United Breweries Limited: India's Beer Crown Jewel

I. Introduction & Episode Roadmap

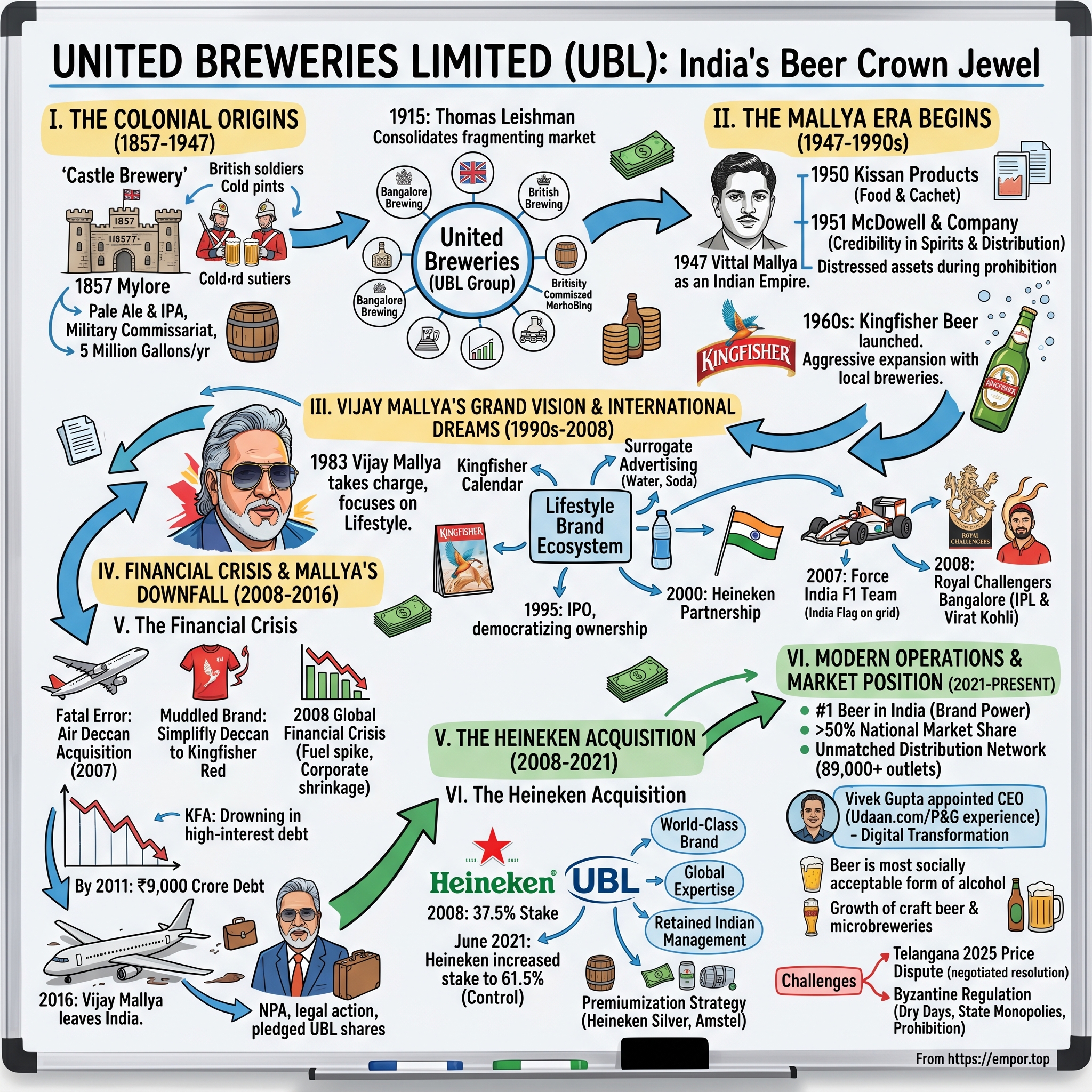

Picture this: It's 1857, and British soldiers stationed in the sweltering heat of colonial India are desperately craving a taste of home—specifically, a cold pint of beer. In the hill stations of South India, enterprising brewers set up shop to quench this thirst, unknowingly planting the seeds of what would become India's beer empire. Fast forward 167 years, and those colonial-era breweries have morphed into United Breweries Limited, a ₹50,768 crore behemoth that commands over half of India's beer market.

The story of UBL isn't just about beer—it's a sweeping saga of colonial enterprise, family dynasties, spectacular rises and catastrophic falls, regulatory chess games, and ultimately, the globalization of an Indian icon. Today, UBL manufactures and sells beer under flagship brands Kingfisher and Heineken, generating ₹9,304 crore in revenue with a promoter holding of 70.8%—those promoters being Dutch brewing giant Heineken N.V., not the flamboyant Indian tycoons who once controlled it.

How did a collection of British Raj-era breweries, consolidated by a Scottish entrepreneur in 1915, become the jewel in the crown of one of India's most notorious business empires, only to be rescued and absorbed by a European multinational? The answer involves three generations of the Mallya family, billions in debt, international fugitive warrants, Formula 1 racing teams, cricket franchises, and the fundamental challenge of selling alcohol in a country where prohibition is written into the constitution.

This is a story about building brands in a market where advertising alcohol is banned, where every state has different rules, where dry days can shut down business without warning, and where cultural attitudes toward drinking vary dramatically from cosmopolitan Mumbai to conservative Gujarat. It's about how Kingfisher became synonymous with the "good times" in Indian popular culture, and how those good times turned very, very bad.

The themes we'll explore cut to the heart of doing business in emerging markets: navigating byzantine regulations, managing political relationships, building distribution moats across vast geographies, the perils of leverage and diversification, and what happens when lifestyle branding becomes indistinguishable from the lifestyle of the brand's creator. We'll see how foreign ownership can be both salvation and challenge, how premiumization strategies work in markets with vast income disparities, and why selling beer in India might be one of the most complex consumer goods businesses on the planet.

II. The British Raj Origins & Early Foundations (1857–1947)

The Nilgiri Hills of South India in 1857 were a refuge—a place where British colonials could escape the oppressive heat of the plains and pretend, for a moment, they were back in the Scottish Highlands. But one thing was missing from this manufactured paradise: proper English beer. The solution came in the form of Castle Brewery, established that year in what would become a pattern repeated across the subcontinent—wherever the British established hill stations and cantonments, breweries followed. The British weren't just establishing administrative outposts in India—they were recreating England in the tropics, complete with their beloved ales. Castle Brewery in Mylore, India, established in 1857, began brewing what would eventually become Kingfisher beer, though that brand wouldn't appear for another century. The British introduced European-style beer to India, with pale ale and Burton ale being imported from England as early as 1716.

The logistics of colonial beer consumption were extraordinary. To protect beer from spoiling during the long journey, brewers increased alcohol content and added extra hops, leading to the invention of India Pale Ale around 1787 by Bow Brewery. By 1892, India was producing nearly 5 million gallons of beer annually, with over half purchased by the military commissariat—though British soldiers reportedly preferred imported beer to local brews, a preference that would shape the market for generations.

Enter Thomas Leishman, a Scotsman with a consolidator's vision. In 1915, as World War I raged and the British Empire approached its zenith, Leishman saw opportunity in fragmentation. He merged Castle Brewery with Nilgiris Brewery, Bangalore Brewing Company, British Brewing Company, and BBB Brewing Company to create United Breweries, a group originally run by British nationals during colonial rule. This wasn't just business expansion—it was industrial strategy applied to a colonial market where distribution networks mattered more than production capacity.

The consolidation made perfect sense in the Indian context. Unlike Britain, where breweries could serve local populations within manageable distances, India's vastness required a different approach. The subcontinent's 1.8 million square miles contained hundreds of princely states, each with its own rules and relationships with the Raj. A brewery in Bangalore couldn't efficiently serve Delhi, 1,700 miles away, without a network of bottling plants, distribution centers, and political relationships.

By the 1920s and 1930s, UBL had become the dominant force in Indian brewing, but the company faced an existential question: What would happen when the British left? The writing was on the wall—Gandhi's independence movement was gaining momentum, the British were exhausted from two world wars, and the old colonial economic structures were crumbling. Foreign-owned businesses across India were scrambling to adapt to the inevitable transition.

The answer came in the form of a 22-year-old Indian who would transform UBL from a colonial enterprise into an Indian empire. In 1947, as India gained independence, Vittal Mallya took over as the first Indian director of United Breweries, becoming chairman of the board just one year later. This wasn't just a changing of the guard—it was a complete reimagining of what an Indian company could be.

III. The Mallya Era Begins: Building an Empire (1947-1990s)

The monsoon of 1946 brought unusual visitors to the offices of United Breweries in Bangalore. Young Vittal Mallya, just 22 years old, had been quietly accumulating shares in the British-controlled company while still a student at Presidency College in Kolkata. His father, a lieutenant colonel in the Indian Army, had instilled in him both discipline and ambition. But what Vittal had that his contemporaries lacked was foresight—he saw that independence would create opportunities for Indians to control businesses that had been British preserves for a century.

In 1946-47 he started acquiring the shares of United Breweries, and the company was bought by Vittal Mallya in 1947. At 22, he was elected as the company's first Indian director in 1947, and after a year, he replaced R. G. N. Price as the company's chairman. This wasn't a hostile takeover—it was a negotiated transition that recognized the changing political reality. The British owners, reading the writing on the wall, preferred selling to a capable Indian rather than risking nationalization or worse.

Vittal Mallya's genius lay not in brewing beer but in seeing United Breweries as a platform for something much larger. First was the addition of McDowell as one of the Group subsidiaries, which The Vittal Mallya-run United Breweries Group bought in 1951. This move helped United Breweries to extend its portfolio to the wines and spirits business. The acquisition of McDowell & Company, founded in 1826 as a trading company serving British colonial needs, was transformative. It gave UB instant credibility in spirits and a distribution network that had been built over 125 years.

But Mallya's vision extended beyond alcohol. The simultaneous move into food products started with the acquisition of Kissan Products in 1950. When Herbertsons was pocketed two decades later, Mallya also bagged its Dipy's division, giving him a virtual stranglehold on a series of processed food products. The Kissan acquisition was particularly shrewd—here was an Indian brand that had already penetrated middle-class households with jams, ketchups, and squashes. It provided cash flow diversification and, crucially, gave UB products that could be openly advertised, unlike alcohol.

As a strategical measure, the Group moved into agro-based industries and medicines. By the 1960s, UB Group wasn't just a brewery—it was becoming one of India's first true conglomerates. Mallya was applying a distinctly Indian business model: using cash flows from established businesses to fund acquisitions across unrelated sectors, leveraging political relationships to navigate licensing requirements, and building an empire that could withstand the volatility of any single industry.

The introduction of Kingfisher beer marked a watershed moment, though Kingfisher, the Group's most visible and profitable brand, made a modest entry in the sixties. The name itself was brilliant marketing—the kingfisher bird, colorful and distinctive, became an instantly recognizable logo that transcended language barriers in a multilingual nation. Unlike the colonial-era brands with their British names and associations, Kingfisher was unapologetically Indian.

New breweries were established in Kerala (Cherthala, 1959), Andhra Pradesh (Hyderabad, 1969), Goa (Ponda, 1971) and Bihar (Hatidah, 1973). By the early 1960s, Mallya, back in Calcutta, gained further control of the liquor market by acquiring Carew & Company Limited and Phipson & Company Limited. This aggressive expansion wasn't just about capacity—it was about navigating India's complex regulatory environment. Each state had different rules about alcohol production and distribution. By establishing local production facilities, Mallya could avoid interstate transportation restrictions and build relationships with state governments.

The 1970s brought the ultimate test of Mallya's business acumen. In 1977, when an official prohibition drive sent the breweries and distilleries into a tailspin, Mallya showed his foresight by buying up or gaining control. While competitors panicked as states like Gujarat and Bihar implemented prohibition, Mallya saw opportunity in crisis. He acquired distressed assets at bargain prices, betting correctly that prohibition would eventually be rolled back in most states due to loss of tax revenue.

In 1981, Mallya controlled 10 breweries and 14 distilleries, seven processed food companies, six investment companies, two small packaging units, three drug firms, soft drinks bottling plants, a battery unit and one of the company's two styrene companies. This sprawling empire was held together by Mallya's personal relationships, his reputation for integrity, and his ability to navigate India's "License Raj"—the complex system of permits and quotas that governed Indian business until 1991.

Yet for all his success, Vittal Mallya was a man of frugal habits who believed in thrift and understatement, values which he tried to inculcate in the young Vijay. He drove a modest car, lived in a relatively simple house, and was known for scrutinizing even small expenses. This stood in stark contrast to the flamboyant style his son would later adopt.

When Vittal Mallya died suddenly in October 1983, he left behind an empire valued at hundreds of crores—massive wealth by Indian standards of the time. But more importantly, he left a business model: build through acquisition, diversify across sectors, maintain strong political relationships, and always keep significant cash reserves. His son Vijay, then 28 years old, inherited not just companies but a playbook for empire-building in India's unique business environment.

IV. Vijay Mallya's Grand Vision & International Dreams (1990s-2008)

The transformation began the moment 28-year-old Vijay Mallya walked into the United Breweries boardroom in October 1983. Where his father Vittal had been frugal and understated, Vijay arrived in a Mercedes, dressed in designer suits, and immediately began talking about taking Indian brands global. The board members, accustomed to Vittal's conservative approach, watched nervously as the young heir outlined plans that seemed impossibly ambitious.

"My father built an empire," Vijay told them. "I'm going to build a lifestyle."

The son of a businessman who was also in the alcoholic beverages business, Mallya became the chairman of United Breweries Group in 1983 at the age of 28, following his father's death. But unlike his father's focus on quiet consolidation, Vijay had a different vision—he wanted to make Indian brands aspirational, to connect them with success, glamour, and what he would famously call "the good times."

The reinvention started with Kingfisher itself. When Vijay Mallya took charge of United Breweries, he noticed that Kingfisher, a beer brand dating back to the 1800s, wasn't being used to its full potential. He proposed investing ₹10 lakhs to relaunch it, not just as a product but as a youthful and energetic brand. The challenge was formidable: India had strict restrictions on alcohol advertising, which meant traditional media promotion was off-limits.

Mallya's solution was brilliant in its simplicity: surrogate advertising. To work around this, Mallya used surrogate advertising by legally promoting Kingfisher-branded bottled water, soda, and lifestyle events. The Kingfisher Calendar, featuring models in exotic locations, became an annual cultural event. Fashion shows, music festivals, and sports sponsorships all carried the Kingfisher brand, creating an ecosystem of aspiration without ever directly advertising beer.

In 1995, the company went public, with shares listed on the Bombay Stock Exchange. This wasn't just about raising capital—it was Mallya's way of democratizing ownership of his empire, allowing middle-class Indians to participate in the success of brands they consumed. The IPO was oversubscribed multiple times, a validation of his lifestyle branding strategy.

In 2000, UBL acquired the rights to produce and market the Heineken brand in India, a strategic move that enhanced its portfolio and market share. This partnership with Heineken was prescient—it gave UBL a premium international brand to complement its mass-market offerings, positioning the company for the premiumization trend that would sweep India in the coming decades.

But Mallya's ambitions extended far beyond beer. Mallya was also the founder and former owner of the defunct Kingfisher Airlines and former co-owner of the Force India Formula One team. He is also a former owner of the Royal Challengers Bangalore cricket team. These weren't random diversifications—they were carefully chosen platforms to project the Kingfisher lifestyle globally.

The Formula 1 venture was particularly audacious. The team was formed in October 2007 when a consortium led by Indian businessman Vijay Mallya and Dutch businessman Michiel Mol bought the Spyker F1 team for €88 million. He revealed that while he had the opportunity to christen the team "Mallya F1," he chose "Force India" to ensure the Indian flag was represented on the global motorsport stage. Mallya, who co-founded Force India in 2007 after acquiring the Spyker F1 team, emphasized his desire to showcase India in Formula One.

"Now I named it Force India, I could have easily named it Mallya Formula 1, like Williams F1, for instance right. Because I wanted to be the Indian flag to be on the grid. I wanted to know that the team with roots in India of all countries, was at the pinnacle of motorsport. That is why I called it Force India and I had the tricolor on the car."

The Royal Challengers Bangalore cricket franchise acquisition showed similar strategic thinking. In a recent conversation on Raj Shamani's podcast, Mallya opened up about how he handpicked Virat Kohli ahead of the inaugural IPL season in 2008, following the youngster's impressive run at the ICC U-19 World Cup, which he won as captain. He said, "Shortly before the actual selection process, they were playing the U-19 World Cup, and I was very impressed with him. So, I picked him, and it's wonderful, 18 years later, he is still there."

These ventures served multiple purposes. "Of course I also used the platform to advertise my brands, including Royal Challenge whisky, White & McKay, which we owned at that time, Kingfisher, then the airline. So the livery of the car and the merchandise around Formula 1 had a lot of our brands on it for promotional purposes. But the core reason was to put an Indian Formula 1 team on the grid."

By the early 2000s, Mallya had transformed himself into India's most visible businessman. Once called the "King of Good Times" due to his extravagant lifestyle, Mallya and his companies have been embroiled in financial scandals, and controversies since 2012. His parties were legendary, his yacht was one of the largest in the world, and his collection of vintage cars was worth millions. This wasn't just personal indulgence—it was brand building. Every appearance, every party, every extravagant purchase reinforced the Kingfisher message: this is what success looks like.

United Breweries Limited – the UB Group's brewing entity, which has undisputed market leadership with a national market share in excess of 50%. The UB Group today controls 60% of the total manufacturing capacity. This dominance wasn't accidental—it was the result of two decades of relentless brand building, strategic acquisitions, and Mallya's ability to navigate India's complex regulatory environment while projecting an image of international sophistication.

The irony was that even as Mallya was building his lifestyle empire, the fundamentals of the beer business remained strong. United Breweries now has greater than a 40% share of the Indian brewing market with 79 distilleries and bottling units around the world. The company had built an unassailable distribution network, strong relationships with retailers, and brand loyalty that transcended generations.

V. The Financial Crisis & Mallya's Downfall (2008-2016)

October 2011. The maintenance hangars at Mumbai Airport were supposed to be bustling with activity, but half of Kingfisher Airlines' fleet sat grounded, their red and white livery dulling under layers of dust. Engineers hadn't been paid in two months. Pilots were threatening to make in-flight announcements about their unpaid salaries. The "good times" that Vijay Mallya had promised were coming to an abrupt, painful end.

The roots of the crisis stretched back to 2007, when Mallya made what would prove to be his fatal error: acquiring Air Deccan. The acquisition of loss-making Bengaluru-based Air Deccan in 2007 made matters worse. It was believed that Vijay Mallya and his team failed to follow due diligence with the airline. The logic seemed sound—Air Deccan's low-cost model would give Kingfisher access to price-conscious consumers while maintaining its premium brand separately. But the execution was disastrous.

An initial name change to Simplifly Deccan, followed by Kingfisher Red, and promotion as the domestic budget Kingfisher airline failed to stem losses and Kingfisher suffered a loss of over ₹10 billion for three consecutive years. The low-cost carrier model required operational discipline that Kingfisher's luxury-oriented management couldn't deliver. Passengers were confused—was Kingfisher premium or budget? The brand positioning that had been Mallya's strength became muddled.

The 2008 global financial crisis hit just as Kingfisher was digesting the Air Deccan acquisition. Fuel prices spiked, corporate travel budgets shrank, and India's aviation market, which had been growing at double digits, suddenly stalled. However, the airline ran into continuous losses since its inception, ran high debts and finally closed its operations on 20 October 2012.

By 2011, the numbers were catastrophic. By 2011, Kingfisher Airlines had racked up over INR 9,000 crore in debt, with little to show in profit. The airline was borrowing just to repay existing loans, a red flag in financial management. On 15 November 2011 the airline released poor financial results, indicating that it was "drowning in high-interest debt and losing money."

The death spiral accelerated with shocking speed. In December 2011, for the second time in two months, Kingfisher's bank accounts were frozen by the Mumbai Income Tax department for non-payment of dues. The firm owed ₹700 million to the tax department at the time. State Bank of India on 5 January 2012 declared Kingfisher Airlines a non-performing asset. SBI is the largest creditor and leader of the consortium of banks.

The human cost was devastating. Kingfisher Airlines delayed salaries of its employees in August 2011, and for four months in succession from October 2011 to January 2012. Protesting at the delays in payment, Kingfisher pilots started making in-flight announcements citing "It is their sense of duty towards the guest that is making them fly despite not being paid salaries for the past two months."

By late 2011, signs of Kingfisher Airlines' collapse were increasingly visible: Flights were frequently delayed or cancelled, disrupting operations nationwide. Pilots, engineers, and ground staff staged protests and strikes due to months of unpaid salaries. A large number of aircraft were grounded because of unpaid fuel bills, maintenance dues, and lease defaults.

The operational collapse was equally dramatic. Since 2008, it has been reported that Kingfisher Airlines has been unable to pay the aircraft lease rentals on time. Kingfisher Airlines has grounded 15 out of 66 aircraft in its fleet as it was unable to meet the maintenance and overhaul expenses. The airline operated about 120 daily flights by March 2012, down from more than 400 earlier.

What made the situation particularly tragic was how it affected United Breweries. To keep Kingfisher Airlines afloat, Mallya pledged over 90% of his shares in United Breweries and United Spirits. The beer business that had funded his dreams was now collateral for his nightmares. The conglomerate was headed by Vijay Mallya, who left India on 2 March 2016, allegedly to escape legal action by Indian banks to whom he owed an estimated ₹9,000 crore in loans.

The banks moved decisively. By 2012, major lenders, including SBI, IDBI, PNB, Bank of Baroda, Bank of India, and United Bank of India, officially classified Kingfisher as a Non-Performing Asset (NPA), triggering legal and financial proceedings. Eventually, after continued operational disruptions and failure to provide a recovery plan, the DGCA suspended Kingfisher Airlines' flying license on October 20, 2012, citing safety and financial viability concerns.

But the real story wasn't just about one airline's failure—it was about how leverage and diversification, the very strategies that had built the Mallya empire, became its undoing. The lifestyle brand that Mallya had so carefully cultivated became a liability. His flamboyant persona, once an asset in building the Kingfisher brand, now made him a lightning rod for public anger about unpaid loans and employee hardships.

VI. The Heineken Acquisition: From Indian Icon to Global Player (2008-2021)

The irony was palpable. As Vijay Mallya's empire crumbled around him in 2008, a lifeline appeared from an unexpected source—not from Indian banks or government bailouts, but from a Dutch brewing giant that had been quietly watching United Breweries for years. In 2008, as the airline's troubles were just beginning, Mallya's UB group struck a landmark deal. The world-famous Dutch beer company, Heineken, bought a 37.5% stake in United Breweries.

This wasn't Heineken's first dance with UBL. Heineken has been continuously building its position in UBL, since obtaining a 37.5 percent stake through its 2008 acquisition of brewer Scottish & Newcastle. The Dutch company had inherited this stake almost by accident, but quickly recognized the strategic value of India's beer market leader. For Heineken, India represented the holy grail of emerging markets—a billion-plus population with rising incomes and beer consumption at just two liters per capita annually, compared to 70+ liters in Europe.

This wasn't just about money. Here's what it meant for UB: A World-Class Brand: UB could now brew and sell Heineken beer in India, instantly adding a super-premium global brand to its offerings. Global expertise: Heineken brought its global expertise in brewing technology and, crucially, in managing supply chains. The partnership gave UBL access to Heineken's portfolio of international brands while allowing Heineken to leverage UBL's unmatched distribution network across India's complex state-by-state regulatory landscape.

Initially, the relationship was collaborative. Heineken maintained a hands-off approach, respecting UBL's local expertise while providing technical support and access to global brands. The arrangement seemed ideal—UBL got a stable, deep-pocketed partner, and Heineken got exposure to one of the world's fastest-growing beer markets without the headache of building operations from scratch.

But as Mallya's financial troubles deepened, the dynamics shifted dramatically. The most crucial blow came in June 2021, when the Debt Recovery Tribunal sold a 15% stake in United Breweries, originally held by Mallya's group companies, to Heineken for ₹5,824.5 crore. This deal tipped the scales. Heineken's stake in UBL rose to 61.5%, giving it majority control over the company Mallya once ruled.

The mechanics of this transition were complex and controversial. Heineken, the second largest beer company in the world, increased its stake in United Breweries (UBL) to 61.5 per cent on Wednesday. The Dutch parent of UBL, which had 45 per cent stake prior to today's transaction, bought the 14.99 per cent stake worth about Rs 5,825 crore held by the Debt Recovery Tribunal. These shares had been seized from Mallya as part of the Indian government's efforts to recover unpaid loans.

Following United Breweries Limited's (UBL) annual general meeting on 29 July 2021, HEINEKEN has obtained control of UBL in India. This follows HEINEKEN's recent acquisition of additional ordinary shares in UBL on 23 June 2021, taking its shareholding in UBL from 46.5% to 61.5%. The transition from Indian icon to subsidiary of a European multinational was complete.

The cultural integration challenges were significant but manageable. Unlike many foreign acquisitions that impose their corporate culture wholesale, Heineken took a nuanced approach. They retained key Indian management, maintained the Kingfisher brand positioning, and continued to operate within India's unique regulatory framework. The message was clear: we're not here to dismantle what works, but to enhance it.

Credit Suisse, however, believes that full control for Heineken would mean more focus on improving mix and profitability at UBL. Say Arnab Mitra and Pratik Rangnekar of the foreign firm, "Once Heineken takes full control of the business, we expect greater focus on premiumisation with brands like Amstel and Heineken Silver, and on cost efficiencies to improve operating profit margins."

The premiumization strategy was already showing results. Moreover, the premium portfolio (Heineken Silver, Ultra Witbier, Amstel) has grown ahead of the overall portfolio in the quarter. This wasn't just about introducing expensive foreign beers—it was about elevating the entire category, using Heineken's global expertise to position beer as an aspirational beverage choice in a market dominated by spirits.

For Mallya, watching from his exile in London, the irony must have been bitter. The international partnership he had cultivated as a strategic advantage had become the vehicle for his complete exit from the company his family had controlled for over seven decades. Vijay Mallya still holds an 8.08% stake in United Breweries, either individually or jointly. However, 98.11% of this stake is pledged, so he has no operational control over the company.

But perhaps the most remarkable aspect of this transition was how little it affected the underlying business. Think about it, Vijay Mallya, the face of the brand, left the company. Yet, Kingfisher beer is still India's #1 beer. This is the ultimate proof of brand power. The distribution networks continued to function, the breweries kept producing, and Indian consumers kept drinking Kingfisher. The brand had transcended its creator.

VII. Modern Operations & Market Position (2021–Present)

September 25, 2023, marked a pivotal moment at UBL's Bangalore headquarters as Heineken's United Breweries appointed Vivek Gupta as its new CEO and managing director for a five-year term. The appointment signaled not just a leadership change, but a fundamental reimagining of UBL's future in modern India.

Vivek joins UBL from India's fastest-growing unicorn, Udaan.com. As Chief Business Officer, he helped build India's most significant and disruptive e-B2B business. Prior to this, he spent over two decades in leadership and commercial roles at P&G, working across various categories, from everyday consumption to premium categories. His last position with P&G was as Managing Director of Australia and New Zealand.

The choice of Gupta was telling. Here was someone who understood both traditional FMCG excellence and digital-age disruption. At 47 years old, Mr. Vivek is an engineering graduate with a Master's in business management from IIM, Ahmedabad. Mr. Vivek is a unique executive with homegrown India and global commercial and leadership experience. He brings solid and broad experience from commercial and leadership roles in MNCs and new-age start-ups, both in international markets and India, which feeds his deep knowledge of go-to-market channels and understanding of operating complex businesses in traditional and digital environments.

His mandate was clear yet challenging. Along with the UBL leadership team, Mr. Vivek will be responsible for driving sustainable growth for the company. He will lead the premiumization of UBL's portfolio, including strengthening the iconicity of Kingfisher. This wasn't about abandoning Kingfisher's mass-market dominance but about building a portfolio that could capture value across all segments of India's evolving beer market.

The modern UBL operates at a scale that would have been unimaginable in the colonial era. United Breweries Limited has undisputed market leadership with a national market share in excess of 50%. The UB Group today controls 60% of the total manufacturing capacity for beer in India. The company manages this through a complex network of owned and contracted facilities across the country, navigating India's state-by-state regulatory maze with expertise honed over decades.

The product portfolio evolution under Heineken's ownership has been strategic and measured. Beyond the flagship Kingfisher family—which includes Premium, Ultra, Strong, and Ultra Max variants—UBL now brews and markets Heineken, Amstel, and other international brands. Each brand is positioned carefully: Kingfisher Strong for the value-conscious mass market, Kingfisher Ultra for urban millennials, and Heineken for the super-premium segment.

But modern operations aren't without challenges. The January 2025 crisis in Telangana illustrated the ongoing complexity of operating in India's regulated alcohol market. United Breweries' earlier announcement on 8 January that it had suspended the supply of beer to TGBCL due to unresolved issues. The company had cited the lack of a basic price revision since 2019-2020, which led to significant financial losses, as well as overdue payments from TGBCL for previous beer supplies.

The Telangana dispute was particularly significant because United Breweries holds 70 per cent share of the Telangana beer market, making its supply cut a significant disruption for consumers and retailers. The state government owed Rs 658.95 crore to UBL, according to State Excise Minister Jupally Krishna Rao.

The resolution came through negotiation rather than confrontation. The decision, which the company called as interim, came after the government reportedly assured the company of price revision in 30 to 45 days. The government also reportedly assured the company that its dues would be cleared in instalments in 12 to 13 months. By February 2025, the state government has increased beer prices by 15% after allowing Telangana Beverages Corporation Limited (TGBCL) to implement the recommendations of the Price-Fixing Committee (PFC).

This episode revealed both the strengths and vulnerabilities of UBL's market position. On one hand, the company's 70% market share in Telangana gave it negotiating leverage—the state couldn't afford to have Kingfisher disappear from shelves. On the other, it highlighted the ongoing challenge of operating in a market where pricing is controlled by state governments that also happen to be your biggest customers.

The competition landscape has evolved dramatically from the duopoly days of UBL and Shaw Wallace. Today, UBL faces challenges from global giants like AB InBev (which owns Budweiser and Corona in India) and Carlsberg, as well as new-age craft brewers like Bira 91. Each competitor attacks a different segment—AB InBev focuses on premium international brands, Carlsberg on value offerings, and Bira on the craft beer niche.

Yet UBL's response has been measured and strategic rather than reactive. The company continues to leverage its unmatched distribution network—reaching over 89,000 outlets across India—and its deep understanding of Indian consumer preferences. While competitors focus on metros and tier-1 cities, UBL's presence extends deep into tier-2 and tier-3 markets where the Kingfisher brand has generational loyalty.

VIII. India's Alcohol Market: Unique Challenges & Opportunities

The paradox of India's alcohol market hits you the moment you try to buy a beer in Gujarat—you can't, at least not legally. This is a state where prohibition has been in place since 1960, yet bootleggers thrive and those with "health permits" can purchase alcohol for "medicinal purposes." Welcome to the byzantine world of Indian alcohol regulation, where every state is its own kingdom with its own rules, and where selling beer can be more complex than running a pharmaceutical company.

India's constitution, in its Directive Principles, actually encourages prohibition. Article 47 states that "the State shall endeavor to bring about prohibition of the consumption except for medicinal purposes of intoxicating drinks." This creates a fundamental tension—alcohol is simultaneously a massive source of state revenue and a product that governments are constitutionally encouraged to ban.

The state-controlled distribution system adds another layer of complexity. In states like Tamil Nadu, Telangana, and Kerala, the government itself is the monopoly buyer and seller of alcohol. Private companies like UBL must sell to state-owned corporations, which then distribute to retail outlets. This means beer companies are essentially selling to a single customer who also happens to be their regulator and tax collector—a negotiating dynamic that would make game theorists weep.

Consider the absurdity of dry days. India has numerous national dry days—Republic Day, Independence Day, Gandhi Jayanti—when alcohol sales are banned. But each state adds its own: election days, religious festivals, death anniversaries of political leaders. Mumbai, the country's commercial capital, has about 12 dry days annually. For a business trying to maintain consistent supply chains and cash flows, it's a logistical nightmare.

The cultural attitudes toward alcohol consumption create another set of challenges. In a country where many households consider drinking taboo and where women consuming alcohol can still raise eyebrows, how do you build a mainstream consumer brand? UBL's answer has been to position beer as the most socially acceptable form of alcohol—lighter, more refreshing, less intoxicating than spirits. The "King of Good Times" messaging was carefully crafted to associate beer with celebration rather than inebriation.

Yet within these constraints lies enormous opportunity. India's per capita beer consumption is just 2 liters annually, compared to 70+ liters in European countries and even 30+ liters in China. With a median age of 28 and rising disposable incomes, the demographic dividend is undeniable. Every year, millions of Indians reach legal drinking age (which varies from 18 to 25 depending on the state—because of course it does).

The growing middle class represents the real prize. McKinsey estimates that India's middle class will grow from 300 million to 580 million by 2030. These consumers don't just want cheap alcohol—they want brands that reflect their aspirations. This premiumization trend is already visible: while overall beer volumes grow at 5-7% annually, premium beer segments are growing at 15-20%.

The rise of craft beer and microbreweries, particularly in cities like Bangalore, Pune, and Gurgaon, signals changing consumer preferences. Young professionals are willing to pay ₹500 for a pint of craft beer when a bottle of Kingfisher costs ₹150. For UBL, this presents both threat and opportunity—competition for the premium segment but also validation that Indian consumers are ready to pay more for differentiated products.

Competition from spirits remains intense. Indians drink approximately 3.9 billion liters of spirits annually compared to just 2.7 billion liters of beer. Whiskey, in particular, dominates—India is the world's largest whiskey market. The cultural preference for spirits is partly economic (better "bang for buck" in terms of alcohol content) and partly social (spirits are associated with special occasions and status).

Wine is emerging as another competitor, particularly among urban women who view it as more sophisticated and socially acceptable than beer or spirits. The Indian wine market, though small at about 2 million cases annually, is growing at 25-30% per year from a low base.

The regulatory environment, while challenging, is slowly liberalizing. States like Haryana and Maharashtra have allowed microbreweries. Karnataka permits beer to be sold in supermarkets. Some states are experimenting with allowing home delivery of alcohol—unthinkable just a few years ago. Each liberalization opens new channels and opportunities for growth.

The COVID-19 pandemic accelerated some of these changes. During lockdowns, several states allowed home delivery of alcohol for the first time. Digital ordering platforms emerged. Premium consumption increased as on-premise consumption shifted to home consumption, where people were willing to "trade up" since they were drinking less frequently.

For companies like UBL, navigating this market requires a unique set of capabilities. You need relationships with dozens of state governments. You need supply chains flexible enough to handle sudden regulatory changes. You need brands that can appeal across vast cultural and economic diversity. And you need patience—the patience to play a long game in a market where the rules can change overnight but the opportunity is generational.

IX. Playbook: Business & Investing Lessons

The UBL story offers a masterclass in navigating emerging markets, but not the kind you'd find in a Harvard Business Review case study. This is messier, more complex, and ultimately more instructive because it shows what happens when Western business models collide with Eastern market realities.

Lesson 1: In Highly Regulated Markets, Distribution Is Everything

UBL's true moat isn't its brands or brewing technology—it's the 89,000 outlets across India that stock its products. Building this network took decades and required relationships with thousands of distributors, each of whom knows their local market intimately. When Bira 91 entered the market with a superior product and hip branding, they struggled for years to match UBL's distribution reach. The lesson: in markets where the government controls key parts of the value chain, owning the last mile becomes even more critical.

Lesson 2: Lifestyle Branding Is Powerful Until the Lifestyle Becomes a Liability

Vijay Mallya's genius was making Kingfisher synonymous with aspiration in a country where beer was considered down-market. The calendar girls, Formula 1 sponsorship, and celebrity endorsements worked—until Mallya's personal excesses became front-page news. When your brand is tied to a personality, you inherit both their successes and their scandals. The fact that Kingfisher survived Mallya's downfall shows the brand had transcended its creator, but it was a close call.

Lesson 3: Foreign Ownership Can Be a Feature, Not a Bug

Conventional wisdom suggests local brands have an advantage in emerging markets. Yet Heineken's acquisition of UBL has been remarkably successful. Why? Because Heineken brought three things UBL desperately needed: capital to weather regulatory storms, technical expertise to improve quality and efficiency, and distance from the Mallya scandal. Sometimes being foreign provides exactly the credibility boost a troubled local brand needs.

Lesson 4: Capital Allocation in Emerging Markets Requires Different Math

In developed markets, you optimize for return on invested capital. In India's beer market, you optimize for survival through regulatory cycles. UBL maintains higher inventory levels than global benchmarks because supply can be disrupted by sudden dry days or state government payment delays. India ranks as the world's eighth-largest alcohol market by volume. However, each state independently regulates alcohol pricing, as liquor sales are a crucial source of tax revenue. In Telangana, alcohol is purchased by the state government and then distributed to retail stores. This means carrying extra working capital that would seem inefficient to a Western analyst but is essential for maintaining market position.

Lesson 5: The Perils of Diversification in Capital-Intensive Industries

The Kingfisher Airlines debacle offers a cautionary tale about empire building. Mallya thought he could leverage the Kingfisher brand across categories—beer to airlines made sense in his lifestyle ecosystem. But airlines and breweries have fundamentally different economics. Breweries generate steady cash flows with moderate capital requirements. Airlines burn cash and require constant capital infusion. When Mallya pledged his UBL shares to fund the airline, he put a stable business at risk for a speculative one. The lesson: related diversification isn't always related in terms of business economics.

Lesson 6: Building Distribution Moats in Complex Geographies

India isn't one market—it's 28 states and 8 union territories, each with different rules, taxes, and consumer preferences. UBL built its moat by being one of the few companies willing to navigate this complexity. They established breweries in multiple states to avoid interstate transport restrictions. They maintained relationships with thousands of local distributors who understood ground realities. This distributed manufacturing and distribution model is capital-intensive and operationally complex, but it creates a moat that's nearly impossible for new entrants to replicate quickly.

Lesson 7: Managing Through Regulatory Volatility

The recent Telangana crisis exemplifies a uniquely Indian business challenge. When your biggest customer (the state government) also controls your pricing and can delay payments indefinitely, traditional negotiating tactics don't work. UBL's response—suspending supply to force negotiation—was risky but calculated. They knew the state couldn't afford to have empty beer shelves for long. The lesson: in markets with concentrated buyer power, your leverage comes from being irreplaceable, not from contracts or legal rights.

Lesson 8: The Premium Paradox in Emerging Markets

India presents a paradox: the mass market is price-sensitive, but there's a growing segment willing to pay 10x for premium products. UBL's portfolio strategy—maintaining Kingfisher Strong for volume while building Heineken and craft brands for margin—shows how to capture both. But execution is tricky. If you premiumize too fast, you lose volume. Too slow, and new entrants capture the high-margin segments. The key is maintaining distinct brand identities so premium doesn't cannibalize mass and vice versa.

Lesson 9: When Debt Becomes Destiny

The UBL story is ultimately about leverage—financial and operational. Vittal Mallya built through acquisitions but maintained conservative leverage. Vijay Mallya levered everything—the balance sheet, the brand, his personal reputation. When you're selling to state governments that can delay payments, when regulations can change overnight, when your brand depends on "good times" messaging, high leverage becomes existential risk. The company that survived was the one that understood this fundamental truth about emerging market volatility.

Lesson 10: The Value of Patient Capital

Heineken's approach to UBL shows the value of patient capital in emerging markets. They didn't immediately integrate operations or impose European management styles. They provided stability during the Mallya crisis, gradually increased their stake as opportunities arose, and only took full control when the timing was right. This patience—foreign capital with local patience—might be the optimal structure for emerging market consumer businesses.

X. Analysis & Bear vs. Bull Case

Bull Case: The Demographic Dividend Is Real

The arithmetic is compelling. India adds 10 million people to its legal drinking age population every year. Per capita beer consumption at 2 liters has nowhere to go but up—even reaching China's 30 liters would mean a 15x increase. With 50%+ market share, UBL is positioned to capture a disproportionate share of this growth.

The premiumization story adds another layer. As Indians travel more, eat out more, and adopt global consumption patterns, beer is becoming socially acceptable beyond its traditional male, urban base. Women's consumption, while starting from near zero, is growing rapidly in metros. The craft beer movement is educating consumers about beer as a sophisticated beverage, not just cheap alcohol.

Heineken's ownership provides strategic advantages beyond capital. Access to global brands like Heineken and Amstel allows UBL to compete in super-premium segments without diluting Kingfisher. Technical expertise in brewing, supply chain, and sustainability helps improve margins. Perhaps most importantly, Heineken's long-term orientation means UBL can invest for market position rather than quarterly earnings.

The regulatory environment, while still complex, is gradually liberalizing. More states are allowing microbreweries, home delivery, and sales in modern retail. The GST implementation, while initially disruptive, has simplified interstate commerce. As state governments face fiscal pressure, they're more likely to liberalize alcohol sales to boost tax revenues.

Market leadership creates a virtuous cycle. UBL's scale allows it to negotiate better with state governments, invest in new products, and maintain the widest distribution network. Competitors face a chicken-and-egg problem: they need scale to be profitable, but need profitability to achieve scale.

Bear Case: Structural Challenges Persist

But the bear case is equally compelling. Company has a low return on equity of 9.73% over last 3 years—hardly the returns you'd expect from a market leader in a growing category. This suggests structural issues beyond temporary headwinds.

The regulatory overhang remains severe. The Telangana crisis showed that even after decades of operations, UBL remains vulnerable to state government whims. With alcohol being a state subject and major revenue source, governments will continue to extract maximum value, keeping industry margins compressed.

Competition is intensifying from multiple directions. AB InBev and Carlsberg have deep pockets and global brands. Craft brewers are cherry-picking the highest-margin consumers. United Spirits (now owned by Diageo) is launching ready-to-drink products that blur the lines between spirits and beer. Even within beer, private label brands from state corporations are emerging.

Debtor days have increased from 96.5 to 117 days, indicating worsening payment terms with state governments. This working capital pressure limits UBL's ability to invest in growth. When your biggest customers consistently pay late, cash flow becomes a constant challenge regardless of reported profitability.

Cultural headwinds persist in large parts of India. States like Bihar and Gujarat, representing over 150 million people, maintain prohibition. Religious and social taboos limit the addressable market. Even in permissive states, occasions for beer consumption remain limited compared to Western markets.

Input cost inflation poses another challenge. Barley, glass bottles, and aluminum cans are all seeing price increases. With state governments controlling selling prices, UBL can't easily pass on cost increases. This margin squeeze is structural, not cyclical.

The mass market, which still drives volumes, remains extremely price-sensitive. Kingfisher Strong competes with country liquor and illegal moonshine in rural areas. Moving consumers up the price ladder is harder than premium market growth suggests.

Climate change adds a long-term risk. Beer production is water-intensive, and many of UBL's breweries are in water-stressed regions. Erratic monsoons affect barley production. Environmental regulations are tightening. These ESG considerations, while manageable now, could become material constraints.

The Verdict: A Complex Investment Case

The investment case for UBL isn't binary—it's a study in navigating contradictions. The company operates in one of the world's most challenging alcohol markets yet maintains dominant market share. It faces constant regulatory pressure yet continues to grow. It's controlled by a foreign multinational yet remains quintessentially Indian in its operations.

For investors, the key question isn't whether India's beer market will grow—it will. The question is whether UBL can capture enough of that growth at sufficient margins to generate attractive returns. The answer depends on your time horizon and risk tolerance.

If you believe India's regulatory environment will gradually liberalize, that premiumization will accelerate, and that Heineken's patient capital and expertise will drive operational improvements, then UBL represents a compelling way to play India's consumption story.

But if you're concerned about regulatory unpredictability, intensifying competition, and structural margin pressure, then UBL's market leadership might not translate into superior returns.

The truth, as often happens in emerging markets, lies somewhere in between. UBL will likely continue to dominate Indian beer, grow revenues, and gradually improve operations. But the path will be volatile, margins will remain under pressure, and returns will reflect the reality of operating in one of the world's most complex consumer markets.

XI. Epilogue & Future Outlook

Ten years from now, what will success look like for United Breweries? The answer depends not just on the company's execution but on how India itself evolves—economically, socially, and regulatorily.

The optimistic scenario sees India's per capita beer consumption reaching 10 liters by 2035—still modest by global standards but a 5x increase from today. In this world, UBL's revenues would exceed ₹50,000 crore, premium brands would constitute 40% of the portfolio, and operating margins would approach international benchmarks. The company would have successfully navigated the transition from volume growth to value growth, much like consumer companies in other Asian markets have done.

This scenario requires several things to go right. State governments would need to view the alcohol industry as a partner in development rather than just a tax cow. This means more predictable pricing policies, timely payments, and gradual liberalization of retail. The cultural acceptance of beer, particularly among women and in tier-2/3 cities, would need to accelerate. And UBL would need to successfully premiumize without losing its mass market stronghold.

The realistic scenario is more nuanced. India's beer market will grow, but unevenly. Metro cities might reach European consumption levels while rural areas remain dry. State-by-state regulation will persist, but digital systems will make compliance easier. UBL will maintain market leadership but at lower margins than global peers. The company will generate steady if unspectacular returns—a classic defensive play in an emerging market.

Competition will intensify but remain rational. The market is big enough for multiple players to grow without destructive price wars. Craft beer will carve out a profitable niche without threatening the mass market. International brands will coexist with local ones. The market structure will resemble China's—a few large players with regional strengths rather than a single dominant force.

The ESG transition presents both risk and opportunity. Water scarcity will force operational changes, but UBL's scale allows it to invest in water recycling and conservation. Carbon neutrality commitments will increase costs but also provide differentiation. Local sourcing of barley through contract farming will reduce supply chain risks while supporting rural incomes. These initiatives, while costly upfront, position UBL for long-term sustainability.

Technology will reshape distribution and consumption patterns. Direct-to-consumer delivery, where permitted, will improve margins and consumer insights. QR codes on bottles will combat counterfeiting—a significant issue in Indian alcohol. Data analytics will optimize production and distribution in ways impossible today. But technology also enables new competitors and business models UBL must adapt to.

The non-alcoholic opportunity deserves special attention. As health consciousness rises and designated driver culture develops, non-alcoholic beer could become a significant category. UBL's distribution network and brand equity position it well for this transition. Kingfisher 0.0 or Heineken 0.0 could capture consumers who want the social experience of beer without the alcohol.

Consolidation seems inevitable. India's beer market remains fragmented with numerous small players. As compliance costs rise and scale becomes more critical, smaller brewers will struggle. UBL, with its balance sheet strength and operational expertise, is well-positioned to acquire distressed assets. Each acquisition would strengthen its manufacturing footprint and eliminate competition.

The generational transition in consumer behavior will be decisive. Indians born after 2000 have grown up in a liberalizing economy with global exposure. They view alcohol consumption differently than their parents. They're willing to experiment, pay for quality, and aren't bound by traditional spirit preferences. This cohort, reaching peak consumption years in the 2030s, will determine whether beer becomes a mainstream beverage or remains niche.

What would failure look like? A scenario where prohibition spreads rather than recedes. Where state governments, facing fiscal pressure, extract even more value from alcohol companies. Where climate change makes barley cultivation unviable and water scarce. Where a new generation rejects alcohol entirely for health or cultural reasons. These aren't probable scenarios, but they're possible enough to warrant consideration.

The United Breweries story—from colonial brewery to Indian icon to global subsidiary—mirrors India's own economic journey. Like the country itself, UBL faces the challenge of modernizing while maintaining identity, of globalizing while remaining local, of growing while managing complexity.

Success won't be measured just in market share or margins but in the company's ability to navigate India's unique challenges while capturing its enormous opportunities. It's a task that requires not just capital and strategy but patience, relationships, and deep cultural understanding.

For Heineken, UBL represents more than just an emerging market subsidiary. It's a laboratory for learning how to operate in complex, regulated markets—lessons applicable from Africa to Southeast Asia. For India, UBL represents the possibility that consumer companies can thrive despite, or perhaps because of, the country's complexity.

The next decade will determine whether United Breweries remains merely the king of Indian beer or becomes something more—a truly global player that happens to be rooted in India. The potential is there. The challenges are real. The outcome remains unwritten.

But one thing is certain: in a country where prohibition coexists with the world's largest whiskey market, where ancient traditions meet modern aspirations, where 28 states means 28 different business environments, the UBL story will continue to be anything but boring.

The good times may have ended for Vijay Mallya, but for United Breweries, they might just be beginning—though they'll look very different from what anyone imagined when Thomas Leishman consolidated those colonial breweries over a century ago.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube