Vardhman Special Steels: The Toyota Way in Punjab

I. Introduction & The "Special" Hook

Picture a foundry floor on the outskirts of Ludhiana on a winter morning in early 2026. Punjab's wheat belt sprawls out beyond the perimeter fence, but inside, the air is dense with the smell of hot metal and the particular high-pitched whine of an electric arc furnace pulling 70 megawatts of grid power through three carbon electrodes the thickness of telephone poles. A ladle of molten steel — roughly 60 tonnes, glowing at around 1,650°C — is being tapped into a continuous caster. The shop-floor supervisor isn't shouting in Punjabi about tonnage. He is walking a Japanese engineer through a yield chart, in English, explaining why this particular heat shows a non-metallic inclusion count of less than three parts per million.

Three parts per million. Most people, asked to picture a steel mill, imagine soot-streaked workers feeding scrap into a furnace to produce rebar for buildings. वर्धमान स्पेशल स्टील्स Vardhman Special Steels Limited (VSSL) makes a different argument. The product that pours out of its Ludhiana plant is not a commodity. It is a piece of metallurgical engineering precise enough that a defect smaller than a grain of pollen — an aluminate inclusion two microns across, lodged inside a crankshaft journal — can fatigue a Toyota engine to failure at 200,000 kilometres. The business of "special steel" is the business of making sure that defect is never there in the first place.[^1]

Here is the stat that makes this story interesting. If you drove a Maruti Suzuki Swift, a Toyota Innova, or a Mahindra SUV off an Indian showroom floor over the past several years, there is a meaningful probability that the steering knuckle holding your front wheel, the gears stepping down the torque inside your transmission, and the crankshaft converting combustion into rotation — the literal "bones" of the drivetrain — were forged from steel melted at a single plant in Punjab. The company that owns that plant has a market capitalisation that, even after years of re-rating, is a tiny fraction of the giants it sells to.1[^3]

This is the Acquired story of how a textile conglomerate's 1970s side-hustle in steel — a vertically-integrated curiosity born of an India still living under the License Raj — got demerged in 2011, spent the next decade re-engineering itself into a specialty metallurgy shop, and then convinced 愛知製鋼 Aichi Steel, the steel arm of the Toyota Group itself, to hand it the playbook for the Toyota Production System and a minority equity cheque.[^4][^5] It is a story about the difference between scale and skill, about the moat that forms when an automotive OEM spends two years approving your steel grade and then designs an entire car platform around it, and about what happens when a family-run promoter business decides — gradually, then all at once — to stop being a "lala" company and start being a professional one.

If you want to understand why specialty steel is a far better business than commodity steel, why Toyota chose Punjab over Pune, why the EV transition might be a tailwind rather than a headwind for the right kind of long-steel maker, and what the next chapter looks like as VSSL doubles its capacity into the late 2020s — settle in. The roadmap runs from the founding of the Vardhman textile empire in the 1960s through the Aichi alliance and into the question every investor in cyclical Indian industrials eventually has to answer: at what price does "quality" become "commodity," and how long can a specialist hold the line?

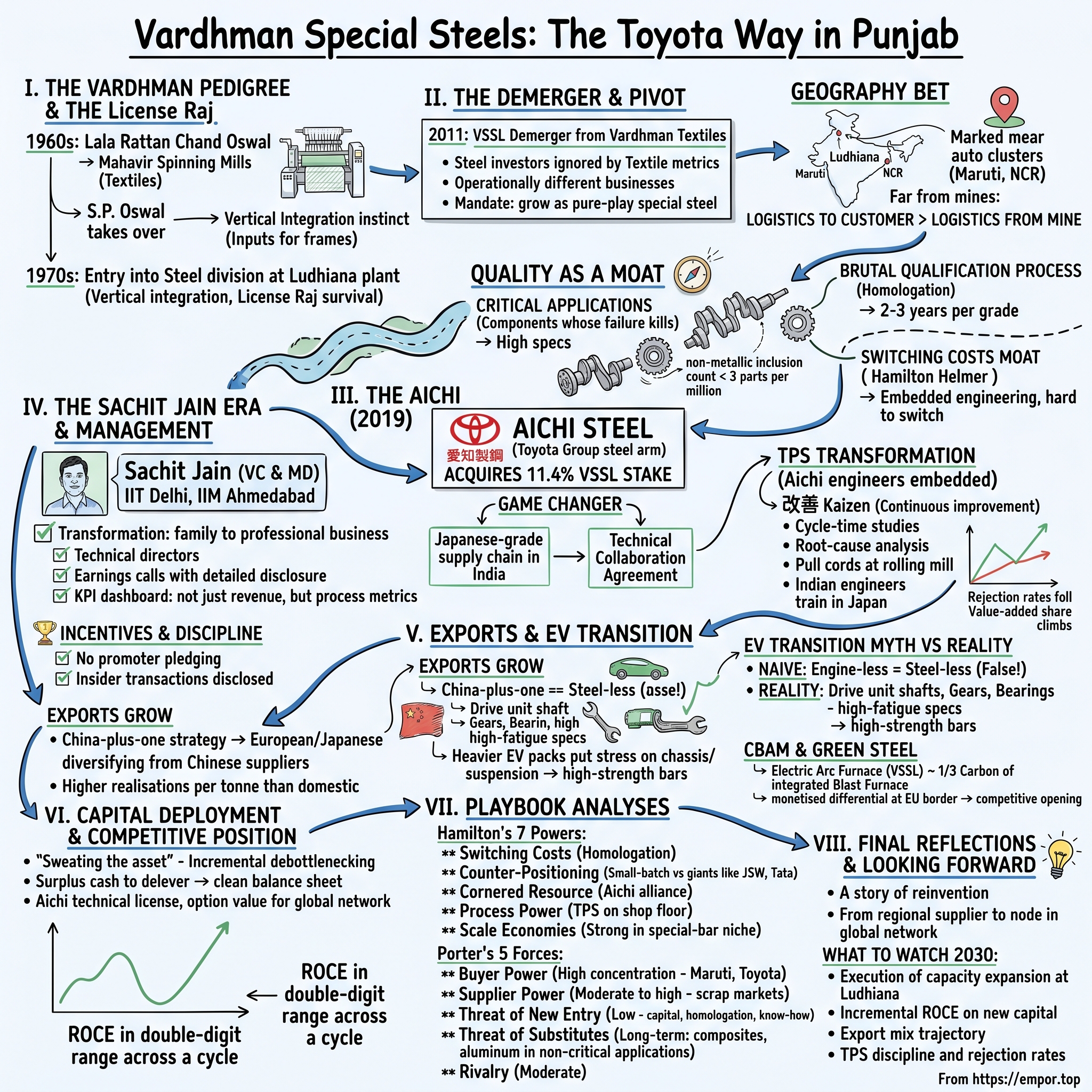

II. The Vardhman Pedigree & The Demerger

Before there was Vardhman Special Steels, there was, simply, Vardhman. And before there was Vardhman, there was a young Punjabi entrepreneur named Lala Rattan Chand Oswal, who, in 1962, set up a small textile unit in Ludhiana under the name Mahavir Spinning Mills. He died unexpectedly in 1965, and the business passed to his then-twenty-something son, सत पाल ओसवाल S.P. Oswal — a name now spoken in Indian industry the way Americans speak of mid-century industrialists. Oswal, an engineering graduate from Punjab University, took an obscure regional spinner and, over the next four decades, built it into one of India's largest vertically-integrated textile groups, with operations stretching from cotton procurement through yarn, fabric, sewing thread, acrylic fibre, and garments.[^6]

The Vardhman Group's instinct, from very early on, was vertical integration. If you spun yarn, why not dye it? If you dyed it, why not weave it? And if you needed industrial inputs — chemicals, machinery, alloy components for your spinning frames — why not make those too? That instinct is what dragged a textile family into specialty steel in the 1970s. The group had originally set up steel operations at its Ludhiana site partly to serve its own engineering needs and partly because, in the closed economy of pre-liberalisation India, vertical integration was less a strategy than a survival mechanism: imports were restricted, licences were scarce, and a manufacturer who could not source his own critical inputs was at the mercy of whoever held the import permit.[^6]

For the better part of three decades, the steel business sat inside the parent Vardhman Group as a relatively quiet division. It made alloy and special steel bars, served a mix of automotive, engineering, and bearing customers, and ran a single integrated unit at Ludhiana. It was profitable but small, and it lived in the shadow of the textile flagship. The problem, by the late 2000s, was that this arrangement no longer suited anyone. Textile investors — who looked at Vardhman for cotton cycles, China-plus-one yarn dynamics, and rupee movements — had no interest in pricing scrap steel. Steel investors, conversely, could not see through the textile holding-company discount to value the metallurgy business on its own merits. And operationally, the two businesses had almost nothing in common: the customer set, the working-capital cycle, the capital intensity, even the regulatory regime were different beasts.

So in 2011, the Vardhman board approved a demerger. The steel division was carved out of Vardhman Textiles and listed separately on the NSE and BSE as Vardhman Special Steels Limited, with the same broad promoter family ownership but a clean, dedicated balance sheet, a separate management team, and a mandate to grow as a pure-play specialty steel company.[^6][^7] In hindsight, this is the inflection point that makes the rest of the story possible. A demerger is, in corporate finance, a fairly mechanical event. But strategically, it forced the steel business to stop being a captive division and start behaving like a standalone business — one with its own cost of capital, its own investor calls, its own narrative to tell.

Then there is the geography, which deserves its own moment. Ludhiana is not, in any conventional industrial logic, where you would put a specialty steel plant. The classical Indian steel belt sits in the east — Jharkhand, Odisha, Chhattisgarh — where iron ore and coking coal are mined and where Tata Steel and SAIL have historically built their integrated works. Ludhiana sits in Punjab, eight hundred kilometres west of the ore mines, in the heart of an agricultural state better known for tractors, hosiery, and bicycle parts. But Ludhiana is also, by accident of history, the auto-component capital of northern India: a dense cluster of forging shops, machining units, and bearing makers that supply the Delhi-NCR automotive corridor anchored by Maruti Suzuki's Gurgaon and Manesar plants. Putting a specialty steel mill in the middle of that cluster — close to the customer, far from the ore — was a bet that, for specialty steel, logistics to the customer mattered more than logistics from the mine. That bet would compound for the next fifteen years.

III. The Strategic Pivot: Quality as a Moat

Imagine, in the early 2010s, sitting in the corner office of the freshly-listed Vardhman Special Steels with a sober view of the competitive landscape. You produce, depending on the year, somewhere around 150,000 to 200,000 tonnes of specialty long steel. Down the road, JSW Steel produces roughly twenty million tonnes of crude steel a year. Tata Steel India produces roughly the same. SAIL, the state-owned behemoth, produces close to twenty million as well. On any conceivable axis of scale — raw material procurement, coking coal contracts, port logistics, integrated power, captive iron ore mines — you lose. Decisively. There is no version of the future where Vardhman Special Steels out-volumes JSW or out-scales Tata.

So you do the only sensible thing: you refuse to play that game. The strategic pivot that defined VSSL's second decade was the conscious decision to leave commodity long products to the giants and instead climb up the value curve into what the industry calls "critical applications" — components whose failure does not merely cost money but can kill someone. This is the philosophical core of specialty steel. A reinforcement bar for a building is allowed a certain looseness of specification because the load it carries is statistically averaged across thousands of bars in a structure. A crankshaft inside a passenger car is allowed almost no looseness at all, because if it fractures at 4,000 RPM, the engine ends.

That distinction translates into something investors should care about: pricing power. Commodity rebar prices are set by global scrap and iron ore benchmarks, and the producer is essentially a price-taker on a thin spread. A "case-hardened, vacuum-degassed, sulphur-controlled, micro-alloy SAE 8620H" bar destined to be forged into a transmission gear is sold on a custom contract, qualified to a specific OEM's chemistry, and re-priced through pass-through formulas that protect the producer's conversion margin even when input costs swing. The unit volumes are smaller. The conversion economics are much, much better.

The hard part is getting there. To sell into the critical-parts list of a global OEM, a steel producer has to go through what the industry calls "homologation" — a brutal, multi-stage qualification process that runs, typically, for two to three years per grade per customer. The OEM and its tier-one suppliers run the candidate steel through fatigue tests, machinability tests, hardenability tests, microstructure analysis, inclusion ratings, and trial production runs across multiple casts. Only when every metallurgical parameter sits inside a tightly-specified envelope across multiple heats does the steel get added to the OEM's approved source list. There is no shortcut. You cannot pay your way in. You have to earn it, heat by heat, batch by batch.

This is why specialty steel approval cycles function, in the language of Hamilton Helmer, as one of the cleanest examples of a Switching Cost moat in heavy industry. Once a Maruti or a Toyota platform is engineered around your steel — with the gear-cutting tools calibrated to your chemistry, the forging shops trained on your microstructure, the heat-treatment lines tuned to your hardenability curves — moving to a different supplier is not just a procurement decision. It is a re-engineering exercise that could cost the OEM weeks of production downtime and millions of rupees in re-validation. The mathematics of that switching cost is what gives a small Punjab mill the ability to hold price discipline against customers who are, on every other axis, vastly more powerful than it is.

VSSL spent the decade after its demerger systematically working through that approval gauntlet. Year by year, the product mix migrated from generic bright bars and free-cutting grades into harder, cleaner, more demanding alloys: case-carburising steels for transmission gears, micro-alloyed steels for crankshafts, bearing-quality steels with ultra-low oxygen, spring steels for valve springs, and a growing list of "controlled-inclusion" grades destined for the safety-critical parts that an auto OEM cannot afford to compromise on.[^1]2 By the late 2010s, the company was no longer competing with rebar mills. It was competing in a much smaller and much more defensible pond.

IV. The Aichi Steel Inflection: The Game Changer

If you want to identify the single moment that re-rated Vardhman Special Steels from "interesting Indian special-steel mid-cap" to "strategically positioned partner of the Toyota ecosystem," you can point to a press release dated August 20, 2019. On that day, the company announced that 愛知製鋼 Aichi Steel Corporation of Japan — the dedicated steel arm of the Toyota Group, with roots going back to a 1934 forge operation founded by 豊田喜一郎 Kiichiro Toyoda himself — had agreed to acquire approximately 11.4% of VSSL through a preferential allotment and an open offer. The deal would make Aichi the single largest non-promoter shareholder, and, more importantly, would bring with it a deep technical collaboration agreement.[^4][^5]

To understand why this mattered, you have to understand what Aichi Steel is. Aichi is not, by global tonnage, a giant. It produces roughly a million tonnes of crude steel a year — a fraction of Nippon Steel or JFE. But within the Toyota Group, Aichi occupies a near-mythical position: it is the source of the steel that goes into Toyota's drivetrains, the proving ground for the metallurgical standards that the entire Toyota supply chain inherits, and a central node in the company's vaunted production philosophy. When Aichi Steel takes a stake in a foreign steel mill, it is not a financial investment. It is the Toyota Group placing a strategic bet on a regional supply node and signalling to its tier-ones that the mill in question is now part of the family.

The "why" of the deal, from Aichi's side, was simple. Toyota's Indian footprint — both directly through Toyota Kirloskar and indirectly through its global alliances with Suzuki — was expanding, and the steel grades that Toyota cars are designed around require a Japanese-grade supply chain. Importing specialty bar steel from Japan or Korea for Indian assembly works at a small scale but breaks economically at a large one. Aichi needed an Indian partner who could meet its specifications. The shortlist of mills in India capable, on day one, of being trained up to that standard was very, very short. VSSL was on it because of the decade of homologation work it had already done.[^9]

The "why" from VSSL's side was even more interesting, and it had relatively little to do with the cash. The preferential allotment did inject equity into the balance sheet, but the truly priceless component was the technical collaboration. Aichi agreed to transfer process know-how across steelmaking, secondary metallurgy, continuous casting, and rolling — the accumulated metallurgical intellectual property of nearly a century of supplying Toyota. Embedded in that transfer was something even rarer: training in the Toyota Production System itself, applied to the unforgiving environment of a steel mill, where the "production line" is a stream of molten metal that cannot be stopped without enormous cost.

The TPS transformation that followed at Ludhiana is, in retrospect, the operational soul of this story. 改善 Kaizen — continuous improvement — sounds, in the abstract, like a poster on a meeting-room wall. Applied to a furnace, it means cycle-time studies on the tap-to-tap interval of every heat, root-cause analysis on every rejected coil, andon cords pulled at the rolling mill the moment a surface defect is detected, and a culture in which the senior-most plant engineer is expected to listen to the most junior operator if the operator has spotted a deviation. The Vardhman shop floor — already disciplined by Indian standards — was rebuilt around this philosophy heat by heat, line by line, year by year, with Aichi engineers embedded on site and Indian engineers seconded for training in Japan.

The output of that transformation showed up in two numbers the company has talked about repeatedly in its filings and presentations: rejection rates and value-added share. Rejection and re-work rates fell materially through the early 2020s, and the share of value-added grades in the product mix climbed steadily into the high-50% range and beyond, depending on the quarter and the cycle.[^1][^9] More importantly, the Aichi alliance opened up Toyota's global supply chain. VSSL steel started being qualified not only for the Indian Toyota platforms but also for export to other Toyota suppliers in Asia, with longer-term ambitions toward Japan and Europe. A company that had previously been a regional supplier became, almost imperceptibly, a node in a global automotive metallurgy network.

V. Management Deep Dive: The Sachit Jain Era

Walk into a VSSL investor meeting and the first thing that strikes you is that Sachit Jain — Vice Chairman & Managing Director, son-in-law of S.P. Oswal, and the man who has effectively run this business since the demerger — does not present like a traditional Indian promoter. There is no entourage. There are no anecdotes about cricket matches with prime ministers. There is, instead, a deck. The deck is detailed, occasionally pedantic, and contains the kind of operating metrics — yield by grade, rejection by line, on-time-delivery by customer — that you would expect from a Japanese plant manager rather than from a Punjabi industrial scion.

The biographical sketch is informative. Sachit Jain is an alumnus of IIT Delhi and IIM Ahmedabad — the dual credential that, in Indian business, marks someone as comfortable in both the engineering and the strategic dialects. He spent years inside the broader Vardhman ecosystem before taking on the steel business at the time of the demerger, and the cultural project he has pursued, more or less openly, is the transformation of a family-controlled industrial business into one that behaves like a professionally-managed one. That sounds, in summary, banal. The execution is not.23

The visible markers of that transformation are everywhere if you know where to look. Independent directors on the board with meaningful technical and audit backgrounds. Quarterly earnings calls run with a level of disclosure that materially exceeds what comparable mid-cap industrials in India provide. A KPI dashboard that lives less around revenue and more around process metrics: tap-to-tap times, energy consumption per tonne, prime yield, customer-wise PPM rejection. Internally, the cultural project has gone further, with a published code of conduct and a deliberate effort to recruit second-line management from outside the family and outside the immediate Vardhman alumni network — a meaningful departure from the "लाला lala" style of north Indian promoter governance in which the family is the management and the management is the family.2

On incentives, the structure is straightforward. The promoter group — broadly the extended Oswal-Jain family — holds approximately 60.6% of the company.[^7] Aichi Steel holds approximately 11.4%. The remainder is split between institutional investors, retail shareholders, and a small foreign component. Promoter pledging has historically been low to nil — an important detail in an Indian context where promoter share pledges have repeatedly been a source of small-cap blow-ups. Insider transactions are disclosed promptly on the exchange. Compensation structures for the senior team are linked to both reported performance and operating KPIs.

There is, of course, a "myth versus reality" worth pausing on. The consensus narrative on Indian promoter businesses is that they extract value from minority shareholders through related-party transactions, opaque cost allocations with sister concerns, and capital allocation decisions that serve the family rather than the listed entity. VSSL's track record on this dimension is, by mid-cap Indian standards, clean. Related-party transactions exist — they always do in a group structure — but they are disclosed, are routinely the subject of explicit board approval, and have not, over the company's listed history, become the kind of recurring scandal that scars investor returns. Conversely, the bull narrative occasionally tips into the assumption that Aichi's presence is a guarantee of Japanese governance standards being imported wholesale. The reality is more nuanced: Aichi is a minority partner with no board control, and the day-to-day decisions are still made by the Indian management. The discipline is real, but it is the discipline of a management team that chose it, not the discipline of an outside-in takeover.

The strategic articulation of where the company wants to go has been packaged, in recent years, under the label of "Vision 2030" — a multi-year roadmap that combines capacity expansion, a steady migration up the value curve, deeper TPS-driven productivity gains, and a deliberate cultivation of the export channel. Whether the company hits those targets exactly is, for any long-horizon investor, less important than the fact that the targets exist, are quantitative, are publicly defended on earnings calls, and are reconciled — quarter by quarter — against actuals.[^1]3

VI. Hidden Segments & The EV Transition

Walk through a Vardhman quarterly disclosure for the first time and your eye is drawn naturally to the headline numbers: tonnage, realisation per tonne, EBITDA per tonne, the auto-versus-bearings-versus-engineering split of the customer mix.[^1] What is easier to miss, and arguably more interesting strategically, is what is happening in two adjacent corners of the business: exports and the segment-mix shift driven by electrification.

Start with exports. For most of its history, VSSL was a domestic supplier — a few percent of revenue trickling out to neighbouring markets, with the bulk of the order book sitting inside India. That changed quietly in the second half of the 2010s, accelerated through the Aichi alliance, and has, by the mid-2020s, become a visible growth engine. The export book now reaches into Europe, Japan, Southeast Asia, and the Middle East, supplying tier-two automotive forgers and bearing makers who in turn feed European OEMs. The strategic logic is the "China-plus-one" of metallurgy. European tier-one auto suppliers, historically dependent on Chinese specialty steel mills for low-cost critical bars, have spent the last several years actively diversifying away — partly because of pandemic-era supply shocks, partly because of geopolitical risk, and partly because European procurement organisations now carry explicit mandates to reduce single-country concentration in safety-critical components.4

An Indian mill that meets Japanese quality standards, is partnered with a Toyota-group company, and prices roughly thirty to forty percent below comparable European production is — once it gets through the homologation gate — exactly the kind of supplier that fits that brief. The relevant detail for investors is that export volumes carry, on average, materially higher realisations per tonne than domestic volumes. The mix shift toward exports is therefore not merely a top-line story; it is a margin story. It is one of the most important slow-burn dynamics in the company's earnings trajectory.

Now the question every investor in an Indian auto-exposed business eventually has to answer: what happens to the order book when electric vehicles eat the internal combustion engine? The naive answer is "very bad things," because half of VSSL's product mix has historically been engine-bound — crankshafts, camshafts, connecting rod inputs, valve springs, fuel-injection components. If those parts disappear, half the demand disappears. The naive answer is wrong in a couple of important ways, and the company has been progressively articulating why.

First, in the powertrain itself: an EV's drivetrain is engine-less but not steel-less. The shafts inside an electric drive unit, the gear sets in the reduction box, the bearings carrying the rotor — all of these still require high-fatigue specialty steel. In some cases, because EV motors operate at much higher RPMs than combustion engines, the metallurgical demands are tighter, not looser. Second, the rest of the vehicle still exists. The steering knuckle, the suspension control arm forgings, the wheel hub bearings, the half-shafts transmitting torque to the wheels — these are all specialty-steel parts, and they all get heavier and stronger in an EV because the vehicle itself is heavier (a typical EV weighs 15-25% more than a comparable ICE vehicle, almost entirely due to the battery pack). A heavier vehicle with higher instant torque puts more stress on the chassis and the suspension, which is exactly where high-strength bar steel earns its margin.2

Then there is a third leg, less obvious but arguably the most strategically important: green steel and carbon. The European Union's Carbon Border Adjustment Mechanism (CBAM) phased in through the mid-2020s, putting a price on the embedded carbon of imported steel.5 For an integrated blast-furnace producer, this is a competitive disaster. For an electric-arc-furnace, scrap-based producer like VSSL — whose carbon intensity per tonne of crude steel is roughly a third of the integrated coal-route producers — it is a competitive opening. The company has been investing in renewable power procurement, energy efficiency, and increasingly granular carbon accounting precisely so that, when a European OEM asks for a verified low-carbon supplier of critical bar steel, the answer is yes, here is the document.

VII. M&A, Capital Deployment & Benchmarking

If you want to test a management team's discipline, watch how they spend their money in a cyclical industry. Steel is one of the most reliably cyclical industries in the world, with prices oscillating violently with global scrap and iron ore movements, currency moves, and end-market demand cycles. The history of Indian metals is littered with cases of producers who confused a cyclical peak for a structural one, levered up to expand capacity at the top, and then spent the next decade restructuring debt as the cycle rolled over. The two cleanest case studies in the special-steel mid-cap space — Sunflag Iron and Steel and Mukand Limited — both carry, in their balance-sheet histories, the scars of exactly this pattern.

Against that benchmark, VSSL has run, by Indian metals standards, an unusually disciplined capital allocation playbook. The dominant theme through the 2010s was "sweating the asset" — incremental debottlenecking of the existing furnace, mill, and finishing lines to push tonnage up without writing a billion-rupee greenfield cheque. Capex was, for years, kept at maintenance and incremental-expansion levels, and the surplus cash was used to delever the balance sheet. The result, by the early 2020s, was a company with one of the cleaner leverage profiles in the Indian specialty-steel space, with credit agencies rewarding the discipline with successive upgrades.[^13]

The Aichi transaction itself is worth a brief revisit through the capital-deployment lens. The 11.4% stake was acquired in 2019 at a price that, taken purely on a then-trailing earnings multiple, was not obviously a windfall for VSSL's existing shareholders.[^4] On a static valuation basis, you could even argue the company "sold itself cheap." But the static valuation lens misses the entire point. The cash from the preferential allotment was almost incidental. The real consideration was the technology licence, the production-system embedding, and — perhaps most importantly — the implicit endorsement that opened doors to the Toyota global supplier network. In intangible terms, the deal was almost certainly priced at a steep discount to the value it created. The right way to think about minority strategic equity deals like this one is rarely the multiple paid; it is the option value of what the partnership unlocks over a decade.

Through the early 2020s, that option value started getting cashed in. The company moved into the next phase of its capacity story: a more meaningful brownfield expansion at Ludhiana, taking installed crude steel capacity from roughly 220,000 tonnes per annum toward the 300,000-plus range, with corresponding investments in secondary metallurgy (vacuum degassing, ladle refining), continuous casting upgrades, and rolling mill modernisation. The expansion has been funded through a careful mix of internal accruals and modest incremental debt, calibrated to keep the leverage ratio inside a range that the credit agencies have signalled comfort with.[^1][^13]

The return profile that has emerged from this discipline is worth dwelling on. Specialty steel is a cyclical business, and in any single year the return on capital employed can swing meaningfully with the steel cycle. But across a cycle, VSSL has managed to compound returns on capital in the double-digit range — a meaningfully better outcome than most Indian commodity-steel producers, and the result not of any single moment of brilliance but of the slow, repeated decisions to take the higher-margin order, accept the lower-tonnage but higher-realisation product, and refuse to chase volume that does not earn its cost of capital.[^1]2 The "what to watch" for investors, going forward, is the relationship between this capex cycle and incremental return on capital. A doubling of capacity that comes through at lower incremental ROCE would be a yellow flag. Capacity expansion that maintains or improves the existing return profile is the signal that the strategy is still working.

The bridge from capital deployment to competitive positioning is direct. Discipline on capex is what allows a smaller company to hold its margin through a cyclical trough — and that durability through the cycle is one of the structural advantages a specialist can build over generalists. Which leads naturally to a deeper look at the moat itself.

VIII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Take Hamilton Helmer's 7 Powers framework, hold it up against Vardhman Special Steels, and the company lights up across more cells than its size would suggest.

Start with Switching Costs, which is the cleanest of the seven powers in this case. The OEM homologation process described earlier is not just a procurement formality. It is an embedded engineering commitment. Once a Maruti or a Toyota platform has been validated around a specific VSSL grade — with the forging suppliers' dies calibrated, the heat-treatment furnaces tuned, the gear-cutting machinery dialled in — the cost of switching to a different supplier for that part is not the per-tonne price differential. It is the prospect of months of re-validation, the risk of failure rates ticking up in the field, and warranty exposure that could run into hundreds of crores of rupees. Switching costs of this sort are, in the language of Helmer, exactly what create durable pricing power, and they explain why VSSL has been able to hold or expand margins through cycles that have crushed commodity steel producers.

Move to Counter-Positioning. The argument here is that VSSL occupies a strategic position that the giants cannot occupy without damaging their own business. JSW Steel and Tata Steel are optimised for volume — millions of tonnes a year through integrated blast-furnace works. A "custom melt" of 200 tonnes of a particular SAE-spec micro-alloy, with a specific inclusion control regime, is, for those companies, an irritation. The setup cost on a giant blast furnace to make 200 tonnes of a specialty grade is fundamentally uneconomic. VSSL's electric-arc-furnace route, with a much smaller heat size, is precisely optimised for that small-batch, high-spec work. The big mills could, in theory, build a dedicated specialty operation. They mostly don't, because the opportunity cost of the dedicated assets — and the cultural retooling required — is high relative to the size of the prize. At the other end, smaller mills with electric-arc furnaces can match the heat size but not the metallurgical discipline. VSSL sits in the gap.

Cornered Resource is the Aichi alliance.[^4][^5] No other listed Indian specialty steel mill has, on its supplier development team, an embedded set of engineers from the steel arm of the Toyota Group transferring half a century of accumulated metallurgical know-how, complete with audit rights, joint product development, and access to the Toyota-group supply network. Trying to replicate that resource is not a question of money; it is a question of relationship and time, both of which compound and neither of which can be bought on the open market. It is, in the strictest sense of the framework, a cornered resource.

Scale Economies are the weakest of the seven for VSSL relative to the giants of commodity steel. But within the specialty-bar niche in India, VSSL has reached a scale that materially exceeds most of its direct domestic peers, and at that niche scale, fixed-cost absorption on the secondary metallurgy and rolling lines does provide a meaningful unit-cost advantage. Process Power, the seventh power, is increasingly visible — the institutionalised TPS practice on the shop floor is a process advantage that compounds quietly, year after year, in yield and reject rates that competitors cannot quickly replicate.

Now flip to Porter's Five Forces — the older, more sober framework — and the picture is more textured.

Buyer power is genuinely high. Maruti Suzuki, Toyota Kirloskar, Tata Motors, Mahindra, and the global tier-ones VSSL exports to are all enormously larger than VSSL itself, with sophisticated procurement organisations whose entire job is to extract margin from suppliers. VSSL's mitigation is the switching-cost moat and the value-add specification of its product — but the underlying buyer concentration is a real constraint on long-run pricing power. Supplier power, in the form of scrap and ferro-alloy markets, is moderate to high — those are commodity markets with global price volatility, and VSSL is, like every electric-arc producer, exposed to scrap-price spikes. Pass-through contracts mitigate but do not eliminate this risk. Threat of new entry into the specialty-steel niche is low: the combination of capital intensity, OEM approval cycles, and metallurgical know-how is a brutal barrier for any greenfield. Threat of substitutes — composites, aluminum, advanced polymer materials in non-critical applications — is the longest-term and quietest threat, and it is the one investors should keep an eye on. Rivalry within the niche is moderate: a handful of focused specialty mills compete on the margin, but the structure of the business prevents the kind of price-destroying glut that periodically afflicts commodity steel.

The synthesis is straightforward. VSSL is not a moat-less commodity producer with a cyclical earnings profile. It is a switching-cost-protected, counter-positioned specialty manufacturer with a cornered strategic resource — operating inside a cyclical industry. Those are different beasts, and they deserve different lenses.

IX. The Bear vs. Bull Case

Time to put the bull and the bear in a room and let them fight it out. The honest version of this exercise requires taking both cases seriously, and there is plenty of evidence for each.

The Bear Case. Start with the macro. Steel — even specialty steel — is a cyclical, scrap-and-iron-ore-linked business, and Vardhman's input cost line moves with global commodity markets that no Punjab management team can control. A sharp scrap-price spike, even with pass-through contracts, compresses spreads in the short term, because the pass-through is never perfectly synchronous. Layer onto that the cyclicality of the Indian passenger vehicle market itself — which has historically swung from double-digit growth to outright contraction in periods of three to five years — and the earnings trajectory of the business is structurally lumpy. A bear can point to any number of historical examples in which Indian metals stocks rallied through a cyclical peak, only to give back years of returns in a single down-cycle.[^14]

Layer in a second bear theme: the slow, steady, decade-out threat of material substitution. Aluminium has been gaining share in body panels and certain chassis components for years. Composite materials are creeping into suspension and structural parts. The bear narrative is not that an EV does not need specialty steel — VSSL itself has refuted that — but that, over fifteen years, the absolute tonnage of specialty-bar steel per vehicle could plateau or decline, even as the vehicle market grows. If that thesis plays out, growth becomes a much harder grind, and the multiple investors are willing to pay for the story has to come down.

A third bear leg: concentration risk on the buyer side. A handful of OEMs account for a meaningful share of VSSL's domestic order book. If any one of them — Maruti, Toyota, Tata Motors — decides to diversify supply for any reason (a procurement reshuffle, a strategic decision to favour an in-country competitor, a long-term shift to imported steel under a different alliance), the revenue impact would be material. That is the price the company pays for the deep, switching-cost-rich relationships that also constitute its moat: the same depth that protects the revenue is the depth that makes any individual customer exit painful.

Finally, the credit and capital cycle. Specialty steel expansion is capital-intensive, and the next phase of VSSL's growth requires successive rounds of capex.[^1] If the company misjudges the cycle and over-builds, or if its incremental ROCE on the new capacity disappoints, the equity story gets meaningfully more complicated. The credit agencies have been favourable on the trajectory, but credit ratings can move both ways, and the early 2020s were a kind environment for industrial credits in India that may not persist indefinitely.[^13]

The Bull Case. Now the other side. The bull case is structural and rests on three pillars that compound together.

The first pillar is the China-plus-one tailwind. European, Japanese, and American OEMs have been actively, sometimes mandatorily, diversifying their specialty-steel supply away from Chinese sources for half a decade. India is the obvious second source on cost grounds, and inside India, the shortlist of mills technically capable of meeting global automotive specifications is small.4 VSSL sits near the top of that shortlist, with the additional credential of a Toyota-group endorsement that no other Indian peer carries. As that re-sourcing wave unfolds over the next several years, the export channel becomes a structurally rising share of the order book, with structurally higher per-tonne realisations.

The second pillar is the green-steel and CBAM tailwind.5 Electric-arc-furnace, scrap-based steelmaking has a carbon profile roughly a third that of integrated blast-furnace steel. As Europe's carbon border adjustment phases in, that carbon differential gets monetised at the border, which is exactly the right place for a low-carbon supplier targeting European OEMs to capture margin. It is a tailwind that the bull case argues has barely begun to play out in the company's reported numbers and will become more visible through the back half of the decade.

The third pillar is the EV myth-busting case described earlier. If the bear narrative on EVs proves overstated — if specialty-bar tonnage per vehicle is roughly flat or even modestly higher in an electric world, and the vehicle market itself grows — then the company's addressable market grows steadily into the late 2020s, with the value-added mix continuing to climb.

There is a holistic point underneath all three pillars: VSSL's competitive position is durably differentiated within a niche, and the optionality on top of that position — exports, green steel, EV chassis — is significant. The bull case is not a bet on commodity prices. It is a bet on the slow compounding of switching-cost-protected market share inside a structurally attractive niche.

For investors trying to compress this entire picture down to the few KPIs that actually matter, three rise above the rest. The first is value-added grade share as a percentage of total volume — the cleanest single indicator of whether the mix-shift strategy is working. The second is EBITDA per tonne through a cycle — the proof, or disproof, that the moat is converting into pricing power. The third is export share of revenue — the leading indicator of how far the China-plus-one and Aichi-driven global expansion has actually travelled. Watch those three over a few years and you will know more about the underlying business than any quarterly earnings beat or miss can tell you.[^1]2

X. Epilogue & Final Reflections

Stand back from the detail for a moment and notice what is actually happening in this story. A textile family from Ludhiana, founded in the 1960s by a man who died young and was succeeded by his twenty-something son, built a steel side-business inside its parent conglomerate, demerged it forty years later, professionalised it through the 2010s, partnered with the steel arm of the Toyota Group in 2019, and has spent the years since methodically transforming itself from a regional supplier into a node in a global automotive metallurgy network. Almost none of the moves in that sequence were obvious at the time. Several of them — the demerger, the Aichi alliance, the willingness to share governance and process control with a Japanese partner — required precisely the kind of patient, multi-generational thinking that Indian family-controlled businesses are routinely accused of lacking.

The Vardhman lesson, then, is not really about steel. It is about reinvention. It is about what happens when a promoter family decides that the old script — the closed, vertically-integrated, family-managed conglomerate optimised for the License Raj — no longer fits the world its grandchildren will inherit, and that the right move is to open the doors, professionalise the management, and bring in a foreign strategic partner whose primary value is not capital but knowledge. In a country whose mid-cap industrial landscape is full of family businesses still grappling with that exact transition, the VSSL playbook is something of a working case study, and the next decade will test whether it generalises or whether it is a one-off.

What to watch, concretely, between now and 2030: the execution of the announced capacity expansion at Ludhiana and the incremental return on the new capital deployed; the trajectory of the export mix as European and Japanese tier-ones continue their re-sourcing away from China; the rejection-rate and yield numbers as a proxy for whether the Toyota Production System discipline is still compounding inside the plant; the continued evolution of the value-added grade mix as the company pushes deeper into bearing-quality, ultra-clean, and micro-alloyed steels; and — most importantly — the way management responds to the inevitable cyclical downturn that will, at some point, test the discipline that has been built over the last decade.

If you started this article thinking of Vardhman Special Steels as a small Indian steel mill, you should end it with a different framing. It is a specialty metallurgy company that happens to be in India, that happens to be partnered with one of the most demanding industrial customers on earth, and that is, slowly and quietly, positioning itself for the years in which global automotive supply chains finish rewiring themselves around the post-China, post-carbon, partly-electrified world. Whether that positioning translates into the kind of compounding returns its bull case envisions will depend on dozens of decisions yet to be made — but the framework for understanding which decisions to watch, and why they matter, is now in place.

References

References

-

Vardhman Special Steels (VSSL) Equity Page — National Stock Exchange of India ↩

-

Toyota's TPS in Indian Steel: A Case Study — Forbes India ↩↩↩↩↩↩

-

Interview with Sachit Jain on Q3 FY24 Performance — Moneycontrol, 2023 ↩↩

-

Special Steel Industry Analysis India — Ministry of Steel, Government of India ↩↩

-

Special Steel Industry Analysis and CBAM Impact — IBEF / Ministry of Steel ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube