Vikram Solar: India's Solar Manufacturing Champion

I. Introduction & Episode Roadmap

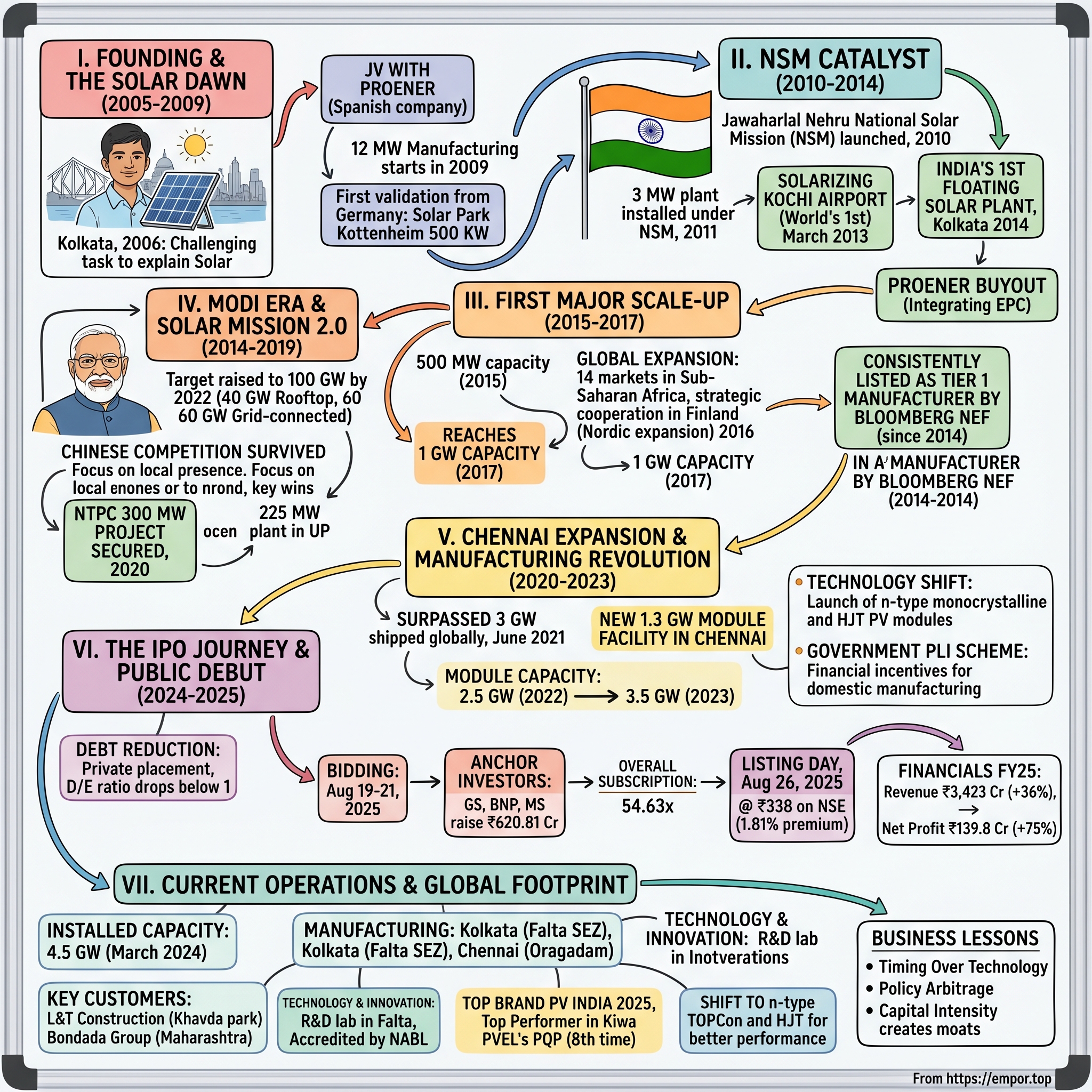

Picture the dusty industrial outskirts of Kolkata in 2006—a city better known for jute mills and colonial-era trading houses than cutting-edge renewable technology. Here, in this unlikely setting, Gyanesh Chaudhary started Vikram Solar as a solar module manufacturing unit, at a time when "solar was not understood well at all. I had to explain to people what I did on a day-to-day basis, and show them how energy can be captured from the sun".

The question wasn't just how to build a solar company in India—it was whether India even needed one. Solar panels were curiosities, expensive imported toys for environmental idealists. Yet Chaudhary, armed with a Business Graduate degree from University of Wales, UK, and a Diploma in Marketing and International Trade from University of Boston and in International Business from Harvard Business School, USA, saw something others didn't: the convergence of India's massive energy deficit and the inevitable decline of solar costs.

Fast forward to today: Vikram Solar boasts a 4.5 GW annual production capacity, making it one of the country's largest solar module manufacturers. The company that once struggled to explain what a solar panel was just launched a ₹2,079.37 Cr IPO and got listed on BSE, NSE on August 26, 2025. This is the story of how a family business from Kolkata rode India's solar revolution from obscurity to the public markets—timing government policy shifts perfectly, surviving Chinese competition, and building one of India's solar manufacturing champions.

II. Founding Story & The Solar Dawn (2005-2009)

The Vikram Group had been around since 1974, a traditional Kolkata business house with interests across manufacturing sectors. But when it was his father's vision to start a solar energy development company, young Gyanesh Chaudhary was handed what seemed like an impossible mandate: build a solar business in a country where electricity itself was a luxury for millions.

The first four years were arduous. In those early days, solar was a solution looking for a problem. Germany and Spain were the only markets that mattered—India's solar installations could be counted on your fingers. A JV between Vikram and Spanish company Proener helped Gyanesh learn more about setting up small solar plants. This partnership wasn't just about technology transfer; it was about learning the grammar of an industry that didn't yet exist in India.

The company commenced manufacturing operations in 2009 with an installed solar PV module manufacturing capacity of 12 MW. To put this in perspective, 12 MW was roughly enough to power 2,000 Indian homes—a drop in the ocean of India's energy needs. But Chaudhary wasn't building for the India of 2009; he was building for the India that was about to emerge.

The first validation came from an unexpected place: Germany. In 2009, Vikram Solar supplied, installed and commissioned 1st phase of 500 KW solar power plant at Solar Park Kottenheim, Germany. For a company that couldn't get Indians interested in solar, selling to the world's most sophisticated solar market was both ironic and prescient. The German project wasn't just about revenue—it was about credibility. If Vikram's modules could work in Germany's exacting conditions, they could work anywhere.

What Chaudhary understood, and what would prove crucial in the coming years, was that solar wasn't really about technology. The technology was largely commoditized—silicon wafers, aluminum frames, glass sheets. Solar was about three things: scale, timing, and government policy. And the biggest policy shift in India's energy history was about to begin.

III. The Jawaharlal Nehru National Solar Mission Catalyst (2010-2014)

The NSM was launched as the Jawaharlal Nehru National Solar Mission by Ministry of New and Renewable Energy on January 11 2010. For Vikram Solar, this wasn't just good news—it was existential validation. Having set up a few projects in India, Vikram found itself at the right place at the right time when the national solar mission started picking momentum.

The mission's initial target seemed ambitious at the time: 20 GW by 2022. But even this "modest" goal represented a massive shift in India's energy thinking. The government wasn't just setting targets; it was creating an entire ecosystem—feed-in tariffs, renewable purchase obligations, viability gap funding. Suddenly, solar wasn't alternative energy; it was inevitable energy.

In 2011, 3 MW solar plants were installed under the National Solar Mission of India. Three megawatts might not sound like much, but in the context of 2011 India, it was a statement project. These weren't demonstration plants anymore; they were commercial installations with real power purchase agreements.

The company's engineering capabilities evolved rapidly during this period. In March 2013, Vikram Solar contributed to the solarisation of World's 1st solar airport in Kochi, Kerala. The Kochi airport project was particularly significant—airports are conservative, risk-averse institutions. If they were going solar, it meant the technology had crossed the credibility chasm.

But the real breakthrough came from an unexpected direction: water. In early 2014, the company designed, installed and commissioned India's first floating solar plant in Kolkata. Floating solar solved a uniquely Indian problem—land scarcity. In a country where every acre was contested, putting solar panels on water bodies was brilliant. It also demonstrated something crucial: Vikram wasn't just a module manufacturer; it was becoming a solar solutions company.

The Spanish partnership that had been so crucial in the early days was reaching its natural conclusion. Proener did not go ahead with further investment, so we bought over and integrated their side of the EPC business. This buyout was more than a corporate transaction—it was Vikram's declaration of independence. The student had become the master.

IV. The First Major Scale-Up (2015-2017)

In 2015, Vikram Solar reached a production capacity of 500 MW—a 40-fold increase from its starting capacity just six years earlier. But scale in India meant nothing if you couldn't compete globally. The company needed international validation, and it went hunting for it in the most unlikely places.

In February 2016, Vikram Solar expanded its presence in Sub-Saharan Africa through a partnership with Powertech Africa, entering 14 new markets. Africa might seem like an odd choice for an Indian solar company, but it made perfect sense. African markets faced similar challenges to India—unreliable grids, distributed populations, intense sunshine. What worked in rural Rajasthan could work in rural Kenya.

The Nordic expansion seemed even more counterintuitive. In October 2016, Vikram Solar formed a strategic cooperation to enter the Finnish market. Finland—a country where the sun barely shows up for half the year—buying solar panels from India? Yet this was precisely the point. If Vikram's panels could generate power in Finland's weak sunlight, they could generate power anywhere. Every Finnish installation was a engineering proof point.

In 2017, the company reached a manufacturing capacity of 1 GW. One gigawatt—enough to power a small city. The company was no longer a startup; it was industrial-scale manufacturing. The achievement was marked by another stamp of credibility: The company has been consistently listed as a Tier 1 solar PV module manufacturer by Bloomberg NEF since 2014.

Bloomberg NEF's Tier 1 classification isn't just a ranking—it's the industry's gold standard for bankability. It means international project financiers trust your modules enough to lend against them. For a company from Kolkata competing against Chinese giants and American technology leaders, this was remarkable.

The US expansion began modestly. The company opened a sales office in Massachusetts, USA in February 2018 and an office in Gurgaon in May. The Massachusetts office was strategic—located in the heart of America's cleantech corridor, close to MIT and Harvard, where the next generation of solar technology was being invented. The Gurgaon office served a different purpose—it was the commercial hub for North India's booming solar market.

V. The Modi Era & Solar Mission 2.0 (2014-2019)

Everything changed in 2014 when Narendra Modi became Prime Minister. Modi gave his approval for increasing the national solar mission capacity from the current 22 gigawatt (GW) to 100 GW by 2022, with 40 GW for rooftop solar electricity generation and 60 GW for large and medium-scale grid-connected solar projects.

This wasn't just an incremental increase—it was a complete reimagining of India's energy future. The new target represented a 5x increase from the original mission. Suddenly, India wasn't trying to catch up with global solar leaders; it was trying to become one.

But with great opportunity came great challenges. Solar and project developers in India began importing solar modules from China as the marginally-lower cost made a big difference at scale. Chinese manufacturers, backed by massive state subsidies and economies of scale, could undercut Indian manufacturers by 20-30%. For many Indian solar companies, this was an existential crisis.

Vikram's response was to focus on what Chinese manufacturers couldn't provide: local presence, custom solutions, and reliability. The company's Bloomberg Tier 1 status became crucial—international buyers and Indian financial institutions trusted Vikram's quality even if it cost more.

The scale of projects was exploding. In 2020, the company secured a 300 MW project from National Thermal Power Corporation Limited (NTPC). NTPC—India's largest power generator, traditionally a coal company—was going solar in a big way. When the coal guys start buying solar panels, you know the energy transition is real.

The company commissioned a 225 MW plant for NTPC in Uttar Pradesh, the largest in the state. Uttar Pradesh, India's most populous state with over 200 million people, had been an energy basket case for decades. The fact that its largest solar plant was using Vikram modules was both a technical achievement and a political statement.

VI. The Chennai Expansion & Manufacturing Revolution (2020-2023)

COVID-19 should have been a disaster for a capital-intensive manufacturer. Supply chains collapsed, workers couldn't come to factories, demand evaporated. But crisis, as they say, reveals character. While competitors retreated, Vikram doubled down.

By June 2021, the company surpassed 3 GW in terms of modules shipped globally and became India's largest module manufacturer with up to 2.5 GW capacity and inaugurated a 1.3 GW module manufacturing facility in Chennai. The Chennai facility wasn't just about adding capacity—it was about geographical diversification and access to ports for export markets.

The expansion continued relentlessly. In 2022, Vikram Solar reached 2.5 GW in module production capacity. In 2023, the company increased its module production capacity to 3.5 GW. But capacity was only half the story. The real revolution was in technology.

In 2024, the company launched n-type monocrystalline cell modules and heterojunction (HJT) PV modules. For the uninitiated, the shift from p-type to n-type cells is like the shift from combustion engines to electric motors—same function, fundamentally different approach, dramatically better performance. HJT technology, combining crystalline silicon with thin-film technology, represents the cutting edge of solar cell efficiency.

Government support came through the Production Linked Incentive (PLI) scheme—a game-changer for domestic manufacturing. The scheme provided financial incentives linked to production volumes, finally giving Indian manufacturers a fighting chance against Chinese imports. Vikram Solar's eligibility for the PLI scheme for its 2.4 GW facility was crucial validation of its manufacturing capabilities.

The numbers told the story of transformation. The company's revenue increased from ₹2,511 crore in FY2024 to ₹3,423 crore in FY2025, marking a notable 36% annual rise. But the real achievement was in profitability: net profit grew from ₹79.7 crore to ₹139.8 crore, while the EBITDA margin remained solid at 14.4% in FY2025.

VII. The IPO Journey & Public Market Debut (2024-2025)

The path to the public markets began with a crucial piece of financial engineering. The company had been carrying significant debt from its expansion phase—a debt-to-equity ratio standing at approximately 1.73x as of March 2024. For capital markets, this was a red flag. After a recent ₹700 crore private placement in June 2024, the D/E ratio was expected to drop below 1.

The IPO itself was a precisely orchestrated affair. Vikram Solar IPO bidding started from Aug 19, 2025 and ended on Aug 21, 2025. The pricing was aggressive but not unreasonable: ₹332.00 per share, valuing the company at over ₹12,000 crores.

The anchor book read like a who's who of global finance. Vikram Solar raised ₹620.81 crore from anchor investors including Goldman Sachs, BNP Paribas, and Morgan Stanley. When Goldman Sachs writes a check, it's not just about the money—it's a signal to the market that serious institutional capital believes in the story.

Market response was emphatic: the IPO was subscribed 54.63 times overall. The institutional portion saw extraordinary demand at 142.79 times, while retail investors subscribed 7.65 times their allocated portion. This wasn't just oversubscription—it was validation.

Listing day, August 26, 2025, was anticlimactic in the best way possible. Shares listed at ₹338 on NSE, reflecting a premium of 1.81% against the issue price. No massive pop, no dramatic crash—just a steady, professional debut befitting a company that had spent two decades building real value.

The IPO proceeds had a clear purpose: backward integration. The company planned to invest in an integrated 3,000 MW solar cell and 3,000 MW solar module manufacturing facility. This wasn't just expansion—it was about controlling the entire value chain, reducing dependence on imported cells, and capturing more margin.

VIII. Financial Performance & Business Model Evolution

The financial trajectory tells a story of disciplined execution and strategic pivots. Revenue from operations increased from Rs 2,073.23 crore in FY23 to Rs 2,510.99 crore in FY24 and Rs 3,423.45 crore in FY2025. That's a 65% increase over two years—impressive for any company, remarkable for a manufacturer competing against Chinese dumping.

The profit story was even more dramatic. Revenue increased by 37% and profit after tax rose by 75% between FY24 and FY25. This wasn't just revenue growth—it was margin expansion, the holy grail of manufacturing.

The Q1 FY26 numbers released in September 2025 showed the momentum continuing. Revenue rose by 79.7 percent year-on-year to ₹1,133.6 crore, while PAT for Q1FY26 grew by 483.9% on a Y-o-Y basis and PAT margins stood at 11.7%. When your profit grows 5x year-over-year, you're not just executing—you're transforming.

The business model had evolved significantly from the early days. Initially, the company was primarily a module manufacturer selling to EPC contractors. By FY23, the mix had shifted: 94% of revenue from modules, 6% from EPC and O&M services. This might seem like doubling down on manufacturing, but it was actually about focus—doing one thing exceptionally well rather than many things adequately.

The order book provided visibility into future growth. Order Book: 10.96 GW as of June 30, 2025, with capacity utilisation at 89.2% during the quarter. For context, 10.96 GW is more than twice the company's current capacity—essentially two years of production already sold.

IX. Current Operations & Global Footprint

Today's Vikram Solar is a far cry from the 12 MW startup of 2009. The company has an installed capacity of 4.5 GW, as on March 2024, with manufacturing facilities at Falta SEZ in Kolkata, West Bengal and Oragadam in Chennai, Tamil Nadu.

The customer wins in 2025 demonstrated the company's strong market position. Vikram Solar secured an order from the Bondada Group to supply 250 MW of high-efficiency solar modules for a project in Maharashtra. The company won a 336MW module supply agreement from L&T Construction for the 2.3GW Khavda solar park in Gujarat. When L&T—India's largest engineering conglomerate—chooses your modules for one of the world's largest solar parks, it's the ultimate vote of confidence.

International presence, while reduced from peak levels, remained strategic. The dramatic shift in export mix—from 61% of revenue in FY24 to just 1% in FY25—might seem concerning, but it reflected a deliberate strategic pivot toward the booming domestic market, where government policies provided better margins and payment certainty.

The distribution network had become a competitive advantage: 42+ distributors covering 600 out of 718 districts in India. This wasn't just about sales reach—it was about service. Solar panels need maintenance, warranties need to be honored, and customers need hand-holding. Having boots on the ground in 600 districts meant Vikram could provide what Chinese importers couldn't: presence.

X. Technology & Innovation Strategy

The technology evolution at Vikram Solar mirrors the global solar industry's relentless pursuit of efficiency. From the polycrystalline cells of 2009 (15% efficiency on a good day) to today's HJT modules pushing past 22%, each percentage point of efficiency represents millions in R&D and retooling costs.

The R&D lab in Falta, West Bengal, accredited by NABL, wasn't just a testing facility—it was where the company's future was being invented. Being the first solar company in eastern India to receive NABL accreditation meant Vikram's test results were accepted globally without question.

Recognized as Top Brand PV India 2025 by EUPD Research, achieving "Top Performer 2025" status in Kiwa PVEL's PQP for the eighth time. PVEL's testing is brutal—modules are subjected to conditions far worse than they'll ever face in the field: thermal cycling from -40°C to 85°C, humidity freeze, damp heat, mechanical stress. Surviving this eight times isn't luck—it's engineering excellence.

The shift to n-type TOPCon and HJT technologies represented a major bet on the future. While p-type PERC cells still dominated the market, n-type cells offered better temperature coefficients (they lost less efficiency in heat), better low-light performance, and lower degradation rates. For a company selling into India's scorching climate, this wasn't just a technology upgrade—it was a competitive necessity.

XI. Playbook: Business & Investing Lessons

Timing Over Technology: Vikram's story isn't about breakthrough innovation—solar cell technology is largely commoditized. It's about being ready when the market inflects. The company built capacity before the JNNSM, not after. When the policy window opened, Vikram was ready to sprint through it.

Vertical Integration as Defense, Not Offense: The move into EPC wasn't about capturing more value chain—it was about survival when Chinese modules flooded the market. When you can't compete on product cost, compete on solution cost. The subsequent retreat from EPC shows discipline—knowing when to advance and when to consolidate.

The Policy Arbitrage: Every successful moment in Vikram's history coincided with a policy shift—JNNSM launch, Modi's 100 GW target, PLI scheme, customs duties on imports. This isn't luck; it's strategy. In industries where government is the biggest customer and regulator, policy IS strategy.

Capital Intensity Creates Moats and Chains: The ₹700 crore required to reduce debt, the ₹1,500 crore IPO for new capacity—these aren't just investments, they're barriers to entry. But they're also chains. High fixed costs mean you must run at high utilization or die. The 48% capacity utilization in FY24 shows how dangerous this game can be.

Technology Transitions as Survival Tests: The shift from poly to mono, PERC to TOPCon—each transition requires hundreds of crores in new equipment. Companies that miss a transition become obsolete. Vikram's ability to fund and execute multiple transitions shows financial and operational strength.

XII. Bull vs. Bear Case

The Bull Thesis: India needs 500 GW of renewable capacity by 2030—that's 80 GW per year for the next five years. With 40% customs duty on imported modules and PLI benefits for domestic manufacturing, Indian manufacturers have unprecedented protection and support. Vikram's 10.96 GW order book provides visibility, while backward integration into cells will improve margins. The company's proven ability to scale—from 12 MW to 4.5 GW—suggests it can execute the next phase of growth.

The Bear Thesis: Running at 48% utilization in FY24 despite booming demand suggests operational issues or market share loss. The dramatic drop in exports (61% to 1%) removes a natural hedge against domestic policy changes. Chinese manufacturers won't disappear—they'll set up Indian factories or find ways around tariffs. The shift to n-type technology requires massive capex just to stay competitive, not to get ahead. Trade receivables at ₹1,228 crore represent more than a third of annual revenue—any payment delays could create a working capital crisis.

The Nuanced Reality: Vikram Solar is neither a sure winner nor a likely loser—it's a leveraged bet on India's energy transition. The company has proven it can survive and thrive through multiple cycles. But the next five years will be different—more competition from Adani and Reliance, technology shifts happening faster, Chinese manufacturers getting creative about market access.

The IPO valuation at 70x P/E prices in perfect execution. Any stumble—a technology bet that doesn't pay off, a large customer default, a policy reversal—and the multiple will collapse. But if India's renewable ambitions are even half-realized, today's valuation might look cheap in hindsight.

XIII. Epilogue: The Future of Indian Solar Manufacturing

Vikram Solar's journey from a 12 MW startup to a 4.5 GW public company isn't just a corporate success story—it's a template for India's manufacturing ambitions. The company proved that Indian manufacturers could compete globally, not through labor arbitrage or cost cutting, but through engineering excellence and strategic positioning.

The next chapter is being written in real-time. The US expansion plans, leveraging the Inflation Reduction Act benefits, could open a massive new market. The backward integration into cell manufacturing will test whether Indian companies can compete across the entire value chain, not just final assembly.

Competition is intensifying from unexpected directions. Reliance, with effectively unlimited capital, is building gigascale factories. Adani, with its infrastructure DNA, is creating integrated renewable energy ecosystems. Waaree, Vikram's closest peer, is expanding aggressively. The cozy oligopoly of Indian solar manufacturing is becoming a knife fight.

Yet the opportunity dwarfs the competition. India's energy consumption will double by 2040. Every percentage point of GDP growth requires massive new power generation. And increasingly, that power must be clean. In this context, Vikram Solar isn't just competing for market share—it's building the infrastructure for India's next phase of development.

The company that once struggled to explain what solar panels were is now helping power a nation's transformation. That's not just a business success—it's a civilizational contribution. And in the end, that might be Vikram Solar's greatest achievement: proving that Indian manufacturing can rise to meet Indian ambitions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube