Techno Electric & Engineering Company: From Power Infrastructure Pioneer to Digital Transformation

I. Introduction & Episode Roadmap

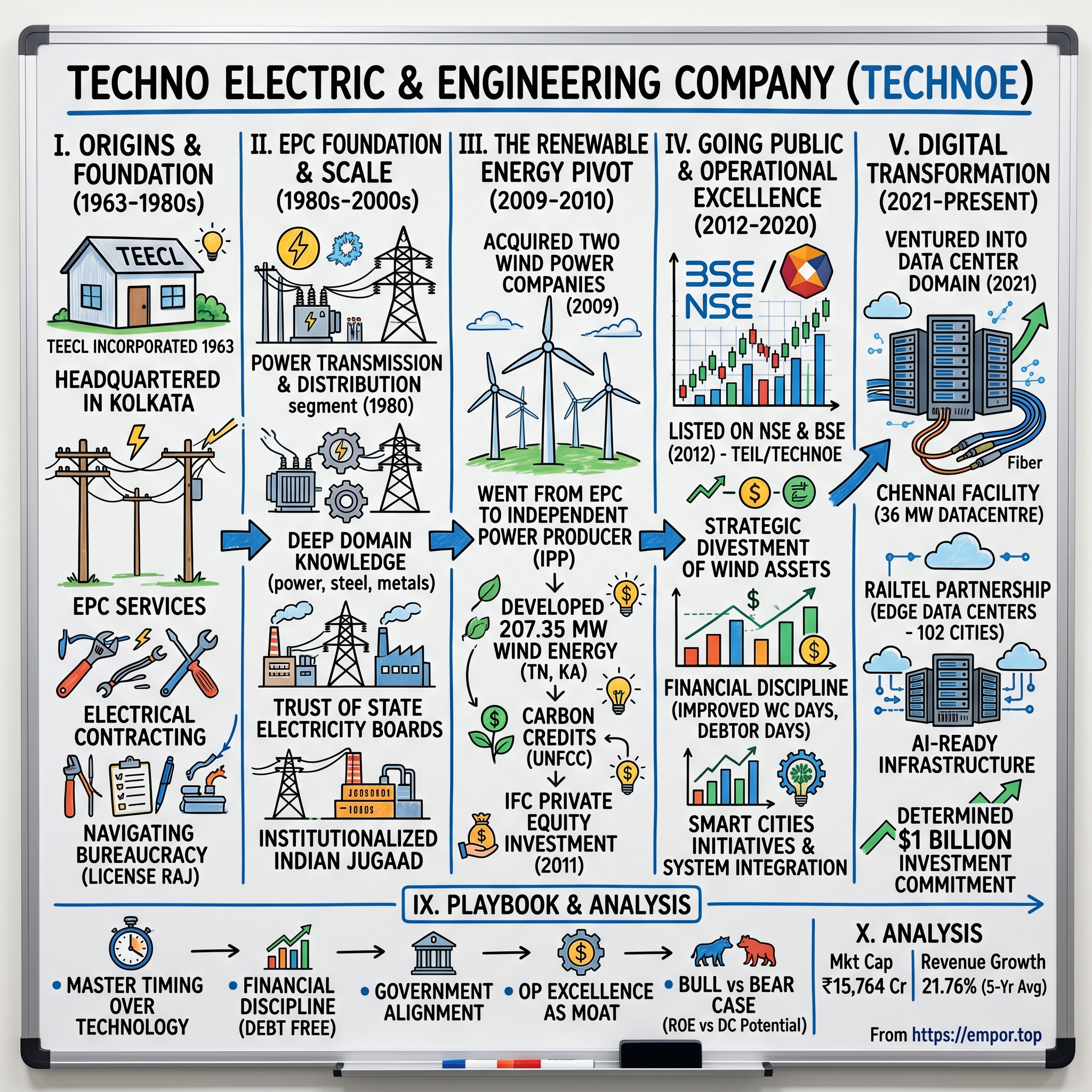

Picture this: It's 1963, and while the world watches the space race unfold and the Beatles begin their global domination, in the bustling city of Kolkata, a quiet revolution begins. A group of engineers establish what would become Techno Electric & Engineering Company, incorporated in 1963 and headquartered in Kolkata. They couldn't have imagined that six decades later, their company would command a market capitalization of ₹15,764 Crore and stand at the forefront of India's digital infrastructure boom.

TEECL is one of India's most important power-infrastructure companies, but that barely scratches the surface of this transformation story. How does a traditional electrical engineering contractor, born in the License Raj era, reinvent itself multiple times—first as a renewable energy pioneer, then as a public market darling, and now as a data center powerhouse?

The answer lies in a series of calculated pivots that read like a masterclass in strategic timing. This is the story of riding India's infrastructure waves at precisely the right moments: entering power transmission when the nation desperately needed grid expansion, pivoting to wind energy just as India embraced renewables, and now betting big on data centers as the country undergoes its digital metamorphosis.

Today's journey takes us through the corridors of power—literally—from state electricity boards to wind farms in Tamil Nadu, from BSE listing bells to hyperscale data centers. It's a story about building the invisible backbone of modern India, one substation, one turbine, one server rack at a time. As we'll discover, Techno Electric's real genius wasn't just in engineering excellence—it was in reading the tea leaves of India's development trajectory and positioning itself ahead of each curve.

II. Origins & Foundation Era (1963–1980s)

The monsoon of 1963 brought more than just rain to Kolkata. As water pooled in the streets of what was then Calcutta, a small group of electrical engineers huddled in a modest office, drafting the incorporation papers for what would become Techno Electric & Engineering Company. India was just 16 years old as an independent nation, Jawaharlal Nehru's vision of industrial self-reliance was taking shape, and the country desperately needed builders—not just of factories and dams, but of the electrical infrastructure that would power them.

TEECL was established with a mission to provide comprehensive Engineering, Procurement and Construction (EPC) services to core sector industries in India. But in those early years, "comprehensive" meant something far more modest than today's mega-projects. The founders started with basic electrical contracting work—wiring industrial facilities, maintaining power equipment, the unglamorous but essential work that kept India's nascent industries running.

The 1960s and 70s were a peculiar time to start an infrastructure company in India. The License Raj meant that every piece of imported equipment needed government approval, every expansion required permits, and building relationships with bureaucrats was as important as engineering expertise. Yet this constraint became TEECL's first competitive advantage. While multinational competitors struggled with red tape, the Kolkata-based firm learned to navigate the labyrinthine corridors of Indian bureaucracy with the finesse of seasoned insiders.

Initially specializing in electrical engineering, Techno Electric diversified its operations over the years to include sectors such as renewable energy, power system engineering, and infrastructure development. But this diversification would come later. The 1970s were about survival and establishing credibility. The company took on projects that larger firms ignored—rural electrification initiatives, small industrial substations, maintenance contracts that required more sweat than sophistication.

By 1980, a crucial inflection point arrived. It entered the power transmission and distribution segment in 1980. This wasn't just a business expansion; it was a strategic bet on India's future. The country's power deficit was becoming a crisis. Industries faced daily power cuts, agricultural pumps ran dry, and the gap between electricity generation and transmission capacity was widening dangerously.

The timing was prescient. India was about to embark on massive power sector expansion in the 1980s, and TEECL had positioned itself perfectly. They had spent nearly two decades building the technical expertise, understanding Indian conditions—from scorching Rajasthan summers to humid Bengal monsoons—and most importantly, earning the trust of state electricity boards who would become their biggest clients.

What set TEECL apart in these formative years wasn't cutting-edge technology or massive capital—it was their deep understanding of Indian realities. They knew how to make equipment work in 45-degree heat with irregular power supply. They understood that project execution in Bihar was different from Tamil Nadu. They built redundancy into their designs because they knew maintenance schedules would slip. This wasn't world-class engineering by global standards, but it was exactly what India needed.

III. The EPC Foundation Years (1980s–2000s)

The year 1980 marked more than just a new decade for Techno Electric—it signaled the company's evolution from a regional contractor to a serious player in India's power infrastructure story. As the company entered the transmission and distribution segment, India itself was transforming. The country's installed power capacity was set to double in the coming decade, and someone had to build the arteries that would carry this electricity from generation plants to factories and homes.

TEECL's rich domain knowledge makes it possible to service the challenging EPC needs of the power, steel, fertilizer, metals and petrochemicals sectors, among others. But "rich domain knowledge" is corporate-speak for something more visceral—this was a company that had engineers who could troubleshoot a substation failure at 2 AM in a remote mining town, who understood why equipment that worked perfectly in European conditions would fail in Indian summers, who knew which vendors could deliver on time and which ones required constant supervision.

The 1980s and 90s were the crucible years. TEECL wasn't just building infrastructure; it was building a reputation. Each successfully commissioned substation, each on-time project delivery in an industry notorious for delays, added another layer to their credibility armor. State electricity boards—notoriously risk-averse and procedurally byzantine—began to trust this Kolkata company with increasingly critical projects.

Consider the typical project from this era: a 220kV substation in interior Maharashtra, timeline of 18 months, budget constraints that would make Western engineers weep. TEECL would mobilize teams who understood that "18 months" really meant "before the next election," that the budget had no room for imported components even if they were superior, and that the local contractor mafia needed to be managed delicately. This wasn't in any engineering textbook—this was institutionalized Indian jugaad, elevated to industrial scale.

The company's approach to talent was equally distinctive. While competitors hired from IITs and sent them for foreign training, TEECL built a cadre of engineers who cut their teeth on Indian projects. These weren't just employees; they were almost missionaries of electrification, spending months in project sites, living in makeshift quarters, solving problems that had no precedent in technical manuals.

By the late 1990s, TEECL had quietly become indispensable to India's power sector. The competitive landscape in the EPC sector remains vigorous, with companies continually innovating to maintain their market share. Competitors like L&T had scale, Siemens had technology, but TEECL had something equally valuable—deep, almost intimate knowledge of Indian power infrastructure and the trust of government clients who valued reliability over flashy credentials.

The numbers from this period tell only part of the story. Projects worth hundreds of crores were executed, but the real asset being built was institutional knowledge. Every project added to their library of solutions—how to deal with rocky terrain in the Deccan, how to protect equipment from salt air in coastal Gujarat, how to expedite environmental clearances in forest areas. This was intellectual property that couldn't be bought or imported.

As the new millennium approached, TEECL stood at another crossroads. The company had mastered the art of EPC in India's power sector, but the landscape was changing. Economic liberalization had opened doors to international competitors, technology was evolving rapidly, and most intriguingly, new opportunities were emerging in renewable energy. The question wasn't whether to evolve, but how fast and in which direction. The answer would define their next decade and transform them from an infrastructure builder to an asset owner.

IV. The Renewable Energy Pivot (2009–2010)

The global financial crisis of 2008 had brought the world's economies to their knees, but in the conference rooms of Techno Electric's Kolkata headquarters, managing director P.P. Gupta saw opportunity where others saw calamity. India's power deficit was chronic—peak shortages regularly exceeded 12%—but the solution couldn't be more coal plants. The world was pivoting toward renewable energy, and India, with its vast coastlines and wind corridors, was perfectly positioned to ride this green wave.

In 2009 it joined the power generation sector by acquiring two wind energy generation companies. This wasn't a tentative toe-dip into renewables; this was a cannonball dive. The entry into this sector was marked by the acquisition of two wind power generating companies, namely Simran Wind Project Private Limited and Super Wind Project Limited.

The Simran acquisition was particularly intriguing. Simran Wind Project, listed in Suzlon Energy 2008-09 Annual Report as a company which is a promoter group entity, came with 50.45 MW capacity, while Super Wind Project Private Limited brought 45 MW. Together, they transformed TEECL overnight from a pure services company to an independent power producer.

The investment application indicated they would be investing Rs 145 crore in setting up wind energy generators of about 21MW in Tamil Nadu. Karnataka is the other state in which it operates. But the real ambition was much larger. Between 2009 and 2013, as an Independent Power Producer, they successfully developed 207.35 MW of wind energy projects in Tamil Nadu and Karnataka for US $200 million.

What made this pivot remarkable wasn't just its scale but its timing. In 2010, Techno Electric took a significant step by venturing into the renewable energy space, focusing on wind energy projects. This move was aligned with India's broader push towards sustainable energy sources. The Indian government had just introduced generation-based incentives (GBI) for wind power, making projects financially viable that weren't before. Carbon credits under the Clean Development Mechanism added another revenue stream.

Notably, the projects were among the first few to secure registration under the United Nations Framework Convention on Climate Change (UNFCC) for Carbon Credits. This wasn't just about generating power; it was about generating multiple revenue streams—selling electricity to state grids, earning carbon credits, and claiming accelerated depreciation benefits.

The technical challenges were formidable. Wind sites in Tamil Nadu's Tirunelveli district faced extreme conditions—scorching heat, corrosive salt air from the nearby coast, and monsoon winds that could exceed 150 km/h. Equipment designed for European wind farms needed substantial modification. TEECL's engineers, drawing on decades of experience making foreign equipment work in Indian conditions, developed innovative solutions—special coatings for turbine blades, modified cooling systems for generators, reinforced foundations that could handle both rocky terrain and seasonal flooding.

By 2013, TEECL had commissioned multiple wind power projects totaling over 546 MW of installed capacity. They weren't just wind farm operators; they had become one of India's significant renewable energy players. The financial engineering was as impressive as the electrical engineering—using non-recourse project financing, optimizing debt-equity ratios for each project, and structuring special purpose vehicles that minimized risk to the parent company.

The wind energy pivot also marked a philosophical shift. For decades, TEECL had been a company that built assets for others. Now, they owned assets that generated predictable cash flows for 20-25 years. In 2011, the Company received private equity investment from International Finance Corporation (IFC), Washington and set up 111.9 MW wind farm in Tamil Nadu. The IFC investment wasn't just capital—it was validation that TEECL could operate at international standards.

But even as wind turbines spun profitably in Tamil Nadu's wind corridors, Gupta and his team were already planning the next transformation. The renewable energy bet had paid off handsomely, but it had also taught them a valuable lesson: asset ownership, combined with their EPC expertise, created a powerful competitive moat. The question was where to apply this learning next. The answer would come from an unexpected source—India's capital markets.

V. Going Public & Capital Markets Entry (2012)

The Bombay Stock Exchange's iconic building on Dalal Street had seen countless dreams made and broken since 1875, but on a humid December morning in 2018, it witnessed something unusual—a reverse merger that would catapult a power infrastructure company into the public markets. Techno Electric's public listing took place in 2012. The company's shares were listed on the National Stock Exchange of India (NSE) and the Bombay Stock Exchange (BSE) under the ticker symbol TEIL. However, the actual trading under the current structure began later, following a complex restructuring.

The path to public markets wasn't straightforward. The Company was incorporated as Simran Wind Project Limited on October 26, 2005. The Company name was thereafter changed from Simran Wind Project Limited to Techno Electric & Engineering Company Limited effective from August 3, 2010. This wasn't just a name change—it was a complete transformation of identity, from a single-purpose wind energy company to a diversified infrastructure powerhouse.

The public listing represented more than access to capital—it was TEECL's coming-of-age moment. For a company that had operated in the shadows of government contracts and private negotiations for nearly five decades, the harsh sunlight of quarterly earnings calls and analyst scrutiny was both challenge and opportunity. P.P. Gupta, more comfortable in project sites than press conferences, had to learn a new language—the language of earnings guidance, return ratios, and investor relations.

Trading Members of the Exchange are hereby informed that effective from Tuesday, December 4, 2018 the equity shares of Techno Electric & Engineering Company Limited shall be listed and admitted to dealings on the Exchange in the list of T Group of Securities. The technical listing was complex, involving a scheme of amalgamation that would have made investment bankers proud.

The market's initial reception was cautiously optimistic. Here was a company with real assets—wind farms generating steady cash flows—and a proven track record in EPC. But institutional investors had questions. How would a company accustomed to the slow pace of government contracts adapt to the quarterly demands of public markets? Could they maintain margins in an increasingly competitive EPC sector?

In FY 2015, the Company bought back the 3.38% stake held by International Finance Corporation, signaling confidence in their own prospects. This buyback was funded entirely through internal accruals—a flex of financial muscle that didn't go unnoticed by market watchers.

The discipline imposed by public listing began showing results. Debtor days have improved from 190 to 108 days. Company's working capital requirements have reduced from 158 days to 92.4 days. These weren't just numbers improving on a spreadsheet—this was a fundamental rewiring of how the company operated. Collection teams were strengthened, project milestones were linked to payments more tightly, and working capital management became a board-level priority.

Being public also meant strategic decisions were now scrutinized differently. When TEECL decided to selectively divest wind assets, the market initially panicked—were they abandoning renewables? But management's communication was clear: The Company sold 44.45 MW of wind power assets at an effective valuation of Rs 2,150 million during Q1 during the FY 2016. In FY 2017, it sold 33 MW of wind energy assets in Tamil Nadu at an effective valuation of Rs 1,650 million. These weren't distress sales but strategic portfolio optimization, recycling capital from mature assets to fund higher-return opportunities.

The public listing also forced transparency in an industry notorious for opacity. Related-party transactions were disclosed, segment-wise performance was reported, and competitive dynamics were discussed openly in investor calls. For a company that had operated on relationships and reputation, this radical transparency was initially uncomfortable but ultimately liberating.

By 2020, TEECL had been a listed entity for several years, and the transformation was complete. The company that once survived on government contracts now had institutional investors from Singapore and London on its shareholder register. The firm that once measured success in successful project completions now tracked return on equity religiously. Most importantly, the access to capital markets meant they could dream bigger—and the biggest dream was just beginning to take shape in the form of ones and zeros rather than megawatts and substations.

VI. Operational Excellence & Scale Building (2012–2020)

If the 2010s began with TEECL's renewable energy pivot, they would be defined by something less glamorous but equally crucial: operational excellence at scale. This was the decade where Techno Electric proved that an Indian infrastructure company could deliver complexity with consistency, whether it was a wind farm in Tamil Nadu or a substation in the Northeast.

Commissioned 146.4 MW of wind energy projects in Tamil Nadu. Executed the electrical works for the 1,320 MW coal-based power plant in Jharkhand. Developed the transmission and distribution network for several smart cities across India. Each project added another layer to their execution capability, another reference point for future bids.

The 1,320 MW coal-based power plant in Jharkhand deserves special attention. This wasn't TEECL's project—they were subcontractors for the electrical works—but the scale was staggering. Imagine orchestrating the electrical infrastructure for a facility that could power a city of 2 million people. The cabling alone stretched hundreds of kilometers, the switchgear installations required precision down to millimeters, and any delay would cascade into millions in liquidated damages.

The smart cities initiative presented different challenges altogether. Unlike traditional projects with single clients and clear specifications, smart city infrastructure involved multiple stakeholders—municipal corporations, state governments, technology vendors, citizen groups. TEECL had to evolve from being pure engineers to becoming system integrators, solution architects, even diplomats mediating between competing interests.

But the real transformation was happening behind the scenes, in how TEECL approached project execution. They developed what they called the "TEECL Way"—a standardized approach to project management that could be replicated across geographies and sectors. Safety protocols that exceeded Indian standards but were practically implementable. Quality assurance processes that caught issues before they became problems. Resource allocation algorithms that optimized equipment utilization across multiple concurrent projects.

The numbers told the story of this operational transformation. The Company employs 450+ professionals (engineering, commercial, graduates and post-graduates), but their productivity per employee had nearly doubled through the decade. Project execution timelines, once measured in years, were now tracked in weeks. Cost overruns, endemic in the infrastructure sector, became rare exceptions rather than the rule.

Technology adoption accelerated. Drone surveys for transmission line routes, digital twins for substation design, predictive maintenance algorithms for wind turbines—TEECL was quietly becoming a technology company that happened to build infrastructure. Young engineers joined not just for the projects but for exposure to cutting-edge tools and methodologies.

The financial discipline was equally impressive. Despite taking on increasingly complex projects, TEECL maintained its near debt-free status. Company is almost debt free. In an industry where leverage was considered normal, even necessary, TEECL's conservative balance sheet was both an anomaly and a competitive advantage. When competitors struggled during economic downturns, TEECL could bid aggressively, knowing they had the financial cushion to weather delays or payment issues.

Strategic partnerships flourished. Rather than trying to do everything in-house, TEECL built a network of specialized partners—equipment manufacturers, technology providers, local contractors. They became the orchestrator of an infrastructure symphony, conducting multiple parties to deliver harmonious results. This asset-light approach to scaling meant they could take on multiple large projects simultaneously without proportionally increasing fixed costs.

The wind energy business, meanwhile, had matured into a cash generation machine. Power purchase agreements with state utilities provided predictable revenue streams for 20-25 years. The operational expertise gained from running wind farms—managing grid integration, optimizing generation based on wind patterns, minimizing downtime through predictive maintenance—became another differentiator in EPC bids.

As the decade drew to a close, TEECL stood at an interesting juncture. They had proven they could execute any power infrastructure project in India, from generation to transmission to distribution. They had demonstrated financial discipline that earned investor trust. They had built operational capabilities that matched global standards. But P.P. Gupta and his leadership team sensed that incremental improvement in traditional infrastructure wouldn't be enough for the next decade. The future belonged to those who could bridge the physical and digital worlds. And so, even as substations were being commissioned and wind turbines installed, plans were being drawn for server racks and cooling systems. The data center transformation was about to begin.

VII. The Data Center Transformation (2021–Present)

The PowerPoint slide seemed almost absurd when P.P. Gupta first presented it to his board in early 2021: Techno Electric, a company that had spent six decades moving electrons through copper wires, would now house servers that moved data through fiber optic cables. The skeptics had valid questions—what did a power infrastructure company know about data centers? The answer, as it turned out, was "more than you might think."

In 2021, we ventured into the data center domain by building on our extensive experience and multidisciplinary expertise in electrical, mechanical, civil, and structural engineering. But calling it a "venture" understates the audacity of the move. This was a billion-dollar bet on India's digital future, leveraging every lesson learned from six decades of infrastructure building.

The timing was exquisite. India's data consumption was exploding—from 2 GB per user per month in 2016 to over 15 GB by 2021. The pandemic had accelerated digital adoption by years. Global hyperscalers were eyeing India hungrily. And critically, data localization regulations meant that data generated in India increasingly needed to be processed and stored within the country.

Through this investment, Techno Digital intends to develop an integrated network of hyperscale and edge data centers targeting a 250 MW cumulative capacity across the country. The $1 billion commitment wasn't just capital allocation—it was a statement of intent. TEECL wasn't dabbling in data centers; they were positioning themselves as serious players in India's digital infrastructure build-out.

The Chennai facility would become their proof of concept. Spanning over 200,000 sqft, this state-of-the-art 36 MW datacentre delivers a hosting capacity of about 2,400 high-density racks and is designed to support flexible power densities from 10kW to 50kW per rack and beyond, making it one of India's most advanced AI-ready infrastructures. The location in SIPCOT IT Park, Siruseri, was strategic—close to submarine cable landing stations, in the heart of Chennai's IT corridor, with access to skilled talent.

But the real innovation was in how TEECL approached data center development. While competitors either came from real estate (and struggled with power and cooling complexities) or from IT (and struggled with construction and infrastructure), TEECL brought unique advantages. They understood power—not just at a theoretical level but at the practical level of managing grid fluctuations, ensuring 99.999% uptime, and designing redundancies that actually worked in Indian conditions.

It will use adiabatic cooling and offer a PUE of 1.35. In a country where most data centers struggled to achieve PUE below 1.8, this was remarkable. The innovation came from applying lessons learned from cooling generator rooms in Rajasthan's 50-degree summers—if you could keep a turbine cool in those conditions, servers were comparatively simple.

The sustainability angle wasn't just greenwashing. The facility sets a new benchmark for sustainable digital infrastructure by deliberately allocating 25 per cent of the total site area to green spaces a first in the region. Having operated wind farms for over a decade, TEECL understood that sustainable operations weren't just about corporate responsibility—they were about long-term operational efficiency and cost optimization.

The edge data center partnership with RailTel was perhaps even more strategic than the hyperscale facilities. Techno Electric and Engineering Co. Ltd. will design, build, finance, operate, and transfer Edge Data Centres (EDCs) as a Business Associate of RailTel Corporation of India Ltd. in 102 cities across India over a twenty-year concession period extendable by five years. This wasn't just about building boxes to house servers—it was about creating the nervous system for Digital India.

This project is expected to be one of the largest deployments of its kind, bringing low-latency computing closer to users in Tier 2 and Tier 3 cities, empowering sectors such as AI, BFSI, telecom, OTT, e-sports, healthcare, e-governance, and manufacturing. Imagine the transformative potential: a doctor in rural Bihar conducting remote surgery with near-zero latency, a student in small-town Odisha accessing cloud-based learning platforms seamlessly, a manufacturer in Coimbatore running AI-powered quality control in real-time.

The financial structuring of the data center business showed sophisticated thinking. Unlike the capital-intensive EPC business with its working capital challenges, data centers offered a different model—high upfront investment but predictable, long-term contracts with blue-chip clients. The payback periods were longer but the returns more certain. It was the wind energy model on steroids—build once, earn for decades.

Ankit Saraiya, Director & CEO, Techno Digital, represented the new generation of leadership, comfortable discussing both MVA capacities and machine learning workloads. The organization was transforming too—hiring data center specialists, partnering with global technology providers, learning the language of SLAs and interconnection agreements.

The market response was initially mixed. Some investors worried about capital allocation—why was a profitable EPC company with a successful renewable energy business venturing into the capital-intensive, highly competitive data center space? But others saw the strategic logic—TEECL was one of the few companies that could handle the full stack of data center development, from land acquisition to grid connectivity to construction to operations. As 2024 unfolded, the Chennai facility approached commissioning, and the true scale of TEECL's ambition became clear. This wasn't just about building data centers—it was about positioning the company at the intersection of India's physical and digital infrastructure. Every substation they built would eventually connect to a data center. Every renewable energy project could power digital infrastructure. Every edge data center would need the kind of electrical expertise TEECL had spent 60 years perfecting.

VIII. Recent Developments & Current Position (2023–2025)

The conference room at TEECL's Kolkata headquarters buzzed with an energy that hadn't been felt since the renewable energy pivot of 2009. It was May 2025, and the Q4 FY25 results had just been released. The company's consolidated net profit jumped 73.7% to Rs 134.65 crore on 85.6% increase in revenue from operations to Rs 815.79 crore in Q4 FY25 over Q4 FY24. But these numbers, impressive as they were, only told part of the story.

The transformation was remarkable at every level. On full year basis, the company's consolidated net profit jumped 57.5% to Rs 422.95 crore on 51% increase in revenue from operations to Rs 2,268.66 crore in FY25 over FY24. For a 62-year-old infrastructure company to deliver such growth in an era of startups and digital disruption was nothing short of extraordinary.

The Chennai data center had become operational, and the inauguration in August 2025 felt like a coronation. Techno Digital, the digital infrastructure arm of Techno Electric & Engineering Company Ltd (TEECL), has announced the inauguration of its 36-MW data center at SIPCOT IT Park, Siruseri, Chennai. This wasn't just another facility launch—it was validation of a strategy that many had questioned.

This next-gen facility is part of Techno Digital's $1 billion investment commitment towards building future-ready, sustainable digital infrastructure across the country. The company had committed serious capital, but more importantly, it had committed its reputation to this digital transformation.

What made the Chennai facility special wasn't just its size but its sophistication. The facility's design includes an on-site 110 kV GIS substation with dual power feeds from independent substations, connected via underground cable paths for reliability and weatherproof operation. This was infrastructure engineering at its finest—redundancy built upon redundancy, reliability engineered into every component.

The order book told its own story of transformation. Revenue guidance: FY 25: 2500 Cr, and the company was well on track to achieve it. But the composition of this order book had changed dramatically. Traditional EPC projects still formed the backbone, but data center development, smart meter installations, and renewable energy projects with battery storage were increasingly prominent.

The RailTel partnership was progressing ahead of schedule. The first few edge data centers were already under construction, and the response from Tier 2 and Tier 3 cities was overwhelming. Local governments, eager to attract digital businesses, were facilitating land acquisition and clearances. With the establishment of Edge Data Centers, data centre vertical is taking significant steps to enhance the digital experience and drive the widespread adoption of digital services among residents of rural and urban areas, thereby contributing to the country's Digital India mission.

Management's communication with investors had evolved too. We want to be in a capex range of INR500 crores to INR700 crores. The total concession period revenues, INR2,800 crores, and there relates to Gogamukh and Bokajan at the moment. And the total capex involved in these two concessions put together is about 750. This wasn't the vague guidance of yesteryears—this was precise capital allocation strategy communicated with clarity.

The stock market had taken notice. Despite broader market volatility, TECHNOE had held steady, supported by improving fundamentals and the promise of the data center business. Institutional investors who had been skeptical were beginning to accumulate positions. The narrative was shifting from "traditional infrastructure company" to "digital infrastructure play with proven execution capability."

But challenges remained formidable. Company has a low return on equity of 12.1% over last 3 years. For all the growth, returns hadn't kept pace with investor expectations. The capital-intensive nature of the data center business meant that returns would be back-loaded—strong cash flows would come, but patience was required.

Competition was intensifying across all segments. In EPC, larger players like L&T were becoming more aggressive. In data centers, global giants like Amazon and Microsoft were building their own facilities while Indian conglomerates like Adani and Reliance were making massive investments. The edge data center space, while promising, was attracting numerous players sensing opportunity.

The leadership team, however, remained confident. P.P. Gupta, now in his seventies but still sharp as ever, spoke of building for the next generation. "With this strategic expansion, Techno Electric reaffirms its commitment to building a high-quality, benchmark digital infrastructure platform. The Chennai Data Center facility is a testament to the group's EPC leadership and financial discipline, ensuring superior returns and long-term value creation for all stakeholders".

As 2025 progressed, the pieces were falling into place. The Chennai data center was ramping up occupancy. The edge data center rollout was accelerating. Traditional EPC projects continued to provide steady cash flows. The wind energy assets, though reduced in size, generated predictable returns. This wasn't just business diversification—it was business evolution, each segment reinforcing the others, creating a platform that could capture value across India's infrastructure transformation. The company that started by wiring factories in 1963 was now wiring the digital economy, and the journey was just beginning.

IX. Playbook: Business & Investing Lessons

Every great business story teaches lessons, but Techno Electric's six-decade journey offers a masterclass in strategic evolution. The playbook isn't about massive capital or revolutionary technology—it's about reading the currents of national development and positioning ahead of the wave.

Lesson 1: Master Timing Over Technology

TEECL never invented anything groundbreaking. They didn't develop new turbine technology for wind farms or revolutionary cooling systems for data centers. Instead, they mastered the art of timing—entering power transmission just as India needed grid expansion, pivoting to renewables when policy support materialized, launching data centers as digital adoption exploded. The lesson? In infrastructure, being early is the same as being wrong, and being late means fighting for scraps. The sweet spot is reading policy signals and market readiness, then moving decisively.

Lesson 2: Bootstrap Financial Discipline

Company is almost debt free—this simple statement represents a philosophy that enabled every strategic pivot. While competitors leveraged up to chase growth, TEECL maintained balance sheet strength that allowed them to invest counter-cyclically. During the 2008 financial crisis, they bought wind assets. During the COVID pandemic, they launched their data center initiative. Conservative finance isn't just about risk management—it's about preserving optionality for transformative bets.

Lesson 3: Government Alignment as Competitive Advantage

From the License Raj to Digital India, TEECL succeeded by aligning with government priorities rather than fighting them. They understood that in India, infrastructure isn't just business—it's nation-building. Their edge data center partnership with RailTel, a government entity, exemplifies this approach. While others saw bureaucracy, TEECL saw partnership opportunity. The lesson? In emerging markets, swimming with the policy current multiplies your strength.

Lesson 4: Compound Domain Expertise

Each business segment TEECL entered built upon previous knowledge. Electrical contracting taught them project execution. Power transmission taught them grid dynamics. Wind energy taught them asset ownership. All of this culminated in data centers—facilities that are essentially power and cooling infrastructure housing IT equipment. The compound effect of domain expertise created barriers competitors couldn't easily cross. A real estate company might build a data center shell, but could they ensure five-nines power availability?

Lesson 5: Capital Allocation as Strategy

TEECL's capital allocation evolution reads like a Harvard case study. Initially, all capital went into working capital for EPC projects—high returns but cash flow negative. The wind energy pivot introduced asset ownership—lower returns but predictable cash flows. These cash flows then funded the data center transformation—high upfront investment but exceptional long-term returns. Each phase funded the next, creating a self-reinforcing cycle of capital deployment.

Lesson 6: Talent Arbitrage Through Localization

While competitors imported expertise, TEECL built indigenous capability. Their engineers might not have had international exposure, but they understood Indian conditions intimately. This wasn't just cost arbitrage—it was knowledge arbitrage. An engineer who's managed a substation during a Gujarat summer understands redundancy in ways no textbook teaches. This localized expertise became invaluable when designing data centers for Indian conditions.

Lesson 7: Platform Thinking Over Product Focus

TEECL evolved from a service provider (EPC) to an asset owner (wind farms) to a platform player (data centers with edge networks). Each evolution expanded their value capture potential. The edge data center network isn't just 102 individual facilities—it's a platform that enables countless digital services. Platform thinking multiplies value in ways linear business models cannot match.

Lesson 8: Financial Metrics That Matter

Over the last 5 years, revenue has grown at a yearly rate of 21.76%, vs industry avg of 10.18%. But TEECL's genius wasn't just growing faster—it was choosing metrics that mattered for each business phase. During the EPC era, they focused on working capital efficiency. For wind energy, it was capacity utilization. For data centers, it's contracted revenue and customer stickiness. Understanding which metrics drive value in each business model enabled superior capital allocation.

Lesson 9: The Power of Patient Capital

TEECL's major transitions—into renewables, public markets, data centers—all required patient capital. Wind farms took 3-4 years to stabilize returns. Data centers require 5-7 years for full payback. But patient capital invested at inflection points generates exponential returns. Impatient capital would have sold the wind assets too early or avoided data centers altogether.

Lesson 10: Operational Excellence as Moat

In commodity businesses like EPC, operational excellence becomes the only sustainable moat. TEECL's ability to deliver projects on time, within budget, in challenging conditions became their calling card. This reputation, built over decades, enabled them to win projects that commanded premium pricing. Operational excellence compounds like interest—invisible daily but transformative over decades.

The meta-lesson? Great infrastructure businesses aren't built through grand strategy alone but through countless operational decisions executed consistently over decades. TEECL's playbook isn't about revolutionary insights but evolutionary excellence—reading the environment, positioning ahead of change, and executing with discipline. In infrastructure, the tortoise doesn't just beat the hare—it builds the racetrack.

X. Analysis & Bear vs. Bull Case

The investment community remains divided on Techno Electric. At ₹15,764 crore market cap, is this a value play in digital infrastructure or a traditional EPC company overreaching? The debate illuminates broader questions about India's infrastructure transformation.

The Bull Case: Riding Three Megatrends

Bulls see TEECL positioned at the intersection of three unstoppable forces. First, India's power infrastructure spending will exceed $500 billion this decade—transmission capacity alone needs to double. Second, renewable energy will attract $280 billion by 2030, and someone needs to build the evacuation infrastructure. Third, data center capacity in India must grow 5x by 2028 to meet digital demand.

Revenue grown at yearly rate of 21.76% over last 5 years, vs industry avg of 10.18%—this isn't just outperformance, it's evidence of structural advantages. TEECL operates in segments where technical expertise matters more than pure capital. Can Adani engineers design a GIS substation for coastal conditions? Can Reliance execute 102 edge data centers across Tier 3 cities? Execution capability at scale remains scarce.

The data center transformation could be genuinely transformational. At current valuations, the market assigns minimal value to the digital infrastructure business. Yet the 36 MW Chennai facility with 2,400 high-density racks designed for 10kW to 50kW per rack represents just the beginning. If TEECL achieves even half their 250 MW target, the data center business alone could justify current valuations.

Bulls point to management quality. P.P. Gupta built this company from scratch, navigated License Raj, economic liberalization, and multiple technology transitions. The second generation, represented by Ankit Saraiya, brings digital-age thinking while respecting operational discipline. This isn't a promoter looking for exit—it's a dynasty building for generations.

The balance sheet provides downside protection. Near-zero debt means TEECL can weather any storm. During downturns, they can acquire distressed assets. During upturns, they can invest aggressively. This financial flexibility is worth a premium in a capital-intensive industry where leverage often proves fatal.

The Bear Case: Structural Challenges

Bears see fundamental issues. Return on equity of 12.1% over last 3 years is pedestrian for a supposedly high-growth company. If TEECL is such a wonderful business, why can't it generate returns above cost of capital consistently? The answer might be that infrastructure in India remains a difficult, low-margin business regardless of segment.

Competition is intensifying everywhere. In EPC, global giants are entering India. In data centers, hyperscalers are building their own facilities—why would Amazon lease from TEECL when they can build themselves? In renewable energy, returns have compressed as everyone from pension funds to private equity chases yield. TEECL's niches are becoming highways.

The data center bet might be poorly timed. Yes, demand is growing, but so is supply—massively. Every Indian conglomerate is building data centers. Global operators are entering India. Hyperscalers are expanding rapidly. In 3-5 years, India might face data center oversupply, crushing returns for everyone. TEECL is entering a gold rush just as everyone else discovers the gold.

Execution risk looms large. Building 102 edge data centers is exponentially more complex than building one hyperscale facility. Each location needs land acquisition, power infrastructure, local permits, and skilled operators. The RailTel partnership adds another layer—government partnerships in India often mean delays, cost overruns, and bureaucratic nightmares.

Bears question capital allocation. Why is a successful EPC company with profitable wind farms venturing into data centers? The skills required are different—data center operations need IT expertise, customer management capabilities, and 24/7 service excellence. TEECL's core competency is project execution, not service operations. This feels like empire building rather than value creation.

The Verdict: Asymmetric Opportunity with Execution Risk

The truth, as always, lies between extremes. TEECL represents a rare breed—an old-economy company successfully transforming for the new economy. The stock offers asymmetric upside if the data center strategy succeeds, with EPC cash flows providing downside protection.

The key variable isn't market demand—India needs everything TEECL builds. It's execution. Can a 62-year-old infrastructure company become a digital infrastructure leader? Can they attract talent to compete with tech companies? Can they maintain service levels that hyperscalers demand?

For investors, TEECL represents a bet on India's infrastructure transformation with a management team that's navigated multiple transitions successfully. The risk-reward depends on your time horizon. Quarter-to-quarter, volatility is guaranteed. But over 5-10 years, the combination of EPC expertise, renewable energy assets, and digital infrastructure exposure offers compelling value.

The bear case is about competition and returns. The bull case is about execution and opportunity. History suggests betting against P.P. Gupta has been expensive. Whether that history repeats in the digital age remains the billion-dollar question.

XI. Epilogue & "What Would We Do?"

Standing at the construction site of TEECL's newest edge data center in a Tier 3 city in Karnataka, you can literally see India's transformation. On one side, traditional electrical infrastructure—transformers, switchgear, cables—the backbone TEECL has built for six decades. On the other, server racks waiting to be installed, fiber optic cables being laid, cooling systems that would make NASA proud. This convergence of old and new economy isn't just symbolic—it's the entire investment thesis.

The Next Decade: Three Scenarios

The optimistic scenario sees TEECL becoming India's digital infrastructure champion. The 250 MW data center target is achieved by 2030. The edge network becomes the backbone for India's 5G rollout, IoT revolution, and AI adoption. Traditional EPC expertise creates a moat in mission-critical infrastructure. The stock re-rates from infrastructure to technology multiples. Market cap touches ₹50,000 crore by 2035.

The base case is more measured. TEECL successfully builds 100-150 MW of data center capacity, becoming a solid Tier 2 player. The edge network faces delays but eventually delivers 50-60 operational facilities. EPC business remains steady but unspectacular. Returns improve gradually to 15-18% ROE. The stock delivers 12-15% annual returns, in line with nominal GDP growth.

The pessimistic scenario sees execution challenges multiplying. Data center development faces delays and cost overruns. The edge network struggles with local opposition and bureaucratic hurdles. Competition in EPC intensifies, compressing margins further. The company remains profitable but fails to justify growth valuations. The stock trades sideways for years, frustrating growth investors while being too volatile for value investors.

What Would We Do?

If we were running TEECL, three priorities would dominate:

First, talent transformation. The biggest risk isn't capital or competition—it's human capital. Data centers require different DNA than EPC projects. We'd aggressively hire from IT services companies, create ESOPs to attract tech talent, and potentially acquire a small data center operator for expertise. Cultural transformation would be prioritized over financial metrics for the next 24 months.

Second, customer concentration. Rather than chasing every opportunity, we'd focus on 3-5 anchor customers for data centers—perhaps one hyperscaler, one Indian tech giant, one government entity. Deep relationships matter more than broad reach. Each edge data center would have an anchor tenant before construction begins. Revenue certainty would trump growth rates.

Third, capital recycling. We'd systematically monetize mature assets to fund growth. The remaining wind farms could be sold to yield-hungry funds. Select EPC projects could be converted to BOT models, then sold to infrastructure funds. This isn't financial engineering—it's recognizing that TEECL's competitive advantage is in development, not permanent ownership.

Key Metrics to Watch

Investors should track five indicators:

- Data center pre-commitments: Capacity booked before construction signals market validation

- Edge network rollout pace: 20+ facilities operational by 2026 would confirm execution capability

- Working capital days: Continued improvement indicates operational excellence

- Talent metrics: Percentage of employees with tech backgrounds should reach 30% by 2027

- Return ratios: ROE exceeding 15% would signal successful transformation

The India Context

TEECL's story can't be separated from India's trajectory. If India becomes a $10 trillion economy by 2035, infrastructure spending will exceed $2 trillion this decade. Digital infrastructure alone could attract $100 billion. In this context, TEECL isn't just riding trends—they're building the rails on which Digital India runs.

The edge data center network could enable possibilities we can't fully imagine. Telemedicine in rural Bihar, AI-powered agriculture in Punjab, real-time manufacturing analytics in Tamil Nadu—TEECL is building the nervous system for India's economic transformation.

Final Thoughts

Great infrastructure companies are built over generations, not quarters. TEECL's journey from electrical contractor to digital infrastructure player spans six decades of India's evolution. The next chapter—becoming a platform for India's digital economy—might be the most ambitious yet.

For investors, TEECL represents a rare opportunity: a company with proven execution capability entering a massive new market with structural advantages. Yes, risks are real—execution challenges, competition, technology shifts. But the asymmetry is compelling. Downside is protected by hard assets and cash flows. Upside could be transformational if India's digital infrastructure boom unfolds as expected.

Perhaps the best lens is temporal. In 2030, will India need more data centers? Absolutely. Will edge computing be critical for 5G and IoT? Certainly. Will someone need to build this infrastructure? Definitely. The question isn't whether the opportunity exists but whether TEECL can capture it.

Betting on TEECL is betting on execution over ideation, experience over exuberance, and ultimately, on India's infrastructure transformation. It's a bet that the company that helped electrify India can help digitize it. History suggests that's not a bad wager. The future will determine if history rhymes in the digital age.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube