Union Bank of India: From Gandhi's Blessing to Digital Banking Giant

The Paradox of Modern India

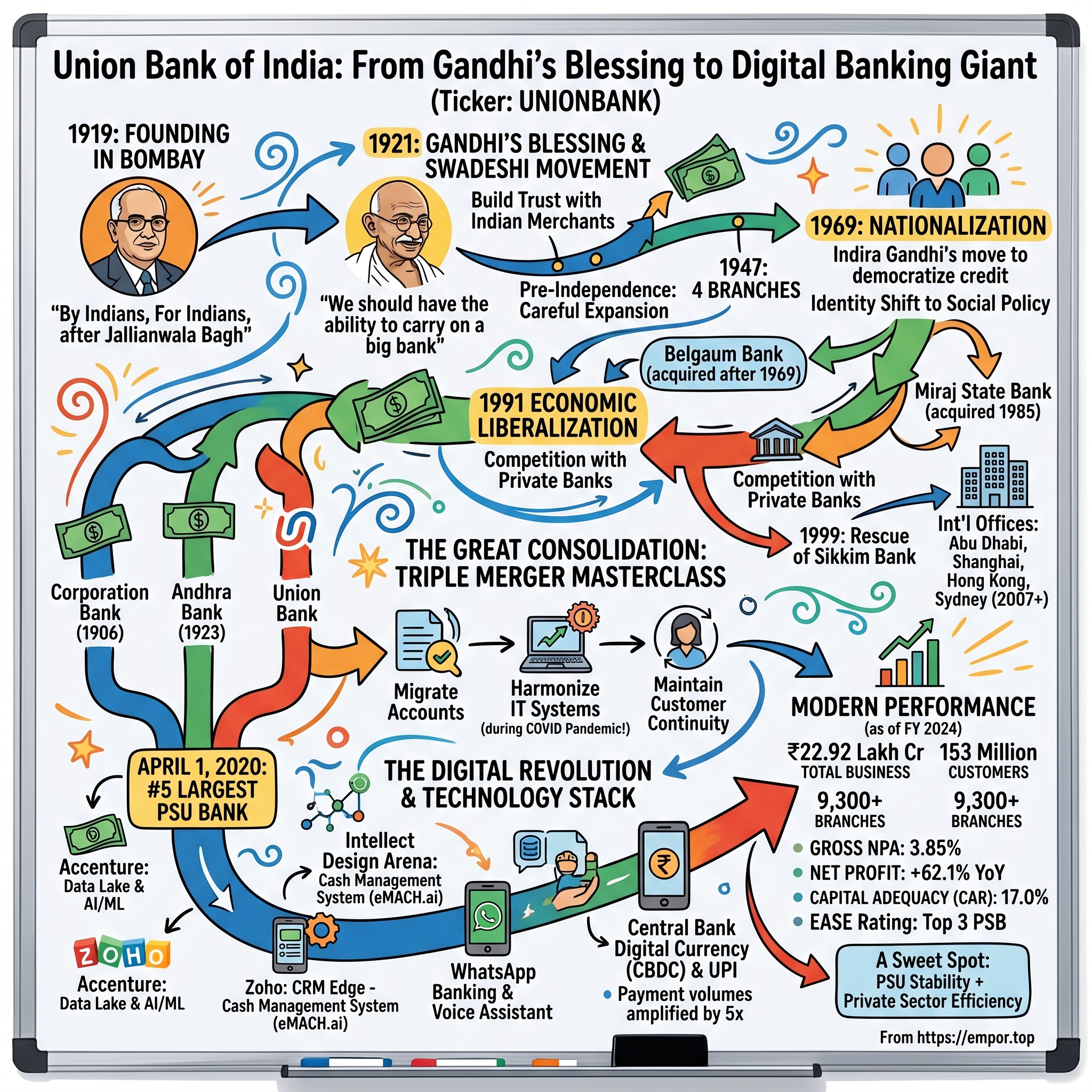

The year is 1921. In a modest building in Bombay, an elderly man in simple white khadi steps forward to address a small gathering of merchants and traders. His voice, though soft, carries the weight of a nation's aspirations. "We should have the ability to carry on a big bank," Mahatma Gandhi declares, "to manage efficiently crores of rupees in the course of our national activities." The handful of people present that day could hardly imagine that the single-branch institution they were inaugurating would, a century later, manage assets worth ₹22.92 lakh crore and serve 153 million customers through artificial intelligence and blockchain technology.

This is the story of Union Bank of India—perhaps the only major financial institution in the world that can claim both Gandhi's blessing and a cutting-edge AI-powered banking platform. It's a tale that spans from the Swadeshi movement to WhatsApp banking, from four branches at independence to becoming India's fifth-largest public sector bank through one of the most audacious merger strategies ever executed during a global pandemic.

The central question isn't just how a bank survives for 105 years—plenty of institutions manage that through sheer inertia. The real mystery is how an organization born in the colonial era, nationalized under socialist policies, and burdened with the legacy systems of three merged entities managed to transform itself into what industry observers now call "the most tech-forward PSU bank in India." This transformation didn't happen through Silicon Valley-style disruption or venture capital injections. It happened through something far more difficult: systematically reimagining a century-old institution while serving the daily banking needs of millions of Indians, from rural farmers to multinational corporations.

Pre-Independence Origins & The Gandhi Connection

The story begins not in a boardroom but in the bustling lanes of Bombay's commercial district, where Seth Sitaram Poddar, a visionary merchant, recognized a fundamental problem: Indian traders and small businessmen were systematically excluded from the formal banking system dominated by British institutions. On November 11, 1919, just months after the Jallianwala Bagh massacre had inflamed nationalist sentiment across India, Poddar established Union Bank of India in Bombay (now Mumbai) with a radical proposition—a bank by Indians, for Indians.

What made Union Bank extraordinary wasn't just its founding mission but who blessed its journey. The Head Office was inaugurated by Mahatma Gandhi in 1921, making it perhaps the only major financial institution in the world to carry such a distinction. Gandhi's presence wasn't ceremonial; it was deeply strategic. The Swadeshi movement was gaining momentum, and economic independence was increasingly seen as inseparable from political freedom. When Gandhi stood before the assembled merchants and declared, "We should have the ability to carry on a big bank, to manage efficiently crore of rupees in the course of our national activities", he was articulating a vision that went beyond banking—he was talking about nation-building through financial sovereignty.

The early years under European management (a pragmatic necessity given the expertise required) were marked by careful expansion and trust-building. The bank's initial focus on small traders and businessmen wasn't just a market segment; it was a political statement. While British banks served the colonial administration and large European trading houses, Union Bank quietly built relationships with the Indian merchant class who would become the backbone of independent India's economy. At the time of India's independence in 1947, the bank had four branches—three in Mumbai and one in Saurashtra in trade centres. This modest footprint reflected both the cautious expansion strategy of the pre-independence era and the fundamental challenge facing Indian banking: how to serve a vast, largely rural population with limited infrastructure and even more limited capital. The contrast with today's scale is staggering—from four branches to over 9,300, from serving a few thousand customers to 153 million. But understanding this transformation requires examining the political earthquake that reshaped Indian banking in 1969.

Nationalization & The Socialist Banking Era

By the time the Indian government nationalized UBI in 1969, it had grown to 240 branches—a sixty-fold increase from independence, yet still a drop in the ocean of India's banking needs. The nationalization wasn't just a policy decision; it was Indira Gandhi's bold gambit to democratize credit and break the nexus between big business and private banks. For Union Bank, this meant a fundamental identity shift from a commercial institution to an instrument of social policy.

The immediate post-nationalization period saw Union Bank embrace its new mandate with remarkable vigor. Shortly after nationalisation, Union Bank of India acquired Belgaum Bank, a private sector bank established in 1930 that had itself merged with the Shri Jadeya Shankarling Bank (Bijapur; incorporated on 10 May 1948) in 1964. This wasn't mere expansion—it was strategic consolidation, absorbing regional players who understood local markets but lacked the scale to survive independently.

In 1985, Union Bank of India acquired Miraj State Bank, which was established in 1929, and had 26 branches. These acquisitions revealed an emerging playbook: identify struggling regional banks with established customer relationships, integrate their operations, and leverage the combined entity's scale to serve previously unbanked populations. This strategy would prove prescient decades later during the mega-merger era.

The License Raj period imposed unique challenges and opportunities. As a PSU bank, Union Bank became the government's vehicle for priority sector lending—agriculture, small-scale industries, and export credit. Branch managers weren't just bankers; they were development officers, tasked with identifying local entrepreneurs and facilitating credit to sectors private banks wouldn't touch. The culture that emerged was distinctive: part banker, part social worker, entirely committed to the notion that banking was a public service rather than a profit center.

This era also saw the formation of what insiders called the "Union Bank way"—a management philosophy that emphasized relationship banking over transaction banking, patient capital over quick returns, and social impact over pure profitability metrics. While critics would later argue this approach created inefficiencies and bad loans, it also built something invaluable: deep trust among India's middle class and small business community. This trust would become Union Bank's most enduring asset.

Liberalization & Finding Identity

The 1991 economic reforms hit India's public sector banks like a cold shower. Foreign banks were suddenly allowed to expand operations, new private sector banks emerged with better technology and aggressive marketing, and customers who had no choice but to queue at PSU banks suddenly had options. For Union Bank, this period represented an existential crisis wrapped in operational challenges.

The technology gap was particularly acute. While ICICI and HDFC were building operations on modern core banking systems, Union Bank was still reconciling ledgers manually across hundreds of branches. The bank's first major technology initiative—implementing core banking solutions—took nearly a decade to complete, a timeline that would be unthinkable in today's digital environment. Branch managers resisted computerization, fearing job losses. Unions protested. Customers, paradoxically, missed the personal touch of passbook updates by hand.

Yet this challenging period also revealed Union Bank's resilience. In 1999, the Reserve Bank of India requested that the Union Bank acquire Sikkim Bank in a rescue after extensive irregularities had been discovered at the non-scheduled bank. This wasn't a strategic acquisition but a rescue operation—the RBI essentially asking Union Bank to clean up someone else's mess. The successful integration of Sikkim Bank's eight branches demonstrated something crucial: Union Bank had developed the institutional capability to absorb and rehabilitate troubled entities, a skill that would prove invaluable two decades later.

The international expansion beginning in 2007 marked a new chapter. Union Bank expanded internationally in 2007, with the opening of offices in Abu Dhabi, United Arab Emirates, and Shanghai in the People's Republic of China. The following year saw the establishment of a branch in Hong Kong, and by 2009, Sydney was added to the network. This wasn't vanity expansion—it was strategic positioning to serve the Indian diaspora and facilitate trade finance for Indian corporates going global. The timing, just before the 2008 financial crisis, seemed unfortunate, but it actually provided Union Bank with a crash course in international risk management that domestic-only banks missed.

The period from 1991 to 2008 was essentially Union Bank's adolescence—awkward, sometimes painful, but ultimately transformative. The bank that emerged was neither the simple community lender of the pre-nationalization era nor the government policy tool of the License Raj. It was something new: a public sector bank that understood it needed to compete like a private player while maintaining its social mandate. This dual identity would define everything that followed.

The Great Consolidation: Triple Merger Masterclass

The announcement came on August 30, 2019, but the timing couldn't have been worse—or perhaps, more perfect depending on your perspective. Finance Minister Nirmala Sitharaman's declaration that Corporation Bank and Andhra Bank merger with Union Bank of India, which will take place on April 1, 2020, was one of the most important mergers during this phase landed just as the Indian economy was slowing and months before anyone had heard of COVID-19.

The numbers were staggering: the proposed merger would create India's fifth-largest public sector bank with assets of ₹14.59 lakh crore and 9,609 branches. But numbers tell only part of the story. This was essentially asking three distinct organizations—each with its own century-long history, culture, and operating philosophy—to become one entity overnight. Corporation Bank, founded in 1906 in coastal Karnataka, had built its reputation serving small traders and agriculturalists. Andhra Bank, established in 1923, was deeply rooted in the Telugu-speaking regions with a strong presence in rural and semi-urban areas. Union Bank brought its Mumbai-centric commercial banking heritage. Three cultures, three systems, three philosophies—one bank.

The share exchange mechanics revealed careful calibration: 325 equity shares of the face value of Rs.10 each fully paid up in Union Bank of India for every 1,000 equity shares of the face value of Rs. 10 each fully paid up held in the Andhra Bank as on the record date, with Corporation Bank shareholders receiving 330 shares per 1,000. These ratios weren't arbitrary—they reflected intricate valuations balancing book value, market price, and future earnings potential.

Then COVID-19 hit. Physical certificates were delayed due to COVID-19-related postal suspensions, but that was the least of the challenges. Imagine trying to integrate three massive IT systems when your technology teams can't meet in person. Or harmonizing HR policies when offices are locked down. Or training thousands of employees on new processes through video calls. The merger officially took effect on April 1, 2020—precisely when India entered one of the world's strictest lockdowns.

MD & CEO Rajkiran Rai G.'s leadership during this period deserves its own case study. While other banks were simply trying to keep branches operational during the pandemic, Union Bank was simultaneously: migrating millions of customer accounts, integrating three core banking systems, rationalizing overlapping branches, harmonizing thousands of products, and reassuring nervous employees about job security—all while managing the surge in digital banking demand as customers avoided physical branches.

In a challenging period of the COVID pandemic, UBI has been able to record deposit growth at 6.35%. The Advances growth was negative at -1.87%, though the retail advances recorded a growth of 10.49%. UBI has been able to reduce its NPA to 4.62% (March 21) from 5.22% (March 20). These numbers, achieved during the first year post-merger amid a global pandemic, represent something close to a miracle in banking integration.

The cultural integration proved even more complex than the technical challenges. Corporation Bank employees, accustomed to their institution's conservative, community-focused approach, suddenly found themselves part of a Mumbai-headquartered behemoth. Andhra Bank's strong regional identity had to be preserved while creating a unified national presence. Union Bank's own employees had to adjust from being the acquirer to being part of a merged entity where they were now a minority.

The masterstroke was the decision to maintain continuity for customers: Account numbers, IFSC codes, MICR codes, and branch operations remained unchanged post-merger. Customers were advised that their banking relationships would continue seamlessly under the umbrella of Union Bank of India. This "no disruption" promise, nearly impossible to execute in practice, became the north star guiding every integration decision.

By any measure, pulling off this three-way merger during a pandemic should have been impossible. That it succeeded—creating a stable, functioning entity that immediately began improving its metrics—stands as perhaps the most impressive operational achievement in Indian banking history. The merger didn't just create a larger bank; it proved that Indian public sector banks could execute complex transformations under the most adverse circumstances imaginable.

The Digital Revolution & Technology Stack

The transformation began quietly in December 2023 when Union Bank of India, a leading public sector bank in India is collaborating with Accenture (NYSE: ACN) to design and develop a scalable and secure enterprise data lake platform with advanced analytics and reporting capabilities. This wasn't just another IT project—it was a fundamental reimagining of how a century-old institution processes information. Using predictive analytics, machine learning and artificial intelligence, this platform will leverage structured and unstructured data from within the bank as well as from external sources to generate business-relevant insights.

What makes Union Bank's digital journey remarkable isn't the technology itself—plenty of banks have data lakes and AI capabilities. It's the velocity and ambition. Consider the implementation of Intellect's Cash Management System: The implementation of PWT commenced on June 19, 2023, and successfully went live in approximately five months, setting a new standard in the industry. Five months. For context, similar implementations at global banks typically take 18-24 months. This wasn't recklessness; it was the product of an organization that had learned, through its merger experience, how to execute complex transformations at unprecedented speed. The partnership between Union Bank of India and Zoho began in 2021 after the merger of Andhra Bank and Corporation Bank with Union Bank of India, which significantly expanded its operations. Since its rollout in 2023, CRM Edge has rapidly become the Bank's primary customer engagement tool and is widely used across the Bank. Automation has streamlined 90-95% of customer query processes, improving internal task management and response times, resulting in greater operational efficiency and higher customer satisfaction.

The technology stack reveals sophisticated thinking about digital architecture. Rather than pursuing a monolithic transformation (the approach that has killed countless bank IT projects), Union Bank opted for a best-of-breed strategy: Accenture for data and AI, Intellect for transaction banking, Zoho for customer relationship management. Each partner brought specific expertise, but more importantly, each system was designed to integrate seamlessly with the others through API-first architecture.

The WhatsApp banking and voice assistant capabilities represent the visible tip of a massive technological iceberg. Behind these consumer-facing innovations lies a complete reimagining of how the bank processes transactions. Payment volumes have amplified by 5x—not through incremental improvements but through fundamental re-engineering of the payment infrastructure. The bank's integration with India's Central Bank Digital Currency (CBDC) and UPI interoperability positions it at the forefront of the country's digital payment revolution.

What's particularly striking is how Union Bank has transformed its relationship with technology vendors. As Sridhar Vembu, Co-founder and CEO of Zoho Corporation, noted: "Our platform's flexibility allowed us to co-create a customised solution that seamlessly integrates with Bank's IT infrastructure, empowering Union Bank to drive its digital transformation with full control over it technology stack while reducing reliance on external vendors." This co-creation model—where the bank maintains strategic control while leveraging vendor expertise—represents a sophisticated approach to technology partnership that many Silicon Valley companies would struggle to execute.

The digital transformation hasn't just improved operational metrics; it's fundamentally changed how Union Bank competes. In the EASE (Enhanced Access & Service Excellence) ratings amongst all PSBs, Union Bank has consistently ranked in the top three, competing effectively with banks that never had to manage legacy system integration or merger complexities. The bank that was once seen as a laggard in technology adoption has become what industry observers now call "the most digitally advanced PSU bank in India."

Modern Performance & Market Position

The numbers tell a remarkable turnaround story. UNION BANK's gross NPA ratio stood at 4.8% as of 31 March 2024 compared to 7.5% in the same period a year ago. The net NPA ratio of UNION BANK was 1.0% in financial year 2024. This compared with 1.7% a year ago. These aren't just incremental improvements—they represent a fundamental shift in asset quality achieved during one of the most challenging economic periods in recent history.

Net profit for the year increased by 62.1% YoY. That's not a typo—a 62% increase in profitability at a time when most global banks were struggling with margin compression and credit losses. Capital Adequacy Ratio (CAR): UNION BANK's capital adequacy ratio (CAR) was at 17.0% as on 31 March 2024 as compared to 16.0% a year ago. This capital buffer, well above regulatory requirements, provides the firepower for future growth while maintaining a safety margin that would make even conservative regulators comfortable.

The latest quarterly results reinforce this momentum. The asset quality profile improved, with gross NPAs declining to 3.85 per cent in December 2024 from 4.83 per cent in December 2023. Net NPAs also declined to 0.82 per cent in December 2024, compared to 1.08 per cent in December 2023. These improvements occurred despite the Reserve Bank of India's increasingly stringent asset classification norms—Union Bank wasn't benefiting from regulatory forbearance but genuinely cleaning up its balance sheet.

The current scale is staggering: 9,300+ branches serving 153 million customers with ₹22.92 lakh crore in total business. To put this in perspective, Union Bank now serves more customers than the entire population of Japan, with assets larger than the GDP of many countries. The government stake at 83.25% provides both stability and implicit sovereign backing, a crucial advantage in a market where trust remains the ultimate currency.

Market performance reflects this operational improvement. The trailing twelve-month earnings per share (EPS) of the bank stands at Rs 23.6, an improvement from the EPS of Rs 18.1 recorded last year. The price to earnings (P/E) ratio, at the current price of Rs 144.0, stands at 5.8 times its trailing twelve months earnings. This valuation, significantly below private sector peers, suggests either the market hasn't fully recognized the transformation or there's still a "PSU discount" being applied.

The geographic and demographic reach provides competitive advantages that pure-play digital banks can't replicate. With 56% of branches in rural and semi-urban areas, Union Bank serves markets where relationship banking still matters more than mobile apps. Yet the bank has successfully straddled both worlds—maintaining its rural presence while building digital capabilities that compete with fintech startups.

Competition remains intense. HDFC Bank and ICICI Bank continue to dominate the premium segments with superior technology and service. State Bank of India's sheer scale—nearly three times Union Bank's size—provides advantages in wholesale banking and government business. New-age fintech companies are cherry-picking profitable segments like payments and consumer lending. Yet Union Bank has found its niche: the sweet spot between PSU stability and private sector efficiency, between traditional banking and digital innovation, between social responsibility and commercial success.

Business Model & Strategic Moats

The PSU bank advantage manifests in subtle but powerful ways. When a small manufacturer needs working capital, the implicit government backing means Union Bank can extend credit where private banks might hesitate. When rural India needs banking services in villages with 2,000 people, Union Bank opens branches while private banks deploy business correspondents. This isn't inefficiency—it's a fundamentally different business model where social returns complement financial returns.

Fee income grew by 36.46 per cent to Rs 2868 crore, though treasury income fell by 9.68 per cent to Rs 700 crore. This fee income diversification represents a crucial strategic shift. Traditional PSU banks relied heavily on net interest margins, making them vulnerable to rate cycles. Union Bank has systematically built fee-generating capabilities across transaction banking, wealth management, and insurance distribution. Non-interest income, including fees, commissions, treasury revenues, and recoveries, rose by 17.02 per cent Y-o-Y to Rs 4,417 crore—a growth rate that would impress even fee-focused private banks.

The rural-urban balance creates unique advantages. With deep rural penetration providing low-cost deposits (though CASA ratios have declined slightly to 33.43%), Union Bank funds urban and corporate lending at attractive spreads. This geographic arbitrage—gathering deposits where competition is limited and deploying them where returns are highest—represents a sustainable competitive advantage that pure urban or pure rural banks can't replicate.

Technology has become an unexpected differentiator in the PSU space. While State Bank of India struggles with legacy systems and other PSU banks lag in digital adoption, Union Bank's post-merger technology stack positions it as the digital leader among government banks. This isn't just about mobile apps—it's about using AI for credit underwriting in rural areas, deploying blockchain for trade finance, and leveraging data analytics for cross-selling.

The comparison to the Tata Group is instructive. Like Tata, Union Bank operates across multiple segments with different economics but unified by common values and trust. Retail banking provides stability, corporate banking drives growth, international operations offer diversification, and digital initiatives create optionality. This conglomerate thinking—unusual in banking—provides resilience that monoline competitors lack.

Capital allocation priorities reveal strategic sophistication. Rather than chasing growth at any cost, the bank has focused on: cleaning up the balance sheet first (NPAs down to 3.85%), building capital buffers (CAR at 16.72%), investing in technology infrastructure, and only then pursuing aggressive growth. This sequencing—fix, strengthen, then grow—reflects learning from past PSU bank failures where growth without foundation led to asset quality disasters.

The government ownership, often seen as a constraint, provides unexpected advantages. In times of crisis, the implicit sovereign guarantee prevents bank runs. During economic downturns, government support ensures survival. For large infrastructure projects, PSU bank participation is often mandatory. These aren't subsidies but strategic advantages built into the Indian financial system's architecture.

Playbook: Lessons for Builders & Investors

The Union Bank story offers counterintuitive lessons that challenge conventional wisdom about banking transformation. First, timing complex mergers during crisis can actually accelerate integration. The COVID pandemic, which should have derailed the three-way merger, instead created urgency and eliminated resistance to change. When everyone accepts that the old ways won't work, transformation becomes possible.

Second, technology partnerships can move faster than in-house development if structured correctly. Union Bank's five-month implementation of a cash management system—versus the industry standard of 18-24 months—happened because they co-created with vendors rather than buying off-the-shelf solutions. This collaborative model, where the bank maintains strategic control while leveraging vendor expertise, represents a new paradigm for enterprise technology deployment.

Third, maintaining customer continuity during massive structural change isn't just good service—it's strategic advantage. By keeping account numbers, IFSC codes, and branch operations unchanged during the merger, Union Bank avoided the customer attrition that typically accompanies bank consolidations. This "change everything but change nothing" approach required extraordinary operational complexity but paid off in customer retention.

The approach to digital transformation offers another lesson: start with the back office, not the front office. While competitors launched flashy mobile apps, Union Bank first built robust data infrastructure and integration capabilities. Only after establishing this foundation did they roll out customer-facing innovations. This sequencing—infrastructure before interface—proved more sustainable than cosmetic digital initiatives.

Managing government ownership while competing with private players requires sophisticated stakeholder management. Union Bank has mastered the art of using government backing when advantageous (crisis situations, large infrastructure deals) while maintaining operational independence in day-to-day decisions. This selective engagement—neither fully government-controlled nor fully autonomous—represents a pragmatic middle path.

The balance between social responsibility and profitability isn't achieved through separate CSR initiatives but through integrated business models. Rural branches aren't charity—they're deposit-gathering engines. Priority sector lending isn't a burden—it's relationship building with tomorrow's corporate clients. This integration of social and commercial objectives creates sustainable competitive advantages.

For investors, Union Bank presents a fascinating study in optionality. With the government holding 83.25% and privatization discussions ongoing, there's potential for significant value unlocking. The Centre has stayed the announcement of privatisation of two public sector banks, but when privatization eventually happens, banks with strong operational metrics and clean balance sheets will command premium valuations.

Bear vs. Bull Case Analysis

The bear case starts with government interference. Despite operational improvements, Union Bank remains subject to political pressures—directed lending, loan waivers, merger mandates. Every election cycle brings new risks of populist policies that prioritize political gains over banking prudence. The 83.25% government stake means minority shareholders have limited influence over strategic decisions.

Competition from nimble private banks and fintechs presents existential challenges. While Union Bank builds comprehensive digital platforms, startups launch single-feature products in weeks. Young Indians increasingly choose digital-first banks, viewing PSU banks as their parents' institutions. The cost structure—with 76,700 employees and 9,300 branches—can't match the efficiency of branch-light digital players.

Asset quality concerns persist despite recent improvements. India's economic cycles remain volatile, and PSU banks traditionally bear disproportionate pain during downturns. With significant exposure to infrastructure and corporate lending, Union Bank remains vulnerable to large ticket defaults. The improved NPAs might reflect economic recovery rather than fundamental risk management improvements.

The regulatory burden continues escalating. Reserve Bank of India's increasingly stringent norms, combined with government directives on priority sector lending, squeeze profitability. Compliance costs keep rising while pricing flexibility remains limited. The dual regulation—RBI for banking, government for ownership—creates conflicting mandates.

The bull case rests on India's GDP growth story. With the economy expected to grow at 6-7% annually, credit demand will expand dramatically. Union Bank, with its established infrastructure and relationships, is perfectly positioned to capture this growth. The current loan book of ₹9.56 trillion could double in 7-8 years through normal economic expansion.

Government support provides downside protection. As seen during COVID, the government won't let major PSU banks fail. This implicit guarantee allows Union Bank to take calculated risks that purely private institutions might avoid. During systemic crises, this backing becomes invaluable, as depositors flee to safety.

Digital transformation is bearing fruit faster than expected. The technology investments made during 2020-2023 are now generating returns through improved efficiency, better cross-selling, and lower customer acquisition costs. With 90-95% of customer queries now automated, operational leverage is improving dramatically.

The valuation discount to private peers creates opportunity. Trading at 5.8 times earnings versus 15-20 times for private banks, Union Bank offers compelling value. Even modest multiple expansion—justified by improving metrics—could generate significant returns. If Union Bank achieves even half the valuation of private peers, the stock could triple.

The improving asset quality trajectory suggests fundamental changes rather than cyclical recovery. The gross NPA reduction from 7.5% to 3.6% over two years, while maintaining credit growth, indicates better underwriting and risk management. The provision coverage ratio above 93% provides buffer for future shocks.

Future Outlook & "What Would We Do?"

The next frontier clearly lies in embedded finance and platform banking. Union Bank should leverage its 153 million customer base to become a financial services platform, not just a bank. Embed banking services into e-commerce, logistics, and healthcare platforms. Partner with fintechs for distribution while maintaining balance sheet and regulatory advantages.

International expansion deserves renewed focus, but with a twist. Rather than opening more physical branches abroad, Union Bank should build digital corridors for the Indian diaspora. Facilitate remittances, provide mortgages for NRI property purchases in India, and offer wealth management for successful emigrants. The 30 million Indian diaspora represents an underserved, highly profitable segment.

Green banking and ESG initiatives aren't just compliance requirements—they're business opportunities. India's renewable energy sector needs ₹30 trillion in financing by 2030. Union Bank should build specialized expertise in solar financing, electric vehicle loans, and green bonds. Early movers in sustainable finance will capture premium valuations and preferential regulatory treatment.

Potential privatization scenarios require preparation. Whether the government reduces stake to 51% or fully privatizes, Union Bank must be ready. This means: cleaning up remaining stressed assets, achieving cost-income ratios comparable to private banks, building management depth beyond government appointees, and creating strategic options that make the bank attractive to potential investors.

Building a fintech subsidiary could unlock significant value. Rather than competing with startups, Union Bank should incubate its own digital ventures. A separately branded digital bank—unencumbered by legacy systems and targeting young professionals—could achieve valuations multiples higher than the parent bank. ICICI's success with ICICI Securities and ICICI Prudential provides a template.

M&A opportunities in the NBFC space deserve consideration. As regulatory arbitrage between banks and NBFCs narrows, distressed NBFCs become attractive acquisition targets. Union Bank could acquire specialized NBFCs in housing finance, vehicle finance, or microfinance, instantly gaining expertise and distribution in high-growth segments.

The strategic priorities for the next five years should be: First, achieve best-in-class status among PSU banks across all metrics. Second, build distinctive capabilities in 2-3 chosen segments (MSMEs, affordable housing, or agriculture technology). Third, create optionality through digital ventures and strategic partnerships. Fourth, prepare for ownership transition while maintaining operational momentum.

Union Bank stands at an inflection point. The heavy lifting of merger integration and digital transformation is largely complete. The balance sheet is clean, the technology stack is modern, and the franchise is strong. Whether the future brings continued government ownership, partial privatization, or complete independence, Union Bank has positioned itself to thrive. The institution that Gandhi blessed a century ago has proved that transformation is possible at any age, under any circumstances, if the will exists.

The ultimate lesson from Union Bank's journey isn't about banking—it's about institutional renewal. In an era when century-old companies regularly disappear, Union Bank has reinvented itself while maintaining its core purpose. It has shown that public sector institutions can compete with private players, that legacy systems can be modernized, and that social responsibility and profitability can coexist. For builders and investors alike, Union Bank's story offers hope that transformation is always possible, even for the most unlikely candidates.

Recent News

The latest quarterly results underscore Union Bank's continued momentum. In the quarter ending December 31, 2024, Union Bank of India achieved a total income of ₹31749.18 crore, a 6.5% increase from ₹29801.98 crore in the same quarter of the previous fiscal year. This growth was primarily driven by a 6.3% rise in interest earned, which amounted to ₹27134.77 crore, up from ₹25520.92 crore in Q3 FY24. The net profit for the quarter was ₹4623.03 crore, reflecting a significant 27.5% increase from ₹3625.39 crore in the corresponding period of the prior year.

The asset quality improvement story continues to gather pace. The asset quality profile improved, with gross NPAs declining to 3.85 per cent in December 2024 from 4.83 per cent in December 2023. Net NPAs also declined to 0.82 per cent in December 2024, compared to 1.08 per cent in December 2023. This dramatic improvement—nearly 100 basis points reduction in gross NPAs year-over-year—demonstrates that the post-merger integration has delivered tangible results in risk management.

Non-interest income, including fees, commissions, treasury revenues, and recoveries, rose by 17.02 per cent Y-o-Y to Rs 4,417 crore. This diversification away from pure interest income provides crucial buffer against rate cycles and demonstrates the success of cross-selling initiatives enabled by the integrated technology platform.

On the leadership front, Ms. A. Manimekhalai has been the Managing Director and Chief Executive Officer of the bank since June 2022. Under her stewardship, the bank has accelerated its digital transformation while maintaining focus on asset quality improvement. The leadership team has been strengthened with SRINIVASAN VARADARAJAN joins the board as Chairman (Non-Executive), in a new position in 2025.

The strategic partnership ecosystem continues to expand. Union Bank of India, one of India's largest public sector banks, and Zoho, a leading global technology company headquartered in Chennai, have achieved a significant milestone in Union Bank of India's digital transformation journey with the successful launch and implementation of CRM Edge – an advanced customer experience platform co-created by both the organisations. At an event commemorating the collaboration at Zoho's rural hub office in Tenkasi, Tamil Nadu, Union Bank of India's MD & CEO, A. Manimekhalai, and Zoho's Co-founder and CEO, Mr. Sridhar Vembu, showcased the shared vision and collaborative efforts that drove this transformational journey. Since its rollout in 2023, CRM Edge has rapidly become the Bank's primary customer engagement tool and is widely used across the Bank.

The Intellect partnership has delivered exceptional results. Intellect Design Arena Ltd, a cloud-native, future-ready multiproduct FinTech company for the world's leading financial and insurance clients, announced that Union Bank of India (UBI) has chosen Cash Management System built on eMACH.ai to automate and elevate their enterprise-wide cash flows. This strategic partnership with Intellect will provide UBI with a fully-integrated Cash & Payments Management platform, which is expected to enhance the experience and operational efficiency of their corporate and SME customers.

Perhaps most impressively, the bank's rural engagement extends beyond banking. The Bank, in its commitment to community development in rural India and Corporate Social Responsibility, contributed to Government High Schools at Melur, Sengottai and SMSS Government Boys Higher Secondary School towards their key infrastructure and sustainability initiatives, such as sanitation improvements and installation of solar power units. This integration of social responsibility with business operations exemplifies the Union Bank philosophy—profit with purpose.

The market's response to these developments remains mixed. Despite the positive financial results, Union Bank of India's shares experienced a slight downturn, closing at ₹105.65, which is a 1.49% decrease, at the end of the trading day. This disconnect between operational performance and market valuation suggests either persistent skepticism about PSU banks or an opportunity for value investors who recognize the transformation underway.

Links & Resources

For those seeking deeper insights into Union Bank's transformation journey, several resources provide valuable context:

Official Sources: - Union Bank of India Annual Reports (www.unionbankofindia.co.in/english/investor-relations.aspx) - RBI Financial Stability Reports (www.rbi.org.in) - Government of India Banking Reform Initiatives (financialservices.gov.in)

Technology Partnership Case Studies:

- Accenture-Union Bank Data Platform Implementation

- Intellect Design Arena Cash Management System Deployment

- Zoho CRM Edge Platform Co-creation Documentation

Industry Analysis: - EASE (Enhanced Access & Service Excellence) Reform Reports - Indian Banks' Association Publications on PSU Bank Transformation - McKinsey Global Institute Reports on Indian Banking

Books on Indian Banking History: - "The Evolution of State Bank of India" by A.K. Bagchi - "Banking Century: A Short History of Banking in India" by D.N. Ghosh - "Nationalization of Banks in India: Retrospect and Prospect" by R.K. Mishra

Regulatory Documents: - RBI Master Directions on Priority Sector Lending - Basel III Implementation Guidelines for Indian Banks - Digital Banking Framework for India

Final Analysis: The Improbable Transformation

Union Bank of India's journey from Gandhi's blessing to digital banking leadership represents more than a corporate success story—it's a masterclass in institutional reinvention under the most challenging circumstances imaginable. The bank that merged three entities during a pandemic, built a cutting-edge technology stack while serving rural farmers, and improved asset quality while growing the loan book has achieved something that management consultants would declare impossible.

The transformation isn't complete. Competition from private banks remains intense, regulatory pressures continue mounting, and the specter of privatization looms. Yet Union Bank has positioned itself uniquely: technologically advanced enough to compete with private players, socially embedded enough to maintain PSU advantages, and operationally efficient enough to thrive under any ownership structure.

For investors, Union Bank presents a compelling asymmetric opportunity. Trading at valuations that imply permanent impairment, the bank offers exposure to India's growth story with limited downside given government backing. The ongoing operational improvements, if sustained, could drive significant multiple expansion even without privatization.

For builders and entrepreneurs, the lessons are profound. Transformation doesn't require starting from scratch—sometimes the greatest innovations come from reimagining existing institutions. The combination of patience, technology, and purpose that Union Bank exemplifies offers a template for renewal that transcends banking.

The institution that Mahatma Gandhi inaugurated with hope for managing "crores of rupees in the course of our national activities" now manages lakhs of crores while pioneering India's digital banking revolution. It's a reminder that in business, as in life, the most improbable transformations often yield the most enduring success. Union Bank hasn't just survived a century of change—it has emerged stronger, more relevant, and better positioned for the next hundred years than at any point in its storied history.

The bank that carries Gandhi's blessing into the age of artificial intelligence stands as testament to a simple truth: institutions that adapt their methods while maintaining their purpose don't just survive—they thrive. For Union Bank of India, the best chapters of its story may still be unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube