Urban Company: The Full-Stack Revolution

I. Introduction: The "Amazon of Services"

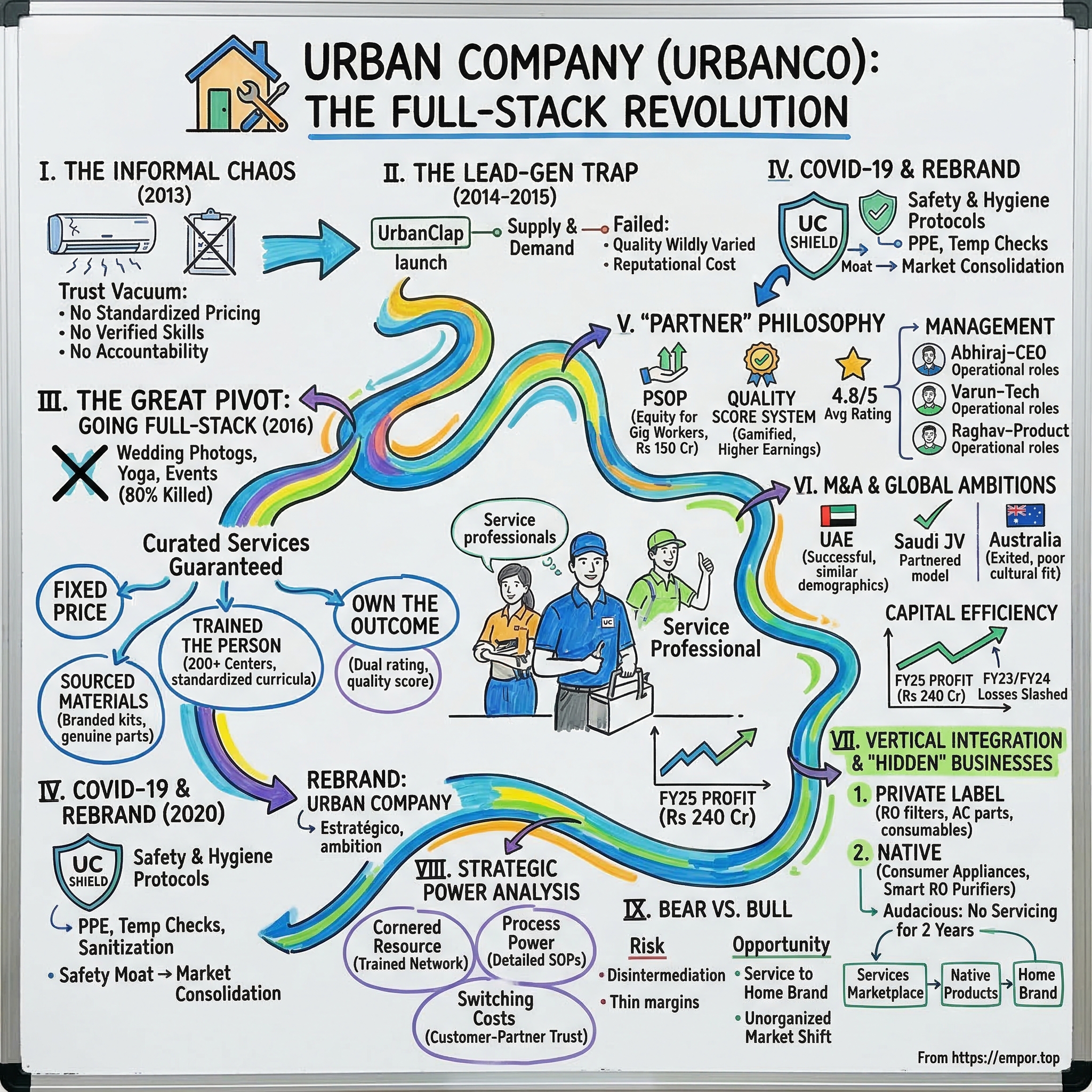

Picture Delhi in the summer of 2013. The mercury has crossed 45 degrees Celsius. Your air conditioner sputters, coughs, and dies. What do you do? You ask your neighbor, who asks his driver, who knows a guy from his village who "does AC work." That guy shows up three hours late, uses a counterfeit capacitor he bought from a back-alley market in Lajpat Nagar, charges you whatever number he feels like, and disappears. When the AC breaks again two weeks later, you have no recourse. No receipt. No warranty. No way to even find him again.

This was the reality for four hundred million Indian households. Home services — plumbing, electrical work, beauty treatments, appliance repair — operated in what economists politely call the "informal sector." In practice, it was a trust vacuum. No standardized pricing. No verified skills. No accountability. The entire industry ran on word-of-mouth referrals and prayers.

Fast forward to today. A consumer in Mumbai opens an app, books a salon-at-home appointment for 3 PM, and at 2:55 PM, a background-verified, company-trained beautician arrives in a branded uniform carrying a standardized kit of products — products that Urban Company itself manufactures. The service follows a precise checklist. The pricing was locked in at the time of booking. And if anything goes wrong, there is a warranty, a complaints mechanism, and a quality score system that determines whether that professional continues to get bookings.

The company behind this transformation, Urban Company, listed on the NSE in September 2025 under the ticker URBANCO, debuting at a 57% premium over its issue price. It commands a market capitalization of roughly $1.9 billion as of March 2026, operates across 51 cities, and has served over seven million customers through a network of more than 50,000 service partners. But what makes Urban Company genuinely interesting is not the scale — it is the thesis. The company's central argument, proven out over a decade of painful pivots, is that in emerging markets with broken infrastructure, you cannot be a thin digital layer sitting on top of chaos. You have to go deep. You have to fix the price, train the person, source the materials, and own the outcome. You have to go full-stack.

This is the story of how three founders who had each failed at their first startups came together to build India's most ambitious experiment in standardizing the unstandardizable — and why the lessons from that journey matter far beyond India's borders.

II. The Founding and The "Lead-Gen" Trap

Before there was Urban Company, there was CinemaBox. In early 2014, Abhiraj Singh Bhal and Varun Khaitan — both IIT Kanpur graduates from the 2005 batch who had gone on to work at Boston Consulting Group — teamed up to build a movie-streaming service for travelers. The idea was to let passengers on planes, trains, and buses stream films during their journeys. It was clever. It was technically interesting. And it died within six months because nobody wanted it badly enough to pay for it.

Meanwhile, halfway across the world, Raghav Chandra — a UC Berkeley computer science graduate who had been working as a software engineer at Twitter in San Francisco — was nursing his own failure. He had built Buggy, an on-demand auto-rickshaw hailing platform in India. It too had gone nowhere.

The three were introduced through mutual friends. What connected them was not just the shared sting of failure but a shared observation: India's consumer internet was exploding, but it was almost entirely focused on physical goods (Flipkart, Snapdeal) or food delivery (Swiggy, Zomato). The services economy — which employed tens of millions of people and generated hundreds of billions of dollars in economic activity — remained stubbornly offline.

In October 2014, they launched UrbanClap. The name was meant to evoke the idea of getting something done with a clap — instant, magical. The initial model was a horizontal marketplace, a kind of digital Yellow Pages on steroids. You could find a yoga teacher, a wedding photographer, a plumber, a pest control service, a makeup artist — all on one platform. The founders, shaped by the "Uber for X" zeitgeist that dominated Silicon Valley at the time, believed that the hard part was simply connecting supply and demand. Build the platform, let the professionals list themselves, take a referral fee, and let the magic of the internet do the rest.

It did not work. Or rather, it worked just well enough to be dangerous. Customers would book a service through UrbanClap, and the professional would either not show up, show up late, do mediocre work, or — most commonly — do acceptable work but at a quality level that varied wildly from one booking to the next. The fundamental problem was attribution of blame. When a plumber hired through UrbanClap botched a pipe repair, the customer did not think, "That plumber was terrible." The customer thought, "UrbanClap sent me a terrible plumber." The platform bore the reputational cost of quality failures it had no ability to control.

This was the lead-generation trap. In high-trust markets like the United States, a light-touch marketplace model could work. Thumbtack and TaskRabbit succeeded because the average American handyman had baseline certifications, insurance, and a cultural expectation of professional conduct. In India, where the services workforce was overwhelmingly informal, untrained, and unregulated, acting as a mere connector was a recipe for brand destruction.

The early funding came quickly — Accel Partners and SAIF Partners (now Elevation Capital) led a seed round in early 2015, followed by a $10 million Series A and then a $25 million Series B from Bessemer Venture Partners before the year was out. Ratan Tata himself made a personal angel investment in December 2015, lending the startup enormous credibility. But the founders knew, even as the money flowed in, that the model was fundamentally broken. Their Net Promoter Scores told a bifurcated story: categories where UrbanClap controlled the experience scored dramatically higher than categories where they merely connected buyer and seller. The data was unambiguous. The question was whether they had the courage to act on it.

III. The Great Pivot: Going Full-Stack

The meeting happened sometime in mid-2016. Abhiraj, Varun, and Raghav sat down with their category managers and looked at the data across every vertical UrbanClap operated in. The numbers painted a stark picture. In categories where the company set the price, trained the professional, and controlled the materials used — beauty services, primarily — customer satisfaction was high, repeat rates were strong, and unit economics were trending positive. In categories where they operated as a pure marketplace — wedding photography, yoga instruction, event planning — the metrics were mediocre at best.

The decision they made was radical. They killed roughly 80% of their categories. Overnight, UrbanClap went from being a platform that could connect you with practically any service professional to one that offered a curated, limited set of services — but with a guarantee of quality. Wedding photographers, yoga teachers, event planners: gone. What remained were categories where standardization was possible and where the company could genuinely own the outcome. Home repairs, appliance servicing, beauty and wellness, cleaning, painting.

But cutting categories was only the first step. The real transformation was in what "full-stack" actually meant in practice. Urban Company did not just connect you with a plumber and hope for the best. It fixed the price in advance so the customer knew exactly what they would pay. It trained the plumber at one of its physical training centers — eventually over 200 across India — using standardized curricula that could last anywhere from three days for basic skills to 45 days for complex specializations. It provided the plumber with a branded toolkit and, critically, with genuine spare parts sourced through the company's own supply chain. It tracked the plumber's performance through a dual rating system and a quality score that directly influenced future bookings and earnings.

This was not a marketplace anymore. This was a service company that happened to use technology as its distribution layer.

The contrast with American competitors is instructive. Thumbtack, founded in 2008, operates as a lead-generation platform to this day. A homeowner posts a job, professionals bid on it, and Thumbtack takes a fee for the connection. It works in America because the average contractor has a license, insurance, and years of training. TaskRabbit, acquired by IKEA in 2017, operates similarly — it connects you with a "Tasker" but does not train that person or control the quality of their work. These companies can afford to be thin digital layers because the underlying infrastructure of professional standards already exists in their markets.

In India, that infrastructure did not exist. Urban Company had to build it from scratch. The training centers were not a nice-to-have; they were the product. The company invested over Rs 72 crore (roughly $9 million) in training and skilling programs, turning raw recruits — many of whom had never held a formal job — into certified professionals. A beautician going through the Urban Company training program spent weeks learning not just technical skills but customer interaction, hygiene protocols, and the proper use of branded products. This investment created something that money alone could not replicate: a workforce with standardized, verifiable skills.

The venture capital community initially scratched its head. Training centers? Physical infrastructure? This was supposed to be a technology company. But Abhiraj and his co-founders understood something that many marketplace founders did not: in India, you could not separate the software layer from the physical reality it was supposed to digitize. If the physical reality was broken, no amount of elegant code would fix it. You had to get your hands dirty.

The bet paid off. By the end of 2016 and into 2017, nearly all of UrbanClap's competitors in the Indian home services space — Housejoy, LocalOye, TaskBob — had either shut down or contracted dramatically. Vy Capital led a $21 million Series C in June 2017, validating the full-stack thesis. The company had found its model. Now it needed to scale it.

IV. COVID-19 and The Rebrand: The Safety Moat

In January 2020, UrbanClap rebranded to Urban Company. The name change was strategic — "UrbanClap" was catchy but parochial, difficult to internationalize, and increasingly mismatched with a company that saw itself as far more than a clap-and-get-it-done marketplace. "Urban Company" signaled ambition: this was a company, not a gimmick. It was a platform for urban living, not a quirky app.

The timing, in retrospect, was almost tragicomic. Within weeks of the rebrand, COVID-19 arrived in India.

For a company whose entire business model depended on sending strangers into people's homes, the pandemic was an existential threat. Home services require physical presence. You cannot clean someone's house over Zoom. You cannot repair an air conditioner through a video call. When India went into its first nationwide lockdown in March 2020, Urban Company's revenue went to zero. Not close to zero. Zero. For approximately six weeks, the company had no business at all. Every service partner was at home. Every customer was behind a locked door. The app was functionally useless.

What happened next became, in the company's narrative, the defining moment of its evolution. Rather than hunker down and wait for the pandemic to pass, Urban Company went on offense. The team designed and implemented what they called "UC Shield" — a comprehensive set of safety and hygiene protocols that were unprecedented in the home services industry. Every service partner was required to wear PPE, including masks and gloves. Temperature checks were mandatory before and after every service. Sanitization kits were provided. Customers could verify their partner's health status through the app. The protocols were not voluntary suggestions; they were enforceable requirements, backed by the company's quality score system.

This might sound like basic common sense, but consider the alternative. The "local guy" — the informal plumber or electrician who had been doing this work for decades — had no access to PPE, no protocol for sanitization, and no institutional backing that could reassure a nervous homeowner. As lockdowns eased and life partially resumed, Indian consumers faced a choice: let the unverified local handyman into their home during a pandemic, or book through Urban Company and get someone who had been health-screened, equipped with PPE, and backed by a corporate safety guarantee.

It was not even close. Urban Company saw a massive consolidation of market share during and after the pandemic. The unorganized sector, which had always been the company's primary competitor, could not match corporate-grade safety standards. Consumers who had previously used local service providers switched to Urban Company and, critically, stayed. Repeat-user rates spiked. The pandemic, which could have destroyed the company, instead became its greatest competitive moat.

There was also a secondary effect. Categories that had never been particularly strong for Urban Company — sanitization, deep cleaning, disinfection services — suddenly became enormous. People who had never heard of Urban Company downloaded the app specifically to get their homes professionally sanitized. Once they were on the platform, many of them began using it for other services as well. The pandemic was both a crisis and the single most effective customer acquisition event in the company's history.

By the time India's vaccination drive was well underway and life returned to something approaching normalcy, Urban Company had emerged fundamentally stronger. The brand had become synonymous with trust in a world where trust in letting a stranger through your front door had been shattered and needed to be rebuilt. And the competitive landscape had been permanently altered — many informal service providers never came back to the market, having found other work during the extended lockdowns.

V. Management, Incentives, and The "Partner" Philosophy

The three founders of Urban Company remain deeply involved in the business. Abhiraj Singh Bhal serves as CEO and is the public face of the company — the one who does the media interviews, presents at investor conferences, and articulates the long-term vision. He brings the strategic rigor of a BCG consultant combined with the missionary zeal of someone who genuinely believes that what Urban Company does has social significance beyond its commercial value. Varun Khaitan oversees technology and operations, the engineering mind behind the platform's architecture and the operational systems that make the full-stack model work at scale. Raghav Chandra, with his Twitter engineering pedigree, leads the product organization, focused on the consumer experience and the increasingly sophisticated algorithmic systems that match customers with partners.

What is notable about the founding team is their staying power. In an Indian startup ecosystem where founder departures and co-founder conflicts are distressingly common, all three remain aligned and operational after more than a decade. Their combined shareholding, estimated at roughly 20-25% of the company, gives them significant skin in the game — they are not hired managers running someone else's company. They are owners.

But the most distinctive feature of Urban Company's approach to human capital is not how it treats its founders or its white-collar employees. It is how it treats its service partners — the 50,000-plus beauticians, plumbers, electricians, and cleaners who are the company's face to the consumer.

In March 2022, Urban Company announced the Partner Stock Option Plan, or PSOP. The plan allocated Rs 150 crore — approximately $20 million — worth of company stock to service partners at near-zero cost. This was, by the company's claim, a global first: gig workers receiving equity ownership in the platform they served on. The stock vests over five to seven years, with allocation determined by a combination of tenure on the platform and performance scores. An evergreen trust was established to manage the program, with an advisory panel ensuring transparent, rules-based allocation.

The cynical reading is that this is a retention tool dressed up as social innovation. In an industry with notoriously high churn — service workers regularly hop between platforms or return to informal work — giving partners a financial stake in the company's long-term success creates a powerful incentive to stay. The vesting schedule ensures that the most experienced, highest-performing partners are the ones most likely to remain on the platform, creating a virtuous cycle of quality improvement.

But the less cynical reading is also valid. Urban Company's service partners are overwhelmingly from lower-middle-class and working-class backgrounds. Many had never held a formal job before joining the platform. The PSOP gives these individuals — beauticians, plumbers, cleaners — something that white-collar tech workers take for granted: a stake in the value they help create. When Urban Company listed on the NSE in September 2025, those stock options became liquid assets. For some partners, the PSOP represented the single largest financial windfall of their lives.

Beyond equity, Urban Company uses a quality score system that functions as a sophisticated incentive mechanism. Every service partner's earnings, booking frequency, and access to premium time slots are determined by their quality score, which is itself a composite of customer ratings, adherence to SOPs, punctuality, and product usage compliance. Partners with higher scores get more bookings, better time slots, and higher earnings. Partners with declining scores get fewer opportunities and, eventually, face removal from the platform. The system effectively gamifies service quality, creating a relentless upward pressure on standards.

The result is visible in the numbers. Urban Company's average service rating hovers around 4.8 out of 5 — a figure that would be impressive for any consumer brand but is almost surreal for an industry that, a decade ago, had no rating system at all. The question for investors is whether this system can maintain its effectiveness as the partner base grows and as the company expands into new cities and categories where the training infrastructure is less mature.

VI. M&A: Global Ambitions and Capital Benchmarking

In March 2020, just as the world was locking down, Urban Company made its most adventurous move yet: it acquired Glamazon, an Australian on-demand beauty startup co-founded by Lauren Silvers and Lisa Maree. Glamazon had raised approximately $1.2 million in funding and had around 1,700 beauty professionals on its platform. The acquisition price was not disclosed but was believed to be in the range of $1-2 million — modest by any measure.

The thesis was straightforward. Australia had a well-developed beauty services market, high smartphone penetration, and affluent consumers willing to pay premium prices for at-home services. If Urban Company's full-stack model could work in India, surely it could work in a market with higher willingness to pay and a more developed consumer base.

It did not work. The problem was not execution; it was cultural fit. In India, salon-at-home services solved a genuine pain point — congested cities, long commutes, limited access to quality salons in many neighborhoods. In Australia, going to a salon was not a friction-filled experience. It was a pleasant outing. The value proposition of at-home beauty services was far weaker, and when COVID lockdowns in Australia's major cities made in-home services intermittently illegal, the unit economics collapsed entirely. Urban Company exited Australia in 2022, writing off the venture as an expensive lesson in market selection.

The contrast with the Middle East is striking. Urban Company entered the UAE in the second half of 2018, and Dubai quickly became its most successful international market. The reasons mirror India's: a transient expatriate population with limited local networks for finding service providers, extreme heat that makes traveling to physical service locations unappealing, and a culture that values at-home convenience. The demographics aligned perfectly with Urban Company's value proposition, and the UAE operation achieved strong economics.

Saudi Arabia presented a more complex challenge. The company initially operated through a wholly owned subsidiary, Urban Company Arabia (UCAIT), but navigating Saudi Arabia's regulatory environment and cultural norms proved difficult. In 2024, Urban Company restructured its Saudi operations through a joint venture with SMASCO, a local services conglomerate, forming Waed Khadmat Al-Munzal for Marketing Co., which launched in January 2025. The original Saudi subsidiary was approved for voluntary dissolution in November 2025. This was a pragmatic move — rather than burning capital trying to crack a complex market alone, the company partnered with someone who already had the local relationships and regulatory expertise.

The broader M&A record is notable for its restraint. Beyond Glamazon, the company made only two small acquisitions in 2016 — GoodService, a hyperlocal concierge app, and HandyHome, a home appliance repair company — both primarily acqui-hires to build out category expertise. Urban Company has grown overwhelmingly through organic means, building its training infrastructure city by city rather than buying its way into new markets.

On capital efficiency, the picture is compelling. Through the "funding winter" of 2022-2023, when global venture capital pulled back dramatically and many Indian startups faced existential crises, Urban Company raised virtually no new capital (only a nominal $144,000 angel round in June 2022). Instead, the company turned its India business EBITDA-positive by late 2022, slashed losses from Rs 308 crore in FY23 to Rs 93 crore in FY24, and then achieved its first full-year consolidated net profit of Rs 240 crore in FY25. The message was clear: this was a company that could survive — and thrive — without the life support of continuous venture capital infusions.

International revenue contributed approximately 13% of consolidated revenue in FY25, at Rs 147 crore out of a total Rs 1,144 crore. The near-term international story is one of disciplined expansion — doubling down on the UAE, entering Saudi Arabia through a joint venture model — rather than the aggressive, capital-intensive land grab that characterized the Australian misadventure.

VII. The "Hidden" Businesses: Vertical Integration

Sometime around 2018 or 2019, Urban Company's operations team noticed a pattern that was both alarming and revelatory. Service partners performing AC repairs and water purifier installations were sourcing spare parts from local markets — Bhagirath Palace in Delhi, Lamington Road in Mumbai — and many of those parts were counterfeit. Fake capacitors, knockoff RO membranes, substandard hair products. The customer received a service that looked professional (the partner arrived in uniform, followed the SOP, used the app) but was undermined at the last mile by a fake component that would fail within months.

This was not a quality problem that could be solved by training alone. It was a supply chain problem. And Urban Company solved it in the most direct way possible: it started sourcing and supplying the parts itself. The company built out a private-label product line for consumables used in its services — everything from hair wax and beauty products to RO filters, AC capacitors, and cleaning solutions. Service partners were required to use these products, which were sourced directly from manufacturers and quality-tested before distribution. The products were branded, often under the "UC" mark, and their use was tracked through the app.

This vertical integration into supply chain was not a glamorous business. It did not generate headlines. But it was quietly transformative. By controlling the inputs, Urban Company could finally guarantee the outputs. A customer booking an AC service knew that the parts installed were genuine, because the company itself had sourced them. The warranty on the service was meaningful because the company stood behind both the labor and the materials.

But the truly ambitious move came in October 2023, when Urban Company launched "Native" — its own line of consumer appliances. The first products were smart RO water purifiers, the Native M1 and M2, featuring ten-stage filtration (RO, UV, copper, alkaline, mineralizer), IoT connectivity through the UC app, and a design-forward aesthetic that would not look out of place in a premium kitchen. The key selling point was audacious: no servicing needed for two years or 12,000 liters, whichever came first. A two-year unconditional warranty was included, and installation was performed by UC-trained professionals.

The strategic logic is elegant. Urban Company had spent years building a services business around appliances made by other companies. Customers would buy a water purifier from Kent or Livpure, and when it needed servicing, they would book a UC partner. But Urban Company captured value only at the service layer — a relatively small, infrequent transaction. By manufacturing its own appliances, the company could capture value at the product layer (higher margin, larger transaction size) and then lock in the servicing relationship (recurring revenue, guaranteed through the two-year service-free design that still eventually requires filter replacement).

Think of it as the printer-and-ink model, but inverted. Instead of selling a cheap printer and making money on expensive ink cartridges, Urban Company sells a premium appliance and makes the servicing nearly free for two years — building trust and brand loyalty that ensures the customer comes back to UC for all their future home needs.

The early traction was encouraging. Native sold over 15,000 units in its first roughly four months, and the company struck a distribution deal with Blinkit for 30-minute delivery with installation within three hours. Segment-level data, while not fully disclosed, suggests that the product business operates at margins roughly double those of the pure services business. If Native can expand beyond water purifiers into other home appliances — air purifiers, washing machines, smart home devices — it represents a fundamental expansion of Urban Company's addressable market, from a services company to a home hardware brand.

This is the hidden business within Urban Company that many investors have not fully appreciated. The services marketplace is the company everyone sees. But the vertically integrated supply chain and the Native product line are where the highest-margin, most defensible value may ultimately reside. A customer who buys a Native water purifier, has it installed by a UC partner, monitors its performance through the UC app, and eventually gets it serviced by UC is a customer who has been captured across the entire value chain. That is not a marketplace relationship. That is brand ownership.

VIII. Strategy Analysis: Hamilton's 7 Powers and Porter's Five Forces

To understand Urban Company's competitive position, it is worth applying Hamilton Helmer's Seven Powers framework — the same analytical lens that Acquired.fm has used to evaluate companies from Netflix to Costco.

The most obvious power is what Helmer calls a Cornered Resource — an asset that a competitor cannot replicate simply by spending money. Urban Company's cornered resource is its network of 50,000-plus trained, background-verified, quality-scored service partners. Building this workforce took a decade. It required over Rs 72 crore in training investment, over 200 physical training centers, and a continuous process of recruitment, training, quality monitoring, and retention. A new entrant to the market cannot simply throw marketing dollars at the problem and expect to build a comparable workforce overnight. Training a beautician through the UC system takes weeks. Training a complex appliance repair specialist takes over a month. This is not a supply base that can be assembled through a marketing blitz — it is a painstakingly cultivated asset.

The second power is Process Power — the institutional knowledge embedded in the company's operating systems. Urban Company has, over ten years, developed detailed Standard Operating Procedures for every service category it offers. A home cleaning service is not performed ad hoc; it follows a specific sequence of steps, uses specific products in specific quantities, and is tracked and verified through the app. These SOPs represent thousands of iterations of testing what works, incorporating customer feedback, and refining the process. The result is that Urban Company has turned what were traditionally "craft" activities — cleaning, beauty treatments, appliance repair — into repeatable, factory-like processes. A new competitor would need years of operational learning to develop comparable SOPs.

The third power is Switching Costs. Once a customer has found a trusted UC partner — a beautician who knows their preferences, a plumber who is familiar with the layout of their home — they are significantly more likely to rebook with the same professional. The company's data suggests that rebooking rates exceed 70% for established customer-partner relationships. This creates a natural stickiness that goes beyond the app's convenience — it is a human relationship, mediated and guaranteed by the platform.

These are genuine, durable competitive advantages. But they are not invincible, and a clear-eyed assessment requires examining the competitive landscape through Michael Porter's Five Forces as well.

Barriers to Entry are high but not insurmountable. The physical training infrastructure, the trained partner network, and the brand trust built through COVID-era safety protocols create significant obstacles for new entrants. However, a well-capitalized "Super App" — Zomato, for instance, which already has Blinkit for quick commerce — could theoretically bundle home services into its existing platform, leveraging its massive consumer base and delivery infrastructure. The entry barrier is the training — you can acquire customers with marketing, but you cannot acquire quality service partners without time and investment.

Buyer Power is fragmented in Urban Company's favor. The company serves millions of individual consumers, none of whom represent a significant share of revenue. No single customer has the leverage to negotiate pricing. However, the consumers' collective voice — expressed through ratings, reviews, and churn behavior — exercises significant indirect power over the platform.

Supplier Power is the most nuanced force. Urban Company's "suppliers" are its service partners, and the relationship is complex. The partners depend on UC for bookings and income, but the most skilled, highest-rated partners have genuine alternatives — they could go independent, join a competitor, or build their own client base. The PSOP and the quality score system are, in part, designed to manage this supplier power dynamic, giving the best partners strong financial incentives to stay on the platform.

Threat of Substitutes remains the unorganized sector. For every service booked through Urban Company, hundreds of equivalent services are performed by informal workers found through word-of-mouth, WhatsApp groups, or society notice boards. These substitutes are typically cheaper, though they offer none of the quality guarantees, safety protocols, or recourse mechanisms that UC provides.

Competitive Rivalry is, at the moment, relatively low among organized players. Urban Company's early competitors — Housejoy, LocalOye, TaskBob — either shut down or became irrelevant years ago. NoBroker has expanded into home services from its real estate base, and HiCare operates in the niche pest control segment, but neither represents a full-stack competitive threat. The more serious competitive risk comes from the potential entry of Super Apps and from international players like Angi (formerly Angie's List) or platforms backed by large conglomerates.

IX. Bear vs. Bull Case

The Bear Case: Disintermediation and Platform Fragility

The most persistent bear argument against Urban Company is the disintermediation risk. The logic is simple: once a skilled beautician has visited a customer's home five or six times, the customer has the beautician's phone number. Why continue paying the UC platform fee when you can book directly? The relationship has been built; the trust has been established. The platform becomes unnecessary overhead.

This is not a theoretical risk. Anecdotal evidence from UC partners and customers suggests that off-platform transactions do occur, particularly for high-frequency services like beauty treatments. Urban Company combats this through a combination of sticks (partners caught transacting off-platform face score penalties and potential removal) and carrots (partners who stay on-platform benefit from the quality score system, the PSOP equity vesting, and guaranteed booking flow). But the bear case argues that as partners become more established and build their own reputations, the incentive to leave the platform grows stronger — and the best partners, the ones most valuable to UC, are precisely the ones with the strongest incentive to go independent.

There is also the margin concern. Urban Company's FY25 EBITDA margin of 1.1% — improved to 5.7% in Q1 FY26 — is positive but thin. The company is profitable, but it is not yet clear whether profitability at scale can reach the levels that would justify a P/E ratio north of 67x. The services business is inherently labor-intensive and local, which limits the operating leverage that technology companies typically enjoy.

The valuation itself warrants scrutiny. At roughly Rs 125 per share, the stock trades well below its 52-week high of Rs 201 but still at a significant premium to its IPO price of Rs 103. The P/E of approximately 67x and P/B of roughly 9x price the company for significant growth in both revenue and margins. If the Native product line does not scale as expected, or if the international expansion remains a modest contributor, the valuation could prove difficult to sustain.

Finally, the regulatory overhang. India's gig economy regulations are evolving, and there is ongoing debate about the classification of service partners — are they independent contractors or effectively employees? Any regulatory change that required Urban Company to provide benefits, minimum wages, or employment protections to its 50,000-plus partners would fundamentally alter the company's cost structure.

The Bull Case: From Service Marketplace to Home Brand

The bull case rests on the idea that Urban Company is in the early innings of a much larger transformation — from a service marketplace to the dominant home services and products brand in India and, eventually, in other emerging markets.

The Native product line is central to this thesis. If Urban Company can successfully expand from water purifiers into other home appliance categories, it creates a flywheel that no competitor can easily replicate. The customer buys a UC appliance, has it installed by a UC partner, monitors it through the UC app, and gets it serviced by UC. Every touchpoint in the appliance lifecycle generates revenue and reinforces brand loyalty. The product margins are substantially higher than service margins, and the recurring servicing relationship ensures ongoing customer engagement.

India's home services market is enormous and overwhelmingly unorganized. Estimates vary, but the addressable market for Urban Company's current service categories runs into tens of billions of dollars, with organized penetration still in the low single digits. Every percentage point of market share shift from the unorganized sector to organized platforms represents billions of dollars in revenue opportunity. And the shift is structural — India's growing urban middle class increasingly values time, convenience, and quality assurance over the marginal cost savings of informal services.

The international opportunity, while still nascent, offers a long runway. The UAE has proven that the model translates to markets with similar demographic characteristics, and the Saudi JV with SMASCO opens the largest economy in the Gulf region without the capital intensity of going it alone.

On valuation, international comps are instructive but imperfect. Angi, the US home services marketplace, trades at a significantly lower multiple but operates a lighter-touch model with lower growth rates. Meituan in China offers a closer analogy as a vertically integrated local services platform but operates at vastly greater scale. Urban Company's premium valuation is justified only if the company can demonstrate sustained revenue growth in the 30-40% range while expanding margins — a tall order but one consistent with the trajectory from FY23 to FY25, where revenue grew at a 53% CAGR while the company swung from deep losses to profitability.

KPIs to Watch

For investors tracking Urban Company's ongoing performance, two metrics matter above all others.

First, Revenue per Service Partner — this captures both demand density and pricing power. If UC can grow revenue without proportionally growing its partner base, it signals improving unit economics and demand concentration. Conversely, if revenue per partner stagnates or declines, it suggests the company is growing by adding bodies rather than by increasing the value extracted per relationship.

Second, Repeat Customer Rate — the percentage of bookings that come from returning customers versus new customers. This is the single best proxy for whether the full-stack model is actually delivering on its promise. High repeat rates mean customers trust the platform and find it indispensable. Declining repeat rates signal quality erosion or disintermediation. The company has historically reported strong repeat metrics, but maintaining them as the platform scales into new cities and categories is the critical test.

X. Conclusion and Playbook Lessons

There is a persistent myth in technology circles that the best companies are "capital-light" — that the winning strategy is always to build a thin software layer, avoid physical assets, and let other people do the hard work. Urban Company's story is a decade-long refutation of that myth.

In 2014, the founders tried the capital-light approach. They built a marketplace, connected buyers with sellers, and hoped that the internet's magic would take care of the rest. It did not. The quality gap was too wide. The trust deficit was too deep. The infrastructure that their software layer needed to sit on simply did not exist.

So they built the infrastructure themselves. They opened training centers. They developed SOPs. They sourced spare parts. They designed safety protocols. They manufactured appliances. At every step, the decision to go deeper — to move from platform to full-stack — contradicted the prevailing wisdom of Silicon Valley and Dalal Street alike. And at every step, it was the right decision.

The playbook lesson is not that every company should go full-stack. It is that in emerging markets where the underlying infrastructure of trust, quality, and standardization does not exist, you cannot be a thin digital layer. If you want to own the customer experience, you have to build the experience from the ground up. Urban Company trained the professionals, sourced the materials, set the prices, and built the brand. It went from three failed entrepreneurs in a small Delhi office to a publicly listed company that has — and this is not hyperbole — fundamentally changed the social standing and economic prospects of tens of thousands of service professionals across India.

Whether Urban Company can sustain its growth trajectory, expand the Native product line into a full home appliance brand, and successfully internationalize beyond the Middle East are open questions. The stock's journey from its IPO listing high of Rs 201 to its current level around Rs 125 suggests that the market is still calibrating its expectations. But the core thesis — that full-stack ownership of the home services experience creates durable, defensible value — has been proven.

The AC still breaks in Delhi. The summer heat has not changed. What has changed is that when it does, there is now a button to press, a trained professional who arrives on time, a genuine spare part in the toolkit, and a company that stands behind the outcome. That, in the end, is what "full-stack" means. Not a technology architecture. A promise.

XI. Top 5 Book and Resource References

-

The High Growth Handbook by Elad Gil — The practical blueprint for scaling startups from Series B through IPO, directly applicable to Urban Company's journey from a scrappy marketplace to a publicly listed company. Particularly relevant are Gil's frameworks on when to hire specialists versus generalists and how to navigate the organizational growing pains of rapid scaling.

-

7 Powers: The Foundations of Business Strategy by Hamilton Helmer — The analytical framework used throughout this analysis to evaluate Urban Company's competitive advantages. Helmer's concepts of Cornered Resource, Process Power, and Switching Costs map directly to UC's trained partner network, operational SOPs, and customer retention dynamics.

-

Urban Company's Annual ESG Report — The primary source for data on partner wealth creation, the PSOP program, and the company's social impact metrics. Essential reading for anyone who wants to understand how Urban Company quantifies its impact on the livelihoods of its service partners.

-

No Rules Rules: Netflix and the Culture of Reinvention by Reed Hastings and Erin Meyer — Urban Company's internal culture, particularly its emphasis on "talent density" and its willingness to make hard decisions (like killing 80% of its categories), draws heavily from Netflix's cultural philosophy. The parallels between Netflix's radical transparency and UC's data-driven quality scoring system are worth exploring.

-

The India Quotient — Research from Kamath Associates and other firms on the rise of India's urban middle class and the phenomenon of "time poverty" among dual-income households. This body of research provides the macroeconomic context for why home services platforms have enormous secular tailwinds in India — as incomes rise and time becomes scarcer, the willingness to pay for convenience and quality grows exponentially.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube