Welspun Enterprises: Building India's Infrastructure Future

I. Introduction & Episode Setup

The year is 2022. In a boardroom overlooking Mumbai's skyline, executives at Welspun Enterprises are about to sign away six highway projects—their crown jewels—for $775 million to Actis, a global private equity giant. For most infrastructure companies, this would signal retreat or distress. But for Welspun, it's the culmination of a masterfully executed capital recycling strategy that would free up resources for their next big bet: India's water crisis.

This is the story of how a construction partnership that began in 1976 transformed into one of India's most intriguing infrastructure plays, navigating the complex maze of government contracts, public-private partnerships, and the peculiar economics of building a nation's backbone. Today, Welspun Enterprises Limited (NSE: WELENT) sits at a market capitalization of ₹6,397 crore, with revenues touching ₹3,554 crore—but these numbers barely scratch the surface of a company that has mastered the art of building, monetizing, and reinventing itself in India's infrastructure goldmine.

The central question isn't just how a modest construction firm became an infrastructure powerhouse. It's how Welspun cracked the code on something far more elusive: turning India's massive infrastructure deficit—estimated at $1.5 trillion—into a sustainable, profitable business model while competitors either overleveraged themselves into oblivion or remained stuck in low-margin EPC contracts.

What makes Welspun particularly fascinating is its chameleon-like ability to adapt. When Build-Operate-Transfer (BOT) projects became risky, they pivoted to Hybrid Annuity Models (HAM). When roads became crowded, they dove into water. When assets matured, they sold at peak valuations and redeployed capital. This isn't just infrastructure development—it's financial engineering married to execution excellence, wrapped in the larger Welspun Group's $2.7 billion empire that spans everything from steel pipes to home textiles.

As India prepares to spend $1.4 trillion on infrastructure by 2025, Welspun Enterprises stands at a crossroads. They've proven they can build roads that connect cities and water systems that quench villages. But can they scale this model while maintaining their disciplined approach to capital? Can they navigate the treacherous waters of government policy shifts, political transitions, and the eternal challenge of infrastructure: getting paid on time?

This is that story—a deep dive into how infrastructure really gets built in India, the art of managing government relationships, and the delicate balance between growth and prudence in a sector littered with spectacular failures. Because in Indian infrastructure, the companies that survive aren't necessarily the biggest or the most connected—they're the ones that understand timing, capital cycles, and most importantly, when to hold and when to fold.

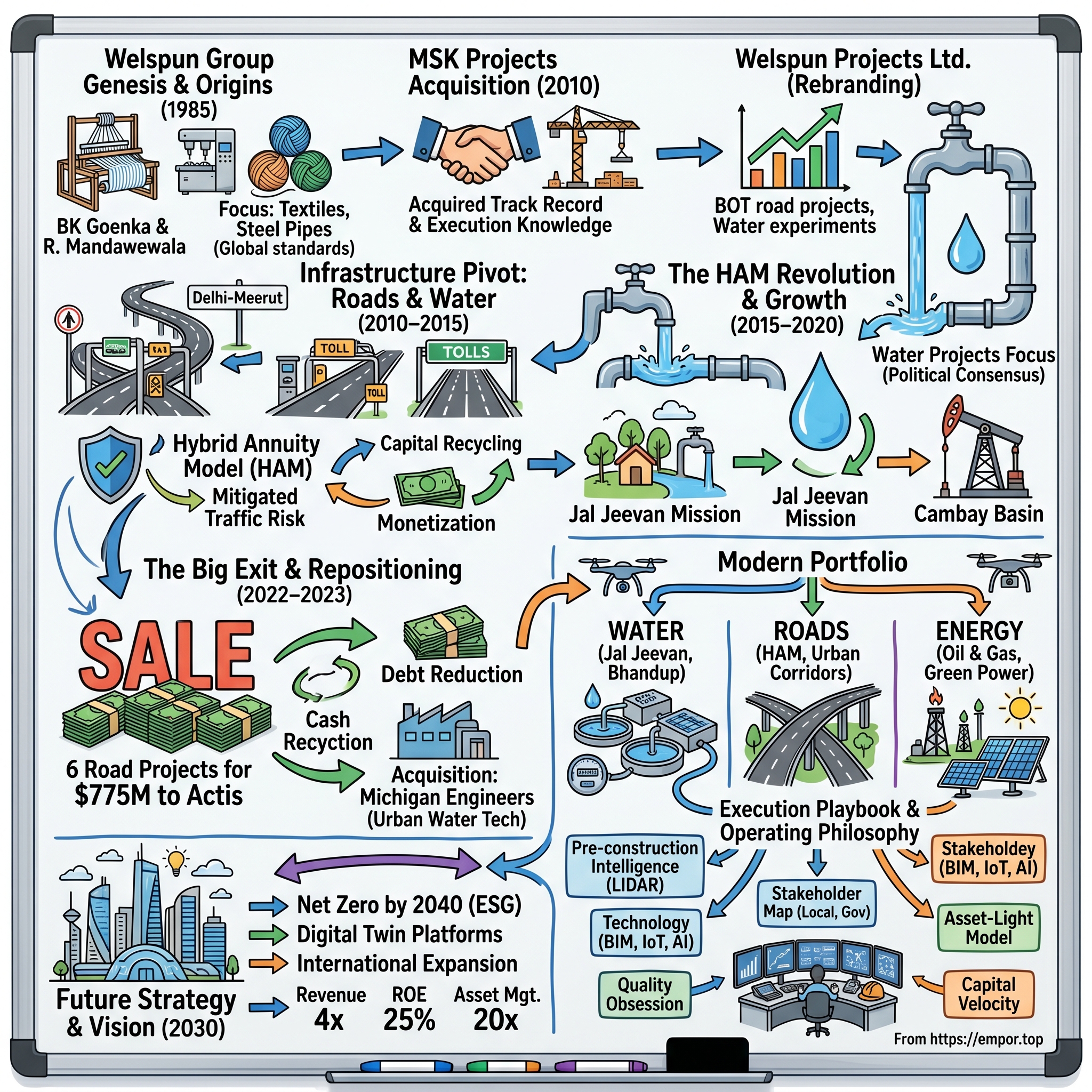

II. The Welspun Group Genesis & Origins

Picture this: 1985, a small industrial town called Palghar, about 100 kilometers north of Mumbai. Two cousins, Balkrishan Goenka and Rajesh Mandawewala, are staring at a modest texturizing unit they've just acquired with $100,000 in borrowed capital. The unit is so small it barely registers on Maharashtra's industrial map. They call it Welspun Winilon Silk Mills—"Wel" for welfare, "spun" for the textile roots that would define their early journey. Neither man could have imagined that this cramped facility would spawn a $5 billion conglomerate that would one day supply steel pipes to Saudi Aramco and bed sheets to Walmart.

The Goenka family had been in trading for generations, but Balkrishan—BK to friends—wanted something different. He'd watched India's textile industry struggle with outdated technology while global competitors raced ahead. His vision was simple yet audacious: bring world-class manufacturing to India, starting with synthetic yarns that local textile mills desperately needed. The timing was prescient—India was still six years away from liberalization, but the seeds of change were already sprouting.

What set the Goenka-Mandawewala partnership apart wasn't just ambition—it was their complementary skills. BK brought the financial acumen and risk appetite; Rajesh brought operational excellence and an engineer's obsession with quality. They had a rule: never enter a business unless they could be among the top three players. It sounds like corporate speak now, but in 1985 India, where family businesses often diversified into anything that seemed profitable, this focus was revolutionary.

By 1989, they'd moved beyond texturizing into terry towels, setting up Welspun India Limited. The domestic market was their learning ground, but their eyes were on exports. They studied global standards obsessively, hired consultants they could barely afford, and most crucially, invested in technology when competitors were cutting costs. A former executive recalls BK spending entire nights on the factory floor, personally checking product quality before shipments. "He'd say, 'Our name goes on every product. One defect, and years of reputation building vanishes.'"

The 1991 liberalization was their catalyst. As India opened up, Welspun was ready. They'd already built relationships with international buyers, understood global quality standards, and most importantly, had the production capacity to scale. By 1995, Welspun India was exporting terry towels to Europe and the US. But the real masterstroke came in 1996 when they backward integrated into spinning, giving them control over their raw material quality—a move that would become the Welspun playbook: vertical integration for quality control and margin expansion.

The late 1990s saw the group's most ambitious diversification yet: steel pipes. The logic was counterintuitive—what did textile manufacturers know about steel? But BK saw what others missed: India's infrastructure boom would need massive amounts of large diameter pipes for oil, gas, and water transmission. More importantly, the technology and quality requirements for these pipes were so stringent that only a handful of global players could meet them. Classic Welspun thinking—enter a market with high barriers to entry, invest heavily in technology, and aim for global standards from day one.

Welspun Gujarat Stahl Rohren, established in 1995, became India's largest line pipe manufacturer within a decade. They didn't just make pipes; they made API-grade pipes that could withstand the harsh conditions of oil fields from Saudi Arabia to the North Sea. The first order from Saudi Aramco in 2001—after three years of grueling qualification processes—validated their strategy. An engineer from that era remembers the celebration: "We knew that if we could satisfy Aramco's standards, we could sell anywhere in the world."

By 2005, the Welspun Group had three distinct verticals—textiles, pipes, and infrastructure—each run independently but sharing the same DNA: global ambitions, technology focus, and an almost obsessive attention to quality. The infrastructure vertical, which would eventually become Welspun Enterprises, was the newest and in many ways the most challenging. Unlike textiles or pipes, where you could control most variables, infrastructure meant dealing with land acquisition, government bureaucracy, and political risk.

The infrastructure opportunity was massive. India's Planning Commission estimated the country needed $500 billion in infrastructure investment between 2007-2012. Roads, airports, ports, power plants—everything needed upgrading. The government, recognizing it couldn't fund this alone, had opened up infrastructure to private participation through various models. For Welspun, with its engineering capabilities from the pipe business and project management skills from setting up large manufacturing facilities, infrastructure seemed like a natural extension.

But infrastructure is a different beast. As we'll see in the next section, Welspun's entry into this sector through the acquisition of MSK Projects would test everything they'd learned about building businesses in India. Because building roads in India isn't just about laying asphalt—it's about navigating the complex intersection of politics, finance, and engineering that defines Indian infrastructure.

III. MSK to Welspun: The Transformation Story (1994–2010)

The conference room at MSK Projects' Delhi office, 2009. M.S. Khurana, the founder who'd built this construction company from a partnership firm in 1976 to a listed entity, is meeting with Welspun Group's leadership. At 70, Khurana knows his company needs fresh capital and new thinking to compete in India's rapidly evolving infrastructure sector. Across the table, BK Goenka sees an opportunity—not just to buy a construction company, but to acquire three decades of relationships, execution knowledge, and most crucially, a platform to enter infrastructure development. The handshake that followed would transform both companies' destinies.

MSK Projects' story begins much earlier, in 1976, when M.S. Khurana started a partnership firm focusing on civil construction. This was pre-liberalization India, where government contracts dominated construction, margins were thin, and payments were... eventual. Khurana built his business the old-fashioned way: one project at a time, one relationship at a time. By 1994, when the firm incorporated as MSK Projects (India) Limited, it had already completed dozens of projects—schools, hospitals, government buildings—unglamorous work that taught invaluable lessons about managing government contracts.

The December 20, 1994 incorporation date marked a inflection point. India was three years into liberalization, and infrastructure was beginning to open up to private participation. Khurana, despite his age, saw the opportunity clearly. The company began bidding for larger projects—highways, bridges, industrial construction. The 2004 IPO, listing on BSE, NSE, and even the regional Vadodara Stock Exchange, raised ₹50 crores—modest by today's standards but significant for a construction company then.

What made MSK Projects attractive wasn't its size—revenues were around ₹300 crores in 2009—but its track record. In infrastructure, where a single delayed project can destroy a company, MSK had something invaluable: 33 years without a major default or dispute. They'd completed projects across 15 states, built relationships with multiple state governments, and most importantly, understood the unwritten rules of Indian infrastructure—when to push, when to wait, and when to walk away.

The 2006 joint venture with BUL (Bharat Udyog Limited) for toll collection management revealed Khurana's forward thinking. While others focused on construction, he recognized that the real money in roads wasn't in building them but in operating them. BUL MSK Infrastructure began managing toll collection for various highway projects, generating steady cash flows and learning the operations side of the business—knowledge that would prove invaluable when BOT (Build-Operate-Transfer) projects became the norm.

Welspun's entry in 2010 wasn't a hostile takeover but a negotiated transition. The Goenka family acquired a controlling stake, but Khurana stayed on as advisor, his team remained intact, and more importantly, the relationships cultivated over decades transferred smoothly. The immediate rebranding to Welspun Projects Ltd. signaled intent—this wasn't just another acquisition for the group but a serious entry into infrastructure.

The first major decision under Welspun ownership was controversial: expanding into energy infrastructure. The company began bidding for power transmission projects and oil & gas pipelines, leveraging the group's expertise from Welspun Corp's pipe business. Critics called it lack of focus; BK Goenka called it synergy. A former executive explains: "We weren't just laying pipes; we were offering complete solutions—manufacturing, laying, and maintenance. No other infrastructure company could match that integration."

Between 2010 and 2015, Welspun Projects underwent a dramatic transformation. Revenue grew from ₹300 crores to over ₹1,500 crores. The company completed six BOT road projects covering 500+ kilometers with capital expenditure exceeding $200 million. But the real achievement was becoming among the first developers to successfully complete an NHAI (National Highways Authority of India) BOT project—the Dewas-Bhopal corridor—on time and within budget.

The Dewas-Bhopal project deserves special attention. Spanning 125 kilometers, it connected Madhya Pradesh's commercial capital with its political capital. The project faced every conceivable challenge—land acquisition delays, cost overruns from commodity inflation, and political changes that threatened to derail everything. Yet Welspun delivered it six months ahead of schedule. How? They deployed what would become their signature approach: over-invest in project management, maintain excessive liquidity buffers, and most crucially, keep all stakeholders—from local farmers to state ministers—constantly engaged.

The 2013 restructuring was perhaps the boldest move yet. Welspun transferred its EPC (Engineering, Procurement, Construction) business to Leighton Welspun, a joint venture with Australian infrastructure giant Leighton Holdings (now CIMIC Group), receiving 7.5% equity in return. On paper, they gave up a ₹1,000 crore revenue stream. In reality, they shed a low-margin, working capital-intensive business while retaining exposure through equity. The message was clear: Welspun wanted to be a developer, not a contractor.

This distinction—developer versus contractor—is crucial to understanding Welspun's strategy. Contractors build projects for others, earning 8-12% margins if they're lucky, dealing with delayed payments and cost overruns. Developers own projects, earning returns over decades through tolls or annuities. It's the difference between being a laborer and a landlord. The capital requirements are higher, the risks greater, but the returns—if you get it right—are exponentially better.

By 2014, as the company prepared for its final transformation to Welspun Enterprises Limited, the foundation was set. They had a strong project pipeline, proven execution capabilities, and most importantly, a clear strategy: focus on PPP (Public-Private Partnership) projects where they could be developers, not just builders. The infrastructure boom that everyone had predicted in 2005 was finally materializing, and Welspun was ready.

But as we'll see in the next section, being ready and succeeding are different things. The shift to HAM (Hybrid Annuity Model) projects would test every assumption about risk, return, and the role of private capital in Indian infrastructure.

IV. The Infrastructure Pivot: Roads & Water (2010–2015)

The National Highways Authority of India headquarters, New Delhi, 2012. The BOT (Build-Operate-Transfer) model that had driven India's highway development for a decade was dying. Across the country, half-completed highways stood as monuments to overleveraged developers and overoptimistic traffic projections. GMR, GVK, Lanco—infrastructure giants were drowning in debt. In Welspun's Mumbai office, the leadership team faced a choice: double down on BOT projects while others retreated, or pivot to something entirely different. They chose both.

This period—2010 to 2015—would define Welspun Enterprises' DNA. While competitors either withdrew from infrastructure or bet everything on BOT projects, Welspun executed a nuanced strategy that seemed contradictory but was actually complementary: complete existing BOT commitments with excellence, selectively bid for new ones, and simultaneously build capabilities in an entirely new vertical—water infrastructure.

The numbers tell part of the story. By 2015, Welspun had completed six BOT road projects covering over 500 kilometers with capital expenditure exceeding $200 million. But the real story was how they completed them. Take the Delhi-Meerut section of NH-24, a 14.5-kilometer stretch that seemed simple on paper but included navigating through some of Uttar Pradesh's most densely populated areas. Land acquisition alone took 18 months. Local protests delayed construction by another six months. Cost overruns hit 30%. Yet Welspun not only completed it but achieved something remarkable: 98% toll collection efficiency in an area notorious for toll evasion.

How? They deployed what internal documents called the "community integration model." Instead of treating locals as obstacles, they made them stakeholders. They hired 70% of toll booth operators from nearby villages, contracted local vendors for maintenance, and most cleverly, offered discounted monthly passes to regular commuters—turning potential toll evaders into paying customers. A senior executive from that period recalls: "Every other developer was fighting with locals. We made them our partners."

The water infrastructure pivot began almost accidentally. In 2011, Welspun bid for a road project in Gujarat that included a small water pipeline component. The road part was straightforward, but the water component—laying 50 kilometers of pipeline to supply water to drought-prone villages—opened their eyes to an opportunity. India's water infrastructure was decades behind its road infrastructure. The technology requirements were similar to their oil & gas pipeline expertise. Most importantly, water projects had something road projects increasingly lacked: political consensus. No politician opposed bringing water to villages.

By 2013, water wasn't just an add-on but a strategic focus. Welspun began building dedicated teams, hiring water engineers from L&T and Suez, and most importantly, studying global best practices in water infrastructure. They sent teams to Israel to understand drip irrigation, to Singapore to study water recycling, and to the Netherlands to learn about flood management. This wasn't typical for an Indian infrastructure company—most relied on conventional approaches. But Welspun understood that India's water crisis would require innovative solutions.

The 2013 infrastructure restructuring—transferring the EPC business to Leighton Welspun for 7.5% equity—was masterful financial engineering. On the surface, they gave up ₹1,000 crores in annual revenue. But dig deeper: EPC margins were 8-10% at best, working capital cycles stretched 180 days, and payment risks were entirely on Welspun. Post-restructuring, they retained exposure to EPC profits through equity while freeing up capital and management bandwidth for higher-return developer projects. The market initially punished the stock—it fell 15% on announcement—but management held firm.

The Leighton partnership brought unexpected benefits. The Australian company's global experience introduced Welspun to international best practices in project management. They implemented sophisticated project tracking systems, introduced safety standards that exceeded Indian requirements, and most importantly, brought discipline to cost estimation. A project manager from that era notes: "Leighton taught us that in infrastructure, the profit is made in planning, not execution. If you've planned right, execution is just following the script."

Meanwhile, the BOT model that had driven India's highway boom was unraveling. The problem was simple but devastating: traffic projections made during India's 2003-2008 boom proved wildly optimistic. Developers had bid aggressively, assuming 15-20% annual traffic growth. Reality was 5-7%. The math stopped working. Banks, burned by infrastructure NPAs, stopped lending. By 2014, not a single BOT project was awarded.

Welspun's response was surgical. They sold stakes in mature projects to financial investors, recycling capital into new opportunities. The Dewas-Bhopal corridor sale to IDFC Alternatives for ₹662 crores—while retaining 13% stake—became the template. They'd developed the project for ₹400 crores, operated it for three years, proven the revenue model, and then sold majority stake at a 65% premium while keeping skin in the game. This wasn't just an exit; it was validation that their assets had real value.

The 2014-15 transformation to Welspun Enterprises Limited was more than a name change. It signaled evolution from a construction company that happened to own infrastructure assets to an infrastructure developer that selectively did construction. The distinction mattered to investors, partners, and especially to the government, which was desperately seeking credible developers for its ambitious infrastructure plans.

By 2015, Welspun Enterprises had emerged from the infrastructure shakeout not just intact but stronger. While peers like Lanco and GVK struggled with debt, Welspun's debt-to-equity ratio remained under 1:1. While others abandoned infrastructure, Welspun's order book grew to ₹5,000 crores. Most importantly, while everyone focused on roads, Welspun had quietly built capabilities in water—a bet that would pay off spectacularly when the government launched the Jal Jeevan Mission.

But the real test was coming. The government, recognizing the BOT model's failure, was about to introduce something new: the Hybrid Annuity Model (HAM). For Welspun, this would be the opportunity they'd been preparing for—a chance to deploy everything they'd learned about infrastructure development, financial engineering, and government relations.

V. The HAM Revolution & Growth Strategy (2015–2020)

Ministry of Road Transport and Highways, New Delhi, January 2016. Union Minister Nitin Gadkari announces the Hybrid Annuity Model (HAM) for highway development. In the audience, infrastructure company executives exchange glances—some skeptical, others calculating. For five years, highway development had been in limbo. The BOT model was dead, killed by aggressive bidding and optimistic projections. The EPC model put all risk on the government, which lacked capacity to manage hundreds of projects. HAM promised a middle path: developers would invest 40%, government 60%, and returns would come through fixed annuities over 15 years, not toll collection. At Welspun's strategy session that evening, the decision was unanimous: HAM was exactly what they'd been waiting for.

To understand why Welspun was so enthusiastic about HAM when others were cautious, you need to understand what HAM really meant. Under BOT, developers took traffic risk—if fewer vehicles used your road, you lost money. Under HAM, the government took traffic risk while developers took construction and availability risk—keep the road available and maintained, get paid. For Welspun, with its proven execution capabilities and conservative financial management, this was ideal. They could focus on what they did best—building quality infrastructure on time—without betting on India's unpredictable traffic patterns.

The first HAM project Welspun bid for tells you everything about their approach. While competitors chased large, high-profile projects, Welspun targeted a relatively modest 40-kilometer stretch in Madhya Pradesh. The location was strategic—they knew the terrain from their earlier Dewas-Bhopal project, had relationships with local administration, and understood the soil conditions that often caused cost overruns. They won the bid not with the lowest price but with the most credible execution plan. An NHAI official later commented: "Others showed us Excel sheets. Welspun showed us photos of similar projects they'd completed."

Between 2016 and 2020, Welspun would win and execute multiple HAM projects worth over ₹10,000 crores. But the real innovation wasn't in winning projects—it was in financing them. HAM required developers to arrange 40% of project cost as equity and debt. Most developers struggled to raise funds; banks were still nursing infrastructure NPAs. Welspun's solution was elegant: they created a fund structure where they retained 26% equity, brought in financial investors for 51%, and gave the remaining 23% to strategic partners like contractors and suppliers who took equity instead of cash payments.

The financial engineering went deeper. Each HAM project was structured as a Special Purpose Vehicle (SPV), isolating risk while allowing focused management. Welspun would typically invest ₹100 crores of equity in a ₹1,000 crore project, leverage it 2:1 with debt, and control a ₹1,000 crore asset with ₹100 crore investment—a 10x asset multiplication. The annuity payments over 15 years would generate 15-18% equity IRR, not spectacular but steady and predictable. In infrastructure, predictable returns are gold.

The 2020 acquisition of Mumbai-Nagpur Prosperity Corridor (MCPTRL) from Essel Group deserves special attention. Essel, overleveraged and desperate for cash, was selling a 95-kilometer operational toll road. Most buyers walked away—the project had environmental clearance issues, land acquisition disputes, and was generating barely enough toll to service debt. Welspun saw opportunity where others saw trouble. They negotiated the purchase price down from ₹2,000 crores to ₹1,100 crores, restructured the debt, resolved 80% of land disputes within six months, and most cleverly, got NHAI to convert a section from toll to HAM, reducing revenue risk.

The Tamil Nadu project signed in 2020—₹2,005 crores for a 26-kilometer elevated corridor—showcased Welspun's evolution. This wasn't just road construction but complex urban infrastructure involving land acquisition in densely populated areas, coordination with multiple utilities, and managing traffic during construction. The project required capabilities Welspun had been building for years: urban planning expertise, stakeholder management skills, and most importantly, the financial strength to manage a two-year construction period before annuities began.

But roads were only half the story. The water infrastructure business that began as an experiment in 2011 was becoming a major growth driver. The government's Jal Jeevan Mission, announced in 2019 with ₹3.6 lakh crore allocation, aimed to provide tap water to every rural household by 2024. For Welspun, with its pipeline expertise from the group's oil & gas business and infrastructure development capabilities, this was a generational opportunity.

The Uttar Pradesh rural water supply project, covering 2,500 villages, became Welspun's showcase. The complexity was staggering: laying 10,000 kilometers of pipeline across diverse terrain, building 50 water treatment plants, and most challenging, creating a maintenance system for villages that had never had piped water. Welspun's approach combined high-tech—using GIS mapping and IoT sensors—with grassroots engagement, training local youth as maintenance technicians. The project's success led to more water contracts, establishing Welspun as a serious player in water infrastructure.

The oil & gas exploration venture with Adani through Adani Welspun Exploration Limited (AWEL) added another dimension. While infrastructure development was the core business, oil & gas exploration offered asymmetric returns—high risk but potentially massive rewards. Welspun's 35% stake in AWEL gave them exposure to multiple exploration blocks without the full capital commitment. By 2020, AWEL had discovered gas in Cambay Basin, validating the strategy.

What made this period remarkable wasn't just growth—revenues doubled from ₹1,500 crores to ₹3,000 crores—but quality of growth. Unlike the previous infrastructure boom that left companies overleveraged, Welspun maintained debt-to-equity under 1.5:1. Unlike peers who chased every opportunity, Welspun remained selective, bidding for maybe one in five projects they evaluated. A board member from this period notes: "The discipline to say no when everyone else was saying yes—that's what separated us."

By end-2020, Welspun Enterprises had transformed from a road developer that did some water projects to an integrated infrastructure developer equally comfortable with highways, water systems, and urban infrastructure. The order book exceeded ₹13,000 crores, providing visibility for five years. More importantly, they'd cracked the code on HAM projects, building a repeatable, scalable model for winning, executing, and monetizing them.

But the biggest decision was yet to come. The infrastructure assets they'd built over a decade were now mature, generating steady cash flows. Financial investors were offering astronomical valuations for operational infrastructure assets. The question was: should Welspun continue owning and operating these assets, or sell them and recycle capital into new opportunities? The answer would reshape the company's future.

VI. The Big Exit & Strategic Repositioning (2022–2023)

December 15, 2022, The Oberoi, Mumbai. Welspun Enterprises' board has just approved the largest transaction in the company's history: selling six operational highway projects to Actis LLP for $775 million (₹6,300 crores). In the boardroom, there's a moment of silence. These weren't just assets; they represented a decade of work, relationships, and reputation building. The Dewas-Bhopal corridor, the Delhi-Meerut stretch, the Gagalheri-Saharanpur-Yamunanagar highway—each had its story, its struggles, its victories. BK Goenka breaks the silence: "We're not selling our past. We're buying our future."

The Actis deal was eighteen months in the making. It began with informal conversations at an infrastructure conference in Singapore where Actis executives expressed interest in Indian road assets. What started as exploratory discussions became serious negotiations by mid-2022. The timing was perfect—or perfectly orchestrated. Global infrastructure funds were desperate for operational assets generating steady returns in a world of negative real interest rates. Indian road assets, with their inflation-linked toll increases and 15-20 year concessions, were exactly what they wanted.

But Welspun wasn't a distressed seller. The six projects were generating ₹800 crores in annual revenue with EBITDA margins exceeding 70%. The assets had minimal debt, stable cash flows, and years of concession remaining. Why sell? The answer lay in Welspun's understanding of capital efficiency and market cycles. A senior executive involved in the deal explains: "We could generate 15% returns by continuing to operate these roads. Or we could sell at valuations implying 8% returns to buyers, book massive profits, and redeploy capital into new projects generating 20%+ returns."

The valuation math was compelling. Welspun had invested approximately ₹2,000 crores in equity across these six projects over the years. The enterprise value of ₹6,300 crores, after adjusting for debt, meant equity value of roughly ₹4,500 crores—a 125% gain. But the real genius was in the structure. Welspun retained 13-20% stake in each project through co-investment vehicles, maintaining exposure to future upside while crystallizing immediate gains. They also secured long-term operations and maintenance contracts, ensuring continued revenue without capital lock-in.

The market reaction was swift and positive—the stock jumped 15% on announcement. But some analysts questioned the strategy. Why sell performing assets? What would Welspun do with ₹4,500 crores in cash? The answer came eight months later with the acquisition of Michigan Engineers.

August 2023. Welspun announces the acquisition of 50.1% stake in Michigan Engineers Private Limited for ₹137 crores. On surface, it seemed modest—Michigan was a mid-sized urban water infrastructure company with ₹500 crore revenue. But this was strategic brilliance disguised as a small acquisition. Michigan brought what Welspun lacked: urban water expertise, relationships with municipal corporations, and most crucially, proven technology for sewage treatment and water recycling.

The Michigan team had spent two decades perfecting the unglamorous but essential business of urban water management. They'd built sewage treatment plants for Pune, water recycling systems for Chennai, and stormwater management for Bangalore. Their expertise wasn't in laying pipes—Welspun could do that—but in designing integrated water systems for cities. With India's urban population expected to hit 600 million by 2030 and water stress affecting 21 major cities, this capability was invaluable.

The integration was swift and surgical. Within three months, Welspun-Michigan had bid for and won projects worth ₹2,000 crores, including a landmark 2,000 MLD (Million Liters per Day) water treatment plant for Mumbai's Bhandup Complex. The synergies were obvious: Welspun's execution capabilities and financial strength combined with Michigan's technical expertise and municipal relationships. A Michigan engineer who lived through the acquisition notes: "We'd been trying to bid for large projects for years but lacked balance sheet strength. Welspun solved that overnight."

The strategic repositioning went beyond acquisitions. Welspun restructured its entire organizational model, creating three distinct verticals: Highway Infrastructure, Water Infrastructure, and Urban Development. Each vertical had independent P&L responsibility, dedicated teams, and separate growth targets. The message was clear: Welspun wasn't just an infrastructure company but three specialized businesses under one roof.

The capital allocation framework post-Actis deal revealed sophisticated thinking. Of the ₹4,500 crores received: ₹1,000 crores went to debt reduction, bringing debt-to-equity to 0.5:1, the lowest among infrastructure peers. ₹1,500 crores was earmarked for new HAM road projects where Welspun's expertise commanded premium returns. ₹1,000 crores allocated to water infrastructure, recognizing the sector's growth potential. ₹500 crores for urban infrastructure opportunities, a new but promising area. The remaining ₹500 crores retained as strategic reserve for opportunistic acquisitions.

This wasn't just capital recycling—it was capital optimization. By selling mature assets at peak valuations and redeploying into higher-growth areas, Welspun was effectively arbitraging between different investor classes. Infrastructure funds like Actis wanted stable, operational assets and would pay premium valuations. Welspun wanted growth and was willing to take development risk for higher returns. Both got what they wanted.

The organizational transformation was equally important. Post-exit, Welspun shifted from asset owner to asset developer and manager. They created Welspun Infrastructure Management Services, offering O&M services not just for their projects but third-party assets too. The logic was simple: why own assets when you could generate fees managing them? By 2023-end, they were managing assets worth ₹15,000 crores while owning assets worth only ₹5,000 crores.

The strategy shift also showed in project selection. Pre-2022, Welspun would bid for any attractive HAM project. Post-2022, they became selective, focusing on projects with additional revenue potential—tolling rights, commercial development, or annuity escalations. They also started structuring deals with early exit options, planning from day one how they'd eventually monetize each asset.

By early 2024, the transformation was complete. Welspun Enterprises had evolved from an infrastructure developer that owned assets to a capital-light infrastructure platform that developed, monetized, and managed assets. Revenue had grown to ₹3,554 crores, but more importantly, Return on Equity had improved from 12% to 18%. The order book stood at ₹13,665 crores, providing five-year visibility. Most significantly, they'd proven that in Indian infrastructure, the real money wasn't in owning assets forever but in creating and recycling them intelligently.

VII. Modern Portfolio: Water, Roads & Energy

March 2024, Brihanmumbai Municipal Corporation (BMC) headquarters. Welspun has just won the contract for a 2,000 MLD water treatment plant at Bhandup Complex—Mumbai's largest water infrastructure project in two decades. The ₹3,000 crore project will serve 4 million residents, processing water from Mumbai's lakes through advanced filtration systems. In the same week, 1,500 kilometers north in rural Uttar Pradesh, Welspun's engineers are commissioning the 500th village under the Jal Jeevan Mission, bringing tap water to households that had relied on hand pumps for generations. This geographic and technological span—from cutting-edge urban water treatment to basic rural water supply—defines Welspun's modern portfolio.

The water infrastructure vertical, which contributed less than 10% of revenues in 2015, now accounts for 40% of the order book. The transformation began with a simple insight: India's water crisis wasn't one problem but three distinct challenges requiring different solutions. Urban areas needed treatment and recycling due to pollution and scarcity. Rural areas needed last-mile connectivity to bring existing water sources to households. Industrial zones needed specialized treatment for effluents and process water. Welspun built capabilities for all three.

The UP Jal Jeevan Mission project showcases the rural model. Covering 2,500 villages across six districts, the project involves laying 15,000 kilometers of pipeline, building 75 water treatment plants, and creating a digital monitoring system for water quality and supply. The complexity isn't just technical—it's social. Each village has different water sources, usage patterns, and local politics. Welspun's solution was radical decentralization. Instead of managing everything from Lucknow, they created cluster offices for every 50 villages, staffed by local engineers who understood regional dynamics.

The digital layer deserves attention. Every water connection has a smart meter transmitting consumption data. Water treatment plants have IoT sensors monitoring quality parameters. A control room in Lucknow tracks everything in real-time. When contamination was detected in a village in Gorakhpur district, the system automatically shut supply, alerted maintenance teams, and rerouted water from alternative sources—all within 30 minutes. This wasn't just infrastructure; it was intelligent infrastructure.

The Bhandup project represents the urban opportunity. Mumbai's water system, built during British rule and incrementally expanded, loses 30% of water to leakage and theft. The new treatment plant won't just process water but includes a complete overhaul of distribution infrastructure in eastern Mumbai. Advanced SCADA (Supervisory Control and Data Acquisition) systems will monitor pressure and flow at thousands of points, identifying leaks within hours instead of days. The project also includes Mumbai's first large-scale water recycling facility, treating sewage for non-potable uses.

The road portfolio, while mature, continues evolving. The focus has shifted from pure highway development to complex urban corridors and expressways. The Tamil Nadu elevated corridor project, now 60% complete, demonstrates this evolution. Building 26 kilometers of elevated highway through populated areas requires skills beyond traditional road construction—utility relocation, traffic management during construction, and managing thousands of affected property owners. Welspun's approach combines engineering excellence with stakeholder management, maintaining dedicated community liaison offices and grievance redressal systems.

The HAM model execution has been refined to near perfection. Welspun now completes most projects 3-6 months ahead of schedule, earning early completion bonuses and improving IRRs by 200-300 basis points. The secret isn't working faster but planning better. They now spend 6-9 months in pre-construction planning, twice the industry average. Detailed soil surveys, advance procurement of critical materials, and pre-qualification of contractors eliminate most execution surprises. A project director explains: "We learned that spending an extra ₹10 crores in planning saves ₹50 crores in execution."

The oil & gas vertical through Adani Welspun Exploration Limited continues as a long-term option. The Cambay Basin discovery is progressing toward commercial production, with gas reserves estimated at 50 BCF (billion cubic feet). While modest by global standards, at current gas prices, this could generate ₹2,000 crores in revenue over the field's life. More exploration blocks are being evaluated, but Welspun's exposure is calibrated—never more than 10% of capital employed, treating it as venture investment rather than core business.

The newest addition to the portfolio is urban infrastructure beyond water. Welspun is now bidding for integrated urban development projects—townships, industrial parks, and logistics hubs. The Dholera Special Investment Region project in Gujarat, where Welspun is developing infrastructure for a 22.5 square kilometer industrial zone, represents this ambition. It combines everything Welspun has learned—roads, water, sewerage, power infrastructure—into integrated offerings.

Financial performance reflects portfolio evolution. Q1 FY2024 numbers show revenues of ₹3,554 crores with EBITDA margins of 23.9%—exceptional for infrastructure. But segment analysis is more revealing: Water infrastructure: 35% of revenue, 28% EBITDA margin. Road development: 50% of revenue, 22% EBITDA margin. Urban infrastructure: 10% of revenue, 20% EBITDA margin. O&M services: 5% of revenue, 40% EBITDA margin.

The margin expansion in O&M services validates the asset-light strategy. Managing ₹15,000 crores of third-party assets generates ₹200 crores in annual fees with minimal capital investment. Welspun has created India's largest independent infrastructure O&M platform, managing everything from toll collection to water treatment plants. The recurring revenue provides stability while development projects drive growth.

Risk management has evolved with the portfolio. Each vertical has independent risk frameworks reflecting different challenges. Water projects face technology risk—treatment processes must meet stringent standards. Road projects face execution risk—delays cost money. Urban projects face stakeholder risk—multiple agencies must coordinate. The company now maintains a ₹500 crore contingency fund, has credit lines worth ₹1,000 crores, and most importantly, never commits more than 30% of capital to a single project.

The order book of ₹13,665 crores provides remarkable visibility—five years of revenue at current execution rates. But composition matters more than size: 45% is water infrastructure, reflecting sector focus. 60% is government contracts with sovereign guarantee. 70% is HAM/annuity-based, ensuring predictable cash flows. 80% is in states where Welspun has prior execution experience.

Looking at Welspun's modern portfolio, you see a company that has mastered the art of platform building. They're not just executing projects but creating repeatable, scalable models for different infrastructure verticals. Each vertical has achieved critical mass, specialized expertise, and independent growth trajectory. This isn't diversification for its own sake but strategic positioning for India's multi-decade infrastructure opportunity.

VIII. Operating Philosophy & Execution Playbook

Inside Welspun's project monitoring room in Mumbai, fifty screens display real-time data from construction sites across India. A excavator in Tamil Nadu has been idle for 47 minutes—a notification pops up. Concrete pouring in UP is running two hours behind schedule—the system automatically alerts backup suppliers. This command center, operational 24/7, embodies Welspun's operating philosophy: infrastructure development is won not through grand strategies but through relentless execution of thousands of small details.

The asset-light model that Welspun pioneered isn't about avoiding assets—it's about optimizing capital velocity. Traditional infrastructure companies follow a build-own-operate model, tying up capital for 15-30 years in single projects. Welspun follows build-operate-monetize-redeploy, turning over capital every 5-7 years. A board member explains the math: "If we generate 18% IRR and turn capital twice in 10 years, effective returns are 40%+. That's the power of capital velocity."

But asset-light doesn't mean risk-light. Welspun takes concentrated development risk, betting their reputation and capital on delivering projects on time. Their mitigation strategy is over-preparation. Before bidding for any project, they conduct what they call "murder boards"—sessions where teams try to kill the project by identifying everything that could go wrong. Only projects that survive this scrutiny move forward. Of 100 projects evaluated, maybe 5 reach bidding stage, and they win 1 or 2. This 1-2% conversion seems inefficient until you realize their project success rate exceeds 95%.

The execution playbook has seven pillars, each refined over hundreds of projects:

Pre-construction Intelligence: Welspun spends 10-15% of project cost before construction begins. Detailed topographical surveys using LIDAR technology, soil testing every 500 meters, utility mapping using ground-penetrating radar. They maintain a database of 10,000+ contractors, rated on 15 parameters from financial strength to safety records. Material procurement begins 6 months before needed, locking in prices and ensuring availability. This front-loading seems expensive until you see competitors facing 20-30% cost overruns from poor planning.

Stakeholder Orchestration: Every project has what Welspun calls a "Stakeholder Map"—identifying everyone from the Chief Minister to the village headman who could impact execution. Each stakeholder gets a customized engagement plan. Senior politicians get quarterly presentations on progress. Local administrators get monthly updates. Village leaders get weekly meetings. Affected families get daily interaction through help desks. A former bureaucrat who worked with Welspun notes: "They understood that in infrastructure, technical competence is necessary but political management is sufficient."

Financial Engineering: Each project is structured to minimize capital lock-in while maintaining control. Typical structure: Welspun invests 26% equity, brings financial partners for 51%, and suppliers/contractors for 23%. But control is maintained through shareholder agreements giving Welspun veto rights on key decisions. Debt is structured with moratoriums during construction, step-up pricing post-completion, and refinancing options when projects stabilize. They maintain relationships with 15 banks and 10 NBFCs, ensuring competitive financing.

Technology Integration: Welspun spends ₹50 crores annually on technology—unusual for an infrastructure company. Every project uses Building Information Modeling (BIM) for design, drones for progress monitoring, and IoT sensors for quality control. The real innovation is data integration. The Mumbai command center receives 10,000+ data points daily from projects, analyzed using ML algorithms to predict delays, identify bottlenecks, and optimize resource allocation. When concrete strength at a UP site showed anomalies, the system flagged it before structural work began, preventing potential disaster.

Quality Obsession: Welspun maintains independent quality teams reporting directly to the CEO, not project directors. Every project has third-party quality auditors with unscheduled inspection rights. They've documented 500+ Standard Operating Procedures covering everything from concrete mixing ratios to document filing systems. Quality costs add 3-5% to project expenses but reduce rework and warranty claims by 10-15%. A competitor CEO grudgingly admits: "Welspun projects might not be cheapest, but you know they'll last the concession period."

Government Relations: Managing government relationships in infrastructure requires delicate balance—close enough to understand requirements, distant enough to maintain independence. Welspun's approach is institutional, not personal. They maintain regular interaction schedules with ministries, sharing industry insights and policy feedback. They've never been involved in major controversies or regulatory violations. When policies change—like the shift from BOT to HAM—they adapt quickly rather than fighting changes.

Capital Recycling Discipline: The decision to hold or sell assets follows a clear framework. Assets are held during development and initial operations (years 0-5) when value creation is highest. Once operational stability is achieved and yields compress (years 5-7), they look for exits. Sales are timed for maximum value—typically when infrastructure funds are raising new funds and need to deploy capital quickly. They maintain relationships with 20+ potential buyers, ensuring competitive tension in sales.

The December 2022 Actis deal exemplified this playbook. Welspun began preparing for sale 18 months before, getting independent traffic studies, cleaning up documentation, and resolving all pending disputes. When Actis expressed interest, five other funds were simultaneously engaged, creating competitive dynamics. The final price—14x EBITDA—was 20% above initial expectations.

Risk management permeates everything. Welspun maintains contingencies at multiple levels: 10% cost contingency in project budgets, 6-month liquidity buffer in corporate treasury, ₹1,000 crores in unutilized credit lines. They hedge commodity prices for major materials, have backup suppliers for critical components, and maintain insurance coverage exceeding industry standards. During COVID-19, when construction stopped nationwide, Welspun had sufficient liquidity to pay workers for three months without revenue—earning loyalty that paid dividends when work resumed.

The working capital management shows operational excellence. Despite industry working capital cycles of 150-180 days, Welspun maintains 90-100 days through aggressive collection, vendor financing, and inventory optimization. They've implemented SAP across operations, enabling real-time tracking of payables and receivables. Monthly CFO reviews with project teams ensure focus on cash conversion. A banker who works with multiple infrastructure companies notes: "Welspun's working capital discipline is exceptional. They treat cash like oxygen."

Human capital strategy reflects long-term thinking. Welspun has 500+ engineers, 70% with 10+ years experience. They poach selectively from competitors but focus on internal development. The Welspun Infrastructure Academy trains 100 engineers annually in project management, financial modeling, and stakeholder management. Retention rates exceed 85%, unusual in infrastructure where poaching is endemic. Compensation includes project bonuses and phantom equity in SPVs, aligning incentives.

The result is an execution machine that delivers predictably in an unpredictable sector. Over the last decade, Welspun has completed 50+ projects worth ₹20,000 crores. Average delay: 2 months versus industry average of 12 months. Average cost overrun: 5% versus industry 20%. These aren't just statistics—they're competitive advantages that compound over time.

IX. Competitive Analysis & Market Position

The infrastructure sector conference at the Taj Mahal Hotel, New Delhi, 2023. During the coffee break, CEOs from India's top infrastructure companies cluster in familiar groups. The L&T and GMR executives discuss mega-projects and international expansion. The regional players from PNC Infratech and Dilip Buildcon compare notes on state government relationships. And then there's Welspun's team, comfortable moving between groups but belonging fully to none. This positioning—neither infrastructure giant nor regional specialist—defines both Welspun's competitive challenge and its opportunity.

Understanding Welspun's market position requires mapping India's infrastructure landscape. At the top sit giants like L&T, with ₹50,000+ crore revenues, executing everything from metros to nuclear plants. Below them are specialized nationals like IRB Infrastructure (toll roads) and NCC Limited (buildings and roads). Then come regional champions like PNC Infratech (North India focus) and Dilip Buildcon (Madhya Pradesh stronghold). Welspun, with ₹3,500 crore revenue, sits in the middle—large enough to bid for major projects, small enough to be nimble.

Let's examine key competitors:

PNC Infratech (Market Cap: ₹8,500 crores): The closest comparable to Welspun. Similar revenue (₹4,000 crores), similar focus (HAM roads and water), similar strategy (asset-light). But dig deeper and differences emerge. PNC is execution-focused, taking EPC projects for quick returns. Welspun is development-focused, taking longer-term positions for higher IRRs. PNC maintains 2:1 debt-to-equity accepting lower ROE for volume. Welspun maintains 0.5:1 debt-to-equity, prioritizing returns over growth. In the 2023 NHAI awards, PNC won 8 projects worth ₹12,000 crores; Welspun won 3 worth ₹5,000 crores. But Welspun's projects had better terms and locations.

Dilip Buildcon (Market Cap: ₹6,000 crores): The regional specialist generating ₹5,000 crore revenue, 80% from three states. Their strategy is political arbitrage—deep relationships with state governments enabling them to win projects others can't. They'll take mining roads in Chhattisgarh that others won't touch. But this focus is also weakness—political changes can destroy the business model overnight. Welspun's geographic diversification across 15 states provides resilience Dilip Buildcon lacks.

IRB Infrastructure (Market Cap: ₹15,000 crores): The toll road specialist operating India's largest portfolio of BOT projects. IRB's model is pure ownership—they build and operate forever, generating ₹7,000 crores annual revenue from tolls. This seemed brilliant during the 2000s boom but became an albatross when traffic growth slowed. IRB's debt exceeds ₹50,000 crores; interest costs consume 60% of operating profit. Welspun's capital recycling model avoided this trap, maintaining flexibility IRB lost.

Ashoka Buildcon (Market Cap: ₹2,500 crores): The cautionary tale. Once a ₹5,000 crore revenue company with ambitious BOT projects, Ashoka overleveraged during the infrastructure boom. When projects underperformed, debt became unsustainable. They've spent five years restructuring, selling assets at distressed valuations. Ashoka proves Welspun's conservative financing wasn't overcautious but prescient.

The competitive dynamics reveal three strategic groups:

Scale Players (L&T, GMR): Compete on capability breadth and balance sheet strength. They win mega-projects others can't execute but accept lower margins for volume. Welspun doesn't compete directly, focusing on mid-sized projects with better economics.

Regional Specialists (Dilip Buildcon, regional contractors): Compete on local relationships and cost. They'll underbid to maintain utilization but struggle with technology and quality. Welspun targets projects where quality matters more than lowest price.

Financial Engineers (IRB, Cube Highways): Compete on capital access and structuring skills. They'll pay aggressive prices for assets betting on financial optimization. Welspun sells to them at peak valuations, recycling capital into development.

Welspun's positioning is deliberate: the "intelligent executor"—more sophisticated than regional players, more focused than giants, more flexible than asset owners. This shows in win rates. In competitive HAM bidding where 10+ players participate, Welspun wins 15-20% of bids versus 8-10% industry average. They achieve this not through aggressive pricing but superior pre-qualification scores based on execution track record.

The water infrastructure market reveals Welspun's differentiation. While competitors treat water as roads-with-pipes, Welspun understands water requires different capabilities—treatment technology, quality management, community engagement. The Michigan Engineers acquisition gave them expertise others lack. In the 2024 Jal Jeevan Mission awards, Welspun won projects in four states; most competitors won in one or two. Geographic diversification plus technical expertise equals competitive advantage.

Market share analysis shows Welspun's selective growth: - HAM roads: 5% market share but 8% of profits (better project selection) - Water infrastructure: 3% of projects but 7% of value (larger, complex projects) - O&M services: 10% of outsourced O&M (fastest-growing segment)

FY2024 performance validates the strategy. Revenue grew 24.78% to ₹3,584 crores while maintaining 23.9% EBITDA margins—industry-leading profitability. Compare this to peers: PNC Infratech: 30% revenue growth, 15% margins (volume over value). Dilip Buildcon: 20% growth, 12% margins (commoditized execution). IRB: 10% growth, 70% margins (toll roads are cash cows but not growing).

The order book composition shows strategic focus: - Welspun: ₹13,665 crores, 60% water and urban (future growth areas) - PNC: ₹15,000 crores, 80% roads (traditional but competitive) - Dilip Buildcon: ₹12,000 crores, 70% state projects (political risk)

Working capital metrics reveal operational differences: - Welspun: 92 days (up from 36 but manageable) - PNC: 120 days (volume pressure on working capital) - Dilip Buildcon: 150 days (state governments pay slowly)

The government's infrastructure push—₹111 lakh crores planned investment—benefits everyone, but Welspun is uniquely positioned. They have execution credibility for government projects, relationships with financial investors for PPPs, and technical capabilities for complex urban and water infrastructure. While competitors fight for traditional road projects, Welspun targets higher-margin niches.

The bear case on competition is real: barriers to entry in infrastructure are falling. Chinese construction equipment reduced capital requirements. HAM model reduced financing needs. Digital tools democratized project management. New entrants like Adani and GR Infraprojects are growing aggressively. The pie is growing but so are the number of players eating it.

Welspun's response is moving up the complexity curve. Simple road projects will commoditize; integrated urban development won't. Basic water supply will see competition; advanced treatment won't. They're building capabilities competitors will take years to replicate. The Michigan acquisition wasn't just buying revenue but buying a decade of learning.

The market recognizes this differentiation partially. At 18x P/E, Welspun trades at premium to PNC (15x) and Dilip Buildcon (12x) but discount to IRB (25x). The market values asset ownership (IRB) over asset development (Welspun), despite development generating higher returns. This valuation gap—between market perception and business reality—creates opportunity for patient investors.

X. Bear vs. Bull Investment Case

The investment committee meeting at a Mumbai mutual fund, 2024. The infrastructure analyst is presenting Welspun Enterprises. "Revenue growing 25%, margins expanding, debt reducing," she begins. The value investor interrupts: "ROE is just 13.4% over three years. Why should we pay 18x earnings for a 13% return business?" The growth investor counters: "Order book provides five-year visibility, water infrastructure is a multi-decade opportunity." The risk manager adds: "Working capital deteriorated from 36 to 92 days. What if it gets worse?" This debate—between evident opportunity and legitimate concerns—defines the Welspun investment dilemma.

The Bull Case

The bull thesis rests on five pillars, each compelling individually, powerful collectively:

India's Infrastructure Megatrend: The numbers are staggering—₹111 lakh crore infrastructure investment planned through 2030. Breaking it down: ₹36 lakh crores for highways, ₹25 lakh crores for railways, ₹20 lakh crores for urban infrastructure, ₹10 lakh crores for water and sanitation. This isn't political rhetoric but budgeted allocation. The government's capital expenditure rose from ₹4.5 lakh crores to ₹11.1 lakh crores in five years. Infrastructure's share of GDP must rise from 4.5% to 7% for India to sustain 7%+ growth. Welspun, with proven execution and government relationships, will capture disproportionate share.

Water Infrastructure Explosion: India's water crisis is existential—21 cities face Day Zero scenarios, 600 million people face water stress, agricultural productivity threatened. The Jal Jeevan Mission's ₹3.6 lakh crore allocation is just the beginning. Urban water infrastructure needs ₹5 lakh crores investment. Industrial water treatment, a ₹50,000 crore market, grows 15% annually. Welspun's early positioning through Michigan Engineers and rural water projects gives them first-mover advantage in a market that will define the next decade.

Capital Recycling Model Validation: The Actis transaction proved Welspun can create and monetize infrastructure assets at attractive returns. They invested ₹2,000 crores, sold for ₹6,300 crores enterprise value, retained partial stakes for upside. This isn't one-time; it's repeatable. Global infrastructure funds have $500 billion dry powder seeking operational assets. Indian infrastructure offers 12-15% dollar returns versus 6-8% in developed markets. Welspun becomes the manufacturing engine for financial investors' deployment needs.

Execution Track Record: In infrastructure, past performance actually indicates future results because reputation matters. Welspun's 95% on-time completion rate, 5% cost overrun versus 20% industry average, zero major disputes in a decade—these create compounding advantages. Government agencies prefer proven executors. Banks offer better terms. Partners choose reliable operators. This reputation moat, built over decades, can't be replicated with capital alone.

Valuation Disconnect: At ₹6,400 crore market cap, Welspun trades at 1.8x book value, 18x P/E, 8x EV/EBITDA. Compare this to global infrastructure developers: Ferrovial (25x P/E), Vinci (15x P/E), but growing 5% versus Welspun's 25%. The market values Welspun like a construction company, not an infrastructure developer. As the business model becomes understood, multiple expansion is likely.

The sum-of-parts valuation reveals hidden value: - Road development business: ₹3,000 crores (10x EBITDA) - Water infrastructure: ₹2,500 crores (12x EBITDA) - O&M platform: ₹1,000 crores (20x EBITDA) - Stakes in operational assets: ₹1,500 crores (market value) - Total: ₹8,000 crores versus ₹6,400 crore market cap

The Bear Case

But bears have legitimate concerns that bulls must address:

ROE Problem: 13.4% average ROE over three years is mediocre. Yes, it's improving—18% in latest quarter—but historical performance matters. Infrastructure is capital-intensive; if you can't generate 20%+ ROE consistently, why not invest in asset-light businesses? The capital recycling model should improve ROE, but proof requires multiple cycles, not one transaction.

Working Capital Deterioration: Days sales outstanding increased from 36 to 92 days—alarming deterioration. Government payments are slowing, projects are getting complex, cash conversion is weakening. If working capital days hit 150 (industry average), Welspun needs ₹1,000 crores additional funding. In infrastructure, working capital problems can spiral quickly.

Execution Risk Concentration: Welspun's order book is concentrated—top 5 projects are 60% of backlog. One major project failure—delays, cost overruns, disputes—could damage reputation and finances. Infrastructure projects are binary: succeed and make 15% IRR, fail and lose everything. Diversification helps but doesn't eliminate project-specific risks.

Government Dependency: 80% of revenues from government contracts creates political risk. Policy changes, like the abrupt BOT to HAM shift, can disrupt business models. Payment delays are endemic—state governments owe contractors ₹2 lakh crores. Election cycles create volatility—new governments review previous contracts. Welspun navigates this well, but swimming against political currents is exhausting.

Competition Intensifying: Barriers to entry are falling. Adani's infrastructure ambitions, GR Infraprojects' aggressive growth, Chinese companies entering through subcontracting—competition is intensifying. HAM projects attract 15-20 bidders versus 5-7 previously. Margins will compress as competition increases. Welspun's differentiation is real but eroding.

Capital Allocation Questions: Welspun has ₹4,500 crores from Actis sale. Deploying this productively is challenging. Infrastructure projects have long gestation—2 years construction, 3 years stabilization. If deployment is slow, ROE suffers. If deployment is fast, execution risk increases. The Michigan acquisition was small; they need larger moves to deploy capital, increasing risk.

The Balanced View

The truth, as always, lies between extremes. Welspun is neither the perfect infrastructure play bulls claim nor the problematic contractor bears fear. It's a company in transition—from contractor to developer, from asset-heavy to asset-light, from roads to water—and transitions are messy.

The bull case is stronger medium-term (3-5 years). India's infrastructure build-out is inevitable, water infrastructure is nascent, and Welspun's positioning is favorable. The bear concerns are valid short-term (1-2 years). Working capital needs management, competition will pressure margins, and capital deployment takes time.

The investment decision depends on time horizon and risk tolerance: - For short-term investors: Wait for working capital improvement and capital deployment clarity - For long-term investors: Current valuation offers attractive entry for a multi-year infrastructure story - For risk-averse investors: The 13% ROE and government dependency are concerning - For growth investors: 25% revenue growth with 24% margins in infrastructure is exceptional

The key monitorables going forward: 1. Working capital days—must stabilize below 100 2. Capital deployment—₹2,000 crores annually minimum 3. Water infrastructure traction—should exceed 50% of order book 4. ROE improvement—sustainable 18%+ needed 5. Further asset monetization—proves model repeatability

Ultimately, Welspun Enterprises is a bet on India's infrastructure future and management's ability to navigate complexity. The opportunity is real, the execution credible, but the risks non-trivial. Like infrastructure development itself, investing in Welspun requires patience, conviction, and tolerance for volatility.

XI. Future Strategy & Vision

The strategy presentation to institutional investors, Mumbai, 2024. Welspun's CEO stands before a slide showing India's map covered in dots—blue for water projects, black for roads, green for urban infrastructure. "By 2030," he says, "we envision Welspun as India's integrated infrastructure platform—not the largest, but the most intelligent. Every infrastructure project will have three components: physical assets we build, digital systems we integrate, and sustainable solutions we implement. We're not just building infrastructure; we're building the operating system for India's growth."

This vision—ambitious yet grounded—reflects Welspun's understanding of infrastructure's evolution. The next decade won't just be about building more but building smarter. Climate change, urbanization, and digitalization will reshape infrastructure requirements. Companies that adapt will thrive; others will become contractors competing on price.

The ESG Transformation

Welspun's future strategy begins with ESG, not as compliance but as competitive advantage. They're targeting Net Zero by 2040, ambitious for an infrastructure company. But the pathway is pragmatic: solar panels on toll plazas generating 50MW by 2025, electric vehicle charging stations at all rest stops, and water recycling in every project reducing consumption 30%. The Bhandup water treatment plant will be India's first carbon-neutral water facility, using biogas from sewage treatment to power operations.

The social component focuses on community development. Every project now includes skill development for 100+ local youth, healthcare camps reaching 10,000+ families, and women's self-help groups creating alternate livelihoods. This isn't charity—it's risk mitigation. Communities that benefit from projects protect them. The UP water project has zero vandalism incidents versus 10-15% industry average because villagers see it as their infrastructure, not government's.

Governance improvements target international standards. Welspun is implementing TCFD (Task Force on Climate-related Financial Disclosures) reporting, unusual for Indian infrastructure. They're creating independent project oversight boards with external experts. Most significantly, they're linking executive compensation to ESG metrics—30% of variable pay depends on safety, environmental, and community scores.

Technology as Differentiator

The digital transformation strategy has three pillars:

Predictive Infrastructure: Using AI/ML to predict maintenance needs before failures occur. Sensors on bridges detect stress patterns, algorithms predict when maintenance is needed, preventing catastrophic failures. The Tamil Nadu elevated corridor has 10,000+ sensors generating 1TB daily data. Early results show 40% reduction in maintenance costs, 60% reduction in downtime.

Digital Twin Development: Creating virtual replicas of physical infrastructure. Before building, engineers test dozens of scenarios virtually. During operations, digital twins enable real-time optimization. The Bhandup plant's digital twin simulates water flow, chemical dosing, and energy consumption, optimizing operations to save ₹50 crores annually.

Integrated Operations Platform: Building India's first Infrastructure-as-a-Service platform. Instead of managing individual assets, Welspun will offer integrated management—monitoring, maintenance, optimization—for any infrastructure. Think of it as AWS for infrastructure. Government agencies and private owners can plug assets into Welspun's platform, paying for outcomes not activities.

Capital Allocation 2.0

The post-Actis capital deployment strategy reveals sophisticated thinking:

Water Infrastructure Dominance (₹2,000 crores): Target 30% market share in organized water infrastructure by 2030. Focus on complex urban projects where technology and expertise matter. Build capabilities in desalination and water recycling for water-scarce regions. Create India's first water infrastructure REIT, allowing retail participation in water assets.

Urban Infrastructure Platform (₹1,500 crores): Partner with state governments for integrated city development. Focus on 20 tier-2 cities undergoing rapid urbanization. Develop expertise in smart city technologies—intelligent traffic management, integrated command centers, IoT-enabled utilities. Position as master developer for industrial corridors and logistics parks.

Green Energy Infrastructure (₹1,000 crores): Develop renewable energy assets alongside traditional infrastructure. Solar canopies over canals, wind turbines along highways, pumped hydro storage at water projects. Target 500MW renewable capacity by 2030, making Welspun energy-positive.

International Expansion (₹500 crores): Selective entry into adjacent markets—Bangladesh, Sri Lanka, Nepal—leveraging India's infrastructure diplomacy. Focus on water projects where India's experience is relevant. Partner with Export-Import Bank for financing, reducing capital requirements.

Organizational Evolution

The human capital strategy recognizes infrastructure's changing needs. Welspun is hiring differently—data scientists alongside civil engineers, sustainability experts alongside project managers. The Welspun Infrastructure Academy is partnering with IITs to create specialized courses in infrastructure technology. They're implementing an ESOP program covering all employees, unusual in infrastructure, aligning everyone with long-term value creation.

The organizational structure is evolving from hierarchical to networked. Instead of vertical silos, Welspun is creating cross-functional teams for each project. The Bhandup project has engineers, data analysts, community specialists, and financial experts working together from conception. This matrix structure is messier but more innovative.

Strategic Partnerships

Welspun recognizes that future infrastructure requires capabilities beyond any single company. Strategic partnerships being explored:

- Technology partnership with Microsoft for AI/IoT integration

- Financial partnership with Canadian pension funds for long-term capital

- Technical partnership with Veolia for advanced water treatment

- Innovation partnership with IIT Bombay for infrastructure research

Risk Management Evolution

Future risks require new frameworks:

Climate Risk: Every project now includes climate scenario analysis. How will assets perform if temperatures rise 3°C? If rainfall patterns shift? If extreme weather increases? Projects are designed for 100-year events becoming 20-year events.

Cyber Risk: As infrastructure digitizes, cyber threats increase. Welspun is building India's first Infrastructure Security Operations Center, monitoring digital threats across assets. They're implementing zero-trust architecture, assuming breach and limiting damage.

Regulatory Risk: Anticipating rather than reacting to policy changes. Welspun maintains a regulatory intelligence unit tracking global infrastructure policies, predicting Indian adoption. They saw the shift to HAM two years early, positioning accordingly.

The 2030 Vision

By 2030, Welspun envisions: - Revenue of ₹15,000 crores (4x current) - EBITDA margins of 30% (vs 24% current) - ROE of 25% (vs 13% historical) - 50% revenues from water and urban infrastructure - 30% revenues from recurring O&M and digital services - Operations across 10 countries - Managing ₹100,000 crores of infrastructure assets

This isn't unbridled optimism but calculated ambition. The infrastructure opportunity is massive, Welspun's capabilities are proven, and their strategy is differentiated. The challenge is execution—maintaining quality while scaling, preserving culture while growing, and staying disciplined while opportunities abound.

The path forward isn't without risks. Technology could disrupt traditional infrastructure. Climate change could strand assets. Political shifts could change priorities. Competition could compress returns. But Welspun's adaptive capacity—shown through multiple pivots from textiles to construction to development—suggests they'll navigate challenges.

Ultimately, Welspun's future depends on India's future. If India grows at 7%+, urbanizes rapidly, and addresses climate change, infrastructure demand will exceed supply for decades. Welspun, positioned at the intersection of traditional infrastructure and modern technology, could become India's infrastructure platform—not the largest but the most valuable.

XII. Key Takeaways & Lessons

As our deep dive into Welspun Enterprises concludes, it's worth stepping back from the details—the HAM models and EBITDA margins, the water projects and highway corridors—to understand what this company's journey really teaches us about building businesses in India's complex infrastructure landscape.

The Power of Strategic Pivots

Welspun's history is essentially a series of calculated pivots, each timed to capture emerging opportunities while avoiding declining ones. From MSK's pure construction to BOT development, from BOT to HAM, from roads to water, from asset ownership to asset recycling—each pivot was executed before forced by circumstances. The lesson isn't that constant change is good but that strategic flexibility matters more than rigid focus in dynamic markets.

Consider the 2013 decision to transfer EPC operations to Leighton Welspun. Conventional wisdom said keep everything in-house for control. Welspun chose capital efficiency over control, freeing resources for higher-return development projects. The 2022 Actis sale followed similar logic—selling performing assets at peak valuations to redeploy into emerging opportunities. This intellectual flexibility—holding strong views weakly—separates winners from survivors in infrastructure.

Capital Recycling as Competitive Advantage

The infrastructure sector globally is littered with companies that built great assets then couldn't let go. They became museums of past success rather than engines of future growth. Welspun cracked the code: infrastructure development is manufacturing, not collecting. Build assets, prove their value, sell to long-term holders, redeploy capital. Rinse and repeat.

This model requires capabilities beyond engineering—understanding capital markets, timing cycles, managing stakeholder transitions. It also requires discipline to sell performing assets when every instinct says hold. The Actis transaction wasn't just a sale but a statement: Welspun is a capital allocator that happens to build infrastructure, not a builder that happens to allocate capital.

Trust as Infrastructure

In a sector where projects span election cycles, involve thousands of stakeholders, and require government approvals at every stage, trust becomes infrastructure itself—invisible but essential. Welspun's investment in relationships—from village headmen to union ministers—isn't networking but building social infrastructure that enables physical infrastructure.

This shows in small details: paying workers during COVID lockdown, honoring contracts despite cost escalations, completing projects despite payment delays. These decisions, individually expensive, collectively create reputation—the ultimate moat in infrastructure. When Welspun bids for projects, their reputation enters the room before their proposal.

Managing Complexity Through Simplicity

Infrastructure projects are inherently complex—thousands of variables, hundreds of stakeholders, dozens of failure points. Welspun's response isn't more complexity but radical simplification. Standard operating procedures for repeatable tasks. Single points of accountability for decisions. Clear escalation matrices for problems. The Mumbai command center monitoring all projects isn't about control but pattern recognition—identifying what's signal versus noise.

This operational philosophy extends to strategy. While competitors diversify into airports, ports, mining, and real estate, Welspun focuses on roads, water, and urban infrastructure. While others chase every opportunity, Welspun maintains strict filters—government counterparty, annuity-based returns, proven geographies. Simplicity in strategy enables excellence in execution.