Tejas Networks: India's Optical Networking Pioneer

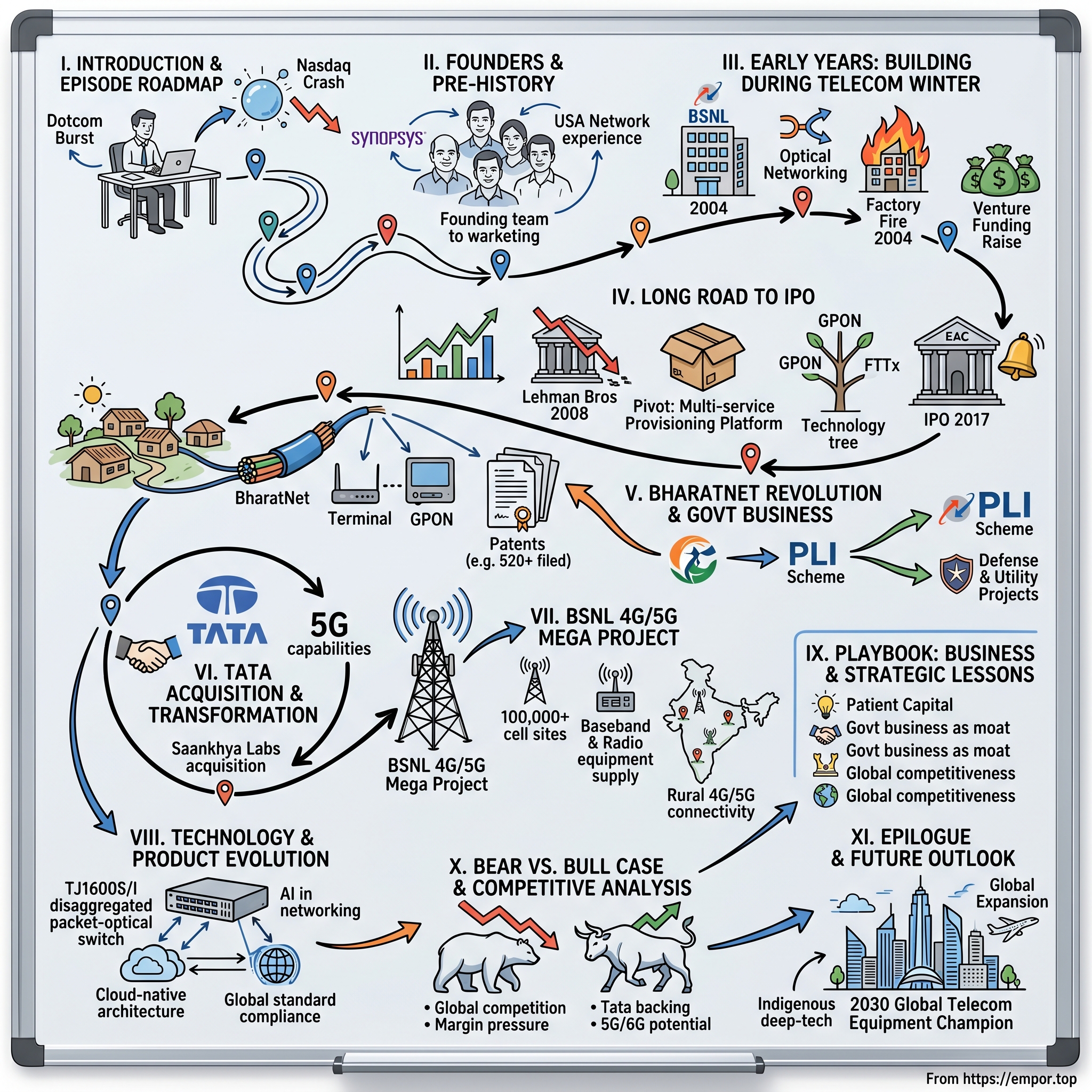

I. Introduction & Episode Roadmap

Picture this: It's May 2000, and the dotcom bubble has just burst. Nasdaq has crashed 37% from its peak. Telecom giants like Nortel and Lucent are hemorrhaging billions. In this apocalyptic landscape for tech startups, a former Electronic Design Automation executive in Bangalore decides now is the perfect time to start India's first serious telecom equipment company. His friends think he's lost his mind.

Twenty-one years later, that same company would be acquired by Tata Sons for ₹1,884 crore, marking one of the most significant deep-tech acquisitions in Indian corporate history. The company? Tejas Networks. The founder? Sanjay Nayak—a man who admits he knew virtually nothing about telecommunications when he started.

Today, Tejas Networks designs and manufactures optical networking products used by telecom service providers, utilities, governments, and defense networks across 75+ countries. They've filed over 520 patents, deployed equipment connecting 40,000 Indian villages, and just completed one of the largest single-vendor telecom deployments globally—supplying over 100,000 cell sites for BSNL's 4G/5G network in just 18 months.

The central question isn't just how a startup survived the telecom winter—it's how an Indian company, founded during the worst possible time, built world-class products that compete with Ericsson, Nokia, and Huawei. How did they convince skeptical government buyers that "Made in India" could mean cutting-edge technology? And why did the Tata Group, after decades of avoiding telecom equipment manufacturing, suddenly decide Tejas was their ticket back into the game?

This is a story about patient capital meeting impatient ambition, about building deep-tech capabilities in a market that didn't believe it was possible, and about how sometimes the worst time to start a company becomes the best foundation for building one. We'll journey from Tejas's EDA roots through the telecom winter, explore their strategic pivot during the global financial crisis, dissect the BharatNet revolution that transformed their fortunes, and examine how the Tata acquisition has positioned them for the 5G era.

Along the way, we'll uncover the playbook for building hardware companies in emerging markets, understand why government business can be both a blessing and a curse, and analyze whether Tejas represents the future of Indian tech—or a relic of an older model. Buckle up—this isn't your typical software startup story.

II. The Founders & Pre-History

The year is 1987. A young engineer named Sanjay Nayak joins Synopsys, an American electronic design automation company that's revolutionizing how semiconductors are designed. Over the next thirteen years, Sanjay would rise to become Managing Director of Synopsys India, building one of the country's most successful software subsidiaries. He had the golden handcuffs—stock options, a corner office, respect in Silicon Valley. Life was good.

But something gnawed at him. Every chip his team helped design would go into products made elsewhere. India was great at services, fantastic at software, but when it came to building actual products—especially complex hardware—the ecosystem was barren. "We were always the back office," Sanjay would later reflect. "I wanted to build something from India that the world would buy as a finished product."

The telecommunications sector beckoned, despite Sanjay's admission that he "didn't know the field." This wasn't false modesty—it was genuine ignorance that, paradoxically, became an asset. While telecom veterans saw constraints, Sanjay saw possibilities. While they knew what couldn't be done, he didn't know enough to be discouraged.

Enter Gururaj "Desh" Deshpande, the serial entrepreneur who'd sold Cascade Communications to Ascend for $3.7 billion and was looking for the next big thing. Desh provided the initial funding, but more importantly, he provided belief. "Sanjay had no telecom experience," Desh would later say, "but he had something more important—the ability to attract talent and the persistence to keep going when everyone said it was impossible."

Soon, Sanjay assembled a dream team. Arnob Roy joined as co-founder, bringing deep telecom expertise from his stint at Cisco. Dr. Kumar Sivarajan, an IIT Bombay alumnus with a PhD from Caltech and experience at IBM Research, came aboard as Chief Technology Officer. This triumvirate—the execution-focused CEO, the industry veteran, and the technical visionary—would form the backbone of Tejas Networks.

The Indian tech ecosystem in 2000 was a study in contradictions. Post-liberalization optimism was colliding with dotcom crash reality. Y2K had put India on the global software map, but hardware? Product companies? That was considered foolhardy. Venture capitalists would literally laugh people out of rooms for suggesting hardware startups. "Software has 80% gross margins," they'd say. "Hardware has 40% if you're lucky. Why would we fund that?"

But Sanjay saw what others missed. India's telecom revolution was just beginning—teledensity was under 3%, mobile phones were luxury items, and the government was about to embark on one of the world's most ambitious connectivity programs. Someone would need to build the infrastructure. Why not an Indian company?

The founding of Tejas Networks in May 2000 wasn't just about starting a company—it was about challenging the fundamental assumption that India could only do services, not products. That complex engineering was somehow beyond Indian capabilities. That competing with global giants was a fool's errand.

Eleven years later, when ELCINA awarded Sanjay "Electronics Man of the Year 2011," the citation read: "For proving that world-class products can be designed and manufactured in India." But in 2000, that proof was still a distant dream. The real question was whether they'd survive long enough to prove anything at all.

III. Early Years: Building During the Telecom Winter (2000–2007)

The conference room at BSNL headquarters in Delhi, 2002. Sanjay Nayak and his team are presenting their optical networking solution. The government officials look skeptical. "Why should we buy from you?" asks a senior bureaucrat. "Lucent, Nortel, Siemens—these companies have been doing this for decades. You've been around for two years. What's your installed base?" The answer—zero meaningful deployments—hangs in the air like smoke from a burnt circuit board.

This was the reality Tejas faced in its early years. They'd developed intelligent network technologies that could transfer data between two points at precisely the speed customers required—a technical achievement that impressed engineers but meant nothing to buyers who'd never heard of them. Product development in India was unprecedented, and customers were understandably skeptical. Could an Indian startup really build carrier-grade equipment that wouldn't fail when millions of subscribers depended on it?

The global environment made everything worse. The telecom winter had set in—Nortel's stock had fallen 95%, Lucent was laying off thousands, and venture capital for telecom equipment had dried up faster than water in the Thar Desert. Yet somehow, against all logic, Tejas Networks managed to raise $100 million in venture funding between 2000 and 2007. Intel Capital, Mayfield Fund, and Battery Ventures all bought into the vision, though not without serious arm-twisting and multiple pivots in the pitch deck.

Then came the night that almost ended everything. January 2004, 2 AM. Sanjay's phone rings. The Tejas facility is on fire. Not a small electrical fire—a full-blown inferno that would destroy most of their infrastructure, prototypes, and test equipment. By dawn, years of work had turned to ash and twisted metal. The team gathered in the parking lot, some crying, others in shock. Insurance would cover maybe 40% of the losses. The venture investors were already nervous. This could be the excuse everyone needed to shut things down.

But here's where the Tejas story diverges from the typical startup narrative. Instead of pivoting or shutting down, leadership made a radical decision: senior executives would take 50% salary cuts, but not a single junior engineer would be laid off. "We told the team—we've lost our equipment, but we haven't lost our knowledge," Sanjay recalled. "We can rebuild the products. We can't rebuild the team."

The response was extraordinary. Engineers worked 16-hour days to recreate designs from memory. Customers who'd been skeptical suddenly became supportive—if this company could survive a fire and keep their commitments, maybe they were worth betting on. Within six months, Tejas had not only recovered but accelerated product development. The TJ100 series of optical add-drop multiplexers started winning contracts, first small ones from private operators, then larger ones from BSNL.

By 2007, the company had achieved something remarkable: exponential financial growth from virtually zero to over $50 million in revenue. They'd built world-class optical networking products that were being deployed not just in India but internationally. The TJ1000 series could handle 10 Gigabit Ethernet speeds when most Indian networks were still struggling with basic broadband. Their packet optical transport platforms were winning competitive bids against Alcatel-Lucent and Huawei.

The technical achievements were impressive, but the cultural transformation was more significant. Tejas had proven that an Indian company could do original R&D, not just customize Western products. They'd shown that Indian engineers, given the right environment and leadership, could innovate at the cutting edge. When senior engineers from Cisco or Nortel visited the Bangalore facility, they'd often express surprise: "This looks like our labs in Silicon Valley."

But success brought new challenges. The company was burning cash faster than revenue was growing. The global financial crisis was looming. Competitors were consolidating. And the Indian telecom market, while growing, was becoming increasingly price-sensitive. The question was no longer whether Tejas could build world-class products—they'd proven that. The question was whether they could build a sustainable business around those products. The next decade would test that proposition in ways no one could have imagined.

IV. The Long Road to IPO (2008–2017)

September 15, 2008. Lehman Brothers collapses. The global financial system freezes. In Bangalore, Sanjay Nayak watches the news with a sinking feeling. Tejas Networks has purchase orders worth $30 million that customers are about to cancel. The venture investors who'd promised a Series D round are suddenly unreachable. The telecom equipment market, already struggling, is about to crater. "We had two choices," Sanjay would later say. "Die slowly by cutting costs, or transform completely."

Tejas chose transformation. While competitors retreated to their core products, Tejas expanded. The logic seemed counterintuitive—why spread resources thinner during a crisis? But the team recognized a fundamental shift: carriers didn't want single-purpose boxes anymore. They wanted platforms that could handle multiple technologies. The era of convergence had arrived, accelerated by the financial pressure to do more with less.

The pivot started with the TJ1400 series—a Swiss Army knife of telecom equipment that combined fiber broadband, mobile broadband, Ethernet, and packet optical transport in a single platform. Engineers called it "Frankenstein's monster" during development because it tried to do everything. Critics said it would be master of none. But customers loved it. Why buy four boxes from four vendors when one box could do it all? By 2010, Tejas was also pioneering GPON (Gigabit Passive Optical Network) and XGS-PON solutions—technologies that would later become critical for India's fiber broadband revolution. The multi-service provisioning platforms they developed could handle everything from legacy TDM to cutting-edge packet switching. It was infrastructure designed for a future that hadn't arrived yet, built by a company that couldn't afford to wait for it.

The darkest moment came in 2012. Revenue had plateaued around $60 million. Competitors were offering products at 40% lower prices. The board was pushing for a sale—better to exit with dignity than bleed to death. But Sanjay and the team had one card left to play: the Indian market was finally ready for their products. The 3G rollout was accelerating. The government was talking about Digital India. If they could just hold on a little longer...

They held on. By 2015, the company had turned profitable, crossing ₹500 crore in revenue. The venture investors who'd written off their investment were suddenly interested again. Investment bankers started circling. The IPO window, closed since 2008 for Indian tech companies, was cracking open.

Tejas Networks IPO bidding started from June 14, 2017 and ended on June 16, 2017, with allotment finalized on June 21, 2017, and shares listed on BSE, NSE on June 27, 2017. The IPO was priced at ₹257 per share, valuing the company at approximately ₹2,350 crore—a remarkable achievement for a company that almost died multiple times.

The company was considered the first listed player in the optical networking equipment space in India, with anchor investors including Abu Dhabi Investment Authority, East Bridge Capital and PremjiInvest. The IPO wasn't just a liquidity event—it was validation. Validation that Indian companies could build complex hardware. That patient capital, however painful, could pay off. That surviving the telecom winter had created a company strong enough to thrive in the spring.

But the IPO also marked a transition. Tejas was no longer a scrappy startup fighting for survival. It was a public company with quarterly earnings calls and institutional investors. The question was whether it could maintain its innovation edge while satisfying the market's demand for predictable growth. The answer would come from an unexpected source: the Indian government's most ambitious connectivity project.

V. The BharatNet Revolution & Government Business

The village of Nohabad in Haryana, 2018. Population: 2,341. Distance from nearest town: 47 kilometers. Internet connectivity: Zero. A Tejas Networks engineer stands in the scorching heat, supervising the installation of a GPON terminal that will bring 100 Mbps broadband to this forgotten corner of India. The local sarpanch watches skeptically. "We've been promised electricity for decades," he says. "Now you're promising internet?" Six months later, that same sarpanch would be conducting video conferences with district officials, and local students would be taking online courses from IITs.

Tejas' GPON solution was deployed in BharatNet, the world's largest greenfield rural broadband rollout delivering high-speed Internet to more than 200 million people, helping connect 40,000 villages with 70% requirement support. This wasn't just a contract—it was a transformation of how India thought about rural connectivity.

The strategic importance of domestic manufacturing in telecom had become painfully clear to the Indian government. China's Huawei and ZTE dominated the market. European vendors like Ericsson and Nokia controlled the high-end. India, despite having one of the world's largest telecom markets, was almost entirely dependent on imports. The security implications were obvious. The economic implications were worse—billions of dollars flowing out annually for equipment that formed the backbone of the nation's digital infrastructure.

With the help of PLI Scheme, Tejas is increasing production to support local demand and reduce $5 billion import bill for the FTTx segment. The Production Linked Incentive scheme wasn't just about subsidies—it was about creating an ecosystem where Indian companies could compete globally. Tejas, with its proven track record and existing manufacturing capabilities, was perfectly positioned to benefit.

But working with the government wasn't easy. The procurement processes were byzantine. Payment cycles stretched to 180 days or more. Every deployment required multiple approvals, site inspections, and compliance certificates. Competitors whispered about favoritism. International vendors complained about protectionism. Tejas had to navigate not just technical challenges but political ones.

The real breakthrough came from trust—built slowly, deployment by deployment. When a cyclone knocked out communication infrastructure in Odisha, Tejas engineers worked 72-hour shifts to restore connectivity. When the government needed emergency COVID-19 communication networks in 2020, Tejas delivered in weeks what typically took months. These weren't just business transactions; they were demonstrations of capability and commitment.

Tejas Networks has filed for 520+ patents, of which 127 have been granted. This intellectual property portfolio became crucial in government evaluations. It proved that Tejas wasn't just assembling imported components but doing genuine R&D. When defense establishments needed secure communication equipment, Tejas could demonstrate that its designs were indigenous, its source code was accessible, and its supply chain was controllable.

The financial impact was transformative. Government business, which contributed less than 10% of revenue in 2015, grew to over 25% by 2020. More importantly, it provided a stable base that allowed Tejas to invest in next-generation technologies. The gross margins might be lower than private contracts, but the volume and predictability made up for it.

Yet success brought scrutiny. Every government contract was dissected by competitors and media. Accusations of crony capitalism surfaced whenever Tejas won a large tender. The company had to maintain spotless compliance records, transparent bidding processes, and arms-length relationships with officials. One scandal could destroy decades of reputation building.

The BharatNet project also exposed Tejas to India's harsh realities. Installing equipment in Naxal-affected areas required security escorts. Monsoons would wash away newly laid fiber cables. Local contractors would disappear with advance payments. Power availability in rural areas was so erratic that Tejas had to design equipment that could function with massive voltage fluctuations.

But these challenges became competitive advantages. International vendors, used to pristine data centers and reliable infrastructure, struggled in India's chaos. Tejas engineers, who'd grown up with power cuts and studied by candlelight, designed products that were practically indestructible. The TJ1400 routers could operate in 50-degree heat without air conditioning. The GPON terminals could survive voltage spikes that would fry European equipment.

By 2021, Tejas had become synonymous with Digital India. But the company was at another inflection point. The 5G era was dawning. Chinese vendors were being pushed out globally. The opportunity was massive, but so was the investment required. Tejas needed a partner with deep pockets and long-term vision. Enter the Tata Group.

VI. The Tata Acquisition & Transformation (2021–Present)

The boardroom at Bombay House, July 29, 2021. Natarajan Chandrasekaran, Chairman of Tata Sons, signs the document that would bring Tejas Networks into the Tata fold. Tata Sons, through Panatone Finvest, initiated investment for 43.35% stake at Rs 1,884 crore—one of the largest tech acquisitions in the group's history. The press release spoke of synergies and strategic fit. But the real story was more nuanced: The Tatas were making a calculated bet that telecom equipment manufacturing would be as strategically important in the 21st century as steel was in the 20th.

The Tata Group's relationship with telecom was complicated. They'd pioneered India's international telecom services through VSNL, only to see it stagnate after privatization. Tata Teleservices had burned billions trying to compete in mobile services before effectively shutting down. But telecom equipment manufacturing? That was virgin territory for the salt-to-software conglomerate.

Tejas Networks looked to use Tata group's backing to expand telecom products portfolio, and in March 2022, acquired 64% of Saankhya Labs, an Indian wireless communication and semiconductor company. This wasn't just an acquisition—it was a strategic pivot. Saankhya Labs brought 5G capabilities, semiconductor design expertise, and over 50 patents in wireless communications. Combined with Tejas's optical networking prowess, the Tata Group suddenly had an end-to-end telecom equipment powerhouse.

By April 2022, Tata Sons increased shareholding to 52.45% majority control. The gradual increase wasn't accidental—it allowed the Tatas to understand the business deeply before taking full control. They discovered a company that was technically brilliant but managerially stretched. Sanjay Nayak, after 23 years at the helm, was ready to pass the baton.

The leadership transition was delicate. Anand Athreya, appointed as CEO & MD designate in 2023, brought a different style—more corporate, more process-oriented, but equally ambitious. The old guard worried about losing the startup culture. The new management worried about scaling without systems. The integration wasn't just about merging companies but merging cultures. The results were spectacular. In Q4-FY25 Tejas completed deliveries of 100,000+ sites for the BSNL 4G/5G network which is one of the largest single-vendor RAN networks delivered in record time. Revenue grew from Rs 4,246 million in FY20 to Rs 25,356 million in FY24—a CAGR of 56.3%. The company achieved consolidated revenue for Q4-FY24 of Rs 1,327 crore (YoY 343%), FY24 revenue of Rs 2,471 crore (YoY 168%), Q4-24 Net Profit of Rs 147 crore and FY24 Net Profit of Rs 63 crore.

The Tata brand brought credibility, especially with international customers who'd been hesitant about buying from a standalone Indian company. The group's financial strength meant Tejas could bid for larger, longer-duration contracts without worrying about working capital. The synergies with other Tata companies—TCS for system integration, Tata Power for smart grid projects, Tata Communications for network services—created a multiplier effect.

But integration wasn't friction-free. The entrepreneurial culture that had defined Tejas—quick decisions, informal processes, equity-based compensation—clashed with Tata's more structured approach. Some key engineers left, worried about becoming another cog in the conglomerate machine. The stock price, which had surged post-acquisition announcement, started showing volatility as investors questioned whether Tejas could maintain its innovation edge under corporate ownership.

The real test came with execution. The BSNL 4G/5G project wasn't just large—it was existentially important for both Tejas and India's telecom sovereignty. Every delay, every technical glitch would be scrutinized. Competitors were waiting for Tejas to stumble, ready with "I told you so" narratives about Indian companies being unable to handle complex projects.

VII. The BSNL 4G/5G Mega Project

The BSNL headquarters war room, August 2023. Maps of India cover every wall, dotted with thousands of red and green pins—red for pending installations, green for completed. A team of 50 engineers works round the clock, coordinating what would become one of the most ambitious telecom deployments in history. The target: 100,000 cell sites across India, from the Siachen Glacier to the Andaman Islands, from the Thar Desert to the Northeast's rainforests. The vendor: Tejas Networks, a company that had never done a wireless deployment of this scale.

The numbers were staggering. Tejas successfully completed supply of baseband and radio equipment for over 100,000 cell sites in BSNL's 4G/5G network—one of the largest single-vendor deployments globally, completed in just 18 months. To put this in perspective, typical deployments of this scale take 3-4 years. Ericsson's largest single deployment in India covered 50,000 sites over two years. Nokia's African expansion hit 30,000 sites in 18 months. Tejas doubled these benchmarks.

The strategic importance for India's telecom sovereignty cannot be overstated. Since the early 2000s, Indian telecom had been dominated by foreign equipment. When the Galwan Valley clash happened in 2020, the vulnerability became acute—Chinese equipment powered significant portions of Indian networks. The government's decision to revive BSNL wasn't just about saving a PSU; it was about creating a credible alternative to foreign dependence.

Technology challenges were immense. India's geography is arguably the world's most challenging for telecom deployment. The equipment had to work at -40°C in Ladakh and +50°C in Rajasthan. Humidity in Kerala could reach 95%. Dust storms in Gujarat could sandblast electronics. Salt air in coastal areas corroded circuits. Tejas engineers didn't just adapt existing designs—they reimagined them. The radio units were hermetically sealed but naturally cooled. The baseband processors could handle power fluctuations from 90V to 440V. The software could self-heal from 80% of common failures.

Competition with global giants intensified during the project. Ericsson, Nokia-Siemens, Huawei (through proxies), Alcatel-Lucent, Ciena, and Adva all lobbied hard, arguing that BSNL was taking unnecessary risks with an untested vendor. International media ran stories questioning whether Tejas could deliver. Some competitors offered equipment at 50% discounts to private operators, trying to prove that Indian alternatives weren't needed.

But Tejas had advantages the giants couldn't match. When BSNL needed custom features for rural deployments, Tejas engineers implemented them in weeks, not months. When sites in Naxal areas needed special security features, Tejas created encrypted, tamper-proof equipment. When the Ministry of Defence wanted specific capabilities for border areas, Tejas complied without asking for extra payments or extended timelines.

Partnering with system integrators for BSNL's 4G tender and supplying products to Bharti Airtel for 5G backhaul showed Tejas could work across ecosystems. They weren't trying to do everything themselves—they understood that modern telecom required collaboration. TCS handled system integration, Tech Mahindra managed field operations, and local contractors did physical installations. Tejas focused on what it did best: designing and manufacturing world-class equipment.

The execution was military in precision. Every morning at 6 AM, regional heads would dial into a central war room. Problems were escalated in real-time. If a site in Assam needed specific equipment, it would be air-shipped from Bangalore within 24 hours. If installation teams faced local protests, government liaisons would intervene immediately. The entire supply chain was reimagined—instead of centralized warehouses, Tejas created 200+ micro-warehouses across India, reducing last-mile delivery time from days to hours.

The human cost was significant. Engineers lived in temporary camps for months. Families complained about absent parents. Some marriages were strained. But there was also pride—immense pride—in doing something no Indian company had done before. "My grandfather built roads after independence," one engineer said. "I'm building digital highways."

By March 2024, the impossible had been achieved. 100,000 sites were operational. BSNL's 4G network, written off as a joke, was suddenly competitive. In blind speed tests, it often outperformed private networks. Rural areas that had never seen broadband were getting 100 Mbps connections. The strategic goal was achieved—India now had a fully indigenous telecom network, immune to international sanctions or supply chain disruptions.

VIII. Technology & Product Evolution

Inside Tejas's Bangalore R&D facility, 2023. A team of engineers huddles around a prototype that looks like something from a science fiction movie—circuits printed on transparent substrates, photonic processors handling terabits of data, AI chips predicting network failures before they happen. This is the TJ1600S/I, what would become the world's largest disaggregated packet-optical switch. Five years ago, this team was debugging basic GPON terminals. The transformation from optical components supplier to multi-technology platform provider represents one of the most ambitious pivots in telecom equipment history.

The evolution started with a fundamental insight: networks were converging. The old world of separate networks for voice, data, video, wireless, and wireline was ending. Service providers wanted unified platforms that could handle everything. But building such platforms required capabilities across the entire technology stack—from photonics to packet processing, from radio frequency to artificial intelligence.

Products on 10G-PON technology, equipment upgradable to 5G, helping private telecom operators with GPON equipment—each product family represented years of R&D and hundreds of millions in investment. The 10G-PON products weren't just faster versions of older technology; they incorporated AI-driven traffic management, quantum-safe encryption, and energy efficiency that reduced power consumption by 60% compared to competitors.

Selling to telecommunications service providers, internet service providers, web-scale internet companies, utility companies, defense companies, and government entities required different approaches for each segment. Telcos wanted five-nines reliability (99.999% uptime). Web-scale companies wanted API-driven automation. Utilities needed equipment that could survive electromagnetic pulses. Defense required sovereign-controlled encryption. Each requirement drove new innovations.

The R&D culture at Tejas was unique in Indian hardware companies. Engineers were encouraged to fail fast and fail cheap. Every Friday was "Demo Day"—anyone could present new ideas, no matter how crazy. The company maintained a "20% time" policy borrowed from Google, where engineers could work on passion projects. Some of the biggest breakthroughs, including the adaptive cooling system that became standard across all products, came from these side projects.

Recent wins validated the technology strategy. The multi-year Vodafone Idea contract proved Tejas could meet the demands of India's most technically sophisticated operator. USA network modernization orders showed international competitiveness—American operators weren't buying Tejas for price but for unique capabilities in brownfield network upgrades. Southeast Asia FTTX pilots demonstrated that Tejas's tropical-optimized equipment outperformed European alternatives. Africa and Mexico DWDM/GPON wins proved the products could work in any environment.

But the real revolution was in software. Tejas realized early that hardware was becoming commoditized—the differentiation lay in software that could make networks intelligent. The TJ5500 network management system wasn't just monitoring equipment; it was predicting failures, optimizing traffic routes, and automatically healing network problems. Machine learning algorithms trained on data from millions of network events could identify issues that human operators would never spot.

The patent portfolio became a strategic weapon. With 520+ patents filed and 335 granted, Tejas could engage in cross-licensing deals with global giants. When Huawei tried to block Tejas from entering certain markets with patent lawsuits, Tejas counter-sued with its own patents. The standoff ended with a comprehensive cross-licensing deal that gave Tejas access to Huawei's vast patent portfolio while protecting its own innovations.

The shift to cloud-native architectures was particularly prescient. While competitors were still selling monolithic hardware boxes, Tejas was disaggregating functions into software that could run on commodity hardware. This wasn't just following trends—it was anticipating where networks would be in five years. When Open RAN standards emerged, Tejas was ready with compliant products while competitors scrambled to adapt.

Yet challenges remained. The technology landscape was evolving faster than ever. 6G standards were already being discussed while 5G was still being deployed. Quantum computing threatened to make current encryption obsolete. Satellite constellations like Starlink were bypassing terrestrial networks entirely. Tejas had to innovate not just to stay competitive but to stay relevant. The question was whether an Indian company, even one backed by the Tatas, could keep pace with Silicon Valley's infinite resources and China's massive scale.

IX. Playbook: Business & Strategic Lessons

The conference room fills with eager founders, all building hardware startups in India. They've come to hear Sanjay Nayak share the Tejas playbook. He starts with a warning: "If you're looking for quick exits or easy money, leave now. Building deep-tech companies in emerging markets is a decade-long marathon through hell." Half the room shifts uncomfortably. The other half leans forward.

Lesson 1: Patient Capital is Not Optional, It's Existential Tejas burned through $100 million before generating significant revenue. The company went through multiple near-death experiences where running out of money was weeks away. But patient investors like Gururaj Deshpande understood that building hardware companies requires different timelines than software. You can't iterate hardware in two-week sprints. Tape-outs cost millions. Certifications take years. If your investors want returns in 3-5 years, don't even start.

Lesson 2: Government Business as Strategic Moat Most startups avoid government contracts—too slow, too bureaucratic, too political. Tejas embraced them. Government contracts provided patient revenue, reference customers, and most importantly, a moat competitors couldn't easily cross. Once you're embedded in government infrastructure, switching costs become prohibitive. The 180-day payment cycles are painful, but the 10-year relationships are priceless.

Lesson 3: Import Substitution Must Meet Global Competitiveness The easy path is building cheaper, lower-quality alternatives for price-sensitive markets. Tejas took the hard path—building products that could compete globally on quality, not just price. This meant hiring expensive talent, investing in R&D at Silicon Valley levels, and accepting lower margins initially. But when global customers started buying Tejas products for capabilities, not cost, the strategy validated itself.

Lesson 4: Surviving Technology Cycles Requires Paranoid Diversification Tejas survived multiple technology transitions—TDM to IP, copper to fiber, 3G to 4G to 5G—because they never bet everything on one technology. While generating revenue from current products, they were always investing in next-generation technologies. When optical networking slowed, wireless picked up. When wireless matured, packet networking emerged. This portfolio approach meant some bets failed, but the company survived.

Lesson 5: Market Downturns are Feature, Not Bug The 2008 financial crisis forced Tejas to become brutally efficient. The 2020 pandemic accelerated digital adoption. Every downturn that should have killed the company made it stronger. Downturns eliminated weak competitors, made talent affordable, and forced customers to consider alternatives to expensive incumbents. Building during downturns means you're battle-tested for upturns.

Lesson 6: The Tata Acquisition Rationale—Strategic Synergies Trump Financial Engineering When Tata acquired Tejas, the financial media focused on multiples and valuations. They missed the strategic logic. Tata needed telecom equipment capabilities for their digital ambitions. Tejas needed patient capital and global credibility. The synergies weren't in cost-cutting but in capability multiplication. TCS's system integration plus Tejas's products created solutions neither could offer alone.

Lesson 7: Culture Eats Strategy, But Process Enables Scale Early Tejas was all culture—passionate engineers working insane hours for equity and purpose. That works till 500 people. Beyond that, you need processes, systems, and hierarchy. The trick is preserving innovation culture while adding corporate discipline. Tejas did this through "two-speed IT"—startups within the company for new products, corporate processes for mature ones.

Lesson 8: Technical Debt is Real Debt Every shortcut taken to meet deadlines, every hack to win contracts, accumulates as technical debt. Tejas learned this painfully when early products needed complete redesigns for scale. Now they follow a simple rule: if you can't maintain it for ten years, don't build it. This means slower initial development but faster long-term growth.

Lesson 9: Talent Density Matters More Than Talent Quantity Tejas could have hired thousands of average engineers cheaply. Instead, they hired hundreds of exceptional ones expensively. The math is counterintuitive—ten great engineers outperform hundred good ones, not by 10x but by 100x. Great engineers attract more great engineers. Average engineers attract more average engineers. Choose your trajectory early.

Lesson 10: Being Indian is Disadvantage and Advantage International customers initially dismissed Tejas for being Indian. But Indian conditions—infrastructure chaos, price sensitivity, extreme diversity—created products that worked anywhere. What doesn't kill you in India makes you globally competitive. The key is converting perceived weakness into demonstrable strength.

The playbook isn't universally applicable. It requires founders willing to defer gratification for decades, investors who measure returns in strategic value not just financial multiples, and teams that find meaning in building something larger than themselves. But for those rare combinations, the Tejas playbook offers a path from startup to strategic asset.

X. Bear vs. Bull Case & Competitive Analysis

The equity research analyst stares at her Tejas Networks model. The numbers tell two completely different stories depending on assumptions. She titles her note: "Tejas Networks: National Champion or Value Trap?" The bull and bear cases are equally compelling.

Bear Case: The Structural Headwinds

Global competition from established giants remains formidable. Ericsson has 57,000 employees and $27 billion in revenue. Nokia runs 92 R&D centers worldwide. Huawei, despite sanctions, still invests $22 billion annually in R&D—more than Tejas's entire market cap. These giants have decades-deep relationships, proven track records at scale, and financial resources to subsidize deals that Tejas cannot match.

Technology disruption risks loom large. Open RAN promises to commoditize radio access networks, reducing differentiation to software running on white-box hardware. Cloud-native solutions from hyperscalers like AWS and Azure are moving up the stack, potentially obviating traditional telecom equipment. Starlink and satellite constellations might leapfrog terrestrial networks entirely. Is Tejas fighting yesterday's war?

The company has a low return on equity of 5.25% over last 3 years and high debtors of 182 days. These metrics suggest operational inefficiencies and working capital stress. Government contracts, while strategic, come with payment delays that strain cash flows. The dependency on large, lumpy contracts creates volatile quarterly results that markets hate.

Dependency on government contracts is a double-edged sword. Net profit fell by more than 40% sequentially, reflecting margin pressures. Tejas Networks is experiencing a working capital crunch with trade receivables surging to Rs 47 billion and inventory levels climbing to Rs 31.2 billion. Change in government priorities, budget constraints, or political shifts could devastate order books. The BSNL success might be unrepeatable—a one-time windfall rather than sustainable competitive advantage.

Bull Case: The Transformation Story

Market cap of ₹9,735 crore with revenue of ₹7,562 crore suggests reasonable valuations for a high-growth technology company. The Tata Group backing provides not just capital but credibility, relationships, and synergies that independent competitors cannot match. This isn't just financial investment—it's strategic commitment from India's most respected conglomerate.

India's push for telecom self-reliance is secular, not cyclical. The government's PLI schemes, security concerns about Chinese equipment, and Digital India initiatives create a multi-decade tailwind. Tejas isn't just benefiting from protectionism—they're building capabilities that align with national strategic priorities.

5G rollout and fiber expansion opportunities are massive. India has 1.2 billion mobile subscribers but only 30 million fiber connections. The 5G rollout is expected to require $70 billion in infrastructure investment. Even capturing 10% of this opportunity would transform Tejas's financials.

The company reported Q3 FY25 revenue of Rs 26 billion, an impressive 4.7x jump year-over-year. Despite margin pressures, the scale achievement demonstrates execution capabilities. The PLI incentive of Rs 123 crore for FY24 provides additional cushion for R&D investments.

Competitive Positioning: The Reality Check

Against Ericsson and Nokia, Tejas cannot compete on global scale or R&D spending. But in specific segments—rural broadband, government networks, tropical deployments—Tejas has demonstrated superior products and service. The strategy isn't to beat giants everywhere but to dominate specific niches.

Versus Chinese competitors, geopolitical tailwinds provide temporary advantage. But Chinese companies are adapting through local partnerships, technology transfers, and price aggression. The window for building sustainable differentiation is narrow.

Compared to other Indian players, Tejas has first-mover advantages, proven scale, and Tata backing that creates significant barriers to entry. But new entrants backed by Reliance or Adani could change dynamics quickly.

The Verdict: Execution Will Determine Destiny

The bear case assumes Tejas remains a subscale player in a consolidating industry. The bull case assumes successful transformation into a global technology leader. Reality will likely be messier—periods of spectacular growth interrupted by painful adjustments, strategic wins offset by competitive losses.

The key variables to watch: International revenue growth (proving global competitiveness), R&D productivity (patents to products conversion), working capital management (collection efficiency), and market share in 5G (validating technology leadership). While the company boasts a strong order book of Rs 26.8 billion, managing financial pressures effectively will be crucial for sustained profitability.

For investors, Tejas represents a complex bet on multiple themes: India's technological ambitions, infrastructure modernization, geopolitical realignment, and the Tata Group's strategic vision. It's not for the faint-hearted or short-term oriented. But for those who believe in India's deep-tech potential, Tejas offers one of the few pure plays available.

XI. Epilogue & Future Outlook

Mumbai, 2030. The telecommunications minister inaugurates India's first 6G trial network. The equipment powering it? Designed and manufactured entirely in India. The vendor? A consortium led by Tejas Networks, now a $10 billion company and India's first global telecom equipment champion. Science fiction? Perhaps. But no more fantastical than a Bangalore startup competing with Ericsson would have seemed in 2000.

India's telecom equipment manufacturing ambitions have evolved from import substitution to global leadership aspirations. The government's vision of making India a global hub for telecom equipment manufacturing, backed by $10 billion in PLI incentives, isn't just industrial policy—it's strategic positioning for a world where digital infrastructure equals national power.

5G/6G technology development prospects position Tejas uniquely. While 5G is about faster speeds, 6G will be about intelligent networks—AI-native, quantum-secure, satellite-integrated. Tejas's early investments in these technologies, combined with India's software prowess, could create unexpected advantages. When networks become software-defined, India's 5 million developers become strategic assets.

Global expansion opportunities are materializing in unexpected places. African countries, wary of Chinese debt traps, are considering Indian alternatives. Latin American operators, facing US-China technology cold war pressures, want neutral vendors. Southeast Asian nations, sharing India's tropical challenges, find Tejas equipment uniquely suited. The addressable market isn't just India's $10 billion but global emerging markets worth $100 billion.

The larger story of Indian deep-tech companies is still being written. Tejas proves that India can build complex hardware, compete globally, and create intellectual property. But one swallow doesn't make a summer. India needs dozens of Tejas-like companies across semiconductors, advanced materials, quantum computing, and biotechnology. The playbook exists; the question is whether India has enough patient capital and persistent founders to replicate it.

Key takeaways for founders and investors crystallize around time horizons and strategic thinking. Building deep-tech companies requires decade-long commitments, billions in patient capital, and tolerance for prolonged losses. But the payoffs—strategic autonomy, technology leadership, ecosystem creation—transcend financial returns. For founders, the message is clear: if you're building hardware in India, think in decades, not quarters. For investors: if you're funding deep-tech, measure success in capability building, not just IRR.

The Tejas story ultimately isn't about one company's success. It's about possibility—the possibility that emerging markets can build world-class technology companies, that hardware can be profitable, that patient capital can create strategic assets. In a world increasingly defined by technology sovereignty, companies like Tejas aren't just business successes; they're national necessities.

As we look toward 2030, several questions will define Tejas's trajectory: Can it maintain innovation velocity under corporate ownership? Will international expansion succeed against entrenched competitors? Can India create a supporting ecosystem of component suppliers and complementary technologies? Will the next technology disruption—quantum, satellite, or something unforeseen—obsolete current investments?

The answers remain uncertain. But what's clear is that Tejas Networks has already achieved something remarkable: proving that an Indian company can compete in the most technology-intensive, capital-heavy, relationship-driven industry in the world. Whether that's the beginning of India's deep-tech revolution or a glorious exception remains to be seen.

For now, in research labs from Bangalore to Boston, engineers are designing networks that will carry humanity's digital future. And increasingly, those engineers are Indian, those designs are indigenous, and those networks are powered by equipment that says "Made in India" with pride, not apology. That transformation—from impossible to inevitable—might be Tejas Networks's greatest contribution. The products will evolve, the technology will change, the leadership will transition. But the belief that India can build anything, compete with anyone, and lead in technology? That's permanent. And that might be worth more than any financial valuation.

[Note: This analysis is based on publicly available information. Any forward-looking statements are speculative. Investors should conduct their own due diligence.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube