Waaree Energies: The Solar King of Bharat

I. Introduction: The "Intel" of Indian Solar

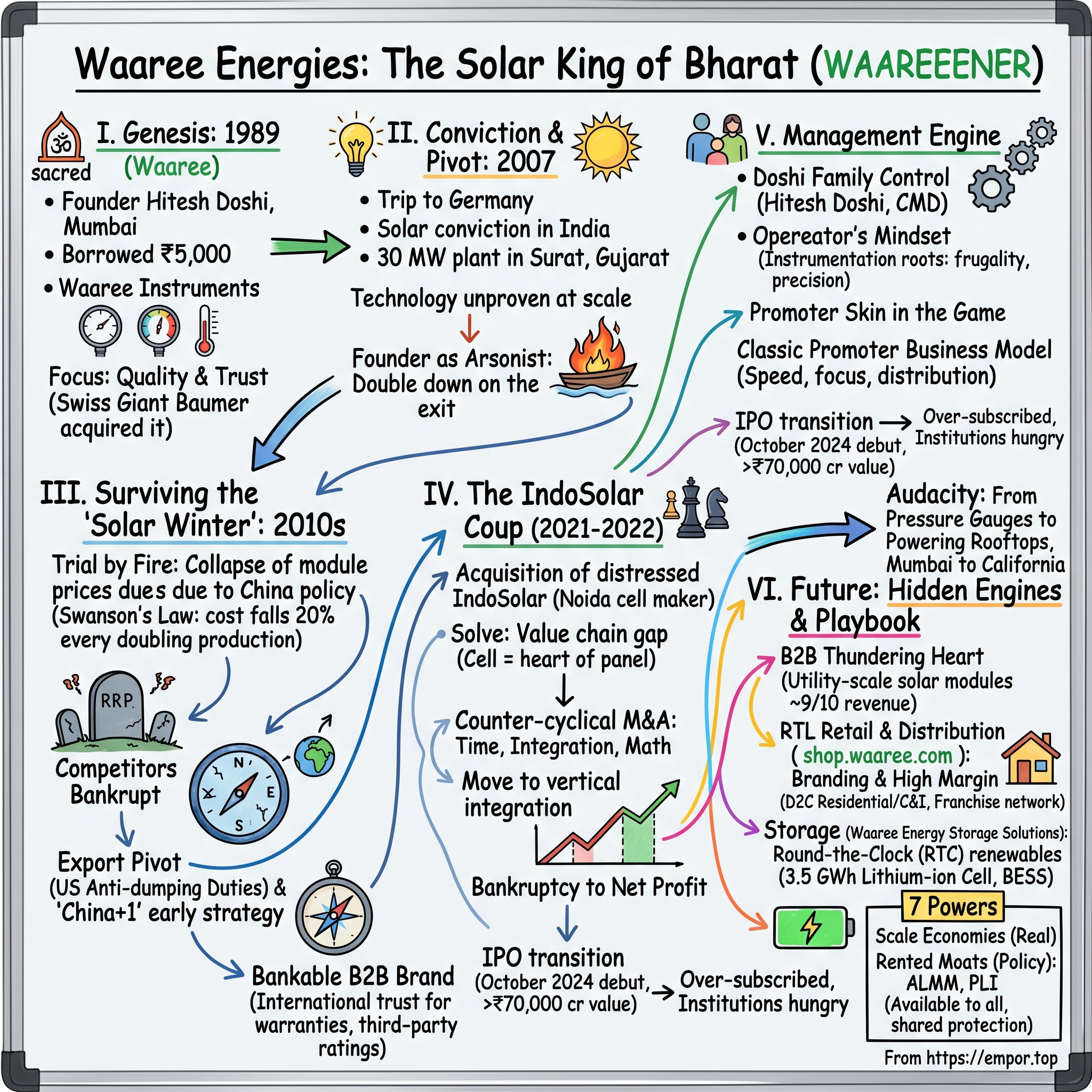

Stand on the rooftop of almost any large warehouse, factory, or government building in India today and look up. There is a decent chance the slab of dark blue glass soaking up the brutal subcontinental sun carries a small logo you may never have noticed: a stylized sun, and the word Waaree. It is not a household name in the way that टाटा Tata or रिलायंस Reliance Industries are. You cannot buy a Waaree phone or fill your car with Waaree fuel. And yet, in the single most important industrial story unfolding in India right now — the race to electrify a billion-and-a-half people without choking the planet — वारी एनर्जीज Waaree Energies has quietly become the largest player on the field.

Here is the headline number that frames everything: as of fiscal year 2025, Waaree operated roughly 12 gigawatts of installed solar module manufacturing capacity, making it the single biggest solar panel maker in India by a wide margin, and one of the larger ones outside China.1 To put that in human terms, a gigawatt is roughly the output of a large conventional power station. Twelve gigawatts of annual manufacturing capacity means Waaree can stamp out enough solar panels every year to, in theory, build a dozen power plants' worth of generation — and it is racing to nearly double that.

This is the kind of company Acquired loves precisely because it provokes an uncomfortable question. On paper, a solar module is a commodity. It is glass, aluminum, silicon, and copper assembled in a sequence that hundreds of factories around the world can replicate. Commodities are supposed to be terrible businesses — price-takers, margin-compressors, value-destroyers. So how did a firm that started life selling pressure gauges out of a one-room Mumbai office become a company that, on its 2024 stock market debut, was worth more than ₹70,000 crore — over $8 billion — and was hailed as a "coming out party" for Indian manufacturing?[^2]

The answer is the thesis of this episode. Waaree is not really a commodity manufacturer that got lucky. It is a story about timing, survival, and policy — about a founder who bet his entire successful business on an unproven technology in 2007, nearly got wiped out by a flood of Chinese imports, found an escape valve in the American export market, and then waited, patiently, for the Indian state to decide that solar manufacturing was a matter of national security. When that moment arrived under the banner of आत्मनिर्भर भारत Atmanirbhar Bharat — self-reliant India — Waaree was the company standing in exactly the right place, with exactly the right capacity, at exactly the right time.

The recurring Acquired theme we will test throughout: is this a low-margin commodity business dressed up in a growth-stock costume, or is it a genuine strategic national champion sitting on a structural moat? The honest answer, as you will see, is that it is both at once — and the tension between those two truths is the most interesting thing about the company. Let us start where every good origin story starts: with a man, a borrowed sum of money, and a problem nobody else wanted to solve.

II. The Genesis: From Pressure Gauges to Photovoltaics

Mumbai, 1989. The Indian economy was still two years away from the liberalization reforms that would unshackle it. Licenses governed everything, foreign exchange was scarce, and the idea of a self-made industrialist building a global business from scratch was, frankly, a fantasy for most. Into this world stepped हितेश चिमनलाल दोशी Hitesh Chimanlal Doshi, a young Gujarati trader with very little capital and a great deal of nerve. The number that gets repeated in nearly every retelling of the founding is striking: he began with roughly ₹5,000 of borrowed money — a sum so small it would barely cover a month's rent.1

What Doshi started was not glamorous. It was a trading business in industrial instrumentation — temperature gauges, pressure gauges, the unsexy plumbing of factories. He registered the name Waaree, a word drawn from his family's roots, carrying connotations of a sacred place and, by extension, trust and steadiness. It is a telling choice. Doshi was not naming a moonshot; he was naming something he wanted to last. Over the following decade-and-a-half, that little gauge business did something quietly remarkable: it became genuinely good. By the mid-2000s Waaree Instruments was not just supplying Indian factories; it was exporting precision instruments to demanding markets like the United States and Canada and had built a reputation solid enough that the Swiss measurement giant Baumer would eventually acquire it.1

Most entrepreneurs would have stopped there. Doshi had done the hard part — he had escaped the trader's trap and built a profitable, exporting manufacturing concern. He could have spent the rest of his career compounding it. Instead, in 2007, he did something that, viewed from the comfort of 2026, looks visionary, but viewed from 2007 looked close to reckless.

The pivot has the quality of a conversion story. On a business trip to Germany — then the undisputed global capital of solar energy, thanks to generous feed-in tariffs — Doshi wandered into a solar trade exhibition. He had no background in photovoltaics. But he started asking questions: how does this glass make electricity, how big could this get, why isn't anyone doing this in India? By his own later telling, he left convinced that solar was not a niche European subsidy game but the next great energy transition, and that India — sun-drenched, energy-hungry, perpetually short of power — was almost criminally underexposed to it.8

Think about what conviction that required. In 2007, solar electricity was eye-wateringly expensive — many times the cost of coal power. India had essentially no domestic solar market to speak of; the National Solar Mission that would later create one was still three years away. The technology was unproven at scale, the supply chain was immature, and the few Indian entrepreneurs dabbling in it were viewed as romantics. Doshi's response was to set up a 30-megawatt solar module manufacturing plant in सूरत Surat, Gujarat — a serious, capital-intensive bet in a market that barely existed.1

Here is the part that reveals the man's psychology. Rather than hedge, Doshi doubled down on the exit. By 2010 he had sold off the very instrumentation business that had made him — Waaree Instruments went to Baumer — and rolled his identity entirely into the solar wager.1 He simultaneously expanded the Surat module capacity from 30 MW toward 250 MW.1 This is the founder-as-arsonist move: he burned the boat that brought him to shore. There was no comfortable gauge business to retreat to if solar failed. He was all-in on a technology that, at the time, most Indian banks and bureaucrats considered a curiosity.

What does this tell a long-term investor about Waaree's DNA? Two things. First, this is a company built around single-decision-maker conviction — the kind of concentrated founder ownership and risk appetite that can produce both spectacular wins and spectacular blowups. Second, Waaree's entire existence is owed to a willingness to enter a market before the economics worked, and then to outlast the period when they didn't. That second trait was about to be tested in the most brutal way imaginable, because the very thing that would make solar cheap enough to win — collapsing module prices — was also the thing that would nearly kill every manufacturer who made them.

III. Surviving the "Solar Winter" and the Export Pivot

If the 2007 pivot was an act of faith, the decade that followed was its trial by fire. And the fire came, as it so often does in modern manufacturing, from China.

To understand what happened, you have to understand the strange physics of the solar learning curve. Solar panels obey what engineers call Swanson's Law — a cousin of Moore's Law — in which the price of modules falls by roughly 20% for every doubling of cumulative production. Through the 2010s, China decided, as a matter of explicit industrial policy, to own that curve. Backed by cheap state credit, cheap power, and enormous subsidized scale, Chinese giants like 隆基绿能 LONGi and 晶科能源 JinkoSolar drove the price of a solar module down by something like 90% over the decade. For the planet, this was a miracle: it is the single biggest reason solar is now the cheapest electricity in human history. For a sub-scale Indian manufacturer in 2013, it was an extinction-level event.

This was the "solar winter." Indian factories that had tooled up expecting to sell modules at one price suddenly found Chinese product landing in Indian ports at prices below their own cost of raw materials. The result was a graveyard. A whole generation of early Indian solar pioneers — companies that had moved at the same time as Waaree, or earlier — simply went bankrupt, their order books vaporized, their loans unserviceable. The most poignant example, as we will see, ended up becoming Waaree's property.

So how did Waaree avoid the graveyard? The conventional answer is "scale and quality," but that is too tidy. The real survival strategy had three legs.

The first was a refusal to compete with China on China's terms inside India's tiny, price-obsessed domestic market alone. The second — and this is the genuinely clever move — was geographic arbitrage on the back of other people's trade wars. Beginning in the mid-2010s, the United States slapped escalating anti-dumping and countervailing duties on Chinese-made solar modules, and then on modules from the Southeast Asian countries where Chinese firms had relocated to dodge the first round of tariffs. This created a peculiar opening: American developers, hungry for panels but legally and politically wary of Chinese supply, needed a credible non-Chinese manufacturer at scale. Waaree, sitting in India — outside the tariff crosshairs — raised its hand.9

The export pivot reframed the entire business. Instead of being a small fish fighting Chinese sharks in a shallow Indian pond, Waaree repositioned itself as one of the few large, bankable, non-Chinese module suppliers on Earth. That word — bankable — is the third and most underrated leg of survival. In solar, a project developer borrows money against twenty-plus years of expected panel output. The lender will only finance panels from manufacturers they trust to still exist, and to honor warranties, two decades out. Passing those international "bankability" tests — the audits, the third-party reliability ratings, the financial-strength screens — is a slow, expensive, unglamorous grind. Waaree spent years building exactly that credibility, which is precisely why an American bank would underwrite a Texas solar farm built on Indian panels.

The strategic insight here is profound, and it is one investors should sit with. Waaree did not win by being the cheapest. It won by being the most trustworthy alternative to the cheapest in a world that had suddenly decided it could not afford to depend on a single country for its energy hardware. The "China+1" logic that would later become a global supply-chain mantra — every buyer wanting at least one credible non-China source — Waaree had stumbled into a decade early, driven not by foresight about geopolitics but by the simple need to find customers who would pay a fair price.

By surviving the winter and quietly becoming an export machine, Waaree had earned the right to play the next game. But survival is defensive. To become a champion, the company would have to go on the attack — and the first great offensive move would come not from building a new factory, but from buying a dead one out of bankruptcy court.

IV. M&A and Capital Deployment: The IndoSolar Coup

Every empire has a deal that marks its transition from survivor to predator. For Waaree, that deal was इंडोसोलर IndoSolar.

The setting was a courtroom, not a boardroom. IndoSolar had once been a proud name in Indian solar cell manufacturing — and note that word, cell, because it matters enormously. A solar module (the panel) is an assembly job; the real technological and value-added heart of the product is the cell, the wafer of silicon that actually converts photons into electrons. For most of its history, Waaree, like nearly all Indian module makers, bought its cells from China and merely assembled them into panels. That made Waaree, in the unflattering phrase used by skeptics, a "glass-and-frame" company — capturing only the thin slice of margin at the very end of the value chain while China kept the fat middle.

IndoSolar made cells. But it had been a casualty of the solar winter, crushed by Chinese competition and drowning in debt. By 2018, its lenders had dragged it into India's insolvency machinery — the corporate insolvency resolution process under the इन्सॉल्वेंसी एंड बैंकरप्सी कोड Insolvency and Bankruptcy Code of 2016 — and by 2021 the company was reporting a deeply negative net worth, a financial corpse waiting for a buyer.[^3]

In 2021, Waaree moved. Working through the bankruptcy process, it agreed to acquire IndoSolar, and the National Company Law Tribunal cleared the resolution in 2022.[^4] On the surface this looked like a modest deal — a distressed cell maker with idle lines in Noida. In reality it was a piece of strategic chess that solved three problems at once.

Problem one: timing. The global solar supply chain was, at that exact moment, in chaos. Post-pandemic, the price of polysilicon — the raw material for cells — had spiked violently, and cell supply was rationed worldwide. Building a brand-new cell factory ("greenfield") takes years of permitting, construction, and commissioning. Buying IndoSolar gave Waaree an existing cell-manufacturing footprint and the engineering know-how almost overnight, precisely when cells were the scarcest and most valuable link in the chain.

Problem two: the integration question. This is the strategic crux. Waaree was making a deliberate bet to move up the value chain — from being a module assembler dependent on Chinese cells toward becoming a vertically integrated maker of its own cells, capturing the richer margin that had been flowing to China. There is a genuine debate in solar between the "asset-light" model (assemble cheaply, stay nimble, avoid capital intensity) and the "vertical integration" model (own more of the stack, control your costs and supply, but sink billions into fabs). Waaree, with the IndoSolar acquisition, planted its flag firmly in the vertical-integration camp.

Problem three: the math. Did Waaree overpay? The honest answer is that the headline price was modest relative to the strategic value, precisely because it was a distressed-asset purchase — the entire point of buying through bankruptcy is that you acquire capacity at a steep discount to what it would cost to build new. The relevant benchmark is cost per megawatt of cell capacity acquired versus the cost to build the same greenfield, and on that basis the IndoSolar route was almost certainly cheaper and, crucially, faster. The proof showed up in the financials: the once-bankrupt IndoSolar swung to a meaningful net profit within a couple of years under Waaree's ownership, and the acquisition let Waaree push its planned cell capacity from around 4 GW toward 5.4 GW, with the Noida lines and a fresh 1.3 GW module facility layered on top.[^3]

The deeper lesson for investors is about capital allocation philosophy. Waaree did not chase prestige acquisitions or diversify into unrelated empires. It used a downturn — and a distressed competitor — to buy exactly the capability it lacked, at the moment that capability was most valuable. That is textbook counter-cyclical, strategically-disciplined M&A. It is the behavior of an operator who understands his own value chain cold.

And understanding the value chain cold is, ultimately, a reflection of the people running the company. To understand why Waaree allocates capital the way it does — concentrated, conviction-driven, occasionally audacious — you have to understand the family whose name is on the building.

V. Management and Ownership: The Doshi Family Engine

There is a particular type of Indian business — the कुटुंब family-controlled industrial house — that does not behave like a Western public company, and Waaree is a pure specimen of the breed. To analyze its governance through a purely Anglo-Saxon "independent board" lens is to miss the point. This is, in the deepest sense, Hitesh Doshi's company, and the entire incentive architecture flows from that fact.

Doshi himself remains Chairman and Managing Director, the dominant figure in strategy and capital allocation.[^2] What is striking about his public persona is how un-flashy it is for a man who, by the time of the 2024 IPO, was reckoned to be worth in the neighborhood of $5 billion.1 He is not a Davos celebrity or a Twitter philosopher. He is, by all accounts, an operator who came up through the discipline of a small trading business, where you survive by knowing your costs to the rupee and your customers by name. That instrumentation-trader's mindset — precision, frugality, a horror of overpaying — is arguably the most underappreciated asset on Waaree's balance sheet. The company's two defining moves, the 2007 all-in pivot and the IndoSolar bankruptcy steal, both bear the fingerprints of a man comfortable making large, lonely, contrarian decisions.

The family runs the business as a genuine engine, with brothers and the next generation woven through the broader Waaree Group, which spans not just Waaree Energies but the separately listed renewables-EPC arm and a sprawl of related ventures. For an outside investor, this is the classic double-edged sword of the promoter-led model. On the upside: skin in the game of a kind that no professionally managed firm can replicate. Even after the IPO, the promoter group retained a commanding majority stake, meaning the Doshis' personal fortunes rise and fall almost entirely with the share price.[^2] When management owns the overwhelming majority of the company, the temptation to enrich oneself at shareholders' expense through reckless empire-building is, in theory, blunted — though never eliminated. The downside, equally real: minority shareholders are passengers, not drivers. Related-party transactions between group entities, succession risk concentrated in one family, and the question of whether a listed company's capital might be deployed for the broader group's ambitions are the standard items on the diligence checklist for any Indian promoter business, and Waaree is no exception.

The genuinely interesting governance story is the transition the IPO forced. For thirty-five years, Waaree was a private, family-run firm that answered to no public market. The decision to list in 2024 meant submitting — for the first time — to the full machinery of quarterly disclosure, independent directors, audit committees, and the unforgiving scrutiny of institutional analysts. This is a wrenching cultural shift for any founder-dominated house, and how gracefully Waaree completes it is itself a thing worth watching. Early signs — detailed quarterly results presentations, explicit forward EBITDA guidance, transparent order-book reporting — suggest a company that understands it is now playing by public-market rules.[^13]

The appetite that greeted that listing tells you how the market judged the trade-off. We will cover the IPO mechanics in the analysis section, but the ownership signal is worth flagging here: the offering was devoured by qualified institutional buyers far more aggressively than by retail investors, with the institutional tranche oversubscribed by orders of magnitude more than the retail portion.2 In plain terms, the sophisticated money — the mutual funds, the foreign institutions, the insurance giants — wanted this far more than the man on the street did. That is usually a constructive signal about the perceived durability of a business, though it also concentrates the register in hands that can exit fast if the thesis cracks.

So we have a founder of rare conviction, a family aligned to the share price by a vast personal stake, and an institutional shareholder base that bought the story. But what is the story they bought beyond solar panels? Because the most interesting parts of Waaree's future may not be the gigawatts of modules at all. They may be hiding in two businesses that barely register on the income statement today.

VI. The Hidden Engines: Retail and Storage

Quick — picture how solar panels get sold. You probably imagined a fleet of executives negotiating a multi-hundred-megawatt contract with a utility or a giant developer, the kind of deal that takes a year and a battalion of lawyers. And you would be right: that B2B, utility-scale business is the thundering heart of Waaree, the engine that throws off the overwhelming majority of revenue. In recent quarters, solar PV modules alone accounted for the lion's share — roughly nine-tenths — of the top line.3 But the most interesting question for a long-term investor is rarely "what drives revenue today?" It is "what could drive margin tomorrow?" And on that question, two small, easily-overlooked businesses deserve a hard look.

The first is hiding in plain sight at a web address: shop.waaree.com. This is Waaree RTL — the retail and distribution arm — and it represents a quiet but potentially profound strategic shift.7 For its entire history, Waaree sold pallets of panels to other businesses. Retail flips that. Through a network of franchised dealers and an e-commerce storefront, Waaree is selling directly to the small commercial customer and the residential rooftop owner — the homeowner in Pune or the small factory in Coimbatore who wants to bolt panels onto their own roof and cut their power bill.

Why does this matter so much? Because of margin and brand. Selling a 500-megawatt contract to a sophisticated developer is a knife-fight on price; the buyer knows exactly what a module costs and squeezes every paisa. Selling a rooftop system to a homeowner is a completely different economic universe. The homeowner is not buying a commodity; they are buying a brand they trust to sit on their roof for twenty-five years, plus the installation, plus the after-sales service. That is a high-margin, brand-driven, fragmented market — exactly the kind of business where a trusted national name can earn returns a commodity manufacturer can only dream of. The Indian government's push for residential rooftop solar, under massive subsidy schemes aimed at putting panels on millions of homes, supercharges the opportunity. If Waaree can convert its manufacturing dominance into a consumer brand — the "Intel Inside" of Indian rooftops — it changes the entire margin profile of the company. That is the hidden gem thesis.

The second hidden engine is the one that keeps energy strategists up at night: storage. Here is the problem with solar in one sentence — the sun sets. A grid that runs on solar produces a flood of power at noon and nothing at 8 p.m. when everyone gets home and switches on the air conditioner. The holy grail of the energy transition is "round-the-clock" renewable power — RTC — and the only way to get there is to store the noon sunshine in batteries and discharge it at night. India's government has begun mandating exactly this, tendering for renewable projects bundled with battery energy storage systems (BESS).

Waaree saw this coming and moved into batteries through Waaree Energy Storage Solutions. The company has been building out lithium-ion cell and BESS manufacturing capacity — a 3.5 GWh facility forms the first phase — and won its first utility-scale storage orders in FY25, with management signaling far larger ambitions to scale battery capacity dramatically in the coming years.4 Today this is a rounding error in revenue. But strategically, it is Waaree attempting to do for storage what it already did for modules: become the dominant domestic manufacturer just as the policy tailwind arrives. If the module business is the present, storage may be the company's claim on the next decade. The same logic extends to its forays into solar inverters, green-hydrogen electrolyzers, and niche segments like floating solar — panels mounted on reservoirs and lakes, a fast-growing category in a land-scarce country — where Waaree has executed marquee projects.4

The investor's takeaway is to watch these two businesses not for what they contribute now, but for the slope of their growth. Retail is the bet on margin expansion; storage is the bet on the next S-curve. A solar module maker that successfully grafts on a consumer brand and a battery franchise stops being a commodity manufacturer and becomes something far more durable. Which brings us to the central analytical question of this entire episode: just how durable is Waaree's position, really? It is time to put the company on the war-game table.

VII. The Playbook: 7 Powers and Porter's Five Forces

We have told the story. Now let us stress-test it. Acquired's favorite tool for this is Hamilton Helmer's 7 Powers framework, which asks a deceptively simple question: what, precisely, stops a competitor from doing what you do and competing your profits away? Let us run Waaree through the powers that actually apply, and then cross-check with Michael Porter's Five Forces. Be warned — this is where the "national champion vs. commodity" tension gets sharpest, because some of Waaree's most-touted advantages turn out to be rented, not owned.

Scale Economies. This is Waaree's most legitimate power, and it is real. At 12 GW of module capacity and rising, Waaree buys polysilicon, solar glass, encapsulants, and aluminum frames in volumes no smaller Indian rival can match.1 When you are the largest buyer in the country, you get the best prices, the first allocation when materials are scarce, and the ability to spread fixed costs — factories, R&D, certifications, distribution — across a vast output. In a business where the difference between profit and loss can be a few percent on the cost of a panel, procurement leverage of this magnitude is a durable, structural edge. The catch: scale economies only protect you against smaller players. They are no defense against an even larger one — which is exactly the threat we will get to.

Cornered Resource — but read the fine print. Waaree's bulls point to two government gifts as moats: the उत्पादन आधारित प्रोत्साहन Production Linked Incentive (PLI) scheme, which pays manufacturers cash incentives for domestic high-efficiency module and cell production, and the Approved List of Models and Manufacturers (ALMM).56 The ALMM is the more powerful of the two. It is, in effect, a government whitelist: for a huge swathe of Indian solar projects — anything government-linked — developers are legally required to buy modules from an approved domestic list, which conveniently excludes Chinese manufacturers.6 This is a moat made of policy: it hands domestic incumbents like Waaree a protected, captive market and walls out the world's cheapest producers.

But here is the crucial analytical point, the one a serious investor must internalize: this is a rented moat, not an owned one. A cornered resource in Helmer's strict sense is something only you possess. ALMM and PLI are available to every qualifying domestic manufacturer, and they exist entirely at the pleasure of the government, which can widen the list, change the rules, or let the protection lapse. Waaree benefits enormously from these policies, but it does not own them, and it does not have them exclusively. The protection is shared with rivals like प्रीमियर एनर्जीज Premier Energies, अडानी सोलर Adani Solar, and विक्रम सोलर Vikram Solar. So the right way to think about ALMM and PLI is as a powerful industry-wide tailwind that lifts all domestic boats — not as a Waaree-specific fortress. The Waaree-specific edge is being the biggest, best-prepared boat when the tide came in.

Switching Costs. These are modest on the pure module side — a developer can buy panels from someone else next quarter. But they grow real on the services side. Once a utility has Waaree's panels deployed across a sprawling solar farm and contracts Waaree for engineering, procurement, construction (EPC) and ongoing operations and maintenance (O&M), a stickiness develops: the warranties, the spare-parts logistics, the performance data, and the operational familiarity all bind the customer to the ecosystem. Bundle in storage and the rooftop brand, and Waaree is trying to build switching costs where the raw product has almost none. This is the strategic purpose of the retail and services push — to manufacture stickiness in a sticky-less business.

Brand. Genuine but nascent. "Bankability" is a B2B brand power Waaree has earned over a decade, and it has real value with lenders and international buyers. A consumer brand is the prize it is still chasing through retail.

Now, Porter's Five Forces, briefly, to round out the picture:

Threat of new entrants is the scariest force on the board, and we will devote the bull/bear section to it, because the entrants are not garage startups — they are रिलायंस Reliance and अडानी ग्रीन Adani Green, two of the most capital-rich conglomerates on the planet.

Supplier power is the China factor, and it is acute. The single biggest swing factor in Waaree's cost base is the price of polysilicon and cells, much of which is still set by Chinese supply dynamics. When polysilicon spikes, Waaree's margins compress unless it can pass the cost through; when it crashes (as it did when China overbuilt), module prices crash with it. This is precisely why backward integration into cells, wafers, and ingots matters so much — every step Waaree takes up the chain is a step away from supplier power and toward controlling its own destiny.

Buyer power is high in utility-scale (sophisticated, price-sensitive developers) and low in retail (which is the whole point of going there). Threat of substitutes is low in the near term — solar is the substitute that is eating coal, not the other way around — though storage chemistry and competing renewables add long-term complexity.

The synthesis: Waaree's moat is real but partly rented and partly under construction. Scale is owned. Policy protection is rented and shared. Switching costs and brand are being built. That is a more nuanced and more honest picture than either the breathless bull or the dismissive bear would have you believe — and it sets up the debate perfectly.

VIII. Analysis: The Bull vs. Bear Case

Let us war-game the two narratives that institutional investors argue about when Waaree comes up, and do it without flinching.

The Bull Case rests on a single, powerful idea: Waaree is the prime beneficiary of three tailwinds blowing in the same direction at once. First, the global "China+1" imperative — every developer in the United States and Europe wanting a credible non-Chinese supplier — gives Waaree a structurally advantaged export position, anchored by its new 1.6 GW factory in Brookshire, Texas, which lets it sell into the lucrative American market from inside the tariff wall.3 Second, the domestic content tailwind: India's own build-out is colossal, and ALMM plus PLI plus rooftop subsidies funnel that demand toward domestic makers, with Waaree first in line by capacity. Third, the company is executing. The financials are not the sleepy numbers of a commodity grinder. In FY25, revenue grew to roughly ₹14,846 crore, up about 28% year-on-year, while net profit more than doubled to roughly ₹1,932 crore — a profit growth of over 100%.3 EBITDA reached ₹3,123 crore, and the order book stood at over 25 GW worth around ₹47,000 crore — multiple years of revenue locked in.3 Momentum carried into Q1 FY26, with net profit up over 90% year-on-year and a global pipeline exceeding 100 GW.4 The bull says: this is a company growing earnings at triple-digit rates, sitting on a multi-year order book, expanding into the world's richest solar market, with a vertical-integration roadmap (modules, cells, wafers, ingots) that will steadily fatten margins. That is a growth stock, not a commodity stock, and the record-breaking IPO was the market ratifying exactly that view.

The Bear Case is equally coherent, and it attacks the bull at its weakest joints. Bear point one: the moat is rented. Strip away ALMM and PLI — both subject to political whim — and what remains is a glass-and-frame assembler in the most ferociously competitive manufacturing industry on Earth, where Chinese players operate at a scale and cost Waaree cannot match. If India ever relaxes its import protections to hit its climate targets faster with cheap Chinese panels, the captive domestic margin could evaporate. Bear point two: the integration could stall. The bull case on margin expansion depends entirely on Waaree successfully and profitably moving up into cells, wafers, and ingots. That is brutally capital-intensive, technologically demanding, and exactly the part of the chain where China is most dominant on cost. If ingot and wafer economics don't work, Waaree is sinking billions into fabs that may never out-compete imports — the classic value-destroying capex trap. Bear point three: U.S. policy risk cuts both ways. The same American trade actions (Section 201 and 301 duties, anti-dumping investigations, domestic-content rules) that opened the export door could slam it shut. A shift in Washington toward protecting American manufacturers, or new duties reaching India, could strand the Texas-and-export thesis.

And then there is the force that frightens the bears most: the conglomerates are coming. This is where the new-entrants analysis bites. रिलायंस Reliance Industries, through its New Energy arm, and the अडानी Adani group, through Adani Solar, have both announced staggeringly large, fully-integrated solar manufacturing ambitions — giga-scale, polysilicon-to-module complexes backed by some of the deepest balance sheets in Asia. These are not the under-capitalized pioneers who died in the solar winter. If Reliance decides to flood the Indian market with cheap, vertically-integrated domestic modules, Waaree's scale advantage over smaller players offers no protection against a larger one with effectively infinite capital.

So how does Waaree actually stack up against the field? The competitive benchmarking is instructive and a little counterintuitive. Against अडानी ग्रीन Adani Green and टाटा पावर Tata Power, the comparison is partly apples-to-oranges: those firms are primarily power generators and developers — they own and operate solar farms and sell electricity — whereas Waaree is fundamentally a manufacturer that sells the hardware. Tata Power Solar and Adani Solar do manufacture, but neither matches Waaree's module scale today. Waaree's defense against the conglomerates, then, is not balance-sheet size — it will lose that contest — but speed, focus, and distribution. Waaree has spent fifteen years building dealer networks, bankability credentials, international certifications, and an export book while the conglomerates were still in other businesses. It is the focused specialist racing to entrench its distribution and brand before the diversified giants can bring their capital fully to bear. Whether focus beats firepower is the open question on which the entire investment thesis ultimately hinges.

If you are going to track this company through that contest, do not drown in the dozens of metrics. Zero in on the few that actually reveal whether the thesis is intact. First and most important: the gross/EBITDA margin trend, read alongside backward-integration progress. This single relationship answers the core question — is Waaree successfully climbing the value chain and escaping commodity economics, or is margin compressing under competition? Watch whether captive cell and wafer capacity actually translates into expanding margins. Second: the order book and its geographic mix, especially the share coming from exports versus domestic, and how much of that export book is the United States — this is the real-time read on the "China+1" and Texas thesis.4 Third, for the optionality: the revenue ramp in the non-module businesses — retail and storage — because that is the leading indicator of whether Waaree is becoming a higher-margin, more durable franchise or remaining a one-product manufacturer. Track those three, and you will know whether the bull or the bear is winning, long before it shows up in the headline number.

IX. Conclusion and Final Reflections

Step back from the gigawatts and the order books, and what is the real story of वारी एनर्जीज Waaree Energies? It is, at its core, the story of a quiet giant that out-executed the conglomerates by simply getting there first and refusing to die.

There is a tendency, when a company emerges as a national champion, to assume it was always destined for greatness — that the founder saw the whole board from the opening move. Waaree's history says otherwise, and that is what makes it instructive. Hitesh Doshi did not foresee India's solar mission, the U.S.-China trade war, the ALMM whitelist, or the global China+1 panic. What he did was make one enormous, conviction-driven bet in 2007 on a technology whose time had not yet come, sell off his safe business to fund it, and then survive. He survived the solar winter that killed his peers. He survived a decade of Chinese price destruction by finding refuge in exports and bankability. And by surviving long enough, he was still standing — at scale, certified, trusted — when the policy tailwinds finally, inevitably, arrived.

That is the first lesson for founders embedded in this story: the power of the pivot is real, but it is worthless without the discipline to outlast the gap between conviction and vindication. Doshi was "right" about solar in 2007, but being right a decade too early bankrupts most people. Waaree's genius was less in the prediction than in the endurance — the boring, unglamorous, cash-preserving, customer-finding grind that kept the company alive through the years when the thesis looked foolish. Markets reward the visionary who is still solvent when the vision comes true.

The second lesson is about the difference between an owned moat and a rented one, and the maturity to know which you have. Waaree's protections — ALMM, PLI, import duties — are powerful, but they are loans from the state, not property. The company's leadership appears to understand this, which is precisely why it is pouring capital into the things it can own: scale, backward integration into cells and wafers, a consumer brand through retail, and a storage franchise for the next decade. The race Waaree is now running is to convert temporary, policy-granted advantages into permanent, structural ones before the protection fades and the conglomerates arrive in force. That race is undecided.

The October 2024 IPO — oversubscribed dozens of times over, with institutions clamoring for allocation and the company valued north of ₹70,000 crore — was rightly called a coming-out party.[^2]2 But the more interesting framing is what it represented for the country. For decades, the Indian growth story was about software, services, and consumption — the back office of the world, not its factory floor. Waaree's debut was a marker that manufacturing, and specifically advanced clean-energy manufacturing, had become an arena where an Indian company could credibly claim global scale and strategic relevance. Whether Waaree ultimately proves to be a durable compounder or a cyclical commodity player riding a policy wave is a question only the next decade will answer — and the answer will be written in the three metrics we flagged: margins and integration, the export order book, and the new engines of retail and storage.

What is not in doubt is the audacity of the journey. A man started with ₹5,000 selling pressure gauges. Today the company that grew from it lights rooftops from Coimbatore to California. In the long, strange history of business, there are worse definitions of building something that lasts — which, fittingly, is exactly what the name Waaree was always meant to signify.

References

-

The Rise of Hitesh Doshi and Waaree Group — Business Standard, 2024-10 ↩↩↩↩↩↩↩↩

-

Waaree Energies IPO Date, Price, Subscription Details — Chittorgarh, 2024-10 ↩↩

-

Waaree Energies Results — Q4 Revenues Up 38%, FY25 Profits Up 107% — Saur Energy, 2025-04-23 ↩↩↩↩

-

Waaree Energies records INR 4,597.18 crore revenue in Q1 FY 2026 — pv magazine India, 2025-07-29 ↩↩↩↩

-

India's Solar PLI Scheme Guidelines — Ministry of New and Renewable Energy (MNRE) ↩

-

India's ALMM (Approved List of Models and Manufacturers) Policy — MNRE Circular ↩↩

-

Waaree RTL: The Direct-to-Consumer Solar Play — Waaree Shop ↩

-

Interview with Hitesh Doshi on Solar Vertical Integration — Moneycontrol, 2024-09 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube