Utkarsh Small Finance Bank: The Soul of the Heartland

I. Introduction & The SFB Thesis

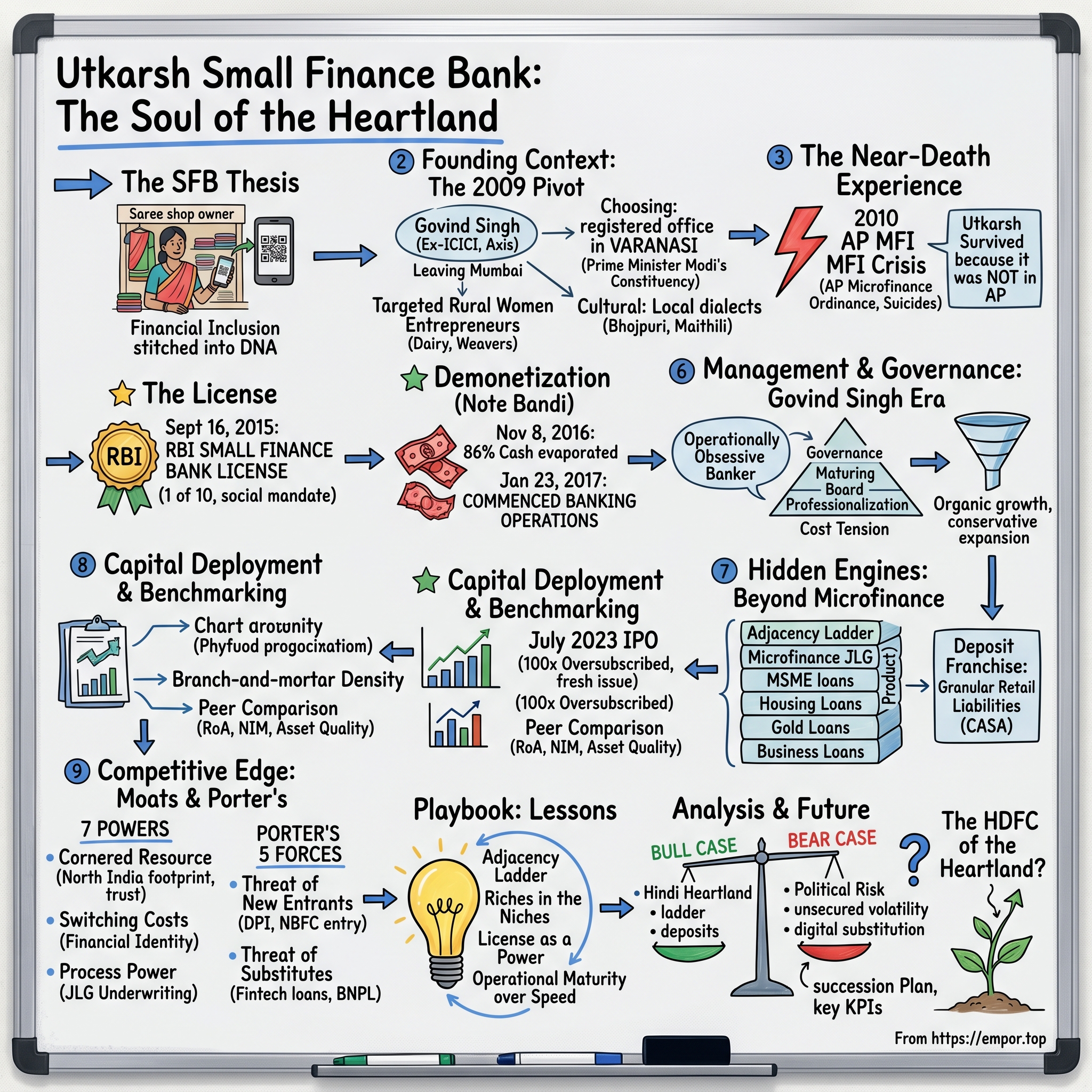

Picture a Tuesday morning in Varanasi वाराणसी. The Ganges is exhaling its slow, silver mist. On a narrow lane behind Kashi Vishwanath temple, a saree-shop owner — three generations into the same one-room store — is plugging in a QR-code stand. She has never owned a credit card. She has never set foot inside a glass-and-marble bank lobby in Mumbai. But on her phone, she has a savings account, a working-capital loan that funded her latest wholesale trip to Surat, and a recurring deposit she opened the day her daughter was born. Every one of those products comes from a bank that did not exist as a bank a decade ago. It carries a Sanskrit name that means "elevation" or "rising progress": Utkarsh उत्कर्ष.

This is the part of India that most foreign capital, and frankly most of corporate Indian banking, has historically refused to underwrite. Mumbai's storied private-sector lenders fight over the top 1% of India — the salaried tech worker, the listed corporate, the affluent NRI. HDFC Bank, ICICI Bank, Kotak Mahindra Bank have spent three decades engineering their portfolios around that customer. The result is one of the most profitable banking ecosystems in the world — and one of the most geographically lopsided. South India and the metros vacuum up capital. The Hindi heartland of Uttar Pradesh and Bihar, home to more than 350 million people, gets the leftovers.

Utkarsh Small Finance Bank was built on the conviction that the leftovers were the opportunity. It is one of ten institutions to whom the Reserve Bank of India handed something extraordinarily rare in 2015 — a लघु वित्त बैंक (Small Finance Bank) license. The SFB experiment, formalized under RBI's Master Direction on Small Finance Banks, is a regulatory invention with no real analog in global banking1. It is a full-scale commercial bank, with the right to accept retail deposits, issue debit cards, run a treasury, and underwrite the entire spectrum of lending — but with a binding social mandate. At least 75% of net credit must flow to "priority sectors," and at least 50% of the loan book must be in tickets smaller than ₹25 lakh. In English: the regulator engineered a bank that is commercially structured but socially constrained, with capital efficiency on one side and financial inclusion stitched into its DNA on the other.

This is the story of how a former ICICI and Axis Bank executive walked away from corner-office Mumbai banking, set up shop in a Tier-3 city most international investors could not find on a map, survived two near-extinction events that wiped out half the Indian microfinance industry, talked the RBI into one of the most coveted licenses in modern Indian finance, and — in 2023 — pulled off one of the most oversubscribed IPOs of the cycle2. It is also the story of an investment debate that genuinely splits sophisticated investors: is Utkarsh the next HDFC Bank of the heartland, or is it a leveraged bet on the most politically volatile geography in India?

We are going to walk through twenty years — from a single microfinance office in Varanasi in 2009 to a public-market institution whose loan book today stretches from बिहार Bihar to Maharashtra. We will dwell on the moments where the company nearly didn't survive, on the founder whose temperament shaped every credit decision, on the hidden product engines that the market still misunderstands, and on the brutal Porter's-and-7-Powers math of why a Mumbai bank cannot simply parachute into rural UP and replicate this. By the end, you'll understand not only Utkarsh but the entire SFB category — and why "small" might be one of the most misleading adjectives in Indian finance.

II. Founding Context: The 2009 Pivot

The standard origin myth of Indian microfinance is a Southern one. It begins in Andhra Pradesh, where SKS Microfinance was scaling at a rate that drew global venture capital and a celebratory 2010 IPO. It ran through Tamil Nadu, where Equitas was building. It touched Karnataka, where Ujjivan and CreditAccess Grameen were planting flags. The geography made sense. Self-help groups had been pioneered in the South. Women's literacy was higher. State governments were ideologically aligned with NGO-led credit. And the operational logistics — paved roads, cellular coverage, reliable branch staffing — were simpler than in any northern state.

Govind Singh looked at this consensus and went the other way.

By the late 2000s, Singh had spent more than two decades inside India's most prestigious financial institutions. UTI in the 1980s, when it was still the country's mutual-fund monopoly. ICICI Bank during the explosive Kamath-era expansion that transformed it from a development institution into India's most aggressive private-sector lender. Axis Bank, where he ran rural and microfinance verticals during the period when private banks first started taking priority-sector seriously as a profit center, not a regulatory tax. He had seen, from the executive corridors of Mumbai, exactly how Indian banks made money — and exactly which 600 million people they refused to underwrite3.

When he left in 2009 to found what was then called Utkarsh Micro Finance Private Limited, he made three contrarian bets simultaneously. The first was geographic: he set up the registered office not in Mumbai or Bengaluru but in Varanasi2 — Prime Minister Modi's future parliamentary constituency, a city whose name is older than most countries, and a place that in 2009 had a banking penetration rate that international development economists would have classified as "frontier market." The second was demographic: instead of chasing the educated salaried borrower, he targeted the rural and peri-urban woman entrepreneur — the dairy farmer with two buffaloes, the saree weaver running a four-loom shed, the kirana shop owner serving 80 families. The third was cultural: he hired loan officers locally, in the dialects that actually move credit decisions in UP and Bihar — Bhojpuri, Maithili, Awadhi — long before anyone in Mumbai had heard the phrase "vernacular banking."

To anyone running a McKinsey-style deck, this was insanity. The cow belt — पिछड़ा क्षेत्र, the so-called "backward belt" — was synonymous with bad infrastructure, political loan-waiver risk, low female literacy, and the kind of cash-economy opacity that made credit underwriting feel like astrology. Most microfinance VCs were stating outright that they would not deploy capital north of Hyderabad.

What Singh saw was the inverse picture. He saw an "unbanked ocean" with no serious competition. The South was getting crowded; MFIs were stepping on each other in Andhra villages, lending to the same women, ratcheting up debt loads. The North was empty — not because the demand wasn't there, but because no one had been patient enough to build the local infrastructure. In a Moneycontrol interview years later, he framed it as a temperament question more than a strategy question: the South was an "auction," the North was a "build." He preferred to build[^4].

The early capital raises were brutal. Most domestic VCs passed. But a small, increasingly impressive cohort of impact-tilted private equity investors — names like Aavishkaar, CDC Group (the UK development finance institution), International Finance Corporation (IFC), and later Norway's Norfund and the Dutch FMO — began deploying capital into the Utkarsh holding entity, eventually known as Utkarsh CoreInvest Limited (UCL)[^5]. By the early 2010s, Utkarsh was demonstrating something rare: that a North Indian rural credit book could be underwritten with collection efficiencies above 98%, that women borrowers in Mau and Ghazipur and Bhagalpur paid back as reliably as borrowers in Tamil Nadu, and that the "cow belt risk premium" was largely a Mumbai prejudice, not a credit reality.

Then, in late 2010, the entire industry caught fire.

III. The Near-Death Experience & The License

October 2010. Hyderabad. The state government of Andhra Pradesh — alarmed by rising reports of borrower suicides linked to aggressive microfinance collection — passed an ordinance that effectively halted all MFI lending in the state4. Within weeks, repayment rates across Andhra collapsed from the high 90s to single digits. Lenders couldn't collect. Politicians went on television telling borrowers they had no obligation to pay. The largest MFIs in the country — many of them backed by global venture capital, many with concentration exposure of 50% or more to AP — saw their portfolios implode. SKS Microfinance, which had IPO'd just three months earlier as the poster child of for-profit microfinance, watched its stock price disintegrate. Several MFIs went into restructuring. The industry's access to bank funding froze. International investors fled.

For an industry barely a decade old in its modern form, the AP MFI Crisis was an extinction event. The casualty count was severe enough that the RBI eventually created a new regulatory category — NBFC-MFI — with hard caps on margins, ticket sizes, and concentration risk. The Malegam Committee's recommendations, published in 2011, became the new operating constitution for the sector[^7].

Utkarsh survived for one reason: it wasn't in Andhra Pradesh.

The geographic obstinance that looked like a strategic error in 2009 — staying out of the South, refusing to chase the easy growth — turned out to be the company's single most important risk-management decision. While the largest MFIs in India were spending 2011 and 2012 negotiating with state governments and rebuilding from rubble, Utkarsh was quietly compounding in UP and Bihar, deepening relationships with women's joint-liability groups, refining its collection cadence, and — crucially — building the only thing that mattered to a future banking regulator: a track record of sober, conservative, repeatable execution in a difficult geography.

That track record paid off on September 16, 2015. On that day, the RBI announced the recipients of its first batch of Small Finance Bank licenses — ten institutions, selected from seventy-two applicants1. The applicant pool included some of the most storied names in Indian non-bank finance. The winners' list read like a quiet revolution: Ujjivan, Equitas, AU Financiers, Janalakshmi, Suryoday, ESAF, Capital, Disha, Fincare — and Utkarsh.

What had Utkarsh shown the RBI? Three things. First, a liability-side strategy that wasn't dependent on bank borrowing — the company had been quietly developing a deposit and CASA capability inside the holding structure before the license was even granted. Second, governance maturity — its board already included independent directors with banking and audit pedigree, not just impact-PE nominees. Third, concentration discipline — the lender had specifically refused to chase the same Andhra growth that had nearly killed the industry. Singh's conservatism, often criticized inside Utkarsh as a brake on growth, suddenly looked like the most valuable asset in the company.

Then, fifteen months later, the second extinction event arrived.

November 8, 2016. 8:15 PM. Prime Minister Modi appeared on national television and announced that ₹500 and ₹1000 notes — accounting for approximately 86% of the cash in circulation in India — would cease to be legal tender at midnight5. नोटबंदी Demonetization. For an institution that was, at that moment, in the middle of converting from an NBFC-MFI into a fully regulated commercial bank, the timing was almost cosmic in its cruelty. The microfinance industry runs on cash. Loan officers collect cash in villages. Borrowers repay in cash. Women save in cash. Overnight, the working capital of literally every customer in Utkarsh's book evaporated.

Collection efficiency, which had been above 99% for years, dropped to the low 80s. Repayment cycles stretched. The entire MFI sector saw NPAs surge through 2017. Several smaller MFIs never recovered.

Utkarsh did. On January 23, 2017, just over two months after demonetization, Utkarsh Small Finance Bank Limited formally commenced banking operations2. It was, by any objective measure, the worst possible moment in modern Indian history to open a new bank. But the conversion was also the company's transformation — from an NBFC drawing wholesale debt to fund onward lending, into a regulated bank that could now build the one liability that compounds forever: low-cost retail deposits.

That conversion is among the hardest operational migrations in financial services. You don't just change a logo. You re-platform a core banking system. You hire treasury, compliance, vigilance, IT-security, and KYC teams that didn't exist before. You re-write every loan agreement, every customer-onboarding flow, every cash-movement protocol to comply with full RBI banking regulation rather than the lighter NBFC framework. You teach village-level loan officers, who had spent their careers running joint-liability group meetings under banyan trees, to also open passbook savings accounts and explain RuPay debit cards in Bhojpuri. The cultural and technical lift was enormous. The fact that Utkarsh executed it during demonetization is, frankly, the single most underrated operational achievement in the company's history.

IV. Management & Governance: The Govind Singh Era

You can usually read the temperament of a CEO in the temperature of their head office. In Govind Singh's Varanasi office, there is no marble lobby, no automated reception, no Bloomberg terminal facing the door. There is a desk, a chair, and — by the consistent recollection of analysts and journalists who have visited — an unusually large amount of paper. Singh is, by every account, an operationally obsessive banker, the kind who can recite branch-level collection statistics from memory and who personally signs off on credit policy changes well below the threshold that any of his Mumbai peers would bother with.

His leadership style traces directly to his career path. Two decades at ICICI Bank during the Kamath build-out taught him scale and systems[^4]. A stint heading rural and microfinance at Axis Bank taught him the operational physics of small-ticket credit in places where the cost of one bad loan is not the principal — it is the entire community's willingness to ever borrow from you again. Multiple years at UTI, before the demerger, taught him the slow patience of institutional asset management. When he set up Utkarsh, he carried all three sensibilities with him, and the consequence is a culture inside the bank that is unusually conservative for the SFB peer set. AU Small Finance Bank, by comparison, ran hard on vehicle finance and is now aggressively building unsecured retail. Equitas Small Finance Bank has been an early experimenter in personal loans and credit cards. Utkarsh, under Singh, has consistently been the SFB that grows slowest, provisions earliest, and writes the most boring annual report.

This is not an accident. It is an investment posture. And the shareholding structure reinforces it.

The promoter of Utkarsh Small Finance Bank Limited is उत्कर्ष कोरइन्वेस्ट Utkarsh CoreInvest Limited (UCL), a non-operating holding company that itself houses the original impact-PE shareholders from the pre-banking era[^5]. As a regulatory requirement under the SFB licensing framework, the promoter was required to hold a minimum stake at the time of bank formation, and a defined glide path to reduce that stake over time. Utkarsh has been steadily walking down that path, with the IPO in 2023 serving as a major milestone in the promoter-dilution journey. The result is a board and ownership structure that is gradually transitioning from "founder + impact PE" to "diversified institutional and retail" — the same evolution that AU and Equitas underwent before it. Singh remains MD and CEO, the operational anchor; but the board increasingly carries the kind of independent directors — career bankers, ex-regulators, audit specialists — that the RBI explicitly favors in regulated lenders.

Compensation philosophy is where the geographic strategy reveals itself most clearly. Indian banking historically prices talent in Mumbai terms. A senior credit officer in BKC commands a multiple of what the same person would earn in Lucknow, even when the actual portfolio risk being managed in Lucknow is materially harder. Utkarsh has had to design an HR system that does the opposite of what every Mumbai bank does: it has to pay a premium for branch managers and credit officers in Tier 3 and Tier 4 towns — Gorakhpur, Muzaffarpur, Patna, Allahabad — because those are the places where individual underwriting quality determines book quality. Meanwhile, in its Mumbai and Bengaluru tech-and-treasury operations, it competes for talent in a market where it is, frankly, not the highest bidder. That tension — paying up for rural execution and paying competitively for urban infrastructure — is the operational tax of being a heartland bank, and it shows up in the cost-to-income ratio whenever you compare Utkarsh to its more metro-tilted peers.

Underneath Singh is a deliberately deep bench of vertical heads — the MSME chief, the housing finance head, the treasury head, the inclusive-banking head. None of them are celebrities. None of them have the personal-brand visibility of, say, a Sanjay Agarwal at AU. That is intentional. Singh has run Utkarsh more like a long-duration mutual fund — quiet, process-driven, methodical — than like a charismatic founder-led growth story. Whether that style scales beyond him is the single most important governance question in the company, and we will come back to it.

V. Hidden Engines: Beyond Microfinance

If you ask a generalist investor in Mumbai or Singapore what Utkarsh Small Finance Bank does, the answer you will get nine times out of ten is: "microfinance." This is the consensus shorthand. It is also, increasingly, wrong.

The truth that the market has been slow to underwrite is that Utkarsh has spent the last five years quietly metamorphosing into something much more interesting than a glorified MFI: a regional commercial bank with a microfinance origin story. The shape of the loan book has been changing — slowly enough that quarterly headlines miss it, but persistently enough that the trajectory is unmistakable. Joint Liability Group (JLG) microfinance — the original product, the one that put Govind Singh on the map — still anchors a meaningful share of the book. But around that anchor, the bank has been building a portfolio of secured and semi-secured products: MSME loans, housing loans, gold loans, business loans against property, and increasingly, commercial vehicle finance.

The MSME book is the most important hidden engine. India has somewhere on the order of 60 million MSMEs — सूक्ष्म, लघु और मध्यम उद्यम Micro, Small and Medium Enterprises — and the credit gap to that sector is one of the largest unmet financing opportunities on the planet. The Reserve Bank's own studies have repeatedly identified MSME under-financing as a structural drag on Indian GDP. Public-sector banks struggle to underwrite small businesses because their credit processes are designed around documentation that MSMEs simply do not have — audited financials, formal employment records, GST history of sufficient vintage. Private-sector banks find the unit economics unattractive at small ticket sizes. The result is an enormous middle that gets neither micro-loans (too big for that) nor corporate credit (too small for that).

Utkarsh's strategic insight here is one of the most important business decisions in the entire SFB universe. It calls this the "adjacency ladder." A woman who borrowed her first ₹20,000 JLG loan five years ago, has now repaid it, has built a credit record inside the Utkarsh system, has graduated her dairy operation from two buffaloes to twelve, and is now ready for a ₹3 lakh equipment loan to buy a chaff cutter and a milk chiller — that woman is not a stranger. She is the safest MSME credit a bank can possibly underwrite, because the bank has watched her cash flows behave for half a decade. Utkarsh's transition from MFI to bank is not a pivot away from microfinance; it is a vertical extension of microfinance, using the original relationship as the underwriting moat for the next, larger, more profitable loan.

The economics of this ladder are striking. Microfinance JLG loans carry high yields but also high operating cost — every loan officer hours-per-rupee is intensive. MSME and secured business loans carry lower yields but dramatically lower operating cost per rupee. As Utkarsh's book has tilted toward those larger tickets, the yield on the overall portfolio has compressed somewhat, but the Net Interest Margin — the actual profitability of the lending business after funding costs — has held up remarkably well, because the funding side has improved even faster than the yield has compressed6.

That brings us to the most underappreciated achievement of the entire transformation: the deposit franchise. When Utkarsh became a bank in early 2017, it had effectively zero retail deposit base. By the late 2010s and into the 2020s, it built a granular retail liability book in geographies where the dominant deposit player is the State Bank of India, the post office network, and a handful of public-sector banks with branches dating back to the bank nationalization era of 1969. Competing with भारतीय स्टेट बैंक State Bank of India on deposits in a UP village is roughly equivalent to opening a coffee shop next door to Starbucks while also being told you must pay slightly higher interest on deposits to win share. Utkarsh has done it by offering meaningfully higher deposit rates than the public-sector incumbents — a structural feature of SFB regulation, which permits more attractive deposit pricing — and by deploying a branch network that is dense in Tier 3 and 4 geographies where the experiential gap between an old PSB branch and a new Utkarsh branch is enormous.

The result is a deposit base that includes a meaningful current and savings account (CASA) component built primarily from retail customers in Hindi-speaking states. The fact that retail deposits have grown to fund the bulk of the loan book is the single most important structural fact about Utkarsh today, because retail deposits — unlike wholesale borrowings — are sticky, repriceable, and compound. This is the moat-building act of any modern bank, and it is the thing that separates "an NBFC with a banking license" from "an actual bank." Utkarsh, gradually, has become the latter.

Underneath the headline split between microfinance and "new-age" verticals, there is a slow but real rebalancing happening — and the bank's own disclosures and the RHP make clear that management's medium-term ambition is to push the secured share materially higher over the coming years2. If you believe that rebalancing happens on schedule, you are underwriting a meaningfully different business than the "MFI in a banking wrapper" that consensus assumes.

VI. Capital Deployment & Benchmarking

July 2023. The IPO market in India had spent most of the previous year in a state of cautious indigestion. Several high-profile listings from the 2021 cohort had broken issue. Foreign portfolio flows had been choppy. The narrative in Mumbai was that the IPO window had closed for anything that smelled like risk.

Then Utkarsh opened its book. The IPO ran from July 12 to July 14, 2023, with a price band of ₹23-25 per share[^10]. The total issue size was approximately ₹500 crore, structured entirely as a fresh issue — meaning that every rupee raised went into the bank's capital base, not into the pockets of selling shareholders. This was, by Indian IPO standards, a relatively small ticket. And then the book opened.

By the close of bidding, the issue was subscribed more than 100 times overall, with the qualified institutional buyer (QIB) portion subscribed roughly 124 times, the non-institutional / HNI portion subscribed at staggering multiples, and even the retail portion oversubscribed by more than 100 times[^10]. To put this in context: a 100x oversubscription on a bank IPO is, in the post-2018 era, almost unheard of. Listing day, on July 21, 2023, the stock opened at a sharp premium to the issue price, registering one of the strongest listing-day pops of any Indian banking IPO in years.

What was the market actually buying? In our view, three things layered on top of each other. The first was valuation: the IPO was priced at a Price-to-Book multiple substantially below where the larger SFBs and CreditAccess Grameen were trading. The second was story: post-COVID, the Indian microfinance and rural-credit sector had emerged from its worst stress cycle in a decade, asset quality had stabilized, and investors were hungry for a relatively clean exposure to the bottom-of-pyramid lending recovery. The third — and this is the under-discussed one — was governance perception: Utkarsh entered the IPO without a single major asset quality crisis, without a CEO-departure controversy, and without the kind of related-party-transaction overhang that had dragged on some of its peers. In a sector where governance shocks have repeatedly evaporated 30% of market cap overnight, that mattered.

Now to the more interesting strategic question: what hasn't Utkarsh done with capital?

Notably, it has not pursued the trophy acquisitions that more aggressive SFBs have flirted with. Some of its peers have explored or executed acquisitions — housing finance companies, NBFCs, regional cooperative-bank assets — as a shortcut to scale. Utkarsh, under Singh, has consistently chosen organic growth over inorganic. The bank's branch network has grown through deliberate "branch-and-mortar density" — adding new physical branches in clusters around existing ones, deepening market share within an existing district before opening a new one2. This is the slow geography of compounding. It is also, frankly, the model that built HDFC Bank into what it became over thirty years.

The benchmarking picture is where the analytical work gets sharper. On Return on Assets (RoA), Utkarsh has historically tracked at or above the SFB median, though below AU Small Finance Bank, which remains the standout profitability story in the sector — driven heavily by AU's secured vehicle finance origins. On Net Interest Margins, Utkarsh's higher microfinance share has structurally given it elevated NIMs relative to a more vehicle-financy AU, but slightly below CreditAccess Grameen, which remains a pure-play MFI6. On asset quality, the post-COVID stress cycle of FY22 and FY23 saw all microfinance-tilted lenders take meaningful provisioning hits. By FY25, the cycle had normalized broadly, though pockets of stress in specific North Indian geographies remained a recurring theme in earnings calls7.

The question of whether Utkarsh "overpaid" for growth during the COVID-19 recovery is genuinely interesting. Several MFI-tilted lenders, including Utkarsh, ran hard on disbursements during FY22 and into FY23 as the post-pandemic credit appetite returned. Some of that growth has subsequently seasoned into elevated credit costs in FY24 and FY25 as the post-pandemic borrower cohort exhibited weaker repayment behavior than the pre-pandemic cohort. This is not unique to Utkarsh — it is a sector-wide story — but it does suggest that the bank's medium-term provisioning may continue to absorb some legacy disbursement vintages even as new origination has been re-tightened.

So the capital story, three years after listing, is one of patient deployment, conservative organic expansion, and a deliberate refusal to chase peers on M&A — bridging neatly to a deeper question: in a market this competitive, what is Utkarsh's actual structural advantage?

VII. Porter's 5 Forces & Hamilton Helmer's 7 Powers

Indian banking, in 2026, is the most competitive consumer financial services market in the world. There are no fewer than a dozen private-sector banks with national ambitions. There are eleven Small Finance Banks. There are payment banks, NBFCs, housing finance companies, gold finance specialists, fintech-NBFCs, and an entire layer of Big Tech distribution coming through Google Pay, PhonePe, Paytm, and increasingly the ONDC stack. Margin pressure is structural. Capital is plentiful for the winners and brutally rationed for everyone else. So when you sit down to think about why a small, regionally concentrated bank in eastern UP could possibly defend its economics against this onslaught, you have to be unusually precise about the source of its edge.

Hamilton Helmer's 7 Powers framework is, in our view, the cleanest lens to apply here. Of the seven — Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power — Utkarsh credibly lays claim to two-and-a-half.

The clearest is Cornered Resource: the North India footprint. This is not the Coca-Cola formula or the Pixar talent cluster. It is something subtler — but, for banking, just as durable. Building a branch network in rural Bihar and eastern UP is not just an investment in physical real estate; it is an investment in trust, in local language fluency, in village-level relationships with sarpanches and self-help group leaders, in the loan officer who has known a borrower's family for three loan cycles. None of these things can be replicated by capital alone. A Mumbai bank that wants to enter Mau or Ghazipur cannot simply rent an office and parachute in tellers. It has to build the social fabric — and the social fabric takes a decade. Utkarsh has had that decade. It is, by some margin, the most embedded private-sector financial institution in many of the districts it operates in. That embeddedness is the cornered resource.

The second power is Switching Costs. Here the dynamic is unusual but real. For a rural micro-entrepreneur in UP, the first "formal" bank account they ever own is a momentous thing — it is the first time their cash flows leave the informal economy and enter the regulated system. The account becomes the spine of their financial identity. The KYC is in place. The aadhaar linkage is in place. The UPI handle is set up. The cheque book, the debit card, the bank QR code at their shop counter, the loan history that lives inside the bank's system — all of it accumulates. Asking that customer to switch to a different bank is asking them to dismantle and rebuild an entire financial identity. Most don't. Customer churn in this segment, across SFB peers, is notably low compared to urban retail banking, and Utkarsh has been a particular beneficiary7.

The half-point I'd give is Process Power, specifically around credit underwriting in the JLG and small-MSME segments. Utkarsh has spent more than fifteen years refining the operational rhythm of group lending in North India — how to size a group, how to time disbursements with crop cycles, how to detect distress before it becomes default. This isn't a technology moat; it's an organizational know-how moat, and it shows up in collection efficiency numbers that consistently beat the industry average through stress cycles. But process power is the most fragile of the 7 Powers, because organizations forget. If the institutional memory leaves with key lieutenants or the underwriting model gets diluted in pursuit of growth, it can evaporate inside two years.

Now to Porter. Of the Five Forces, the two that matter most for Utkarsh's medium-term economics are threat of new entrants and threat of substitutes.

The threat of new entrants in rural North India was, until recently, near-zero — and it is precisely this that allowed Utkarsh to build undisturbed for a decade. That equation is now changing, in two specific ways. First, Digital Public Infrastructure. UPI, the Account Aggregator framework, OCEN, ONDC — collectively, India's "DPI stack" — has dramatically lowered the cost for a Mumbai-based bank or fintech to service a customer in a UP village without owning a physical branch there. Sourcing can be digital. KYC can be digital via aadhaar. Cash flow visibility can be obtained via Account Aggregator-fed bank statements. The branch-and-mortar moat is not gone, but it has been partially de-fanged. Second, NBFC entry. As the post-IL&FS NBFC sector rebuilt itself, several well-capitalized players — Bajaj Finance, in particular — pushed deeper into Tier 3 and Tier 4 distribution. Bajaj does not need a branch in Gorakhpur to lend in Gorakhpur. It needs a distribution partner and a smartphone6.

The threat of substitutes is the parallel concern. The biggest substitute for a microfinance JLG loan today isn't another MFI loan — it is, increasingly, a digitally underwritten unsecured personal loan from a fintech-NBFC, or a Buy-Now-Pay-Later facility riding on UPI rails. For a rural woman with two years of UPI transaction history, that digital underwriting alternative is genuinely competitive on speed and convenience, even if not on price.

Where Porter cuts in Utkarsh's favor is buyer power (rural borrowers have weak negotiating leverage relative to a formally regulated bank) and supplier power (in banking, the "supplier" is the deposit base, and Utkarsh's growing retail CASA franchise materially reduces supplier-power risk relative to wholesale-funded NBFCs). And then there is rivalry: intense in the metros, far less intense in the deep heartland geographies where Utkarsh actually competes.

Net-net, Utkarsh's moat is not infinite. It is real, it is regional, and it is being slowly eroded at the edges by digital substitution. The investment question is whether the bank can scale into its secured-lending and CASA build-out faster than the moat erodes — and that is the question we will turn to next.

VIII. Playbook: Business & Investing Lessons

Strip Utkarsh down to its operating principles, and three rules emerge. These rules are not unique to Utkarsh — most great regional banks share them — but Utkarsh's story is one of the cleanest expressions of them in modern Indian finance.

Rule one: the adjacency ladder. Don't lend to strangers — lend more to the customers you already know. The single most expensive thing in banking is acquiring a new credit relationship. The single cheapest is extending an existing one. Utkarsh's transition from micro-loans to MSME loans is the textbook execution of this principle. The same JLG woman who borrowed ₹20,000 in 2018 may take a ₹3 lakh secured business loan in 2024 and a ₹15 lakh housing loan in 2027. Every step up the ladder is dramatically more profitable than acquiring a brand new customer at the same ticket size, because the underwriting is cheaper (you already know her cash flows), the operational cost is lower (she's already on your CASA rails), and the loyalty is deeper. This is what HDFC Bank did at the urban-affluent end of the market in the 1990s and 2000s — built a savings account customer, then sold them a credit card, then a personal loan, then a home loan, then wealth management — and it is what Utkarsh is attempting to do at the rural-aspirational end. The market is a generation behind in giving credit for it.

Rule two: the riches are in the niches. Pick a geography and dominate it before expanding. India has 28 states. Most banks make the strategic mistake of being "present everywhere, dominant nowhere." Utkarsh chose UP and Bihar and went deep before it ever went wide. The result is a level of brand recognition and physical density in those states that pan-India peers cannot easily replicate. There is a useful analogy here to the great regional banks of the 20th-century United States — Wells Fargo's San Francisco roots, NationsBank's Charlotte roots — institutions that won their original markets first and only then expanded outward. Utkarsh has, in many ways, been writing a similar playbook for India.

Rule three: in Indian banking, the license itself is a 7 Power. Anyone with capital can start an NBFC. Almost no one can start a bank. The RBI hands out commercial bank licenses with extreme parsimony — in the entire post-liberalization era, fewer than fifteen private-sector banking licenses have been granted. The SFB framework was the first material widening of this aperture, and even there, only ten licenses were issued in the first round. That license is, functionally, a regulatory moat. It permits Utkarsh to accept retail deposits — the cheapest funding in finance. It permits CASA — the cheapest of the cheap. And it permits the bank to operate in a regulatory perimeter that is structurally privileged versus the NBFC alternative.

The implication of this last rule is one of the most important investing observations in the entire Indian financial sector: regulatory alpha is a real and durable source of moat. The market under-prices it because regulatory moats don't show up in growth rates — they show up in funding costs, in the right to compound through stress cycles when NBFCs are getting locked out of capital markets, and in the operational permission set to build a real banking franchise rather than a leveraged lending vehicle. The 2018 IL&FS crisis and the subsequent NBFC funding squeeze proved this point vividly: every NBFC, no matter how well-managed, was at the mercy of wholesale capital markets. Every bank — including the youngest SFBs — had retail deposits to fund through the cycle.

A fourth, slightly meta lesson worth noting: the best moment to underwrite a financial institution is not when its growth is fastest, but when its operational maturity is highest. Utkarsh's growth in FY26 looks distinctly slower than its peak years. But its institutional plumbing — its core banking system, its risk frameworks, its branch operating model, its compliance posture — is in dramatically better shape than it was during the high-growth years. For long-duration investors, this maturity inflection often matters more than the immediate growth narrative, because it is precisely what permits the next ten years of compounding without an accident.

IX. Analysis & Bear vs. Bull Case

Every long-duration banking thesis eventually collapses into a single bilateral debate: bull case or bear case. For Utkarsh, that debate is unusually balanced — which is, paradoxically, what makes it interesting.

Myth vs. Reality. Before the cases, the consensus narratives worth re-examining:

- Myth: Utkarsh is a microfinance company with a banking label. Reality: Microfinance is still the largest single segment, but the secured and MSME share has been climbing steadily and the medium-term mix shift is the actual investment story2.

- Myth: SFBs are essentially the same business model. Reality: AU is a vehicle-finance bank, Equitas is a diversified urban-tilted bank, CreditAccess is a pure MFI, and Utkarsh is a heartland-MFI-evolving-into-regional-commercial-bank. The dispersion of outcomes across the SFB peer group is enormous, and the assumption of category homogeneity has been a recurring mistake among generalist investors.

- Myth: Loan waivers will eventually destroy lenders in UP and Bihar. Reality: Loan waivers in India have historically targeted public-sector bank agricultural loans, not microfinance or SFB credit. The risk is non-zero but the historical precedent does not support the doomsday version of this concern.

The Bull Case. The bull case for Utkarsh rests on three pillars stacked on top of each other. First, the demographic dividend of the Hindi heartland. UP alone has a population larger than every country in the world except China, India, and the United States. Bihar's per-capita income, though still well below the national average, has been growing faster than the national average for most of the last decade. The aspirational consumption and credit appetite in these states is structurally explosive, and Utkarsh is among a small handful of institutions positioned to underwrite it. Second, the adjacency ladder execution. If management can continue to migrate JLG borrowers up the credit ladder into MSME and housing — without losing underwriting discipline — the resulting book mix will look meaningfully more like a commercial bank than an MFI, with the corresponding RoA expansion. Third, the deposit franchise compounding. Retail deposits in rural North India, once acquired, are exceptionally sticky. The "HDFC Bank of the heartland" framing is more than marketing; it captures a real long-duration compounding mechanism if the franchise holds.

The Bear Case. The bear case is equally specific, and equally serious. First, political risk. Bihar and UP are the most electorally turbulent states in India. Any state government can, at any time, introduce a loan-waiver scheme, a regulatory clampdown on collection practices, or a populist intervention that disrupts repayment culture. The 2010 Andhra crisis was caused by precisely such a state-level intervention, and while the post-AP regulatory framework has reduced this risk, it has not eliminated it. Second, unsecured lending volatility. Microfinance remains a high-yield, high-volatility business. Stress cycles compress profitability sharply. Investors with low tolerance for cyclical credit costs find this segment uncomfortable, and the FY24-FY25 cycle showed elevated provisioning across the sector7. Third, digital substitution. The DPI stack is a long-term threat to the branch-density moat, and the speed of substitution may exceed the speed of Utkarsh's deposit-side compounding.

Key Person Risk. Then there is the question every analyst raises but few have a satisfying answer to: what happens to Utkarsh without Govind Singh? The bank has been substantially built and shaped by one person's risk temperament. The board has been progressively professionalizing, and the bench beneath Singh has been deepening, but the institutional culture — the conservatism, the geographic discipline, the patient compounding — is still indistinguishable from the founder's personal philosophy. Indian banking has more than one example of a regional bank that lost its character within five years of founder transition. This is not a theoretical risk. It is a real, embedded uncertainty that no amount of governance documentation fully resolves. For long-duration investors, the succession plan deserves as much diligence as the loan book.

Light second-layer overlays worth flagging. A handful of contextual items shape the risk picture without being headline factors. Credit ratings on the bank's instruments from agencies like CRISIL and ICRA have generally held in the investment-grade range; any downgrade would meaningfully raise wholesale funding costs2. Several FII shareholders inherited from the impact-PE era will continue to be sellers as part of natural portfolio rotation, which can create episodic supply pressure in the stock. The bank's auditor opinions through the IPO and post-listing period have been unqualified, with no going-concern flags2. Macro overlays — monsoon variability, rural inflation, fuel price shocks — disproportionately affect this borrower base and should be tracked alongside the company-specific numbers.

The KPIs that actually matter. For an institution this complex, the temptation is to drown in metrics. Resist it. The two-and-a-half KPIs that genuinely matter for ongoing performance tracking are: first, GNPA in the JLG / microfinance book, because that is where stress shows up first and where provisioning surprises originate; second, the secured-book share of total advances, because that single ratio is the cleanest expression of whether the strategic transition is actually happening; and a half-KPI, CASA ratio and retail deposit share, because that is where the long-term funding cost story is written. Tracking these three together gives you a real-time view of whether the thesis is intact, without getting lost in the noise of quarterly NIM movements.

X. Epilogue & Outro

Step back and the shape of the Utkarsh story is unusual. Most great financial institutions are built either at the top of the market — affluent banks for affluent customers — or at the bottom — pure microfinance for the very poor. Utkarsh has spent seventeen years building in the middle, in the "missing middle" of Indian banking, which is also the demographic middle of the country. Eastern UP and Bihar are where most of India actually lives, works, and aspires. They are also where most of Indian capital has chosen not to go.

If the bull case plays out — if the adjacency ladder works, if the deposit franchise compounds, if the political risk stays in the tail rather than the body of the distribution — Utkarsh will look, ten years from now, like one of the more important institutional bets on the economic awakening of the Hindi heartland. There is a real possibility that the bank that comes out of the next decade is recognizable as the early-stage version of a much larger, much more diversified regional commercial bank. The HDFC-of-the-heartland framing is ambitious, but it is not implausible.

If the bear case plays out — if a political shock disrupts collection culture, if digital substitution outpaces secured-lending build-out, if a succession transition dilutes the operating culture — the bank could spend a decade compounding at a pace that meaningfully underwhelms the multiples it has traded at in its more euphoric moments. Both outcomes live, today, in the same business.

What's clear is that the institution Utkarsh has become is not the institution it was in 2009, when a former corporate banker rented an office in Varanasi and started lending ₹10,000 tickets to women in पूर्वांचल Purvanchal villages. It is also not yet the institution that its most ambitious investors believe it will become. It is, somewhere in the middle of that arc — closer to the second than to the first, but with the most important chapters still unwritten.

The longer-term thing the Utkarsh story illustrates is that financial inclusion, done with operational discipline, can become a commercial moat rather than a charitable subsidy. The SFB experiment that the RBI launched in 2015 was, in its essence, a wager that India's social and commercial banking objectives did not have to be in tension. A decade later, with multiple SFBs listed, several profitable, and at least a handful — Utkarsh included — building real franchises in geographies that traditional banking had abandoned, the wager looks like one of the more successful regulatory experiments in modern emerging-markets finance. The bigger story is not really about one bank in Varanasi. It is about whether a country of 1.4 billion people, the majority of whom live outside the major metros, can build the financial plumbing it needs from regional institutions that grew up alongside their customers rather than from national institutions that parachuted down to them.

The Ganges keeps flowing past the shop on Vishwanath Gali. The saree-owner closes out the day's UPI ledger. Somewhere on Airport Road in Varanasi, on the third floor of Utkarsh Tower, Govind Singh — or whoever sits in his chair next — opens tomorrow's branch-level collection report. The work, in the end, is unglamorous. That, more than anything else, is the point.

References

References

-

Master Direction – Issue and Pricing of Shares by Private Sector Banks / Small Finance Banks framework — Reserve Bank of India ↩↩

-

Microfinance in India: State of the Sector Report — MicroSave / M-CRIL ↩

-

NSE India Company Profile: UTKARSHBNK — National Stock Exchange of India ↩

-

Comparison of SFB Peers: AU vs Equitas vs Utkarsh — Financial Express ↩↩↩

-

Utkarsh SFB Q4 FY24 Earnings Call Transcript — Utkarsh Small Finance Bank ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube