VARROC: From Bajaj's Captive Supplier to Global Auto Giant

I. Introduction & Episode Roadmap

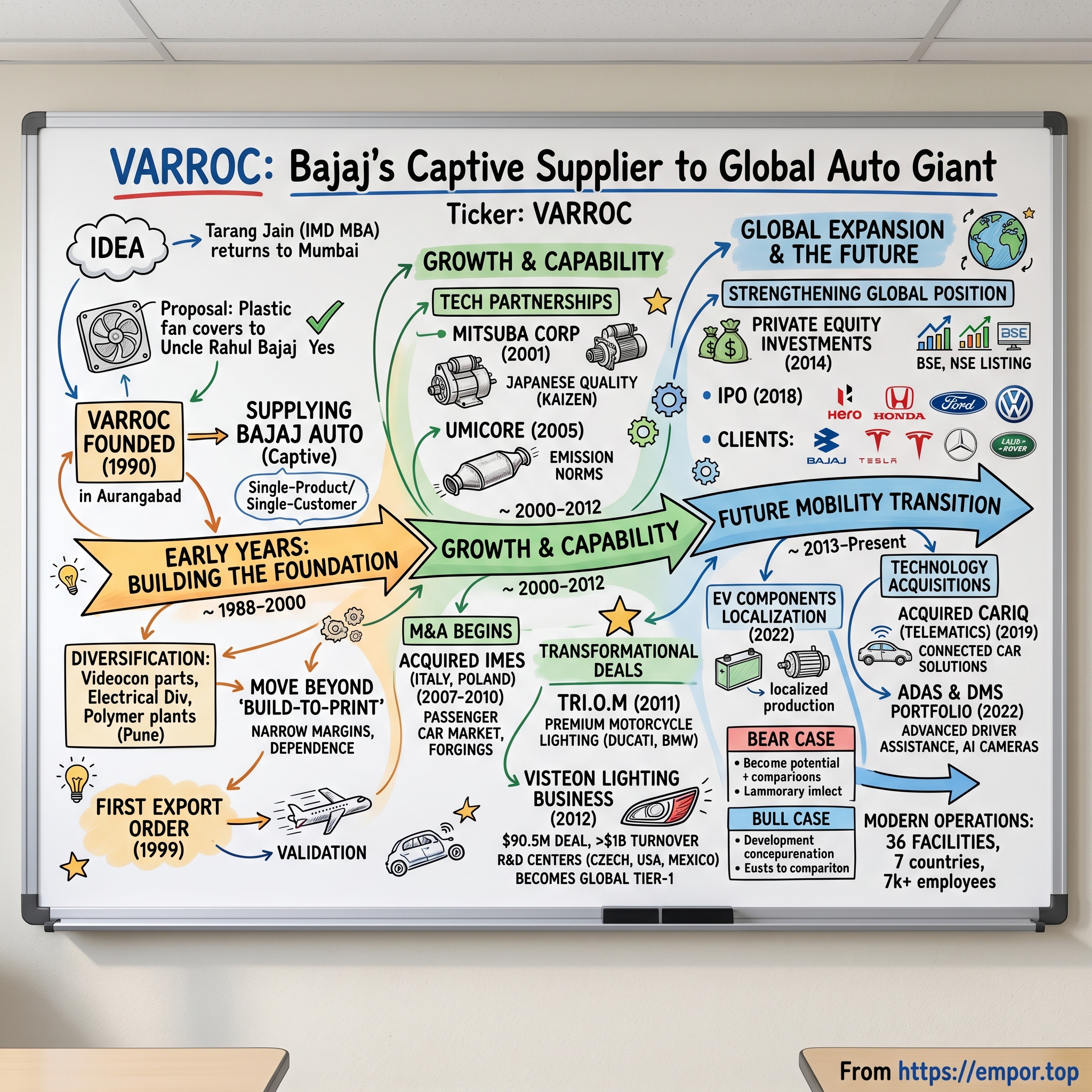

Picture this: A young MBA graduate returns from Switzerland to Mumbai in the late 1980s, walks into his uncle's office—Rahul Bajaj, the legendary industrialist—and proposes something audacious. "What if we replaced all your aluminum and steel fan covers with plastic?" The uncle is skeptical. Metal is durable, proven, trusted. But the nephew persists, and that single idea would spark the creation of what is today Varroc Engineering—a ₹8,440 crore automotive components giant with 36 manufacturing facilities spanning 10 countries. Varroc Engineering is the story of how family connections, strategic vision, and calculated risks transformed a small captive supplier into a multinational automotive components manufacturer. Today, the company stands as an Indian multinational automotive component manufacturer specializing in exterior lighting systems, powertrains, electrical and electronics, body and chassis parts, with 36 manufacturing facilities across 10 countries and a market cap of ₹7,967 crore.

The central question that drives this narrative: How did a Bajaj Auto captive supplier evolve into a global Tier-1 automotive giant? The answer lies in a complex interplay of family business dynamics, strategic acquisitions, and an unrelenting push toward global expansion—a journey that began with plastic fan covers and now spans advanced driver assistance systems and EV components.

II. The Bajaj Connection & Founding Story

The Mumbai monsoons of 1988 were particularly heavy that year, but inside the Bajaj corporate offices, a different kind of storm was brewing. Tarang Jain, fresh from his MBA at IMD Business School in Lausanne, Switzerland, sat across from his maternal uncle, Rahul Bajaj—the legendary industrialist who had transformed Bajaj Auto into India's two-wheeler giant. Between them lay sketches of plastic components, engineering diagrams, and what seemed like an absurd proposition.

"Uncle, think about it," Tarang pressed, his voice carrying the confidence of youth mixed with European business school polish. "Every aluminum and steel fan cover on your scooters adds weight, cost, and complexity. Plastic can do the same job—lighter, cheaper, more versatile."

Rahul Bajaj, a man who had built his empire on metal and mechanical precision, was skeptical. The Bajaj name meant reliability, durability—qualities traditionally associated with metal, not plastic. But there was something about his nephew's conviction, perhaps reminiscent of his own battles to modernize Bajaj Auto decades earlier. The family ties run deeper than just business. Tarang's mother Suman is the sister of Rahul Bajaj, and his father Naresh Chandra Jain founded Varroc, while his identical twin brother Anurang Jain runs another car components company, Endurance Technologies. But the lineage extends even further back—the twins are the great-grandsons of Jamnalal Bajaj, whom Mahatma Gandhi considered his fifth son.

This heritage meant something. Jamnalal Bajaj had started the Bajaj Group in 1926 and convinced Gandhi to open an ashram in Maharashtra in 1932, where the family stayed until 1948. The weight of this legacy sat on young Tarang's shoulders as he made his proposal to his uncle.

After earning his bachelor's degree from University of Mumbai and an MBA from IMD Business School in Lausanne, Switzerland, Tarang had returned with fresh eyes and European perspectives on manufacturing efficiency. After graduating from Sydenham College of Commerce and Economics, he had apprenticed with local companies and interned at Kaycee Industries Ltd, where his father was chairman, before joining Bajaj Auto.

The plastic idea wasn't just about material substitution—it was about reimagining what Indian manufacturing could be. "We gave Bajaj Auto the idea of converting the aluminium fan and steel fan covers into plastic, which they accepted. And with that, in 1990, I started supplying plastic moulded components to Bajaj Auto", Tarang would later recall.

That single "yes" from Rahul Bajaj became the foundation stone of Varroc Engineering. But what started as a nephew leveraging family connections would evolve into something far more ambitious—a vision to move beyond captive supply, beyond build-to-print manufacturing, to become a global technology leader in automotive components.

III. Early Years: Building Beyond Bajaj (1990–2000)

Varroc was established by Tarang Jain in 1990 in Aurangabad, not Pune where most automotive suppliers clustered. The choice was deliberate—land was cheaper, labor more available, and critically, Bajaj Auto was setting up operations there. But Aurangabad in 1990 was no industrial paradise. Power cuts were frequent, skilled workers scarce, and the monsoons turned the roads into rivers of mud.

The first factory was modest—a shed with injection molding machines that Tarang had sourced second-hand from Taiwan. The early days were grueling. Tarang would spend eighteen-hour days on the factory floor, troubleshooting machines, training workers who had never seen plastic molding equipment, and driving samples to Bajaj's facility himself when deadlines loomed.

"Around that time, Videocon also happened to come to Aurangabad, and they too gave us some parts to make for their televisions and washing machines". This was Varroc's first diversification—a critical move that demonstrated the company wasn't content being a single-customer supplier. The Videocon parts were different—consumer durables required different tolerances, aesthetics, and durability standards than automotive components. Each new requirement became a learning opportunity.

Between 1992 and 1998, Varroc underwent aggressive product diversification and capacity expansion. The company started electrical and metallic divisions, moving beyond just polymers. The company procured other components businesses from Bajaj such as painted parts, PU foam seats, air filters and mirrors. These, however, were all built-to-print jobs, where Varroc had little design or technological input.

This limitation gnawed at Tarang. Build-to-print meant thin margins, zero intellectual property, and complete dependence on the customer's design capabilities. "This roused Tarang Jain to think beyond a mere build-to-print business and extend his expertise to more stimulating and profitable ventures. 'We decided that we didn't want to do just built-to-print components but also be a proprietary part supplier'".

By 1997, Varroc had expanded beyond Aurangabad, starting polymer manufacturing facilities in Pune and Aurangabad. The Pune facility was strategic—it put Varroc in India's automotive heartland, closer to emerging customers like Tata Motors and Volkswagen's planned India operations.

The late 1990s marked a crucial transition. By 1999, Varroc entered the export domain, supplying to international customers. The first export order—plastic components for a European motorcycle manufacturer—was small, barely worth €50,000. But it represented something larger: validation that an Indian supplier could meet European quality standards.

The turn of the millennium found Varroc at an inflection point. It had grown from a single-product, single-customer operation to a diversified supplier with multiple divisions, multiple locations, and the beginnings of an international footprint. Revenue had crossed ₹100 crore, employment had grown to over 500 people, and most importantly, the company had developed capabilities beyond just manufacturing—it could now participate in design and development.

IV. Technology Partnerships & Capability Building (2000–2010)

The new millennium opened with Tarang Jain standing in a Tokyo boardroom, making his pitch to executives at Mitsuba Corporation. The Japanese were skeptical—why partner with an Indian company that had barely a decade of experience? But Tarang had done his homework. He knew Mitsuba needed a foothold in India's growing two-wheeler market, and Varroc could provide the local manufacturing and relationships they lacked.

In 2001, Varroc expanded capabilities by collaborating with Mitsuba Corporation for automobile parts. The partnership was structured carefully—Mitsuba would provide technology for starter motors and alternators, while Varroc would handle manufacturing and local market development. The Japanese insisted on their legendary quality standards, sending engineers to Aurangabad for months to train Varroc's workforce in concepts like kaizen and poka-yoke.

2005 brought another strategic collaboration, this time with Belgium's Umicore for automotive catalytic converters. The timing was prescient—India was about to implement stricter emission norms, and every two-wheeler would need catalytic converters. The Umicore partnership gave Varroc access to precious metal coating technologies that few Indian companies possessed.

But the real game-changer came in 2007. Tarang had been eyeing European acquisitions for years, studying distressed assets that could provide technology and market access. The opportunity came in the form of IMES, an Italian forging company with operations in Poland. IMES was bleeding money, its European customers concerned about supply continuity. Tarang moved fast, acquiring the company for a fraction of its asset value. Between 2007 and 2010, Varroc acquired IMES, Poland and Italy to strengthen forging business in European markets, off-road and oil drilling industry. The IMES acquisition was transformational—the acquired company had a forging capacity of 110,000 tons per year, giving Varroc instant scale in European markets. "We wanted to enter the passenger car market and this has got us in. In the passenger car market, we are focused on forgings, engine valves where we already have customers like GM and Fiat in Europe", Tarang explained.

The integration wasn't smooth. Polish workers were suspicious of Indian ownership, Italian engineers skeptical about maintaining quality standards. Tarang spent months shuttling between Aurangabad, Warsaw, and Milan, building trust, retaining key talent, and slowly turning the operations profitable.

The company also invested in manufacturing capability for polymers in National Capital Region to cater to OEMs in North India. This was a strategic move to get closer to emerging customers like Maruti Suzuki and Honda's expanding operations in the Delhi-NCR region.

Throughout this period, Varroc was building something less visible but equally crucial—engineering capabilities and R&D centers. The company established technical centers in Pune and Chennai, hiring engineers from IITs and training them in advanced CAD/CAM technologies. These weren't just cost centers; they were investments in moving up the value chain from manufacturer to technology partner.

By 2010, Varroc had transformed from an Indian supplier with international customers to a truly global company with manufacturing and engineering capabilities across continents. Revenue had crossed ₹2,000 crore, the company employed over 3,000 people globally, and critically, Bajaj Auto now represented less than 50% of total revenue—a psychological milestone that marked Varroc's evolution from captive supplier to independent force.

V. The Game-Changing Acquisitions (2011–2012)

Detroit, January 2012. The North American International Auto Show was in full swing, but in a conference room at the Renaissance Center, a different kind of automotive drama was unfolding. Tarang Jain sat across from Visteon executives, finalizing what would become the most transformative deal in Varroc's history.

Visteon, the former parts division of Ford Motor Company, was in distress. Having emerged from bankruptcy in 2010, it was divesting non-core businesses to focus on electronics and interiors. Their global lighting business—with 2011 revenue of $531 million—was on the block. For most Indian companies, this would have been an impossibly large bite. For Tarang, it was the opportunity he'd been waiting for.

But first came 2011, when Varroc acquired European two wheelers lighting organization Tri.O.M. S.p.A. including its R&D center. Tri.O.M wasn't just another forging company—it was a technology leader in high-end motorcycle lighting, supplying to Ducati, BMW Motorrad, and KTM. The acquisition gave Varroc something precious: European design credibility and relationships with premium motorcycle manufacturers.

Then came the Visteon deal. In 2012, Varroc's turnover crossed the US$1 billion mark with the acquisition of Visteon's Lighting Business along with its two R&D centers. The numbers were staggering for an Indian auto component company: $90.5 million for a business generating over half a billion in revenue.

What Varroc acquired was more than just revenue. The deal included manufacturing and engineering facilities in Czech Republic, Mexico, and India, along with 4,200 employees. These weren't just factories—they were state-of-the-art facilities supplying to Ford, Volkswagen, Renault, and other global OEMs. The Czech facility, in particular, was a jewel—located in the heart of European auto manufacturing, with proximity to German luxury car makers.

The R&D centers were equally valuable. One in Plymouth, Michigan—the heart of American automotive engineering—and another in Europe. These centers held 184 patents and employed over 900 engineers working on next-generation lighting technologies including LED systems and adaptive lighting.

But there was more. In 2013, the company expanded its global lighting business by acquiring Visteon's holding in a 50/50 joint venture with Beste Motor Co. Ltd. ("TYC") to manufacture automotive lighting in China, namely Varroc TYC. China was the world's largest and fastest-growing auto market, and this gave Varroc a manufacturing foothold there.

The integration challenge was immense. Varroc was acquiring a business larger than itself, with operations in countries where it had no presence, serving customers it had never worked with, using technologies it was still learning. Tarang assembled a global integration team, bringing in McKinsey consultants and industry veterans to manage the transition.

The cultural challenges were equally daunting. American engineers in Plymouth wondered about working for an Indian company they'd never heard of. Czech workers feared cost-cutting and job losses. Mexican operations worried about investment priorities. Tarang's approach was counter-intuitive—instead of imposing Varroc's way of doing things, he absorbed the best practices from Visteon's operations, essentially using the acquisition to upgrade Varroc's own processes.

By the end of 2012, Varroc had transformed from a $500 million Indian company to a $1.5 billion global Tier-1 supplier. The company was now the sixth-largest automotive exterior lighting manufacturer globally. The acquisition hadn't just added scale—it had fundamentally changed Varroc's position in the global automotive value chain.

VI. Global Expansion & Market Position (2013–2017)

The integration of Visteon's lighting business was like assembling a massive jigsaw puzzle while riding a roller coaster. Each piece—Czech Republic, Mexico, China, India—had its own complexity, its own culture, its own challenges. But by 2013, the picture was starting to come together, and it was impressive.

In the gleaming Varroc Lighting Systems facility in Novy Jicin, Czech Republic, production lines hummed with precision, churning out headlamps for the new Volkswagen Golf. A few thousand miles away in Tepotzotlán, Mexico, workers assembled taillights for the Ford F-150, America's best-selling truck. In China, the newly consolidated Varroc TYC operation was ramping up to serve the exploding Chinese auto market.

2014 brought validation from an unexpected quarter—private equity. PE Investments by Omega TC Holdings and Tata Capital Financial Services injected fresh capital, valuing Varroc at over $2 billion. For Tarang, this wasn't just about money—it was about governance, about preparing Varroc for its next evolution as a public company.

The PE investors brought discipline. Monthly board meetings became rigorous reviews of performance metrics. Quality standards were standardized across global operations. Financial reporting was upgraded to international standards. The family business was becoming an institution.

2015 saw strategic partnerships proliferate. Varroc partnered with Heraeus for catalytic converters, anticipating India's move to stricter emission norms. The Sa-Ba acquisition in Turkey extended Varroc's reach into another fast-growing market. A partnership with Scorpion Automotive brought security products for two-wheelers—an emerging category as vehicle theft became a concern in developing markets.

His clients include Bajaj Auto, Hero, Honda, Ford, the Volkswagen Group, Tesla, Jaguar Land Rover, Fiat-Chrysler and Daimler. The Tesla relationship was particularly noteworthy—Varroc supplied lighting for the Model S and Model X, putting an Indian company at the forefront of the electric vehicle revolution.

The numbers told the story of transformation. The company posted a turnover of ₹8,600 crore in FY15-16 and then achieved double-digit growth in FY 16-17 to touch ₹10,300 crore in sales. Varroc had become the second largest Indian auto component group by consolidated revenue for FY 2017.

But growth brought complexity. Managing operations across time zones, currencies, and cultures was exhausting. Quality issues in one plant could jeopardize relationships globally. A strike in Mexico could impact deliveries to Ford, affecting the relationship in other markets. The company needed systems, processes, and most importantly, people who could think and act globally.

This period also saw the next generation stepping in. Tarang Jain's elder son, Arjun, joined the family business in 2013. He had studied in the US, double majoring in Economics and Political Science at Vassar, a liberal arts college in upstate New York. "I started at Varroc in 2013, in the strategy function", Arjun recalled. Fresh from a stint at Bain & Company in Mumbai, he brought modern consulting frameworks to a company that had grown through entrepreneurial instinct.

The global expansion wasn't just about geography—it was about capability. Varroc was no longer just manufacturing parts; it was co-developing products with OEMs, participating in platform development from concept stage, and even developing proprietary technologies. The company had seven R&D centers employing over 900 engineers, filing dozens of patents annually.

By 2017, About 70 per cent of Tarang Jain's business was abroad and the rest in India. Varroc had successfully transformed from an Indian company with international operations to a truly global company that happened to be headquartered in India.

VII. IPO & Public Market Journey (2018–Present)

The summer of 2018 was particularly hot in Mumbai, but inside the air-conditioned conference rooms of the Bombay Stock Exchange, the atmosphere was electric. After nearly three decades as a private company, Varroc was about to test public market appetite for its global ambitions.

Varroc Engineering IPO is a bookbuilding of Rs 1,945.77 crores. Varroc Engineering IPO bidding started from June 26, 2018 and ended on June 28, 2018. Varroc Engineering IPO price band is set at ₹967 per share. The pricing was aggressive—at 29 times earnings compared to the industry average of 42—but the Varroc name and its global footprint commanded premium valuations.

The IPO roadshows were grueling. Tarang and his team crisscrossed from Mumbai to Singapore, London to New York, telling Varroc's story to institutional investors. The pitch was compelling: a global Tier-1 supplier with 70% revenues from international markets, relationships with every major OEM, and positioned for the electric vehicle transition.

The shares got listed on BSE, NSE on July 6, 2018. The stock opened at ₹1,076, a 11% premium to the issue price. VARROC reached its all-time high on Sep 3, 2018 with the price of 1,178.70 INR. For a brief moment, Varroc was valued at over ₹18,000 crore, making Tarang Jain and his family billionaires on paper.

But public markets are unforgiving masters. The initial euphoria gave way to reality as global headwinds gathered. The automotive industry was entering a downturn, electric vehicles were disrupting traditional suppliers, and then came COVID-19. The all-time low was 120.00 INR and was reached on Apr 3, 2020, a devastating 90% decline from the peak. The post-IPO journey has been marked by volatility. The company has delivered a poor sales growth of -6.02% over past five years. Company has a low return on equity of -4.63% over last 3 years. The automotive industry's structural shifts—electrification, shared mobility, autonomous driving—created uncertainty about traditional suppliers' future.

Yet recent quarters show signs of recovery. Varroc Engineering Limited reported a strong financial performance for the quarter ended June 30, 2025 (Q1 FY26), with net profit surging to ₹107.4 crore, marking a 215% increase from ₹34.1 crore in the same quarter last year. Revenue from operations stood at ₹2,027.5 crore, up from ₹1,893.8 crore in Q1 FY25, reflecting healthy growth in topline.

Post-IPO, the promoter and promoter group held approximately 75% of outstanding equity shares, demonstrating the family's continued confidence in the business despite market volatility. The public market journey, while challenging, has brought discipline—quarterly earnings calls, analyst scrutiny, and pressure for consistent performance that has made Varroc a more professional organization.

The COVID-19 pandemic tested Varroc like never before. Global auto production collapsed, OEMs cancelled orders, and liquidity became paramount. But the crisis also accelerated trends—the shift to EVs, the importance of supply chain resilience, the need for digital capabilities—that Varroc had been preparing for.

VIII. Modern Operations & Business Segments

Walk into Varroc's state-of-the-art facility in Chennai today, and you're witnessing the culmination of three decades of evolution. Robots dance in synchronized precision, welding components with tolerances measured in microns. In the design center next door, engineers manipulate 3D holographic models of next-generation headlamps, simulating aerodynamics and thermal management. This is modern Varroc—a far cry from the shed in Aurangabad where it all began.

Varroc Lighting Systems (VLS), headquartered out of Plymouth, Michigan, is a supplier of exterior lighting for passenger cars and commercial vehicles. The division has six manufacturing plants across North American, European, and Asian countries and six Engineering centers in the Czech Republic, France, China, Germany, Poland, Mexico, Romania and India.

The business architecture reflects strategic evolution. Triom Two-Wheeler Lighting, the lighting system arm of Varroc for the two-wheeler industry, develops electronics and lighting solutions for the automotive market in India and Europe. The division produces high quality two-wheeler lighting systems. It has four manufacturing plants – two in Europe, one in Vietnam, and one in Mexico – as well as an engineering center in Italy.

The polymer division remains the backbone of Indian operations—now the largest polymer solution provider to two-wheeler industry in India. What started with plastic fan covers has evolved into complex multi-material assemblies integrating electronics, sensors, and even smart features. The division operates ten plants across India, each specializing in different polymer technologies—injection molding, blow molding, vacuum forming, and painting.

Varroc's Electrical division offers complete solutions in electrical components and assemblies for the two, three, four wheeler, off-road as well as commercial vehicles segments. The product portfolio spans from simple switches to complex electronic control units, from traditional alternators to EV traction motors and battery management systems.

The numbers tell the scale story: 36 manufacturing facilities, 7 R&D centres, over 7,000 employees across 7 countries. But numbers don't capture the complexity of managing this global operation. Each facility must meet local customer requirements while maintaining global quality standards. Each R&D center must contribute to global innovation while addressing regional market needs.

Product development has become increasingly sophisticated. Where once Varroc waited for customer specifications, today it co-develops products from concept stage. The company's engineers sit in OEM design centers, participating in vehicle platform development years before production begins. This forward integration has made Varroc indispensable to its customers—not just a supplier but a technology partner.

The customer portfolio reads like a who's who of global automotive: Two-wheeler giants like Bajaj, Hero, Honda; passenger car majors like Volkswagen Group, Ford, Stellantis; luxury brands like Jaguar Land Rover, Tesla; commercial vehicle leaders like Daimler, Volvo. Each relationship carefully cultivated over years, each requiring different capabilities, different approaches.

Quality has become religion. Zero-defect programs, Six Sigma initiatives, Industry 4.0 implementations—Varroc has embraced them all. The company's quality metrics rival Japanese suppliers—PPM (parts per million) defect rates in single digits, on-time delivery above 99%, customer satisfaction scores consistently above 90%.

But modern operations aren't just about manufacturing excellence. They're about anticipating the future. Varroc's plants are increasingly flexible, capable of switching between ICE and EV components. The workforce is being reskilled—mechanical engineers learning electronics, production workers becoming robot programmers.

The supply chain has been reimagined post-COVID. Dual sourcing for critical components, regional supply networks to reduce dependence on single countries, digitization for real-time visibility. What was once managed on Excel sheets is now orchestrated through AI-powered supply chain platforms predicting disruptions before they occur.

IX. Technology & Future Mobility

The conference room at Varroc's Pune R&D center feels more like a Silicon Valley startup than a traditional auto supplier. Young engineers debate neural network architectures for computer vision. A prototype autonomous emergency braking system sits on a test bench. Screens display real-time data from connected vehicles across India. This is Varroc's bet on the future—becoming an auto technology company, not just a components manufacturer.

The transformation began with a seemingly small acquisition. 2019 Acquired CarIQ, a leading Telematics solution provider. CarIQ wasn't a traditional auto supplier—it was a cloud technology company providing connected car solutions. The acquisition signaled Varroc's intent to play in the software-defined vehicle era.

The renamed Varroc Connect platform represents a leap into the digital realm. Cloud-connected telematics that can track vehicle health, driver behavior, predictive maintenance needs. For two-wheeler manufacturers, this means offering services like theft protection, crash detection, and usage-based insurance—transforming a mechanical product into a connected service platform.

2022 Extension of product portfolio to ADAS, Driver Monitoring Systems, and Video Telematics. ADAS (Advanced Driver Assistance Systems) puts Varroc at the forefront of vehicle safety technology. The company's DMS (Driver Monitoring Systems) use infrared cameras and AI to detect driver drowsiness, distraction, even emotional state—critical for semi-autonomous vehicles where human attention is still required.

The EV transition presents both threat and opportunity. Traditional products like catalytic converters and engine components face obsolescence. But 2022 Began localized production of 2-Wheeler & 3-Wheeler EV components in India. Varroc now manufactures traction motors, DC-DC converters, battery management systems—the building blocks of electric vehicles.

R&D investments tell the commitment story—3% of total revenue, among the highest in Indian auto component industry. The money flows into next-generation technologies: solid-state lighting using OLEDs, LiDAR integration for autonomous vehicles, V2X communication systems for connected infrastructure.

The innovation isn't happening in isolation. Partnerships with startups bring agility—computer vision algorithms from Israeli companies, battery technology from Korean firms, software platforms from Silicon Valley. Joint development programs with universities—IIT Bombay for materials science, University of Michigan for autonomous systems—keep Varroc at the cutting edge.

Patents have become a key metric—from a handful in 2010 to over 200 today. But more important than quantity is the nature of innovation. Varroc's patents increasingly cover software algorithms, system architectures, and user experiences—not just mechanical designs. This shift from hardware to software IP reflects the industry's transformation.

The challenge is managing this transition while maintaining current business. ICE vehicles will dominate for another decade, especially in emerging markets. Varroc must excel at both—producing millions of traditional components while developing futuristic technologies. It's like rebuilding an aircraft while flying.

Talent has become the critical constraint. Varroc now recruits from IITs and NITs, competing with IT companies for software engineers. The company has established innovation labs in Bangalore and Pune—startup-like environments where young engineers can experiment without corporate constraints.

The manufacturing footprint is evolving too. New facilities are designed for flexibility—production lines that can switch between EV and ICE components, modular layouts that can accommodate new technologies, digital twins that simulate production before physical implementation.

X. Playbook: Business & Investing Lessons

The Varroc story offers a masterclass in strategic evolution, each phase teaching distinct lessons about building a global business from emerging market roots.

The Captive Supplier Evolution Model

Most auto component companies in India remain trapped as captive suppliers—dependent on single customers, competing on cost, with minimal bargaining power. Varroc's journey from Bajaj's captive supplier to global Tier-1 demonstrates the pathway out: start with operational excellence to earn trust, use cash flows to build capabilities, then leverage those capabilities to diversify customers and geographies. The key insight: don't abandon your anchor customer too quickly—use their volume to fund your independence.

Family Business Dynamics: Leveraging Connections While Building Independence

The Bajaj connection opened doors, but Tarang was careful not to become dependent on it. By 1999, he was already exporting. By 2010, Bajaj represented less than 50% of revenue. By 2017, less than 30%. This gradual weaning was deliberate—maintaining the relationship while reducing dependence. The lesson: family connections are launching pads, not landing strips.

Strategic M&A: The Visteon Acquisition as Transformational Deal

Most Indian companies make safe, small acquisitions. Tarang bet the company on Visteon's lighting business—acquiring a company with revenue larger than Varroc itself. But the genius wasn't in the size but the timing and structure. Visteon was distressed, giving Varroc negotiating leverage. The business came with customers, technology, and global footprint—everything Varroc needed to leapfrog decades of organic growth. The lesson: transformational M&A requires courage, but distressed situations offer asymmetric risk-reward.

Geographic Diversification Strategy

Varroc didn't just export from India—it manufactured locally in target markets. The Czech facility served European customers who wanted JIT delivery. The Mexico plant addressed NAFTA requirements. The China JV provided market access in a protected economy. This "in the market, for the market" approach meant higher capital requirements but deeper customer relationships. Today, 70% of revenue comes from outside India—insulation from any single market's cyclicality.

Managing Cyclical Automotive Industry

Auto is brutally cyclical—boom periods followed by devastating downturns. Varroc's approach: diversify across vehicle segments (two-wheelers, passenger cars, commercial vehicles), geographies (developed and emerging markets), and technologies (ICE and EV). When European car sales collapsed in 2008, Indian two-wheelers boomed. When COVID hit passenger vehicles, commercial vehicles for e-commerce thrived. Portfolio diversification isn't just theory—it's survival.

Corporate Governance and Sustainability Focus

The 2014 PE investment and 2018 IPO forced governance upgrades—independent directors, audit committees, transparency in related party transactions. Initially seen as compliance burden, these became competitive advantages. Global OEMs prefer suppliers with institutional governance. ESG metrics—carbon footprint, water usage, social responsibility—have become order qualifiers. Varroc's early adoption positioned it ahead of peers.

Balancing OEM Relationships vs. Independence

The eternal supplier dilemma: OEMs want dedicated capacity and exclusive technology but won't guarantee volumes. Varroc's solution: segment customers and products. Commodity products like plastic parts—supplied to everyone. Proprietary technology like lighting systems—exclusive arrangements with strategic customers. Different customers, different strategies. With Volkswagen, Varroc is a system integrator. With Hero, a volume supplier. With Tesla, a technology partner.

The playbook isn't without flaws. The company's recent financial performance shows the challenges of this model—high capital intensity, margin pressure from OEMs, technology transition risks. But the strategic framework—evolve from supplier to partner, leverage M&A for capability building, maintain portfolio diversification—remains sound.

XI. Analysis & Bear vs. Bull Case

The investment case for Varroc presents a fascinating dichotomy—compelling strategic position undermined by recent financial performance, global footprint offset by execution challenges, technology capabilities shadowed by industry disruption risks.

Bull Case: The Strategic Moat

Start with ownership. Tarang Jain (born 1962/1963) is an Indian billionaire businessman, the CEO and 86% owner of Varroc, an Indian two- and four-wheeler parts manufacturer. As of October 9, 2024, Anurang Jain and his family were ranked 88th on Forbes' list of India's 100 richest individuals, with a net worth of US$3.65 billion. This isn't a professional manager optimizing quarterly earnings—it's an owner-operator with skin in the game, thinking in decades not quarters.

The global Tier-1 supplier status is hard-won and harder to replicate. The company's Global Lighting Business, which focuses on the design, manufacture, and supply of exterior lighting for passenger vehicles, is the sixth-largest tier-1 automotive exterior lighting manufacturer globally and one of the top three independent exterior lighting players (by market share in 2016). In automotive, supplier relationships are sticky—switching costs are high, validation periods long, trust earned over decades.

Customer diversification provides resilience. From two-wheelers to passenger cars, from Bajaj to BMW, from India to Europe—Varroc isn't dependent on any single customer, segment, or geography. When Indian auto sales slumped, European operations provided cushion. When ICE faces headwinds, EV components offer growth.

The technology transition is an opportunity disguised as threat. Yes, catalytic converters will disappear. But EVs need more sophisticated lighting (to compensate for silent operation), more electronics (battery management, power electronics), more software (connected services, ADAS). Varroc's early investments in these areas—CarIQ acquisition, ADAS development, EV component localization—position it ahead of traditional suppliers.

VARROC ENGINEERING LTD. EBITDA is 7.93 B INR, and current EBITDA margin is 8.55%. While margins have compressed, they remain positive and above many peers. The company generates cash, funds R&D, and maintains dividend payments—signs of fundamental business health.

Bear Case: The Performance Reality

The numbers paint a sobering picture. The company has delivered a poor sales growth of -6.02% over past five years. Company has a low return on equity of -4.63% over last 3 years. For a company in supposedly high-growth emerging markets, serving supposedly booming EV transition, these numbers disappoint.

The stock performance reflects market skepticism. VARROC reached its all-time high on Sep 3, 2018 with the price of 1,178.70 INR, and its all-time low was 120.00 INR and was reached on Apr 3, 2020. Even after recovery, the stock trades well below IPO highs, suggesting fundamental concerns beyond market volatility.

Auto industry disruption is existential. EVs don't just replace engines with motors—they fundamentally restructure the supply chain. Tesla manufactures many components in-house. Chinese EV makers like BYD are vertically integrated. The Tier-1 supplier model itself faces questioning.

Margin pressure is structural, not cyclical. OEMs face their own profitability challenges and squeeze suppliers. New Chinese competitors offer similar quality at lower prices. Technology components require higher R&D spending but don't necessarily command premium pricing. The economics of the business are deteriorating.

High debt levels constrain flexibility. Capital-intensive acquisitions and expansions have loaded the balance sheet. In a downturn, fixed costs and interest payments could pressure cash flows. The company lacks the financial flexibility to make transformative investments or acquisitions.

Geographic exposure cuts both ways. Yes, diversification provides resilience. But it also means exposure to multiple challenges—European recession, Chinese competition, Indian market volatility. Managing this complexity requires exceptional execution, which recent performance questions.

The Verdict: Transformation in Progress

Varroc stands at an inflection point. The old model—labor arbitrage from India, supplying mechanical components to established OEMs—is dying. The new model—technology-driven, software-enabled, EV-focused—is emerging but unproven.

Recent quarterly performance offers hope. The 215% profit growth in Q1 FY26, while from a low base, suggests operational improvements taking hold. New business wins of ₹2.9 billion indicate customer confidence. Debt reduction of ₹3 billion shows financial discipline.

The investment case ultimately depends on execution. Can Varroc successfully navigate the EV transition? Can it maintain relevance as vehicles become computers on wheels? Can it generate returns that justify the risk? The strategic pieces are in place—global footprint, customer relationships, technology capabilities. But strategy without execution is hallucination.

For fundamental investors, Varroc presents a classic value-or-trap dilemma. Trading at distressed valuations despite strategic assets, improving operations despite industry headwinds, investing in future despite current challenges. The next 24 months will likely determine whether this is a turnaround story or a value trap.

XII. Epilogue & "If We Were CEOs"

Standing in his office overlooking the Aurangabad factory where it all began, Tarang Jain faces the most critical decisions of his three-decade journey. The auto industry is undergoing its greatest transformation since Henry Ford's assembly line. Every assumption, every business model, every competitive advantage is being questioned.

If we were running Varroc today, the strategic priorities would be clear but execution would be complex:

Priority 1: Radical Portfolio Simplification

Varroc tries to be everything to everyone—polymers to electronics, two-wheelers to commercial vehicles, India to Mexico. This complexity creates diseconomies of scale. We would identify core businesses with sustainable competitive advantages—likely lighting systems and EV components—and divest or shutdown the rest. Yes, revenue would shrink initially, but margins and returns would improve.

Priority 2: Double Down on Software and Services

Hardware is becoming commoditized; software is where value creation happens. The CarIQ acquisition was smart but subscale. We would acquire a larger telematics/software company, even if it meant taking on debt or diluting equity. The goal: recurring revenue streams from connected services, predictive maintenance, usage-based insurance. Transform from a components supplier to a mobility solutions provider.

Priority 3: The China Question

China is both the largest auto market and the most competitive. Varroc's JV gives market access but limited control. We would either commit fully—establishing wholly-owned R&D and manufacturing—or exit completely. Half-measures don't work in China. Given the geopolitical tensions and local competition, exit might be the prudent choice, redeploying capital to India and other emerging markets.

Priority 4: EV-Native Manufacturing

Current facilities are retrofitted for EVs—suboptimal. We would establish a greenfield EV-components facility, designed from ground up for battery systems, power electronics, and electric drivetrains. Location would be strategic—perhaps Tamil Nadu near the emerging EV cluster, or Gujarat near the battery plants. This would signal commitment to EV transition and attract new customers.

Priority 5: Partnerships Over Independence

The old model of independent Tier-1 suppliers is ending. We would seek strategic partnerships—potentially giving an OEM minority stake in exchange for guaranteed volumes and technology transfer. Volkswagen or Stellantis, facing their own EV transitions, might value a committed partner in India. This would reduce independence but ensure survival.

Priority 6: Fix the Balance Sheet

Current debt levels limit strategic flexibility. We would pursue a rights issue, even at current depressed valuations, to deleverage the balance sheet. Use the proceeds to pay down debt and fund the EV transition. Dilution is painful but bankruptcy is fatal.

Priority 7: Talent Revolution

The current workforce, skilled in mechanical engineering and traditional manufacturing, isn't equipped for the software-defined future. We would establish a Varroc Technology Center in Bangalore, hiring software engineers from India's IT industry. Create a dual-track organization—traditional business run from Aurangabad, new business from Bangalore—until the transformation is complete.

The path forward isn't easy. The Q1 FY26 results show improvement—revenue of ₹2,027 crore, profit of ₹107 crore—but the industry is moving faster than Varroc's transformation. The next 18-24 months are critical. Either Varroc emerges as a technology-enabled, EV-focused, software-savvy supplier, or it becomes another casualty of industry disruption.

The irony is striking. Varroc began by replacing metal with plastic—a material transition that seemed radical in 1990. Today, it faces another transition—from mechanical to electrical, from hardware to software, from products to services. The question isn't whether Varroc can survive this transition, but whether it can thrive through it.

Looking ahead, the India opportunity remains compelling. Two-wheeler electrification is accelerating. The government's PLI schemes incentivize local manufacturing. Global OEMs are establishing India as an export hub. Varroc, with its three-decade heritage, global capabilities, and local manufacturing, is well-positioned—if it can execute the transformation.

The Varroc story isn't finished. From a nephew's idea about plastic fan covers to a global automotive supplier, from Aurangabad to Plymouth, from family business to public company—each transformation seemed impossible until it was done. The next transformation—to a technology company that happens to make auto components—might be the most challenging yet. But if history is any guide, betting against Tarang Jain and Varroc might be premature.

The ultimate question for investors isn't whether Varroc was a great company—it clearly was. Or whether it's facing challenges—it clearly is. The question is whether it can reinvent itself once more, as it has done repeatedly over three decades. The answer will determine whether Varroc becomes a case study in transformation or a cautionary tale of disruption.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube