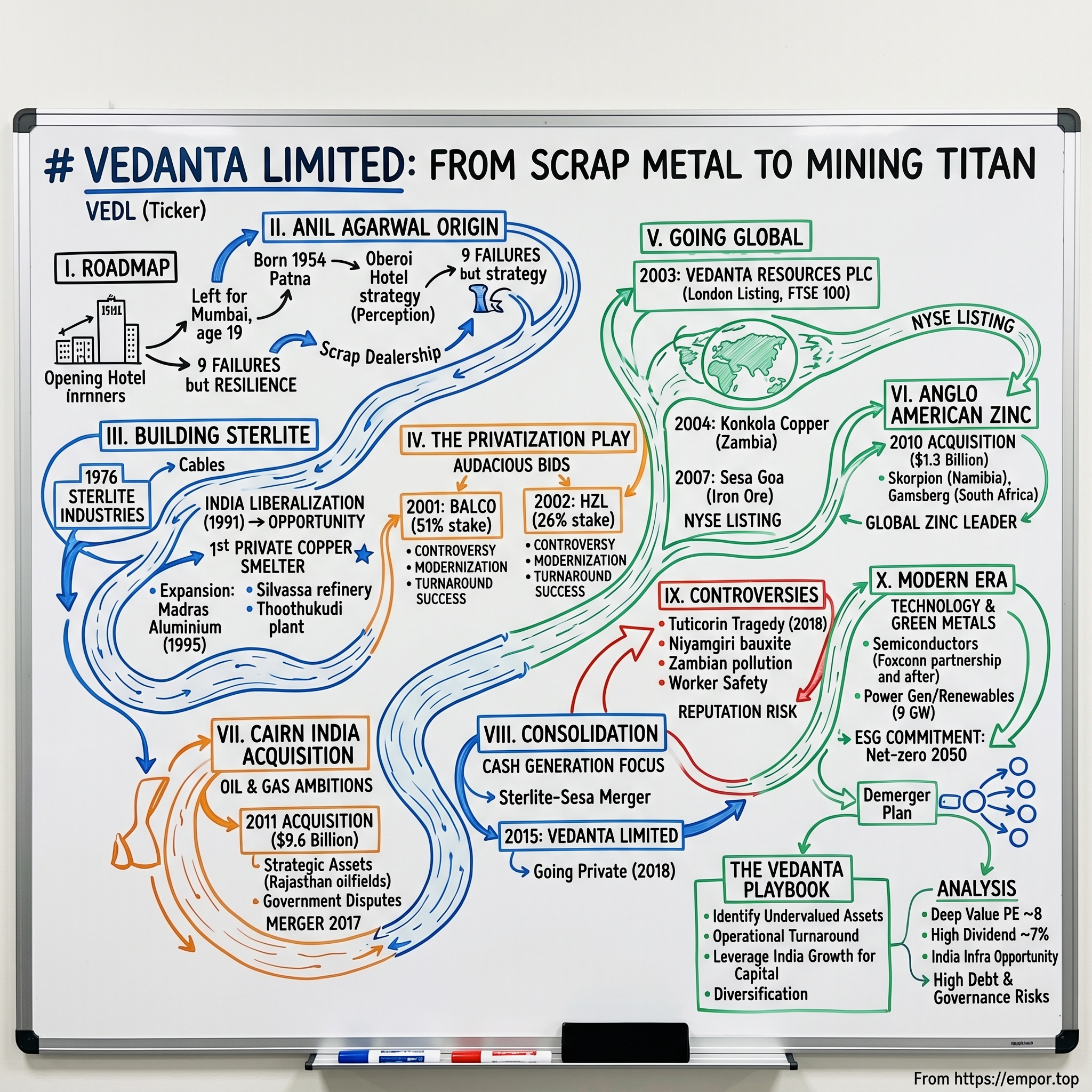

Vedanta Limited: From Scrap Metal to Mining Titan

I. Introduction & Roadmap

The story of Vedanta Limited reads like a Bollywood script written by a business strategist—a young man from Bihar with nothing but ambition transforms a scrap metal trading operation into one of the world's largest natural resources conglomerates. Today, with a market capitalization of ₹1,72,272 Crore on the NSE, Vedanta stands as India's diversified mining titan, straddling zinc, lead, silver, copper, aluminum, iron ore, and oil & gas across multiple continents.

But how does a scrap metal trader with no formal mining background build an empire that rivals century-old mining houses? How does an entrepreneur from Patna end up ringing the bell at the London Stock Exchange, becoming the first Indian company to list there? And perhaps most intriguingly, how does one navigate the treacherous waters of commodity cycles, political upheavals, and environmental controversies while maintaining aggressive growth?

This is the story of Anil Agarwal and Vedanta—a tale of emerging market entrepreneurship at its most audacious. It's about spotting opportunities where others see liabilities, whether in India's moribund public sector units or in Anglo American's non-core assets. It's about timing commodity supercycles, leveraging India's growth story for global capital, and building from the ground up in one of the world's most capital-intensive industries.

The Vedanta playbook isn't just about mining metals; it's about mining opportunities. From the liberalization of India's economy in 1991 to the current infrastructure supercycle, Agarwal has positioned his company at the intersection of India's development needs and global commodity markets. Along the way, he's faced everything from violent protests in Tamil Nadu to ethical disinvestment by the Church of England, yet the empire continues to expand.

What makes Vedanta particularly fascinating for students of business strategy is its counter-intuitive approach to value creation. While Western mining majors were divesting from emerging markets, Agarwal was doubling down. When commodity prices crashed, he was acquiring. When everyone questioned the logic of an Indian company buying African copper mines or Irish zinc operations, he was already planning the next acquisition.

This isn't just another corporate success story—it's a masterclass in contrarian thinking, operational excellence, and the art of turning government liabilities into private profit. As we trace Vedanta's journey from a Bombay trading firm to a global mining powerhouse, we'll uncover the strategies, the controversies, and the sheer audacity that built one of India's most valuable—and most debated—corporate empires.

II. The Anil Agarwal Origin Story

The journey of Anil Agarwal reads like the ultimate emerging market entrepreneurship story—equal parts audacity, timing, and an almost supernatural ability to spot value where others see only rust. Born into a Marwadi family in Patna, Bihar, India, his father Dwarka Prasad Agarwal ran a small aluminum conductor business. This wasn't the privileged background of a Tata or Birla heir—this was lower-middle-class India, where dreams often died before they could take flight.

Born on January 24, 1954, in a lower-middle-class Marwari family in Patna, Agarwal's early years were defined by constraint and aspiration in equal measure. He completed his schooling at Patna's Miller School but never got the opportunity to study in college due to family struggles. At fifteen, he made a decision that would define his trajectory—rather than pursuing higher education, he would join his father's aluminum conductor business, learning the fundamentals of metal trading from the ground up.

But the real story begins at nineteen. "I left Bihar with only a tiffin box, bedding, and dreams in my eyes"—this wasn't just a young man leaving home; this was an exodus from the familiar into the unknown. Mumbai in 1973 wasn't just India's commercial capital; it was a city that could swallow ambitions whole. For a young man from Patna with no connections, no capital, and no formal business education, it was both the promised land and potential graveyard of dreams.

The Oberoi Hotel strategy remains one of the most audacious moves in Indian business folklore. Picture this: a nineteen-year-old from Bihar, with barely any money, deciding to stay at one of Mumbai's most prestigious hotels. At Rs 200 per day—a fortune in 1973—Agarwal managed this feat for three months by sleeping in the hotel but managing food and laundry from outside. Why? Because he understood something fundamental about business that most MBAs never learn: perception is reality. Being seen at the Oberoi meant being taken seriously by the businessmen who frequented its lobbies and restaurants. It was his Harvard Business School, his finishing school, his gateway to understanding how the elite operated.

For the next ten years, he tried his luck with nine different businesses but all of them failed. Think about that—a decade of failure. Most entrepreneurs give up after one or two failed ventures. Agarwal endured nine. Each failure wasn't just a financial setback; it was a masterclass in what didn't work. From trading to small manufacturing ventures, each collapse taught him something crucial about cash flow, market dynamics, and most importantly, timing.

The turning point came in 1976 when he founded what would become Sterlite Industries. But even this wasn't a straight line to success. After leaving his father's aluminium conductors making business, he came down to Mumbai as a scrap dealer to build an empire in aluminum, copper, zinc, and iron in 1976. The initial business model was deceptively simple: collect scrap metal from cable companies and sell it at a profit. It wasn't glamorous, but it was cash-generative, and more importantly, it gave him deep insights into the metal supply chain.

In 1976, Agarwal founded Hamsher Sterling Corporation, a manufacturer of enameled copper, among other products, with a bank loan. This was followed by the acquisition of Shamsher Sterling Corporation in 1979, marking his first real foray into manufacturing rather than pure trading. The transition from trader to manufacturer was crucial—it meant moving up the value chain, controlling quality, and most importantly, capturing more margin.

"Jo sir pe kafan bandh ke chalte hai, woh lene ke dene calculation nahin karte. Hum Bihari log hai, Bihar se aaye hai…kuch kar guzarenge" (people who wear a shroud on their heads do not calculate profit and loss. We are Bihari people, we have come from Bihar...but we were sure to do something), Agarwal would later reflect at the India Today Conclave 2023. This wasn't just bravado—it was a philosophy. While others calculated risk-reward ratios, Agarwal was playing a different game entirely.

The personal side of Agarwal is equally fascinating. A devotee of the Hindu God Krishna and a strict vegetarian who enjoys cycling, he married Kiran Gupta, his fellow cyclist and family friend. This wasn't the typical industrialist lifestyle of clubs and cocktails—Agarwal maintained his middle-class values even as his wealth grew exponentially.

What makes Agarwal's origin story particularly compelling is how he turned every disadvantage into an advantage. No college degree? He learned business on the streets of Mumbai. No connections? He created them by positioning himself at the Oberoi. No capital? He started with scrap metal and bank loans. This wasn't just entrepreneurship; it was alchemy—turning base metals, quite literally, into gold.

The psychological profile that emerges is of someone with an almost pathological tolerance for risk and failure. Nine failed businesses would break most people. For Agarwal, they were tuition fees for an education no university could provide. "When I was 14-15 years old, I used to go to Renukut with my father. From Patna we used to go to Benaras, and from there we used to take a shared taxi and go to Renukut"—these early journeys with his father weren't just travel; they were apprenticeships in understanding the aluminum business from the ground up.

By the time we reach the early 1980s, Agarwal had transformed from a scrap dealer into a serious player in the cable manufacturing business. The foundation was set, but the real empire-building was yet to come. What he had learned in those first difficult years in Mumbai—about cash flow, about relationships, about timing, and most importantly, about spotting opportunity in distress—would become the template for everything that followed.

The Anil Agarwal origin story isn't just about one man's rise from poverty to wealth. It's about the transformation of Indian entrepreneurship itself—from the License Raj era of connections and permits to a new model based on operational excellence and financial engineering. It's about how someone from Bihar, with no formal business education, could eventually list a company on the London Stock Exchange and sit across the table from global mining giants as an equal.

Most importantly, it's about resilience. "However, he did not give up"—four simple words that encapsulate not just Agarwal's journey, but the entire Vedanta story. In an industry where commodity cycles can destroy decades of value creation in months, where environmental controversies can shut down billion-dollar plants overnight, where political winds can turn favorable deals into nightmares, not giving up isn't just a character trait—it's a survival strategy.

As we'll see in the chapters that follow, every major acquisition, every controversial decision, every billion-dollar bet can be traced back to lessons learned in those early Mumbai years. The scrap dealer who slept at the Oberoi to project success would one day own copper mines in Zambia, zinc operations in Ireland, and oil fields in Rajasthan. But at heart, he remained what he always was—a trader who understood that in the commodity business, timing isn't just important; it's everything.

III. Building Sterlite: The Copper Foundation (1976-1999)

The period from 1976 to 1999 represents the foundational phase of what would become the Vedanta empire—a quarter-century journey from scrap metal trading to India's first private copper smelter. This wasn't just business building; it was institution creation in a country where the government had monopolized heavy industry for decades.

The late 1970s and early 1980s saw Agarwal methodically building his cable manufacturing business. After acquiring Shamsher Sterling Corporation in 1979, he spent the next seven years understanding the copper value chain from the ground up. In 1986, he set up Sterlite Industries to manufacture jelly-filled cables—a seemingly modest venture that would become the launching pad for something far more ambitious.

The real transformation began with India's economic liberalization in 1991. When Prime Minister P.V. Narasimha Rao and Finance Minister Manmohan Singh opened up the Indian economy, Agarwal saw an opportunity that most missed. While others were focused on software and services, he recognized that India's infrastructure boom would require massive amounts of base metals. More importantly, he understood that the government's monopoly on metal production through companies like Hindustan Copper was unsustainable.

In 1992, Sterlite had been allotted 500 acres of land by Maharashtra Industrial Development Corporation to set up a 60,000 tonne per annum copper smelter and associated facilities in the coastal district of Ratnagiri. This was a watershed moment—the first time a private company was attempting to break into the copper smelting business in India. But the journey would prove anything but smooth.

On 13 December 1993, over 30,000 people of the city marched to the unit and demolished the quarters for the construction workers and some other structures. After that incident Sterlite was relocated to Thoothukudi. This early confrontation with environmental opposition would become a recurring theme in Vedanta's story, but Agarwal's response revealed his operational philosophy: when faced with resistance, relocate and recalibrate rather than retreat.

The Tamil Nadu government proved more receptive. On August 1, 1994, the Tamil Nadu Pollution Control Board (TNPCB) issued a No Objection Certificate asking the company to carry out an Environmental Impact Assessment (EIA). By 1993, Sterlite Industries became the first private company in India to set up copper smelter and refinery—a historic achievement that broke decades of government monopoly.

Sterlite Industries acquired Madras Aluminium in 1995. This acquisition wasn't just about adding capacity; it was about diversification within the metals space. Agarwal was building a portfolio approach to commodities, understanding that different metals had different cycles and that diversification could provide stability during downturns.

The Silvassa operations marked another crucial expansion. Sterlite copper operates a copper refinery and two copper rod plants in Silvassa, within the Union Territory of Daman & Diu. The refinery was completed in February 1996 but the smelter was not commissioned until October 1996. This demonstrated Agarwal's strategy of building multiple production centers to reduce regulatory and operational risk.

Sterlite operated the largest copper smelter plant in India, in Thoothukudi from 1998 to 2018. By the late 1990s, Sterlite had transformed from a cable manufacturer into India's dominant private sector copper producer. The business model was elegantly simple yet difficult to execute: import copper concentrate (since India had limited copper deposits), smelt it using modern technology, and sell refined copper to India's rapidly growing infrastructure sector.

The financial engineering during this period was equally impressive. The Indian copper industry consists primarily of custom smelters as there are limited copper deposits in the country. The available deposits are owned by the government-owned Hindustan Copper, which was the only producer in India until 1995. Sterlite's entry fundamentally changed this dynamic, introducing competition and efficiency into a moribund sector.

What made Sterlite's copper foundation particularly robust was its understanding of the global copper market dynamics. The business wasn't just about processing metal; it was about arbitraging the difference between treatment and refining charges (TcRc) and finished copper prices. When copper concentrate was cheap relative to refined copper, margins expanded. When the spread narrowed, operational efficiency became crucial.

The cash flow generation from the copper business was remarkable. Unlike many Indian companies that relied heavily on debt, Sterlite generated substantial free cash flow from its operations. This cash would become the war chest for future acquisitions. Every ton of copper processed wasn't just revenue; it was ammunition for the next phase of expansion.

The technological capabilities built during this period were equally important. Running a copper smelter isn't just about having the equipment; it's about managing complex chemical processes, dealing with environmental regulations, maintaining consistent quality, and optimizing energy consumption. The operational expertise developed at Thoothukudi and Silvassa would later be applied to zinc smelting in Rajasthan, aluminum refining in Odisha, and copper mining in Zambia.

The regulatory navigation during these years deserves special mention. Three state governments, Gujarat, Goa, and Maharashtra have refused permission to the Vedanta Group to set up its 40,000 tonnes capacity due to its high polluting nature of the Sterlite copper smelting plant before the company managed to convince the Tamil Nadu government. This pattern of rejection and eventual acceptance revealed Agarwal's persistence and his ability to work with different state governments to find mutually beneficial arrangements.

The controversy that would later engulf Sterlite's copper operations had its seeds in this period. Since its commencement in 1997, the plant had been found on numerous occasions to flout the pollution norms with impunity and foregone permit requirements by pollution regulators, as observed by the courts. The tension between rapid industrialization and environmental protection was built into the business model from the beginning.

But there was another controversy that tested the company's resilience. In 2001, Sterlite industries, BPL and Videocon were found guilty by SEBI of having colluded with Harshad Mehta and 17 brokers in a bid to corner shares and rig shares prices. This resulted in a ban on the company from accessing capital markets for 2 years. This setback could have derailed expansion plans, but Agarwal used the period to focus on operational improvements and prepare for the next phase of growth.

The international ambitions were already taking shape by the late 1990s. The copper business had proven that an Indian company could compete with global players in terms of cost and efficiency. The operational template was established: acquire or build assets, improve efficiency, generate cash, and reinvest in growth. The management team was battle-tested, having dealt with everything from environmental protests to regulatory investigations.

What's remarkable about this period is how Agarwal transformed what was essentially a commodity processing business into a cash-generation machine. The copper smelting operations weren't technologically revolutionary or strategically complex. They were simply well-executed, generating consistent returns that could fund more ambitious ventures.

The foundation built during these years would prove crucial for what came next. The operational expertise in running smelters, the relationships with equipment suppliers and technology partners, the understanding of global commodity markets, the ability to manage environmental and regulatory challenges—all of these capabilities would be leveraged in the dramatic expansion that followed.

By 1999, Sterlite was generating hundreds of crores in revenue and substantial profits. The company had proven that private sector efficiency could outperform public sector monopolies. More importantly, it had created a template for growth that could be replicated across other metals and geographies. The scrap dealer from Bihar had become a serious industrialist, but the real empire building was just beginning.

The copper foundation wasn't just about the metal; it was about proving a concept. If a private company could successfully challenge the government's monopoly in copper, what about zinc? What about aluminum? What about iron ore? The possibilities seemed endless, and Agarwal had both the cash flow and the credibility to pursue them. The stage was set for the next phase: acquiring and turning around the government's own assets.

IV. The Privatization Play: BALCO & HZL (2001-2003)

The years 2001 to 2003 marked the most audacious phase of Agarwal's empire building—the acquisition of two crown jewels of India's public sector: Bharat Aluminium Company (BALCO) and Hindustan Zinc Limited (HZL). This wasn't just privatization; it was a masterclass in turning political winds into corporate opportunity, transforming sick government companies into cash-generating machines, and weathering fierce opposition to emerge stronger.

In February 2001, Government of India in a major dis-investment deal, approved the sale of its 51% stake in BALCO to Sterlite Industries (now Vedanta Limited) for Rs.551.5 crores. The timing was crucial—India's BJP-led NDA government under Atal Bihari Vajpayee was pushing an aggressive disinvestment agenda to balance the budget and reduce the fiscal deficit. Agarwal recognized this as a once-in-a-generation opportunity.

In the 1990s, as the Indian government began to sell off sick (non-performing) companies, Sterlite began to bid for them. They were able to bid successfully for BALCO and Hindustan Zinc Limited, both bankrupt companies that had been closed down for 4 years. But this characterization understates the complexity of what Agarwal achieved. These weren't just any companies—they were strategic assets in sectors the government had monopolized since independence.

Incorporated in 1965, BALCO was a profit making Public Sector Company which had played a crucial role in increasing the usage of aluminium over a wide spectrum of products ranging from household utensils to aerospace and defense sectors. Prior to its disinvestment the company reported an annual turnover of Rs 898 crores in 2000, with a profit of Rs 56 crores. This wasn't a complete basket case—it was an underperforming asset with significant potential.

The BALCO acquisition immediately triggered massive controversy. Marred with political controversy and allegations of corruption by the opposition, the disinvestment deal further stalled the work at BALCO. Instigated by the local politicians, the workers of Chhattisgarh plant went on an indefinite strike 3rd March 2001 which lasted for 67 days. The opposition Congress party, led by then Chhattisgarh Chief Minister Ajit Jogi, alleged massive corruption in the deal.

Ajit Jogi, then Chief Minister of Chhattisgarh alleged that a kick back of Rs 100 crores was paid to the high ranking officials. These allegations would dog the deal for years, but Agarwal pressed forward. His strategy wasn't to fight the political battle directly but to focus on operational transformation.

At the time of disinvestment BALCO had two running units, one in Korba Chhattisgarh and another in Bidhanbag, West Bengal, with a total of 7000 employees. The employee opposition was fierce, but Agarwal had a playbook: introduce voluntary retirement schemes to reduce the workforce, modernize operations, and dramatically increase production capacity.

Moreover the cash reserve of 437 crore which the BALCO had accumulated was not enough for its modernization which would require a sum of Rs 4000 crores. This was the key insight—the government couldn't or wouldn't invest the capital needed for modernization. Private ownership could unlock value that public ownership couldn't.

While the BALCO controversy raged, Agarwal was already moving on his next target. In 2001, as part of the Government of India's disinvestment program of loss-making PSUs, the company was put up for sale. In April 2002, Sterlite Opportunities and Ventures Limited (SOVL) made an open offer for acquisition of shares of the company; consequent to the disinvestment of Government of India's (GOI) stake of 26% including management control to SOVL and acquired additional 20% of shares from public, pursuant to the SEBI Regulations 1997.

The Hindustan Zinc acquisition was even more strategic than BALCO. Hindustan Zinc Limited was incorporated from the erstwhile Metal Corporation of India on 10 January 1966 as a Public Sector Undertaking (PSU). This gave Agarwal control over India's zinc production—a metal crucial for galvanizing steel and with growing global demand.

Sterlite Industries emerged as the highest bidder, offering Rs 40.5 per share for the government's stake. The transaction was completed in April 2002. But this was just the beginning. In August 2003, SOVL acquired additional shares to the extent of 18.92% of the paid up capital from GOI in exercise of call option clause in the share holder's agreement between GOI and SOVL. With the above additional acquisition, SOVL's stake in the company went up to 64.92%.

The transformation of HZL post-acquisition was remarkable. The former PSU, headquartered in Rajasthan, saw its profits rise manifold in the 17 years after privatisation. The full-year profits as on 31 March 2019 stood at Rs 7,956 crore, as against Rs 68 crore in the full year ending March 2002. This wasn't just incremental improvement—it was complete transformation.

The company's production capacity of zinc, lead and silver has also increased more than five-fold since disinvestment — to 1.1 million tonnes from 0.2 million tonnes per annum in 2002. Agarwal had proven that private ownership could unlock value that decades of government control couldn't.

The operational improvements at both companies followed a similar pattern. First, reduce the workforce through voluntary retirement schemes while retaining critical talent. Second, invest heavily in modernization and capacity expansion—something the government had been unable or unwilling to do. Third, implement modern management practices and tie compensation to performance. Fourth, leverage global best practices and technology partnerships.

But the political backlash was severe. Sterlite's 2001 acquisition of state-owned BALCO sparked one of the major Indian political controversies of that year. Allegations were widely made that India's Bharatiya Janata Party-led government deliberately prevented BALCO from modernising successfully on its own terms and with its own funds.

The criticism wasn't just about the deal terms—it was about the principle of privatizing strategic assets. It supplied aluminium to other major public enterprises, involved in manufacturing of aircrafts, missiles etc. With privatization the financial and other powers were transferred to SIL and the government now has to negotiate on former's terms. Critics argued that national security interests were being compromised.

Agarwal's response was to deliver results. By demonstrating that privatized companies could be more efficient, more profitable, and better contributors to the exchequer through taxes, he was making an argument that transcended politics. The numbers spoke for themselves—HZL alone was now worth more than what the government received for selling both BALCO and HZL combined.

HZL was incorporated as a public sector firm in 1996, and Atal Bihari Vajpayee's NDA government, in August 2000, decided to disinvest 26 per cent of its equity through a strategic sale. The government retained a significant stake, giving it comfort while allowing private management to drive operational improvements.

The template established during these acquisitions would define Vedanta's growth strategy for the next two decades: identify undervalued government assets, bid aggressively, weather the political storm, implement operational improvements, and generate cash for the next acquisition. It was a playbook that worked in India and would soon be applied internationally.

Both deals were heavily underpriced and lacked transparent bidding. Overnight, a blacklisted company became the owner of India's strategic mineral wealth. Critics would continue to question the deals' fairness, but from Agarwal's perspective, he had taken the risk when no one else would, invested capital the government couldn't, and delivered returns that vindicated the privatization policy.

The controversy around these acquisitions also revealed Agarwal's political acumen. Rather than directly confronting opposition, he focused on building relationships with state governments where the operations were located. In Rajasthan, where HZL operated, and in Chhattisgarh, where BALCO was based, he became a major employer and contributor to state revenues. This local support often trumped national political opposition.

Vedanta owns 64.9% of the share capital in HZL and has management control. This structure—majority control with significant government stake—became the model for managing politically sensitive acquisitions. It gave Vedanta operational control while maintaining government involvement and oversight.

The success of these privatizations had broader implications for India's economic policy. "PSUs are not the most efficient units when it comes to tech upgradation, human resources, marketing and business processes. Strategic disinvestment brings in the private sector and is a good way of maximising profits. It has been seen, both internationally and in India, that any government company that is privatised manages to increase its value with the introduction of new technology and business processes."

By 2003, Agarwal had transformed from a successful copper smelter operator into the poster child for India's privatization program. He controlled aluminum through BALCO, zinc through HZL, and copper through Sterlite. The cash flow from these operations was substantial and growing. More importantly, he had proven that an Indian entrepreneur could take on established public sector units and transform them into world-class operations.

The privatization play wasn't just about acquiring assets—it was about changing the narrative around Indian entrepreneurship. If Indian companies could successfully turn around domestic public sector units, why couldn't they acquire and manage international assets? This question would drive the next phase of Vedanta's expansion as Agarwal set his sights on the global stage.

V. Going Global: London Listing & International Expansion (2003-2007)

The period from 2003 to 2007 represents Vedanta's transformation from an Indian metals company into a global mining powerhouse. To access international capital markets, Anil Agarwal and his team incorporated Vedanta Resources Plc in 2003 in London. At the time of its listing, Vedanta Resources Plc, was the first Indian firm to be listed on London Stock Exchange, on 10 December 2003, Vedanta Resources became the parent company of the group through a process of internal restructuring of group companies and their shareholding.

This wasn't just a listing—it was a statement. For the first time, an Indian company that had grown organically rather than through colonial legacy was accessing the deepest capital markets in the world. It was first listed on the London Stock Exchange in 2003 when, as Vedanta Resources, it raised US$876 million through an initial public offering. In late 2003, the parent company Vedanta Resources went public with the listing on the London Stock Exchange (LSE). This initial public offering (IPO) was the second-largest in the United Kingdom that year.

The London listing fundamentally changed Vedanta's trajectory. Vedanta resources is the first Indian company to be listed in the London stock exchange in December 2003. It is an FTSE 100 metals and mining company with its headquarters located in London, UK and is India's largest non – ferrous company based on their revenues. The company now had access to institutional capital, sophisticated debt markets, and most importantly, credibility on the global stage.

The capital raised wasn't left idle. In 2004 Vedanta Resources Plc announced a global bond offering and acquired Konkola Copper Mines in Zambia, Africa. The Konkola acquisition was particularly strategic—it gave Vedanta control over one of Africa's largest copper mines. Vedanta owns 79.4% of KCM's share capital and have management control of the company. KCM's other shareholder is ZCCM Investment Holdings plc. The government of Zambia has a controlling stake in ZCCM Investment Holdings plc.

The Konkola deal demonstrated Agarwal's ability to operate in challenging jurisdictions. Zambia wasn't India—it required navigating different political systems, managing relationships with African governments, and dealing with infrastructure challenges that made India look straightforward by comparison. But the asset was world-class, and Agarwal understood that in the commodity business, asset quality ultimately trumps everything else.

In 2007, Vedanta Resources acquired a controlling stake in Sesa Goa Limited, India's largest producer-exporter of iron ore. In April 2007, Vedanta Limited, which was primarily focused on mining and manufacturing copper, zinc and aluminium, expanded into the iron ore segment through the acquisition of Sesa Goa. The company acquired a 51% controlling stake in Sesa Goa from Japan's Mitsui & Company for $981 million (or roughly Rs 4,900 crore).

The Sesa Goa acquisition was transformative in multiple ways. First, it gave Vedanta exposure to iron ore, completing its portfolio across base metals. Second, Sesa Goa was a profitable, well-run company with established operations and export relationships. Unlike BALCO or HZL, this wasn't a turnaround story—it was about adding a crown jewel to the portfolio.

Originally founded as Sesa Goa, a Portuguese company, Sesa Goa was purchased by Vedanta (then known as Sterlite industries) in the 1990s. The company had a colonial pedigree and established relationships with Japanese and Chinese steel mills. For Vedanta, it represented instant credibility in the iron ore market.

The international expansion wasn't limited to marquee acquisitions. In 2006, the company acquired Sterlite Gold, a gold mining business. While this venture would later prove less successful, it demonstrated Agarwal's appetite for diversification across the entire metals spectrum.

In 2007, the company also became listed on the New York Stock Exchange (NYSE). The dual listing in London and New York gave Vedanta access to the two deepest capital markets in the world. It also subjected the company to the scrutiny of sophisticated institutional investors, forcing improvements in governance and disclosure.

What's remarkable about this period is the speed of execution. In just four years, Vedanta went from being an Indian company with domestic operations to a global mining major with assets in Africa, exposure to multiple commodities, and listings on premier international exchanges. This transformation required not just capital but also management bandwidth, operational expertise, and most importantly, credibility with international stakeholders.

The financial engineering during this period was sophisticated. The London-listed Vedanta Resources became the holding company for the entire group, with various Indian subsidiaries sitting below it. This structure allowed Agarwal to raise debt at the holding company level, deploy it in operating subsidiaries, and upstream dividends to service the debt. It was leveraged growth, but intelligently structured.

It is an FTSE 100 metals and mining company with its headquarters located in London, UK and is India's largest non – ferrous company based on their revenues. The company is principally situated in India, although they have possessions and operations in other locations such as Zambia and Australia. Vedanta Resources is mainly invested in copper, zinc, Aluminium businesses, however the company is now adding to their portfolio by diversifying into a commercial power generation business.

The operational philosophy during this expansion was consistent: acquire quality assets, improve operational efficiency, and generate cash for the next acquisition. Each asset was viewed not in isolation but as part of an integrated portfolio that could weather commodity cycles. When copper prices were down, zinc might be up. When aluminum struggled, iron ore might compensate.

The governance structure evolved during this period as well. Being listed in London meant adhering to UK corporate governance standards, having independent directors, and maintaining arms-length transactions with related parties. While critics would later question some practices, the formal structures of a global corporation were being put in place.

The cultural transformation was equally significant. Vedanta was no longer just an Indian company; it was becoming a global organization. This meant hiring international talent, implementing global best practices, and most importantly, thinking beyond India's borders. The company that had started as a scrap metal dealer in Mumbai was now competing with Rio Tinto, BHP, and Anglo American for assets.

Vedanta Resources, headquartered in London, is a globally diversified natural resources conglomerate, with interests in zinc, lead, silver, copper, iron ore, aluminium, power generation, and oil and gas. The greatest share of its assets, however, is in India; Agarwal lives in London. This geographic split—operations in India, headquarters in London—would become both a strength and a source of controversy.

The relationships built during this period were crucial for future growth. Investment bankers who worked on the London IPO would finance future acquisitions. Institutional investors who bought into the growth story would provide patient capital during downturns. Technology partners who helped modernize Indian operations would support international expansions.

By 2007, Vedanta had achieved what seemed impossible just a decade earlier. It was a globally recognized mining company with diversified operations, strong cash flows, and access to international capital markets. The foundation was set for even more ambitious moves. The question was no longer whether Vedanta could compete globally, but how far Agarwal's ambitions would take the company.

The success of the international expansion validated Agarwal's vision. An Indian entrepreneur could build a global mining major. Emerging market companies could acquire and successfully operate developed market assets. The commodity supercycle that was driving China's growth could be leveraged by an Indian company with global operations. As 2007 drew to a close, with commodity prices soaring and global growth seemingly unstoppable, Vedanta appeared positioned to become one of the world's mining giants. The stage was set for the next phase of expansion, one that would test the limits of Agarwal's ambitions and Vedanta's operational capabilities.

VI. The Anglo American Zinc Deal: Becoming a Global Player (2010)

The 2010 acquisition of Anglo American's zinc portfolio marked Vedanta's emergence as a truly global mining powerhouse. Anglo American plc announces that it has agreed to sell its portfolio of zinc assets to Vedanta Resources plc for a total consideration of $1,338 million on an attributable, debt and cash free basis. This wasn't just another acquisition—it was a statement that an Indian company could compete for and win world-class assets against established Western mining majors.

Anglo American Zinc comprises the Skorpion mine in Namibia, the Lisheen mine in Ireland and a 74% interest in Black Mountain Mining in South Africa, which holds 100% of the Black Mountain mine and the Gamsberg project. The portfolio spanned three continents, each asset with its unique operational challenges and opportunities. Of the total consideration, $698 million relates to the Skorpion mine, $308 million relates to the Lisheen mine and $332 million relates to Anglo American's 74% interest in Black Mountain Mining.

The strategic logic was compelling. Anil Agarwal, Chairman of Vedanta, said: "We are delighted to have reached this agreement with Anglo American to acquire their portfolio of zinc assets. These high quality assets complement Vedanta's existing portfolio, creating the largest zinc and lead producer in the world." With Hindustan Zinc already under its belt, this acquisition would cement Vedanta's position as a global zinc leader.

The Skorpion mine in Namibia was particularly unique. Skorpion is a unique mine in several ways. Firstly, it is a supergene zinc ore body composed of alluvial accumulations of zinc carbonate and silicate minerals of detrital nature deposited within a palaeochannel. There are no other currently commercially viable deposits of this type. It is also one of the few mines in the world that currently mines zinc oxides, a mixture of non-sulphidic zinc minerals such as smithsonite, hydrozincite, tarbuttite and willemite. Finally, it is the only zinc processing facility to use solvent extraction-electrowinning metallurgy to process and refine its zinc products (others using conventional smelting and roasting).

It was established at a cost of US$450 million by Anglo American in 2003. It is the tenth-largest zinc mine in the world, and the largest employer in Rosh Pinah, providing 1,900 jobs. The operational scale was significant, and the technology was cutting-edge. The Skorpion SX-EW plant creates Special High Grade, ultra-pure zinc cathode as a primary product, which is so low in impurities that it commands a price premium.

The Lisheen mine in Ireland represented Vedanta's first operational footprint in Western Europe. This wasn't just about accessing ore; it was about demonstrating that an Indian company could operate successfully in a developed, highly regulated market. The Irish operations would provide valuable experience in managing environmental standards and stakeholder relationships that would be crucial for future expansion.

Black Mountain Mining in South Africa came with an additional prize—the Gamsberg project. We intend to rapidly develop Gamsberg, one of the largest high quality zinc projects in the world, leveraging our world-class large project development expertise. Significant organic growth potential through Gamsberg, one of the largest undeveloped zinc deposits in the world, with JORC mineral resource of 186mt ore. Planned production capacity is 400ktpa of zinc metal, with an operating life in excess of 20 years and further exploration potential.

The financial impact was immediate and substantial. Substantially increases Vedanta's zinc and lead production capacity, increasing annualised production capacity from 1,064ktpa to 1,462ktpa (an increase of 37 per cent.) This represented approximately 11 percent of the global zinc market—a scale that put Vedanta in the same league as century-old mining houses.

Anglo American Zinc produced 350,000 tonnes of contained zinc in 2009, generating gross revenues of $717 million and EBITDA of $227 million. These were profitable, cash-generating assets, not turnaround stories. Anglo American was divesting as part of a strategic refocus, and Vedanta was the beneficiary.

The deal structure was sophisticated. The consideration agreed with Vedanta is based on effective economic ownership, including profits and cash flows, passing to Vedanta as of 1 January 2010. This meant Vedanta would capture the entire year's economic benefit, even though the deal closed later.

Completion of the transaction is expected to be in stages, with separate completion dates for Skorpion, Lisheen and Black Mountain Mining. This phased approach allowed Vedanta to manage the integration complexity while ensuring each asset received appropriate attention.

The operational philosophy for these acquisitions was clear. Vedanta has consistently demonstrated a track record of successfully integrating and investing in its acquisitions, and we look forward to working with the high quality management team and employees of Anglo American Zinc, Exxaro and the local communities towards growing the business. We are committed, as we are throughout all of our operations world wide, to maintaining the highest health and safety standards, and to the sustainable development of these operations.

Anglo American plc announces the completion of the sale of its Skorpion zinc mine in Namibia to Vedanta Resources plc for cash proceeds of US$707 million. The Skorpion completion in November 2010 marked the first successful closure, demonstrating Vedanta's execution capabilities.

The integration challenges were significant. Managing operations in Namibia required understanding local labor relations, government expectations, and infrastructure constraints. Prior to going into Care & Maintenance, Skorpion Zinc's total employment stood at 1,800 with 96% being local Namibians. Maintaining social license while driving operational improvements required delicate balancing.

In South Africa, the Black Mountain acquisition came with additional complexity. Exxaro Resources Limited, Anglo American's black economic empowerment partner in Black Mountain Mining, holds a 26% interest in the company and has a pre-emptive right to match Vedanta's offer in respect of this asset. Navigating South Africa's BEE requirements while maintaining operational control tested Vedanta's diplomatic skills.

Anglo American completed the $364 million sale of its Black Mountain Mining zinc interests to Vedanta Resources on Saturday 5th February 2011. The successful completion demonstrated Vedanta's ability to manage complex multi-jurisdictional transactions.

The technology transfer was equally important. It was acquired by Vedanta Resources Plc in 2010 from Anglo and became part of Vedanta Zinc International. Vedanta wasn't just buying mines; it was acquiring operational expertise, technology, and management systems that could be applied across its global portfolio.

The future potential was significant. In order to create a sustainable life for Skorpion Zinc and shorten the care and maintenance gap. Our focus is currently on the Refinery Conversion Project, which will enable co-treatment of both sulphides and oxides to produce refined metal. Significant work has been put into the Refinery Conversion project, including the completion of the bankable feasibility study. Once completed, the Refinery will process zinc concentrate from Vedanta Group companies located in South Africa, add value in Namibia, and export the refined product.

The financial commitment to future development was substantial. NAD 6.5 billion has been set aside for the future of Skorpion Zinc which is promising massive Socio-Economic benefits with a projection of approx. 1 300 direct employment, 12 730 induced employment from the Refinery Conversion Project.

The deal's success validated Vedanta's global ambitions. On 10 May 2010, Vedanta announced the acquisition of Anglo American's zinc assets for a total cash consideration of US$1 338 million (R9.3 billion), on an attributable, debt and cash free basis. Anglo Zinc comprises the 100%-owned Skorpion mine in Namibia, the 100% owned Lisheen mine in Ireland, and the 74% owned Black Mountain Mines, which include the Black Mountain mine and Gamsberg project in South Africa.

The Anglo American zinc acquisition represented a watershed moment for Vedanta and Indian corporate ambition more broadly. An Indian company had successfully acquired premier mining assets from one of the world's most established mining houses, integrating operations across three continents while maintaining operational continuity. The deal proved that emerging market companies could be acquirers rather than just targets, that operational excellence could transcend geographic boundaries, and that financial engineering combined with operational expertise could create value even in mature assets.

By the end of 2010, Vedanta had truly become what Agarwal had envisioned—a global natural resources major with world-class assets, diversified geography, and the scale to compete with anyone. The zinc portfolio alone made it one of the world's largest producers, but more importantly, it had proven that an Indian entrepreneur could build a truly global mining empire. The stage was set for the next ambitious move—entering the oil and gas sector through the acquisition of Cairn India.

VII. The Cairn India Acquisition: Oil & Gas Ambitions (2011-2017)

The acquisition of Cairn India between 2011 and 2017 represented Vedanta's boldest diversification yet—a $9.6 billion bet that a mining company could successfully operate in the oil and gas sector. In fact, in 2011, Vedanta Group acquired 58.5% controlling interest in Cairn India from its UK parent, Cairn Energy Plc. The case study discusses the biggest deal in Indian oil sector in which miner and London listed company, Vedanta announced to acquire up to 60% stake in oil and gas exploration company Cairn India for $9.6 billion.

Cairn India was an Indian oil and gas exploration and production company, headquartered in Gurgaon, India. The company was merged with Vedanta Limited. But this was no ordinary oil company—it held the keys to India's energy security ambitions through its Rajasthan oil fields.

The Mangala field in Rajasthan, which was discovered in January 2004, is the largest onshore oil discovery in India in more than 20 years. The Mangala, Bhagyam and Aishwariya (MBA) fields have gross recoverable oil reserves and resources of over one bn boe. This wasn't just about barrels of oil; it was about reducing India's dependency on imports and capturing value from a strategic national asset.

The deal structure was complex and controversial from the start. Of this, 20% was acquired by Vedanta Ltd and 38.5% by Twinstar Mauritius Holdings, Ltd, which is a special purpose vehicle wholly owned by Vedanta Resources Plc. The acquisition by TMHL was funded by $4.43 billion of debt funded partly by banks and by Cairn India. The financial engineering was aggressive—using debt and even Cairn India's own resources to fund its acquisition.

State-run company Oil and Natural Gas Corporation (ONGC), being a joint venture partner in eight out of ten oil blocks of Cairn India does not accept the deal and reserves pre-emption rights. ONGC's opposition wasn't just procedural—it reflected deep concerns about a private company, particularly one with no oil and gas experience, controlling such strategic assets.

The deal got locked in a dispute with the government over the payment of royalty. Later the government gave conditional approval to the deal provided Cairn India treated royalty as a cost recoverable item, withdraw all arbitration proceedings and obtain a no-objection certificate from Oil and Natural Gas Corporation. The regulatory hurdles would drag on for years, testing Agarwal's patience and financial resources.

While waiting for approvals, Vedanta demonstrated its commitment to the deal. While waiting on government approval on its agreement with Cairn Energy, Vedanta acquired an additional 18.5% on the open market including a 10.4% stake from Petronas for $1.5 billion. This aggressive move showed Agarwal's confidence in the asset despite regulatory uncertainty.

Top 250 Global Energy Company Rankings by Platts, ranked Cairn India for being the World's fastest-growing energy company in 2011. Vedanta wasn't just buying an oil company; it was acquiring one of the most dynamic energy players in the emerging markets.

The operational assets were world-class. Cairn has stakes in the oil producing blocks – 70% in Rajasthan RJ-ON90/1, 22.5% in Revva and 40% in Cambay block CB-OS/2. In its largest field in Rajasthan, the company estimates gross proved and probable reserves and resources at 1.3 bn barrel of oil equivalent (boe) and gross recoverable risked prospective resources of 5.

The Rajasthan block, covering 10,000 km², is situated in the Barmer district. The breakthrough discovery of Mangala in 2004 stands as the largest onshore discovery in India to date. This milestone marked the beginning of our journey in Rajasthan, laying a strong foundation for our success in the region.

The strategic rationale for the acquisition was multi-faceted. The merger – a $2.3 billion all-share deal -- will consolidate Vedanta's position as one of the world's largest diversified natural resources companies like BHP Billiton and Rio Tinto and the merged entity will have a pro forma market cap of $15.6 billion. Agarwal was building a resources conglomerate that could rival the global majors.

As far as Cairn India is concerned, the deal will help it to diversify earnings from oil and gas to electricity and an array of commodities from copper to zinc to aluminum. The shareholders of Cairn India will also gain from Vedanta's asset base and output increase forecast compared with Cairn India's moderate output growth plan.

The production profile was impressive and growing. The Ravva oil and gas field in the Krishna- Godavari Basin was developed in partnership with Cairn India, ONGC, Videocon and Ravva Oil, under a production sharing contract (PSC) that runs until 2019. Currently, eight unmanned offshore platforms are being operated. A 225-acre onshore processing facility at Surasaniyanam processes natural gas and crude oil from the Ravva field. The Ravva onshore terminal operates to the internationally environmental standard – ISO 14001 – and has the capacity to handle 70,000 barrels (11,000 cubic metres) of oil per day, 95 million cu ft (2.7 million m3) per day at standard conditions of natural gas and 110,000 bbl (17,000 m3) per day of injection water.

Cairn India plans to drill in excess of 450 wells in the Rajasthan block over a three-year period; includes 100 Exploration and Appraisal (E&A) wells and the balance as development wells to sustain and enhance production. The growth potential was significant, requiring the kind of capital that Vedanta could provide.

The political significance of the deal couldn't be overstated. This Deal has earmarked a beginning of a new era in the Indian oil industry; which led Mr. Jaipal Reddy, Minister of Petroleum and Natural Gas, Union of India, to assert while addressing the World Petroleum Congress on December 5, 2011 that: "two major investment decisions made by major companies BP (British Petroleum) and Vedanta ... have re-established faith in the hydrocarbon potential in India".

Cairn Oil & Gas, part of Vedanta Limited, is India's largest private oil and gas exploration and production company, contributing more than a quarter of India's domestic crude oil production and driving energy security for India in a sustainable and responsible way. Post-acquisition, Vedanta would become a critical player in India's energy security.

With a world-class resource base, the company has an interest in 62 blocks in India covering a total acreage of more than 61,114 square kilometres with gross 2P (Gross Proved Plus Probable Reserves) and 2C (Gross Contingent Reserves) in excess of 1.1 bn boe. The scale of operations was staggering, making Vedanta a major force in Indian energy.

The integration challenges were significant. Oil and gas was a completely different business from mining—different technology, different regulations, different stakeholder management. Dixit is the fifth CEO to have left the company since Vedanta completed the acquisition of Cairn India in December 2011. The high turnover in leadership suggested the difficulties in managing this diversification.

But the financial logic was compelling during commodity boom times. For Cairn, the merger will help it to withstand commodity price shocks as in a volatile price environment, a stronger balance sheet can manage cash flows very well. Diversification across commodities could theoretically smooth out cyclical volatility.

The merger will also make Vedanta Resources less complex, with its subsidiaries coming down to four from nine in 2011. The corporate simplification was as important as the operational synergies.

The eventual merger in 2017 marked the culmination of a six-year journey. The company was delisted from the NSE and the BSE on 25 April 2017 following its merger with its parent company Vedanta Limited. The full integration had taken years longer than anticipated, but Vedanta had finally absorbed one of India's most valuable energy assets.

Now the Company plans to invest $3 billion in the next three years in finding more oil and raising output from Rajasthan oilfields. The commitment to future investment demonstrated that this wasn't just financial engineering but a long-term strategic bet on India's energy sector.

The Cairn India acquisition represented both the apex and the turning point of Vedanta's expansion strategy. It proved that Agarwal's ambitions knew no sectoral boundaries—if it came out of the ground and generated cash, Vedanta would consider it. But it also stretched the company's management bandwidth, balance sheet, and credibility to their limits. The prolonged regulatory battles, the integration challenges, and the massive debt burden would shape Vedanta's strategy for years to come. As commodity prices began their long decline from 2014 onwards, the wisdom of such aggressive diversification would be severely tested.

VIII. Consolidation & Simplification (2013-2018)

After years of aggressive expansion across commodities and geographies, Vedanta entered a phase of consolidation driven by necessity rather than choice. The commodity supercycle that had fueled Agarwal's empire-building was ending, and the complex corporate structure built through numerous acquisitions needed rationalization.

The merger of Sesa Goa and Sterlite Industries was announced in 2012, as part of the Vedanta Group's consolidation. This wasn't just administrative tidying—it was a fundamental restructuring aimed at creating a simpler, more efficient organization that could weather the coming storm in commodity markets.

The Sterlite-Sesa Goa merger was transformational. In 2015, Sterlite Industries and Sesa Goa announced their merger and finally merged into a single entity in August 2015. In 2015, Sesa Sterlite changed its name to Vedanta Limited. The new entity would house all of Vedanta's Indian operations under one umbrella, simplifying the corporate structure and improving operational synergies.

The rationale for consolidation was multi-faceted. First, the complex web of subsidiaries and cross-holdings had become difficult for investors to understand and value. Second, multiple listed entities meant duplicated costs, regulatory requirements, and management attention. Third, the debt taken on during the expansion phase needed to be managed more efficiently, which required consolidated cash flows.

The merger will also make Vedanta Resources less complex, with its subsidiaries coming down to four from nine in 2011. This dramatic simplification would make the company more transparent to investors and easier to manage operationally.

The commodity market environment had turned decisively negative by 2013-2014. Iron ore prices had collapsed from their 2011 peaks, aluminum was in global oversupply, and even zinc prices were under pressure. The aggressive leverage taken on during the boom years suddenly looked dangerous as cash flows declined.

Vedanta's debt issues were attributable to regulatory hurdles and weak commodity prices, which hit the cash-flows of group companies. The gloomy macroeconomic environment for the commodities market as a result of sharp decline in commodity prices has had a negative impact on the net profits of Vedanta.

In this environment, Vedanta needed to optimize its portfolio and focus on cash generation rather than growth. Non-core assets were identified for disposal, capital expenditure was curtailed, and operational efficiency became the mantra across all operations.

On 11 April 2017, Cairn India merged with Vedanta Limited to consolidate its position as one of the largest diversified natural resources companies in the world. The Cairn India merger, delayed for years by regulatory hurdles, finally provided the simplified structure Agarwal had been seeking.

But even as Vedanta consolidated existing operations, opportunistic acquisitions continued where value was compelling. In 2018 Vedanta Limited acquired control of Electrosteels Steels Limited. Electrosteel Steels had been constructing an integrated steel plant at Siyaljori in Jharkhand. The acquisition through India's new bankruptcy process showed that Vedanta could still find value in distressed assets.

The ultimate consolidation move came in 2018 when Agarwal decided to take Vedanta Resources private. In September 2018, Anil Agarwal taking Vedanta Resources private represented the logical conclusion of the simplification strategy. Without public market scrutiny and quarterly earnings pressure, Agarwal could focus on long-term value creation and navigate the cyclical downturn.

The operational improvements during this period were significant. Technology adoption accelerated, with digital initiatives improving productivity across mines and smelters. Cost reduction programs were implemented systematically, with targets set for each business unit. The focus shifted from volume growth to margin improvement.

Working capital management became a priority. Inventory levels were optimized, receivables collection was accelerated, and payment terms with suppliers were renegotiated. Every basis point of efficiency mattered in a low commodity price environment.

The portfolio optimization wasn't just about selling assets—it was about focusing capital and management attention on the most promising opportunities. The zinc business, with its strong position in India through HZL, remained a cash cow. The aluminum business, despite challenging market conditions, had potential given India's growing demand. The oil and gas business, now fully integrated, provided diversification and growth potential.

Human capital management during this period was crucial. The consolidation inevitably meant redundancies and reorganization. Retaining key talent while reducing costs required careful handling. Performance management systems were overhauled to align with the new reality of margin-focused operations rather than growth at any cost.

The stakeholder management challenges during consolidation were significant. Minority shareholders in various subsidiaries needed to be treated fairly during mergers. Regulators required extensive documentation and justification for each transaction. Environmental and social obligations couldn't be neglected even as costs were cut.

The delisting of Vedanta Resources from the London Stock Exchange marked the end of an era. The company that had used London listing as a springboard for global expansion was retreating to focus on its core markets and operations. But this wasn't a retreat from ambition—it was a strategic repositioning for the next phase of growth.

Financial restructuring accompanied operational consolidation. Debt was refinanced at lower rates where possible, maturities were extended, and the overall capital structure was optimized for a lower commodity price environment. The focus on free cash flow generation over revenue growth marked a maturation of the business model.

The environmental and regulatory challenges continued during this period. The closure of the Sterlite Copper plant in Tuticorin following protests in 2018 was a major blow, removing a significant profit contributor. The Goa mining ban affected iron ore operations. These setbacks reinforced the need for a diversified portfolio and better stakeholder engagement.

By the end of 2018, Vedanta had emerged as a leaner, more focused organization. The sprawling empire built through two decades of acquisitions had been consolidated into a more manageable structure. The company was better positioned to handle commodity cycles, with improved operational efficiency and a simplified corporate structure.

The consolidation phase proved that Vedanta could adapt to changing market conditions. The same entrepreneurial agility that had driven aggressive expansion could be redirected toward optimization and efficiency. While growth remained the long-term objective, the company had learned to be patient and selective.

As Vedanta entered 2019, it was a different company from the aggressive acquirer of the previous decade. The focus had shifted from empire-building to value creation, from complexity to simplicity, from leverage to cash generation. The foundation was being laid for the next phase of growth, one that would be more measured but potentially more sustainable.

IX. Controversies & Challenges

No story of Vedanta would be complete without examining the numerous controversies that have shadowed its growth. From environmental violations to human rights concerns, from regulatory battles to tragic incidents, Vedanta's journey has been marked by persistent challenges to its social license to operate.

In March and April 2018, there were renewed mass protests against the company's plans to set up a second smelting complex and to demand a shutdown of its Thoothukudi (Tuticorin) smelting plants, on grounds of violating environmental regulations. On 22 May 2018 the protests took a deadlier turn as 13 people were killed and several others injured, following a police shooting. The Tuticorin tragedy became a defining moment, crystallizing opposition to Vedanta's operations and raising fundamental questions about corporate responsibility.

The roots of the Tuticorin conflict ran deep. The copper smelter had faced opposition since its inception, with local communities raising concerns about pollution, health impacts, and environmental degradation. Despite being one of Vedanta's most profitable operations, contributing nearly 40% of India's copper production, the plant had operated under a cloud of controversy for two decades.

The environmental allegations were serious and persistent. In 2004, a committee of the Indian Supreme Court charged that Vedanta had dumped thousands of tons of arsenic-bearing slag near its factory in the Indian state of Tamil Nadu, resulting in major poisoning of the environment and neighbouring population. These weren't isolated incidents but part of a pattern that critics argued showed systematic disregard for environmental regulations.

The Niyamgiri controversy in Odisha represented another flashpoint. In 2005, another committee of the Indian Supreme Court charged that Vedanta had forced over one hundred indigenous families from their homes in the Indian state of Odisha, where it sought to mine bauxite. According to the committee's report: "An atmosphere of fear was created through the hired goons", and residents were "beaten up by the employees of M/s Vedanta".

The Niyamgiri hills weren't just a source of bauxite—they were sacred to the Dongria Kondh tribe. Vedanta's plans to mine these hills became a global cause célèbre, attracting support from international human rights organizations and celebrities. The image of a multinational corporation threatening indigenous people's sacred lands was devastating for Vedanta's reputation.

International condemnation followed. Vedanta's actions in Odisha were rebuked by the British commerce agency, and the Church of England investment funds sold their shares in the company in protest. When the Church of England divests from your company on ethical grounds, it sends a powerful signal about reputational risk.

The pattern extended beyond India. In Zambia, Vedanta dumped hazardous waste into the Kafue River, from its copper mine there, according to a lawsuit filed by 2,000 residents, resulting in widespread human illness and the death of fish. A local judge stated: "This was lack of corporate responsibility and criminal and a tipping point for corporate recklessness".

The Zambian operations faced additional scrutiny. In 2014, an audit was begun by Zambian officials due to suspicions that Vedanta had not been paying its proper fees to the government. In addition, "hundreds of former mine workers are fighting Vedanta for severance or disability pay." These disputes undermined Vedanta's narrative of bringing development and prosperity to Africa.

Worker safety remained a persistent concern. A chimney under construction by Gannon Dunkerley & Company at the Balco smelter in Korba, Chhattisgarh collapsed on 23 September 2009, killing at least 40 workers. Balco and GDCL management have been accused of negligence in the incident. Such tragedies raised questions about whether cost-cutting and efficiency drives were compromising safety standards.

The pattern of violations was documented extensively. The committee submitted its report on 16 August 2010, saying "The Vedanta Company has consistently violated the Forest Conservation Act [FCA], the Forest Rights Act [FRA], the Environment Protection Act [EPA] and the Orissa Forest Act in active collusion with the State officials. Allowing mining by depriving two primitive tribal groups of their rights over the proposed mining site to benefit a private company would shake the faith of the tribal people in the laws of the land".

The government's response was sometimes severe. Based on a panel report, the government of India has served a show cause notice on the company on why its Stage I environment clearance should not be cancelled. The threat of losing licenses and clearances was a constant sword hanging over Vedanta's operations.

The Goa mining controversy added another dimension. The state's iron ore mining sector, in which Vedanta was a major player through Sesa Goa, was shut down following findings of massive illegalities. The Supreme Court-appointed Shah Commission found systemic violations, illegal mining outside approved areas, and environmental destruction. While not solely responsible, Vedanta was caught up in the broader crackdown.

The financial implications of these controversies were significant. Plant closures meant lost production and revenue. Legal battles consumed management time and resources. Reputational damage made financing more expensive and partnerships more difficult. The Tuticorin plant closure alone reportedly cost Vedanta over $200 million in annual profits.

But perhaps the most significant impact was on Vedanta's social license to operate. In an era of increasing environmental consciousness and social activism, Vedanta became a lightning rod for opposition to extractive industries. Every new project faced scrutiny and potential opposition. Expansion plans were delayed or cancelled due to protests and regulatory hurdles.

The Justice Aruna Jagadeesan Commission has not found any "specific evidence" that points to the involvement of either Sterlite Industries, as claimed by a few activist groups, or any outfit, as alleged by the then government and a few individuals such as actor Rajinikanth, in the violence of May 22, 2018. Even when investigations cleared Vedanta of some allegations, the reputational damage was already done.

The company's response to these controversies evolved over time. Initially dismissive of critics, Vedanta gradually recognized the need for better stakeholder engagement. CSR spending increased dramatically, with investments in education, healthcare, and community development around its operations. Environmental management systems were upgraded, and sustainability reporting became more comprehensive.

In 1992, Anil Agarwal created the Vedanta Foundation as the vehicle through which the group companies would carry out their philanthropic programs and activities. In the financial year 2013–14, the Vedanta group companies and the Vedanta foundation invested US$49.0 million in building hospitals, schools and infrastructure, conserving the environment and funding community programs that improve health, education and livelihood of over 4.1 million people. The initiatives were undertaken in partnership with the government and non-governmental organizations (NGOs).

Yet critics argued that CSR spending couldn't compensate for environmental damage and human rights violations. The fundamental tension between extractive industry profits and community/environmental wellbeing remained unresolved. Vedanta's controversies became case studies in business schools about the challenges of operating in developing countries with weak regulatory frameworks and vulnerable populations.

The international nature of Vedanta's operations meant that controversies in one location affected its reputation globally. Following the death of 13 people during violent protests against the mining giant's Sterlite copper smelter in Tuticorin, Tamil Nadu, in May, UK's opposition Labour Party had called for Vedanta Resources to be delisted from the London Stock Exchange. John McDonnell, the shadow chancellor, said removing Vedanta Resources from the London financial markets would prevent reputational damage from the "rogue" company, which has been operating "illegal" mining concerns for years.

The controversies also highlighted the governance challenges within Vedanta. The concentration of ownership with the Agarwal family, the complex corporate structure, and the aggressive growth strategy all contributed to governance concerns. International investors increasingly questioned whether proper oversight and controls were in place.

As Vedanta moved forward, managing its controversial legacy became as important as managing its operations. The company that had built its fortune by acquiring and turning around distressed assets now faced the challenge of turning around its own distressed reputation. The path forward required not just operational excellence but a fundamental reimagining of how a resources company could operate sustainably and responsibly in the 21st century.

X. Modern Era: Technology & Energy Transition (2019-Present)

The post-2019 era has seen Vedanta attempt to reinvent itself for a new economic paradigm defined by energy transition, technological disruption, and heightened ESG scrutiny. The company that built its fortune on traditional mining and smelting now positions itself as essential to the green revolution and India's technological ambitions.

The most audacious move came in semiconductors. According to Forbes Vedanta and Foxconn would jointly invest about $20 billion in 2022 to build semiconductor and display plants in the Indian state of Gujarat, with Vendanta having 60% stakes in the venture. This represented a dramatic departure from Vedanta's core competencies, venturing into high-technology manufacturing that required entirely different capabilities.

The semiconductor ambitions aligned with India's strategic priorities. As global supply chains reconsidered their China dependence, India positioned itself as an alternative manufacturing hub. Vedanta, with its deep pockets and government relationships, seemed well-positioned to capitalize on this shift. The partnership with Foxconn, the world's largest electronics manufacturer, provided crucial technical expertise.

However, the semiconductor venture proved more challenging than anticipated. In July 2023, the Foxconn partnership ended, with both parties citing differing views on the project's direction. The failure highlighted the difficulties of diversifying into technologically complex sectors, even with substantial capital and partnerships. Yet Vedanta persisted, announcing plans to go solo and invest $15 billion in display and semiconductor manufacturing.

The energy transition presented both challenges and opportunities. As the world pivoted toward renewable energy and electric vehicles, demand patterns for metals fundamentally shifted. Copper, nickel, and aluminum—all core to Vedanta's portfolio—became "green metals" essential for renewable infrastructure and electric vehicles. A single wind turbine requires tons of copper; an electric vehicle uses four times more copper than a conventional car.

In March 2024, Vedanta announced a transformative investment plan. March 2024: $6 billion investment announced, targeting $2.5 billion additional EBITDA The investment focused on expanding production of critical minerals for the energy transition while improving operational efficiency through technology adoption.

The technology transformation within existing operations has been equally significant. Artificial intelligence and machine learning are being deployed across mines and smelters to optimize production, predict equipment failures, and improve safety. Digital twins of major operations allow for scenario planning and optimization without disrupting actual production. Automation is reducing costs while improving safety in hazardous environments.

Vedanta's positioning in EV metals has become central to its strategy. EV metals positioning: copper, nickel, aluminum The company is investing heavily in expanding copper production capacity, recognizing that the electrification of transport and renewable energy deployment will drive unprecedented demand. Nickel operations are being optimized for battery-grade production. Aluminum, essential for lightweighting vehicles, is seeing renewed investment.

The power generation strategy has evolved significantly. Power generation and renewable energy Vedanta operates one of India's largest private power generation portfolios, with 9 GW of capacity. Increasingly, this includes renewable energy, both for self-consumption to reduce carbon footprint and as a business opportunity. The company has announced plans for 5 GW of renewable energy capacity by 2030.

The current portfolio reflects both continuity and change. Current portfolio: zinc, lead, silver, copper, aluminium, iron ore, oil & gas While the core commodities remain the same, how they're produced, marketed, and positioned has fundamentally changed. Zinc is now marketed for galvanizing renewable energy infrastructure. Aluminum is positioned for the automotive transition. Oil and gas operations emphasize cleaner production and carbon capture potential.

India's infrastructure supercycle opportunity represents the domestic growth story. India's ambitious infrastructure plans—from smart cities to industrial corridors—require massive quantities of basic materials. Vedanta, as India's largest private metals producer, is uniquely positioned to benefit. The government's production-linked incentive schemes and infrastructure spending provide a multi-decade growth runway.

ESG considerations have moved from periphery to center. Vedanta has committed to net-zero carbon emissions by 2050, with an interim target of 25% reduction by 2030. Water recycling rates exceed 35% across operations. The company publishes detailed sustainability reports and has tied executive compensation to ESG metrics. While critics remain skeptical given past controversies, the shift in focus is undeniable.

The demerger plans announced in 2023 represent another strategic pivot. Vedanta plans to split into six independent listed companies—aluminum, oil and gas, power, steel and ferrous materials, base metals, and Vedanta Limited (retained entity). The logic is compelling: each business faces different market dynamics, requires different capabilities, and appeals to different investors. Separate listings could unlock value by allowing more focused strategies and targeted capital allocation.

Promoter holding at 56.38% ensures that the Agarwal family maintains control even after demerger. This concentrated ownership remains both a strength—enabling quick decision-making and long-term thinking—and a concern for governance advocates.

The financial performance in the modern era reflects both commodity market volatility and operational improvements. Despite challenging markets, Vedanta has maintained strong cash generation through cost reduction and operational excellence. Debt levels, while still significant, have been managed through asset sales and refinancing. The company has returned to regular dividend payments, signaling confidence in cash generation capabilities.