Thermax: Engineering India's Energy Transition

I. Introduction & Episode Roadmap

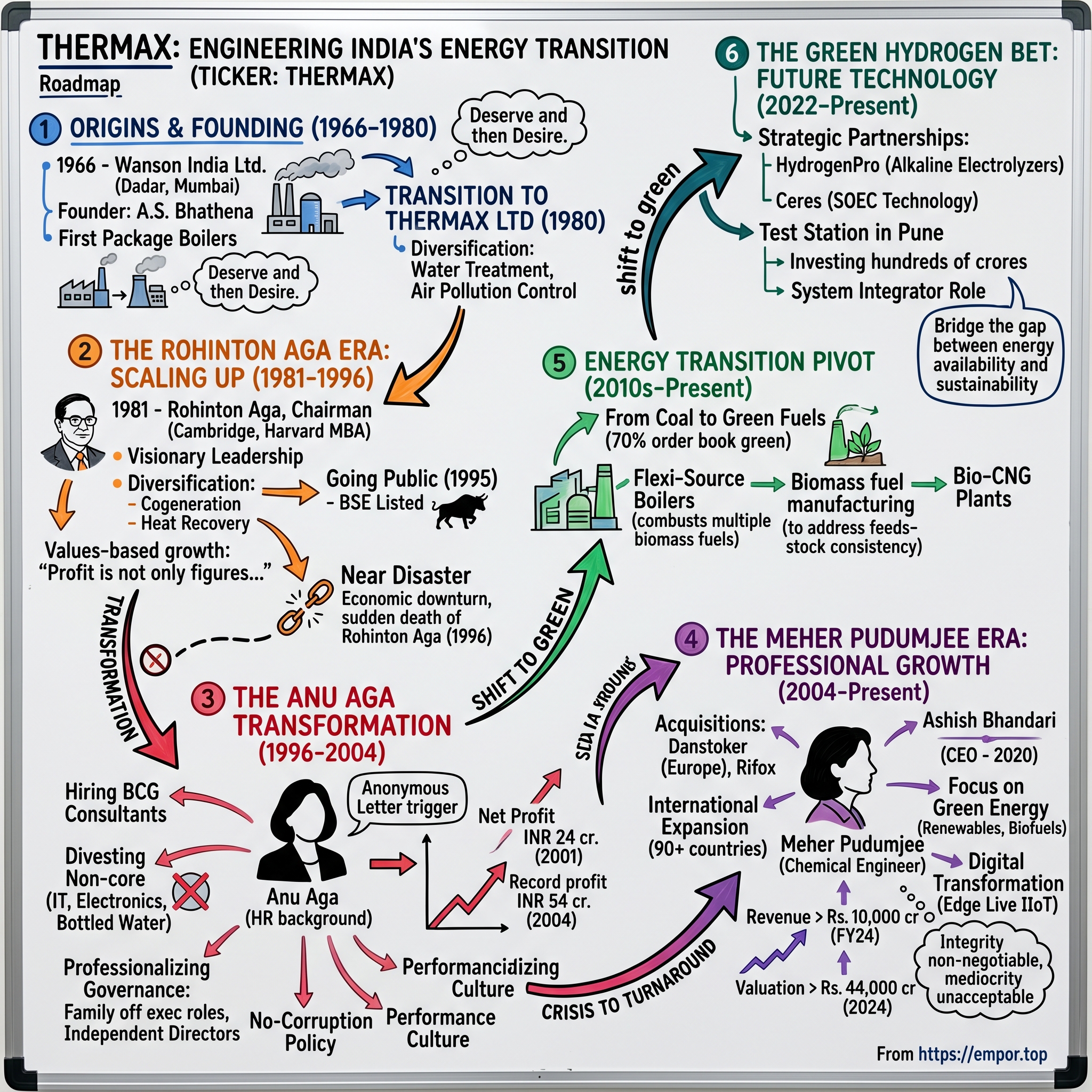

Picture this: It's 1966 in post-independence India, where industrial licenses are gold and imported technology is a luxury. In a small workshop in Dadar, Mumbai, A.S. Bhathena is assembling his first package boiler—a humble beginning for what would become a ₹39,297 crore energy solutions powerhouse. Today, Thermax stands at the intersection of India's industrial heritage and its green future, with 70% of its order book dedicated to clean energy solutions.

The question isn't just how a small boiler manufacturer transformed into India's trusted partner in energy transition—it's how a family business navigated economic liberalization, survived near-death experiences, and positioned itself at the forefront of technologies that didn't exist when it started. This is the story of three generations of leadership, each facing their own existential challenge: Bhathena's import substitution, the Aga family's professionalization crusade, and now Meher Pudumjee's bet on green hydrogen.

Thermax today offers integrated solutions across the entire energy value chain—heating, cooling, power generation, water treatment, air pollution control, and specialty chemicals. But the real story lies in how it got here: through crisis-driven transformations, counter-intuitive strategic choices, and a radical commitment to ethics in an industry notorious for corruption.

What makes Thermax particularly fascinating for students of business is its repeated ability to reinvent itself. This isn't a linear growth story—it's a series of near-disasters turned into competitive advantages. From Anu Aga's decision to fire family members from executive positions to the current pivot away from fossil fuels that still generate 30% of revenues, Thermax has consistently chosen long-term sustainability over short-term comfort.

As we dive into this journey, we'll explore how a company built on coal-fired boilers is now betting hundreds of crores on green hydrogen, why a grieving widow's leadership style became a Harvard case study, and what Thermax's evolution tells us about India's broader industrial transformation. This is as much a story about values and leadership as it is about technology and markets.

II. Origins & Founding Story (1966-1980)

The year is 1966. India's industrial landscape is a peculiar mix of socialist ideals and capitalist ambitions, where getting a license to manufacture anything requires navigating a bureaucratic maze that would make Kafka proud. In this environment, A.S. Bhathena collaborated with a Belgian company, Wanson, to commence business operation as Wanson India Ltd., manufacturing small boilers at a unit in Dadar, Mumbai.

But Bhathena wasn't your typical industrialist. He began his career as a 'worker-entrepreneur' in 1947, with the founding of a partnership firm – National Steel, manufacturing sterilizers, autoclaves and other hospital equipment. This background shaped his management philosophy profoundly. He was a keen practitioner of 'Management by wandering about,' through which he kept in constant touch with his staff and workers. A S Bhathena was a passionate advocate of achieving success through merit and hard work. His favorite quote was: 'Deserve and then desire.'

The timing of Wanson India's founding was no accident. India's Second Five-Year Plan (1956-61) had prioritized heavy industrialization, creating enormous demand for industrial boilers. But importing them was expensive and difficult under the foreign exchange constraints of the era. Bhathena saw the gap: India needed someone who could manufacture quality boilers locally, with international technology but adapted to Indian conditions—erratic power supply, varying coal quality, and extreme weather conditions.

The Belgian connection was strategic. Wanson was a respected name in industrial heating, but they needed a foothold in the protected Indian market. For Bhathena, it meant access to technology without the massive R&D investment that would have been impossible for a startup. This technology transfer model would become the template for Indian industrial development—not copying, but adapting and eventually innovating.

The company was renamed Thermax Limited in 1980, marking a critical transition. The name change wasn't just cosmetic—it signaled independence from the Belgian partner and ambition beyond being a local licensee. By this time, the company had begun manufacturing equipment related to cogeneration, air pollution control, water treatment and absorption refrigeration.

What's remarkable about this diversification is its prescience. In 1980, environmental regulations in India were virtually non-existent. The Air (Prevention and Control of Pollution) Act had just been passed in 1981. Yet Bhathena was already building capabilities in pollution control equipment. This wasn't environmental activism—it was pattern recognition. He had seen how regulations evolved in Europe and bet that India would follow a similar trajectory, just delayed by a decade or two.

The early product portfolio tells a story of pragmatic innovation. The Vaporax and Thermopac boilers weren't technological marvels—they were reliable, maintainable machines designed for Indian conditions. While competitors chased prestigious large-scale projects, Thermax focused on the unglamorous middle market: textile mills, pharmaceutical plants, food processing units. These customers couldn't afford downtime and valued service over specifications.

The journey from Vaporax and Thermopac – products from the early years, to the current stable of products; from bagging our first export order to establishing a presence in the overseas markets, has been an arduous one. That first export order—details are scarce but it likely went to a neighboring country facing similar infrastructure challenges—validated something important: Thermax's "good enough" technology had global relevance in emerging markets.

By 1980, when Bhathena prepared to hand over the reins, Thermax had evolved from a single-product company to an industrial conglomerate in miniature. The foundation was set: technical competence, customer focus, and most importantly, a culture that valued merit over connections in an economy where the opposite was often true. The stage was set for the next act, where his son-in-law would take these solid but modest foundations and build something far more ambitious.

III. The Rohinton Aga Era: Scaling Up (1981-1996)

In 1981, when Bhathena was succeeded by his son-in-law Rohinton Aga as chairman, India was on the cusp of transformation. The License Raj still ruled, but whispers of liberalization were beginning. Born in 1935, Rohinton hailed from a Parsi family in Bombay. A graduate in economics from Cambridge, he also was an alumni of the Harvard University Graduate School of Business Administration. This combination—Cambridge economics and Harvard MBA—was rare in 1980s India, where most industrialists were either self-made entrepreneurs or inheritors of family businesses.

Rohinton was a seer, a dreamer and above all a great doer. His leadership transformed Thermax from a small boiler company, to a multi-divisional engineering force, with a focused vision to provide solutions that conserving energy and preserve the environment. But this transformation wasn't immediate or obvious. Rohinton faced a classic succession challenge: how to honor the founder's legacy while preparing for a radically different future.

His first insight was that Thermax couldn't remain a boiler company. The industrial landscape was shifting—Indian companies were becoming more sophisticated, environmental consciousness was growing globally, and competition from both domestic players and potential foreign entrants (once liberalization happened) would intensify. Rohinton believed that businesses need to be built on foundations of enduring values. 'Profit is not only a set of figures, but of values,' he often reminded his teams.

The diversification strategy under Rohinton wasn't scattershot—it followed a logic of adjacencies. From boilers, Thermax moved into heat recovery systems (capturing waste heat from the boilers they were already selling). From heat recovery, they moved into cogeneration (using that captured heat to generate power). Each step built on existing customer relationships and technical capabilities while expanding the value proposition.

The company's move into water treatment exemplifies this approach. Industrial customers using Thermax boilers needed treated water to prevent scaling and corrosion. Rather than let specialized water treatment companies capture this business, Thermax developed in-house capabilities. This wasn't just about capturing more revenue—it was about becoming indispensable to customers by solving multiple interconnected problems.

By the early 1990s, India's economic landscape was shifting dramatically. The 1991 balance of payments crisis forced liberalization, dismantling the License Raj almost overnight. Foreign companies could now enter India, Indian companies could access foreign technology more easily, and the cozy protections that had sheltered domestic industry were disappearing. For many Indian companies, this was terrifying. For Thermax under Rohinton, it was validation of a strategy already in motion.

In February 1995, the company went public and listed on the Bombay Stock Exchange. The timing was deliberate. Post-liberalization capital markets were booming, foreign institutional investors were entering India, and there was appetite for well-managed, technically competent companies. The IPO wasn't just about raising capital—it was about institutionalizing Thermax, creating liquidity for stakeholders, and establishing market discipline.

The public listing also forced transparency and professional governance practices that would prove crucial in the crisis to come. Quarterly reporting, independent directors, audit committees—these weren't just compliance requirements but cultural shifts that moved Thermax from being a closely-held family business to a professionally-managed corporation, even while family control was maintained.

What's often overlooked about Rohinton's era is his focus on creating management depth. He systematically hired professionals from IITs and IIMs, sent promising managers abroad for training, and created a culture where meritocracy could coexist with family ownership. This wasn't common in 1980s India, where family businesses typically reserved key positions for family members and trusted retainers.

He gained recognition as a visionary entrepreneur and a management thinker. But vision without execution is hallucination, and Rohinton understood this. He invested heavily in manufacturing capabilities, R&D facilities, and most importantly, in building a service network. In the industrial equipment business, the sale is just the beginning—maintenance, repairs, upgrades, and operational support generate recurring revenue and customer stickiness.

By 1996, Thermax had evolved from a ₹10 crore boiler manufacturer to a ₹400 crore diversified engineering conglomerate. The company had international operations, a portfolio spanning energy and environment solutions, and a reputation for technical excellence and ethical business practices. Rohinton had successfully navigated the transition from protected markets to liberalized competition, from single products to integrated solutions, from family business to professional corporation.

He was a director of the Thermax Company till 1996, when he died of a massive stroke. The timing could not have been worse. India's economy was experiencing post-liberalization volatility, industrial growth was slowing, and Thermax was in the middle of ambitious expansion plans. The company that Rohinton had built for the future would now have to navigate that future without him. The question wasn't just about succession—it was about survival.

IV. The Anu Aga Transformation: Crisis to Turnaround (1996-2004)

The scene is February 1996. Anu Aga is returning from London after spending six months with her daughter Meher, who had just given birth. Her husband Rohinton is driving from Pune to Mumbai to receive her at the airport—a gesture of love after a long separation. He never makes it. A massive heart stroke takes his life on that journey. Within 48 hours, the board of Thermax meets and decides: the 54-year-old widow with 62% family ownership must take charge.

At that time, the Indian economy was in the midst of a severe downturn. Despite the fact that she had little background in either business or engineering, she immediately recognized that the company was out of depth and needed major re-structuring. The numbers told a brutal story: Thermax's share price had fallen from Rs. 400 to Rs 36. The company that had gone public just a year earlier was now facing existential crisis.

Anu's background couldn't have been more different from a typical industrialist. She had graduated with a B.A. in economics from St Xavier's College, Mumbai, and held a post-graduate degree in medical and psychiatric social work from the Tata Institute of Social Sciences. She had been a Fulbright Scholar. Her career at Thermax began only in 1985 in Human Resources—a "soft" function in a hard engineering company. She headed the HR function from 1991 to 1996.

The board's calculation in appointing her was cynical. As Anu herself later reflected: some board members assumed she could be bullied. They were catastrophically wrong. But first came the moment of reckoning that changed everything—an anonymous letter.

The immediate trigger for change was an anonymous letter from a shareholder blaming her for inaction. She had thought that poor performance mainly affected her and her family, the majority shareholders. Suddenly, she realised that as a public limited company they had to protect the interests of the 40-odd per cent shareholders who had placed their faith in Thermax.

This letter didn't just wound her pride—it awakened her sense of duty. The realization was profound: ownership without competence is betrayal of trust. She was convinced that management was out of its depth and needed outside help. But when she proposed hiring consultants, the resistance was fierce. Her senior executives resisted the idea. Most men find it difficult to seek help because it comes in the way of their 'macho image'.

The decision to hire Boston Consulting Group was revolutionary for its time. Indian family businesses rarely admitted weakness, let alone paid foreign consultants to diagnose their problems. She knew she needed to seek expert financial advice, despite reluctance from the company's board members to seek outside help and pay for the services. But Anu understood something her executives didn't: "I wasn't afraid to say, 'I don't know'".

What BCG found was a company that had lost its way. Thermax had diversified into many non-core businesses like IT, electronics, bottled water, which added to the top line but eroded profits. The diversification under Rohinton had been strategic; under his successors, it had become scattershot. Thermax had been over-ambitious, getting into unrelated areas instead of concentrating on its core competence. With the help of the Boston Consulting Group, Thermax got out of unrelated fields and also downsized effectively.

The turnaround required surgery, not medicine. The turnaround focused on divesting non-core businesses. They restructured into six core businesses in the areas of energy and environment. But the human cost was enormous. Many divisions had to close down and several employees were asked to leave. Thanks to the graciousness of those employees, they left without bitterness.

The most radical decision was professionalizing governance. In the first few years of her leadership, Aga took the decision to remove family members from executive positions and instead place them on the Thermax board. This included her own daughter Meher. Aga dismissed the entire board, including her daughter Meher Pudumjee, she replaced them with fresh members who could restructure the entire company's business.

They reconstituted the board to bring in more independent directors. The promoter members stepped down from executive positions, and operational aspects were left to a nonfamily professional team led by the managing director. For a Parsi family business in the 1990s, this was heresy. But Anu understood that the company's survival depended on competence, not bloodlines.

The cultural transformation was equally dramatic. By downsizing and improving operational efficiency, they were able to bring down employee cost from 16 per cent of turnover to less than 7.5 per cent, on a larger sales base. They also brought in a performance culture. This wasn't just cost-cutting—it was about creating accountability where entitlement had prevailed.

But perhaps the most controversial stance was on corruption. Her commitment to responsibility led her to take a hardline stance against corruption within Thermax. She convinced Thermax board members to institutionalize a no-corruption policy as part of the company's corporate culture. In an industry where "commission" and "facilitation fees" were standard operating procedure, Thermax would compete on merit alone.

The results validated every difficult decision. In April, Thermax announces turnaround results with a net profit of INR 24 crores. On August 19, Thermax declares 50% dividend, the highest since going public. By 2004, Thermax registers highest ever profit after tax of INR 54 crores.

The transformation wasn't just financial—it was philosophical. "Profit is not a set of figures, but a set of values," said Anu Aga, quoting her late husband. She had taken his words and made them operational reality. In her eight years as company chair, Aga transformed the energy and environmental engineering business. During her tenure, Thermax Global was labeled one of Asia's best small businesses, and she became one of the world's wealthiest businesswomen.

The personal cost of this transformation cannot be understated. In 1997, just as the turnaround was beginning, tragedy struck again. Her 25-year-old son Kurush was killed in a road accident. To lose a husband and son within two years while stewarding a corporate turnaround would break most people. Anu found strength in Vipassana meditation and in the very work that seemed overwhelming.

The most difficult and yet the most important move was to change the mindset and the culture of the company. She had inherited a company built on relationships and run it into one built on processes. She had taken a family business and made it institutionally robust. Most importantly, she had proven that crisis could catalyze transformation if leadership had the courage to acknowledge weakness and seek help.

By 2004, Thermax was ready for its next chapter, and so was Anu. The succession planning was as thoughtful as the turnaround itself, setting the stage for another woman to lead Thermax into the 21st century.

V. The Meher Pudumjee Era: Professional Growth (2004-Present)

In 2004, Aga took the decision to step down as chairperson and selected her daughter, Meher Pudumjee, as her successor. The handover was as unconventional as everything else about Anu's leadership. She publicly announced her retirement before Meher had formally accepted—a calculated move that created external pressure for continuity while respecting her daughter's autonomy.

She took over as Chairperson on October 5, 2004, after the retirement of Mrs. Anu Aga. But Meher wasn't walking into a cushy inheritance. A postgraduate in Chemical Engineering from the Imperial College of Science & Technology, London, Meher joined Thermax as a trainee engineer in August 1990. A year later, along with her husband Pheroz Pudumjee, they took over the responsibility of turning around a Thermax subsidiary company in the UK.

This UK assignment was formative. Away from the family name's shadow, Meher had to prove herself on merit alone. The subsidiary's turnaround within three years established her credentials as a problem-solver, not just an heir. After her return to India in September 1996, she was appointed on the Board of Directors. With her newly acquired interest in Finance, she worked closely with the treasury and working capital management functions of Thermax.

The timing of her ascension was fortuitous. India's infrastructure boom was accelerating, driven by 8-9% GDP growth. But Meher understood that riding the wave wasn't enough—Thermax needed to position itself for the inevitable downturn. Her first major strategic decision was counterintuitive: instead of chasing growth at any cost, she focused on operational excellence and margin improvement.

Then came 2008. The 2008 financial crisis, also known as the global financial crisis (GFC) or the Panic of 2008, was a major worldwide financial crisis centered in the United States. For Thermax, heavily dependent on industrial capex, this should have been catastrophic. Orders dried up, projects were cancelled, and competitors began desperate price-cutting.

But Meher had prepared for this moment. The operational improvements meant Thermax could maintain profitability even at lower volumes. More importantly, she saw opportunity where others saw disaster. The World Economic Forum in 2008 selected her as a Young Global Leader for her professional accomplishment, commitment to society and potential to contribute to shaping the future of the world. She was selected CEO of the Year, 2009 by Business Standard.

The recognition wasn't just ceremonial—it reflected a remarkable achievement. While competitors retreated, Thermax went on an acquisition spree. She expanded its international operations by acquiring Danstoker A/S and its German subsidiary, Omnical Kessel, in November 2010. In March 2012, the company acquired Rifox-Hans Richter GmbH, a manufacturer of steam accessories, and later took a 33% stake in Pune-based First Energy, a producer of biomass stoves and pellet fuel for residential and commercial use.

These weren't random purchases. Danstoker brought European environmental technology, crucial for India's tightening emission norms. Rifox added high-margin aftermarket products. First Energy provided entry into distributed renewable energy. Each acquisition filled a capability gap while providing geographic or product diversification.

The results validated the strategy. By 2012, Thermax reported annual revenues exceeding ₹5,000 crore (approximately USD $1 billion). But revenue growth was just one metric. A leader who walks the talk, she has doubled Thermax Ltd's turnover over a decade, restructured the business, expanded into renewable energy, and advanced the company's digital transformation to enhance asset performance.

The digital transformation deserves special attention. While competitors focused on hardware, Meher understood that software and services would drive future differentiation. Thermax began embedding IoT sensors in equipment, offering predictive maintenance, and selling outcomes rather than products. A boiler sale became a steam-as-a-service contract. A water treatment plant became a zero-liquid-discharge guarantee.

During her tenure as chairperson, Thermax developed solar thermal and photovoltaic panels to reduce environmental impact. This wasn't greenwashing—it was strategic positioning for India's energy transition. Meher recognized that Thermax's fossil fuel heritage could be either an albatross or an advantage. She chose to make it an advantage: who better to help industries decarbonize than a company that understands their existing processes intimately?

The governance evolution under Meher has been subtle but significant. Unlike her mother's crisis-driven transformation, Meher's changes have been evolutionary. Professional managers were given more autonomy. The board became more diverse—not just in demographics but in expertise, bringing in digital, sustainability, and international experience.

As of FY24, the company had over 40 subsidiaries (20 in India), 14 manufacturing sites (10 in India), and a sales and service network across 90-plus countries. This global footprint wasn't built through ego-driven expansion but through careful capability building. Each market entry followed a template: start with projects, establish service capability, then consider local manufacturing.

The cultural transformation has been equally important. Meher maintained the ethical standards her mother established while adding performance orientation. The message was clear: integrity was non-negotiable, but mediocrity was unacceptable. This combination attracted talent that might otherwise have gone to multinationals or startups.

In 2022, Meher Pudumjee and her mother, Anu Aga, were ranked seventh on the Kotak Private Banking-Hurun Leading Wealthy Women 2021 list, with an estimated net worth of ₹14,530 crore. She was ranked as the 5th most influential woman in family-owned businesses in India, according to the 2024 Barclays Private Clients Hurun India report, which noted Thermax's valuation at ₹44,000 crore.

But perhaps Meher's greatest achievement has been managing the transition to professional management while maintaining family control. In 2020, she appointed Ashish Bhandari as Managing Director & CEO—the first outsider to hold operational control. This wasn't abdication but evolution. The family remained committed shareholders and board members while professional management ran daily operations.

The company operates through four reportable segments which are industrial products, industrial infra, green solutions, and chemicals. What's remarkable is how these segments have been rebalanced under Meher's leadership. Green solutions, virtually non-existent in 2004, now represents the growth engine. Industrial infra has shifted from pure construction to technology integration. Even chemicals has moved toward specialty and sustainable products.

Looking at Meher's two-decade tenure, the transformation is striking. She inherited a recovered but traditional industrial company and built a diversified, technology-enabled, sustainability-focused conglomerate. Revenue has grown over 10x, but more importantly, the business model has fundamentally evolved. Thermax is no longer selling equipment—it's selling solutions, services, and outcomes. The next chapter of this transformation would require betting on technologies that didn't yet exist at commercial scale.

VI. The Energy Transition Pivot: Green Solutions (2010s-Present)

The transformation began with a simple observation: India's rice farmers were burning 23 million tonnes of paddy straw every year, creating the toxic smog that choked Delhi every winter. Meanwhile, industrial plants were burning expensive imported coal for their energy needs. In Northern India, rice straw burning by farmers (double firing) pollutes the air, impacting Delhi and surrounding areas. This worsens the Air Quality Index (AQI). This solution allows the use of rice straw as fuel, which provides farmers with an income incentive and eliminates the need to burn it.

This wasn't just an environmental problem—it was a massive arbitrage opportunity disguised as agricultural waste. Thermax's response would reshape not just its business model but India's entire approach to industrial energy.

This surge in green solutions marks a strategic pivot for the company shifting from a 60-70% dependence on fossil fuels in their traditional boiler business to a focus on sustainable alternatives. The shift wasn't gradual—it was deliberate and dramatic. By 2024, in Thermax's industrial heating range, biomass already accounts for more than 70 per cent of its sales.

The technical challenge was formidable. As coal costs escalated and waste fuels presented inconsistency challenges, an industry-wide plea arose for a boiler capable of efficiently combusting a diverse range of 10-15 fuels for both steam and power generation. While existing boilers could handle biomass fuels like rice husk or wood chips, these lacked the flexibility to tackle trickier options like agricultural waste or municipal solid waste. The Flexi-Source rises to the challenge, offering industry unparalleled fuel flexibility.

The Flexi-Source solution wasn't just an engineering achievement—it was a business model innovation. One minute you're hearing about mustard stalks being turned into fuel, and the next, about cutting-edge Flexi Source systems that can run on up to 11 different kinds of fuels. "More importantly," Bhandari points out, "we take what is wasted within the plant currently and give it back to them in the form of useful energy." The company captures the steam from potato frying, uses it to power chillers for cooling, and recycles the recovered water vapor back into the system to wash more potatoes.

Thermax, with its integrated energy and environment solutions, is helping India unlock the energy potential of Bio-CNG, Green Hydrogen, coal gasification, waste-to-energy, and waste heat recovery. Enabling the energy transition calls for the collective efforts of stakeholders across multiple sectors. Cognizant of the importance of policy alignment and industry participation, Thermax collaborates with farmers, municipal bodies, businesses, and other concerned stakeholders to commercialise the production of clean fuels. The company offers technologies, solutions, and services to support the multi-fuel strategy it champions.

The bio-CNG push exemplifies this multi-stakeholder approach. Secures orders exceeding Rs. 500 crore for the establishment of five bio-CNG plants But execution proved harder than expected. "Last year, Thermax lost a fair bit of money in stabilizing these bio-CNG plants," Bhandari admits. This transparency about failures is rare in Indian corporate culture—and indicative of how seriously Thermax takes its transition role.

The renewable energy expansion shows similar ambition. Another initiative aligned towards clean energy is the installation of 1 GW of hybrid renewable energy solutions by FY 2027. These will be intra-state and inter-state projects, helping industries with a variety of offerings, including round-the-clock clean electricity requirements. Amongst the 290 MWp (commissioned and under construction) is our latest state-of-the-art wind and solar bundled captive power project comprising 100 MW wind and 90 MWp solar, located in Thoothukudi, Tamil Nadu, which is being evacuated at 110 kV in a phased manner.

The technology partnerships reveal the sophistication of Thermax's approach. Over the years, Thermax has formed technology partnerships with global majors, including Babcock & Wilcox, USA (boilers), Balcke-Duerr GMBH, Germany (dry electrostatic precipitators, regenerative air gas heaters and pulse jet bag filters), Lambion Energy Solutions, Germany (grate technologies) and Marsulex Environment Technologies, USA (wet and semi-dry flue gas desulphurisation technology), Power Roll (developing unique, low-cost and lightweight, flexible solar films), Steinmuller Babcock Environment (Municipal Solid Waste fired waste to energy boilers) and ExactSpace Technologies (AI solutions to decarbonise industrial plants and eliminate unplanned failures).

But technology alone doesn't drive transformation—business model innovation does. The build-own-operate model represents a fundamental shift from selling equipment to selling outcomes. To address the ~200 tonnes/day of biomass fuel requirement, the company has developed dedicated fuel manufacturing facilities to ensure optimum fuel quality and quantity across the year. Operated under the build-own-operate model, with this project, the client is relieved of the responsibility of operating and managing part of their steam and power requirements while also achieving nearly 48,000 tonnes/year of equivalent CO2 reduction against furnace oil.

The digital layer amplifies this transformation. Thermax's IIoT platform, Edge Live, has seen breakneck adoption since launching in 2022. It now monitors over 4,800 assets across 200+ plants in 22 countries. "We want to be able to monitor a variety of data that industrial plants give out," Bhandari says, "starting with assets that Thermax is particularly comfortable with and we know very well, which are at the heart of energy for any given plant." Edge Live isn't just about uptime; it's about insight — unlocking 2 to 10 per cent efficiency gains with machine learning, diagnostics, and real-time analytics.

The gasification initiative shows how Thermax leverages its heritage while embracing the future. Furthermore, Thermax aims to develop gasification plants with carbon capture capabilities to process coal ranging from 100 to 500 TPD. Based on fluidised bed coal gasification technology, Thermax has implemented a pilot gasifier project at its factory in Pune in partnership with IIT Delhi, with support from the Department of Science and Technology. This indigenously developed technology converts high-ash Indian coal into value-added fuels. It is particularly beneficial for hard-to-abate industries like the steel sector and aligns with the Prime Minister's vision of gasifying 100 million tonnes of coal by 2030.

The impact metrics validate the strategy. Replacing coal with waste dramatically lowers CO2 emissions. A typical 4 MW plant using Flexi-Source avoids over 90,000 tons of annual CO2 compared to coal by minimizing transportation-related emissions and uncontrolled waste burning.

MD and CEO Ashish Bhandari, on the occasion, said, "For 50 years, Thermax has played a vital role in India's energy landscape. We are continuously driving sustainability through innovation, cross-functional expertise and partnerships. To address the country's unique energy challenges, we have pioneered technologies for converting waste to energy and are investing in newer areas such as hybrid renewables, biofuels, green hydrogen, and more. As a trusted partner in energy transition, our commitment is to bridge the gap between energy availability and sustainability." With these focussed efforts, Thermax is poised to make substantial contributions towards a greener future.

The financial performance reflects this transformation. Thermax reported a consolidated revenue of Rs. 10,389 crore in FY 2024-25, marking an 11.4% increase from Rs. 9,323 crore in FY 2023-24. But more important than revenue growth is the composition change—green solutions now drive both growth and margins.

What makes Thermax's green pivot remarkable isn't just its scale but its pragmatism. This isn't a company abandoning its core business for fashionable green technologies. It's systematically converting its deep understanding of industrial processes into transition solutions. Every paper mill that switches from coal to agricultural waste, every chemical plant that captures waste heat, every municipality that converts garbage to power—these aren't just environmental wins. They're proof points that the energy transition can be profitable, scalable, and immediate. The next chapter would require even bigger bets on technologies that were still in laboratories.

VII. The Green Hydrogen Bet: Future Technology (2022-Present)

The scene is March 2023. Australia's mining billionaire Andrew Forrest's Fortescue Future Industries signs a Memorandum of Understanding with Thermax Limited to explore green hydrogen projects, including new manufacturing facilities, in India. For Thermax, a company built on coal-fired boilers, this represented the ultimate transformation—betting on a technology that could make its legacy business obsolete.

But the Fortescue partnership, announced with fanfare, would become a cautionary tale. This deal is viewed positively for Thermax. It secures a new partner following the earlier tie-up with Fortescue Future Industries that fell through. The failure wasn't disclosed publicly, but industry insiders knew the truth: cultural misalignment, differing timelines, and disagreement over technology choices had doomed the collaboration.

Rather than retreat, Thermax doubled down. CEO Ashish Bhandari stated the company is prepared to invest hundreds of crores. He emphasized the role of green hydrogen in decarbonizing hard-to-abate industries like steel, petrochemicals, and fertilizers. The commitment wasn't just financial—it was existential. Thermax understood that green hydrogen wasn't competing with its existing business; it was the future of its existing customers.

The technology strategy reveals sophisticated thinking. Instead of betting on a single electrolyzer technology, Thermax pursued multiple partnerships. Strategic collaboration with Ceres Power Holdings for non-exclusive, global license agreement to manufacture, sell and service stack array modules based on Ceres' advanced solid oxide electrolysis (SOEC) technology. SOEC operates at high temperatures, making it ideal for industrial applications where waste heat is available—exactly Thermax's sweet spot.

The Ceres partnership was particularly strategic. "In India, significant strides are being made towards embracing renewable energy sources, particularly green hydrogen, as the country targets to produce 5 million metric tonnes of green hydrogen by 2030. We are excited to partner with Ceres to bring advanced solid oxide electrolysis (SOEC) technology to India. By leveraging our expertise in thermal management, we aim to offer a highly efficient and cost-effective hydrogen production solution that will accelerate the energy transition in India and globally."

But SOEC wasn't enough. Different applications require different technologies. Strategic partnership with HydrogenPro for alkaline electrolysers with exclusive rights in India for supply, installation, commissioning, and after-sales services. Alkaline electrolyzers are proven, reliable, and cost-effective for large-scale applications—perfect for India's ambitious green hydrogen targets.

The HydrogenPro deal showcased Thermax's evolved approach. Under the partnership, HydrogenPro will supply electrolysis stacks — the core modules that split water into hydrogen and oxygen. These will come with future upgrades and technical support. Thermax will have exclusive rights for the Indian market. It will manufacture key systems and balance-of-plant components for integration with these stacks. Moreover, a test station for short stacks will be set up at its Pune facility.

This wasn't just technology transfer—it was capability building. Through a detailed technology transfer, Thermax will engineer and manufacture critical system components and balance-of-plant elements, integrating them with HydrogenPro's stacks. Both companies will collaborate closely on the joint development of next-generation solutions to address evolving market demands.

The market opportunity justified the multi-technology approach. Furthermore, the recent approval of the National Green Hydrogen Mission by India's Union Cabinet, which aims to increase domestic production of green hydrogen to 5 MMT per annum by 2030 and reduce fossil fuel imports by over Rs. 1 lakh crore, is a significant boost. The Performance Linked Incentive (PLI scheme), under India's National Green Hydrogen Mission, could be leveraged for setting up any new manufacturing capacity.

The execution challenges are formidable. Green hydrogen currently costs $4-6 per kilogram to produce, while grey hydrogen from natural gas costs $1-2. For green hydrogen to be competitive, electrolyzer costs need to fall by 70%, renewable electricity prices need to stay below 2 cents per kWh, and capacity utilization needs to exceed 40%. These aren't incremental improvements—they require fundamental breakthroughs.

Thermax's approach to these challenges is pragmatic. FFI is on a mission to replace fossil fuels by producing green electrons from renewable energy and then converting these green electrons into green hydrogen. Rather than waiting for perfect economics, Thermax is creating demand through integrated solutions. A steel plant doesn't just need hydrogen—it needs heat recovery, water treatment, and process integration. Thermax can provide all of these, making the hydrogen economics part of a larger value proposition.

The financial commitment is substantial but measured. The company has already committed Rs 100 crore internally for this segment. It expects revenue contribution from FY27, supported by multiple bids for green hydrogen projects in the country. This isn't a moonshot—it's a calculated bet with defined milestones and fallback options.

The technical challenges extend beyond electrolyzers. Hydrogen is the smallest molecule in the universe, making it notoriously difficult to store and transport. It embrittles steel, leaks through microscopic gaps, and requires compression or liquefaction for practical use. Thermax's decades of experience with industrial gases, high-pressure systems, and materials science become crucial differentiators.

Phil Caldwell, CEO of Ceres, commented: "I am pleased to announce our SOEC systems partnership with Thermax, an engineering leader with expertise in heat integration and waste heat recovery processes and deep industrial customer relationships. This system licence agreement will take Ceres into the Indian market which is rapidly becoming one of the most dynamic and increasingly important markets for green hydrogen, green steel and green ammonia."

The partnership strategy reveals a deeper truth about technology transitions. Thermax isn't trying to become an electrolyzer technology leader—it's becoming a system integrator and solution provider. The value isn't in the electrolyzer stack but in making it work reliably in an Indian cement plant, with fluctuating power supply, extreme temperatures, and minimal maintenance capability.

Jarle Dragvik, CEO, HydrogenPro, highlighted, "India is one of the fastest-growing hydrogen markets, driven by robust renewable energy development. Partnering with Thermax provides us with a strong foothold in the country. Together, we aim to enable industry decarbonisation through green hydrogen, especially in sectors lacking renewable alternatives."

The green hydrogen bet isn't just about technology—it's about timing. India's renewable capacity is growing at 15-20% annually, creating periods of excess generation that need storage or alternative use. Industrial clusters are forming around renewable resources. Carbon pricing mechanisms are emerging. The pieces are falling into place for green hydrogen to move from pilot projects to commercial scale.

For Thermax, green hydrogen represents both the biggest risk and greatest opportunity in its history. Success would position it at the center of India's energy transition. Failure would mean significant write-offs and credibility loss. But as Ashish Bhandari notes, "Our association with HydrogenPro marks an important step in expanding our green hydrogen portfolio... This partnership reinforces our commitment to advancing industrial decarbonisation and supporting India's energy transition." The die is cast. Thermax is betting that the future of industrial energy is hydrogen-powered, and it intends to be the company that makes it happen in India.

VIII. Business Model & Competitive Position

Operating globally through 34 international and 22 domestic offices, 14 manufacturing facilities – 10 in India and 4 overseas, spanning Europe and South East Asia, Thermax has evolved from a local boiler manufacturer to a global engineering conglomerate. But understanding its true competitive position requires dissecting its carefully constructed business architecture.

The company operates through four reportable segments which are industrial products, industrial infra, green solutions, and chemicals. Each segment tells a different story about Thermax's evolution and competitive dynamics.

Industrial Products (40% of revenue): This is Thermax's cash cow, offering small capacity boilers & heating equipment, absorption chillers/heat pumps, air pollution control equipment/systems, water & waste recycle including associated services and EPC. The segment revenue grew by 55% between FY22 and FY24, supported by strong growth in the metal, cement and food & beverage sectors. What's remarkable is the margin profile—standardized products with recurring service revenue create an annuity-like business model.

Industrial Infra: The big-ticket EPC projects—power plants, large boilers, turnkey solutions. This is where Thermax competes with L&T, BHEL, and international players. It's capital-intensive, working capital-heavy, and cyclical. But it's also where relationships matter most. A cement plant CEO doesn't change vendors lightly when a shutdown costs millions per day.

Green Solutions: The future growth engine, encompassing renewable energy, waste-to-energy, and emerging technologies. Currently smaller in revenue but growing fastest, with order bookings increasingly skewed toward this segment. This is where Thermax's transformation narrative plays out—from selling boilers to selling decarbonization.

Chemicals: The hidden gem, contributing steady margins through specialty chemicals and ion exchange resins. With manufacturing facilities in Dahej and global customers, this segment provides geographic and sectoral diversification while leveraging Thermax's deep understanding of industrial processes.

The financial metrics reveal both strength and challenge. Revenue: 10,354 Cr, Profit: 669 Cr—respectable but not spectacular. The company has a low return on equity of 13.3% over last 3 years, reflecting the capital intensity of the business. Stock is trading at 7.96 times its book value, suggesting market optimism about future growth rather than current profitability.

The ownership structure is telling: Promoter Holding: 62.0%—Family control remains absolute. This creates both stability and questions about governance. The Aga-Pudumjee family's track record of professional management provides comfort, but concentrated ownership in a capital-intensive business limits financial flexibility.

The order book dynamics reveal the business model's evolution. Order balance for Q3FY25 was Rs 11,383 crore, up 6% from Q3FY24. But composition matters more than size. Green solutions and services are growing faster than traditional equipment, improving both margin profile and revenue predictability.

Competition varies dramatically by segment. In small boilers, Thermax faces local manufacturers competing on price. In large projects, it battles BHEL (government backing), L&T (execution capability), and MNCs like GE and Siemens (technology edge). In green solutions, new entrants backed by private equity are emerging monthly. In chemicals, global giants like Dow and BASF dominate.

Thermax's competitive advantages are subtle but significant:

Installed Base: Thousands of Thermax boilers across India create a service annuity and replacement cycle. A plant manager who's used Thermax equipment for decades won't switch for a 5% price difference.

Integration Capability: Unlike pure-play equipment vendors, Thermax can integrate heating, cooling, water treatment, and pollution control. For a pharmaceutical plant needing validated systems, one-stop shopping reduces complexity and risk.

Local Manufacturing with Global Technology: Through partnerships, Thermax accesses world-class technology while manufacturing locally. This combination—global quality at local prices with local service—is hard to replicate.

Ethics Premium: In industries where kickbacks are common, Thermax's no-corruption stance attracts MNCs and ESG-conscious customers willing to pay premiums for clean dealing.

Energy Transition Credibility: Having successfully pivoted from coal to biomass, Thermax has credibility in helping customers navigate energy transition—crucial when CEOs bet careers on net-zero commitments.

The vulnerabilities are equally important:

Technology Dependence: Most breakthrough technologies come through partnerships. If partners decide to go direct or find other Indian partners, Thermax's differentiation erodes.

Capital Constraints: With family ownership limiting equity dilution and debt capacity constrained by cyclical cash flows, Thermax can't match the investment firepower of global competitors or well-funded startups.

Talent Challenge: Competing for digital and cleantech talent against startups offering stock options and MNCs offering global careers is increasingly difficult.

Transition Risk: Currently, 70% of Thermax's order book is dedicated to green energy solutions, with the remaining 30% focused on fossil fuel projects. Managing this transition without alienating traditional customers or sacrificing near-term profitability requires delicate balance.

The international expansion shows both ambition and pragmatism. Rather than chasing prestige projects in developed markets, Thermax focuses on emerging markets with similar challenges—Africa, Southeast Asia, Middle East. Here, Indian engineering's value proposition—good enough quality at affordable prices—resonates.

The R&D focus is in line with the company's commitment to cut its carbon footprint by 50 per cent by 2030. But R&D spending as a percentage of revenue remains modest compared to global engineering companies. This reflects a conscious choice—fast follower rather than technology pioneer. The competitive landscape reveals fundamental truths about Thermax's position. BHEL major competitors are Suzlon Energy, Tube Investments, Thermax, 3M India, Honeywell Automation, AIA Engineering, Inox Wind. Market Cap of BHEL is ₹86,198 Crs. While the median market cap of its peers are ₹34,071 Crs. Despite BHEL's larger size, it seems to be less financially stable compared to its competitors. Altman Z score of BHEL is 2.35 and is ranked 8 out of its 8 competitors.

The comparison with L&T is more telling. "We maintain L&T as our top pick in the E&C (engineering and construction) space, due to comfortable leverage position, strong order book position (Rs 145,768 crore, up 27 per cent in Q3), superior return ratios and less dependence on capital markets for raising equity for funding projects. On the other hand, we continue to maintain our negative stance on BHEL, owing to structural issues like heightened competition, margin erosion and slowing of order inflows."

This positioning—smaller than giants like L&T and BHEL but more focused and financially disciplined—is actually Thermax's sweet spot. Thermax's top 9 competitors are BHEL, ABB, Honeywell, Fontus Water, Alstom, Hitech Systems, Thermodyne Engineering Systems, Kirloskar Proprietary and Siemens. Together they have raised over 9.1B between their estimated 639.6K employees. Thermax has 4,127 employees and is ranked 6th among it's top 10 competitors.

The employee productivity metrics are revealing. While competitors average 71,523 employees, Thermax operates with just over 4,000. This isn't understaffing—it's strategic focus. Thermax doesn't try to be everything to everyone. It picks battles where its integrated solutions approach and deep customer relationships create genuine differentiation.

BHEL is perceived as one of Thermax's biggest rivals. BHEL generates $1.9B more revenue than Thermax. But revenue isn't everything. BHEL's government ownership brings both advantages (preferential treatment in PSU orders) and disadvantages (bureaucratic decision-making, political interference). Thermax's private ownership allows faster decision-making and strategic pivots—crucial in rapidly evolving energy markets.

The international competitor comparison is equally instructive. ABB competes in the Industrial Machinery & Equipment field. Compared to Thermax, ABB has 105,843 more employees. But ABB's global scale comes with global costs. In India's price-sensitive market, Thermax's local manufacturing and lower overhead structure allow it to compete effectively on total cost of ownership.

The customer perception metrics provide another angle. 8 Employees rate Thermax's Overall Culture a 70/100, which ranks it 2nd against its competitors, below L&T Co. 7 Employees rate Thermax's Employee Net Promoter Score a -15, which ranks it 2nd against its competitors, below L&T Co. While concerning, these metrics reflect the challenges of transformation—moving from equipment supplier to solution provider requires cultural changes that create internal friction.

The sectoral positioning is crucial. Unlike diversified conglomerates like L&T (which spans infrastructure, defense, technology), Thermax maintains laser focus on energy and environment. This specialization creates deeper expertise but also concentration risk. When industrial capex slows, Thermax has fewer buffers than diversified competitors.

The technology partnership strategy differentiates Thermax from both ends of the competitive spectrum. Unlike BHEL, which tries to develop everything in-house, or pure traders who simply import, Thermax selectively partners for critical technologies while maintaining manufacturing and integration capabilities. This allows faster technology adoption without massive R&D investments.

The green transition creates both opportunity and threat. New entrants backed by climate-focused private equity are emerging monthly, unencumbered by legacy businesses or manufacturing assets. But Thermax's installed base and customer relationships provide a moat—industrial customers won't trust their critical processes to startups, regardless of technology superiority.

The financial services comparison is telling. While L&T has evolved into a financial services conglomerate with significant NBFC operations, Thermax remains purely industrial. This focus prevents dilution but also limits capital recycling opportunities that boost ROE for diversified competitors.

Looking ahead, the competitive dynamics are shifting. The traditional boundaries between power generation, industrial equipment, and environmental solutions are blurring. Data and software are becoming as important as hardware. Chinese competitors are moving upmarket. Global players are localizing. In this fluid environment, Thermax's ability to remain relevant depends not on competing head-to-head with larger players but on finding niches where its unique combination of local presence, global technology access, and deep customer relationships create sustainable advantage.

The ultimate competitive truth is this: Thermax isn't trying to be the biggest or the most technologically advanced. It's trying to be the most trusted partner for Indian industry's energy transition. In a market where relationships still matter, where service quality trumps product specifications, and where local presence beats global brand, that's a defensible position. Whether it's defensible enough against the coming wave of disruption—from Chinese scale, startup innovation, and technology convergence—remains the multi-billion rupee question.

IX. Playbook: Business & Leadership Lessons

The Thermax story offers a masterclass in managing paradoxes. How do you professionalize a family business without losing its soul? How do you maintain ethical standards in a corrupt industry without becoming uncompetitive? How do you transition from fossil fuels to green energy without abandoning loyal customers? The answers lie not in choosing sides but in synthesizing opposites.

The Aga Model of Family Business Professionalization

The transformation under Anu Aga has become a Harvard case study, but its lessons are often misunderstood. The key wasn't removing family from the business—it was redefining family involvement. Family members moved from executive to governance roles. They remained committed shareholders but hired professional managers for operations. This wasn't abdication—it was evolution.

The model works because it addresses the fundamental tension in family businesses: emotional attachment versus rational decision-making. By separating ownership from management, the Aga family could maintain long-term commitment while enabling professional excellence. When Meher eventually became chairperson, she had proven herself through performance, not inheritance.

Crisis as Catalyst

Every major transformation at Thermax followed a crisis. The 1996 economic downturn and Rohinton's death catalyzed professionalization. The 2008 financial crisis enabled international expansion through acquisitions. The climate crisis is driving the green hydrogen pivot. This pattern isn't coincidental—it reflects a deeper truth about organizational change.

Crisis creates permission for radical action. When Anu fired family members and hired BCG, she could point to existential threat. When Meher acquired European companies during the recession, she could cite once-in-a-lifetime valuations. Crisis silences critics, unifies stakeholders, and accelerates decision-making. The lesson isn't to wait for crisis but to recognize and even manufacture the burning platform for change.

Ethics as Competitive Advantage

In the first few years of her leadership, Aga took the decision to remove family members from executive positions and instead place them on the Thermax board. But the more radical decision was the no-corruption policy. In an industry where "facilitation fees" are standard, this seemed like competitive suicide.

Yet it became a moat. MNCs preferred dealing with Thermax because it eliminated corruption risk. Talented professionals joined because they could work without compromising integrity. Banks offered better terms because governance standards reduced risk. The lesson: in markets where everyone compromises, refusing to compromise becomes differentiation.

But this only works with genuine commitment. Token ethics policies while tolerating backdoor dealings destroy credibility. Thermax lost orders, fired salespeople, and walked away from markets to maintain standards. This visible sacrifice created internal and external credibility that no PR campaign could achieve.

Long-term Thinking in Cyclical Industries

Industrial equipment is inherently cyclical. When the economy booms, everyone orders capacity. When it busts, orders disappear. Most companies respond by hiring in booms and firing in busts, expanding aggressively then retrenching desperately. Thermax chose a different path.

During downturns, Thermax invests—in R&D, acquisitions, capability building. During upturns, it focuses on execution and margin improvement rather than aggressive expansion. This counter-cyclical approach requires financial discipline (maintaining cash reserves during good times) and emotional discipline (resisting euphoria and despair).

The payoff comes through cycles. While competitors exhaust themselves with violent swings, Thermax steadily gains share. Customers value stability—knowing Thermax will honor warranties, supply spares, and provide service regardless of market conditions. Employees value predictability—knowing their jobs aren't hostage to quarterly results.

Technology Partnerships versus In-house Development

Thermax's approach to technology is pragmatic rather than prideful. Unlike BHEL's insistence on indigenous development or startups' obsession with proprietary technology, Thermax freely partners, licenses, and adapts. This seems like weakness—admitting you can't develop everything yourself.

But it's actually strength. Technology partnership allows Thermax to offer cutting-edge solutions without massive R&D investment. It can pivot quickly—from Fortescue to HydrogenPro in green hydrogen when the first partnership failed. It can serve customers immediately rather than waiting years for in-house development.

The key is maintaining integration capability. Thermax doesn't just resell partner technology—it adapts, integrates, and enhances it for Indian conditions. This creates value for both partners (market access) and customers (localized solutions). It's not about owning all technology but owning the customer relationship and solution delivery.

Managing Energy Transition

Currently, 70% of Thermax's order book is dedicated to green energy solutions, with the remaining 30% focused on fossil fuel projects. This ratio encapsulates the transition challenge. Abandon fossil fuels too quickly, and you lose revenue and relationships. Transition too slowly, and you become obsolete.

Thermax's approach is customer-centric rather than technology-centric. Instead of preaching about green energy, it helps customers reduce costs and meet regulations. A biomass boiler is positioned as fuel flexibility, not environmental virtue. Green hydrogen is about energy security, not just emissions. This pragmatic framing makes transition a business decision rather than moral choice.

The lesson extends beyond energy. Any industry facing disruption—retail to e-commerce, automotive to electric, banking to digital—faces similar challenges. The key is making the new technology serve existing customer needs rather than forcing customers to adopt new paradigms.

Values-Based Sustainability

"Profit is not only a set of figures, but of values," Rohinton often reminded his teams. This philosophy, easy to state but hard to implement, became Thermax's true differentiator. It means walking away from profitable but unsustainable businesses. It means investing in employee development even when poaching is easier. It means honoring commitments even when contracts allow escape.

This isn't altruism—it's strategy. In industries with long asset lives and relationship-based selling, reputation compounds over decades. Every ethical choice builds trust equity that eventually converts to commercial value. Every compromise erodes it. The challenge is maintaining this discipline when competitors take shortcuts and markets reward quarterly performance.

The Role of Professional Management

The appointment of Ashish Bhandari as CEO in 2020—the first non-family CEO—represents the culmination of professionalization. But this wasn't abandonment by the family. Meher remains chairperson, family remains majority shareholder, and values remain non-negotiable. Professional management operates within family-defined boundaries.

This hybrid model—family values with professional execution—combines the best of both worlds. Family ownership provides patient capital and long-term thinking. Professional management brings expertise and objectivity. The tension between them creates healthy debate rather than destructive conflict.

Digital Transformation in Industrial Companies

Thermax's IIoT platform Edge Live seems incongruous for a boiler company. But it represents a fundamental insight: in mature industries, competitive advantage increasingly comes from software and services rather than hardware. A boiler is a commodity; predictive maintenance is differentiation.

The lesson for industrial companies is that digital transformation isn't about replacing physical products with digital ones. It's about wrapping physical products with digital services. It's about using data to predict failures, optimize operations, and demonstrate value. It's about moving from selling products to selling outcomes.

Building Resilience Through Diversification

Thermax's four-segment structure—industrial products, industrial infra, green solutions, chemicals—provides resilience through diversification. When one segment struggles, others compensate. But this isn't random diversification. Each segment leverages common capabilities: thermal engineering, industrial customer relationships, project management.

The lesson is that diversification should build on core strengths rather than abandon them. Thermax's move into chemicals leveraged its understanding of industrial processes. Its green solutions build on existing customer relationships. This related diversification provides resilience without losing focus.

The Thermax playbook ultimately isn't about specific strategies but about managing contradictions. Family ownership with professional management. Global technology with local manufacturing. Legacy business with future technologies. Ethics with competitiveness. The ability to hold these tensions without resolving them—to live in the paradox rather than choosing sides—may be the most important lesson of all.

X. Analysis & Investment Case

The numbers tell a story of competent execution but not explosive growth. Revenue: 10,354 Cr, Profit: 669 Cr represents a profit margin of 6.5%—respectable for engineering companies but not exceptional. Company has a low return on equity of 13.3% over last 3 years, reflecting the capital intensity of the business and conservative financial management.

The valuation puzzle is more intriguing. Stock is trading at 7.96 times its book value, a premium typically reserved for high-growth technology companies, not industrial conglomerates. This disconnect between current performance and market valuation suggests investors are betting on transformation, not continuation.

The Bull Case: Riding the Energy Transition Wave

India's energy transition represents a multi-trillion-dollar opportunity. India targets to produce 5 million metric tonnes of green hydrogen by 2030. Solar capacity additions of 15-20 GW annually. Industrial decarbonization mandates tightening yearly. In this context, Thermax's positioning as a "trusted partner in energy transition" isn't marketing—it's strategic positioning for a generational shift.

The order book composition supports this thesis. 70% green solutions speaks to market demand, not company push. Customers are voting with purchase orders for Thermax's transformation. The recent partnerships—Ceres for SOEC, HydrogenPro for alkaline electrolyzers—provide technology access without massive capital commitment.

The competitive moat remains intact despite industry evolution. Thousands of installed systems create replacement and service annuities. Deep customer relationships built over decades don't transfer easily to new entrants. The ability to integrate multiple solutions—heating, cooling, water treatment, pollution control—becomes more valuable as environmental regulations complex.

The financial position enables strategic flexibility. Limited debt, family commitment to long-term ownership, and steady cash generation from legacy businesses fund transformation without dilution or financial stress. This patient capital is crucial for technologies like green hydrogen that require years to commercialize.

The Bear Case: Execution Risks in Unproven Markets

The green hydrogen reality check is sobering. "Last year, Thermax lost a fair bit of money in stabilizing these bio-CNG plants," admits leadership. If bio-CNG—a relatively simple technology—causes losses, what happens with complex electrolyzer systems? The Fortescue partnership failure, though unpublicized, suggests execution challenges in new domains.

Capital intensity remains problematic. Major green energy projects require enormous upfront investment with long payback periods. Thermax's balance sheet, while solid, can't match the firepower of global giants or sovereign-backed Chinese competitors. In auctions where lowest cost wins, financial muscle matters more than technical competence.

Competition from Chinese players intensifies yearly. Chinese manufacturers offer electrolyzers at 50% of Western prices. In solar, Chinese dominance is complete. In wind, it's growing. Thermax's strategy of partnering with Western technology providers might position it perfectly wrong—high cost without technology ownership.

The technology risk looms large. Thermax doesn't own core technology in any emerging segment. If Ceres finds a better Indian partner or goes direct, Thermax loses SOEC capability overnight. If HydrogenPro's technology becomes obsolete, Thermax's electrolyzer business evaporates. Building businesses on licensed technology creates perpetual vulnerability.

Management bandwidth constraints are visible. The same leadership team managing legacy businesses is driving transformation. Unlike startups with singular focus or conglomerates with infinite resources, Thermax must transform while performing. This juggling act inevitably compromises both.

The India Energy Transition Opportunity

India's energy paradox creates unique opportunities. Energy demand growing at 6-7% annually requires all sources—renewable and fossil. Industrial customers need reliable baseload power, not intermittent renewables. Environmental regulations tighten while affordability remains paramount. This complexity favors integrators over specialists.

Thermax's hybrid solutions—biomass co-firing in coal plants, waste heat recovery, industrial solar—address this paradox. They're not pure green but greener. They're not cheapest but affordable. They're not revolutionary but implementable. In India's pragmatic energy transition, "good enough" beats perfect.

The government's production-linked incentives (PLI) for green hydrogen manufacturing could be transformative. If Thermax establishes electrolyzer manufacturing with government support, it could achieve cost competitiveness with Chinese players while maintaining technology access through partnerships.

The industrial customer base provides natural early adopters. Refineries need hydrogen for desulfurization. Steel plants seek alternatives to coking coal. Fertilizer companies require ammonia feedstock. These customers already trust Thermax for critical equipment—extending to hydrogen is evolutionary, not revolutionary.

Valuation Considerations

At current valuations, the market prices in successful transformation. The P/B ratio of 7.96 implies either significant hidden assets or enormous future value creation. Neither is obvious. The physical assets are fairly valued. The future value depends on successful execution of unproven strategies.

Peer comparison provides context. BHEL trades at distressed valuations despite larger size and government backing. L&T commands premium valuations but offers diversification Thermax lacks. Global peers like Siemens trade at higher multiples but with stronger technology portfolios.

The key question: Is Thermax a value trap or transformation story? The answer depends on time horizon. Near-term, traditional businesses face headwinds—industrial capex remains weak, competition intensifies, margins compress. Long-term, energy transition creates enormous opportunities—if Thermax can capture them.

Risk-Reward Framework

The asymmetry isn't clearly favorable. Downside risks—technology obsolescence, execution failures, competition—could destroy 50% of value. Upside potential—becoming India's energy transition champion—might create 2-3x returns. But probability-weighted, the expected value is modest.

For fundamental investors, Thermax presents a fascinating study in transformation. It's not a simple bet on green energy—dozens of pure-plays offer that. It's a bet on incumbent adaptation, on the ability of a 58-year-old boiler company to reinvent itself for the hydrogen economy.

The investment case ultimately depends on belief—not in technology or markets, but in management's ability to navigate unprecedented change. The Aga family's track record of successful transformation provides comfort. But past performance, as every disclaimer notes, doesn't guarantee future results.

For long-term investors seeking exposure to India's energy transition, Thermax offers a differentiated proposition—not the highest growth or newest technology, but possibly the safest path through an uncertain transition. Whether safety is sufficient in a revolution remains to be seen.

XI. Epilogue & Future Outlook

India's net-zero commitment by 2070 seems distant, but for industrial companies, 2070 is just two equipment replacement cycles away. A cement plant commissioning a coal-fired kiln today will operate it until 2050. This temporal mismatch—long-lived assets in a rapidly changing policy environment—creates both opportunity and existential risk for companies like Thermax.

The industrial decarbonization challenge is more complex than often acknowledged. Unlike power generation, where solar and wind provide clear alternatives, industrial heat has no simple substitute. You can't make steel with solar panels or cement with wind turbines. High-temperature processes require energy density that only combustion or electricity can provide. This is where Thermax's expertise becomes crucial—not in eliminating fossil fuels but in transitioning to cleaner alternatives.

Thermax's positioning for the next decade reflects this nuanced understanding. Rather than abandoning its core competence in thermal engineering, it's applying it to new fuels and processes. A biomass boiler uses the same thermodynamic principles as a coal boiler. A hydrogen combustion system leverages decades of burner design experience. The expertise transfers even as the fuel transforms.

What would success look like in 2035? Thermax would be India's leading provider of industrial decarbonization solutions, with green hydrogen systems generating 30% of revenue. The installed base would include hundreds of waste-to-energy plants, thousands of biomass boilers, and dozens of green hydrogen facilities. International operations would contribute 40% of revenue, primarily from emerging markets facing similar energy transitions.

But success isn't guaranteed. Multiple scenarios could unfold:

The Acceleration Scenario: Climate events accelerate policy action. Carbon pricing makes green solutions economically superior. Technology costs plummet faster than expected. In this world, Thermax's early positioning pays off handsomely. The order book explodes, margins expand as scale economics kick in, and the company becomes a global champion in industrial decarbonization.

The Gradual Transition Scenario: Change happens, but slowly. Fossil fuels remain dominant through 2040. Green technologies improve incrementally. Policy support remains inconsistent. Here, Thermax muddles through—growing steadily but not spectacularly, managing the decline of legacy businesses while nurturing emerging ones. Returns are adequate but not exceptional.

The Disruption Scenario: Breakthrough technologies obsolete current approaches. Direct air capture eliminates the need for emission reduction. Fusion power makes all current energy technologies redundant. Chinese manufacturers achieve insurmountable cost advantages. In this world, Thermax's carefully built capabilities become stranded assets.

The key risks are both obvious and subtle:

Technology Risk: Every major growth initiative depends on unproven technology. Green hydrogen has never been deployed at scale. Waste-to-energy faces feedstock and efficiency challenges. If technologies fail to mature as expected, growth evaporates.

Execution Risk: Thermax is attempting simultaneous transformation across multiple dimensions—technology, business model, geography. The complexity multiplies failure points. One major project failure could damage credibility irreparably.

Financial Risk: Energy transition requires massive capital investment with uncertain returns. If Thermax overcommits to capital-intensive projects that underperform, financial stress could force distressed asset sales or dilutive capital raising.

Competitive Risk: Global giants are investing billions in energy transition. Startups are innovating rapidly. Chinese manufacturers are scaling aggressively. Thermax's middle position—neither the most innovative nor the lowest cost—could become untenable.

Yet opportunities abound:

The India Advantage: India's energy demand growth creates room for all technologies. Unlike developed markets where renewables replace fossil fuels, India needs both. This "all of the above" approach favors integrators like Thermax.

The Incumbent Advantage: Industrial customers are conservative. They won't bet critical processes on unproven suppliers. Thermax's 58-year track record provides trust that no startup can match.

The Partnership Ecosystem: By building relationships with multiple technology providers, Thermax can offer whatever solution proves optimal. This flexibility is valuable in uncertain technology evolution.

The Service Opportunity: As systems become more complex, service becomes more valuable. Thermax's installed base and service network create recurring revenue streams that pure equipment suppliers lack.

Looking ahead, several factors will determine Thermax's trajectory:

Policy Evolution: Will India implement carbon pricing? Will green hydrogen subsidies materialize? Will environmental regulations tighten? Policy determines market demand more than technology capability.

Technology Maturation: Will electrolyzer costs fall 70% as predicted? Will carbon capture become economical? Will novel technologies emerge? Technology evolution determines competitive dynamics.

Capital Availability: Will climate finance flow to India? Will capital markets fund long-gestation projects? Will family shareholders support aggressive investment? Capital access determines growth potential.

Management Execution: Can Thermax maintain focus while diversifying? Can it attract talent for new technologies? Can it maintain culture through transformation? Execution determines whether potential becomes reality.

The final reflection brings us full circle to A.S. Bhathena's philosophy: "Deserve and then desire." Thermax has built deserving capabilities—technical competence, customer relationships, ethical standards, financial strength. Whether these translate to desired outcomes—market leadership, sustainable growth, successful transformation—depends on forces beyond complete control.

What's certain is that Thermax's journey from a small boiler manufacturer to energy transition partner represents more than corporate evolution. It embodies India's broader transformation from post-colonial manufacturer to global technology participant. It demonstrates that family businesses can professionalize without losing soul, that ethical standards can be competitive advantage, that incumbents can adapt to disruption.

The next decade will determine whether Thermax becomes a case study in successful transformation or a cautionary tale of incumbent inertia. The pieces are in place—technology partnerships, market position, financial resources, leadership commitment. But in the energy transition, as in all revolutions, victory belongs not to the strongest or smartest, but to the most adaptable.