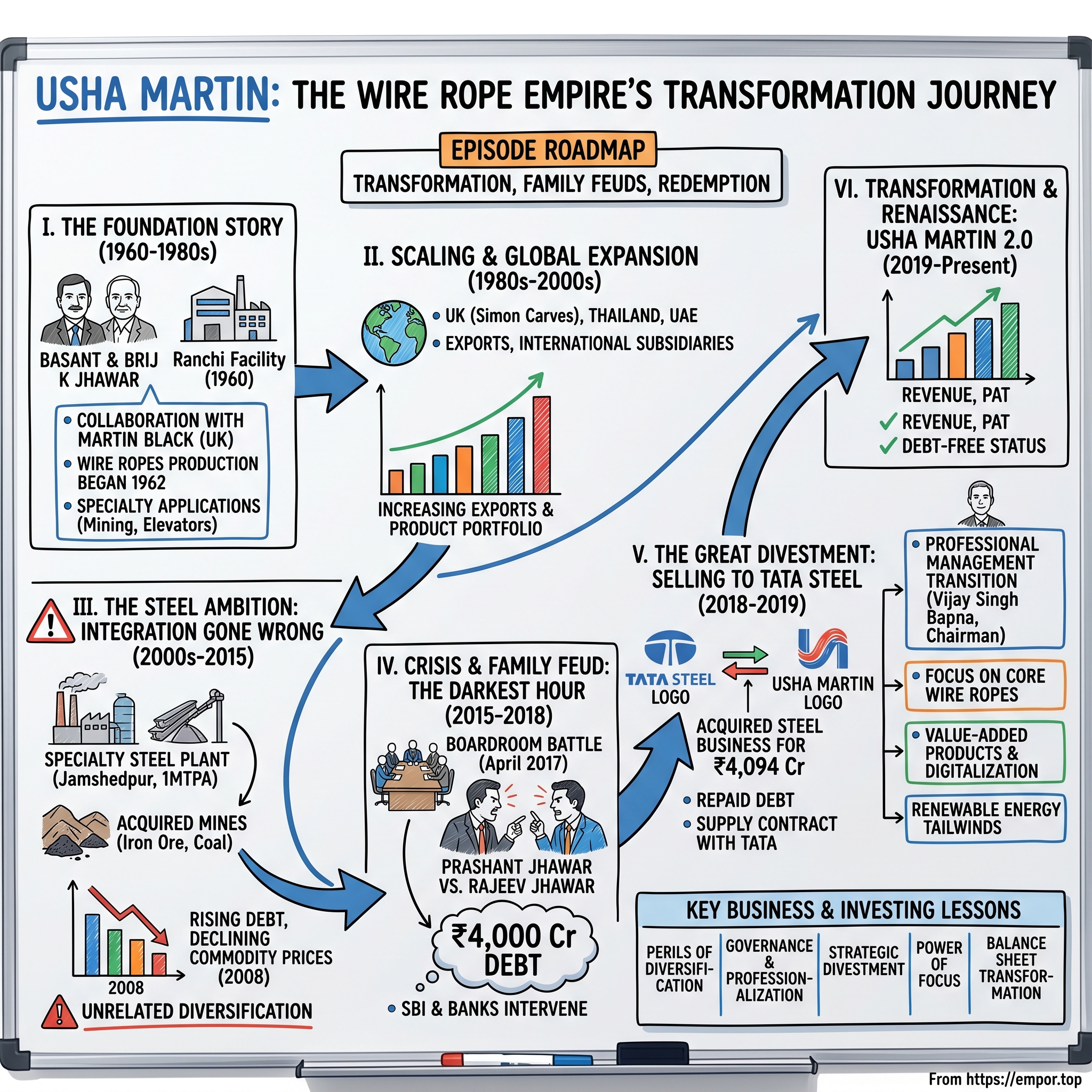

Usha Martin: The Wire Rope Empire's Transformation Story

I. Introduction & Episode Roadmap

Picture this: A 60-year-old Indian manufacturing company, drowning in ₹4,000 crores of debt, family members fighting in boardrooms, and analysts writing obituaries. Fast forward five years—the same company sits debt-free, with margins expanding, and the stock up over 300%. This is the resurrection story of Usha Martin Limited.

Today, Usha Martin commands a market capitalization of ₹10,703 crores, standing as India's undisputed leader in specialty steel wire rope solutions. But the journey here reads like a Shakespearean drama—complete with ambitious expansion, family feuds, near-death experiences, and an unlikely redemption arc that would make any turnaround specialist jealous.

The question that frames our exploration: How did a family-run wire rope manufacturer from Ranchi survive a debt crisis that should have killed it, navigate bitter family disputes that tore apart its founding dynasty, and emerge stronger after selling off what many considered its crown jewel—the steel business?

This isn't just another corporate survival story. It's a masterclass in strategic retreat, the perils of vertical integration, and why sometimes the best way forward is to go back to your roots. Over the next few hours, we'll dissect how Usha Martin transformed from a debt-laden conglomerate to a focused, profitable specialty manufacturer—and what this metamorphosis teaches us about Indian family businesses, capital allocation, and the art of corporate reinvention.

II. The Foundation Story: Jhawar Brothers & Wire Dreams (1960–1980s)

The year was 1960. India had been independent for just thirteen years, and the nation's industrial landscape resembled a vast construction site—steel girders rising, bridges spanning rivers, mines boring into the earth. In this environment of nation-building fervor, a commerce graduate named Basant Kumar Jhawar saw opportunity where others saw chaos. Wire ropes—the unglamorous steel cables that lift, pull, and hold—would be his ticket to industrial prominence.

Basant Jhawar, a commerce graduate, founded Usha Martin in 1960 at Ranchi in collaboration with Martin Black of UK. The choice of Ranchi wasn't accidental—it sat in the mineral-rich heart of what would become Jharkhand, close to coal mines and steel plants that would need his products. He was later joined by his younger brother Brij K Jhawar, a mechanical engineer, creating a partnership that combined commercial acumen with technical expertise.

The brothers moved with remarkable speed. The first wire rope reel rolled out of the company in 1962. But even before production began, they had pulled off something extraordinary—their public issue in 1961 was oversubscribed by more than 300 per cent. In an era when capital markets were nascent and industrial ventures were viewed with skepticism, this response signaled something special about the Jhawar vision.

The early numbers tell a story of breakneck expansion. In 1963, the company paid its maiden dividend and doubled the production from 3,600 tonnes to 7,200 tonnes in just two-and-a-half years. This wasn't just growth—it was validation of a fundamental insight: post-independence India's infrastructure boom would create insatiable demand for industrial components that most people never thought about.

What made Usha Martin different wasn't just timing or location—it was the brothers' approach to technology and quality. The collaboration with Martin Black brought Scottish wire rope expertise to Indian soil, a technology transfer that would prove crucial. While competitors focused on basic products, the Jhawars bet on specialty applications—mining ropes that could withstand extreme conditions, elevator cables that demanded zero-failure reliability.

By the 1970s, the company had established what would become its crown jewel: the Ranchi facility. Over the years Usha Martin expanded its operations and established manufacturing facilities in several locations in India and internationally, with sales offices, distribution networks, and subsidiaries in countries like the United States, the United Kingdom, Dubai, Thailand, and Singapore. The Punjab unit followed in 1974, spreading manufacturing capacity across northern India.

The brothers complemented each other perfectly—Basant handling commercial strategy and financial engineering, Brij focusing on manufacturing excellence and technical innovation. They built a culture that was simultaneously family-run and professionally managed, Indian in ownership but global in ambition. Their sons would eventually join the business, setting the stage for both tremendous growth and, decades later, bitter conflict.

III. Scaling & Diversification: Becoming a Global Player (1980s–2000s)

The 1980s marked a pivot from domestic dominance to global ambition. Under the second generation's leadership—with sons joining the founding brothers—Usha Martin transformed from an Indian manufacturer serving local markets into a multinational corporation competing on the world stage.

By the late 1970s, Usha Martin had begun exporting its products, thereby paving the way for international expansion. This wasn't just about selling overseas; it was about fundamentally reimagining what an Indian manufacturing company could become. By 1980, the company was recognized for its innovative approaches and quality manufacturing processes, which earned it several quality certifications, including those from ISO.

The 1990s brought financial engineering to match the operational expansion. In 1993, Usha Martin became a publicly listed company, allowing it to access additional capital for further growth. This IPO wasn't just about raising money—it was about institutionalizing a family business, bringing in professional managers, and creating the governance structures necessary for international operations.

Then came the acquisition spree that would define Usha Martin's global footprint. In 2001, Usha Martin acquired the wire rope business of Simon Carves Group in the UK, enhancing its technological capabilities and expanding its product range. This acquisition marked a strategic move toward becoming a global leader in wire rope manufacturing. This wasn't just buying assets—it was acquiring centuries of British wire rope expertise, customer relationships in developed markets, and most importantly, credibility in industries where "Made in India" still faced skepticism.

The company's international expansion followed a deliberate hub-and-spoke model. It established sales offices, distribution networks, and subsidiaries in several countries worldwide, including the United States, the United Kingdom, Dubai, Thailand, and Singapore, thus gaining a global presence. Each location was chosen strategically—Dubai for Middle Eastern oil and gas markets, Thailand for Southeast Asian infrastructure projects, UK for European engineering applications.

During the year, the company acquired a majority stake in Usha Siam Steel Industries Public Ltd Company, Bangkok, which is engaged in manufacture of wire ropes. Also they acquired 80% stake in Brunton Shaw Ltd, UK, from Carclo Group. These weren't random purchases—they were carefully selected pieces of a global puzzle, each bringing specific technological capabilities or market access.

The product portfolio expanded dramatically during this period. The company has supplied wire ropes for various applications in sectors such as oil and gas, mining, elevators, cranes, bridges, and general engineering. But the real innovation wasn't in making more products—it was in understanding that different markets needed different solutions. Oil rigs in the North Sea required different specifications than mines in Australia or elevators in Singapore skyscrapers.

By the early 2000s, Usha Martin had achieved something remarkable: With a robust presence in over 100 countries, Usha Martin has become a significant player in the wire rope industry. The company that had started with a single factory in Ranchi now operated manufacturing facilities across continents, employed thousands globally, and competed head-to-head with century-old European and American manufacturers.

The numbers tell the story of transformation. With six decades of manufacturing excellence, Usha Martin excels in offering a comprehensive range of value-added products and services to suit all types of critical environments. But beneath the corporate success lay the seeds of future problems—the aggressive expansion had been funded by debt, and the family's next generation was beginning to have different visions for the company's future.

IV. The Steel Ambition: Backward Integration Gone Wrong (2000s-2015)

The boardroom at Usha Martin's Kolkata headquarters in 2004 must have crackled with energy. Steel prices were soaring, China's infrastructure boom was driving global commodity demand, and the logic seemed irrefutable: why buy steel from others when you could make it yourself? The decision to pursue backward integration would prove to be the most consequential—and ultimately destructive—in the company's history.

In its quest to have a fully integrated business model, the Company started its steel business in 1974 at Jamshedpur (Jharkhand) and also acquired Iron Ore mines which are at Barajamda (Jharkhand) and Coal mine. But what started as a modest captive steel facility for wire rope production morphed into something far more ambitious. The early 2000s saw massive expansion—In the year 1995, the company commissioned mini blast furnace at Jamshedpur to reduce cost and improve productivity. Also, they commissioned second SMS at Jamshedpur to enhance capacity to 350000 TPA.

The strategy was to place the Company distinctly in a unique position by combining both ends of value chain, from mining to high value wire ropes and further providing end use solutions on its key product applications. The decision was with aim of providing benefits of quality, consistency, and self-sufficiency in principal raw materials.

The ambition kept growing. By the mid-2000s, what had begun as backward integration transformed into a full-fledged steel business. The acquisition involves UML's 1.0 MnTPA specialty steel plant in Jamshedpur that makes alloy based long products, a functional iron ore mine, a coal mine under development and captive power plants. This wasn't just about making steel for wire ropes anymore—this was about becoming a steel company.

The timing initially seemed perfect. Global steel prices were on a tear, driven by China's insatiable appetite for raw materials. Infrastructure projects across India were multiplying. The company raised capital through multiple routes—debt, equity, warrants—all predicated on the assumption that steel prices would keep climbing and demand would remain robust.

But here's where the strategic miscalculation becomes clear: In this instance, a similar thing happened when the specialty steel business become larger than what is required for captive consumption. What started as vertical integration had become unrelated diversification. The wire rope business needed perhaps 200,000 tonnes of steel annually; Usha Martin had built capacity for one million tonnes.

The financing structure revealed the precariousness of the strategy. However, profits from WWR business was not enough to compensate interest payment on debt taken mainly for expansion of steel business. The company was essentially using cash flows from its profitable, established wire rope business to service debt taken for an unprofitable, cyclical steel business.

Then came 2008. The global financial crisis sent commodity prices crashing. Steel, which had been trading at historic highs, plummeted. Chinese demand evaporated overnight. What looked like strategic brilliance in 2006 now appeared as dangerous overextension. The slowdown in steel prices turned fortune for the company. It started eroding its net worth due to losses in Steel Business. At the same time, its borrowing increased 4 folds. Raising debt levels & volatility in steel business became a nightmare for Usha Martin.

The numbers told a brutal story. Usha Martin, which had a debt of over Rs 37.00 billion and a revenue of Rs 34.41 billion in the last fiscal year—debt had exceeded annual revenues. Interest costs were consuming operational profits. The steel division, meant to strengthen the company, was now threatening its survival.

By 2015, the situation had become untenable. The wire rope business remained profitable but couldn't generate enough cash to service the mountain of debt accumulated for steel expansion. Banks were getting nervous. Credit lines were being questioned. And within the founding family, tensions about the strategic direction were reaching a breaking point.

V. Crisis & Family Feud: The Darkest Hour (2015-2018)

The April 2017 board meeting at Usha Martin's headquarters would go down as one of the most dramatic in Indian corporate history. The family run business stood witness to not only financial trauma but also family issues. What began as strategic disagreements over debt and divestment had exploded into an all-out war between the founding brothers' sons—cousins who had once worked side by side to build a global empire.

In April 2017, the board had passed a resolution, moved by the SBI nominee, to strip Prashant Jhawar of his post as the non-executive chairman and also trim the power of Basant Jhawar, 83, as chairman emeritus. The resolution didn't come from the family—it came from the banks, specifically State Bank of India, which had watched with growing alarm as the company's debt burden threatened to consume it entirely.

The family structure that had once been Usha Martin's strength had become its greatest vulnerability. The father-son duos of Basant-Prashant Jhawar and Brij-Rajeev Jhawar held 25.5% respectively in the company. Equal ownership meant equal power—at least in theory. But when crisis struck, equality became paralysis.

Prashant and his father BK Jhawar had been under attack from banks, too. The allegation against them was that, despite several reminders from banks, the son-father duo did not complete the documentation process relating to the pledge of their stakes to the concerned banks. This irked the lenders, who decided to move a resolution against them. However, Rajeev Jhawar met all the compliances required by the banks.

The boardroom dynamics had shifted decisively. Meanwhile, in February 2018, the Usha Martin board reappointed Rajeev as the managing director. All the other board members, including the six independent directors and the nominee director of the State Bank of India, had voted in Rajeev's favour. This wasn't just a corporate appointment—it was a palace coup, orchestrated with the backing of lenders who saw Rajeev as their best hope for recovering their loans.

The allegations flew thick and fast. The family patriarch has now opened up on the bitter battle alleging back-stabbing by his nephew Rajeev, the managing director of the company, by orchestrating his removal on the sly. Basant Jhawar didn't mince words, accusing his nephew of betrayal and manipulation.

But beneath the personal animosity lay fundamental business disagreements. In February 2017, despite having meagre 1 MTPA capacity steel plant, the Company announced that it is evaluating divestment of its original Wire & Wire Ropes Business. The reason for announcing divestment of its original business i.e., WWR business instead of steel business could be focus on steel business, stable revenue & profitability of the WWR business, heavy capex already done in steel business etc.

This was the heart of the conflict: Prashant and Basant wanted to sell the profitable wire rope business and keep the troubled steel division. Rajeev and the banks saw this as insanity—selling the crown jewel to keep the millstone. Company's endeavour to address the debt burden by looking for a buyer for Wire and Wire Ropes business was not met with success. With no other option left, the company announced that it has also started evaluating divesting its steel business.

The human cost of the feud was devastating. Brothers who had built a business together over decades now communicated through lawyers. Cousins who had grown up in the same compound refused to speak. The differences among the founding brothers Brij Kishore Jhawar and Basant Jhawar has not only reached the court and the law enforcement agencies, but the octogenarians industrialists are now washing their dirty linen in public.

By 2018, the situation had reached a climax. With the special resolution for the continuation of Basant Jhawar, 83, as the non-executive director of Usha Martin defeated in the vote by shareholders, the co-founder of the group stepped down following an extraordinary general meeting (EGM) held on March 30. The founder had been voted out of his own company.

The banks had effectively taken control, using their leverage to install management they trusted. "My focus is clearly on the company's growth and nothing else," Rajeev says. With the family feud still raging but board control secured, Rajeev could finally execute the plan that would save Usha Martin: selling the steel business to Tata.

VI. The Great Divestment: Selling to Tata Steel (2018-2019)

September 22, 2018 marked the beginning of Usha Martin's resurrection when Tata Steel announced it would acquire UML's steel business for Rs 4,300-4,700 crore. After months of negotiations, competing bids, and boardroom battles, UML stated in a stock exchange filing that this sale would help achieve "significant reduction" of its debt.

The negotiation had been a high-stakes poker game with India's biggest names in steel at the table. Besides Tata Steel, JSW Steel, the Kalyani group, Liberty and Vedanta had expressed an interest in buying the steel division of UML. Each potential buyer knew Usha Martin was desperate, yet the assets—particularly the Jamshedpur plant's strategic location next to Tata Steel's own facilities—had genuine value.

For Tata Steel, the logic was compelling. Tata Steel has a disproportionate skew towards flat steel products now while Usha Martin has an integrated steel-making business with predominantly long steel products which get better margins. Tata Steel, which has a capacity of 27.5 million tonne, has a disproportionate skew towards flat steel products now while Usha Martin has an integrated steel-making business with predominantly long steel products which get better margins.

But the real drama lay in the structure of the deal. Tata Sponge Iron Limited, a subsidiary of Tata Steel Limited, acquired the steel business of Usha Martin Limited (UML) in 2019 for ₹4,094 crore (US$480 million). The acquisition involved UML's 1.0 MnTPA specialty steel plant in Jamshedpur that makes alloy-based long products, a functional iron ore mine, a coal mine under development, and captive power plants.

The final price—Rs 4,094 crore—was lower than the initial range, reflecting the harsh realities discovered during due diligence. Tata Sponge Iron Limited has completed the acquisition of steel business undertaking of UML including captive power plants, today, pursuant to a cash consideration (after adjustment for negative working capital and debt like items) payable to UML of Rs. 4,094 crore, which is subject to further hold backs of Rs.640 crore, pending transfer of some of the assets including mines and certain land parcels.

The "negative working capital" adjustment was a polite way of saying the steel business was bleeding cash. The Rs 640 crore holdback reflected uncertainty about transferring mines and land—assets tangled in regulatory approvals and legal complexities. For Usha Martin's lenders, though, even this reduced price was a godsend.

April 9, 2019, marked the closing. Tata Sponge Iron Limited, a subsidiary of Tata Steel Limited, has acquired the steel business of Usha Martin Limited (UML), a company release said Tuesday. The transaction was more than just an asset transfer—it was a complete transplant. All employees of the steel division became Tata employees overnight, their futures suddenly more secure under the Tata umbrella.

For Rajeev Jhawar, this was vindication. The cousin he'd battled, the uncle who'd accused him of betrayal—they'd wanted to keep the steel business and sell wire ropes. He'd fought for the opposite and won. The amount realised from the transaction has been utilised to pare its debt. In FY 2020, consolidate debt of Usha Martin improved substantially. It has repaid substantial debt pertaining to the steel business and thereby improved its credit rating.

But perhaps the masterstroke was what came after the sale. The Company has also signed a five-year supply contract with Tata Steel at fair market price. Usha Martin would continue buying steel from its former division, now owned by Tata, ensuring supply continuity for its wire rope business. The seller had become the customer—a elegant solution that benefited both parties.

The market's reaction was swift and positive. Debt that had peaked at over Rs 4,000 crores began melting away. Credit ratings that had been slipping toward junk status began their climb back. The company that had seemed destined for insolvency courts had pulled off one of Indian corporate history's great escapes.

Looking back, the Tata deal represented more than just a financial transaction. It was an acknowledgment that Usha Martin's venture into steel—however logical it seemed in 2004—had been a strategic mistake. Sometimes the best deal is the one that undoes a previous deal. Sometimes going backward is the only way forward.

VII. Transformation & Renaissance: Usha Martin 2.0 (2019-Present)

The transformation that began in 2019 wasn't just financial—it was cultural, strategic, and operational. Q1 FY26 showed Revenue Rs.887.2 Cr (+7.4% YoY), PAT Rs.100.8 Cr, and eliminated net debt. These numbers tell a remarkable story: a company that had nearly drowned in debt was now debt-free, generating steady profits, and growing again.

The most visible sign of change came at the top. Mr. Vijay Singh Bapna holds a Master of Commerce degree from the University of Udaipur, Rajasthan, and is a qualified Chartered Accountant. Over his distinguished career spanning more than four decades, he has held senior leadership positions with renowned corporate groups, including Aditya Birla Group, Essar Group, Ispat Industries, Reliance Petroleum, Vedanta Group, Indorama Group, and Welspun Group both in India and internationally. His expertise encompasses key areas such as accounting, costing, taxation, project implementation, and plant operations.

Bapna's appointment as Chairman marked a decisive shift from family-dominated governance to professional management. Here was someone who had worked across India's biggest industrial houses, understood turnarounds, and brought credibility that the fractured Jhawar family could no longer provide alone.

Under this new leadership structure—Mr. Rajeev Jhawar is a prominent Indian industrialist with over three decades of experience in strategic management. An alumnus of Ranchi University and London Business School, he began his career as Sr. Vice President (Commercial) at Usha Martin Limited and, in 1998, was appointed as Managing Director of the Company. Under his visionary leadership, the Usha Martin Group has achieved remarkable growth, fostering a meritocratic culture and significantly enhancing stakeholder value. His sharp business acumen, leadership capabilities, and strategic decision making have propelled the Group to a higher growth trajectory, cementing its position as one of the global leaders in the wire rope industry.—Usha Martin began its renaissance.

The strategy was clear: focus relentlessly on what the company did best—wire ropes. Commenting on the performance Mr. Rajeev Jhawar, Managing Director said, "In the backdrop of challenging macroeconomic conditions, Usha Martin commenced FY25 on a positive note, reporting revenues of ~Rs. 826 crore and achieving an operating EBITDA margin of 18.6%. Our core wire ropes division continued to perform well, contributing 72% to our overall consolidated revenues.

The transformation wasn't just about cutting debt and costs. It was about reimagining what Usha Martin could become. During this quarter our primary focus was on ramping up the newly established lines for our value-added products. As we enhance utilization levels, we anticipate a stronger performance in the second half of the year. Value-added products—specialized ropes for offshore drilling, high-performance elevator cables, customized mining solutions—commanded premium prices and higher margins.

Digital transformation became a priority. The company that had relied on relationships and reputation began investing in data analytics, predictive maintenance systems, and customer relationship management platforms. In the face of global headwinds, our strategy in our international operations remains to enhance our reach and capture market share by delivering world-class quality products and services. Our integration of international businesses with Indian operations continues to drive growth synergies, further strengthening our position.

The balance sheet transformation was nothing short of remarkable. From a debt-to-equity ratio that had threatened the company's existence, Usha Martin achieved something almost unheard of in Indian manufacturing: becoming net debt-free. The company that banks had once circled like vultures was now generating cash, paying dividends, and investing in growth.

Operational excellence initiatives kicked in across all facilities. The Ranchi plant, which had been the company's first, underwent modernization. Quality certifications were renewed and expanded. Customer satisfaction scores, which had suffered during the crisis years, began climbing back.

The market began to take notice. Mkt Cap: 10,594 Crore (up 3.61% in 1 year). The stock, which had been written off by many analysts, began its steady climb. Institutional investors who had fled during the crisis started returning. International customers who had worried about supply continuity renewed long-term contracts.

Looking ahead, our focus remains on value-driven volume expansion to enhance our operational and financial performance. We anticipate maintaining the development momentum as we build on progress from multiple growth initiatives. With world-class capabilities and inherent strengths Usha Martin has developed over six decades, we believe we are well-positioned to create sustainable value for all stakeholders.

The "Usha Martin 2.0" journey wasn't just corporate jargon—it represented genuine rebirth. A company that had lost its way chasing unrelated diversification had returned to its core competence. A family business torn apart by feuds had embraced professional management. A debt-laden manufacturer had become financially robust. The transformation was complete, but the journey toward becoming a global wire rope leader was just beginning.

Current Business & Market Position

Today's Usha Martin stands as a testament to focus and specialization. Usha Martin Ranchi facility is one of the world's largest wire rope manufacturing facility under one roof. Spread across an area of more than 100 acres, this is the first manufacturing facility established by Usha Martin, since its inception in 1961. What began as a single plant has evolved into a global manufacturing powerhouse.

The product portfolio tells a story of deep technical expertise. Usha Martin Ltd is primarily engaged in manufacture and sale of steel wires, strands, wire ropes, cords, related accessories, etc. It is also involved in sale of other products such as wire drawing and allied machines. The company offers a range of specialty wire ropes, high-quality wires, low relaxation prestressed concrete steel strands (LRPC), bespoke end-fitments, accessories, and related services. It also manufactures jelly-filled and optical fiber telecommunication cables.

The global footprint reveals strategic positioning. Our manufacturing facilities are located in India, the UK, Thailand, and UAE. Our distribution, sales, and service centers are spread worldwide at strategic locations to provide uninterrupted and customized services to our clients. This unit, set up in 1974 in the northern state of Punjab in India is spread over 8 hectare and employs about 700 people, making it the largest wire & wire rope unit in Northern India. It produces high quality wires and wire ropes that finds application in Automobiles, Detonators, Textile, and other engineering sectors.

The market position is impressive despite the years of turmoil. The major players operating in the Wire-Rope market include WireCo WorldGroup Inc., Bridon-Bekaert The Ropes Group, Tokyo Rope International, Usha Martin, Gustav Wolf GmbH, Wire Rope Corporation of America Inc., Jiangsu Langshan, Kiswire Ltd., Teufelberger Holding AG and Pfeifer Drako Drahtseilwerk GmbH are the top companies to hold the market share in Wire-Rope Market Being mentioned alongside century-old European and American giants validates Usha Martin's global standing.

The numbers reveal both capacity and capability. We manufacture more than 100,000 MT of wire ropes annually. Our wire rope ranges from 1.5 mm to 155 mm diameter in size, 1370 to 2160 N/mm2 in grade, are available in all construction and configuration. This range—from tiny 1.5mm cables to massive 155mm monsters—demonstrates unmatched technical versatility.

The application diversity showcases the criticality of Usha Martin's products. The company has supplied wire ropes for various applications in sectors such as oil and gas, mining, elevators, cranes, bridges, and general engineering. Infrastructure and construction projects: The firm has been involved in supplying steel products, including wire ropes and strands, for infrastructure and construction projects. This includes projects such as bridges, flyovers, metro rail systems, and other large-scale construction initiatives. Oil and gas industry: Usha Martin has provided wire ropes and steel products for offshore oil and gas exploration and production projects. These products are used in applications like drilling rigs, offshore platforms, and subsea operations. Mining industry: The company has supplied wire ropes for various mining applications, including hauling, lifting, and material handling in both underground and open-cast mines. Elevators/lifts: Usha Martin manufactures wire ropes used in elevator systems for commercial buildings, residential complexes, and industrial facilities. These wire ropes ensure safe and reliable vertical transportation. Wind energy: Usha Martin has been involved in the supply of steel wire ropes for wind turbines. These wire ropes are used for tasks such as hoisting, installation, and maintenance of wind turbine components.

The value-added services differentiate Usha Martin from commodity producers. We offer tailor-made products with value-added services, including socketing, cutting, coiling, spooling, pre-stressing jobs, and all turnkey project solutions. We work in tandem with our customers through our service team to extract the best performance from our products. Undertake installation & inspection of wire ropes and crane wire ropes for different applications, including NDT, and conduct a wide range of training programs for customers. The company has established comprehensive service centres worldwide, equipped with advanced rigging facilities to offer customised solutions to our clients. This is further supported by a broad network of dealers, ensuring timely product delivery to customer sites.

Customer testimonials validate the quality proposition. We have been consistently using steel wire ropes manufactured by the Usha Martin Group since 2005. Over the years, their strong commitment to quality, reliability, and timely delivery has been truly commendable. With nearly two decades of experience working with their products, we can confidently recommend the Usha Martin brand for rope solutions across a wide range of applications.

The global wire rope market context provides perspective. The global wire-rope market size was valued at $9.1 billion in 2023, and is projected to reach $14.4 Billion by 2032, growing at a CAGR of 5.3% from 2024 to 2032. The wire rope encompasses the production, distribution, and utilization of a specialized type of cable constructed from multiple strands of metal wire twisted or braided together. These ropes find extensive application across various industries, including construction, mining, transportation, marine, and telecommunications. Wire ropes are known for their exceptional strength, durability, and flexibility, making them ideal for lifting, towing, and securing heavy loads in diverse environments.

The financial metrics confirm the operational turnaround. Mkt Cap: 10,594 Crore (up 3.61% in 1 year); Revenue: 3,535 Cr; Profit: 403 Cr While growth has been modest— The company has delivered a poor sales growth of 10.0% over past five years—the focus has been on profitability and financial health rather than aggressive expansion.

IX. Playbook: Business & Investing Lessons

The Usha Martin saga offers a masterclass in what to do—and especially what not to do—in building and managing an industrial enterprise. Each phase of the company's journey carries distinct lessons that transcend industry boundaries.

The Perils of Unrelated Diversification

Usha Martin's venture into steel manufacturing stands as a cautionary tale about the seductive logic of vertical integration. What seemed strategically sound—controlling your raw material supply—became an existential threat. The company needed 200,000 tonnes of steel annually for wire ropes but built capacity for one million tonnes. This wasn't vertical integration; it was unrelated diversification masquerading as strategic synergy.

The lesson is clear: backward integration only makes sense when the scale economics align with your core business needs. Otherwise, you're essentially running two separate businesses with different economics, capital requirements, and risk profiles. Usha Martin learned this lesson at a cost of nearly ₹4,000 crores in debt.

Family Business Governance: The Ticking Time Bomb

The Jhawar family feud reveals a structural problem in many Indian family businesses: governance structures that work in good times collapse under stress. Equal ownership (25.5% each faction) created deadlock precisely when decisive action was needed most. The boardroom battles between Basant-Prashant and Brij-Rajeev weren't just personality clashes—they reflected fundamentally different visions for the company's future.

The solution came from an unlikely source: the lenders. Banks, particularly SBI, effectively forced professionalization by backing the faction (Rajeev) they believed could execute a turnaround. The lesson? Family businesses need governance structures that can function especially during crisis, not despite it. Independent directors shouldn't be ceremonial—they should have real power to break deadlocks.

Strategic Divestment as Survival Tool

The sale to Tata Steel demonstrates that sometimes the best deal is admitting a mistake. Usha Martin's initial instinct—to sell the profitable wire rope business and keep the struggling steel division—shows how emotional attachment and sunk cost fallacy can cloud judgment. Rajeev Jhawar's decision to do the opposite, despite family opposition, saved the company.

The masterstroke was structuring the deal to maintain the supplier relationship. Usha Martin continued buying steel from its former division, now owned by Tata. This elegant solution preserved operational continuity while removing financial burden—a template for how to execute strategic retreats.

The Power of Focus

Post-divestment Usha Martin is a fundamentally different company. By returning to its core competence—wire ropes—the company rediscovered what made it successful in the first place. The improved margins, eliminated debt, and renewed growth demonstrate that in business, doing one thing excellently beats doing many things adequately.

Professional Management Transition

Vijay Singh Bapna's appointment as Chairman marked a crucial transition. Here was someone with no family ties, extensive turnaround experience, and credibility with institutional stakeholders. His presence gave comfort to lenders, investors, and customers that Usha Martin was serious about transformation.

The lesson extends beyond family businesses: when crisis strikes, bringing in outside expertise isn't admitting failure—it's acknowledging that different situations require different skills. The Jhawars' willingness to cede operational control while maintaining ownership showed maturity rare in Indian promoters.

Balance Sheet Transformation

Usha Martin's journey from ₹4,000 crores debt to debt-free status offers a playbook for financial restructuring: - Asset sales must be strategic, not desperate (waiting for the right buyer—Tata—rather than accepting the first offer) - Use proceeds to pare debt immediately, resisting temptation for new ventures - Focus on cash generation over growth until financial stability returns - Rebuild stakeholder confidence through consistent execution, not grand promises

Capital Allocation Discipline

The post-crisis Usha Martin shows remarkable capital allocation discipline. Instead of rushing back into expansion, the company focused on: - Operational excellence in existing facilities - High-margin value-added products - Working capital optimization - Selective international market development

This patience—choosing profitability over growth—reflects hard-won wisdom about the dangers of over-leverage.

Crisis as Catalyst

Perhaps the most profound lesson is that crisis, while painful, can catalyze necessary change. Without the debt crisis, the Jhawar family might never have professionalized management. Without the near-death experience, Usha Martin might have remained a subscale player in both steel and wire ropes, excellent at neither.

The company that emerged from crisis—focused, professionally managed, financially strong—is arguably better positioned than the pre-crisis version despite being smaller in revenue terms. Sometimes getting smaller is the path to getting stronger.

The Investor's Perspective

For investors, Usha Martin offers several lessons: - Turnaround situations require patience—the stock took years to recover - Management quality matters more in crisis than in growth phases - Balance sheet repair precedes earnings growth - Sometimes the best investments are in companies that have already made their biggest mistakes

The transformation from a complex conglomerate to a focused manufacturer, from family-dominated to professionally-managed, from debt-laden to debt-free, provides a template for evaluating similar situations. The key insight: successful turnarounds require not just financial restructuring but fundamental strategic and cultural change.

X. Analysis & Bear vs. Bull Case

The investment case for Usha Martin presents a fascinating study in contrasts—a company that has emerged from near-death but faces questions about its growth trajectory in a commoditizing global market.

Bull Case: The Renaissance Story

The optimists see Usha Martin as a classic turnaround story still in early innings. Q1 FY26: Revenue Rs.887.2 Cr (+7.4% YoY), PAT Rs.100.8 Cr, net debt eliminated, transformation progress. The debt-free balance sheet represents a complete reversal from the crisis years, providing flexibility for growth investments or returning cash to shareholders.

The valuation metrics suggest a quality business: P/E of 26.5, ROCE of 18.8%, ROE of 15.8%. These aren't the numbers of a commodity manufacturer but rather a specialized industrial company with competitive moats. The ROCE particularly stands out—generating 18.8% returns on capital employed in a manufacturing business indicates pricing power and operational efficiency.

Global infrastructure spending provides multi-decade tailwinds. India's ₹100 trillion infrastructure pipeline, China's Belt and Road Initiative, and developed markets' infrastructure renewal programs all require massive quantities of specialized wire ropes. Usha Martin's position as one of the few global-scale manufacturers positions it to capture disproportionate share.

The renewable energy transition opens new markets. Wind turbines require specialized cables for installation and maintenance. Offshore wind farms need marine-grade wire ropes that few manufacturers can produce. Solar farms require specialized lifting equipment during construction. These emerging applications offer higher margins than traditional uses.

Management quality has transformed. Under professional leadership, the company has shown discipline in capital allocation, focus on operational excellence, and willingness to invest in technology. The cultural transformation from family-run to professionally-managed is still yielding benefits.

The international footprint provides natural hedging. Manufacturing in India, Thailand, UK, and Dubai allows Usha Martin to serve local markets efficiently while managing currency and geopolitical risks. This global presence is expensive to replicate, creating barriers to entry.

Bear Case: The Structural Challenges

Skeptics point to structural headwinds that no amount of operational excellence can overcome. The company has delivered a poor sales growth of 10.0% over past five years. This anemic growth rate raises questions about whether wire ropes are a sunset industry facing technological disruption.

Chinese competition looms large. Chinese manufacturers, backed by state support and massive scale, continue to expand globally. Their willingness to accept lower margins pressures pricing across all markets. Usha Martin's premium positioning works in specialized applications but limits addressable market.

The commodity cycle exposure remains despite the steel divestment. Wire rope demand correlates strongly with mining, construction, and oil & gas capex—all highly cyclical industries. The next downturn could severely impact profitability even without the debt burden of the past.

Customer concentration risk persists. Large customers—mining giants, oil majors, infrastructure contractors—have significant negotiating power. The loss of a major customer or pressure on pricing from key accounts could materially impact margins.

Technology disruption threatens traditional applications. Synthetic ropes increasingly compete with steel in certain applications. Automation in ports and mining reduces demand for traditional wire rope applications. The elevator industry is exploring alternatives to steel cables.

Limited growth without acquisition. Organic growth in wire ropes is inherently limited by end-market growth rates. Without the balance sheet capacity or appetite for major acquisitions, Usha Martin may struggle to grow beyond GDP rates.

Promoter holding patterns raise governance concerns. Promoter Holding: 42.4% with recent decreases. The ongoing reduction in promoter holding could signal lack of confidence or preparation for exit, creating overhang on stock price.

ESG concerns in core markets. Mining and oil & gas—core customers—face increasing ESG scrutiny. Reduced investment in these sectors could structurally reduce demand for specialized wire ropes.

The Balanced View

The truth likely lies between these extremes. Usha Martin is neither a spectacular growth story nor a declining commodity producer. It's a specialized industrial company with strong market positions in niche applications, facing moderate growth but generating solid returns.

The company's transformation is real and substantial. Moving from near-bankruptcy to debt-free, from family feuds to professional management, from unfocused conglomerate to specialized manufacturer—these aren't cosmetic changes but fundamental restructuring.

Yet structural challenges are equally real. Five-year sales growth of 10% tells us this isn't a high-growth business. Chinese competition isn't disappearing. Technology disruption, while slow, is real.

The investment case may depend on time horizon and risk tolerance: - For value investors: A debt-free manufacturer trading at reasonable multiples with improving returns on capital - For growth investors: Limited organic growth potential may disappoint - For turnaround specialists: The heavy lifting is done; future returns will be more modest - For dividend investors: Strong cash generation and no debt could support attractive payouts

The key variables to monitor:

- Infrastructure spending in India and globally

- Pricing discipline despite Chinese competition

- Success in value-added products and new applications

- Capital allocation decisions with the debt-free balance sheet

- Any signs of promoter exit or strategic sale

XI. Epilogue & "If We Were CEOs"

Standing at the helm of Usha Martin today would be both exhilarating and daunting. The crisis has passed, the balance sheet is repaired, but the question remains: what next? The company that survived by shrinking must now figure out how to thrive through growing—but growing smart, not just growing big.

Technology and Innovation Leadership

The first priority would be establishing Usha Martin as the technology leader in wire ropes—a seemingly mundane product ripe for innovation. Consider the parallel with elevator cables: for decades, steel cables were the only option until Schindler introduced carbon fiber ropes, revolutionizing high-rise construction. Usha Martin needs its own revolutionary moment.

This means dramatically increasing R&D spending, currently modest for a company of this size. Partner with IITs and international universities on materials science research. Explore graphene-enhanced steel, smart ropes with embedded sensors for predictive maintenance, and bio-based alternatives for specific applications. The goal: make Usha Martin synonymous with wire rope innovation, commanding premium prices through technological differentiation.

Renewable Energy Platform

The energy transition represents a generational opportunity. Offshore wind farms require specialized mooring systems, installation cables, and maintenance equipment—all high-margin, technically demanding applications. Solar farms need specialized lifting equipment during construction. Battery factories require precision handling systems.

Create a dedicated renewable energy division with its own P&L, management team, and growth targets. Acquire a small European company specializing in offshore wind applications to gain technology and credibility. Set an audacious goal: 30% of revenues from renewable energy applications by 2030.

Consolidation Architect

The global wire rope industry remains fragmented despite consolidation pressures. Many family-owned manufacturers in Europe and North America face succession challenges. Asian producers outside China struggle with scale and technology access.

Position Usha Martin as the consolidator of choice. Use the debt-free balance sheet judiciously to acquire complementary businesses—not for scale but for technology, customer relationships, or geographic presence. Focus on $50-100 million acquisitions that can be easily integrated rather than transformational deals that risk repeating past mistakes.

Direct Customer Revolution

Currently, much of Usha Martin's business flows through dealers and distributors—necessary intermediaries but also margin eroders. The B2B world is finally embracing digital transformation, creating opportunities for direct customer relationships.

Build a world-class digital platform that allows customers to specify, order, track, and manage wire rope purchases directly. Provide real-time pricing, availability, and technical specifications. Add value through predictive maintenance algorithms, usage optimization tools, and lifecycle management services. The goal: become not just a supplier but an essential partner embedded in customers' operations.

Sustainability Leadership

ESG isn't just compliance—it's competitive advantage. Usha Martin should become the world's first carbon-neutral wire rope manufacturer. This isn't greenwashing but hard-nosed business strategy. Major mining companies and oil giants, under pressure from investors, increasingly prefer suppliers with strong ESG credentials.

Invest in renewable energy for manufacturing facilities. Develop recycling programs for end-of-life wire ropes. Create transparent supply chains with blockchain tracking. Publish detailed sustainability reports that become industry benchmarks. The premium for "green" wire ropes might be small initially but will grow as carbon taxes and regulations proliferate.

Service Transformation

Move beyond manufacturing to become a solutions provider. Don't just sell wire ropes—sell uptime, safety, and peace of mind. Offer comprehensive service contracts that include installation, inspection, maintenance, and replacement. Use IoT sensors to monitor rope condition in real-time, predicting failures before they occur.

This service transformation requires different capabilities—field service teams, software development, data analytics—but generates recurring revenues and deeper customer relationships. The model exists in other industries (Rolls-Royce's "Power by the Hour" for aircraft engines); adapt it for wire ropes.

Geographic Expansion 2.0

Unlike the previous international expansion focused on manufacturing, the next phase should be market-focused. Africa's infrastructure boom, Southeast Asia's urbanization, and Latin America's mining expansion all represent underserved markets.

But instead of building factories, establish technical centers that provide specification, training, and support. Partner with local distributors who bring market knowledge while Usha Martin provides technical expertise. The capital-light model reduces risk while capturing growth.

Cultural Revolution

Perhaps most importantly, complete the cultural transformation begun during the crisis. The company that was nearly destroyed by family feuds and poor governance must become a beacon of professional management.

Implement world-class talent management: recruit from IITs and global business schools, create clear career paths, link compensation to performance. Build a culture of innovation where failure is tolerated if it advances learning. Make Usha Martin the employer of choice for India's engineering talent.

The North Star

The vision would be clear: Transform Usha Martin from India's leading wire rope manufacturer to the world's most innovative industrial solutions company. Not the biggest—that game leads to commoditization. Not the cheapest—that race to the bottom destroys value. But the smartest, most innovative, most customer-centric.

In five years, success would mean: - 50% of revenues from products that don't exist today - EBITDA margins expanded by 500 basis points through mix shift to value-added offerings - Recognition as the technology leader through patents, publications, and customer testimonials - A services business generating 25% of profits - Acquisition of 3-5 strategic targets that accelerate capability building - Stock price appreciation that reflects transformation from manufacturer to solutions provider

The beauty of Usha Martin's position today is that the existential threats have passed. The company has earned the right to be ambitious again—but ambitious with wisdom, growth with discipline, expansion with focus. The next chapter isn't about survival but about defining what excellence looks like in an industry that most consider mature.

The wire rope might seem like yesterday's technology, but Usha Martin could make it tomorrow's solution. After all, every wind turbine, every skyscraper, every mine, every port still needs wire ropes. The question isn't whether demand will exist but who will capture the value in serving it. Coming from the brink of destruction, Usha Martin has the scars, the wisdom, and now the balance sheet to write its own future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube