The Leela: The Palace Pivot and the Private Equity Reset

I. Introduction: The Definition of Indian Luxury

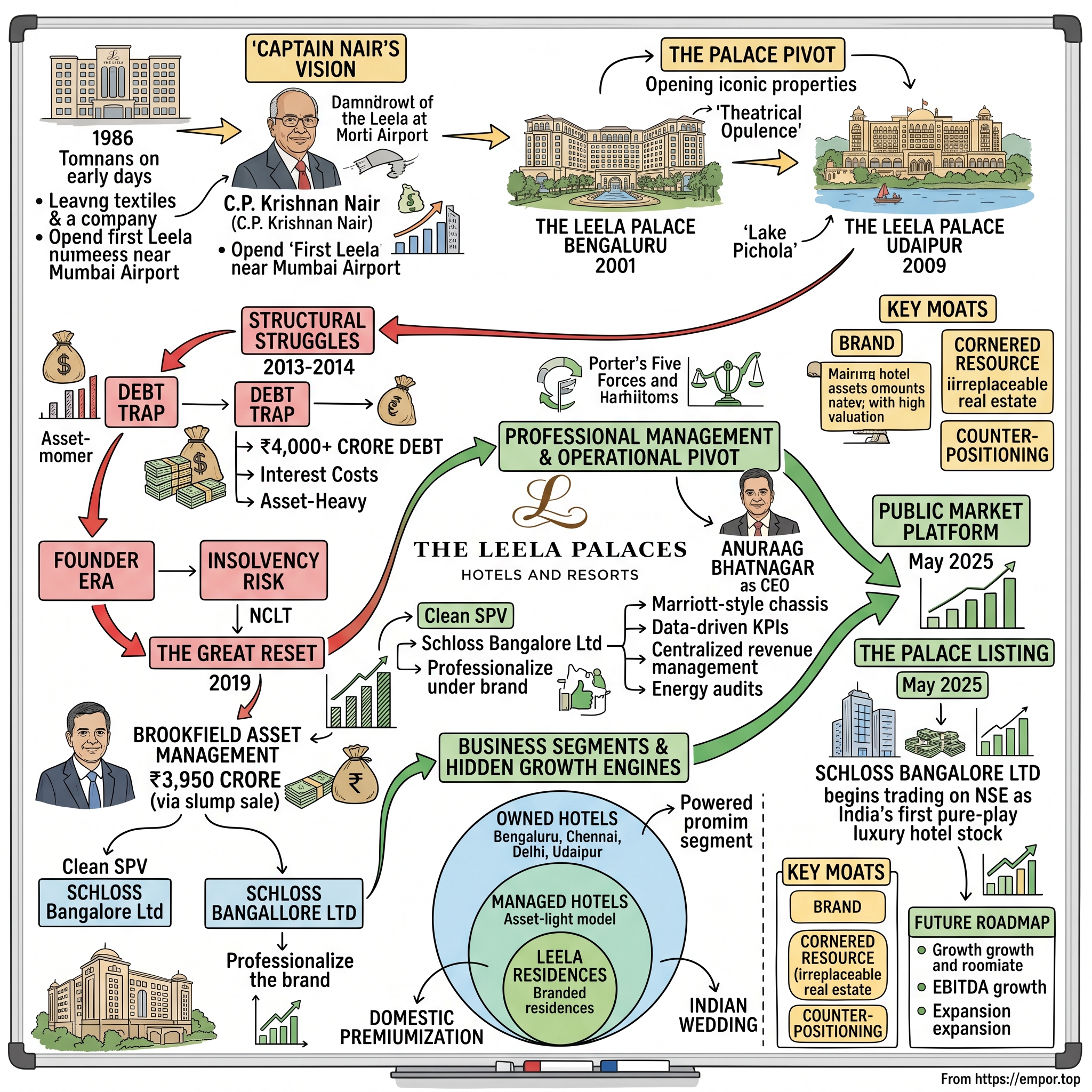

It was an October evening in 2018 inside the marble corridors of the National Company Law Tribunal in Mumbai. JPMorgan-led creditors, ITC, lenders, the Nair family, and a phalanx of insolvency lawyers were arguing over the carcass of लीला Leela — once the most opulent hospitality brand India had ever produced. The company that owned the chandelier-festooned Leela Palace Bengaluru, the lake-fronting Leela Goa, and the gilded Leela New Delhi was, by every standard accounting metric, insolvent. Debt had ballooned past ₹4,000 crore. The founder, then in his nineties, watched from a distance as the empire he had begun building at age 65 — an empire he had explicitly designed to outlast him — was being unbundled in real time.

Six years later, on a humid May morning in 2025, the bell rang at the National Stock Exchange in Mumbai. Schloss Bangalore Limited — German for "castle," now the holding entity of The Leela Palaces, Hotels and Resorts — began trading as the first true pure-play luxury hotel stock on Indian markets.[^1] The same brand that almost died in administration was suddenly being valued by public investors at a figure that, when the dust settled, exceeded what the family had borrowed to build it in the first place.

How does a company go from the brink of liquidation to one of the most anticipated hospitality listings in Indian history in under seven years? That is the story.

The Leela aesthetic occupies a very specific psychological niche in the Indian luxury hierarchy. ताज Taj, run by Indian Hotels Company (IHCL), sells heritage — you stay at the Taj Mahal Palace in Mumbai partly because the building itself is a national landmark that survived the 2008 attacks. ओबेरॉय Oberoi, operated by EIH Ltd., sells clinical perfection — a kind of restrained, white-glove minimalism beloved by corporate road warriors and discerning Asian tourists. The Leela carved out a third lane: theatrical, almost cinematic opulence — what an Indian wedding planner once described as "the maximalist palace of your imagination, except real."

This episode is the story of how that aesthetic was built by a textile entrepreneur in his sixties; how a family-led, asset-heavy, debt-funded expansion collapsed; how ब्रुकफील्ड Brookfield Asset Management paid ₹3,950 crore to professionalize one of India's most emotionally resonant brands;[^2] and how that pivot ended in a public listing that re-rated the entire Indian hospitality category.

It is, in other words, the perfect Acquired case study: founder myth, financial hubris, distressed-asset acquisition, and operational reset — all wrapped in marble, gold leaf, and rose petals.

II. The Legacy Context: Capt. Nair and the Vision

The man who would build the Leela was, until age 65, in the textile business. चित्तपुरम पलानी कृष्णन नायर C.P. Krishnan Nair — Captain Nair to everyone — was born in 1922 in the small town of Kannur in northern Kerala. He served in the British Indian Army during the Second World War, which is where the "Captain" came from and which he would invoke for the rest of his life. After independence, he built a textile-export business called Leela Lace, named after his wife, Leela Nair. By the 1980s, Leela Lace was a sturdy, mid-sized exporter — successful but unremarkable.

What was remarkable was what Captain Nair did next. In 1986 — at an age when most Indian businessmen of his generation were handing over to sons and retiring to genteel obscurity — he opened the first Leela hotel in Mumbai. It was a Kempinski affiliation property near the international airport, designed to capture the cargo executives, airline crews, and visiting industrialists who had nowhere palatial to sleep on the Mumbai airport approach.1 The location was, by conventional hotelier standards, terrible — too far from the business district, surrounded by warehouses. The location was also, in retrospect, genius: by the late 1990s, every Mumbai-bound multinational executive who valued a short cab ride to the terminal was sleeping at the Leela.

The "Palace" pivot came later — and this is the strategic move that defined the brand. Through the late 1990s and 2000s, Indian luxury hospitality was dominated by ताज Taj's heritage properties (genuine 19th-century palaces purchased or leased from royal families) and Oberoi's tasteful, internationally calibrated 5-stars. Captain Nair made a contrarian bet: he would build new "palaces" from scratch, in cities that had no maharaja heritage to draw on.

The Leela Palace Bengaluru opened in 2001 — built on land that had been the site of a defunct textile mill, designed in a Vijayanagar architectural pastiche complete with hand-carved teak and a sweeping lily pond.1 When it opened, Bengaluru's tech boom was just turning into a flood. Every IBM, Cisco, and Goldman Sachs executive arriving to oversee a new India operation needed somewhere to stay that signalled importance. The Leela Palace, with its peacock-themed lobby and turbaned doormen, signalled importance.

This was followed by The Leela Palace Udaipur (2009), set on the shore of पिछोला Lake Pichola with views of the City Palace and the famous ताज Taj Lake Palace floating across the water; The Leela Palace Chennai (2013), built on a stretch of Bay of Bengal coastline; and The Leela Palace New Delhi (2011), a 254-room marble fantasia in the diplomatic enclave of Chanakyapuri.[^1]

Each property was a statement. Each property also cost a fortune.

And here we arrive at the strategic mistake that, fairly or not, defines the founder-era of the Leela. While Captain Nair was building palaces, the global luxury hospitality industry had already pivoted. Marriott, Hilton, Four Seasons, Hyatt — these companies had become brand-and-management businesses. They licensed their flags to wealthy local owners who bore the real-estate risk. The hotel chain itself kept management fees and royalties, with virtually zero capital tied up in land or buildings. Asset-light, capital-efficient, infinitely scalable.

The Leela went the other way. The company owned the land, owned the building, owned the operating company. Worse, much of the expansion was funded with rupee-denominated bank debt at Indian interest rates, which during the 2008-2014 cycle ran in double digits. The Leela New Delhi alone reportedly cost over ₹1,400 crore to build — a per-key construction cost that, even by Manhattan standards, would have been aggressive.[^5]

By 2013, the math was inescapable. Interest costs were consuming most of operating profit. The expansion that had built Captain Nair's monument was also building a debt trap. When he passed away in 2014, his sons inherited not just one of India's most coveted hospitality brands but also one of its most indebted ones. The two were the same balance sheet.

III. The Great Reset: The 2019 Brookfield Acquisition

By 2017, Hotel Leelaventure — the listed parent — was running out of options. The promoter family had already pledged most of their shares to lenders. The company was attempting to sell the Leela Goa property to JM Financial. Lenders led by JPMorgan Chase had taken control of a significant chunk of equity through debt-to-equity conversions. And the looming presence of the दिवालियापन और दिवालिया संहिता Insolvency and Bankruptcy Code of 2016 — India's new, faster, and more creditor-friendly bankruptcy regime — meant that anyone holding Leela debt could now force a resolution.[^5]

ITC, the cigarettes-to-hotels conglomerate, made an opening move with a public letter to SEBI objecting to the proposed asset sale. ITC had ambitions to upgrade its own luxury portfolio and saw Leela as a strategic prize. The Nair family resisted. Lenders dithered. The asset went on the block.

The winning bid came from somewhere most Indian observers did not expect: ब्रुकफील्ड Brookfield Asset Management, the Toronto-headquartered alternative asset manager that managed over half a trillion dollars globally but had until then been known in India mainly for office parks and infrastructure assets, not luxury hotels. On March 18, 2019, Brookfield announced a binding agreement to acquire four owned hotels — Bengaluru, Chennai, Delhi, Udaipur — plus a development project in Agra, the Leela brand itself, and the management contracts for properties not directly owned. Headline price: ₹3,950 crore, roughly $570 million at the time.[^2]

The structure mattered. This was not a stock acquisition of Hotel Leelaventure. It was a slump sale of identified assets into a new Brookfield-controlled special-purpose vehicle, eventually housed under Schloss Bangalore Limited. The residual public-listed shell — renamed HLV Ltd — was left holding the Leela Mumbai property and the legacy debt overhang. Brookfield had performed a kind of surgical extraction: the brand, the trophy assets, the operating system — all moved into a clean entity, free of the family's other liabilities.[^2]

Did Brookfield overpay? At the time, the consensus was mixed. ₹3,950 crore for roughly 1,200 owned keys worked out to around ₹3.3 crore per key — high by any objective per-key metric, particularly given that the Indian hospitality sector was emerging from a multi-year RevPAR (revenue per available room) trough. IHCL and EIH were trading at meaningful multiples of book and benefiting from a recovering domestic travel cycle. But neither would have paid what Brookfield paid, because neither needed what Brookfield needed: a single, instantly credible, top-of-stack luxury brand with no integration baggage.

The "sum of parts" valuation told a different story. The Leela New Delhi alone, on its 7-acre Chanakyapuri parcel, was arguably worth a meaningful chunk of the headline price just for the land. The Leela Bengaluru sat on prime CBD-adjacent real estate in one of India's tightest hotel-supply markets. Udaipur was, in a hospitality sense, irreplaceable — there is exactly one Lake Pichola, and the land plots on it are not being made anymore. Strip out the real-estate value of the four trophy assets and the residual implied price for the brand and management business was, on some analyst spreadsheets, close to zero.

This is the Brookfield playbook in miniature. The firm operates a large global real estate fund family and a separate infrastructure platform. It buys irreplaceable assets, often during periods of seller distress, with very long-duration capital that does not need to flip in three years. The Leela fit the template precisely: an asset-heavy, brand-led platform whose underlying real estate could not be replicated, owned by a family that had run out of balance-sheet runway.

The clean-break dimension was equally important. By acquiring assets — not equity — Brookfield insulated the new entity from any contingent liabilities, tax disputes, or shareholder litigation tied to the founder family's other holdings. The brand walked across the table without its baggage. That single piece of structuring is, in retrospect, what made the IPO six years later possible.

IV. Modern Management: The Professional Pivot

Walking into the executive offices of The Leela in suburban Mumbai in 2020, a visitor would have noticed two things immediately. First, the Brookfield branding was conspicuously absent — the new owners had decided, correctly, that the equity here was in the Leela name, not in the parent's. Second, the people in the room were not from the old Leela.

The CEO seat went to अनुराग भटनागर Anuraag Bhatnagar, a hospitality executive who had spent two decades inside Marriott's Indian operations, including running the Marriott India and Maldives portfolio.[^6] Bhatnagar's background mattered for one specific reason: Marriott, more than any other global chain, had built India's most sophisticated revenue-management and franchise-operations playbook. Bringing that operating culture into a brand that had historically been run on owner instinct was the entire pivot.

The change in operating philosophy was profound and, in places, ruthless. Under the founders, the Leela had been run with a certain warmth — a family business at scale, where senior managers were on first-name terms with the Nairs and where decisions, including capital decisions, often hinged on what the family thought "the brand stood for." Under Brookfield, the same property network was put on what one industry executive described as "a Marriott-style operating chassis." Revenue management was centralized. Procurement was consolidated. Energy and utility costs — historically a quiet drain on Indian luxury hotel margins — were audited line by line. Property-level GMs got new KPIs that mapped to EBITDA-per-room and guest experience scores rather than headline occupancy.

The governance change was equally consequential. Brookfield held more than 90 percent of the equity in Schloss Bangalore at the point of the IPO filing.[^1] In a market historically dominated by promoter-family-controlled hotel companies (the Tatas at IHCL, the Oberois at EIH, the ITC management at ITC Hotels), this was the first major Indian luxury hospitality platform run by a global institutional sponsor on a clean-cap-table basis. The board was rebuilt with independent directors drawn from hospitality, real estate, and consumer-brand backgrounds. Management incentives were tied explicitly to operating metrics rather than to family preference.

There is a subtle but important point here for investors. Family-run hospitality businesses in India have historically traded at a discount to their underlying asset value because the market — fairly or not — prices in the agency cost of family decisions. Capex on a pet project, a hire driven by relationship rather than competence, a strategic pivot dictated by a generational succession — these are real risks in a long-duration capital-intensive business. By removing the family layer entirely, Brookfield created the first Indian luxury hospitality vehicle where the principal-agent problem was, by design, a Western-style sponsor-management one rather than a founder-dynasty one.

The cultural transition was not painless. Several long-serving Leela executives departed in the eighteen months following the acquisition. Some properties experienced service-level dips during the transition, particularly during the COVID-19 disruption that hit the Indian hospitality industry in 2020-21. But the operating chassis built during those years became the foundation for the post-pandemic recovery. When luxury demand snapped back in 2022 and 2023 — particularly the Indian weddings and inbound diaspora traffic that the Leela's properties were designed for — the new system captured the upside in margin, not just in revenue.

This is what a professional reset actually looks like: not glamorous, mostly invisible from the lobby, but compounding quietly inside the P&L for years.

V. Business Segments and the Hidden Growth Engines

To understand what Schloss Bangalore actually owns today, picture the brand portfolio as three concentric circles.

The innermost circle is the owned portfolio: the Leela Palace properties in Bengaluru, New Delhi, Chennai, Udaipur, plus the Leela Goa and Leela Mumbai (re-acquired or re-incorporated into the brand network through different structures). These are the trophy assets. They are also the assets that consume the most capital and generate the highest absolute profit dollars per property. According to the company's draft red herring prospectus, the four core Palace properties contributed the overwhelming majority of operating EBITDA in the financial year preceding the IPO filing.[^1] This is the brand's heart and, in a candid moment, its concentration risk.

The middle circle is the managed portfolio — properties that fly the Leela flag but are owned by third-party real estate sponsors. This is where the asset-light pivot lives. The economics here are structurally different: Schloss collects a base management fee (typically a percentage of revenue) plus an incentive fee linked to GOP (gross operating profit) margins. Capital tied up: essentially zero. Margin profile: very high. Growth rate: in theory, limited only by the supply of credible owner-partners willing to invest in luxury hotel construction in Indian Tier 1 and Tier 2 markets.

The outermost circle — and the most interesting hidden business — is लीला रेजिडेंसेज Leela Residences. This is the branded-residence model that Marriott, Four Seasons, and Aman have used globally to monetize the brand without the capital intensity of owning hotels. The structure is elegant: a real-estate developer builds a luxury condominium tower; the units are sold to wealthy buyers at a meaningful premium because they bear the Leela name and are serviced by Leela hospitality staff. The Leela collects a licensing fee on the sales plus an ongoing service fee on the residences in perpetuity. The first major deployment of this model was at Bhartiya City in Bengaluru, with further pipeline announced in the IPO prospectus.[^1]

For investors, the residences segment is the most underappreciated value driver in the platform. It monetizes the single most valuable thing the Leela owns — the brand — at the highest possible incremental margin and with negligible capital. It also creates a flywheel: every Leela Residence sold becomes a permanent advertisement for the brand to ultra-high-net-worth Indians.

Sitting on top of these three circles is what the industry calls the भारतीय शादी Indian wedding segment — the single most important demand driver for Indian luxury hospitality and the segment where the Leela is structurally advantaged. A flagship wedding at the Leela Palace Udaipur or the Leela Palace New Delhi typically books out the entire property for several days, generates a multiple of normal room-night revenue per key, and locks in catering, banquet, and ancillary spend at premium pricing. Business Standard reported in early 2024 that luxury hotels in India were seeing record wedding bookings, with marquee dates extending into 2027.3 The Indian wedding industry, by various consulting estimates, is comparable in size to the global cruise industry; the Leela captures a structurally disproportionate share of its highest-spending tail.

The other compounding tailwind is what management calls "domestic premiumization." Indian outbound travel was historically a leakage problem for domestic hospitality — every Indian millionaire wedding in Bangkok or Dubai was a property-night the Leela did not earn. Post-2020, with international travel disrupted and Indian high-net-worth wealth growing faster than the global average, that flow has partially reversed. The growth rate of the Indian ultra-high-net-worth segment — by Knight Frank and similar estimates — runs roughly double the rate of standard luxury, and the Leela's average room rates in flagship markets like Udaipur, Delhi, and Bengaluru have led the industry as that wealth has migrated into experiential consumption.[^8]

The strategic insight is this: the Leela is no longer just a hotel company. It is a luxury-brand platform with three monetization vectors — owned hotels, managed hotels, and residences — riding on a structural Indian luxury demand wave. That repositioning is what justifies the IPO valuation differential against its peers.

VI. Porter's Five Forces and Hamilton's Seven Powers

If you put The Leela through a competitive-structure analysis, three things become obvious quickly.

The primary power is brand. In Hamilton Helmer's Seven Powers framework, a brand becomes a durable competitive moat when it allows the holder to charge a higher price for an objectively similar product. The Leela does this consistently across markets. In Delhi, the Leela Palace and the Taj Palace are both five-star marble-and-chandelier properties within a few kilometers of each other; the Leela's average daily rate during peak wedding season runs at a notable premium. The Leela name has become the signal — particularly in the Indian wedding and corporate offsite market — that price is not the consideration. Couples announcing a "Leela wedding" are communicating something about their family that they could not communicate as efficiently via any other brand.

The second is cornered resource: irreplaceable real estate. The Leela Palace Udaipur sits on lakefront acreage on Lake Pichola that cannot be replicated; Indian heritage and zoning law makes new lakefront luxury hotel construction on Pichola functionally impossible. The Leela New Delhi sits on a 7-acre parcel in Chanakyapuri, the diplomatic enclave, where new hotel land is unavailable at any price. The Leela Bengaluru sits on a CBD-adjacent parcel of a size that would, today, be unobtainable without a multi-thousand-crore land bill. The supply curve is not just inelastic — it is effectively vertical.

The third is counter-positioning. IHCL operates not just the Taj but also the mid-market Vivanta and the budget-luxury Ginger brands. EIH operates Oberoi at the top and Trident below it. Both have economically rational reasons for those sub-brands — they smooth occupancy and amortize central overheads — but they also dilute brand purity. A Vivanta wedding is not a Taj wedding; the consumer knows the difference. The Leela, by contrast, has stayed structurally pure-play luxury. There is no Leela Express, no Leela Lite. The brand promises one thing and delivers it everywhere. That positioning, post-Brookfield, has been deliberately reinforced rather than diluted.

Where the moat is shallower: switching costs for individual travelers are essentially zero. A business executive picking between Leela New Delhi, Taj Palace, and the Oberoi New Delhi for a one-night stay has minimal lock-in. But — and this is the strategic asymmetry — switching costs for luxury wedding planners, large corporate MICE events (meetings, incentives, conferences, exhibitions), and ultra-high-net-worth repeat clients are very high. A wedding planner who has run twenty events at the Leela Palace Udaipur has built tacit knowledge about every banquet hall, every catering team, every contingency the property handles. That planner does not casually move a marquee event to a competitor.

The Porter's Five Forces analysis reinforces the picture. Bargaining power of suppliers is low — Indian hospitality has abundant labor, contract food and beverage supply chains, and standard furniture and fixtures supply. Bargaining power of buyers is split: high for individual transient guests, low for the wedding and MICE buyers who are constrained by venue availability and brand prestige. Threat of new entrants is moderate at the property level (new hotels can be built) but very low at the brand level (no one is creating a new credible Indian luxury hotel brand from scratch). Threat of substitutes — international destinations, alternative event venues, palace-hotel competitors — exists but is partially offset by domestic premiumization. Competitive rivalry among the top three Indian luxury players (Leela, Taj, Oberoi) is intense but rational; none of them has shown any inclination to engage in destructive price competition at the top of the market.

The composite picture is of a business with a small number of very durable moats — brand and cornered resource — combined with a structural demand tailwind. It is precisely the profile that Brookfield bought, and precisely the profile being underwritten by public-market investors.

VII. The IPO and the Future Roadmap

The IPO conversation around Schloss Bangalore had been a year-long anticipation in Indian capital markets. Bloomberg first reported in September 2024 that the Brookfield-backed entity had filed for an IPO targeting roughly $600 million.2 The DRHP, filed with SEBI in the same period, laid out the structure: a fresh-issue component to deleverage the balance sheet and an offer-for-sale component allowing Brookfield to partially monetize its position while retaining majority control.[^1]

The fresh-issue mathematics were straightforward. Despite the operational reset, Schloss Bangalore had carried debt from the original acquisition and from subsequent capital expenditure on property upgrades. The IPO proceeds were earmarked primarily for deleveraging — paying down term loans and reducing the platform's interest burden. The remaining proceeds were positioned as general corporate purposes, including the potential for acquiring iconic boutique luxury properties to expand the network.

The bull case from public-market underwriters rested on three pillars. First, the structural Indian luxury consumption wave — captured in the same data that drives the bull case for रिलायंस Reliance Retail's luxury vertical and for premium Indian consumer-goods companies. Second, the global scarcity of listed pure-play luxury hotel stocks; most global hospitality majors are either asset-light brand companies (Marriott, Hilton) or diversified across luxury-to-budget tiers (Accor, IHG), leaving very few public vehicles that offer clean pure-play luxury hotel exposure. Third, the operating leverage embedded in the Leela's cost structure — once a luxury hotel is built and staffed, incremental room-night revenue drops to the operating line at a very high incremental margin.

The bear case is just as articulable, and any honest investor needs to hold both. Concentration risk is real: a handful of properties contribute the overwhelming majority of EBITDA, which means a localized disruption at any one trophy asset — a fire, a regulatory shutdown, a city-level demand shock — has outsized P&L impact.[^1] Luxury travel demand is cyclical and correlated with both global financial conditions and Indian discretionary spending; the segment held up well through the post-pandemic recovery, but a meaningful Indian recession or a geopolitical shock that crushes inbound diaspora travel would hit the company harder than a more diversified hospitality peer. Capital intensity, despite the asset-light pivot, remains significant: maintaining a flagship Leela Palace property at peak presentation standards costs real money every year. And the valuation premium that the Leela commands at IPO — relative to IHCL and EIH on a per-key or EBITDA basis — leaves limited room for execution disappointment.[^8]

The Mint comparative analysis in October 2024 made the valuation framing explicit: the Leela was being priced at a meaningful premium per key to its listed peers, justified by the pure-play luxury positioning, the higher average room rates, and the asset-light optionality through residences and managed contracts.[^8] Whether that premium proved appropriate would depend, as always, on the next several years of operating performance.

The KPIs to actually watch are narrower than the full investor-deck dashboard. First and most important: RevPAR (revenue per available room) for the owned portfolio. RevPAR captures both occupancy and average daily rate in a single number, and for a luxury hotel platform it is the cleanest read on demand strength and pricing power. Second: management and residence-fee revenue as a percentage of total revenue — this is the proxy for how successfully the company executes the asset-light pivot. The higher this ratio climbs over time, the more the platform looks like a brand business rather than a real-estate business, and the higher the multiple it can sustain. Third (for the patient investor): EBITDA margin at the consolidated level — if Brookfield's operating reset actually compounds, this number should drift upward over time rather than oscillate around a flat mean.

Everything else — quarterly noise around weather, election cycles, individual property renovations — is secondary.

VIII. Playbook: Business and Investing Lessons

There is a "myth vs reality" frame worth holding up against this story.

The myth is that the Nair family lost the Leela because Indian banks were predatory, because the global financial crisis crushed luxury travel, or because the family was unlucky. The reality is more sobering and more useful: the Leela went into distress because the operating model — owning every asset, financing with rupee debt at peak rates, building at peak land prices — was structurally fragile. Marriott, Hilton, and Hyatt had already shown that the durable economics in global hospitality belonged to the brand and the operator, not the property owner. The Nairs built a magnificent product on a financing structure that the global industry had already moved past. That is the deeper lesson, and it generalizes well beyond hotels: in capital-intensive consumer businesses, the structure of how growth is funded often matters more than the quality of the growth itself.

The Brookfield playbook is the contrapositive. Buy a brand whose underlying asset value is masked by financial distress. Strip out the family's other liabilities through a clean asset-purchase structure. Install a global-standard operating chassis under professional management. Hold for five-to-seven years through an operating reset, capturing both margin expansion and a cyclical demand recovery. Then crystallize value through a public market listing while retaining control. This is private-equity-style value creation applied to a real-asset platform, and it is the same template Brookfield has deployed across logistics, office, and infrastructure assets globally. The Leela is the most prominent Indian application of that template.

There is a related lesson on pricing power, which is perhaps the most under-discussed feature of luxury hospitality. Inflation — Indian inflation in particular, which has historically run higher than developed-market norms — erodes margin in most consumer businesses. Luxury hospitality is different. When the cost of staff, food, energy, and consumables rises, the Leela passes those costs through in average daily rate, and the wedding planner booking the Leela Palace Udaipur three years in advance does not noticeably resist. The brand carries the price. Over long holding periods, luxury businesses with genuine pricing power compound real value in a way that most consumer categories do not. This is the structural reason why luxury — in hospitality, in goods, in residential real estate — is one of the cleanest long-term inflation hedges in the Indian economy.

A final structural observation: family-run Indian businesses transitioning to institutional ownership are a category that has produced repeated wealth creation over the past two decades. The pattern is consistent — a founder builds an irreplaceable consumer or industrial asset, financial constraints or generational succession force a transition, professional management compounds the underlying franchise, and a public listing crystallizes the value gap. The Leela is one expression of that pattern. Investors paying attention to it will recognize the silhouette in other categories — consumer products, financial services, healthcare — and will be alert to the same setup elsewhere.

IX. Conclusion

Captain Nair died in 2014, ten years before the company he founded reached its public listing under a different owner, a different management team, and a different operating philosophy. He never saw the IPO bell. He also never saw the insolvency proceedings that came perilously close to dismantling his life's work. In some sense, he was spared both.

What endures from his era is the aesthetic. Walk into any Leela Palace today and the experience is recognizably his: the gilt, the lily ponds, the courteous theatrical hospitality that announced — to a generation of Indians who had grown up under colonial-era hotel codes — that India could build palaces of its own that did not need to apologize for being modern. That product vision was the founder's gift to the brand, and no amount of professional management could have substituted for it.

What changed under Brookfield is everything else. The capital structure, the operating chassis, the governance, the strategic horizon. The institutional reality of the Leela in 2026 is unrecognizable from the family-office reality of the Leela in 2016. A public investor buying a share of Schloss Bangalore today is buying Captain Nair's product wrapped in someone else's discipline.

Whether the Leela brand is stronger today than it was twenty years ago depends entirely on what one values. By the metric of cultural resonance — the brand's status among Indian wedding planners, ultra-high-net-worth travelers, and corporate event organizers — it is, by any honest measure, at its strongest point ever. By the metric of operational durability — balance sheet resilience, governance quality, capacity to compound through cycles — it is unambiguously stronger than at any prior period in its history. By the metric of founder myth — the singular, romantic, against-the-odds story of an army captain turned textile exporter who, at 65, decided to build palaces — that era has closed.

The Leela has crossed over from being one man's monument to being a public market platform. The next chapter belongs to spreadsheets, quarterly earnings calls, and the slow compounding logic of institutional hospitality. It is a different kind of story. It is also, for the patient investor, the kind of story that tends to be worth following.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube