Vinati Organics: The Chemical Monopoly Nobody Knows About

I. Introduction & Episode Teaser

Picture this: A chemical company you've never heard of controls 65% of the global market for two obscure compounds with unpronounceable names—ATBS and IBB. No Silicon Valley venture capital, no flashy marketing campaigns, no viral TikToks. Just a father-daughter duo in Maharashtra, India, quietly dominating supply chains that touch everything from your shampoo to the oil rigs in the North Sea.

This is the story of Vinati Organics—a ₹16,988 crore market cap company that most investors have never encountered, yet one that embodies perhaps the purest form of competitive advantage: becoming so essential to global supply chains that customers have no viable alternative.

The question that should haunt every investor: How did a former Aditya Birla executive, starting with just ₹57 lakhs of personal savings in 1989, build what Warren Buffett would call the ultimate moat—a legal monopoly in specialty chemicals that even Chinese manufacturers can't crack?

What you're about to discover isn't just another corporate success story. It's a masterclass in finding the intersection of chemistry, patience, and market dynamics. It's about choosing products so niche that only three companies worldwide even attempt to make them—and then systematically eliminating the competition through superior execution.

By the end of this journey, you'll understand why sometimes the best businesses aren't the ones revolutionizing industries, but those perfecting a single, critical compound that nobody else wants to touch. You'll see how a near-bankruptcy experience in 2006 became the catalyst for global domination. And you'll learn why, in specialty chemicals, being boring is beautiful.

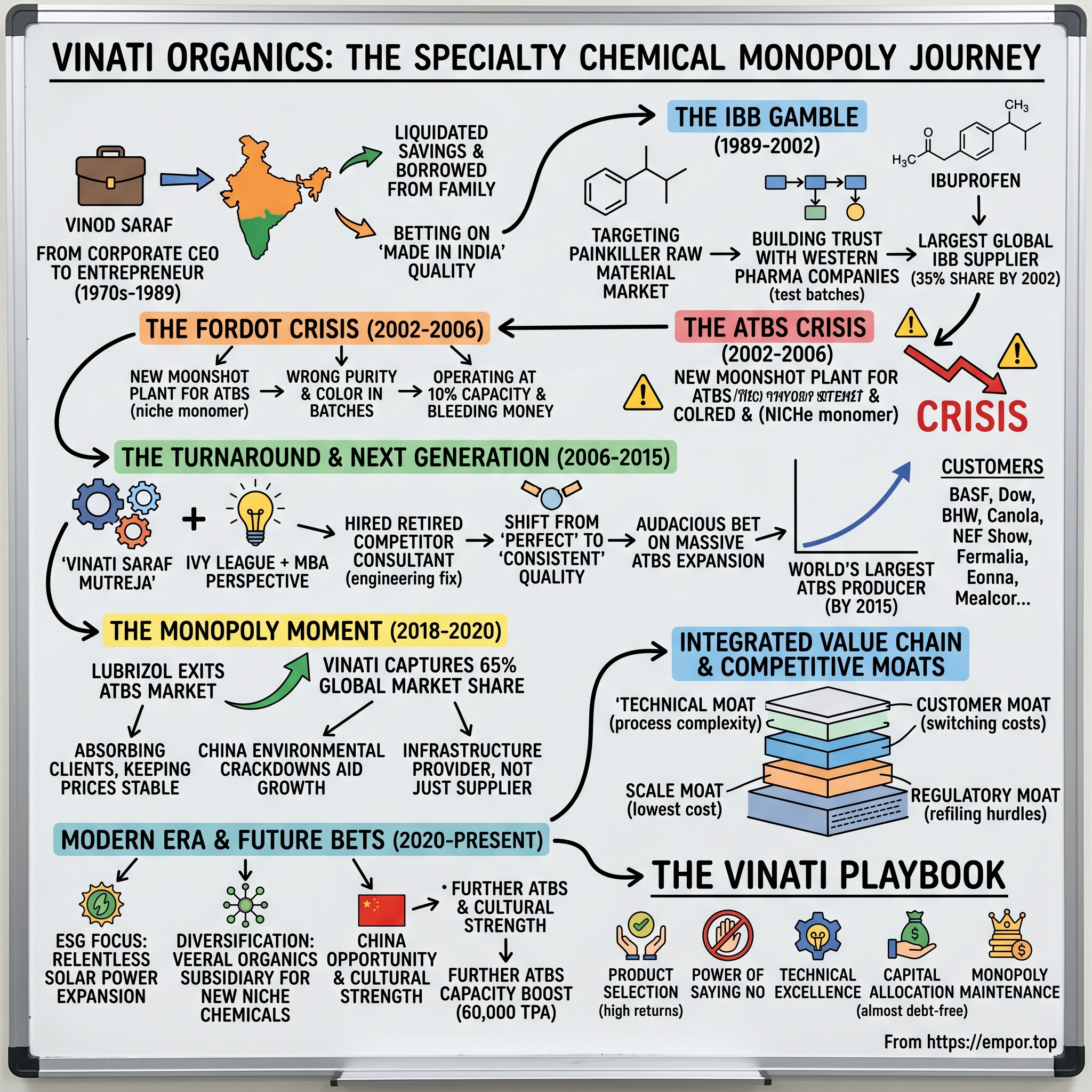

II. The Founder's Journey: From CEO to Entrepreneur (1970s-1989)

The dusty streets of Rajasthan in the 1950s seem an unlikely birthplace for a global chemical empire. Vinod Saraf grew up in a modest business family—his father ran a small trading operation, the kind where every rupee was counted twice and business lessons came not from Harvard case studies but from watching cash flow struggles firsthand.

Young Vinod's trajectory seemed destined for the predictable arc of middle-class Indian ambition: good grades, engineering degree, safe corporate job. And for two decades, that's exactly what happened. He joined the Aditya Birla Group, one of India's most prestigious conglomerates, climbing steadily through the ranks at Grasim Industries, Modern Syntex, and the Bhilwara Group. By his early 40s, he'd reached the summit—Managing Director of Mangalore Refinery and Petrochemicals Limited.

This is where most stories would end. Corner office, driver, company flat, kids in good schools. The Indian corporate dream realized.

But something gnawed at Vinod. During his Birla years, he'd noticed something peculiar about India's chemical industry. While everyone chased volume in commodity chemicals—competing on razor-thin margins, fighting Chinese imports—nobody wanted to touch the complex, specialized molecules that required deep technical expertise. These weren't sexy products. Isobutyl benzene (IBB) doesn't exactly roll off the tongue at cocktail parties.

The decision to leave came in 1989, at age 42—precisely when prudent men double down on job security. His colleagues thought he'd lost his mind. Why leave the Birla empire at the peak of your career? His extended family worried. Friends questioned his judgment.

The financial gymnastics that followed would make any startup founder wince. Vinod liquidated everything—his entire life savings of ₹57 lakhs. When that wasn't enough for the ₹14 crore project he envisioned, he turned to the Indian middle-class entrepreneur's bank of last resort: friends and family. Borrowed from his brother. Mortgaged assets. Convinced skeptical relatives that making an obscure chemical called IBB—the primary raw material for Ibuprofen—was worth betting their savings on.

The first plant would be just 1,200 tonnes per annum. For context, that's roughly what a mid-sized Chinese chemical factory produces in a slow month. But Vinod wasn't thinking about volume. He was thinking about something his Birla days had taught him: in chemicals, you can either race to the bottom on price, or you can own a niche so completely that price becomes irrelevant.

Standing in an empty plot in Mahad, Maharashtra, in late 1989, Vinod Saraf wasn't just building a chemical plant. He was betting that Indian manufacturing could compete not on cost, but on quality and reliability in markets where trust mattered more than price. It was a contrarian bet in an India still emerging from the License Raj, where "Made in India" was more apology than advertisement.

The machinery was secondhand, bought from European plants upgrading their equipment. The technology was licensed, not developed. The customers were theoretical—American pharmaceutical companies who'd never heard of Vinati Organics and had no reason to trust an unknown Indian supplier with a critical raw material.

But Vinod had one advantage his corporate peers lacked: the hunger of a man who'd burned every bridge, liquidated every safety net, and had nowhere to go but forward. In the Birla Group, failure meant a bad appraisal. At Vinati Organics, failure meant personal bankruptcy and the humiliation of returning, hat in hand, to the corporate world he'd rejected.

III. The IBB Gamble: Building India's First Ibuprofen Supply Chain (1989-2002)

The year 1991 marked two inflection points for India: economic liberalization unleashed by Manmohan Singh's reforms, and a small chemical plant in Mahad, Maharashtra, producing its first batch of Isobutyl Benzene. One would reshape a nation; the other would quietly revolutionize a global supply chain.

Vinod Saraf's choice of IBB wasn't random. During his Birla days, he'd observed a curious market dynamic: Ibuprofen was becoming the world's painkiller of choice, yet its key raw material, IBB, was controlled by a handful of Western suppliers who treated it as an afterthought—a side business to their main petrochemical operations. The entire global Ibuprofen industry, worth billions, depended on a chemical that nobody wanted to specialize in.

The first reality check came quickly. American pharmaceutical companies—the biggest Ibuprofen producers—wouldn't even return his calls. Why would Pfizer or Johnson & Johnson risk their supply chain on an unknown Indian company? The Made in India stigma was real. Quality concerns were paramount. And frankly, why fix what wasn't broken? Their existing suppliers were expensive but reliable.

What followed was a grinding, humbling education in trust-building that MBA programs don't teach. Vinod became a frequent flyer to New Jersey and North Carolina, camping out in corporate lobbies, begging for 15-minute meetings with procurement managers. His pitch was simple: "Give me your smallest order. Your test batch. The one you don't care about."

The breakthrough came from an unexpected source—a mid-sized American generic drug manufacturer facing a supply crunch. Their regular supplier had allocation issues, and they needed 50 tonnes of IBB urgently. It was a small order, almost insulting for a plant built to produce 1,200 tonnes annually. Vinod took it.

That first shipment in 1992 became company lore. Vinod personally supervised the loading, flew to America to be there when it arrived, and stood in the customer's quality lab as they tested every parameter. When the results came back—purity levels actually exceeding their usual supplier—the purchasing manager's surprise was visible. "You're 15% cheaper and higher quality. What's the catch?"

There was no catch, just economic logic his competitors had missed. Western IBB producers made it as a byproduct of larger petrochemical operations, treating it as a distraction. For Vinati, IBB was the main event. Every process optimization, every quality improvement, every cost reduction focused on this single molecule. It's the difference between a restaurant that happens to serve coffee and a specialty roaster—obsession breeds excellence.

By 1995, Vinati was supplying 500 tonnes annually to American customers. By 1998, 1,000 tonnes. The growth came not from aggressive sales but from a phenomenon common in specialized B2B chemicals: once you're validated and approved, switching costs become prohibitive. Each customer required 18-24 months of testing, validation, and regulatory approval to switch suppliers. Every successful delivery raised the switching barrier higher.

The numbers tell the story: Revenue grew from ₹8 crores in 1992 to ₹44 crores by 2001. But the real victory wasn't financial—it was strategic. By 2002, Vinati Organics had become the largest IBB supplier globally, commanding 35% market share. The boy from Rajasthan had quietly cornered a market that Big Chemical didn't even know was worth cornering.

But success in IBB created a new problem. With essentially one product, Vinati was vulnerable. A technology shift, a patent change, or a major competitor's entry could destroy everything. Vinod needed a second act. He found it in an even more obscure chemical: ATBS (2-Acrylamido-2-methylpropane sulfonic acid). If IBB was niche, ATBS was microscopic—a specialty monomer used in such tiny quantities that global demand was just 30,000 tonnes.

The technology came from National Chemical Laboratory in Pune, India's premier chemical research institution. The opportunity seemed perfect: only two companies worldwide made ATBS—Lubrizol and Toagosei—and both treated it as a minor product line. The market was growing steadily, driven by enhanced oil recovery and water treatment applications.

What could go wrong?

IV. The ATBS Crisis: Near-Death Experience (2002-2006)

The Lote facility in 2002 was Vinod Saraf's moonshot—a gleaming new plant designed to produce ATBS using cutting-edge technology from NCL Pune. The investment was massive for a company of Vinati's size, funded by IBB profits that could have been distributed as dividends or saved for a rainy day. Instead, everything went into ATBS.

The first batch came out wrong. Not catastrophically wrong—just wrong enough that customers wouldn't accept it. The purity was off by 2%. The color was slightly yellow instead of water-white. The molecular weight distribution showed unexpected peaks. In commodity chemicals, these variations might be acceptable. In specialty chemicals serving pharmaceutical and semiconductor industries, they were deal-breakers.

The second batch was worse. Then the third. The technology that worked perfectly in NCL's lab scaled poorly to industrial production. It's a common problem in chemical engineering—what works in a 100-liter reactor fails mysteriously in a 10,000-liter vessel. The physics change. Heat transfer patterns shift. Impurities that were negligible at small scale become catastrophic at large scale.

By 2004, Vinati Organics was bleeding money. The ATBS plant was operating at 10% capacity, producing mostly waste. The numbers were brutal: ₹66 crores in total revenue (mostly from IBB), ₹2 crores in profit, and an ATBS division losing money every month. For context, the company had invested nearly ₹50 crores in the ATBS facility—25 times their annual profit.

The board meetings became tense affairs. Independent directors questioned the ATBS strategy. Bankers worried about loan repayments. Even loyal employees began wondering if the boss had finally overreached. The whispers grew louder: Sell the ATBS plant. Cut losses. Focus on IBB where you're winning.

Vinod's diary from this period, shared years later with a business magazine, reveals the psychological toll: "Meeting with Bank of Baroda—asked for extension on loan terms. Humiliating. They know we're struggling... Consultant from Germany says our process is fundamentally flawed. Starting from scratch means another ₹30 crores... Board meeting tomorrow. Must convince them to hold on."

The crisis deepened in 2005 when their largest IBB customer threatened to diversify suppliers, concerned about Vinati's financial stability. The very success in IBB was now at risk because of the ATBS disaster. It's the entrepreneur's nightmare: your moonshot threatening to destroy your core business.

By early 2006, Vinod was seriously considering two options: shutting down the ATBS unit and writing off the entire investment, or finding a buyer for the distressed asset. Potential acquirers were already circling—one Chinese company offered to buy the plant for ₹15 crores, less than a third of what Vinati had invested.

The Hollywood version would have Vinod experiencing a eureka moment, solving the problem through sheer brilliance. The reality was more prosaic and more profound. His daughter Vinati had just returned from America—University of Pennsylvania for chemistry, then Purdue for chemical engineering, finally Kellogg for her MBA. She walked into a company in crisis, her father's life work hanging by a thread.

What happened next would transform not just ATBS production, but the entire trajectory of Vinati Organics.

V. The Turnaround: Enter the Next Generation (2006-2015)

Vinati Saraf Mutreja arrived at her father's company in 2006 with credentials that sparkled—Ivy League education, chemical engineering expertise, fresh MBA—but she walked into a disaster. The ATBS plant was hemorrhaging money. Morale was shattered. Her father, the man who'd conquered IBB, looked defeated.

Her first week was spent not in the boardroom but on the production floor, testing samples, reviewing process parameters, talking to operators who'd been running failed batches for four years. What she discovered was both simple and profound: they were trying to force NCL's academic process into an industrial framework without adapting to commercial realities.

"The chemistry was right," she would later explain, "but the engineering was wrong."

Her solution was counterintuitive, almost insulting to Indian pride: hire a retired Lubrizol executive as a consultant. Lubrizol, their main competitor in ATBS, the company they were trying to beat. The board was incredulous. Why would a Lubrizol veteran help them? Wouldn't this be industrial espionage in reverse?

But Vinati had done her homework. The consultant, whose name remains confidential to this day, had retired after 30 years at Lubrizol, working specifically on ATBS production. He had no non-compete obligations, no loyalty bonus to protect. He was 68, living in Ohio, and frankly, bored. The offer of six months in India, helping solve a chemical puzzle, appealed to his engineering pride more than retirement golf.

The consultant's first observation cut deep: "You're trying to make pharmaceutical-grade purity for industrial applications. Your customers don't need 99.9% purity—they need 98% consistently. You're over-engineering and under-delivering."

The fix required completely reimagining the process. Instead of pursuing maximum purity in a single step, they broke it into stages. Instead of exotic catalysts from Europe, they found local alternatives that were "good enough." Instead of continuous processing, they moved to batch production that allowed better quality control. Every change went against the original NCL design, but every change worked.

The first acceptable batch came in March 2007. By June, they were producing consistently. By December, they had their first international customer—ironically, a Lubrizol competitor who needed a secondary supplier. The numbers shifted dramatically: 2007 revenue hit ₹95 crores with ₹8 crores profit. 2008: ₹130 crores revenue, ₹18 crores profit. The ATBS plant wasn't just working; it was printing money.

But Vinati's real genius wasn't fixing the technical problems—it was recognizing the market opportunity everyone else missed. While studying global ATBS demand, she noticed something odd: consumption was growing 15% annually, but capacity wasn't expanding. Lubrizol and Toagosei seemed content with their existing plants. No new entrants were emerging despite attractive margins.

She dug deeper. Enhanced oil recovery, especially in North Sea operations, was driving massive ATBS demand. Shale fracking in America needed ATBS for drilling fluids. Water treatment plants globally were switching to ATBS-based polymers. Yet supply remained tight. Why?

The answer was hidden in corporate strategy documents and industry reports: both Lubrizol and Toagosei viewed ATBS as a mature, slow-growth business. Their capital was allocated to sexier opportunities—electric vehicle lubricants, semiconductor chemicals, renewable energy materials. ATBS was the profitable but boring cousin nobody wanted to dance with.

Vinati convinced her father to make an audacious bet: expand ATBS capacity from 3,000 tonnes to 26,000 tonnes by 2015. It would make Vinati Organics the world's largest ATBS producer, bigger than Lubrizol, bigger than Toagosei. The board was skeptical—why provoke sleeping giants?

"Because," Vinati argued in a board presentation that's now company legend, "they're not sleeping—they're divesting. Look at their capital allocation. Look at their investor presentations. ATBS is never mentioned. We're not competing for their attention; we're below their attention."

The expansion proceeded in phases, each funded by the previous phase's cash flow. No dramatic debt binges, no dilutive equity raises. Just patient, compound growth. By 2012, they hit 15,000 tonnes capacity. By 2015, 26,000 tonnes. Each expansion came with cost reductions—scale economies that their competitors couldn't match without similar investments they weren't willing to make.

The customer acquisition strategy was surgical. Instead of competing on price, Vinati emphasized security of supply. "We're not the cheapest," their sales pitch went, "but we're the only supplier for whom ATBS is the main business. When there's a shortage, who gets priority—Lubrizol's thousand products or our two?"

The client roster that emerged reads like a who's who of global chemicals: BASF, Dow, Akzo Nobel, SNF, Nalco, Chemtall, Clariant. These weren't small purchase orders. These were multi-year contracts with volume commitments, the kind that let you sleep soundly knowing next quarter's revenue is locked in.

By 2015, the transformation was complete. Revenue touched ₹612 crores. Profit hit ₹89 crores. The ATBS division that almost killed the company was now contributing 40% of revenue at margins that made IBB look pedestrian. The failing plant that Vinod almost sold for ₹15 crores was generating that much profit every quarter.

But the real victory was organizational. The father-daughter dynamic that could have been fraught with tension—tradition versus modernity, experience versus education—became a competitive advantage. Vinod handled government relations and financial management. Vinati drove technology and customer relationships. They disagreed often but decided quickly. No bureaucracy, no politics, just two aligned owners making decisions in hours that would take competitors months.

In 2018, recognizing the generational transition was complete, Vinod stepped back and Vinati became Managing Director. She was 38, leading a company with global monopolistic positions in two critical chemicals. The announcement was understated, buried in a regulatory filing. But in the specialized world of chemical manufacturing, everyone noticed.

Because something else was about to happen that would transform Vinati Organics from a successful niche player into a global monopoly: Lubrizol was about to exit ATBS entirely.

VI. The Monopoly Moment: Lubrizol's Exit & Market Domination (2018-2020)

The December 2018 announcement was buried in a technical trade publication, the kind chemical purchasing managers read over morning coffee. Lubrizol, the American specialty chemical giant, was exiting ATBS production entirely, immediately increasing Vinati's market share from 40% to 65%.

For Vinati Saraf Mutreja, sitting in her Mahad office reviewing the news, it was the culmination of a decade-long bet. She'd predicted this moment back in 2010, telling her father that Lubrizol would eventually abandon ATBS. Not because it wasn't profitable—ATBS margins were excellent—but because it wasn't strategic to Lubrizol's future.

The signs had been visible for years if you knew where to look. Lubrizol's investor presentations never mentioned ATBS. Their R&D budget allocation showed zero spending on ATBS process improvements. Their recent acquisitions focused on electric vehicle lubricants and bio-based chemicals. ATBS was generating cash but receiving no love—the corporate equivalent of a forgotten savings account.

Following Lubrizol's decision to stop production of ATBS, Vinati Organics became the largest producer of ATBS in the world. But becoming the largest wasn't the same as becoming dominant. That required a more delicate dance.

The immediate challenge was absorbing Lubrizol's customers without triggering antitrust concerns or pricing backlash. Vinati's approach was counterintuitive: instead of raising prices to capture monopoly rents, they kept pricing stable, even offering long-term contracts at locked rates. The message to customers was clear: "We're not Lubrizol. We won't abandon you when something shinier comes along."

The customer acquisition happened in waves. First came the panicked buyers who needed immediate supply—enhanced oil recovery operations can't simply pause while sourcing new vendors. Then came the strategic purchasers, the BASFs and Dows of the world, who recognized that having a single dominant supplier was risky but having no supplier was catastrophic.

Vinati expanded ATBS capacity from 26,000 TPA to 40,000 TPA, funded entirely from internal accruals. No debt, no equity dilution. The expansion wasn't just about volume—it was about creating spare capacity that would discourage new entrants. Why would anyone invest hundreds of crores to enter a market where the incumbent had 40% unutilized capacity and could crush prices if threatened?

The financial impact was staggering. Revenue jumped to ₹253 crores, rising 57% year-over-year, with profit after tax doubling to ₹65 crores. EBITDA hit ₹95 crores, rising more than 100% year-over-year. These weren't software margins built on code and hope—these were industrial margins built on reactors and chemistry.

But the real transformation was strategic. With 65% global market share in both ATBS and IBB, Vinati wasn't just a supplier—it was infrastructure. When Dow Chemical needs ATBS for their acrylic acid production, when BASF requires IBB for their pharmaceutical intermediates, they call Vinati. Not because Vinati is cheapest, but because Vinati is inevitable.

The China factor amplified everything. In 2018, environmental crackdowns in China shuttered dozens of chemical plants, including several attempting to produce ATBS. The Chinese government's blue-sky initiative, aimed at reducing pollution before major political events, inadvertently handed Vinati a gift: their most likely future competitors were being regulated out of existence.

By 2019, Vinati crossed two psychological milestones: $160 million in revenue and $1 billion in market capitalization. The company that Vinod almost sold for ₹15 crores in 2006 was now worth over ₹10,000 crores. The ATBS plant that nearly bankrupted them was generating more cash than they could deploy.

The board meetings from this period, according to attendees, had an almost surreal quality. Independent directors who'd counseled caution during the expansion were now asking why they weren't expanding faster. Bankers who'd been reluctant to lend were now pitching unnecessary credit facilities. The government of Maharashtra, which had barely noticed Vinati's existence, suddenly wanted to feature them in investment promotion materials.

Vinati Saraf Mutreja's response was characteristically understated. In a rare media interview, when asked about becoming a monopoly, she replied: "We don't think of ourselves as a monopoly. We think of ourselves as the only company that cares enough about these molecules to do them properly."

VII. The Business Model: Integrated Value Chain & Competitive Moats

To understand Vinati's dominance, you must first understand the economics of specialty chemicals—a business where being second-best means being worthless.

The selection criteria Vinod Saraf established in 1989 remains unchanged, almost religious in its adherence: produce only niche chemical products with target of 15-20% return on investment and payback period of up to 5 years. The process must be clean and green, with potential to convert residual waste into other products. It sounds simple. It's not.

Consider what this means in practice. When evaluating a new molecule, Vinati doesn't ask "Can we make this?" They ask: "Can we be the lowest-cost producer globally within five years?" If the answer is no, they walk away. No ego investments, no strategic diversifications, no chasing hot trends. Just cold, disciplined capital allocation.

The manufacturing philosophy is equally stark: Advanced technology, economies of scale, and environmental friendly processes, have helped the Company to be a key manufacturer in speciality chemicals space. The Company is very strong in terms of process innovation, where it has established a process which is greener as well as cheaper.

The integrated value chain is where the magic happens. Take IBB production. Most competitors treat it as a standalone process—buy raw materials, produce IBB, sell to pharma companies. Vinati went deeper. They backward-integrated into Isobutylene production, one of the key raw materials. They forward-integrated into butyl phenol derivatives. Every integration reduced costs, improved quality control, and raised switching barriers for customers.

The numbers validate the strategy. Company is almost debt free despite massive capacity expansions. Over the last decade, Vinati has delivered an average Return on Capital Employed (ROCE) of 33%—not Silicon Valley software margins, but for a capital-intensive chemical business, it's spectacular.

The competitive moats are layered like a Russian doll, each protecting the next:

Technical Moat: CARE Ratings believes that VOL's competitive advantage in both its product segments is expected to sustain in the medium term, as the manufacturing processes are not easy to replicate, and the same acts as an entry barrier for new entrants. This isn't just about having the recipe—it's about years of process optimization, understanding how temperature variations of 0.5°C affect yield, knowing which impurities matter and which don't.

Scale Moat: Being the lowest-cost producer creates a vicious cycle for competitors. Vinati can price just below new entrant breakeven while still earning 30% EBITDA margins. Why would anyone invest ₹200 crores to enter a market where the incumbent can destroy your economics at will?

Customer Moat: Since our inception in 1989, we have evolved from being a single product manufacturer to an integrated business, offering a wide range of products to some of the largest industrial and chemical companies across US, Europe and Asia. Once BASF or Dow validates Vinati as a supplier—a process taking 18-24 months—switching becomes institutionally impossible. The procurement manager who suggests changing suppliers bears career risk if anything goes wrong.

Regulatory Moat: Every customer's FDA filing, every environmental permit, every safety certification lists Vinati's products and processes. Changing suppliers means refiling, retesting, recertifying. In pharma applications, this can take three years and millions of dollars.

The capital allocation framework is textbook Buffett: minimize dilution, avoid debt, reinvest at high returns. Every expansion funded from internal accruals. No glamorous acquisitions. No unrelated diversifications. Just patient compound growth in molecules nobody else wants to perfect.

The export strategy amplifies everything: We export our products to more than 35 countries and our customers are present across the US, South America, Europe and Asia. By serving global markets from India's cost base, Vinati captures developed market pricing with emerging market costs. It's regulatory arbitrage, labor arbitrage, and currency arbitrage rolled into one.

But perhaps the most underappreciated moat is cultural. In a family-run business where the founders still walk the plant floor, where the MD knows every customer personally, where a quality complaint reaches the top within hours—speed and accountability become competitive advantages. While competitors form committees to study market opportunities, Vinati has already built the plant.

The recent recognition tells the story: The Gold Rating now places Vinati Organics in the top 5% of more than 100,000 companies evaluated globally! This recognition underscores our commitment to sustainability and ethical business practices. In an industry often associated with pollution and corner-cutting, Vinati's environmental credentials become another differentiator.

VIII. Modern Era: ESG, Expansion & Future Bets (2020-Present)

The sprawling solar panels that now cover Vinati's facilities catch the Maharashtra sun at an angle that would make any ESG investor smile. But this isn't greenwashing—it's hard-nosed economics dressed in environmental virtue.

In 2021-22, the Company commissioned 14MW solar power plant. Similarly, Solar Power Plant of 6.5 MW at Solapur also commissioned. The timing wasn't accidental. Global chemical customers, particularly European ones, were demanding carbon footprint reductions from suppliers. Vinati could have bought carbon credits or issued sustainability reports. Instead, they built power plants.

The expansion continued relentlessly. The Board has approved an additional 7.5 MW Solar Power with a CAPEX of Rs 35 crore and is expected to be commissioned by March 2022. By 2023, they'd added another layer: 7MW plant at Solapur Karajagi and 7.5MW plant at Osmanabad Tuljapur. Total solar capacity: over 35MW, making them largely self-sufficient in daytime power needs.

But solar panels don't capture the real transformation happening inside Vinati's boardroom. The company that built its fortune on two molecules was finally, carefully, diversifying.

During FY20-21, Veeral Organics Pvt. Ltd. was incorporated as 100% subsidiary of Vinati Organics Limited on October 5, 2020. This wasn't just another subsidiary—it was Vinati's answer to the succession question every family business faces: what happens when the third generation arrives?

The Veeral Organics strategy was elegant: The company has formed VOPL, a 100% owned subsidiary, for manufacturing niche speciality chemicals. VOPL is undertaking a CAPEX of approx. Rs 250 crores. This CAPEX comprises 5 new products. Keep the core business pristine, experiment in the subsidiary. If new products fail, the parent remains untouched. If they succeed, integrate them into the main operations.

The product selection followed the same ruthless criteria established in 1989: niche molecules, limited global competition, essential applications. No commodity chemicals, no me-too products, no riding market trends. Just patient identification of molecules where Vinati could become indispensable.

The ATBS expansion announcement in 2023 sent a clear message to any potential competitors: don't even try. Expanding capacity from 40,000 TPA to 60,000 TPA when you already control 65% of the global market isn't about meeting demand—it's about creating a barrier so high that entry becomes economically irrational.

The China opportunity crystallized everything. It is among the few companies that have been able to deal with the cost advantage of Chinese counterparts over the past few years. While others complained about Chinese competition, Vinati recognized that China's environmental crackdowns were creating a once-in-a-generation opportunity. Chinese plants shut down for pollution violations don't restart quickly. Environmental compliance in China had gone from joke to existential threat for chemical manufacturers.

The financial performance reflected this strategic positioning. Revenue: 2,248 Cr · Profit: 415 Cr in recent years, with Net profit of Vinati Organics rose 25.05% to Rs 101.19 crore in the quarter ended June 2022. Sales rose 31.05% to Rs 506.32 crore in the quarter ended June 2022.

The 2023 milestone was particularly sweet: Consolidated revenue hit ₹2,157.13 crore, up 28.67% year-over-year. PAT stood at ₹458 crore. EBITDA surged 37% to ₹595 crore. For context, the entire company was worth less than ₹600 crore in 2010. Now they generated that in EBITDA alone.

But perhaps the most telling indicator of Vinati's evolution was what they didn't do. No flashy acquisitions despite having cash. No entry into electric vehicle chemicals despite the hype. No blockchain initiatives or AI announcements. Just steady, patient expansion in molecules that matter.

The recognition came from unexpected quarters. Ms. Vinati Saraf Mutreja was conferred upon "Business Leader of the Year" award by the Economic Times in the ETPrime Women Leadership Awards 2023. The Economic Times announced 19 winners across 15 award categories selected from 76 profiles shortlisted from a record-breaking number of over 5,000 applications.

The irony wasn't lost on industry observers. A company making obscure chemicals in Maharashtra was winning more accolades than flashy tech startups. But that's the thing about industrial monopolies—they don't need press releases when customers have no alternatives.

IX. Playbook: Building a Chemical Monopoly

The Vinati Organics playbook reads like a contrarian manifesto in an industry obsessed with scale and diversification. While chemical conglomerates chase hundreds of products, Vinati obsesses over two. While competitors pursue volume, Vinati pursues pricing power. While others fear concentration risk, Vinati sees focus as a feature, not a bug.

Rule 1: Product Selection as Destiny

The strict criteria—minimum 20% return on investment, 5-year payback maximum—sounds simple until you realize what it means in practice. It means walking away from 99% of opportunities. It means watching competitors chase hot markets while you perfect a molecule nobody's heard of. It means explaining to investors why you're not entering high-growth segments that everyone else is pursuing.

The discipline extends to the selection process itself. Every potential product undergoes a three-stage filter: Is there a technical moat we can build? Will customers face high switching costs? Can we become the lowest-cost producer globally? If any answer is no, they walk away. No exceptions, no "strategic" investments, no betting on potential.

Rule 2: The Power of Saying No

Over the last decade, VOL has delivered an average ROCE of 33%—not because they're geniuses at everything, but because they only do things where they can be geniuses. They've turned down opportunities in lithium-ion battery chemicals (too commoditized), agricultural chemicals (too regulated), and pharmaceutical APIs (too competitive). Each rejection was painful. Each looks brilliant in hindsight.

The cost discipline is religious. Manufacturing processes are not easy to replicate, and the same acts as an entry barrier for new entrants. But this isn't about having secret formulas—it's about thousands of micro-optimizations that compound over decades. The temperature profile that saves 2% on energy costs. The catalyst regeneration process that extends life by 20%. The waste recovery system that turns disposal costs into revenue. None revolutionary individually, transformative collectively.

Rule 3: Customer Concentration as Competitive Advantage

Conventional wisdom says customer concentration is dangerous. Vinati flips this: when you have 65% market share and your top ten customers represent 60% of revenue, you're not dependent on them—they're dependent on you. The relationship dynamics invert. You're not a vendor; you're infrastructure.

The customer management philosophy is subtle. Never squeeze on price when you have leverage—that triggers strategic reviews and alternative sourcing initiatives. Instead, be boringly reliable. Answer technical queries in hours, not days. Fly to customer sites for minor issues. Make yourself so embedded in their operations that replacing you becomes unthinkable.

Rule 4: Capital Allocation as Religion

Company is almost debt free. This isn't luck or conservatism—it's strategy. Debt creates pressure for growth, and pressure for growth leads to bad decisions. By funding expansion from cash flow, Vinati maintains the luxury of patience. They can wait five years for a product to mature. They can weather downturns without restructuring. They can say no to bad deals.

The dividend policy—maintaining a healthy payout of 19.4%—seems generous for a growth company. But it serves a purpose: it forces discipline. If you must pay dividends, you can't waste cash on vanity projects. Every rupee of capital expenditure must compete with the alternative of returning cash to shareholders.

Rule 5: Technical Excellence as Table Stakes

In specialty chemicals, being 98% pure when customers need 99% means being 0% valuable. Vinati learned this painfully with ATBS, then built an organization where quality isn't a department but a theology. Every operator knows that a single bad batch can destroy customer relationships built over decades.

The R&D philosophy is revealing: they don't try to invent new molecules—that's for pharma companies with billion-dollar budgets. Instead, they perfect manufacturing processes for known molecules. Less glamorous, more profitable. Why discover a new compound when you can become the best in the world at making an existing one?

Rule 6: Succession as Strategy

The father-daughter transition at Vinati wasn't just smooth—it was synergistic. Vinod brought relationships and experience. Vinati brought technical expertise and global exposure. Neither tried to be the other. Both recognized their complementary strengths.

This extends throughout the organization. The average tenure of senior management exceeds 15 years. The head of production started as a junior engineer. The CFO joined as an accountant. This isn't sentimentality—it's institutional knowledge preservation. In a business where small process improvements compound over decades, employee retention becomes competitive advantage.

Rule 7: Monopoly Maintenance

Having 65% market share isn't the end—it's the beginning of a different game. Now you must discourage entry without triggering antitrust scrutiny. Price just below the point where new investment becomes attractive. Maintain excess capacity that signals you can flood the market if threatened. Be helpful to potential competitors in other products so they don't target yours.

The environmental and sustainability investments serve double duty. Yes, they reduce costs and please ESG investors. But they also raise the bar for new entrants. Matching Vinati's carbon footprint requires solar installations. Meeting their safety standards requires investment. Competing on sustainability requires years of track record. Each improvement widens the moat.

The Meta-Lesson

The Vinati playbook ultimately isn't about chemicals—it's about the power of focus in an age of distraction. While everyone else chases the new new thing, Vinati perfects the old old thing. While competitors diversify to reduce risk, Vinati concentrates to increase returns. While others fear obsolescence, Vinati knows that boring industrial processes that work don't become obsolete—they become infrastructure.

The irony is perfect: in trying to avoid risk through diversification, most chemical companies increase risk through complexity. In accepting concentration risk, Vinati achieves the ultimate diversification—customers who can't leave, competitors who won't enter, and margins that won't compress.

X. Bear vs. Bull Case & Valuation Analysis

The investment case for Vinati Organics presents a fascinating paradox: a company with monopolistic market positions trading at valuations that suggest competitive markets. The debate isn't whether Vinati is a good business—that's obvious. It's whether the market has already priced in every molecule of future success.

The Bear Case: Priced for Perfection

The most glaring concern jumps off the valuation metrics. At current prices around ₹1,644, Vinati trades at a P/E multiple exceeding 40x—steep for a chemical company, even one with monopolistic positions. The bears argue the market has already priced in perfect execution for the next decade. Any stumble—a quality issue, a plant accident, a key customer loss—could trigger a violent derating.

Customer concentration remains the sword of Damocles. Despite the theoretical switching costs, the reality is that Vinati's top ten customers represent over 60% of revenue. If BASF or Dow decided to backward integrate, or if a Chinese competitor achieved quality parity, the revenue impact would be immediate and severe. The company's own success in displacing established suppliers proves that moats in specialty chemicals aren't impregnable.

The product concentration risk is equally stark. ATBS contributes 40-50% of revenue, IBB another 20-30%. That's 70-80% of revenue from two molecules. One technological disruption—a new synthetic pathway, a bio-based alternative, a customer reformulation—could obsolete decades of optimization. Remember, Kodak also had 90% market share once.

China looms as the perpetual threat. Yes, environmental regulations have shuttered many Chinese plants. But China doesn't stay down. They're building new, compliant facilities in chemical parks with state-of-the-art pollution controls. When (not if) Chinese manufacturers achieve Western quality standards in ATBS and IBB, pricing power evaporates overnight.

The management key person risk can't be ignored. Vinati Saraf Mutreja is exceptional, but she's one person. The deep customer relationships, the technical knowledge, the strategic vision—much of it resides in a single individual. Public companies shouldn't trade at premiums based on individual brilliance.

Growth constraints are mathematical. When you already have 65% market share, where does growth come from? The global ATBS market grows at 8-10% annually. Even if Vinati captures all incremental growth, that's hardly the expansion multiple that justifies current valuations. The law of large numbers isn't negotiable.

The Bull Case: Monopoly Rents Are Just Beginning

The bulls counter with a different narrative: Vinati isn't expensive; it's misunderstood. This isn't a chemical company; it's a toll collector on critical industrial infrastructure. The 65% market share understates the reality—in many applications, Vinati is the only viable supplier.

The balance sheet provides the margin of safety: essentially debt-free with consistent cash generation. This isn't a leveraged bet on commodity chemicals. It's a self-funded compounder with the financial flexibility to weather any storm. In a rising rate environment, debt-free businesses become increasingly valuable.

The import substitution opportunity remains massive. India imports thousands of specialty chemicals that Vinati could manufacture. The company's track record—taking IBB from import to export, conquering ATBS from a standing start—suggests they can repeat the playbook. Each new molecule adds another monopoly to the portfolio.

Management's conservatism is a feature, not a bug. They expect margins to stay at current levels of 30% over the next couple of years—no hockey stick projections, no transformation stories. This understated guidance history means positive surprises are likely. When management sandbags consistently, earnings beats become predictable.

The sustainability tailwind is accelerating. Global supply chains are restructuring around ESG criteria. Vinati's environmental investments, previously seen as costs, become competitive advantages. European customers facing carbon border adjustments need suppliers with clean production. Vinati qualifies; most competitors don't.

The optionality in new products is underappreciated. The Veeral Organics subsidiary is developing five new molecules with the same monopolistic potential as ATBS and IBB. Even if only one succeeds at scale, it could add 50% to current revenues at higher margins. The market assigns zero value to this pipeline.

The Valuation Reality Check

Strip away the narratives and focus on the numbers. Vinati trades at approximately 40x P/E, 25x EV/EBITDA, and 8x Price/Book. For context, global specialty chemical leaders like BASF trade at 15x P/E, Clariant at 20x. The premium is substantial.

But those comparisons miss the point. BASF makes thousands of products; Vinati makes two. Clariant operates in competitive markets; Vinati operates in monopolies. The question isn't whether Vinati deserves a premium—it's how much.

The DCF models tell different stories depending on assumptions. Assume 15% revenue growth and 30% EBITDA margins for five years, then 8% terminal growth, and Vinati is fairly valued. Assume 10% revenue growth and margin compression to 25%, and it's overvalued by 40%. The sensitivity to assumptions is extreme.

The Synthesis View

Perhaps both bears and bulls are right—just on different timeframes. Short-term, Vinati appears overvalued by conventional metrics. Any disappointment could trigger a 30-40% correction. But long-term, owning a piece of industrial infrastructure with 65% global market share and expanding applications might be cheap at any price.

The real question isn't valuation—it's business quality. If Vinati maintains its monopoly positions and successfully launches even two new molecules over the next decade, today's price will look quaint. If competition emerges or demand shifts, today's price will look insane.

For value investors, Vinati presents a dilemma: exceptional business, uncomfortable price. For growth investors, it offers clarity: monopolistic positions in expanding markets. For index investors, it's irrelevant: too small to matter.

The market's judgment is clear: Vinati trades at premium valuations because the market believes monopolies in specialty chemicals are worth premium prices. Whether that belief proves prescient or naive will determine whether buying at current levels is brilliant or foolish.

But here's the thing about monopolies: they tend to last longer than anyone expects. Until they don't.

XI. The Legacy Question: Can Monopolies Last?

The conference room in Mumbai's Bandra-Kurla Complex, where Vinati's board meets, has witnessed a transition that breaks the pattern of Indian family businesses. No feuds, no splits, no professional CEO brought in to mediate. Just a father recognizing his daughter's moment and stepping aside gracefully.

Ms. Vinati Saraf Mutreja was conferred upon "Business Leader of the Year" award by the Economic Times in the ETPrime Women Leadership Awards 2023. The recognition matters less than what it represents: the market's acknowledgment that the second generation hasn't just preserved the business—they've transformed it.

But can the monopoly last? History suggests caution. Dow Chemical once dominated chlorine production. DuPont owned nylon. Eastman Kodak monopolized film. Each seemed invincible until they weren't. The question isn't whether Vinati's monopoly will end—it's whether they'll see it coming.

The challenges are already visible. When you have 65% global market share in your core products, mathematics becomes your enemy. Growing at 15% annually means finding new customers that don't exist or taking the remaining 35% from competitors who'll fight desperately. Neither path is easy.

The next generation problem looms larger. Vinati Saraf Mutreja is exceptional, but will her children be? The third generation in family businesses faces unique challenges—they didn't build it, didn't save it, just inherited it. The hunger that drove Vinod Saraf to mortgage everything, the desperation that pushed Vinati to hire a competitor's consultant—will that DNA survive prosperity?

The company's answer is structural: professional management layers, independent directors with real power, systems that don't depend on individual brilliance. But culture can't be systematized. The willingness to spend four years fixing ATBS quality, the patience to build customer relationships over decades, the discipline to say no to easy opportunities—these are cultural, not structural.

The Expansion Paradox

What happens when you already dominate your market? Vinati faces three choices, each with its own risks:

Option 1: Expand into adjacent molecules. The Veeral Organics subsidiary represents this path—new products, same philosophy. But replicating monopoly success isn't formulaic. For every ATBS, there might be ten failures. The capital invested in failures could destroy returns from successes.

Option 2: Geographic expansion. Build plants in other countries, closer to customers. But this sacrifices the India cost advantage and introduces political risk. A plant in Europe or America might satisfy customer concerns about supply chain concentration, but at what cost to margins?

Option 3: Forward or backward integration. Make the products that use IBB and ATBS, or make the raw materials that go into them. But this means competing with customers or suppliers—dangerous territory that could trigger retaliation.

The company seems to be choosing Option 1, carefully, slowly. Five new products in development, each following the same selection criteria that identified IBB and ATBS. It's the most conservative choice, also the most likely to preserve the monopoly characteristics that define Vinati.

The Technology Question

Specialty chemicals seem immune to disruption—after all, molecules don't change. But manufacturing processes do. Continuous flow chemistry, AI-optimized reactions, biological synthesis—each could obsolete Vinati's carefully optimized batch processes.

More threatening is substitution. What if enhanced oil recovery—ATBS's biggest application—becomes obsolete as the world shifts to renewables? What if Ibuprofen gets replaced by a better painkiller that doesn't need IBB? The company that lives by niche molecules can die by them too.

Vinati's response has been to diversify applications, not products. ATBS now goes into water treatment, construction chemicals, personal care. IBB derivatives expand into fragrances and antioxidants. Same molecules, different customers. It's elegant but insufficient if the core molecule becomes obsolete.

The ESG Wild Card

The chemical industry sits at the intersection of essential and evil in public perception. Essential because modern life requires chemicals. Evil because of pollution, accidents, health concerns. Vinati has navigated this carefully—solar plants, zero discharge facilities, safety certifications. But public perception can shift suddenly.

What if ATBS gets linked to environmental damage in fracking operations? What if IBB faces health scrutiny? The science might be sound, but public opinion doesn't require scientific rigor. One viral documentary, one activist campaign, one regulatory overreaction could destroy demand overnight.

The Succession Solution

The most intriguing aspect of Vinati's future is how they're solving succession. Not through family alone, not through professional management alone, but through a hybrid that preserves entrepreneurial energy while adding professional discipline.

The creation of Veeral Organics as a subsidiary for new ventures is masterful. It gives the next generation their own platform to build on, their own mistakes to make, their own victories to claim. Success adds to the parent; failure doesn't contaminate it.

The systematic building of second-tier management—promoting from within, rotating responsibilities, creating depth—suggests a company preparing for perpetuity, not just the next quarter. When your competitive advantage is institutional knowledge, employee retention becomes succession planning.

The Ultimate Question

Can Vinati's monopoly last another decade? The honest answer is: probably, but with caveats. The switching costs, technical barriers, and customer relationships create enormous inertia. Customers won't change suppliers for 10% price differences when the chemical represents 0.1% of their costs but could shut down production if contaminated.

But monopolies require vigilance. The moment Vinati becomes complacent—delays a capacity expansion, ignores a quality complaint, takes a customer for granted—competitors pounce. The paranoia that built the monopoly must persist to maintain it.

The deeper question is whether monopoly is even the right goal. Perhaps the next decade's challenge isn't maintaining 65% market share but finding the next ATBS and IBB. Not protecting the castle but building new ones.

For investors, the legacy question translates simply: Is Vinati a dynasty in the making or a empire at its peak? The answer won't be clear for years. But in specialty chemicals, where product lifecycles span decades and customer relationships span generations, betting on continuity has historically beaten betting on disruption.

The Saraf family built a monopoly from nothing. Whether they can maintain it through prosperity will determine if Vinati Organics becomes a case study in building wealth or preserving it. The difference, in the end, might matter more than the monopoly itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube