Universal Cables: The Story of India's Power Infrastructure Pioneer

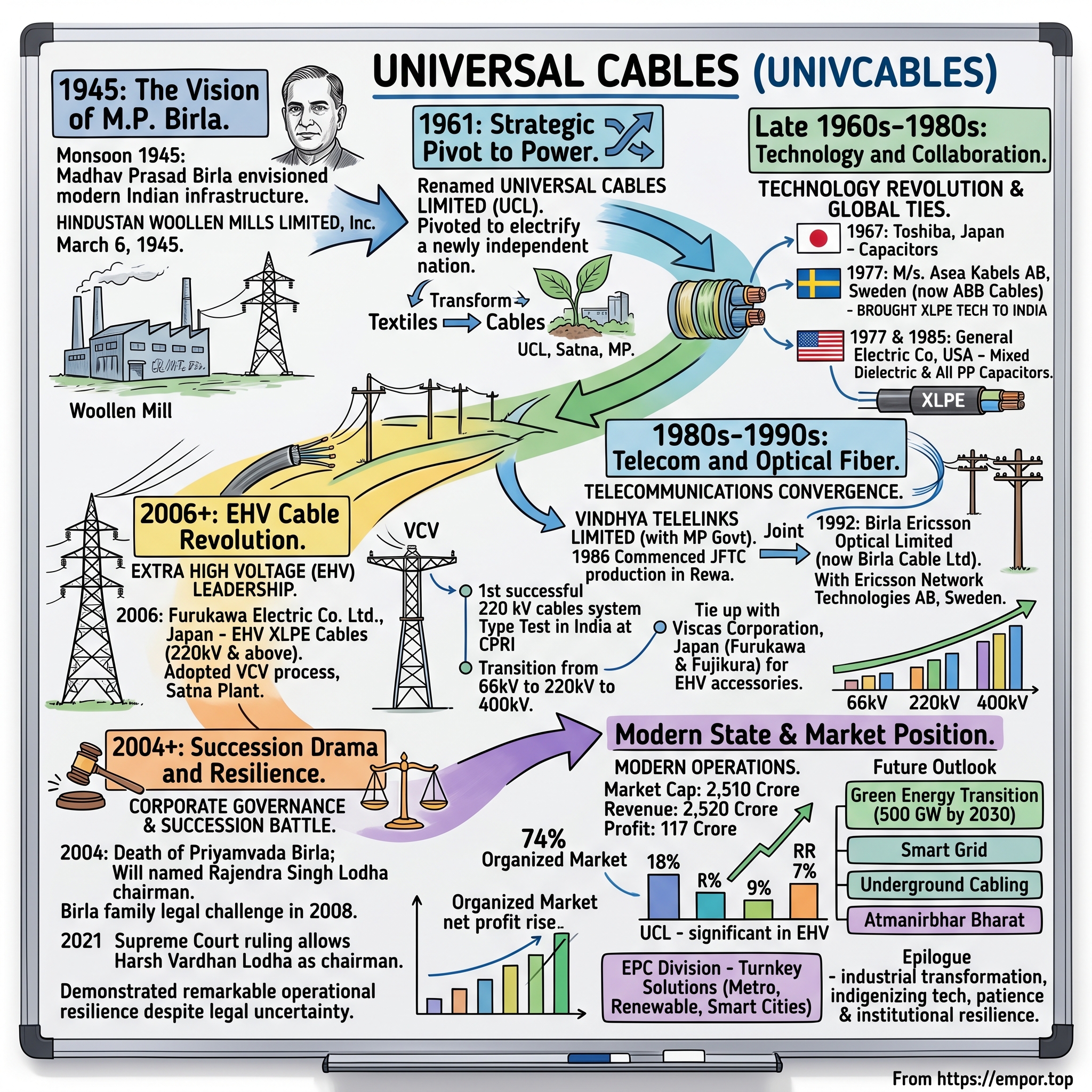

The monsoon of 1945 had just begun retreating from the Indian subcontinent when Madhav Prasad Birla, scion of one of India's most prominent business families, stood at the precipice of a transformative decision. With the Second World War drawing to a close and independence on the horizon, the thirty-something industrialist saw an opportunity that few others could envision—India would need more than political freedom; it would need the sinews of modern infrastructure to power its destiny. On March 6, 1945, in the industrial heartland of central India, he incorporated a company that would begin its journey as Hindustan Woollen Mills Limited. This wasn't just another venture for the Birla family empire; it was a calculated bet on India's industrial future.

The timing was audacious. While the rest of the country was consumed with the independence movement, M.P. Birla was already thinking about what would come after. The woollen mills venture, however, was merely a prologue to a much grander industrial narrative. By 1961, recognizing the shifting priorities of a newly independent nation hungry for electrification, the company shed its textile identity and emerged as Universal Cables Limited (UCL). This transformation wasn't cosmetic—it represented a fundamental reimagining of purpose, from clothing bodies to electrifying a nation.

The company was incorporated on March 6, 1945, and was promoted by M.P. Birla, initially known as Hindustan Woollen Mills Limited before being renamed Universal Cables Limited in 1961. The metamorphosis reflected the entrepreneurial agility that would become a hallmark of the M.P. Birla Group—the ability to read the tea leaves of economic change and pivot decisively.

What makes this origin story particularly compelling is its context within the broader M.P. Birla Group ecosystem. Madhav Prasad wasn't just building a cable company; he was constructing an industrial conglomerate that would touch everything from cement to jute, from chemicals to telecommunications. Universal Cables would become a crucial node in this network, benefiting from group synergies while maintaining its distinct technological edge. The company's registered office in P.O. Birla Vikas, Satna, Madhya Pradesh, would eventually become synonymous with cable manufacturing excellence in India, though few could have predicted this trajectory in those early days.

The M.P. Birla Legacy & Founding Vision

Universal Cables Limited was established in 1945 by late Shri M.P. Birla with a modern plant for manufacture of Paper Insulated Cables, though sources vary on whether the manufacturing facility was commissioned in 1962. The industrial landscape of post-independence India was dominated by a handful of visionary families, and among them, Madhav Prasad Birla occupied a unique position. Born into the illustrious Birla family in 1918 as the son of R.D. Birla, Madhav Prasad had inherited not just wealth but an industrial mindset that viewed business as nation-building.

The M.P. Birla Group's philosophy was distinctive—while other industrialists of the era focused on trading or single-industry dominance, Madhav Prasad believed in creating industrial ecosystems. Each company within the group wasn't an isolated entity but a complementary piece of a larger industrial puzzle. This approach would prove prescient as Universal Cables evolved, allowing it to leverage group resources for technology acquisition, financial muscle, and market access that standalone competitors couldn't match.

The initial focus on paper-insulated cables wasn't arbitrary. In the 1960s, this was the dominant technology globally for power transmission. The decision to establish manufacturing capabilities for these cables demonstrated remarkable foresight—India's Five Year Plans had begun emphasizing industrial development and rural electrification. The Satna plant location itself was strategic, situated in the mineral-rich region of Madhya Pradesh with access to raw materials and positioned to serve both northern and central Indian markets.

What distinguished M.P. Birla's approach was his insistence on technological excellence from day one. Unlike many Indian industrialists of the era who were content with trading or assembly operations, he invested in genuine manufacturing capabilities. The company's early focus on quality and technical standards would establish a reputation that would prove invaluable when seeking international collaborations in the decades to come. This wasn't just about making cables; it was about establishing India's credentials as a serious manufacturing destination.

The cultural DNA of the M.P. Birla Group—emphasizing long-term thinking, technological absorption, and reinvestment in capabilities—would profoundly shape Universal Cables' trajectory. When Madhav Prasad passed away in 1990, he left behind not just a company but an institutional framework that would enable it to navigate technological disruptions, market cycles, and even succession crises that lay ahead.

The Technology Revolution: XLPE & Global Collaborations

The year 1977 marked a watershed moment in Universal Cables' history, one that would fundamentally alter not just the company's trajectory but the entire Indian cable industry's technological landscape. In 1977, collaborating with M/s. Asea Kabels AB, Sweden (now called ABB Cables), UCL brought XLPE technology to India. This wasn't merely a technology transfer; it was a leap across generations of cable manufacturing capability.

To understand the magnitude of this shift, one must appreciate what XLPE (Cross-Linked Polyethylene) represented. Paper-insulated cables, the industry standard until then, had inherent limitations—susceptibility to moisture, limited temperature tolerance, and complex installation requirements. XLPE cables, by contrast, offered superior electrical properties, better thermal characteristics, lighter weight, and crucially, much easier installation and maintenance. It was the difference between telegraph and telephone, between propeller planes and jets.

The collaboration with Asea Kabels AB wasn't easily won. The Swedish company, a global leader in cable technology, had multiple suitors across Asia. What tipped the scales in Universal Cables' favor was the M.P. Birla Group's track record of successful technology absorption and its commitment to genuine manufacturing rather than mere trading. The negotiations, conducted over months of correspondence and site visits, involved not just commercial terms but detailed discussions about quality standards, training protocols, and market development strategies.

The Capacitor Division commenced operation in 1967 in collaboration with Toshiba, Japan for manufacture of Paper and Power Capacitors, and in 1977 entered into technical collaboration with General Electric Company of USA for Mixed Dielectric Capacitors and in 1985 for All PP Dielectric Capacitors. This multi-pronged approach to technology acquisition revealed a sophisticated strategy—rather than depending on a single technology partner, Universal Cables was building a portfolio of collaborations with global leaders across different product segments.

The implementation of XLPE technology at the Satna plant required massive investments in new equipment, extensive retraining of the workforce, and a complete reimagining of production processes. Swedish engineers spent months in Satna, working alongside Indian counterparts to ensure successful technology transfer. The first XLPE cable rolled off the production line in 1978 was more than a product—it was a symbol of India's growing technological capabilities.

What made Universal Cables' approach particularly successful was its emphasis on not just importing technology but indigenizing it. The company established dedicated R&D facilities to adapt XLPE technology to Indian conditions—the extreme heat of Rajasthan, the humidity of coastal regions, the unique requirements of Indian utilities. This localization capability would become a key differentiator, allowing Universal Cables to offer products better suited to Indian conditions than pure imports.

The Vindhya Telelinks Joint Venture & Group Expansion

The 1980s brought a new dimension to India's infrastructure ambitions—the telecommunications revolution was beginning to stir, and Universal Cables positioned itself at the forefront of this transformation. Vindhya Telelinks Limited was established as a joint venture between Universal Cables Limited and Madhya Pradesh State Industrial Development Corporation Limited, with its primary mandate to manufacture Jelly Filled Telephone Cables (JFTC), commencing commercial production at its Rewa plant in 1986.

The Vindhya Telelinks venture represented a new model of growth—leveraging public-private partnerships to enter emerging technology segments. The collaboration with the Madhya Pradesh government wasn't just about accessing capital or land; it was about aligning corporate strategy with state development priorities. The Rewa plant, constructed with machinery from global leaders like Maillefer of Switzerland and Pourtier of France, became a showcase of modern manufacturing in what was then considered a backward region.

The M.P. Birla Group, founded by Lt. Madhav Prasad Birla with Birla Corporation Ltd. established in 1919 as the flagship company, had come a long way and established leadership in several industries, with Birla Ericsson, Universal Cables, and Birla Furukawa Fibre Optics making the Group a dominating player in the Indian Cables industry. This expansion into telecommunications cables wasn't opportunistic but strategic—the group recognized that power and communication infrastructure would increasingly converge.

The technical complexity of jelly-filled telephone cables was considerable. These cables required precise control of insulation thickness, careful application of petroleum jelly for moisture protection, and sophisticated quality control to ensure signal integrity. The learning curve was steep, but Universal Cables' experience with technology absorption from the XLPE venture proved invaluable. The company didn't just transfer manufacturing equipment; it transplanted entire quality systems and process philosophies.

By 1992, recognizing the potential of optical fiber technology, the group made another bold move. Birla Ericsson Optical Limited (later renamed Birla Cable Limited) was established as a joint venture with Ericsson Network Technologies AB of Sweden. This wasn't just about manufacturing optical fiber cables; it was about positioning for the digital revolution that was still a decade away. The Swedish partner brought not just technology but also relationships with global telecom operators, opening export opportunities that purely domestic players couldn't access.

The synergies between Universal Cables, Vindhya Telelinks, and Birla Ericsson were carefully orchestrated. While each company maintained operational independence, they shared technical knowledge, customer relationships, and even manufacturing facilities where it made sense. A customer looking for a complete telecommunications infrastructure solution could find everything from power cables to optical fibers within the group—a one-stop-shop approach that proved highly successful in winning large projects.

The EHV Cable Revolution & Technical Leadership

As India entered the new millennium, its power transmission requirements were undergoing a fundamental shift. The old 66kV and 110kV transmission lines were proving inadequate for the country's growing energy needs. Universal Cables recognized this inflection point and made what would prove to be one of its most important strategic decisions. In 2006, Universal Cables entered into a technical collaboration agreement with Furukawa Electric Co. Ltd., Japan for making EHV XLPE Cables (220kV and above), adopting the VCV (Vertical Continuous Vulcanization) process at its Satna Plant, with the collaboration covering cable designing, manufacturing, laying, jointing, testing and installation.

The VCV technology represented a quantum leap in cable manufacturing capability. Unlike the conventional Continuous Catenary Vulcanization (CCV) process, VCV technology involved massive 120-130 meter high towers where cables were extruded vertically, allowing for superior molecular cross-linking and more uniform electrical properties. The investment required was staggering—not just in equipment but in creating an entire ecosystem of testing facilities, quality systems, and specialized workforce training.

The 220 kV Cables prototype sample manufactured by UCL has been successfully Type Tested as a complete cable system at CPRI, Bangalore creating a landmark as this is the first successful 220 kV cables system Type Test in India. This achievement wasn't just technical; it was symbolic of India's growing self-reliance in critical infrastructure technologies. The Type Test at Central Power Research Institute involved subjecting the cables to extreme conditions—high voltage impulses, thermal cycles, mechanical stress—over extended periods. Success meant that Indian-manufactured cables could now compete with the best in the world.

The progression from 220kV to 400kV capabilities didn't happen overnight. Universal Cables gradually transitioned from 66kV to 220kV, and subsequently to 400kV, a big leap for any Indian company in the extra-high voltage segment. Each voltage level brought exponential increases in technical complexity. The 400kV cables required insulation systems that could withstand electrical stresses that would instantly vaporize ordinary materials, joints that maintained perfect electrical continuity over decades, and installation procedures that resembled precision surgery more than construction work.

UCL also tied up with Viscas Corporation, Japan (Power Cable Alliance of Furukawa & Fujikura) for sourcing new generation cable jointing accessories for 220 kV and above. This partnership was crucial because in EHV systems, the cable joints are often the weakest links. A cable might perform perfectly, but a faulty joint could bring down an entire transmission line. Viscas brought decades of experience in developing joints that could match the cable's performance over its entire service life.

The EHV capability transformed Universal Cables from a commodity cable manufacturer to a technology leader. Utilities that previously had to import EHV cables at enormous cost and long lead times could now source them domestically. The company's order book swelled with prestigious projects—metro rail systems requiring specialized power cables, renewable energy projects needing sophisticated interconnection systems, smart cities demanding underground cable networks that wouldn't have been economically viable with imports.

The Succession Drama & Lodha Era

The early hours of July 3, 2004, marked the beginning of one of corporate India's most dramatic and protracted succession battles. When Priyamvada Birla died in 2004, she gave the Rs 5000 crore estate to her close accountant, Rajendra Singh Lodha, who became chairman of Birla Corporation, with the estate including key holdings in Birla Corporation, Vindhya Telelinks, and Universal Cables. The news sent shockwaves through Kolkata's business establishment and the broader Birla family constellation.

Priyamvada Birla, widow of M.P. Birla who had died in 1990, had run the group with a combination of strategic delegation and selective intervention. Her management style was unique—she rarely visited factories or attended operational meetings, preferring to work through trusted lieutenants while focusing on major strategic decisions. Rajendra Singh Lodha, a chartered accountant who had served the family for decades, had gradually become her most trusted advisor, eventually being appointed co-chairman of Birla Corporation in 2001.

The Birla family challenged the Lodha family in court in 2008 about the contents of the will, and the case changed course with the sudden death of RS Lodha in October 2008, after which his son Harsh Vardhan Lodha was to inherit the estates as declared in Priyamvada's will written in 1999. The legal battle that ensued would become one of the longest-running corporate succession disputes in Indian history.

For Universal Cables, this succession drama created a peculiar situation. On one hand, the company needed to continue its operational excellence and technological advancement. On the other, the uncertainty over ultimate ownership created challenges in long-term strategic planning and major investment decisions. Credit lines became more expensive as banks factored in governance risks. Joint venture partners expressed concerns about stability. Key executives wondered about their future.

On 19 September 2020, the Calcutta High Court ordered the removal of Harsh Vardhan Lodha from all directorships, but in July 2021, the Supreme Court ruled that Harsh Vardhan Lodha can continue as director and chairman in Birla Corporation, Universal Cables, Vindhya Telelinks and Birla Cable. This judicial seesaw created a complex operating environment where management had to navigate not just market competition but also legal uncertainty.

Despite the boardroom battles, Universal Cables demonstrated remarkable operational resilience. The company continued to win major orders, maintained its technology partnerships, and even expanded capacity during this period. This resilience can be attributed to several factors: the professional management layer below the board level that continued to function effectively, the strong institutional relationships built over decades that transcended ownership issues, and the technical competence that made Universal Cables indispensable to India's infrastructure buildout regardless of who sat in the chairman's office.

The Lodha era, despite its controversies, also brought certain positives. The family's chartered accountancy background meant rigorous financial controls and improved working capital management. The focus shifted from empire-building to optimization of existing assets. The company's financial performance during this period, while not spectacular, remained steady—a creditable achievement given the circumstances.

Modern Operations & Market Position

Today's Universal Cables operates in a dramatically different environment from its founding era, yet certain constants remain—the emphasis on technology, the focus on quality, and the ability to navigate complex market dynamics. With market capitalization of 2,510 Crore, revenue of 2,520 Crore, and profit of 117 Crore, Universal Cables has established itself as a significant player in India's electrical infrastructure sector.

The company's manufacturing footprint now extends across multiple locations, with the Satna facility remaining the crown jewel for EHV cable production. The product portfolio spans an impressive range—from basic low-voltage household wires to sophisticated 500kV XLPE cables that form the backbone of India's power transmission network. This breadth isn't just about variety; it's about maintaining relevance across the entire electrical value chain.

Recent financial performance shows resilience despite challenging conditions, with net profit rising significantly in certain quarters—for instance, a 488.73% increase to Rs 32.91 crore in the quarter ended June 2025 compared to the previous year, though full-year results show more volatility with sales rising 19.19% to Rs 2408.39 crore in the year ended March 2025. These numbers reveal a company navigating the cyclical nature of infrastructure spending with varying degrees of success.

The competitive landscape has intensified dramatically. In the organized segment controlling about 74% of India's wire and cable market, no single player tops one-fifth share, with Polycab leading at 18% market share, followed by KEI Industries at 9% and RR Kabel at 7%. Universal Cables, despite its technological prowess in the EHV segment, faces stiff competition from these larger players who have advantages in distribution reach, brand spending, and financial muscle.

However, the company faces challenges with poor sales growth of 8.95% over the past five years and a low return on equity of 6.57% over the last 3 years, though it maintains promoter holding at 61.9%. These metrics point to structural challenges—the EHV segment, while technically sophisticated, is project-based with long gestation periods and working capital intensity that pressures returns.

The Engineering, Procurement, and Construction (EPC) division has emerged as a crucial growth driver. Rather than just manufacturing cables, Universal Cables now offers complete turnkey solutions—from design and manufacturing to installation and commissioning. This evolution from product supplier to solution provider commands higher margins and creates stickier customer relationships. Major metro projects, renewable energy installations, and smart city initiatives increasingly prefer single-point accountability that the EPC model provides.

Technological capability remains the company's strongest differentiator. The R&D facility at Satna, recognized by the Ministry of Science & Technology, continues to develop new products suited to India's unique requirements. Recent innovations include cables designed for solar installations that can withstand extreme temperature cycling, specialized cables for electric vehicle charging infrastructure, and fire-resistant cables for critical installations like hospitals and data centers.

Playbook: Business & Strategic Lessons

Universal Cables' seven-decade journey offers rich lessons for understanding how industrial enterprises navigate technological discontinuities, market evolution, and governance challenges. The company's playbook reveals several strategic patterns worth examining.

The technology absorption strategy stands out as particularly sophisticated. Rather than pursuing the latest technology for its own sake, Universal Cables demonstrated remarkable discipline in selecting technologies that aligned with India's infrastructure evolution. The progression from paper-insulated cables to XLPE to EHV systems mirrors India's own development trajectory. Each technology adoption was timed to coincide with market readiness—too early would mean inadequate demand; too late would mean missing the opportunity window.

The approach to international partnerships reveals another layer of strategic thinking. Unlike many Indian companies that locked themselves into exclusive arrangements, Universal Cables maintained a portfolio of technology partners—Swedish for XLPE, Japanese for EHV, American for capacitors. This diversification provided negotiating leverage, access to best-in-class technologies across segments, and reduced dependency risks. The company also insisted on comprehensive technology transfer, including not just manufacturing know-how but also design capabilities, testing protocols, and installation expertise.

Capital allocation decisions reflect a conservative yet opportunistic philosophy. Major capacity expansions were undertaken only when demand visibility was clear—the EHV investment followed confirmation of government's transmission expansion plans, the optical fiber ventures coincided with telecom liberalization. This discipline helped avoid the overcapacity traps that plagued many infrastructure companies, though it may have also meant missing some growth opportunities.

The conglomerate structure, often criticized by modern management theory, proved advantageous in several ways. Cross-selling opportunities between group companies, shared technical knowledge, and financial support during cyclical downturns provided resilience that standalone competitors lacked. The ability to offer integrated solutions—power cables from Universal, telecom cables from Vindhya, optical fiber from Birla Cable—became a significant competitive advantage in large projects.

Managing cyclical demand in infrastructure required developing multiple coping mechanisms. The company maintained a diverse product portfolio to reduce dependence on any single segment. The EPC division provided some revenue stability through service contracts even when product sales were sluggish. Geographic diversification, though limited, helped smooth out regional variations in infrastructure spending. The focus on replacement and maintenance markets provided a baseline demand even during new project slowdowns.

The succession planning failure offers a cautionary tale that resonates across Indian family businesses. The lack of clear succession planning created nearly two decades of uncertainty that undoubtedly impacted growth potential. The legal battles consumed management attention, increased cost of capital, and made strategic partners wary. Yet the company's survival through this period also demonstrates the importance of institutional strength—robust systems, professional management, and strong customer relationships can sustain a business even through governance crises.

Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Applying Michael Porter's Five Forces framework to Universal Cables reveals a complex competitive landscape with both structural advantages and challenges. The supplier power in the cable industry is moderate to high, driven primarily by the commodity nature of key raw materials. Copper and aluminum prices, determined by global markets, can swing dramatically, and cable manufacturers have limited ability to pass through cost increases immediately due to contract structures and competitive pressures. However, Universal Cables' long-standing relationships with suppliers and group buying power provide some mitigation.

Buyer power presents a more challenging dynamic. The primary customers—government utilities, large contractors, and infrastructure developers—wield significant negotiating leverage. Purchase decisions for EHV cables often involve elaborate tendering processes where technical specifications are table stakes and price becomes the differentiator. The concentration of buying power in a few large utilities further strengthens their position. Universal Cables has attempted to reduce buyer power through the EPC model, which bundles products with services, making price comparisons more difficult.

The threat of substitutes remains relatively low in the core cable market—there simply aren't viable alternatives to cables for power transmission. However, technological evolution presents subtle substitution risks. Distributed generation through rooftop solar reduces the need for transmission infrastructure. Wireless technologies, while not substituting power cables, have dramatically impacted the copper telecom cable market. Universal Cables' diversification into optical fiber and specialized cables represents a response to these substitution dynamics.

New entrants face significant barriers in the EHV segment where Universal Cables has its strongest position. The capital requirements for VCV technology run into hundreds of crores. The technical expertise takes years to develop. Customer certifications and track records cannot be quickly established. However, in lower voltage segments, barriers are more surmountable, and new players, often backed by large conglomerates, continue to enter the market.

Competitive rivalry has intensified significantly over the past decade. The organized sector has consolidated around a few large players, each with distinct competitive strategies. Polycab leverages distribution strength, KEI focuses on project execution capabilities, while newer entrants like RR Kabel emphasize brand building and premiumization. Universal Cables' response has been to double down on technical differentiation in the EHV segment while maintaining presence across the value chain.

Hamilton Helmer's 7 Powers framework provides another lens to evaluate Universal Cables' competitive position. Scale economies clearly exist in cable manufacturing—the high fixed costs of equipment, technology, and certifications create cost advantages for larger players. Universal Cables benefits from scale in the EHV segment but lacks the overall scale of competitors like Polycab in the broader market.

Network effects are largely absent in the cable industry—one customer using Universal Cables doesn't make it more valuable for other customers. This absence of network effects means the company cannot rely on self-reinforcing growth dynamics and must win each customer through direct value proposition.

Counter-positioning opportunities exist in Universal Cables' focus on the EHV segment. While mass-market players optimize for volume and distribution, Universal Cables has built capabilities in high-voltage applications that require different manufacturing processes, quality standards, and technical expertise. This specialization creates a defensible niche, though the size of this niche limits growth potential.

Switching costs provide meaningful competitive advantage in the EHV segment. Utilities that have standardized on Universal Cables' products face significant costs in switching—new certifications, compatibility testing, retraining of maintenance staff, and risk of system integration issues. These switching costs are much lower in commodity cable segments, explaining why Universal Cables faces more competition there.

The "UNISTAR" brand carries weight in B2B segments where technical reputation matters. Decades of successful installations, particularly the landmark 220kV type testing achievement, have built credibility that new entrants cannot quickly replicate. However, brand power in industrial products is limited compared to consumer markets—technical specifications and price often outweigh brand considerations.

Cornered resources in the form of technical collaborations and certifications provide some competitive advantage. The relationships with Furukawa and Viscas aren't easily replicable—these partnerships were built over decades and involve deep technical integration. The various international certifications and approved vendor status with major utilities create barriers for competitors. However, these resources aren't truly "cornered" as competitors can, with time and investment, develop similar capabilities.

Process power, accumulated through 45+ years of manufacturing experience, represents Universal Cables' most sustainable advantage. The tacit knowledge embedded in manufacturing processes, quality systems, and technical problem-solving capabilities cannot be easily codified or transferred. This explains why even well-funded new entrants struggle to match Universal Cables' performance in sophisticated applications.

Bear vs. Bull Case

The bull case for Universal Cables rests on several structural factors that should drive long-term value creation. India's power infrastructure requirements remain massive—the government's target of 500 GW renewable capacity by 2030 will require enormous investments in transmission infrastructure. As renewable energy sources are often located far from consumption centers, high-voltage transmission becomes critical. Universal Cables, with its proven EHV capabilities, stands to benefit disproportionately from this transmission buildout.

The technology moat in the EHV segment provides pricing power and competitive insulation. With only a handful of domestic manufacturers capable of producing 400kV cables, Universal Cables operates in a quasi-oligopolistic market segment. The recent push for "Atmanirbhar Bharat" (self-reliant India) further advantages domestic manufacturers over imports. The company's complete solution capability—from manufacturing to installation—positions it well for complex infrastructure projects where execution capability matters as much as product quality.

Promoter holding at 61.9% demonstrates continued commitment despite the succession challenges, suggesting confidence in long-term prospects. The resolution of the Lodha succession dispute, while not ideal, at least provides clarity that was missing for years. The company's technical partnerships remain strong, with Japanese partners continuing to provide technology updates and support despite the governance uncertainty.

The expansion into adjacent segments like renewable energy cables, electric vehicle charging infrastructure, and data center cabling provides new growth avenues. These segments are growing faster than traditional power cables and offer better margins. The company's R&D capabilities and manufacturing flexibility allow it to quickly develop products for these emerging segments.

However, the bear case presents equally compelling concerns. The company has delivered poor sales growth of 8.95% over the past five years and maintains a low return on equity of 6.57% over the last 3 years. These metrics suggest structural challenges in converting technical capability into financial performance. The capital intensity of the EHV business means that even successful projects may not generate attractive returns on invested capital.

The governance overhang, while legally resolved, continues to impact corporate reputation and relationships. The two-decade-long succession battle has left scars—key executives who departed, partnerships that weren't renewed, investments that were deferred. Rebuilding institutional credibility takes time, and competitors have used this period to strengthen their own positions.

Working capital intensity remains a persistent challenge. Large infrastructure projects involve extended payment cycles, and Universal Cables often needs to fund significant working capital before receiving payment. This cash conversion cycle pressure limits the company's ability to invest in growth or return cash to shareholders. The situation is exacerbated by the bargaining power of large utility customers who can dictate payment terms.

Competition from larger, better-capitalized players poses an existential challenge in commodity segments. Polycab's distribution reach, Havells' brand power, and newer entrants' aggressive pricing make it difficult for Universal Cables to compete profitably outside its EHV niche. The company faces a strategic dilemma—abandoning lower-margin segments would reduce scale and increase dependence on cyclical EHV orders, but competing in these segments destroys value.

The cyclical nature of infrastructure spending adds another layer of risk. Government capex plans, while ambitious on paper, often face implementation delays due to land acquisition issues, environmental clearances, or funding constraints. A slowdown in infrastructure spending directly impacts Universal Cables' order book and capacity utilization. The company's operating leverage means that revenue declines translate into disproportionate profit impacts.

Technology disruption, while not immediate, looms as a long-term threat. Advances in superconducting materials, wireless power transmission, or distributed generation could fundamentally alter power infrastructure requirements. While these technologies are not commercially viable today, Universal Cables needs to invest in understanding and preparing for these potential disruptions, adding another cost burden.

Key Inflection Points & Future Outlook

The history of Universal Cables is punctuated by critical inflection points that fundamentally altered its trajectory. The 1977 XLPE technology introduction transformed the company from a commodity manufacturer to a technology leader. This wasn't just about new products; it established a template for technology absorption that would guide future expansions. The success of XLPE implementation gave Universal Cables credibility with international partners, opening doors for subsequent collaborations.

The 1986-1992 period of group expansion into telecom cables and optical fiber represented a strategic bet on convergence—the recognition that power and communication infrastructure would become increasingly interlinked. While this diversification added complexity, it also provided resilience during downturns in any single segment and created cross-selling opportunities that pure-play competitors couldn't match.

The 2004-2021 succession crisis, while disruptive, also revealed the company's institutional strength. The ability to maintain operations, retain key customers, and even expand capabilities during this period demonstrates that Universal Cables had evolved beyond dependence on any individual or family. The crisis forced professionalization of management and strengthening of systems that might not have occurred otherwise.

The 2009-2015 EHV capability building from 220kV to 400kV represents perhaps the most important technical inflection point. This progression established Universal Cables as one of the few Indian companies capable of supporting ultra-high-voltage transmission—a capability that becomes increasingly valuable as India's power consumption grows and transmission distances increase.

The post-COVID infrastructure boom and renewable energy push mark the most recent inflection point. The pandemic initially disrupted operations and delayed projects, but the subsequent government stimulus focused heavily on infrastructure development. The accelerated renewable energy adoption, driven by both policy push and improving economics, creates sustained demand for transmission infrastructure.

Looking ahead, several themes will likely shape Universal Cables' future. The green energy transition presents both opportunities and challenges. While renewable energy projects require extensive cabling, they also tend to be more price-sensitive than traditional utility projects. The company needs to develop cost-competitive products without compromising quality—a difficult balancing act.

Smart grid evolution will require new types of cables with embedded sensors, communication capabilities, and advanced materials. Universal Cables' R&D capabilities position it well for this transition, but significant investments in new technologies will be required. The company's collaboration with international partners becomes even more critical as smart grid technologies are still evolving globally.

The underground cabling trend in urban areas, driven by aesthetics, safety, and land constraints, favors Universal Cables' high-voltage expertise. Underground cables require superior insulation, thermal management, and installation expertise—all areas where the company has competitive advantages. However, underground projects also involve longer execution times and higher working capital requirements.

Make in India and import substitution policies create a favorable environment for domestic manufacturers. The government's focus on reducing import dependence in critical infrastructure provides both protection from international competition and pressure to continuously upgrade capabilities. Universal Cables needs to balance leveraging policy support with maintaining international competitiveness.

Digital transformation of power distribution, including technologies like digital twins, predictive maintenance, and AI-based grid optimization, will change how cables are designed, manufactured, and maintained. Universal Cables needs to develop digital capabilities not just in manufacturing but also in how it interfaces with increasingly sophisticated utility customers.

ESG compliance and sustainable manufacturing are becoming increasingly important for infrastructure suppliers. Universal Cables needs to invest in reducing its carbon footprint, developing recyclable products, and ensuring responsible sourcing of raw materials. These investments, while necessary, add to cost pressures in an already competitive market.

Epilogue & Takeaways

The story of Universal Cables is ultimately a narrative about industrial transformation in post-independence India. From its origins as a woollen mill in 1945 to becoming a provider of 400kV transmission systems, the company's evolution mirrors India's own journey from an agrarian economy to an emerging industrial power. The technical capabilities that Universal Cables built through patient collaboration with global partners helped establish India's credibility as a serious manufacturing destination, not just a market for foreign products.

The importance of technology partnerships in emerging markets cannot be overstated. Universal Cables' success in absorbing and indigenizing technologies from Sweden, Japan, and the United States provides a template for how developing country firms can climb the technology ladder. The key wasn't just licensing technology but building internal capabilities to adapt, improve, and eventually innovate. This approach required patient capital, long-term thinking, and willingness to invest in capabilities that might not generate immediate returns.

The succession planning failure offers sobering lessons for family businesses everywhere. The lack of clear succession planning didn't just create legal battles; it froze strategic decision-making for nearly two decades. The contrast between Universal Cables' technical excellence and governance challenges highlights how soft factors can undermine hard capabilities. Modern family businesses need to institutionalize succession planning long before it becomes necessary.

Viewing India's infrastructure story through the lens of Universal Cables reveals both achievements and missed opportunities. The company's technical successes in developing EHV capabilities demonstrate what Indian industry is capable of achieving. Yet the financial performance challenges highlight structural issues—fragmented markets, payment delays, and intense competition—that prevent technical excellence from translating into superior returns.

For investors, Universal Cables presents a complex proposition. The company possesses genuine technical capabilities and operates in segments with high entry barriers. The infrastructure buildout story in India remains compelling, and Universal Cables is well-positioned to benefit from transmission expansion. However, the financial metrics suggest that capturing value from these opportunities remains challenging. The company might be better viewed as a strategic asset—valuable for its capabilities and market position—rather than a pure financial investment.

For founders and managers, Universal Cables offers several key insights. First, technical capability alone doesn't guarantee financial success; it must be combined with operational excellence, financial discipline, and strategic clarity. Second, governance matters as much as strategy—the best-laid plans can be derailed by succession disputes or boardroom battles. Third, in cyclical industries, resilience matters more than growth—the ability to survive downturns determines long-term success.

The future of Universal Cables will likely be determined by its ability to navigate three transitions simultaneously: the technology transition to smart, sustainable infrastructure; the market transition from government-dominated to more diverse customer base; and the governance transition to professional management while retaining entrepreneurial agility. Success in any one dimension won't suffice; the company needs to excel across all three.

As India stands at the cusp of massive infrastructure expansion—500 GW of renewable energy, smart cities, electric vehicle charging networks, industrial corridors—companies like Universal Cables will play a crucial enabling role. The cables that Universal manufactures are more than copper and insulation; they are the arteries through which India's economic lifeblood flows. The company's journey from a small woollen mill to a provider of critical infrastructure encapsulates both the achievements and ongoing challenges of Indian industry.

The Universal Cables story ultimately reminds us that building industrial capabilities is a generations-long endeavor requiring patient capital, technology partnerships, and institutional resilience. While financial markets may focus on quarterly results, the real value creation in infrastructure businesses happens over decades. Universal Cables has survived and evolved through India's entire post-independence history. Whether it can thrive in India's next chapter remains an open question—one whose answer will be written in copper, aluminum, and optical fiber across the expanding infrastructure landscape of the world's most populous nation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube