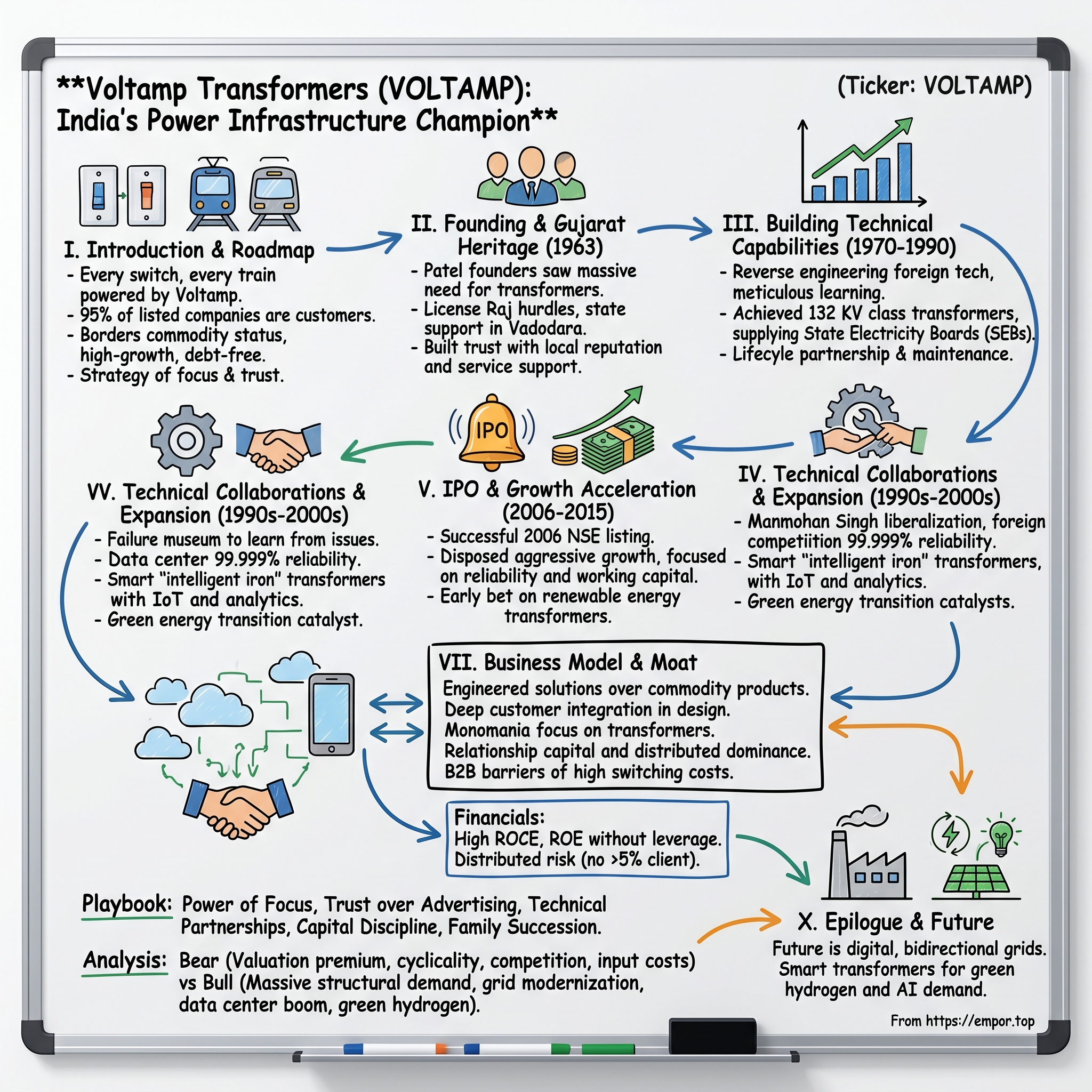

Voltamp Transformers: The Making of India's Power Infrastructure Champion

I. Introduction & Episode Roadmap

Picture this: Every time you flip a switch in an Indian office building, charge your phone at a metro station, or watch steel being forged in a blast furnace, there's a good chance the electricity powering that moment passed through a transformer made in a nondescript industrial estate in Vadodara, Gujarat. The company behind these ubiquitous gray boxes? Voltamp Transformers—a name that most investors have never heard of, despite the fact that 95% of India's listed companies are its customers.

Here's the snapshot that makes you sit up: ₹8,074 crore market cap, ₹1,930 crore in revenue, ₹326 crore in profit. Not bad for a company that makes what is essentially a commodity product—or so you'd think. But here's where it gets interesting: over the last five years, Voltamp has delivered a profit growth CAGR of 29.7% while maintaining an almost debt-free balance sheet. In an industry notorious for working capital stress and cyclical downturns, these numbers are borderline miraculous.

The central question we're exploring today is deceptively simple: How did a small workshop founded in 1963 in Vadodara become the go-to transformer supplier for virtually every major corporation in India? It's a story that spans six decades, three generations of the Patel family, multiple economic cycles, and the entire arc of India's industrial development.

We'll journey from the company's founding in the shadow of the License Raj, through technical collaborations with German engineering firms, to its current position as a critical supplier to data centers and renewable energy projects. Along the way, we'll uncover the counterintuitive strategies that allowed a boring industrial company to build one of the most enviable moats in Indian manufacturing.

Why does this story matter? Because in our obsession with software and consumer brands, we often forget that the physical economy still runs on hardware—unglamorous, essential hardware that requires decades of expertise to manufacture reliably. Voltamp's story is about the power of focus, the importance of trust in B2B relationships, and why sometimes the best businesses are the ones nobody wants to talk about at cocktail parties.

II. The Founding Story & Gujarat's Industrial Heritage

The year was 1963. Jawaharlal Nehru was still Prime Minister, the Green Revolution hadn't begun, and most of India was literally in the dark—only 3% of villages had electricity. In Vadodara, a city better known for its Maratha palaces than its industries, three men from the Patel community were having conversations that would shape India's power infrastructure for the next six decades.

Lalitkumar H. Patel, Babubhai H. Patel, and Navinchandra Patel weren't revolutionaries or visionaries in the Silicon Valley sense. They were practical men who understood a fundamental truth: if India was going to industrialize, it would need transformers—thousands upon thousands of them. Every factory, every power line, every industrial facility would need these devices to step voltage up or down. The import restrictions of the era meant foreign transformers were expensive and hard to procure. The opportunity was hiding in plain sight.

The Patels started with a small workshop in Makarpura, an industrial area of Vadodara that would later become Gujarat's engineering hub. Their initial capital was modest—pooled family savings and small loans from local banks who knew them personally. This wasn't venture capital; this was community capital, the kind where your reputation was the only collateral that mattered.

What's fascinating about the founding is how unglamorous it was. No grand vision statements, no disruption rhetoric. Just three engineers who believed they could build transformers as good as the imported ones, maybe better, definitely cheaper. They incorporated as a private limited company in 1967, a full four years after they'd started operations—a reminder that in those days, you proved your business worked before you formalized it.

The post-independence context is crucial here. This was Nehruvian socialism at its peak—the License Raj controlled who could manufacture what and in what quantities. Getting a license to manufacture transformers wasn't just about paperwork; it was about convincing bureaucrats that you had the technical capability to produce a critical infrastructure component. The Patels spent months shuttling between Vadodara and Delhi, carrying technical drawings and sample components, essentially teaching government officials what transformers did and why domestic production mattered.

Gujarat itself was undergoing a transformation. The state had just been carved out of Bombay State in 1960, and its first Chief Minister, Jivraj Mehta, was actively courting entrepreneurs. "Gujarat ni asmita"—Gujarati pride—wasn't just cultural; it was economic policy. The state government fast-tracked industrial licenses, provided land at subsidized rates, and most importantly, created an ecosystem where business wasn't seen as exploitation but as nation-building.

For the Patels, the early challenges were almost comically basic by today's standards. Copper had to be imported through government quotas. Specialized steel for transformer cores came from Rourkela Steel Plant when they felt like supplying it. Even getting consistent electricity to run their manufacturing equipment was a challenge—ironic for a company making transformers. They often worked nights when power supply was more stable, a practice that continued well into the 1970s.

But perhaps the biggest challenge was market education. In 1963, most Indian companies buying transformers didn't trust domestic manufacturers. The perception was that Indian-made meant inferior quality—a stigma that took years to overcome. The Patels' strategy was simple but laborious: they would personally visit every potential customer, often camping outside factories for days to get meetings with purchase managers. They offered something foreign suppliers couldn't: immediate service support. A transformer failure could shut down an entire factory; having the manufacturer two hours away instead of two continents away was a compelling value proposition.

By the end of the 1960s, Voltamp had established itself as a reliable, if small, player in the transformer market. They weren't the biggest or the most technically advanced, but they had something more valuable: the trust of their early customers, many of whom would remain clients for the next five decades. The foundation was set for what would become one of India's most enduring industrial success stories.

III. Early Years: Building Technical Capabilities (1970–1990)

January 1970 marked a watershed moment for Voltamp—not with fanfare or press releases, but with the quiet hum of their first 10,000 KVA transformer coming to life in the test bay. To understand the significance, consider this: most of their competitors were still manufacturing transformers below 1,000 KVA. This wasn't just a 10x improvement; it was a leap into an entirely different league, one that could serve steel plants and large industrial complexes rather than just small factories.

The story of how they achieved this leap reveals much about Voltamp's DNA. Unable to afford foreign consultants or technology transfers, the Patels adopted what they called "reverse engineering with respect"—they would buy damaged or decommissioned foreign transformers at scrap prices, meticulously disassemble them, study every component, and then figure out how to manufacture equivalents using Indian materials and methods. Babubhai Patel would later joke that they learned more from broken Westinghouse transformers than from any textbook.

The learning curve was steep and sometimes dangerous. In 1973, during testing of a 5,000 KVA unit, an insulation failure caused an explosion that destroyed three months of work and nearly killed two engineers. Rather than hide the failure, Voltamp invited their customer—Hindustan Zinc—to inspect the damage and participate in the root cause analysis. This radical transparency, unusual in an era of blame-shifting, earned them something more valuable than a contract: a reputation for integrity.

By 1981, Voltamp achieved another technical milestone: manufacturing 132 KV class transformers. The significance can't be overstated—132 KV transformers were the backbone of state electricity transmission networks. Until then, State Electricity Boards (SEBs) had to import these or buy from BHEL, the government-owned behemoth. Voltamp's entry into this segment was enabled by an unlikely source: retired BHEL engineers who joined them as consultants, bringing decades of expertise and, crucially, the trust of SEB procurement departments.

The relationship with SEBs deserves special attention. These were monolithic organizations, slow to pay, slower to decide, but once you were approved as a vendor, the orders were massive and multi-year. Voltamp's strategy was patient relationship-building. They would supply one transformer at a loss if needed, just to get on the approved vendor list. They stationed service engineers at SEB substations for free, ostensibly for "training" but really to ensure their transformers never failed. When Gujarat State Electricity Board had a crisis in 1983—multiple transformer failures during peak summer—Voltamp mobilized its entire workforce to provide emergency replacements within 72 hours, a feat that became legend in utility circles.

By 1986, the company had scaled up to manufacturing 50 MVA, 132 KV power transformers. The economics of this business were fascinating: a single 50 MVA transformer could cost ₹50-60 lakhs (enormous money in 1986), but the profit margins were thin—often under 10%. The real money wasn't in the sale but in the lifetime service contract. Voltamp pioneered what they called "lifecycle partnership"—they wouldn't just sell you a transformer; they'd maintain it for 25 years, essentially creating an annuity stream from a one-time sale.

The pre-liberalization era posed unique challenges. Foreign exchange was scarce, so importing specialized components required navigating bureaucratic mazes. Voltamp's solution was localization—they systematically replaced imported components with domestic alternatives. When they couldn't find Indian suppliers for specialized insulation paper, they worked with a Pune-based company to develop it. When German cooling fans were too expensive, they collaborated with Crompton Greaves to design equivalents. This wasn't just cost-cutting; it was building an ecosystem.

Quality control in this era was more art than science. Without sophisticated testing equipment, Voltamp relied on what they called "generational knowledge"—senior technicians who could diagnose problems by sound, smell, and intuition. The famous story goes that Lalitkumar Patel could tell if a transformer's oil needed treatment just by rubbing a drop between his fingers. This tactile expertise couldn't be documented in ISO procedures, but it prevented countless field failures.

The 1980s also saw Voltamp's first international foray—not through exports, but through reverse migration of talent. Indian engineers who had worked at Voltamp were recruited by Middle Eastern utilities, and they specified Voltamp transformers in their projects, creating an unexpected export market. By 1989, Voltamp was supplying transformers to Kuwait, UAE, and Saudi Arabia—markets that would provide crucial foreign exchange in the coming liberalization era.

As the 1990s approached, Voltamp had transformed from a small workshop to a serious industrial player with over 500 employees and annual revenues crossing ₹25 crores. But the real transformation was yet to come. Economic liberalization would bring competition, opportunity, and the need for a completely different playbook.

IV. Technical Collaborations & Expansion (1990s–2000s)

July 1991. Finance Minister Manmohan Singh had just announced economic liberalization. In Voltamp's Vadodara boardroom, the mood was tense. "The Germans are coming, the Japanese are coming," one board member said, referring to the imminent entry of Siemens and Toshiba into the Indian transformer market. The consensus among industry watchers was clear: domestic manufacturers would be roadkill on the highway of globalization.

Navinchandra Patel, who had taken over operational leadership, had a different view. At a management meeting that has since become company lore, he pulled out a list of Voltamp's top 100 customers and asked a simple question: "Will Reliance stop buying from us because Siemens has arrived? Will L&T abandon a 20-year relationship for a marginally better transformer?" The answer, he believed, was no—if Voltamp could match international quality while maintaining its service advantage.

The strategy that emerged was counterintuitive: instead of seeing foreign companies as threats, Voltamp would partner with them. But not as junior partners or toll manufacturers—as technology equals. The first breakthrough came in 1998 with Mora Transformatoren GmbH, a mid-sized German company specializing in vacuum resin impregnated dry-type transformers. The negotiation took eighteen months and nearly fell apart multiple times over intellectual property rights. Voltamp insisted on not just licensing but technology transfer with the right to improve and indigenize. The Germans initially balked—why would they create a future competitor?

The answer came during a site visit to Vadodara. The Mora team was amazed to find Voltamp engineers had modified a 1970s-era winding machine to achieve tolerances comparable to their computerized equipment. "Your jugaad is better than our automation," the German technical director reportedly said. The partnership was signed with unprecedented terms: Voltamp could modify German designs for Indian conditions and even export to markets where Mora wasn't present.

The year 2000 brought another strategic pivot: induction furnace transformers. This was a niche nobody wanted to touch—the power quality issues in steel plants made these transformers prone to failure, and most manufacturers considered them more trouble than they were worth. Voltamp saw opportunity in difficulty. They embedded engineers in steel plants for months, studying failure patterns, harmonic distortions, and temperature cycles. The result was a transformer designed specifically for Indian steel plants' notorious operating conditions—over-engineered where it mattered, cost-optimized where it didn't.

The real coup came in 2002 with the partnership with Hochspannungstechnik und Transformatorbau GmbH (HTT) for cast resin dry-type transformers. These were the Ferraris of the transformer world—used in metros, airports, and hospitals where fire safety was paramount. The technology was closely guarded; only five companies globally had mastered it. HTT chose Voltamp over larger competitors because of one incident: during due diligence, they found Voltamp had voluntarily recalled 15 transformers due to a potential insulation issue that hadn't caused any failures yet. "This is German thinking in an Indian company," the HTT evaluation report noted.

The technology transfer wasn't just about blueprints and machinery. Voltamp sent 30 engineers to Germany for six-month stints, not just to learn processes but to understand the philosophy of precision engineering. These engineers came back as evangelists for what they called "zero-defect manufacturing"—a radical concept in an Indian industry that accepted 2-3% failure rates as normal.

Meanwhile, the domestic market was exploding. The Indian economy was growing at 8-9% annually, and power demand was surging. But Voltamp made a curious choice: instead of maximizing volume, they focused on complexity. When NTPC needed transformers for ultra-critical supercritical power plants, when Reliance needed specialized units for the world's largest refinery at Jamnagar, when Delhi Metro needed compact transformers that could fit in underground stations—Voltamp said yes to projects others deemed too challenging.

The conversion to a public limited company in 2006 was driven by an unusual problem: success. Major customers like L&T and Siemens wanted to increase orders but were hitting internal limits on exposure to private companies. "We need you to be more transparent," L&T's procurement head told them. Going public wasn't about raising capital—Voltamp was already cash-positive—it was about institutional credibility.

The IPO in September 2006 became a watershed moment. Priced at ₹290, it was oversubscribed 17 times, with institutional investors putting in bids worth ₹2,400 crores for an issue size of ₹140 crores. But here's what's remarkable: the roadshow presentations barely mentioned growth projections or market expansion. Instead, they focused on one slide showing 40-year relationships with customers. "We're not selling equity, we're selling trust," Navinchandra Patel told investment bankers, who thought he was crazy. The market thought otherwise.

Post-IPO, Voltamp could have gone on an acquisition spree or diversified into adjacent businesses. They did neither. The capital was deployed with almost boring predictability: technology upgrades, quality certifications, and slowly expanding capacity. When asked by analysts why they weren't more aggressive, the response was telling: "A transformer failure can black out a city. Our customers don't want aggressive; they want reliable."

By 2008, Voltamp had achieved something remarkable: they were simultaneously vendors to competing companies. Siemens and ABB, bitter rivals in the power equipment space, both sourced transformers from Voltamp. BHEL, which competed with Voltamp in some segments, bought specialized transformers from them for complex projects. This wasn't just market success; it was market validation at the highest level.

V. The IPO & Growth Acceleration (2006–2015)

The NSE opening bell on September 26, 2006, marked more than Voltamp's debut as a public company—it was the moment a 43-year-old family business stepped into the harsh spotlight of quarterly earnings calls and analyst scrutiny. The first question from a fund manager was predictably aggressive: "Your capacity utilization is only 70%. Why should we believe you can deploy IPO proceeds efficiently?" Navinchandra Patel's answer would define Voltamp's relationship with capital markets for the next decade: "Because we've never built capacity we couldn't fill with orders. We build demand first, capacity second."

This philosophy was immediately tested. The IPO had raised ₹140 crores, and the board had approved an ambitious expansion: from 3,000 MVA annual capacity to 9,000 MVA by 2008. The conventional approach would be to build one large, state-of-the-art facility. Voltamp chose differently—three smaller expansions at existing sites, each targeted at specific market segments. The logic was risk mitigation: if one market slowed, the others could compensate.

The 2008 financial crisis provided an unexpected vindication of this strategy. While competitors with massive, integrated plants ran at 40% utilization, Voltamp maintained 75% by quickly shifting production lines between export orders (which crashed) and domestic infrastructure projects (which the government accelerated as stimulus). A visiting McKinsey consultant studying Indian manufacturing called it "accidentally brilliant strategy"—though there was nothing accidental about it.

The Vadadla facility, commissioned in 2009 with a ₹35 crore investment, embodied Voltamp's evolved manufacturing philosophy. Instead of automation for automation's sake, they implemented what they called "appropriate technology." CNC winding machines sat next to manual assembly stations. German-imported vacuum drying ovens operated alongside locally fabricated testing equipment. The plant manager, a 30-year Voltamp veteran, explained: "A Rs. 2 crore robot can wind coils perfectly, but our Rs. 50,000-per-year technician can wind coils perfectly and tell you why the copper feels different today."

By 2010, Voltamp had quietly become one of India's largest transformer manufacturers with 13,000 MVA capacity. But the real story wasn't capacity—it was capability. When the Delhi Metro needed transformers that could handle regenerative braking (trains feeding power back to the grid), only Voltamp and ABB could deliver. When ONGC needed transformers for offshore platforms that could withstand salt spray and cyclonic conditions, Voltamp developed a specialized coating that became industry standard. These weren't just sales; they were engineering victories that competitors couldn't easily replicate.

The customer list from this period reads like a who's who of Indian industry, but the way these relationships developed is instructive. Take the example of Jindal Steel. In 2011, their Angul plant faced repeated transformer failures due to harmonic distortions from electric arc furnaces. Voltamp didn't just supply replacement transformers; they stationed a team at Angul for three months, redesigned the transformers with custom harmonic filters, and guaranteed zero failures for five years. They delivered on that guarantee. Jindal hasn't bought transformers from anyone else since.

The international expansion during this period was notably cautious. While competitors chased large orders in Africa and Southeast Asia, often getting burned by payment defaults, Voltamp focused on what they called "Indian ecosystem exports"—supplying transformers to Indian companies' overseas projects. When L&T won a contract in Dubai, when Tata Projects built infrastructure in South Africa, when Reliance set up facilities in Malaysia, Voltamp transformers went along. This strategy meant lower margins but virtually zero bad debts.

Financial performance during this period was remarkably consistent: revenues grew from ₹380 crores in FY2007 to ₹890 crores in FY2015, while PAT expanded from ₹28 crores to ₹67 crores. But the number that really mattered was working capital days—in an industry notorious for 180-day cycles, Voltamp maintained 90-100 days. How? By choosing customers carefully and walking away from orders that didn't meet their payment terms. "We'd rather run at 80% capacity with good customers than 100% with bad ones," became an internal mantra.

The promoter restructuring in 2014—amalgamating Kunjal Investments Private Limited with Voltamp—was presented as a corporate simplification exercise. The real story was more nuanced. The second generation of the Patel family was taking charge, and they wanted clear, unambiguous ownership structures. No holding companies, no cross-holdings, no complex structures that could create conflicts. "We're engineers running an engineering company," said the new generation. "Let's keep the corporate structure as simple as our transformers."

One decision from this period stands out for its long-term thinking. In 2013, when solar and wind power were still considered fringe, Voltamp began developing specialized transformers for renewable energy. The business case was terrible—volumes were low, specifications kept changing, and customers were mostly undercapitalized developers. The board questioned the focus. Management's response: "Every power transition in history needed new transformer technology. We're betting renewable energy is a transition, not a fad." That bet would pay off spectacularly in the coming decade.

By 2015, Voltamp had evolved from a family-run manufacturer to a professionally managed corporation, yet it retained its core DNA: technical excellence, customer obsession, and an almost pathological aversion to financial engineering. While peers leveraged up for growth, Voltamp remained nearly debt-free. While others diversified into real estate or trading, Voltamp stayed focused on transformers. Boring? Perhaps. But as the next phase would show, sometimes boring is beautiful.

VI. Modern Era: Consolidation & Leadership (2015–Present)

The boardroom at Voltamp's Makarpura headquarters has a peculiar tradition. Every quarter, before discussing financial results, they review what they call the "failure museum"—a presentation of every transformer failure, every customer complaint, every service delay. On March 2019, this presentation had just one slide: "Zero failures in data center transformers for 24 consecutive months." In an industry where 0.5% failure rate is considered world-class, this was unprecedented. The story of how Voltamp achieved this—and leveraged it to dominate emerging sectors—defines their modern era.

The inflection point came in 2016 when Amazon Web Services was scouting locations for Indian data centers. Their requirement was specific: transformers with 99.999% reliability (five nines), capable of handling massive load fluctuations, and vendors who could provide 24/7 support. Most manufacturers balked at the service level agreements—penalties for even minutes of downtime could run into crores. Voltamp not only accepted these terms but proposed something radical: resident engineers who would predict failures before they occurred using IoT sensors and predictive analytics.

This wasn't Voltamp's traditional wheelhouse. The company that had built its reputation on mechanical engineering excellence was now talking about cloud-connected transformers and machine learning algorithms. The transformation was led by an unlikely alliance: second-generation Patel family members who had returned from US universities and veteran engineers who had spent decades reading transformer behavior through instinct. Together, they created what customers now call "intelligent iron"—transformers that report their own health status.

The new Jarod facility, commissioned in FY2025, represents this philosophy in concrete and steel. Spread across 50 acres, it's not the size that's impressive (competitors have larger facilities) but the design thinking. The factory is divided into "cells," each capable of producing complete transformers independently. This isn't just operational flexibility; it's risk management. If one cell goes down, others continue. If a customer needs ultra-urgent delivery, an entire cell can be dedicated to their order. The capital cost was 40% higher than a traditional layout, but production flexibility increased by 200%.

The numbers tell a compelling story: revenue reached ₹1,930 crores in FY2024, with profit after tax of ₹326 crores—a net margin of 16.9% in an industry where 8-10% is standard. But the real story is market position. When CRISIL analyzed the transformer industry in 2023, they found something remarkable: 95% of NSE-listed companies were Voltamp customers. This wasn't market dominance; it was market ubiquity. The strategic decisions made during this period reveal a company at the peak of its powers yet paranoid about complacency. When private equity firms approached with buyout offers valuing Voltamp at 25x earnings (astronomical for an industrial company), the Patel family's response was instructive: "We're not in the business of selling companies; we're in the business of building them." This wasn't just family sentiment—it was strategic thinking about the value of independence in a consolidating industry.

The green energy transition became Voltamp's unexpected growth catalyst. As an increase in demand for electricity and transformers has been projected over the next 5 to 6 years period, the company positioned itself at the intersection of renewable generation and grid stability. Solar and wind farms needed specialized transformers that could handle reverse power flow and voltage fluctuations. Voltamp didn't just supply these; they pioneered "grid-friendly" transformers with built-in power quality management—essentially making renewable energy more palatable to traditional grids.

The promoter holding decrease from 50% to 37.8% over three years raised eyebrows, but the reality was more nuanced. This wasn't distress selling but strategic dilution—bringing in institutional investors who could open doors in international markets. When Singapore's Temasek picked up a stake, it wasn't just for returns; they wanted Voltamp transformers in Southeast Asian smart city projects.

Voltamp Transformers Ltd expects to complete the construction of its new transformer manufacturing facility by July 2026, with annual capacity of around 6000 MVA in the first phase. The capital outlay for the new unit is around INR 200 crore ($23.9 million), which will be financed through internal accruals—a testament to their cash generation capabilities.

The current order book tells its own story: opening order book of Rs.840.66 crore with new order inflow from April 1, 2024 to around July 29, 2024 standing at Rs.639 crore, providing revenue visibility of Rs.1,479.66 crore. This isn't just backlog; it's validation from customers voting with purchase orders.

Yet challenges loom. Managing the supply chain, which includes sourcing raw material and components at budgeted costs and in time, will be the key challenge, while the recent uptick in input prices, led by industrial metal prices and scarcity of CRGO, is likely to result in higher input cost. Voltamp's response has been characteristic: long-term contracts with suppliers, strategic inventory building, and most importantly, the ability to pass through cost increases due to their technical differentiation.

The modern Voltamp is a study in contrasts: a 60-year-old company that acts like a startup in R&D, a family business run with multinational governance standards, a manufacturer of century-old technology that's essential for 21st-century infrastructure. As one longtime customer put it: "They're boring in all the right ways and innovative where it matters."

VII. The Business Model & Competitive Advantages

Walk into any Voltamp sales meeting and you'll notice something unusual: engineers outnumber salespeople three to one. This isn't poor resource allocation; it's the essence of their business model. "We don't sell transformers," a senior executive explains, "we sell engineered solutions that happen to be transformers." In an industry where products are often commoditized, this distinction has created a moat that's proven remarkably durable.

The product portfolio appears straightforward: oil-filled transformers (60% of revenue), cast resin transformers (25%), unitized substations (10%), and specialty products like induction furnace transformers (5%). But this categorization masks the complexity. Within oil-filled transformers alone, Voltamp manufactures over 500 variants—different voltage classes, cooling mechanisms, winding configurations, each optimized for specific applications. A transformer for a cement plant handles different stresses than one for a data center, though both might be rated identically.

The manufacturing capability to produce transformers up to 160 MVA and 220 KV class puts Voltamp in an exclusive club—only six manufacturers in India have this capability, and only two (including Voltamp) combine it with cast resin technology. But capability alone doesn't explain their 95% penetration among listed companies. The answer lies in what customers call the "Voltamp ecosystem."

Consider the lifecycle of a typical transformer sale. It starts 18-24 months before delivery when a customer is still designing their facility. Voltamp engineers embed themselves in the design process, optimizing not just transformer specifications but entire electrical layouts. They'll suggest ways to reduce cable runs, improve power factor, minimize harmonics—often saving customers crores in capital costs before selling them a single transformer. This consultative approach means that by the time purchase orders are raised, Voltamp isn't competing; they're specified into the project.

The service advantage deserves special attention. With 70,000 installations across India and overseas, Voltamp has created what is essentially a distributed monitoring network. Their service teams don't just respond to failures; they predict them. Oil analysis, thermal imaging, partial discharge testing—these aren't revenue centers but customer retention tools. The data is staggering: Voltamp monitors over 15,000 transformers monthly, generating terabytes of performance data that feed back into design improvements.

This brings us to an underappreciated aspect of the business model: institutional memory monetization. Every transformer failure, every service call, every customer complaint over 60 years has been documented and analyzed. This isn't just quality control; it's accumulated wisdom that manifests in subtle design choices—a different gasket material for coastal installations, modified cooling fins for dusty environments, enhanced surge protection for facilities near lightning-prone areas. Competitors can copy products but not six decades of failure analysis.

The working capital dynamics reveal sophisticated financial engineering disguised as operational excellence. In an industry where 150-180 day cycles are standard, Voltamp maintains 90-100 days through several mechanisms. First, staged payments: 30% advance, 60% on delivery, 10% after commissioning—cash flow positive before manufacturing begins. Second, supplier financing: long-term relationships mean extended payment terms without interest. Third, selective customer base: they've walked away from government contracts with 270-day payment terms, preferring private sector clients who pay faster.

The B2B dynamics create natural barriers to entry that aren't immediately obvious. Transformer failure can cost a steel plant ₹50 lakhs per day in lost production. A data center outage can trigger SLA penalties running into crores. In this context, saving 10% on transformer cost by switching vendors is irrational risk-taking. Voltamp's 30-year relationships with customers like L&T and Siemens aren't just commercial; they're technical partnerships where switching costs are measured not in money but in accumulated trust.

Perhaps the most elegant aspect of the business model is how boring it appears to potential competitors. Venture capitalists aren't funding transformer startups. Tech companies aren't trying to disrupt this space. Chinese competitors find that competing on price alone doesn't work when total cost of ownership over 25 years matters more than initial purchase price. The very characteristics that make transformers unsexy—long sales cycles, capital intensity, technical complexity—are what make Voltamp's position defensible.

The financial metrics validate this model: ROCE of 29.1% in a capital-intensive business, ROE of 21.7% without leverage, and consistent 15-17% net margins in an industry where 8-10% is standard. But the number that best captures the model's strength is customer concentration: no single customer exceeds 5% of revenue, yet customer retention exceeds 95%. This isn't dependence; it's distributed dominance.

An analyst once asked why Voltamp doesn't expand into adjacent electrical equipment. The answer was revealing: "Every hour spent on circuit breakers or switchgear is an hour not spent becoming better at transformers. In 60 years, we've learned that focus isn't a limitation; it's a superpower." In a world obsessed with diversification, Voltamp's monomania seems almost radical. The results suggest it might also be right.

VIII. Playbook: Business & Investing Lessons

There's a slide in Voltamp's internal training program that would make Silicon Valley founders cringe: a graph showing revenue growth averaging 12% annually over 60 years. No hockey sticks, no exponential curves, just a steady upward line that looks almost boring. "This is what compound excellence looks like," the trainer explains. The lessons from Voltamp's journey offer a masterclass in building enduring industrial businesses—principles that run counter to much of contemporary business wisdom.

The Power of Focus: In six decades, Voltamp has resisted every diversification temptation. When power equipment peers expanded into real estate during the 2003-2007 boom, Voltamp stayed with transformers. When the infrastructure boom made construction equipment attractive, they passed. Even adjacent products like switchgear and panels, which use the same customers and channels, were avoided. This monomaniacal focus had compound effects: deeper expertise, stronger reputation, better economics. As one board member noted: "Every time we were tempted to diversify, we instead invested in becoming better at transformers. That's why we have 30% ROCE in a business others struggle to get 15%."

Building Trust in B2B: Voltamp's approach to relationship building seems almost quaint in the age of digital marketing. No celebrity endorsements, minimal advertising, no social media campaigns. Instead, they have what they call "trust deposits"—hundreds of small actions that build credibility. When a customer's transformer failed due to their own maintenance error, Voltamp replaced it for free. When a competitor's transformer exploded at a refinery, Voltamp engineers helped investigate even though they might lose the replacement order. These aren't in any ROI calculation, but they're why procurement managers stake their careers on Voltamp transformers.

Technical Partnerships vs. Technology Acquisition: While competitors acquired foreign companies or licensed technology wholesale, Voltamp's approach was nuanced. Their German partnerships weren't subordinate relationships but collaborative ventures where Indian frugal engineering met German precision. The ability to modify and improve licensed technology, rather than just implementing it, created unique products suited for Indian conditions—something pure technology transfer could never achieve.

Capital Allocation Discipline: The temptation after the successful IPO must have been immense—leverage up, make acquisitions, expand aggressively. Voltamp did none of these. Capital allocation followed a simple hierarchy: technology upgrades first, capacity expansion second, and only when existing capacity exceeded 80% utilization. No marquee acquisitions, no unrelated diversification, no financial engineering. This discipline meant lower growth rates but higher returns on capital—a trade-off many companies talk about but few execute.

Family Business Succession: The transition from founders to second generation to professional management could fill a business school case study. Key principles emerged: family members had to prove competence externally before joining, professional managers were given real autonomy, and family disputes were resolved outside the boardroom. The decision to merge the holding company with the operating company sent a signal: this wasn't a family extracting value from a business but a family committed to a business.

Riding Waves Without Leverage: India's infrastructure boom created massive opportunities, and the temptation to leverage up for growth was significant. Voltamp's approach was different: grow with customers, not ahead of them. When L&T expanded internationally, Voltamp followed. When data centers boomed, they were ready. But they never bet the company on sector forecasts. This meant missing some opportunities but also avoiding the debt traps that crippled competitors during downturns.

The Innovation Paradox: In a 150-year-old industry, what innovation looks like is subtle but crucial. Voltamp's innovations weren't breakthrough technologies but incremental improvements: transformers that needed 20% less maintenance, designs that reduced failure rates from 0.5% to 0.1%, coatings that extended life from 25 to 30 years. Individually minor, collectively they created products that customers couldn't replicate with cheaper alternatives.

Relationship Capital Compounding: Every long-term customer relationship became a competitive advantage that compounded over time. A 30-year relationship with Siemens meant understanding their global specifications, being pre-qualified for projects, and having informal information channels that no new competitor could match. These relationships weren't just commercial; they were technical partnerships where switching costs grew over time.

The Boring Business Advantage: Voltamp's executives joke that they're in the "world's most boring business," but this is a feature, not a bug. Boring means predictable demand, rational competition, and limited disruption risk. While exciting businesses attract capital and competition, boring businesses can quietly compound returns for decades. As one investor noted: "I'd rather own a boring business with exciting returns than an exciting business with boring returns."

Patience as Strategy: In an era of quarterly capitalism, Voltamp played a different game. Customer relationships were measured in decades, not quarters. Capacity investments were evaluated over 10-year horizons. Employee tenures averaged 15+ years. This patience wasn't passive; it was strategic. While competitors optimized for immediate returns, Voltamp optimized for durability.

The meta-lesson from Voltamp's playbook is that sustainable competitive advantages in industrial businesses come not from any single brilliant strategy but from the accumulation of hundreds of good decisions over decades. It's not about disruption but about evolution, not about revolution but about relentless incremental improvement. In a business world obsessed with transformation, Voltamp proves that sometimes the best strategy is to keep doing what you're doing, just a little better each year.

IX. Analysis & Bear vs. Bull Case

The investment community's view on Voltamp presents a fascinating dichotomy. Bulls see an infrastructure play on India's unstoppable electrification. Bears see a cyclical manufacturer trading at premium valuations in a commoditizing industry. Both have compelling arguments, but as with most investment debates, the truth requires nuance beyond surface metrics.

The Bull Case:

Start with the macro backdrop: India's per capita electricity consumption at 1,200 kWh is one-third of the global average. Every analyst projection shows this doubling by 2030. Simple math suggests transformer demand should double too, but the reality is more complex—and more bullish. Grid modernization means replacing not just failed transformers but functioning ones that can't handle bidirectional power flow from renewable sources. The shift from centralized to distributed generation multiplies transformation points. A single solar park needs dozens of transformers where a thermal plant needed just a few.

The numbers support this narrative: Company has delivered good profit growth of 29.7% CAGR over last 5 years, dramatically outpacing industry growth of 10-12%. This isn't just riding a wave; it's taking market share. The financial metrics are even more compelling: ROCE of 29.1% and ROE of 21.7% in a capital-intensive business, achieved while being almost debt free.

The customer base provides the moat: 95% of listed companies as clients isn't just market dominance; it's infrastructure lock-in. These aren't relationships that change with price quotes. When Siemens has been buying transformers from you for 30 years, switching to save 5% makes no sense given the technical, operational, and relationship risks.

The data center opportunity alone could double Voltamp's addressable market. India needs 15-20 GW of data center capacity by 2030, up from 1 GW today. Each MW of data center capacity needs roughly 2 MVA of transformer capacity, but with redundancy requirements, it's closer to 4 MVA. That's 60,000-80,000 MVA of new transformer demand—about six years of Voltamp's current production—from just one sector.

Green hydrogen, electric vehicle charging infrastructure, battery storage systems—each represents massive transformer demand that didn't exist five years ago. Voltamp's early investments in these segments position them to capture disproportionate share as these markets mature.

The financial resilience is remarkable: Company has been maintaining a healthy dividend payout of 30.4% while funding all expansion from internal accruals. This isn't financial engineering; it's operational excellence generating real cash flows.

The Bear Case:

Yet the stock market seems unconvinced: Mkt Cap: 7,982 Crore (down -39.5% in 1 year). This isn't just general market weakness; it's specific concern about Voltamp's future. The bears have legitimate worries.

First, the valuation question. At 26x trailing earnings, Voltamp trades at premiums to both Indian and global transformer manufacturers. ABB's power products division trades at 18x, Siemens' similar business at 15x. The premium assumes continued outperformance, but history shows industrial cycles can turn quickly.

The promoter holding decrease is concerning: Promoter holding has decreased over last 3 years: -12.2% to the current Promoter Holding: 37.8%. While management explains this as strategic dilution, markets wonder if insiders are cashing out at peak valuations.

Competition from Chinese manufacturers is intensifying. Chinese transformers cost 20-30% less, and while quality gaps existed historically, they're narrowing. More concerning, Chinese companies are willing to accept 5% margins to gain market share—a price war Voltamp can't win despite operational excellence.

The cyclical nature of capital goods is inescapable. Current demand is driven by capex cycles that historically last 5-7 years before sharp corrections. With interest rates rising globally and infrastructure spending potentially peaking, the next down cycle could be severe.

Technology disruption, while seemingly distant, isn't impossible. Solid-state transformers, though currently 10x more expensive, could revolutionize power distribution. If costs fall following solar panel or battery trajectories, traditional transformers could face existential threats within a decade.

Input cost pressures are mounting: The recent uptick in input prices, led by industrial metal prices and scarcity of CRGO, is likely to result in higher input cost in the years ahead. With copper at multi-year highs and specialized steel in short supply, margin compression seems inevitable.

Customer concentration risk is real despite diversification. The top 20 customers contribute 40% of revenues. If even a few defer capex or switch vendors, impact would be material.

The Synthesis:

The truth likely lies between these extremes. Voltamp is neither a perpetual compounding machine nor a cyclical value trap. It's a well-managed industrial company in a structurally growing market but facing legitimate challenges.

The infrastructure thesis remains intact—India needs massive electrical infrastructure investment regardless of economic cycles. But the pace and profitability of this build-out are variables, not constants. Voltamp's competitive position is strong but not impregnable. Their advantages in service, relationships, and technical capability are real but eroding slowly as competitors improve.

The financial metrics suggest quality, but the market pricing suggests skepticism. This disconnect often creates opportunity, but it can also signal information asymmetry. The promoter selling could be portfolio rebalancing or knowledge of challenges ahead—impossible to know definitively.

For investors, Voltamp represents a classic quality-versus-value debate. The business quality is undeniable, but at current valuations, future returns depend on continued execution excellence and market share gains—not impossible, but not guaranteed. The margin of safety that value investors seek isn't present, while the growth that momentum investors want is decelerating.

Perhaps the most balanced view comes from understanding Voltamp as a GARPy proposition—Growth at a Reasonable Price—if one believes India's infrastructure story and Voltamp's execution capability. It's not cheap enough for deep value investors nor growing fast enough for growth investors, but for quality-focused investors with decade-long horizons, the risk-reward could be attractive.

X. Epilogue & Future Outlook

Standing at the new Jarod facility construction site, you can see the future of Indian power infrastructure taking shape—literally. The skeletal framework of what will be transformers of up to 250 MVA capacity, in the 220 kV class rises against the Gujarat sky. But more interesting than the physical infrastructure is what it represents: a bet that India's energy transition will need not just more transformers, but fundamentally different ones.

The energy transition isn't just about adding renewable capacity; it's about reimagining the grid. The traditional model—large power plants sending electricity one way to passive consumers—is dying. The future grid is bidirectional, decentralized, and digital. Every rooftop solar installation, every electric vehicle, every battery storage system is both a consumer and potential producer of power. This complexity multiplies the need for transformation points exponentially.

Consider the mathematics: India aims for 500 GW of renewable capacity by 2030. But renewable plants typically need 3-4 times more transformers per MW than conventional plants due to their distributed nature and lower capacity factors. Add grid stability requirements, redundancy needs, and the replacement of aging infrastructure, and you're looking at transformer demand that could be 5-10x current levels. Voltamp's planned capacity addition of 6,000 MVA seems almost conservative in this context.

The data center opportunity deserves special attention. India's data localization requirements, combined with AI's computational demands, are driving unprecedented data center construction. But these aren't traditional data centers—they need transformers that can handle massive, instant load variations as AI training cycles spike and drop. Voltamp's early work with hyperscalers has given them unique insights into these requirements, positioning them to capture disproportionate share of this high-margin segment.

The technology evolution within transformers is accelerating. Digital transformers with embedded sensors and analytics capabilities are moving from concept to commercial reality. Voltamp's partnership with Indian IoT startups to develop "smart transformers" that predict their own maintenance needs could be a game-changer. Imagine transformers that optimize their own performance based on load patterns, ambient conditions, and grid requirements—this isn't science fiction but engineering reality within this decade.

Green hydrogen presents another transformative opportunity. Electrolyzer plants need specialized transformers that can handle unique power quality requirements. With India targeting 5 million tonnes of green hydrogen production by 2030, each requiring roughly 50 MW of electrolyzer capacity, the transformer opportunity is massive and technically challenging—exactly Voltamp's sweet spot.

The leadership transition underway is crucial. The third generation of the Patel family, many with international engineering and business education, brings fresh perspectives while respecting institutional knowledge. Their focus on sustainability—not just as compliance but as product differentiation—could open new markets. Transformers with lower losses, longer life, and recyclable components command premium pricing in developed markets.

Yet challenges loom large. The global supply chain disruptions have exposed vulnerabilities in specialized component sourcing. Managing the supply chain, which includes sourcing raw material and components at budgeted costs and in time, will be the key challenge. Voltamp's response—backward integration into critical components—requires capital and expertise outside their traditional competence.

The competitive landscape is evolving rapidly. Global majors like Hitachi and Schneider, previously focused on developed markets, are aggressively entering India. Chinese manufacturers are moving up the value chain. New-age companies are experimenting with solid-state transformers. Voltamp's response will determine whether they remain leaders or become another industrial has-been.

The financial markets' current skepticism, reflected in the stock's underperformance, might be missing the forest for the trees. Yes, current valuations embed high expectations. Yes, competition is intensifying. But the structural drivers of transformer demand—electrification, renewable transition, digital infrastructure—are multi-decade themes just beginning.

What would success look like in 10 years? A Voltamp that's not just larger but fundamentally different: a technology company that happens to manufacture transformers rather than a manufacturing company trying to add technology. A company whose transformers don't just transform voltage but enable the energy transition. A company whose boring products enable exciting futures.

The final reflection brings us full circle. In 1963, three engineers in Vadodara began making transformers because India needed them. In 2034, their successors will still be making transformers because India—and the world—will need them even more. The products might be smarter, the manufacturing more automated, the customers more demanding, but the core mission remains: enabling the flow of power that drives human progress.

Voltamp's story reminds us that in our obsession with disruption, we sometimes forget that civilization runs on companies that do important things reliably, repeatedly, and incrementally better. Not every business needs to change the world; some just need to power it. In transformers, as in investing, the biggest returns often come not from transformation but from compound excellence executed over decades.

The boring business of making transformers might just be one of the most exciting investments of the next decade—if you have the patience to wait and the wisdom to recognize that sometimes, the future looks remarkably like the past, just at a larger scale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube