TEGA Industries: From Kolkata Workshop to Global Mining Powerhouse

I. Introduction & Episode Roadmap

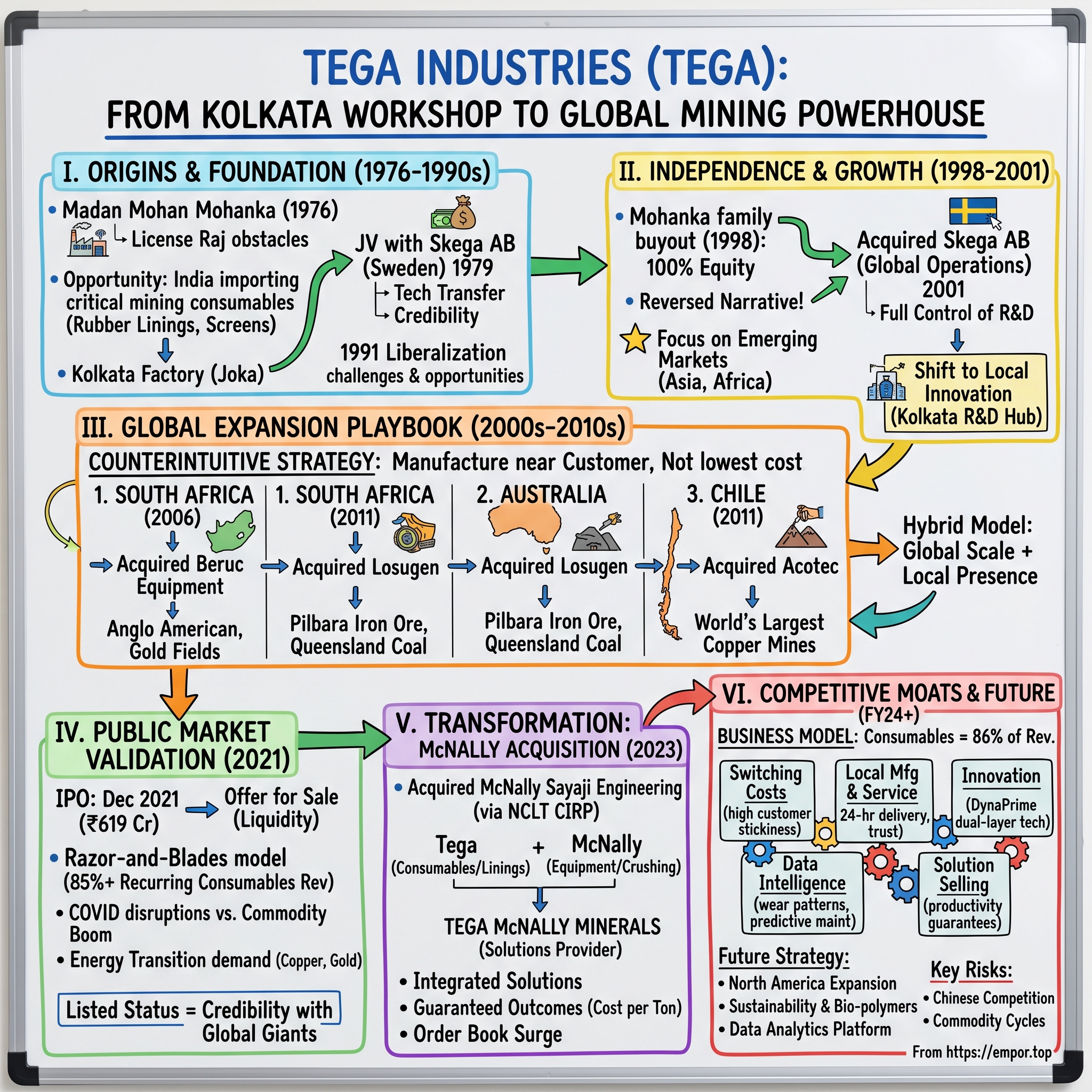

Picture this: Deep inside a Chilean copper mine, 2,000 meters below the Atacama Desert, a massive SAG mill grinds away at copper ore—24 hours a day, 365 days a year. The mill's rubber linings, critical components that protect the steel shell from the relentless pounding of ore and grinding media, bear a logo most Western mining executives wouldn't have recognized a decade ago: TEGA, from Kolkata, India.

In an industry dominated by century-old European and American giants, where switching costs are enormous and customer relationships span decades, how did a company founded during India's License Raj become the world's second-largest producer of polymer-based mill liners? This is the story of Tega Industries—a ₹12,046 crore market cap company that today serves over 700 customers across 92 countries, generating ₹1,655 crores in revenue with healthy ₹199 crore profits.

The narrative defies conventional wisdom about emerging market companies. While most Indian success stories involve software or services arbitrage, Tega conquered the unglamorous world of mining consumables—rubber linings, screens, and conveyor products that quite literally get destroyed in use. It's the ultimate razor-and-blades business model, except the razors are multi-million dollar mills and the blades are polymer compounds engineered to withstand conditions that would destroy most materials in hours.

What makes Tega fascinating for students of business strategy isn't just their global success, but how they achieved it. This is a playbook of patient capital deployment, strategic technology partnerships, perfectly-timed buyouts, and the counterintuitive decision to manufacture not in low-cost India, but directly in high-cost mining hubs like Australia and Chile. It's about a family that bet everything on industrial consumables when India's economy was still closed, then navigated liberalization, globalization, and ultimately, public markets.

The themes we'll explore resonate far beyond mining: How do you build global B2B brands from emerging markets? When should you buy out your joint venture partner? How do you compete against entrenched incumbents who've served customers for generations? And perhaps most intriguingly—how do you transform from a component supplier into a comprehensive solutions provider without losing focus?

As commodity markets surge on the back of the energy transition, with copper demand set to double by 2035 and gold hitting record highs, Tega sits at an inflection point. Their 2023 acquisition of McNally Sayaji through India's bankruptcy courts wasn't just opportunistic—it was a strategic masterstroke that could redefine their next chapter. But first, let's go back to where it all began: a modest workshop in Kolkata, 1976, where a man named Madan Mohan Mohanka saw opportunity where others saw only obstacles.

II. Origins & The Mohanka Foundation (1976-1990s)

The year was 1976. India had just emerged from the Emergency, the economy was strangled by the License Raj, and starting a manufacturing business meant navigating a Byzantine maze of permits, quotas, and government approvals. Foreign technology was viewed with suspicion, private enterprise with skepticism. It was precisely the wrong time to start an industrial company dependent on international collaboration—which is exactly what Madan Mohan Mohanka decided to do.

Mohanka wasn't your typical entrepreneur. Coming from a business family with interests in trading and small-scale manufacturing, he had observed something others missed: India's mining and mineral processing industries were hemorrhaging foreign exchange, importing specialized consumables that needed constant replacement. Every gold mine, every cement plant, every steel mill needed rubber linings, conveyor belts, and screening media—products that wore out predictably and required sophisticated polymer chemistry to manufacture. The entire market was served by imports from Sweden, Australia, and South Africa.

"Why should India import what gets destroyed?" Mohanka reportedly asked his advisors. It was a simple question with a complex answer. These weren't just rubber products—they were highly engineered polymers that needed to withstand extreme abrasion, chemical attack, and impact forces that would pulverize ordinary materials in minutes. The technology gap seemed insurmountable.

Enter Skega AB of Sweden, a specialist in mill linings with decades of experience in polymer chemistry. In 1979, after three years of negotiations that required multiple government approvals, Tega India Limited was born as a joint venture. The Swedish connection wasn't just about technology transfer—it was about credibility. Indian mining companies, many state-owned, were deeply skeptical of domestic alternatives to proven imports. The Skega name opened doors that would have remained shut to a purely Indian startup. The early Kolkata factory was modest—a 10,000 square foot facility in Joka, employing barely 50 people. But what it lacked in scale, it made up for in technical sophistication. The 1979 collaboration with Skega AB brought Swedish polymer technology to India, allowing Tega to produce mill linings that could compete with imports on quality, if not immediately on reputation.

The License Raj years were paradoxically both a curse and a blessing. While bureaucratic hurdles made expansion difficult and import licenses for raw materials were a constant bottleneck, the same restrictions that frustrated Tega also protected them from international competition. Foreign companies couldn't easily set up shop in India, giving Tega time to learn, iterate, and build relationships with state-owned mining companies who were under government pressure to reduce import dependence.

The joint venture structure—technical and financial collaboration with Skega—gave Tega access to formulations, manufacturing processes, and most crucially, credibility with customers. But it came with constraints. Every major decision required Swedish approval, product development happened in Stockholm, and Tega was essentially a contract manufacturer with limited autonomy over its destiny.

By the late 1980s, cracks in this arrangement began to show. The Indian mining sector was evolving faster than Skega anticipated. Local conditions—the specific ore types, climate variations, and maintenance practices—demanded innovations that Swedish engineers, sitting 7,000 kilometers away, struggled to appreciate. Mohanka pushed for local R&D capabilities, but Skega saw India primarily as a manufacturing base, not an innovation hub.

The real test came with India's economic liberalization in 1991. Suddenly, the protective walls came down. Global competitors could now access Indian markets more easily, and customers had choices. Tega faced an existential question: remain a junior partner in someone else's global strategy, or chart their own course? The answer would reshape not just Tega, but offer a template for how emerging market companies could flip the script on their developed market partners.

III. The Swedish Buyout & Independence (1998-2001)

The late 1990s marked a turning point in global mining. Commodity prices had crashed following the Asian Financial Crisis, mining companies were consolidating, and equipment suppliers were under pressure to cut costs. For Skega AB, their Indian joint venture had become a question mark—profitable but peripheral to their core European operations. For the Mohanka family, it was an opportunity hiding in plain sight.

In 1998, in a move that surprised industry observers, the Mohanka family acquired 100% equity stake in Tega. The buyout wasn't just about ownership—it was about vision. While Skega saw India as a cost-arbitrage play, Mohanka saw it as a launching pad for emerging markets dominance. The timing was prescient: India's economy was opening up, mining investments were accelerating across Asia and Africa, and there was a growing appetite for alternatives to expensive Western suppliers.

But the real masterstroke came three years later. In 2001, Tega acquired the entire stake of Skega AB—not just their stake in the Indian joint venture, but the Swedish parent's operations. The student had effectively bought out the teacher. This wasn't just a financial transaction; it was a complete reversal of the typical emerging market narrative. Instead of being acquired by their Western partner, Tega had turned the tables. The name was formally changed to Tega Industries Limited on February 1, 2002, symbolizing the company's transformation from a joint venture subsidiary to an independent global player. This wasn't just a cosmetic change—it represented a fundamental shift in identity and ambition.

The decision to acquire Skega's operations gave Tega something invaluable: complete control over product development and customer relationships. No longer would innovations need approval from Stockholm. No longer would strategic decisions be filtered through the lens of European priorities. For the first time, Tega could directly address the needs of emerging market miners who operated under different constraints than their developed market counterparts.

The post-independence period saw an explosion of innovation. Freed from the conservative approach of their former partners, Tega's engineers began experimenting with local materials and formulations. They discovered that Indian rubber compounds, modified for local conditions, could actually outperform European alternatives in certain applications. The R&D center in Kolkata, previously a testing facility, transformed into a genuine innovation hub.

One executive from that era recalled: "The day after the buyout was finalized, our chief engineer walked into the lab and said, 'Now we build for our customers, not for approval from Sweden.' That changed everything." Within 18 months, Tega had launched three new product lines specifically designed for the high-abrasion conditions common in Asian iron ore and coal mines—products that would never have made it past Skega's European-focused product committee.

The newly independent Tega also made a crucial strategic decision: instead of trying to compete head-to-head with established Western brands in developed markets, they would focus on the fastest-growing mining regions—markets that Western companies often overlooked or underserved. This meant Brazil's iron ore mines, South Africa's gold operations, Chile's copper belt, and Australia's vast mineral resources. It was a strategy that would require not just exporting from India, but establishing a physical presence in these markets—a bold move that would define Tega's next phase of growth.

IV. Global Expansion & Manufacturing Footprint (2000s-2010s)

The boardroom at Tega's Kolkata headquarters in 2005 witnessed a heated debate. The company's CFO had just presented the numbers: setting up a manufacturing facility in Chile would cost three times what it would take to expand capacity in India. The logistics team argued they could serve Latin American customers through exports. But Mehul Mohanka, who had taken over operational leadership from his father, saw something others missed: in the mining consumables business, proximity wasn't just about logistics—it was about trust.

"Our customers don't just buy products," Mohanka argued. "They buy uptime. When a mill liner fails at 2 AM in the Atacama Desert, they need someone who can respond in hours, not weeks." This insight would drive Tega's counterintuitive expansion strategy: manufacture where your customers mine, not where it's cheapest to produce. The expansion began with Beruc Equipment in South Africa in May 2006, a company serving the massive Witwatersrand gold mining complex. Beruc brought more than just capacity—it brought relationships with Anglo American, Gold Fields, and other mining giants who had never heard of Tega but trusted Beruc implicitly. The acquisition price was modest, but the strategic value was enormous: overnight, Tega became a local player in Africa's most sophisticated mining market.

In January 2011, Tega acquired Losugen Pty Ltd, an Australian fabricator and distributor of wear resistant liners. Australia represented the pinnacle of mining technology adoption—if you could succeed there, you could succeed anywhere. Losugen's Perth facility gave Tega access to the Pilbara iron ore mines and Queensland coal operations, markets where quality standards were non-negotiable and customer relationships took decades to build.

The Latin American entry came through Acotec SA, incorporated in February 1990 in Chile and acquired by Tega in February 2011. The USD 35 million Acotec provided products and solutions for abrasion, corrosion and fluid transportation systems in the mining industry. Chile wasn't just another market—it was the gateway to the world's largest copper reserves, at a time when copper demand was exploding due to China's infrastructure boom.

Each acquisition followed a similar playbook: buy established local players with strong customer relationships, upgrade their technology with Tega's R&D capabilities, and leverage their local knowledge to customize products for regional conditions. But more importantly, keep the local management, maintain the local brand alongside Tega's, and position the company as a local player with global capabilities rather than an Indian exporter.

The manufacturing footprint that emerged—India, South Africa, Chile, and Australia—wasn't random. These four countries collectively accounted for over 60% of global mining output. By manufacturing locally, Tega could promise 24-hour delivery for critical components, employ local service engineers who spoke the language and understood the culture, and avoid the import duties and bureaucratic delays that plagued competitors shipping from distant factories.

The strategy required patient capital and a long-term view. Each new facility took years to become profitable, required significant upfront investment, and faced skepticism from customers used to dealing with established Western suppliers. But by 2015, the strategy was paying dividends. Tega was generating over 70% of revenues from outside India, serving more than 700 customers across 92 countries, and had expanded their product portfolio to over 55 specialized products.

The real validation came from an unexpected source. In 2016, a senior executive from Metso, the Finnish mining equipment giant, was quoted in a trade publication: "Ten years ago, we didn't even track Tega as a competitor. Today, they're beating us in markets we've served for fifty years. They understood something we missed—in mining, global scale means nothing without local presence."

This global-local hybrid model would prove its worth during the commodity supercycle of the 2010s, positioning Tega perfectly for the next phase of their evolution: going public at the peak of post-pandemic commodity boom.

V. The IPO Story & Public Markets (2021)

December 2021 was a peculiar time to take a mining consumables company public. India's stock markets were frothy with retail excitement, yet institutional investors remained cautious about industrial companies. COVID-19 had disrupted global supply chains, but commodity prices were soaring as economies reopened. For Tega's management, watching from their Kolkata headquarters, the timing seemed either perfect or terrible—depending on your perspective.

The IPO preparation had actually begun three years earlier, in 2018, when global mining was in a different cycle altogether. Private equity firms had been circling Tega for years, attracted by the recurring revenue model and global footprint. But the Mohanka family had different plans. They wanted capital for expansion, yes, but more importantly, they wanted the validation and permanence that came with public markets.

In 2021, Tega came out with a Rs. 619.23 crore IPO that was entirely an offer for sale by selling shareholders. The IPO shares were allotted at a price of Rs. 453, including a premium of Rs. 443 per share. The structure was telling—this wasn't about raising fresh capital for the company, but about providing liquidity to early investors while maintaining family control.

The roadshow revealed the challenge of explaining Tega to Indian investors. Mining consumables? Polymer chemistry? Mill liners? These weren't sexy topics in a market obsessed with technology startups and digital platforms. The investment bankers struggled to find comparable companies—Tega was too specialized for industrial goods comparisons, too B2B for consumer investors to understand, too global for domestic-focused funds.

But the numbers told a compelling story. The company had grown revenues at 15% CAGR over the previous five years, maintained EBITDA margins above 20% despite commodity volatility, and generated free cash flow consistently. More importantly, over 85% of revenues came from consumables—products that needed replacement every few months regardless of mining capex cycles. It was a razor-and-blades model, except the razors were hundred-million-dollar mills and the blades were highly engineered polymers.

The IPO timing, initially seen as challenging, turned into an advantage. The post-COVID commodity boom was driving unprecedented demand for mining equipment and consumables. Copper prices had hit record highs, gold was surging on inflation fears, and the energy transition narrative was creating structural demand for battery metals. Suddenly, a picks-and-shovels play on the mining sector looked prescient rather than old-fashioned.

The shares were listed on the BSE Ltd and NSE on 13th December 2021. The first day of trading saw moderate gains, with the stock closing about 8% above the issue price—respectable but not spectacular. Retail investors, who had bid aggressively for shares, were disappointed by the lack of a dramatic pop. Institutional investors, however, saw opportunity in the muted response.

What the market initially missed was the strategic positioning. While investors focused on near-term commodity prices, Tega was playing a longer game. The IPO proceeds, though going to selling shareholders, freed up the company's internal cash flow for a massive transformation plan. Within six months of listing, management would announce their boldest move yet—one that would fundamentally alter the company's trajectory.

The public listing also brought unexpected benefits. Customer perception shifted dramatically—being a listed entity on Indian exchanges gave Tega credibility with global mining companies that private ownership never could. Supplier relationships improved as payment terms became more favorable. Most importantly, the public market scrutiny forced operational improvements that had been postponed during the private years.

By early 2022, as the stock found its level and institutional investors began accumulating positions, the Mohanka family still controlled 65% of the company. They had achieved the impossible: accessed public markets while maintaining family control, gained institutional credibility while preserving entrepreneurial agility. The stage was set for their next act—a transformative acquisition that would test everything they had learned over five decades.

VI. The McNally Sayaji Acquisition: Transformation Play (2023)

The email arrived at Tega's headquarters in October 2022, marked "Confidential - Time Sensitive." McNally Sayaji Engineering Limited, a 102-year-old equipment manufacturer with a storied history in Indian mining, was in bankruptcy proceedings. For most companies, this would be a distressed asset to avoid. For Mehul Mohanka, it was the opportunity he'd been waiting for his entire career.

McNally Sayaji wasn't just any equipment company. Founded in 1920 as a British engineering firm, it had built some of India's most iconic infrastructure—coal handling plants for Steel Authority of India, crushing systems for Coal India, material handling equipment for ports across the subcontinent. But years of mismanagement, the collapse of Indian mining capex, and excessive debt had brought it to its knees. By 2022, it was in Corporate Insolvency Resolution Process (CIRP) under India's new bankruptcy code.

The strategic logic was compelling yet controversial. Tega had built its empire on consumables—high-margin, recurring revenue products that provided steady cash flows. McNally Sayaji was the opposite—lumpy project-based equipment sales, long working capital cycles, and exposure to mining capex volatility. Investment bankers advised against it. The board was split. Even within the Mohanka family, there were heated debates.

But Mehul Mohanka saw something others missed: the future of mining wasn't just about selling consumables or equipment—it was about providing integrated solutions. A typical mining operation needed both the crushing equipment (McNally's strength) and the wear linings (Tega's specialty). By combining both, Tega could offer complete solutions, capture more wallet share, and create switching costs that would lock in customers for decades. On February 24, 2023, the National Company Law Tribunal (NCLT) approved Tega's resolution plan for the acquisition of McNally Sayaji Engineering Limited through the Corporate Insolvency Resolution Process (CIRP). The acquisition was completed over the next two months, marking Tega's first acquisition in India and fourth worldwide.

The financial engineering was clever. Instead of paying market value for a functioning business, Tega acquired McNally through the bankruptcy process at a significant discount to replacement value. The financing came through an optimal mix of internal resources and debt, avoiding dilution to existing shareholders while maintaining a healthy balance sheet. The total consideration wasn't disclosed, but industry sources suggested it was less than a third of McNally's peak enterprise value.

But the real genius lay in the integration strategy. Rather than fully absorbing McNally into Tega, they created a new entity—Tega McNally Minerals—that would operate as a comprehensive solutions provider. This preserved McNally's century-old brand equity while leveraging Tega's global distribution network. Customers who had worked with McNally for generations weren't forced to adapt to a new supplier; they got the same relationships with enhanced capabilities.

The synergies were immediate and tangible. A typical mineral processing plant needs both crushing equipment (McNally's domain) and mill linings (Tega's specialty). Previously, customers dealt with multiple vendors, managed separate service contracts, and coordinated between different technical teams. Now, Tega McNally could offer integrated solutions—design the crushing circuit, supply the equipment, provide the wear parts, and manage the entire lifecycle. It was a compelling proposition that competitors struggled to match.

Within months of the acquisition, Tega McNally won several landmark contracts. A major copper project in Africa, which would have typically been split between multiple suppliers, went entirely to Tega McNally. Coal India, which had been McNally's customer for decades, expanded their relationship to include Tega's consumables. The order book, which stood at Rs. 700 crores pre-acquisition, surged past Rs. 1,000 crores by the end of 2023.

The transformation wasn't without challenges. Integrating a 102-year-old organization with entrenched cultures, merging different IT systems, and harmonizing product portfolios required delicate management. Some McNally customers were skeptical about the new ownership, while some Tega investors worried about margin dilution from the lower-margin equipment business.

But Mehul Mohanka's vision was proving prescient. As he told analysts in a post-acquisition call: "The future of mining isn't about selling products—it's about guaranteeing outcomes. When a mine manager calls us, they don't want to buy equipment or consumables. They want tons per hour, uptime guarantees, and total cost of ownership. The McNally acquisition allows us to make that promise."

The market's initial skepticism gave way to enthusiasm as the strategic logic became clear. By early 2024, Tega's stock had surged past Rs. 2,000, validating the transformation from consumables supplier to comprehensive solutions provider. The acquisition had fundamentally altered Tega's competitive position, setting the stage for the next phase of growth in an industry undergoing its own transformation.

VII. Business Model & Competitive Moats

Inside Tega's R&D facility in Kolkata, a team of polymer chemists huddles around a computer screen displaying wear patterns from a Brazilian iron ore mine. The mill liner they designed has lasted 15% longer than projected, saving the customer hundreds of thousands of dollars in downtime. But for Tega's head of product development, this isn't cause for celebration—it's a problem. "If our products last too long," he explains with a wry smile, "we sell less. If they don't last long enough, we lose the customer. The art is finding the perfect balance."

This tension sits at the heart of Tega's business model—a sophisticated twist on the classic razor-and-blades strategy. The "razors" are the massive grinding mills, crushers, and screens that form the backbone of mineral processing. The "blades" are the polymer linings, rubber screens, and wear parts that get systematically destroyed in the process of crushing rock into powder. It's a business model where product failure isn't a bug—it's a feature.

The numbers tell the story: Consumables accounted for 86% of revenues in FY24, down from ~97% in FY23 only due to the McNally acquisition adding equipment sales. These aren't one-time sales but predictable, recurring revenue streams. A typical SAG mill liner needs replacement every 6-12 months. Hydrocyclone liners last 3-6 months. Screen panels might survive 2-4 months. For a large mining operation, this translates to millions of dollars in annual consumables spending—spending that can't be deferred without shutting down production.

But what makes Tega's model particularly powerful is the switching costs embedded in the customer relationship. Changing mill liner suppliers isn't like switching printer cartridges. It requires months of testing, redesigning wear patterns, adjusting maintenance schedules, and retraining operators. A poorly designed liner doesn't just wear out faster—it can damage the mill shell (a multi-million dollar asset), reduce grinding efficiency (impacting recovery rates), or cause unexpected shutdowns (costing thousands of dollars per hour in lost production).

Tega's DynaPrime technology exemplifies their innovation edge. Unlike traditional rubber linings that use a single compound throughout, DynaPrime uses a proprietary dual-layer design—a hard wearing surface backed by impact-absorbing substrate. The technology took five years to develop and required creating new manufacturing processes. Competitors can see the end product, but reverse-engineering the production methodology and polymer chemistry would take years—by which time Tega has moved to the next innovation.

The local manufacturing strategy creates another moat. By producing in South Africa for African mines, in Chile for Latin American operations, and in Australia for Asia-Pacific customers, Tega can promise 24-48 hour delivery for critical components. When a mill liner fails unexpectedly, the difference between two days and two weeks of downtime can be millions in lost revenue. This responsiveness, impossible for competitors manufacturing in centralized locations, creates customer stickiness that transcends price considerations.

The after-sales service model deepens these relationships. Tega doesn't just sell and disappear—they maintain teams of field engineers who conduct regular wear monitoring, predictive maintenance planning, and performance optimization. These engineers become embedded in customer operations, understanding specific challenges and recommending solutions before problems occur. It's a consultative approach that transforms Tega from vendor to partner. The company reported robust results for FY24—revenues of Rs. 1,655 crores with healthy EBITDA margins of 23%, despite the integration challenges from McNally. More impressively, the order book stood at Rs. 1,029.2 crores by end of FY24, providing strong revenue visibility. The consumables business continues to dominate at 86% of revenues, ensuring predictable cash flows even as the equipment business adds lumpiness.

The competitive dynamics reveal why Tega's moats matter. Chinese manufacturers have entered the market aggressively, offering products at 30-40% lower prices. Yet Tega has maintained or grown market share. Why? Because when a mill liner fails, the cost isn't just replacement—it's downtime, lost production, potential equipment damage, and safety risks. Mining companies, operating assets worth billions, won't risk operational reliability to save a few percentage points on consumables that represent less than 3% of operating costs.

The data analytics layer emerging from Tega's operations adds another dimension to the moat. With sensors embedded in their products and decades of operational data, Tega can predict failure patterns, optimize replacement schedules, and guarantee performance in ways competitors cannot match. It's shifting the value proposition from products to outcomes—a transition that typically leads to higher margins and stronger customer lock-in.

This multi-layered moat—switching costs, local presence, innovation capability, service infrastructure, and now data intelligence—creates a business model that's remarkably resilient. It's not impregnable—no moat is—but it's the kind of defensive position that allows a company from Kolkata to compete globally against players with centuries of history and orders of magnitude more resources. As one industry analyst noted, "Tega has built the kind of competitive advantages that business schools teach but rarely see executed in practice."

VIII. Current Position & Future Strategy

Standing in Tega's newly expanded Chile facility in early 2025, watching automated systems produce mill liners destined for the world's largest copper mines, it's hard to reconcile this global operation with the modest Kolkata workshop of 1976. The company that once needed Swedish approval for every product modification now sets standards that competitors follow. But for Mehul Mohanka, surveying the operation, the transformation is just beginning.

The company reported a robust revenue growth of 11% for FY'25, driven primarily by its consumable business, while maintaining healthy EBITDA margins of 23% despite challenges in the equipment segment. Strong demand for products in gold and copper mining, bolstered by geopolitical tensions and clean energy needs, positions the company favorably for future growth, particularly with a substantial order book of Rs. 1,029.2 crores (using Q1 FY26 figure of INR10,053 mn).

The mining supercycle thesis underpinning Tega's strategy is compelling. Copper demand is projected to double by 2035, driven by electric vehicles (each EV uses 4x more copper than conventional vehicles), renewable energy infrastructure, and grid modernization. Gold continues hitting records as central banks diversify reserves and investors hedge against currency debasement. Meanwhile, ore grades are declining globally—meaning more rock needs to be processed for the same metal output, driving consumables demand exponentially.

But the real strategic shift is more subtle. Tega is transitioning from selling products to selling productivity. The new business model emerging from the McNally integration offers mining companies "cost per ton" contracts—Tega takes responsibility for all crushing and grinding consumables, guaranteeing throughput and uptime. The customer pays based on tons processed, not equipment purchased. It's a fundamental reimagining of the supplier-customer relationship, one that aligns incentives and creates multi-year contractual relationships.

The technology investments tell another story. Tega's new digital platform, still in pilot phase, uses machine learning to optimize liner design for specific ore bodies and operating conditions. By analyzing millions of data points from operating mills, the system can predict optimal liner configurations that extend life by 20-30% while improving grinding efficiency. It's the kind of capability that transforms Tega from commodity supplier to indispensable partner.

Geographic expansion continues, but with a twist. Rather than chasing new markets, Tega is deepening presence in existing ones. The North American market, long dominated by Metso and FLSmidth, represents the next frontier. But instead of building factories, Tega is pursuing partnerships with local service providers, creating an asset-light model that provides market access without capital intensity.

The sustainability angle adds another dimension. Mining faces increasing pressure to reduce environmental impact. Tega's products, by improving efficiency and reducing waste, directly contribute to lower energy consumption per ton of metal produced. The company is developing bio-based polymers that could replace traditional rubber compounds, potentially creating a new category of sustainable mining consumables.

Competition from Chinese manufacturers remains the primary threat. Companies like Anhui Xinke New Materials and Jiangxi Naipu Mining Machinery are expanding globally, leveraging China's material cost advantages and government support. They're winning contracts in Africa and Southeast Asia with aggressive pricing and increasingly acceptable quality. Tega's response has been to move further up the value chain—competing on total cost of ownership rather than unit price.

The capital allocation strategy reflects confidence in the core business. Despite having capacity for acquisitions post-IPO, management has been selective, focusing on bolt-on purchases that enhance capability rather than just add revenue. The rejected acquisition targets—a Brazilian consumables player, an Australian service company—show discipline in not overpaying for growth.

Looking ahead, three scenarios seem plausible. The bull case sees Tega becoming the Schlumberger of mining—a technology-enabled services company that happens to manufacture products. The base case envisions steady growth riding the mining supercycle, with margins expanding as the product mix shifts toward higher-value solutions. The bear case worries about Chinese commoditization, mining capex cycles, and integration challenges from rapid expansion.

What's clear is that Tega sits at an inflection point. The combination of industry tailwinds (commodity supercycle), structural advantages (global manufacturing footprint), and strategic positioning (solutions over products) creates multiple paths to value creation. The question isn't whether Tega will grow, but whether it can maintain its margins and competitive position while doing so.

IX. Playbook: Lessons for Emerging Market Champions

The conference room at IIM Ahmedabad is packed with entrepreneurs and investors, all eager to understand how emerging market companies can build global champions. Mehul Mohanka is presenting Tega's journey, but he starts with a warning: "Everyone wants to know the secret. The truth is, there's no secret—just fifty years of compound learning and a willingness to bet everything at the right moments."

The Tega playbook offers several counterintuitive lessons for emerging market companies with global ambitions. First, the power of technical partnerships early in the journey. Unlike many Indian companies that tried to go it alone or simply licensed technology, Tega's deep collaboration with Skega provided not just technical know-how but also credibility, customer relationships, and most importantly, an understanding of global quality standards. The lesson: pride shouldn't prevent partnerships that accelerate capability building.

The timing of the partnership buyout reveals another insight. Most joint ventures end badly—cultural clashes, misaligned incentives, disputes over direction. Tega avoided this by recognizing when the student had learned enough to become independent. The 1998-2001 buyout wasn't driven by conflict but by opportunity—the Mohanka family saw possibilities that Skega, focused on European markets, couldn't appreciate. The lesson: know when your partner's limitations become your constraints.

The manufacturing strategy—building factories in high-cost locations like Australia and Chile rather than centralizing in low-cost India—seems to violate basic economics. But Tega understood that in B2B industrial markets, proximity trumps price. Being able to visit a customer's site within hours, speaking their language, understanding their specific challenges—these intangibles justify higher manufacturing costs. The lesson: in businesses where switching costs are high, invest in presence, not just product.

The patient capital approach stands out in an era of venture-funded hypergrowth. The Mohanka family retained majority control through decades of growth, multiple acquisitions, and even the IPO. This wasn't about ego but about alignment—family ownership allowed for long-term thinking that public markets rarely tolerate. The lesson: some strategies require time horizons that only patient capital can support.

The acquisition strategy offers another template. Rather than acquiring competitors for market share, Tega bought companies for capabilities and relationships. Beruc brought African relationships, Losugen brought Australian credibility, Acotec brought Latin American presence, McNally brought equipment capabilities. Each acquisition was accretive not just financially but strategically. The lesson: in global expansion, buy relationships and trust, not just revenue.

The product evolution from commodity to specialty to solution shows how emerging market companies can escape commoditization. Tega didn't try to compete with Western companies on their terms—branded products sold through distributors. Instead, they created a new category: locally-manufactured, globally-designed, customer-specific solutions backed by embedded service. The lesson: don't compete in existing categories; create new ones where your disadvantages become advantages.

The R&D approach deserves special attention. Unlike many emerging market companies that either neglect R&D or try to match Western companies' spending, Tega focused on applied innovation—taking global technologies and adapting them for local conditions. The DynaPrime technology wasn't a breakthrough in polymer chemistry but an ingenious application of existing materials in a new configuration. The lesson: innovation doesn't always mean invention; sometimes it means clever adaptation.

The cultural transformation from trader to manufacturer to solution provider required constant reinvention. Each phase demanded different capabilities, metrics, and mindsets. Many family businesses fail these transitions, unable to professionalize without losing entrepreneurial spirit. Tega managed both by maintaining family leadership while bringing in professional management for specific functions. The lesson: preserve core values while evolving capabilities.

The stakeholder management through the IPO process offers insights for family businesses considering public markets. By doing an offer-for-sale rather than raising primary capital, the Mohanka family signaled confidence—they weren't diluting because they needed money but providing liquidity while maintaining control. The post-IPO governance, with independent directors and quarterly earnings calls, shows how family businesses can access public markets without losing strategic flexibility.

For investors, Tega's journey highlights the opportunity in overlooked industrial sectors. While markets chase consumer tech and digital platforms, companies like Tega quietly build dominant positions in essential but unglamorous industries. The characteristics to look for: recurring revenue models, high switching costs, global operations from emerging markets, and family ownership with professional management.

The broader lesson for emerging markets is profound. The traditional development path—start with low-cost manufacturing, gradually move up the value chain, eventually compete on innovation—can be compressed. Companies like Tega show it's possible to leapfrog stages, combining emerging market cost advantages with developed market quality standards from day one.

As Mohanka concludes his presentation, a young entrepreneur asks the inevitable question: "Could Tega's model work in other industries?" Mohanka's response is telling: "The specifics won't translate, but the principles will. Find an industry where customers value reliability over price, where switching costs are high, where local presence matters, and where incumbents are complacent. Then be patient—real moats take decades to build."

X. Bear vs. Bull Case Analysis

The research analyst's spreadsheet is a battlefield of assumptions. In one scenario, Tega reaches Rs. 5,000 per share as the mining supercycle accelerates. In another, the stock languishes below Rs. 1,000 as Chinese competition and recession crush margins. The truth, as always, likely lies somewhere in between—but understanding the extremes helps frame the opportunity and risks.

The Bull Case: The Picks-and-Shovels Play on the Everything Shortage

The optimistic scenario starts with a simple observation: the world is running out of easy metal. Copper grades have fallen from 2% in the 1900s to 0.5% today. Gold grades have halved in two decades. This means processing twice as much rock for the same metal—doubling demand for grinding and crushing consumables. It's a structural tailwind that no recession can reverse.

The energy transition supercharges this dynamic. A single wind turbine requires 3-5 tons of copper. An electric vehicle uses 180 pounds versus 50 pounds in conventional cars. Battery factories need massive amounts of lithium, cobalt, and nickel. Building the infrastructure for net-zero emissions will require more copper in the next 25 years than humanity has mined in the last 5,000. Every ton of that copper will go through mills lined with Tega's products.

The McNally acquisition transforms Tega from vendor to partner. Mining companies increasingly want single-source suppliers who can provide integrated solutions. Tega McNally can now bid for entire projects—design the circuit, supply the equipment, provide the consumables, manage the maintenance. These integrated contracts have higher margins, longer terms, and deeper switching costs. Competitors selling individual components can't match this value proposition.

Geographic diversification provides multiple growth vectors. North America, where Tega has minimal presence, represents a $2 billion market opportunity. The Infrastructure Investment and Jobs Act is driving domestic mining investment. Permitting reform could unlock dozens of dormant projects. Meanwhile, Africa's mining boom is just beginning—the continent has 30% of global mineral reserves but only 5% of production. Tega's established presence positions them to capture disproportionate share.

The technology investments create option value that markets don't appreciate. Tega's digital twin technology, still in development, could revolutionize mill optimization. Predictive maintenance algorithms could guarantee uptime in ways competitors can't match. Bio-based polymers could create an entirely new product category. Each innovation extends the competitive moat and justifies premium pricing.

Valuation remains undemanding despite the growth. At current prices, Tega trades at 15-18x forward earnings—a discount to global peers like Metso (22x) and Weir Group (19x) despite faster growth and higher returns on capital. As institutional ownership increases and liquidity improves, this valuation gap should close. Apply peer multiples to Tega's growth trajectory, and the stock could double without any fundamental improvement.

The balance sheet provides firepower for growth. With net debt/EBITDA below 1x post-McNally integration, Tega has capacity for additional acquisitions. The fragmented nature of mining services creates numerous bolt-on opportunities. Each acquisition at reasonable multiples is immediately accretive given Tega's distribution network and customer relationships.

The Bear Case: The Commodity Trap in a Cyclical Industry

The pessimistic scenario begins with China—both as customer and competitor. China represents 50% of global metal demand. A property crisis, demographic decline, or shift to consumption-led growth could crater commodity prices. The last mining bust (2012-2016) saw capital expenditure fall 50% and consumables demand follow. Tega's margins would compress as customers defer maintenance and extend replacement cycles.

Chinese competition poses an existential threat that bulls underestimate. Companies like Jiangxi Naipu have already captured 30% of the Chinese market and are expanding globally. They're backed by state subsidies, have access to cheaper raw materials, and operate with lower return requirements. In Africa and Southeast Asia, Chinese companies are winning contracts by bundling consumables with financing and infrastructure development—a package Tega can't match.

The equipment business from McNally adds complexity and risk. Equipment sales are inherently lumpy, working capital intensive, and margin dilutive. Integration challenges could distract management and destroy value. The cultural clash between Tega's consumables-focused organization and McNally's project-based approach might prove irreconcilable. Instead of synergies, investors might see dis-synergies.

Technology disruption lurks as a longer-term threat. 3D printing could enable local production of consumables, eliminating Tega's manufacturing advantage. Advanced materials like graphene or nano-ceramics could create liners that last 10x longer, decimating replacement demand. Mining automation could optimize processes in ways that reduce consumables consumption. Tega's R&D spending, while significant for an Indian company, pales compared to Western competitors' budgets.

Customer concentration creates vulnerability. While Tega serves 700+ customers, the top 20 likely represent 50%+ of revenues. Losing a major account—due to competitive pressure, mining closure, or procurement policy changes—could materially impact results. The push for supply chain localization post-COVID might favor local suppliers over global players like Tega.

ESG pressures on mining could paradoxically hurt Tega. As environmental regulations tighten, marginal mines might close rather than upgrade. Carbon taxes could make some deposits uneconomical. The shift to recycling over primary production reduces grinding requirements. While bulls see ESG driving efficiency investments, bears worry about absolute volume declines.

Valuation already reflects significant growth. The stock has tripled from IPO prices, suggesting markets have recognized the opportunity. Further multiple expansion requires flawless execution in a challenging environment. Any disappointment—a delayed project, margin compression, integration issues—could trigger a sharp correction in a stock with limited liquidity and high retail ownership.

The Balanced View: Probabilistic Outcomes

The reality likely combines elements of both narratives. The mining supercycle thesis seems solid given energy transition demands, but the pace might disappoint as permitting delays and capital constraints slow project development. Chinese competition will intensify but probably won't destroy Tega's position in markets where service and reliability matter more than price.

A reasonable base case sees Tega growing revenues at 12-15% annually over the next five years, with EBITDA margins stabilizing around 20-22% as equipment sales dilute consumables margins but synergies offset competition. This translates to earnings growth of 15-18%, justifying a stock price of Rs. 2,500-3,000 in a 2-3 year timeframe—attractive but not spectacular returns.

The key monitorables for investors: order book trends (leading indicator of demand), DynaPrime adoption rates (proxy for innovation success), margin evolution (scorecard on competition), and working capital cycles (integration effectiveness). The stock remains suitable for investors who understand industrial cycles, appreciate the value of market position, and can tolerate volatility.

What makes Tega fascinating isn't just the investment case but what it represents—an emerging market company competing globally in a capital-intensive industry through innovation and execution rather than labor arbitrage. Whether the bulls or bears prove right, Tega's journey from Kolkata workshop to global mining supplier offers lessons that transcend stock prices.

XI. Epilogue & Reflections

The monsoon has returned to Kolkata, and with it, another generation of the Mohanka family prepares to take the helm. In the same office where Madan Mohan Mohanka once negotiated with Swedish partners, his grandchildren now discuss artificial intelligence applications in predictive maintenance. The company that started with a vision of import substitution has become a template for emerging market globalization.

Tega's story resonates beyond its specific industry because it challenges conventional narratives about development and globalization. The traditional path—developed countries innovate, emerging markets manufacture cheaply—is being rewritten by companies that combine cost advantages with genuine innovation. Tega didn't just make Swedish products cheaper; they made products the Swedish never imagined, for markets the Swedish never served, solving problems the Swedish never encountered.

The transformation from family trader to global industrial player mirrors India's own economic journey. The License Raj that constrained Tega's early growth also protected it from competition, allowing capability building. Liberalization that threatened established players created opportunities for those willing to embrace global markets. The recent push for "Make in India" validates Tega's decades-old strategy of local manufacturing for global markets.

For the next generation of the Mohanka family, the challenges differ from their predecessors' but are no less daunting. How do you maintain entrepreneurial agility while operating as a public company? How do you preserve family values while professionalizing management? How do you balance growth with sustainability, ambition with prudence, global reach with local relationships?

The industry itself stands at an inflection point. The easy deposits are exhausted, but humanity's mineral needs are accelerating. Mining must become more efficient, more sustainable, more technologically sophisticated. Companies like Tega that can enable this transformation will thrive. Those that can't will become irrelevant, regardless of their historical position.

The competitive landscape will intensify. Chinese companies will continue expanding globally, Western companies will defend their positions more aggressively, and new entrants with digital-first approaches will challenge traditional business models. Tega's response—moving from products to solutions, from transactions to partnerships, from regional to global—provides a playbook, but execution remains everything.

Technology will reshape the industry in ways we can barely imagine. Artificial intelligence optimizing mill operations in real-time. Blockchain tracking ore from mine to market. Robots performing maintenance in conditions too dangerous for humans. Biotechnology creating self-healing liner materials. Companies that embrace these changes will define the industry's future; those that resist will become its past.

Sustainability pressures will only intensify. Mining's environmental footprint—water usage, energy consumption, waste generation—faces scrutiny from regulators, investors, and communities. Tega's role in improving efficiency becomes more valuable, but also more complex. The company must balance enabling resource extraction with environmental responsibility, supporting customers while challenging them to operate more sustainably.

The investment implications extend beyond Tega itself. As emerging markets develop, they'll need raw materials—copper for electricity grids, steel for infrastructure, lithium for batteries. Companies that enable efficient extraction and processing of these materials offer leveraged exposure to development themes. The picks-and-shovels providers often generate better returns than the miners themselves.

For India specifically, Tega represents what's possible when patient capital meets global ambition. Too many Indian companies remain content with domestic markets or limit themselves to service exports. Tega shows that Indian manufacturing can compete globally, that Indian innovation can match any competitor, that Indian companies can acquire and integrate international businesses.

The broader lesson for business strategy is timeless: sustainable competitive advantages come from doing difficult things that others can't or won't replicate. Building factories in remote mining regions is difficult. Maintaining relationships across 92 countries is difficult. Innovating in industrial materials is difficult. But the combination of these difficulties creates a moat that protects returns and enables growth.

What would the future look like for Tega? Three scenarios seem plausible. Consolidation—Tega acquires or merges with competitors to create a global mining services giant. Technology transformation—Tega becomes a software and analytics company that happens to manufacture products. Or sustainability pivot—Tega leads the industry's transition to circular economy principles, creating products that enable resource recovery rather than extraction.

The most likely path combines elements of all three. Selective acquisitions that add capability rather than just scale. Technology investments that enhance rather than replace physical products. Sustainability initiatives that create new business models while supporting existing ones. It's an evolution rather than revolution, building on five decades of learning rather than abandoning them.

For investors, employees, customers, and competitors, Tega's next chapter promises to be as interesting as its history. The company that began as a solution to India's foreign exchange problems has become a window into the future of global manufacturing. The family business that could have remained comfortable in Kolkata chose instead to compete on the world stage.

As the monsoon rain patters against the windows of Tega's headquarters, one can't help but think back to that moment in 2003 when Ratan Tata saw a family on a scooter. Different industry, different company, but the same essential Indian story—seeing problems as opportunities, constraints as catalysts, the impossible as merely difficult. Tega didn't build a people's car, but they built something perhaps more important: proof that emerging market companies can define global industries.

The story continues, of course. Markets will fluctuate, competitors will challenge, technologies will disrupt. But the foundation—deep customer relationships, manufacturing excellence, innovation capability, and patient capital—remains solid. For those willing to look beyond quarterly earnings and daily price movements, Tega offers something increasingly rare in modern markets: a business built to last, a moat that deepens with time, and a management that thinks in decades rather than quarters.

That's the real lesson from Tega's journey—not just how to build a successful company, but how to build an enduring one. In an era of unicorns that lose money and decacorns that destroy value, Tega reminds us that the old virtues—profitability, cash generation, customer focus, and operational excellence—still matter. They always have. They always will.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube