliably manufacture a complex fixed-dose combination for diabetes that requires precise release profiles, switching costs become enormous. The client has invested in validating your facility, training your staff on their product, and integrating you into their supply chain. They won't switch to save 2% on costs.

Lesson 3: Capital Efficiency in Capital-Intensive Industries

Pharmaceutical manufacturing is capital-intensive. A single production line can cost crores. The temptation is to leverage aggressively, build capacity ahead of demand, and hope revenue catches up. Many Indian pharmaceutical companies have destroyed value this way.

Windlas took the opposite approach. They grew organically, reinvesting cash flows rather than taking on debt. They built capacity in steps, ensuring utilization before expanding. WINDLAS BIOTECH's cash flow from operating activities (CFO) during FY24 stood at Rs 1 billion, an improvement of 78.6% on a YoY basis. This cash generation funded growth without dilution or dangerous leverage.

Lesson 4: The Trust Premium

In B2B businesses, especially in regulated industries, trust is everything. Windlas understood that reliability was more valuable than being the cheapest option. They invested in quality systems that might have seemed like overkill. They maintained redundancy that looked inefficient. They prioritized on-time delivery over margin optimization.

This trust premium manifests in multiple ways. Clients are willing to pay more for reliability. They're more likely to award new products to trusted partners. They provide better payment terms. Over time, these small advantages compound into sustainable competitive advantages.

Lesson 5: Geographic Arbitrage

Building in Dehradun wasn't just about cost savings—it was about creating a different operating model. Lower costs allowed investment in quality systems. Distance from pharmaceutical hubs reduced employee poaching. Government incentives improved economics. What seemed like a disadvantage became a strategic asset.

Lesson 6: The Portfolio Approach to Growth

Rather than betting everything on one strategy, Windlas built a portfolio. CDMO for stability. Trade generics for margins. Exports for growth. Injectables for the future. This portfolio approach reduced risk while maintaining growth. When CDMO growth slowed, trade generics compensated. When domestic markets saturated, exports provided outlets.

Lesson 7: Public Markets as a Catalyst, Not a Destination

The IPO wasn't an exit—it was a growth enabler. Despite the disappointing listing, Windlas used public market discipline to become stronger. Quarterly reporting imposed planning rigor. Investor scrutiny encouraged strategic clarity. Access to capital markets provided growth fuel. The stock price would follow fundamentals eventually.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Compounding Machine

Leading position in growing CDMO market: The domestic industry is expected to grow between 12-14% per annum for the foreseeable future, a few % points higher than the expected growth rate for domestic formulations at 9-10% CAGR. Windlas isn't just participating in this growth—they're positioned to outgrow it through market share gains and movement up the value chain.

Injectable facility opening new revenue streams: The injectables facility has the potential to generate about 100 Cr INR in revenues at peak utilization with an EBITDA margin profile of 18-20%. This isn't just incremental revenue—it's margin-accretive growth that could transform the company's financial profile.

Strong financial performance and cash generation: Over the past 5 years, WINDLAS BIOTECH net profit has grown at a CAGR of 37.6%. This isn't a story of hope—it's a track record of delivery. The cash generation provides self-funded growth potential without dilution or dangerous leverage.

Expanding institutional business with government support: The Jan Aushadhi program and other government initiatives to improve healthcare access create tailwinds for efficient generic manufacturers. Windlas's cost leadership and quality credentials position them perfectly for this opportunity.

Complex generics portfolio with high barriers to entry: Each complex product in their portfolio represents a mini-monopoly or oligopoly. The technical barriers, regulatory requirements, and switching costs create sustainable competitive advantages that should support pricing power and margins over time.

Bear Case: The Structural Concerns

High concentration in domestic market: More than 95% of Windlas Biotech Ltd's revenues are from India. This concentration exposes them to Indian regulatory changes, pricing pressures, and economic cycles. A single adverse regulatory change could impact the vast majority of their business.

Listed at discount, stock volatility: The stock listed at an 11.6% discount to issue price and has shown significant volatility. This creates challenges in using equity as acquisition currency and might signal underlying concerns that public markets perceive but aren't immediately obvious.

Intense competition in CDMO space: With players like Akums operating at 10x the scale and global giants entering India, competition is intensifying. Price pressure is constant. Client concentration risk remains. One lost major client could significantly impact revenues.

Working capital pressures as business scales: Pharmaceutical manufacturing is working capital intensive. As Windlas scales, working capital requirements grow proportionally. This could pressure cash flows and require external funding, potentially diluting returns.

Regulatory risks in pharma manufacturing: A single FDA warning letter can shut down a facility. A data integrity issue can ban products from key markets. Quality problems can destroy decades of reputation overnight. These aren't theoretical risks—they regularly destroy value in pharmaceutical companies.

The Balanced View

The truth, as always, lies somewhere in between. Windlas has built a solid business with demonstrable competitive advantages. The financial performance has been excellent. The strategic positioning is sound. But the challenges are real—competition is intensifying, regulatory requirements are increasing, and the domestic concentration is concerning.

For investors, the question isn't whether Windlas is a good company—it clearly is. The question is whether it's a good investment at current valuations. Trading at around ₹999 per share versus an IPO price of ₹460, the market has recognized the quality. But with the injectable facility still ramping up and trade generics growth continuing, there might be more upside ahead.

XII. Epilogue & Recent Developments

The Production Power-Up

In 2024-25, it enhanced the production infrastructure with the commissioning of the Plant-2 extension facility. This wasn't just adding capacity—it was strategic expansion. The Plant-2 extension was designed with flexibility in mind, able to handle both large-volume generic products and smaller-batch complex formulations.

The timing was perfect. As the injectable facility was coming online, having additional oral solid capacity meant Windlas could take on new CDMO clients without compromising existing relationships. It's the manufacturing equivalent of adding lanes to a highway before traffic builds up.

The GMP Grand Slam

January 2025 brought validation that every pharmaceutical manufacturer craves: Windlas Biotech has received GMP certification for its new injectable facility from the Uttarakhand Food Safety & Drugs Administration, following an inspection in December 2024. This certification enhances the company's reputation and ability to meet increasing demands for quality injectable products.

With all five manufacturing plants now GMP-compliant, Windlas has achieved something remarkable in Indian pharmaceutical manufacturing—a clean sweep. No regulatory overhangs. No facilities under warning letters. No quality concerns limiting growth. This positions them to capture opportunities that competitors with regulatory issues cannot pursue.

What Success Looks Like in Five Years

If Windlas executes on their strategy, what might 2030 look like?

The injectable facility would be running at full capacity, contributing ₹100 crores in high-margin revenue. The trade generics business would have crossed ₹250 crores, becoming a meaningful profit contributor. Exports would have expanded from 5% to 15-20% of revenues, de-risking the domestic concentration. Total revenues would approach ₹1,500 crores with EBITDA margins in the high teens.

More importantly, Windlas would have evolved from a regional CDMO player to a national champion with global relevance. The company would be a strategic partner to global pharmaceutical companies looking to leverage India's manufacturing advantages. The injectable capability would have opened doors to higher-value products and more sophisticated partnerships.

Key Metrics to Watch

For those tracking Windlas's progress, several metrics will tell the story:

Injectable facility utilization: The ramp-up pace will indicate market acceptance and execution capability. Reaching 50% utilization within two years would be excellent.

Trade generics growth rate: Maintaining 25%+ growth would validate the market opportunity and execution capability. Any slowdown would raise questions about competition or market saturation.

Client concentration: Adding new major CDMO clients while maintaining existing relationships would reduce risk and validate the value proposition. The top five clients should ideally contribute less than 50% of CDMO revenue.

EBITDA margins: Sustained expansion above 15% would confirm the business model's evolution toward higher-value products. Any compression would signal competitive pressure or execution issues.

Export contribution: Growth from 5% to double digits would indicate successful international expansion and risk diversification.

The Windlas Way Forward

As we look at Windlas Biotech today—trading at ₹999 per share, generating over ₹750 crores in revenue, operating five GMP-certified plants—it's easy to forget that this company started with a shuttered facility and a founder's determination. The journey from zero to here wasn't linear. There were setbacks, course corrections, and moments of doubt.

But through it all, certain principles remained constant. Quality over quantity. Trust over transactions. Complexity over commoditization. These principles, embedded in the company's DNA by Ashok Kumar Windlas and carried forward by his sons, have created a business that's both financially successful and strategically positioned for the future.

The pharmaceutical industry will continue evolving. Regulations will tighten. Competition will intensify. Technology will disrupt traditional models. But companies that combine manufacturing excellence with strategic thinking, operational efficiency with innovation, family values with professional management—these companies will not just survive but thrive.

Windlas Biotech's story is far from over. The injectable facility is just beginning to contribute. The trade generics business has room to grow. International markets remain largely untapped. The next chapter—whether it brings continued independence, strategic partnerships, or perhaps even acquisitions—will be shaped by decisions made today.

For investors, Windlas represents a bet on India's pharmaceutical manufacturing capability, on the CDMO industry's consolidation, on the growing demand for quality generic medicines. It's a bet that complexity creates value, that trust generates returns, that patient capital can build lasting businesses.

For the industry, Windlas demonstrates that regional players can compete with national champions, that family businesses can professionalize without losing their soul, that manufacturing excellence remains valuable in an increasingly digital world.

And for anyone studying business strategy, Windlas offers lessons in focus, patience, and execution. In a world obsessed with disruption and overnight success, Windlas built a ₹2,000 crore business through two decades of consistent execution, strategic evolution, and unwavering commitment to quality.

The best businesses aren't always the flashiest. Sometimes they're the ones quietly manufacturing tablets in the Himalayan foothills, building trust one batch at a time, creating value through reliability rather than revolution. That's the Windlas way. And based on the evidence, it works.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube