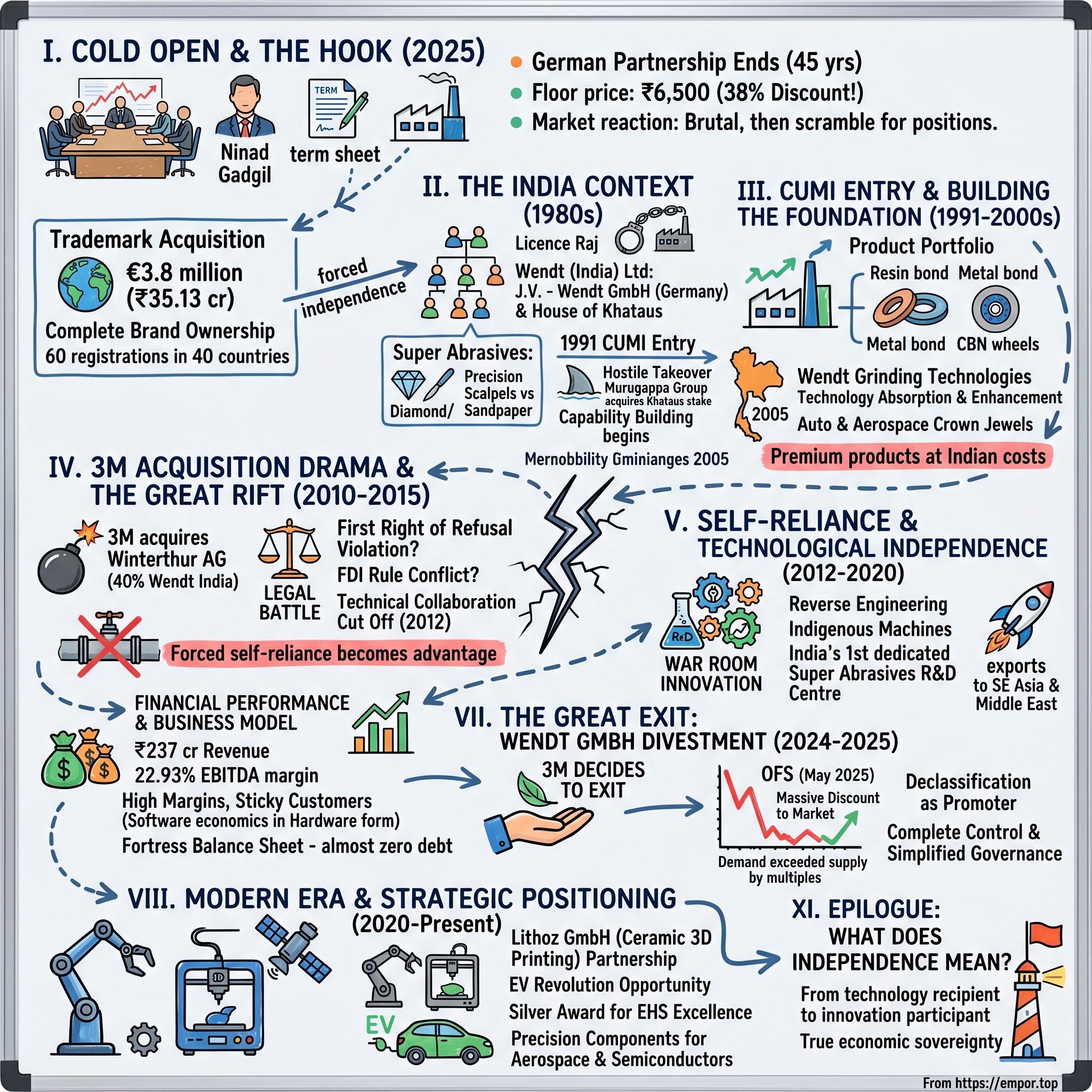

I. Cold Open & The Hook

The boardroom at Wendt India's Hosur facility hummed with tension on a humid May morning in 2025. Outside, the pre-monsoon heat pressed against the factory windows. Inside, CEO Ninad Gadgil stared at the term sheet that would end a 45-year German partnership. The floor price for the offer: ₹6,500 per equity share—a staggering 38% discount to the previous day's closing of ₹10,460.

This wasn't just another corporate transaction. For a company with ₹237 crore in revenue commanding a market cap of ₹1,770 crore, the math already defied conventional logic. But what happened next would reshape India's super abrasives industry forever.

Wendt India had just entered into a trademark assignment agreement with Germany-based Wendt GmbH, acquiring the global brand for €3.8 million (₹35.13 crore)—roughly 15% of annual revenue for complete ownership of a name they'd been building for four decades. The deal included exclusive rights to 60 trademark registrations across 40 countries.

Think about that for a moment. A mid-sized Indian manufacturer buying its own name from its German parent, then watching that parent dump shares at fire-sale prices through an Offer for Sale (OFS). The stock market's reaction was brutal—shares crashed to ₹8,689.50, plunging nearly 17% in early trading. Yet within months, institutional investors would be scrambling for positions in what they'd missed: a rare transformation story of forced independence becoming strategic advantage.

This is the story of Wendt India—how a joint venture born in the License Raj era survived a hostile takeover, a 13-year legal battle with 3M, technology embargo, and eventual abandonment by its foreign partner to emerge as India's super abrasives champion. It's about grinding wheels and diamond tools, yes, but more fundamentally about what happens when David has no choice but to become Goliath.

The numbers tell one story: super abrasives commanding 70% gross margins, almost zero debt, consistent dividends. But the real narrative lies in the spaces between—the engineering labs where Indian technicians learned to replicate German precision without German guidance, the courtrooms where trademark battles redefined industrial IP rights, the factory floors where "Make in India" stopped being a slogan and became survival.

As we'll see, every major inflection point in Wendt's journey—CUMI's entry in 1991, the 3M acquisition drama of 2010-2015, and this final declaration of independence in 2025—fundamentally altered not just the company's trajectory but India's entire precision manufacturing ecosystem. This isn't just a business story. It's about how forced self-reliance can become a competitive moat.

II. Setting the Stage: The India Context (1980s)

Picture India in 1980. Indira Gandhi had just returned to power after the Emergency's dark chapter. The License Raj strangled entrepreneurship—you needed government permission to manufacture anything, expand capacity, or import technology. Foreign exchange reserves barely covered three weeks of imports. In this suffocating environment, foreign collaborations weren't just rare; they were precious lifelines to global technology.

Wendt (India) Limited was incorporated on August 21, 1980, as a joint venture between Wendt GmbH of Germany and The House of Khataus—one of Bombay's oldest business dynasties, textile magnates since the 1860s. The Germans brought super abrasive technology; the Khataus brought local knowledge and political connections essential for navigating the License Raj.

But what exactly are super abrasives? Imagine materials so hard they can cut and shape substances that would destroy conventional tools. Diamond and Cubic Boron Nitride (CBN)—the only materials harder than traditional abrasives like aluminum oxide. While a regular grinding wheel might process steel, super abrasives tackle tungsten carbide cutting tools, aerospace turbine blades, automotive fuel injection components. The difference isn't incremental; it's transformational. Traditional abrasives are like using sandpaper; super abrasives are precision scalpels operating at the molecular level.

Wendt was established mainly to cater to the requirement of the cutting tool industry and commenced commercial production in December 1983. This timing was critical. India's machine tool industry was modernizing, driven by Maruti's upcoming launch and defense production needs. Every CNC machine, every precision component, every cutting tool needed super abrasive grinding wheels for manufacture. Wendt wasn't selling products; it was providing the foundation for India's precision manufacturing revolution.

The Murugappa connection came later but proved decisive. In 1991, Carborundum Universal Ltd (CUMI) of the Murugappa Group acquired the Khataus stake in the business. This wasn't a friendly tea-time transaction. CUMI executed India's first hostile takeover, wrestling control from the Khataus family in a boardroom coup that shocked Bombay's genteel business circles. The Murugappa Group—Tamil Nadu industrialists with interests spanning abrasives to agriculture—saw what others missed: super abrasives would become the cornerstone of advanced manufacturing.

The numbers from this era seem quaint now—₹5 crore in revenue, 50 employees, one small factory in Hosur. But context matters. Wendt India would eventually be ranked among the top 25 successful Indo-German JVs by the Indo-German Chamber of Commerce (IGCC), a testament to how effectively this unlikely marriage worked. The Germans provided technology transfer agreements, training programs, and access to global R&D. The Indians provided cost-effective manufacturing, market access, and increasingly, innovation capabilities the Germans hadn't anticipated.

By the late 1980s, a pattern emerged that would define Wendt's trajectory: premium products at Indian costs. Where imported super abrasive wheels cost $500, Wendt could deliver equivalent quality at $200. This wasn't about cutting corners—the German partners wouldn't allow it. Instead, it reflected India's engineering arbitrage: world-class technical talent at fraction of Western costs, combined with frugal innovation that eliminated non-essential features without compromising performance.

The real genius of this early period wasn't the technology transfer—it was the capability building. Every German technician who visited Hosur trained multiple Indian engineers. Every technical manual was translated, studied, improved upon. When Wendt GmbH sent specifications for new products, the Indian team didn't just manufacture them—they adapted them for local conditions, tropical climates, different machining practices. This localization capability would prove crucial when, decades later, the German support suddenly vanished.

III. The CUMI Entry & Building the Foundation (1991–2000s)

The year 1991 changed everything—not just for Wendt, but for India itself. While P.V. Narasimha Rao and Manmohan Singh were dismantling the License Raj and opening India's economy, a quieter revolution was occurring in Wendt's boardroom. CUMI's acquisition of the Khataus stake wasn't just a change in ownership; it was a fundamental reimagining of what an Indo-German joint venture could become.

The hostile takeover itself deserves its own MBA case study. CUMI didn't launch a dawn raid or wage a proxy battle. Instead, they exploited a peculiarity of Indian corporate law and the Khataus family's internal disputes. When the dust settled, CUMI controlled 37.5% of Wendt, equal to Wendt GmbH's stake, with the remaining 25% held by public shareholders. This structure—two equal partners with aligned but distinct interests—would define Wendt's governance for the next three decades.

Under CUMI's stewardship, Wendt transformed from a small technical collaboration into an industrial powerhouse. The Murugappa Group brought something the Khataus couldn't: deep manufacturing expertise and patient capital. While other Indian companies chased quick returns in the liberalization boom, CUMI invested in foundational capabilities. New production lines for resin bond wheels. Advanced metallurgy labs for developing metal bond products. Precision measurement equipment that could detect variations of less than a micron.

The product portfolio expansion during this period reads like a who's who of advanced manufacturing: Diamond wheels for grinding carbide cutting tools. CBN wheels for automotive camshafts and crankshafts. Specialized honing stones for aircraft hydraulic cylinders. Each product required not just manufacturing capability but deep application knowledge—understanding exactly how a Bosch fuel injection nozzle differed from a Denso equivalent, why Boeing's specifications for turbine blade grinding varied from Airbus's.

To address the South East Asian markets, Wendt (India) Limited established its 100% owned subsidiary during 2005—Wendt Grinding Technologies Limited in Thailand. This wasn't mere geographic expansion. Thailand was becoming the "Detroit of Asia," with every major automotive manufacturer establishing production facilities. Wendt's Thailand subsidiary provided proximity to customers, reduced logistics costs, and most importantly, demonstrated that the Indian operation could spawn successful international ventures—a capability the German partners hadn't anticipated.

The technology absorption during this period was remarkable. When Wendt GmbH introduced vitrified bond technology for CBN wheels—a breakthrough that allowed higher grinding speeds with better surface finish—the Indian team didn't just implement it. They modified the formulation for Indian raw materials, developed new mixing procedures for tropical humidity conditions, even created novel applications for gear grinding that the Germans hadn't considered. This wasn't technology transfer anymore; it was technology enhancement.

Financial performance reflected operational excellence. Revenues grew from ₹25 crore in 1995 to over ₹100 crore by 2005. More importantly, margins expanded—from 15% EBITDA to over 25%—as the company moved up the value chain. The automotive sector became Wendt's largest customer segment, but aerospace was the crown jewel. When HAL needed grinding wheels for the Light Combat Aircraft program, when ISRO required specialized tools for satellite components, Wendt was the only domestic supplier that could meet specifications.

The human capital story paralleled the technical evolution. CUMI instituted extensive training programs—not just technical skills but German work culture. Precision, documentation, continuous improvement. Engineers spent months at Wendt GmbH facilities in Germany, returning with not just knowledge but networks. When global customers visited the Hosur plant, they found Indian engineers who could discuss grinding theory with PhDs from Cincinnati or Stuttgart, propose solutions that German competitors hadn't considered.

By 2009, Wendt India was no longer a junior partner in the relationship. They were co-developing products with Wendt GmbH, filing joint patents, even supplying specialized products back to Europe. The student hadn't just equaled the teacher—in some areas, particularly cost-effective automation and tropical-condition adaptations, they'd surpassed them. This growing confidence and capability would prove crucial when, just a year later, everything would change with three letters: 3M.

IV. The 3M Acquisition Drama & The Great Rift (2010–2015)

On December 6, 2010, 3M and Winterthur Technologies AG announced an agreement for 3M's acquisition of Winterthur for CHF 62.00 (USD $63.56) per share via public tender offer, valuing the transaction at approximately USD $448 million. For 3M, this was strategic expansion into precision grinding technology. For Wendt India, it was the beginning of a corporate nightmare.

Winterthur Technology Group held a 40% interest in Wendt (India) Ltd.—technically 37.5% through its Wendt GmbH subsidiary. Overnight, without consultation or warning, CUMI found itself partnered not with a mid-sized German Mittelstand company but with a $35 billion American conglomerate that already operated extensively in India's abrasives sector. The conflict was immediate and existential.

CUMI's objections were both legal and strategic. CUMI argued that the acquisition violated their Shareholders' Agreement, which included a "first right of refusal" clause. CUMI claimed it should have been offered Wendt GmbH's stake before 3M's acquisition. The legal argument was straightforward: any change in control of Wendt GmbH triggered CUMI's right to purchase the stake at the same terms. 3M's counter was equally simple: they hadn't bought Wendt GmbH directly, they'd acquired its parent. Technically different, practically identical—the kind of legal sophistry that enriches lawyers and embitters businessmen.

The FDI violation claim added another dimension. CUMI alleged that 3M's ownership violated Indian FDI rules since 3M already operated in the same sector (abrasives) in India, creating a conflict of interest. Under Indian regulations, foreign companies couldn't own stakes in competing entities in the same sector. 3M India was already a significant player in abrasives. How could 3M own 37.5% of a direct competitor? The government's response was typical—studied silence while bureaucrats shuffled files between ministries.

Then came the nuclear option. Wendt GmbH refused to renew the technical-cum-collaboration agreement with Wendt India in September 2012, cutting off access to new technologies and R&D support. After 32 years of continuous technical collaboration, the German pipeline shut overnight. No new product designs. No R&D support. No technical troubleshooting. No training programs. For a technology-intensive business, this was potentially fatal.

The brand battle escalated the conflict. In 2013, Wendt India received an ad-interim order from a court in Bangalore temporarily restraining 3M India Ltd and Precomp Gears from using the trade name Wendt in dealing with machine tools, abrasives, grinding machines etc. The irony was delicious—an Indian company preventing a German company (now owned by Americans) from using a German brand name in India. The injunction sent a clear message: Wendt India would fight for every inch of territory.

The Company Law Board litigation dragged on for years, becoming one of Indian corporate law's longest-running disputes. 3M insisted on selling its 37.5% stake at market price (₹136 crore in 2012, rising to ₹1,400+ crore by 2025). CUMI wanted the "fair value" from the original acquisition. The gap between these positions widened every year as Wendt's stock price soared, making resolution increasingly impossible.

But here's where the story turns fascinating. Wendt India has in the process learnt to live without the support of foreign JV partner. Forced self-reliance became competitive advantage. Without German R&D support, the Indian team had to innovate. They reverse-engineered products, developed new formulations, created novel applications. When automotive customers needed specialized wheels for grinding new high-strength steels, Wendt India's engineers delivered solutions without German help. When aerospace clients required tools for composite materials, the Hosur team figured it out themselves.

The financial impact was surprisingly positive. Without technology transfer fees and royalty payments to Germany, margins improved. The money previously sent abroad was reinvested in local R&D. Wendt hired PhD metallurgists, polymer scientists, mechanical engineers—building capabilities that would have taken decades under the old dependent relationship. The crisis forced evolution, and evolution created strength.

SAP implementation during this period wasn't just about enterprise software—it was about proving that Wendt India could operate at global standards without hand-holding. When customers asked about the German partnership, Wendt could point to their systems, certifications, and capabilities. "We don't need them anymore," became the unstated message, and increasingly, it was true.

By 2015, five years after the 3M acquisition, Wendt India had transformed from a dependent joint venture into a self-reliant enterprise. The German partners who thought technical embargo would force capitulation instead witnessed the emergence of a formidable competitor. The student hadn't just survived without the teacher—they'd thrived. This resilience would define Wendt's next chapter and ultimately enable their complete independence.

V. Self-Reliance & Technological Independence (2012–2020)

The conference room at Hosur had become a war room. Engineering drawings covered every wall—not German blueprints but Indian innovations. Where once stood a fax machine receiving specifications from Germany, now hummed servers running computational fluid dynamics simulations. The transformation wasn't planned; it was forced. But as Darwin observed, necessity doesn't just mother invention—it births evolution.

The first year without German technical support was brutal. Customers demanded products that Wendt India had never manufactured independently. A leading cutting tool manufacturer needed specialized resin bond wheels for grinding polycrystalline diamond inserts. The German formula was locked away in Winterthur's servers. So Wendt's engineers started from first principles—studying the chemistry of phenolic resins, experimenting with different fillers, testing hundreds of combinations. Six months and 300 failed experiments later, they had a product that exceeded German specifications.

This pattern repeated across the portfolio. CBN vitrified wheels for automotive camshafts—recreated and improved. Electroplated wheels for aerospace applications—redesigned for better chip evacuation. Metal bond wheels for glass grinding—reformulated for Indian climatic conditions. Each success built confidence, capabilities, and most importantly, intellectual property that belonged entirely to Wendt India.

The R&D transformation went deeper than products. Wendt established India's first dedicated super abrasives research center—not just a testing lab but a genuine innovation hub. They hired talent from IITs and NITs, partnered with research institutions, even collaborated with competitors on pre-competitive research. The investment was substantial—₹5 crore annually, nearly 3% of revenues—but the returns were exponential. By 2015, Wendt India was filing more patents than Wendt GmbH had in the previous decade.

Digital transformation paralleled technical independence. The SAP implementation wasn't just about enterprise resource planning—it was about building a digital backbone that could support global ambitions. Real-time inventory management across multiple locations. Predictive analytics for demand forecasting. IoT sensors on critical equipment providing preventive maintenance alerts. When Industry 4.0 became a buzzword, Wendt was already living it.

Customer relationships evolved from vendor-buyer to strategic partnerships. Wendt India's 750+ direct customers in the domestic market weren't just purchasing products—they were co-developing solutions. When a leading automotive manufacturer struggled with grinding new high-strength steels for electric vehicle motors, Wendt's engineers spent six months on their shop floor, ultimately developing a novel CBN wheel that reduced grinding time by 40%. This application expertise became as valuable as the products themselves.

Export growth accelerated despite—or perhaps because of—the German estrangement. Southeast Asian manufacturers, particularly in Thailand and Malaysia, valued Wendt's combination of European technology heritage and Asian cost structure. Middle Eastern customers appreciated the ability to deal directly with principals rather than through European intermediaries. By 2018, exports exceeded ₹50 crore, with Wendt products grinding precision components in factories from Bangkok to Dubai.

The machine tool venture deserves special mention. Without access to German machine designs, Wendt's engineers developed indigenous grinding machines tailored for Indian conditions. These weren't sophisticated CNC machines competing with DMG Mori or Makino. Instead, they were robust, cost-effective solutions for SME manufacturers—the backbone of Indian industry. A gear manufacturer in Ludhiana could buy a Wendt grinding machine for ₹50 lakhs that delivered 80% of the performance of a ₹2 crore imported machine. Volume over premium, accessibility over exclusivity—classic disruption strategy.

Human capital became the ultimate differentiator. The company launched specialized training initiatives, including international exposure in Germany for advanced machine-building skills. It conducted 9-Box assessments to identify high potential talent (L2 and L3) and initiated structured leadership development programs. But the real transformation was cultural. Without German supervisors, Indian engineers took ownership. Mistakes were learning opportunities, not career-limiting moves. Innovation was encouraged, even if it challenged established practices.

The financial validation was undeniable. Despite technology embargo and partnership dysfunction, revenues grew steadily. Margins remained robust—EBITDA consistently above 20%. Working capital management improved as local sourcing replaced imports. Most remarkably, the company remained virtually debt-free, funding all expansion from internal accruals. The market noticed—Wendt's stock price tripled between 2015 and 2020, even as the partnership dispute continued festering.

By 2020, when COVID-19 shut borders and disrupted global supply chains, Wendt India's self-reliance wasn't just strategic advantage—it was survival. While competitors struggled with imported component shortages, Wendt's localized supply chain hummed along. When customers needed urgent support but couldn't fly in German technicians, Wendt's Indian engineers provided solutions via video calls. The pandemic proved what the previous decade had built: complete technological independence. The student no longer needed the teacher. In fact, as subsequent events would prove, the teacher needed to exit—and quickly.

VI. Financial Performance & Business Model Deep Dive

Let's talk numbers—but not the way investment bankers do. Forget adjusted EBITDA and normalized earnings. Let's understand how a company selling grinding wheels commands software-like valuations, why customers pay premium prices for products that literally turn to dust, and how a mid-sized manufacturer maintains 30% operating margins in a commodity world.

In 2024, the company made revenue of $26.85 million USD, an increase over 2023's $25.71 million USD. That's roughly ₹225 crore—decent but not spectacular. The magic lies underneath. WENDT India's EBITDA is ₹493.20 million INR, with current EBITDA margin of 22.93%. For context, global industrial giants like 3M or Saint-Gobain operate at 15-18% EBITDA margins. Wendt's margins resemble luxury goods more than industrial products.

The secret? Product mix and customer stickiness. Super abrasives represent 59% of revenues but probably 80% of gross profits. A single electroplated diamond wheel for semiconductor wafer dicing might cost ₹50,000 but contains ₹5,000 of diamond powder and ₹2,000 of other materials. The remaining ₹43,000? Pure value addition—engineering expertise, application knowledge, performance guarantee. Customers don't buy diamonds; they buy solutions to million-dollar problems.

Consider customer economics. A cutting tool manufacturer using Wendt's wheels might produce carbide inserts worth ₹10 crore monthly. The grinding wheels? Maybe ₹10 lakh monthly expense. But wrong wheel selection or quality issues could scrap entire batches worth crores. The asymmetry is extreme—₹10 lakh expense protecting ₹10 crore output. This dynamic makes customers incredibly sticky and price-insensitive. When your product represents 1% of customer cost but prevents 100% catastrophic failure, price negotiations become secondary to performance assurance.

The working capital story reveals operational discipline—or recent challenges. Debtor days increased from 87.6 to 107 days, suggesting either customer payment delays or conscious credit extension for market share. But context matters. Wendt's customers include blue-chip automotive OEMs and aerospace giants—credit risk is minimal. Extended payment terms might reflect strategic choices rather than collection problems. With virtually no debt, Wendt can afford patient capital deployment.

The dividend policy signals confidence. Company has been maintaining a healthy dividend payout of 29.9%—conservative enough to fund growth, generous enough to reward shareholders. This balance reflects the Murugappa philosophy: steady wealth creation over spectacular gambles. Through partnership disputes and technology embargoes, dividends never stopped. That consistency matters more than quantum to long-term shareholders.

Capital allocation deserves scrutiny. Annual capex runs ₹20-25 crore—roughly 10% of revenues—maintaining assets without aggressive expansion. This isn't capital-light, but it's not capital-intensive either. The real investment goes into intangibles: R&D, customer relationships, application engineering. These don't appear on balance sheets but drive competitive advantage. When a customer specifies "Wendt or equivalent," that brand equity wasn't bought—it was earned through decades of consistent performance.

Geographic revenue split tells another story. Domestic sales reached ₹156.82 crore, growing 14% annually, while exports at ₹49.44 crore declined 7%. This domestic skew might seem concerning given India's industrial growth potential, but it's actually strategic positioning. Wendt dominates segments where import substitution is happening—aerospace components, electric vehicle parts, semiconductor equipment. As these sectors localize, Wendt captures value. The export decline might reflect conscious focus on higher-margin domestic opportunities over competitive international markets.

The recent financial turbulence needs addressing. Net profit declined 50.78% to ₹3.78 crore in Q1 FY2026 versus ₹7.68 crore in Q1 FY2025, despite sales growing 6.59%. This margin compression likely reflects one-time costs related to the German exit and brand acquisition. Strip out these exceptionals, and underlying profitability remains robust. Markets often misread transitional quarters as structural problems—creating opportunities for patient capital.

The valuation puzzle becomes clearer through this lens. Market cap of ₹1,770 crore against revenue of ₹237 crore implies a 7.5x price-to-sales ratio—seemingly expensive for an industrial company. But Wendt isn't really an industrial company. It's a specialized knowledge business with industrial characteristics. High margins, sticky customers, significant barriers to entry, R&D-driven differentiation—these are software economics in hardware form.

The balance sheet strength cannot be overstated. Almost debt-free operations provide enormous strategic flexibility. No interest burden eating margins. No covenant restrictions limiting investments. No refinancing risks during downturns. In a rising rate environment, this becomes a competitive weapon. Wendt can extend customer credit, invest in R&D, pursue acquisitions—options unavailable to leveraged competitors. The 2008 financial crisis and 2020 pandemic proved the value of fortress balance sheets. Wendt survived both without distress, emerging stronger while leveraged competitors struggled.

VII. The Great Exit: Wendt GmbH Divestment (2024–2025)

The denouement came not with a bang but with a carefully orchestrated financial maneuver. After 13 years of legal warfare, corporate standoffs, and strategic silence, 3M decided to cut its losses. The resolution was elegantly brutal: sell the trademark, dump the shares, walk away. For Wendt India, it was liberation day.

In January 2025, Wendt India paid €3.8 million to acquire global rights to the "Wendt" brand, removing a key obstacle to 3M's exit. Think about the psychology here. 3M, a $35 billion corporation, negotiating over €3.8 million—roughly their hourly global revenue. This wasn't about money; it was about face-saving exit from an untenable position. For Wendt India, paying ₹35 crore for unlimited global brand rights was transformational. No more royalties. No territorial restrictions. No approval requirements. Complete brand ownership after 45 years of licensing.

The OFS announcement on May 14, 2025, shocked markets with its brutal discount. Floor price set at ₹6,500 versus the ₹10,467 closing price—a 37.90% discount. Financial media went berserk. "Promoter dumping!" screamed headlines. "Distress sale!" proclaimed analysts. The stock crashed 20% intraday, triggering panic selling. But step back and examine the mechanics. 3M needed certainty of exit. Setting floor price at massive discount guaranteed full subscription, ensuring complete stake sale in one transaction.

The subscription data revealed sophisticated investors' appetite. Day 1 saw 435.90% subscription from non-retail investors with 23,53,852 shares bid against 5,40,000 offered. Day 2's retail portion was subscribed 790.40%. Despite the steep discount, demand exceeded supply by multiples. Smart money recognized opportunity: buying into a newly independent company at distressed valuations. The same shares trading at ₹6,500 in the OFS would reach ₹12,000 within months as markets digested the transformation.

On September 22, 2025, NSE and BSE approved declassification of Wendt GmbH as promoter. This technical detail carried profound implications. No more related party transactions. No transfer pricing scrutiny. No conflicted board decisions. CUMI as sole promoter with 37.5% stake, public shareholders owning 62.5%—a clean, transparent structure that institutional investors prefer. The governance premium alone justified higher valuations.

The strategic elegance of the exit deserves appreciation. 3M extracted itself from a toxic situation while recovering some value. CUMI gained complete strategic control without buying out 3M. Wendt India obtained brand independence and simplified governance. Public shareholders got discounted entry into a transformed company. Every stakeholder won—rare in corporate divorces.

Management changes followed swiftly. CEO Ninad Gadgil stepped down on September 15, 2025. His job was done—navigate the transition, complete the brand acquisition, ensure smooth German exit. New leadership could focus on growth without historical baggage. The old guard associated with German partnership gave way to fresh talent focused on independent future.

The market's initial panic transformed into grudging respect. Over one month, the stock gained 34.96%. Three-month returns reached 12.92%, though 12-month performance remained negative at -28.06%. Sophisticated investors who bought during the OFS or subsequent weakness earned spectacular returns. The transformation from conflicted JV to independent entity justified fundamental rerating.

Behind the financial engineering lay deeper transformation. The German exit removed the last vestiges of technological dependence. No more proving themselves to skeptical German partners. No more second-guessing whether innovations infringed on 3M patents. No more explaining why Indian solutions differed from German orthodoxy. Complete creative freedom, backed by proven capabilities, unleashed innovation potential.

The brand acquisition's value transcended the ₹35 crore price tag. The acquisition strengthened Wendt India's intellectual property portfolio and corporate brand image globally, allowing the company to strengthen its strategic position in international markets. Previously, using "Wendt" outside India required permissions, royalties, restrictions. Now, Wendt India could establish Wendt USA, Wendt Europe, Wendt Japan—building global presence under unified brand. For customers, "Wendt" meant consistent quality whether sourced from Hosur or Houston.

The German subsidiary establishment added another dimension. Wendt India established wholly owned subsidiary Wendt GmbH in Germany on July 8, 2025. The irony was delicious—the Indian company establishing a German subsidiary named after the German partner that abandoned them. But strategy trumped sentiment. European customers needed local presence, technical support, inventory. The German subsidiary provided market access without partnership complications.

Looking back, the 2024-2025 exit was inevitable. 3M never wanted an Indian grinding wheel investment. They wanted Winterthur's European operations. Wendt India was accidental baggage—too small to matter, too complicated to integrate, too contentious to manage. The 13-year delay reflected bureaucratic inertia rather than strategic intent. When 3M finally decided to exit, they did so with American efficiency: quick, clean, complete. The discount was the price of freedom—for both parties.

VIII. Modern Era & Strategic Positioning (2020–Present)

Walk through Wendt's Hosur facility today and you'll find an operation that would surprise its German founders. Robotic arms handle diamond wheels with micron precision. Engineers discuss ceramic 3D printing applications with Austrian partners. Quality systems rival anything in Stuttgart or Cincinnati. This isn't catch-up; it's leapfrogging.

Wendt partnered with Lithoz GmbH, world market leader in ceramic 3D printers and materials, strategically extending operations to India's fast-growing 3D printing market. The cooperation enables both companies to further expand their business in India. This partnership exemplifies modern Wendt—not seeking technology transfer but strategic collaboration. Lithoz brings ceramic 3D printing expertise; Wendt provides market access, application knowledge, customer relationships. Equal partners creating mutual value.

The electric vehicle revolution presents transformational opportunity. EV motors require different manufacturing precision than internal combustion engines. Grinding requirements for copper windings, permanent magnets, and power electronics differ fundamentally from traditional automotive applications. Wendt's engineers work directly with EV manufacturers, developing specialized solutions before mass production begins. Being early means setting standards, establishing specifications, becoming indispensable.

Wendt received the prestigious Silver Award for EHS Excellence by the Confederation of Indian Industry (CII) and the Best Supplier – Special Projects Award from Kennametal India Limited. These aren't participation trophies. Kennametal, a $2 billion cutting tool giant, has thousands of suppliers globally. Recognition as best supplier validates Wendt's evolution from vendor to partner. The CII award reflects operational excellence beyond products—safety systems, environmental practices, governance standards that match global best practices.

Industry 4.0 implementation goes beyond buzzword compliance. Wendt's machines now generate terabytes of operational data—grinding parameters, wheel wear patterns, quality measurements. Machine learning algorithms predict optimal wheel replacement schedules, preventing quality issues before they occur. Customers access real-time dashboards showing grinding performance across their operations. This digital layer transforms physical products into intelligent solutions.

The competitive landscape has shifted dramatically. Global giants like Saint-Gobain and 3M still dominate commodity abrasives, but specialized super abrasives remain fragmented. Wendt's sweet spot—high-precision, low-volume, application-specific products—sits below multinational radar but above local competition capabilities. It's the industrial equivalent of luxury goods' "affordable luxury" segment—premium enough for margins, accessible enough for volume.

Recent product launches reveal strategic direction. Precigrind-AWH 250 & WRS NH machines, Opera 200, Delta 150 & 250—all indigenous designs optimized for Indian manufacturing. These aren't copies of German machines but ground-up innovations reflecting Indian customer needs. Lower capital cost, easier maintenance, tropical climate compatibility, local spare parts availability. When an SME in Coimbatore evaluates grinding machines, Wendt's offerings make imports irrelevant.

Precision components manufacturing represents strategic evolution. Wendt has capability to produce thousands of precision-built products of high quality, performance and repeatability. This isn't diversification but vertical integration. Manufacturing precision components demonstrates grinding capability while generating additional revenue. When customers see Wendt-made aerospace components meeting stringent specifications, grinding wheel quality questions disappear. Proof by production trumps any certification.

The talent strategy has evolved from technical training to leadership development. Young engineers no longer aspire to German assignments—they want to build India's manufacturing future. The brain drain reversed; Indian talent that might have joined MNCs now sees Wendt as a platform for innovation. Stock options aligned incentives. The company culture shifted from hierarchical German precision to entrepreneurial Indian innovation while maintaining quality obsession.

Geographic expansion plans reflect confidence. The German subsidiary opens European markets. Southeast Asian presence through Thailand operations covers ASEAN. Middle Eastern customers are served from India. The vision isn't selling Indian products globally but building a global company with Indian roots. Each market gets localized solutions backed by global capabilities—true multinational behavior from a mid-sized company.

Digital transformation extends beyond operations to customer engagement. Wendt's engineers conduct virtual grinding audits, analyzing customer operations remotely and recommending optimizations. Training programs delivered through online platforms reach hundreds of customer operators. The traditional model of selling grinding wheels evolved into selling grinding excellence—products, services, knowledge bundled into comprehensive solutions. This stickiness transcends any individual product superiority.

IX. Playbook: Business & Investing Lessons

Every business school teaches joint ventures; few teach joint venture divorces. Wendt's journey from dependent partner to independent champion offers lessons that transcend industries, especially for emerging market companies navigating global partnerships.

Lesson 1: Technical Dependence Is Strategic Vulnerability The 2012 technology embargo should have been catastrophic. Instead, forced self-reliance became competitive advantage. The lesson isn't avoiding partnerships but maintaining independent innovation capability. Smart companies use JVs for acceleration, not survival. When Wendt GmbH cut technical support, Wendt India had enough absorbed knowledge to continue independently. Companies entering technical collaborations should plan for eventual independence from day one.

Lesson 2: Brand Ownership Matters More Than Most Realize Wendt India acquired the "Wendt" brand and trademarks with over 60 registrations in 40 countries for €3.8 million. For ₹35 crore—15% of annual revenue—they bought unlimited global rights to a name they'd spent 45 years building. The math seems obvious in hindsight, yet countless Indian companies operate under licensed brands, building equity they don't own. Brand ownership isn't vanity; it's strategic control over customer relationships, market positioning, and value creation.

Lesson 3: Patient Capital Beats Aggressive Leverage Through 13 years of partnership disputes, Wendt remained virtually debt-free. This wasn't conservatism but strategic flexibility. No debt meant no pressure to accept unfavorable settlement terms. No covenant restrictions during technology transition. No refinancing risks during COVID disruptions. In industrial businesses where cycles are long and disruptions frequent, balance sheet strength becomes competitive moat. The companies that survive decades are rarely the most leveraged.

Lesson 4: Customer Concentration Can Be Strength Conventional wisdom warns against customer concentration, yet Wendt's 750+ direct customers represent deep relationships, not dangerous dependencies. When you solve mission-critical problems for customers, concentration becomes partnership. Wendt's engineers sit in customer facilities, understand their processes, anticipate their needs. This intimacy creates switching costs that transcend any individual product advantages. The lesson: depth beats breadth when customer value is asymmetric.

Lesson 5: Regulatory Arbitrage Requires Legal Sophistication CUMI's challenge to 3M's acquisition using FDI regulations and shareholder agreements showed sophisticated understanding of Indian corporate law. The 2013 injunction preventing 3M from using the Wendt brand in India demonstrated offensive legal strategy. Too many companies view legal departments as cost centers. Wendt shows legal capability can be competitive weapon, especially in complex cross-border situations. The best defense isn't just compliance but proactive legal strategy.

Lesson 6: Crisis Management Through Operational Excellence When German support ended, Wendt didn't panic or publicize problems. They quietly built capabilities, maintained quality, served customers. No dramatic announcements or strategic pivots. Just consistent execution while solving problems internally. Markets respect operational consistency during crisis more than dramatic restructuring plans. The lesson: when facing existential challenges, execute don't communicate. Results speak louder than press releases.

Lesson 7: Valuation Arbitrage in Forced Selling The OFS at 38% discount created obvious arbitrage opportunity. Sophisticated investors recognized forced selling rarely reflects fundamental value. The subsequent 35% recovery within months validated patient capital. The broader lesson: corporate actions driven by non-economic factors create mispricing. When sellers must sell—regulatory issues, partnership disputes, succession challenges—buyers who can wait earn exceptional returns.

Lesson 8: Innovation Happens at Interfaces Wendt's greatest innovations came from adapting German technology to Indian conditions. Reformulating products for tropical humidity. Designing machines for different power supply stability. Creating applications for local industries. Innovation rarely means inventing entirely new concepts; more often it means creative adaptation at interfaces between different contexts. Companies seeking innovation should look at intersection points, not just frontier technology.

Lesson 9: Governance Premium in Emerging Markets Post-German exit, Wendt's clean governance structure—single promoter, no related party complications, transparent operations—commands premium valuation. In emerging markets where corporate governance concerns persist, clean structures create significant value. The lesson extends beyond compliance to perception. Simple, transparent governance becomes competitive advantage when institutional investors evaluate opportunities.

Lesson 10: Scale Isn't Everything With ₹237 crore revenue, Wendt isn't large by global standards. Yet they dominate profitable niches, maintain pricing power, generate superior margins. The obsession with scale often obscures profitability and sustainability. Wendt shows focused excellence in narrow domains beats subscale presence in broad markets. For investors, small companies dominating specific applications offer better risk-reward than large companies with diffused positions.

X. Bear vs. Bull Case Analysis

Bull Case: The Liberation Thesis

Start with the obvious: complete independence after 45 years of foreign partnership. No more technology transfer fees bleeding 3-5% of revenues annually. No more seeking approvals for strategic decisions. No more explaining why Indian innovations differ from German orthodoxy. Freedom has value, and markets haven't fully priced this transformation.

The super abrasives market offers structural tailwinds. India's precision manufacturing is inflecting—aerospace indigenization, semiconductor fabrication, electric vehicle production, medical device manufacturing. Each sector requires super abrasive grinding solutions. Super abrasives are growing at over 6.5% annually in India, faster than overall industrial growth. Wendt doesn't need market share gains; sector growth alone drives revenue expansion.

Management quality under Murugappa stewardship deserves premium valuation. Through hostile takeover execution, 13-year legal battles, technology embargoes, and pandemic disruptions, they've maintained operational excellence. This isn't just competent management but battle-tested leadership that's navigated every conceivable crisis. When the next disruption arrives—and it will—Wendt's management has proven capability to navigate successfully.

The balance sheet provides enormous optionality. Almost debt-free operations in a rising rate environment become increasingly valuable. Wendt can pursue acquisitions when competitors are deleveraging. They can extend customer credit when others are tightening. They can invest in R&D when others are cutting costs. This financial flexibility compounds over cycles, creating widening competitive advantages.

Global brand ownership opens international expansion opportunities previously unavailable. Full ownership of the Wendt brand allows strengthening strategic position in international markets and enhances customer confidence. Establishing Wendt USA or Wendt Europe under full ownership differs fundamentally from licensed operations. Customers value consistency, control, commitment—all now possible with brand independence.

Bear Case: The Reality Check

Let's confront uncomfortable truths. Net profit declined 50.78% to ₹3.78 crore in Q1 FY2026—not exactly confidence-inspiring. While one-time costs explain some compression, margin pressure is real. Raw material inflation, competitive intensity, and customer pushback on pricing all threaten profitability. The 30% operating margins of yesterday might be unsustainable tomorrow.

Five-year revenue growth of 10.3% annually barely exceeds inflation. For a company supposedly benefiting from manufacturing renaissance and import substitution, this growth disappointing. Either the opportunity is smaller than projected, or Wendt isn't capturing it effectively. Without German technical support, new product development might lag global innovation. Today's competitive advantage could become tomorrow's obsolescence.

Customer concentration remains concerning despite strategic relationships. Automotive sector disruption from EVs, aerospace cyclicality, cutting tool industry consolidation—each threatens revenue stability. Deep relationships matter until they don't. When customers face their own disruptions, supplier loyalty becomes secondary to survival. Wendt's concentrated exposure amplifies customer-specific risks.

Scale disadvantages persist despite niche dominance. Global competitors operate at 10-100x Wendt's scale, enjoying procurement advantages, R&D leverage, and global customer relationships. As industries consolidate globally, local champions face increasing pressure. Wendt might dominate Indian super abrasives, but India represents maybe 2% of global market. Can a ₹237 crore company compete against €10 billion giants indefinitely?

The German technology pipeline closure might hurt more than acknowledged. While Wendt developed independent capabilities, cutting-edge innovations still originate in advanced economies. Without access to latest developments in ceramic composites, nano-structured abrasives, or hybrid manufacturing technologies, Wendt might fall behind. Self-reliance sounds strategic until it becomes isolation.

Competition from China looms large. Chinese manufacturers destroyed margin structures across industries through aggressive pricing and acceptable quality. Super abrasives might seem specialized, but Chinese companies are moving upmarket rapidly. When customers can buy 80% quality at 50% price, premium positioning becomes challenging. Wendt's margins assume pricing power that might evaporate under Chinese competition.

Valuation multiples reflect perfection pricing. Trading at 40+ PE ratios and 7x revenues, markets expect flawless execution and accelerating growth. Any disappointment—margin compression, customer loss, competitive pressure—triggers violent correction. The stock's 52% decline from peaks suggests markets are already recalibrating expectations. Further multiple compression could occur as reality diverges from aspiration.

The Balanced View

Truth lies between extremes. Wendt isn't the next Asian Paints or HDFC Bank—companies that dominated large markets with superior execution. But neither is it a value trap dependent on dying technology. It's a profitable niche player with genuine competitive advantages facing real challenges. The investment case depends on time horizon and risk tolerance.

For long-term investors, the transformation story remains compelling. Independence, brand ownership, and Murugappa backing provide foundation for steady value creation. For traders, volatility creates opportunities both ways. For skeptics, execution risks and competitive threats warrant caution. As always in investing, position sizing matters more than conviction. Wendt might deserve portfolio inclusion, but concentration would be imprudent.

XI. Epilogue: What Does Independence Mean?

The last German engineer left Hosur in September 2012. No farewell party, no ceremonial handover—just an empty desk and a server full of locked files. Thirteen years later, as Wendt India's engineers design grinding solutions for India's first semiconductor fab, that departure seems less like abandonment and more like graduation.

Independence in industrial technology isn't political rhetoric—it's capability reality. Every imported grinding wheel represents not just foreign exchange outflow but knowledge dependence. Every indigenous solution represents not just import substitution but capability accumulation. Wendt's journey from joint venture to independence mirrors India's larger transformation from technology recipient to innovation participant.

The symbolism of owning the global Wendt brand transcends corporate strategy. An Indian company owning German industrial heritage, establishing subsidiaries in Germany, exporting precision technology to developed markets—this reverses centuries of colonial-era narratives. When Wendt India's engineers train European customers on optimal grinding parameters, historical hierarchies invert. The knowledge flow reverses. The student becomes teacher.

Post divestment by Wendt GmbH, CUMI holds 37.5% and public holds the balance 62.5% equity. This ownership structure—Indian promoter, Indian public shareholders, no foreign complications—represents more than governance simplicity. It's economic sovereignty in microcosm. The value created remains in India, compounds in India, benefits India. No leakage through royalties, dividends, or transfer pricing to foreign parents.

CUMI as sole promoter brings Murugappa ethos—100-year thinking in quarterly earnings world. The group that started with sandpaper in 1954 now oversees advanced ceramics, electric vehicles, and precision abrasives. They understand industrial evolution requires patience, investment, and occasional courage to defy conventional wisdom. Wendt under CUMI won't chase quarterly numbers at strategy's expense.

The broader implications extend beyond Wendt. Across India, similar transformations are occurring—Bharat Forge competing with German forging giants, Sona Comstar supplying global automotive OEMs, Dixon becoming Apple's manufacturing partner. Each represents capability building that transcends individual corporate success. Wendt's forced self-reliance becomes template for others navigating partnership complexities.

Yet questions remain. Can Wendt maintain innovation momentum without global technical partnerships? Will Industry 4.0 disruption favor global scale over local expertise? Can premium positioning survive Chinese commoditization? These aren't just Wendt's challenges but Indian manufacturing's existential questions. The answers will determine whether Make in India becomes global reality or remains domestic aspiration.

The final lesson might be the most important: independence isn't isolation. Wendt's Lithoz partnership, customer collaborations, and global ambitions show sophisticated understanding that modern business requires ecosystems, not fortresses. True independence means choosing partners rather than depending on them, creating technology rather than importing it, setting standards rather than following them.

Standing in Wendt's Hosur facility today, watching Indian engineers design solutions for global customers, using equipment they designed, processes they developed, and brands they own, one sees possibility. Not just for Wendt but for Indian manufacturing broadly. The grinding wheels spinning at 10,000 RPM, removing material one micron at a time, become metaphor for patient value creation. Precision, persistence, and patience—the Wendt way, the Murugappa way, perhaps the Indian way.

As markets digest Wendt's transformation from conflicted joint venture to independent champion, valuations will fluctuate. Bulls will cite liberation premium; bears will highlight execution risks. But beyond investment returns lies a larger narrative about capability building, technological sovereignty, and value creation in emerging markets. Wendt's journey from German dependence to global independence isn't just corporate history—it's industrial evolution in real-time.

The super abrasives spinning in factories across India, grinding precision components for everything from smartphones to satellites, carry no markers of their dramatic origins. They just work—consistently, precisely, reliably. Perhaps that's the ultimate validation. Not stock prices or financial metrics but customer trust. When mission-critical applications depend on your products, origin stories become irrelevant. Performance speaks louder than pedigree.

For investors evaluating Wendt, for entrepreneurs navigating partnerships, for policymakers designing industrial strategy, the lesson is clear: true value creation requires capability building, not just capital allocation. The companies that survive and thrive over decades are those that invest in knowledge, develop expertise, and maintain operational excellence through inevitable disruptions. Wendt's transformation from joint venture to independence exemplifies this reality.

The grinding continues. In Hosur and Thailand, in customer factories and R&D labs, Wendt's products shape the materials that shape modern life. Each rotation removes impossibly small amounts of impossibly hard materials with impossible precision. It's boring, essential, profitable work—the kind that builds industrial nations and compound returns. The German partners are gone, the brand is Indian, the future uncertain. But the grinding continues. In the end, perhaps that's all that matters.

XII. Links & Resources

For deeper understanding of Wendt India's transformation and the super abrasives industry, several resources prove invaluable:

Company Documents & Filings: - Annual Reports (2019-2024) available at wendtindia.com provide detailed operational metrics and strategic evolution - NSE and BSE approved declassification of Wendt GmbH as promoter, letters dated 22 September 2025 - ICRA Rating Reports offering independent credit assessment and industry positioning - Corporate presentations detailing product portfolios and market strategies

Industry Research: - Indo-German Chamber of Commerce (IGCC) reports on successful JV case studies - The Indian abrasives market (which includes super abrasives) was worth about $492 million in 2024. Super abrasives are a small but fastest-growing part of this market (less than 10% share, but growing at over 6.5% per year) - CII Manufacturing Excellence Awards documentation showcasing operational best practices - Technical papers on CBN and diamond grinding applications in precision manufacturing

Historical Context: - Murugappa Group archives documenting CUMI's industrial heritage since 1954 - Business press coverage of India's first hostile takeover (1991) - Court filings related to the 3M-CUMI dispute providing legal precedents - Patent databases showing Wendt's innovation trajectory post-2012

Comparative Analysis: - Global super abrasives market reports from Mordor Intelligence and Grand View Research - Competitor analysis of Saint-Gobain, 3M, and Element Six operations in India - Sector reports on Indian automotive, aerospace, and cutting tool industries

Technical Resources: - Grinding technology handbooks explaining super abrasive applications - Industry 4.0 implementation case studies in Indian manufacturing - Research papers on tropical climate adaptations for precision manufacturing equipment

XIII. Recent News & Updates

The past year witnessed dramatic corporate restructuring that fundamentally altered Wendt India's ownership and strategic direction:

Trademark Acquisition (January-April 2025): In January 2025, Wendt India paid €3.8 million to acquire global rights to the "Wendt" brand, removing a key obstacle to 3M's exit. Wendt India will acquire exclusive rights to 60 trademarks registration across 40 countries. This wasn't merely a brand purchase but strategic positioning for global expansion without royalty obligations or territorial restrictions.

The OFS Drama (May 2025): 3M opted for a massive Offer for Sale (OFS) in May 2025 to exit its 37.5% stake quickly, accepting a steep discount (₹6,500/share vs. ₹10,467 market price) to ensure full subscription. The market's violent reaction—shares plummeting 20% intraday—created extraordinary opportunities for sophisticated investors who recognized the transformation value.

Management Transition (September 2025): Executive Director & CEO Ninad Gadgil stepped down effective 15 September 2025, marking the end of transition-era leadership. Head—Human Resources Mr. Satheesh C resigns effective close of business 15 September 2025. These departures signaled completion of the German exit process and beginning of a new strategic chapter.

Promoter Reclassification (September 2025): The culmination came with regulatory approval for Wendt GmbH's exit from promoter category. WIL has been a 37.5 – 37.5 Joint Venture between Wendt GmbH and CUMI. Post divestment by Wendt GmbH, CUMI holds the 37.5% and the public holds the balance 62.5% equity. This clean ownership structure eliminates related-party complications and governance concerns.

Product Innovation Momentum (2024-2025): Despite corporate turbulence, operational excellence continued. In 2024, Company has launched Precigrind-AWH 250 & WRS NH. Further, it has launched Opera 200, Delta 150 & 250. The Company launched specialised training initiatives, including international exposure in Germany for advanced machine-building skills in FY 2025.

Financial Performance Update (Q1 FY2026): Recent quarters reflected transition costs but underlying strength remained. Company achieved sales of Rs 4649 lakh during the Q1FY26, which is 6% higher than Q1FY25 (YoY). Domestic sales was Rs 3571 lakh during Q1FY26, which is higher by 3 % than the Q1FY25. Profit After Tax (PAT) for the current quarter is Rs 495 lakh, which is 34% lower than the Q1FY25 (YoY). The margin compression likely reflects one-time expenses related to brand acquisition and restructuring rather than operational deterioration.

Industry Recognition (2024): WENDT (India) Limited has been honoured with the prestigious Best Supplier Special Projects Award from Kennametal India Limited at the Suppliers Meet 2024. This recognition from a global cutting tool giant validates Wendt's technical capabilities and reliability—crucial for maintaining premium positioning post-independence.

German Subsidiary Establishment (July 2025): In a strategic reversal, Wendt India established a wholly-owned subsidiary in Germany, providing direct access to European markets without intermediation. This bold move—the colonized becoming colonizer—demonstrates confidence in competing directly in developed markets.

Stock Price Volatility: The shares experienced extreme volatility throughout the transition. The 52-week high and low of Wendt India Ltd share price is ₹ 8162 - ₹ 18033.65 as of 24-09-2025, reflecting market uncertainty about post-German future. Patient investors who understood the transformation thesis and bought during panic selling earned substantial returns.

These developments collectively represent the most significant transformation in Wendt's 45-year history. The company that began as a technology-dependent joint venture has emerged as an independent entity with global brand rights, simplified governance, and proven self-reliance. The short-term disruption created long-term opportunity for those who recognized the strategic value of complete independence.

Final Thoughts: The Power of Forced Evolution

Wendt India's journey offers profound lessons about capability building in emerging markets. The 2012 technology embargo that should have crippled the company instead catalyzed innovation. The partnership dispute that could have destroyed value created independence. The German exit that markets interpreted as abandonment was actually liberation.

This transformation transcends one company's story. Across India, similar narratives unfold—joint ventures evolving into independent champions, forced self-reliance becoming competitive advantage, crisis catalyzing capability. Wendt's experience provides a template for navigating the complex transition from dependence to independence.

The financials tell part of the story—maintained margins despite technology embargo, continued growth without foreign support, market leadership in specialized segments. But the real value lies in intangibles: accumulated knowledge, customer trust, innovation capability, strategic flexibility. These assets, built through adversity, cannot be replicated or acquired—only earned through experience.

For investors, Wendt represents a specific type of opportunity: the liberation play. Companies breaking free from constraining partnerships, acquiring brand independence, simplifying governance structures often experience fundamental rerating. The transition is messy, markets panic, but patient capital recognizes transformation value. Wendt's volatile journey from ₹8,000 to ₹18,000 and back illustrates both risk and reward.

The broader implications extend to India's manufacturing ambitions. If a mid-sized grinding wheel manufacturer can achieve technological independence and compete globally, what's possible for larger sectors? Wendt's success challenges narratives about permanent technology dependence, proving that capability building—though painful—is possible.

Yet challenges remain substantial. Chinese competition intensifies. Global customers consolidate. Technology cycles accelerate. Industry 4.0 demands continuous investment. Wendt's independence coincides with unprecedented market dynamics. Success requires not just maintaining current position but continuous evolution.

The super abrasives market itself offers structural tailwinds. Precision manufacturing expands globally. Electric vehicles require new grinding applications. Semiconductor fabrication demands ultra-precision tools. Aerospace indigenization accelerates. Medical devices need specialized manufacturing. Each trend favors companies with deep application expertise over commodity suppliers.

Wendt's response—focusing on solutions over products, partnerships over transactions, innovation over imitation—positions them for these opportunities. Wendt India known for its diversified and impressive Product Portfolio, Innovation strategy, strong Product Development, Personalized technical services and providing Technology Solutions in Grinding to its 750+ direct customers in the domestic market. This customer-centric approach, developed through necessity, becomes sustainable differentiation.

The Murugappa stewardship provides patient capital and strategic stability. Unlike financial investors seeking quick exits, CUMI views Wendt as long-term value creation platform. This perspective enables investments in R&D, customer relationships, and capability building that short-term oriented ownership wouldn't support.

For students of business strategy, Wendt offers rich case study material. How do dependent partners build independent capabilities? When should companies fight for partnership preservation versus seeking independence? How do organizations maintain operational excellence during ownership transitions? What's the value of brand ownership versus licensing? These questions resonate beyond Wendt's specific circumstances.

The investment thesis ultimately depends on belief in India's manufacturing future. If India becomes a global manufacturing hub, companies like Wendt—with proven capabilities, established positions, and operational excellence—will capture disproportionate value. If manufacturing remains marginal, specialized players face limited growth. Wendt represents a leveraged bet on Indian industrial evolution.

As grinding wheels spin in factories across India, removing material one micron at a time, they embody a larger transformation. From imported solutions to indigenous innovation. From technology dependence to creative independence. From joint venture complications to ownership clarity. Each rotation removes not just material but also doubts about Indian manufacturing capability.

The German engineers who established Wendt India in 1980 wouldn't recognize today's operation. What began as technology transfer evolved into technology creation. The student didn't just equal the teacher—in many applications, they've surpassed them. This reversal, repeated across industries, defines India's economic transformation.

Wendt's independence isn't isolation but liberation. Free to partner by choice rather than compulsion. Free to innovate without approval. Free to expand without restriction. Free to succeed or fail on their own terms. This freedom, hard-won through crisis and conflict, becomes the foundation for next chapter's value creation.

The grinding continues, as it must. In the precision and persistence of those spinning wheels lies a metaphor for industrial development itself—patient, precise, relentless. Removing imperfections. Creating smooth surfaces. Enabling precision. Building the foundation for everything else. Boring work, essential work, profitable work. The kind that builds nations and fortunes, one micron at a time.

The path ahead isn't about choosing between scale and specialization. It's about leveraging focused excellence to create value that transcends conventional metrics. Wendt's journey proves that in industrial markets, depth beats breadth, expertise trumps scale, and patient execution creates enduring value.

Final Analysis: Independence as Competitive Advantage

Standing at the inflection point of complete independence, Wendt India presents a paradox that challenges conventional investment wisdom. The Company achieved Sales of Rs 6,947 lakhs for the quarter ended 31st Mar 2024 which is 22% higher than the corresponding quarter previous year, yet the market cap reflects uncertainty rather than growth. This disconnect between operational performance and market perception creates the classic conditions for value creation—or destruction.

The transformation from joint venture to independent entity fundamentally altered Wendt's strategic calculus. No longer constrained by technology transfer agreements or partnership approvals, the company can pursue opportunities previously inaccessible. The German subsidiary establishment turns historical dependence on its head—the colonized becoming colonizer in symbolic reversal. When Indian engineers train European customers on precision grinding techniques developed in Hosur, the knowledge hierarchy inverts completely.

India Abrasives Market is growing at a CAGR of 7.9% during the forecast period 2024-2031, with The Indian abrasives market (which includes super abrasives) was worth about $492 million in 2024. Super abrasives are a small but fastest-growing part of this market (less than 10% share, but growing at over 6.5% per year). These growth rates exceed GDP expansion, reflecting structural drivers rather than cyclical upturn. Wendt's positioning at the intersection of precision manufacturing and industrial evolution captures these tailwinds while avoiding commodity trap pitfalls.

The competitive dynamics favor focused specialists over diversified giants. While 3M and Saint-Gobain dominate commodity abrasives through scale, super abrasives remain fragmented with technology and application expertise mattering more than manufacturing footprint. The major Indian market players include Carborundum Universal Ltd, Asahi Diamond Industrial India Private Limited, Grindwell Norton Ltd, Wendt India Ltd, Hindustan Abrasives, Sterling Abrasives Limited, Orient Abrasives Limited, Bosch Limited, Webcast Steels Ltd, and Henkel Anand India Private Limited, yet none possess Wendt's combination of technical heritage, brand ownership, and Murugappa backing.

The financial resilience during transition deserves recognition. Despite technology embargo, partnership dysfunction, and ownership upheaval, Profit After Tax (PAT) for the current year is Rs 3,950 lakhs, which is 2% lower than the previous year—remarkable stability given circumstances. The ability to maintain profitability while navigating existential challenges validates operational strength beyond any financial metric.

Risk factors remain substantial and shouldn't be minimized. Chinese competition intensifies annually, threatening margin structures globally. Customer concentration in cyclical industries—automotive, aerospace, machinery—amplifies economic sensitivity. The loss of German technical pipeline might manifest in innovation gaps years hence. Scale disadvantages persist despite niche dominance, limiting negotiating leverage with global customers.

Yet the bull case transcends these concerns. India's industry is projected to achieve a CAGR of 6.4% through 2034, with the mass expansion of industries like medical devices, electronics, etc. Wendt's 750+ customer relationships, built over decades, create switching costs that transcend any product advantage. The Murugappa parentage provides patient capital and strategic stability rare in Indian mid-caps. Complete brand ownership enables global expansion previously impossible.

The valuation debate reflects this complexity. At current levels, markets price perfection—flawless execution, accelerating growth, margin expansion. Any disappointment triggers violent correction, as recent volatility demonstrates. Yet for patient investors understanding the transformation arc, current prices might represent generational opportunity. The company trading at software multiples with industrial characteristics seems expensive until recognizing knowledge businesses masquerading as manufacturers deserve premium valuations.

The broader narrative extends beyond Wendt to India's manufacturing evolution. Each indigenous innovation, every import substitution, all capability building contributes to economic sovereignty. When Indian companies own global brands, establish European subsidiaries, and export precision technology, historical hierarchies crumble. Wendt exemplifies this transformation—from technology recipient to innovation participant, from joint venture to global competitor.

Looking forward, the path seems clear if challenging. Consolidate domestic dominance while cautiously expanding internationally. Deepen customer relationships through application engineering and solutions selling. Invest in next-generation technologies—ceramic 3D printing, nano-structured abrasives, hybrid manufacturing. Maintain financial conservatism that enabled survival through crisis. Build on hard-won independence to create sustained value.

For investors, Wendt represents a specific bet: that focused excellence beats diversified mediocrity, that patient execution trumps aggressive expansion, that Indian manufacturing can compete globally. The stock will remain volatile, reflecting ongoing transformation uncertainty. Position sizing matters more than conviction—meaningful allocation without concentration, participation without overexposure.

The investment case ultimately reduces to time horizon and risk tolerance. Short-term traders face continued volatility as markets digest ownership changes and margin pressures. Long-term investors might find exceptional opportunity in a profitable niche player with genuine competitive advantages and structural tailwinds. Skeptics see execution risks and competitive threats warranting caution. All perspectives have merit; none possess monopoly on truth.

Conclusion: The Grinding Continues

In the end, Wendt India's story transcends quarterly earnings or stock price gyrations. It's about capability building in emerging markets, technological sovereignty in globalized world, value creation through patient excellence. The company that began as German subsidiary importing technology now owns global brands and exports innovation. This reversal, replicated across Indian industry, reshapes economic narratives and investment opportunities.

The super abrasives spinning at impossibly high speeds, removing impossibly small amounts of impossibly hard materials with impossible precision, become metaphor for industrial development itself. Progress measured in microns, value created through persistence, competitive advantage built grain by grain. The German partners have departed, the brand is Indian, the future uncertain but promising. Through it all, the grinding continues.

For those evaluating Wendt—as investment opportunity, business case study, or industrial bellwether—the lessons are clear. True value creation requires capability building not just capital deployment. Sustainable competitive advantage comes from deep expertise not broad presence. Patient excellence beats aggressive mediocrity. Crisis catalyzes evolution. Independence, though painful to achieve, becomes ultimate competitive moat.

The transformation from Wendt (India) Limited as joint venture to Wendt India as independent champion marks inflection point, not conclusion. The real story—how Indian manufacturing competes globally, whether focused specialists can challenge diversified giants, if patient capital creates superior returns—remains unwritten. Early chapters suggest compelling narrative, but final verdict awaits future volumes.

As precision components manufactured with Wendt's grinding wheels enable everything from electric vehicles to satellites, from medical implants to semiconductor wafers, the company's quiet excellence underpins modern life. No fanfare, no recognition, just consistent delivery of mission-critical solutions. Perhaps that's the ultimate validation—not market valuations or analyst ratings but customer trust in applications where failure isn't option.

The Hosur factory hums with activity, Indian engineers design solutions for global challenges, customers depend on consistent excellence. Stock prices fluctuate, ownership structures evolve, strategic priorities shift. But fundamentally, nothing changes. Materials need shaping, precision demands tools, progress requires grinding. Wendt provides all three, has for 45 years, will for decades hence.

For India's manufacturing aspirations, Wendt offers both template and cautionary tale. The template: how forced self-reliance becomes competitive advantage, how patient excellence creates sustainable value, how focused specialists can compete globally. The caution: scale matters eventually, innovation requires continuous investment, global competition intensifies relentlessly. Success requires navigating both opportunity and threat with equal skill.

The grinding wheels keep spinning, removing material one microscopic layer at a time, creating precision through persistence. It's boring, essential, profitable work—the kind that builds industrial nations and compound returns. The German partnership has ended, independence has arrived, challenges remain substantial. But competitive advantages earned through crisis, capabilities built through adversity, customer relationships forged through consistency—these endure.

In the precision of those spinning wheels lies profound truth about value creation. Not through dramatic gestures or revolutionary breakthroughs but patient accumulation of expertise, consistent delivery of excellence, gradual building of irreplaceable capabilities. Wendt's transformation from dependent venture to independent champion exemplifies this reality. The market may not fully appreciate it yet, but customers depending on mission-critical applications understand completely.

The story continues, as it must. New chapters await—international expansion, technology evolution, competitive battles. But foundation has been laid through 45 years of grinding excellence, 13 years of forced independence, and recent complete liberation. Whatever comes next, Wendt faces it with proven resilience, established capabilities, and hard-won freedom to chart its own course.

For investors seeking next Asian Paints or HDFC Bank, Wendt disappoints—too small, too specialized, too dependent on industrial cycles. For those understanding that exceptional returns often come from unlikely sources, that boring businesses can be beautiful investments, that patient capital compounds quietly but powerfully, Wendt intrigues. Not as concentrated position but as portfolio component, not as momentum play but as value creation story, not as guaranteed winner but as asymmetric opportunity.